Embed Size (px)

Citation preview

AHG - Australia’s largest automotive retailer

About AHG• Automotive retail and logistics group founded in 1952• Largest automotive retailer in Australia by sales, profitability

and market capitalisation– 103 high profile passenger and commercial vehicle

dealerships throughout Australia– Franchises covering 10 of the top 11 selling automotive

brands– Diversified income in new and used cars, service, parts,

finance and insurance• Other revenue streams from logistics

– Amcap Distribution Centre– Rand Transport– KTM Sportmotorcyles– VSE/GTB

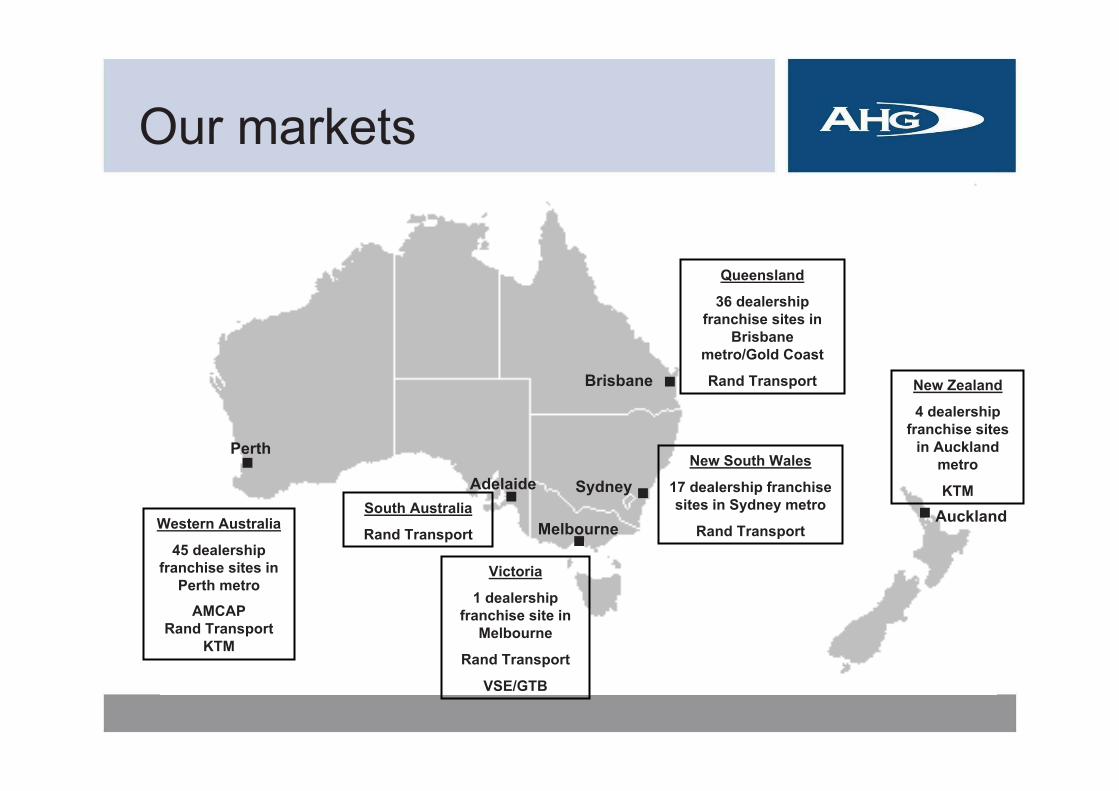

Our markets

PerthNew South Wales

17 dealership franchise sites in Sydney metro

Rand Transport

Brisbane .Queensland

36 dealership franchise sites in

Brisbanemetro/Gold Coast

Rand Transport New Zealand

4 dealership franchise sites

in Auckland metro

KTM.Auckland

.Western Australia

45 dealership franchise sites in

Perth metro

AMCAP Rand Transport

KTM

.Melbourne. .

Victoria

1 dealership franchise site in

Melbourne

Rand Transport

VSE/GTB

SydneyAdelaideSouth Australia

Rand Transport

Financial overview

¹ from continuing operations excluding impact of unusual items * Broker Forecast (average)

0

1000

2000

3000

4000

FY06 FY07 FY08 FY09

$m

Revenue¹

0102030405060

FY06 FY07 FY08 FY09 FY10*

$m

NPAT¹

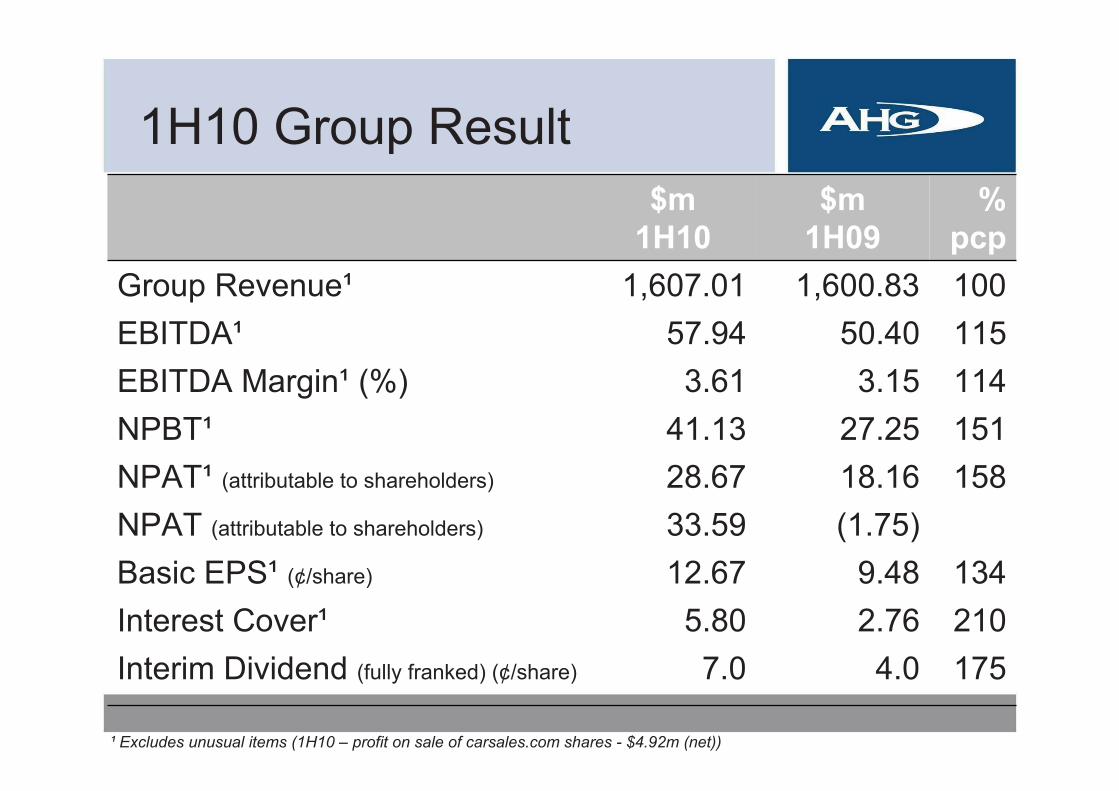

1H10 Group Result

¹ Excludes unusual items (1H10 – profit on sale of carsales.com shares - $4.92m (net))

$m1H10

$m1H09

%pcp

Group Revenue¹ 1,607.01 1,600.83 100EBITDA¹ 57.94 50.40 115EBITDA Margin¹ (%) 3.61 3.15 114NPBT¹ 41.13 27.25 151NPAT¹ (attributable to shareholders) 28.67 18.16 158NPAT (attributable to shareholders) 33.59 (1.75)Basic EPS¹ (¢/share) 12.67 9.48 134Interest Cover¹ 5.80 2.76 210Interim Dividend (fully franked) (¢/share) 7.0 4.0 175

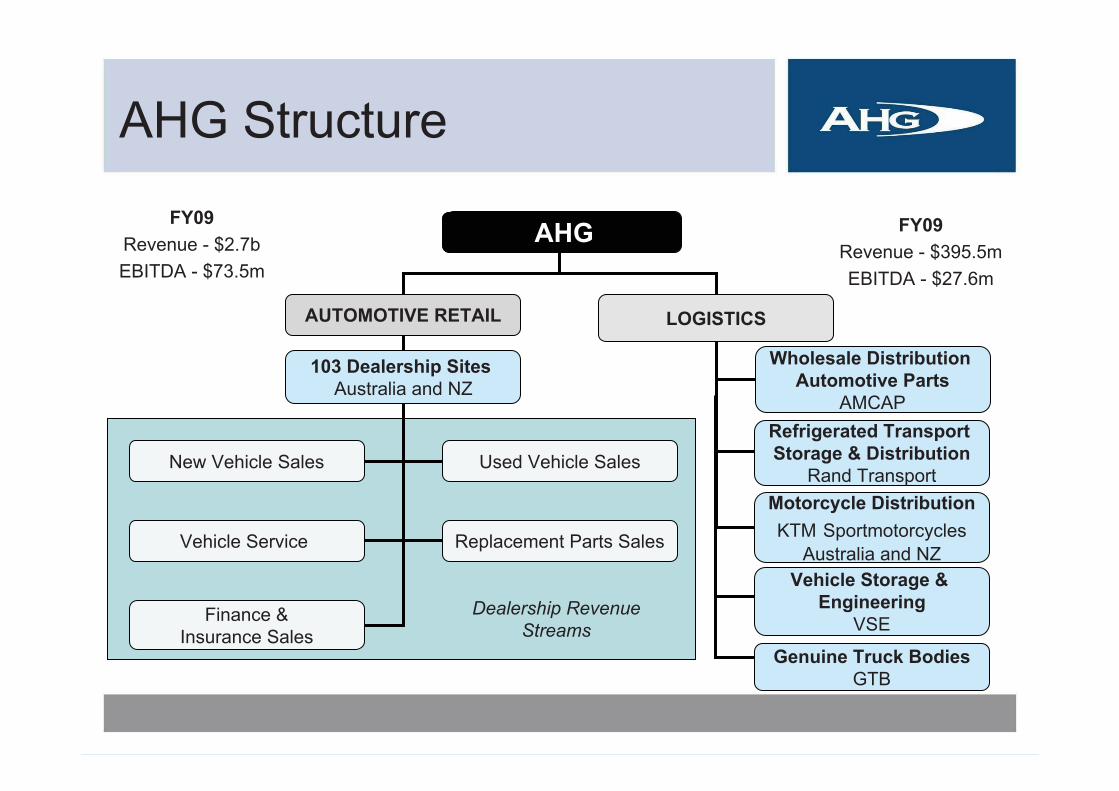

AHG Structure

AHG

AUTOMOTIVE RETAIL

New Vehicle Sales Used Vehicle Sales

Vehicle Service Replacement Parts Sales

Finance &Insurance Sales

103 Dealership Sites Australia and NZ

LOGISTICS

Wholesale Distribution Automotive Parts

AMCAP

Motorcycle DistributionKTM Sportmotorcycles

Australia and NZ

Dealership Revenue Streams

FY09Revenue - $2.7bEBITDA - $73.5m

FY09Revenue - $395.5mEBITDA - $27.6m

AHG

Vehicle Storage & Engineering

VSE

Refrigerated Transport Storage & Distribution

Rand Transport

Genuine Truck BodiesGTB

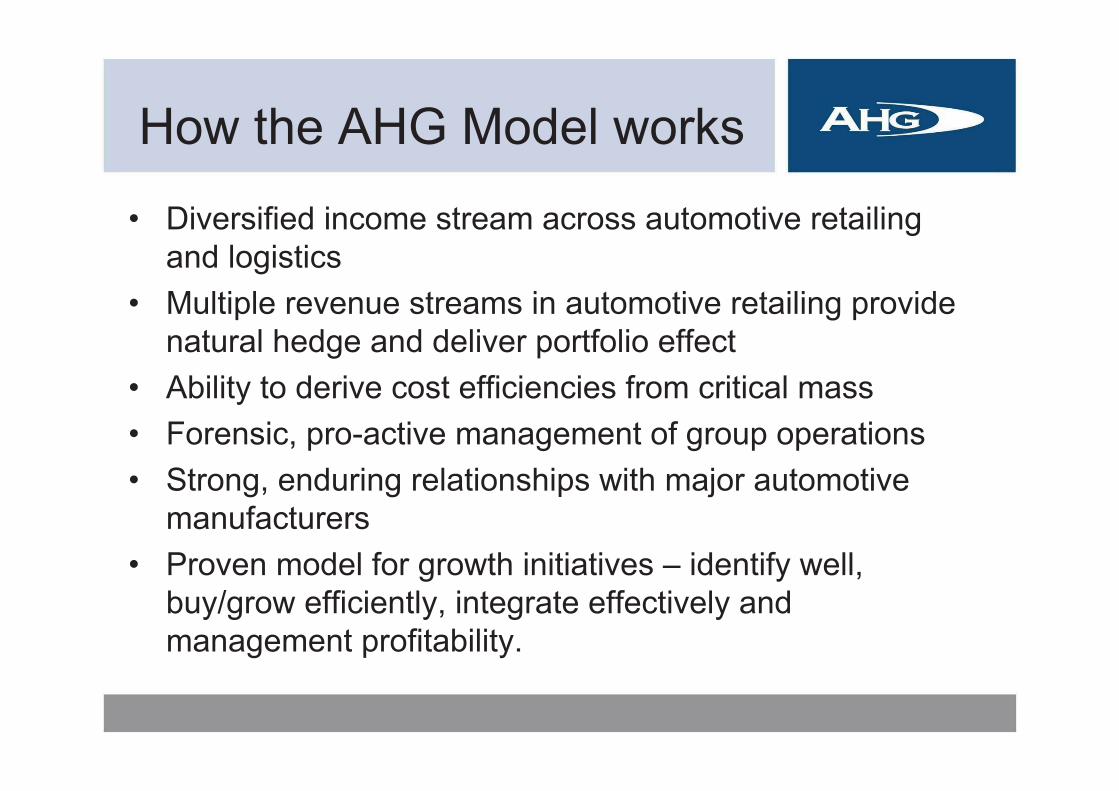

How the AHG Model works

• Diversified income stream across automotive retailing and logistics

• Multiple revenue streams in automotive retailing provide natural hedge and deliver portfolio effect

• Ability to derive cost efficiencies from critical mass• Forensic, pro-active management of group operations• Strong, enduring relationships with major automotive

manufacturers• Proven model for growth initiatives – identify well,

buy/grow efficiently, integrate effectively and management profitability.

Automotive

Automotive

• Strong and experienced management team

• Strict processes and controls

• Continue to implement best practices

• Continued organic and greenfield growth

• Strong balance sheet facilitates acquisition opportunities

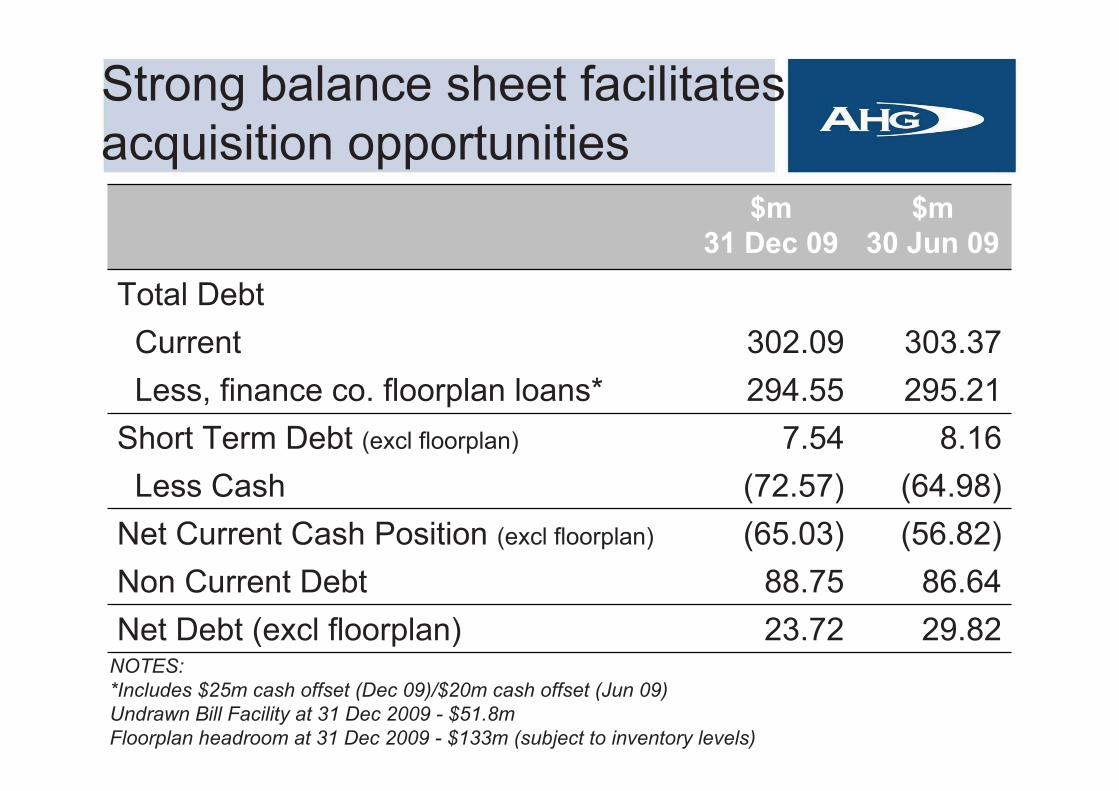

Strong balance sheet facilitates acquisition opportunities

NOTES:*Includes $25m cash offset (Dec 09)/$20m cash offset (Jun 09)Undrawn Bill Facility at 31 Dec 2009 - $51.8mFloorplan headroom at 31 Dec 2009 - $133m (subject to inventory levels)

$m31 Dec 09

$m30 Jun 09

Total DebtCurrent 302.09 303.37Less, finance co. floorplan loans* 294.55 295.21

Short Term Debt (excl floorplan) 7.54 8.16Less Cash (72.57) (64.98)

Net Current Cash Position (excl floorplan) (65.03) (56.82)Non Current Debt 88.75 86.64Net Debt (excl floorplan) 23.72 29.82

Automotive Holdings Group Limited 11

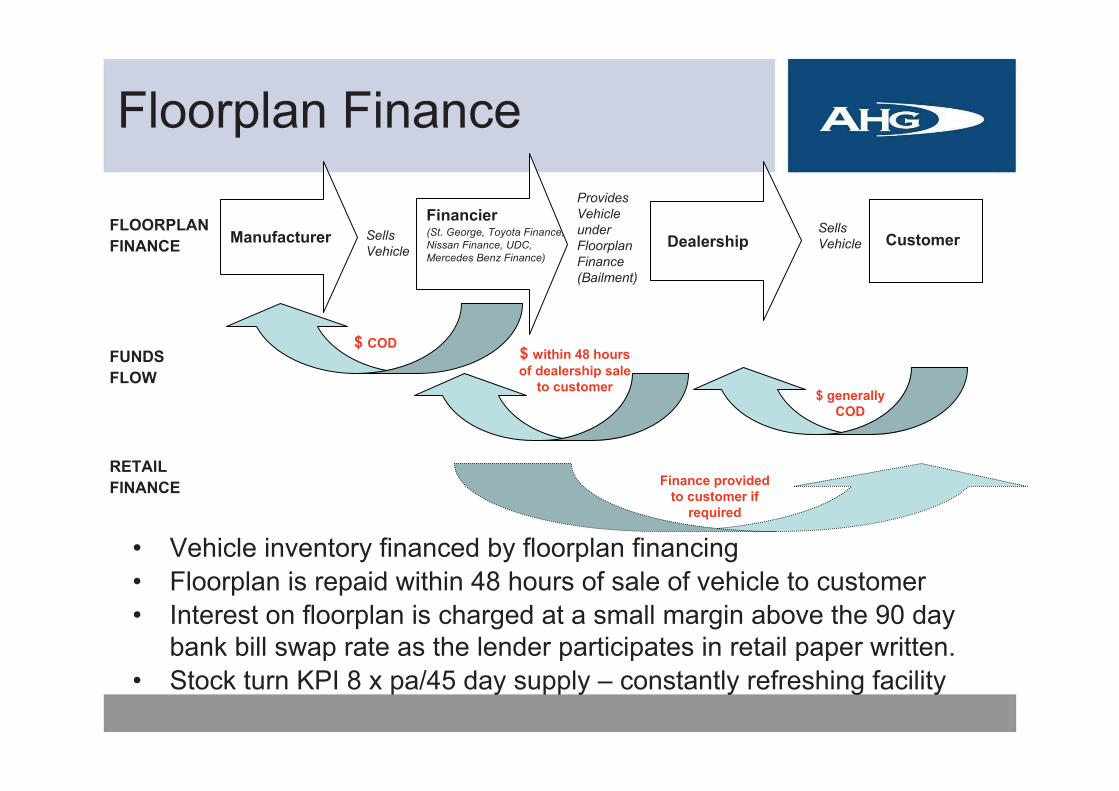

• Vehicle inventory financed by floorplan financing• Floorplan is repaid within 48 hours of sale of vehicle to customer• Interest on floorplan is charged at a small margin above the 90 day

bank bill swap rate as the lender participates in retail paper written.• Stock turn KPI 8 x pa/45 day supply – constantly refreshing facility

ManufacturerFinancier(St. George, Toyota Finance, Nissan Finance, UDC, Mercedes Benz Finance)

Dealership CustomerSellsVehicle

SellsVehicle

$ generally COD

$ within 48 hours of dealership sale

to customer

$ COD

FLOORPLANFINANCE

FUNDSFLOW

RETAILFINANCE

Provides Vehicle under Floorplan Finance (Bailment)

Finance provided to customer if

required

Floorplan Finance

Logistics

Logistics

• Rand Transport - Australia’s largest refrigerated transport company

• Amcap- mature business to maintain a strong market position

• KTM- pricing pressures for 2010

• VSE/GTB- Trading conditions for engineering and GTB to improve following ease of supply issues - storage not expected to recover until 2H CY10

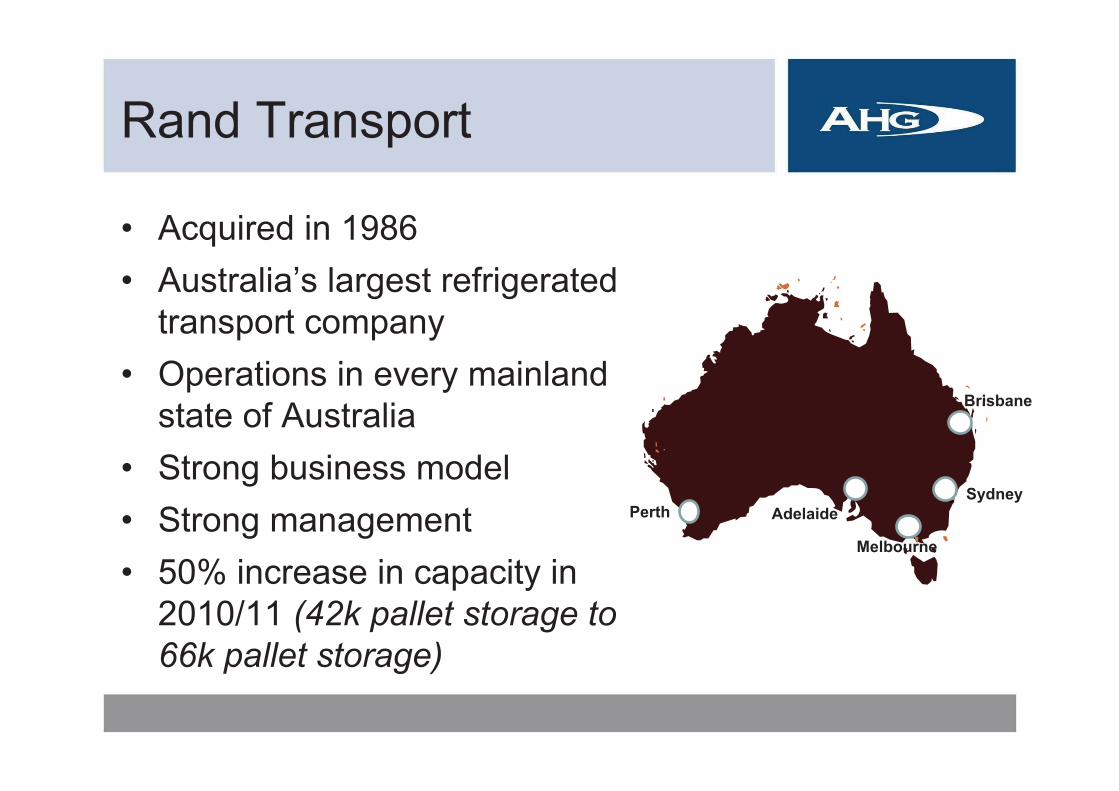

Rand Transport

• Acquired in 1986• Australia’s largest refrigerated

transport company• Operations in every mainland

state of Australia • Strong business model• Strong management• 50% increase in capacity in

2010/11 (42k pallet storage to 66k pallet storage)

Perth Adelaide

Melbourne

Sydney

Brisbane

Melbourne Coldstore (Artist’s Impression)

GROUPOUTLOOK

Group Outlook

• Consumer and business sentiment remains high¹• Low unemployment• Low interest rates• Strong management and resilient business model to

continue to deliver solid financial results • Maintain strong business practices• Acquisition opportunities

¹ Westpac-Melbourne Institute Survey of Consumer Sentiment – 10 Feb 2010/NAB’s Monthly Business Survey & Economic Outlook – Jan 2010

AHG - Australia’s largest automotive retailer

APPENDICES

20

Board of Directors• Bronte Howson (Managing Director) – 28 years in

automotive and logistics, 22 years with AHG, 10 as MD/CEO.

• Hamish Williams (Executive Director Strategy and Planning) –17 years with AHG, including 13 years as Finance Director.

• Bob Branchi (Non-Exec Chairman) – 53 years industry experience, 28 as a Director at AHG.

• David Griffiths (Independent Non-Exec Director and Deputy Chairman) – 15 years experience in equity capital markets, mergers and acquisitions and the corporate advisory sector.

• Greg Wall (Independent Non-Exec Director) 30 years banking and finance experience, 10 years CEO StateWest Credit Society Ltd.

21

Board of Directors• John Groppoli (Independent Non-Exec Director)

Ex partner of national law firm Deacons from 1987 to 2004, currently MD of Milners Pty. Ltd. a leading Australian brand marketing group specialising in high end home products.

• Peter Stancliffe (Independent Non-Exec Director) 35 years experience in management of major corporations in Australia and overseas. Former CEO of Australian National Industries Limited and Pirelli Cables Limited.

• Michael Smith (Independent Non-Exec Director)Strategy consultant with considerable experience in strategy, marketing and finance. Current Chairman of Synergy, WA’s largest energy retailer and iiNet, director of 7-Eleven Stores.

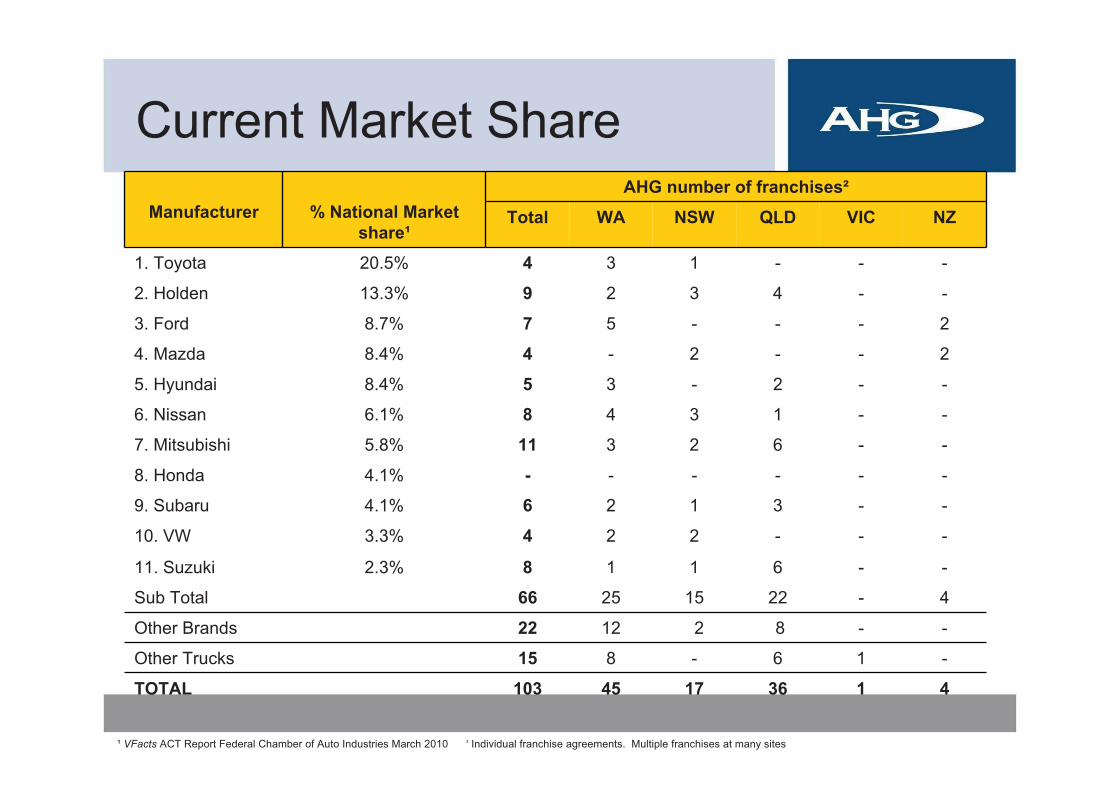

Manufacturer % National Market share¹

AHG number of franchises²

Total WA NSW QLD VIC NZ

1. Toyota 20.5% 4 3 1 - - -

2. Holden 13.3% 9 2 3 4 - -

3. Ford 8.7% 7 5 - - - 2

4. Mazda 8.4% 4 - 2 - - 2

5. Hyundai 8.4% 5 3 - 2 - -

6. Nissan 6.1% 8 4 3 1 - -

7. Mitsubishi 5.8% 11 3 2 6 - -

8. Honda 4.1% - - - - - -

9. Subaru 4.1% 6 2 1 3 - -

10. VW 3.3% 4 2 2 - - -

11. Suzuki 2.3% 8 1 1 6 - -

Sub Total 66 25 15 22 - 4

Other Brands 22 12 2 8 - -

Other Trucks 15 8 - 6 1 -

TOTAL 103 45 17 36 1 4

¹ VFacts ACT Report Federal Chamber of Auto Industries March 2010 ² Individual franchise agreements. Multiple franchises at many sites

Current Market Share

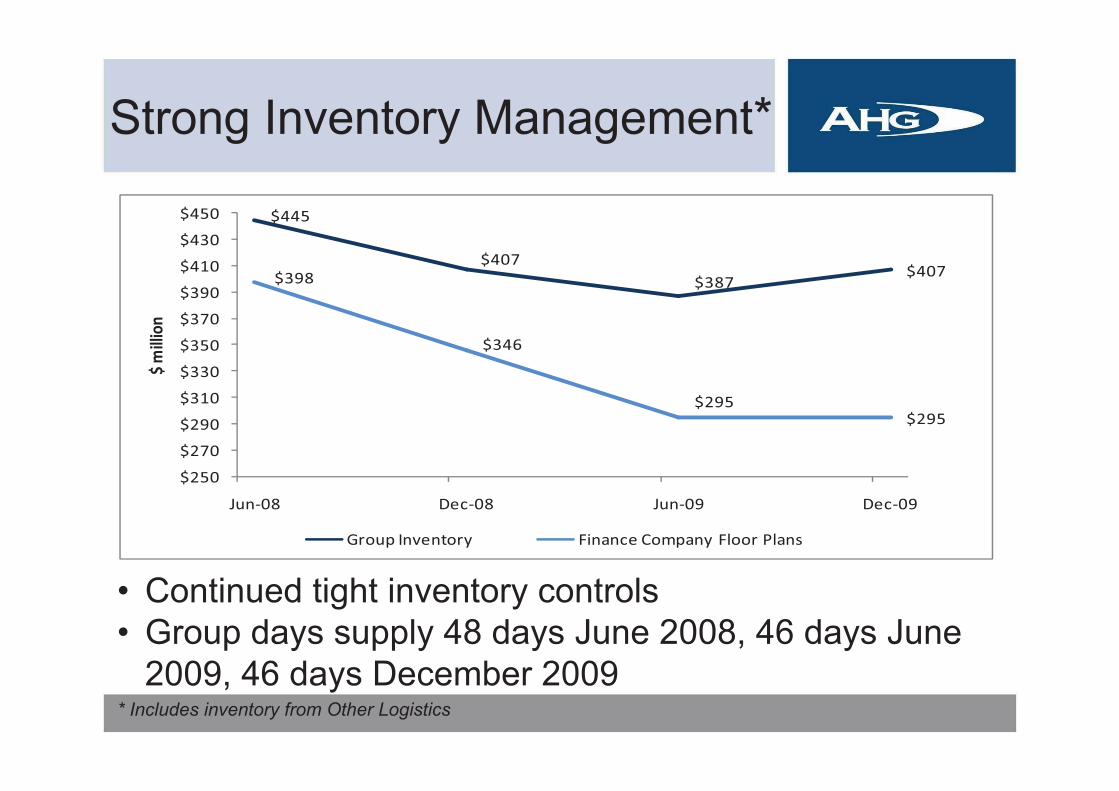

Strong Inventory Management*

• Continued tight inventory controls• Group days supply 48 days June 2008, 46 days June

2009, 46 days December 2009* Includes inventory from Other Logistics

$445

$407$387

$407$398

$346

$295$295

$250

$270

$290

$310

$330

$350

$370

$390

$410

$430

$450

Jun�08 Dec�08 Jun�09 Dec�09

$�million

Group�Inventory Finance�Company�Floor�Plans

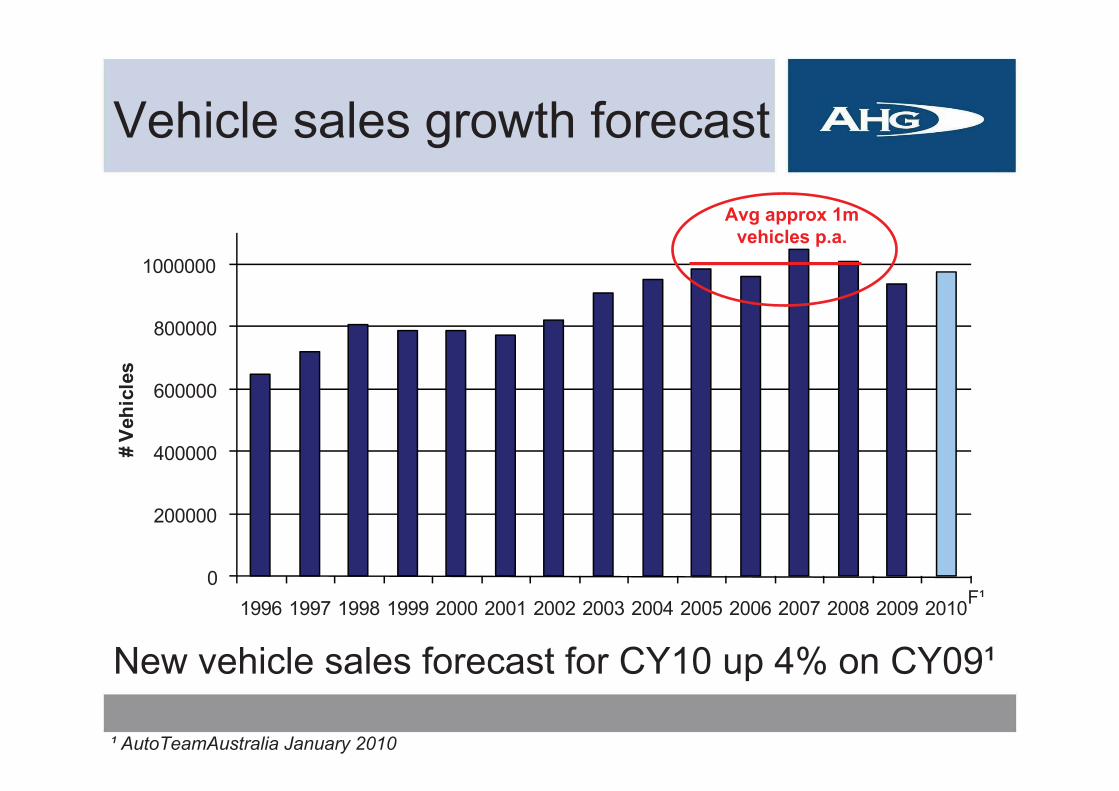

Vehicle sales growth forecast

0

200000

400000

600000

800000

1000000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

# Ve

hicl

es

F¹

¹ AutoTeamAustralia January 2010

New vehicle sales forecast for CY10 up 4% on CY09¹

Avg approx 1m vehicles p.a.