Embed Size (px)

DESCRIPTION

Ageing and the Tax Implied in Public Pension Schemes: Simulations for Selected OECD Countries*. Robert Fenge / Martin Werding Ifo Institute for Economic Research & CESifo. * Generous support by the Economic and Social Research Institute (ESRI) - PowerPoint PPT Presentation

Citation preview

Ageing and the Tax Implied in Public Pension Schemes:

Simulations for Selected OECD Countries*

Robert Fenge / Martin Werding

Ifo Institute for Economic Research & CESifo

* Generous support by the Economic and Social Research Institute (ESRI)of the Japanese Government is gratefully acknowledged.

The Impact of Ageing on Public Pensions

Concepts of measurement:

• Net pension liabilities

• General government fiscal balances

• Generational accounting

• “Implicit taxes”

Implicit taxes: definition #1

• Implicit tax falling on “generation t”: ITt = NPV (contributionst) – NPV (benefitst+1)

• Implicit tax rate: t = ITt / wt = [twt – pt+1 / (1+rt +1)] / wt =

)(1

111

1

)1)(1(1

t

tt

t

tt r

ng

• Extension to an N-period setting ...

Implicit taxes: definition #2

• straightforward from the simple algebra of pensions

• well-founded in pension theory (Sinn 2000): 0 < 0; N00 = –ID0; ID0 = Ntt, t = 1

• easy to apply to an empirical context (Thum / Weizsaecker 2000; Fenge / Werding 2001)

• suited to analyse welfare effects at an individual level

Implicit taxes: applicationto real-world pension schemes

• Financial projections for public pension schemes in selected OECD countries(CESifo Pension Model)

• Stylised biographies for representative individuals (covering disability pensions, old-age pensions, and survivor pensions)

• The rôle of assumptions ...

• Impact of policy responses

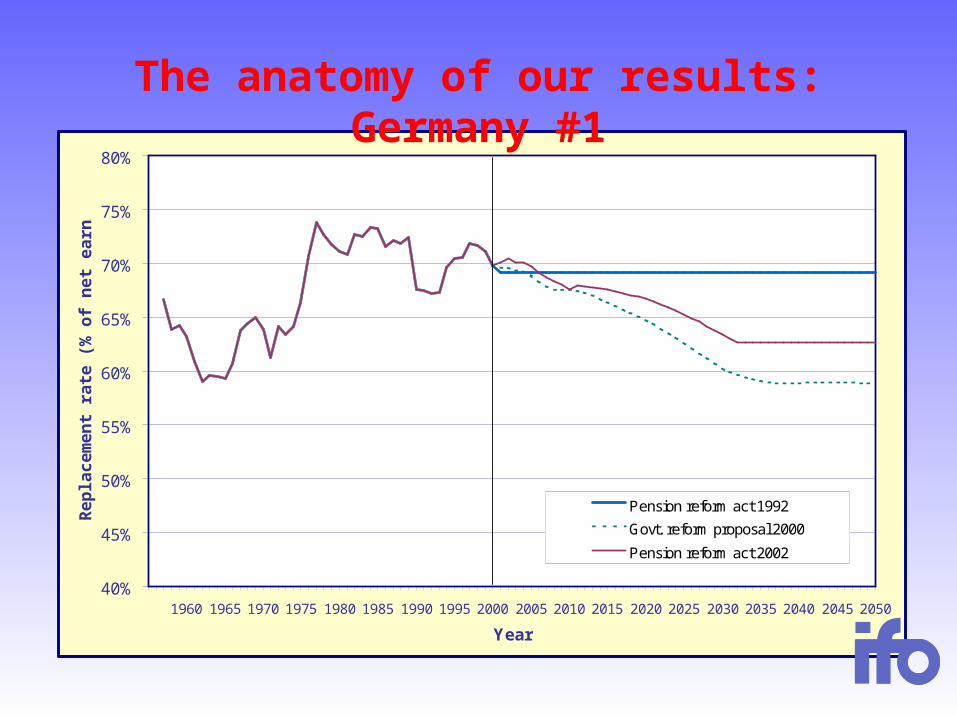

40%

45%

50%

55%

60%

65%

70%

75%

80%

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Year

Re

pla

ce

me

nt

rate

(%

of

ne

t e

arn

ing

s)

Pension reform act 1992

Govt. reform proposal 2000

Pension reform act 2002

The anatomy of our results: Germany #1

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

30%

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Year

Co

ntr

ibu

tio

n r

ate

(%

of

gro

ss

ea

rnin

gs

)

Pension reform act 1992

Govt. reform proposal 2000

Pension reform act 2002

The anatomy of our results: Germany #2

Incremental reforms: Germany

6%

8%

10%

12%

14%

16%

18%

20%

22%

1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

Age cohorts (by year of birth)

Imp

licit

ta

x r

ate

(%

of

life

tim

e e

arn

ing

s)

Pension reform act 1992

Govt. reform proposal 2000 (benefit level –15%)

Pension reform act 2002 (benefit level –10%)

Fixing contribution rates: Austria

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

Age cohorts (by year of birth)

Imp

licit

ta

x r

ate

(%

of

life

tim

e e

arn

ing

s)

Fixed contribution rate

Fixed level of benefits

CPI indexation (p. after award): France

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

Age cohorts (by year of birth)

Imp

licit

ta

x r

ate

(%

of

life

tim

e e

arn

ing

s)

Current law

Pre-1993 law

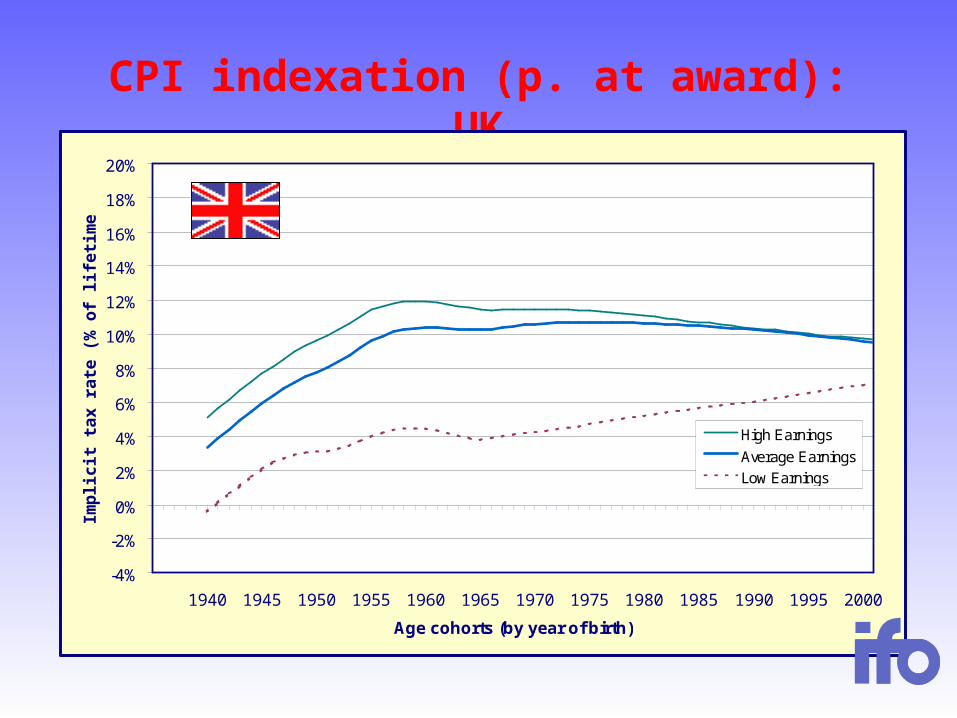

CPI indexation (p. at award): UK

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

Age cohorts (by year of birth)

Imp

licit

ta

x r

ate

(%

of

life

tim

e e

arn

ing

s)

High Earnings

Average Earnings

Low Earnings

Partial pre-funding: USA

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

Age cohorts (by year of birth)

Imp

licit

ta

x r

ate

(%

of

life

tim

e e

arn

ing

s) Trust fund

Pure PAYG

A “funded” system: Japan

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

Age cohorts (by year of birth)

Imp

licit

ta

x r

ate

(%

of

life

tim

e e

arn

ing

s)

Status quo 1999: constant level of benefits

Reform 2000: level of benefits -15%

Concluding remarks

• Not surprisingly, ageing causes a general upward trend in implicit tax rates

• Levels and curvatures of tax profiles are highly country-specific

• Effectiveness of different policy measures can be illustrated

• Is tax smoothing useful?

Annex

The standardised agent’s biography*

* Basic assumptions for the case of Germany. Probability of disablement andconditional life expectancies adapted to national averages.

UK: The impact of wage indexation

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

Age cohorts (by year of birth)

Imp

licit

ta

x r

ate

(%

of

life

tim

e e

arn

ing

s)

High Earnings

Average Earnings

Low Earnings

UK: The effects of contracting-out

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

Age cohorts (by year of birth)

Imp

licit

ta

x r

ate

(%

of

life

tim

e e

arn

ing

s)

Average Earnings (Contracted in)

Average Earnings (Contracted out)Earnings uprating

Price Uprating