Embed Size (px)

Citation preview

© OECD/IEA 2014

Overview on Advanced Biofuels Developments

3rd GBEP Bioenergy Week Medan, 28 May 2015

Simone Landolina

and Adam Brown

© OECD/IEA 2014

Talk plan

Why biofuels are important

Advanced biofuels: outlook, markets, technologies

Crucial role of energy innovation… and oil prices!

© OECD/IEA 2014

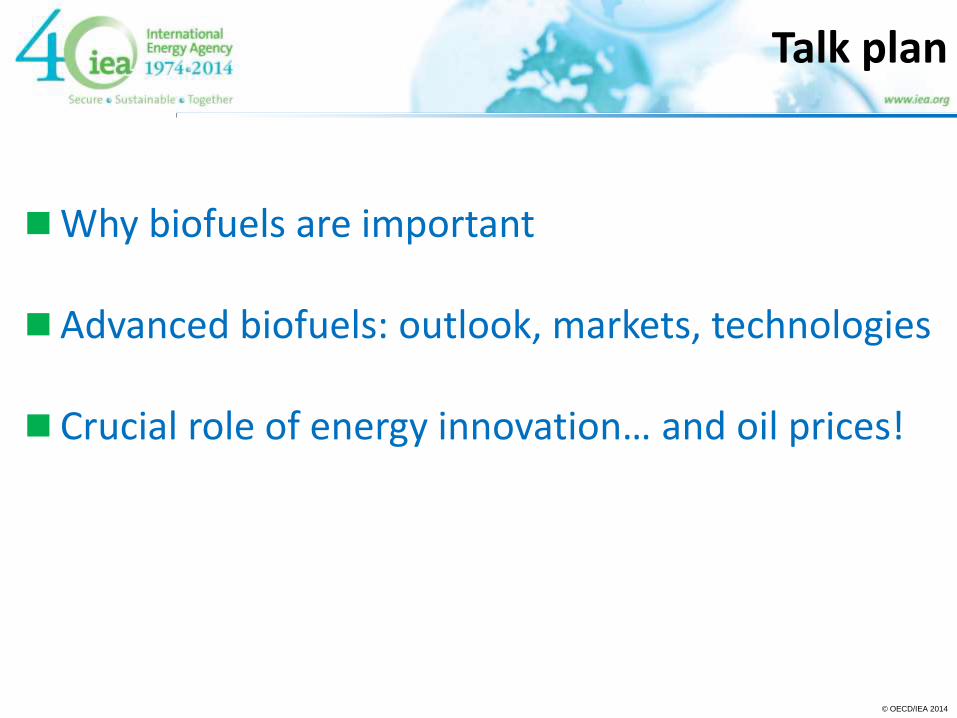

Bioenergy plays a role in all sectors

Global bioenergy use by sector in the IEA New Policies Scenario

Bioenergy increases in all sectors, except for the traditional use of solid biomass, reducing the need for fossil fuels and often increasing energy self-sufficiency

200

400

600

800

1 000 Mtoe 2012

2040

Traditional*

of which:

Power generation

Industry Transport Buildings Other

* Includes traditional use of solid biomass in households.

Source: World Energy

Outlook 2014

© OECD/IEA 2015

© OECD/IEA 2014

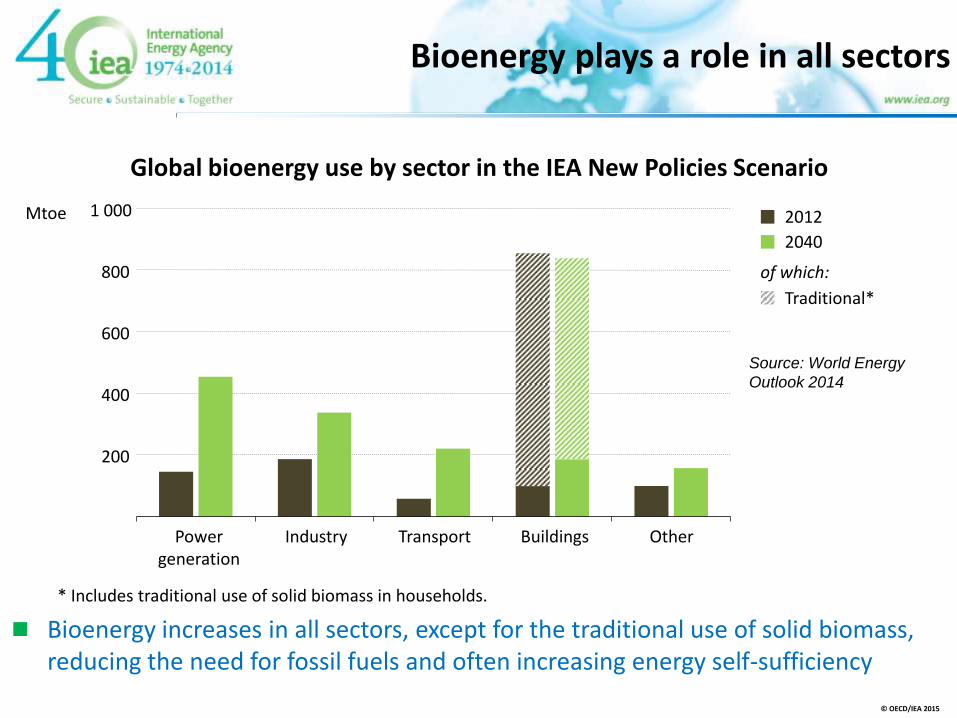

Biofuels Contribution to Emissions Reduction in Transport Sector

Efficiency improvements are the most important low-cost measure to reduce transport emissions

Biofuels can reduce global transport emissions by 2.1 Gt CO2-eq. in 2050

To achieve these reductions, all biofuels must provide considerable life-cycle GHG emission reductions

Source: IEA Technology Roadmap

Biofuels for Transport (2011)

© OECD/IEA 2015

© OECD/IEA 2014

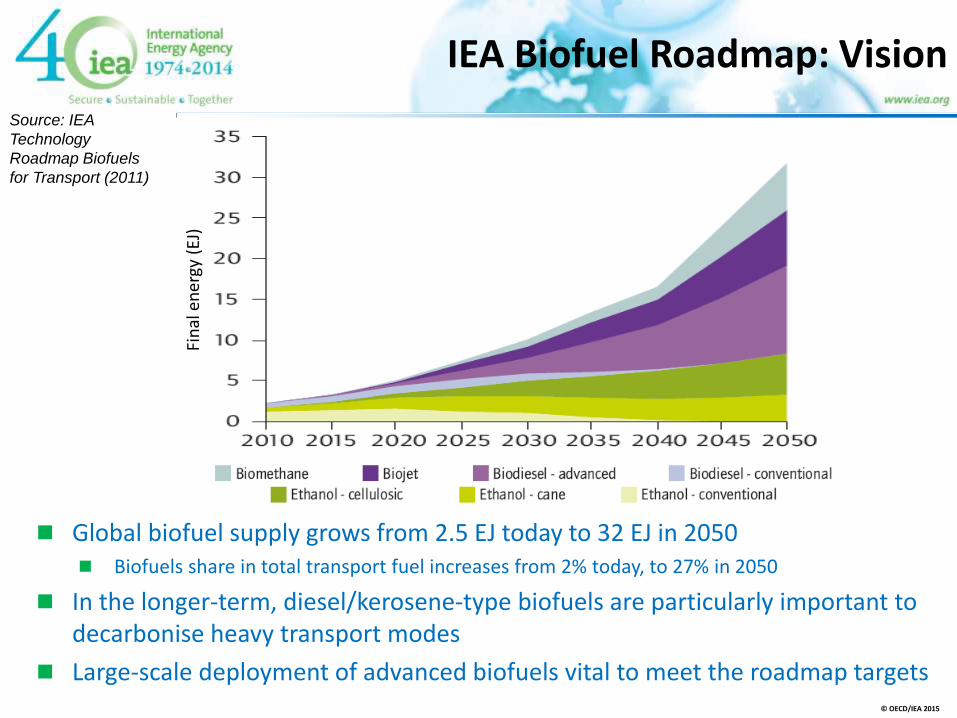

IEA Biofuel Roadmap: Vision

Global biofuel supply grows from 2.5 EJ today to 32 EJ in 2050 Biofuels share in total transport fuel increases from 2% today, to 27% in 2050

In the longer-term, diesel/kerosene-type biofuels are particularly important to decarbonise heavy transport modes

Large-scale deployment of advanced biofuels vital to meet the roadmap targets

Fin

al e

ner

gy (

EJ)

Source: IEA

Technology

Roadmap Biofuels

for Transport (2011)

© OECD/IEA 2015

© OECD/IEA 2014

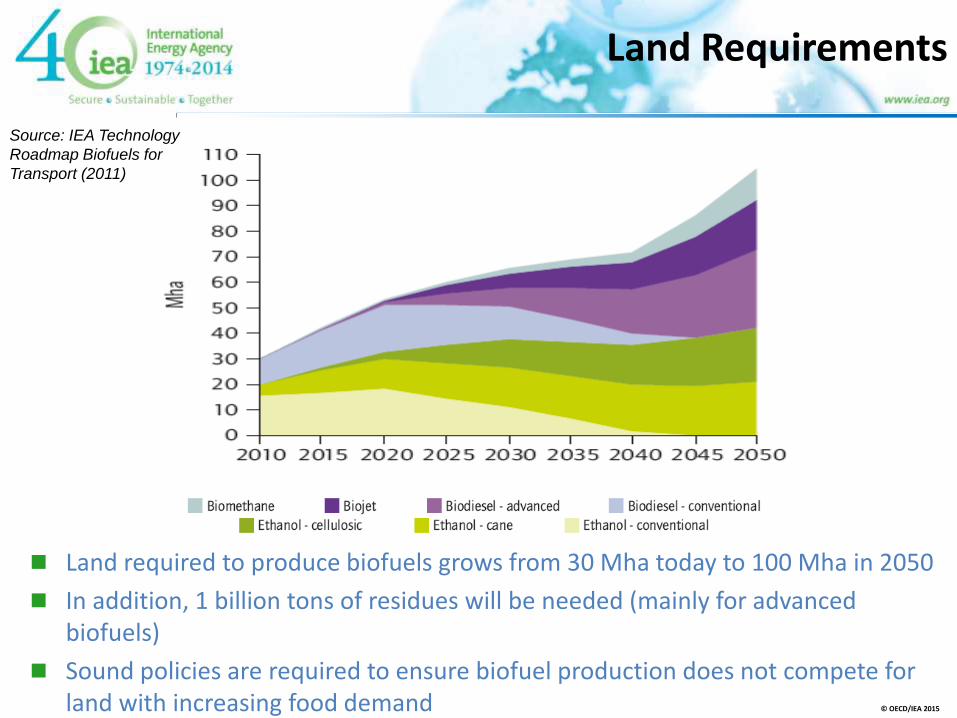

Land Requirements

Land required to produce biofuels grows from 30 Mha today to 100 Mha in 2050

In addition, 1 billion tons of residues will be needed (mainly for advanced biofuels)

Sound policies are required to ensure biofuel production does not compete for land with increasing food demand

Source: IEA Technology

Roadmap Biofuels for

Transport (2011)

© OECD/IEA 2015

© OECD/IEA 2014

When is a biofuel “advanced”?

Better C balance

Substitutes fossil fuel

Based on wastes/residues or efficient crops

© OECD/IEA 2015

© OECD/IEA 2014

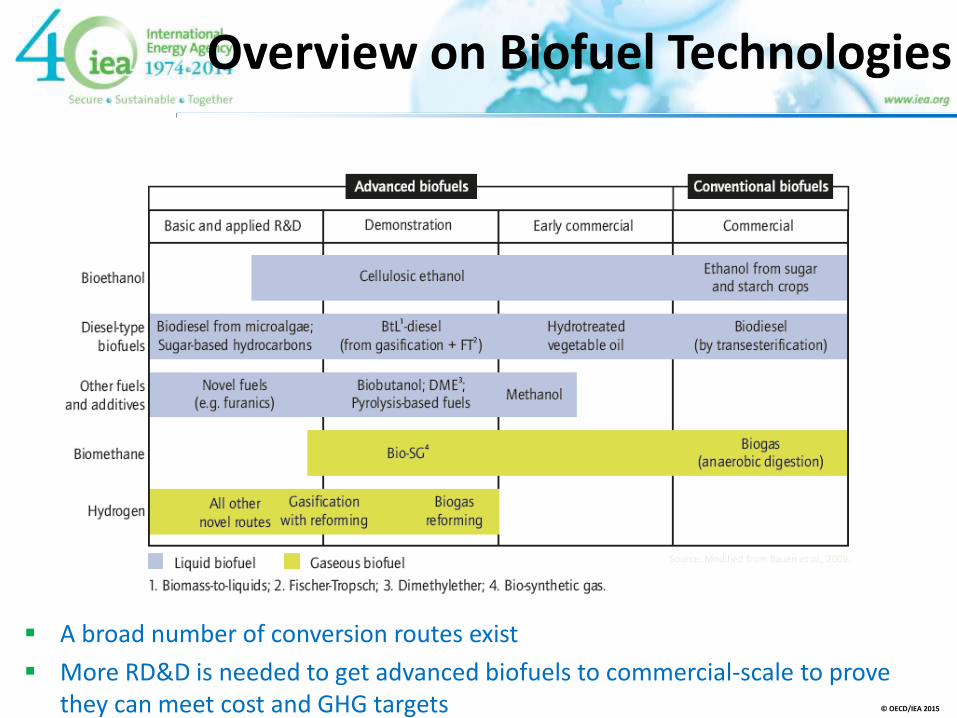

Overview on Biofuel Technologies

A broad number of conversion routes exist

More RD&D is needed to get advanced biofuels to commercial-scale to prove they can meet cost and GHG targets

Source: Modified from Bauen et al., 2009.

© OECD/IEA 2015

© OECD/IEA 2014

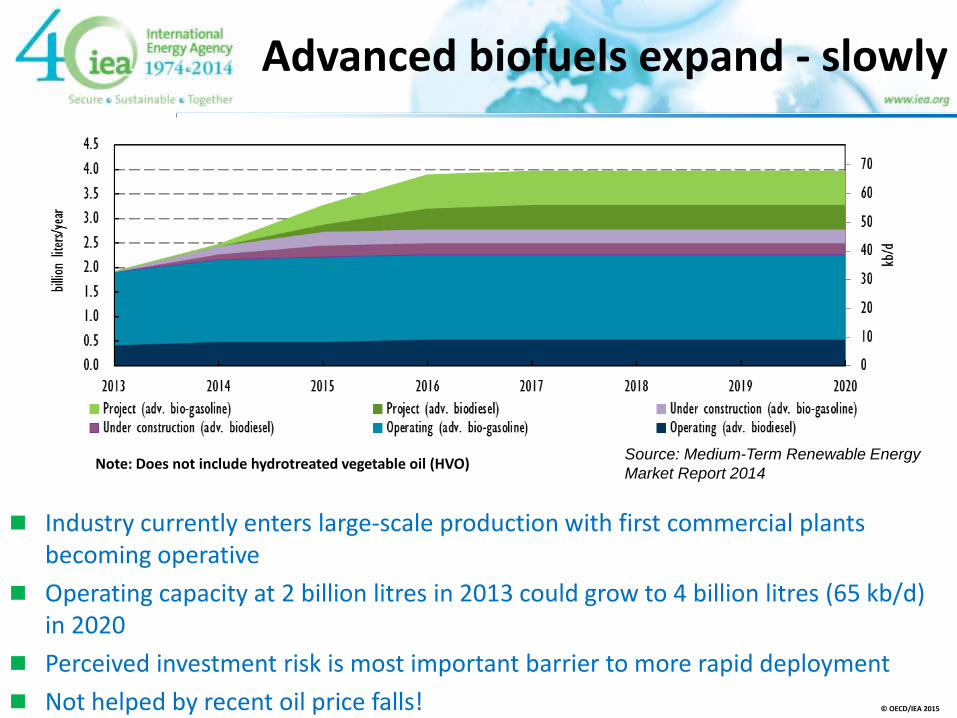

Advanced biofuels expand - slowly

Industry currently enters large-scale production with first commercial plants becoming operative

Operating capacity at 2 billion litres in 2013 could grow to 4 billion litres (65 kb/d) in 2020

Perceived investment risk is most important barrier to more rapid deployment

Not helped by recent oil price falls!

Note: Does not include hydrotreated vegetable oil (HVO)

© OECD/IEA 2015

Source: Medium-Term Renewable Energy

Market Report 2014

© OECD/IEA 2014

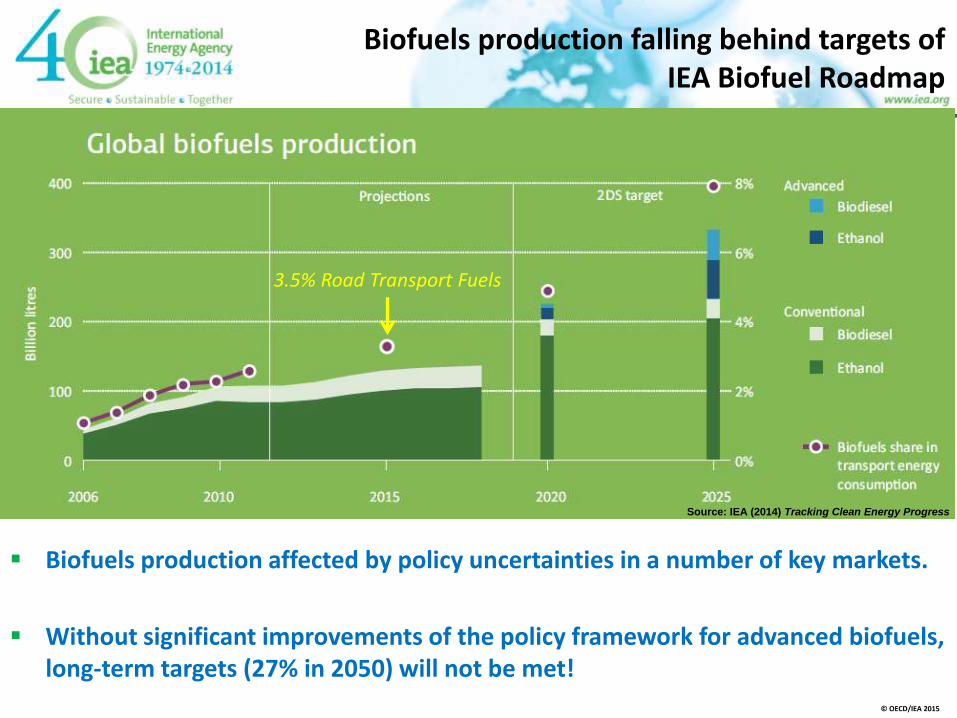

Biofuels production falling behind targets of IEA Biofuel Roadmap

Biofuels production affected by policy uncertainties in a number of key markets.

Without significant improvements of the policy framework for advanced biofuels, long-term targets (27% in 2050) will not be met!

Source: IEA (2014) Tracking Clean Energy Progress

© OECD/IEA 2015

3.5% Road Transport Fuels

© OECD/IEA 2014 © OECD/IEA 2015

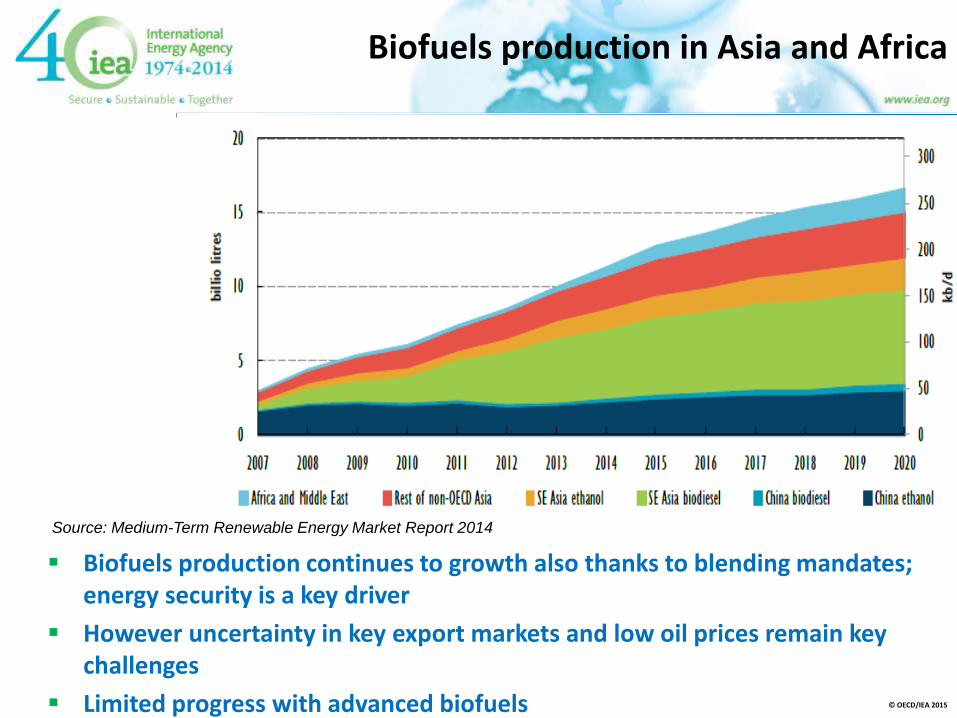

Biofuels production continues to growth also thanks to blending mandates; energy security is a key driver

However uncertainty in key export markets and low oil prices remain key challenges

Limited progress with advanced biofuels

Source: Medium-Term Renewable Energy Market Report 2014

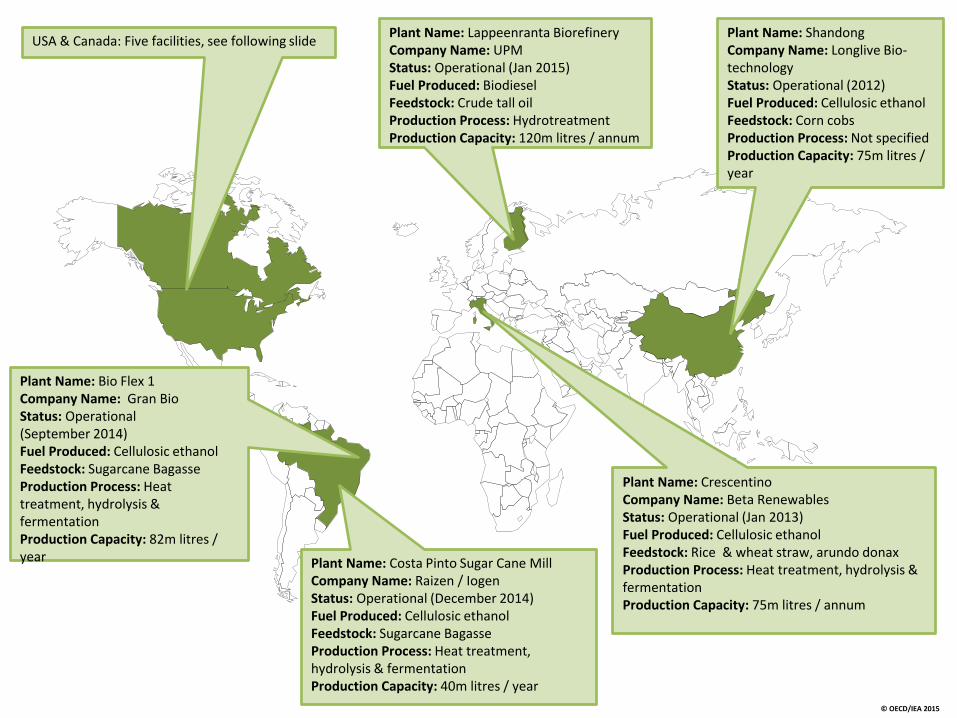

Biofuels production in Asia and Africa

Plant Name: Lappeenranta Biorefinery Company Name: UPM Status: Operational (Jan 2015) Fuel Produced: Biodiesel Feedstock: Crude tall oil Production Process: Hydrotreatment Production Capacity: 120m litres / annum

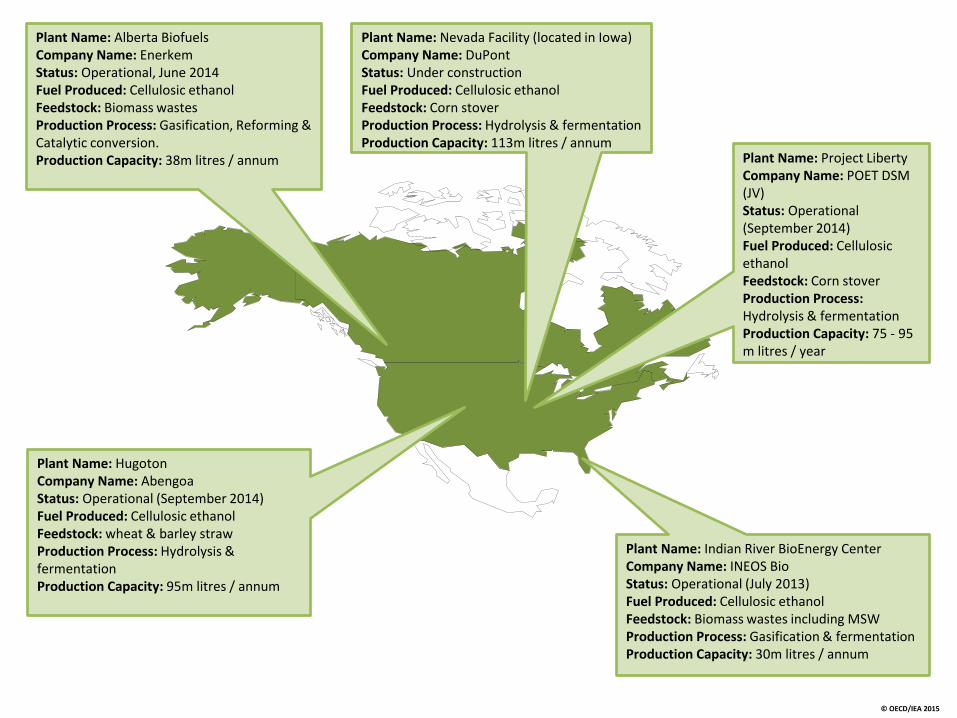

USA & Canada: Five facilities, see following slide

Plant Name: Crescentino Company Name: Beta Renewables Status: Operational (Jan 2013) Fuel Produced: Cellulosic ethanol Feedstock: Rice & wheat straw, arundo donax Production Process: Heat treatment, hydrolysis & fermentation Production Capacity: 75m litres / annum

Plant Name: Bio Flex 1 Company Name: Gran Bio Status: Operational (September 2014) Fuel Produced: Cellulosic ethanol Feedstock: Sugarcane Bagasse Production Process: Heat treatment, hydrolysis & fermentation Production Capacity: 82m litres / year Plant Name: Costa Pinto Sugar Cane Mill

Company Name: Raizen / Iogen Status: Operational (December 2014) Fuel Produced: Cellulosic ethanol Feedstock: Sugarcane Bagasse Production Process: Heat treatment, hydrolysis & fermentation Production Capacity: 40m litres / year

Plant Name: Shandong Company Name: Longlive Bio-technology Status: Operational (2012) Fuel Produced: Cellulosic ethanol Feedstock: Corn cobs Production Process: Not specified Production Capacity: 75m litres / year

© OECD/IEA 2015

Plant Name: Nevada Facility (located in Iowa) Company Name: DuPont Status: Under construction Fuel Produced: Cellulosic ethanol Feedstock: Corn stover Production Process: Hydrolysis & fermentation Production Capacity: 113m litres / annum

Plant Name: Indian River BioEnergy Center Company Name: INEOS Bio Status: Operational (July 2013) Fuel Produced: Cellulosic ethanol Feedstock: Biomass wastes including MSW Production Process: Gasification & fermentation Production Capacity: 30m litres / annum

Plant Name: Hugoton Company Name: Abengoa Status: Operational (September 2014) Fuel Produced: Cellulosic ethanol Feedstock: wheat & barley straw Production Process: Hydrolysis & fermentation Production Capacity: 95m litres / annum

Plant Name: Project Liberty Company Name: POET DSM (JV) Status: Operational (September 2014) Fuel Produced: Cellulosic ethanol Feedstock: Corn stover Production Process: Hydrolysis & fermentation Production Capacity: 75 - 95 m litres / year

Plant Name: Alberta Biofuels Company Name: Enerkem Status: Operational, June 2014 Fuel Produced: Cellulosic ethanol Feedstock: Biomass wastes Production Process: Gasification, Reforming & Catalytic conversion. Production Capacity: 38m litres / annum

© OECD/IEA 2015

© OECD/IEA 2014

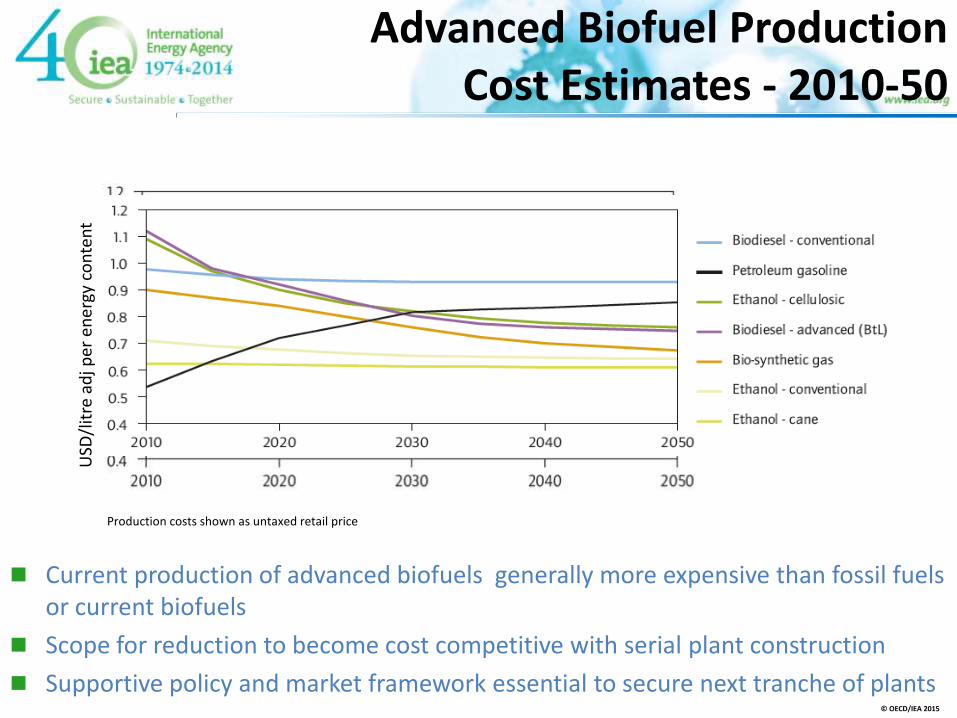

Advanced Biofuel Production Cost Estimates - 2010-50

Current production of advanced biofuels generally more expensive than fossil fuels or current biofuels

Scope for reduction to become cost competitive with serial plant construction

Supportive policy and market framework essential to secure next tranche of plants

Production costs shown as untaxed retail price

© OECD/IEA 2015

USD

/lit

re a

dj p

er e

ner

gy c

on

ten

t

© OECD/IEA 2014

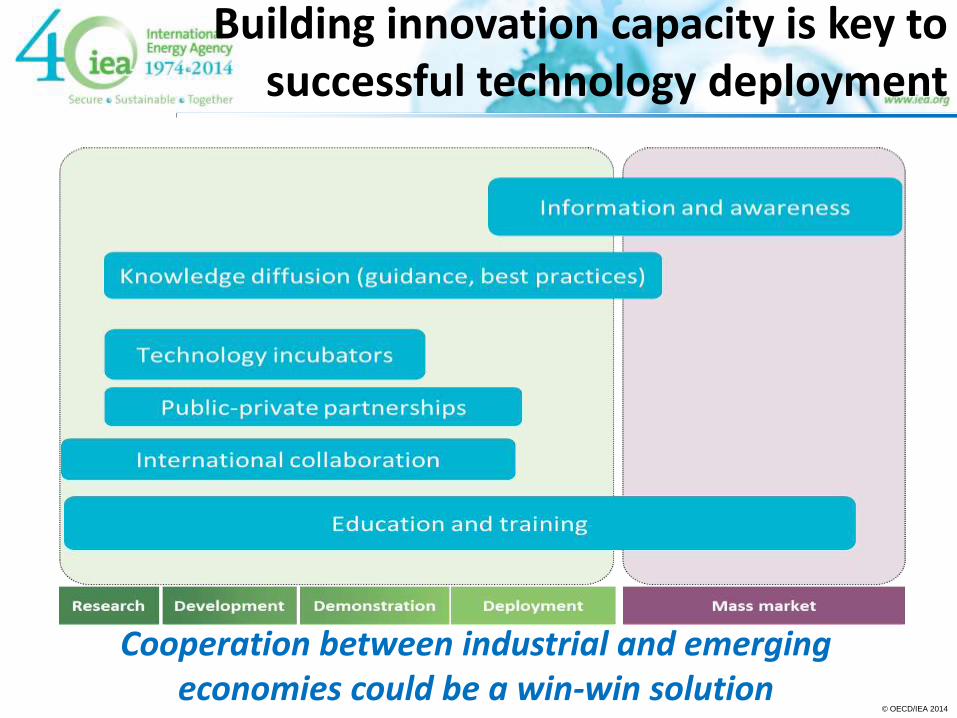

Building innovation capacity is key to successful technology deployment

Cooperation between industrial and emerging economies could be a win-win solution

© OECD/IEA 2014

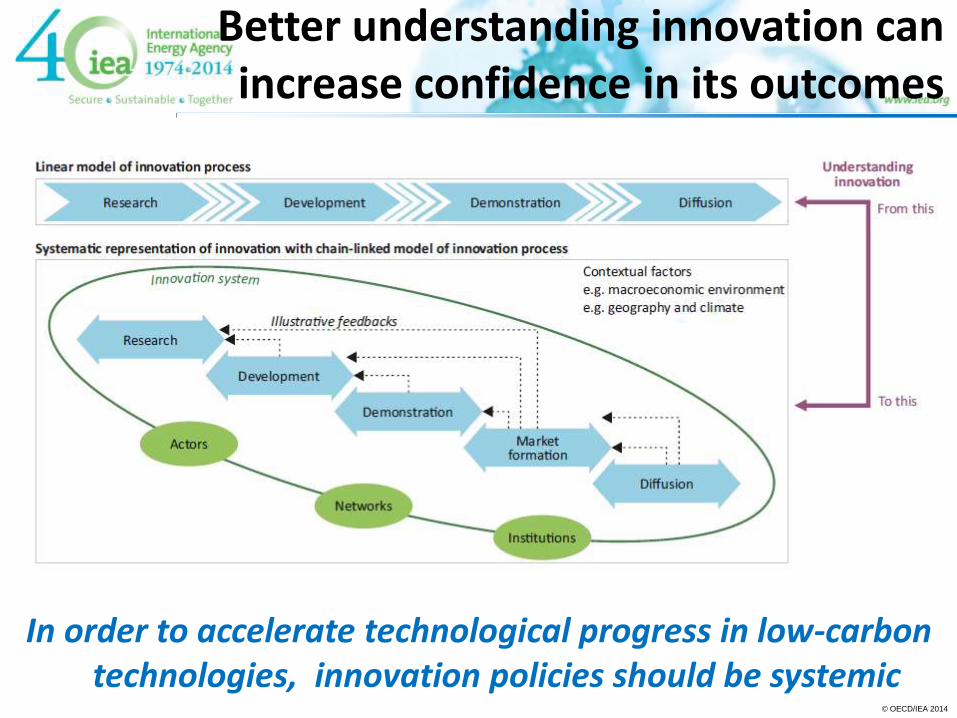

Better understanding innovation can increase confidence in its outcomes

In order to accelerate technological progress in low-carbon technologies, innovation policies should be systemic

© OECD/IEA 2014

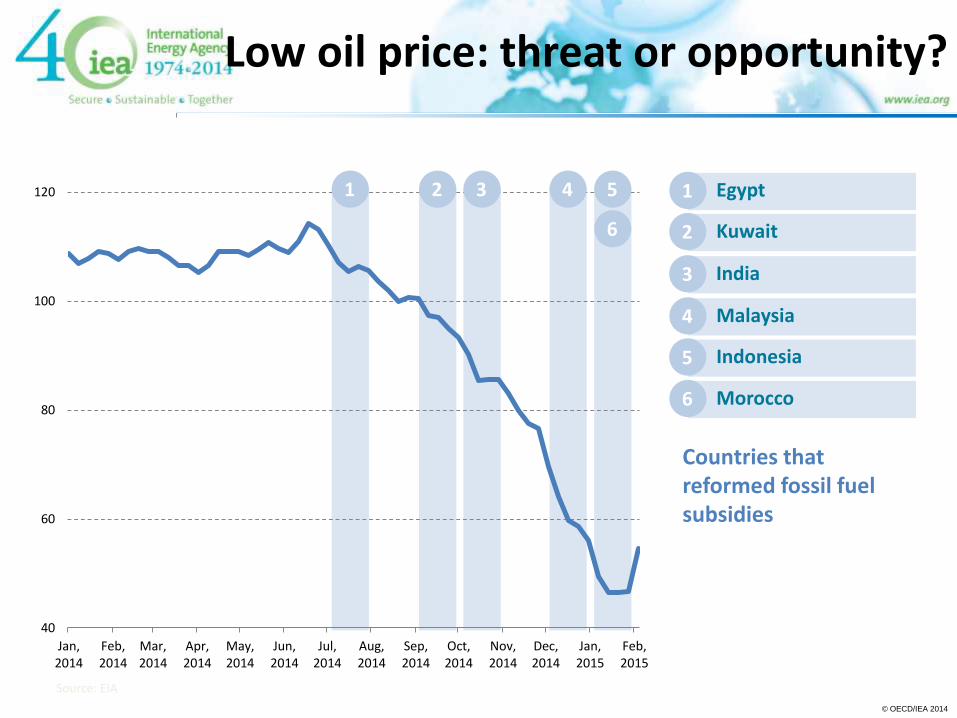

Low oil price: threat or opportunity?

Source: EIA

1 Egypt

2 Kuwait

3 India

4 Malaysia

5 Indonesia

6 Morocco

40

60

80

100

120

Jan,2014

Feb,2014

Mar,2014

Apr,2014

May,2014

Jun,2014

Jul,2014

Aug,2014

Sep,2014

Oct,2014

Nov,2014

Dec,2014

Jan,2015

Feb,2015

6

1 2 4 5 3

Countries that reformed fossil fuel subsidies

© OECD/IEA 2014

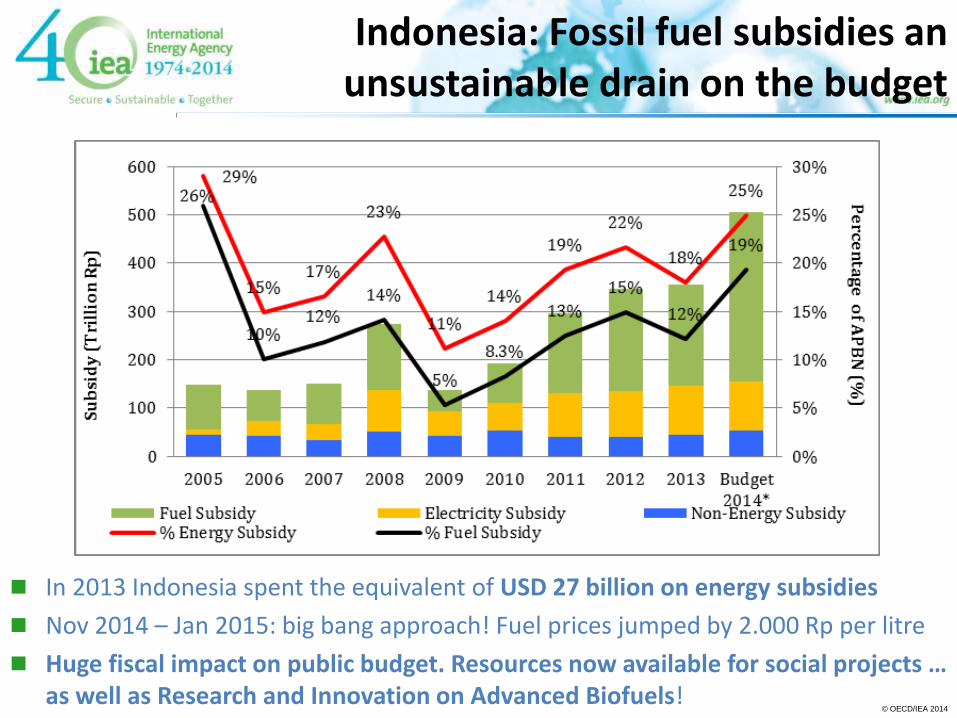

Indonesia: Fossil fuel subsidies an unsustainable drain on the budget

In 2013 Indonesia spent the equivalent of USD 27 billion on energy subsidies

Nov 2014 – Jan 2015: big bang approach! Fuel prices jumped by 2.000 Rp per litre

Huge fiscal impact on public budget. Resources now available for social projects … as well as Research and Innovation on Advanced Biofuels!

© OECD/IEA 2014

Conclusions

Advanced biofuels an essential step to a low carbon transport sector

Offer good carbon savings and lower land-use impacts than conventional biofuels

Progress has been slower than hoped for, and well below road map expectations.

Interesting developments with large scale demonstration of technology but products not yet cost competitive R&D

A supportive policy framework which allows the next generation of plants to be built and operated is essential, perhaps by providing loan guarantees and by creating quota for such fuels

Low oil prices represent a unique opportunity for subsidy reform

© OECD/IEA 2015

© OECD/IEA 2014 © OECD/IEA 2015

Thank you for your attention!