Embed Size (px)

Citation preview

AEROSPACE & DEFENSE

“Why Strategic Electronics”?

1 USA

2 China

3 Russia

4 Saudi Arabia

5 UK

6 Japan

7 Germany

8 France

9 India

10 Brazil

Sources: CIA.gov, CIA World Factbookhttp://www.globalfirepower.com/defense-spending-budget.asp

‘India is one of the leading spenders in Defense” Defense

We are focusing on developing India's defense industry with a sense of mission. This is why it is at the heart of the "Make in India" programme – Shri. Narendra Modi, PM, INDIA

3

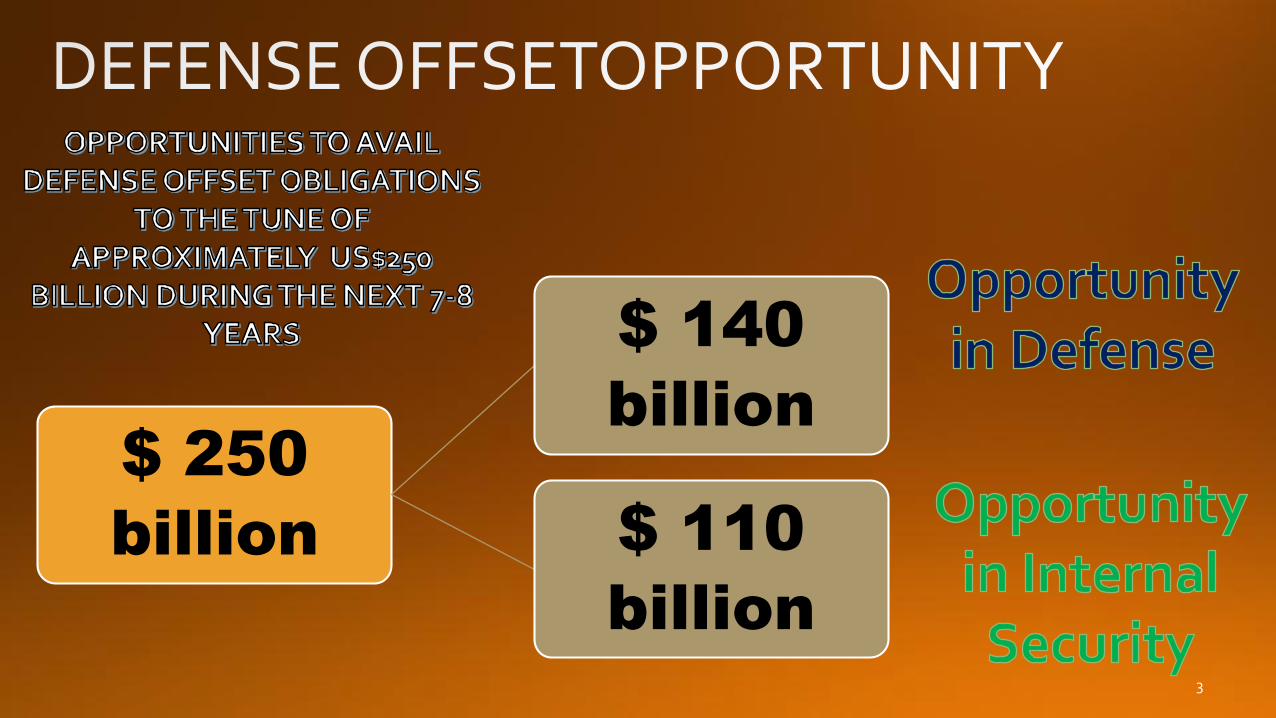

$ 250

billion

$ 140

billion

$ 110

billion

4

The recently concluded DEFTRONICS 2014 saw a powerful line-up of industry experts, governmentofficials, strategists, policy makers and business leaders discussing various defence related policies like theoffset policy, procurement policy and FDI in defence, the licensing policy and foreign trade. A lot wasdiscussed and debated. And while we work on a detailed synopsis of the event, here is a brief of how theevent was kicked off and the salient points discussed during the inauguration.

Electronica India 2014 and productronica India 2014 ended with a strong result of 13,906 visitors. 341 exhibitors, representing 713 companies, showcased their products, solutions and services at the trade fairs from September 23 to 25, 2014

DEFTRONICS 2014 – had 40 speakers including Thought leaders & policy makers & 350 conference attendees

Key Speakers at DEFTRONICS 2014

Peter GutsmiedlCEO

Airbus D&S India

Dave RansonMD – MOOG

Andleeb ShadmanCOO - Airbus

Som Pal ChoudhuryMD – Analog Devices

Rahul GangalRoland Berger

GopiChand KatragaddaGroup CTO TATA Sons

Paul KlonowskiDirector A&D,

Analog Devices

Kishore JayaramanPresident – India & South Asia

Rolls Royce

Anup VittalMD - Safran Engg.

Services India

Ram PrasadMD - Rockwell Collins

Dr. A Sivathanu Pillai CEO & MD

BrahMos Aerospace

Shyam Chetty,Director, NAL

6

Inauguration & Theme address

Keynote address on Defense Procurement Policy (DPP)

Panel Session I: Indian Defense Manufacturing

Panel Session II: Foreign Direct Investment (FDI) in Defense & Aerospace – What should India do to bridge gaps in capability

Buyer-Seller Meet

Panel Session III: R&D and Innovation in Aerospace and Defense

Panel Session IV: Future Technology Trends in Defense, Aerospace & Internal Security

Panel Session V: The MAKE programs of MoD - ‘Where rubber meets the road’

Panel Session VI: Panel on Opportunities and Challenges of Indian Start-Ups in Defense Industry=

Summary & Recommendation

7

8

• Capital spending in India’s defence budget is expected to grow to approximately 154,000 crores by 2018.

• The ESDM industry is expected to provide employment to more than 2 lakh skilled and semi-skilled workers by 2015.

• The government plans to achieve 50% of demand for high impact products through high-value added manufacturing will boost the growth of India’s defence sector.

• Re-introduction of services as a valid offset avenue is a welcome step.

• Government funding would go a long way in promoting R&D in the ESDM industry, but there is an urgent need to monitor the utilisation of funds.

• A standard operating procedure on the lines of USA’s Defence Advanced Research Projects Agency (DARPA) model must be formalised.

• The current FDI cap of 49% should probably be re-considered after a year if it has not been able to incentivise foreign OEMs to invest and transfer proprietary technology into India.

Recommendations from IESA-PwC Report at Deftronics

9

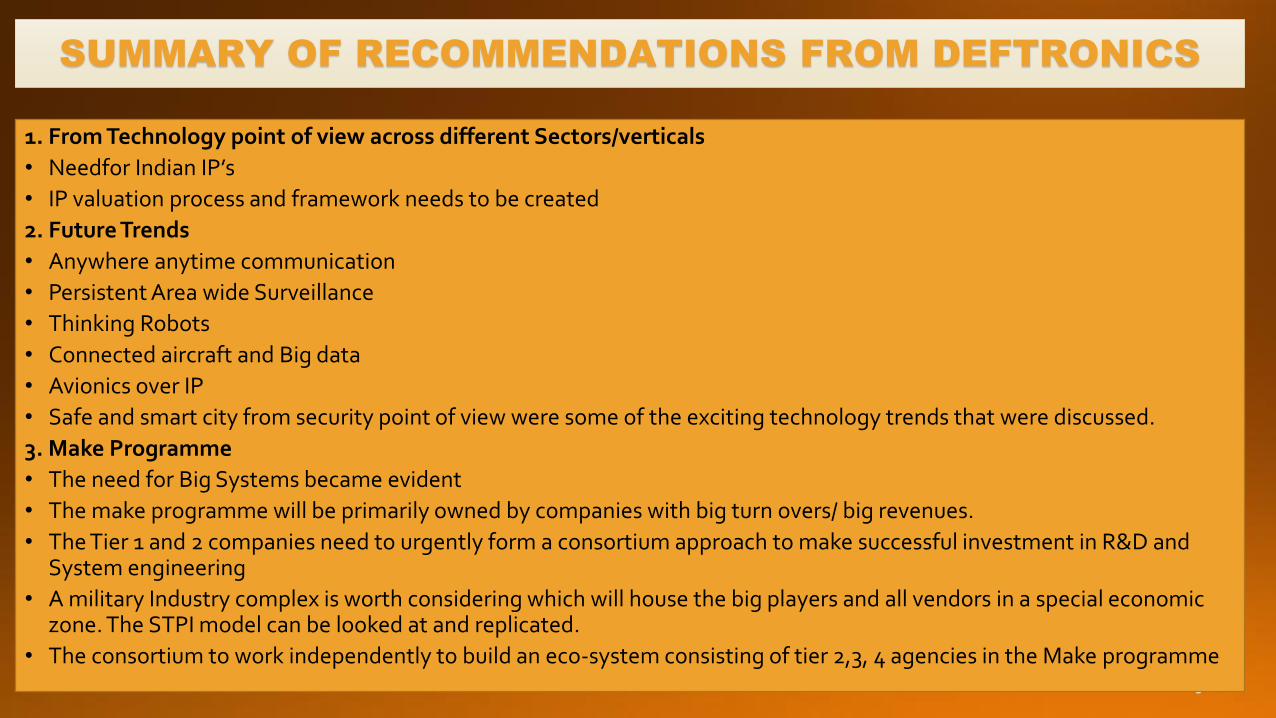

1. From Technology point of view across different Sectors/verticals

• Needfor Indian IP’s

• IP valuation process and framework needs to be created

2. Future Trends

• Anywhere anytime communication

• Persistent Area wide Surveillance

• Thinking Robots

• Connected aircraft and Big data

• Avionics over IP

• Safe and smart city from security point of view were some of the exciting technology trends that were discussed.

3. Make Programme

• The need for Big Systems became evident

• The make programme will be primarily owned by companies with big turn overs/ big revenues.

• The Tier 1 and 2 companies need to urgently form a consortium approach to make successful investment in R&D and System engineering

• A military Industry complex is worth considering which will house the big players and all vendors in a special economic zone. The STPI model can be looked at and replicated.

• The consortium to work independently to build an eco-system consisting of tier 2,3, 4 agencies in the Make programme

SUMMARY OF RECOMMENDATIONS FROM DEFTRONICS

10

4. Policies

• DPP 2013 is well understood now.

• Buy Indian Offers – opportunities for partnerships were seen

• FDI @49% is seen as limiting by OEM’s.

• FDI for Technology or Capital- needs definition and differentiation (IESA)

• LTIPP- 15 years – seems to be too vague. Can we get a 5 year list w/o losing the 15 year perspective?

• The definition of ‘Indian companies’ need a relook.

• A need for a formal platform for dialog with MOD is much needed

• Karnataka Aerospace policy- can it be replicated at national level- IESA partner states? (IESA)

• Some taxation issues still remain. Ex:- MRO, Service tax, Transfer pricing for MNC’s etc.

• Defense export policy etc.

4. Manufacturing

• Long lead time to get business from investments

• Can there be an alternate to NCNC model- like DARPA in US

• Can there be a separate fund for Non DRDO Organizations

• Can DRDO become more of handholding agency like DARPA for critical IP development

• How to safeguard the stake holder investments – if government were to give money for technology development to outside the government entities?

• Approval process and need for transparency

• How to make it easy to work with DRDO and Defense PSU’s

SUMMARY OF RECOMMENDATIONS FROM DEFTRONICS

11

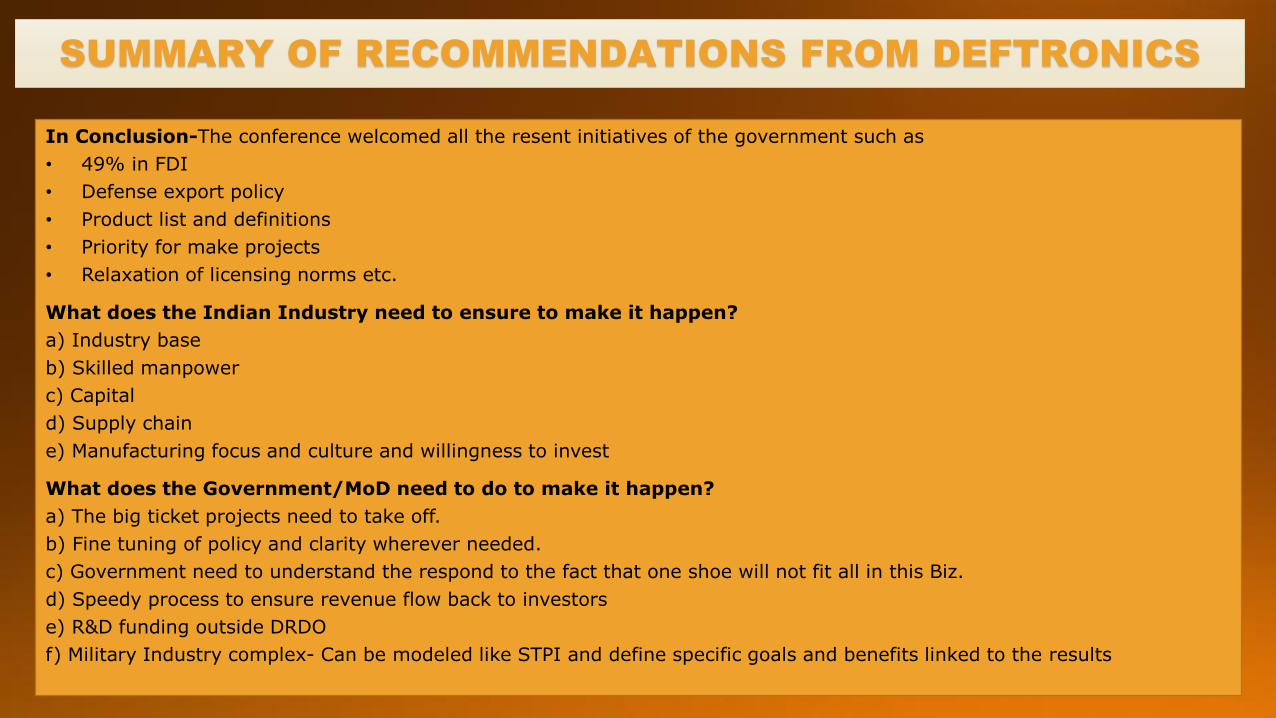

In Conclusion-The conference welcomed all the resent initiatives of the government such as

• 49% in FDI

• Defense export policy

• Product list and definitions

• Priority for make projects

• Relaxation of licensing norms etc.

What does the Indian Industry need to ensure to make it happen?

a) Industry base

b) Skilled manpower

c) Capital

d) Supply chain

e) Manufacturing focus and culture and willingness to invest

What does the Government/MoD need to do to make it happen?

a) The big ticket projects need to take off.

b) Fine tuning of policy and clarity wherever needed.

c) Government need to understand the respond to the fact that one shoe will not fit all in this Biz.

d) Speedy process to ensure revenue flow back to investors

e) R&D funding outside DRDO

f) Military Industry complex- Can be modeled like STPI and define specific goals and benefits linked to the results

SUMMARY OF RECOMMENDATIONS FROM DEFTRONICS

Media Coverage at DEFTRONICS 2014

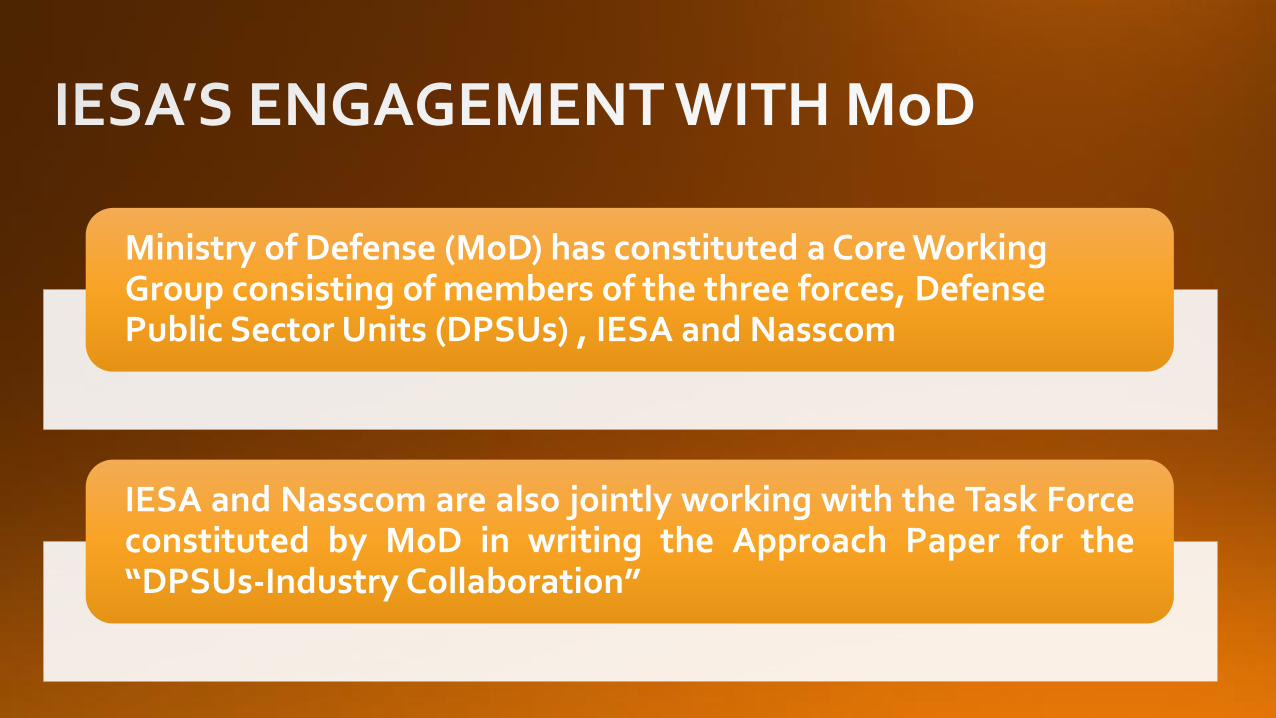

Ministry of Defense (MoD) has constituted a Core Working Group consisting of members of the three forces, Defense Public Sector Units (DPSUs) , IESA and Nasscom

IESA and Nasscom are also jointly working with the Task Forceconstituted by MoD in writing the Approach Paper for the“DPSUs-Industry Collaboration”

Company Name Aeronics eMaroh Venkat RamanAirbus Andleeb ShadmanAnalog Devices India Pvt. Ltd. Somshubhro Pal ChoudhuryARM Embedded Technologies Pvt. Ltd. Shiv TurmariDAC Intl. D. A. MohanideaForge Ankit MehtaInfotech Enterprises Ltd. Manjunatha HebbarMOOG David RansonsNAL Shyam Shetty /MainakRambus Chip Technologies (I) Pvt. Ltd. K. KrishnamoorthySLN Technologies Pvt. Ltd. Anilkumar MuniswamySugosha consultancy Col KuberTata Power SED R MuralidharanTE Connectivity Sanjay HanduTrigyn Technologies ShyamXilinx Neeraj Varma