Embed Size (px)

Citation preview

© Practising Law Institute

To order this book, call (800) 260-4PLI or fax us at (800) 321-0093. Ask our Customer Service Department for PLI Order Number 185480, Dept. BAV5.

Practising Law Institute1177 Avenue of the Americas

New York, New York 10036

Advanced Licensing Agreements 2017

Volume One

INTELLECTUAL PROPERTYCourse Handbook Series

Number G-1307

Co-ChairsMarcelo Halpern

Ira Jay LevyJoseph Yang

© Practising Law Institute

5

Advanced Business Issues in Trademark Licensing

Paula Jill Krasny

Culhane Meadows PLLC

Submitted by: Paula Jill Krasny

Culhane Meadows PLLC

Attachment 1: Copyright 2016 Charles River Associates. Reprinted with permission.

Attachment 2: Reprinted with permission.

If you find this article helpful, you can learn more about the subject by going to www.pli.edu to view the on demand program or segment for which it was written.

1-347

© Practising Law Institute

1-348

© Practising Law Institute

3

Trademark practitioners serve their clients best when they truly understand the client’s business concerns, help them realize more revenue through licensing, and minimize the risk of financial and business loss. In addition to providing an update on recent quality control cases, this paper outlines some business issues arising in the context of trademark licensing with which lawyers should familiarize themselves to add value to their clients’ businesses.

QUALITY CONTROL

Without quality control provisions, a trademark license runs the risk of being an uncontrolled or “naked” license that can result in abandonment of the licensed mark. Quality control provisions run the gamut from being heavily negotiated to altogether ignored in the agreement.

Because uncontrolled licensing can result in trademark abandonment, licensors should not ignore or give inadequate attention to quality control provisions. Here are some issues to consider when drafting and negotiating quality control provisions: 1. What makes practical sense in the context of the business? 2. Is there a mechanism in place for actually inspecting the quality of

the products or services offered under the licensed mark? a. Note quality control can be delegated to a third party (but not

necessarily to the licensee). b. Right to inspect marketing materials, websites, factories, sales

techniques, anything that will affect how the brand is used or will be perceived.

3. Not just the mere right to inspect, exercising that right. Survey of 2016 Quality Control Cases (as of September 30, 2016) – No significant federal cases. – Each of these T.T.A.B. cases is non-precedential.

CB Specialists, Inc. v. Central Avenue Deli, LLC d/b/a Lucky Dill Deli (T.T.A.B. September 26, 2016) (non-precedential decision). – Opposition proceeding against registration of a mark – The trademark Applicant applied to register a LUCKY

DILL (and design) mark for restaurant services. The

1-349

© Practising Law Institute

4

Opposer opposed based on prior use of LUCKY DILL for restaurant services.

– Opposer’s family owned various restaurants in Florida that operated in whole or part under the LUCKY DILL name.

– Applicant purchased one of the LUCKY DILL restaurants that had originally been owned by Opposer’s family. The restaurant had been sold several times; Applicant bought the restaurant from a third party.

– Applicant filed a trademark application for LUCKY DILL (and design), and asserted that the prior owners of the res-taurant used LUCKY DILL marks. Applicant was aware of the Opposer’s LUCKY DILL restaurants and tried to differentiate its brand by from the others. For example, it developed a new logo to use with its mark.

– To defend the opposition, the Applicant argued that the Opposer abandoned its pleaded marks through naked licensing. It argued that family did not exercise reasonable control over the parties that had purchased and operated LUCKY DILL restaurants.

– As the restaurants were initially expanding, Opposer did have reasonable control over the use of LUCKY DILL. The new restaurants were opened by Opposer’s son who was trained in the family business. There were site visits to the new restaurants, tastings, attendance at openings. TTAB found an implied license.

– The son sold three of the restaurants. Each owner was permitted to use the LUCKY DILL name. Two of the restaurants were sold as on ongoing business, but the TTAB did not find that the name was sold with the restaurants. The son did visit/inspect the restaurants that he had sold. The two restaurants with the implied license subsequently closed.

– The third restaurant, which the Applicant purchased, came with the “THE LUCKY DILL DELI” name and “any vari-ations thereof” for that location in St. Petersburg, FL, along with the right to relocate within a 3-mile radius.

1-350

© Practising Law Institute

5

– Because Opposer had exercised control over the LUCKY DILL restaurants they initially opened, and the son had exercised control over the marks when he sold two of the restaurants, there was no naked licensing.

Elephant & Castle Inc. v Original Joe’s Franchise Group, 2016 WL 3015158 (T.T.A.B. May 23, 2016) (non-precedential decision). – Motion for Summary Judgment in a trademark opposition

proceeding on issue of abandonment of mark through uncontrolled licensing denied because of existence of material issues of fact.

– Opposer asserted common law rights in ELEPHANT & CASTLE (and design) for restaurant services dating back to 1974.

– ELEPHANT & CASTLE restaurant chain started in Port-land, Oregon. Sharon Pera’s (“Pera”) parents acquired the restaurant in 1968 (“E&C Oregon”). Around 1973 or 1974, Pera’s parents opened a restaurant in Hawaii (“E&C Hawaii”).

– Around 1980/81, Pera’s parents sold E&C Hawaii (but not the ELEPHANT & CASTLE mark) to Emilio Quinton (“Quinton”).

– In 1993, E&C Group acquired E&C Oregon, the ELEPHANT & CASTLE trademark and federal registration therefor, which subsequently expired in 2008, for failure to renew. Part of the transaction included a license back of the mark so that the licensed restaurants, namely E&C Oregon and E&C Hawaii, could use the ELEPHANT & CASTLE mark. The license agreement had quality control language as well as inspection rights.

– There were various corporate changes whereby EC Res-taurants acquired E&C Group’s assets, including the ELEPHANT & CASTLE trademark. Eventually, owner-ship of the mark and restaurants were transferred to The Applicant, Original Joe’s Franchise Group.

– Opposer argued that the ELEPHANT & CASTLE mark was abandoned by virtue of uncontrolled use of the mark by E&C Hawaii after Pera’s parents sold the restaurant to

1-351

© Practising Law Institute

6

its general manager, Quinton. Opposer argued that Pera’s statements that Quinton was free to operate the Hawaiian restaurant as he chose after the sale let to abandonment of the mark.

– Opposer also argued that after E&C Group acquired the ELEPHANT & CASTLE trademark and licensed it back to E&C Oregon and E&C Hawaii, it failed to exercise control over their respective uses of the mark.

– Applicant argued that there was quality control because Pera worked at E&C Hawaii for at least five years after her parents sold the Hawaii restaurant to Quinton. In addition, her mother, the owner of E&C Oregon, spent six months a year in Hawaii, and there was a close connection between E&C Oregon and E&C Hawaii. Furthermore, Quinton managed E&C Oregon, assisted in the opening of the Hawaii restaurant and managed the Hawaii res-taurant up until purchasing it.

LuckyU Enterpises, Inc. DBA Giovanni’s Original White Shrimp Truck v. Aragona, 2016 WL 4437728 (T.T.A.B. March 18, 2016) (non-precedential decision). – Trademark cancellation proceeding. Respondent sold his

shrimp truck business to Petitioner. Respondent alleged that the asset purchase agreement was a license, rather than a sale, of the trademarks.

– T.T.A.B. found that the purchase agreement did not contain licensing provisions, such as royalty payments, and there were inadequate quality control provisions to ensure consistency of the product. Thus, the asset purchase agreement assigned, rather than licensed, the marks to Petitioner.

– To the extent Respondent had any rights in the marks, Respondent abandoned them through non-use without an intent to resume use. Respondent’s registrations were cancelled.

Lessons Learned: 1. Have well documented agreements 2. Exercise QC rights/keep records

1-352

© Practising Law Institute

7

HOLDING COMPANIES

Trademark ownership is often driven by tax and other business considerations. The goal is to put the IP owner in a jurisdiction that taxes the royalty income at a low rate or does not tax it at all. The licensee can also deduct the royalty payments. Moreover, the royalty streams can be monetized. Licensing structures are at the crux of these structures, and the tax and business people driving them may not know about some of the intricacies involved with trademark licensing.

Often the trademarks need to be migrated to an IP holding company, which, in turn, will license the trademarks to related companies and third parties. Migration can occur: ○ By Assignment ○ By Licensing. The tax consequences may be too great to outright

assign the marks. Transfer of Trademarks

○ To tax lawyers, a license can be a “transfer.” ○ Need to determine if the migration is occurring by means of a

license or an assignment. Ownership

○ Tax: Beneficial ownership – entity that invests in and builds up the goodwill in the mark

○ Trademark: legal record owner Goodwill

○ Tax – typically want to depreciate goodwill. ○ Trademark - want goodwill to be worth a lot. It goes to potential

damages in trademark infringement litigation. In addition, the higher the brand equity, the more the company is worth.

○ Be careful not to separate the goodwill from the U.S. trade-marks. You could end up with an “assignment in gross,” which separates the goodwill from the trademark and invalidates the trademark. In many jurisdictions, goodwill can be separated from the trademark without destroying the trademark rights, but not in the US.

1-353

© Practising Law Institute

8

Be careful of trademark multiple owners. ○ You may no longer have a “single source,” which can destroy

the trademark rights. Consumers identifying a product with one source: basis

of trademark rights. Lack of single source can lead to generic names/loss of

trademark rights. E.g., CELLOPHANE, ASPIRIN. ○ Issues of enforcement.

Who can bring suit? Who is damaged? Discovery for multiple companies.

○ In the US, only the “owner” of the mark is entitled to the regis-tration. 15 U.S.C. § 1051(a)(1). Filings could be void ab initio if filed in the name of the wrong entity.

○ Tax implications. Intercompany licensing

○ Needs to be arm’s length. ○ Royalties

Rate should be comparable to third party licenses. Royalties also have to comply with transfer pricing guide-

lines, which is how companies charge their related com-panies/holding companies/subsidiaries for goods and services.

DHL case ○ DHL (US company) owned the US rights to the mark. ○ DHL enters into a royalty-free license with DHLI (International) ○ DHLI files TM applications outside the US and pays for reg-

istrations, enforcement and advertising. Acts like the trademark owner.

○ In connection with due diligence for an acquisition by foreign investors in 1992, an issue was identified. The IRS could impute a royalty from DHLI’s use of DHL’s trademark. It was rec-ommended that DHLI purchase the DHL trademark, which was valued at $20M.

1-354

© Practising Law Institute

9

○ IRS Audit IRS argued that DHL owned the worldwide rights, making

the value $600M, and (despite the license agreement), DHL argued that DHL owned only the US rights, making the value $20M.

IRS took the position that royalties should have been paid for 1990-92 for use of DHL by DHLI. Assessed transfer pricing penalties of $163M.

Structure and Purpose of the Holding Company ○ Avoid sham structure

Employees by the holding company at the location Economic substance and business purpose Pay for all related expenses Formal license agreements with related companies

○ Manage the trademarks and use by related companies and third parties Enforce quality control Enforce/police marks Collect royalties

ROYALTY AUDITS

Are licensees paying all royalties due? See attached Charles Rivers Associates “Licensing and Royalty

Audits” document

INSURANCE

Liability runs up the chain to the licensor who is responsible for the torts of its licensees and franchisees

Not just traditional product liability any more – cyberliability issues. Naming licensor as additional named insured Need to understand and carefully draft an insurance clause that that

is tailored to the specifics of the transaction.

1-355

© Practising Law Institute

10

Get insurance counsel and possibly a broker involved. There are too many terms of art involved, e.g., aggregate limits, primary and non-contributory, separation of insureds, severability of interests, tail coverage.

See attached Willis Towers Watson document that provides an over-view of various types of business insurance.

1-356

© Practising Law Institute

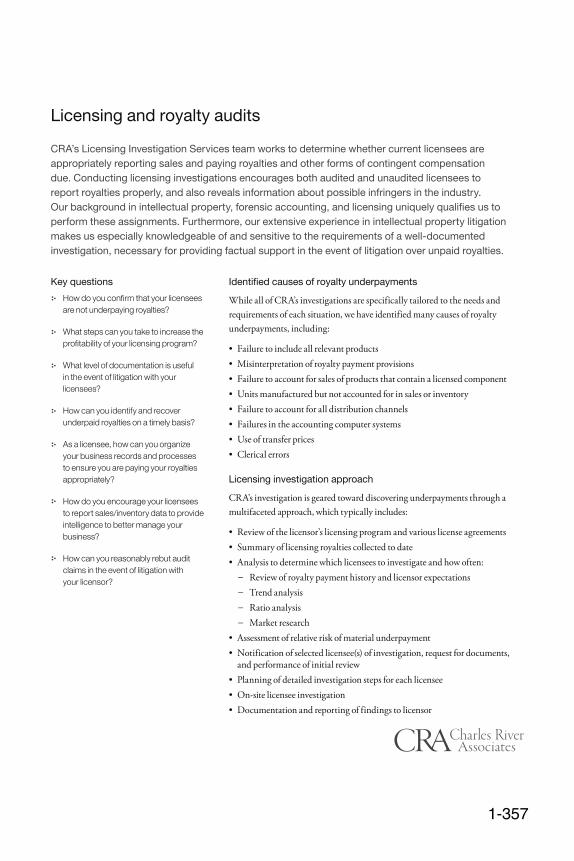

Licensing and royalty audits

CRA’s Licensing Investigation Services team works to determine whether current licensees are appropriately reporting sales and paying royalties and other forms of contingent compensation due. Conducting licensing investigations encourages both audited and unaudited licensees to report royalties properly, and also reveals information about possible infringers in the industry. Our background in intellectual property, forensic accounting, and licensing uniquely qualifies us to perform these assignments. Furthermore, our extensive experience in intellectual property litigation makes us especially knowledgeable of and sensitive to the requirements of a well-documented investigation, necessary for providing factual support in the event of litigation over unpaid royalties.

Key questions

How do you confirm that your licensees are not underpaying royalties?

What steps can you take to increase the profitability of your licensing program?

What level of documentation is useful in the event of litigation with your licensees?

How can you identify and recover underpaid royalties on a timely basis?

As a licensee, how can you organize your business records and processes to ensure you are paying your royalties appropriately?

How do you encourage your licensees to report sales/inventory data to provide intelligence to better manage your business?

How can you reasonably rebut audit claims in the event of litigation with your licensor?

Identified causes of royalty underpayments

While all of CRA’s investigations are specifically tailored to the needs and requirements of each situation, we have identified many causes of royalty underpayments, including:

• Failure to include all relevant products • Misinterpretation of royalty payment provisions • Failure to account for sales of products that contain a licensed component • Units manufactured but not accounted for in sales or inventory • Failure to account for all distribution channels • Failures in the accounting computer systems • Use of transfer prices • Clerical errors

Licensing investigation approach

CRA’s investigation is geared toward discovering underpayments through a multifaceted approach, which typically includes:

• Review of the licensor’s licensing program and various license agreements • Summary of licensing royalties collected to date • Analysis to determine which licensees to investigate and how often:

– Review of royalty payment history and licensor expectations– Trend analysis– Ratio analysis– Market research

• Assessment of relative risk of material underpayment • Notification of selected licensee(s) of investigation, request for documents, and performance of initial review

• Planning of detailed investigation steps for each licensee • On-site licensee investigation • Documentation and reporting of findings to licensor

1-357

© Practising Law Institute

Case studies

• A US affiliate of a global video systems and games manufacturer retained CRA to investigate the royalty payments received from one of its distribution licensees. Pre-site analysis included preparation of document and information requests and verification of the mathematical accuracy of the royalty statements. On-site inspection and post-site analysis involved detailed reconciliation of the royalty statements with licensee documents, including sales invoices, inventory records, credit memos, and financial statements. Through the efforts described above, CRA identified and formally documented underreported royalties in excess of $600,000.

• A creator of graphic arts retained CRA to assist in the development and implementation of a companywide, global licensing program. CRA developed a policies and procedures manual for licensing activities, drafted a general audit workplan, and evaluated the appropriateness of an existing licensee’s royalty payments.

• A US city retained a CRA expert to review the completeness of rent payments from a music and live entertainment amphitheater, as part of a counterclaim against the owners of that amphitheater. The findings report that was issued to the city regarding underpaid rent from ticket sales, concessions, merchandising, and sponsorship revenue resulted in a dismissal of the venue owner’s claim, as well as a $30 million settlement paid to the city.

• A major computer manufacturer engaged CRA to investigate the royalty payments of several licensees in Europe and Asia of a patent for an important computer component. CRA conducted extensive pre-site analyses in preparation for on-site visits to each licensee, and identified several million dollars in underpaid royalties.

• A college research foundation licensed the use of its proprietary protein growth technology to a major US biotechnology company. The foundation suspected that the company was underpaying its royalty obligations, and retained CRA to perform a royalty audit. CRA consultants with expertise in microbiology interviewed the licensee’s technical personnel, revealing that numerous products, which were being produced using the licensed process, had been excluded from royalty calculations. The licensee had previously denied that these products were produced using the licensed technology. Additionally, it was discovered that the licensee had failed to pay royalties on various products produced for “research” purposes.

• A dispute between a video game publisher and the developer of a console game franchise resulted in a CRA expert being retained as a court-appointed independent expert charged with reviewing the reported contingent compensation stemming from more than $3 billion in worldwide sales. On-site inspection and post-site analysis identified certain underpayment issues while otherwise confirming the material reasonableness of amounts reported to the developer. The issuance of the findings report led the parties to reach a confidential settlement.

Contact

Sabera Choudhury Principal Chicago +1-312-377-2335 [email protected]

www.crai.com/ip

Copyright 2016 Charles River Associates

Licensing and royalty audits

1-358

© Practising Law Institute

Insurance Coverage Overview

March 7, 2016

1-359

© Practising Law Institute

1-360

© Practising Law Institute

P a g e 1 |

Description of Insurance Policies/Coverages (Domestic) 1. General Liability. A standard insurance policy issued to business organizations to protect them

against liability claims for bodily injury (BI) and property damage (PD) arising out of premises, operations, products, and completed operations; and advertising and personal injury (PI) liability.

2. Commercial Property. A standard insurance policy issued to business organizations to protect them against direct physical damage to covered property from a covered peril. Covered property includes buildings, inventory, office furniture & fixtures, leasehold improvements and business interruption.

3. Business Interruption coverage. Insurance coverage for loss of your net income suffered by a business organization as a result of not being able to use property damaged by a covered cause of loss during the time required to repair or replace it. A simple formula for BI is “net income + continuing expense + extra-ordinary expenses”.

4. Hired & Non-Owned Automobile. Hired provides coverage when a vehicle is rented for business. Non-owned covers an auto that is used in connection with the Named Insured’s business but that is neither owned, leased, hired, rented, nor borrowed by the named insured. In other words, it applies to employees using their own vehicles on company business (but it excludes the owner of the vehicle).

5. Workers Compensation. The system by which no-fault statutory benefits prescribed in state law are provided by an employer to an employee (or the employee's family) due to a job-related injury (including death) resulting from an accident or occupational disease. Part One of the policy covers the employer's statutory liabilities under workers compensation laws, and Part Two covers liability arising out of employees' work-related injuries that do not fall under the workers compensation statute.

6. Employee Benefits Liability. Coverage provided under the General Liability, protects an employer for an error or omission in the administration of an employee benefit program.

7. Excess/Umbrella. A policy designed to provide protection against catastrophic losses. It generally is written over various primary liability policies, such as the business auto policy (BAP), commercial general liability (CGL) policy, and employers’ liability coverage (WC). The umbrella policy serves three purposes: it provides excess limits when the limits of underlying liability policies are exhausted by the payment of claims; it drops down and picks up where the underlying policy leaves off when the aggregate limit of the underlying policy in question is exhausted by the payment of claims; and it provides protection against some claims not covered by the underlying policies, subject to the assumption by the named insured of a self-insured retention (SIR).

8. Technology Errors & Omissions Insurance. A type of insurance designed to cover providers of technology services or products. Tech E&O policies cover both liability and property loss exposures. Major liability insuring agreements include losses resulting from: (1) technology services, (2) technology products, (3) media content, and (4) network security breaches. Key property insuring

1-361

© Practising Law Institute

P a g e 2 |

agreements provide coverage for extortion threats, crisis management expense, and business interruption.

9. Cyber and Privacy Insurance. A type of insurance designed to cover consumers of technology services or products. More specifically, the policies are intended to cover a variety of both liability and property losses that may result when a business engages in various electronic activities, such as selling on the Internet or collecting data within its internal electronic network.

Most notably, but not exclusively, cyber and privacy policies cover a business' liability for a data breach in which the firm's customers' personal information, such as Social Security or credit card numbers, is exposed or stolen by a hacker or other criminal who has gained access to the firm's electronic network. The policies cover a variety of expenses associated with data breaches, including: notification costs, credit monitoring, costs to defend claims by state regulators, fines and penalties, and loss resulting from identity theft.

In addition, the policies cover liability arising from website media content, as well as property exposures from: (a) business interruption, (b) data loss/destruction, (c) computer fraud, (d) funds transfer loss, and (e) cyber extortion.

Cyber and privacy insurance is often confused with technology errors and omissions (tech E&O) insurance. In contrast to cyber and privacy insurance, tech E&O coverage is intended to protect providers of technology products and services, such as computer software and hardware manufacturers, website designers, and firms that store corporate data on an off-site basis. Nevertheless, tech E&O insurance policies do contain a number of the same insuring agreements as cyber and privacy policies.

10. Commercial Crime policy. A crime insurance policy that is designed to meet the needs of organizations other than financial institutions (such as banks). A commercial crime policy typically provides several different types of crime coverage, such as: employee dishonesty coverage; forgery or alteration coverage; computer fraud coverage; funds transfer fraud coverage; kidnap, ransom, or extortion coverage; money and securities coverage; and money orders and counterfeit money coverage.

11. Directors and Officers Liability. A type of liability insurance covering directors and officers for claims made against them while serving on a board of directors and/or as an officer. D&O liability insurance can be written to cover the directors and officers of for-profit businesses, privately held firms, not-for-profit organizations, and educational institutions. In effect, the policies function as "management errors and omissions liability insurance," covering claims resulting from managerial decisions that have adverse financial consequences.

12. Employment Practices Liability. A type of liability insurance covering wrongful acts arising from the employment process. The most frequent types of claims covered under such policies include: wrongful termination, discrimination, sexual harassment, and retaliation. In addition, the policies cover claims from a variety of other types of inappropriate workplace conduct, including (but not limited to) employment-related: defamation, invasion of privacy, failure to promote, deprivation of a career opportunity, and negligent evaluation. The policies cover directors and officers, management personnel, and employees as insureds.

1-362

© Practising Law Institute

P a g e 3 |

13. Fiduciary Liability. Insurance covering the responsibility on trustees, employers, fiduciaries, professional administrators, and the plan itself with respect to errors and omissions (E&O) in the administration of employee benefit programs as imposed by the Employee Retirement Income Security Act (ERISA).

14. Kidnap Ransom and Extortion. A type of insurance that covers losses arising from the kidnap and holding for ransom of a corporate employee or from the threat to do harm to a person or to certain property if a ransom is not paid. Accordingly, special crime policies are also termed "kidnap, ransom, and extortion" insurance. The policies generally cover some or all of the following perils: (1) kidnapping an insured person; (2) bodily injury (BI) extortion (a threat to kidnap, injure, or kill an insured person); (3) property damage (PD) extortion (a threat to damage or pollute property, tamper with the insured's product, or reveal a trade secret or other proprietary information of the insured); (4) wrongful detention (involuntary confinement of an insured person); or (5) hijacking. The categories of loss covered by the policies include ransom money payments; wrongful detention costs (costs of attempting to locate and secure the release of the victim); in transit/delivery expenses (for confiscation, disappearance, or destruction of ransom money during delivery); other expenses (reward payments to informants, interest on loans of ransom money, fees for security consultants); judgments, settlements, and defense costs (for lawsuits by a victim or victim's family alleging negligence on the part of the employer); and death or dismemberment payments (for a victim or insured person involved in handling the incident).

15. Business Travel Accident. Business travel accident insurance (aka “accidental death and dismemberment" insurance) is carried by many employers as an employee benefit. The policy provides scheduled benefits as a percentage or multiple of employees' compensation in the event they suffer a described injury or death, but only while traveling on company business.

1-363

© Practising Law Institute

P a g e 4 |

Description of Policies/Coverages and Terms (International) 1. Controlled Master Insurance Program. An insurance program for a multinational business

wherein the coverage terms and conditions apply on a blanket basis to all of the insured's international operations. Local underlying policies are issued overseas to support the centralized program. Unlike global insurance programs, master insurance programs do not typically include the United States in their coverage territory; a separate domestic program is usually arranged for U.S. multinationals under this approach.

2. Compulsory Insurance. Those lines of insurance that are required by law for companies operating in a particular territory; typically automobile third-party liability, work injury, and some forms of professional liability.

3. Freedom of Services. Insurance rules of the Member Countries of the European Economic Area (EEA) were harmonized in order to develop and encourage a single insurance market in the European Union. The FoS enables an insurer based in one country of the EEA to underwrite and service risks in any of the other EEA countries under one insurance contract. The benefit of the FoS is that it is an admitted insurance contract in the EEA and can provide Primary and DIC/DIL coverage.

4. Admitted Insurance/”Ground-up”. A policy issued by insurer licensed or registered in that country.

5. Difference in Condition/Difference in Limits (DIC/DIL). A policy that “wrap” around local policy coverage on an excess/difference-in-conditions basis to bring available insurance up to the desired level of coverage.

6. U.K. EL. You must get Employers’ Liability (EL) insurance as soon as you become an employer - your policy must cover you for at least £10 million and come from an authorized insurer. This insurance will help you pay compensation if an employee is injured or becomes ill because of the work they do for you.

1-364

© Practising Law Institute

P a g e 5 |

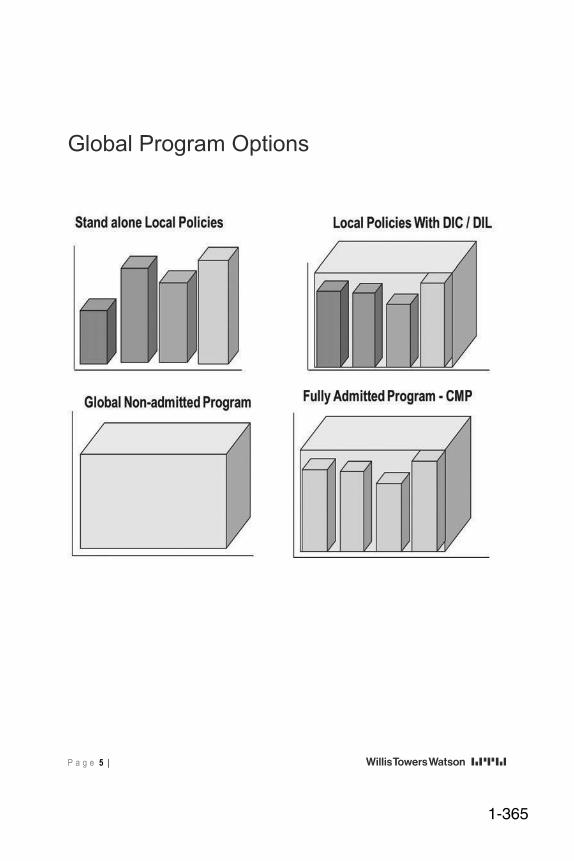

Global Program Options

1-365

© Practising Law Institute

NOTES

1-366