Embed Size (px)

Citation preview

»AES CorporationSanford C. Bernstein Strategic Decisions Conference 2007June 1, 2007 Andres Gluski, AES Chief Operating Officer

AES Corporation 2

» Safe Harbor Disclosure

Certain statements in the following presentation regarding AES’s business operations may constitute “forward looking statements.” Such forward-looking statements include, but are not limited to, those related to future earnings, growth and financial and operating performance. Forward-looking statements are not intended to be a guarantee of future results, but instead constitute AES’s current expectations based on reasonable assumptions. Forecasted financial information is based on certain material assumptions. These assumptions include, but are not limited to, continued normal or better levels of operating performance and electricity demand at our distribution companies and operational performance at our generation businesses consistent with historical levels, as well as achievements of planned productivity improvements and incremental growth from investments at investment levels and rates of return consistent with prior experience. For additional assumptions see the Appendix to this presentation. Actual results could differ materially from those projected in our forward-looking statements due to risks, uncertainties and other factors. Important factors that could affect actual results are discussed in AES’s filings with the Securities and Exchange Commission including but not limited to the risks discussed under Item 1A “Risk Factors” in the Company’s Annual Report on Form 10-K for the year ended December 31, 2006, as well as our other SEC filings. AES undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

AES Corporation 3

» AES Overview

AES has a strong position in the industry through portfolio diversification

› Geographic diversity

› Fuel Diversity

› Technology diversity

› Business line diversity: generation and distribution

› Growing portfolio of businesses in adjacent markets

AES Corporation 4

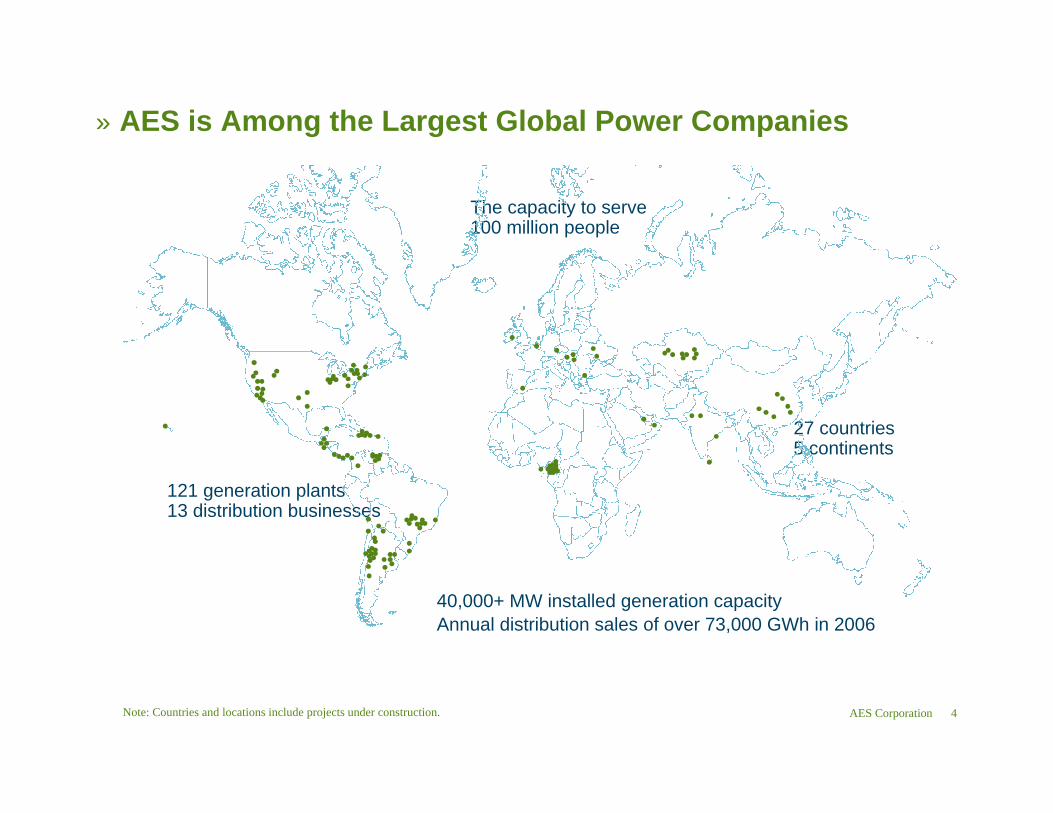

» AES is Among the Largest Global Power Companies

Note: Countries and locations include projects under construction.

The capacity to serve 100 million people

121 generation plants13 distribution businesses

40,000+ MW installed generation capacityAnnual distribution sales of over 73,000 GWh in 2006

27 countries5 continents

AES Corporation 5

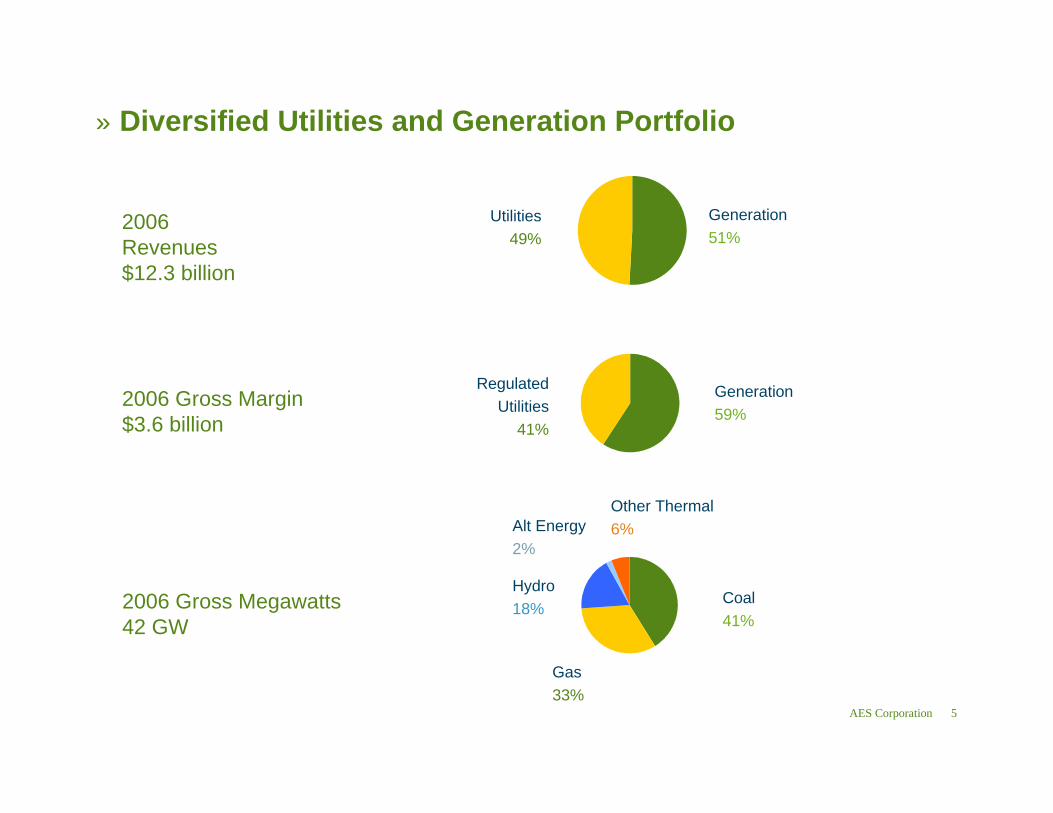

» Diversified Utilities and Generation Portfolio

Generation51%

2006 Revenues$12.3 billion

Utilities49%

Generation59%

2006 Gross Margin$3.6 billion

RegulatedUtilities

41%

2006 Gross Megawatts42 GW

Coal41%

Gas33%

Hydro18%

Alt Energy2%

Other Thermal6%

AES Corporation 6

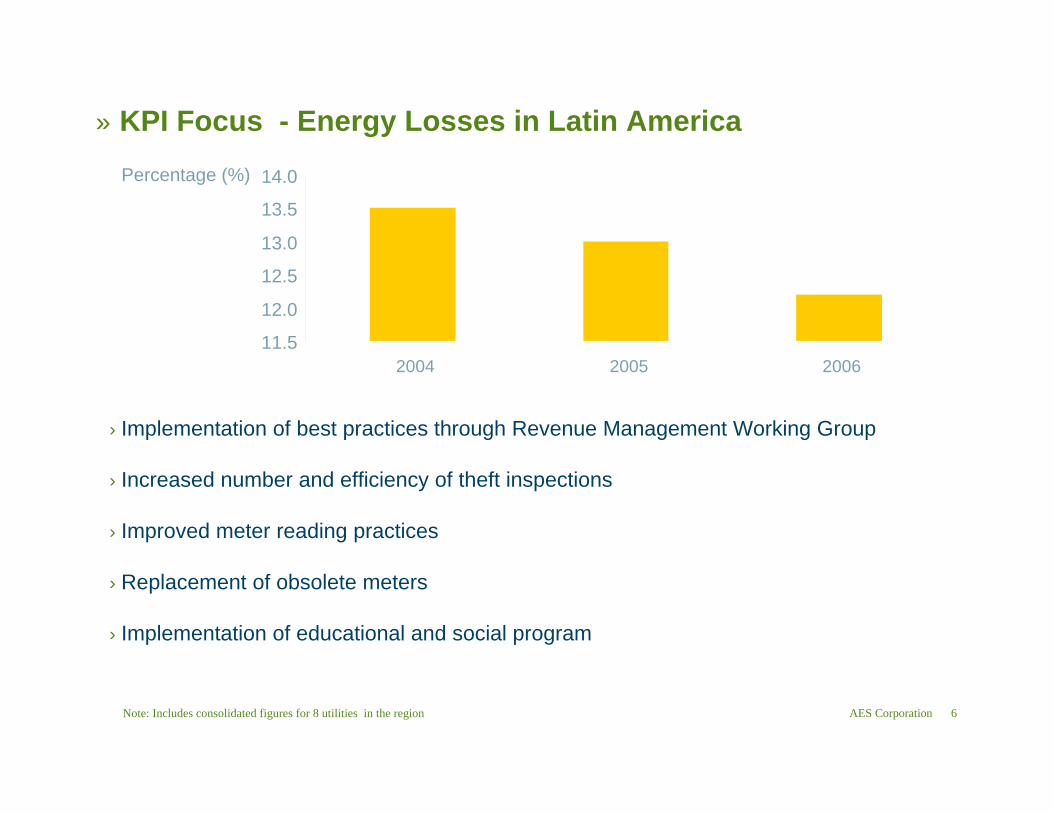

» KPI Focus - Energy Losses in Latin America

Note: Includes consolidated figures for 8 utilities in the region

Percentage (%)

› Implementation of best practices through Revenue Management Working Group

› Increased number and efficiency of theft inspections

› Improved meter reading practices

› Replacement of obsolete meters

› Implementation of educational and social program

11.5

12.0

12.5

13.0

13.5

14.0

2004 2005 2006

AES Corporation 7

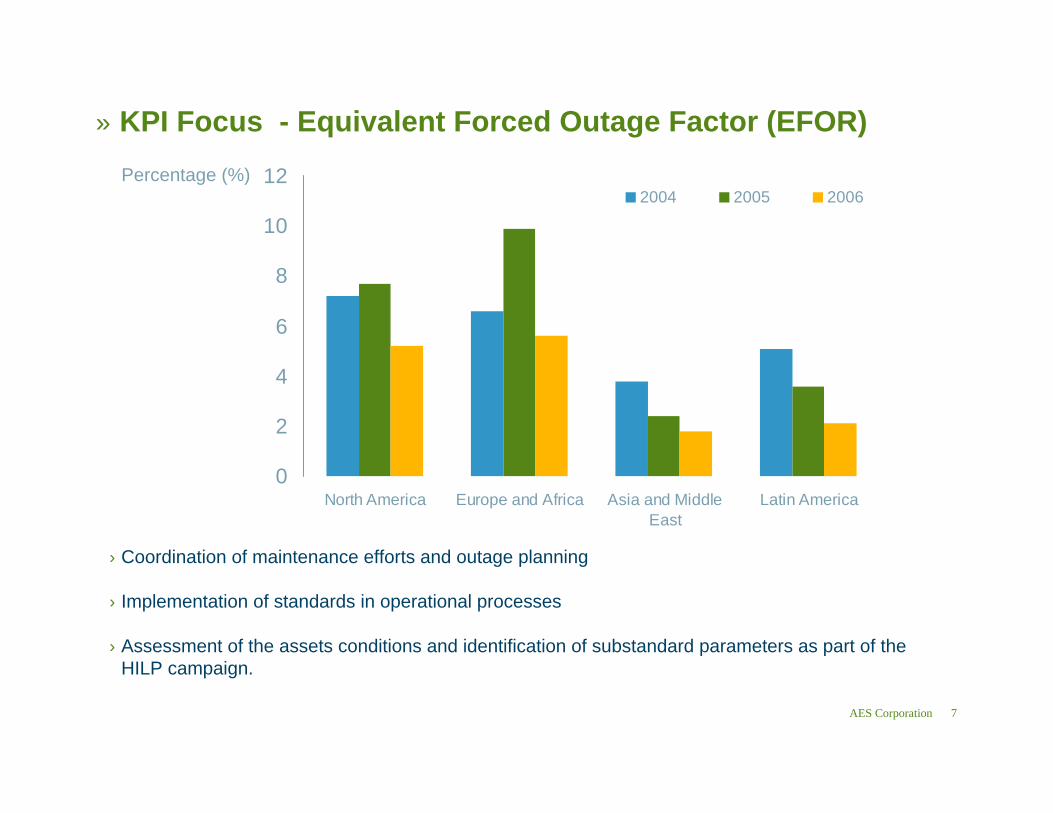

» KPI Focus - Equivalent Forced Outage Factor (EFOR)

0

2

4

6

8

10

12

North America Europe and Africa Asia and MiddleEast

Latin America

2004 2005 2006Percentage (%)

› Coordination of maintenance efforts and outage planning

› Implementation of standards in operational processes

› Assessment of the assets conditions and identification of substandard parameters as part of the HILP campaign.

AES Corporation 8

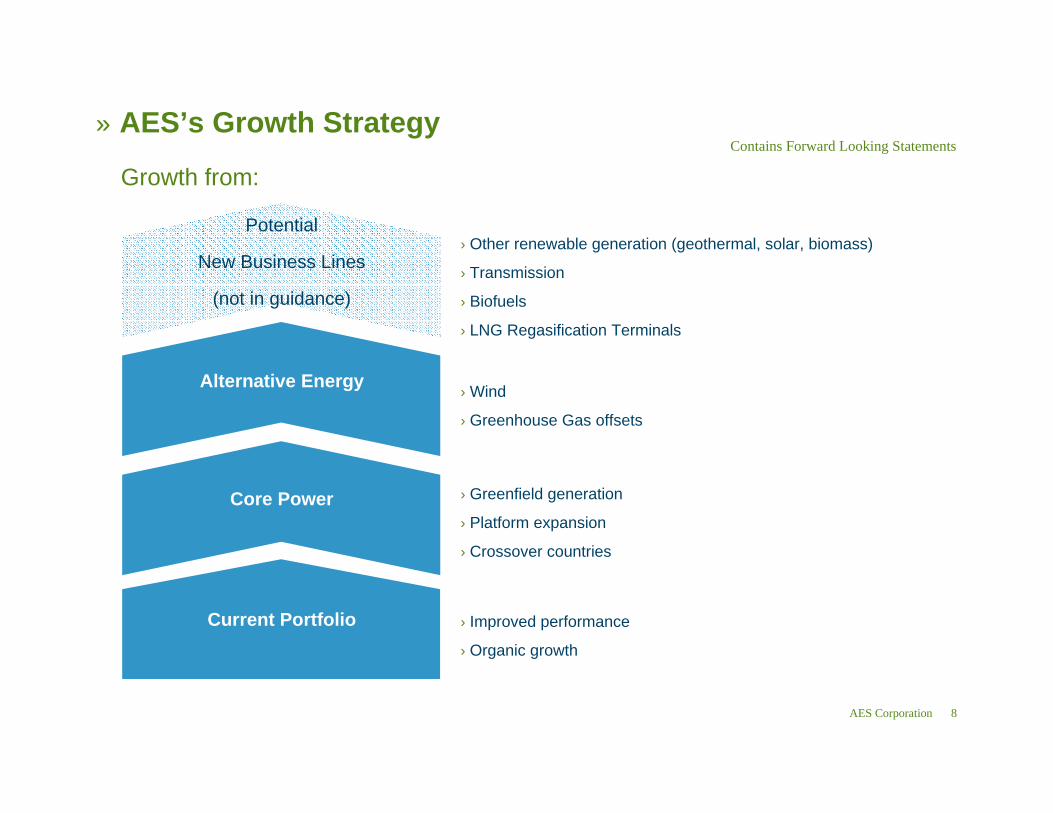

Potential

New Business Lines

(not in guidance)

» AES’s Growth Strategy

Growth from:

Current Portfolio

Core Power

Alternative Energy

› Improved performance

› Organic growth

› Greenfield generation

› Platform expansion

› Crossover countries

› Wind

› Greenhouse Gas offsets

› Other renewable generation (geothermal, solar, biomass)

› Transmission

› Biofuels

› LNG Regasification Terminals

Contains Forward Looking Statements

AES Corporation 9

» A World of Opportunities

2 Billion Tons(3)

(2008-2012)

100,000 MW(2)

500-700 GW(1)

Global Potential within next 5 years

26 million tons / year

2,100 MW

6,500 MW(4)

AES Growth Assumptions in 2011 Guidance

Greenhouse Gas Offsets

Wind

Power

(1) CERA and IEA forecasts (2006)(2) Emerging Energy Research (March 2007)(3) World Bank (2007)(4) Includes Greenfield and M&A

Contains Forward Looking Statements

AES Corporation 10

» Development Pipeline

› Under construction projects:

– Maritza East 670 MW coal fired plant in Bulgaria– Guacolda III 152 MW coal fired plant at Gener (Chile)– Ventanas III 267 MW coal fired plant at Gener (Chile)– Changuinola 223 MW hydro plant in Panama– Buffalo Gap II 233 MW wind farm in Texas– Amman East (1) 370 MW gas-fired plant in Jordan

› In 2006 commercial operations commenced at:

– Cartagena 1,200 MW gas fired plant in Spain– Buffalo Gap 1 121 MW wind farm in Texas– Los Vientos 125 MW diesel/gas peaker in Chile

(January 2007)

LocationMWProject

Qatar2,600 Ras Laffan

Indonesia1,200 Musi Rawas

India1,200 Chattisgath

Turkey400ICTAS Energy India1,200 OPGC

Kazakhstan1,500 Kazakhstan

N Ireland400 Kilroot

Puerto Rico500 Puerto Rico 2

US600 Shady Pt 2

El Salvador200 Fonseca

Chile520 Alto Maipo

Chile532 Angamos

Panama213 Changuinola 2

Vietnam1,200 Mong Duong

› Current Development Pipeline has over 20 GW of specifically identified advanced stage opportunities representing over 40 projects in 20 countries

› AES core strength in project development is bringing pipeline cycle to completion

› Selected projects beyond early stage development:

(1) Amman East commenced construction in April 2007

Contains Forward Looking Statements

AES Corporation 11

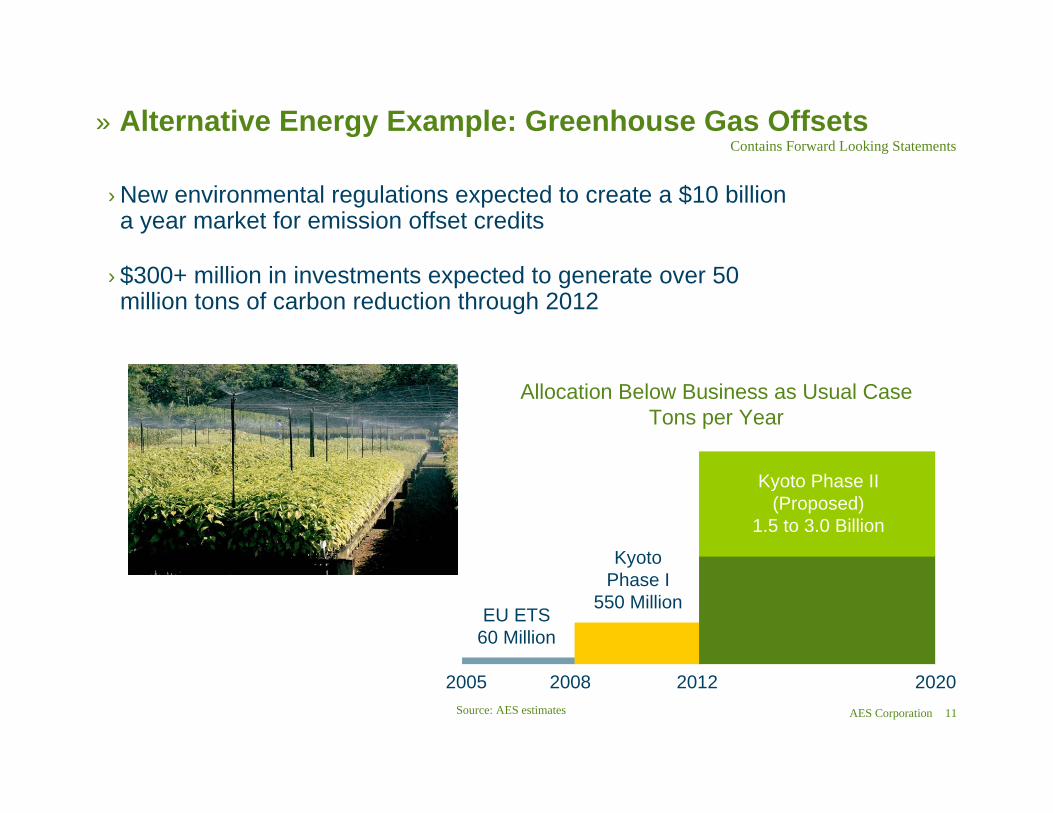

» Alternative Energy Example: Greenhouse Gas Offsets

› New environmental regulations expected to create a $10 billion a year market for emission offset credits

› $300+ million in investments expected to generate over 50 million tons of carbon reduction through 2012

2005 2008 2012 2020

Allocation Below Business as Usual CaseTons per Year

EU ETS60 Million

KyotoPhase I

550 Million

Kyoto Phase II(Proposed)

1.5 to 3.0 Billion

Source: AES estimates

Contains Forward Looking Statements

AES Corporation 12

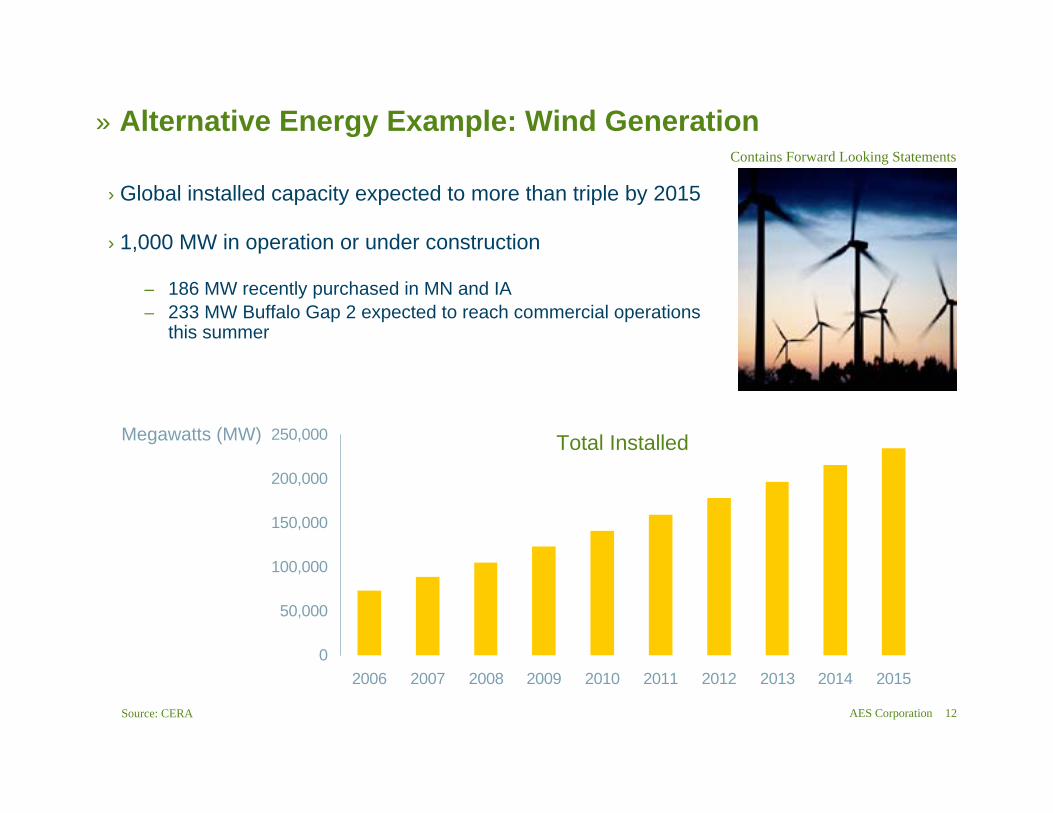

» Alternative Energy Example: Wind Generation

› Global installed capacity expected to more than triple by 2015

› 1,000 MW in operation or under construction

– 186 MW recently purchased in MN and IA– 233 MW Buffalo Gap 2 expected to reach commercial operations

this summer

Kyoto Phase II(Proposed)

1.5 to 3.0 Billion

Contains Forward Looking Statements

0

50,000

100,000

150,000

200,000

250,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Total Installed

Source: CERA

Megawatts (MW)

AES Corporation 13

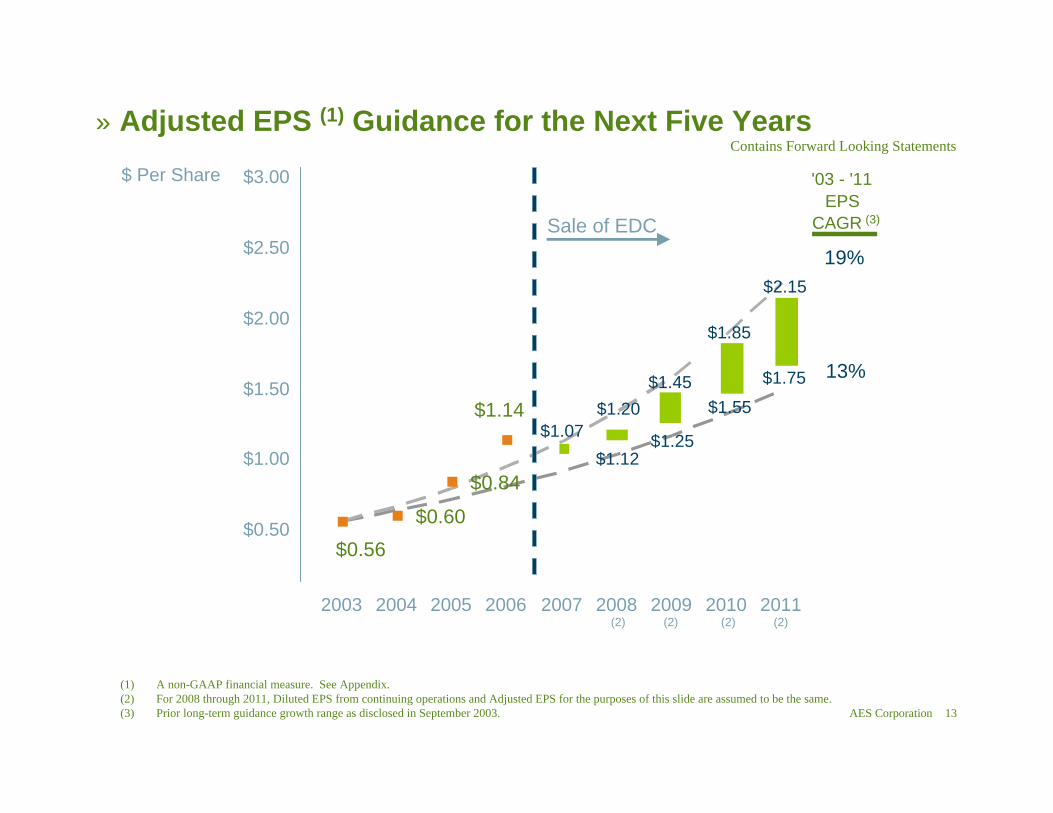

(1) A non-GAAP financial measure. See Appendix.(2) For 2008 through 2011, Diluted EPS from continuing operations and Adjusted EPS for the purposes of this slide are assumed to be the same. (3) Prior long-term guidance growth range as disclosed in September 2003.

» Adjusted EPS (1) Guidance for the Next Five YearsContains Forward Looking Statements

$1.12$1.25

$1.55

$1.75

$2.15

$1.85

$1.45

$1.07$1.20

$0.60

$0.84

$1.14

$0.56$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

2004 2005 2006 2007 2008 2009 2010 2011

13%

19%

'03 - '11 EPS

CAGR (3)Sale of EDC

2003(2)(2) (2)(2)

$ Per Share

AES Corporation 14

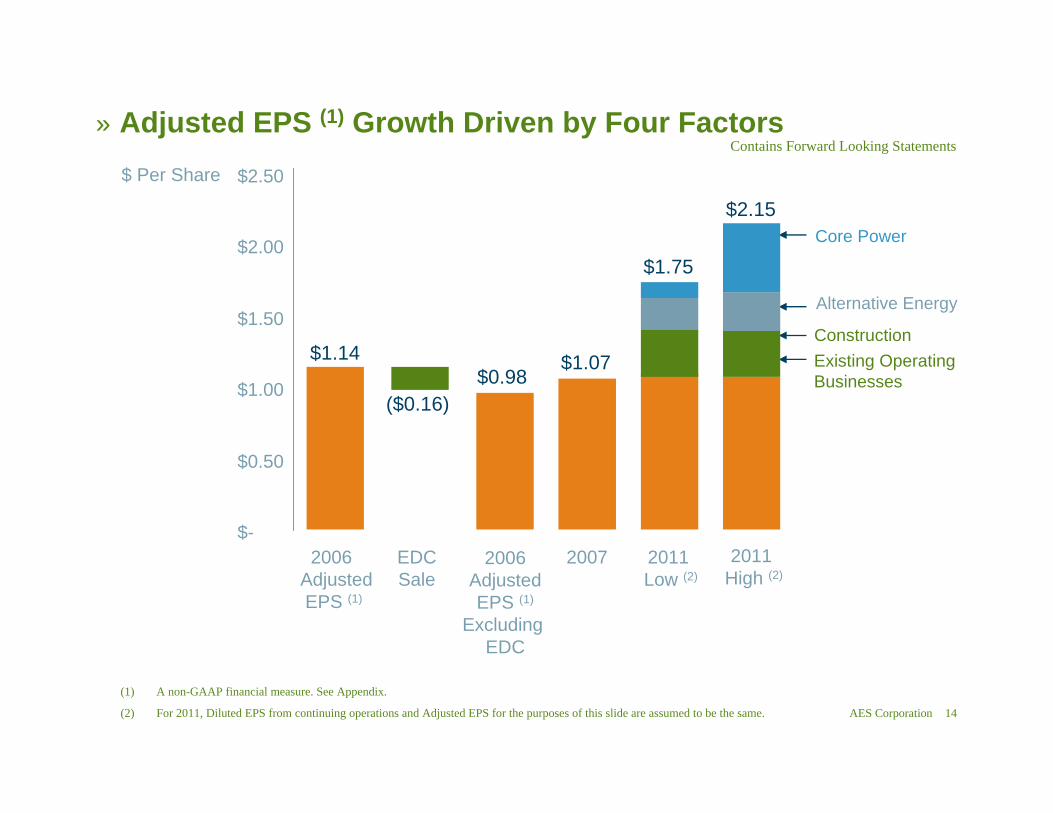

(1) A non-GAAP financial measure. See Appendix.

(2) For 2011, Diluted EPS from continuing operations and Adjusted EPS for the purposes of this slide are assumed to be the same.

» Adjusted EPS (1) Growth Driven by Four Factors

($0.16)

$1.14$0.98

$1.07

$1.75

$2.15

$-

$0.50

$1.00

$1.50

$2.00

$2.50

2006 AdjustedEPS (1)

EDCSale

2006AdjustedEPS (1)

Excluding EDC

2007 2011 Low (2)

2011 High (2)

Existing Operating Businesses

Alternative Energy

Core Power

Construction

Contains Forward Looking Statements

$ Per Share

AES Corporation 15

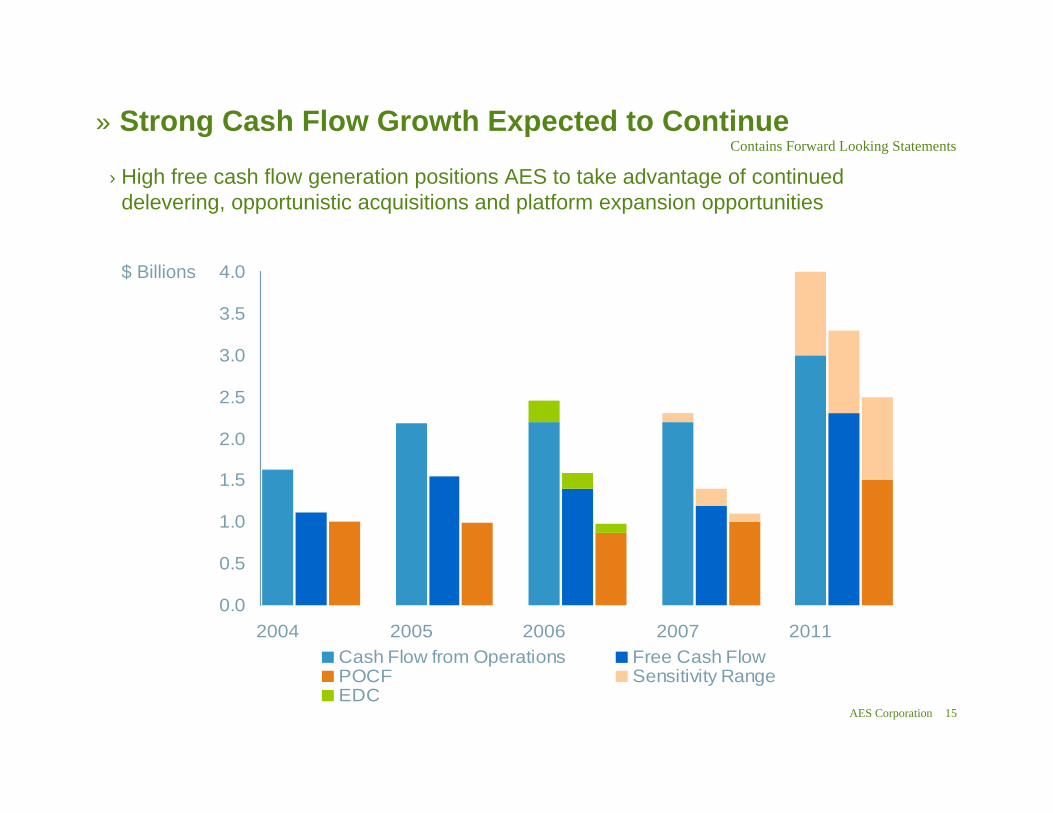

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2004 2005 2006 2007 2011Cash Flow from Operations Free Cash FlowPOCF Sensitivity RangeEDC

» Strong Cash Flow Growth Expected to Continue

› High free cash flow generation positions AES to take advantage of continued delevering, opportunistic acquisitions and platform expansion opportunities

Contains Forward Looking Statements

$ Billions

AES Corporation 16

» Why Invest in AES?Contains Forward Looking Statements

› Global demand for power continues to grow

› AES is well positioned to leverage market opportunities and industry dynamics

–Global reach, local insights–Portfolio diversity, financial flexibility

› Focused on long-term value creation with sustained growth in EPS and cash flow

AES Corporation 17

» Appendix

AES Corporation 18

» AssumptionsForecasted financial information is based on certain material assumptions. Such assumptions include, but are not limited to: (a) no unforeseen external events such as wars, depressions, or economic or political disruptions occur; (b) businesses continue to operate in a manner consistent with or better than prior operating performance, including achievement of planned productivity improvements including benefits of global sourcing, and in accordance with the provisions of their relevant contracts or concessions; (c) new business opportunities are available to AES in sufficient quantity to achieve its growth objectives; (d) no material disruptions or discontinuities occur in GDP, foreign exchange rates, inflation or interest rates during the forecast period; and (e) material business-specific risks as described in the Company’s SEC filings do not occur individually or cumulatively. In addition, benefits from global sourcing include avoided costs, reduction in capital project costs versus budgetary estimates, and projected savings based on assumed spend volume which may or may not actually be achieved. Also, improvement in certain KPIs such as equivalent forced outage rate and commercial availability may not improve financial performance at all facilities based on commercial terms and conditions. These benefits will not be fully reflected in the Company’s consolidated financial results.

The cash held at qualifying holding companies (QHCs) represents cash sent to subsidiaries of the Company domiciled outside of the U.S. Such subsidiaries had no contractual restrictions on their ability to send cash to AES, the Parent Company. Cash at those subsidiaries was used for investment and related activities outside of the U.S. These investments included equity investments and loans to other foreign subsidiaries as well as development and general costs and expenses incurred outside the U.S. Since the cash held by these QHCs is available to the Parent, AES uses the combined measure of subsidiary distributions to Parent and QHCs as a useful measure of cash available to the Parent to meet its international liquidity needs. AES believes that unconsolidated parent company liquidity is important to the liquidity position of AES as a parent company because of the non-recourse nature of most of AES’s indebtedness.

AES Corporation 19

› Adjusted earnings per share – Defined as diluted earnings per share from continuing operations excluding gains or losses associated with (a) mark-to-market amounts related to FAS 133 derivative transactions, (b) foreign currency transaction impacts on the net monetary position related to Brazil, Venezuela, and Argentina, (c) significant asset gains or losses due to disposition transactions and impairments, and (d) early retirement of recourse debt. AES believes that adjusted earnings per share better reflects the underlying business performance of the Company, and is considered in the Company’s internal evaluation of financial performance. Factors in this determination include the variability associated with mark-to-market gains or losses related to certain derivative transactions, currency gains and losses, periodic strategic decisions to dispose of certain assets which may influence results in a given period, and the early retirement of corporate debt.

› Free cash flow – Net cash flow from operating activities less maintenance capital expenditures. Maintenance capital expenditures reflect property additions less growth capital expenditures. AES believes that free cash flow is a useful measure for evaluating our financial condition because it represents the amount of cash provided by operations less maintenance capital expenditures as defined by our businesses, that may be available for investing or for repaying debt.

› Subsidiary distributions – Cash distributions (primarily dividends and interest income) from subsidiary companies to the parent company and qualified holding companies. These cash flows are the source of cash flow to the parent to meet corporate interest, overhead, cash taxes, and discretionary uses such as recourse debt reductions and corporate investments.

» Definitions of Non-GAAP Financial Measures

AES Corporation 20(1) A non-GAAP financial measure.

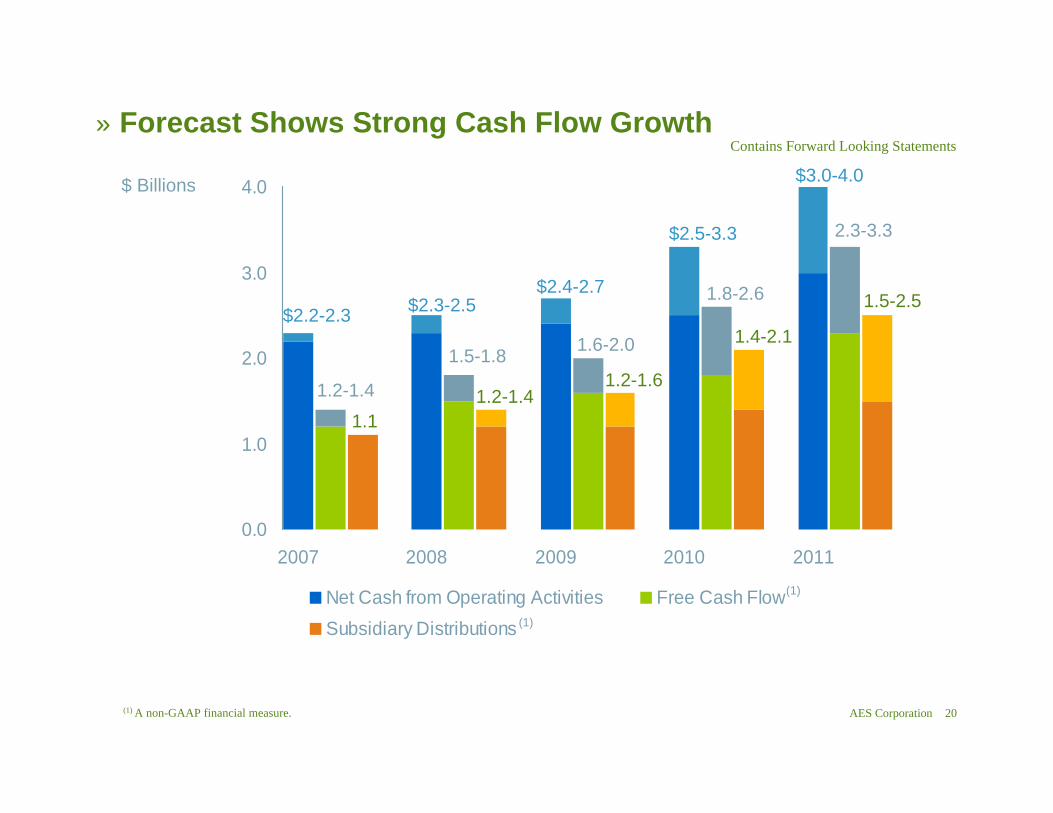

» Forecast Shows Strong Cash Flow GrowthContains Forward Looking Statements

0.0

1.0

2.0

3.0

4.0

2007 2008 2009 2010 2011

Net Cash from Operating Activities Free Cash FlowSubsidiary Distributions

$2.4-2.7$2.3-2.5$2.2-2.3

$2.5-3.3

$3.0-4.0

1.5-1.8

1.2-1.4

1.6-2.0

1.8-2.6

2.3-3.3

1.2-1.41.1

1.2-1.6

1.4-2.1

1.5-2.5

$ Billions

(1)

(1)

AES Corporation 21

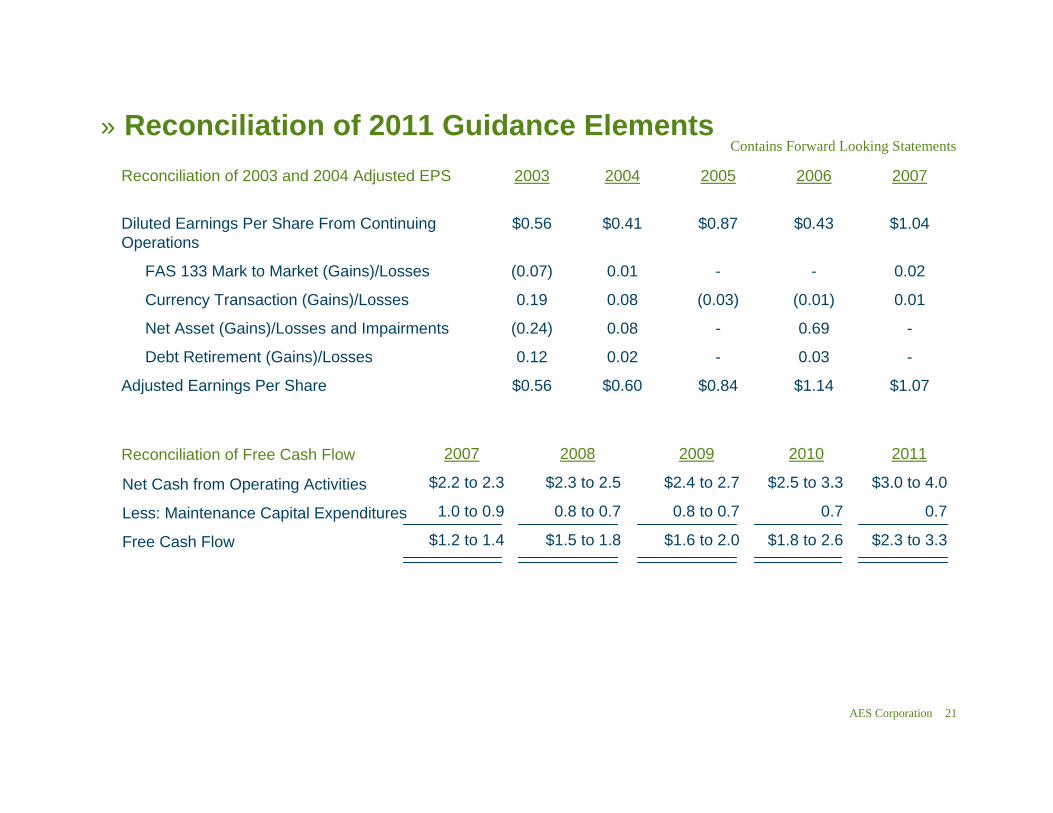

» Reconciliation of 2011 Guidance Elements

$0.60

0.02

0.08

0.08

0.01

$0.41

2004

$0.84

-

-

(0.03)

-

$0.87

2005

$1.14

0.03

0.69

(0.01)

-

$0.43

2006

$1.07

-

-

0.01

0.02

$1.04

20072003Reconciliation of 2003 and 2004 Adjusted EPS

$0.56

0.12

(0.24)

0.19

(0.07)

$0.56

Adjusted Earnings Per Share

Debt Retirement (Gains)/Losses

Net Asset (Gains)/Losses and Impairments

Currency Transaction (Gains)/Losses

FAS 133 Mark to Market (Gains)/Losses

Diluted Earnings Per Share From Continuing Operations

Reconciliation of Free Cash Flow

Net Cash from Operating Activities

Less: Maintenance Capital Expenditures

Free Cash Flow

$2.4 to 2.7

0.8 to 0.7

$1.6 to 2.0

20092008

$2.3 to 2.5

0.8 to 0.7

$1.5 to 1.8

$2.5 to 3.3

0.7

$1.8 to 2.6

2010

$3.0 to 4.0

0.7

$2.3 to 3.3

20112007

$2.2 to 2.3

1.0 to 0.9

$1.2 to 1.4

Contains Forward Looking Statements

![[PPT]PowerPoint Presentation - AES Corporation | …aes-corp.com/wp-content/uploads/2015/09/Dealer_ppt_Oct... · Web viewTECHNOLOGY Dealer url Dealer logo View ‘How Mesh Radio Technology](https://img.pdfslide.us/doc/110x75/5b8742527f8b9a162d8e9ec0/pptpowerpoint-presentation-aes-corporation-aes-corpcomwp-contentuploads201509dealerpptoct.jpg)