Embed Size (px)

Citation preview

AFRICANECONOMIC OUTLOOKIN 2016

AFRICANECONOMIC OUTLOOKIN 2016

Featured ArticlesECONOMIC OUTLOOK FOR SUB-SAHARAN AFRICA IN 2016NIGERIA’S CURRENCY CONUNDRUM AMIDST THE OIL PRICE SLUMPETHIOPIA – NAVIGATING THE NEW NORMALSOUTH AFRICA OUTLOOK 2016: STAGFLATION IS THE MOST LIKELY OUTCOMENIGERIA’S ECONOMIC OUTLOOK & GROWTH PROSPECTS IN 2016REBUILDING GHANA’S ECONOMIC FUNDAMENTALS: PROSPECTS AND THREATS IN 2016 AND BEYOND

Exclusive InterviewsFRANCOIS CONRADIE |NKC AFRICAN ECONOMICSSAMIR GADIO | STANDARD CHARTERED BANKTHEA FOURIE | IHS ECONOMICS AND COUNTRY RISKANDREA MASIA | RMB MORGAN STANLEYTIAGO DIONISIO | EAGLESTONE SECURITIES

Featured ArticlesECONOMIC OUTLOOK FOR SUB-SAHARAN AFRICA IN 2016NIGERIA’S CURRENCY CONUNDRUM AMIDST THE OIL PRICE SLUMPETHIOPIA – NAVIGATING THE NEW NORMALSOUTH AFRICA OUTLOOK 2016: STAGFLATION IS THE MOST LIKELY OUTCOMENIGERIA’S ECONOMIC OUTLOOK & GROWTH PROSPECTS IN 2016REBUILDING GHANA’S ECONOMIC FUNDAMENTALS: PROSPECTS AND THREATS IN 2016 AND BEYOND

Exclusive InterviewsFRANCOIS CONRADIE |NKC AFRICAN ECONOMICSSAMIR GADIO | STANDARD CHARTERED BANKTHEA FOURIE | IHS ECONOMICS AND COUNTRY RISKANDREA MASIA | RMB MORGAN STANLEYTIAGO DIONISIO | EAGLESTONE SECURITIES

MARCH 2016

www.capitalmarketsinafrica.com

Editorial

EDITORIAL TEAM

Associate EditorMichael Osu

Contributing ExpertsTunde AkoduMichael Osu

Advertising & SalesTola Ketiku

Welcome to the first edition of INTO AFRICA, a new publication from Capital Markets in Africa, the leading “one-stop” platform for Africa’s fastest-growing Financial, Capital Markets and Wealth Management industry. This publication is aimed at providing you with fresh insight INTO AFRICA’s

emerging capital markets where we believe Africa is set for a challenging yet defining year ahead as it continues to build Investor confidence in the wider global community.

In 2015, Africa experienced its slowest economic growth rate since the 1998 global financial crisis. The Sub-Saharan Africa real GDP growth fell from 5.0 percent in 2014 to 3.75 percent in 2015 (IMF’s estimates). The downside risks in 2015 (low commodity prices, a slowing in China’s growth and uncertainty in the level of USA’s real growth rate) are expected to spill-over to 2016 but with reduced impact. As a result, IMF predicts that the region’s real growth will rebound to 4.0 percent in 2016 (against 4.3 percent predicted in the October 2015 IMF’s predictions).

For 2016 some economists and analysts believe Africa is at a tipping point and so this first edition of INTO AFRICA, focuses on the African Economic Outlook in 2016. Economic predictions can sometimes be guess work or very subjective so, for a balanced view, we interviewed 5 leading Africa-focused economists and analysts from African and global banking giants to give their views on the Economic Outlook for Africa in 2016. They are: FRANCOIS CONRAIE (Head of Research, NKC African Economics, South Africa), SAMIR GADIO (Head of Africa Strategy, Standard Chartered Bank), THEA FOURIE (Sub-Saharan Africa Senior Economist, ANDREA MASIA, (Economist, RMB Morgan Stanley Research), IHS Economics and Country Risk) and TIAGO DIONISIO (Chief Economist, Eaglestone Securities).

How will countries like Nigeria, South Africa, Ghana and Ethiopia navigate pressure from commodity slumps, China’s slow growth and falling Oil prices? For answers read Celeste Fauconnier, Nema

Ramkhelawan-Bhana and Neville Mandimika (Africa Analysts, Rand Merchant Bank, South Africa) who provide us with tangible insight into sub-Saharan Africa economies. They state that Africa will be forced to weather a considerable storm in 2016 as resource-laden economies address structural inefficiencies that were exposed by the staggering fall in commodities prices in 2015.

Looking at Nigeria, Africa’s largest economy, we bring you commentaries from two experts Pabina

Yinkere (Head of Research, Vetiva Capital Management Nigeria) and Ayodeji Ebo (Head, Investment Research, Afrinvest Securities Limited, Nigeria). Pabina gives the implications of a commodity price slump on Nigeria’s currency while Ayodeji provides a general economic outlook for Nigeria in 2016 in the article: Nigeria’s Economic Outlook & Growth Prospects in 2016.

On South Africa’s growth outlook, Sizwe Nxedlana (Chief Economist, First National Bank, South Africa) gives his verdict in South Africa Outlook 2016: Stagflation is the most likely outcome and suggests that significant policy uncertainty, negative ratings actions and slow foreign capital outflows explains the deteriorating Outlook.

Alan Cameron (Economist, Exotix Partner London) in his special commentary titled: Ethiopia –

Navigating the new normal 2016 suggests a difficult year for Ethiopia due to the adverse climactic effects of El Niño and questions about China’s commitment to the “One Belt, One Road” strategy.

Finally, find out what Courage Kingsley Martey, Economist at Databank Group, thinks is required for Ghana to restore Investor confidence in his contribution Main Risks to rebuilding Ghana’s

Fundamentals.

Kind regards,

Michael Osu

Associate Editor Capital Markets in Africa

Connect with the Editor on Linkedin.

Follow us on twitter @capitaMKTafrica.

To subscribe to INTO AFRICA, please send an email to [email protected].

Don’t forget to visit our website at www.capitalmarketsinafrica.com for the latest news, bespoke analysis, investment events and outlooks.

ENJOY!DISCLAIMER:The contents of this publication are general discussions reflecting the authors’ opinions of the typical issues involved in the respective subject areas and should not be relied upon as detailed or specific advice, or as professional advice of any kind. Whilst every care has been taken in preparing this document, no representation, warranty or undertaking (expressed or implied) is given and no responsibility or liability is accepted by CAPITAL MARKETS IN AFRICA or the authors or authors’ organisations as to the accuracy of the information contained and opinions expressed therein.

CONTENTSEconomic Outlook for sub-Saharan Africa in 2016

Nigeria’s currency conundrum amidst the oil price slump

Ethiopia – Navigating the new normal

South Africa Outlook 2016: Stagflation is the most likely outcome

Nigeria’s Economic Outlook & Growth Prospects in 2016

Rebuilding Ghana’s Economic Fundamentals: Prospects and Threats in 2016 And Beyond

Exclusive Interviews

FRANCOIS CONRADIEHead of Research at NKC African EconomicsSAMIR GADIO Head of Africa Strategy, FICC, Standard Chartered BankTHEA FOURIESub-Saharan Africa Senior Economist, IHS Economics and Country RiskANDREA MASIARMB Morgan StanleyTIAGO DIONISIOAssistant Director Chief Economist, Eaglestone Securities

To place adverts, sponsored features or commentaries in INTO AFRICA or on our website www.capitalmarketsinafrica.com, please contact [email protected]

Capital Markets in Africa provides both global and local players the advantage of international and local expertise. When you want ACCESS to the African Financial and Capital Markets or simply to keep an eye on what’s trending in Africa’s Capital Markets THINK Capital Markets in Africa.

VISIT WWW.CAPITALMARKETSINAFRICA.COM

Bespoke Analysis, Educative Articles & Intelligent ReportsInsightful Commentaries & In-depth Reviews

Unbiased Opinions/Views & Exclusive InterviewsUncover Africa’s INVESTMENT Opportunities & Threats

MANAGING AFRICAN EQUITYPORTFOLIOS IN A CHALLENGINGENVIRONMENTPaul Clark, Portfolio Manager, Ashburton Investments

4 | www.capitalmarketsinafrica.com

The clouds have gathered and sub-Saharan Africa (SSA) will be forced to weather a considerable storm in 2016 as resource-laden economies address structural inefficiencies that were exposed by the staggering fall in commodities prices in 2015.

The current cyclical downturn in commodities prices as well as less-supportive financial conditions resulted in a sharp deceleration in the region’s growth momentum. The economic struggles of the region are expected to continue over the medium term - the International Monetary Fund estimates real GDP growth for 2015 will amount to 3.75% in SSA, while in 2016, 4.25% is expected.

Given the austere 2015 backdrop where central banks had to strike a balance between economic growth and currency weakness, we expect that monetary policy will largely be hawkish as central banks continue their bid to defend their currencies against a strong dollar. With international reserves having declined markedly, the temptation might be to manipulate interest rates more than was the case in 2015. The effectiveness of such measures will prove challenging in the face of currency volatility.

Subdued commodity prices and concerns over dual deficits are likely to exert depreciatory pressure on various currencies in 2016, particularly those which are directly correlated to resource prices. Exogenous factors will impact the more globally traded currencies like the rand, Kenyan shilling and Mauritian rupee. The extent to which central banks smooth currency fluctuations will depend on the nature of their influence on domestic foreign exchange markets, via direct intervention and regulation, and the effectiveness of resources at their disposal. Exchange rates will act as an automatic stabiliser to correct fiscal and current account imbalances.

To add to SSA’s woes, the appetite for local currency assets petered out in 2015 as the unprecedented currency weakness eroded investor returns. Regulatory adjustments will prove challenging this year and authorities are likely to lean against the wind to stabilise financial markets but risk speculative outflows. In addition, sustained fiscal indiscipline will render fiscal policy inflexible in the event of an exogenous shock. Economies plagued by bloated wage bills, subsidies and/or contingent government liabilities will have to contend with mounting fiscal pressures, which might necessitate sharp and disorderly adjustments.

Weaker growth prospects in more developed economies could erode tax revenues, thereby slowing efforts to reduce budget deficits. Revenue growth is limited in resource-rich economies, implying greater shortfalls in budget financing. Despite an expected modest upturn in commodities in 2017, the mobilisation of revenues accruing from the sale of primary commodities will be slow, increasing the burden on domestic taxation.

Looking specifically at the resource-rich countries, the oil-exporting economies like Nigeria and Angola were hardest hit in 2015 and the economic pressure will certainly continue in 2016 and 2017 given the deteriorated outlook for the oil price. Both countries will grow below 4% in 2016 from levels of 7% over the past decade.

Mozambique’s strong growth over the past five years will now be hampered by lower global coal prices and infrastructure inadequacies, bursting the country’s mining boom bubble and causing some firms to cut production and investment. However, capital investment into the coal and oil and gas industries will keep growth rates above 6% over the forecast period. Middle income, resource-driven economies like Zambia and Ghana are also facing commodities price problems, especially from a copper and gold sector perspective, which are key foreign exchange earners. Together with the deteriorating fiscal environment and the consolidation as a consequence, growth will remain at the cusp of 5% in 2016.

Botswana and Namibia will face similar challenges as diamond revenues, specifically, are negatively affected by weak global demand, elevated stock levels and tight credit conditions for diamond site holders. But Namibia will experience some respite due to increased uranium production as the Husab mine comes online, while zinc, copper and gold production increases. The only non-resource-driven economy in our portfolio, Kenya, will in fact receive a boost from the downturn in the commodities price cycle, especially as fuel purchases make up a large chunk of the import bill. Also, Kenya will continue making progress toward establishing itself as a global energy producer. But sudden shocks to the exchange rate, terror threats, further monetary policy tightening and potential fiscal folly ahead of the 2017 presidential elections are key risks to our 6% average growth outlook for 2016 and 2017.

The South African economy will not escape the dominant global themes namely demographics, deleveraging, shrinking trade and disinflation. With financial conditions tightening in a weak rand environment, we think an outright local recession should not be dismissed. We expect the bottom in the cycle to be shown by a mere 0.6% expansion in 2016.

Unfortunately, the risk list is long for SSA and illustrates how sensitive SSA economies remain to internal and external shocks. Investment and economic diversity are key to overcoming some of these hurdles, but in SSA, these solutions are slow in progress. The biggest risks for 2016 and 2017 include: fiscal consolidation (with lower social spending as a consequence); low commodity prices; droughts; electricity shortages; lower consumer spending; funding challenges; a further China economic downturn; dollar gains; lower FDI; and geopolitical risk. Though global headwinds are likely to dissipate towards the end of 2016, their impact will linger well into 2017, amplifying domestic challenges.

ECONOMIC OUTLOOK FORSUBSAHARAN AFRICA IN 2016Celeste Fauconnier, Nema ‘Ramkhelawan-Bhana & Neville Mandimika, Africa Analysts at Rand Merchant Bank

6 | www.capitalmarketsinafrica.com

EXCLUSIVE INTERVIEWS

FRANCOIS CONRADIE

CMinAfrica: Looking back at 2015, in your opinion, what were the significant changes you noticed in the global economy and its impact on African economies?

Francois Conradie: The most important change in the global economy in 2015 was the broad collapse of most commodity prices. That collapse itself was a consequence of a more fundamental macroeconomic change that will continue to inform the global environment for several years, at least: the end of cheap credit and the rebalancing of China’s economy.

In many ways the 2015 commodity price collapse represents a continuation of the financial crisis that hit developed markets in 2008. China, thanks to tight State control over the economy and the economy’s sheer size, was able to defer deleveraging for a few years longer. But ultimately the debt binge started looking dangerous (especially in State-owned enterprises), and flabby demand from the developed world led the Communist Party’s technocrats to conclude that it was time to switch the nature of the economy from its focus on exporting to domestic consumption.

The result was an immediate and drastic reduction in Chinese orders for raw materials. The effect on Africa, where many economies remain undiversified and dependent on the exportation of raw materials, was severe. Currencies collapsed across the continent as inflows of foreign currency suddenly slowed markedly, and this resulted in immediate inflationary pressures as imported goods cost more in local currency terms. Governments, especially the oil exporters, faced (and continue to face) fiscal pressures as revenues declined, and many companies in the mining sector had to close their doors or reduce the scale of their operations.

CMinAfrica: Looking into 2016, what are the key opportunities and downside risks to watch out for in African economies?

Francois Conradie: The currency weakness that resulted from the commodity price slide, as disruptive as it is of older economic models, does present a window of opportunity for the development of a domestic secondary

sector and the further diversification of Africa’s economies. By making imported goods more expensive, inflation creates space for African entrepreneurs to start producing local substitutes, and it is these entrepreneurs that will, in the long run, change commodity-exporting economies into diversified ones.

At the same time weaker local currencies boost the incomes of African exporters who sell goods in which global prices have not fallen, especially farmers. The increase in their local currency receipts helps to mitigate the damage to overall consumption demand resulting from the commodity price collapse.

We see risk flowing from the dangers of unrest and labour action as poorer Africans, hit hardest by inflation and by the spending cuts enacted by cash-strapped governments, take to the streets to voice their displeasure. Strikes will further spook an already pessimistic business sector, while harsh police actions – unfortunately all too likely – will make the news across the world and fuel perceptions of Africa as a risky place to invest and do business.

CMinAfrica: Please provide your views on economic prospects in 2016 of: Senegal, Cameroon and Ivory Coast or any two or three Frontier African countries of your choice?

Francois Conradie: Ivory Coast will be one of Africa’s outstanding success stories in 2016. Its membership of the West African Economic and Monetary Union (WAEMU) means that it uses the regional currency, the CFA franc, which is in practice pegged to the euro. WAEMU member countries like Ivory Coast have thus been spared the inflation that threatens to have such harmful effects elsewhere on the continent. The economic policies of President Alassane Ouattara are well thought out and successful, and his liberal policies have attracted enough capital to his country to enable the launch of several major projects and the setting up of new companies. The fact that the country is busily reconstructing after a conflict that has taken up most of the past 15 years also boosts output, and underpins forecasts that GDP will grow by over 9% a year for the next two years.

FRANÇOIS CONRADIE HEAD OF RESEARCH AT NKC AFRICAN ECONOMICS. FRANÇOIS STUDIED A BA IN POLITICS, PHILOSOPHY AND ECONOMICS AT THE UNIVERSITY OF STELLENBOSCH, AND HOLDS AN MPHIL IN FUTURES STUDIES FROM THE SAME UNIVERSITY.

ANDREA MASIA ECONOMIST COVERING SOUTH AFRICA & OTHER SUB-SAHARAN AFRICAN MARKETS. ANDREA PREVIOUSLY HELD RESEARCH ROLES IN THE BANKING AND TELECOMMUNICATIONS SECTORS, AND HOLDS A MASTER’S DEGREE IN ECONOMICS FROM THE UNIVERSITY OF THE WITWATERSRAND.

SAMIR GADIOHEADS THE AFRICA STRATEGY TEAM, BASED IN LONDON. SAMIR HOLDS A PHD AND MA IN ECONOMICS FROM FORDHAM UNIVERSITY AND A BSC. IN ECONOMICS FROM THE RUSSIAN PEOPLES' FRIENDSHIP UNIVERSITY. HE SPEAKS ENGLISH, FRENCH AND RUSSIAN.

THEA FOURIESENIOR ECONOMIST, SUB-SAHARAN AFRICA AND FORMS PART OF THE ECR-ECONOMICS TEAM (ECONOMICS AND COUNTRY RISK) AT HER GROUP.

TIAGO DIONISIOASSISTANT DIRECTOR & CHIEF ECONOMIST, EAGLESTONE SECURITIES. TIAGO HAS OVER 15 YEARS’ EXPERIENCE IN INVESTMENT BANKING AND WRITES REGULARLY ON EMERGING & AFRICAN MARKET ECONOMIES.

What five top Africa focused Economists say on Africa's Economic Outlook for 2016

African Economic Outlook in 2016 | 7

EXCLUSIVE INTERVIEWS

While it does not promise the same stellar economic growth as Ivory Coast, Senegal is nonetheless expected to keep showing GDP growth of more than 5% a year until at least 2018 – no mean feat in the current depressed global environment. It is also a WAEMU member, with the protection against inflation that implies, and growth is concentrated in the secondary and tertiary sectors. If it can address its infrastructure issues (and it is trying hard), further healthy growth in industry can be expected.

SAMIR GADIO

CMinAfrica: Looking back into 2015, in your opinion, what were the significant changes you noticed in the global economy and its impact on African economies?

Samir Gadio: It is fair to say that 2015 was a challenging year for African capital markets. The strong USD negatively weighed on the fortunes of African currencies, lower commodity prices also resulted in pronounced pressure on the exchange rates of oil and copper producers, portfolio flows into frontier Sub-Sahara Africa were generally muted - if not negative - and Eurobond spreads widened significantly by year end in line with high-yield EM sovereigns. There were selected market opportunities, however, as short-dated yields in Kenya backed up aggressively in October to support the KES, and given that Uganda allowed its yield curve to shift significantly higher to underpin the UGX. Although foreign investors had largely exited the Nigerian market by Q3-2015, more accommodative liquidity and formal monetary conditions in the last few months of the year resulted in a substantial rally in the sovereign yield curve.

CMinAfrica: Looking at 2016, what are the key opportunities and downside risks to watch out for in African economies?

Samir Gadio: Looking into 2016, investors will probably seek to unlock value in SSA Eurobonds whose yields have risen to multi-year highs. Yet, this will require a catalyst for sustained yield compression, mainly a turn in the oil price cycle or at least more supportive global risk positioning. For the time being, defensive names such as Cote d’Ivoire and Senegal, and idiosyncratic stories (Ghana, Cameroon) will probably be more optimal investment opportunities on the Eurobond side. On the FX side, we expect the Nigerian naira and Angola kwanza to come under further pressure amid low oil prices, declining FX reserves and persistent FX shortages. In Nigeria’s case, this means that foreign investors will probably remain exposed to offshore non-deliverable forwards ahead of a likely NGN devaluation rather than the onshore fixed income market. There are interesting duration opportunities likely to emerge in other domestic SSA fixed income markets: we expect Uganda and Ghana’s yield curves to shift lower, barring further pronounced exchange rate weakness, as the authorities normalize their interest rate regime. In Kenya, the recent uptick in yields – amid a heavy redemption profile in H1-2016 – may translate into relative duration gains in the bond market in H2.

ANDREA MASIA

CMinAfrica: Looking back at 2015, in your opinion, what were the significant changes you noticed in the global economy and its impact on African economies?

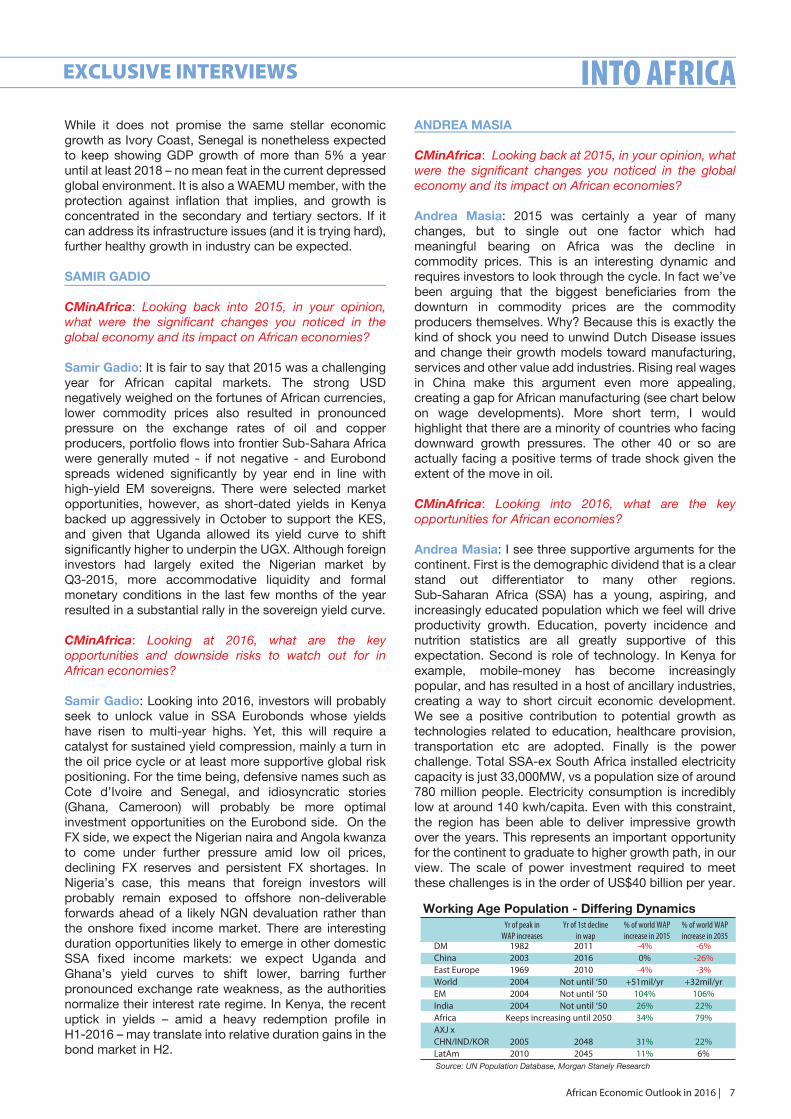

Andrea Masia: 2015 was certainly a year of many changes, but to single out one factor which had meaningful bearing on Africa was the decline in commodity prices. This is an interesting dynamic and requires investors to look through the cycle. In fact we’ve been arguing that the biggest beneficiaries from the downturn in commodity prices are the commodity producers themselves. Why? Because this is exactly the kind of shock you need to unwind Dutch Disease issues and change their growth models toward manufacturing, services and other value add industries. Rising real wages in China make this argument even more appealing, creating a gap for African manufacturing (see chart below on wage developments). More short term, I would highlight that there are a minority of countries who facing downward growth pressures. The other 40 or so are actually facing a positive terms of trade shock given the extent of the move in oil.

CMinAfrica: Looking into 2016, what are the key opportunities for African economies?

Andrea Masia: I see three supportive arguments for the continent. First is the demographic dividend that is a clear stand out differentiator to many other regions. Sub-Saharan Africa (SSA) has a young, aspiring, and increasingly educated population which we feel will drive productivity growth. Education, poverty incidence and nutrition statistics are all greatly supportive of this expectation. Second is role of technology. In Kenya for example, mobile-money has become increasingly popular, and has resulted in a host of ancillary industries, creating a way to short circuit economic development. We see a positive contribution to potential growth as technologies related to education, healthcare provision, transportation etc are adopted. Finally is the power challenge. Total SSA-ex South Africa installed electricity capacity is just 33,000MW, vs a population size of around 780 million people. Electricity consumption is incredibly low at around 140 kwh/capita. Even with this constraint, the region has been able to deliver impressive growth over the years. This represents an important opportunity for the continent to graduate to higher growth path, in our view. The scale of power investment required to meet these challenges is in the order of US$40 billion per year.

Working Age Population - Differing DynamicsYr of peak in

WAP increasesYr of 1st decline

in wap% of world WAPincrease in 2015

% of world WAPincrease in 2035

DM 1982 2011 -4% -6%China 2003 2016 0% -26%East Europe 1969 2010 -4% -3%World 2004 Not until ‘50 +51mil/yr +32mil/yrEM 2004 Not until ‘50 104% 106%India 2004 Not until ‘50 26% 22%Africa Keeps increasing until 2050 34% 79%AXJ x CHN/IND/KOR 2005 2048 31% 22%LatAm 2010 2045 11% 6%Source: UN Population Database, Morgan Stanely Research

8 | www.capitalmarketsinafrica.com

EXCLUSIVE INTERVIEWS

CMinAfrica: What would be your views on the economic prospects in 2016 of two or three Frontier African countries of your choice?

Andrea Masia: In Nigeria, macroeconomic policy choices which prioritise a closed capital account over a more liberalised foreign exchange market are severely impacting industrial supply chains. With the outlook for the terms of trade remaining weak, we expect GDP to expand by just 3.5% in 2016 and 4.5%Y in 2017. Risks are firmly skewed to the downside. Our concerns lie mainly in the manufacturing and retail sectors, which have collapsed from the stellar growth rates of previous years. In Kenya, we expect GDP growth to accelerate towards 6.0%Y in 2016 and 6.2%Y in 2017 as agricultural production gathers steam, commercial banks intensify their use of technological innovation, and as the ongoing improvements in transport networks help to free up distribution bottlenecks, buoying retail activity in the process. Elsewhere, the government’s commitment to deliver on capital deepening should also provide meaningful support to growth.

Finally in Ghana, all eyes will be on fiscal policy and the authority’s promise of fiscal consolidation under the current IMF programme. The 2016 budget forecasts a deficit of 5.3% of GDP. Underpinning this forecast is the important intent to keep the growth in public sector compensation below 14%Y – an ambition which, if achieved, would be a definitive success for the country.

THEA FOURIE

CMinAfrica: Looking back at 2015, in your opinion, what were the significant changes you noticed in the global economy and what were their impact on African economies?

Thea Fourie: The fall in international commodity prices on the back of lower growth in China had a significant impact on both oil and no-oil exporters. Currencies came under severe pressure, which fuelled inflation in the region. Some countries showed a slow policy response to the weaker currencies particularly Zambia and Mozambique, which added to the inflationary pressures. Foreign reserve holdings tapered down, leaving little cushion against the currency weakness.

CMinAfrica: Looking into 2016, what are the key opportunities and downside risks to watch out for in African economy?

Thea Fourie: Downside risks: The El Nino impact on the region places agricultural production, food prices, poverty and social unrest under the spotlight again. Sharp uptick in inflation and interest rates, combined with a shift towards some fiscal discipline leaves little room to support economies in the coming year. FDI inflows is expected to taper down even more as commodity prices remain under pressure. Current account and reserve holdings unlikely to improve. More countries approaches the IMF to have access to

non-concessional borrowing. Upside risk: The China-Africa relationship remains strong. China is expected to continue borrowing to the region and focus more on industrial development than before. Countries such as Angola, South Africa, Zambia benefit from Chinese support. Public sector fixed investment is expected to continue, however at a much slower pace. Some countries such as Mozambique will attract investment through natural gas development.

CMinAfrica: Please provide your views on economic prospects in 2016 of two or three Frontier African countries: Zambia and Mozambique?

Thea Fourie: Mozambique could be one of the fastest growing economies within the sub-Saharan African region, should natural gas development continue. A final investor decision is still pending, but prospects appear positive. The country moved to an IMF staff monitored program which means that fiscal and monetary policy will be more “healthy” going forward. Political concerns such as the recent outbreak between FRELIMO and RENAMO is not expected to delay natural gas developments. Low gas prices and lacklustre global demand is a bigger risk in this view.

Zambia is set for a tough year. The El Nino drought meant less electricity supply to the economy, electricity will have to be imported. Agricultural production, a large contributor to overall growth is also expected to suffer. A low copper price means less investment and some mines as suspended operations. The country is heading for elections in August 2016, and would like to avoid IMF assistance. It is our view however that they will have to move towards a staff monitored program in the near term for balance of payments support.

TIAGO DIONISIO

CMinAfrica: Looking back at 2015, in your opinion, what are the significant changes you noticed in the global economy and its impact on African economy?

Tiago Dionisio: In 2015, the global economy, and Africa in particular, was mostly impacted by three major reasons. First, the gradual deceleration in China and the rebalancing of its economic growth model away from investment and manufacturing toward consumption and services. Second, the significant drop in most commodity and energy prices. And third, the increased expectations that the Fed was going to start increasing interest rates in the US while other central banks (like the ECB) continued to ease monetary policy. The combination of these three issues impacted global trade and capital flows and increased external and fiscal vulnerabilities among commodity exporting countries in Africa, namely oil producers like Nigeria and Angola. Apart from external issues, economic activity in some African countries was also affected by domestic factors such as political instability and conflict as well as infrastructure bottlenecks like electricity shortages. CMinAfrica: Looking into 2016, what are the key opportunities and downside risks to watch out for in

African Economic Outlook in 2016 | 9

EXCLUSIVE INTERVIEWS

African economy?

Tiago Dionisio: We believe the three reasons mentioned above (the rebalancing in China’s economy, persistently low commodity prices and tighter global financial conditions) will continue to be the most important risks to watch out for in Africa this year. China is the main trading partner of a significant number of African countries (like Angola, Nigeria, South Africa and DRC) and so trade flows are expected to be impacted by slower Chinese economic activity. Persistently low commodity prices are also likely to depress export receipts (despite the depreciation of most African currencies against the dollar), impacting the contribution of net exports to real GDP growth and external imbalances. Moreover, low commodity prices should continue to hurt fiscal receipts and are likely to continue to require further cuts in public spending levels. Other risks worth noting include the impact that further currency depreciation could have on inflation and external debt levels. All in all, 2016 presents a good opportunity to (1) implement structural reforms and accelerate economic diversification, (2) improve the efficiency of public spending and broaden the tax base away from the commodities sector and (3) improve the business environment so that it attracts further foreign direct investment inflows.

CMinAfrica: Please provide your views on economic prospects in 2016 for Angola and Mozambique?

Tiago Dionisio: Angola, the country faces a challenging year ahead and the uncertainty around the outlook on oil prices presents considerable threats to the government’s budget execution and its economic growth perspectives. First, according to our calculations, if average oil prices remain at around US$ 30 per barrel this year this would have a negative impact of 16% on the government’s budgeted revenue forecast for 2016. In other words, it means that revenues would fall short of expectations by nearly US$ 3.6 billion (at the current exchange rate) and that the budget deficit would rise to 9.5% of GDP ceteris paribus (vs. 5.5% of GDP currently expected). And second, we have recently lowered our real GDP growth estimates for 2016 to 3.2% (vs. 3.5% previously), as we expect non-oil growth to remain relatively weak. This figure is marginally lower than the Angolan authorities’ target of 3.3%. We then expect a modest improvement to 3.6% in 2017.

More positively, we note that the government recently accelerated its fuel subsidy reform, which is expected to bring important savings to the public coffers. Three increases in domestic fuel prices since September 2014 coupled with the latest introduction of a free pricing system led to the elimination of subsidies on most fuels this year. According to the 2016 budget proposal, the government forecasts subsidies of AOA 447 billion for the energy sector. This is US$ 2.8 billion at the current exchange rate or 3.1% of GDP. The authorities should also aim to improve the quality of public spending, namely by reducing current expenditure levels, which remain excessively high at 81% of total public spending in 2016 (or 24.5% of GDP). The introduction of a new investment law in 2015 should also help attract more foreign investment in the country.

The new law is expected to facilitate doing business in Angola as it is more straightforward, easier to understand and presents few restrictions than previous laws.

All in all, we expect the government to remain focused on its social and infrastructure programs in the near term, particularly as we move into an election year in 2017, but some constraints are likely to exist due to the low oil price environment. This means that the local authorities could also postpone less crucial investment projects. Efforts to diversify the economy and broaden the non-oil tax base remain key challenges ahead. We do not see the announcement of a revised 2016 budget as imminent, but this scenario should not be ruled out if oil prices remain at these levels for too much longer.

Mozambique - Real GDP growth decelerated to 6.1% YoY in the first three quarters of 2015. This is well below the 8% rate recorded in the same period of the previous year. We estimate growth of 6.3% for the whole of 2015 and 6.5% this year, which remains below the country’s growth potential. Mozambique currently faces several headwinds that will likely prevent it from expanding at the rates witnessed in the last decade (average of 7.3%). These include (1) a significant drop in commodity prices, namely aluminium and coal (its main exports) and (2) a deceleration in FDI in the country. We believe both the prices of these two commodities, which together account for about 40% of the country’s exports, and FDI are not expected to see a material recovery in the foreseeable future.

The Mozambican authorities have recently implemented several corrective measures like a tighter fiscal and monetary policy stance as well as a reform of the foreign exchange market to help restore macroeconomic stability following the sharp drop in commodity prices. The country is also expected to benefit from international loans like the ones recently agreed with the IMF (US$ 286 million over an 18-month period) to help bring some stability and aid from the European Union (US$ 740 million over the next five years) to support several development projects. However, we believe that short-term risks remain skewed to the downside, as persistently low commodity prices, further depreciation of the local currency and an uncertain global economic outlook could put additional pressure on economic activity in the country this year.

Meanwhile, growth is expected to improve to 7.2% in 2017 and average close to double-digits in the period 2017-20 on the back of the anticipated investments in the natural gas projects in the north of the country. Local officials reportedly expect more than US$30 billion will be invested initially in this sector to build capacity to produce 20 million tons per year of liquefied natural gas (LNG), with first exports due to start no sooner than in 2020. This is huge for a country where GDP currently stands at more than half of that amount. Mozambique will need to proceed with its reform agenda, which among should include measures that will help secure (1) more inclusive and broad based economic growth, (2) a tight control of public spending and greater fiscal transparency, (3) natural resource wealth management, (4) greater financial services inclusion and (5) an improved business environment.

10 | www.capitalmarketsinafrica.com

Since June 2014, oil prices have fallen by 70% to around $30/bbl as a result of global supply glut. Data from the Central Bank of Nigeria shows that Nigeria’s monthly exports (mainly oil) fell from an April 2014 high of $8.8 billion to $3.6 billion as at December 2015. This sharp decline in export revenue has had far reaching implications for the Nigerian economy. With the resulting current account deficit from weaker exports, Nigeria’s currency, the Naira, has come under immense pressure as dollar scarcity hit the country’s foreign exchange markets. This situation has led the central bank to adjust the exchange rate, first from NGN/USD 155 to 168, and then to 198, as well as introduce various measures to stem the pressure on the currency, including tightening monetary policy and introducing exchange controls; unfortunately, the pressure on the currency has failed to abate even as the Central Bank has maintained its policy to continue with current exchange rate regime for now. Whilst most other commodity export nations have since floated their currencies or made adjustments to accommodate the decline in global commodity prices, the move in Nigeria’s currency at 23% falls far below contemporaries and the decline in oil, its main export which accounts for 95% of foreign exchange earnings.

Enter exchange controlsThe Naira weakened 10% in 2015, although since the closure of the WDAS/RDAS window in February 2015, the currency has traded range bound between 197 and 199. Recall that the currency markets were harmonized to allow for better flexibility in the control of FX supply, thereby moderating the attrition in reserves. The CBN has consistently shown its commitment to defending the currency through various monetary policy tools; combining these with several administrative measures. In June 2015, the CBN excluded importers of 41 items, including rice and cement, from accessing foreign exchange at the official window. Whilst these measures

have so far proved successful in stabilizing the currency at the official market, the parallel market rate has seen significant pressure and deviated by as much as 50% from the official rate due to supply shortages.

The tightness in the FX market is having repercussions on local businesses as import-dependent concerns struggle. With the CBN giving priority to matured Letters of Credit (LCs) for the importation of petroleum products as well as imports of raw materials and machinery, all of which constituted about 75% of total imports as at Q3 2015, many banks have cut trade lines and are not granting new LCs. Over the last couple of months, banks have had to reduce their customers’ international payment and ATM limits, with many reducing the limits from $50,000 to as low as $5,000 annually, $1,000 monthly and $100 daily whilst a few have announced to customers that they would not be able to use naira debit cards for some international transactions.

Lately, the CBN announced the discontinuance of sales of FX to Bureau De Changes (BDCs) on several grounds such as the BDCs’ abandonment of the original objective of their establishment, use of fake documentation in rendering weekly returns to the CBN and illegal purchase of foreign exchange multiple times from the CBN amongst others. Effectively, all BDCs have been directed to source their foreign exchange from autonomous sources going forward. In as much as the CBN’s reasons behind the cut in dollar sales to BDCs are legitimate, one could argue that preservation of fast depleting foreign reserves might have been central in this move. Nigeria’s foreign reserves have declined from $43 billion in January 2014 to around $28 billion currently - representing about 6 months of import cover. The import cover buffer has been supported by a decline in imports to $4.1 billion as at December 2015 from the 2014 average of $5.6 billion.

NGN/USD Performance

Source: Bloomberg, Abokifx.com, Vetiva Research

NIGERIA’S CURRENCY CONUNDRUMAMIDST THE OIL PRICE SLUMPPabina Yinkere, Head of Research, Vetiva Capital Management

Russia

Brazil

Angola

South Africa

Ghana

Nigeria

124%

80%

62%

54%

29%

23%

% Deviation in Commodity Exporting Countries in last 18 months

Source: Bloomberg, Vetiva Research

African Economic Outlook in 2016 | 13

Running low on policy arsenals, time to adjust the rate?At what point do the policy arsenals run out and supporting the currency becomes unsustainable? It is understandable that the CBN does not want to carryout repetitive cycles of devaluation, but the challenge is that some of these measures employed over the last couple of months have hampered FX liquidity and hurt confidence in the exchange rate regime. For now, the Governor has said that the CBN will continue to prioritize FX supply

around raw material, plants and equipment imports. In the event the CBN deems an exchange rate adjustment as the next appropriate response to the currency conundrum, popular opinions indicate that an adjustment of no less than 25% would be sufficient in the near term. This will effectively peg the exchange rate at around NGN/USD 250 (around the 6-month forward rate). Nonetheless, an adjustment of the currency at this point is only a short term measure as long as there remains a fundamental shortfall in the country’s dollar receipts. This low oil price regime presents the best opportunity for Nigeria to diversify export earnings away from oil - to serve as long term measures to address currency concerns and steer growth.

Contributor’s ProfileMr. Pabina Yinkere is Head of Research at Vetiva Capital Management, a Lagos based investment bank. He possesses vast experience in investment analysis and market research. Pabina’s valuation and investment strategy supports over N40 billion (USD 200 million) assets under management and a broad clientele base of domestic and international investors.

Jan-

14Fe

b-14

Mar

-14

Apr

-14

May

14Ju

n-14

Jul-1

4Au

g-14

Sep-

14O

ct-1

4N

ov-1

4D

ec-1

4Ja

n-15

Feb-

15M

ar-1

5A

pr-1

5M

ay15

Jun-

15Ju

l-15

Aug-

15Se

p-15

Oct

-15

Nov

-15

Dec

-15

Exports (FOB) Imports (CIF)

Source: CBN, Vetiva Research

10,0009,0008,0007,0006,0005,0004,0003,0002,0001,000

0

Executive Summary: Ethiopia has been one of the major success stories in Africa over the past decade, delivering rapid growth, widespread poverty reduction, significant infrastructure improvements and general macro stability. Yet for all the long-term bullishness Ethiopia’s medium-term prospects, 2016 looks to be a difficult year in which it will struggle with adverse climactic effects of El Niño and questions about China’s commitment to the “One Belt One Road” strategy.

An African Success StoryEthiopia has been one of the great success stories Africa’s “miracle decade”: growth has averaged 10.4% in the last ten years; poverty has been reduced by over 30 percentage points; and mean monthly incomes have increased by over 25%. In the context of Africa, what’s even more impressive is that Ethiopia has achieved this while maintaining a gini coefficient (a widely accepted measure of income inequality) of just 0.336, on a par with a developed country. Growth has been both rapid and inclusive.

Ethiopia’s growth model appears well-suited to a global environment of low commodity prices. Not only is the country a net oil importer (more on the external account dynamics later) but it has never relied on a rising terms of trade in general sense as the most import source of growth. Chart 1 below shows the terms of trade index for a basket of African countries, calculated as the price of their exports divided by the price of their imports.

For mono-line commodity economies like Angola and Nigeria, the impact of rising oil prices and trade globalisation was dramatic: in 2002, it would have taken 19 barrels of crude oil import a single Sanyo flip phone; by 2008, the same (range of) phone could be imported for less than a single barrel of oil. So while all economies grew rapidly in the first decade of the 21st Century,

depending on the economy, this growth had very different foundations. An in an era where an improvement in the trade on that scale is unlikely to recur, these economies accordingly have different prospects for sustained high rates of growth.

Getting the Right Growth ModelFrom a regional perspective, the other striking feature of the chart above is that the economies of East Africa never received the same boost from the terms of trade as their peers in West or Southern Africa. If not commodity prices then, what was driving growth in this part of the continent? The simple answer is “investment” -- and nowhere is this more true than Ethiopia. While the average economy in Africa has achieved investment-to-GDP rates of just over 20% in the last 15 years, Ethiopia can boast of a ratio of 32% over this period, and almost 40% in the last couple years. In stark contrast to the rest of the continent, this is also driven to a very large extent by the State itself, which spends more on development projects than on recurring costs such as public sector wage bills and overheads.

In an era where consumption growth is unlikely to be driven by commodity prices, government balance sheets are far more stretched (limiting the scope for growth via rising wage bills/leverage) and export prices are generally under pressure, the investment-driven model offers the best hope for sustaining GDP growth. Yet this model is not opened to all African markets: it requires a coherent, long-term strategy (Ethiopia’s so-called “Growth and Transformation Plans”); a strong ability to execute (the counter-benefit of Ethiopia’s politically repressive system of government); and access to large pools of financing, assuming these are not available domestically (China is a committed partner).

Coping with El NiñoIn spite of some very important structural strengths, 2016

12 | www.capitalmarketsinafrica.com

ETHIOPIA NAVIGATING THE NEW NORMALAlan Cameron, Economist, Exotix Partner

African Economic Outlook in 2016 | 13

will not be a walk in the park for Ethiopia. First, there is the impact of El Niño. Although countries along the equator seem to have been spared the worst of the erratic weather conditions, the same cannot be said of the Horn of Africa, where food shortages are now a significant problem. According to reports from the UN’s Food and Agriculture Organisation (FAO), drought conditions have resulted in a rise in the number of food-insecure from 4.5 million in August to 8.2 million by the end of October (and possible even more today). The situation has been exacerbated by the presence of nearly 750,000 refugees and asylum seekers, which has put additional pressure on the country’s limited resources.

To the Government’s credit, it has taken a pro-active approach to managing the crisis, calling early for international aid putting in place mechanisms to replace failed local crops with imported ones. In October 2015, for example, it put out a tender for 1 million metric tons of imported wheat, which compares to the average of 420,000 tons in the five years preceding that, and 750,000 in 2011, the last time that there was a big drought in Africa. Commentary from the World Bank suggests that a further 500,000 tons will be need over the course of FY2015/16, saddling the country with an extra import bill of over US$1bn.

The difficulties resulting from adverse weather conditions show up in the economic data in two important ways. First, prices: food price inflation picked up from an average of 7.4% in FY2014/15 to 14% in July-December 2015, at one point even exceeding 16%. At a regional level, food price inflation reached over 20% in the drought-affected region of Afar and over 28% in Addis Ababa, where demand is high and markets were tight. In agriculturally-dependent country, with segmented regional markets, this will gradually spill over into non-food inflation, which hit a high of 9.7% in July 2015 and has remained elevated since.

Second, and more importantly, is the impact on the external accounts. Although data for Q4 2015 is not yet available, an additional import bill of US$1bn is very large in the context of an trade deficit of around averaging US$2.7bn per quarter and an overall balance of payments surplus that struggles to remain in the black, in spite of large-scale investment and support from abroad. Measure in months of imports, the US$1bn would amount to roughly three quarters of one month’s imports or 30% of existing stock of FX reserves. Off-setting the shock of the drought will therefore require some form of external support – the World Bank and others are apparently helping with financing – at time when there are many other global crises competing with Ethiopia’s.

Africa’s Elephant in Room: ChinaIn a broader sense, one of the big questions for Africa over the coming years is whether China will remain a committed partner, even as its own economy continues to slow. The early indications are promising: at the triennial China-Africa summit in December 2015, Chinese premier Xi Jinping pledged another US$60bn in support

to Africa, split between preferential loans and export credit lines (US$35bn), grants (US$5bn), SME financing (US$5bn) and general investment (US$15bn). This will help finance the widening trade deficit that many African countries will run with China in 2016, as the impact of lower commodity prices bite.

But there is a bigger picture concern for the Chinese. In the 18 months since June 2014, the Peoples Bank of China (PBoC) has lost nearly 663bn in FX reserves, despite running a current account surplus that exceeded US$339bn over this period. This implies that leakages through the financial account – which is officially closed, but in practice quite porous – now exceed US$1trn. Although China has plenty of ammunition to keep fighting this problem, US$3.3trn to be precise, at current depletion rates this is not the war chest that many might have assumed.

For countries like Ethiopia, which have relied on Chinese funding and expertise for a whole range of projects from the extension of Bole Airport (in Addis Ababa) to the construction of the Djibouti-Addis standard-gauge railway, the question is whether China will continue to prioritise these projects if it continues haemorrhaging reserves. Beyond any far-sighted strategic goals such as the “One Belt One Road” concept, these African projects provided a convenient outlet for the recycling of China’s external surplus, which may no longer exist in the future.

Market Implications and OutlookEthiopia’s maiden US$ eurobond has held up relatively well through the current global rout, trading from just above par (spread 426bp) in July 2015 to just under 87 (spread 696bp) at present. This compares to 104bp move in the EMBI Global spread over this period, but to a 282bps move in the spread of African sovereigns as a whole. Nevertheless, if and when it does come back to market in 2016, the global mood to be such that a greater focus its placed on vulnerabilities rather than its strengths, which will ultimately make the debt more costly.

Contributor’s ProfileAlan Cameron joined Exotix as an economist in March 2015 and he is responsible for covering a range of African and South Asian markets including Nigeria, Kenya, Egypt, Sri Lanka, Bangladesh and Vietnam. Prior to Exotix he spent 4 years working with FCMB plc, a universal bank headquartered in Lagos, providing research coverage to institutional investors based in the US and Europe. Before that, Alan worked on the Africa research desk at BMI, a Fitch Group company based in London. Alan holds a Masters degree in international economics from Johns Hopkins University and an undergraduate degree from the University of Paris IV (Sorbonne).

14 | www.capitalmarketsinafrica.com

Global economic growth should lift over the next two years as activity in major developed countries grinds higher while the severe deceleration experienced by several major emerging countries fades. However, this improvement is unlikely to provide a meaningful boost to those emerging economies that are dependent on exporting commodities and are highly indebted like Brazil, Russia and South Africa. This is even more so the case given the uncertainty surrounding China’s growth prospects, at a time when policy makers remain focused on rebalancing the economy away from a focus on fixed investment in support of manufactured exports, towards a more consumption-based, service oriented model which is likely to be less resource intensive.

While the steady improvement in US economic activity is good news for the global economy, it gave the Fed scope to begin raising its policy rate in December. This was the first hike in more than a decade. We expect more rate hikes from the Fed over the next two years. Higher dollar funding costs will pose a challenge to indebted governments, households and corporates the world over.

Against this global backdrop, the South African growth outlook has deteriorated further over the last few weeks. Significant policy uncertainty following the recent changes in the Ministry of Finance, negative rating actions from credit rating agencies, slowing foreign capital inflows, in part related to the latest asset sell-off in EMs and in particular China and the growing risk of an even more aggressive pro-cyclical monetary policy response are to blame. In addition, ongoing structural constraints will hamper South Africa’s ability to grow employment, increase private sector investment and reap the full benefits of a weak exchange rate and somewhat stronger global growth in advanced economies. As a result, growth in household, corporate and government income will remain limited, while rising inflation and higher interest rates will erode real purchasing power. We expect the South African economy to grow by 0.5% this year rising to 1.2% in 2017.

After averaging 4.6% in 2015 inflation will rise over the next two years. It is expected it to be above the target band in the second half of 2016 and the first half of 2017. The potential for meaningful drought-induced food price increases, coupled with sharp electricity price tariff hikes and more pronounced currency pass-through pose upside risk to this relatively negative inflation projection.

The Reserve Bank (SARB) delivered a rate hike of 50 basis points at it January meeting. Despite the weak growth backdrop the SARB is likely to continue to raise

interest rates. Given the deterioration in South Africa’s sovereign credibility it doesn’t have a choice. We will need higher interest rates to entice foreign investors and to compensate them for the additional country risk they face. That we are now perceived as a riskier investment destination is reflected in the sharp increase in government borrowing costs since early December. Failure by the SARB to react to this with higher interest rates will threaten even more rand weakness and higher inflation. Apart from a significantly weaker exchange rate and inflation outlook, recent communication from the SARB suggests a lower tolerance level for above-target inflation outcomes and elevated inflation expectations. We expect rates to be increased by an additional 100 basis points over the next 18 months with the repo rate peaking at 7.75%.

The downside risk to this downbeat central expectation is high. There are several events and developments that could result in even slower growth, higher inflation and higher interest rates. Domestically these include a severe drought, a February Budget that fails to restore credibility and the potential for protracted labour unrest should the wage negotiations in the platinum sector which are scheduled for around mid-year not be concluded amicably. On the global front how aggressive (or not) the Fed hikes interest rates will be important to monitor, as will be growth developments in China and related to that dynamics in commodity markets.

This classic stag-flationary environment typically constrains asset class returns. From a valuation perspective local equities look somewhat expensive in the short term although they retain investment merit in the long term. Rand hedges, companies that derive a large proportion of revenue and profits in hard currency, will continue to play an important role in any equity portfolio. Bonds appear to represent fair value with the significant rise in yields and should produce inflation beating returns in the longer term.

Finally, the prioritisation of economic growth that leads to an accelerated implementation of much delayed structural change would represent a positive surprise. In such a case the rand would in all likelihood respond favourably, with inflation and interest rates turning out lower and economic growth higher than we currently forecast. Nevertheless, there has been little evidence of this over the last half decade. In sum, expect even lower growth and higher inflation. It’s also called stagflation.

SOUTH AFRICA OUTLOOK 2016:STAGFLATION IS THE MOSTLIKELY OUTCOMESizwe Nxedlana, Chief Economist First National Bank, South Africa

African Economic Outlook in 2016 | 15

NIGERIA’S ECONOMIC OUTLOOK& GROWTH PROSPECTS IN 2016Ayodeji Ebo, Head, Investment Research, Afrinvest Securities Limited

The year 2015 began with an overwhelming apprehension about the survival of Nigeria as a nation. Devastated by insurgency and militancy in the North-Eastern and Southern regions, plunging oil prices in the global space and the general election related political anxiety, the economy was brought to a state of ‘’Suspended Animation” in the first half of the year. However, gains from a peaceful and successful conduct of the general elections were off-set by poor monetary policy responses, delayed fiscal policy pronouncements and relentless decline in oil prices. The weakness in the system was reflected in the pace of GDP growth which slowed from 6.22% in 2014 to 3.96%, 2.35% and 2.84% in Q1, Q2 and Q3:2015 respectively, currency volatility, higher inflation rate and a poor equities market performance of -17.4% Y-o-Y.

With oil prices at record low, 2015 was indeed a challenging one for the fiscal authorities given the mono-product revenue structure. The fundamental structure of the economy and revenue allocation to states was impeded as the country experienced the sharpest drop in revenue due to lower oil prices. A review of government revenue indicated that oil revenue contracted to N2.6tr in Q3:2015 relative to N5.4bn in prior period. With historical revenue structure mainly skewed to oil, we are of the view that fiscal crisis poses a major threat to social stability in 2016. Despite the massive bailout handed by the Federal Government (FG) to states governments due to lower federal allocations and poor capacity to generate internal revenues in 2015, another bailout seems imminent the abilities of states to generate revenue remain unchanged while overheads which ratcheted up during the last oil boom are not brought down. A further deterioration in government revenue and the balance sheet of the States may trigger civil unrest.

In response to the faltering economic performance, the FG proposed an expansionary N6.1tn budget for 2016 (20.2% larger than 2015 budget) with focus on investment in key infrastructure and social welfare spending. An optimistic drive to increase non-oil revenue (projected at N1.5tn vs. N606.0bn as at September 2015), through enhanced tax proceeds and revenue from independent sources is noteworthy while 30.0% capital spending is planned to be deficit financed. Although the fiscal spending plan is necessitated, we believe the expansionary framework appears ambitious given that Independent revenue sources remains an unknown item that is yet to be proven while VAT and other taxes may be constrained this year due to economic setbacks. Nevertheless, any shortfall that may arise from the seemingly ambitious oil benchmark, can be off-set by devaluation.

Domestic Macroeconomic OutlookSub-Optimal Growth Momentum to Persist: As experienced in 2015, adjustment to lower crude oil prices will remain a crucial

theme for the domestic economy in 2016. In estimating the impact of lower commodity prices on the performance of commodity dependent economies, the IMF pointed out in October 2015, that weak commodity prices may subtract an average of 2.5% from GDP growth of energy exporters between 2015 and 2017. Remarkably, a review of the performance of the Nigerian economy in 2015 indicated that the predictions of the IMF analysis has held true.

In projecting the performance of the Nigerian economy in 2016, we analyse the demand composition of the Nigerian GDP using available data from the NBS as at Q2:2015 as shown with breakdown in the chart below. From this demand perspective, the impact of lower oil prices will further drag government revenue, consumption spending, net export and the overall pace of output growth in 2016. Based on the fact that crude oil export accounts for 90.0% of the country’s total export, we believe stronger consumer spending and net export in Nigeria remain linked to higher oil prices.

As noted earlier, fiscal spending which is proposed to total N6.1tn, with 30.0% or N1.8tn expected to go into capital expenditure, it appears government spending which accounted for 6.0% of GDP may be only driver of growth in 2016. The downside to the budget proposal however remains the likelihood of further decline in oil prices which is benchmarked at US$38.0/b together with the somewhat optimistic non-oil revenue given the adverse effect of macroeconomic pressure on corporate earnings and taxable income. Expectation for increased borrowing – the Minister of Finance recently announced additional US$4.0bn borrowing from multilateral sources - and the gains from TSA implementation are however anticipated to cushion the downside to revenue projection.

Chart 1: Crude Oil Prices Trend (1989 -2016f)Source: Bloomberg, Afrinvest Research

+ + + =

Chart 2: GDP Composition by Expenditure as at Q2: 2015Source: NBS, Afrinvest Research

16 | www.capitalmarketsinafrica.com

In light of current realities, Afrinvest Research estimates GDP growth at 3.5% in 2016 as against 3.0% in 2015. To grease the wheel of output growth, we recommend policy harmonization between the fiscal and monetary team as well as the use of forward guidance to reduce uncertainty in the domestic investment environment.

Inflationary Pressures will persist: We expect headline inflation to remain under pressure in 2016 albeit moderately as further decline in oil prices and the associated effect on external reserves pressure exchange rate. The CBN’s insistence on retaining its administrative measure on foreign exchange transactions and the associated pressures on parallel market rates will continue to induce cost push inflation. However, inflation rate may not rise as fast as observed in 2015 due to base factors. Hence headline inflation may settle at a Y-o-Y average of 9.6% in 2016.

Currency Peg Adjustment Imminent: While we acknowledge the significant challenges that confronted the CBN during 2015 and presently, we observe that some of the policies are characterized by major inconsistencies, conflicts and policy reversals. Against an objective to drive real sector development by the CBN, monetary policy in 2015 was largely driven by policy responses to developments in the global oil market and its impact on the exchange rate. In a bid to conserve external reserves and protect the value of the naira, the exchange rate was tightly held by the apex bank in 2015. Relative to huge currency depreciation across emerging and frontier markets– Brazil (-35.1%), South Africa (-25.2%), Kenya (-11.4%), and Ghana (-15.5%)– the naira depreciated by only 9.0% at the official market in 2015 due to administrative measures put in place by the CBN. However, parallel market rate depreciated 28.2% from N191.00/US$1.00 in December 2014 to close the year at N266.0/US$1.00. Notwithstanding the easy monetary policy and TSA implementation, the restrictive FX policy and poor policy response by the monetary authority isolated a significant amount of capital flow into the country as concerns surrounding the appropriate pricing of the naira lingered.

Nigeria traditionally commands very strong autonomous foreign exchange inflows traceable to oil receipt from IOCs, remittances, and capital importation (loans, portfolio and direct investment) which cushions the FX liquidity position of banks

and support the country’s balance of payments. The series of restrictive foreign exchange policies (including ban on dollar cash deposits which was recently reversed) and failure to take a decisive step on repricing the naira have led to a drop in autonomous FX inflows in 2015; down 36.9% Y-o-Y compared to a 26.6% drop in CBN FX inflows.

With Nigeria being the largest recipient of remittances in Africa and 6th largest in the world, an adoption of a more flexible exchange rate mechanism alongside structural reforms to attract foreign investment could boost autonomous FX supply into the Nigerian market as inflows from remittances would be crucial following the simultaneous reduction in capital importation and oil related inflows.

Monetary Policy Rate - Hawkish or Dovish? As against a hawkish stance in late 2014 where MPR was increased from 12.0% to 13.0% and left unchanged till November 2015, the MPC reverted to a dovish stance in its last sitting in 2015, slashing MPR by 2.0% to 11.0% and CRR from 25.0% to 20.0%. Equally in its first sitting in 2016, its maintained status quo notwithstanding the apparent impediment in the economy. The MPC’s argument stemmed from the view that reducing MPR together with increased system liquidity will spur real sector lending as banks would expand their loan books to facilitate real sector investment. However, we believe this position was counterproductive given our weakening macroeconomic horizon, higher interest rate environment in the US and further decline in oil prices.

In the interim, we believe the MPC might consider other measures to spur real sector growth and deflect the likelihood of the economy slipping into a recession while harmonizing its policy framework with that of the fiscal team. The persistent uptick in headline inflation rate as noted earlier suggests that further reduction in MPR will shrink real rate of interest in the economy. Thus, MPR may be increased by 1.0% to 12.0% in 2016.

Chart 3: Headline Inflation in Nigerian from 2003 to 2015 (+ 2016 Forecast)Source: NBS, CBN, Afrinvest Research

Chart 3: FX Rate, External Reserves and Crude Oil Price (1985 to 2015+ Forecast)Source: CBN, Bloomberg, Afrinvest Research

African Economic Outlook in 2016 | 17

Ghana’s 3-year fiscal adjustment program currently underway with technical and Extended Credit Facility support from the IMF is aimed at rebuilding the country’s fundamentals following a sharp deterioration induced by election-related excesses and external imbalance.

Policy slippages and associated extensive central bank financing in the run up to the 2012 elections have significantly undermined Ghana’s fundamentals with double digit fiscal deficit for three consecutive years. The shock of an over-heated economy was transmitted through the balance of payment as the wider current account deficit fuelled currency instability with a pass-through to inflation rate. The continued decline in Ghana’s key commodity prices (cocoa, gold and crude oil) coupled with acute power supply shortages also dented investor and consumer confidence in 2015.

Main Risks to Rebuilding Ghana’s Fundamentals:As Ghana commenced the rebuilding process aimed at restoring macroeconomic stability and investor confidence, fiscal adjustment over three years under the IMF program (since Apr-2015) remains the cornerstone upon which sustainably strong fundamentals would be built.

Continuing with the front-loaded approach to fiscal adjustment, the government of Ghana commenced 2016 with policy measures to mitigate the threats from lower commodity prices and tighter global financial markets. Given the negative outlook for commodity prices and the anticipated shift in US monetary policy stance in 2016 (and beyond), Ghana (and Africa in general) is confronted with a new dispensation which requires policy calibration consistent with reality. The downward pressure on commodity prices poses significant risks to Ghana’s fiscal adjustments through the shocks to projected revenues from commodity exports while the tight financial markets would limit the scope for external and domestic borrowing. A major condition under the IMF program is the elimination of central bank financing for government deficit in 2016 and beyond, emphasizing the need for government to increase tax revenue (currently around 16% of GDP) to sustain fiscal operations.

The Uncertainty of Lower Crude Oil Price:From a fiscal perspective, the lower crude oil price (with a negative outlook) poses a risk to government’s projected revenue for the 2016 fiscal year. The 2016 budget presented by Ghana’s finance minister in Nov-2015 anticipates $502.10 million as total petroleum revenue using a benchmark price of $53.05pb. However, with average daily price of Brent hovering around $32pb at the start of Feb-2016, the threats to government’s anticipated revenue from crude oil is quite elevated and would require a policy response to mitigate the risks to Ghana’s fundamentals. There appears to be limited scope for a sustainable recovery in crude oil price in the near term as the anticipated return of Iran’s supply would sustain the

downward pressure. Furthermore, OPEC’s new strategy of defending market share rather than price has dampened the outlook for a near term recovery in crude oil price while co-operation with non-OPEC producers for production cuts appears doubtful.

The anticipated rebound in Ghana’s GDP growth critically hinges on increased production of oil and gas from the oil fields currently being developed (mainly the Tweneboa-Enyenra-Ntomme [TEN] and Sankofa) from Mid-2016 and beyond. Although the collapse in crude oil price poses little threat to oil production from the wells already drilled, continuous exploration for new fields could be hampered by threats to the viability of additional investments at the prevailing price. According to Ghana’s Energy Commission (2015 energy outlook for Ghana), viability of the TEN fields was based on a projected price of $80pb, indicating elevated risks to production at full capacity if crude oil price continues its downward trend. Ultimately, the downward pressure on crude oil price poses a major threat to a strong recovery in real GDP growth on the back of hydrocarbon production.

From a balance of payments (BOP) perspective however, the decline in crude oil price bodes well for rebuilding gross reserves as a lower import bill for crude oil reduces the pressure on foreign currency reserves. Consequently, the reduced pressure on foreign currency reserves should provide a cushion for the Ghana cedi against elevated depreciation pressures in 2016 and beyond. Latest data from the Bank of Ghana revealed that total expenditure on crude oil & gas import in 2015 ($2.05 billion) was $1.64 billion less than the level for 2014. This is mainly a direct consequence of the downward trend in Brent price which closed 2015 at $36.71pb, corresponding to a 44% annual loss. Ultimately, the decline in crude oil price has resulted in a saving of $1.64 billion in 2015 for oil imports, easing the pressure on foreign currency reserves. The completion of Ghana’s gas processing plant at Atuabo (in the Western region) and the anticipated uptake of gas from the TEN and Sankofa oil fields from 2017 is also expected to further reduce the gas import bill. Ghana’s Energy Commission expects the completion of all the new oil & gas fields to add between 300 and 500 million standard cubic feet of gas per day by the year 2020 to support sustainable gas-powered electricity supply. Ghana’s oil refinery, the Tema Oil Refinery (TOR), is expected to resume operations in Q1-2016 following the completion of works on the Residue Fluid Catalytic Cracking (RFCC) plant. With refinery capacity of 45,000 barrels per day, TOR could potentially supply at least 50% of Ghana’s daily demand for refined petroleum products, further easing the petroleum import bill and enabling the rebuilding of gross reserves.

A robust reserve of foreign currencies is necessary to restore investor confidence and anchor exchange rate expectations which would support the cedi and engineer macroeconomic

REBUILDING GHANA’S ECONOMICFUNDAMENTALS: PROSPECTS ANDTHREATS IN 2016 AND BEYONDCourage Kingsley Martey, (Senior Economic Analyst, Databank Research)

18 | www.capitalmarketsinafrica.com

stability in 2016 and beyond. The rebuilding process already commenced in 2015 as gross reserves increased by ~7.7% y/y to close 2015 at $5.88 billion. The nominal increase in gross reserves in 2015 corresponds to 3.5 months of import cover compared to the 3.8 months equivalent in 2014, indicating that a faster growth rate in foreign currency reserves would be required to support the rising total import bill. It is therefore expected that as real GDP growth rebounds on the back of industrial and agricultural expansion, export revenue should be boosted by increased productivity and value addition to support foreign exchange inflows beyond 2016.

Restoring Debt Sustainability:Rebuilding Ghana’s economic fundamentals cannot be achieved without restoring fiscal and debt sustainability, admittedly, a crucial focus of the ongoing 3-year IMF program. Ghana’s public debt has recorded sustained increase over the past few years owing mainly to an increase in the real debt stock as well as vulnerability to the cedi’s depreciation. The total public debt increased by 16.7% during the first 9-months of 2015 to GH¢92.2 billion (69.1% of GDP), driven mainly by a 22.7% surge in the external debt component to GH¢54.5 billion. Apart from the increase in the debt stock due to higher borrowing, the surge in the external debt (relative to the domestic debt) also reveals the adverse impact of the cedi’s depreciation on Ghana’s debt sustainability. Consequently, a stable exchange rate in 2016 and beyond is necessary to restore debt sustainability and

rebuild Ghana’s economic fundamentals.

Another threat to restoring debt sustainability is the frequent and large volume of maturing short term debts which continue to strain government’s liquidity position, resulting in a high rollover risk. The government of Ghana’s decision to restructure the debt portfolio by issuing longer-dated debts to gradually reduce the debt service obligation on the shorter-end of the debt portfolio has started yielding some results. The yields for short term debts (Treasury bills) have assumed a downward trend since Nov-2015 following the issue of a 5-year bond (GH¢516.53 million) and a $1 billion Eurobond to ease the refinancing burden. Sustainability of the downward trend in yields for short term Treasury securities is however threatened by the elevated inflationary expectations and possible recurrence of depreciation pressures in Q1-2016 as the real returns of investors would be adversely affected. Consequently, yields for the 91-day and 182-day Treasury bills appear to have levelled off marginally above 22% and 24% respectively as the low investor appetite threatens the sustainability of the government’s quest to reduce interest obligations. Without a sustained decline in inflation rate (which stood at 17.7% in Dec-2015) and exchange rate stability, restoring debt sustainability through lower interest cost would be undermined. The prospect of a strong rebound in GDP growth after 2016 should however support debt sustainability, ensuring a gradual decline in the debt-to-GDP ratio over the medium.

African Economic Outlook in 2016 | 19

AFRICAN CAPITAL MARKET UPDATES

Compiled by Capital Markets in Africa

Country Name Index Name Index at 29-Feb 1-month % YTD % 1-Year % 1-Year Low 1-Year High 30 Days Volatility %

Botswana BSE DCI 10,233 -1.98 -3.48 6.67 9,590 11,097 3.061BRVM IC Comp 303 4.56 -0.32 16.21 256 309 10.343Egypt EGX 30 6,147 2.57 -12.26 -34.14 5,526 9,820 30.101Ghana GSE ALSI 1,972 -1.59 -1.14 -9.45 1,950 2,390 4.698Kenya FTSE NSE15 142 3.82 -2.52 -19.16 136 176 10.387Malawi MSE ALSI 14,264 -2.02 -2.05 -4.69 14,278 16,142 3.039Mauritius SEMDEX 1,811 -1.75 -0.02 -10.30 1,790 2,025 8.578Morocco MORALSI 8,908 0.11 -0.19 -14.84 8,790 10,548 7.541Namibia Local 877 3.13 1.35 -25.25 767 1,214 40.313Nigeria NIG ALSI 24,571 2.74 -14.22 -18.38 22,331 35,843 20.528Rwanda RSEASI 131 -0.08 -0.08 -4.97 131 162 0.130South Africa JSE ALSI 49,415 0.56 -2.52 -7.37 45,976 55,355 25.028Swaziland SSX ALSI 335 2.22 2.40 11.82 300 335 3.445Tanzania DAR ALSI 2,377 3.74 1.85 -12.01 2,218 5,005 319.661Tunisia TUNIS 5,288 -2.36 4.88 -2.83 4,812 5,781 10.588Uganda USE ALSI 1,749 -0.59 -0.82 -15.34 1,712 2,095 11.954Zambia LuSE ALSI 5,575 0.39 -2.78 -9.35 5,549 6,150 3.585Zimbabwe IDX (USD) 99.50 -3.44 -13.37 -40.48 99 167 8.341

Country Name Index Name Index at 29-Feb 1-month % YTD % 1-Year % 1-Year Low 1-Year High 30 Days Volatility %