Embed Size (px)

Citation preview

8/9/2019 Advancements in Banking

http://slidepdf.com/reader/full/advancements-in-banking 1/16

IMPACT OF EMERGINGIMPACT OF EMERGING

TRENDS AND ADVANCEMENTSTRENDS AND ADVANCEMENTSIN THE GLOBAL BANKINGIN THE GLOBAL BANKINGAND FINANCIAL SERVICESAND FINANCIAL SERVICES

INDUSTRYINDUSTRY

Terrence W. FarrellTerrence W. Farrell

Presentation to Caribbean Association of Indigenous BanksPresentation to Caribbean Association of Indigenous Banks

ConferenceConferenceSt Lucia, November 14-16, 2004St Lucia, November 14-16, 2004

8/9/2019 Advancements in Banking

http://slidepdf.com/reader/full/advancements-in-banking 2/16

8/9/2019 Advancements in Banking

http://slidepdf.com/reader/full/advancements-in-banking 3/16

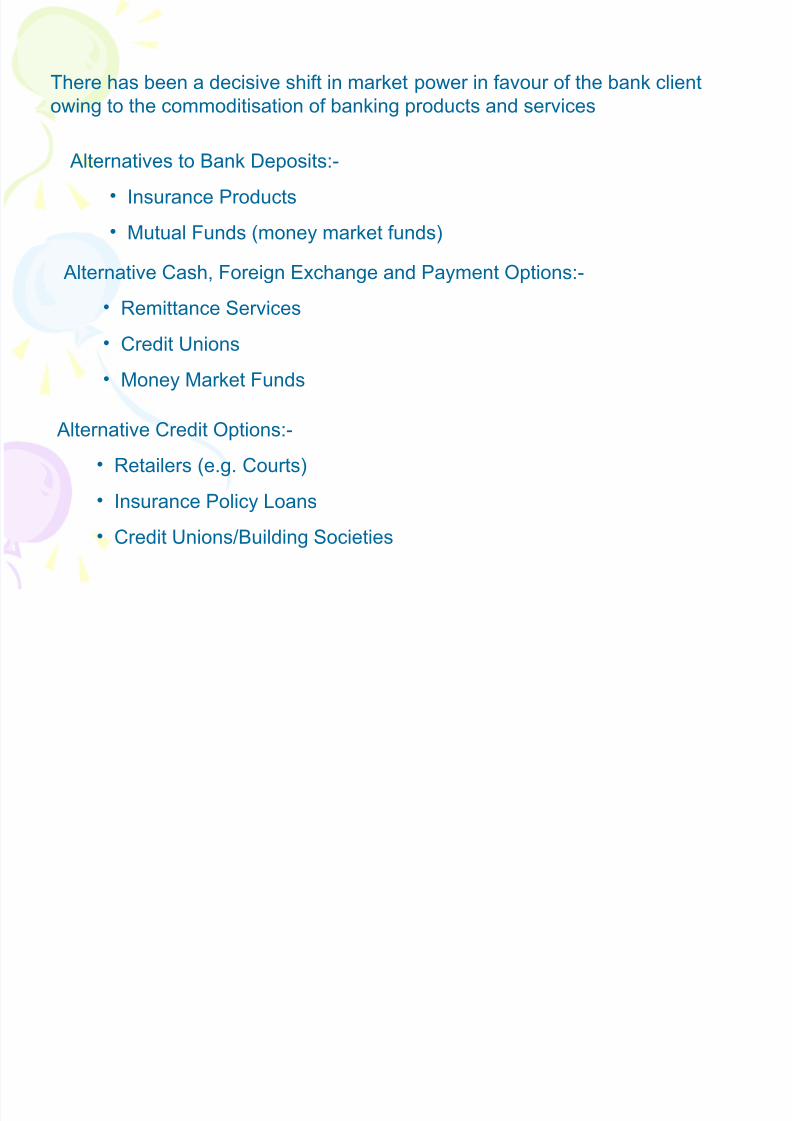

There has been a decisive shift in market power in favour of the bank clientowing to the commoditisation of banking products and services

Alternatives to Bank Deposits:-

• Insurance Products

• Mutual Funds (money market funds)

Alternative Cash, Foreign Exchange and Payment Options:-• Remittance Services

• Credit Unions

• Money Market Funds

Alternative Credit Options:-

• Retailers (e.g. Courts)

• Insurance Policy Loans

• Credit Unions/Building Societies

8/9/2019 Advancements in Banking

http://slidepdf.com/reader/full/advancements-in-banking 4/16

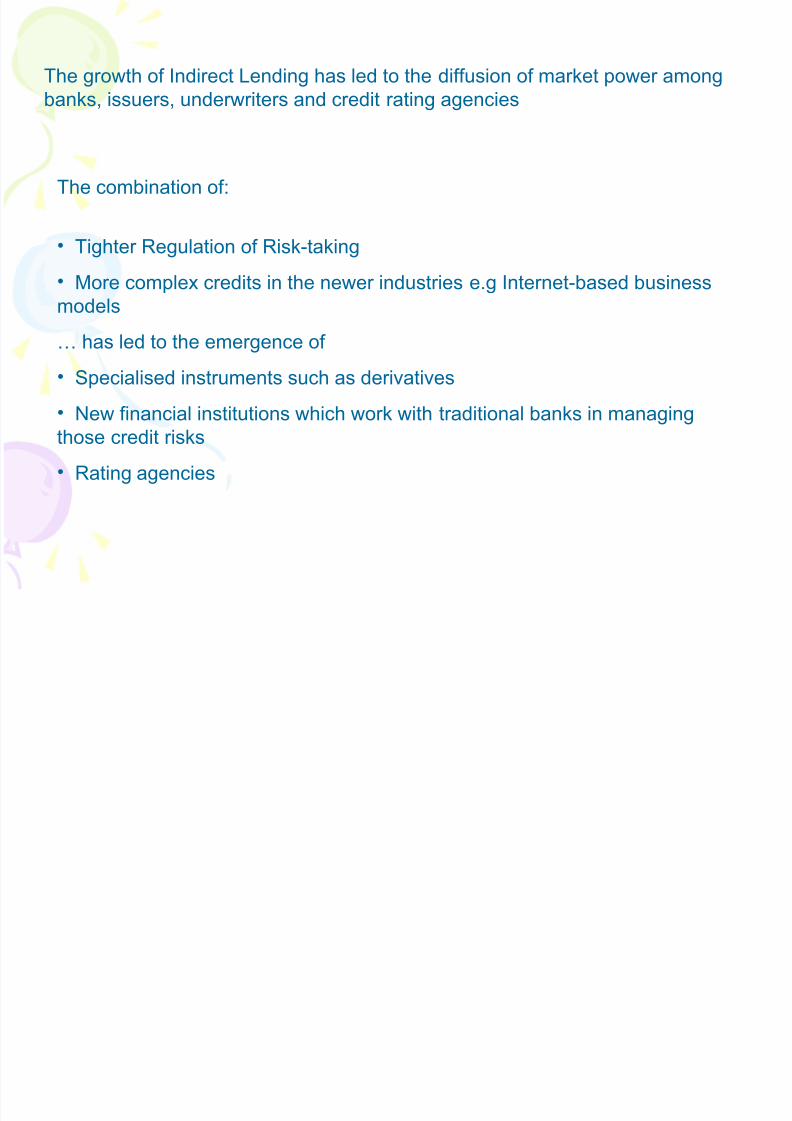

The growth of Indirect Lending has led to the diffusion of market power amongbanks, issuers, underwriters and credit rating agencies

The combination of:

• Tighter Regulation of Risk-taking

• More complex credits in the newer industries e.g Internet-based businessmodels

… has led to the emergence of

• Specialised instruments such as derivatives

• New financial institutions which work with traditional banks in managingthose credit risks

• Rating agencies

8/9/2019 Advancements in Banking

http://slidepdf.com/reader/full/advancements-in-banking 5/16

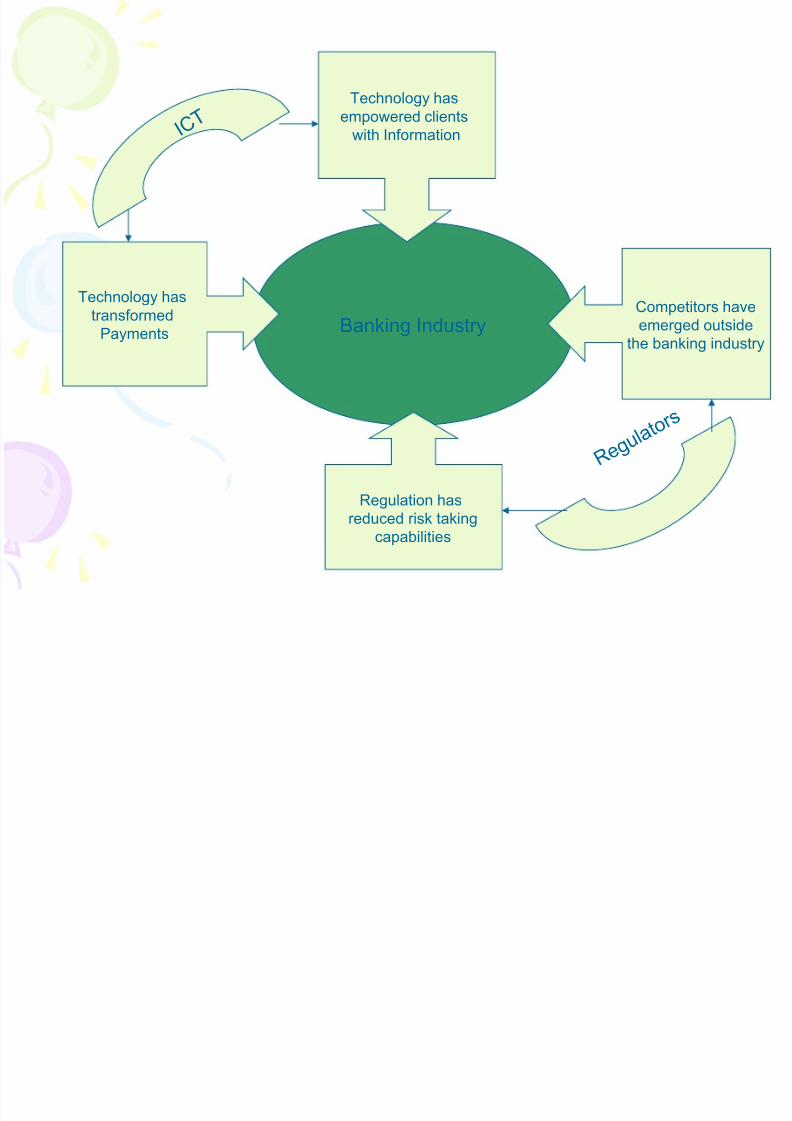

Banking Industry

Technology hastransformed

Payments

Technology hasempowered clients

with Information

Regulation hasreduced risk taking

capabilities

Competitors haveemerged outside

the banking industry

I C T

R e g u l a

t o r s

8/9/2019 Advancements in Banking

http://slidepdf.com/reader/full/advancements-in-banking 6/16

IMPACT OF THE CHANGES IN THE BANKING INDUSTRY

ON COMMERCE

• Transactions are now instantaneous; float has been largely eliminated;

cash can be swept and managed much more efficiently.

• Households and firms can effect many transactions Anywhere, Anytime,and increasingly ANYHOW (Voice, Wireless, Call Centre, Internet, Cellphone)

• Scope for fraud (identity theft, interception of transactions, etc) has grownsignificantly

8/9/2019 Advancements in Banking

http://slidepdf.com/reader/full/advancements-in-banking 7/16

IMPACT OF THE CHANGES IN THE BANKING INDUSTRY

ON THE BANKING INDUSTRY ITSELF

• Erosion of margins – supernormal profits in banking have disappeared;

incremental earnings growth is achieved through consolidation• Scale is crucial to bank profitability; banks have had to become regional,national or global in scope and reach

• Continual investment in technology is a business imperative, even thoughmuch of that investment is defensive and confers no long term sustainable

competitive advantage• Yet, banks have to strive to achieve and maintain customer intimacy andloyalty

8/9/2019 Advancements in Banking

http://slidepdf.com/reader/full/advancements-in-banking 8/16

Some predictions made in 1995/6 about the future of Financial Services

P. Gosling, Financial Services in the Digital Age

On the Bank Branch:-

• The traditional bank branch is on death row – along with some of thetraditional banks

• The proportion of transactions conducted by branches will fall from40 per cent in 1993 to less than 20 per cent in 2000

• “…electronic banking is going to handle 80 per cent of alltransactions in perhaps five years” (1996)

• Four alternative visions of the bank branch:-

• General retail centre with kiosks operating as electronic brokersbut still owned by bank

• Branch as a franchised operation

• Freelance branch

• Electronic bank

8/9/2019 Advancements in Banking

http://slidepdf.com/reader/full/advancements-in-banking 9/16

Summary and ConclusionSummary and Conclusion• The banking industry today is vastly different from just 20 years

ago• Banks have less market power and the industry has maintained

profitability because on restrictions on entry and because of consolidation

• Banks will struggle to maintain margins in the Payments business

• The Credit business has become more specialised and banks areplaying a less important role• Bank consolidation will continue as will other means of controlling

and reducing costs such as:-– Business Process Outsourcing– Franchising– Use of Information and Communications Technologies to shift ‘work’ on

to the customer– Streamlining and rationalising branch locations

• Banks will become an element of Integrated Financial Servicesorganisations, which will incorporate a range of services aroundpayments, credit, securities, insurance and mutual funds.

8/9/2019 Advancements in Banking

http://slidepdf.com/reader/full/advancements-in-banking 10/16

CARIBBEAN IMPLICATIONSCARIBBEAN IMPLICATIONS• The process of consolidation in the region is

well advanced• Banks in the region will have to move more

quickly to deploy information andcommunications technologies• The experience of banks owning insurers or

vice versa in the region has perhapsprejudiced regulators, but the move towardIFS is inevitable

8/9/2019 Advancements in Banking

http://slidepdf.com/reader/full/advancements-in-banking 11/16

THANK YOUTHANK YOU

8/9/2019 Advancements in Banking

http://slidepdf.com/reader/full/advancements-in-banking 12/16

8/9/2019 Advancements in Banking

http://slidepdf.com/reader/full/advancements-in-banking 13/16

• Imaging• Web-based

transactions

• Security

• Basel II• Gramm-Leach-

Bliley (eliminated

restrictions of Glass-Steagall)

• Riegle-Neal (inter-state banking)

8/9/2019 Advancements in Banking

http://slidepdf.com/reader/full/advancements-in-banking 14/16

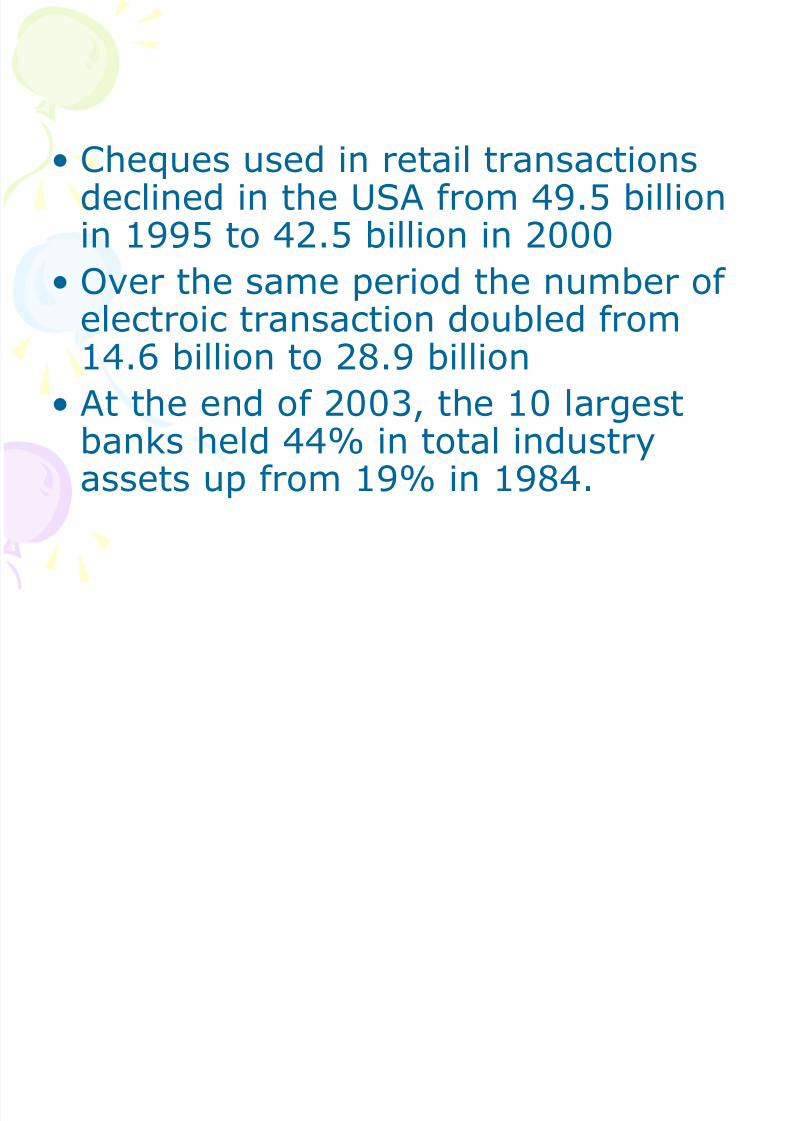

• Cheques used in retail transactionsdeclined in the USA from 49.5 billionin 1995 to 42.5 billion in 2000

• Over the same period the number of electroic transaction doubled from14.6 billion to 28.9 billion

• At the end of 2003, the 10 largestbanks held 44% in total industryassets up from 19% in 1984.

8/9/2019 Advancements in Banking

http://slidepdf.com/reader/full/advancements-in-banking 15/16

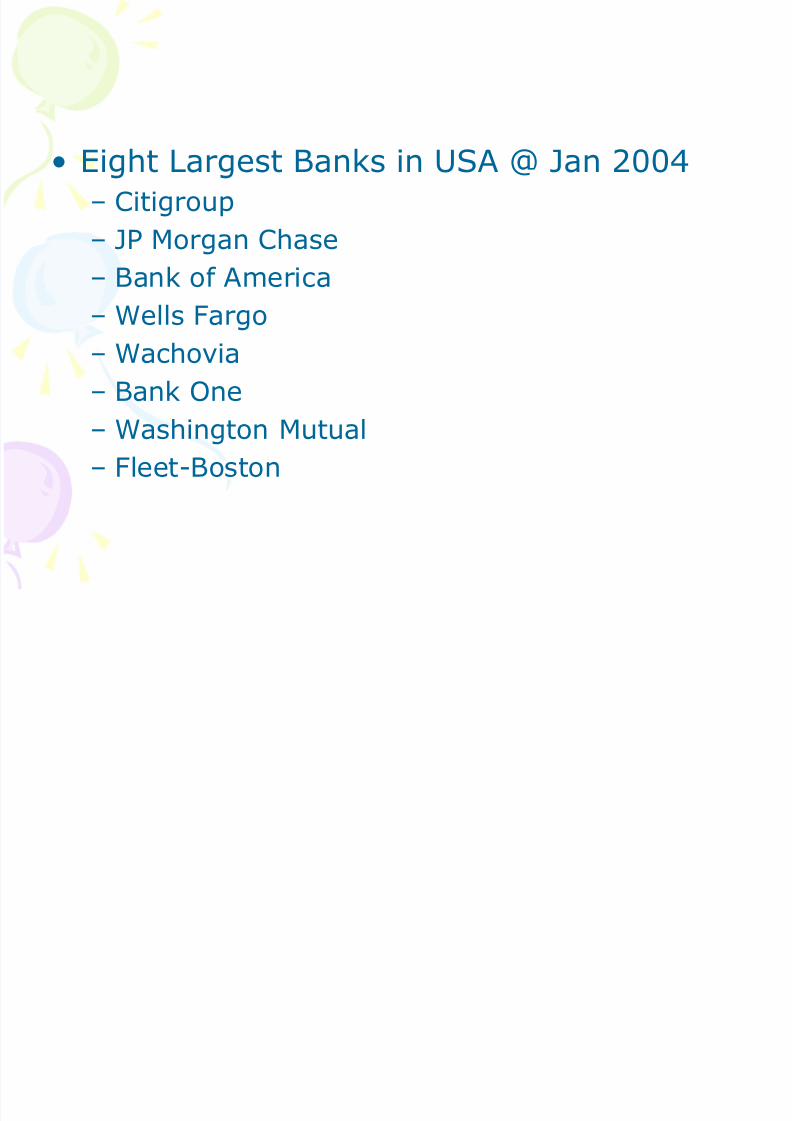

• Eight Largest Banks in USA @ Jan 2004– Citigroup– JP Morgan Chase

– Bank of America– Wells Fargo– Wachovia– Bank One– Washington Mutual– Fleet-Boston

8/9/2019 Advancements in Banking

http://slidepdf.com/reader/full/advancements-in-banking 16/16

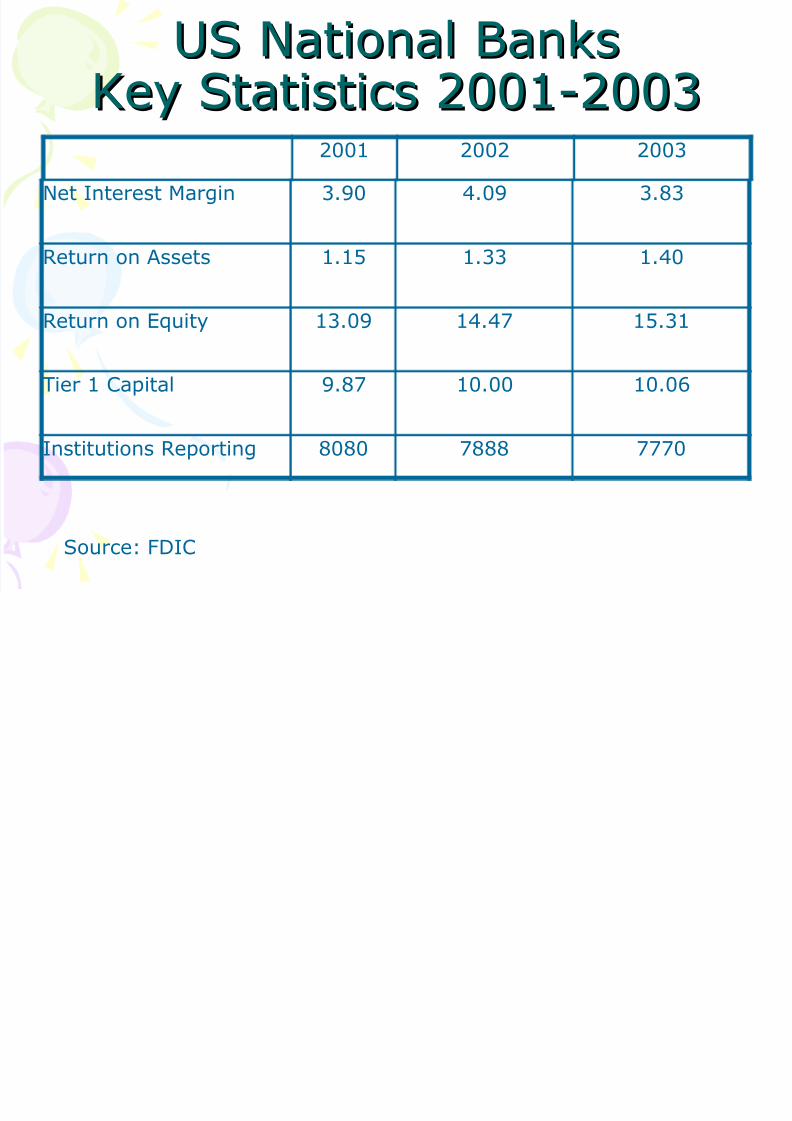

US National BanksUS National BanksKey Statistics 2001-2003Key Statistics 2001-2003

2001 2002 2003

Net Interest Margin 3.90 4.09 3.83

Return on Assets 1.15 1.33 1.40

Return on Equity 13.09 14.47 15.31

Tier 1 Capital 9.87 10.00 10.06

Institutions Reporting 8080 7888 7770

Source: FDIC