Embed Size (px)

Citation preview

Full-year results

Twelve months ended 31st December 2012

Adrian Ringrose, Chief Executive

Tim Haywood, Group Finance Director

27th February 2013

Capital Markets Update

30 April 2013

Who you will be meeting

Phil Clark

Business Development

Director

George Franks

Managing Director –

Interserve International

Adrian Ringrose

Chief Executive

Tim Haywood

Group Finance Director

Lord Adonis

Ian Hayes

Operations Director

Today’s itinerary

• 2010-2015 development .Adrian Ringrose

• SustainAbilities Tim Haywood

• The healthcare market Phil Clark

• UK outsourcing and infrastructure Lord Adonis

• Support Services and Construction International George Franks

• Equipment Services Ian Hayes

• Lunch (approximately 1pm)

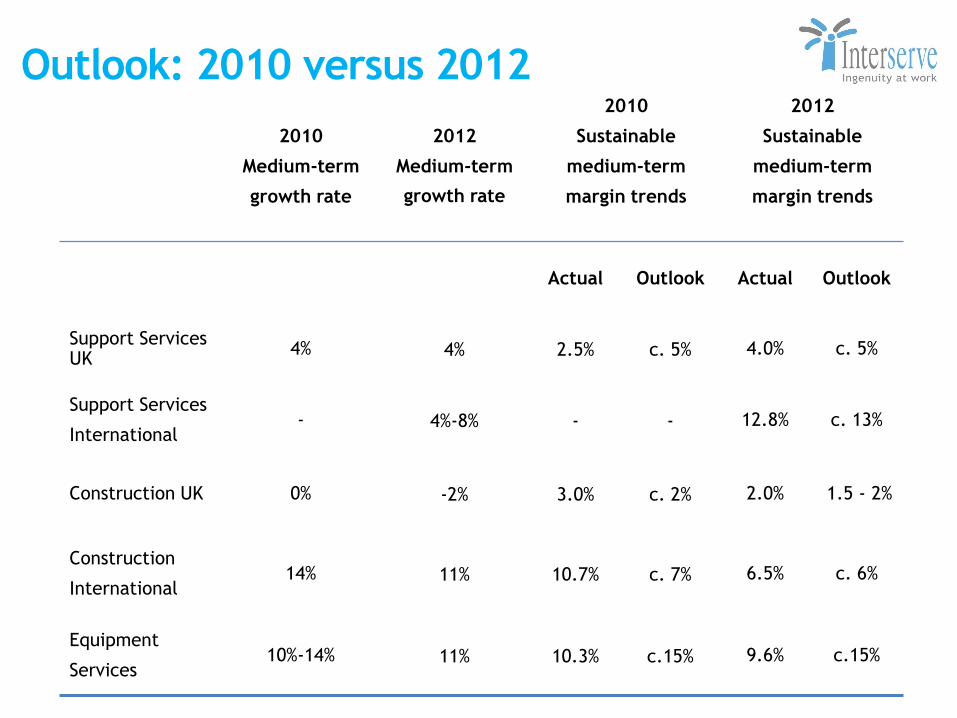

2010

Medium-term

growth rate

2012

Medium-term

growth rate

2010

Sustainable

medium-term

margin trends

2012

Sustainable

medium-term

margin trends

Actual Outlook Actual Outlook

Support Services UK

4% 4% 2.5% c. 5% 4.0% c. 5%

Support Services

International - 4%-8% - - 12.8% c. 13%

Construction UK 0% -2% 3.0% c. 2% 2.0% 1.5 - 2%

Construction

International 14% 11% 10.7% c. 7% 6.5% c. 6%

Equipment

Services 10%-14% 11% 10.3% c.15% 9.6% c.15%

Outlook: 2010 versus 2012

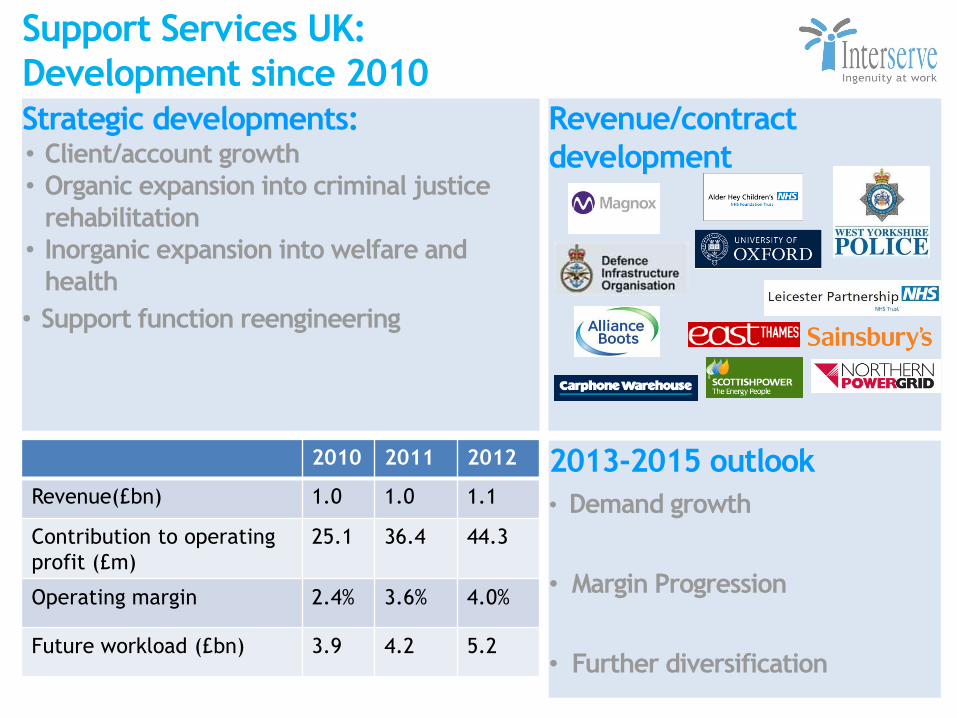

Support Services UK:

Development since 2010

Strategic developments: • Client/account growth

• Organic expansion into criminal justice

rehabilitation

• Inorganic expansion into welfare and

health

• Support function reengineering

2010 2011 2012

Revenue(£bn) 1.0 1.0 1.1

Contribution to operating

profit (£m)

25.1 36.4 44.3

Operating margin 2.4% 3.6% 4.0%

Future workload (£bn) 3.9 4.2 5.2

Revenue/contract

development

2013-2015 outlook

• Demand growth

• Margin Progression

• Further diversification

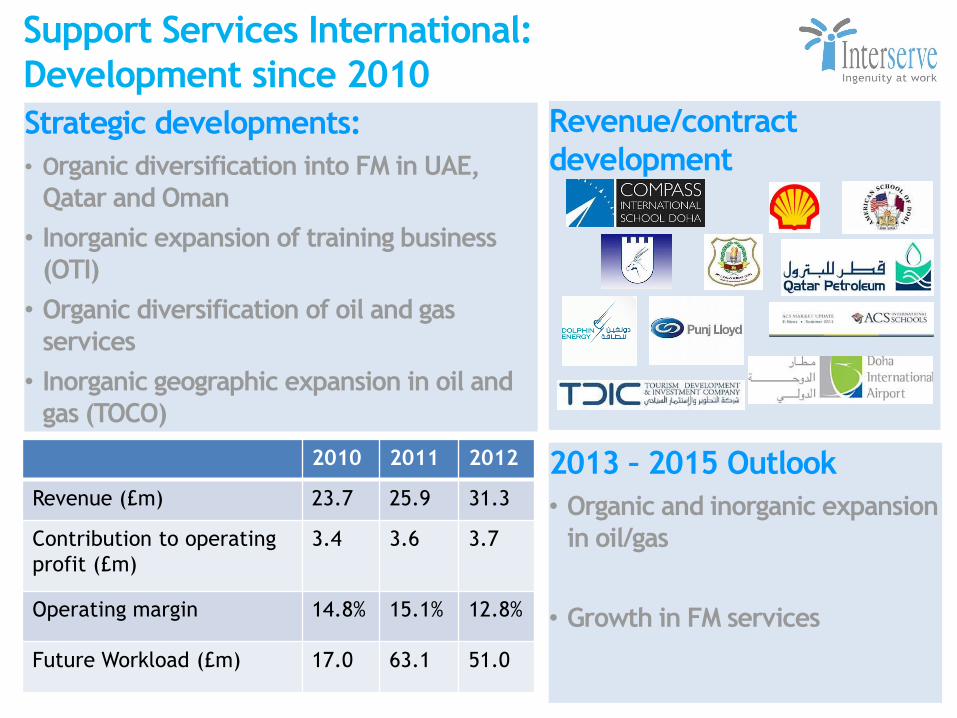

Support Services International:

Development since 2010

Strategic developments:

• Organic diversification into FM in UAE,

Qatar and Oman

• Inorganic expansion of training business

(OTI)

• Organic diversification of oil and gas

services

• Inorganic geographic expansion in oil and

gas (TOCO)

2010 2011 2012

Revenue (£m) 23.7 25.9 31.3

Contribution to operating

profit (£m)

3.4 3.6 3.7

Operating margin 14.8% 15.1% 12.8%

Future Workload (£m) 17.0 63.1 51.0

Revenue/contract

development

2013 – 2015 Outlook

• Organic and inorganic expansion

in oil/gas

• Growth in FM services

Revenue/contract

development

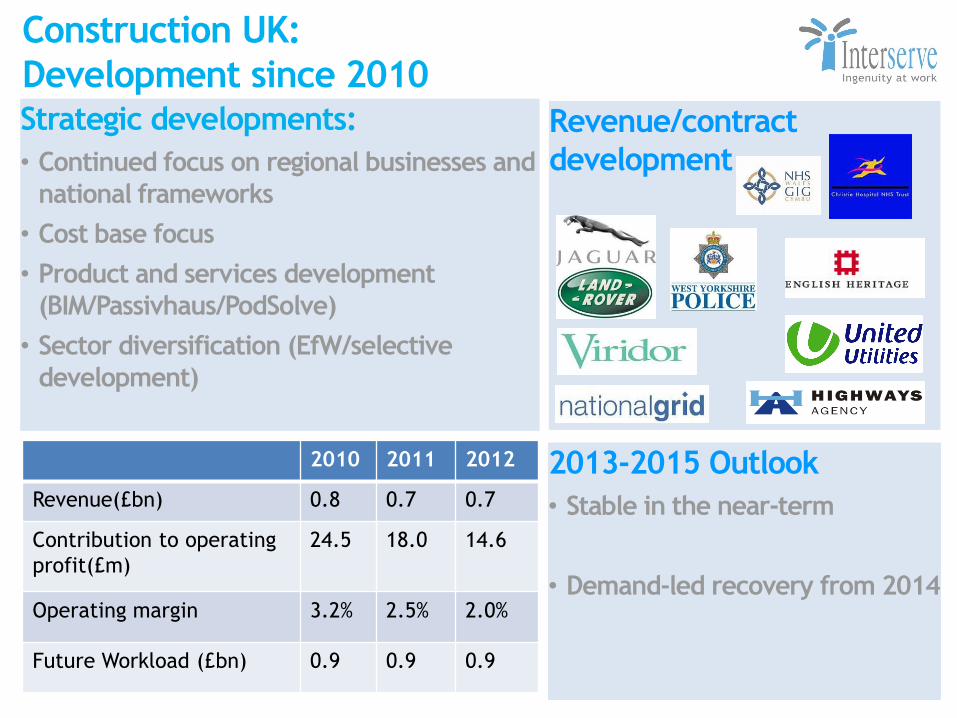

Construction UK:

Development since 2010

Strategic developments:

• Continued focus on regional businesses and

national frameworks

• Cost base focus

• Product and services development

(BIM/Passivhaus/PodSolve)

• Sector diversification (EfW/selective

development)

2010 2011 2012

Revenue(£bn) 0.8 0.7 0.7

Contribution to operating

profit(£m)

24.5 18.0 14.6

Operating margin 3.2% 2.5% 2.0%

Future Workload (£bn) 0.9 0.9 0.9

2013-2015 Outlook

• Stable in the near-term

• Demand-led recovery from 2014

Revenue/contract

development

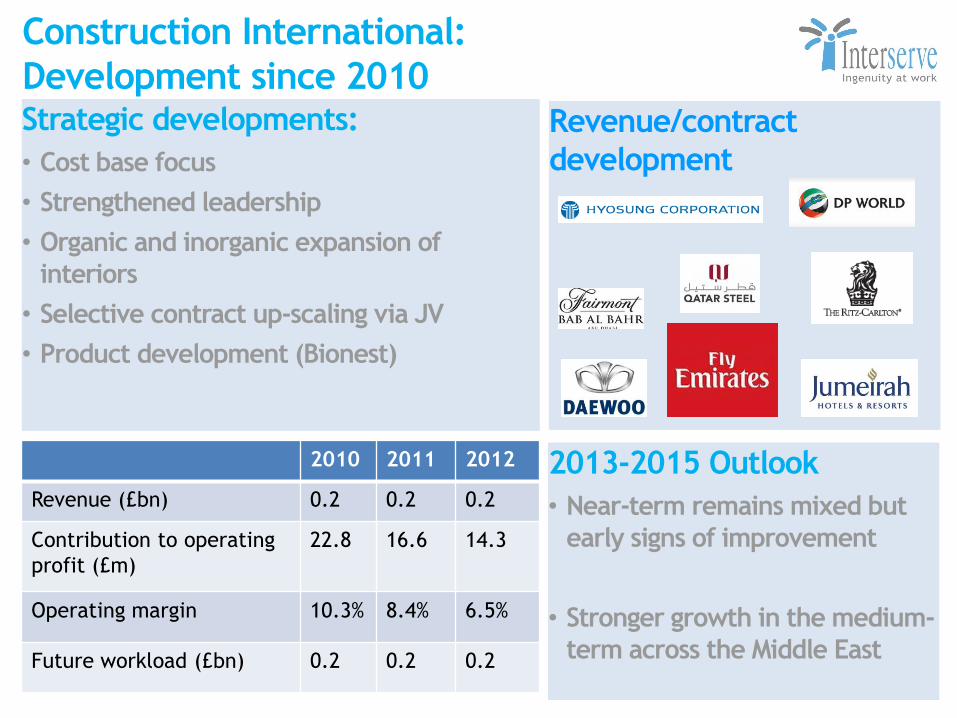

Construction International:

Development since 2010

Strategic developments:

• Cost base focus

• Strengthened leadership

• Organic and inorganic expansion of

interiors

• Selective contract up-scaling via JV

• Product development (Bionest)

2010 2011 2012

Revenue (£bn) 0.2 0.2 0.2

Contribution to operating

profit (£m)

22.8 16.6 14.3

Operating margin 10.3% 8.4% 6.5%

Future workload (£bn) 0.2 0.2 0.2

2013-2015 Outlook

• Near-term remains mixed but

early signs of improvement

• Stronger growth in the medium-

term across the Middle East

Equipment Services:

Development since 2010

Strategic developments:

• Global fleet management – Capex restraint

and increased transfers

• Flexible operating model

• Back-office off-shoring to high skill/low

cost geographies

• Geographical expansion

• Product Development

2010 2011 2012

Revenue (£m) 139.9 154.3 167.5

Contribution to operating

profit (£m)

14.4 13.6 16.0

Operating margin 10.3% 8.8% 9.6%

Cruise ship terminal, Hong Kong

2013-2015 outlook

• Development through flexible

global presence

• Individual markets mixed but

continued growth in the

portfolio

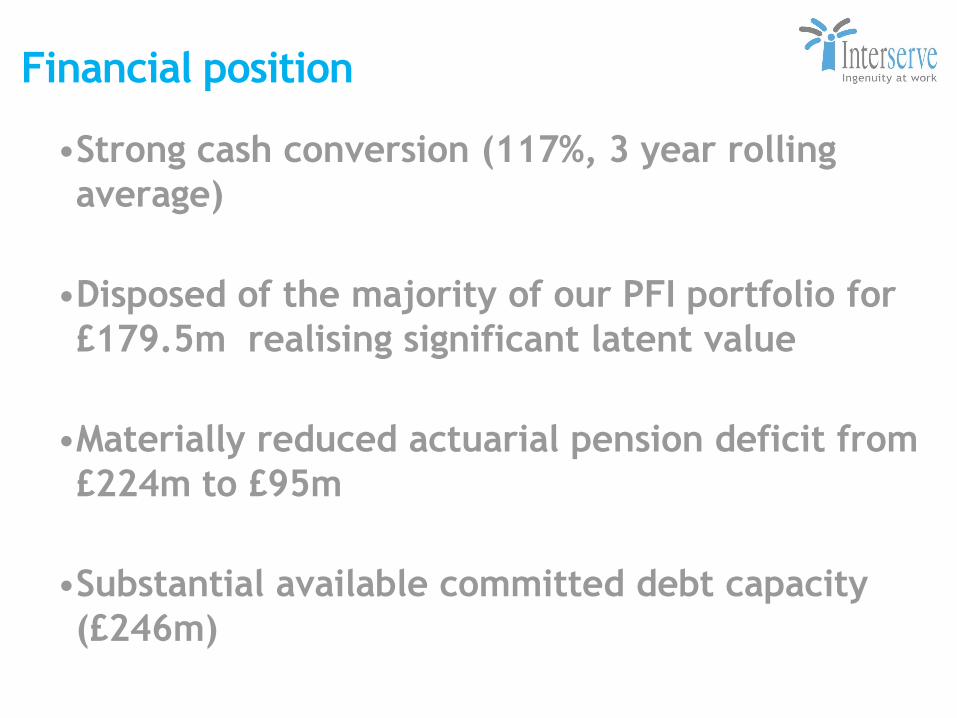

Financial position

•Strong cash conversion (117%, 3 year rolling

average)

•Disposed of the majority of our PFI portfolio for

£179.5m realising significant latent value

•Materially reduced actuarial pension deficit from

£224m to £95m

•Substantial available committed debt capacity

(£246m)

Group-wide developments

• Developing the Interserve brand

• Driving greater sustainability

• Account management

• Talent management

• Learning and development

• Health and Safety

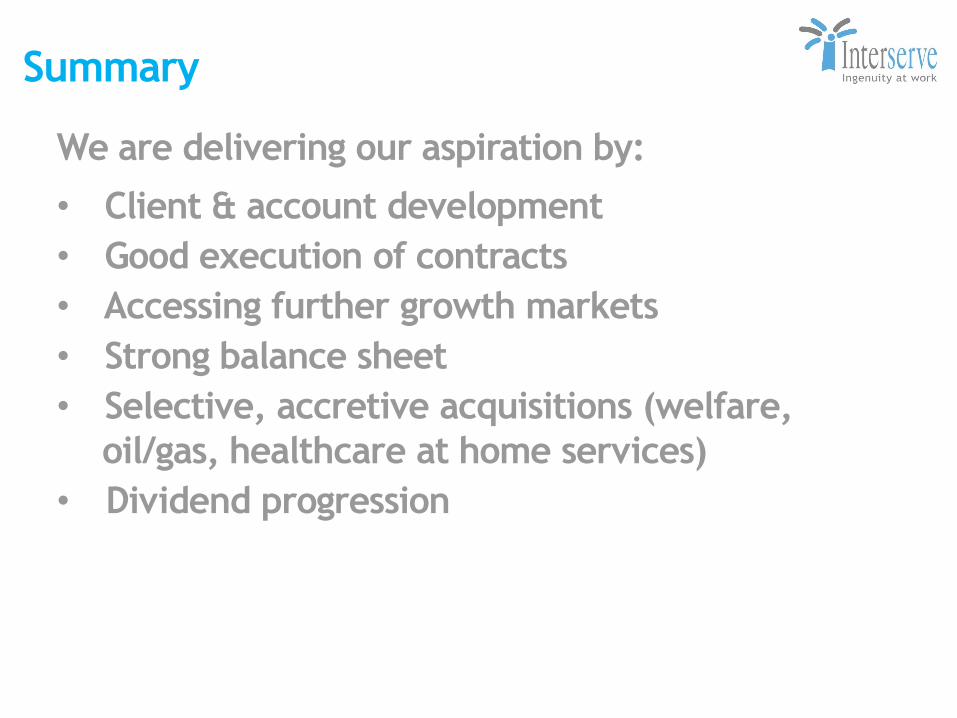

Summary

We are delivering our aspiration by:

• Client & account development

• Good execution of contracts

• Accessing further growth markets

• Strong balance sheet

• Selective, accretive acquisitions (welfare,

oil/gas, healthcare at home services)

• Dividend progression

Tim Haywood –

Sustainable performance

commercial value

Understanding and managing

risk - technical, reputational

Stewardship, resource scarcity,

supply chain complexity, human

capital management

Improved reporting, better

articulation of business strategy

and impacts of material factors

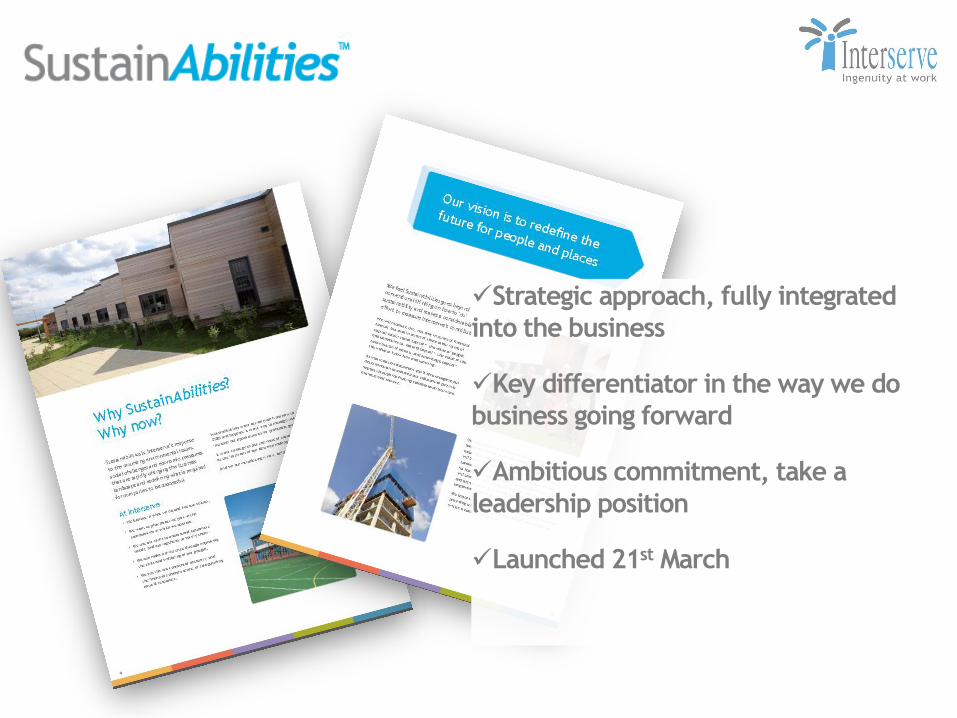

Strategic approach, fully integrated

into the business

Key differentiator in the way we do

business going forward

Ambitious commitment, take a

leadership position

Launched 21st March

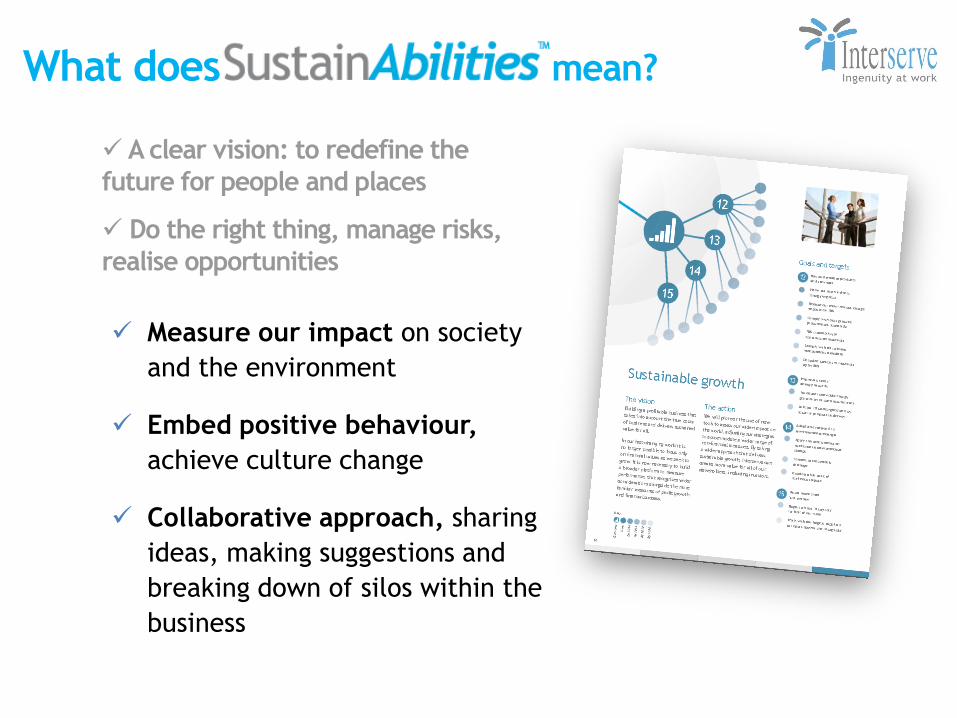

A clear vision: to redefine the

future for people and places

Do the right thing, manage risks,

realise opportunities

Measure our impact on society

and the environment

Embed positive behaviour,

achieve culture change

Collaborative approach, sharing

ideas, making suggestions and

breaking down of silos within the

business

What does mean?

Natural resources, drinking water, breathable air, energy, raw materials

Social connections, benefits, roles, networks, employment, trust, belonging, wellbeing, health

Skills, knowhow, experience, apprenticeships, graduate training schemes, employees, education

Financial management, growth, profit, reporting

Measure our impact beyond traditional financial metrics:

4 Capitals

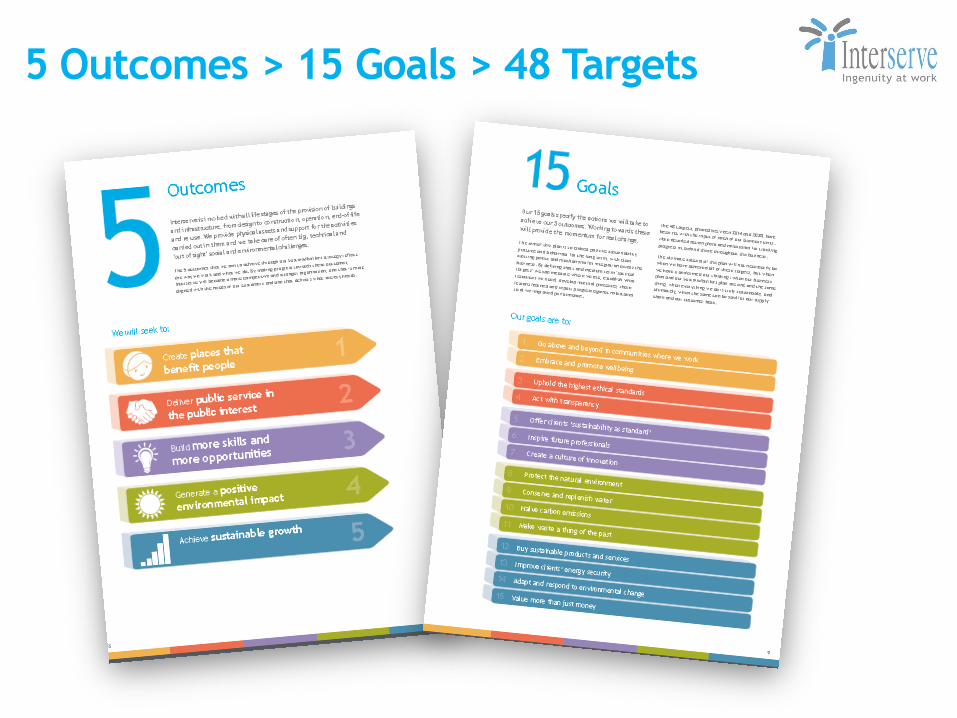

5 Outcomes > 15 Goals > 48 Targets

Phil Clark –

Healthcare market

AGENDA

Introduction

• The Healthcare Market

• Interserve Strategy

• Non-Clinical Services – Leicester

Project

• Clinical Services – Advantage

Healthcare

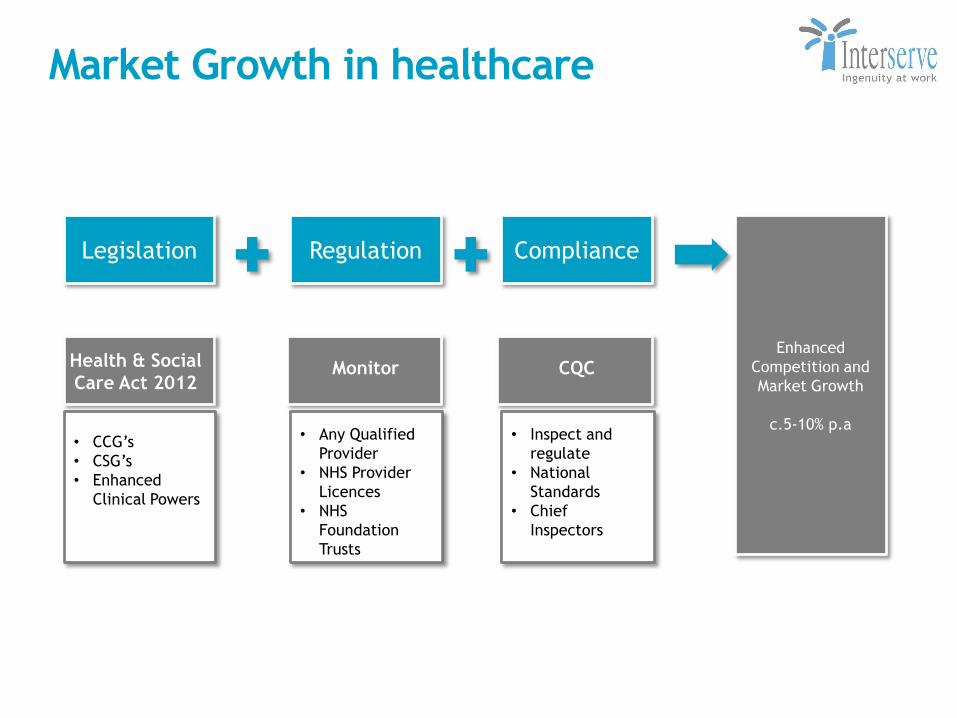

The Healthcare Market

Legislation

Market Growth in healthcare

Regulation Compliance

Enhanced

Competition and

Market Growth

c.5-10% p.a

Health & Social

Care Act 2012

• CCG’s

• CSG’s

• Enhanced

Clinical Powers

Monitor

• Any Qualified

Provider

• NHS Provider

Licences

• NHS

Foundation

Trusts

CQC

• Inspect and

regulate

• National

Standards

• Chief

Inspectors

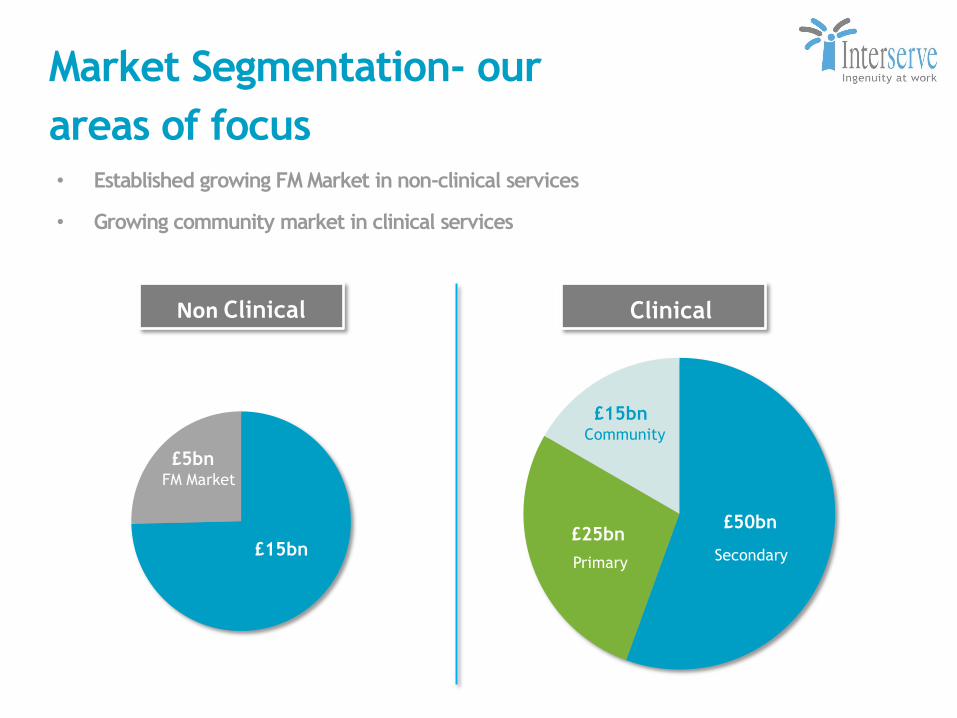

£50bn

Market Segmentation- our

areas of focus

Non Clinical Clinical

Secondary

Community

Primary

£15bn

£15bn

£5bn FM Market

£25bn

• Established growing FM Market in non-clinical services

• Growing community market in clinical services

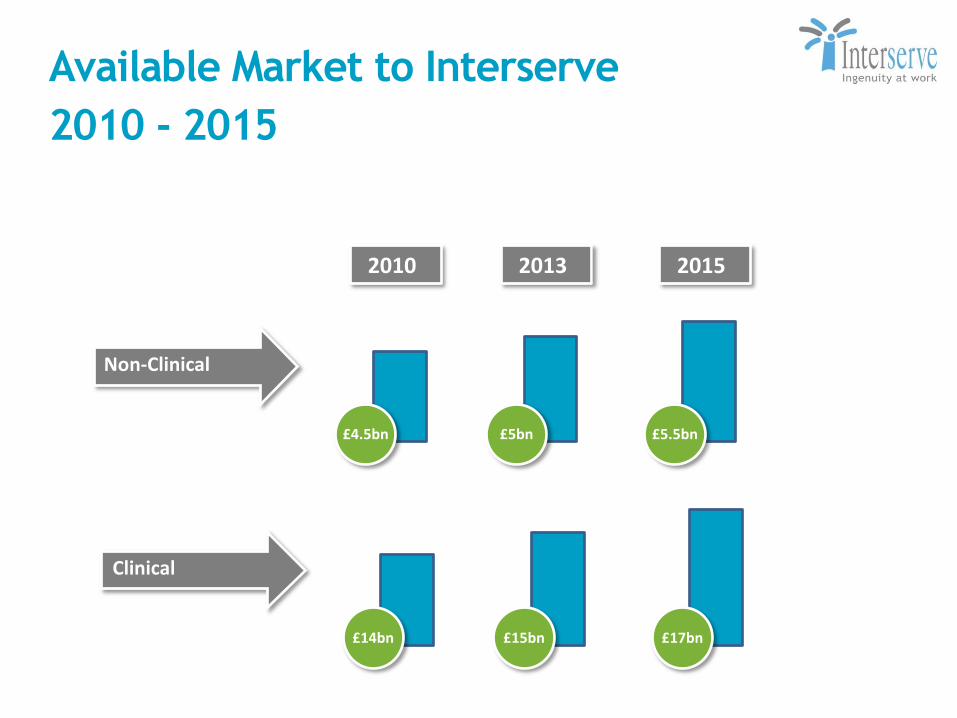

Available Market to Interserve

2010 - 2015

Non-Clinical

£4.5bn

Clinical

£14bn

£5bn

£15bn

2013

£5.5bn

£17bn

2015 2010

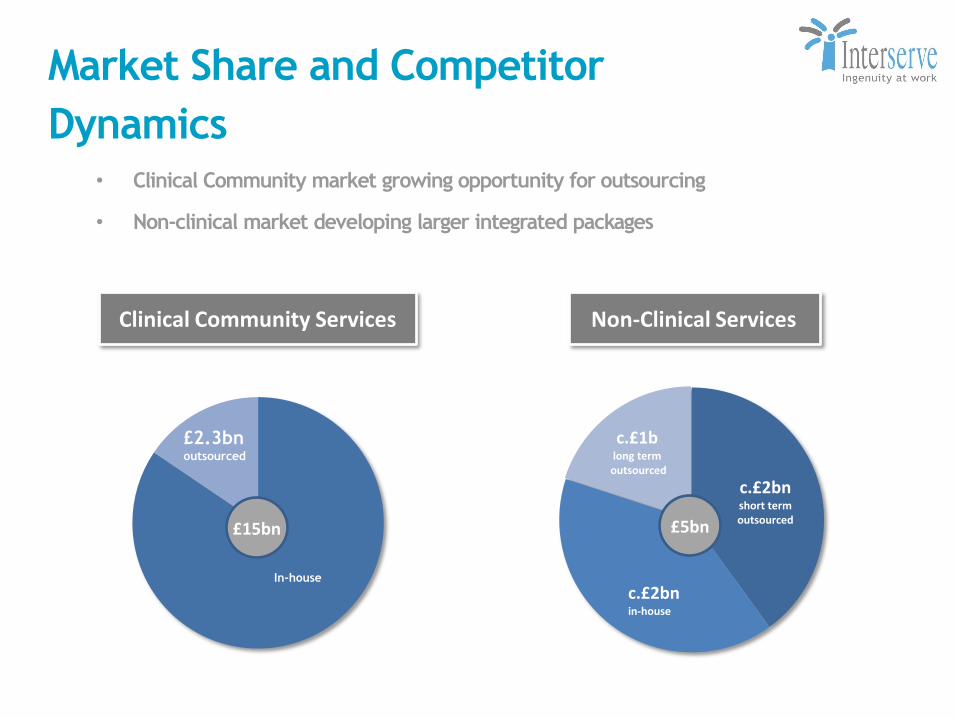

Market Share and Competitor

Dynamics

In-house

£2.3bn outsourced

Clinical Community Services Non-Clinical Services

c.£2bn short term outsourced

c.£2bn in-house

c.£1b long term

outsourced

£15bn £5bn

• Clinical Community market growing opportunity for outsourcing

• Non-clinical market developing larger integrated packages

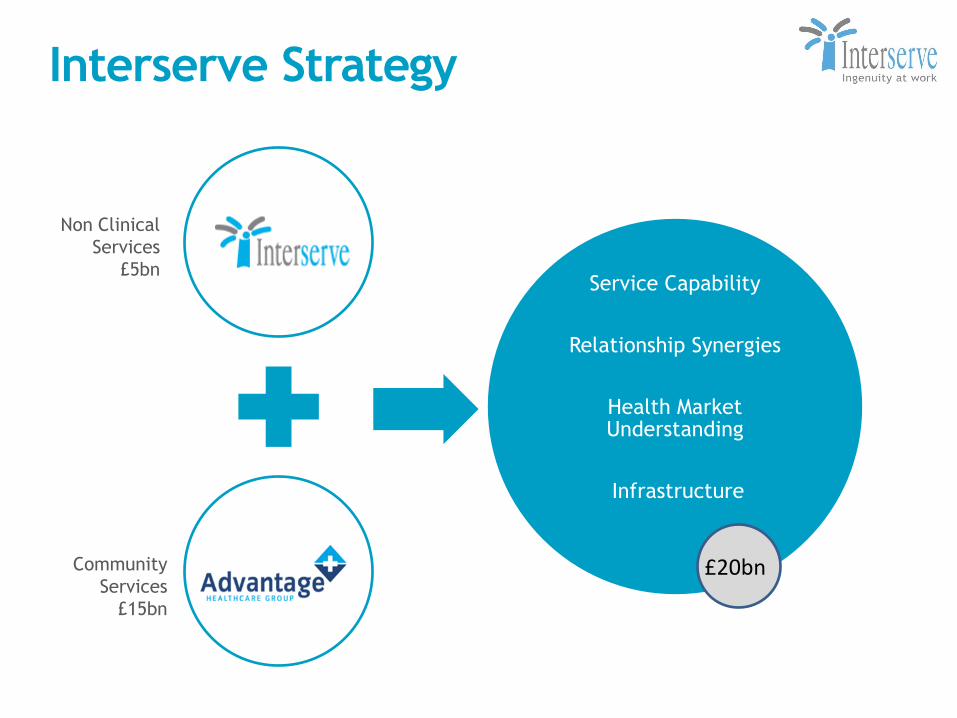

Interserve Strategy

Interserve Strategy

Service Capability

Relationship Synergies

Health Market Understanding

Infrastructure

Non Clinical

Services

£5bn

Community

Services

£15bn

£20bn

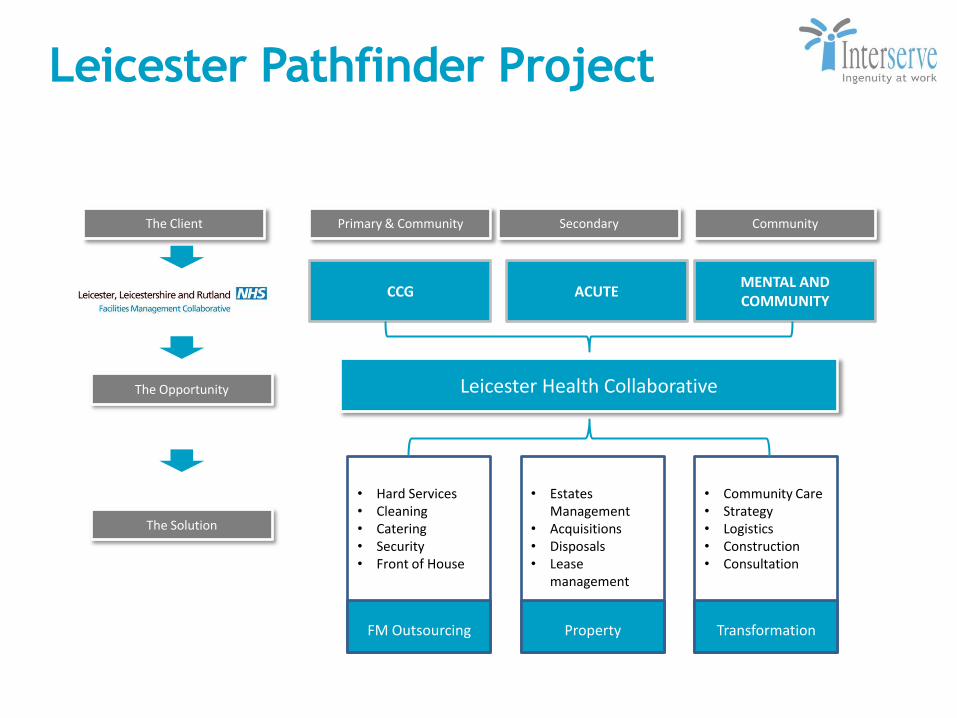

Non-Clinical Services – Leicester Project

Primary & Community Secondary Community The Client

CCG ACUTE MENTAL AND COMMUNITY

Leicester Health Collaborative The Opportunity

The Solution

FM Outsourcing

• Hard Services • Cleaning • Catering • Security • Front of House

Property

• Estates Management

• Acquisitions • Disposals • Lease

management

Transformation

• Community Care • Strategy • Logistics • Construction • Consultation

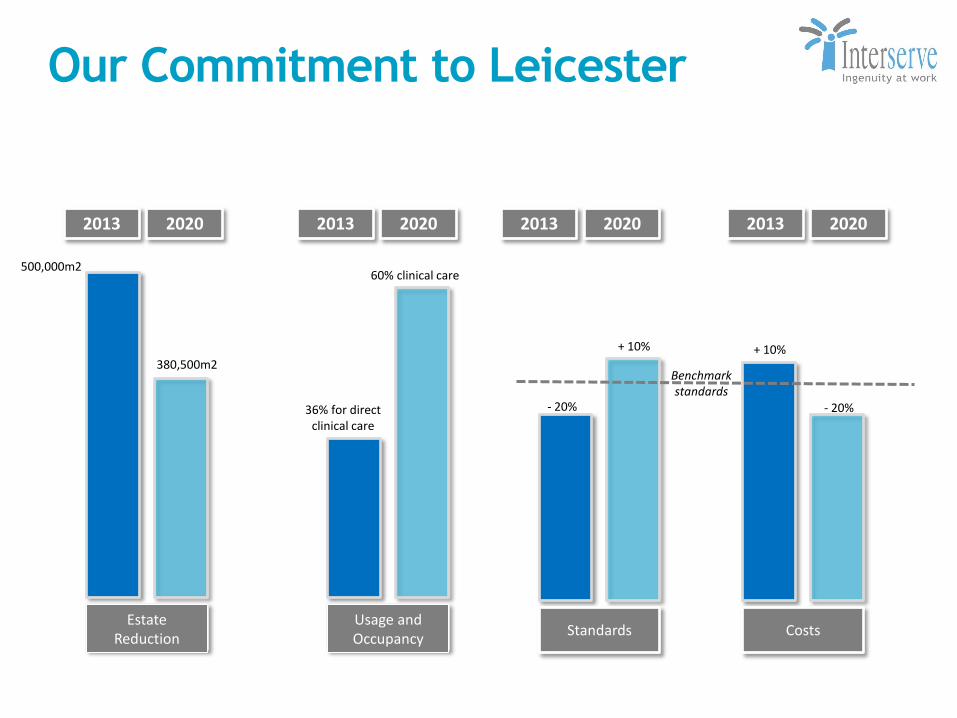

Leicester Pathfinder Project

Estate Reduction

500,000m2

380,500m2

Usage and Occupancy

60% clinical care

36% for direct clinical care

Standards Costs

+ 10%

Our Commitment to Leicester

- 20%

Benchmark standards

2013 2020 2013 2020 2013 2020 2013 2020

- 20%

+ 10%

Property Non Clinical Transformation

Interserve Saving

Total Spend

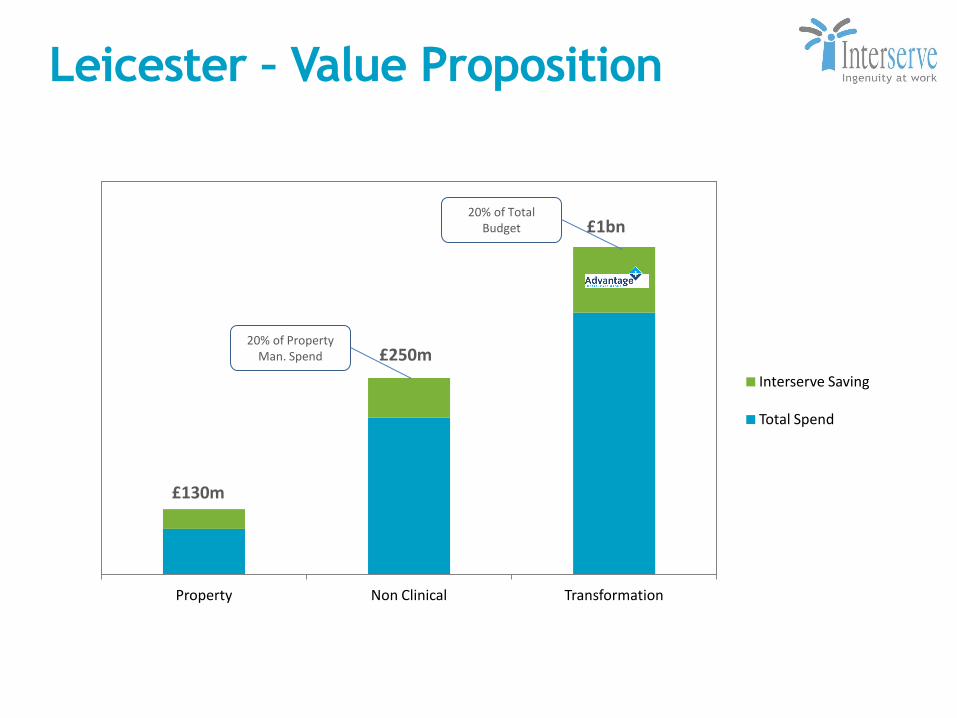

Leicester – Value Proposition

20% of Total Budget

20% of Property Man. Spend

£1bn

£250m

£130m

Aligned Commercials

Clinical Understanding

Guaranteed Savings

Local Company

Integrated Service

Capability

Track records of delivery

Complement not Compete

Key features to our approach

Partner Approach

Leicester Growth Opportunities

Other local NHS customers

Regional Government customers

New NHS Frameworks across the UK

NHS Property Services

Nottingham NHS Trust

Leicester City Council

Leicester County Council

Southampton

Leeds

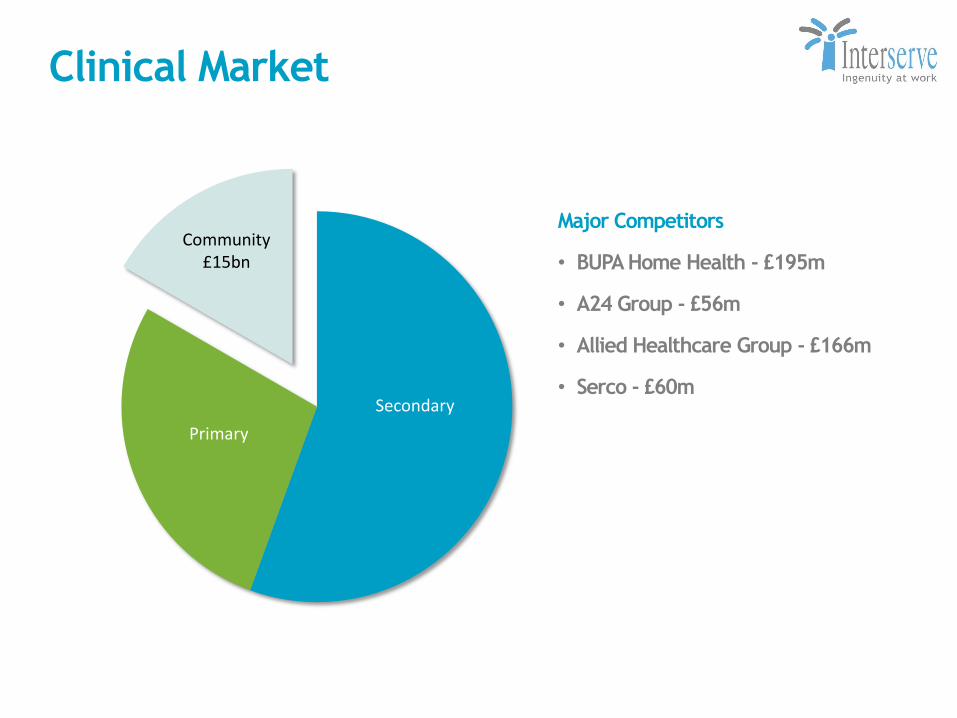

Clinical Services -

Clinical Market

Community £15bn

Secondary

Primary

Major Competitors

• BUPA Home Health - £195m

• A24 Group - £56m

• Allied Healthcare Group - £166m

• Serco - £60m

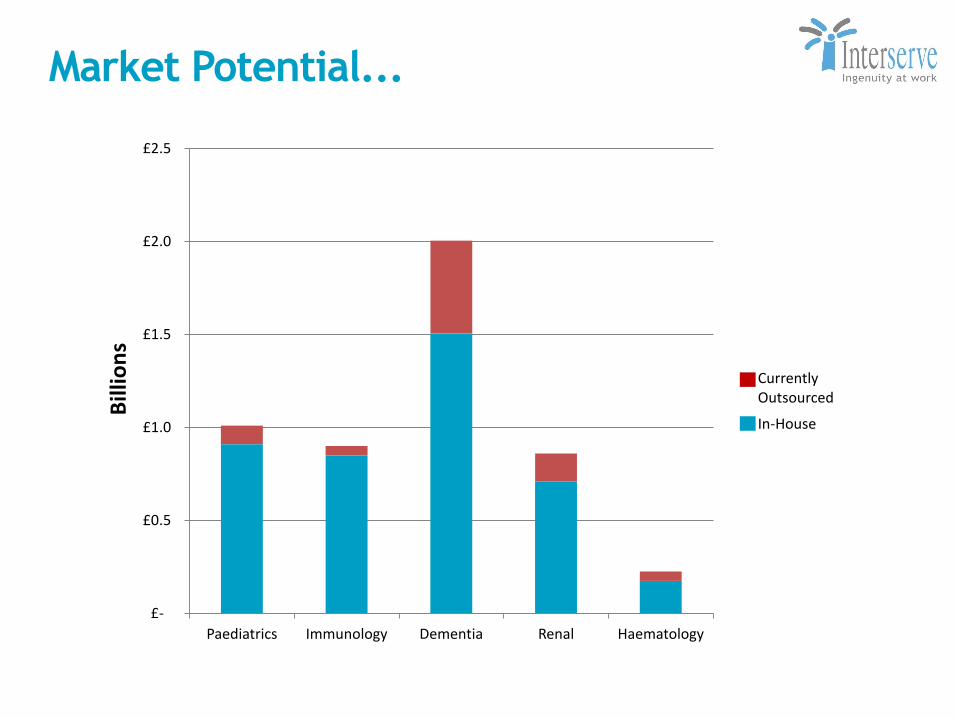

Market Potential...

£-

£0.5

£1.0

£1.5

£2.0

£2.5

Paediatrics Immunology Dementia Renal Haematology

Bill

ion

s

Currently Outsourced

In-House

Paediatric Sector – Market potential

Advantage current capability

• Over 30% revenue through paediatric cases

• Prime provider in London and South East

Barriers To Entry

• Recruitment

• Highly regulated, high profile and sensitive

market

Market Fragmentation

• 90% undertaken by NHS

• Over 200 registered private suppliers

• No major player

Growth Sector

• 35% savings achievable

• Larger , longer packages

• higher margins

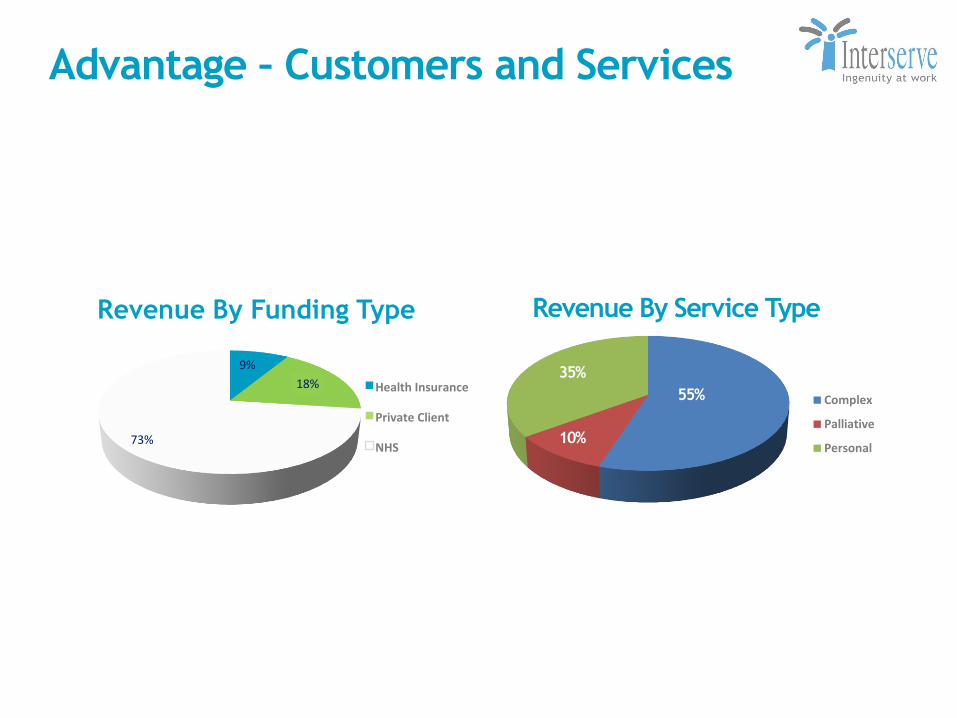

Advantage – Customers and Services

9%

18%

73%

Revenue By Funding Type

Health Insurance

Private Client

NHS

Complex

Palliative

Personal

Revenue By Service Type

55%

10%

35%

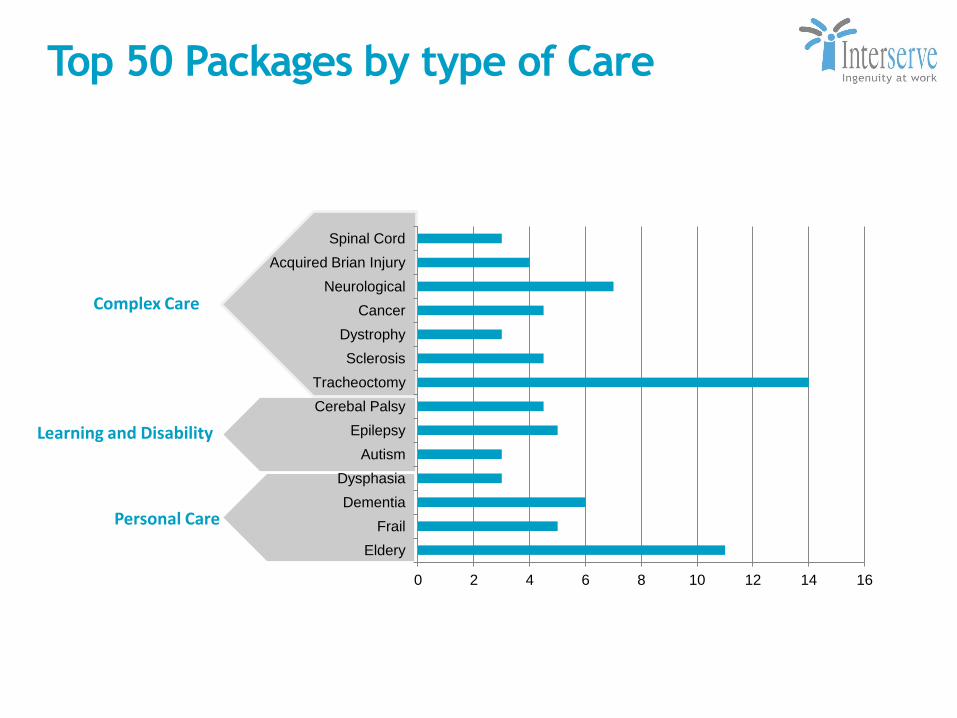

Top 50 Packages by type of Care

0 2 4 6 8 10 12 14 16

Eldery

Frail

Dementia

Dysphasia

Autism

Epilepsy

Cerebal Palsy

Tracheoctomy

Sclerosis

Dystrophy

Cancer

Neurological

Acquired Brian Injury

Spinal Cord

Complex Care

Learning and Disability

Personal Care

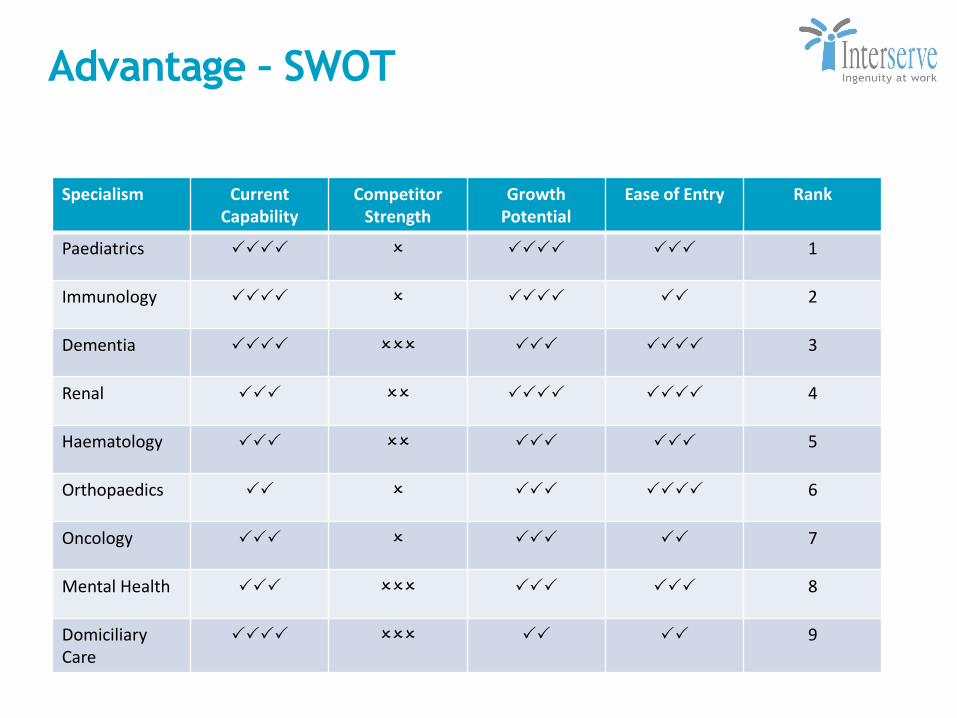

Advantage – SWOT

Specialism Current Capability

Competitor Strength

Growth Potential

Ease of Entry Rank

Paediatrics PPPP O PPPP PPP 1

Immunology PPPP O PPPP PP 2

Dementia PPPP OOO PPP PPPP 3

Renal PPP OO PPPP PPPP 4

Haematology PPP OO PPP PPP 5

Orthopaedics PP O PPP PPPP 6

Oncology PPP O PPP PP 7

Mental Health PPP OOO PPP PPP 8

Domiciliary Care

PPPP OOO PP PP 9

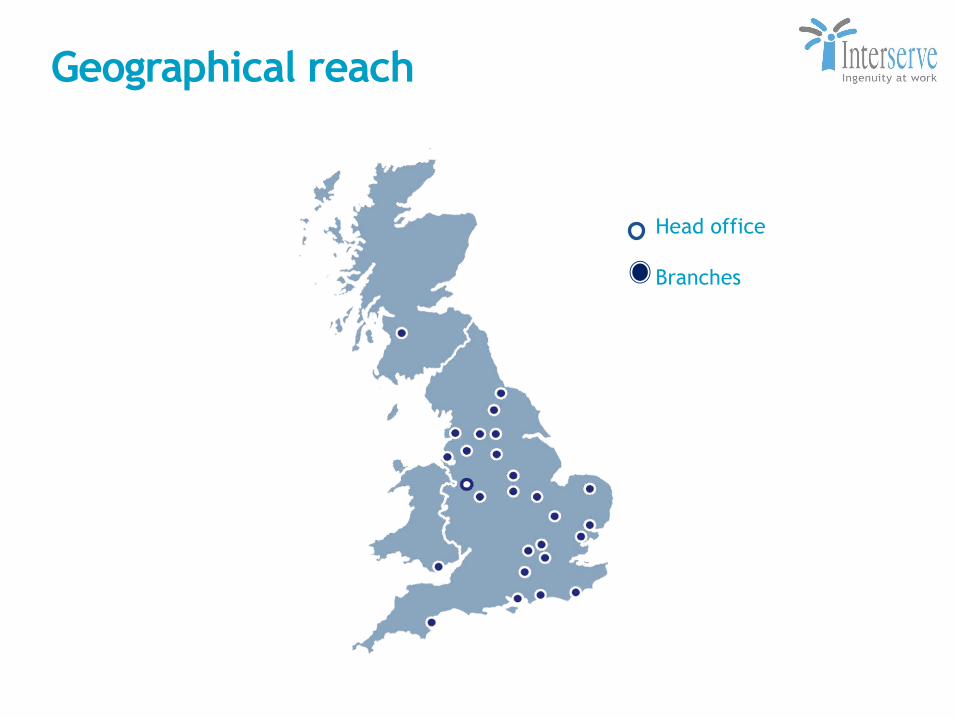

Geographical reach

Head office

Branches

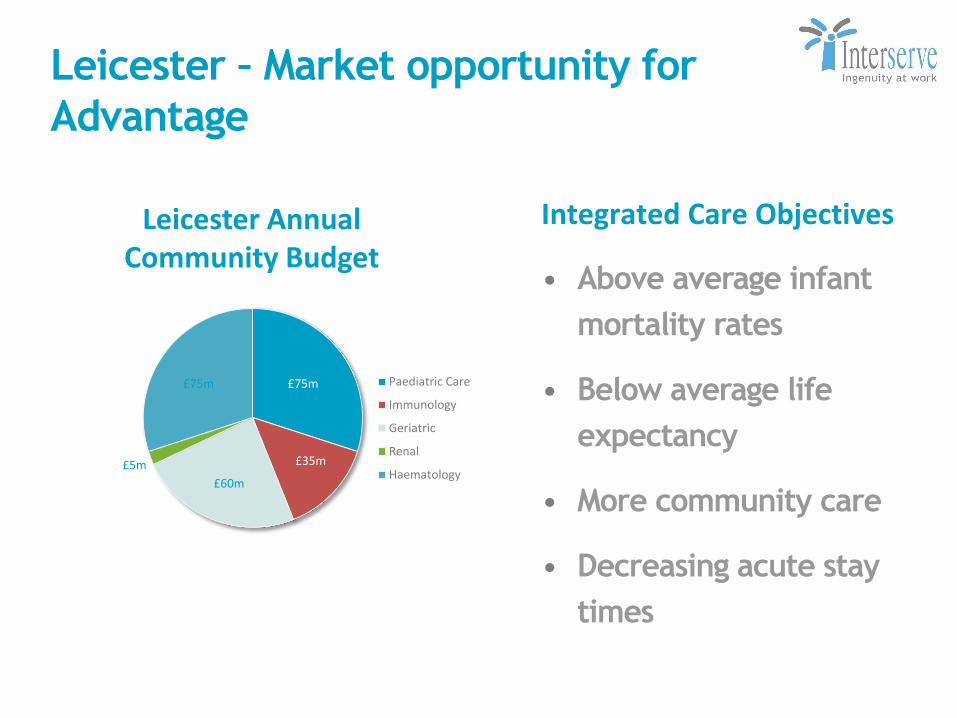

Leicester – Market opportunity for

Advantage

£75m

£35m

£60m

£5m

£75m Paediatric Care

Immunology

Geriatric

Renal

Haematology

Integrated Care Objectives

• Above average infant

mortality rates

• Below average life

expectancy

• More community care

• Decreasing acute stay

times

Leicester Annual Community Budget

Summary

• Healthcare outsourcing is a growing market (5-10%) and has significant potential for more

• Community and estate management are fastest developing

• Advantage Healthcare well positioned to take advantage of the Community market

• Leicester is a unique arrangement applicable to other estates in the UK

Questions

Lord Adonis – UK

Outsourcing and

Infrastructure

Questions

Coffee Break

Construction and

Support Services

International:

George Franks

Geographical Reach

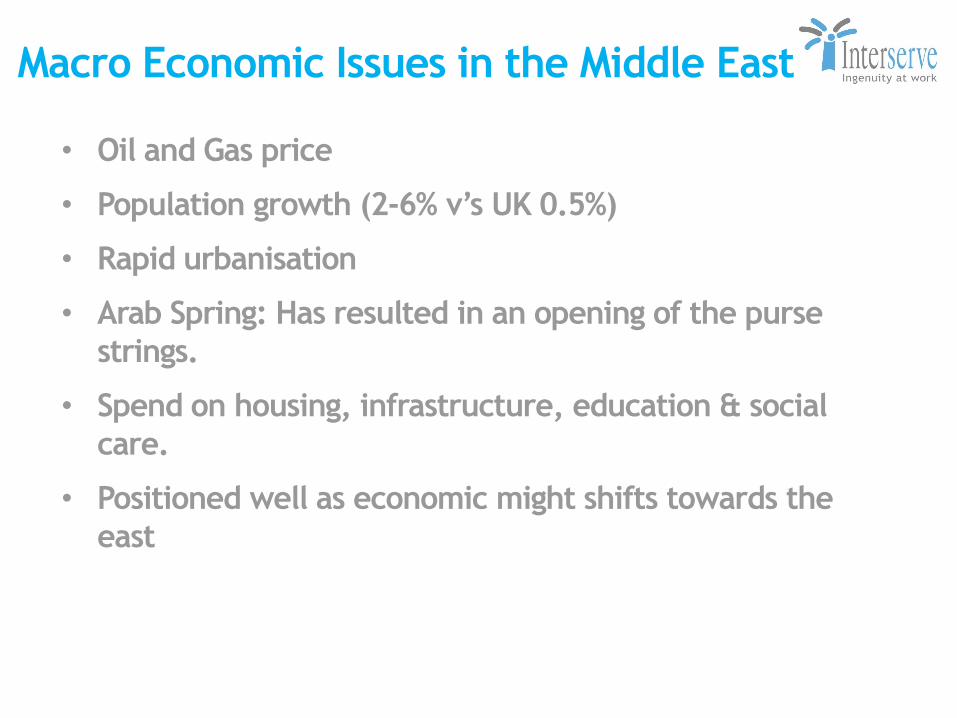

Macro Economic Issues in the Middle East

• Oil and Gas price

• Population growth (2-6% v’s UK 0.5%)

• Rapid urbanisation

• Arab Spring: Has resulted in an opening of the purse

strings.

• Spend on housing, infrastructure, education & social

care.

• Positioned well as economic might shifts towards the

east

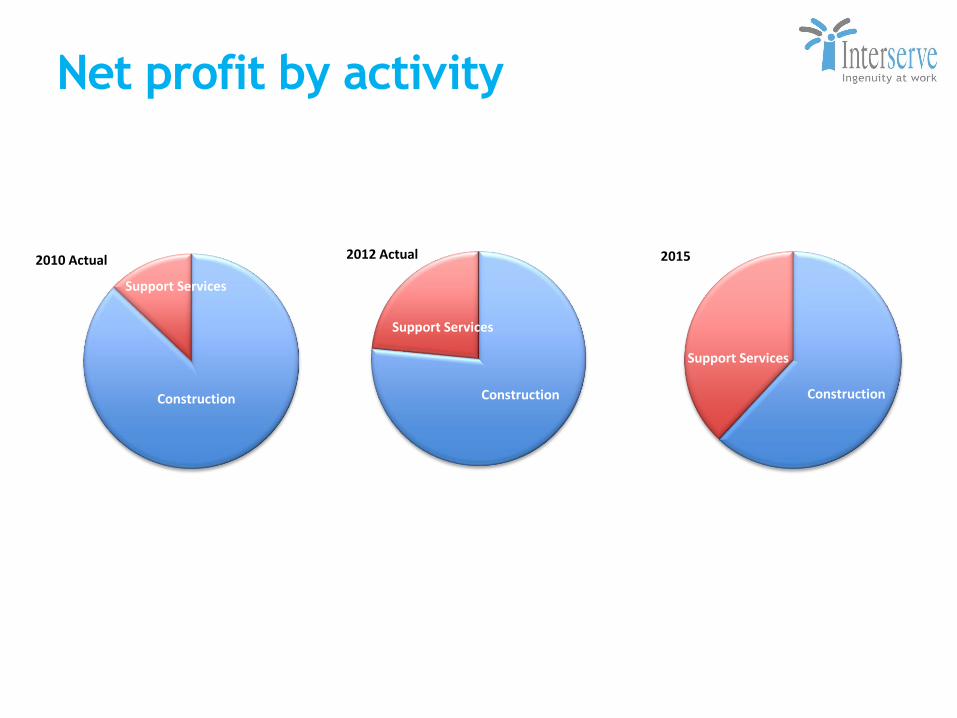

Net profit by activity

2010 Actual

Construction

Support Services

Construction

Support Services

2012 Actual

Construction

Support Services

2015

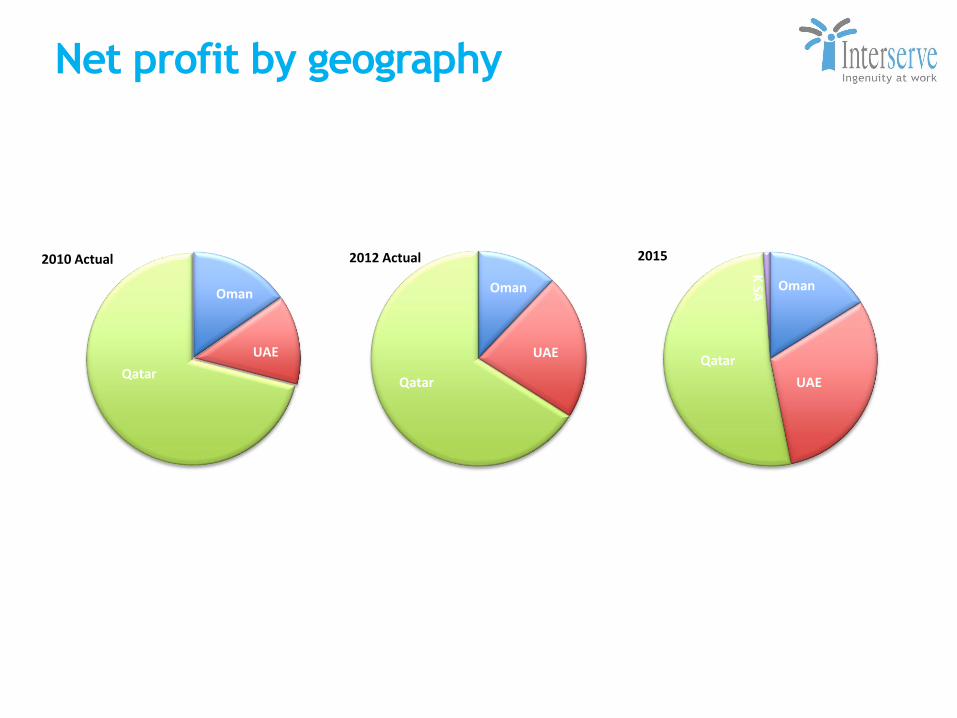

Net profit by geography

Oman

Qatar

2010 Actual 2012 Actual

Oman

UAE

Qatar

2015

Oman

UAE

Qatar

K SA

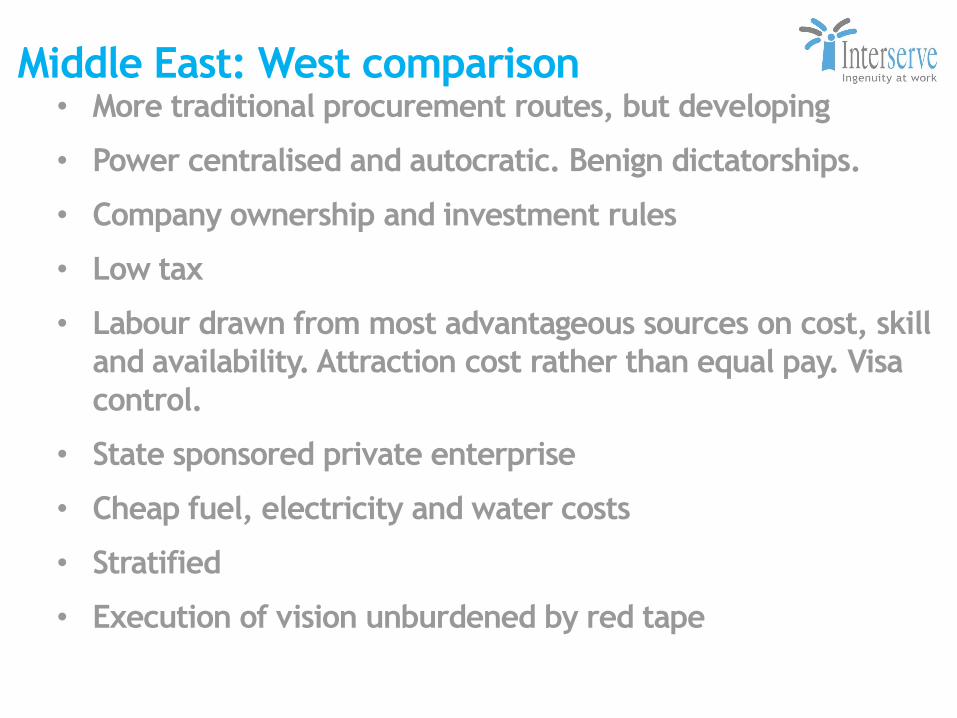

Middle East: West comparison • More traditional procurement routes, but developing

• Power centralised and autocratic. Benign dictatorships.

• Company ownership and investment rules

• Low tax

• Labour drawn from most advantageous sources on cost, skill

and availability. Attraction cost rather than equal pay. Visa

control.

• State sponsored private enterprise

• Cheap fuel, electricity and water costs

• Stratified

• Execution of vision unburdened by red tape

Middle East businesses

Construction International

• 1981 Khansaheb Civil Engineering

LLC (UAE)

• 1981 Douglas OHI LLC (Oman)

• 1995 Khansaheb Hussain LLC (UAE)

• 1996 Gulf Contracting Co. WLL

(Qatar)

• 2009 DOHI equity increased to 49%

Support Services International

• 2000 How United Services

WLL (Qatar)

• 2007 Madina Group WLL

(Qatar)

• 2010 Occupational Training

Institute LLC (Oman)

• 2010 Khansaheb Group LLC

(UAE)

• 2013 TOCO LLC (Oman)

Construction International

• Market still tight in all 3 countries of operation

• Strategy to hold our nerve, avoid diving in and taking low

margin/high risk work, maintain capabilities and wait for the upturn.

• UAE looks set to recover first

• Qatar will recover soon but too many new entrants to the market are

depressing prices.

• Oman remains competitive.

• We have taken time over the last three years to

• Strengthen and re-organise our businesses

• Improve efficiency

• Replace overtime with productivity schemes

• Open up new procurement routes and develop our internal

supply chain

• Grow our specialist divisions and target growth opportunities

Strategy Outcomes

Buildings (Jumeirah Beach Residences) Civils (Al Furjan)

Support Services Specialist Divisions (Ritz Carlton Hotel)

Strategy Outcomes

Construction (Sohar Court) Construction (Al Sukri)

Civils (Sur IPP) Specialist (HSBC Fit-Out)

Strategy Outcomes

Construction (Barzan) Spacemaker (Barzan)

Bionest Specialist Div. (Commercial Law Court)

Support Services International: 2012

• Two principal areas of operation, engineering and

facilities services

• Expanded our reach – acquisition of TOCO

• Grown our offering – Shutdowns and increased customer

base

• Senior team seconded in to International from Interserve

UK to grow the facilities services business as a strategic

priority.

• Ability to support with resource and infrastructure from

existing businesses

• Looking for suitable acquisitions/ investments in UAE,

Oman and KSA

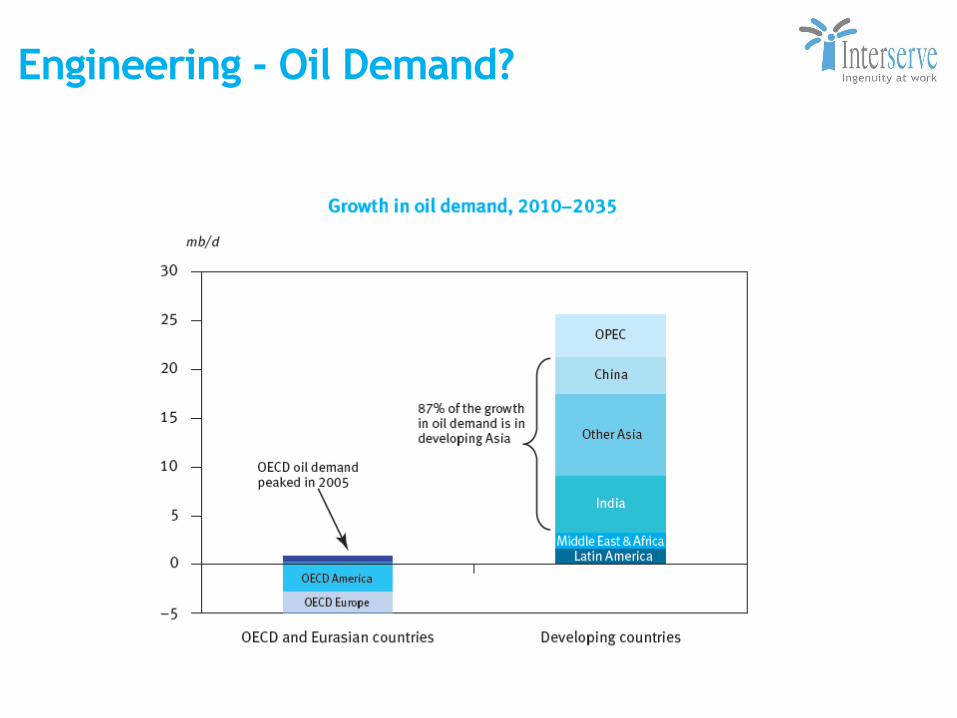

Engineering - Oil Demand?

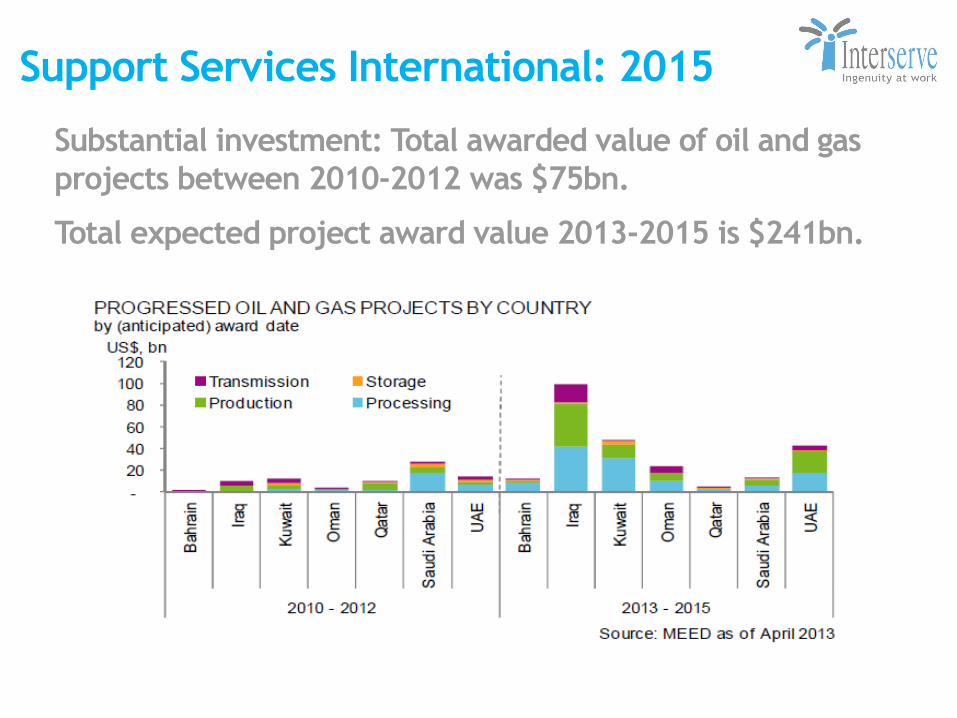

Support Services International: 2015

Substantial investment: Total awarded value of oil and gas

projects between 2010-2012 was $75bn.

Total expected project award value 2013-2015 is $241bn.

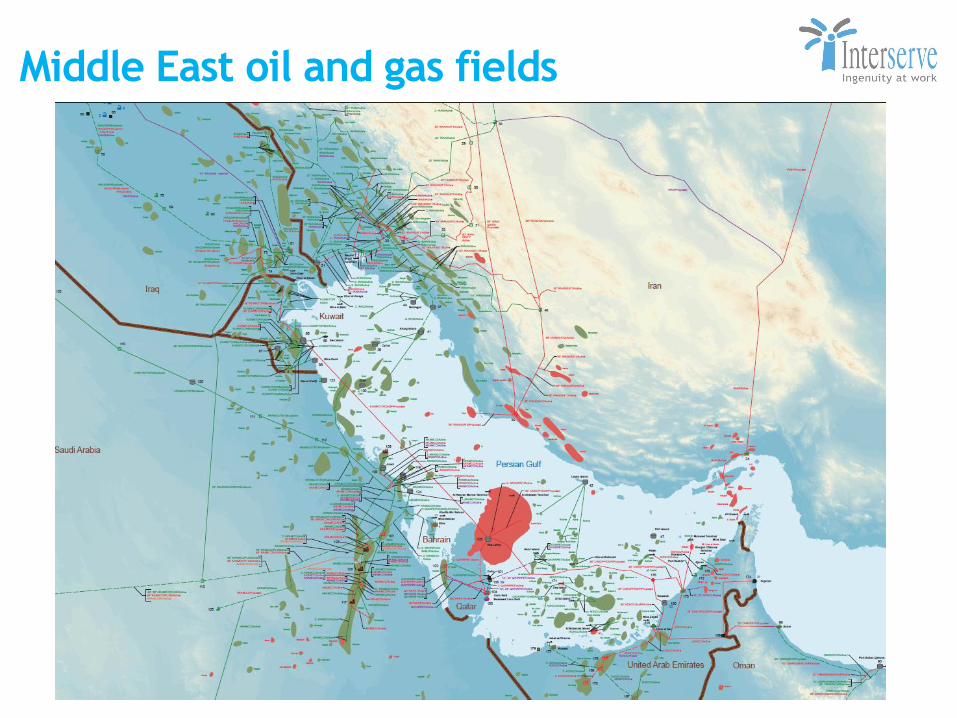

Middle East oil and gas fields

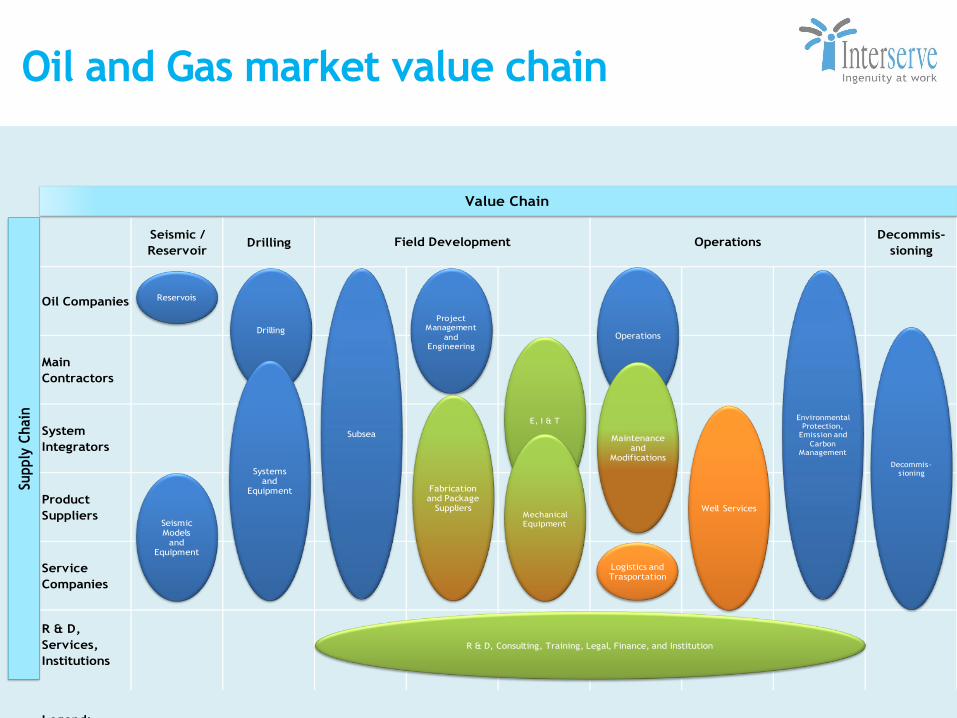

Oil and Gas market value chain

Seismic /

ReservoirDrilling

Decommis-

sioning

Oil Companies

Main

Contractors

System

Integrators

Product

Suppliers

Service

Companies

R & D,

Services,

Institutions

Legend:

Madina only

TOCO

Field Development Operations

Madina & TOCO

Supply

Chain

Value Chain

Reservois

Seismic Models

and Equipment

Drilling

Systemsand

Equipment

Subsea

Project Management

and Engineering

Fabrication and Package

Suppliers

E, I & T

Mechanical Equipment

Operations

Maintenanceand

Modifications

Logistics and Trasportation

Well Services

Environmental Protection,

Emission and

Carbon Management

Decommis-sioning

R & D, Consulting, Training, Legal, Finance, and Institution

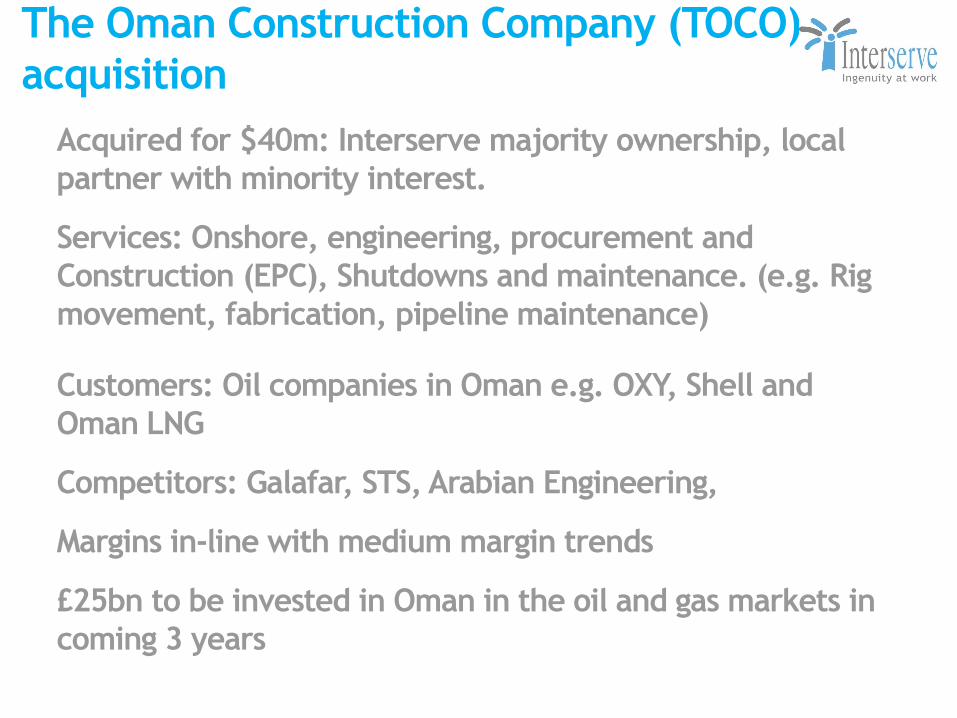

The Oman Construction Company (TOCO)

acquisition

Acquired for $40m: Interserve majority ownership, local

partner with minority interest.

Services: Onshore, engineering, procurement and

Construction (EPC), Shutdowns and maintenance. (e.g. Rig

movement, fabrication, pipeline maintenance)

Customers: Oil companies in Oman e.g. OXY, Shell and

Oman LNG

Competitors: Galafar, STS, Arabian Engineering,

Margins in-line with medium margin trends

£25bn to be invested in Oman in the oil and gas markets in

coming 3 years

65

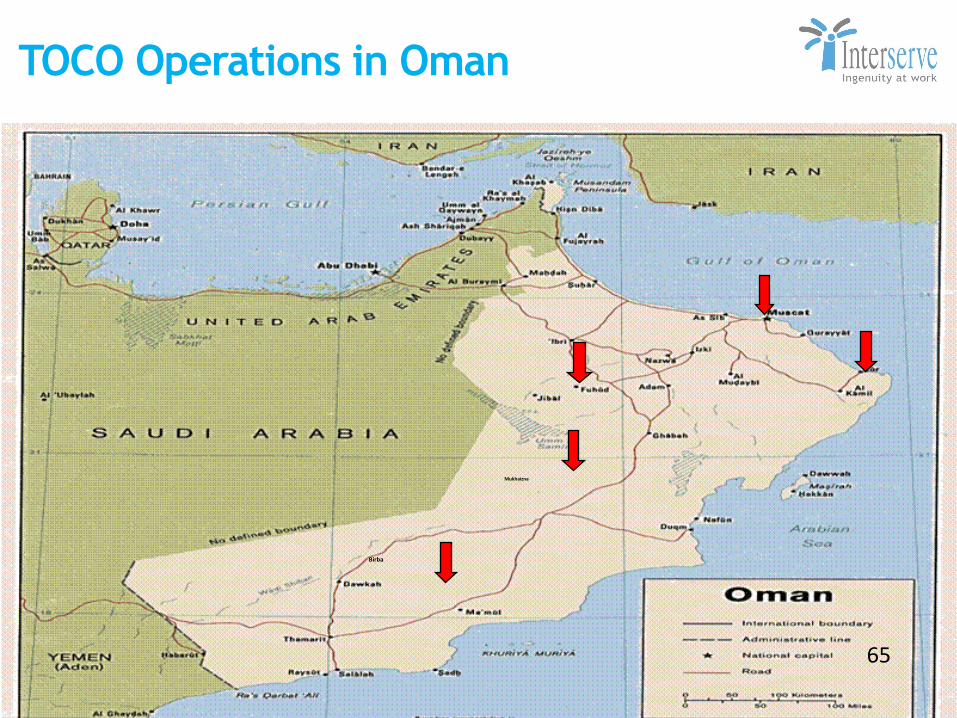

TOCO Operations in Oman

Birba

Mukhaizna

New Oilfield Construction Services

Contract On 02nd April 2013 The Oman Construction

Co. LLC (TOCO) was awarded an Oilfield

Construction Services Contract to provide

Oilfield Construction Services in the North of

Oman by one of the major Oil and Gas

Companies based in Oman

The Scope Of Work includes:

• Pipelines / Flow lines / Plant Piping

Fabrication & Installation including NDT,

Pigging, Cleaning & Hydrostatic Testing and

wellhead Hook-ups and Well-pad Piping

• Installation of Equipment (Rotary and

Static)

• Hot Tapping

• Supply & Installation of Insulation

• Painting & Coating

• Civil Works & Steel Structural Works

• Operation & Maintenance Works

Support Services International

Facilities Services market:

• Hard and soft services currently delivered through Khansaheb Group

and How United Services. T/O Circa £13m p.a.

• We are demonstrating margin of 10%, and above, deliverable at site.

• Currently sectors include; residential, education, hospitality,

industrial, retail, health, defence and commercial.

• Focus on growth through, organic means, supporting new start ups

and acquisition.

• Development support is being provided from Group centre and bid

support from Support Services in the UK for strategic bids.

• Aim to register majority owned businesses in Oman and KSA in 2013

• Sustainability becoming more important

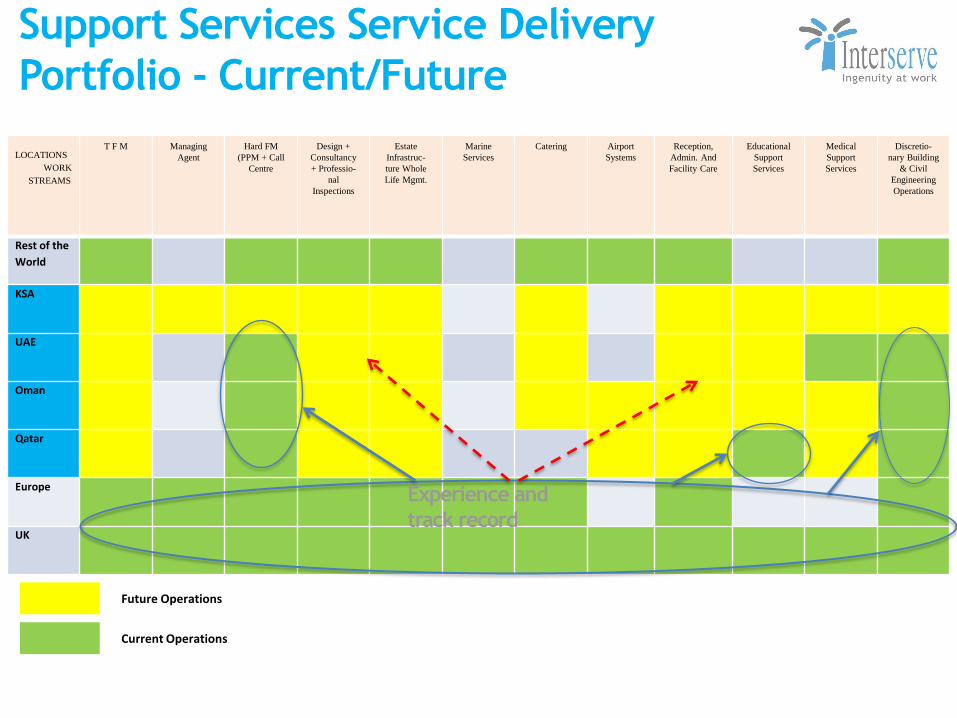

Future Operations

LOCATIONS

WORK

STREAMS

T F M Managing

Agent

Hard FM

(PPM + Call

Centre

Design +

Consultancy

+ Professio-

nal

Inspections

Estate

Infrastruc-

ture Whole

Life Mgmt.

Marine

Services

Catering Airport

Systems

Reception,

Admin. And

Facility Care

Educational

Support

Services

Medical

Support

Services

Discretio-

nary Building

& Civil

Engineering

Operations

Rest of the

World

KSA

UAE

Oman

Qatar

Europe

UK

Support Services Service Delivery

Portfolio - Current/Future

Current Operations

Experience and

track record

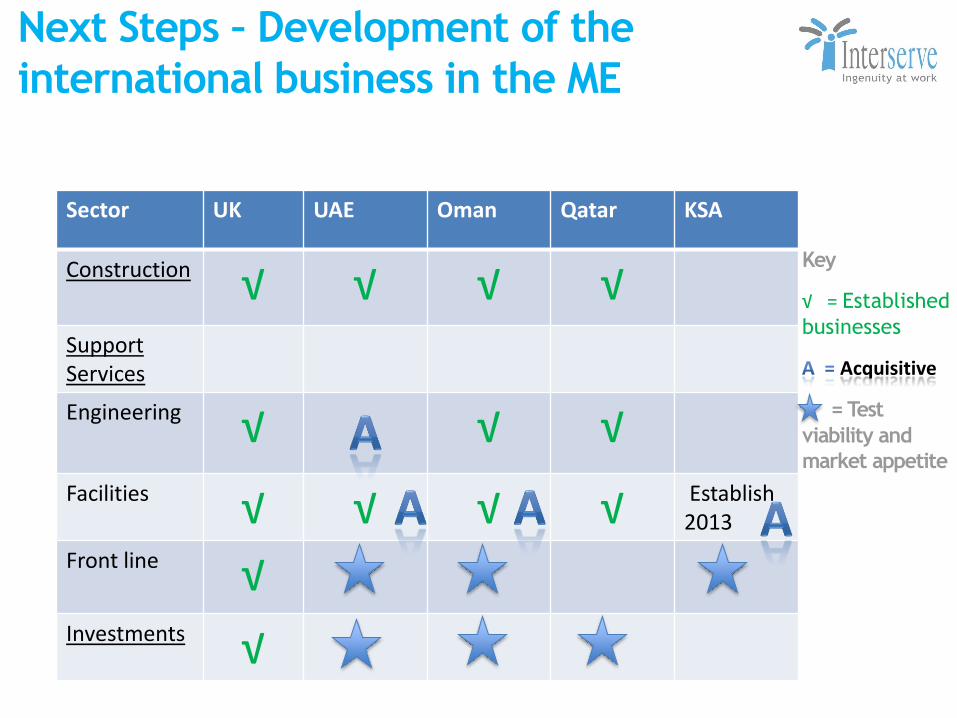

Next Steps – Development of the

international business in the ME

Sector UK UAE Oman Qatar KSA

Construction √ √ √ √ Support Services

Engineering √ √ √ Facilities √ √ √ √ Establish

2013

Front line √ Investments √

Key

√ = Established

businesses

Acquisitive

= Test

viability and

market appetite

Summary

• Recovery in construction is coming, maintain and

position to take advantage. Construction will continue to

be a major part of our business.

• Expansion of support services (engineering and facilities)

a strategic priority to become a significant player in ME

by 2015. Thus developing a more balanced portfolio.

• Look into new markets where we believe opportunities

exist at acceptable risk and we can bring value.

• Test market appetite for investment offerings and

frontline services

Equipment Services:

Ian Hayes

Building Strong Core businesses

Expand Internationally

Capturing related expansion

opportunities

H1 2012 Highlights

Disposal of PFI Assets

Frontline public services (Justice, Welfare,

Health)

Energy-from-waste (Westbury/Glasgow/

Peterborough)

[Omani industrial sector]

Equipment Services: Panama, Chile, Colombia

and export growth

Middle East interiors businesses

Expansion into Omani oil and gas services

Future Workload Growth

Revenue and profit growth

Strong Cash Conversion

Strategy Outcomes

Interserve Equipment Services

RMD Kwikform

Vision and Strategy

We aspire to be the Best Formwork and Shoring Company in the World

To manage a de-centralised portfolio of companies with a Divisional overlay that binds them together to:

• Operate accident free

• Live our values

• Be market driven

• Seek to be in the top 3 of each of our operating markets

Financial targets - profit growth, ROCE, double digit margins

Building Strong Core businesses

Expand Internationally

Capturing related expansion

opportunities

H1 2012 Highlights

Disposal of PFI Assets

Frontline public services (Justice, Welfare,

Health)

Energy-from-waste (Westbury/Glasgow/

Peterborough)

[Omani industrial sector]

Equipment Services: Panama, Chile, Colombia

and export growth

Middle East interiors businesses

Expansion into Omani oil and gas services

Future Workload Growth

Revenue and profit growth

Strong Cash Conversion

Strategy Outcomes Note - Insert photo of Shroud / roof over Hotel in Abu Dhabi so i can talk to how we add value as part of next slide

Drivers of the Business

RMDk Value add

Utilisation

Margin

Markets / competitors

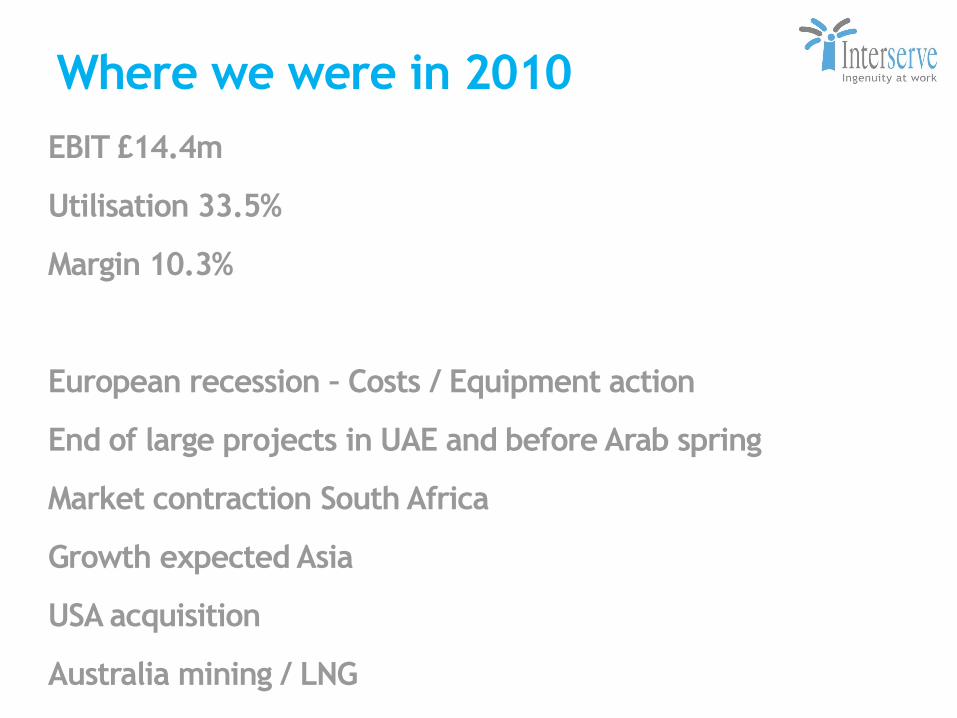

Where we were in 2010

EBIT £14.4m

Utilisation 33.5%

Margin 10.3%

European recession – Costs / Equipment action

End of large projects in UAE and before Arab spring

Market contraction South Africa

Growth expected Asia

USA acquisition

Australia mining / LNG

Where are we at end 2012?

Revenue +19.7%

EBIT £16.1m (+11.8%)

Utilisation 44.3% (+32%)

Transferred £41m of equipment in 2012

Saudi Arabia growth

Reduced costs Europe

Reorganised South Africa

H2 2012 USA price growth

New Territories, branches and Product Development

Building Strong Core businesses

Expand Internationally

Capturing related expansion

opportunities

H1 2012 Highlights

Disposal of PFI Assets

Frontline public services (Justice, Welfare,

Health)

Energy-from-waste (Westbury/Glasgow/

Peterborough)

[Omani industrial sector]

Equipment Services: Panama, Chile, Colombia

and export growth

Middle East interiors businesses

Expansion into Omani oil and gas services

Future Workload Growth

Revenue and profit growth

Strong Cash Conversion

Strategy Outcomes Insert Photo of ME / Saudi project

Building Strong Core businesses

Expand Internationally

Capturing related expansion

opportunities

H1 2012 Highlights

Disposal of PFI Assets

Frontline public services (Justice, Welfare,

Health)

Energy-from-waste (Westbury/Glasgow/

Peterborough)

[Omani industrial sector]

Equipment Services: Panama, Chile, Colombia

and export growth

Middle East interiors businesses

Expansion into Omani oil and gas services

Future Workload Growth

Revenue and profit growth

Strong Cash Conversion

Strategy Outcomes

Building Strong Core businesses

Expand Internationally

Capturing related expansion

opportunities

H1 2012 Highlights

Disposal of PFI Assets

Frontline public services (Justice, Welfare,

Health)

Energy-from-waste (Westbury/Glasgow/

Peterborough)

[Omani industrial sector]

Equipment Services: Panama, Chile, Colombia

and export growth

Middle East interiors businesses

Expansion into Omani oil and gas services

Future Workload Growth

Revenue and profit growth

Strong Cash Conversion

Strategy Outcomes Insert Photo – Australia project

Building Strong Core businesses

Expand Internationally

Capturing related expansion

opportunities

H1 2012 Highlights

Disposal of PFI Assets

Frontline public services (Justice, Welfare,

Health)

Energy-from-waste (Westbury/Glasgow/

Peterborough)

[Omani industrial sector]

Equipment Services: Panama, Chile, Colombia

and export growth

Middle East interiors businesses

Expansion into Omani oil and gas services

Future Workload Growth

Revenue and profit growth

Strong Cash Conversion

Strategy Outcomes

Outlook to end 2015? Margin range c.15%

Utilisation range c.50%

Growth in ME , Qatar and Saudi Arabia

Australasia – Far East growth offsets some reduction in

Australia

Modest recovery Europe

USA pricing level growth

Infrastructure sector potential – fleet investment

New start Colombia, Iraq, Export and other opportunities

Summary Building on client relationships and investing in new

opportunities

Optimising deployment of hire fleet equipment

Improved Utilisation to c50%

Pricing strength

Medium term margin trend of 15%

Questions

Investor relations contact:

Matt Hickman, Investor Relations Manager

0118 960 2280