Embed Size (px)

Citation preview

•J

r

f,

OFFICE OF THE PRINCIPAL COMMISSIONER OF C. G. S. T., AHMEDABAD - SOUTH.

WW STT^FcT #7.G. S. T. BHAVAN, AMBAWADI, AHMEDABAD - 380 015

S'. $■. §T55T, STT^rar^t, 3lg<Hcil«llCi - 3^0 o?(j

^T.¥.F. No. : STC/04-13/Vodafone/0&/2020-21 DIN no. : 20201264WS0000888C88

3TT^r cTT^ST: Date of Order: 28.12.2020snft #r HTfUST: Date of Issue : 28.12.2020

c&TTT mfccT / Passed by: ShH Mohit AgraWdl, ADDITIONAL COMMISSIONER******************** *************************

xw 3JT$?r w./Order-In-Original No.28/CGST/Ahmd-South/ADC/MA/2020*******************************************************************************

21F yirl 3TT ciifcjV) (^it) ^>1", (foloi4i) folk; ^fF 3H^7 oll'fl f^TT ^RIT 3?T^i (iol4i)

f5rldlcl ^7 folk' f^:?]o^7 Wdw ollcfl

This copy is granted free of charge for private use of the person(s) to whom it is sent.

3TT^9r ^ SFif 3RfH,s? JOTtg' ch<cH| ^ rfr 9F 577 371^1 3TW^H (3PfroT),

ofTTOfr 3T55T, 5 3^ atfrlpf ■dchdl % I

3^77 3i41o) MSi'tii't 37T^?r HTJfroT plol 3f?l^T 3Ttf5T 3^” 5W 2^177 TTP-cT $7 ciiTl^ ^ St ■Hip SftcTT" STfT^T ^7 3nsfr 7TTf|rt7 I 57TT7 7W 2.00/- #^7 ?7c=37 eP17 5fr77 ^nte^ I

Any person deeming himself aggrieved by this Order may appeal against this order in Form E.A.l to Commissioner (Appeals), Central GST, Central GST Bhavan, Near Government Polytechnic, Ambawadi, Ahmedabad -15 within sixty days from date of its communication. The appeal should bear a court fee stamp of Rs.2.00/- only.

3377 3t4lrt St Wfcl'y) Jt TTTW 77. 5-fr-l ^ cwfSltf ^7 5177ft tuf^U I STT^TT 4)<r{TlJJ JcHlS (31 dirt)P^rtlOrtl, 2001 #7 PlAliH 3 #7 37T^t7t #7 37777777' STfrfpRfTcfelt 3123777 f^TTJ TTlf^C I fTT^TTTITTPliHrif<T|f<5)f1 5>t TTH^rT f^737 oin.1 :

The Appeal should be filed in form No. E.A.-l in duplicate. It should be filed by the appellants in accordance with provisions of Rule 3 of the Central Excise (Appeals) Rules, 2001. It shall be accompanied with the following:3Ctrl STdteT ^>T ilfrl I Copy of the aforesaid appeal.

T?Iu<M ^t £7t vifrlin (377^ 7747 37T 377^47 ^t tWlftfrot yfrlfolf^ pl®Tl faTTT^* 3l41cH

#t 37^ ^) 3T2J4T 34r7 377^?7 # yirT fStfETT 77 2.00/- 477 <t-4I4M'11 ?7rt47 ^475/ <7^77

eftari snf^xj' iCopies of the Decision (one of which at least shall be certified copy of the order appealed against) or copy of the said Order bearing a court fee stamp of Rs. 2.00/-.

577 377^77 #7 ft77i7 3TT414r7(3Tdt57) # 7JF47 ^7 7.5% 3757 7p47 tjfr ^jfe7 477 f%4727 % 37*747 5T5f RhSi

vdrtlrtl #7 57^ # f^5727 % 377477 374727777 477^7 37,:ffc:7 ^t 317 7147cft ft I

An appeal against this order shall lie before the Commissioner (Appeal) on payment of 7.5% of the duty demanded where duty or duty and penalty are in dispute, or penalty, where penalty alone is in dispute."

Tf^^/Reference : DENOVO ADJUDICATION, under the direction of Commissioner (Appeal) order no. AHM-EXCUS-001-APP-002-2018-19 dated 21.05.2018, in respect of W13fr 'gyHT'tf. / No. 980 dated 19.5.2014 bearing C. No. DL-ll/ST/R-XX/Vodafone/SCN/45/2010 dated 19.05.2014, issued to M/s. Vodafone Mobile Services Limited (Formerly known as M/s Vodafone Essar Mobile ServicesI imitpHl

BRIEF FACTS OF THE CASE

The present proceedings are denovo proceedings based on Commissioner (Appeals-II), Central Excise, Ahmedabad’s OIA No.AHM-EXCUS-001-APP-002- 2018-19 dated 21.05.2018 issued in respect of appeal filed by M/s. Vodafone Mobile Services ltd., Ahmedabad against OIO No:AHM-SVTAX-000-JC-033-16-17 dated 28.02.2017, issued by the Joint Commissioner, Service Tax Commissionerate, Ahmedabad. The brief facts of the case are as under:

2. M/s Vodafone Mobile Services limited (formerly known as M/s. Vodafone Essar Mobile Service Limited), C-48, Okhla Industrial Area, Phase-II, New Delhi-110020 (hereinafter referred to as the ‘assessee’ was mainly engaged in providing Telecommunication Services (Telephone/Cellular Services) and were holding Service Tax Registration No.AAACS4457QST001 under Section 69 of the Finance Act, 1994 for Telecommunication Services, BSS, GTA Services, Sponsorship Service, BAS, IPR Development and Supply of Content Service. During the course of audit, it was observed that the assessee had incurred foreign currency expenses which were shown as Roaming Charges under the head foreign currency expenses in their balance sheet. In order to provide services to its subscribers, the assessee had entered into roaming agreements with various service providers located beyond the geographical area of the assessee’s network. The visited networks provided services to assessee’s subscribers on behalf of the assessee and charged the assessee as per their tariff. It appeared that the services received by the assessee fell under the category of ‘Business Auxilliary Service’ in terms of sub-clauses(iii) and (vi) of Section 65(19) of the Act and the assessee, being recipient of services, appeared liable to pay service tax on the expenses shown in their balance sheets under the head ‘roaming charges’ in terms of Rule 3 of the Taxation of Services provided from outside India and Received in India Rules, 2006 and in terms of Rule2(l)(d)(iv) of Service Tax Rules, 1994 read with Section 66A of the Finance Act, 1994.

Accordingly, following show cause notices for different periods were issued by the Commissioner of Service Tax, New Delhi: (i) SCN for Rs. 19,93,10,780/- for the period from 2005-06 to 2009-10 dated 07.10.2010. (ii) SCN for Rs.3,56,76,893/- for the period 2010-11 dated 03.10.2011 and (iii) SCN for Rs.3,37,47,109/- for the period 2011-12 dated 15.10.2012.

3.

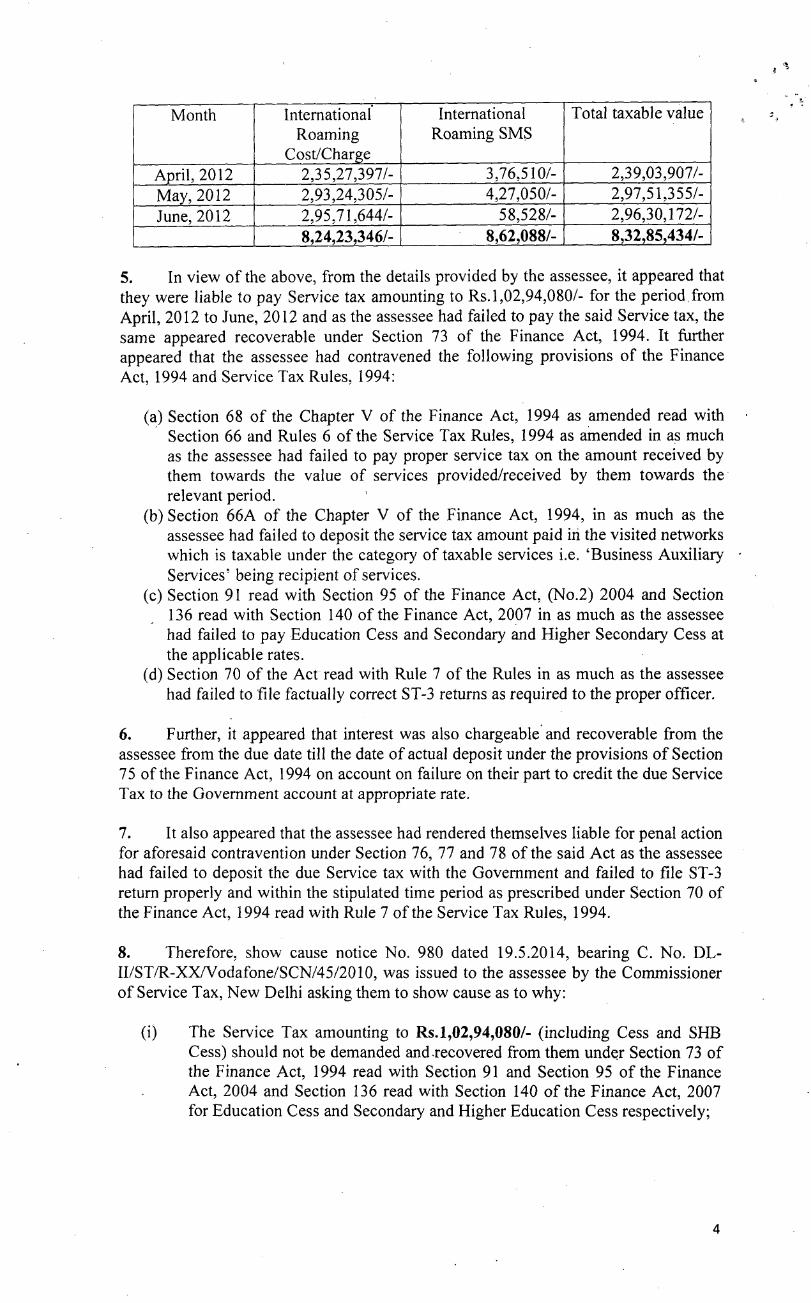

In view of the above, the assessee was asked to submit the details of the taxable value realized under the category of ‘Business Auxilliary Services during the period from 01.04.2012 to 31.03.2013 and the assessee vide their letter dated 29.04.2014 stated that they were not discharging Service Tax on payment made to Foreign Telecom operator for international outbound roaming services prior to 30.06.2012 as at that time they were of the view that the said transaction was not liable to be taxed under ‘Business Auxilliary Service’ under reverse charge. Accordingly, they submitted taxable value for the First quarter of 2012-13 in respect of international outbound roaming Cost and International roaming SMS cost on which they have not paid service tax. Further, w.e.f. 1st July, 2012 onwards, they started depositing service tax on payment made to Foreign telecom operator for international outbound roaming services and Rs.3,44,84,131/- had been deposited in Service Category ‘Telecommunication services’ under reverse charge mechanism for international outbound roaming cost from 01.07.2012 to 31.03.2013 based on payment made to Foreign roaming operator. Thus, they provided both the details of non-payment of service tax for the period 01.04.2012 to 30.06.2012 and payment of service tax for the period from 01.07.2012 to 31.03.2013. Details of International Roaming Cost and International Roaming SMS for the period from 01.04.2012 to 30.06.2012 were as follows:

4.

*

Total taxable valueInternational Roaming SMS

InternationalMonthRoaming

Cost/Charge2,39,03,907/-3,76,510/-2,35,27,397/-April, 20122,97,51,355/-4,27,050/-2,93,24,305/-May, 20122,96,30,172/-58,528/-2,95,71,644/-June, 20128,32,85,434/-8,62,088/-8,24,23,346/-

In view of the above, from the details provided by the assessee, it appeared that they were liable to pay Service tax amounting to Rs. 1,02,94,080/- for the period from April, 2012 to June, 2012 and as the assessee had failed to pay the said Service tax, the same appeared recoverable under Section 73 of the Finance Act, 1994. It further appeared that the assessee had contravened the following provisions of the Finance Act, 1994 and Service Tax Rules, 1994:

5.

(a) Section 68 of the Chapter V of the Finance Act, 1994 as amended read with • Section 66 and Rules 6 of the Service Tax Rules, 1994 as amended in as muchas the assessee had failed to pay proper service tax on the amount received by them towards the value of services provided/received by them towards the relevant period.

(b) Section 66A of the Chapter V of the Finance Act, 1994, in as much as the assessee had failed to deposit the service tax amount paid in the visited networks which is taxable under the category of taxable services i.e. ‘Business Auxiliary • Services’ being recipient of services.

(c) Section 91 read with Section 95 of the Finance Act, (No.2) 2004 and Section 136 read with Section 140 of the Finance Act, 2007 in as much as the assessee had failed to pay Education Cess and Secondary and Higher Secondary Cess at the applicable rates.

(d) Section 70 of the Act read with Rule 7 of the Rules in as much as the assessee had failed to file factually correct ST-3 returns as required to the proper officer.

Further, it appeared that interest was also chargeable and recoverable from the assessee from the due date till the date of actual deposit under the provisions of Section 75 of the Finance Act, 1994 on account on failure on their part to credit the due Service Tax to the Government account at appropriate rate.

6.

It also appeared that the assessee had rendered themselves liable for penal action for aforesaid contravention under Section 76, 77 and 78 of the said Act as the assessee had failed to deposit the due Service tax with the Government and failed to file ST-3 return properly and within the stipulated time period as prescribed under Section 70 of the Finance Act, 1994 read with Rule 7 of the Service Tax Rules, 1994.

7.

Therefore, show cause notice No. 980 dated 19.5.2014, bearing C. No. DL- II/ST/R-XX/Vodafone/SCN/45/2010, was issued to the assessee by the Commissioner of Service Tax, New Delhi asking them to show cause as to why:

8.

0) The Service Tax amounting to Rs. 1,02,94,080/- (including Cess and SHB Cess) should not be demanded and recovered from them under Section 73 of the Finance Act, 1994 read with Section 91 and Section 95 of the Finance Act, 2004 and Section 136 read with Section 140 of the Finance Act, 2007 for Education Cess and Secondary and Higher Education Cess respectively;

4

(ii) Interest should not be demanded and recovered from them under the provisions of Section 75 of the Act;Penalty under Section 76 of the Finance Act, 1994, as amended, should not be imposed upon them for failure to pay appropriate Service Tax in accordance with the provisions of Section 68 of the Finance Act, 1994 as amended, read with Rule 6 of Service Tax Rules, 1994;Penalty should not be imposed on them under Section 77(2) of the Finance Act, 1994 for failure to furnish factually correct ST-3 returns as prescribed under Section 70 ibid read with Rule 7 of the Service Tax Rules, 1994; and Penalty in terms of Section 78 of the Finance Act, 1994 should not be imposed upon them for contravention of various provisions of the Finance Act, 1994 and the rules made thereunder.

(iii)

(iv)

(v)

The show cause notice thereafter was transferred to the Principal Commissioner of Service Tax, Ahmedabad and thereafter to the Joint Commissioner, Service Tax, Ahmedabad in pursuance of Notification No.44/2016-ST dated 28.09.2016.

9.

Defense submission at the time of Original Adjudication:

The assessee submitted their reply to the show cause notice vide letter (received on 26.12.2016) denying the charges made in the show cause notice and stated that theirs is a company engaged in the business of providing Telecommunication Services(Telephone/Cellular Services); that they were holder of the Service Tax Registration No.AAACS4457QST001 under Section 69 of the Finance Act, 1994 for Telecommunication Services, Business Support Service, Goods Transport Agency Service, Sponsorship Service, Business Auxiliary Service, Intellectual Property Service, Development and Supply of Content service; that they have regularly filed their ST-3 returns during the relevant period; that to provide uninterrupted service to its subscribers, the assessee had entered into agreements with various foreign telecom operators for international roaming services and call termination services. The main submissions of the assessee were as under:

10.

The allegations contained in the SCN are solely based on the objections raised during the Audit of the assessee’s records conducted by the Department in January, 2010, proposes to demand service tax solely based on the said objections and no further investigations were carried out by the Department to substantiate the objection raised during audit. It is a settled legal position that SCN cannot be issued merely based on audit objections without any independent investigation of such objections and reliance is placed in the following case laws:

> Swastik Tin Works v/s. CCE, 1986 (25) ELT.798 (Tri.)> Indian Plastics ltd. v/s. CCE, 1988 (35) ELT 434 (Tri.)> Shree Uma Foundries pvt.ltd. v/s. CCE, 2009 (15) STR.758.

The SCN is liable to be dropped on this ground alone.

(0

The present SCN alleges that the Foreign Mobile Operators are providing services to the assessee’s subscribers on behalf of the assessee, thus services provided by Foreign Mobile Operators are covered under ‘Business Auxiliary Service’, therefore, the assessee is liable to pay service tax under reverse charge mechanism. The assessee has submitted that the Foreign Mobile Operators are not providing any service on behalf of the assessee but are providing services to the subscribers and the assessee is only making payments for the services received by the subscriber directly from the Foreign Mobile Operators. Roaming is a general term that refers to the extending of the connectivity service in a location that is different from the home location where the services are registered. Roaming ensures that the wireless device keeps connected to the home network without loosing the connection when

(ii)

* *'

it travels outside its home network. The assessee has submitted that they have entered into agreements with foreign mobile operators to provide the said roaming facility to its customers/subscribers when they travel abroad.

(Hi) The definition of ‘Business Auxiliary Service’ as amended from time to time clearly shows that the following services are taxable under this category:

Promotion of goods produced or provided by the client. Marketing of goods produced or provided by the client. Sale of goods produced or provided by the client. Promotion of services provided by the client.Marketing of services provided by the client.Customer care service provided on behalf of the client. Procurement of input goods or services for client. Production of goods on behalf of the client.Provision of service on behalf of the client.Services as a commission agent.

i.11111.

iv.v.vi.vu.vm.ix.x.

Further, certain services which are incidental or auxiliary to the aforementioned services (main services) are also covered under clause (vii) of the definition of ‘business auxiliary service’. . The SCN alleges that the foreign mobile operator is undertaking provision of service in the form of providing network to the subscribers on behalf of the assessee and therefore, is covered under clause(iii) and (vi) of Business Auxiliary Service. The assessee has referred to the meaning of ‘on behalf of from various dictionaries and has concluded that ‘on behalf of indicates an action undertaken representing somebody else i.e. when you do something on behalf of someone, you are representing that someone, who was otherwise obliged to do it. As the language itself suggests, the said clause contemplates a situation when a service provider (say ‘X’) provides certain service to a third party customer (say ‘Z’) on behalf of his client ( say ‘Y’). The service provided by ‘X’ is one which ‘Y’ was supposed to provide to ‘Z’. Instead, ‘Y’ engages ‘X’ to provide the same to ‘Z’ on his behalf. The assessee in this regard has also placed reliance on the decision of the Hon’ble Tribunal as well as on the cases of Auto Coats v/s. CCE, Coimbatore - 2009 (15) STR 398 (Tri-Chen), Rathour Engg.Works v/s. CCE, Chandigarh 2012 (27) STR 37(Tri-del.), Sonic Watches ltd. v/s. CCE, Vadodara 2011 (21) STR 34 (Tri-Ahmd.) and Gedee Weller pvt.ltd. v.CCE & ST, Coimbatore 2010 (18) STR 417 (Tri-Chennai). The assessee seeks to place reliance on Circular No.F.No.B2/8/2004-TRU, dated 10.09.2004, wherein the Department clarified that in order to fall within the scope of business auxiliary service, the services have to be carried out by the service provider (i.e. agent,) on behalf of the client. Further, the assessee has also argued that if the foreign mobile operator was acting on behalf of the assessee, then it would not have had this right to suspend or terminate the services of the roaming subscribers without the authorization from the assessee which clearly shows that it is providing the said service directly to subscribers, on a Principal to Principal basis. The assessee in this regard, further places reliance on the decision of Hon’ble High Court of Bombay in the case of Superintendent of Stamps v/s. Breul & Co., AIR 1944 Bom 325 wherein it was held that where in terms of the contract the relationship between two parties is that of principal to principal, one cannot be said to be acting as an agent of another.

(iv) As per Clause 6 of the Agreement, the subscriber may receive services different from that provided by the assessee. The only requirement of the foreign mobile operator is to ensure that same standard is maintained as it is providing to its own subscriber. The relevant excerpt of the agreement is reproduced herein below:

6

6. Implementation of the network and services.

6.1.4. Both parties agree that the Roaming Subscribers, sharing roaming may experience conditions of service different from the conditions in their HPMN. However, conditions or service shall not differ substantially from those provided to the subscribers of the VPMN Operator. ’’

The assessee has submitted that had the foreign mobile operator been acting on behalf of the assessee, it would be obligated to provide the same services as the assessee would itself be providing to its subscribers. Further new condition would not have been imposed on the subscribers by the Foreign Mobile Operators, i.e. the VPMN. However, from the above clause it is again clear that the foreign mobile operator treats the roaming subscriber as its own temporary subscribers, as it is obligated to provide services similar to the one it is providing to its own subscriber. From the above, it is clear that the foreign mobile operator is providing service directly to subscribers and not on behalf of the assessee. Since the services are provided directly to subscribers, the same cannot be classified under Business Auxiliary Service.

(v) It is submitted that the services provided by the Foreign Mobile Operator are in the nature of Telecommunication Services as envisaged under the Finance Act, 1994. Prior to 01.06.2007, the said service would have been covered under the category of‘telephone service’. ‘Telephone Service’ was defined as herein below:

Section 65(105) (b):‘any service provided to a subscriber, by the telegraph authority in relation to a telephone connection ’

With effect from 01.06.2007, ‘telephone service’ was brought under the broader category of ‘Telecommunication Service’. Therefore, post 01.06.2007, the said activity falls under the category of‘Telecommunication Service’. The definition of Telecommunication Service is reproduced hereinbelow:

(109a) ‘telecommunication service’ means service of any description provided by means of any transmission, emission or reception of signs, signals, writing, images and sounds or intelligence or information of any nature, by wire, radio, optical, visual or other electro-magnetic means or systems, including the related transfer or assignment of the right to use capacity for such transmission, emission or reception by a person who has been granted a license under the first proviso to sub-section (1) of section 4 of the Indian Telegraph Act, 1885 and include- (i)voice mail, data services, audio tex services, video tex services, radio paging; (infixed telephone services including provision of access to and use of the public switched telephone network for the transmission and switching of voice, data and video, inbound and outbound telephone service to and from national and international destinations;(iii) cellular mobile telephone services including provision of access to and use of switched or non-switched networks for the transmission of voice, data and video, inbound and outbound roaming service to and from national and international destinations;(iv) carrier services including provision of wired or wireless facilities to originate, terminate or transit calls, charging for interconnection settlement or termination of domestic or international calls, charging for jointly used facilities including pole attachments, charging for the exclusive use of circuits, a leased circuit or a dedicated link including a speech circuit, data circuit or a telegraph circuit;

(v) Provision of call management services for a fee including call waiting, call forwarding, caller identification, three-way calling, call display, call return, calf screen, call blocking, automatic call-back, call answer, voice mail, voice menus and video conferencing;(vi) private network services including provision of wired or wireless telecommunication link between specified points for the exclusive use of the client;(vii) data transmission services including provisions of access to wired or wireless facilities and services specifically designed for efficient transmission of data; and (viii)communication through facsimile, pager, telegraph and telex, but does not include service provided by-(a) any person in relation to on-line information and database access or retrieval or both referred to in sub-clause (zh) of clause (105);(b) a broadcasting agency or organization in relation to broadcasting referred to in subclause (zk) of clause (105);(c) any person in relation to ‘internet telecommunication service referred to in subclause (zzzu) of clause (105); ’

Section 65(105)(zzzx)Any service provided or to be provided to any person, by the telegraph authority in relation to telecommunication service;

Further, the Central Board of Excise and Customs vide Circular No.90/1/2007-ST dated 03.01.2007, in relation to in-bound roaming subscriber has clarified that the local network provides telecommunication service to the roaming subscriber as its own subscriber on a temporary basis. Thus, it is clear that even the Department itself is of the view that said service provided by the Visiting Network to the roaming subscriber, is in the nature of ‘Telecommunication Service’, and is provided to the subscriber on a Principal-to-Principal basis. Thus, the reasons explained in the Circular will apply in the present case also. Therefore, the foreign mobile operator is not providing any service to the assessee, the service is directly being provided to the subscriber. The role of the Host Network provider i.e. the assessee, is only to pay to the foreign mobile operator for the said telecommunication service on behalf of the subscriber. The assessee has placed reliance on Circular No.96/7/2007-ST dated 23.08.2017, wherein the Department in relation to ‘Authorised Service Station Service’ clarified that in the case of‘free servicing’, the service provided will continue to be ‘authorised Service Station Service’ only, even though the payment is made by the manufacturer on behalf of the customers. Similarly, in the instant case also, the ‘Telecommunication Service’ is being provided by the foreign mobile operator to the roaming subscriber. Only the consideration for the same is being paid by the assessee on behalf of the subscriber. Thus no service tax can be demanded from the assessee.

(vi) Activity carried out by foreign mobile operator should be classified under specific entry i.e. ‘Telecommunication Service’ and not general entry, i.e. ‘Business Auxiliary Service’; that when international inbound and outbound roaming is covered under a specific category in the Finance Act, 1994, classification under a general category for the purpose of taxation goes against the provision of Section 65A of the Finance Act, 1994; that CBEC vide Letter F.No.137/21/2011-ST dated 19.12.2011 clarified that the International Private Leased Circuit service is not classifiable under ‘Business Support Service’ and the same will be classified under ‘Telecommunication Service’ and in this regard, further reliance is placed on the decision in the case of M/s. Infosys Technologies ltd. v. CST, Bangalore, Final Order Nos.20282, 202094 & 20293/2014. Further, it is submitted that in terms of Section 65A(2)(a) of the Finance Act, 1994, the entry providing more specific description shall be preferred over entry providing general description; that in the

8

present case, more specific description is ‘Telecommunication Service’ and therefore the present service will get covered under ‘Telecommunication Service’; that service received by assessee is not taxable under ‘Telecommunication service’ as the foreign mobile service provided is not a telegraph authority in terms of provisions of the Finance Act, 1994; that the activity which is excluded from one service cannot be taxed under any other service and in this regard, reliance is placed on the decision in the case of Mahesh Sunny Enterprise pvt.ltd. v. CST, New Delhi, 2014-VII-54-DEL-ST. In support of the above submission, the assessee has also relied upon the decision of the Hon’ble Gujarat High Court in the case of Darshan Hosiety Works v. Union of India, 1980 (6) ELT 390 (Guj), wherein a similar question arose and the Hon’ble High Court held that where a special provision deals with a particular thing or class of things, a more general provision even though its terms would cover the particular thing or class of things is excluded from application thereto by reason of the particular provision. They have also relied on the decision of the Hon’ble Supreme Court in the case of Dunlop India limited v. Union of India, AIR 1977 SC 597 and on the Hon’ble Tribunal in the case of Dr.Lal Parth Lab Private Limited v. CCE, 2006(4)STR 527(T). They have also relied on the case of Monsanto Manufacturers pvt.lltd. v. CCE, Ghaziabad, 2013(32)STR 364 (Tri-Del) and United Enterprises v. CCE & ST, Patna, 2013 (29) STR 605 (Tri-Kolkata) wherein it has been held that the most specific description shall be preferred to sub-clauses providing a more general description. In light of the above, it is submitted that when the activity carried out by the foreign mobile operator is in the nature of ‘Telecommunication Service, demand under the category of ‘Business Auxiliary Service’ is not maintainable. Even if the service are provided by the Foreign Mobile Operators to subscriber, the same cannot be charged to service tax under ‘Telecommunication Service’ or ‘Telephone Service’.

(vii) It is submitted that the service provided by the foreign mobile operators cannot be made taxable under the Act, as the Finance Act, 1994 makes only a ‘Telegraph Authority’ liable to tax under ‘Telecommunication Services’ as per Section 65(105)(zzzx). B.42 Section 65(105)(zzzx) of the Finance Act, 1994 defines the telecommunication service as:

Section-65- In this chapter, unless the context otherwise requires-(105) Taxable service means any service provided or to be provided-(zzzx) to anyperson, by the Telegraph authority in relation to telecommunication service.

-)In view of the above definition, telephone/telecommunication service provided by a ‘telegraph authority’ alone is liable to service tax.

Section 65(111) of the Finance Act, 1994 defines ‘Telegraph Authority’ as:

Section 65-In this chapter, unless the context other requires- (111) Telegraph authority has the meaning assign to it in Clause(6) of Section 3 of the Indian Telegraph Act, 1885 and includes a person who has been granted a license under the first proviso to sub-section(l) of Section 4 of that Act.

Section 3(6) of the Indian Telegraph Act, 1885, reads:(6) ’telegraph authority ’ means the Director General of [Posts and Telegraphs], and includes any officer empowered by him to perform all or any of the functions of the telegraph authority under this Act;

Foreign telecom operators have not obtained a license under the first proviso to Section 4(1) of the Indian Telegraph Act, 1885 and therefore is not a Telegraph ,. -Authority as defined under Section 65(111) of the Finance Act, 1994. Since the service is not provided by a telegraph authority therefore no service tax can be levied on the payment made by the assessee to the foreign telecom operators in the present case. Reliance is placed on the following cases:

• Infosys ltd. v. CST, Bglr 2014-TIOL-409-CESTAT-Bangalore• TCS E-Serve Ltd. v. CST, Mumbai 2014 (33) STR 641 (Tri-Mumbai)• Induslnd Media & Communication Ltd. v. CCE, Delhi 2013 (32) STR 418 (Tri-

Delhi)

Further, reliance is also placed on the Instruction F.No. 137/21/2011-ST., dated 15.7.2011 wherein it has been clarified that the services provided cannot be covered under Telecommunication Service and therefore it is clear, that under no circumstances the activities carried out by the foreign mobile operator be said to be taxable under the Finance Act, 1994. Therefore, the assessee cannot be said to be liable to pay any service tax and the demand of service tax proposed by the SCN is liable to be dropped.

(viii) The foreign mobile operators are providing the said services to the subscribers directly, thus the subscribers being the recipient of service are liable to pay service tax under reverse charge. Assuming but not conceding that the foreign mobile operators are providing telecommunication/telephony service, they are providing the same to the subscribers and not to the assessee and therefore, if at all, any one is liable to pay service tax, it is the subscribers and not the assessee, as only the service recipient is liable to pay tax under the reverse charge mechanism as per Section 66 A of the Finance Act, 1994.

To provide uninterrupted service to subscribers, the assessee had entered into agreements with various foreign telecom operators for international roaming services and call termination services under which the subscriber of the assessee goes abroad and uses the telecom network of the foreign telecom operator and the service provided by the foreign telecom operator is consumed and used in that country. This view is supported by Circular No.90/1/2007-S.T., dated 03.01.2007 wherein it was clarified that during the period of roaming, the Indian telecom service provider provides telephone service to an international in-bound roamer which is delivered and consumed in India and, therefore, it is not an export of service. International practice treats the telephone service provided to an in-bound roamer by the visited network, for the purposes of taxation, in the same manner as a telephpne service provided to any home subscriber. Accordingly, the domestic telecom operators providing roaming service to international in-bound roamers are liable to pay service tax on the amount received through the home network on account of service provided to such international roaming subscriber. It is clear from the above Circular that the Department considers the service provided by a domestic telecom service provider to in bound roaming subscribers as service delivered and consumed in India. Therefore, as a corollary it shall also follow that service provided by a foreign telecom service provider to in bound roaming subscribers in their country shall be services delivered and consumed in their respective country.The assessee has submitted that any service provided and consumed entirely outside India, cannot be considered as import of service in India, in view of the provisions of Section 64 of the Finance Act, 1994. The provisions contained in Section 64 of the Finance Act, 1994 extend to the whole of India and not beyond India and provides as under:

(ix)

(x)

10

“Extent, commencement and application:This Chapter extends to the whole of India except the State of Jammu and Kashmir. It shall come into force on such date as the Central Government may, by notification in the Official Gazette, appoint. It shall apply to taxable services provided on or after the commencement of this Chapter.

From the perusal of the above, it is clear that service tax is leviable only on specified services as defined in the Finance Act, 1994 and that the Act extends to whole of India, excluding the State of Jammu and Kashmir and the above section does not make any specific mention about the Finance Act having extra territorial applications.

The service tax is leviable only when the activity of rendering of the prescribed service takes place in the taxable territories of India. In this regard, assessee has placed reliance on the decision of the Constitution Bench of the Hon’ble Supreme Court in Bengal Immunity Co.ltd. v. State of Bihar, (1955) 2 SCR 603, which stated that the laws of a nation apply to all its subjects and to all things and acts within its territories. The Constitution Bench observed the inappropriate application of the nexus theory as settled and applicable to income tax provisions for interpreting the sales tax provisions and went to the extent of calling it an evil amongst others which was finally sought to be remedied by the Parliament by enacting Article 286 of the Constitution. The Hon’ble Supreme Court observed that to counter the evil regarding application of nexus theory on the taxing aspect of sale the Parliament substituted nexus theory with situs theory keeping in view the concept that there can be only one situs of sale unlike nexus theory where a sales transaction was being broken up into its constituents and tax was being collected by various States by creating a nexus with any of the constituents of sale. The assessee submitted that the above observations of the Constitution Bench of the Hon’ble Supreme Court in the context of sales tax provisions and legal history pertaining thereto were squarely applicable on the taxing aspect and statutory provisions for service tax also. Section 64 uses the phrase ‘This Chapter extends to the whole of India except the State of Jammu and Kashmir’ which is identical to Section 1(2) of the MRTP Act. The assessee submitted that the said phrase had been examined by the Hon’ble Supreme Court in Haridas Exports v. All India Float Glass Manufacturers’ Assn., (2002) 6 SCC 600 wherein it held as under:“In our opinion, the MRTP Commission has no extraterritorial jurisdiction. The action of an exporter to India when performed outside India would not be amenable to jurisdiction of the MRTP Commission. The MRTP Commission cannot pass an order determining the export price of an exporter to India or prohibiting him to export to India at a low or predatory price ”.

(xi)

As stated in the foregoing paragraphs, with the introduction of Section 66A any services received by a person residing in India will be a taxable service, even if service is rendered by a non-resident in India but nowhere specifies that it extends the applicability of service tax beyond India; that the effect of this Section cannot be extended to bring services rendered outside India in the service tax net but merely provides that if the services are rendered by a non-resident in India to a resident in India, they shall be deemed to be taxable service in the hands of the Indian recipient of service and the Indian recipient will be the person liable to pay service tax under Rule 2(l)(d)(iv) of the Service Tax Rules, 1994; that in the absence of Section 66A specifying that it is extending the applicability of service tax beyond India, it has to be read harmoniously with Section 64 which inter alia states that services provided in India only is taxable. The assessee has submitted that above submissions, regarding applicability of the Finance Act, 1994 to cover

(xii)

only those services, which are provided in India, is also evident from various circulars, notifications and trade notices issued by the Department which are - binding on the Department and the Department cannot take a stand contrary to their own circulars. In this regard the assessee has placed reliance on the following case laws:

"Va

> Union of India v. Arviva Industries(I) ltd. 2008(10)STR 534 (SC).> CCE, Mumbai v. Hindoostan Spinning and Wvg.M.ltd. and Anr., (2009) 14

SCC 221.> State of Tamil Nadu and Anr. V. India Cements ltd. and Anr., (2011) 40

VST225 (SC).> Kalyani Packaging Industry v. Union of India(UOI), 2004 (168) ELT 145

(SC).> Collector of Central Excise, Meerut v. Maruti Foam (P) ltd., 2004 (164) ELT

394 (SC).> CCE, Bolpur v. Ratan Melting and Wire Industries, 2008(231)ELT22(SC).

Reliance is placed on the notes on clauses of the Finance Bill, 2006 which provided that the new Section 66A is inserted with a view to levy service tax on taxable services provided from outside India and received in India and the marginal note to Section 66A of the Finance Act, 1994 is to cover only those services which are provided from outside India and received in India. The relevant text is reproduced as under:

(xiii)

Notes on clauses of the Finance Bill, 2006 relating to Insertion of Section 66A in ■ the Act:Service TaxClause 68 of the Bill seeks to amend Chapter V of the Finance Act, 1994 relating to service tax in the manner, namely:-(3) sub-clause (c)seeks to insert new Section 66A, with a view to levy service tax on taxable services provided or to be provided from outside India and received in India. ’

The assessee has also submitted that the CBEC has issued a Circular F.No.Bl/4/2006-TRU dated 19.04.2006 after introduction of Section 66A and Import of Service Rules which clarifies that for the purpose of levy of service tax the service provider must be located outside India and the service receiver must be located in India and such services must be received in India. The assessee has also placed reliance on the judgement given by the Hon’ble Delhi High Court in M/s. Orient Crafts ltd. v. Union of India & Anr., 2006 (4) STR 81 (Del.HC) wherein the Hon’ble High Court had, inter alia, upheld the validity of Section 66A and Import of Service Rules. The assessee has submitted that in this case the services are never received in India and therefore the same are not eligible to service tax within the provisions of the Finance Act, 1994 and that even after the introduction of Rule 2(l)(d)(iv) of Service Tax Rules, 1994, the Department in the circular/clarification in October, 2003 and reported in (2003) 158 ELT T23-T-37 clarified as follows:“Q 3.8) Would the service provided abroad liable for payment of Service Tax?

Ans. No, the services rendered abroad shall not attract service tax as the levy covers only the services provided within India. ”

(Further, reliance has been placed on the case of Travel Corporation(India) ltd. v. CST, Mumbai-I 2014-TIOL-1547-CESTAT-Mumbai wherein it has been held that the Finance Act authorizes the levy and collection of tax for providing a destination and consumption based taxable service but does not authorize levy and collection of tax, for a service provided and consumed beyond the Indian territory.

12

In view of the above, there is no import of service in India and therefore, the service provided by the foreign mobile operator under the international roaming arrangement would not be liable to service tax.

(xiv) If they are liable to pay service tax on the amount remitted to foreign telecom operators, service tax so paid by the assessee is admissible as credit as the said service amounts to input service for providing output service to their subscribers. It is an undisputed fact that the amount paid by the assessee to foreign telecom operators is towards roaming services availed by the subscribers of the assessee during their visit to foreign countries for which the assessee is raising bills on their subscribers towards the charges for domestic usage as well as international roaming usage; that the assessee is charging service tax from the subscribers on the total bill amount including the charges towards international roaming usage and thus, the services received from the foreign telecom operators, which is in turn used for providing taxable services to the subscribers, will qualify as input service for the purposes of Cenvat Credit. In this regard, the assessee places reliance on Rule 3(l)(ixa) of the Cenvat Credit Rules, 2004 which is inserted with effect from 18.04.2016, reads as follows:

“(ixa) the service tax leviable under section 66A of the Finance Act ”

In this regard, the assessee has placed further reliance on the Trade Notice issued by the Commissioner of Central Excise, Madurai vide Circular No.43/2008 dated 11.09.2008 which states as under:

“4. The recipient of the service is required to pay service tax under Section 66A though the service is actually provided not by the recipient but by a person located in a country other than India. Such taxable services, not being actually provided by the person liable to pay service tax, are not treated as ‘output services ’for the purpose of Cenvat Credit Rules, 2004. However, service tax paid under Section 66AO(sic) (Section 66A) is available as ‘input credit' under Cenvat Credit Rules, 2004 provided the said services are used as input services by the manufacturer or producer offinal products or a provider of output taxable service. ”

Similarly, a clarification was issued by the Commissioner of Central Excise and Service Tax, Jamshedpur vide Trade Notice No.21/JAM/2008(S.Tax), dated 6.8.2008. The assessee further placed reliance on the CBEC Circular F.No.B 1/4/2006, dated 19.04.2006 [2006(2) STR.C5] which clarified the admissibility of Cenvat credit of service tax paid under Section 66A on the taxable services provided from outside India and received in India and used as input services for the taxable outputs, as follows:“4.2.13 the treatment of the recipient of service, as the deemed service provider under Section 66A is only for the purpose of charging service tax on the taxable services received from outside the country. Services provided from outside India and received in India, therefore, not treated as taxable service provided by the recipient for the purpose of Cenvat Credit Rules, 2004. However, where such service is used as an input for providing any taxable output, the service tax paid on such service can be taken as input credit. ”

The assessee further placed reliance on the clarification issued by the Department vide Circular No.F.No.354/148/2009-TRU dated 16.07.2009 wherein it has been clarified that Service Tax paid under Section 66A of the Finance Act, 1994 is admissible as credit; that the assessee is eligible to avail Cenvat credit of service tax paid in terms of Section 66A of the Act. The assessee has submitted that no tax can be demanded in case of a revenue neutral situation and has relied on the

decision in the case of Jay Yuhsin Ltd. v. Commissioner of Central Excise, New Delhi, 2000(119) ELT 718 (Tribunal-LB). Therefore, it is submitted that it is a 4 clear case of revenue neutral situation and therefore the demand under the SCN is liable to be dropped. The assessee has relied on the following judgements wherein it has been held that once the tax payable is availed as credit, thereby making the entire exercise revenue neutral, there is no question of any demand of tax and therefore the proceeding initiated by the SCN is liable to be dropped on this ground alone.

* -*»■

> International Audit ltd. v. CCE, 2005(183) ELT 239(SC).> CCE v. Narayan Polyplast ltd., 2005(179) ELT 20(SC).> CCE v. Narmada Chematur Pharma, 2005(179) ELT 276(SC).> CCE v. Coca-Cola India pvt.ltd., 2007 (213) ELT 490 (SC).> CCE v. Jamshedpur Beverages, 2007 (214) ELT 321 (SC).

Without prejudice to the above and presuming without admitting, that even if any service tax is payable, the payments made by the assessee cannot be taken as the value of the taxable service as it would be inclusive of the amount of service tax; that in the case of excise duty also, it has been held that the amount received should be taken as cum-duty price and the value should be derived there from, by excluding the duty alleged to be payable as required under Section 4(4)(d)(ii) of the Central Excise Act, 1944. In support of this the assessee relied on the Larger Bench decision of the CESTAT in the case of Sri Chakra Tyres, 1999 (108) ELT 361 which has been affirmed by the Hon’ble Supreme Court as the departmental appeal has been dismissed vide Order dated 26.02.2002 reported in 2002 (141) ELT A279 (SC). The assessee also relied on the decision of the Hon’ble Supreme Court in the case of CCE v. Maruti Udyog limited, 2002 (49) RLT 1 (SC), wherein it has been held that the deduction under Section 4(4)(d)(ii) is allowable, even in situations where no duty was paid at the time of removal. The assessee further placed reliance on the case of Commissioner v. Advantage Media Consultants 2009 (14) STR J49 (SC) wherein it has been held that Service tax being an indirect tax, was borne by consumer of goods/services and the same was collected by assessee and remitted to Government and total receipts for rendering services should be treated as inclusive of Service Tax due to be paid by ultimate customer unless Service Tax was paid separately by customer. Furthermore, Section 67(2) of the Finance Act, 1994 states that consideration shall include the service tax paid or payable along with the said consideration. Hence, in light of the above, it is clear that for service tax calculation, the amount paid by the assessee should be considered as cum tax payment and service tax should be calculated accordingly.

(xv)

(xvi) The show cause notice has proposed to recover interest under Section 75 of the Act. The SCN further proposes to impose penalty under Section 76, 77(2) and 78 of the Act. The recovery of interest under Section 75 of the Finance Act, 1994 is not sustainable since the Service Tax itself is not payable and the assessee has not contravened any of the provision of the Act. A bare perusal of Section 75 of the Finance Act, 1994 shows that when a person who is liable to pay service tax as per the provisions of Section 68 of the Finance Act, 1994, fails to pay service tax then the person is liable to pay interest at the prescribed rate. However, assessee is not liable to pay service tax on the International Outbound Roaming Services provided by the foreign mobile operators from outside. India based on the submissions made above and therefore, the interest is not recoverable from the assessee since the service tax itself is not payable on the same amount.

(xvii) The assessee has not contravened any of the provisions of the Act and therefore, no penalty is imposable under Sections 76, 77(2) & 78 of the Act. In any case, no

14

penalty is imposable as service tax itself is not payable by the assessee. Further, for imposing penalty, there should be an intention to evade payment of service tax, or there should be suppression or concealment of the value of taxable services; that the assessee was always under bonafide belief that the services received by them are not taxable and such bona fide belief was based on the grounds given above and the assessee had no intention to evade payment of service tax as mentioned in the grounds above, therefore, no penalty was imposable. Further, there is no allegation in the SCN that assessee has suppressed the facts from the Department. In support of their view, reliance has been placed on the decision of the Hon’ble Supreme Court in the case of Hindustan Steel ltd. v. The State of Orissa reported in AIR 1970 (SC) 253. The above decision of the Apex Court, was followed by the Tribunal in the case of Kellner Pharmaceuticals ltd. v/s. CCE, reported in 1985 (20) ELT 80, and it was held that proceedings under Rule 173Q are quasi-criminal in nature and as there was no intention on the part of the assessee to evade payment of duty, the imposition of penalty cannot be justified and the ratio of these decisions applies in all force to the present case. In the present case, there was no intention to evade payment, hence no penalty can be proposed on the assessee. As regards penalty under Section 78, the assessee has submitted that the SCN nowhere states that there was any intention on the part of assessee to evade payment of service tax but the SCN has merely proposed to impose penalty under Section 78 without giving any reason; that the assessee did not commit any positive act for evading service tax; that the department was aware of all the activities undertaken by the assessee ever since the first SCN was issued to the assessee and therefore, since there was no intention to evade payments of Service tax, penalty under Section 78 of the Act cannot be imposed on the assessee. SCN proposing penalty under Section 78 of the Act is liable to be dropped on this ground alone. Reliance has been placed on the following case laws:

• Shree Renuka Sugars ltd. v. CCE 2007 (210) ELT 385 (Tri.-Bang.)• Jalla Industries v. CCE 2000 (117) ELT 429 (Tri.Mum)• Rivaa Textile Inds. Ltd. v. CCE 2006 (197) ELT 555 (Tri.-Mum)• CCE v. Syncom Formulation ltd. 2004 (172) ELT 77 (Rei.Del.)• Hyderabad Polymers(P)ltd. v. CCE 2004 (166) ELT 151 (SC)• Nizam Sugar Factory v. CCE 2006 (197) ELT.465 (SC)

The assessee has further submitted that for imposing penalty, there should be an intention to evade payment of tax, or there should be suppression or concealment; that there is no suppression or concealment on behalf of the assessee as the assessee communicated all the information required by the department; that the figures are coming out of the balance sheet and it is submitted that the balance sheet is a public document and therefore, no question of suppression or concealment arises at all. Also, there is no allegation in the SCN that the assessee has suppressed the facts from the Department.

(xviii) The present demand is pursuant to an audit objection raised by the audit team and all details and documents were verified by the audit team; that any queries raised by the audit team were properly answered by the assessee and therefore, there was

question of any suppression of facts or intent to evade payment of tax to impose the penalty and when the demand is based on audit objection, there cannot be any suppression on the part of the assessee. The assessee relied on the following judgements wherein consistently it was held that when the duty demand is based on an audit objection, there cannot be any allegation of suppression:

no

> CCE v. Punjab Chem & Pharm, 2001 (135) ELT 227

> Asia Automative ltd. v. CCE, 1999 (113) ELT 841> Nadiad Silicate & Chem v. CCE, 1995 (80) ELT 891> Haryana Co-op Sugar v. State, 1997 (107) STC 103> Indian & Eastern Newspaper v. CIT, 1979 (4) SCC 248> Bharat Agriculture & Mechanical Engg.Co. v. State of Bihar, 2006 (148)

STC 372 (Patna)> Shree Uma Foundries pvt.ltd. v. CCE, 2008 (222) ELT 317

V

Further, the assessee had disclosed the information relating to payment made to foreign mobile operators in their Balance Sheets and the Department had gathered information about the payments received and made by the assessee from the above said public documents. Therefore, suppression/malafide intention cannot be invoked if the demand is sought to be made based on information contained in public documents. In this regard, reliance is placed on the following judgements:

(xix)

> Anantpur Textiles ltd. v. CCE 1994 (72) ELT 48 (Tri.)> Hindalco Industries ltd. v. CCE 2003 (161) ELT 346 (Tri.)> Kirloskar Oil Engines ltd. v. CCE 2004 (178) ELT 998 (Tri.)

The assessee has submitted that, the present c issue involves interpretation of complex legal provisions and in some Commissionerates, the service tax demand is raised under ‘Telecommunication Service’. In this regard reliance is placed in the case of M/s. Vodafone Digilink from Jaipur Commissionerate. Therefore, imposition of penalty is not warranted in the present case. In this regard, reliance is placed on the following judgements:

> Ispat Industries ltd. v. CCE, 2006 (199) ELT 509 (Tri.-Mum)> Secretary, Twon Hall Committee v. CCE, 2007 (8) STR 170 (Tri.-Bang.)> CCE v. Sikar Ex-serviceman Welfare Coop Society ltd., 2006 (4) STR 213

(Tri.-Del)> Haldia Petrochemicals ltd., v. CCE, 2006 (197) ELT.97(Tri.-Del.)> Siyaram Silk Mills ltd. v. CCE, 2006 (195) ELT 284 (Tri.-Mumbai)> Fibre Foils ltd. v. CCE 2005 (190) ELT 352 (Tri.-Mumbai)> ITELIndustriespvt.ltd.v. CCE, 2004 (163) ELT 219 (Tri.-Bang) ,

The assessee was of the opinion that no service tax is payable on the international roaming services provided by the foreign mobile operators and the bona-fide belief of the assessee is based on the submission made above. Thus, the assessee solely acted on the bona-fide belief and have relied on the following case laws in support of their contention that in case the assessee was under a bona-fide belief, then there cannot be said to be any suppression:

(xx)

> CCE v. Vineet Electrical Industries pvt.ltd. 2002 (144) ELT A292> CCE v. Raptakos Brett & Co. 2006 (194) ELT 101 (Tri.-Mum)> CCE v. Rishabh Velveleen (P) ltd. 1999 (114) ELT 839 (Tri.)> Pee Jay Apparels (P) ltd. v. CCE 2001 (135) ELT 842 (Tri.-Del)> Cosmic Dye Chemical v. CCE 1995 (75) ELT 721 (SC)

(xxi) Penalties under Section 76 and 78 of the Act cannot be simultaneously imposed as they are mutually exclusive i.e. Section 78 is applicable if the non-payment of service tax is due to reasons specified therein with an intention to evade payment of service tax whereas Section 76 is applicable in cases other than those covered under Section 78 of the Act. In this regard, reliance is also placed on the following cases:

16

> CST, Bangalore v. Motor World - 2012 (27) SIR 225 (Kar)> The Financers v. CCE, Jaipur -2007 (8) STR 7 (Tri.Del),> CCE, Ludhiana v.Silver Oak Gardens Resort 2008 (9) STR 481 9Tri.-Del.)> Commissioner of Central Excise, Ludhiana v. Pannu Property Dealers & Ors

2009(14) STR 687

(xxii) Section 80 provides that no penalty shall be imposed on the assessee for any failure if the assessee proves that there was reasonable cause for the said failure; that the Finance Act, 1994 statutorily provides for waiver of penalty and the penal provisions are to be taken only as safeguard against contravention and in the present case there was a reasonable cause for non payment of service tax which is evident from the submissions made above. In view of the foregoing, the proposals to invoke the penal provisions of Section 76, 77(2) & 78 of the Finance Act, 1994 are liable to be dropped. In this regard, reliance is placed on the following judgements:

> ETA Engineering ltd. v. CCE, Chennai, 2004 (174) ELT 19 (Tri-LB)> Flyingman Air Courier pvt.ltd. v. CCE 2004 (170) ELT 417 (Tri.-Del.)> Star Neon Singh v. CCE, Chandigarh 2002 (141) ELT 770 (Tri.-Del.)> Medpro Pharma pvt.ltd. v. CCE 2006 (4) STR 322 (Tri.-Del)

In the light of the above submissions, the assessee submitted that the interest proposed to be recovered and penalty proposed to be imposed in the SCN is liable to be dropped.

Original Adjudication:

The adjudicating authority discussed that the assessee has received service from other telecom operators located beyond geographical area of the assessee’s network, as per roaming agreements between the two, which falls under the erstwhile category ‘Business Auxiliary service’ as defined under Section 65(19) and as specified as a taxable service under Section 65(105)(zzb) of the Finance Act, 1994; that whenever subscribers of the assessee visit foreign lands, international roaming ensures that they get uninterrupted connectivity and for this purpose, assessee engages other telecom operators; that it is alleged that overseas operators provide service to the assessee’s subscribers and charge to the assessee as per agreed tariff rates, and therefore service rendered by overseas operators amounts to providing ‘Business Auxiliary Service’ to the assessee. Assessee’s liability to pay service tax arises in terms of Section 66A of the Finance Act, 1994 and Rule 2(l)(d)(iv) of the Service Tax Rules, 1994. It is also alleged in the show cause notice that during the period from April, 2012 to June, 2012, the assessee has paid an amount of Rs.8,32,85,434/- to overseas telecom operators as roaming charges on which a total service tax of Rs. 1,02,94,080/- was payable.

11.

12. The adjudicating authority has discussed the contentions of the assessee as well as his findings, as under:

The assessee has argued that SCN has been issued merely on the basis of audit objection without independent application of mind. It may be true that the issue was first detected during audit process and subsequently show cause notices were being issued, the present SCN being fourth in the series. The audit presently is a detailed process wherein records of the assessee are examined in detail and wherever discrepancies are noticed, show cause notices are issued. Audit reports are based on assessee’s records and are normally self contained and accompanied by relied upon documents hardly necessitating further inquiry. In the liberalized era of self assessment, this

(i)

practice of issuing show cause notices based on audit objections is a well accepted practice as objections raised during audit go through a vetting 5 process. I therefore do not find any force in the assessee’s argument that the show cause notice should be dropped on this ground alone.

(ii) The assessee contends that the arrangement between the assessee and foreign mobile operators does not amount to business auxiliary service as foreign telecom operators are providing service to the subscribers and that foreign mobile operators are not providing any service on behalf of the assessee but are providing service directly to the subscribers, whereas, in terms of clause(iii) and (vi) of the definition of ‘Business Auxiliary Service’, the service provider should act as an agent of the client and undertake any service on behalf of the client. The service provided directly to the subscribers, according to the assessee, is classifiable under Telecommunications services and not under Business Auxiliary services. As per the roaming process described by the assessee, when a subscriber turns on the mobile device outside the home network (assessee’s domestic network), the new visited network identifies the said device as not registered with its own system and thus attempts to identify its home network. Had assessee been a direct receiver of service from the foreign operator, the visited network (network of foreign telecom operator) would have identified the mobile device. Further, if there is roaming agreement between the domestic operator (assessee) and foreign operator, visited network will not provide interconnection, which suggests that even the foreign operator is allowing the subscriber use its network and in this case, the client is the assessee and not the subscriber. Further, for allowing its network to be used by the subscriber of the assessee, foreign operator is charging to the assessee and not the subscriber. Foreign operator may deny the usage of its network on the advice of the assessee. All this clearly suggests that foreign telecom operator is providing service to the subscriber on behalf of the assessee and not to the subscriber directly.

(iii) The assessee contented that foreign operator has right to suspend its services to the subscriber in circumstances where it would suspend or terminate services to its own subscribers, that had the foreign operator been acting on behalf of the assessee it would not have had the right to suspend or terminate the services of roaming subscribers without authorization from the assessee, This, according to the assessee, shows that the foreign operator is providing services to the roaming subscriber directly, on a principal to principal basis. This argument of the assessee fails to make any impact because some of the circumstances listed by the assessee, under which, the services can be suspended or terminated, are also applicable to foreign operator’s own subscribers. The circumstances appear standard in nature, for example, subscriber using defective or illegal equipment, or suspected fraudulent or unauthorized use. The circumstances are such that under such circumstances any network may suspend or terminate the services and there is no distinction between the subscribers of the assessee and the foreign operator’s own subscribers as far as these circumstances are concerned. I therefore do not agree with this contention.

(iv) The assessee further argues that subscribers may not receive identical services from the foreign mobile operator as it would from the assessee, that had the foreign operator been acting on behalf of the assessee, it would be obligated to provide the same services as the assessee itself would be providing. Therefore, according to the assessee, foreign operators treat the

18

subscribers as their own temporary subscribers and accordingly subscribers are getting the services directly from the foreign operators and not on behalf of the assessee. In this regard I note that the services provided by the foreign operators are not substantially different from the services provided by the assessee as recorded in clause 6 of the Agreement reproduced by the assessee. It is an accepted fact that quality of service may differ from operator to operator due to various reasons and that cannot be a ground to argue that foreign operator is providing services directly to the roaming subscriber.

(v) With regard to the assessee’s submission that services provided by foreign mobile operators are in the nature of telecommunication services, I note that in terms of Section 65(105)(zzzi) of the Finance Act, 1994, taxable service means any service provided or to be provided to any person, by the telegraph authority has the meaning assigned to it in clause(6) of section 3 of the Indian Telegraph Act, 1885 and includes a person who has been granted a license under the first proviso to sub-section (1) of section 4 of the Act. Section 3(6) of Indian Telegraph Act, 1885 reads as follows-telegraph authority means the Director General of (Posts and Telegraph), and includes any officer empowered by him to perform all or any of the functions of Telegraph Authority under this Act. From the definitions quoted, it is clear that foreign mobile operator is not a Telegraph Authority as they do not hold any license under the Indian Telegraph Act, 1885, and consequently, services provided by foreign mobile operator cannot be classified as telecommunication services as specified under Section 65(105)(zzzi) of the Finance Act, 1994.

(vi) The ‘Business Auxiliary Service’, under which the impugned services are sought to be classified as per show cause notice, have been defined under Section 65(19) of the Finance Act, 1994 as under-

‘Business Auxiliary Service ’ means any service in relation to,- Promotion or marketing or sale of goods produced or provided by or belonging to the client; or

(ii) Promotion or marketing of service provided by the client; or

0)

[explanation - For the removal of doubts, it is hereby declared that for the purposes of this sub-clause, “service provided in relation to promotion or marketing of service provided by the client, ” includes any service provided in relation to promotion or marketing of games of change, organized, conducted or promoted by the client, in whatever for or by whatever name called, whether or not conducted online, including lottery, lotto, bingo;](Hi) any customer care service provided on behalf of the client; or(iv) procurement of goods or services, which are inputs for the client; or

[Explanation - For the removal of doubts, it is hereby declared that for the purposes of this sub-clause, "inputs" means all goods or services intended for use by the client;]

(v) production or processing of goods for, or on behalf of the client; or(vi) provision of service on behalf of the client; or(vii) a service incidental or auxiliary to any activity specified in sub-clauses (i) to (vi), such as billing, issue or collection or recovery of cheques, payments, maintenance of accounts and remittance, inventory management,

evaluation or development of prospective customer or vendor, public relation services, management or supervision, and includes services as a * commission agent, but does not include any activity that amounts to "manufacture " of excisable goods.

Explanation - For the removal of doubts, it is hereby declared that for the purposes of this clause, -

(a) "Commission Agent" person who acts on behalf of another person and causes sale or purchase of goods, or provision or receipt of services, for a consideration, and includes any person who, while acting on behalf of another person -(i) deals with goods or services or documents of title to such goods or services; or .(ii) collects payment of sale price of such goods or services; or(Hi) guarantees for collection or payment for such goods or services; or (iv) undertakes any activities relating to such sale or purchase of such goods or services;

a*

The relevant fact of the case is that the assessee has engaged the foreign mobile operator to provide uninterrupted service to its subscribers who visit foreign lands and foreign operators charge the assessee on agreed tariff rates. The foreign operator therefore is providing services to assessee’s visiting subscribers on behalf of the assessee only and for that reason, the services provided fall in the category of services specified in clause (iv) and (vi) of the definition of business auxiliary service as reproduced above.

(vii) With regard to the assessee’s contention that the liability to pay service tax is on subscribers as the foreign operators have provided telecommunication service to the subscribers, it has been already discussed that there are agreements between the assessee and foreign mobile operators for provision of service to the visiting subscribers and it is the assessee who is making payments in foreign currency for roaming services provided by foreign operators. The visiting subscribers have neither entered into any agreement with the foreign mobile operators nor have they made any payments to the foreign operators so as to establish any direct relationship between the subscribers and foreign mobile operators. Therefore, the assessee is the service recipient in this case and in terms of reverse charge mechanism assessee is liable to discharge the service tax liability as a recipient of service.

(viii) The assessee has further contended that the service provided by the foreign mobile operators has been received and consumed outside India and therefore Section 66A has no application in the present case. Section 66A was introduced in the Finance Act, 2006 and contained provisions relating to import of services in India. The Section prescribed the situations under which a service would be considered as imported in India and thus recipient of service would be liable to pay tax. For ease of ready reference, I reproduce the section as under-

66A. Charge of service tax on services received from outside India - (1) Where any service specified in clause(105) of section 65 is, - (a) Provided or to be provided by a person who has established a business or has a fixed establishment from which the service is provided or to be

20

provided or has his permanent address or usual place of residence, in a country other than India, and(b) Received by a person(hereinafter referred to as the recipient) who has his place of business, fixed establishment, permanent address or usual place of residence, in India,

Such service shall, for the purposes of this section, be taxable service, and such taxable service shall be treated as if the recipient had himself provided the service in India, and accordingly all the provisions of this Chapter shall apply:

Provided that where the recipient of the service is an individual and such service received by him is otherwise than for the purpose of use in any business or commerce, the provisions of this sub-section shall not apply:

Provided further that where the provider of the service has his business establishment both in that country and elsewhere, the country, where the establishment of the provider of service directly concerned with the provision of service is located, shall be treated as the country from which the service is provided or to be provided.

(2) Where a person is carrying on a business through a permanent establishment in India and through another permanent establishment in a country other than India, such permanent establishments shall be treated as separate persons for the purposes of this section.

Explanation 1.- A person carrying on a business through a branch or agency in any country shall be treated as having a business establishment in that country.

Explanation 2. — Usual place of residence, in relation to a body corporate, means the place where it is incorporated or otherwise legally constituted.

The assessee’s contention is that the provision of service has taken place outside the taxable territory of India, hence no service tax levy is attracted. I, however, find that foreign mobile operators, having no fixed establishments in India, have provided service to the assessee, who, being recipient of service with its place of business, fixed establishment, permanent address and usual place of residence in India, is liable to pay the service tax in terms of Section 66A ibid. Further, in a reverse case of telecom operators in India providing roaming services to international inbound subscribers, Mumbai Tribunal has held in the case of Vodafone Essar Cellular Limited v. CCE Pune-III [2013 (31) STR 738 (Trib.-Mumbai)] that such arrangement of provision of roaming services to international inbound subscribers would not amount to export of services. By same analogy, the roaming services provided by foreign mobile operators to Indian subscribers visiting foreign lands would amount to import of services, and accordingly, service tax levy is justified in terms of Section 66A ibid.

(ix) The assessee has further argued that the entire exercise is revenue neutral as the service tax paid by them would be available to them as Cenvat credit. The availability of Cenvat credit on input services is subject to the provisions of Cenvat Credit Rules, 2004 and this cannot be decided in the present proceedings. Moreover, if the assessee’s argument of revenue neutrality is considered then every case where Cenvat is available would be

a case of revenue neutrality and that would render the Cenvat Credit Rules, 2004 redundant. Hence, I do not concur with this argument of the assessee. A decision of Mumbai Tribunal in the case of Safe & Sure Marine Services Pvt. Ltd. v. CCE [2012(28) STR 30(Trib.-Mumbai)] is worth mention in the context of revenue neutrality, wherein Hon’ble Tribunal observed as under-

*4

The appellant has also argued that as far as M/s. SICAL is concerned, after 1-5-2006, M/s. SICAL has discharged the Service tax liability on the entire amount and, therefore, they are not required to pay Service Tax as they are only sub-contractors. This argument is totally incorrect especially in the context of a Value Added Tax Regime, which is in force in India. Under the Value Tax regime, which applies to Service Tax also, the provider of taxable service has to discharge the Service tax liability and if such services are used as input services by other service provider or manufacturer of the goods down the line, they can avail input service credit on the service tax paid by the input service provider. There is no exemption on input service credit on the service provider under the law. The entire scheme of invoice based Value Added Tax, which is in force, envisages payment of tax at each stage of taxable event and availment of credit of tax so paid at the subsequent stage. If this tax regime, which is in force, has to be given any meaningful effect, then it is mandatory that the Service Tax liability is discharged as and when taxable services are rendered by the service provider.

The assessee has also disputed the calculation of tax liability stating that service tax if at all payable is incorrectly calculated by the department as the value taken for calculation of service should be considered inclusive of service tax. In this regard, I note that sum tax benefit sought by the assessee is applicable where it is established from the records/documents that the value charged is in fact inclusive of service tax. In the present case, it is by virtue of Section 66A of the Finance Act, 1994 that the assessee has become liable to pay service tax on the charges paid to foreign mobile operators, hence there is no question of inclusion of service tax in the charges paid to service providers. Also, the assessee at all times has believed that there is no levy of tax applicable in the case, then where is the question of including the service tax in the charges paid to the service providers. Thus, I do not find any incorrectness in the tax calculation.

(x)

(xi) In view of the foregoing discussion, I find that the service tax of Rs.l,02,94,080/-(inclusive of Education cess) demanded in the show cause notice dated 19.05.2014 was payable by the assessee for the period April- 2012 to June-2012 and since assessee has failed to pay, it is liable to be recovered under Section 73(1) of the Finance Act, 1994. Further, since there is obvious delay in payment of service tax, I also find that the assessee liable to pay interest in terms of Section 75 of the Finance Act, 1994 for delay in payment of service tax as proposed in the show cause notice.

(xii) The show cause notice has further proposed penalties under Section 76, 77(2) and 78 of the Finance Act, 1994. As far as penalties under Section 76 and 78 are concerned, the amended penalty provisions as amended from 14.05.2015, would apply here in view of transitional provisions of Section 78B of the Finance Act, 1994, according to which the amended penalty provisions shall apply in the cases of pending adjudication as on 14.05.2015. As per amended provisions, penalty of Section 78 is attracted where service tax has not been paid by reason of fraud, collusion, suppression of facts etc.

22

which are necessary ingredients for invoking proviso to Section 73(1) of the Finance Act, 1994, whereas penalty of section 76 is attracted in other cases, i.e., other than the cases of fraud, collusion etc. The present show cause notice dated 19.5.2014 is a periodic demand notice, invocation of proviso to Section 73(1) is not justified and resultantly, penalty under Section 78 cannot be imposed. Penalty provisions of Section 76 are, however, clearly invokable considering the case of non-payment of service tax by reason other than fraud, suppression of facts, etc. and accordingly, I find that the assessee is liable to pay penalty under amended Section 76 of the Finance Act, 1994. With regard to penalty under Section 77 of the Finance Act, 1994, it is a fact that the assessee has failed to self assess the service tax demanded in the notice and declare the same in the service tax return filed for the relevant period. This is in contravention of the provisions of Section 70 of the Finance Act, 1994 and Rule 7 of the Service Tax Rules, 1994. Since such a contravention attracts penalty provisions of Section 77(2) of the Finance Act, 1994,1 find that assessee is liable to pay penalty under Section 77(2) of the Finance Act, 1994.

In view of the above, the Joint Commissioner vide OIO No:AHM-SVTAX-000- JC-033-16-17 dated 28.02.2017 confirmed the service tax demand of Rs. 1,02,94,080/- under Section 73(1) of the Finance Act, 1994 alongwith interest under Section 75 of the Finance Act, 1994, imposed a penalty of Rs. 10,29,408/- under Section 76 of the Finance Act, 1994 and a penalty of Rs. 10,000/- under Section 77(2) of the Finance Act, 1994.

13.

Being aggrieved with the aforesaid decision, the assessee preferred appeal before the Commissioner (Appeals), Central Tax, Ahmedabad. The Commissioner (Appeals), Central Tax, Ahmedabad, vide Order-in-Appeal No.AHM-EXCUS-001- APP-002-18-19 dated 06.06.2018, issued from F. No.V2(ST)46/Ahd-II/2017-18, allowed the appeal by way of remand with a direction to the adjudicating authority to examine the facts of the case in the light of the Hon’ble Delhi Tribunal’s order cited at 2017(6)GSTL67(Tri.-Del.).

14.

Denovo Proceedings:

In pursuant to the order in Appeal by the Commissioner (Appeals), the matter

has been taken up for adjudication afresh, as directed by the Commissioner (Appeals), Central Tax, Ahmedabad.

15.1 I find that the said assessee was earlier registered under the Jurisdiction of the Commissioner of Service Tax, Ahmedabad. Consequent to the issue of the Notification No. 12/2017-Central Excise (NT) to 14/2017-Central Excise (NT) all dated 09.06.2017, appointing the officers of various ranks as Central Excise officers & reallocating the jurisdiction of the Central Excise Officers and Trade Notice No. 001/2017 dated 16.06.2017 issued by the Chief Commissioner, Central Excise & Service Tax, Ahmedabad Zone, the said assessee is now registered under the Jurisdiction of the Commissioner, Central Goods and Service Tax, Ahmedabad South.

15.

15.2 I find that the Hon’ble Commissioner (Appeals) has observed as under:

“(5. / find that the issue to be decided in the instant case is whether the service tax liability arises under reverse charge mechanism on the roaming

charges paid by the appellant to foreign telecom operator under business auxiliary services.

*4.

7. First of all, 1 find that the issue in question is a part of various periodical demands raised against the appellant. In the demands for other periods, the appellant contested the Order-in-Original successfully before the CESTAT and the Tribunal, vide it’s order No.ST/A/55606/2017-CU(DB), dated 26.07.2017 in Appeal No.ST/51934/2014-CU(DB) cited at 2017(6)G.S.T.L.67 (Tri.-Del) set aside the demand. Further I find that the