Embed Size (px)

Citation preview

AGEC 420, Lec 40 1

Agec 420

HW #8: Regression – Fri. May 3HW #9: Options in TradeSim – Wed, May 8HW #10 - ungradedExam 3: Friday, May 3 - Review session, May 2, 7pm, WA 41

TodayTime valueOption ‘Delta’Position diagrams

AGEC 420, Lec 40 2

Checking Account

Initial balance ($10 * 85) $850 Wheat trade margin -$175Corn trade margin - $125

Withdrawals -$300

Balance in checking $550

AGEC 420, Lec 40 3

Margin Account

Deposits ($175, $125) $300.00 Wheat trade (bot 2820, sold 2714) -$105.00Commissions/Fees - $25.12Corn trade (bot 2292, at 2180) -$112.50Commissions/Fees - $25.11

Withdrawals -$267.73

Balance in margin account $32.27

AGEC 420, Lec 40 4

$$$

• Checking $550.00

• Margin $ 32.27– Balance $582.27 (= $6.85/person)

AGEC 420, Lec 40 5

Markets

• CBOT: http://www.cbot.com/

• CME: http://www.cme.com/

AGEC 420, Lec 40 6

Aug’02 Cattle

AGEC 420, Lec 40 7

Options - review

Call option:– right to buy the underlying futures contract – at the specified strike price

Put option:– right to sell the futures at the strike price

ReadingPurcell & Koontz – Ch 7 (pp203-224)CBOT Publication – on web page

8 AGEC 420, Lec 40

Put – Call Parity

Futures @ ????Strike Put Call

230 76 134240 135 94250 206 65260 286 47270 373 33

9 AGEC 420, Lec 40

Put – Call Parity

Futures @ 2356Strike Put Call

230 76 134240 135 94250 206 65260 286 47270 373 33

AGEC 420, Lec 40 10

Time value

• Reflects the market’s expectation for an option to have additional intrinsic value

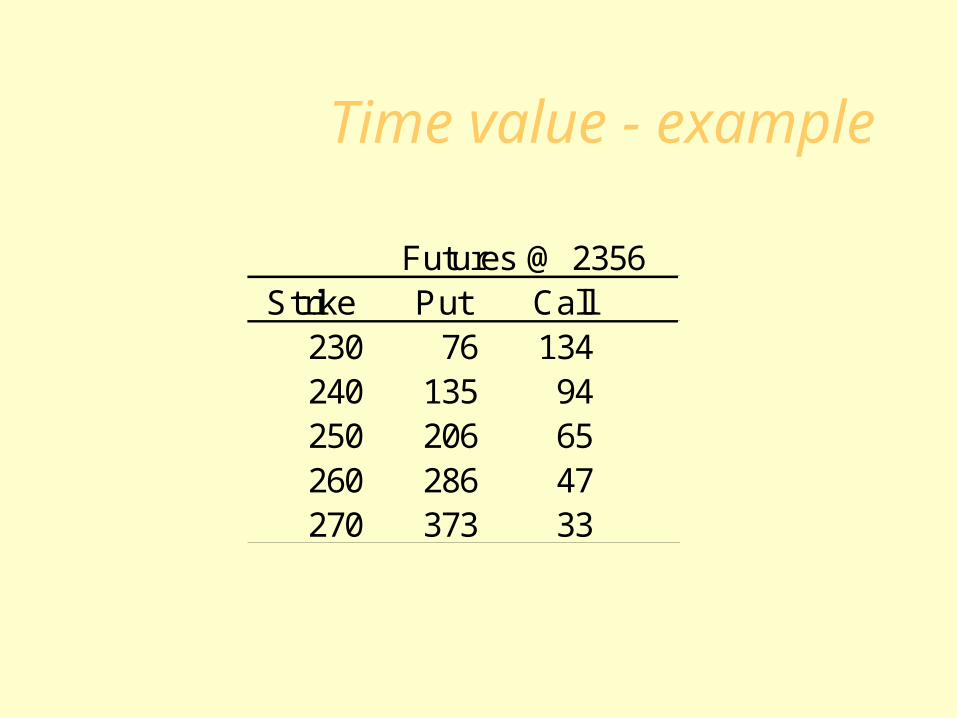

Time value - example

Futures @ 2356Strike Put Call

230 76 134240 135 94250 206 65260 286 47270 373 33

Time value of Puts

Futures @ 2356Strike Put (TV) Call

230 76 134240 135 93 94250 206 64 65260 286 47 47270 373 33 33

AGEC 420, Lec 40 13

Time value

• Reflects the market’s expectation for an option to have additional intrinsic value

• Options farther in- or out-of-the –money have lower time value (lower probability of additional intrinsic value)

• “Time decay”: the decline in time value as time passes: Time decay is more rapid as expiration approaches.

AGEC 420, Lec 40 14

Option Delta

• Option prices don’t change as quickly as futures prices

15 AGEC 420, Lec 40

Futures @ 2356 Futures @ 2394 (+36)Strike Put Call Put

230 76 134 62 (-14)240 135 94 114 (-21)250 206 65 183 (-23)260 286 47 260 (-26)270 373 33 342 (-31)

Delta – example with Puts

AGEC 420, Lec 40 16

Calculating Option Delta

• Futures price change = +3¾

Option Change Delta

230 Put - 1½ 1½ / 3¾ = 0.4

240 Put - 21/8 21/8 / 3¾ = 0.56

250 Put - 23/8 23/8 / 3¾ = 0.63

260 Put - 2¾ 2¾ / 3¾ = 0.73

17 AGEC 420, Lec 40

Futures @ 2356 Futures @ 2394 (+36)Strike Put Call Put Call

230 76 134 62 (-14) 154 (+20)240 135 94 114 (-21) 110 (+16)250 206 65 183 (-23) 77 (+12)260 286 47 260 (-26) 55 (+6)270 373 33 342 (-31) 40 (+6)

Delta – example with Calls

AGEC 420, Lec 40 18

Values for Delta

• Delta = d option price / d futures price– varies between 0 and 1

Option Delta (abs. value)Deep out-of-the-money near 0Out-of-the money 0 to 0.5At-the-money approx 0.5In-the-money 0.5 to 1.0Deep in-the-money near 1.0

AGEC 420, Lec 40 19

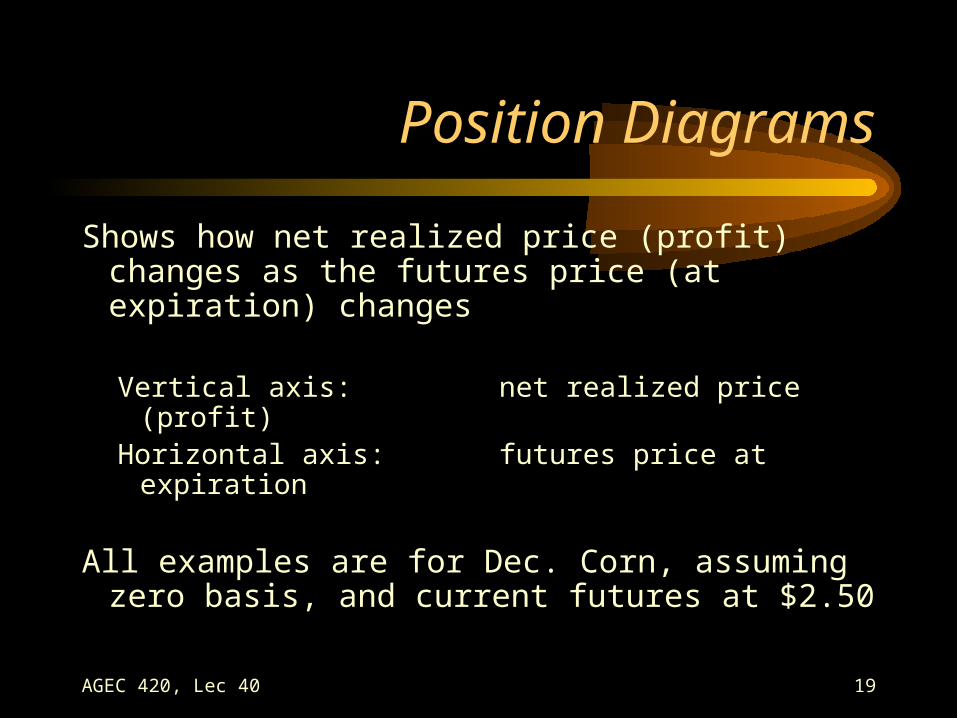

Position Diagrams

Shows how net realized price (profit) changes as the futures price (at expiration) changes

Vertical axis: net realized price (profit)

Horizontal axis: futures price at expiration

All examples are for Dec. Corn, assuming zero basis, and current futures at $2.50

Long Cash

Net Price 2.80

2.50

2.20

2.20 2.50 2.80Futures Price

Cash

Short Futures @ 2.50

Net Profit +30

0

-30

2.20 2.50 2.80

+20

+10

-10

-20

Futures Price

Futures

Long Cash + Short Futures @ 2.50

Net Price

2.502.20 2.50 2.80

CashFutures

Hedge

2.80

2.70

2.60

2.40

2.30

2.20

Futures Hedge

AGEC 420, Lec 40 23

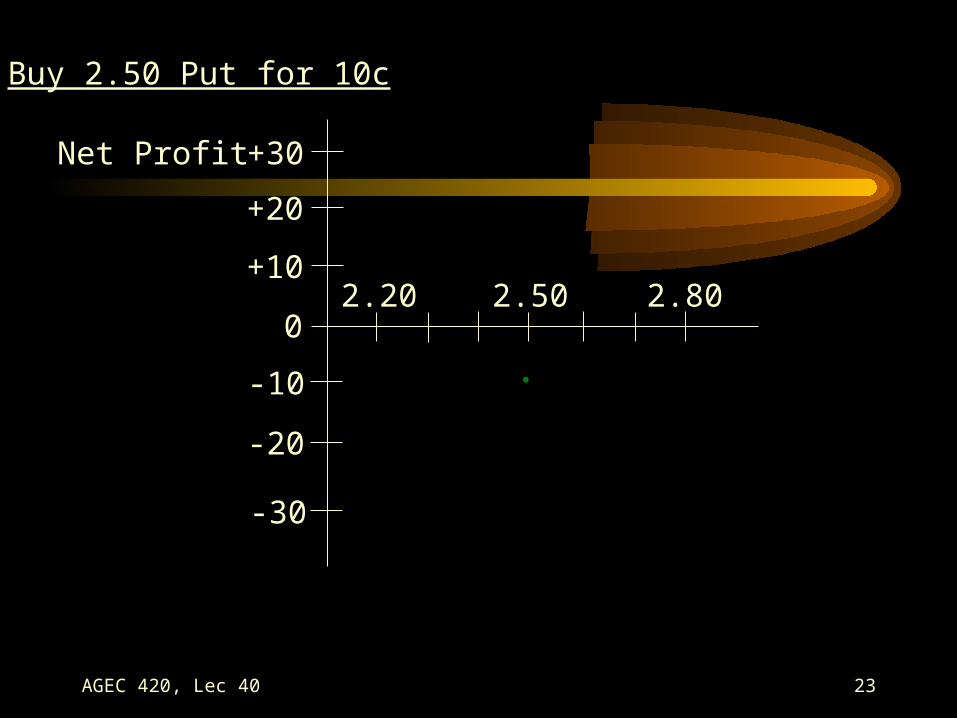

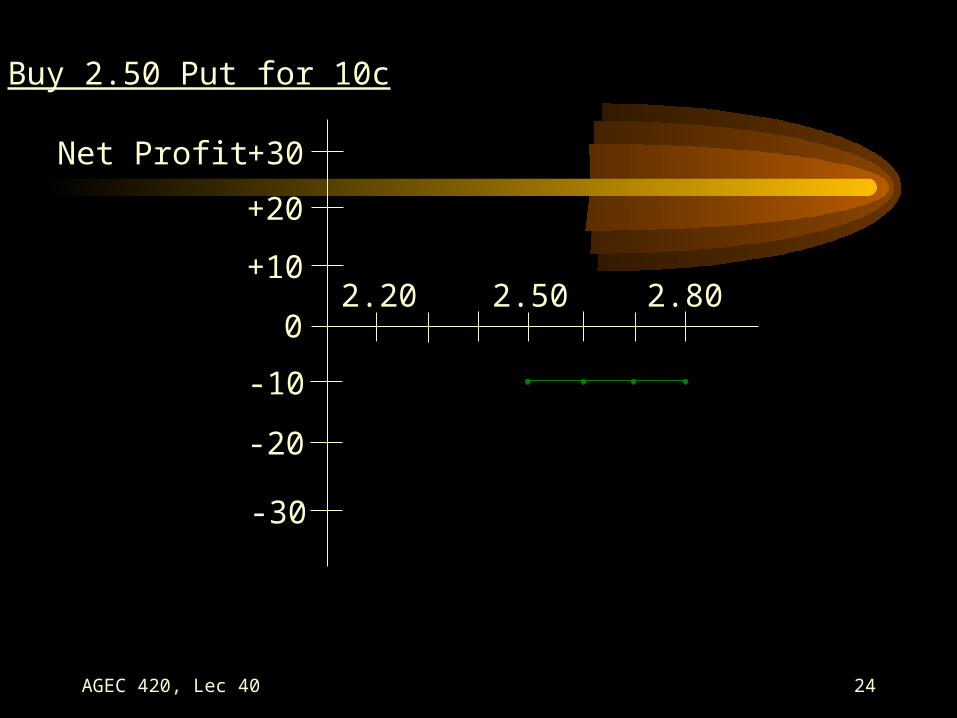

Buy 2.50 Put for 10c

Net Profit +30

0

-30

2.20 2.50 2.80

+20

+10

-10

-20

AGEC 420, Lec 40 24

Buy 2.50 Put for 10c

Net Profit +30

0

-30

2.20 2.50 2.80

+20

+10

-10

-20

AGEC 420, Lec 40 25

Buy 2.50 Put for 10c

Net Profit +30

0

-30

2.20 2.50 2.80

+20

+10

-10

-20

AGEC 420, Lec 40 26

Buy 2.50 Put for 10c

Net Profit +30

0

-30

2.20 2.50 2.80

+20

+10

-10

-20

AGEC 420, Lec 40 27

Hedge with a 2.50 Put

Net Price 280

250

220

2.20 2.50 2.80

270

260

240

230

PutCash

Hedge

AGEC 420, Lec 40 28

Price Floor

For a short hedger buying put options:

Price Floor = Strike price – Premium + Basis

AGEC 420, Lec 40 29

Sell 2.50 Put for 10c

Net Profit +30

0

-30

2.20 2.50 2.80

+20

+10

-10

-20

AGEC 420, Lec 40 30

Buy 2.50 Call for 10c

Net Profit +30

0

-30

2.20 2.50 2.80

+20

+10

-10

-20

AGEC 420, Lec 40 31

Sell 2.50 Call for 10c

Net Profit +30

0

-30

2.20 2.50 2.80

+20

+10

-10

-20

AGEC 420, Lec 40 32