Embed Size (px)

Citation preview

Red Gillen

Advanced Mobile Banking Defined

A Mobile-Centric Financial Institution (Jibun Bank) Case Study

August 2010

Content

3 Executive Summary5 Introduction6 In Mobile Banking, What Is “Advanced?”

15 Jibun Bank Overview23 Jibun Bank Offerings and Underlying Technical Systems34 Conclusion36 Leveraging Celent’s Expertise38 Related Celent Research

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 3

Executive Summary

In North America and the European Union, mobile banking has made great strides in the past three years. The largest of banks down to the smallest of credit unions now offer it. Originally offered as one modal-ity (i.e., text, mobile web, app), it is now commonly offered by financial institutions in all three modalities. Functionality that was considered innovative in 2007 has been commoditized. On a seemingly weekly basis, banks and technology vendors alike compete with each other to make announcements about offering the most advanced mobile bank-ing services.

But what truly is the definition of “advanced” mobile banking in 2010?

The answer depends on what side of mobile banking one examines. In terms of front end, customer-facing functionality in North America and the EU, state-of-the-art features include mobile remote deposit capture, person-to-person payments, and real time transactional alerts. Although mobile payments are beginning to emerge, they are limited to pilots, with years to go before commercial rollout.

On the back end, the definition of advanced systems configuration is connectivity between the mobile front end and multiple core and ancillary systems. This allows bank customers to have a view of all their accounts, such as checking, savings, loans, mortgages, credit cards, etc.

However, this definition will need to change if banks are to fully lever-age the mobile channel and its use cases. The problem with current “advanced” back end systems configuration is that it is largely static; it either waits for the bank customer to interact with it (e.g., balance inquiry), or it presents data that is the same as in any other channel (e.g., online, ATM). To be truly advanced, back end systems must be configured in a dynamic way that no other bank channel can mimic and that leads to beneficial changes in customer behavior or the use of a new bank product. Ultimately, these customer behavior changes or new product usage must lead to either reduced bank costs or increased bank revenues.

To do so, core and ancillary back end systems must be configured in a way that intelligently and seamlessly navigates customers among them. For example, upon a large check being cleared, DDA and check-

4 Copyright 2010 © Celent, a division of Oliver Wyman, Inc.

ing imaging systems would work in concert to send a real time transaction mobile alert to a bank customer, with a link to the check image. This alert would ask the customer to text back “N” if she does not recognize the transaction. Should the customer do so, the intelli-gence would exist to forward the information to a CRM system, which would in turn initiate a customer service call.

In Celent’s view, this is what advanced mobile banking looks like. Unfortunately, most North American and EU banks’ systems do not orchestrate like this today. To find an excellent example of advanced mobile banking, one must turn to Japan, a historically advanced mar-ket in terms of mobile services.

A meaningful case study is that of Jibun Bank, a mobile-centric bank with the right pedigree; it is owned by a financial institution (the Bank of Tokyo Mitsubishi UFJ) and a mobile carrier (KDDI). Jibun Bank offers a number of mobile front end features (e.g., ATM lock) that would be the envy of any North American or European bank. However, what makes Jibun Bank’s offering especially amazing is that it also offers new products (account opening, loan origination, FX transactions) with direct revenue impact, entirely within the mobile channel.

These key products would in no way be possible if Jibun Bank’s back end systems did not work in a collaborative manner. In the case of mobile account opening alone, AML, KYC, CIF, transactional account, card processing, and CRM systems are integrated with each other. Jibun Bank was able to accomplish its offerings through the use of both Oracle’s FLEXCUBE banking platforms and a series of business alliances.

Jibun Bank provides a map toward truly advanced mobile banking. If North American and European banks are to offer mobile banking with the ability to either change customer behavior or sell-in new products, the Jibun Bank lesson is clear; banks must move away from their cur-rent siloed configurations, whose only ability to fuse back end systems is to present data within a front end user interface.

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 5

Introduction

The catalyst for this report was the submission of Jibun Bank as a 2010 Celent Model Bank Award nominee. Upon examination of Jibun Bank’s use of innovative technology and a comparison with other banks’ nom-inations, it became obvious to Celent that it had found an intriguing award candidate. Jibun Bank’s multichannel approach was fantastically unique and earned it one of Celent’s Model Bank Awards.

Although Jibun Bank was featured in the report Celent Model Bank 2010: Case Studies of Effective Technology Usage in Banking, May 2010, the description was too short to provide an in-depth understanding of its offerings. Because of this, Celent decided to dedicate an entire report to Jibun Bank, mapped against the context of mobile banking capabilities currently found in North America and Europe.

Celent analysts spent a week in Japan, conducting Japanese-language primary research with Jibun Bank executive management, product management, and IT management. In addition, Celent conducted interviews with Jibun Bank’s two corporate shareholders: the Bank of Tokyo Mitsubishi UFJ and KDDI.

This report is divided into three sections. The first section takes a broad look at the current state of mobile banking technology in North America. In particular, this section aims to define what constitutes the current definition of advanced mobile banking. The second section provides an overview of Jibun Bank, including its history, customer seg-ments, and performance. The third section provides a detailed look at Jibun Bank’s feature functionalities, with a close examination of the bank’s stand-out functionalities: mobile account opening and mobile loan origination. This report ends with an overview of Jibun Bank’s selection of Oracle’s FLEXCUBE product as its core banking system.

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 6

In Mobile Banking, What Is “Advanced?”

Every week in North America, there seems to be one press release or another, from either a financial institution (FI) or a vendor, touting advanced mobile banking technology. However, the term “advanced” is a relative one; is the technology advanced compared to the FI's existing technology? Is it advanced when matched against domestic competi-tors’ technology? Or is this technology truly a world class leader?

To create a meaningful context for comparing Jibun Bank to its North American counterparts, the following section will briefly examine the status of mobile banking technology in North America as of the second quarter of 2010. Technology will be examined from both the front end feature functionality and back end integration perspectives.

Advanced Mobile Front End TechnologyIn the US, mobile banking is generally viewed to have become a reality in 2007, when major banks such as Bank of America, JPMorgan Chase, and Wells Fargo started offering mobile functionality. This functional-ity has generally fallen into one of two major categories: informational services and money movement. With the growing adoption of smart phones (e.g., phones with large screens and QWERTY keyboards, and often employing Android, Blackberry, iPhone, or Windows operating systems), mobile devices have gradually moved from being used for voice-centric use cases to mobile-centric use cases. This, in turn, has led to the ongoing advancement of mobile banking features.

In 2007, given that mobile banking in general was new, any functional-ity was considered advanced. Most functionalities being made available for the first time then consisted of the following informa-tional services, the main exception being account-to-account (A2A) transfers:

Balance inquiry

Transaction history

ATM/branch location lookup

A2A intrabank transfers

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 7

Although considered advanced just three years ago, the above func-tionalities have become commoditized table stakes in 2010; it is now assumed that any FI with a passable mobile banking offering provides these features.

In 2008, many FIs innovated by adding money movement functionality to their mobile banking services. More specifically, FIs began offering mobile versions of online bill pay, including the ability to pay individ-ual payees with US mailing addresses. Just as is the case with online bill pay, mobile bill pay leverages the ACH funds transfer networks, which requires a two-day to four-day settlement period. Notably and almost without exception, mobile bill pay does not allow users to set up payees; rather, this typically is still done via the online bill channel. Nonetheless, mobile bill pay has become a common feature, and in 2010 would hardly be considered advanced.

By 2009, FIs such as USAA (and a couple of credit unions) pushed money movement advanced functionality to a new level by offering mobile remote deposit capture (RDC). In July 2010, MChase announced its own mobile RDC product. However, as of the writing of this report, no other major US bank has made this service commercially available; as such, mobile remote deposit capture arguably retains its advanced status.

Innovation has taken place in 2010 in both the informational services and money movement categories. On the informational side, real time transactional alerts (e.g., bank customers receiving text alerts within seconds of payment cards being used) are being increasingly rolled out. On the money movement side, person-to-person (P2P) payments (i.e., using only recipients’ mobile phone numbers or email addresses for funds transfer routing purposes) are some of the newest mobile bank-ing features to be commercially rolled out.

New mobile banking registration methods have also arrived in 2010. Although using the mobile channel to sign up for mobile banking intu-itively makes sense, the simple truth is that most mobile banking registration currently takes place via the online channel. However, a small number of banks such as Key Bank and Wells Fargo have recently begun to offer mobile-based registration for mobile banking,1 which enables “offline” (non-Internet) mobile phone customers to enjoy the features of electronic banking.

1. Wells Fargo uses mobile browsers and ATMs for registration, Key Bank uses call centers for registration.

8 Copyright 2010 © Celent, a division of Oliver Wyman, Inc.

As can be seen in Figure 1 on page 8, innovative mobile banking prod-ucts and services are inherently less available than older, less innovative offerings.

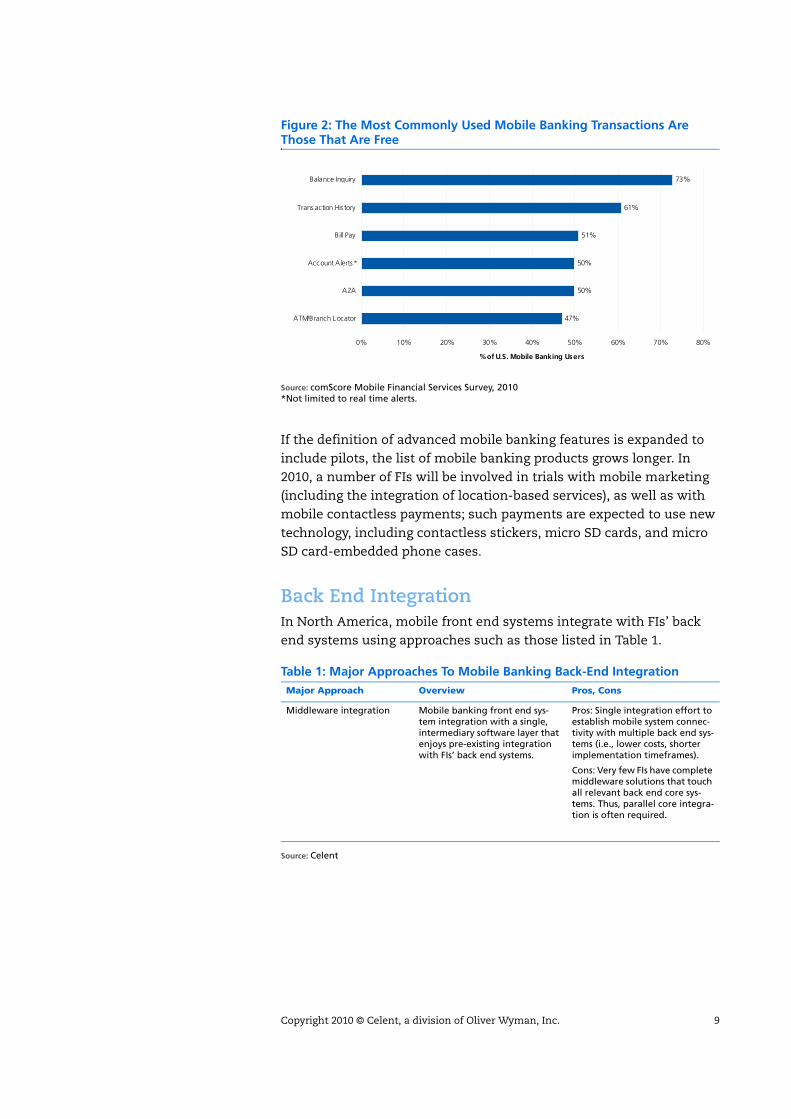

Based on Celent interviews, press releases, and industry information, it appears that innovation during the rest of 2010 and first half of 2011 will be marked by more of the same; i.e., more widespread commercial rollout of mobile RDC, P2P payments, and real time transaction alerts. An important fact to point out is that almost all mobile banking trans-actions depicted in Figure 1 do not result in any direct revenue for FIs. The only exception is P2P, which some banks are starting to offer; for example, in Canada, mobile versions of Interac email money transfers have a fee of CDN $1.50. However, as depicted in Figure 2, P2P is not even registering in mobile banking usage surveys, implying that FIs are not making significant direct revenue from mobile banking.

Figure 1: As Is Typically the Case, Innovation Lags Commercial Availability

Source: Celent, based on research of top 15 North American banks (top 10 US banks, top five Canadian banks)

0

2

4

6

8

10

12

Balan

c e Inqu

iry

T xn H

istory

A2A

ATM/B

ranch

L ocato

r

Bill P ay

Mul

ti-Acc

ount A

c ces s

Real-Tim

e Car

d T xn

Aler

tsP2P

Mobile

Re gistra

tion

Mob

ile R

DC

NF C Pay

ment

s

# o

f F

Is

2009/10 Commercial Launch

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 9

If the definition of advanced mobile banking features is expanded to include pilots, the list of mobile banking products grows longer. In 2010, a number of FIs will be involved in trials with mobile marketing (including the integration of location-based services), as well as with mobile contactless payments; such payments are expected to use new technology, including contactless stickers, micro SD cards, and micro SD card-embedded phone cases.

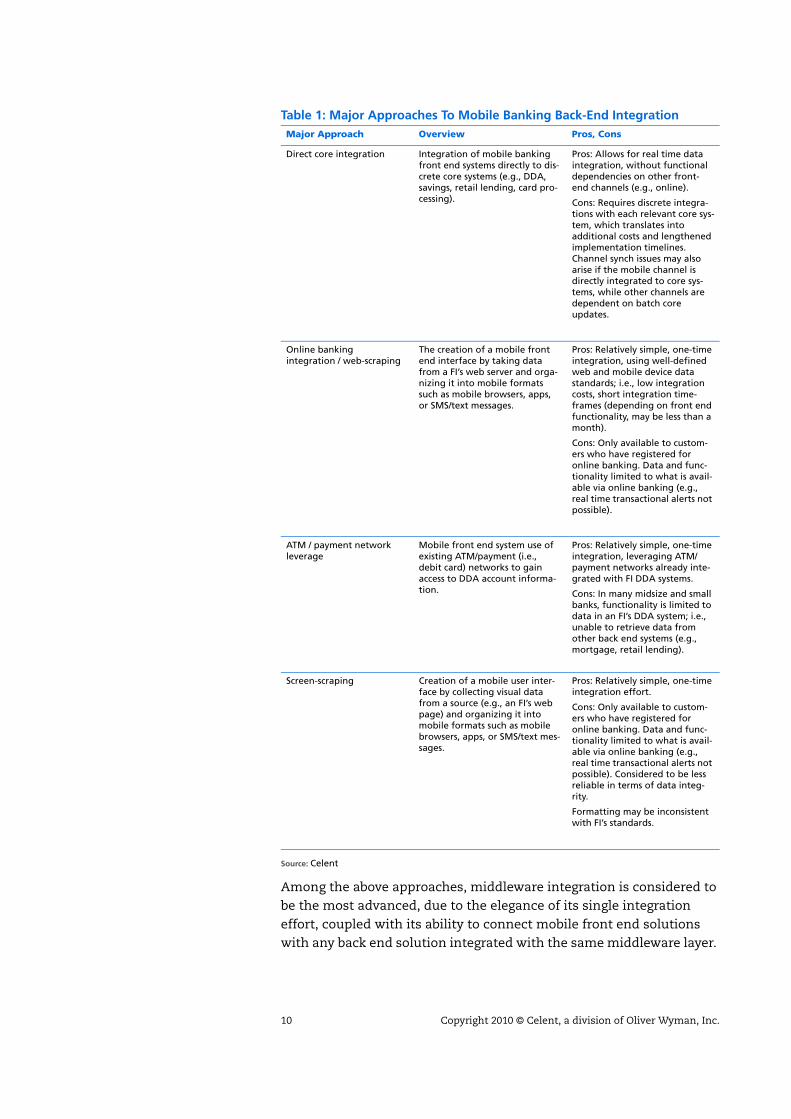

Back End IntegrationIn North America, mobile front end systems integrate with FIs’ back end systems using approaches such as those listed in Table 1.

Figure 2: The Most Commonly Used Mobile Banking Transactions Are Those That Are Free

Source: comScore Mobile Financial Services Survey, 2010*Not limited to real time alerts.

Table 1: Major Approaches To Mobile Banking Back-End IntegrationMajor Approach Overview Pros, Cons

Middleware integration Mobile banking front end sys-tem integration with a single, intermediary software layer that enjoys pre-existing integration with FIs’ back end systems.

Pros: Single integration effort to establish mobile system connec-tivity with multiple back end sys-tems (i.e., lower costs, shorter implementation timeframes).

Cons: Very few FIs have complete middleware solutions that touch all relevant back end core sys-tems. Thus, parallel core integra-tion is often required.

Source: Celent

47%

50%

50%

51%

61%

73%

0% 10% 20% 30% 40% 50% 60% 70% 80%

ATM/Branch Locator

A2A

Account Alerts*

Bill Pay

Trans action His tory

Balance Inquiry

% of U.S. Mobile Banking Users

10 Copyright 2010 © Celent, a division of Oliver Wyman, Inc.

Among the above approaches, middleware integration is considered to be the most advanced, due to the elegance of its single integration effort, coupled with its ability to connect mobile front end solutions with any back end solution integrated with the same middleware layer.

Direct core integration Integration of mobile banking front end systems directly to dis-crete core systems (e.g., DDA, savings, retail lending, card pro-cessing).

Pros: Allows for real time data integration, without functional dependencies on other front-end channels (e.g., online).

Cons: Requires discrete integra-tions with each relevant core sys-tem, which translates into additional costs and lengthened implementation timelines. Channel synch issues may also arise if the mobile channel is directly integrated to core sys-tems, while other channels are dependent on batch core updates.

Online banking integration / web-scraping

The creation of a mobile front end interface by taking data from a FI’s web server and orga-nizing it into mobile formats such as mobile browsers, apps, or SMS/text messages.

Pros: Relatively simple, one-time integration, using well-defined web and mobile device data standards; i.e., low integration costs, short integration time-frames (depending on front end functionality, may be less than a month).

Cons: Only available to custom-ers who have registered for online banking. Data and func-tionality limited to what is avail-able via online banking (e.g., real time transactional alerts not possible).

ATM / payment network leverage

Mobile front end system use of existing ATM/payment (i.e., debit card) networks to gain access to DDA account informa-tion.

Pros: Relatively simple, one-time integration, leveraging ATM/payment networks already inte-grated with FI DDA systems.

Cons: In many midsize and small banks, functionality is limited to data in an FI’s DDA system; i.e., unable to retrieve data from other back end systems (e.g., mortgage, retail lending).

Screen-scraping Creation of a mobile user inter-face by collecting visual data from a source (e.g., an FI’s web page) and organizing it into mobile formats such as mobile browsers, apps, or SMS/text mes-sages.

Pros: Relatively simple, one-timeintegration effort.

Cons: Only available to custom-ers who have registered for online banking. Data and func-tionality limited to what is avail-able via online banking (e.g., real time transactional alerts not possible). Considered to be less reliable in terms of data integ-rity.

Formatting may be inconsistent with FI’s standards.

Table 1: Major Approaches To Mobile Banking Back-End IntegrationMajor Approach Overview Pros, Cons

Source: Celent

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 11

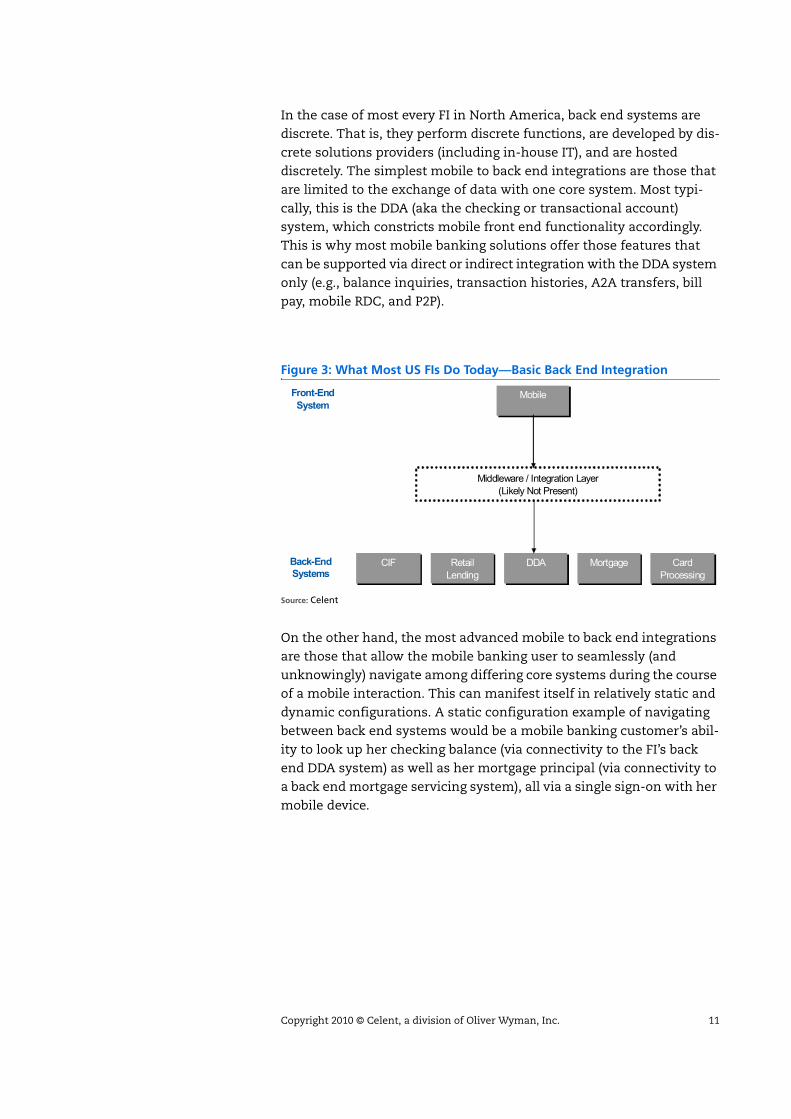

In the case of most every FI in North America, back end systems are discrete. That is, they perform discrete functions, are developed by dis-crete solutions providers (including in-house IT), and are hosted discretely. The simplest mobile to back end integrations are those that are limited to the exchange of data with one core system. Most typi-cally, this is the DDA (aka the checking or transactional account) system, which constricts mobile front end functionality accordingly. This is why most mobile banking solutions offer those features that can be supported via direct or indirect integration with the DDA system only (e.g., balance inquiries, transaction histories, A2A transfers, bill pay, mobile RDC, and P2P).

On the other hand, the most advanced mobile to back end integrations are those that allow the mobile banking user to seamlessly (and unknowingly) navigate among differing core systems during the course of a mobile interaction. This can manifest itself in relatively static and dynamic configurations. A static configuration example of navigating between back end systems would be a mobile banking customer’s abil-ity to look up her checking balance (via connectivity to the FI’s back end DDA system) as well as her mortgage principal (via connectivity to a back end mortgage servicing system), all via a single sign-on with her mobile device.

Figure 3: What Most US FIs Do Today—Basic Back End Integration

Source: Celent

Front-EndSystem

Back-EndSystems

CIFCIF Retail LendingRetail

LendingDDADDA

Middleware / Integration Layer(Likely Not Present)

MobileMobile

Card Processing

Card Processing

MortgageMortgage

12 Copyright 2010 © Celent, a division of Oliver Wyman, Inc.

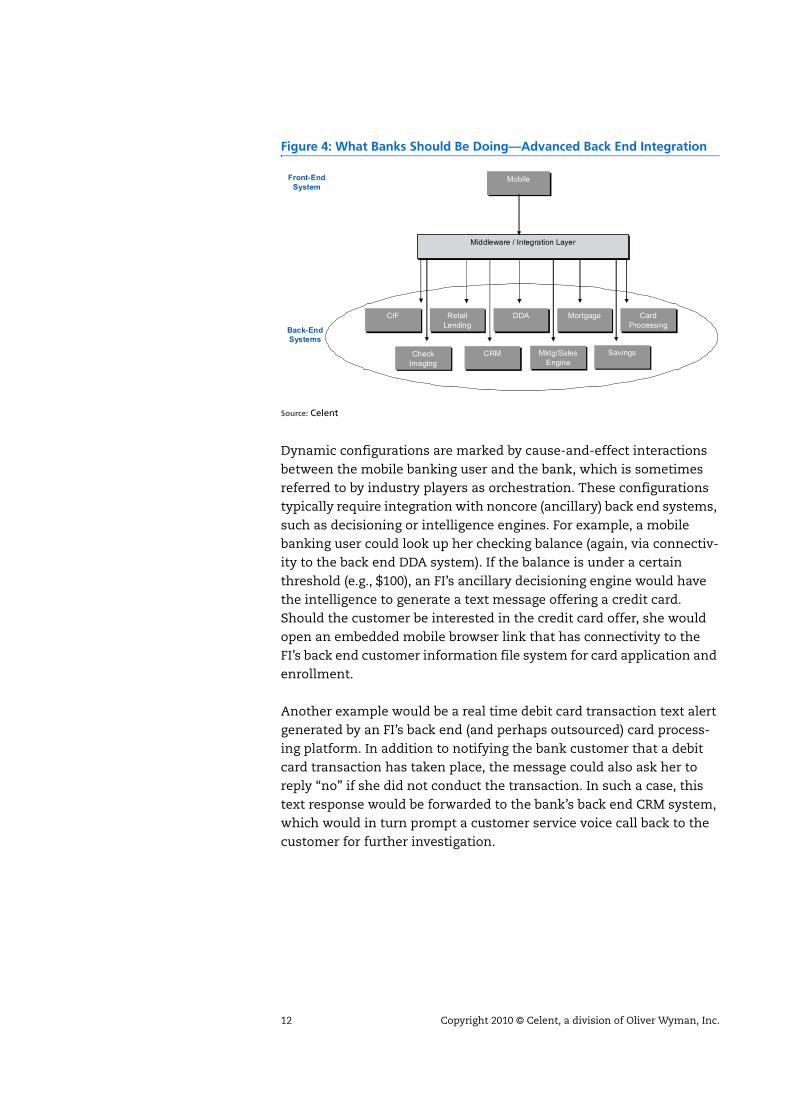

Dynamic configurations are marked by cause-and-effect interactions between the mobile banking user and the bank, which is sometimes referred to by industry players as orchestration. These configurations typically require integration with noncore (ancillary) back end systems, such as decisioning or intelligence engines. For example, a mobile banking user could look up her checking balance (again, via connectiv-ity to the back end DDA system). If the balance is under a certain threshold (e.g., $100), an FI’s ancillary decisioning engine would have the intelligence to generate a text message offering a credit card. Should the customer be interested in the credit card offer, she would open an embedded mobile browser link that has connectivity to the FI’s back end customer information file system for card application and enrollment.

Another example would be a real time debit card transaction text alert generated by an FI’s back end (and perhaps outsourced) card process-ing platform. In addition to notifying the bank customer that a debit card transaction has taken place, the message could also ask her to reply “no” if she did not conduct the transaction. In such a case, this text response would be forwarded to the bank’s back end CRM system, which would in turn prompt a customer service voice call back to the customer for further investigation.

Figure 4: What Banks Should Be Doing—Advanced Back End Integration

Source: Celent

Front-EndSystem

Back-EndSystems

CIFCIF Retail LendingRetail

LendingDDADDA

Middleware / Integration LayerMiddleware / Integration Layer

MobileMobile

Card Processing

Card Processing

MortgageMortgage

CheckImagingCheck

ImagingCRMCRM Mktg/Sales

EngineMktg/Sales

EngineSavingsSavings

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 13

Advanced Back End Integration ExamplesAdvanced back end integration, although relatively rare, is beginning to take hold in North American markets. This section briefly lists exam-ples of relatively advanced, commercially available mobile banking technology at top US FIs.

Bank of America: America’s largest retail FI (in terms of retail deposits) allows its customers to look at checking, savings, and credit card accounts, which requires integration across multiple core back end systems.

Chase: The retail mobile banking solution offered by Chase Bank allows customers to see checking, savings, credit card, home equity, auto, and mortgage accounts. Furthermore, the Chase solution allows retail customers to transfer funds between these accounts, which entails integration with the related, multiple core back end systems. Chase’s mobile RDC also integrates check imaging systems with the DDA system.

CIBC: In Canada, CIBC allows for funds transfers among deposit, Visa, and line of credit accounts. This requires inte-gration across DDA, retail lending, and credit card processing back end systems.

Citibank: Like Chase, Citibank offers its customers access to multiple accounts, including checking, savings, credit card, mortgage, home equity line or loan, and personal line or loan accounts. Citi also mirrors Chase in offering its customers the ability to transfer funds between these accounts, thus requiring integration with multiple back end systems. Addi-tionally, Citi enables iPhone users to access their Thank You loyalty points accounts, presumably supported by a noncore back end system.

TD Banking Financial Group (TD): TD in Canada offers another example of mobile banking with integration to mul-tiple, core back end systems, including those that support checking, savings, investment, credit card, and credit line (e.g., mortgage) accounts. Given TD’s wealth management and insurance lines of business, the same app that is used for mobile banking also offers features such as (voice-based) trading and insurance claim data capture.

USAA: As of the writing of this report, USAA may have one of the most advance mobile banking offerings, which includes not only visibility into multiple accounts but mobile remote deposit capture as well. Of particular note is USAA’s “Auto Circle” product, which offers mobile-base auto shopping

14 Copyright 2010 © Celent, a division of Oliver Wyman, Inc.

tools and loan origination. It is the first of its kind in the nation and requires significant coordination among various back end systems.

US Bank: Like many of the other FIs in this section, US Bank allows its retail customers to access most of the accounts that are accessible via online banking, including checking accounts, savings, credit cards, and other loans and lines of credit. In doing so, US Bank has integrated its mobile banking solution with numerous core, back end systems.

Wells Fargo: Wells Fargo also allows its retail customers to view multiple accounts (including small business accounts) through its mobile solution. One of Wells’ relatively unique offerings is its CEO Mobile service, which enables corporate clients to view their corporate accounts, as well as initiate/approve/reject wire payments; combined, these features also require multiple, core back end system integration.

It is important to note that the above examples of integration with multiple, core back end systems are of the static rather than the dynamic variety. That is to say, whereas these mobile banking solu-tions enable customers to use a single interface to access data stored in differing back end systems, they do not direct customers from one sys-tem to another as part of an intelligent decisioning or orchestration process. From an orchestration perspective, what is largely missing is the ability to offer customers contextually meaningful products (e.g., lines of credit, overdraft protection, customer service calls) and then enable enrollment in those products, all within the confines of the mobile channel.

In some use cases, orchestration need not be terribly complex; i.e., it can be enabled via integration to a single core back end system. For example, if a low checking account balance text alert is generated by a DDA system, a value-added orchestration would be the ability to ask the customer if she wants to transfer money from a savings account (and to process her response) within the same DDA system. Yet, this is indeed a rare feature. It would thus appear that in mid-2010, the ability to offer contextually meaningful products and services demarcates advanced from mature mobile banking technologies.

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 15

Jibun Bank Overview

Formation and Business ApproachThe previous sections described the features and functionalities which currently define advanced mobile banking. However, there are less than a handful of banks in the world that surpass this definition. Jibun Bank, a mobile-centric bank in Japan, is one of them.

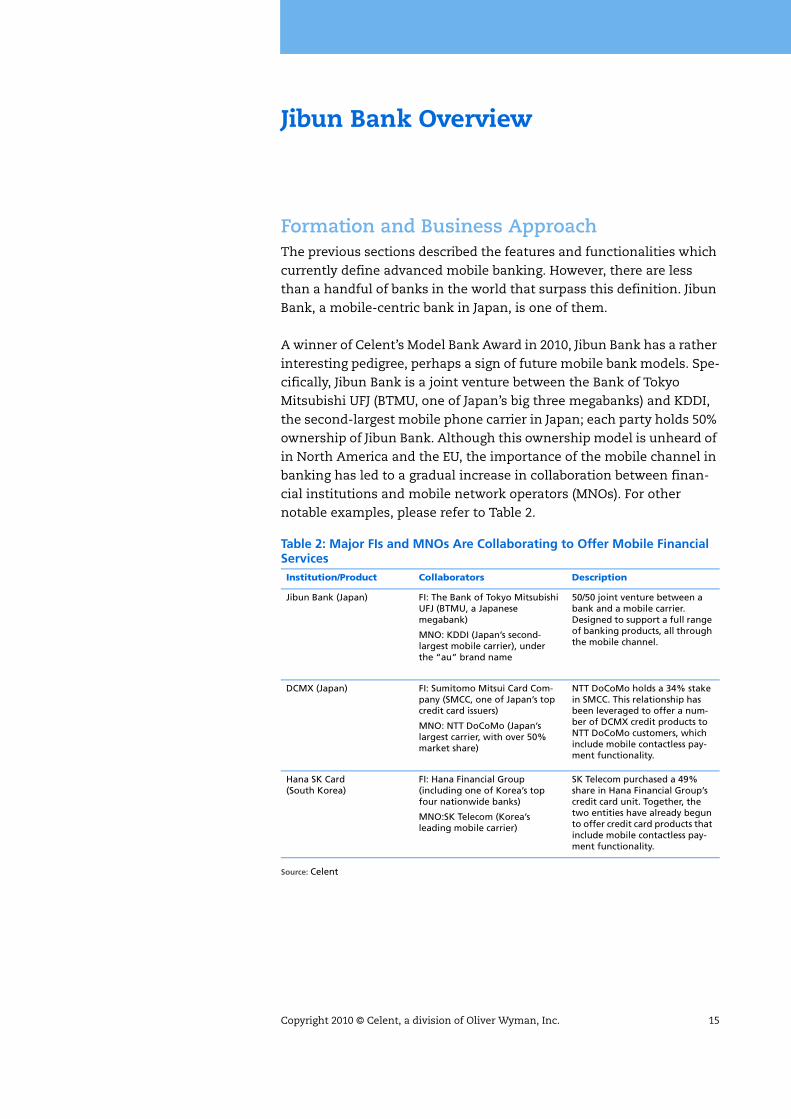

A winner of Celent’s Model Bank Award in 2010, Jibun Bank has a rather interesting pedigree, perhaps a sign of future mobile bank models. Spe-cifically, Jibun Bank is a joint venture between the Bank of Tokyo Mitsubishi UFJ (BTMU, one of Japan’s big three megabanks) and KDDI, the second-largest mobile phone carrier in Japan; each party holds 50% ownership of Jibun Bank. Although this ownership model is unheard of in North America and the EU, the importance of the mobile channel in banking has led to a gradual increase in collaboration between finan-cial institutions and mobile network operators (MNOs). For other notable examples, please refer to Table 2.

Table 2: Major FIs and MNOs Are Collaborating to Offer Mobile Financial ServicesInstitution/Product Collaborators Description

Jibun Bank (Japan) FI: The Bank of Tokyo Mitsubishi UFJ (BTMU, a Japanese megabank)

MNO: KDDI (Japan’s second- largest mobile carrier), under the “au” brand name

50/50 joint venture between a bank and a mobile carrier. Designed to support a full range of banking products, all through the mobile channel.

DCMX (Japan) FI: Sumitomo Mitsui Card Com-pany (SMCC, one of Japan’s top credit card issuers)

MNO: NTT DoCoMo (Japan’s largest carrier, with over 50% market share)

NTT DoCoMo holds a 34% stake in SMCC. This relationship has been leveraged to offer a num-ber of DCMX credit products to NTT DoCoMo customers, which include mobile contactless pay-ment functionality.

Hana SK Card (South Korea)

FI: Hana Financial Group (including one of Korea’s top four nationwide banks)

MNO:SK Telecom (Korea’s leading mobile carrier)

SK Telecom purchased a 49% share in Hana Financial Group’s credit card unit. Together, the two entities have already begun to offer credit card products that include mobile contactless pay-ment functionality.

Source: Celent

16 Copyright 2010 © Celent, a division of Oliver Wyman, Inc.

In Jibun Bank’s case, the principal collaborators had complementary rationales for starting a new, mobile-centric bank:

The Bank of Tokyo Mitsubishi UFJ (BTMU): For years, BTMU held a very clear view that its relationships with younger customers was increasingly becoming weaker compared to relationships with older generations who make branch visits or transact based on corporate relationships. As branch and corporate transactions are not considered effective commu-nication channels for younger customers, BTMU was concerned about relying on these channels; less touch points would make it difficult to migrate these customers into mainstream mortgage or wealth management customers. Given this, BTMU recognized the need to increase its younger customer base and ways to interact with it. With the advanced state of mobile technology and adoption in Japan, the bank realized that a key success factors to attract such younger customers was to meet their mobile lifestyle needs.

At the same time, BTMU realized that its existing front- and back-end systems were of such scale and of such cross-inte-gration that they could not be changed quickly enough to offer attractive mobile banking services and products for

BanKO (Philippines) FI: Bank of the Philippine Islands (BPI, the oldest and third-largest bank in The Philippines)

MNO: Globe Telecom (second-largest mobile carrier in The Philippines)

Both BPI and Globe are subsid-iaries of Ayala Corporation. Globe Telecom has been offering its G-CASH mobile payment ser-vice since 2007. Collaboration with BPI will allow for mobile-based microfinance transactions.

Yet unnamed (South Korea) FI: BC Card (Korea’s largest credit card company)

MNO: KT (Korea’s second-largest mobile carrier)

It has been widely reported that KT is looking to buy a control-ling stake in BC Card, to emulate the Hana SK Card model. Final ownership terms have not yet been disclosed.

MTN Banking (South Africa) FI: Standard Bank

MNO: MTN

A joint venture between an FI and an MNO, MTN Banking is mobile-centric, allowing depos-its via cash loads (at retailers) and salary disbursements. Funds access is through a MasterCard-branded payment card or P2P payments.

Table 2: Major FIs and MNOs Are Collaborating to Offer Mobile Financial ServicesInstitution/Product Collaborators Description

Source: Celent

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 17

young mobile users. Simply creating a mobile version of BTMU’s online banking services was not an attractive option—many potential younger customers do not have computers at home, and cannot easily use work computers for personal reasons. Furthermore, given the busy lifestyles of younger consumers, bank branches were not considered a viable, support channel. In other words, the mobile channel had to be developed in a way that would obviate the need for other channels. Not being able to do this on its own in a rapid time frame, BTMU felt the need to start from scratch, lever-aging the expertise of a mobile carrier, KDDI.

KDDI: A number of drivers led to KDDI’s decision to partici-pate in the Jibun Bank venture. The first was a high-level strategic objective of the company, to make the mobile phone an indispensable part of its customers’ lifestyles. KDDI’s plan to meet this objective was to offer a number of data-related services that consumers would use on a daily basis, including financial services. These kinds of data ser-vices would lead not only to increased data service fees but also to greater customer retention.

Leading up to KDDI’s decision to collaborate with BTMU, there was also a need to legitimize mobile data content. As is often the case with other new electronic media, the mobile space had witnessed an initial upsurge in “adult” content; offering mobile financial services was seen as an effective way to counter negative public perceptions.

However, there was another important reason for KDDI’s decision to launch a mobile-centric bank alongside BTMU. In 2005, KDDI’s chief rival, NTT DoCoMo, purchased a 34% share in the Sumitomo Mitsui Card Company. With this invest-ment, NTT Docomo had a stake in the financial services market, leading to the introduction of its DCMX line of credit products,1 all of which offered mobile wallet (osaifu keitai) and mobile contactless payment functionality. If KDDI was going to compete with NTT DoCoMo to be an indispensable part of consumers’ lives, it too had to offer mobile financial services. However, KDDI decided to take a slightly different route. Rather than just offering monoline, consumer credit products, KDDI wanted to offer a financial services platform, which could only be realized by starting a bank.

1. For more information about NTT DoCoMo’s DCMX mobile credit products, please refer to the Celent report Lessons from the Mobile Payments Leader: What the World Can Learn from the Japa-nese Market, June 2010.

18 Copyright 2010 © Celent, a division of Oliver Wyman, Inc.

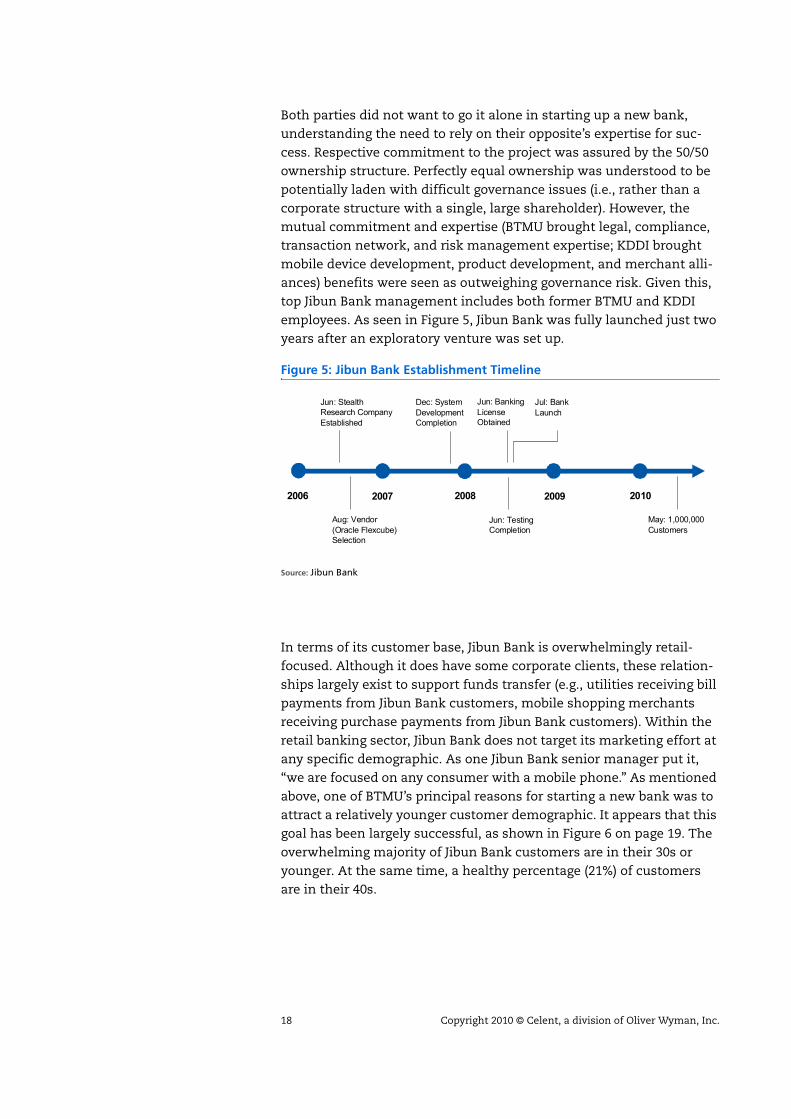

Both parties did not want to go it alone in starting up a new bank, understanding the need to rely on their opposite’s expertise for suc-cess. Respective commitment to the project was assured by the 50/50 ownership structure. Perfectly equal ownership was understood to be potentially laden with difficult governance issues (i.e., rather than a corporate structure with a single, large shareholder). However, the mutual commitment and expertise (BTMU brought legal, compliance, transaction network, and risk management expertise; KDDI brought mobile device development, product development, and merchant alli-ances) benefits were seen as outweighing governance risk. Given this, top Jibun Bank management includes both former BTMU and KDDI employees. As seen in Figure 5, Jibun Bank was fully launched just two years after an exploratory venture was set up.

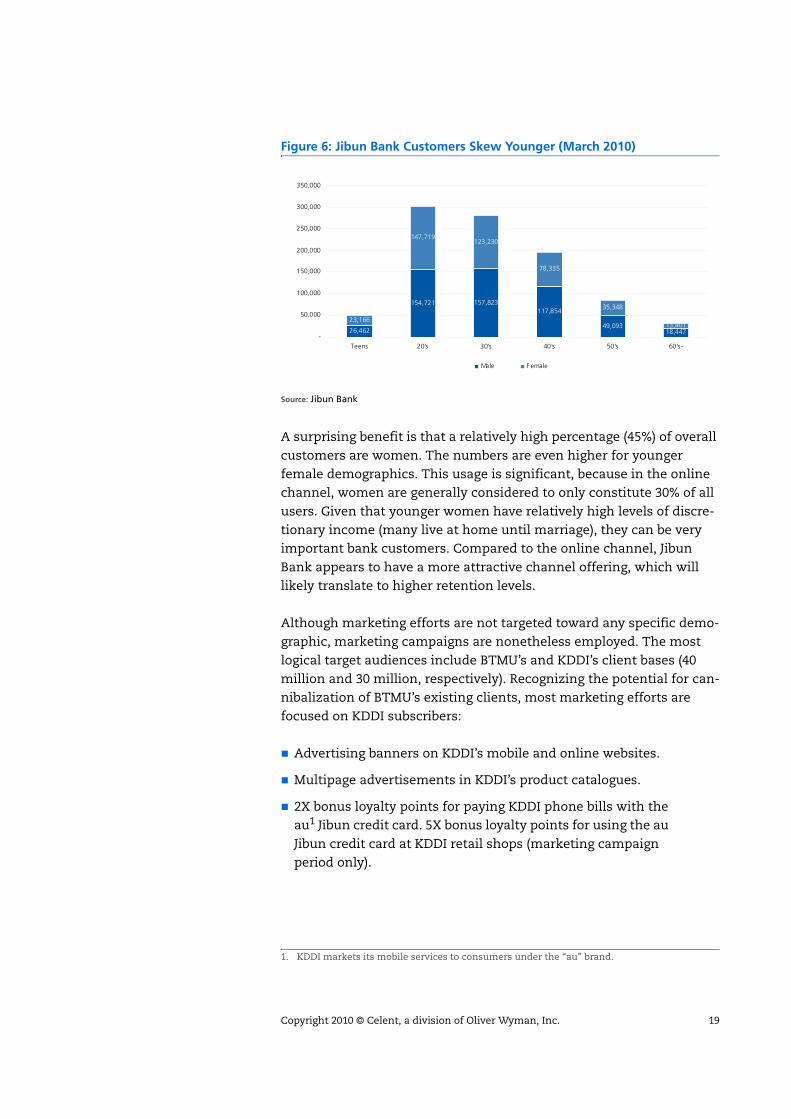

In terms of its customer base, Jibun Bank is overwhelmingly retail-focused. Although it does have some corporate clients, these relation-ships largely exist to support funds transfer (e.g., utilities receiving bill payments from Jibun Bank customers, mobile shopping merchants receiving purchase payments from Jibun Bank customers). Within the retail banking sector, Jibun Bank does not target its marketing effort at any specific demographic. As one Jibun Bank senior manager put it, “we are focused on any consumer with a mobile phone.” As mentioned above, one of BTMU’s principal reasons for starting a new bank was to attract a relatively younger customer demographic. It appears that this goal has been largely successful, as shown in Figure 6 on page 19. The overwhelming majority of Jibun Bank customers are in their 30s or younger. At the same time, a healthy percentage (21%) of customers are in their 40s.

Figure 5: Jibun Bank Establishment Timeline

Source: Jibun Bank

2006 2007 2008 2009 2010

Jun: StealthResearch CompanyEstablished

Aug: Vendor(Oracle Flexcube)Selection

Dec: SystemDevelopmentCompletion

Jun: TestingCompletion

Jun: BankingLicenseObtained

Jul: BankLaunch

May: 1,000,000Customers

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 19

A surprising benefit is that a relatively high percentage (45%) of overall customers are women. The numbers are even higher for younger female demographics. This usage is significant, because in the online channel, women are generally considered to only constitute 30% of all users. Given that younger women have relatively high levels of discre-tionary income (many live at home until marriage), they can be very important bank customers. Compared to the online channel, Jibun Bank appears to have a more attractive channel offering, which will likely translate to higher retention levels.

Although marketing efforts are not targeted toward any specific demo-graphic, marketing campaigns are nonetheless employed. The most logical target audiences include BTMU’s and KDDI’s client bases (40 million and 30 million, respectively). Recognizing the potential for can-nibalization of BTMU’s existing clients, most marketing efforts are focused on KDDI subscribers:

Advertising banners on KDDI’s mobile and online websites.

Multipage advertisements in KDDI’s product catalogues.

2X bonus loyalty points for paying KDDI phone bills with the au1 Jibun credit card. 5X bonus loyalty points for using the au Jibun credit card at KDDI retail shops (marketing campaign period only).

Figure 6: Jibun Bank Customers Skew Younger (March 2010)

Source: Jibun Bank

1. KDDI markets its mobile services to consumers under the “au” brand.

26,462

154,721 157,823117,854

49,09318,447

23,166

147,719123,230

78,335

35,348

13,401

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Teens 20's 30's 40's 50's 60's -

Male F emale

20 Copyright 2010 © Celent, a division of Oliver Wyman, Inc.

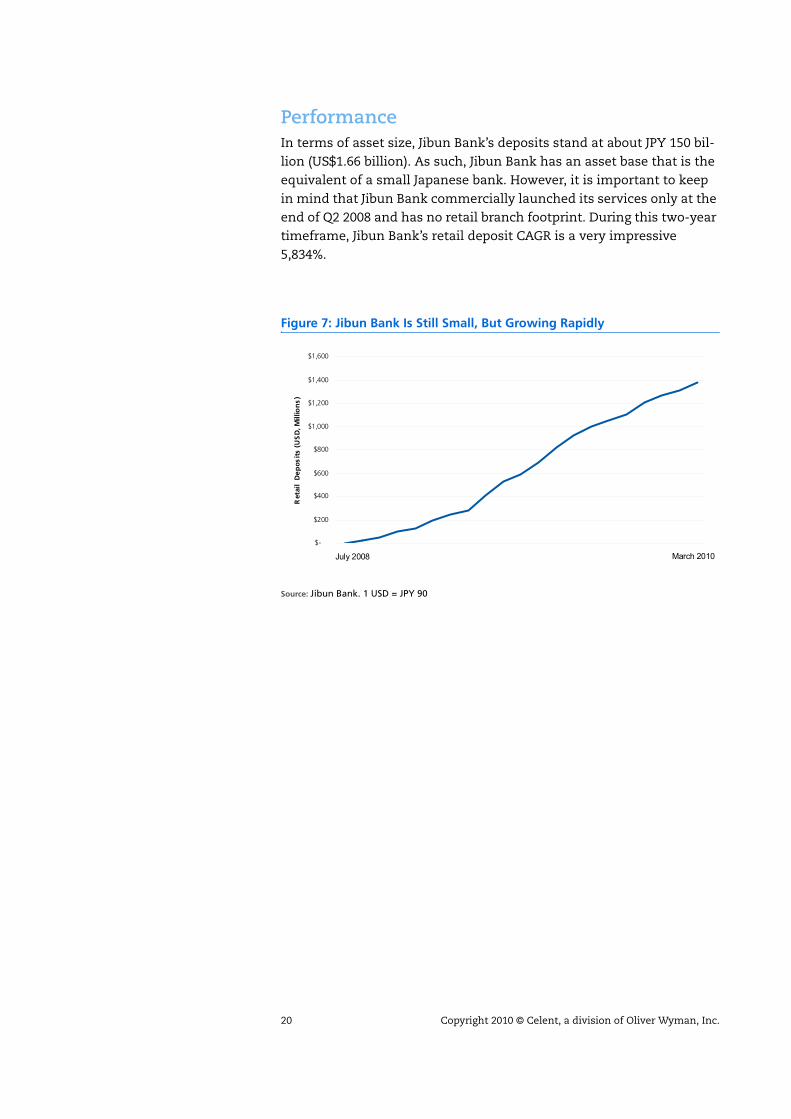

PerformanceIn terms of asset size, Jibun Bank’s deposits stand at about JPY 150 bil-lion (US$1.66 billion). As such, Jibun Bank has an asset base that is the equivalent of a small Japanese bank. However, it is important to keep in mind that Jibun Bank commercially launched its services only at the end of Q2 2008 and has no retail branch footprint. During this two-year timeframe, Jibun Bank’s retail deposit CAGR is a very impressive 5,834%.

Figure 7: Jibun Bank Is Still Small, But Growing Rapidly

Source: Jibun Bank. 1 USD = JPY 90

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

Ret

ail

Dep

osit

s (U

SD

, Mill

ion

s)

July 2008 March 2010

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 21

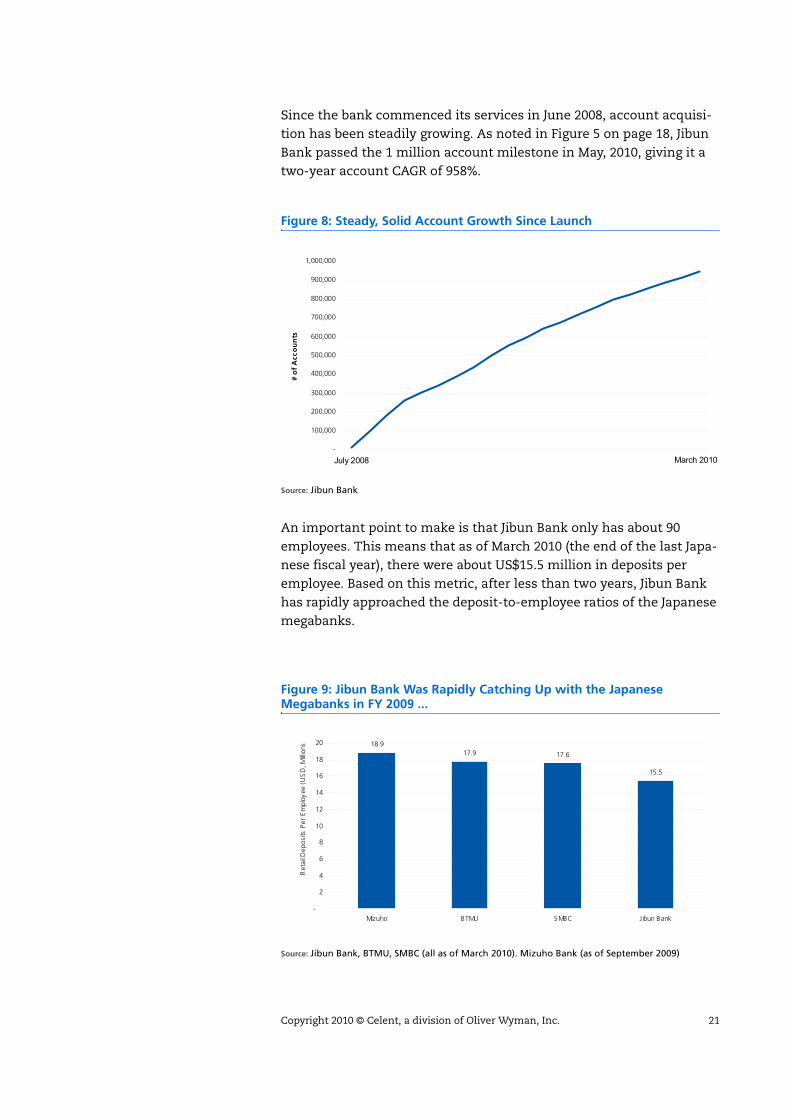

Since the bank commenced its services in June 2008, account acquisi-tion has been steadily growing. As noted in Figure 5 on page 18, Jibun Bank passed the 1 million account milestone in May, 2010, giving it a two-year account CAGR of 958%.

An important point to make is that Jibun Bank only has about 90 employees. This means that as of March 2010 (the end of the last Japa-nese fiscal year), there were about US$15.5 million in deposits per employee. Based on this metric, after less than two years, Jibun Bank has rapidly approached the deposit-to-employee ratios of the Japanese megabanks.

Figure 8: Steady, Solid Account Growth Since Launch

Source: Jibun Bank

Figure 9: Jibun Bank Was Rapidly Catching Up with the Japanese Megabanks in FY 2009 ...

Source: Jibun Bank, BTMU, SMBC (all as of March 2010). Mizuho Bank (as of September 2009)

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

# o

f A

cco

un

ts

July 2008 March 2010

18.917.9 17.6

15.5

-

2

4

6

8

10

12

14

16

18

20

Mizuho BTMU SMBC Jibun Bank

Ret

ail D

epo

sits

Per

Em

ploy

ee (

US

D, M

illion

s

22 Copyright 2010 © Celent, a division of Oliver Wyman, Inc.

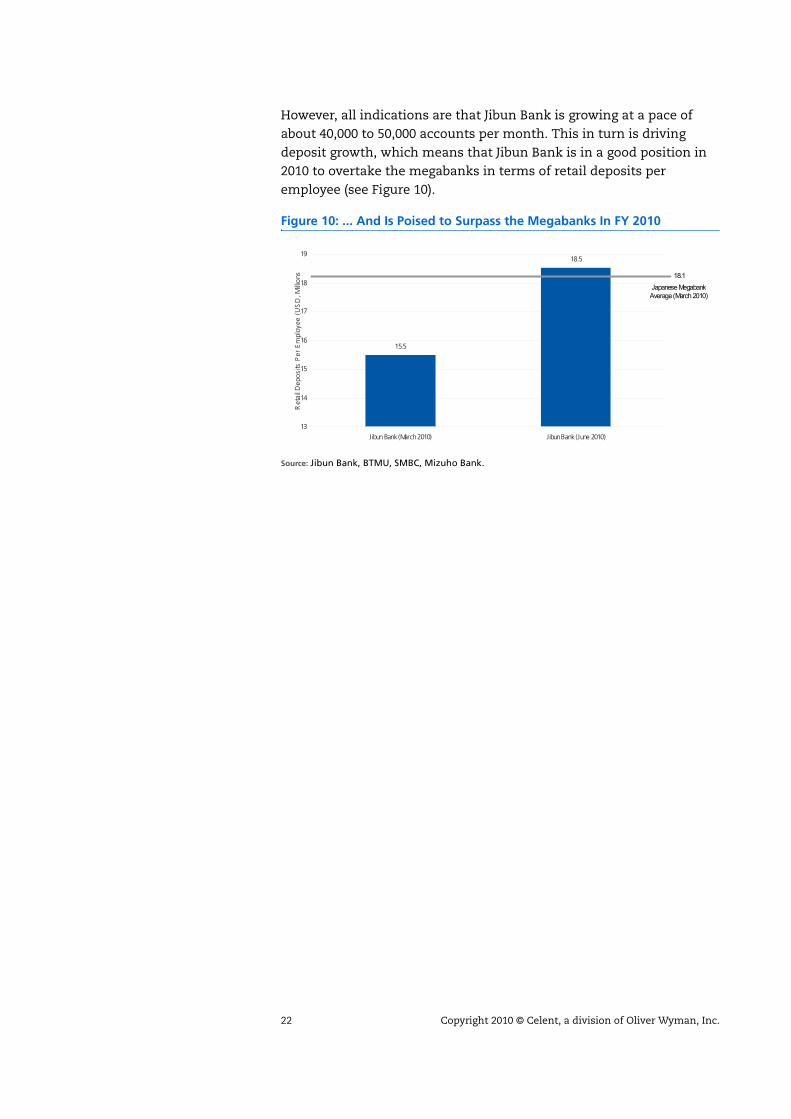

However, all indications are that Jibun Bank is growing at a pace of about 40,000 to 50,000 accounts per month. This in turn is driving deposit growth, which means that Jibun Bank is in a good position in 2010 to overtake the megabanks in terms of retail deposits per employee (see Figure 10).

Figure 10: ... And Is Poised to Surpass the Megabanks In FY 2010

Source: Jibun Bank, BTMU, SMBC, Mizuho Bank.

15.5

18.5

13

14

15

16

17

18

19

Jibun Bank (March 2010) Jibun Bank (June 2010)

Ret

ail D

epo

sits

Per

Em

ploy

ee (

US

D, M

illio

nsJapanese MegabankAverage (March 2010)

18.1

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 23

Jibun Bank Offerings and Underlying Technical Systems

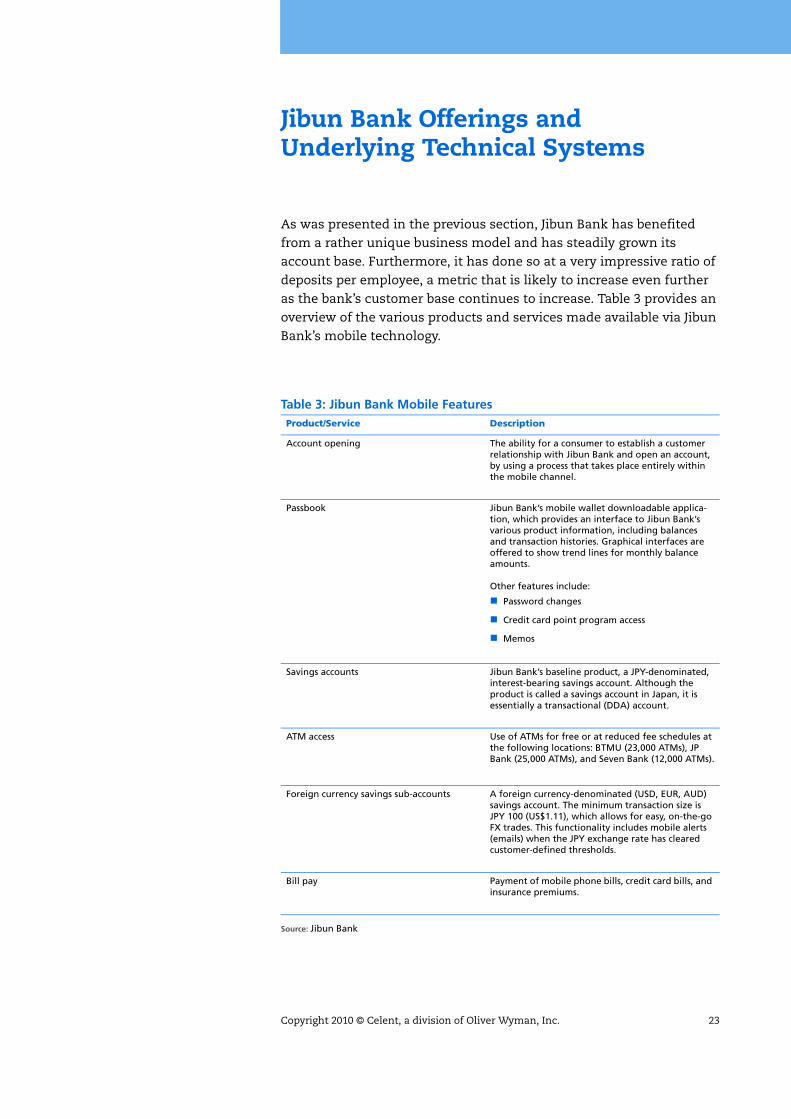

As was presented in the previous section, Jibun Bank has benefited from a rather unique business model and has steadily grown its account base. Furthermore, it has done so at a very impressive ratio of deposits per employee, a metric that is likely to increase even further as the bank’s customer base continues to increase. Table 3 provides an overview of the various products and services made available via Jibun Bank’s mobile technology.

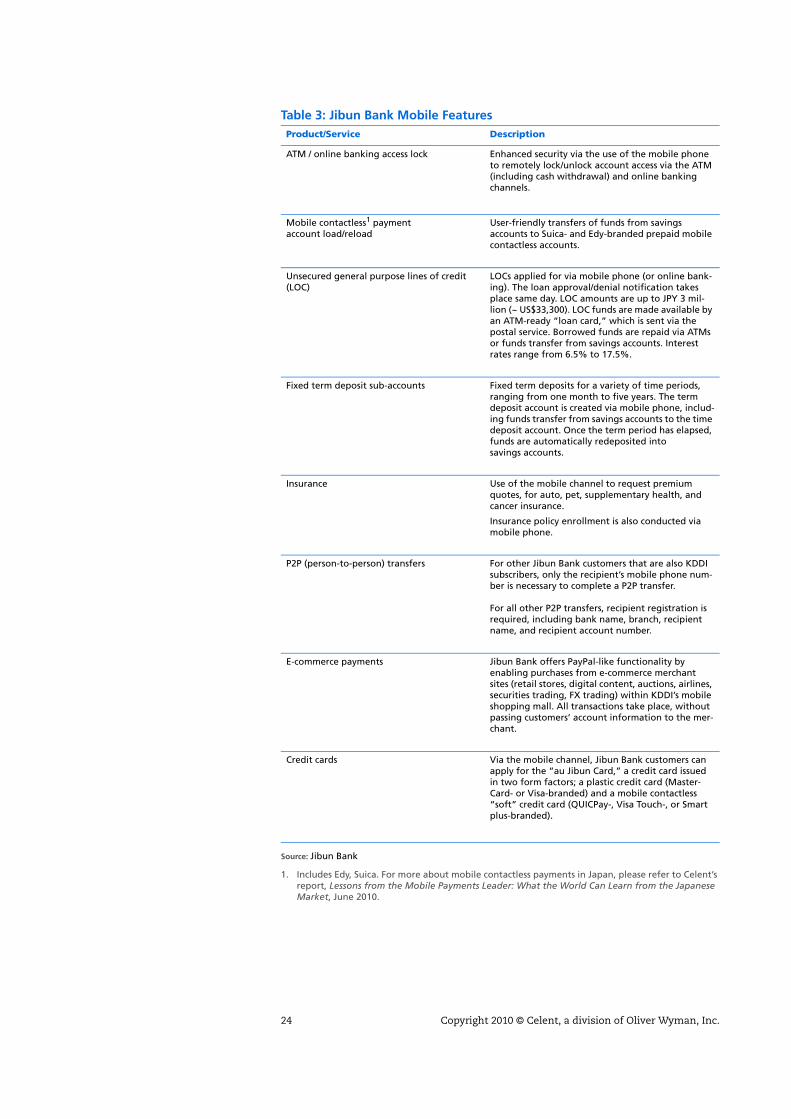

Table 3: Jibun Bank Mobile FeaturesProduct/Service Description

Account opening The ability for a consumer to establish a customer relationship with Jibun Bank and open an account, by using a process that takes place entirely within the mobile channel.

Passbook Jibun Bank’s mobile wallet downloadable applica-tion, which provides an interface to Jibun Bank’s various product information, including balances and transaction histories. Graphical interfaces are offered to show trend lines for monthly balance amounts.

Other features include:

Password changes

Credit card point program access

Memos

Savings accounts Jibun Bank’s baseline product, a JPY-denominated, interest-bearing savings account. Although the product is called a savings account in Japan, it is essentially a transactional (DDA) account.

ATM access Use of ATMs for free or at reduced fee schedules at the following locations: BTMU (23,000 ATMs), JP Bank (25,000 ATMs), and Seven Bank (12,000 ATMs).

Foreign currency savings sub-accounts A foreign currency-denominated (USD, EUR, AUD) savings account. The minimum transaction size is JPY 100 (US$1.11), which allows for easy, on-the-go FX trades. This functionality includes mobile alerts (emails) when the JPY exchange rate has cleared customer-defined thresholds.

Bill pay Payment of mobile phone bills, credit card bills, and insurance premiums.

Source: Jibun Bank

24 Copyright 2010 © Celent, a division of Oliver Wyman, Inc.

ATM / online banking access lock Enhanced security via the use of the mobile phone to remotely lock/unlock account access via the ATM (including cash withdrawal) and online banking channels.

Mobile contactless1 payment account load/reload

User-friendly transfers of funds from savings accounts to Suica- and Edy-branded prepaid mobile contactless accounts.

Unsecured general purpose lines of credit (LOC)

LOCs applied for via mobile phone (or online bank-ing). The loan approval/denial notification takes place same day. LOC amounts are up to JPY 3 mil-lion (~ US$33,300). LOC funds are made available by an ATM-ready “loan card,” which is sent via the postal service. Borrowed funds are repaid via ATMs or funds transfer from savings accounts. Interest rates range from 6.5% to 17.5%.

Fixed term deposit sub-accounts Fixed term deposits for a variety of time periods, ranging from one month to five years. The term deposit account is created via mobile phone, includ-ing funds transfer from savings accounts to the time deposit account. Once the term period has elapsed, funds are automatically redeposited into savings accounts.

Insurance Use of the mobile channel to request premium quotes, for auto, pet, supplementary health, and cancer insurance.

Insurance policy enrollment is also conducted via mobile phone.

P2P (person-to-person) transfers For other Jibun Bank customers that are also KDDI subscribers, only the recipient’s mobile phone num-ber is necessary to complete a P2P transfer.

For all other P2P transfers, recipient registration is required, including bank name, branch, recipient name, and recipient account number.

E-commerce payments Jibun Bank offers PayPal-like functionality by enabling purchases from e-commerce merchant sites (retail stores, digital content, auctions, airlines, securities trading, FX trading) within KDDI’s mobile shopping mall. All transactions take place, without passing customers’ account information to the mer-chant.

Credit cards Via the mobile channel, Jibun Bank customers can apply for the “au Jibun Card,” a credit card issued in two form factors; a plastic credit card (Master-Card- or Visa-branded) and a mobile contactless “soft” credit card (QUICPay-, Visa Touch-, or Smart plus-branded).

1. Includes Edy, Suica. For more about mobile contactless payments in Japan, please refer to Celent’s report, Lessons from the Mobile Payments Leader: What the World Can Learn from the Japanese Market, June 2010.

Table 3: Jibun Bank Mobile FeaturesProduct/Service Description

Source: Jibun Bank

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 25

A scan of this list makes it quickly obvious that the majority of these products and features are not currently offered by mobile banking solutions found in North America and Europe. This is truly impressive.

Most of these products and features should give most bankers food for thought and merit further discussion. This report will focus on two products which Celent finds particularly intriguing and unique: account opening and loan origination.

Account OpeningJibun Bank’s account opening feature was designed to support two major underlying business philosophies. The first philosophy is to be in tune with the mobile lifestyles of its targeted customer base. This was compounded by the fact that Jibun Bank does not have a physical branch network and that personal computer access is not a certainty for Japanese consumers. As a result, Jibun Bank’s only option was to offer a mobile-only account opening capability,1 which in English can be translated as Quick Account Setup.

The second philosophy is to provide extremely high levels of customer satisfaction. Given Jibun Bank’s lack of a brick-and-mortar presence and physical personnel, this means that a quick customer feedback loop is of extreme importance.

The Quick Account Setup process is portrayed in Figure 12 on page 27. The conditions for potential customers to open an account are the following:

Customers must be living in Japan and have a residential mailing address.

Only one account per customer is allowed.

Enrollees must have some form of personal identification (driver’s license).

A mobile phone and a mobile email address are required.

Children aged 15 and younger must have parental approval (in which case, a paper application must be used).

In the case of mobile-only account opening, customers must download Jibun Bank’s mobile application.

Customers must also be KDDI subscribers.2

1. However, Jibun Bank does offer account opening via the Internet and paper applications as well.

2. Non-KDDI subscribers must use the other account opening options.

26 Copyright 2010 © Celent, a division of Oliver Wyman, Inc.

From a customer experience perspective, the Quick Account Setup pro-cess entails six major steps.

1. The customer downloads the Jibun Bank mobile app and selects the “Account Setup” option.

2. Next, the customer enters all the required information1 in the account setup page. Some of this data may be prepopulated, based on the customer’s existing mobile phone registration information.

3. The customer then takes a picture of his/her driver’s license with his/her mobile phone, which he/she then sends to Jibun Bank (via the app), along with the entered data.

4. After Jibun Bank reviews the customer’s application, an email is sent to the registered mobile email address, indicating that the account has been established.

5. The customer later receives a Jibun Bank ATM card via registered mail.

6. Customers then fund their account via salary direct deposits, trans-fers from other banks, or deposits via partner ATMs.

Step 4 usually takes place over the course of one to two days. The entire process can be completed within four days. Customers can then fund their account via salary direct deposits, or cash deposits at BTMU, JP Bank, or 7-11 ATMs. From there on, they can take advantage of all the products and services listed in Table 3 on page 23.

Of course, what takes place in the back end is transparent to the cus-tomer and is actually quite complicated. A number of steps and systems are required to enable Jibun’s Quick Account Setup process (see Figure 12).

1. First and last name, mailing address (including postal code), date of birth, mobile phone number, mobile email address, desired password, and KDDI mobile web portal password.

Figure 11: Jibun Bank ATM Card—Simple, Debit Card Functionality

Source: Jibun Bank

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 27

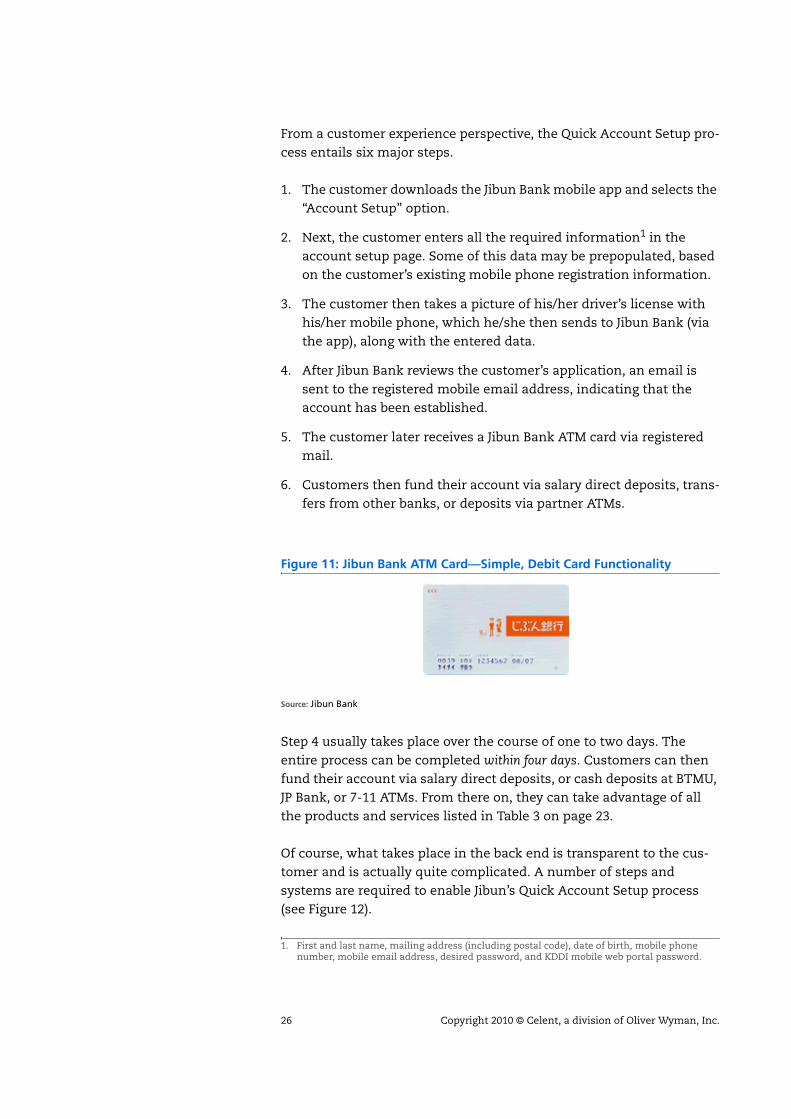

The account setup data sent via the new customer’s mobile phone is passed via Oracle’s FLEXCUBE Connect product onto Jibun’s back end core banking system: Oracle’s FLEXCUBE Retail product. From there, a series of system orchestration procedures unfold.

First, FLEXCUBE takes the applicant-provided data and conducts an anti-money laundering (AML) check; this consists of running the appli-cant’s name and mobile phone number against an industrywide blacklist, as well as matching the data against KDDI’s files (i.e., to determine if the same applicant name / mobile phone number match exist in KDDI’s customer information system).

Second, should the applicant pass the AML check, FLEXCUBE then sends the applicant’s data to Dai Nippon Printing (DNP), which pro-vides a number of processing services in addition to its legacy printing services. DNP’s account opening system sets up an account application file and converts the data (both applicant info and digitized photo of the applicant’s drivers license) into paper data sheets. These data sheets are then sent to experts within DNP’s account opening center, who compare and verify the validity of the provided information. For security reasons, most of this validation process is proprietary to DNP, and the details of it are unknown even to Jibun Bank.

Figure 12: Account Opening Process Overview

Source: Jibun Bank, Celent

FLEXCUBE

Retail

FLEXCUBE

RetailAccount Opening System

Account Opening System

Dai Nippon Printing

Account Opening Ctr

Account Opening Ctr

CustomerData Sheet

Driver’sLicenseSheet

Card Production

Card Production

Driver’sLicense

FLEXCUBE

Connect

FLEXCUBE

Connect

Jibun Bank

CIFModule

AMLModule

1. 2.

3.

4.

5.

ISIDeMarket“Brain”

ISIDeMarket“Brain”

28 Copyright 2010 © Celent, a division of Oliver Wyman, Inc.

Third, once the validity of the applicant’s information has been veri-fied, DNP instructs Jibun Bank to establish an account within FLEXCUBE’s customer information file module. As of this point, the applicant’s account resides within Jibun Bank’s system.

In the fourth step, Jibun Bank once again relies on DNP. In this case, the new customer’s data is sent to DNP’s card production unit, which issues the ATM card (see Figure 11 on page 26) and sends it via regis-tered mail to the customer. The card has to be received at the account-registered address by a resident, who signs delivery receipt.

The fifth step only occurs if the ATM card is undeliverable via regis-tered mail. In such cases, DNP notifies Jibun Bank’s eMarket Brain call center/IVR system (from ISID, a Japanese bank technology vendor). The call center/IVR system then places a call to the customer’s mobile phone number to determine how/when to best deliver the ATM card.

This entire account opening process constitutes an excellent example of how a bank’s back end systems (all outsourced, all hosted offsite) work in concert with each other to seamlessly and transparently navi-gate customers through a complex process.

Loan OriginationAs is the case with most banks, Jibun Bank seeks to drive revenue through its loan portfolio.1 However, unlike other banks, Jibun Bank had to develop this portfolio within its business philosophy of support-ing its customers’ mobile lifestyles and providing the highest levels of customer satisfaction while working within the confines of a mobile-only or online-only bank presence.

From a customer experience perspective, the loan process is straightforward and user-friendly:

1. Existing customers apply for the Jibun Loan via their Jibun Bank mobile banking app on their mobile phones.2 In the case of no changes in customer information (i.e., following the opening of their original account), there is no need for customers to enter any additional demographic data. Loan applicants who are not Jibun Bank customers must first open an account.

2. Usually on the same business day, customers receive an email in their mobile phones (or computers) that the loan has been approved or declined. Additionally, they are informed of the maxi-

1. As described in Table 3 on page 23, this product actually functions like a LOC—i.e., loaned funds do not need to be spent.

2. Loan applications can also take place via Jibun Bank’s website.

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 29

mum loan amount and applicable interest rate. For customers applying for a line of credit greater than JPY 1 million (~US$11,250), approval is subject to the submission of supporting financial state-ments, such as pay stubs or tax forms.1

3. A loan account is created, and loan funds are made available to customers.

4. In less than one week, customers receive a Jibun Loan card, which can be used to withdraw funds from partner ATMs. Alternatively, customers may transfer funds from their loan accounts to their savings accounts.

Customers repay their loans either via transfer from their savings accounts or by depositing funds at partners’ ATMs. In the case of loan funds withdrawals or repayments via such ATMs, there are no transac-tion fees.

Once again, the simplicity of customers’ experiences with the loan origination process is supported by a highly complex, behind-the-scenes array of back end systems. Figure 14 on page 30 depicts the overall loan origination process.

1. Customers must send copies (via postal services) to Jibun Bank’s loan department.

Figure 13: Jibun Bank’s Novel Approach to Loan Funds Distribution: An ATM-Based Loan Card

Source: Jibun Bank

30 Copyright 2010 © Celent, a division of Oliver Wyman, Inc.

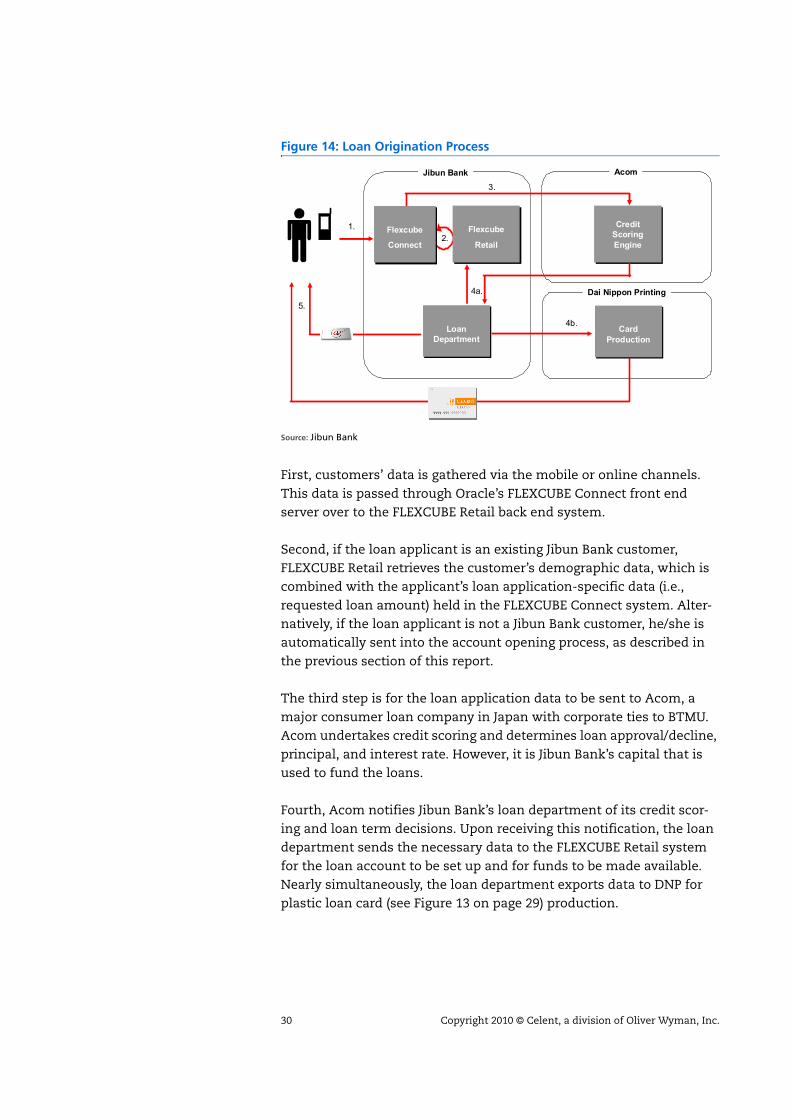

First, customers’ data is gathered via the mobile or online channels. This data is passed through Oracle’s FLEXCUBE Connect front end server over to the FLEXCUBE Retail back end system.

Second, if the loan applicant is an existing Jibun Bank customer, FLEXCUBE Retail retrieves the customer’s demographic data, which is combined with the applicant’s loan application-specific data (i.e., requested loan amount) held in the FLEXCUBE Connect system. Alter-natively, if the loan applicant is not a Jibun Bank customer, he/she is automatically sent into the account opening process, as described in the previous section of this report.

The third step is for the loan application data to be sent to Acom, a major consumer loan company in Japan with corporate ties to BTMU. Acom undertakes credit scoring and determines loan approval/decline, principal, and interest rate. However, it is Jibun Bank’s capital that is used to fund the loans.

Fourth, Acom notifies Jibun Bank’s loan department of its credit scor-ing and loan term decisions. Upon receiving this notification, the loan department sends the necessary data to the FLEXCUBE Retail system for the loan account to be set up and for funds to be made available. Nearly simultaneously, the loan department exports data to DNP for plastic loan card (see Figure 13 on page 29) production.

Figure 14: Loan Origination Process

Source: Jibun Bank

Flexcube

Retail

Flexcube

Retail

CreditScoring Engine

CreditScoring Engine

Dai Nippon Printing

Card Production

Card Production

Flexcube

Connect

Flexcube

Connect

Jibun Bank

1. 2.

3.

4a.

5.

LoanDepartment

LoanDepartment

Acom

4b.

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 31

Then fifth, the loan department notifies the applicant via email of the loan decision and borrowing terms. The new loan customer then receives the loan card, again sent via registered mail to the physical mailing address used for the customer’s account.

Again, this is another example of advanced mobile banking at work, linking multiple back end systems to seamlessly and transparently complete a complex task. What makes Jibun Bank’s back end processes and systems more impressive is that fact that many of them are man-aged by outside entities. This approach has allowed Jibun Bank to outsource a significant proportion of its operations to best-of-breed players. And, in the case of loan origination, Jibun Bank has been able to achieve what many banks dream of accomplishing with the mobile banking (i.e., not mobile payments) channel: direct monetization.

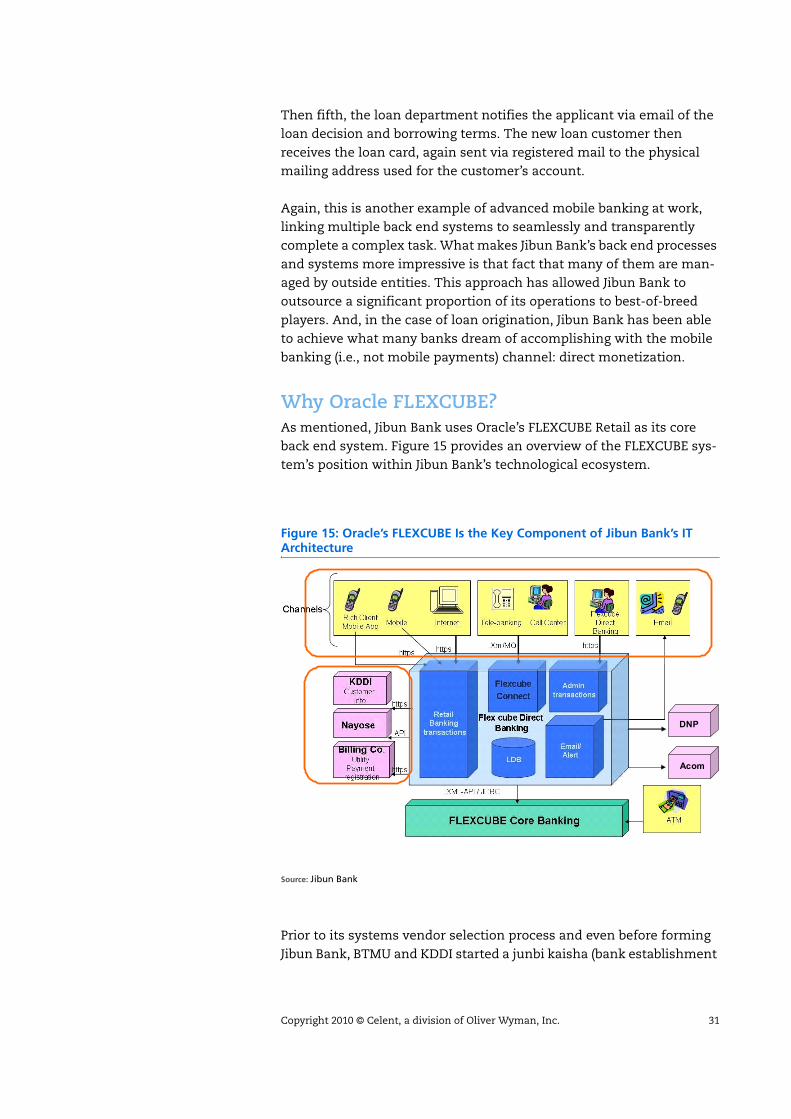

Why Oracle FLEXCUBE?As mentioned, Jibun Bank uses Oracle’s FLEXCUBE Retail as its core back end system. Figure 15 provides an overview of the FLEXCUBE sys-tem’s position within Jibun Bank’s technological ecosystem.

Prior to its systems vendor selection process and even before forming Jibun Bank, BTMU and KDDI started a junbi kaisha (bank establishment

Figure 15: Oracle’s FLEXCUBE Is the Key Component of Jibun Bank’s IT Architecture

Source: Jibun Bank

DNP

Acom

32 Copyright 2010 © Celent, a division of Oliver Wyman, Inc.

investigation company) in 2006. The purpose of this company was to lay the groundwork for the eventual Jibun Bank launch. As mentioned earlier in this report, it was quickly decided that trying to leverage BTMU’s legacy system would take up too many budgetary and time resources, and that bank systems would have to be built from scratch. The stealth company consisted of 20 employees from both BTMU and KDDI. Professional backgrounds in this group were various:

IT systems

Retail banking

Planning

Banking and mobile product development

Alliances

Once the stealth team had been established, a major consulting firm1 was engaged to lead the systems vendor selection process. With this consulting firm, a vendor scoring system was developed, but given time constraints (the original plan was to launch Jibun Bank in 2007), the potential vendor list was quickly narrowed down to less than five companies.

Once this list had been agreed upon, the RFP process began. Some of the main requirement categories were the following:

Support of all planned banking products via the mobile channel

Yen-denominated accounts as base accounts

Multicurrency accounts

Integration with Zengin, the Japanese domestic interbank settlement network

Integration with Cafis, the Japanese domestic ATM network operated by NTT Data

The ability to build upon Phase 1 capabilities with potential future mobile offerings, such as mutual funds and invest-ments/trading

Extremely high service levels

Previous implementations in the Japanese market

1. For confidentiality reasons, the name of the consulting firm has been intentionally omitted.

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 33

Short time to launch, perhaps one of the most important requirements.

When the RFPs came back from the vendors, the vendor names were hidden, and the lead candidate was selected. As it turned out, the only system that could fulfill these RFP requirements was considered to be Oracle’s FLEXCUBE.

The next major step for the investigation company and consulting firm was due diligence. This included speaking with a reference client in Japan, Shinsei Bank, a relatively new bank in the Japanese market. Shinsei Bank had shown repeatable results with FLEXCUBE technology, which was encouraging to the investigation company / consulting team. Another form of due diligence was to look at the number and types of FLEXCUBE implementations outside of Japan; it was very important to the team that Oracle had a broad and steady enough cli-ent base to prevent it from leaving the banking core systems market. FLEXCUBE passed this background check as well.

With this, Oracle was chosen as Jibun Bank’s core system provider. As is typically the case, implementation issues arose. Perhaps somewhat unique to doing business in Japan was the language issue. Most mem-bers of the investigation company did not speak English fluently, nor did the Oracle team speak Japanese fluently. As a result, interpreters and translators were often required, which slowed down the develop-ment process.

Another major speed bump in the development process was FLEX-CUBE’s lack of a solid mobile front end system in Japan. Although Shinsei had implemented FLEXCUBE Retail as a back end system in Japan years earlier, it did so without launching a mobile front end. Because of this, considerable mobile capability development effort was required of Oracle. However, once the mobile front end was finally completed, it was robust enough that Oracle was able to sell it back into Shinsei Bank.

Given the various issues, implementation of the Oracle FLEXCUBE sys-tems took longer than expected. The purchase decision was made in August 2006, and development was completed in December 2007. Although the soon-to-be Jibun Bank management team was hoping for a development-to-launch timeline of only one year, this goal was per-haps too aggressive. Development alone took 16 months, and Jibun Bank also made the decision to undertake a longer testing period. However, the final result is a bank which, from a technology and func-tionality perspective, can claim to be one of the world’s foremost mobile banks.

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 34

Conclusion

Essentially unheard of in 2007, mobile banking has made great strides in the North American market. During the course of the last three years, mobile banking innovation has continued at an unwavering pace, leading to ongoing redefinition of the term advanced mobile banking. Features that were considered advanced in 2007 have since become commodities.

As of 2010, a number of mobile banking front end functionalities are considered to be advanced. These include remote deposit capture, P2P payments, real time transactional alerts, and offline registration. Mobile payment functionality is beginning to emerge, but only in pilots, not commercial rollouts.

In terms of mobile banking back end integration, the status quo is characterized by front end connectivity with DDA (transactional account) core systems, the most basic integration model. However, newer integrations and especially those at larger banks have pro-gressed to the point where the mobile front end is connected to multiple back end systems, allowing bank customers mobile access to all their accounts (e.g., checking, savings, loan, mortgage, credit card, etc.) at a given FI. Although Celent considers this integration model to be the current definition of advanced, it is clear that this definition will soon evolve. It will come to embody orchestration across multiple back end systems to create meaningful interactions with mobile customers.

One of the best examples of a bank offering advanced mobile banking technology is Jibun Bank in Japan. A 2010 winner of Celent’s Model Bank Award, Jibun Bank is part of a growing trend of collaboration between FIs and mobile carriers; Jibun Bank is owned by BTMU (a Japa-nese megabank) and KDDI (Japan’s second-largest mobile carrier). Jibun Bank was founded by these two entities as a way to acquire and retain customers who increasingly lead mobile-centric lifestyles.

In terms of front end technology, Jibun Bank offers a long list of fea-tures that are far advanced beyond any mobile banking functionality currently found in North America. Examples include FX transactions, ATM/online banking lock, fixed time deposit accounts, and contactless payment card reloads.

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 35

In addition, Jibun Bank offers some truly amazing mobile banking functionality. One is new account opening, entirely done via the mobile phone. Another is mobile-only loan origination. Although account opening and loan origination are bread-and-butter, necessary func-tions that banks need to perform, Celent is unaware of any other bank in the world that is able to do so solely within the confines of the mobile channel.

In each of these functions, a number of back end systems had to inter-act with each other, shepherding customer data across multistep processes. From these processes, brand new products (i.e., new accounts, new loans) were generated. In other words, Jibun’s function-ality is not representative of the status quo: customers using a mobile front end to access existing information residing in a single back end system. Rather, Jibun Bank’s offering is a concrete example (perhaps the best example) of what advanced mobile banking truly looks like.

The core banking system behind this technology is Oracle’s FLEXCUBE Retail product. FLEXCUBE was chosen for its ability to fulfill the bank’s business requirements. In fact, it was the only product that Jibun Bank felt was right for the project. The functionality that exists today is a foundation for Jibun Bank’s planned future products, an indication that FLEXCUBE will be able to grow with the bank. As is the case with any major systems implementation project, the FLEXCUBE install was not without its issues. However, the end result was the launch of a fully functioning bank, likely the most advanced mobile bank in the world.

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 36

Leveraging Celent’s Expertise

If you found this report valuable, you might consider engaging with Celent for custom analysis and research. Our collective experience and the knowledge we gained while working on this report can help you streamline the creation, refinement, or execution of your strategies.

Analyst AccessMost Celent subscribers have unlimited free analyst access. If you have a question about this report, you can reach out to the author to gain deeper insight into the report’s findings. Please contact your Celent account manager for more details.

Support for BanksTypical projects we support related to transaction processing technologies:

Vendor shortlisting and selection. We perform discovery specific to you and your business to better understand your unique needs. Based on our industry knowledge, we then objectively create and administer a custom RFI/RFP process with selected banking technology vendors, to assist you in making rapid and accurate vendor choices.

Business practice evaluations. We spend time evaluating your busi-ness processes, particularly in banking industry product development, benchmarking and channel-building. Based on our knowledge of the market, we identify potential process or technology constraints and provide clear insights that will help you implement industry best practices.

IT and business strategy creation. We collect perspectives from your executive team, your front line business and IT staff, and your custom-ers. We then analyze your current position, institutional capabilities, and technology against your goals and competitors’ initiatives in the financial services space. If necessary, we help you reformulate your technology and business plans to address short-term and long-term needs.

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 37

Support for VendorsWe provide services that help you refine your product and service offerings. Examples include:

Product and service strategy evaluation. Based on our familiarity with banks across the globe, we help you assess your market position in terms of functionality, technology, and services. Our strategy work-shops will help you target the right financial institutions and map your offerings to their needs.

Market messaging and collateral review. Based on our extensive expe-rience with your potential banking industry clients, we assess your marketing and sales materials—including your website and any collateral.

Market penetration. Celent understands markets globally with ana-lysts in the United States, Canada, Europe, India, China, Japan, and other countries. We can help your company understand market dynamics and enter new markets more effectively.

Copyright 2010 © Celent, a division of Oliver Wyman, Inc. 38

Related Celent Research

The View from the Mobile NFC Finish Line: Bank Economics in a Mature Mobile NFC Payments WorldSeptember 2009

Mobile B2X: The Next Mobile Payment Wave in International MarketsJanuary 2010

Are Banks from Mars, Mobile Banking Technology Vendors from Venus?March 2010

Lessons from the Mobile Payments Leader: What the World Can Learn from the Japanese MarketJune 2010

Copyright Notice

Prepared byCelent, a division of Oliver Wyman, Inc.

Copyright © 2010 Celent, a division of Oliver Wyman, Inc. All rights reserved. This report may not be reproduced, copied or redistributed, in whole or in part, in any form or by any means, without the written permission of Celent, a division of Oliver Wyman (“Celent”) and Celent accepts no liability whatsoever for the actions of third parties in this respect. Celent is the sole copyright owner of this report, and any use of this report by any third party is strictly prohibited without a license expressly granted by Celent. This report is not intended for general circulation, nor is it to be used, reproduced, copied, quoted or distributed by third parties for any purpose other than those that may be set forth herein without the prior written permission of Celent. Neither all nor any part of the contents of this report, or any opinions expressed herein, shall be disseminated to the public through advertising media, public relations, news media, sales media, mail, direct transmittal, or any other pub-lic means of communications, without the prior written consent of Celent. Any violation of Celent’s rights in this report will be enforced to the fullest extent of the law, including the pursuit of monetary damages and injunctive relief in the event of any breach of the foregoing restrictions.

This report is not a substitute for tailored professional advice on how a specific financial institution should execute its strategy. This report is not investment advice and should not be relied on for such advice or as a substitute for consultation with professional accountants, tax, legal or financial advisers. Celent has made every effort to use reliable, up-to-date and comprehensive information and analysis, but all information is provided without warranty of any kind, express or implied. Infor-mation furnished by others, upon which all or portions of this report are based, is believed to be reliable but has not been verified, and no warranty is given as to the accuracy of such information. Public information and industry and statistical data, are from sources we deem to be reliable; however, we make no representation as to the accuracy or completeness of such information and have accepted the informa-tion without further verification.

Celent disclaims any responsibility to update the information or conclusions in this report. Celent accepts no liability for any loss arising from any action taken or refrained from as a result of information contained in this report or any reports or sources of information referred to herein, or for any consequential, special or similar damages even if advised of the possibility of such damages.

There are no third party beneficiaries with respect to this report, and we accept no liability to any third party. The opinions expressed herein are valid only for the pur-pose stated herein and as of the date of this report.

No responsibility is taken for changes in market conditions or laws or regulations and no obligation is assumed to revise this report to reflect changes, events or condi-tions, which occur subsequent to the date hereof.

North America Europe Asia

USA

200 Clarendon Street, 12th Floor

Boston, Massachusetts 02116

Tel.: +1.617.262.3120

Fax: +1.617.262.3121

USA

1166 Avenue of the Americas

New York, NY 10036

Tel.: +1.212.541.8100

Fax: +1.212.541.8957

USA

Four Embarcadero Center, Suite 1100

San Francisco, California 94111

Tel.: +1.415.743.7900

Fax: +1.415.743.7950

France

28, avenue Victor Hugo

75783 Paris Cedex 16

Tel.: +33.1.73.04.46.19

Fax: +33.1.45.02.30.01

United Kingdom

55 Baker Street

London W1U 8EW

Tel.: +44.20.7333.8333

Fax: +44.20.7333.8334

Japan

The Imperial Hotel Tower, 13th Floor

1-1-1 Uchisaiwai-choChiyoda-ku, Tokyo 100-0011

Tel: +81.3.3596.0020

Fax: +81.3.3596.0021

China

Beijing Kerry CentreSouth Tower, 15th Floor1 Guanghua Road

Chaoyang, Beijing 100022

Tel: +86.10.8520.0350Fax: +86.10.8520.0349

India

Level 14, Concorde BlockUB City, Vittal Mallya Road

Banglalore, India 560001

Tel: +91.80.40300538Fax: +91.80.40300400

For more information please contact [email protected] or:

Red Gillen