Embed Size (px)

Citation preview

1 Issued 17 November 2014.

CIRCULAR 10P/2015

(Replacing Circular 09P/2014)

AGREED UPON PROCEDURES FOR REGISTERED AUDITORS

REPORTING ON FACTUAL FINDINGS IN TERMS OF

THE CENTRAL SECURITIES

DEPOSITORY (CSD) RULES AND

THE FINANCIAL MARKETS ACT (FMA)

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

2 Issued 17 November 2014.

AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

.01 The purpose of this Circular is to provide guidance for Registered Auditors when reporting in terms of the Central Securities Depository (CSD) Rules and the Financial Markets Act (FMA) on the Participant’s compliance with the relevant sections of the FMA, Board Notices 96 and 100 of 2013 published in Government Gazette No. 36494. Board Notice 96 provides details regarding the responsibilities of a Participant for maintaining the accounting records and internal controls to which this Circular relates. Board Notice 100 provides details regarding the matters to be reported on by the Auditor of a Regulated Person.

.02 This Circular contains the ‘agreed-upon procedures’ to be performed by the Registered Auditor of a Participant (Participant includes “Primary Participant” and “Secondary Participant” where applicable) regarding the implementation and operating effectiveness of key controls (identified by management of the Participant), that are designed to meet the control objectives (specified by Strate (Pty) Limited [Strate]), for transactions relating to the settlement, custody and administration, of Strate eligible securities. The format for the Registered Auditor’s factual findings report is set out in the appendix.

.03 The procedures to be performed have been agreed by the Participants

and the Controlling Body of Strate. The Circular has been approved

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

3 Issued 17 November 2014.

by the Controlling Body of Strate, specifically the Strate Regulatory and Supervisory Committee.

Introduction .04 The Strate Circular 10P/2015 sets out the agreed upon procedures

to be performed by Registered Auditors1 reporting on factual findings in respect of compliance by Participants with the CSD Rules, in respect of their implementation of internal controls to meet specified objectives for their settlement, custody and administration of Strate eligible securities.

.05 Circular 09P/2014 has been replaced to correct a reference to the

applicable FMA Board Notice. .06 The CSD Rules2 relating to the reporting responsibilities of

Registered Auditors, require: “8.1.5 The Registered Auditor of the Participant must submit a factual

findings report annually to the Controlling Body, within 90 (ninety) calendar days after the financial year-end of the Participant which complies with the Strate Circular, the Act and Rules. The Registered Auditor responsible for the audit of the SARB or a Participant which is also a bank, must submit the factual findings report within 6 (six) months after the financial year-end of such bank Participant or the SARB.

8.1.6 The Registered Auditor of the Participant must annually report to the Controlling Body whether or not:

8.1.6.1 The Participant complies with the requirements of the Act and the Rules regarding the maintenance of Securities Accounts; and

1 Registered Auditor means an individual or firm registered as an auditor with the Independent Regulatory Board for Auditors in terms of the Auditing Profession Act, 26 of 2005. 2 The CSD Rules are appropriately amended with the permission of Strate to accommodate changes resulting from the enactment of the Auditing Profession Act, 26 of 2005.

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

4 Issued 17 November 2014.

8.1.6.2 The Participant complies with the Rules relating to the reconciliation of Securities Accounts to the Central Securities Accounts kept by the CSD.”

8.1.6.3 The Participant complies with Rule 5.1.1, and on the adequacy of the arrangements made and measures taken by such Participant on holding of sufficient Securities in terms of Rule 5.1.

Responsibility of the management of the Participant .07 The management of the Participant are required to design,

implement and maintain the operating effectiveness of adequate systems of internal control throughout the financial year, relevant to the business conducted by the Participant as set out more fully in the FMA, the CSD Rules, Board Notice 96 and 100 of 2013.

.08 For the purposes of the agreed-upon procedures engagement, the management of the Participant are required to identify the key controls implemented by them and to provide evidence to their Registered Auditors, that the operating effectiveness of such controls has been maintained throughout the period reported on, to meet the control objectives, specified by Strate (described in the agreed-upon procedures section of this Circular.)

.09 For the purposes of the report of factual findings, the management of the Participant are required to provide explanations for any deviations from and /or exceptions identified in the implementation or operating effectiveness of key controls.

Auditor’s responsibilities .10 The Registered Auditor conducts the agreed-upon procedures

engagement in accordance with the International Standard on Related Services, “Engagements to perform agreed-upon procedures regarding financial information” (ISRS 4400).

.11 The responsibility for determining the adequacy and appropriateness of the agreed-upon procedures to be performed by the Registered

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

5 Issued 17 November 2014.

Auditor is that of Strate and the Participant. The Registered Auditor has no responsibility for determining the adequacy or appropriateness of the procedures for the purpose of this engagement. The Registered Auditor carries out the procedures agreed upon, and uses the evidence obtained as the basis for the report of factual findings to Strate in the format indicated in the appendix.

.12 The Registered Auditor of the Participant is required to have an understanding of the relevant sections of the FMA and applicable Notices, the CSD Rules, Directives issued by Strate, the Companies Act and the STT Act in order to perform this agreed-upon procedures engagement.

Sample selection

.13 The sample size and the basis of selection is to be agreed annually between the Controlling Body of Strate (specifically STRATE Supervision), the Participant and the Registered Auditor in a tri-partite meeting before the commencement of the agreed-upon procedures engagement. The report of factual findings of the Registered Auditor is to state the size of the sample selected for testing each relevant control objective. (The sample will be drawn from the full period to which the agreed upon procedures engagement relates).

Reporting

.14 The Registered Auditor reports on factual findings in terms of ISRS 4400, in the format set out in the appendix to this Circular.

.15 When reporting exceptions, the Registered Auditor shall include sufficient information, where applicable, to enable Strate to investigate the transactions. This information shall include the following:

SAFIRES order number – System operated by Strate for Equities Securities (including warrants);

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

6 Issued 17 November 2014.

MMSS / ETME order number – System operated by Strate for Money Market Securities;

Strate Bonds System Trade Leg Number;

Settlement date;

Client name;

Client Securities Account number;

Client Segregated Depository Account number;

ISIN – International Securities Identification Number;

Quantity of Securities; and

Explanation provided by the Participant’s management.

Agreed-upon procedures

.16 The Registered Auditor shall perform the following agreed-upon procedures, where applicable to the Participant, and shall report the factual findings on these procedures: Client Mandates

1. From the Participant’s client list, select a sample of clients and perform the following procedures:

1.1 For each client determine if a client mandate is in place, and through inspection determine whether the mandate contains the information prescribed in CSD Rule 5.7.3.

1.2 For all client mandates selected, verify that the records are kept in a secure location (for example, a locked cabinet with access control, or a vault) or there is evidence that the records are kept at a filing service provider. In the case where records are kept at a filing service provider, a signed service level agreement is in place to confirm that the records are secure.

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

7 Issued 17 November 2014.

Dematerialisation and Rematerialisation – Equities

2. Document the key controls identified by the Participant’s management that address each of the control objectives listed below in respect of dematerialisation and rematerialisation transactions:

2.1 Loss of physical securities is prevented.

2.2 Securities details are completely and accurately loaded onto the Participant’s system.

2.3 Errors made in submissions to transfer secretaries are detected on a timely basis.

2.4 Securities for dematerialisation that are rejected by a transfer secretary are completely and accurately recorded.

2.5 “Resident” batches are processed separately from “non-resident” batches in respect to broker clients.

2.6 Duplication in orders is detected.

2.7 The securities holding of the client’s Securities Account or Segregated Depository Account is accurately increased/ decreased following the completion of a dematerialisation and rematerialisation transaction.

3. Select a sample of both dematerialisation and rematerialisation orders from the Participant’s order records and test through inspection and observation whether the key controls identified by the Participant’s management have been implemented and whether they operated effectively during the period reported on for each item selected.

Immobilisation, Dematerialisation and Withdrawals – Bonds

4. Document the key controls identified by the Participant’s management that address each of the control objectives listed below in respect of immobilisation, dematerialisation and withdrawal transactions:

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

8 Issued 17 November 2014.

4.1 Loss of physical securities is prevented.

4.2 Securities details are completely and accurately loaded onto the Participant’s system.

4.3 Errors made in submissions to the CSD are detected on a timely basis.

4.4 Securities for immobilisation and/ or dematerialisation that are rejected by the CSD are completely and accurately recorded.

4.5 Duplication in orders is detected.

4.6 The securities holding of the client’s Securities Account or Segregated Depository Account is accurately increased/ decreased following the completion of an immobilisation, dematerialisation and/ or withdrawal transaction.

5. Select a sample of immobilisation, dematerialisation and

withdrawal orders from the Participant’s order records and test through inspection and observation whether the key controls identified by the Participant’s management have been implemented and whether they operated effectively during the period reported on for each item selected.

Rematerialisation – Money Markets

6. Document the key controls identified by the Participant’s management that address each of the control objectives listed below in respect of rematerialisation transactions:

6.1 Securities details are completely and accurately loaded onto the Participant’s system.

6.2 Turnaround times are kept to within seven business days.

6.3 Errors made in submissions to Strate and/ or Issuers are detected on a timely basis.

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

9 Issued 17 November 2014.

6.4 Requests for rematerialisation that are rejected by Strate and/ or Issuers are completely and accurately recorded.

6.5 Duplication in orders is detected.

6.6 The securities holding of the client’s Money Market Securities Ownership Register Account is accurately decreased following the completion of a rematerialisation transaction.

7. Select a sample of rematerialisation orders from the Participant’s order records and test through inspection and observation whether the key controls identified by the Participant’s management have been implemented and whether they operated effectively during the period reported on for each item selected.

Operation of Securities Accounts / Segregated Depository Accounts

8. Document the key controls identified by the Participant’s management that address each of the control objectives listed below in respect of Securities Accounts and/ or Segregated Depository Accounts:

8.1 The accuracy of client details is established when opening Securities Accounts and/ or Segregated Depository Accounts on the Participant’s system.

8.2 Securities Accounts and/ or Segregated Depository Accounts are opened in accordance with the CSD Rules, and

8.2.1 If the Securities Account and/ or Segregated Depository Account is opened in the name of a nominee, the nominee is approved in terms of section 76 of the FMA, the CSD Rules and Directives; and

8.2.2 If the Securities Account and/or Segregated Depository Account is opened in the client’s

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

10 Issued 17 November 2014.

“own name”, the own name client complies with the FMA, the CSD Rules, and Directives.

8.3 Subsequent changes (opening, maintaining, altering or closing) to Securities Accounts and/ or Segregated Depository Accounts, if any, are duly authorised and accurately executed.

8.4 The securities holdings of the Participant are segregated from the securities holdings of the Participant’s clients.

8.5 Each Participant’s client’s holdings are segregated from the holdings of other clients.

8.6 Holdings that are Strate eligible (dematerialised securities) are distinguished from those holdings that are not (certificated securities).

8.7 If a Participant records a pledge or cession to secure a debt on behalf of a client in a Securities Account and/ or Segregated Depository Account, this is done in accordance with CSD Rules 6.7.4 and 7.8 where applicable.

8.8 Statements of holdings have been sent to clients at least bi-annually.

9. Select a sample of Securities Account and Segregated Depository Account opening and modification transactions from the transaction history reflected on the Participant’s custody system and test through inspection and observation whether the key controls identified by the Participant’s management have been implemented and whether they operated effectively during the period reported on for each item selected.

10. Select a sample of Securities Accounts and Segregated Depository Accounts from the Participant’s client list, and determine whether Directives SA.3 and SA.4, SA.7, SE.2 and CSD Rules 5.9.1, 6.6 and 6.7 are being adhered to.

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

11 Issued 17 November 2014.

Balancing

11. Document the key controls identified by the Participant’s management that address each of the control objectives listed below in respect of balancing procedures:

11.1 For each ISIN, balancing of the Participant’s client holdings with the aggregate holding in that ISIN takes place on a daily basis.

11.2 For each ISIN, the Participant’s aggregate holding agrees to the corresponding Central Securities Account / Segregated Depository Account at Strate on a daily basis.

11.3 With respect to 11.1 and 11.2 the Participant ensures that imbalances are resolved and cleared within 24 hours. NOTE: Imbalances relating to for example; the processing of a dematerialisation or rematerialisation order, or, the processing of a corporate action, are not regarded as a discrepancy or transgression if reconciled and resolved / cleared within 24 hours.

11.4 In respect of securities, the system, or other adequate controls prevents processing of negative balances.

11.5 The Strate Compliance Officer reviews and signs off the activities, which have been undertaken by the Participant in 11.1 and 11.2, on a daily basis.

12. Select a sample of daily ISIN balancing procedures and test

through inspection and observation whether the key controls identified by the Participant’s management have been implemented and whether they operated effectively during the period reported on for each item selected.

13. Inspect a sample of the Participant’s client statements and/ or

client Securities Accounts on the Participant’s custody system that covers the period reported on to determine if there are any negative balances.

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

12 Issued 17 November 2014.

Settlement

14. Document the key controls identified by the Participant’s management that address each of the control objectives listed below in respect of settlement procedures:

14.1 Every entry in a Securities Account and/ or Segregated Depository Account is executed pursuant to a corresponding Authorising Instruction, a Standing Instruction or a BEE Instruction in terms of the Client Mandate or BEE Contract.

14.2 Every entry in a Securities Account and/ or Segregated Depository Account is executed in accordance with the Strate Settlement and Operational Windows Directives.

15. Select a sample of settlement transactions, covering the financial period reported on, from the transaction history reflected on the Participant’s custody system and, for each item selected, perform the following procedures:

15.1 Inspect and observe whether the key controls identified by the Participant’s management have been implemented and whether they operated effectively during the period reported on.

15.2 Agree the client settlement instructions communicated in a supporting fax or SWIFT message to the details entered into the Participant’s custody system.

15.3 Agree the details entered into the Participant’s custody system to the applicable message standard sent to Strate confirming the transaction.

15.4 Agree the details of the transaction as reflected in the Strate records to the client statement with the aim of evaluating whether the client receives true value (cash and securities) on the same day as settlement takes place.

15.5 Agree the underlying transaction to the CSD system with the use of the applicable transaction reference number to

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

13 Issued 17 November 2014.

determine whether the transaction has been reported to Strate.

15.6 Select a sample of transactions that have not been reported to Strate for settlement and determine the reasons for such internal book entries.

Securities Transfer Tax Act (STT Act) – Equities

16. Document the key controls identified by the Participant’s management that address each of the control objectives listed below in respect of settlement procedures:

16.1 The Participant’s system automatically defaults the STT indicator to "YES" when capturing a client instruction.

16.2 The indicator can only be changed in certain circumstances (when advised by the client) and when relevant supporting documentation is obtained.

17. Observe the entering of the Participant’s client instruction on the Participant’s custody system to determine whether the system defaults to levy STT.

18. Select from the transaction history reflected on the Participant’s custody system a sample of off-market transactions, which cover the financial period reported on, where the STT indicator has been changed so that no STT is levied, and inspect the relevant supporting documentation to confirm that it meets the requirements of the STT Act.

19. Select a sample of the Participant’s client mandates and determine whether these mandates contain a "blanket" mandate from the client to change the tax indicator for all transactions (i.e. the STT indicator should only be changed on a case-by-case basis).

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

14 Issued 17 November 2014.

Corporate Actions – Equities

20. Document the key controls identified by the Participant’s management that address each of the control objectives listed below in respect of Corporate Actions:

20.1 All Corporate Action Announcements and all subsequent updates are detected and acted upon within the timeframes stipulated in the CSD Rules and Directives.

20.2 All clients having a holding in the applicable ISIN on Record Date and to which the Announcement relates, have received copies of all such Strate Corporate Action Announcements.

20.3 If clients have not received Announcements in terms of 20.2, inspect evidence that the client mandate adheres to Rule 5.8.4.

20.4 The missing of deadlines of the Corporate Action by both the Participant and its clients is prevented.

20.5 The Participant’s client responses on elective events are accurately captured on a timely basis as per the CSD Rules and Directives and the client mandate.

20.6 Strate is accurately notified of client elections on elective events on a timely basis as per the CSD Rules and Directives.

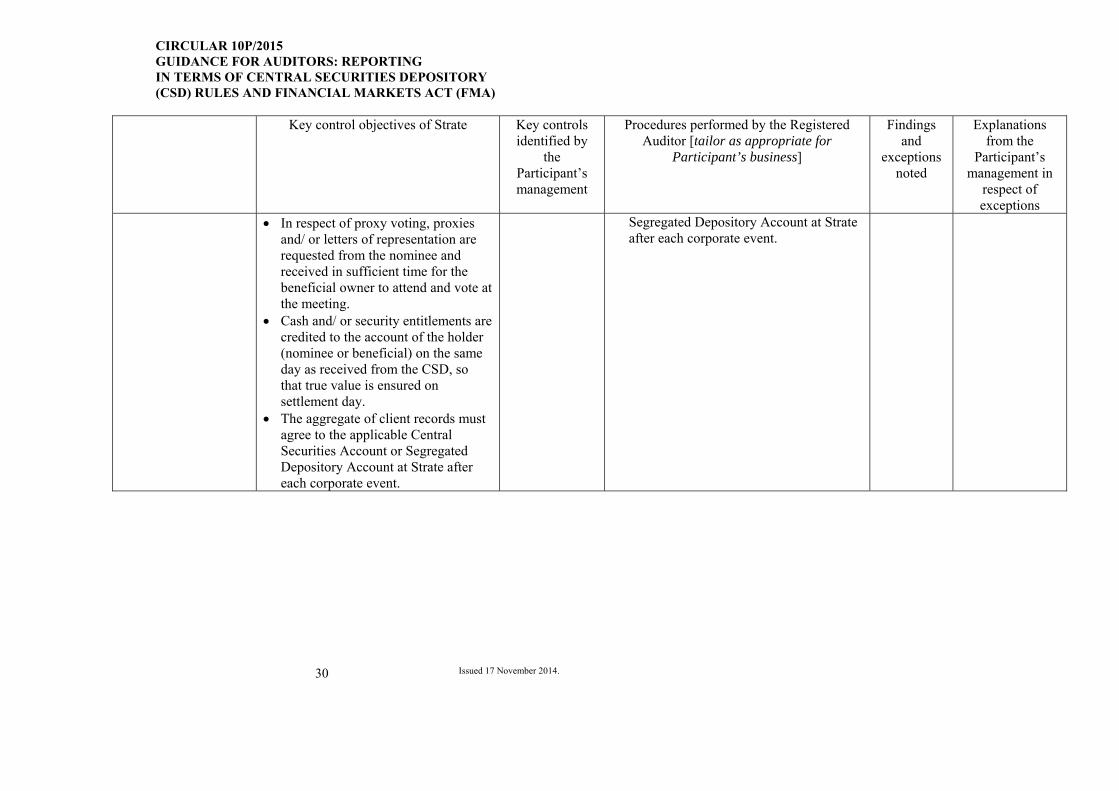

20.7 In respect of proxy voting, proxies and/ or letters of representation are requested from the nominee and received in sufficient time for the beneficial owner to attend and vote at the meeting.

20.8 Cash and/ or security entitlements are credited to the account of the holder (nominee or beneficial) on the same day as received from the CSD, so that true value is ensured on settlement day.

21. Select a sample of corporate events from the Participant’s diary of such events, for the period reported on, and, for each item selected, perform the following procedures:

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

15 Issued 17 November 2014.

21.1 Inspect and observe whether the key controls identified by the Participant’s management have been implemented and whether they operated effectively during the period reported on.

21.2 Inspect the Participant’s record of clients that have holdings in the applicable ISIN on Record Date and, for the sample of clients selected, inspect the Participant’s copy of the notification / Announcement, as well as any updates where salient information has been included or changed, to such clients of the event. Determine whether the notification / Announcement or subsequent update thereof is dated within the time period prescribed in the CSD Rules and Directives.

21.3 Inspect the reconciliation prepared by the Participant to prove that the aggregate of client records agrees to the applicable Central Securities Account or Segregated Depository Account at Strate after each corporate event.

Capital Events – Bonds

22. Document the key controls identified by the Participant’s management that address each of the control objectives listed below in respect of coupon and maturity payments:

22.1 All notices of payments are detected and acted upon within the timeframes stipulated in the CSD Rules and Directives.

22.2 Cash entitlements are credited to the account of the holder (nominee or beneficial) on the same day as received from the CSD, so that true value is ensured on settlement day.

23. Select a sample of events from the Participant’s diary of such events covering the period reported on, and for each item selected, perform the following procedures:

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

16 Issued 17 November 2014.

23.1 Inspect and observe whether the key controls identified by the Participant’s management have been implemented and whether they operated effectively during the period reported on.

23.2 Inspect the reconciliation prepared by the Participant to prove that the aggregate of client cash entitlements agrees to the cash entitlement to be received in respect of the Central Securities Account or Segregated Depository Account maintained at Strate.

Capital Events – Money Markets

24. Document the key controls identified by the Participant’s management that address each of the control objectives listed below in respect of coupon and maturity payments:

24.1 All notices of payments are detected and acted upon within the timeframes stipulated in the CSD Rules and Directives.

24.2 Cash entitlements are credited to the account of the beneficial holder or foreign nominee on the same day as received from the CSD, so that true value is ensured on settlement day.

25. Select a sample of events from the Participant’s diary of such events covering the period reported on, and for each item selected, perform the following procedures:

25.1 Inspect and observe whether the key controls identified by the Participant’s management have been implemented and whether they operated effectively during the period reported on for each item selected.

25.2 Inspect the reconciliation prepared by the Participant to prove that the aggregate of client cash entitlements agrees to the cash entitlement received in the South African Multiple Options System.

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

17 Issued 17 November 2014.

BEE Securities

26. Document the key controls identified by the Participant’s management that address each of the control objectives listed below in respect of BEE Securities:

26.1 For any Non-Controlled Client, who is the beneficial owner of BEE Securities, that the BEE Contract has been concluded, and any BEE Certificate or identity document, as the case may be, required in terms of the BEE Contract, has been obtained.

26.2 For all BEE Contracts selected, verify that the records are kept in a secure location (for example, a locked cabinet with access control, or a vault), or there is evidence that the records are kept at a filing service provider. In the case where records are kept at a filing service provider, a signed service level agreement is in place to confirm that the records are secure.

26.3 Where BEE Securities have been pledged, that statements to the Client or the person to whom the securities have been pledged or ceded, indicate that the BEE Securities may only be transferred in accordance with the BEE Contract.

27. Select a sample of BEE Securities custody positions, covering the financial period reported on, and for each item selected, perform the following procedures:

27.1 Inspect and observe whether the key controls identified by the Participant’s management have been implemented and whether they operated effectively during the period reported on. 27.2 Determine if a BEE Contract and any BEE Certificate or identity document, as the case may be, is in place.

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

18 Issued 17 November 2014.

27.3 Determine if statements (in respect of paragraph 26.3) indicate that the BEE Securities may only be transferred in accordance with the BEE Contract.

Segregated Depository Accounts – Equities and Bonds

28. Where a Segregated Depository Account has been opened, determine if a client mandate is in place with the Primary Participant, and through inspection determine whether the mandate contains the provision as stated in Rule 6.13.4.

29. Where a client has chosen to appoint the Participant as a Secondary Participant, determine if a client mandate is in place, and through inspection determine whether the mandate contains the provision as stated in Rule 6.13.4.

30. Where a client has chosen to appoint the Participant as a

Secondary Participant, determine if the Participant has provided written proof to the CSD that it has assented to act as a Secondary Participant in terms of CSD Rule 6.13.4.

31. Select a sample of Segregated Depository Accounts and determine and verify that these same accounts have been opened and are active at the CSD.

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

19 Issued 17 November 2014.

APPENDIX

Set out below is the format of the report of factual findings in compliance with the CSD Rules and the FMA. REPORT OF FACTUAL FINDINGS OF THE REGISTERED AUDITOR TO [INSERT NAME OF PARTICIPANT] AND THE CONTROLLING BODY OF STRATE ON FACTUAL FINDINGS

Scope We have performed the procedures agreed with [insert name of participant] (the Participant) and the Controlling Body of Strate enumerated in the attached table with respect to the implementation and operating effectiveness of the Participant’s system of internal control for the year ending [insert year end]. Our engagement was undertaken in accordance with the International Standard on Related Services 4400, Engagements to Perform Agreed-upon Procedures Regarding Financial Information and was performed solely to assist the Participant in reporting to Controlling Body of Strate on its compliance with the requirements of the Financial Markets Act No 19 of 2012, the Central Securities Depository (CSD) Rules, and Notices 96 and 100 of 2013, issued by the Financial Services Board in terms of the Financial Markets Act. The responsibility for determining the adequacy or otherwise of the procedures agreed to be performed is that of the Controlling Body of Strate and the Participant. Procedures and findings Our procedures and findings are detailed in the attached table, initialled for identification purposes. In addition, the attached schedule includes explanations by management of the Participant, regarding any deviations from and/ or exceptions identified in the implementation or operating effectiveness of key controls to meet the control objectives for each relevant transaction type specified by Strate. We are not required to and have not performed any

CIRCULAR 10P/2015 AGREED UPON PROCEDURES FOR REGISTERED AUDITORS REPORTING ON FACTUAL FINDINGS IN TERMS OF THE CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND THE FINANCIAL MARKETS ACT (FMA)

20 Issued 17 November 2014.

additional procedures to corroborate management’s explanations and provide no assurance in regard to them.

Because the procedures do not constitute either an audit or a review made in accordance with International Standards on Auditing or International Standards on Review Engagements, we do not express any assurance on the implementation and operating effectiveness of the controls identified by management. Had we performed additional procedures, other matters might have come to our attention, which we would have reported to you. Restriction on use and distribution Our report and the attached schedule are solely for the purpose set forth in the first paragraph of this report and for your information, and are not to be used for any other purpose or to be distributed to any other parties. This report relates only to the matters specified in our report of factual findings, and does not extend to the implementation or operating effectiveness of the internal controls of the Participant taken as a whole. <Insert name of firm that is the Registered Auditor, unless on firm’s letterhead> <Insert name of individual partner / director responsible for the engagement> Registered Auditor Address Date

CIRCULAR 10P/2015 GUIDANCE FOR AUDITORS: REPORTING IN TERMS OF CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND FINANCIAL MARKETS ACT (FMA)

21 Issued 17 November 2014.

Key control objectives of Strate Key controls identified by

the Participant’s management

Procedures performed by the Registered Auditor [tailor as appropriate for

Participant’s business]

Findings and

exceptions noted

Explanations from the

Participant’s management in

respect of exceptions

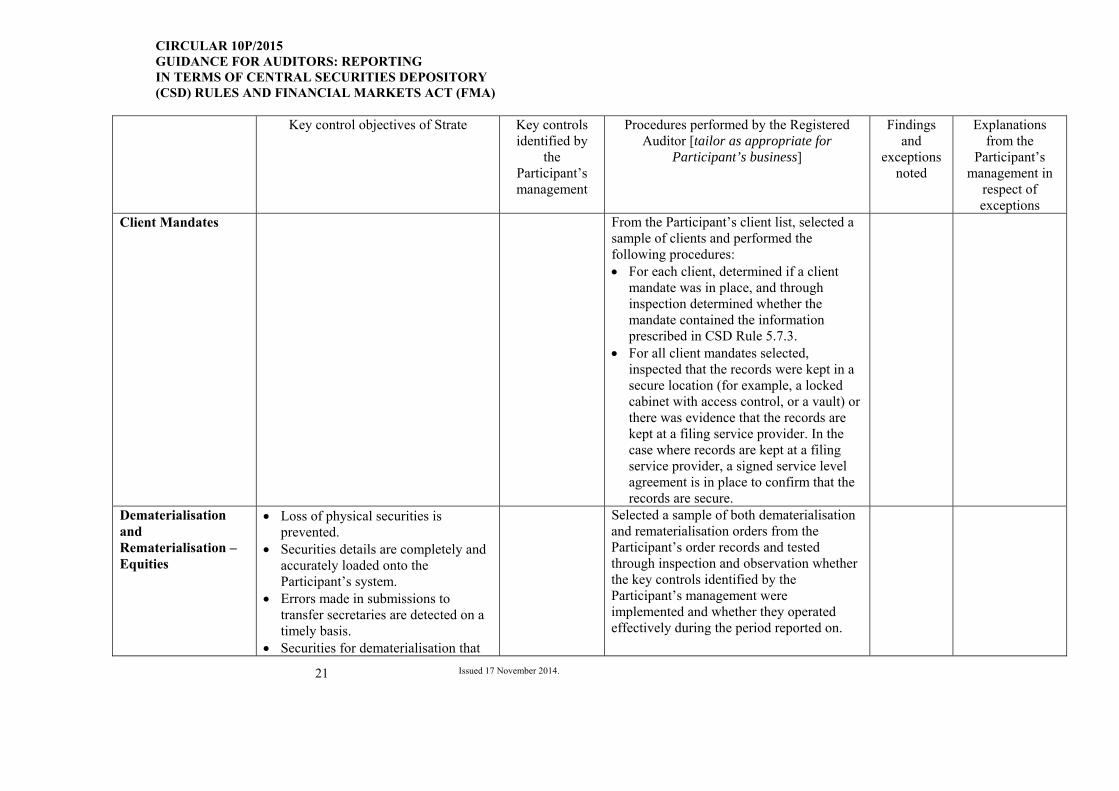

Client Mandates

From the Participant’s client list, selected a sample of clients and performed the following procedures: For each client, determined if a client

mandate was in place, and through inspection determined whether the mandate contained the information prescribed in CSD Rule 5.7.3.

For all client mandates selected, inspected that the records were kept in a secure location (for example, a locked cabinet with access control, or a vault) or there was evidence that the records are kept at a filing service provider. In the case where records are kept at a filing service provider, a signed service level agreement is in place to confirm that the records are secure.

Dematerialisation and Rematerialisation – Equities

Loss of physical securities is prevented.

Securities details are completely and accurately loaded onto the Participant’s system.

Errors made in submissions to transfer secretaries are detected on a timely basis.

Securities for dematerialisation that

Selected a sample of both dematerialisation and rematerialisation orders from the Participant’s order records and tested through inspection and observation whether the key controls identified by the Participant’s management were implemented and whether they operated effectively during the period reported on.

CIRCULAR 10P/2015 GUIDANCE FOR AUDITORS: REPORTING IN TERMS OF CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND FINANCIAL MARKETS ACT (FMA)

22 Issued 17 November 2014.

Key control objectives of Strate Key controls identified by

the Participant’s management

Procedures performed by the Registered Auditor [tailor as appropriate for

Participant’s business]

Findings and

exceptions noted

Explanations from the

Participant’s management in

respect of exceptions

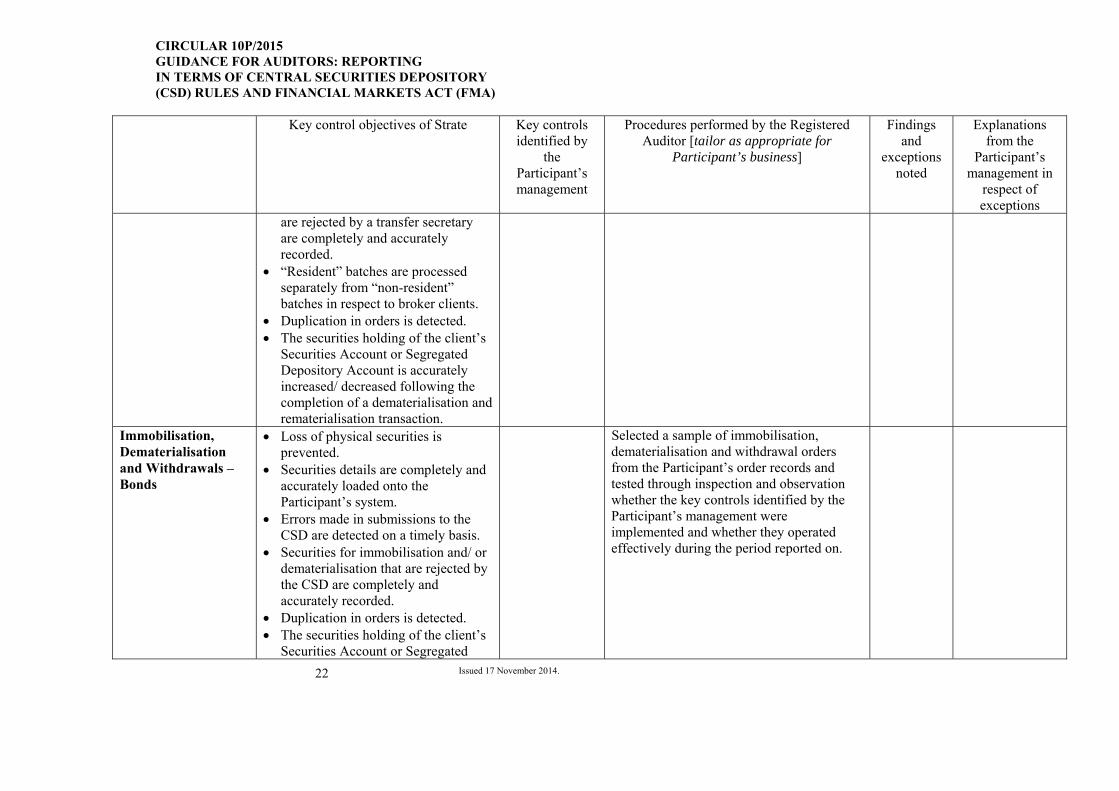

are rejected by a transfer secretary are completely and accurately recorded.

“Resident” batches are processed separately from “non-resident” batches in respect to broker clients.

Duplication in orders is detected. The securities holding of the client’s

Securities Account or Segregated Depository Account is accurately increased/ decreased following the completion of a dematerialisation and rematerialisation transaction.

Immobilisation, Dematerialisation and Withdrawals – Bonds

Loss of physical securities is prevented.

Securities details are completely and accurately loaded onto the Participant’s system.

Errors made in submissions to the CSD are detected on a timely basis.

Securities for immobilisation and/ or dematerialisation that are rejected by the CSD are completely and accurately recorded.

Duplication in orders is detected. The securities holding of the client’s

Securities Account or Segregated

Selected a sample of immobilisation, dematerialisation and withdrawal orders from the Participant’s order records and tested through inspection and observation whether the key controls identified by the Participant’s management were implemented and whether they operated effectively during the period reported on.

CIRCULAR 10P/2015 GUIDANCE FOR AUDITORS: REPORTING IN TERMS OF CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND FINANCIAL MARKETS ACT (FMA)

23 Issued 17 November 2014.

Key control objectives of Strate Key controls identified by

the Participant’s management

Procedures performed by the Registered Auditor [tailor as appropriate for

Participant’s business]

Findings and

exceptions noted

Explanations from the

Participant’s management in

respect of exceptions

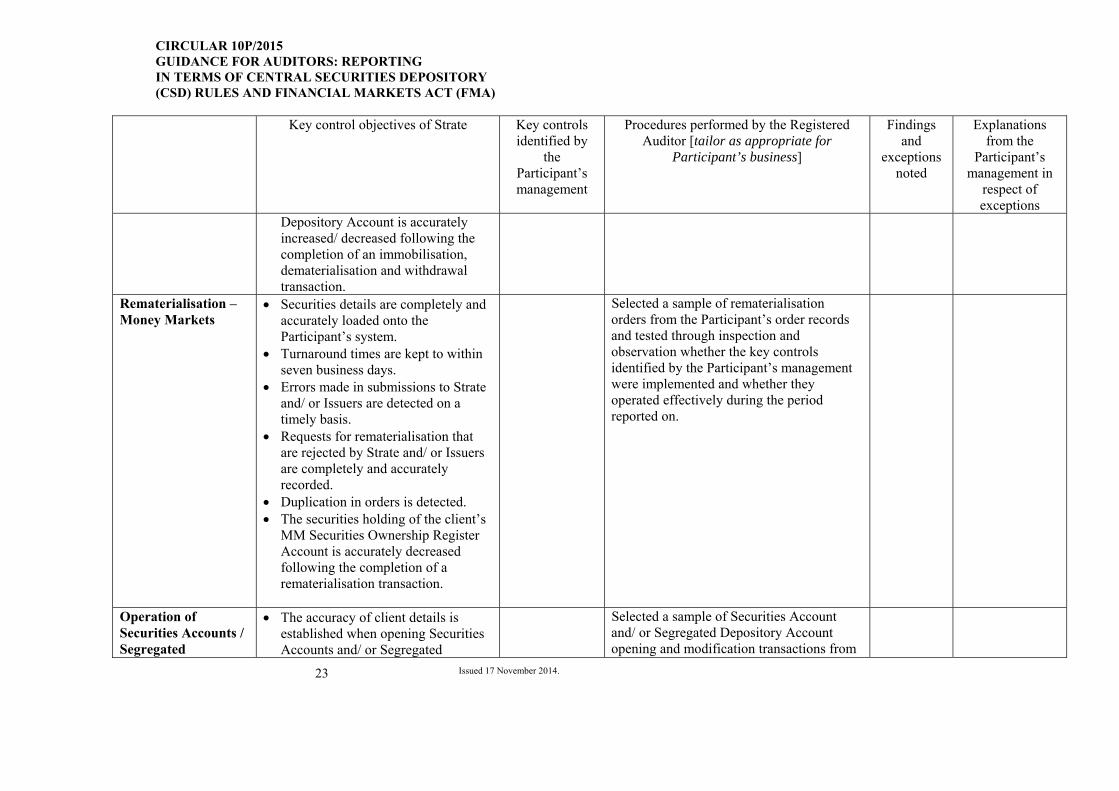

Depository Account is accurately increased/ decreased following the completion of an immobilisation, dematerialisation and withdrawal transaction.

Rematerialisation – Money Markets

Securities details are completely and accurately loaded onto the Participant’s system.

Turnaround times are kept to within seven business days.

Errors made in submissions to Strate and/ or Issuers are detected on a timely basis.

Requests for rematerialisation that are rejected by Strate and/ or Issuers are completely and accurately recorded.

Duplication in orders is detected. The securities holding of the client’s

MM Securities Ownership Register Account is accurately decreased following the completion of a rematerialisation transaction.

Selected a sample of rematerialisation orders from the Participant’s order records and tested through inspection and observation whether the key controls identified by the Participant’s management were implemented and whether they operated effectively during the period reported on.

Operation of Securities Accounts / Segregated

The accuracy of client details is established when opening Securities Accounts and/ or Segregated

Selected a sample of Securities Account and/ or Segregated Depository Account opening and modification transactions from

CIRCULAR 10P/2015 GUIDANCE FOR AUDITORS: REPORTING IN TERMS OF CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND FINANCIAL MARKETS ACT (FMA)

24 Issued 17 November 2014.

Key control objectives of Strate Key controls identified by

the Participant’s management

Procedures performed by the Registered Auditor [tailor as appropriate for

Participant’s business]

Findings and

exceptions noted

Explanations from the

Participant’s management in

respect of exceptions

Depository Accounts

Depository Accounts on the Participant’s system,

Securities Accounts and/ or Segregated Depository Accounts are opened in accordance with the CSD Rules, - Where the Securities Account or

Segregated Depository Account is opened in the name of a nominee, the nominee is approved in terms of section 76 of the FMA, the CSD Rules, and Directives.

- Where the Securities Account or Segregated Depository Account is opened in the client’s “own name”, the own name client complies with the FMA, the CSD Rules, and Directives.

Subsequent changes (opening, maintaining, altering or closing) to Securities Accounts and/ or Segregated Depository Accounts, if any, are duly authorised and accurately executed.

The securities holdings of the Participant are segregated from those of its clients.

the transaction history reflected on the Participant’s custody system and tested through inspection and observation whether the key controls identified by the Participant’s management were implemented and whether they operated effectively during the period reported on. Selected a sample of Securities Accounts and Segregated Depository Accounts from the Participant’s client list, and determined whether Directive SA.3, SA.4, SA.7, SE.2 and CSD Rule 5.9.1, 6.6 and 6.7 were being adhered to.

CIRCULAR 10P/2015 GUIDANCE FOR AUDITORS: REPORTING IN TERMS OF CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND FINANCIAL MARKETS ACT (FMA)

25 Issued 17 November 2014.

Key control objectives of Strate Key controls identified by

the Participant’s management

Procedures performed by the Registered Auditor [tailor as appropriate for

Participant’s business]

Findings and

exceptions noted

Explanations from the

Participant’s management in

respect of exceptions

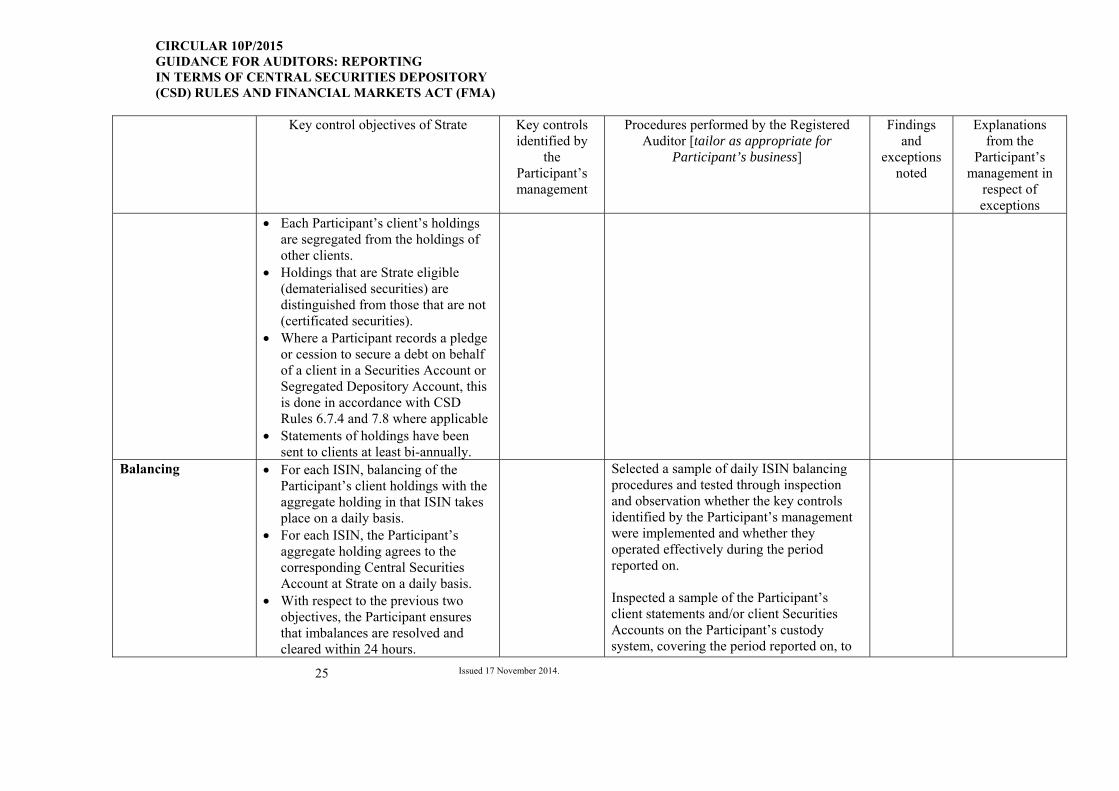

Each Participant’s client’s holdings are segregated from the holdings of other clients.

Holdings that are Strate eligible (dematerialised securities) are distinguished from those that are not (certificated securities).

Where a Participant records a pledge or cession to secure a debt on behalf of a client in a Securities Account or Segregated Depository Account, this is done in accordance with CSD Rules 6.7.4 and 7.8 where applicable

Statements of holdings have been sent to clients at least bi-annually.

Balancing

For each ISIN, balancing of the Participant’s client holdings with the aggregate holding in that ISIN takes place on a daily basis.

For each ISIN, the Participant’s aggregate holding agrees to the corresponding Central Securities Account at Strate on a daily basis.

With respect to the previous two objectives, the Participant ensures that imbalances are resolved and cleared within 24 hours.

Selected a sample of daily ISIN balancing procedures and tested through inspection and observation whether the key controls identified by the Participant’s management were implemented and whether they operated effectively during the period reported on.

Inspected a sample of the Participant’s client statements and/or client Securities Accounts on the Participant’s custody system, covering the period reported on, to

CIRCULAR 10P/2015 GUIDANCE FOR AUDITORS: REPORTING IN TERMS OF CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND FINANCIAL MARKETS ACT (FMA)

26 Issued 17 November 2014.

Key control objectives of Strate Key controls identified by

the Participant’s management

Procedures performed by the Registered Auditor [tailor as appropriate for

Participant’s business]

Findings and

exceptions noted

Explanations from the

Participant’s management in

respect of exceptions

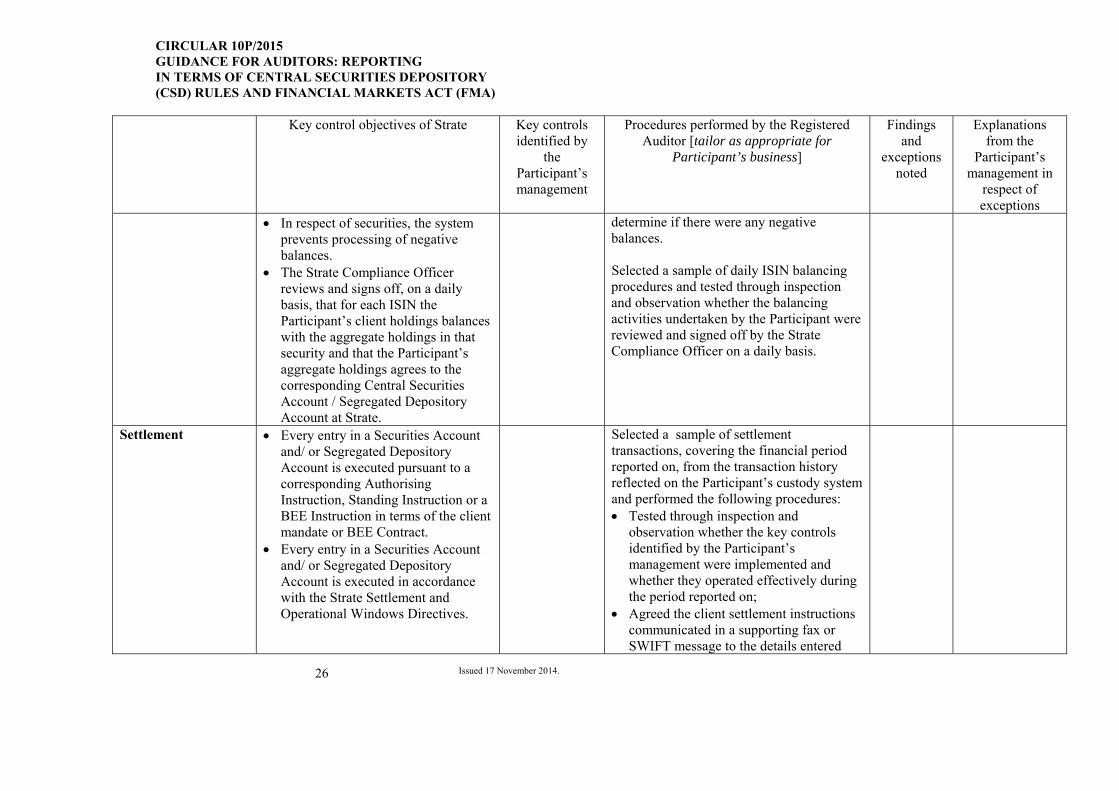

In respect of securities, the system prevents processing of negative balances.

The Strate Compliance Officer reviews and signs off, on a daily basis, that for each ISIN the Participant’s client holdings balances with the aggregate holdings in that security and that the Participant’s aggregate holdings agrees to the corresponding Central Securities Account / Segregated Depository Account at Strate.

determine if there were any negative balances. Selected a sample of daily ISIN balancing procedures and tested through inspection and observation whether the balancing activities undertaken by the Participant were reviewed and signed off by the Strate Compliance Officer on a daily basis.

Settlement Every entry in a Securities Account and/ or Segregated Depository Account is executed pursuant to a corresponding Authorising Instruction, Standing Instruction or a BEE Instruction in terms of the client mandate or BEE Contract.

Every entry in a Securities Account and/ or Segregated Depository Account is executed in accordance with the Strate Settlement and Operational Windows Directives.

Selected a sample of settlement transactions, covering the financial period reported on, from the transaction history reflected on the Participant’s custody system and performed the following procedures: Tested through inspection and

observation whether the key controls identified by the Participant’s management were implemented and whether they operated effectively during the period reported on;

Agreed the client settlement instructions communicated in a supporting fax or SWIFT message to the details entered

CIRCULAR 10P/2015 GUIDANCE FOR AUDITORS: REPORTING IN TERMS OF CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND FINANCIAL MARKETS ACT (FMA)

27 Issued 17 November 2014.

Key control objectives of Strate Key controls identified by

the Participant’s management

Procedures performed by the Registered Auditor [tailor as appropriate for

Participant’s business]

Findings and

exceptions noted

Explanations from the

Participant’s management in

respect of exceptions

into the Participant’s custody system. Agreed the details entered into the

Participant’s custody system to the applicable message standard sent to Strate confirming the transaction.

Agreed the details of the transaction as reflected in the Strate records to the client statement for evaluating whether the client received true value (cash and securities) on the same day as the settlement took place.

Agreed the underlying transaction to the CSD system through the use of the applicable transaction reference number to determine whether the transaction was reported to Strate.

Selected a sample of transactions that have not been reported to Strate for settlement and determine the reasons for such internal book entries.

Securities Transfer Tax Act (STT Act) – Equities

The Participant’s system automatically defaults the STT indicator to "YES" when capturing a client instruction.

The indicator can only be changed in certain circumstances (when advised by the client) and when relevant

Observed that the Participant’s client instruction was entered into the Participant’s custody system to determine whether the system defaults to levy STT. Selected a sample of off-market transactions from the transaction history reflected on the

CIRCULAR 10P/2015 GUIDANCE FOR AUDITORS: REPORTING IN TERMS OF CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND FINANCIAL MARKETS ACT (FMA)

28 Issued 17 November 2014.

Key control objectives of Strate Key controls identified by

the Participant’s management

Procedures performed by the Registered Auditor [tailor as appropriate for

Participant’s business]

Findings and

exceptions noted

Explanations from the

Participant’s management in

respect of exceptions

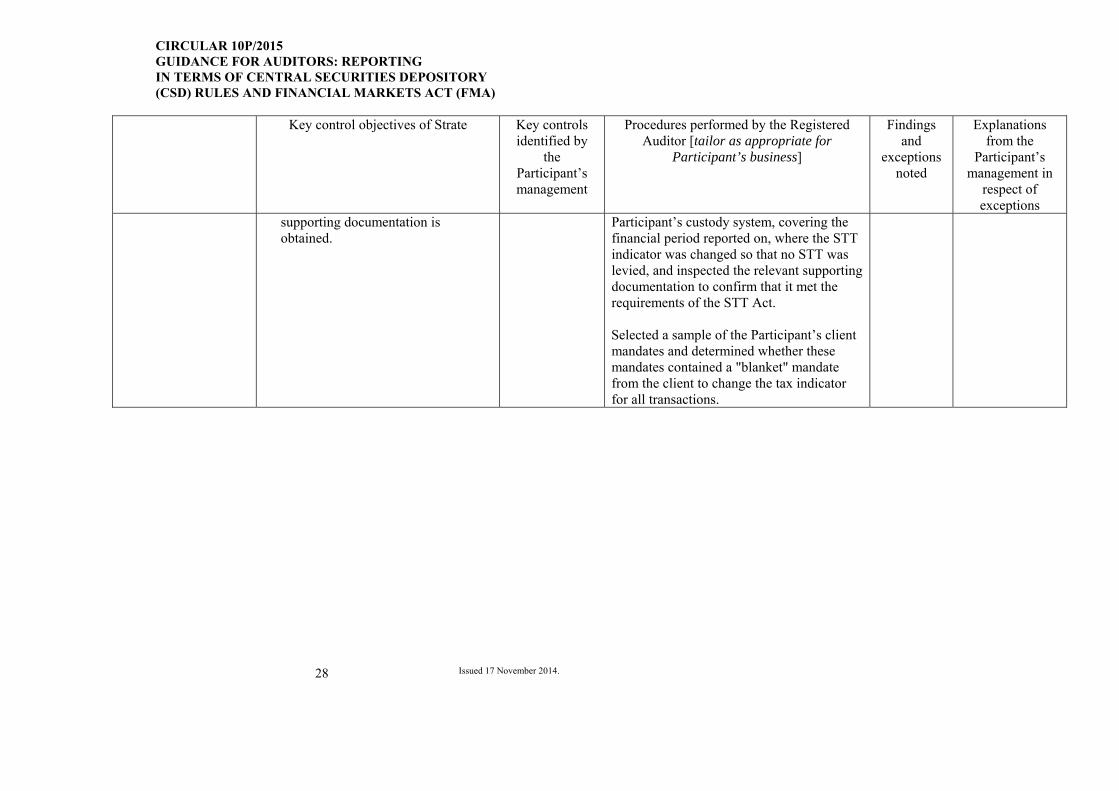

supporting documentation is obtained.

Participant’s custody system, covering the financial period reported on, where the STT indicator was changed so that no STT was levied, and inspected the relevant supporting documentation to confirm that it met the requirements of the STT Act. Selected a sample of the Participant’s client mandates and determined whether these mandates contained a "blanket" mandate from the client to change the tax indicator for all transactions.

CIRCULAR 10P/2015 GUIDANCE FOR AUDITORS: REPORTING IN TERMS OF CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND FINANCIAL MARKETS ACT (FMA)

29 Issued 17 November 2014.

Key control objectives of Strate Key controls identified by

the Participant’s management

Procedures performed by the Registered Auditor [tailor as appropriate for

Participant’s business]

Findings and

exceptions noted

Explanations from the

Participant’s management in

respect of exceptions

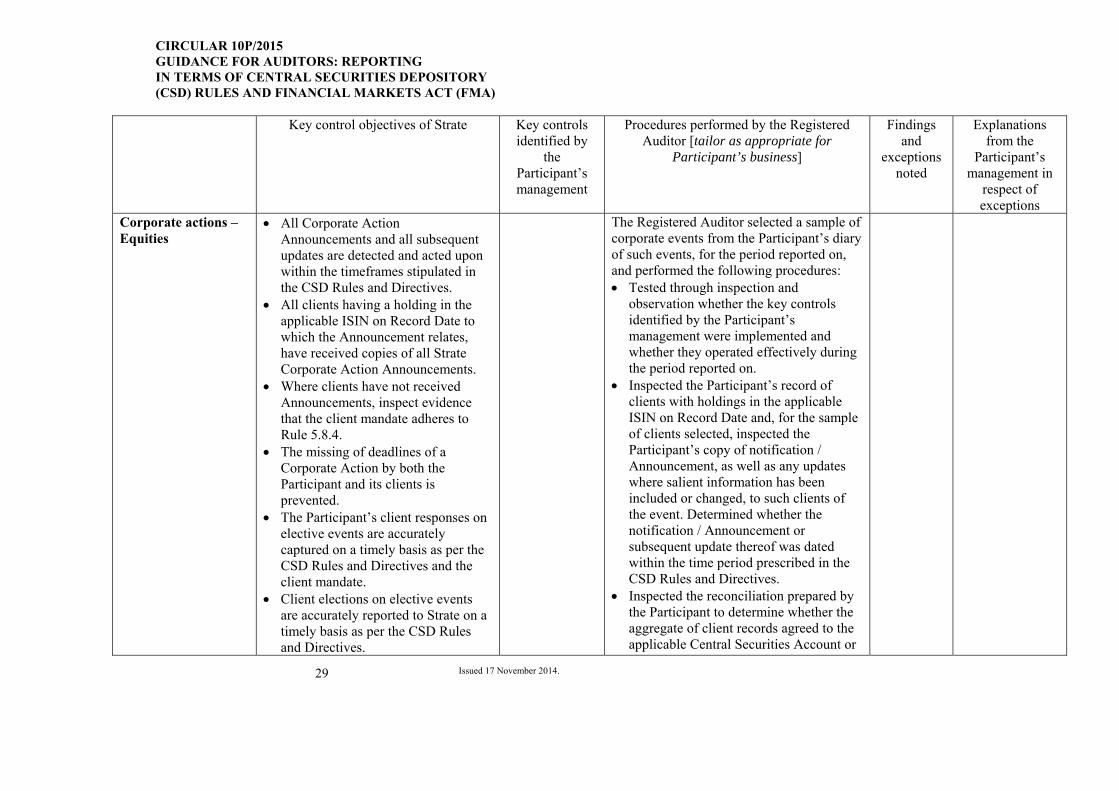

Corporate actions – Equities

All Corporate Action Announcements and all subsequent updates are detected and acted upon within the timeframes stipulated in the CSD Rules and Directives.

All clients having a holding in the applicable ISIN on Record Date to which the Announcement relates, have received copies of all Strate Corporate Action Announcements.

Where clients have not received Announcements, inspect evidence that the client mandate adheres to Rule 5.8.4.

The missing of deadlines of a Corporate Action by both the Participant and its clients is prevented.

The Participant’s client responses on elective events are accurately captured on a timely basis as per the CSD Rules and Directives and the client mandate.

Client elections on elective events are accurately reported to Strate on a timely basis as per the CSD Rules and Directives.

The Registered Auditor selected a sample of corporate events from the Participant’s diary of such events, for the period reported on, and performed the following procedures: Tested through inspection and

observation whether the key controls identified by the Participant’s management were implemented and whether they operated effectively during the period reported on.

Inspected the Participant’s record of clients with holdings in the applicable ISIN on Record Date and, for the sample of clients selected, inspected the Participant’s copy of notification / Announcement, as well as any updates where salient information has been included or changed, to such clients of the event. Determined whether the notification / Announcement or subsequent update thereof was dated within the time period prescribed in the CSD Rules and Directives.

Inspected the reconciliation prepared by the Participant to determine whether the aggregate of client records agreed to the applicable Central Securities Account or

CIRCULAR 10P/2015 GUIDANCE FOR AUDITORS: REPORTING IN TERMS OF CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND FINANCIAL MARKETS ACT (FMA)

30 Issued 17 November 2014.

Key control objectives of Strate Key controls identified by

the Participant’s management

Procedures performed by the Registered Auditor [tailor as appropriate for

Participant’s business]

Findings and

exceptions noted

Explanations from the

Participant’s management in

respect of exceptions

In respect of proxy voting, proxies and/ or letters of representation are requested from the nominee and received in sufficient time for the beneficial owner to attend and vote at the meeting.

Cash and/ or security entitlements are credited to the account of the holder (nominee or beneficial) on the same day as received from the CSD, so that true value is ensured on settlement day.

The aggregate of client records must agree to the applicable Central Securities Account or Segregated Depository Account at Strate after each corporate event.

Segregated Depository Account at Strate after each corporate event.

CIRCULAR 10P/2015 GUIDANCE FOR AUDITORS: REPORTING IN TERMS OF CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND FINANCIAL MARKETS ACT (FMA)

31 Issued 17 November 2014.

Key control objectives of Strate Key controls identified by

the Participant’s management

Procedures performed by the Registered Auditor [tailor as appropriate for

Participant’s business]

Findings and

exceptions noted

Explanations from the

Participant’s management in

respect of exceptions

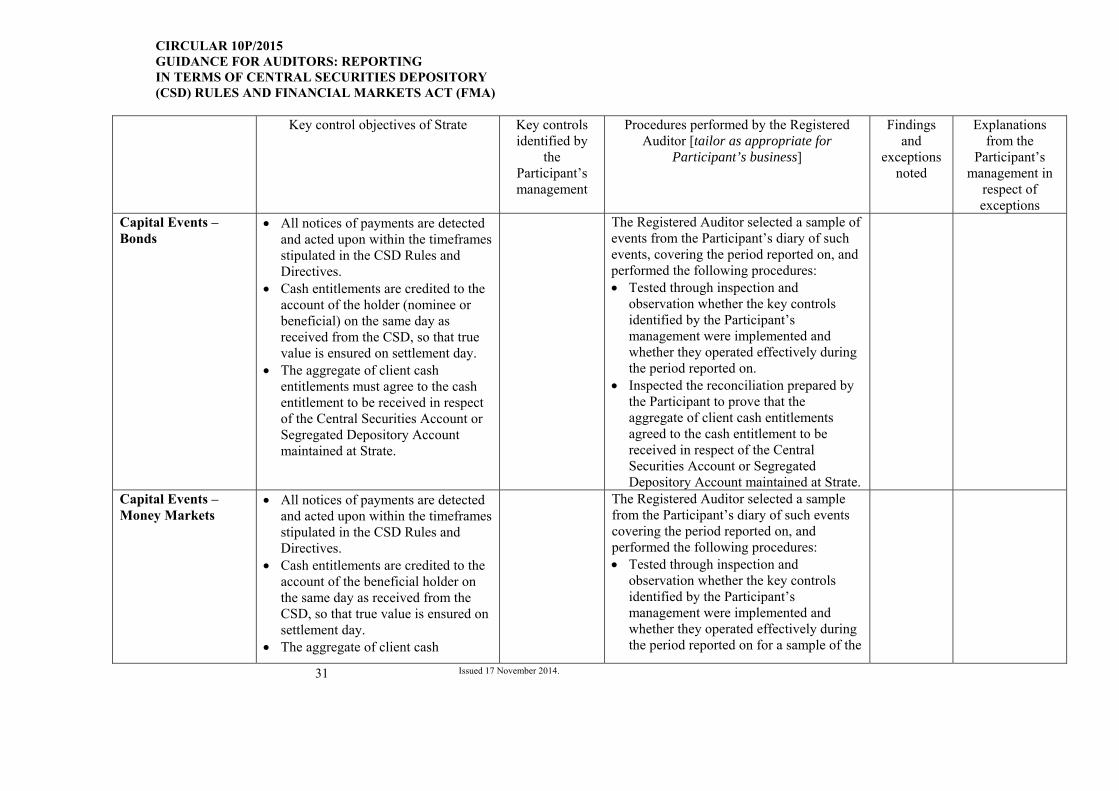

Capital Events – Bonds

All notices of payments are detected and acted upon within the timeframes stipulated in the CSD Rules and Directives.

Cash entitlements are credited to the account of the holder (nominee or beneficial) on the same day as received from the CSD, so that true value is ensured on settlement day.

The aggregate of client cash entitlements must agree to the cash entitlement to be received in respect of the Central Securities Account or Segregated Depository Account maintained at Strate.

The Registered Auditor selected a sample of events from the Participant’s diary of such events, covering the period reported on, and performed the following procedures: Tested through inspection and

observation whether the key controls identified by the Participant’s management were implemented and whether they operated effectively during the period reported on.

Inspected the reconciliation prepared by the Participant to prove that the aggregate of client cash entitlements agreed to the cash entitlement to be received in respect of the Central Securities Account or Segregated Depository Account maintained at Strate.

Capital Events – Money Markets

All notices of payments are detected and acted upon within the timeframes stipulated in the CSD Rules and Directives.

Cash entitlements are credited to the account of the beneficial holder on the same day as received from the CSD, so that true value is ensured on settlement day.

The aggregate of client cash

The Registered Auditor selected a sample from the Participant’s diary of such events covering the period reported on, and performed the following procedures: Tested through inspection and

observation whether the key controls identified by the Participant’s management were implemented and whether they operated effectively during the period reported on for a sample of the

CIRCULAR 10P/2015 GUIDANCE FOR AUDITORS: REPORTING IN TERMS OF CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND FINANCIAL MARKETS ACT (FMA)

32 Issued 17 November 2014.

Key control objectives of Strate Key controls identified by

the Participant’s management

Procedures performed by the Registered Auditor [tailor as appropriate for

Participant’s business]

Findings and

exceptions noted

Explanations from the

Participant’s management in

respect of exceptions

entitlements must agree to the cash entitlements received in the South African Multiple Options System.

Participant’s clients from each of those events.

Inspected the reconciliation prepared by the Participant to prove that the aggregate of client cash entitlements agreed to the cash entitlement received in the South African Multiple Options System.

CIRCULAR 10P/2015 GUIDANCE FOR AUDITORS: REPORTING IN TERMS OF CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND FINANCIAL MARKETS ACT (FMA)

33 Issued 17 November 2014.

Key control objectives of Strate Key controls identified by

the Participant’s management

Procedures performed by the Registered Auditor [tailor as appropriate for

Participant’s business]

Findings and

exceptions noted

Explanations from the

Participant’s management in

respect of exceptions

BEE Securities

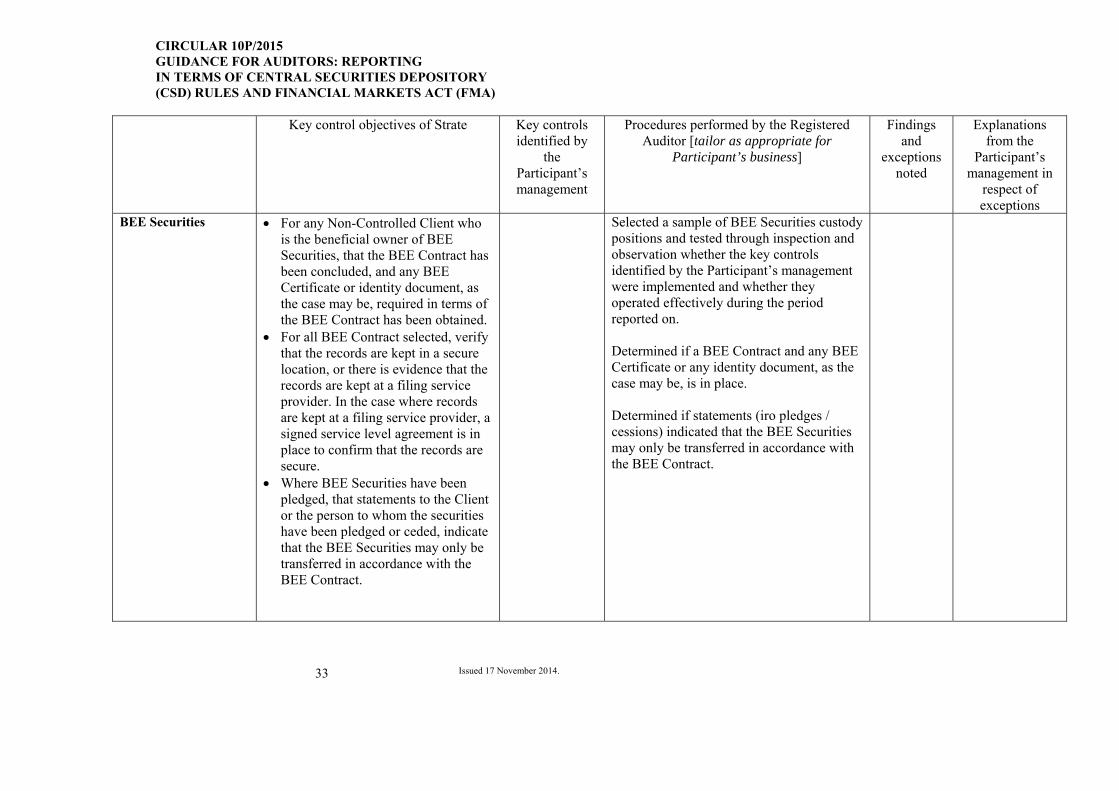

For any Non-Controlled Client who is the beneficial owner of BEE Securities, that the BEE Contract has been concluded, and any BEE Certificate or identity document, as the case may be, required in terms of the BEE Contract has been obtained.

For all BEE Contract selected, verify that the records are kept in a secure location, or there is evidence that the records are kept at a filing service provider. In the case where records are kept at a filing service provider, a signed service level agreement is in place to confirm that the records are secure.

Where BEE Securities have been pledged, that statements to the Client or the person to whom the securities have been pledged or ceded, indicate that the BEE Securities may only be transferred in accordance with the BEE Contract.

Selected a sample of BEE Securities custody positions and tested through inspection and observation whether the key controls identified by the Participant’s management were implemented and whether they operated effectively during the period reported on. Determined if a BEE Contract and any BEE Certificate or any identity document, as the case may be, is in place. Determined if statements (iro pledges / cessions) indicated that the BEE Securities may only be transferred in accordance with the BEE Contract.

CIRCULAR 10P/2015 GUIDANCE FOR AUDITORS: REPORTING IN TERMS OF CENTRAL SECURITIES DEPOSITORY (CSD) RULES AND FINANCIAL MARKETS ACT (FMA)

34 Issued 17 November 2014.

Key control objectives of Strate Key controls identified by

the Participant’s management

Procedures performed by the Registered Auditor [tailor as appropriate for

Participant’s business]

Findings and

exceptions noted

Explanations from the

Participant’s management in

respect of exceptions

Segregated Depository Accounts – Equities and Bonds

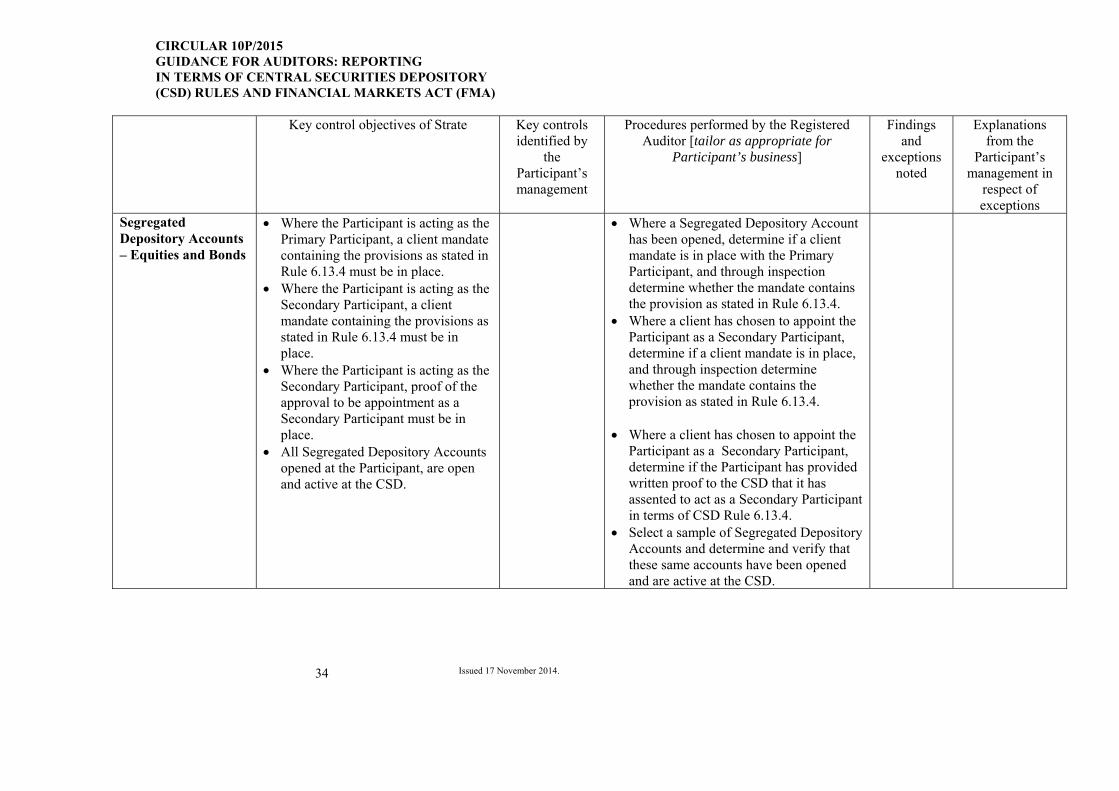

Where the Participant is acting as the Primary Participant, a client mandate containing the provisions as stated in Rule 6.13.4 must be in place.

Where the Participant is acting as the Secondary Participant, a client mandate containing the provisions as stated in Rule 6.13.4 must be in place.

Where the Participant is acting as the Secondary Participant, proof of the approval to be appointment as a Secondary Participant must be in place.

All Segregated Depository Accounts opened at the Participant, are open and active at the CSD.

Where a Segregated Depository Account has been opened, determine if a client mandate is in place with the Primary Participant, and through inspection determine whether the mandate contains the provision as stated in Rule 6.13.4.

Where a client has chosen to appoint the Participant as a Secondary Participant, determine if a client mandate is in place, and through inspection determine whether the mandate contains the provision as stated in Rule 6.13.4.

Where a client has chosen to appoint the

Participant as a Secondary Participant, determine if the Participant has provided written proof to the CSD that it has assented to act as a Secondary Participant in terms of CSD Rule 6.13.4.

Select a sample of Segregated Depository Accounts and determine and verify that these same accounts have been opened and are active at the CSD.