Embed Size (px)

Citation preview

WHO TO CONTACT

For Additional Registrations:

-Call Strafford Customer Service 1-800-926-7926 x10 (or 404-881-1141 x10)

For Assistance During the Program:

-On the web, use the chat box at the bottom left of the screen

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register

additional people, please call customer service at 1-800-926-7926 x10 (or 404-881-1141 x10). Strafford

accepts American Express, Visa, MasterCard, Discover.

• Listen on-line via your computer speakers.

• Respond to five prompts during the program plus a single verification code. You will have to write down

only the final verification code on the attestation form, which will be emailed to registered attendees.

• To earn full credit, you must remain connected for the entire program.

Advanced Multistate Taxation of

Partnerships and Individual Partners Business vs. Nonbusiness Income Characterization, Reconciling Conflicting States Tax Treatments and More

WEDNESDAY, JANUARY 27, 2016, 1:00-2:50 pm Eastern

Tips for Optimal Quality

Sound Quality

When listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, please e-mail [email protected]

immediately so we can address the problem.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

January 27, 2016

Advanced Multistate Taxation of Partnerships and Individual Partners

Ned Leiby

Director, Income and Franchise Taxes

Ryan

Jennifer A. Zimmerman

Attorney

Horwood Marcus & Berk Chartered

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

5

Jennifer A. Zimmerman Horwood Marcus & Berk Chartered

STATE TAXATION OF PASS-THROUGH ENTITIES

Key Issues and Current Developments

6

• Partnerships

– General Partnerships

– Limited Partnerships

– Joint Ventures

– Alliances

– Private Equity Funds

– Hedge Funds

• Multi-member LLCs taxed as partnerships

• SMLLCs (“disregarded entities”)

• S corporations

• Specialized Entities: RICs, REITs, REMICs, Cooperatives and Some Trusts

(Note: we will reference “PTEs” and “partners”)

How We Define “Pass-Through Entities”

7

• The last 20 years reflect a substantial increase in the use of PTEs

• The increase was driven by federal tax law and state entity laws

• Corporate income tax was declining at the same time government revenue needs were increasing

• Pass-through planning was led by federal tax benefits: avoidance of double taxation, maximization of losses and incentives and allowance for flexibility

Brief History of PTEs

8

State-Federal Conformity Issues

9

The issue of federal-state conformity actually raises two separate questions:

#1 - Characterization: Does the state’s tax law follow the federal characterization of the PTE under the “check-the-box” rules?

#2 - Pass-through Treatment: Does the state’s tax law follow the federal tax treatment of income of “partnerships” and “disregarded entities”?

State Conformity Overview

10

#1 – Characterization

• Most states respect entity characterization under federal “check-the-box” regulations – An LLC that is a disregarded entity for federal tax is a

disregarded entity for state tax purposes

• Some Notable (Income Tax) Exceptions: – MA (large S corporations and SMLLCs are taxable as S

Corp if owned by S Corp) – NH (all PTEs taxed at entity level, even sole

proprietorships) – RI (corporate-owned SMLLC is taxed as a C Corp)

11

#2 – Pass-Through Treatment

• Most States Also Follow Federal Pass-through Treatment

– No tax on the PTE, but tax on the partners

• Some Notable Exceptions and Variations:

– Entity-level taxes (IL, NH, ME, MI, OH, OK, TN, TX)

– Don’t forget local jurisdictions (Phili, DC, NYC)

– Entity-level capital stock and fees (NY, PA, others)

– Withholding/estimated tax/partner consent rules (many)

– Composite filing rules (many)

• Some States Also Provide Exemption for Investment Partnerships and Their Partners

12

Reminder of “Other” Filings

Remember that PTEs are generally not disregarded for non-income taxes, including:

State registrations and filing fees

Non-Income Taxes: Most Sales and Use Taxes

Some Franchise / Privilege Taxes

Excise Taxes (“sin taxes” – tobacco, alcohol, etc.)

Property Taxes

Real Estate Transfer Taxes

Employment Taxes

13

Conformity Conflicts “Jurisdictional Mismatches” may occur. Example:

– PTE operates solely in NH; 70% corporate partner domiciled in UDITPA state, conducts business in many states; PTE distributive share is “non-business” income

– NH: Applies entity-level tax on PTE (BPT & BET) using water’s edge combination apportionment factors (no business/non-business distinction)

– Domicile state: taxes entire 70% share of “nonbusiness” income to the Partner in state of commercial domicile

NPH LLC

70%

Corporate Partner

Multistate Business

Domiciled in UDITPA

State

$ Distributive Share =

Non-business Income

100% in NH

PTE

Partner

14

Nexus Issues Affecting Partners

15

Central Nexus Issue

• Key Nexus Question: – May a state in which the PTE is doing business subject

a nonresident corporate partner to the state’s corporate income (or franchise tax) on its distributive share of partnership income, even if the corporate partner has no independent activity in the state?

• Key Policy Question: – Is it correct to tax a nonresident limited partner on its

2% distributive share but not a nonresident shareholder on its 2% stock ownership in a corporation?

16

Constitutional Framework • Due Process Clause

– Two requirements: (1) Taxpayer must have sufficient “minimum contacts” with the taxing state and (2) income must have a “rational relationship” to intrastate values of the enterprise

– Concern is the “fundamental fairness of government activity” (Quill

Corp. (1992))

– A state may not subject to tax a nonresident on its ownership of stock in a domestic corporation under the DPC (Shaffer v. Heitner (1977))

• Commerce Clause

– Four Part Test: (1) Substantial Nexus, (2) Fairly Apportioned, (3) Nondiscrimination, (4) Fairly Related (Complete Auto (1977))

• “Unitary” Principles

– The “lynchpin of apportionability … is the unitary-business principle” (Mobil Oil (1980))

17

General Rule

• General Rule: The vast majority of states consider a corporation’s ownership of an interest in a partnership doing business in the state to be sufficient to create nexus for the corporation, even if the corporate partner has no other contact with the state.

• Issues: – What theories support this conclusion?

– What constitutional principles prohibit taxation?

– Does the same rule apply to members of LLCs?

– Does the same rule apply to limited partners?

18

How Have the Cases Come Out?

Borden (IL 2000):

NRLP taxable because LP interest is sufficient

“minimum connection”

Non-Resident Limited Partners (NRLP”) TAX

NO

TAX

Village SM (NJ 2013):

NRLP taxable because LP had in-state presence / connection

UTELCOM (LA 2011): NRLP not taxable –

under state statute

BIS (NJ 2011) / Dutton (VA 2007): NRLP with no connections not taxable –

under Constitution

Lanzi (AL 2006): NRLP not taxable -

under Constitution

(akin to stock)

19

Ancillary Nexus Issue #1 – “Nexus Only” • Key Issue: Some states require (or allow) combined/consolidated returns

only for corporate affiliates that have nexus with the state (“nexus-only” filings). See Iowa Code Sec. 422.37(2). Does an out-of-state partner qualify as a “nexus” member solely on the basis of the activities of in-state PTE?

• Example: A and C are eligible, but is B by virtue of PTE?

Corp B

(no nexus)

PTE

(nexus)

Corp D

(no nexus)

Corp C

(nexus)

Corp A

(nexus)

20

Ancillary Nexus Issue #1 – “Nexus Only” • Considerations:

– Yes, but only if the Partner B is taxable in the state by virtue of the PTE’s activities? So, does this mean that a 2% GP may be an eligible member but a 2% LP may not? What impact could this have on the return?

– No, if Partner B is only a passive limited partner because a corporate shareholder would not be taxable by virtue of its subsidiary’s nexus?

– No, if the state consolidated return statute can be strictly construed to only include the corporate member (Partner B) based on its own individual activities?

21

Ancillary Nexus Issue #2 – Throw-Back, Throw-Out, Joyce/Finnegan

• Situation 1: Should a corporate

partner’s sales to a destination state where it has no independent nexus be thrown back if the PTE has nexus in the state but it does not?

• Situation 2: Should a PTE’s sales to a destination state where is has no independent nexus be thrown back if the corporate partner has nexus in the destination state but it does not?

Partner

(State A)

PTE

(State B)

State A

Partner

(State A)

PTE

(State B)

State B

22

Ancillary Nexus Issue #2 – Throw-Back, Throw-Out, Joyce/Finnegan

• Considerations:

– No throwback in either case in states that attribute the activities of the PTE to the partner (e.g., the partner has nexus in the state)?

– No throwback only in Situation 1 because a partner can have nexus in the state by virtue of the PTE but a PTE cannot have nexus in a state by virtue of a partner?

– Does it matter if the state adopts Joyce or Finnegan? • In Joyce states, a PTE’s sales (Situation 2) may be subject to throwback despite the fact that the

partner has nexus because each entity’s factors are calculated independent of the others.

• Does it matter if the PTE can be an eligible “member” of a unitary group as opposed to just corporations being eligible members?

– What is the right answer from a policy perspective?

– Should you evaluate a “nexus” position to prevent throwback?

23

Ancillary Nexus Issue #3– PL 86-272

• Key Issue: – PL 86-272 generally precludes a state from imposing an income tax on an

entity whose activities within the state are limited to solicitation of sales of TPP and ancillary activities. Should the activities of an in-state PTE that exceed PL 86-272 subject the out-of-state partner to tax?

• Considerations: – Similar considerations as throw-back – who is the taxpayer?

– MA: if a foreign corporate partner is unitary with its in-state partnership, the activities of the partners are deemed to be the activities of the partner for determining whether the income if the partner is precluded under 86-272 (830 CMR 63.39.1(8)(a))

– Does PL 86-272 apply to the income derived from the PTE? Or does PL 86-272 apply to the corporate partner as the taxpayer under the corporate income tax?

24

Ancillary Nexus Issue #3– PL 86-272 • Example: Arizona Dept. of Rev. v. Central Newspapers (11/3/09):

• Holding: AZ may include Ponderay’s sales in the Partners’ sales factor numerator because the taxpayer is the Parent and its activities exceeded 86-272. 86-272 does not make certain income tax-exempt – it prevents a state from exercising taxing jurisdiction over a corporate partner.

Partners

Ponderay

• Partners = no AZ nexus; Parent has AZ nexus

• Ponderay = AZ nexus but protected by 86-272

• Parent elected to file as part of consolidated

AZ return, including Partners

• Agreement that Ponderay distributive share

was business income included in AZ return

• Issue: whether Ponderay’s sales are

excluded from the consolidated return sales

factor numerator on the basis of 86-272?

13.5%

Parent

25

Division of the Tax Base - Apportionment

26

• Key Question: – Once the partner is taxable and the amount and character of the PTE’s

tax base has been determined, what method is used to “divide” the partner’s tax base among the states to accomplish fair apportionment?

• Different Approaches:

1. Partner Level (Unitary) Method

2. Partnership Level (Non-Unitary) Method

3. Business/Nonbusiness Income Classifications

4. Methods for Special Issues

Central Tax Base Issue

ADVANCED MULTISTATE TAXATION OF PARTNERSHIPS AND INDIVIDUAL PARTNERS

ALLOCATION VS. APPORTIONMENT

AGGREGATE VS. ENTITY ISSUES

Ned Leiby

January 27, 2016

Multistate Taxation: Compliance & Planning Considerations

• How is FTE income taxed?

• Resident individual owners

• Nonresident individual owners

• Corporate owners

• Tiered FTE structures

• What states require filing of FTE tax returns?

― Individual and corporate owner filing

requirements/considerations

― Availability/Requirements for withholding/composites

28

Multistate Taxation: Compliance & Planning Considerations

• FTE may need to file and information return:

― With state in which it is organized

― With state(s) in which it does business

― With state(s) in which it derives income

― States in which it derives losses (no income) may not require the

filing of a tax return.

― Passive activity loss (NOL?) considerations:

― Is there a need to establish losses absent a state filing

requirement?

― Impact on carryovers and composite filings

― Disposition of assets/interest and any state gain recognition

― With states in which it has a resident owner

― Information only: No sourced income(loss)

29

30

Multistate Taxation: Compliance & Planning Considerations

Nexus Business/Nonbusiness

Determination Unitary vs Non-

unitary

Sourcing: Apportionment or

Allocation

Corp. / Individual

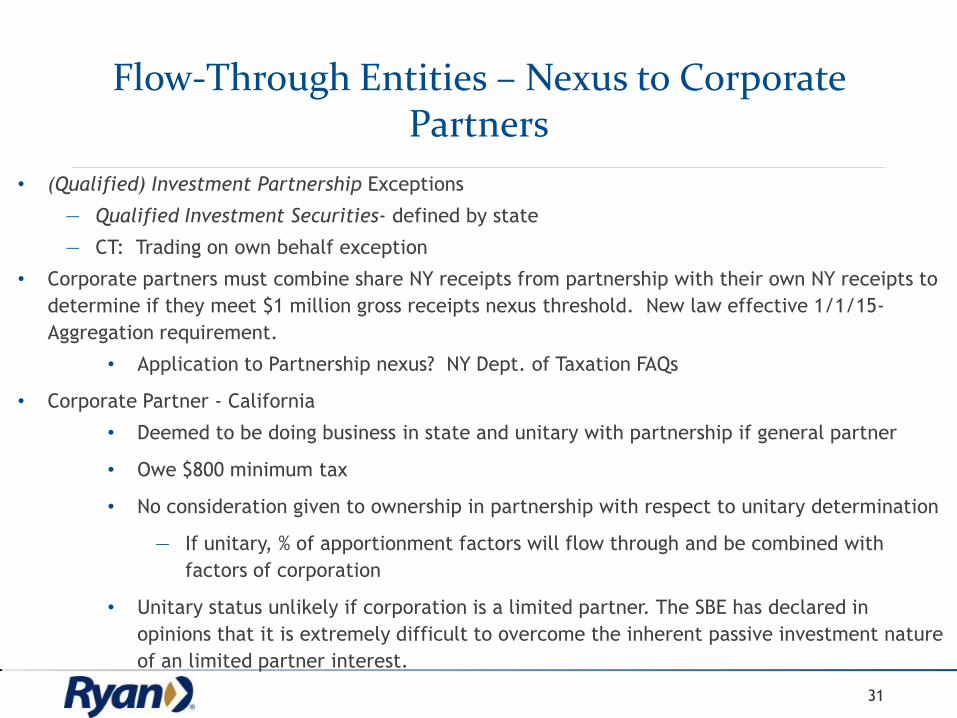

Flow-Through Entities – Nexus to Corporate Partners

• (Qualified) Investment Partnership Exceptions

― Qualified Investment Securities- defined by state

― CT: Trading on own behalf exception

• Corporate partners must combine share NY receipts from partnership with their own NY receipts to

determine if they meet $1 million gross receipts nexus threshold. New law effective 1/1/15-

Aggregation requirement.

• Application to Partnership nexus? NY Dept. of Taxation FAQs

• Corporate Partner - California

• Deemed to be doing business in state and unitary with partnership if general partner

• Owe $800 minimum tax

• No consideration given to ownership in partnership with respect to unitary determination

― If unitary, % of apportionment factors will flow through and be combined with

factors of corporation

• Unitary status unlikely if corporation is a limited partner. The SBE has declared in

opinions that it is extremely difficult to overcome the inherent passive investment nature

of an limited partner interest.

31

Nonresident Income From Investment Partnership

“Investment Partnership” Defined per state law; however, in

general:

• 90% of the cost of the total assets of the investment

partnership must consist of investment securities, bank or

financial institution deposits, office space and equipment

reasonably needed to carry on investment activities.

• 90% of its gross income must come from interest, dividends

and gains from sale or exchange of qualifying investment

securities.

32

State Non-Conformity with Federal Passive Activity Loss (“PAL”) Rules (IRC § 469)

• Most states piggy-back federal treatment

Exceptions

• California

― CA Form 3801

― Modifies § 469

― Definition of Passive Activities (Real Property Trade or Business

Professional)

― Calculation of loss on disposition

― Limitation amounts

― Differing basis considerations/tracking

• Maryland

― PALs are limited, based on ratio of loss calculated on federal Form 8582

33

State Non-Conformity with Federal Passive Activity Loss (“PAL”)Rules (IRC § 469)

Pennsylvania

• Income grouped into categories; however, net losses from one

category cannot offset income from different categories.

• Carryover of disallowed losses not allowed.

• Spouses may not offset one another’s income/losses

New Jersey

• Income grouped into categories; however, net losses for each group of

income is disallowed

• Carryover of disallowed losses not allowed

34

State Taxation of Nonresidents on Sales of Their Partnership Interests

• Note differences in implications for individual partners versus corporate

partners.

• Individual Income Tax Purposes

― Most states treat the gain as sale of an intangible thereby sourcing

the sale to state of domicile/residency.

― Some states require a nonresident to allocate nonbusiness gain based

on where partnership had activity.

• Nonresident-Sourced to California if the property has a business situs in

California

• Intangible property do not gain a California situs merely because of the

partnership conducts business in California

― Appeal of Ames, 87-SBE-042 ( SBE 6/17/87); Appeal of Bass, 89-

SBE -004 (SBE 1/29/89)

35

State Taxation of Nonresidents on Sales of Their Partnership Interests

• Corporate rules may differ. Implications for a corporate partner

largely depend on whether the gain arises from business income or

nonbusiness income.

― If the sale is considered nonbusiness, − the gain is typically

allocated to the state of commercial domicile. − several states,

including California, have rules to allocate the nonbusiness gain

based on the underlying partnership’s property or sales factors.

― If the sale is considered business income, then the gain is

included in the apportioned tax base.

― Many states have rules that would exclude the proceeds from the

sale of a partnership interest from the sales factor.

― California’s new market sourcing regulation includes the sale of

partnership interest in the sales factor based on the underlying

partnership’s factors.

36

California Sale of Partnership Interest Nonbusiness Income

• Corporate Tax Rules – Nonbusiness Income

― CRTC § 25125(d) provides for look through treatment on the sale of a

partnership interest held as a nonbusiness asset.

― If more than 50% of the underlying partnership’s assets consist of tangible

property, gain allocated to California based on the ratio of tangible property

in California to tangible property everywhere, determined at the time of sale.

― If more than 50% of underlying partnership’s assets consist of intangibles, gain

allocated to California based on the partnership’s prior year sales factor.

37

California Sale of Partnership Interest Business Income

• Corporate Tax Rules – Business Income

― Computing California Sales Factor − For sales after 1/1/2013, market sourcing

rules in CCR § 25136-2 provide for look through treatment for sale of

partnership and closely held corporations.

― If more than 50% of the underlying partnership’s assets consist of tangible

property, then proceeds are assigned to the numerator of the sales factor by

averaging the underlying partnership’s payroll and property factors.

― If more than 50% of underlying partnership’s assets consist of intangibles,

then proceeds are assigned to the numerator of the sales factor based on the

underlying partnership’s sales factor.

38

Special Rules: Sale of PTP Interests

• Some states have special allocation rules for sale of publicly-traded

limited partnership (“PTP”) interests.

• Implications for IRC § 751 (“hot assets”) income

• Implications for separate activity rules for PTPs

• Sourcing based on state apportionment factor

― IA

― ID

― OK

― MT

39

Michigan

• Flow-Through Entities

― Malpass v. Dept. of Treasury (2013)

― Multistate business income may be reported by

individuals through either the unitary or separate-entity

method

― Earlier case law held that the sole shareholder of an S

corp could not combine apportionment factors of unitary

S corps

40

Entity vs. Aggregate

Business/ Nonbusiness Determination

• For corporate partners is the business/nonbusiness income determination

made at the partnership level or partner level?

― Majority of states have not addressed

• Arizona & Illinois

― Requires partner level determination

― Arizona Corporation Tax Ruling No 94-2 (4/4/1994)

― Illinois Admin. Code tit. 86, §§ 100.3500(a)(3), 100.3500(b)(1)

• Alabama

― Requires partnership level determination. Alabama Supreme Court ruled

gain from the sale of partnership assets was not business income to the

corporate partners because such sales were not in the regular course of

the partnership’s trade or business.

41

42

Line 1, 2, 3 are

net income. These

amounts usually

are not be included

in partner’s

apportionment

factor- depending

on state and

partner’s

relationship with

partnership

P&L % may be

different than

capital %

PARTNER K-1

Business/Nonbusiness

Investment Partnership ?

43

Page 2: CA K-1

Differences between CA

And federal amounts

44

Page 3: CA K-1

Amounts should

match amount on

Form 592-B. CA

K-1 issued

whether or not

composite return

is filed. NOTE:

Separate Returns.

If estimates paid

with composite,

then likely no w/h.

Be Wary of Different Apportionment Rules/Special Industries

• Be aware of differences in apportionment factor methodology for

corporations and partnerships

― Some states adopt the corporate apportionment rules for determining

sourcing of nonresident partnership income

― States that use individual income sourcing rules have many gaps and the

sourcing guidance is out dated.

• Example : CT, NY, PA

― Corporation- Single Factor

― Partnership- Three Factor (Weighted)

― Attendant Nexus Considerations

― CT – Economic Nexus

45

Flow-Through Entities Apportionment and Corporate Partners

• Approaches used by states

• Partnership/Entity Level Approach- Corporate partner includes only

its share of the income/loss of pass through entity as apportioned by

the entity, but does not include its share of property, payroll and

sales.

― Should any K-1 line items be reflected in factor if business income ?

• Partner/Aggregate Level Approach = “Flow-up of factors”

― Corporate partners combine their percentage share of the pass-through

entity’s apportionment factors with their own apportionment factors

46

• California

― If partners are unitary with partnership, then partnership’s factors flow-up to the

unitary partner(s).

― If partner(s) are not unitary, then no flow-up

― If partner(s) and partnership are not unitary, but the income is considered

business income, then partners must apportion partnership income separately

from their other business income.

― California's regulation regarding the treatment of partnership income does not

distinguish between a limited and general partnership interest. Because

partnership law prohibits a limited partner from exercising a management role

with respect to a limited partnership, absent a unitary relationship between the

general and limited partner, unity between the limited partnership and its

limited partners on the basis of strong centralized management is

unlikely. However, combination may be a consideration if the partnership and the

limited partner share operational ties.

47

Entity vs. Aggregate Calculation of Apportionment Factor

Illinois: Five Different Apportionment Methods

Apportionment Issues

• Non-Unitary Partnership (No Factor Flow Up) − IITA Sec. 305 (a) and (b)

• Unitary Partnership (Factor Flow Up) − 86 Ill. Admin. Code 100.3380(d)

• Partnership Complete Member of Unitary Group

− 86 Ill. Admin. Code 100.3380(d)(4)

• Investment Partnership under General Rule − IITA Sec. 305(c-5)

• Investment Partnership Income Treated as Business Income − IITA Sec. 305(c-5)

48

Entity vs. Aggregate Calculation of Apportionment Factor

Illinois

• A partnership is required to use combined reporting when engaged in a unitary business with one of its

partners. If unitary, the partner's distributive share of the business income and apportionment factors of

the partnership must be included in that partner's business income and apportionment factors. If the

partner had no other activities in Illinois, the partner would apportion the sum of it income plus its share

of the partnership income to Illinois using the partnership Illinois sales factors and the partnership

everywhere sales factors. In determining the business income of the partnership, transactions between

the unitary partner, or members of its unitary business group, and the partnership are not eliminated.

However, all transactions between the unitary business group and the partnership are eliminated for

purposes of computing the apportionment factors of the partner and of any other member of the unitary

business group. Ill. Admin. Code tit. 86, § 100.3380(d). However, this rule does not apply:

― 1. to shares of income from partnerships whose business activity outside the United States is 80

percent or more of its total business activity;

― 2. where the partnership has a different apportionment method than the corporate partner; or

― 3. where the partnership is not in the same general line of business or a step in a vertically

structured enterprise with the corporate partner. Ill. Admin. Code tit. 86, § 100.3380(c).

49

Entity vs. Aggregate Calculation of Apportionment Factor

• Florida (Fla. Admin. Code Ann. r. 12C-1.015(10))

• Partnership factors flow through to the corporate partners

• Apportionment occurs at the partner level

• Compliance reporting considerations for tiered partnerships

• Massachusetts (Mass. Regs. Code tit. 830, § 63.38.1)

• Partnership factors flow through to corporate partners, if partnership

and corporate partners are engaged in “related business activities.” •

• If they are not engaged in related business activities, corporate

partners separately account for partnership income and apportion it

using only the partnership’s factors.

• If corporation owns less than 50% of LP, presumed not to be doing

business in Massachusetts, and apportionment is at partnership level

50

Entity vs. Aggregate Calculation of Apportionment Factor

• New Jersey (NJ Admin. Code tit.18, §18:7-7.6(g)(3))

• Partnership factors flow through to corporate partners, if the

partnership and partners are unitary

• If not unitary, apportion partnership income at the partnership level

and report distributive share of apportioned taxable income without

regard to the partners’ separate apportionment factors

• Note BIS, LP decision

― Interplay with w/h

• Oklahoma (Okla. Admin. Code §710:50-17- 51(15)(A))

• Partnership factors do not flow through to the corporate partners.

Income is apportioned at the partnership level and allocated to the

state by the corporate partners.

51

Illinois – Tiered Partnership Structure

• If a partnership and a partner are engaged in a unitary business and the partnership is a partner in a

second partnership, the partner's share of the first partnership's share of the base income apportioned

to Illinois by the second partnership must be included in the partner's Illinois net income. This

treatment applies if the partner is not engaged in a unitary business with the second partnership.

However, if the partner is engaged in a unitary business with the second partnership, the partner's

share of the first partnership's share of the business income and apportionment factors of the second

partnership must be included in the partner's business income and apportionment factors.

• If the partnership is a partner in a second partnership and one of its partners is engaged in a unitary

business with the second partnership, that partner must include in its business income and

apportionment factors its share of the partnership's share of the second partnership's business income

and apportionment factors. (See Example later in this deck)

• Generally, when a corporation's activities and its partnership's activities are not considered to be in a

unitary group, the partnership allocates its nonbusiness income and apportions its business income

which is then added to the corporation's other business income apportioned to Illinois

and nonbusiness income allocated to the state. The Illinois income is calculated at the partnership

level and merely reflects the partner's share of the partnership income as post–apportionment

income or loss.

52

Non-unitary Partnership Income Reporting

53

IL-1120:

Non-unitary

Partnership

Business

Income

54

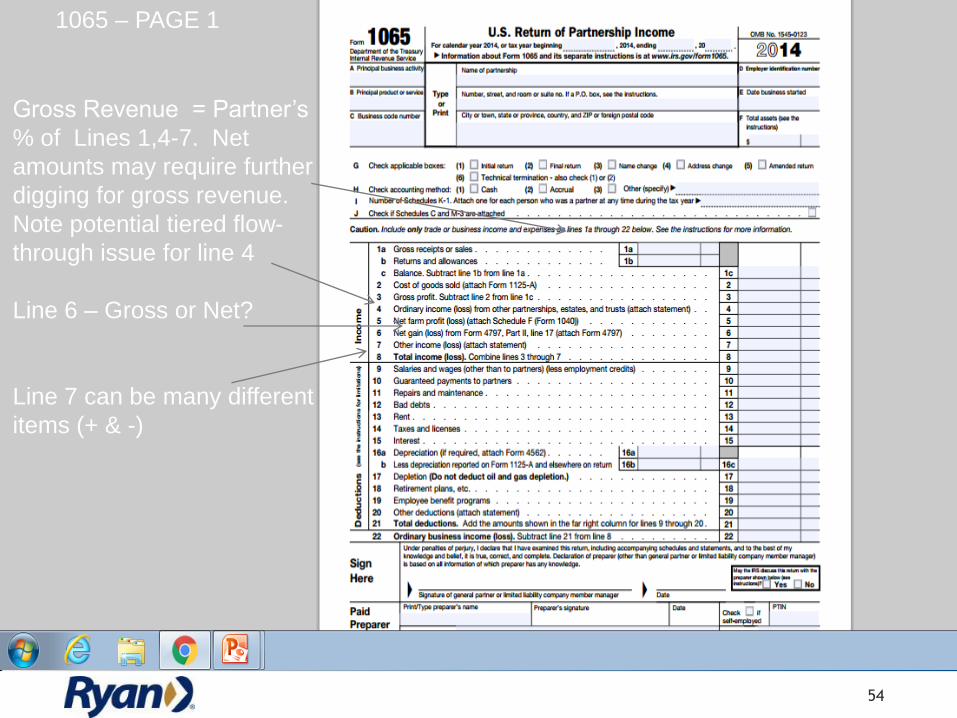

Gross Revenue = Partner’s

% of Lines 1,4-7. Net

amounts may require further

digging for gross revenue.

Note potential tiered flow-

through issue for line 4

Line 6 – Gross or Net?

Line 7 can be many different

items (+ & -)

1065 – PAGE 1

55

Make special note of items of

foreign income flowing through

as this may impact

apportionment.

SCHEDULE K

Entity vs. Aggregate Apportionment-Example

EXAMPLE

Orange Corp. operates exclusively in State A and generates $2,000,000 of taxable income.

It has total revenue of $5,000,000. Orange Corp. is also a general partner in Golden

Partnership owning 30% of capital and the same P&L%. Golden generated a taxable loss of

($1,000,000) on total revenue of $ 20,000,000 and operates in States B & C.

56

Golden Partnership

Orange Corp. (GP)

30%

Example: Flow-Through Apportionment

Orange Corp. Sales % Sales State Income (Loss)

State A $5,000,000 100% $2,000,000

State B $0 0% $0

State C $0 0% $0

Total $5,000,000 100% $2,000,000

57

Golden Partnership

Sales % Sales

State Income (Loss)

State A $0 0% $0

State B $15,000,000 75% ($ 750,000)

State C $ 5,000,000 25% ($ 250,000)

Total $20,000,000 100% ($1,000,000)

Example: Flow-Through Apportionment

Orange Corp. Direct Golden Line 28

Federal Taxable Income

$2,000,000 ($300,000) $1,700,000

58

Entity Only Scenario

State A $2,000,000

State B ($225,000)* (75% x $300,000)

State C ($ 75,000)* (25% x $300,000)

Total $1,700,000

* Sourced on State K-1 issued by Golden

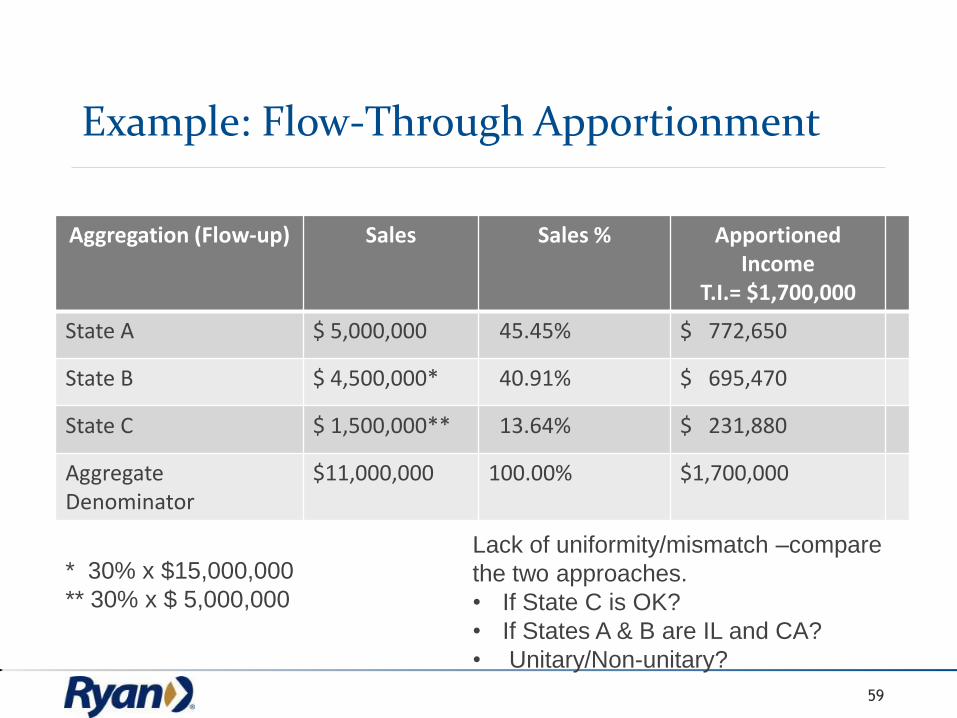

Example: Flow-Through Apportionment

Aggregation (Flow-up) Sales Sales % Apportioned Income

T.I.= $1,700,000

State A $ 5,000,000 45.45% $ 772,650

State B $ 4,500,000* 40.91% $ 695,470

State C $ 1,500,000** 13.64% $ 231,880

Aggregate Denominator

$11,000,000 100.00% $1,700,000

59

* 30% x $15,000,000

** 30% x $ 5,000,000

Lack of uniformity/mismatch –compare

the two approaches.

• If State C is OK?

• If States A & B are IL and CA?

• Unitary/Non-unitary?

Factor Flow-up and Tiered Partnership

Direct Factors from

OP, LLC use 25%

25%

60

20%

15%

Effective Rate = 20% + (15% * 25%)

= 20% + 3.75%

= 23.75%

OP, LP

OP, LLC

INC.

Factor Flow-up and Tiered Partnership

Impact of L.P. interest

on effective rate

calculation?

Can a limited

partner be unitary?

61

20%

L.P.

15%

G.P.

OP, LP

OP, LLC

INC. 25%

L.P.

Additional Considerations For Preparers of Returns

• What information to pass through to partners/investors.

• Does reporting through factor data to partners create confusion for partners

absent significant disclosure?

• Unitary determination must be made at partner level (or jointly with partnership –In

Practice?)

• What do tiered partnerships do?

• Does characterization of receipts of the partnership flow through to the partners?

Michigan – RAB 2015-5 states that receipts that flow through from the partnership that

are not “taxed” at the entity level (because they are protected by P. L. 86-272) are not

protected at the corporate partner level – Flow through receipts are from an investment,

and not from the sale of tangible property

• What percentages to use for performance fee allocations to G.P.s?

• Any impact of proposed regs. under IRC §707(a)(2)(A) (7/23/15)

• Treats certain partnership distributions as disguised payments for services

• Significant entrepreneurial risk requirement

62

Additional Considerations For Preparers of Returns

• Individual partner filing requirements by state

• Need for establishing loss carryovers/state buckets?

• PTPs treated as separate activities

• Receiving/passing through relevant data for estimates

• Asset Managers: Impact of 12/29/15 notice of change to text of proposed market-

based sourcing regulation (CCR § 25-136-2)

• Trends

― Expansion of w/h and composite requirements

― State level impact of new rules adopted by IRS for partnership audit

assessments ???

• Different state basis for partnership or assets?

― Depreciation non-conforming states

― Losses allowed/suspended

63

64

Thank You!

Ned Leiby

Ryan, LLC

www.ryan.com

65

• Key Issue: – In some states, if a “business/nonbusiness income” regime exists, and

the distributive share is determined to be nonbusiness income, such income is allocated to the appropriate state, instead of apportioned (e.g., to the state of domicile or other sourcing rules applicable to nonbusiness income).

• Considerations: – Do the allocation rules look to the partner or partnership? For

example, if dividend income is allocable to domicile, do you look to the partner’s or the partnership’s commercial domicile?

– What is the impact if it is non-business income as opposed to business income?

#3 – Business / Nonbusiness Issues

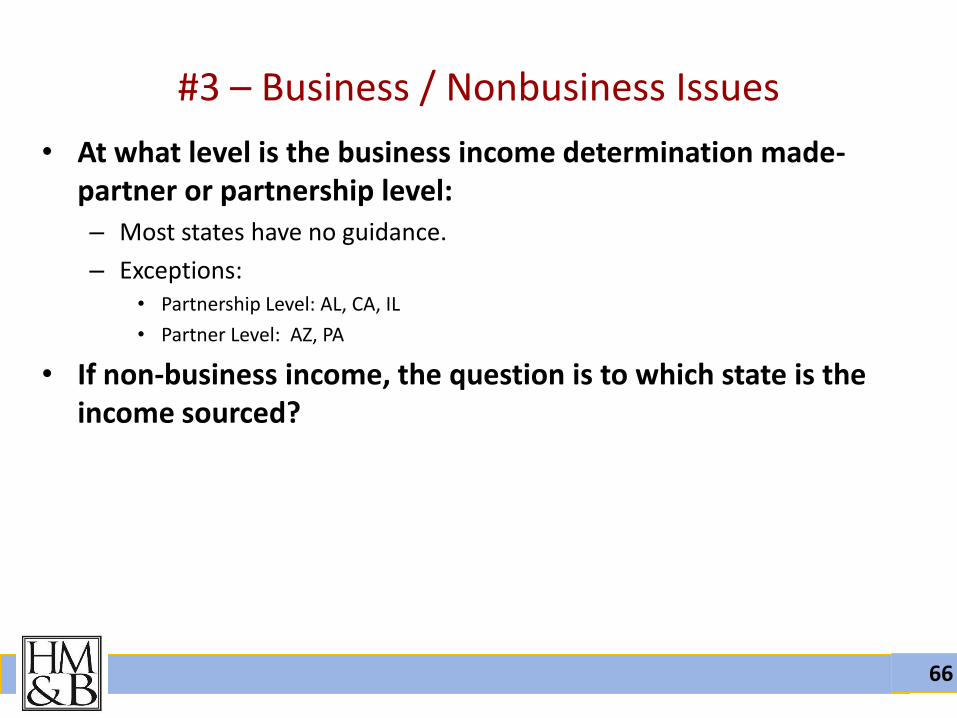

66

• At what level is the business income determination made- partner or partnership level: – Most states have no guidance.

– Exceptions: • Partnership Level: AL, CA, IL

• Partner Level: AZ, PA

• If non-business income, the question is to which state is the income sourced?

#3 – Business / Nonbusiness Issues

67

Business / Nonbusiness Example

• Net Income: $1,000,000

• Dividends: $500,000

• Retail: $500,000

Corporation A

• Limited Partner

• 40% Profits Interest / 40% Capital Interest

• Distributive Share: $400,000

• Business: Investment

Corporation A’s State Tax Return:

1. Assume retail is business income/apportionable

2. Assume dividends are nonbusiness income

allocable outside of state

4. Non-Unitary (LP/no control, 40% capital)

5. $250,000 state tax liability

• Retail: $150,000 ($200,000 x 75% appt)

• Dividends: $200,000 ($200,000 x 0%)

Liability may vary depending upon domicile rule!

A

PTE

68

(a) What problems exist with tiered partnerships? – Timing Issues / Withholding Regimes / Composite Returns

(b) Do the same sourcing rules apply if the partnership has individual partners instead of corporate? – Some states adopt the corporate apportionment rules for

determining sourcing of nonresident partnership income (e.g., MA)

– For those states that still apply individual income sourcing rules, many of the sourcing guidance remains vague and archaic

– Differences may include whether the sale is treated as a sale of an intangible or sale of tangible assets, and whether gain is source to situs of partnership

#4 – Special Issues

69

Business/Non-Business Income

70

Business v. Non-Business Income

• Transactional Test – Income arising from transactions and activity in

the regular course of the taxpayer's trade or business

• Functional Test – Includes income from tangible and intangible

property if the acquisition, management, and disposition of the property constitute integral parts of the taxpayer's regular trade or business operations

71

Transactional Test

• Identify transactions and activity occurring in the regular trade or business – Generally, all transactions that are dependent

upon or contribute to the operations

• Three standard tests: – Frequency and regularity of transactions

– Former business practices

– Subsequent use of proceeds (reinvestment or distribution)

72

Functional Test

• Identify whether the transaction is an integral part of the taxpayer’s trade or business

– Focus on whether property was used in trade or business

– Frequency is generally irrelevant

– In the case of a disposition of assets, state may look at whether the disposition itself is an integral part of the business operations (e.g., IA, AL, TN, NC, IL, PA)

73 73

74

Business v. Non-Business Income

• Minnesota

– Firstar Corp v. Commr. Rev.

– Capital gain from sale of office building was nonbusiness income

– Applied transactional test

• Infrequent: Taxpayer had not previously sold commercial property

• Subsequent use of proceeds: Not reinvested in the ongoing business operations – treated as dividend to shareholders

75

Business v. Non-Business Income

• California

– Jim Beam Brands Co v. FTB

• Gain from the sale of a unitary subsidiary is business income

• Applied functional test

• Gain was business income because the property while owned by taxpayer was used to produce business income

• Court rejected argument that disposition of property is not an integral part of the business

76

Business v. Non-Business Income

• Is business/non-business income determination made at:

– The partnership level?

– The partner level?

• Not much guidance; only a handful of states have addressed in public guidance

77

Compliance Headaches/ Withholding Requirements

78

• Key Issues: – The obligation of nonresident partners to file

returns and pay taxes in every state where a partnership does business creates an administrative nightmare for both state tax authorities, PTE management and partners

– Must a nonresident partner file returns in every state where a PTE does business?

– What method is required/optional – nonresident filing, withholding regime or composite filing?

Compliance / Administrative Issues

79

• General Rule: withholding at the source is generally required for PTEs with nonresident partners. – Typically pay at the highest individual or corporate tax rate (multiplied

by the owner’s distributive share of income attributable to the state)

• Typical Exemptions: – Partner provides an exemption certificate certifying it will file/pay tax

individually

– Partner is tax-exempt

– Partner files as part of a composite return

– PTE is a specialized entity (e.g., investment partnership)

– Partner is not a nonresident

Withholding Regimes

80 2014 State & Local Tax Webinar, AGN North America 80 80

81 2014 State & Local Tax Webinar, AGN North America 81 81

82

• Some states have threshold based on income or tax – May be applied to the entity or to a specific owner

– Ex. MI- Requires PTEs with Michigan-sourced business income of over $200,000 to withhold on behalf of owners that are PTEs or corporations

– Other states thresholds very low

• Some rates impose rate differentials that become complex with tiered structures – Lower tier may have to look to upper tier

– Ex. MI- requires withholding for both PTE and corporate owners at the full 6% corporate. If the PTE knows the ultimate owner of the upper-tier PTE is a non-resident individual, it may instead withhold at the individual rate, currently 4.25%.

Withholding Challenges

83

• In some states, withholding may not be compulsory – May depend on type of owner, i.e. trust, corproration

– May depend on type of PTE

– May exempt certain type of entities

• Sometimes voluntary at option of PTE and/or owners

• Also it may make sense to withhold – May eliminate need to disclose taxpayer sensitive information. .

Withholding Challenges

84

• Some states allow owners to explicitly elect out of withholding. – Waiver usually required

– May be perpetual or required to be renewed

– Keep part of books and records

– May need to provide to state

• Why elect not to withhold? – Owner has losses in state and no tax will be due

– Owner already making estimated tax payments

– Prefer to file composite return

Withholding Elections

85

• Under-report which results in penalties – Based on difference in tax rates between PTE and owner

• Tiered Entities- special risks – Withholding may be required by all levels and then there are

duplicative payments • In this situation may want to elect out.

– Run higher risk of under-reporting

– Attributable to differences in apportionment methodologies between the business and the owner

Withholding Risks

86

• Timing issues with estimated tax payments – Often quarterly payments but seasonal business.

• Under-report which results in penalties – Based on difference in tax rates between PTE and owner

• Tiered Entities- special risks – Withholding may be required by all levels and then there are

duplicative payments • In this situation may want to elect out.

– Run higher risk of under-reporting

– Attributable to differences in apportionment methodologies between the business and the owner

Withholding Risks

87

• Conflict between state reporting requirements and legal requirements for the PTE – Ex. S corporations

– Distributions made to owners must be made on a basis proportionate to ownership, otherwise the S-corporation runs the risk of inadvertent termination of its S-election under 2 scenarios:

• Owners are residents of multiple states and participation in withholding is limited to non-residents.. Disproportionate distributions can result in termination of the S-corporation election.

• When the PTE is owned by different types of entities under different withholding regime.

Withholding Risks

88

• Typical Conditions: – Requirement of an election/consent to participate is common (some

require consent to be submitted, some require it to be executed and available but not filed, some require an annual filing)

– Limitation of composite returns to individual partners (no corporate or PTE partners but some allow trust members to participate)

– Preclusion of composite returns if the partner has in-state income from other sources

– Agreement that PTE is authorized to resolve any audit/pay deficiency

Composite Regimes

89 2014 State & Local Tax Webinar, AGN North America 89 89

90

Why Is It a Nightmare?

• Lack of uniformity among withholding/composite regimes. Variations include:

– Composite return wherein nonresident consents to taxation

– Nonresident withholding required

– Estimated tax payments are required

– Withholding done but PTE remains contingently liable

• Thresholds of minimum distributions vary

• Lack of clear guidance and forms within each state

• Compliance software is often outdated

• Communication/documentation to/from partners not always timely

• Difficulties exist in how to account/report refunds and audit issues to partners

91

Why Is It a Nightmare?

• Complexities with multi-tiered structures as outlined herein

• PTE funding issues should be established for partner liabilities

• Transferee liability/management after PTE ceases operations

• Partners not subject to withholding or composite return must typically agree to submit to the jurisdiction of the state and agree to pay tax on the owner’s distributive share of PTE income

– Be careful – do you want to submit to the jurisdiction of the state? Do you have a choice?

92

Take-Aways

93

• Develop a “due diligence” checklist for all PTEs

• Establish multistate matrix addressing:

Significant jurisdictional/nexus rules

State method of dividing the tax base

Specialized issues (credits, throwback, etc.)

Required forms (withholding, etc.)

Specialized entity exemptions

• Confer with business development / legal teams on proper terms to include in entity agreements (reporting requirements, deadlines, information management, audit management)

SALT Department Tools

94

QUESTIONS?

THANK YOU!

Breen M. Schiller T: (312) 606-3220

Horwood Marcus & Berk Chartered 500 W. Madison Street, Suite 3700

Chicago, IL 60661 www.saltlawyers.com

Jennifer A. Zimmerman T: (312) 606-3247