Embed Size (px)

Citation preview

ME29 / Prime / Final 1

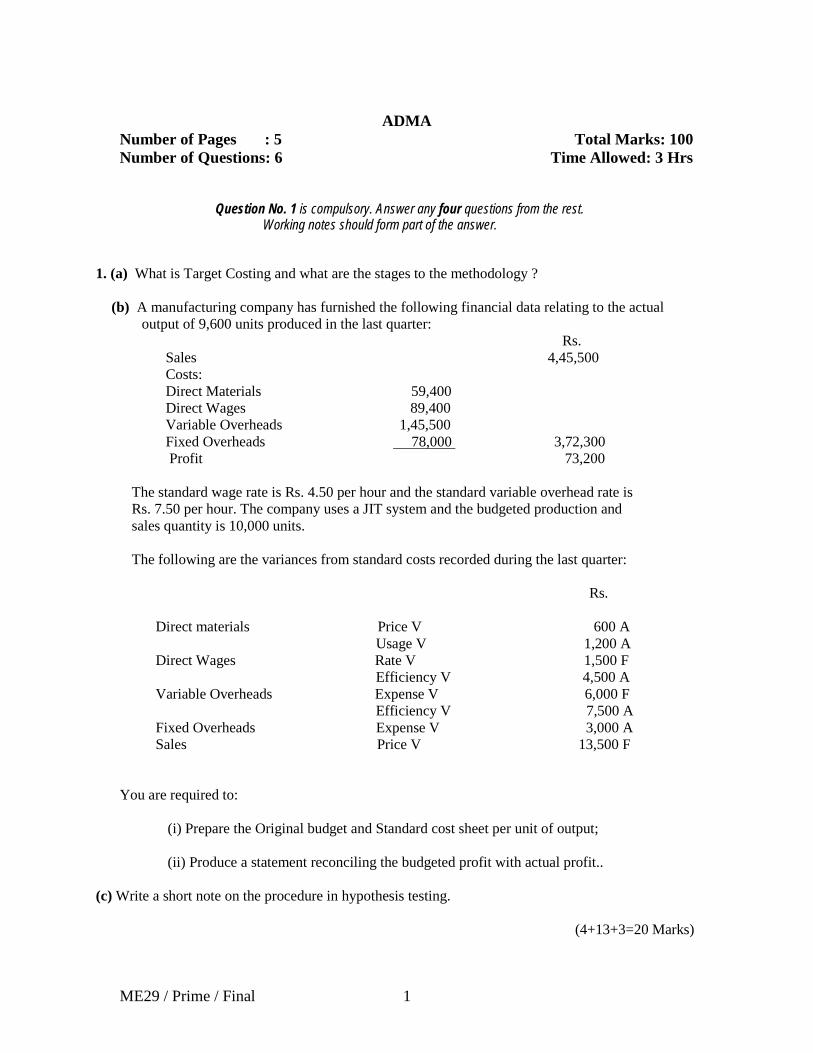

ADMA Number of Pages : 5 Total Marks: 100 Number of Questions: 6 Time Allowed: 3 Hrs

Question No. 1 is compulsory. Answer any four questions from the rest. Working notes should form part of the answer.

1. (a) What is Target Costing and what are the stages to the methodology ?

(b) A manufacturing company has furnished the following financial data relating to the actual output of 9,600 units produced in the last quarter: Rs.

Sales 4,45,500 Costs: Direct Materials 59,400 Direct Wages 89,400 Variable Overheads 1,45,500 Fixed Overheads 78,000 3,72,300 Profit 73,200

The standard wage rate is Rs. 4.50 per hour and the standard variable overhead rate is Rs. 7.50 per hour. The company uses a JIT system and the budgeted production and sales quantity is 10,000 units. The following are the variances from standard costs recorded during the last quarter:

Rs.

Direct materials Price V 600 A Usage V 1,200 A

Direct Wages Rate V 1,500 F Efficiency V 4,500 A

Variable Overheads Expense V 6,000 F Efficiency V 7,500 A

Fixed Overheads Expense V 3,000 A Sales Price V 13,500 F

You are required to:

(i) Prepare the Original budget and Standard cost sheet per unit of output; (ii) Produce a statement reconciling the budgeted profit with actual profit..

(c) Write a short note on the procedure in hypothesis testing.

(4+13+3=20 Marks)

ME29 / Prime / Final 2

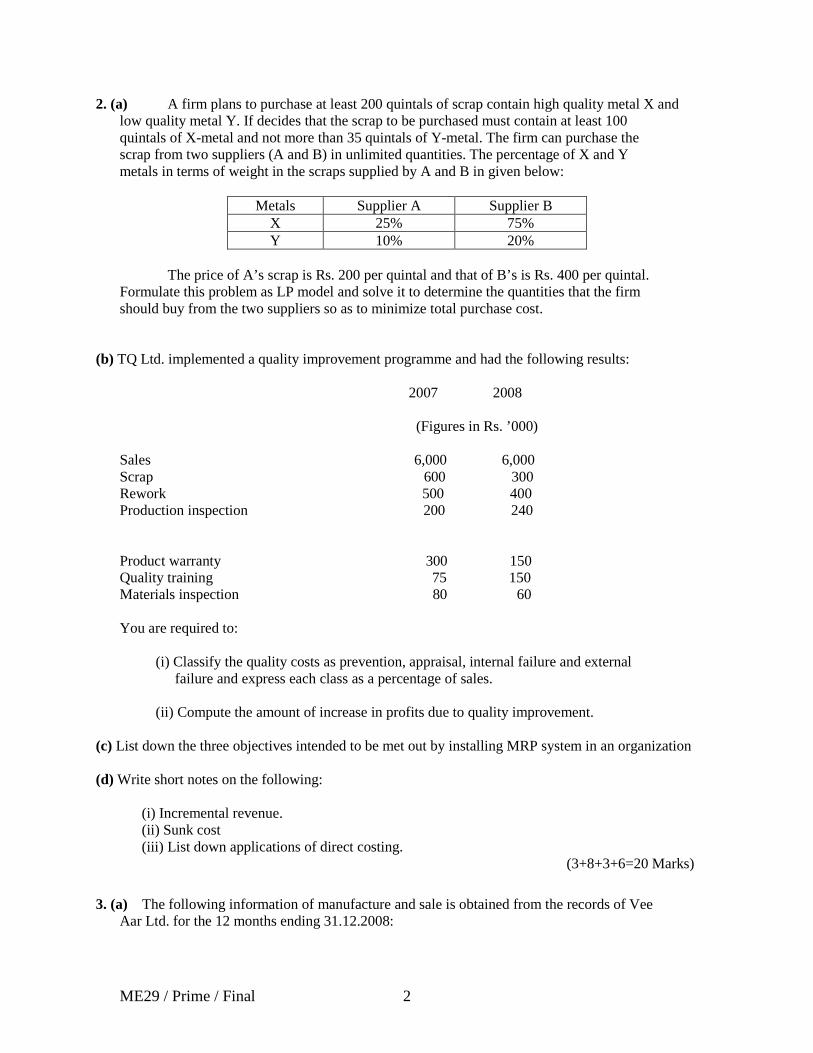

2. (a) A firm plans to purchase at least 200 quintals of scrap contain high quality metal X and low quality metal Y. If decides that the scrap to be purchased must contain at least 100 quintals of X-metal and not more than 35 quintals of Y-metal. The firm can purchase the scrap from two suppliers (A and B) in unlimited quantities. The percentage of X and Y metals in terms of weight in the scraps supplied by A and B in given below:

Metals Supplier A Supplier B X 25% 75% Y 10% 20%

The price of A’s scrap is Rs. 200 per quintal and that of B’s is Rs. 400 per quintal. Formulate this problem as LP model and solve it to determine the quantities that the firm should buy from the two suppliers so as to minimize total purchase cost.

(b) TQ Ltd. implemented a quality improvement programme and had the following results: 2007 2008 (Figures in Rs. ’000) Sales 6,000 6,000 Scrap 600 300 Rework 500 400 Production inspection 200 240 Product warranty 300 150 Quality training 75 150 Materials inspection 80 60 You are required to:

(i) Classify the quality costs as prevention, appraisal, internal failure and external failure and express each class as a percentage of sales. (ii) Compute the amount of increase in profits due to quality improvement.

(c) List down the three objectives intended to be met out by installing MRP system in an organization (d) Write short notes on the following:

(i) Incremental revenue. (ii) Sunk cost (iii) List down applications of direct costing.

(3+8+3+6=20 Marks)

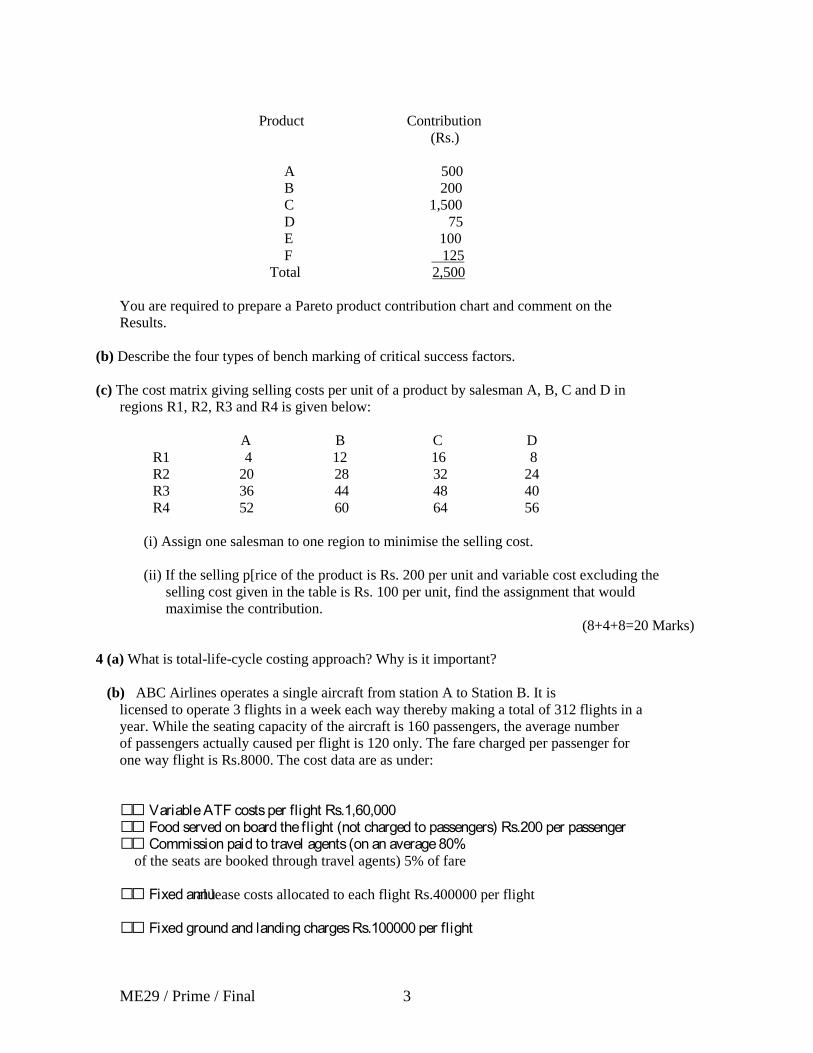

3. (a) The following information of manufacture and sale is obtained from the records of Vee Aar Ltd. for the 12 months ending 31.12.2008:

ME29 / Prime / Final 3

Product Contribution (Rs.) A 500 B 200 C 1,500 D 75 E 100 F 125 Total 2,500 You are required to prepare a Pareto product contribution chart and comment on the Results.

(b) Describe the four types of bench marking of critical success factors.

(c) The cost matrix giving selling costs per unit of a product by salesman A, B, C and D in regions R1, R2, R3 and R4 is given below: A B C D R1 4 12 16 8 R2 20 28 32 24 R3 36 44 48 40 R4 52 60 64 56

(i) Assign one salesman to one region to minimise the selling cost. (ii) If the selling p[rice of the product is Rs. 200 per unit and variable cost excluding the selling cost given in the table is Rs. 100 per unit, find the assignment that would maximise the contribution.

(8+4+8=20 Marks)

4 (a) What is total-life-cycle costing approach? Why is it important?

(b) ABC Airlines operates a single aircraft from station A to Station B. It is licensed to operate 3 flights in a week each way thereby making a total of 312 flights in a year. While the seating capacity of the aircraft is 160 passengers, the average number of passengers actually caused per flight is 120 only. The fare charged per passenger for one way flight is Rs.8000. The cost data are as under: Variable ATF costs per flight Rs.1,60,000 Food served on board the flight (not charged to passengers) Rs.200 per passenger Commission paid to travel agents (on an average 80% of the seats are booked through travel agents) 5% of fare Fixed annual lease costs allocated to each flight Rs.400000 per flight Fixed ground and landing charges Rs.100000 per flight

ME29 / Prime / Final 4

Fixed salaries of flight crew allocated to each flight Rs.60000 per flight Required:

(i) Compute the operating income on each one-way flight between stations A and B. (ii) The company has been advised that in case the fare is reduced to Rs.7500 per flight per passenger, the average number of passengers per flight will increase to 132. Should this proposal be implemented? Show your calculations. (c) What is trend? What are the various methods of fitting a straight line to a time series?

(4+12+4=20 Marks)

5(a) Explain, how the implementation of JIT approach to manufacturing can be a major source of competitive advantage.

(b) A project consists of seven activities and the time estimates of the activities are furnished as under:

Activity Optimistic Days Most likely Days Pessimistic Days

1-2 4 10 16 1-3 3 6 9 1-4 4 7 16

2-5` 5 5 5 3-5 8 11 32 4-6 4 10 16 5-6 2 5 8

Required:

(i) Draw the network diagram. (ii) Identify the critical path and its duration. (iii) What is the probability that the project will be completed in 5 days earlier than the critical path duration? (iv) What project duration will provide 95% confidence level of completion (Z0.95 =1.65)?

Given:

Z 1.00 1.09 1.18 1.25 1.33

Probability 0.1587 0.1379 0.1190 0.1056 0.0918

ME29 / Prime / Final 5

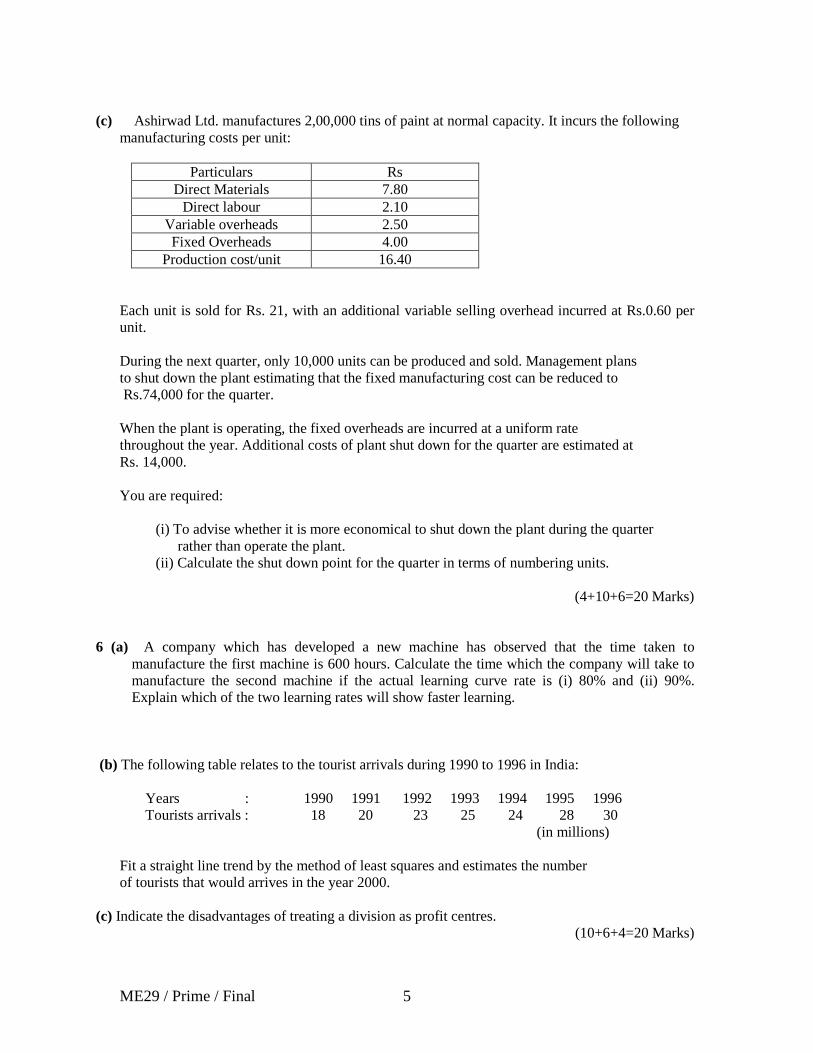

(c) Ashirwad Ltd. manufactures 2,00,000 tins of paint at normal capacity. It incurs the following

manufacturing costs per unit:

Particulars Rs Direct Materials 7.80

Direct labour 2.10 Variable overheads 2.50 Fixed Overheads 4.00

Production cost/unit 16.40 Each unit is sold for Rs. 21, with an additional variable selling overhead incurred at Rs.0.60 per unit. During the next quarter, only 10,000 units can be produced and sold. Management plans to shut down the plant estimating that the fixed manufacturing cost can be reduced to Rs.74,000 for the quarter. When the plant is operating, the fixed overheads are incurred at a uniform rate throughout the year. Additional costs of plant shut down for the quarter are estimated at Rs. 14,000. You are required:

(i) To advise whether it is more economical to shut down the plant during the quarter rather than operate the plant. (ii) Calculate the shut down point for the quarter in terms of numbering units.

(4+10+6=20 Marks)

6 (a) A company which has developed a new machine has observed that the time taken to manufacture the first machine is 600 hours. Calculate the time which the company will take to manufacture the second machine if the actual learning curve rate is (i) 80% and (ii) 90%. Explain which of the two learning rates will show faster learning.

(b) The following table relates to the tourist arrivals during 1990 to 1996 in India: Years : 1990 1991 1992 1993 1994 1995 1996 Tourists arrivals : 18 20 23 25 24 28 30 (in millions) Fit a straight line trend by the method of least squares and estimates the number of tourists that would arrives in the year 2000.

(c) Indicate the disadvantages of treating a division as profit centres. (10+6+4=20 Marks)

ME29 /Prime /Final 1

PRIME ACADEMY 29th

SQ AQ SP SQ SP AQ SP AP AQ AP 59,400

SESSION MODEL EXAM ADVANCED MANAGEMENT ACCOUNTING– NEW SYLLABUS

SUGGESTED ANSWERS

1 a) Target Costing: It is a management tool used for reducing a product cost over its entire life cycle. It is driven by external Market factors. Marketing management prior to designing and introducing a new product determines a target market price. This target price is set at a level that will permit the company to achieve a desired market share and sales volume. A desired profit margin is then deducted to determine the target maximum allowable product cost. Target costing also develops methods for achieving those targets and means to test the cost effectiveness of different cost cutting scenarios. Stages of Target Costing: 1. Conception (planning) Phase: Under this stage of life cycle, competitors products are to be

analysed, with regard to price, quality, service and support, delivery and technology. The features which consumers would like to have like consumer value etc. established. After preliminary testing, the company may be asked to pinpoint a market niche, it believes, is under supplied and which might have some competitive advantage.

2. Development phase: The design department should select the most competitive product in the

market and study in detail the requirement of material, manufacturing process along with competitors cost structure. The firm should also develop estimates of internal cost structure based on internal cost of similar products being produced by the company. If possible the company should develop both the cost structures (competitors and own) in terms of cost drivers for better analysis and cost reduction.

3. Production phase: This phase concentrates its search for better and less expensive products,

cost benefit analysis in different features of a product priority wise, more towards less expensive means of production, as well as production techniques etc.

1 b) Direct Materials:

Usage variance Price variance 1200 A 600 A AQ SP = 58,8001 SQ SP = 57,6002 Standard cost of materials for actual output of 9,600 units = Rs. 57,600. Hence, standard cost per unit is 57,600 / 9,600 = Rs. 6.

ME29 /Prime /Final 2

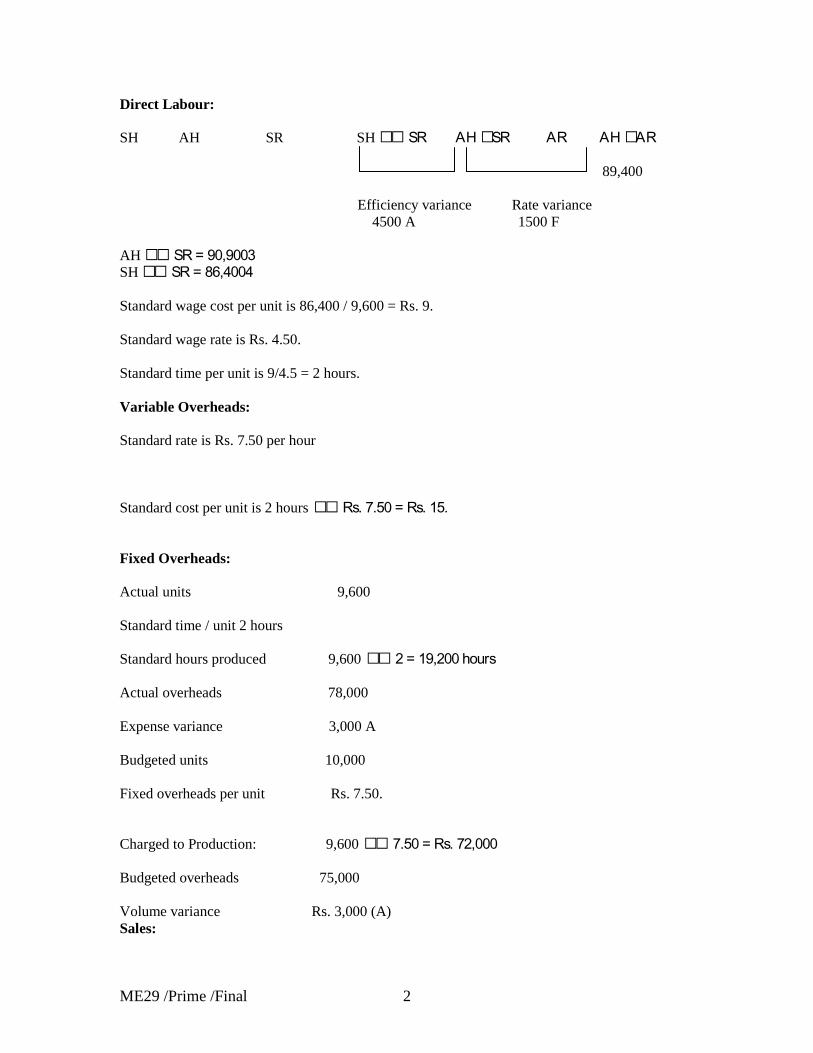

Direct Labour: SH AH SR SH SR AH SR AR AH AR 89,400 Efficiency variance Rate variance 4500 A 1500 F AH SR = 90,9003 SH SR = 86,4004 Standard wage cost per unit is 86,400 / 9,600 = Rs. 9. Standard wage rate is Rs. 4.50. Standard time per unit is 9/4.5 = 2 hours. Variable Overheads: Standard rate is Rs. 7.50 per hour Standard cost per unit is 2 hours Rs. 7.50 = Rs. 15. Fixed Overheads: Actual units 9,600 Standard time / unit 2 hours Standard hours produced 9,600 2 = 19,200 hours Actual overheads 78,000 Expense variance 3,000 A Budgeted units 10,000 Fixed overheads per unit Rs. 7.50. Charged to Production: 9,600 7.50 = Rs. 72,000 Budgeted overheads 75,000 Volume variance Rs. 3,000 (A) Sales:

ME29 /Prime /Final 3

SQ AQ SP SQ SP AQ SP AP AQ AP 4,45,500 Price variance 13,500 F AQ SP = 4,32,0005 Actual units = 9,600 Standard price is 4,32,000 / 9,600 = Rs. 45 per unit. Original Budget and Standard Cost Sheet: Budget Standard Cost Units budgeted 10,000 Sales 4,50,000 45.00 Direct materials @ Rs. 6 per unit 60,000 6.00 Direct Wages 90,000 9.00 Variable Overheads @ Rs. 15 per unit 1,50,000 15.00 Fixed overheads @ Rs. 7.50 per unit 75,000 7.50 Total costs 3,75,000 37.50 Profit 75,000 7.50 Sales volume variance is (9,600 – 10,000) 7.50 = Rs. 3,000 A Reconciliation Statement: Budgeted Profit 75,000 Sales volume variance 3,000 A Standard profit 72,000 Sales price variance 13,500 F Total 85,500

ME29 /Prime /Final 4

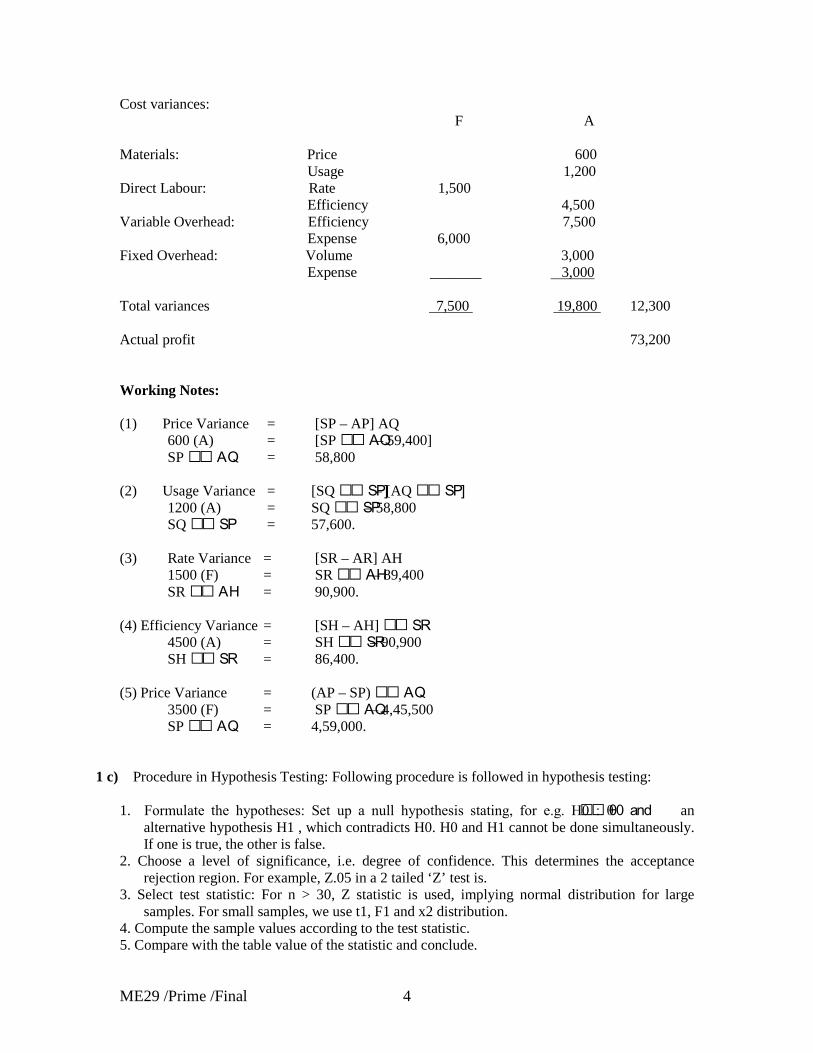

Cost variances: F A Materials: Price 600 Usage 1,200 Direct Labour: Rate 1,500 Efficiency 4,500 Variable Overhead: Efficiency 7,500 Expense 6,000 Fixed Overhead: Volume 3,000 Expense _______ 3,000 Total variances 7,500 19,800 12,300 Actual profit 73,200 Working Notes: (1) Price Variance = [SP – AP] AQ 600 (A) = [SP AQ – 59,400] SP AQ = 58,800 (2) Usage Variance = [SQ SP] – [AQ SP] 1200 (A) = SQ SP – 58,800 SQ SP = 57,600. (3) Rate Variance = [SR – AR] AH 1500 (F) = SR AH – 89,400 SR AH = 90,900. (4) Efficiency Variance = [SH – AH] SR 4500 (A) = SH SR – 90,900 SH SR = 86,400. (5) Price Variance = (AP – SP) AQ 3500 (F) = SP AQ – 4,45,500 SP AQ = 4,59,000.

1 c) Procedure in Hypothesis Testing: Following procedure is followed in hypothesis testing: 1. Formulate the hypotheses: Set up a null hypothesis stating, for e.g. H0 : θ θ0 and an

alternative hypothesis H1 , which contradicts H0. H0 and H1 cannot be done simultaneously. If one is true, the other is false.

2. Choose a level of significance, i.e. degree of confidence. This determines the acceptance rejection region. For example, Z.05 in a 2 tailed ‘Z’ test is.

3. Select test statistic: For n > 30, Z statistic is used, implying normal distribution for large samples. For small samples, we use t1, F1 and x2 distribution.

4. Compute the sample values according to the test statistic. 5. Compare with the table value of the statistic and conclude.

ME29 /Prime /Final 5

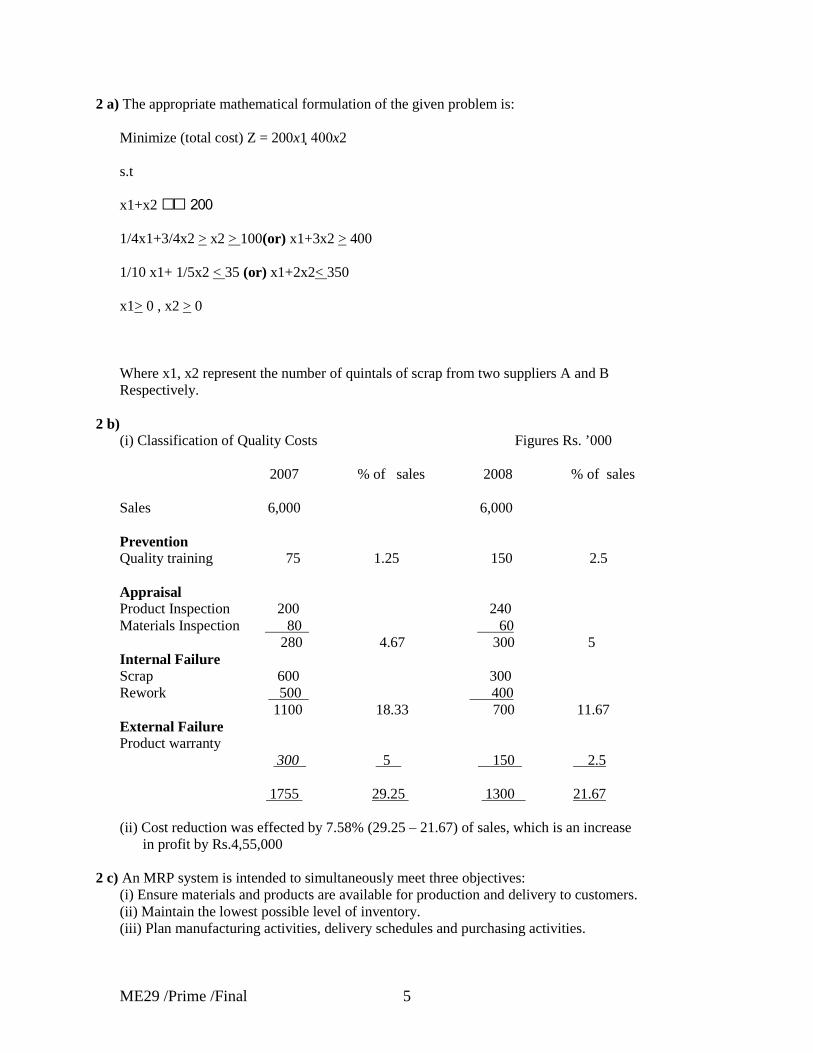

2 a) The appropriate mathematical formulation of the given problem is: Minimize (total cost) Z = 200x1 400x2 s.t x1+x2 200 1/4x1+3/4x2 > x2 > 100(or) x1+3x2 > 400 1/10 x1+ 1/5x2 < 35 (or) x1+2x2< 350 x1> 0 , x2 > 0 Where x1, x2 represent the number of quintals of scrap from two suppliers A and B Respectively.

2 b) (i) Classification of Quality Costs Figures Rs. ’000 2007 % of sales 2008 % of sales Sales 6,000 6,000 Prevention Quality training 75 1.25 150 2.5 Appraisal Product Inspection 200 240 Materials Inspection 80 60 280 4.67 300 5 Internal Failure Scrap 600 300 Rework 500 400 1100 18.33 700 11.67 External Failure Product warranty 300 5 150 2.5 1755 29.25 1300 21.67 (ii) Cost reduction was effected by 7.58% (29.25 – 21.67) of sales, which is an increase in profit by Rs.4,55,000

2 c) An MRP system is intended to simultaneously meet three objectives: (i) Ensure materials and products are available for production and delivery to customers. (ii) Maintain the lowest possible level of inventory. (iii) Plan manufacturing activities, delivery schedules and purchasing activities.

ME29 /Prime /Final 6

2 d) (i) Incremental revenue: It is the additional revenue that arise from production or sale of a group

of additional units. It is one of the two concepts the other being incremental cost. Both these concepts helps in decision making process.

(ii) Sunk cost: costs which remain static under all circumstances. These are also called historical

costs incurred in the past having no impact on any decisions made in the organization in future. Amortisation of past expenses is the clearest kind of sunk cost. Eg: amount paid on purchase of land etc.

(iii) The applications of direct costing are as under:

(i) Stock valuation. (ii) Close down decisions. (iii) Minimum quantity to be produced to recover pattern or mould cost.

3 a) Let us rearrange the products in descending order of contribution and find out the cumulative contribution percentage. Product Contribution Cumulative Cumulative contribution contribution (Rs.) (Rs.) (%) C 1,500 1,500 60 A 500 2,000 80 B 200 2,200 88 F 125 2,325 93 E 100 2,425 97 D 75 2,500 100 2,500 On analysis it is found that 80% of the total contribution is earned by two products C and A. The position of these products needs protecting, perhaps through careful attention to branding and promotion. The other products should be investigated to see whether their contribution can be improved through increased prices, reduced costs, increased sales volume, etc.

3 b) The Benchmarking is of following types: (i) Competitive benchmarking: It involves the comparison of competitors products, processes and

business results with own. (ii) Strategic benchmarking: It is similar to the process benchmarking in nature but differs in its

scope and depth. (iii) Global benchmarking: It is a benchmarking through which distinction in international

culture, business processes and trade practices across companies are bridged and their ramification for business process improvement are understood and utilized.

(iv) Process benchmarking: It involves the comparison of an organisation critical business

processes and operations against best practice organization that performs similar work or deliver similar services.

ME29 /Prime /Final 7

(v) Functional Benchmarking or Generic Benchmarking: This type of benchmarking is used when organisations look to benchmark with partners drawn from different business sectors or areas of activity to find ways of improving similar functions or work processes.

(vi) Internal Benchmarking: It involves seeking partners from within the same organization, for

example, from business units located in different areas. (vii) External Benchmarking: It involves seeking help of outside organisations that are known to

be best in class. External benchmarking provides opportunities of learning from those who are at the leading edge, although it must be remembered that not every best practice solution can be transferred to others.

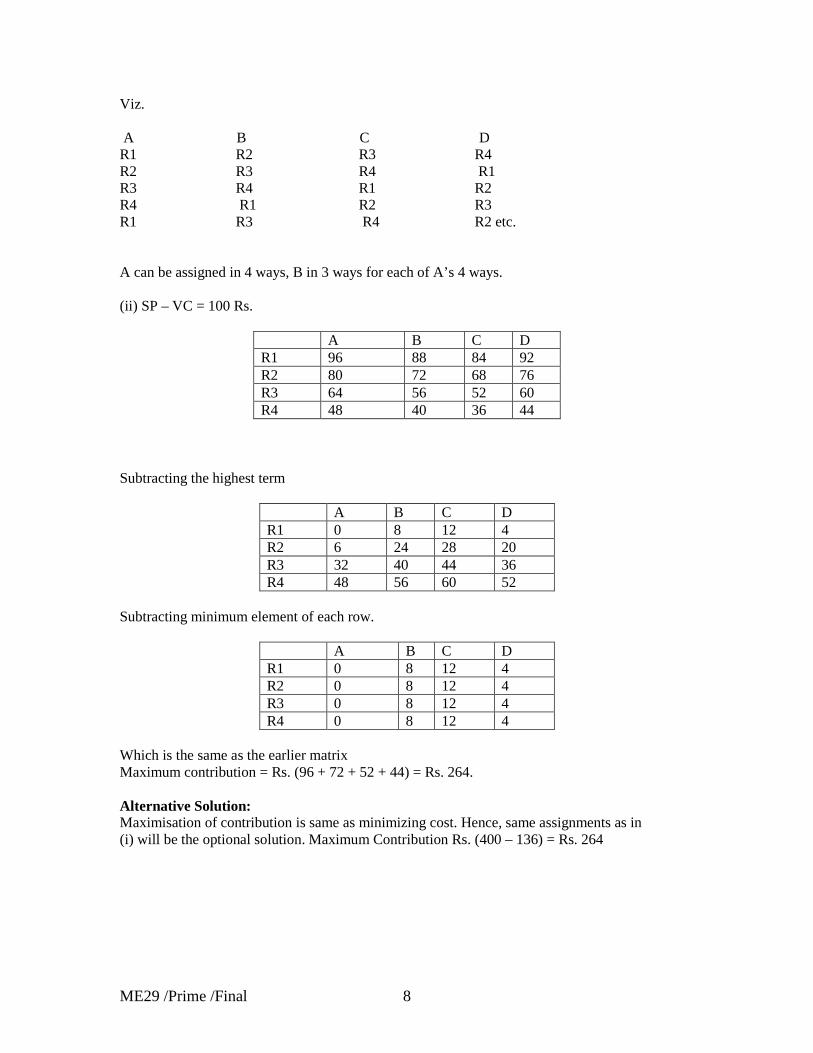

3 c) i)

A B C D R1 4 12 16 8 R2 20 28 32 24 R3 36 44 48 40 R4 52 60 64 56

Subtracting minimum element – each row. A B C D R1 0 8 12 4 R2 0 8 12 4 R3 0 8 12 4 R4 0 8 12 4 Subtracting minimum element – each column A B C D 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Minimum no. of lines to cover all zeros = 4 = order of matrix. Hence optional assignment is possible. Minimum cost = 4 + 28 + 48 + 56 = 136. = AR1 + BR2 + CR3 + DR4 Since all are zeros, there are 24 solutions to this assignment problem.

ME29 /Prime /Final 8

Viz. A B C D R1 R2 R3 R4 R2 R3 R4 R1 R3 R4 R1 R2 R4 R1 R2 R3 R1 R3 R4 R2 etc. A can be assigned in 4 ways, B in 3 ways for each of A’s 4 ways. (ii) SP – VC = 100 Rs.

A B C D R1 96 88 84 92 R2 80 72 68 76 R3 64 56 52 60 R4 48 40 36 44

Subtracting the highest term

A B C D R1 0 8 12 4 R2 6 24 28 20 R3 32 40 44 36 R4 48 56 60 52

Subtracting minimum element of each row.

A B C D R1 0 8 12 4 R2 0 8 12 4 R3 0 8 12 4 R4 0 8 12 4

Which is the same as the earlier matrix Maximum contribution = Rs. (96 + 72 + 52 + 44) = Rs. 264. Alternative Solution: Maximisation of contribution is same as minimizing cost. Hence, same assignments as in (i) will be the optional solution. Maximum Contribution Rs. (400 – 136) = Rs. 264

ME29 /Prime /Final 9

4 a) Total life cycle costing approach: Life cycle costing estimates tracks and accumulates the costs over a product’s entire life cycle from its inception to abandonment or from the initial R & D stage till the final customer servicing and support of the product. It aims at tracing of costs and revenues on product by Product basis over several calendar periods throughout their life cycle. Costs are incurred along the product’s life cycle starting from product’s design, development, manufacture, marketing, servicing and final disposal. The objective is to accumulate all the costs over a product life cycle to determine whether the profits earned during the manufacturing phase will cover the costs incurred during the pre and post manufacturing stages of product life cycle. Product life cycle costing is important for the following reasons: (i) When non-production costs like costs associated with R & D, design, marketing, distribution

and customer service are significant, it is essential to identify them for target pricing, value engineering and cost management. For example, a poorly designed software package may involve higher costs on marketing, distribution and after sales service.

(ii) There may be instances where the pre-manufacturing costs like R & D and design are

expected to constitute a sizeable portion of life cycle costs. When a high percentage of total life cycle costs are likely to be so incurred before the commencement of production, the firm needs an accurate prediction of costs and revenues during the manufacturing stage to decide whether the costly R & D and design activities should be undertaken.

(iii) Many costs are locked in at R & D and design stages. Locked in or Committed costs are

those costs that have not been incurred at the initial stages of R & D and design but that will be incurred in the future on the basis of the decisions that have already been taken.

For example, the adoption of a certain design will determine the product’s material and labour inputs to be incurred during the manufacturing stage. A complicated design may lead to greater expenditure on material and labour costs every time the product is produced. Life cycle budgeting highlights costs throughout the product life cycle and facilitates value engineering at the design stage before costs are locked in. Total life-cycle costing approach accumulates product costs over the value chain. It is a process of managing all costs along the value chain starting from product’s design, development, manufacturing, marketing, service and finally disposal.

ME29 /Prime /Final 10

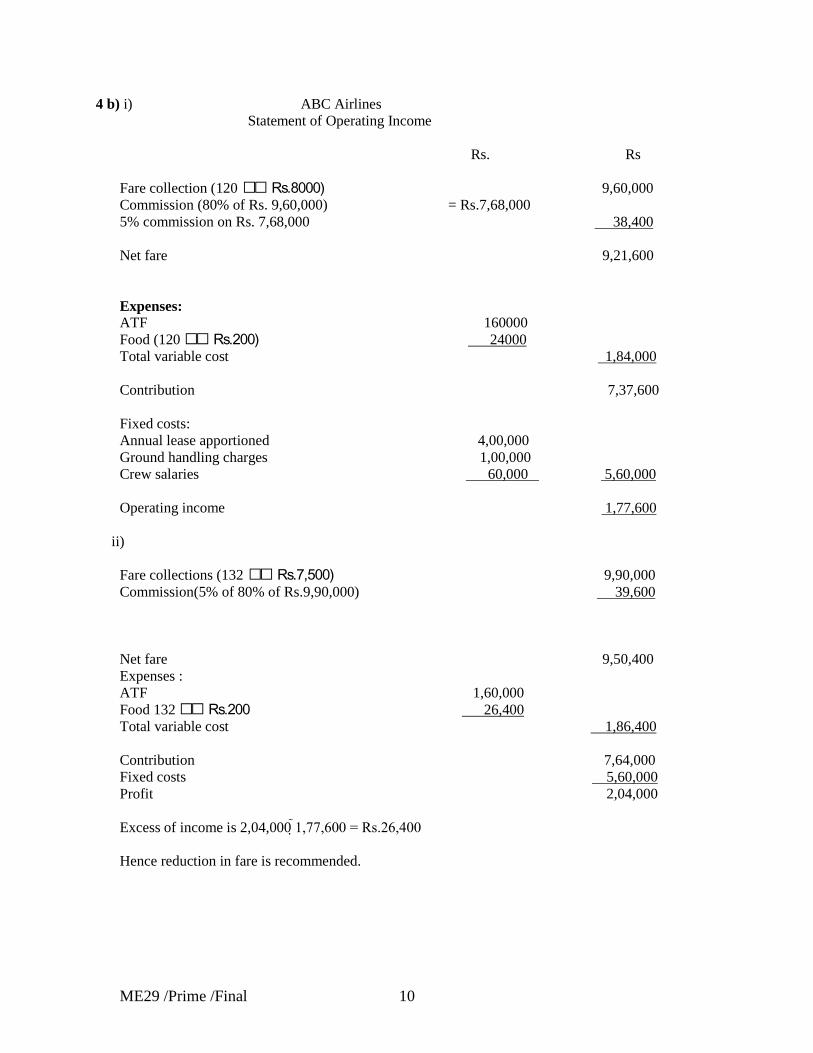

4 b) i) ABC Airlines Statement of Operating Income Rs. Rs Fare collection (120 Rs.8000) 9,60,000 Commission (80% of Rs. 9,60,000) = Rs.7,68,000 5% commission on Rs. 7,68,000 38,400 Net fare 9,21,600 Expenses: ATF 160000 Food (120 Rs.200) 24000 Total variable cost 1,84,000 Contribution 7,37,600 Fixed costs: Annual lease apportioned 4,00,000 Ground handling charges 1,00,000 Crew salaries 60,000 5,60,000 Operating income 1,77,600

ii) Fare collections (132 Rs.7,500) 9,90,000 Commission(5% of 80% of Rs.9,90,000) 39,600 Net fare 9,50,400 Expenses : ATF 1,60,000 Food 132 Rs.200 26,400 Total variable cost 1,86,400 Contribution 7,64,000 Fixed costs 5,60,000 Profit 2,04,000 Excess of income is 2,04,000 1,77,600 = Rs.26,400 Hence reduction in fare is recommended.

ME29 /Prime /Final 11

4 c) Trend is the long term movement of a time series. Any increase or decrease in the values of a variable occurring over a period of several years gives a trend. The various methods of fitting a straight line to a time series are: (i) Free hand method. (ii) The method of semi-averages. (iii) The method of moving averages. (iv) The method of least squares.

5 a). JIT provides competitive advantage in the following ways: (i) Stocks of raw materials and finished goods are eliminated, stock holding costs are avoided. (ii) JIT aims at elimination of non-value added activities and elimination of cost in this direction

will improve competitive advantage. (iii) It affords flexibility to customer requirements where the company can manufacture

customized products and the competitive advantage is thereby improved. (iv) It focuses the direction of performance based production of high quality product. (v) It minimize waiting times and transportation costs.

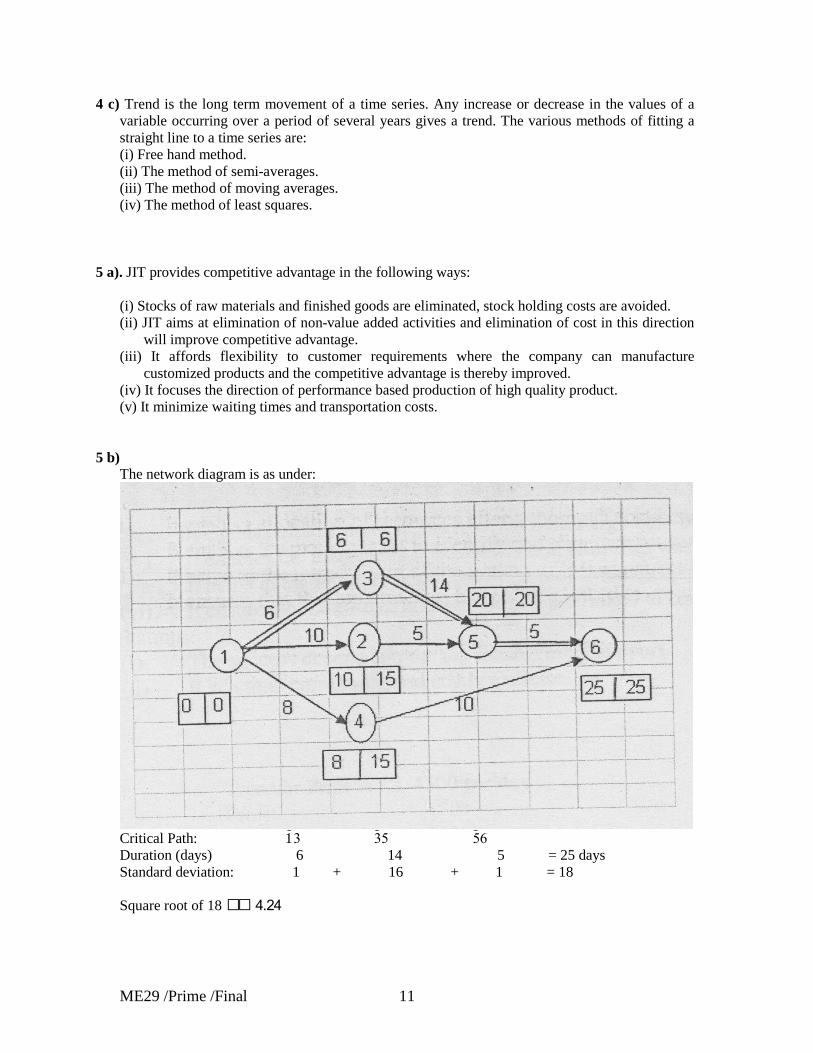

5 b) The network diagram is as under:

Critical Path: 1 3 35 56 Duration (days) 6 14 5 = 25 days Standard deviation: 1 + 16 + 1 = 18 Square root of 18 4.24

ME29 /Prime /Final 12

Probability that the project will be completed five days earlier: Z= 20-25 = -1.18 4.24 According to probability values given in the question probability is 11.9% To obtain 95% confidence level: 1.65 = X-25 4.24 X-25=6.996 X= 32 days.

5 c) Contribution per tin = Selling Price – Variable cost = 21 – (7.8 + 2.1+ 2.5 + 0.6) = Rs. 8 per tin. Loss on operation: Fixed cost per annum = 2,00,000 units 4 per unit = 8 lakhs. Fixed cost for 1 quarter = 8/4 = 2 lakhs Rs. Fixed cost for the quarter 2,00,000 Less: Contribution on operation (8 10,000) 80,000 Expected loss on operation (1,20,000) Loss on shut down: Rs. Unavoidable Fixed Cost 74,000 Additional shut down cost 14,000 Loss on shut-down (88,000) Conclusion: Better to shut down and save Rs. 32,000. Shut-down point (number of units) = Avoidable Fixed Cost Contribution per unit = 2,00,000-88,000 8 = 1,12,000 8 = 14,000 units

ME29 /Prime /Final 13

6 a) (i) Actual learning curve rate is 80%.

Time taken to produce the first machine = 600 hours Average time taken to produce two machines = 600 80% hours = 480 hours. Cumulative time taken to produce two machines = 480 2 hours = 960 hours. Time taken to produce the second machine = (960 600)hours = 360 hours.

(ii) Actual learning curve rate is 90%.

Time taken to produce the first machine = 600 hours Average time taken to produce two machines = 600 90% hours = 540 hours. Cumulative time taken to produce two machines = 540 2 hours = 1080 hours. Time taken to produce the second machine = (1080 600) hours = 480 hours. The time taken to produce the second machine is lower at 80% learning rate. Hence 80% learning rate shows faster learning rate.

6 b) Fitting straight line Trend by the Method of Least square

Year X

Tourist Arrival (in millions) Y

X

XY

X2

1990 18 -3 -54 9 1991 20 -2 -40 4 1992 23 -1 -23 1 1993 25 0 0 0 1994 24 1 24 1 1995 28 2 56 4 1996 30 3 90 9

N= 7 , Sum of Y = 168 , sum of X = 0 , Sum of XY = 53 , Sum of X2 = 28 The equation of the straight line trend is : Y = a + bx Since Sum of X = 0 , a = Sum of Y = 168 = 24 N 7 And b = Sum of XY = 53 = 1.893 Sum of X2 28

ME29 /Prime /Final 14

Hence Y = 24 + 1.893x Estimated Number of tourists that would arrive in 2000 Y = 24 + 1.893 (7) = 24 + 13.251 = 37.251 million.

6 c) The possible disadvantage of treating a division as profit centre are as under:

(i) Divisions may compete with each other and may take decisions to increase profit at the expense of other divisions thereby overemphasizing short term results.

(ii) It may adversely affect co-operation between divisions and lead to lack of harmony in achieving organizational goals of the company. Thus it becomes difficult to achieve the concept of goal congruence.

(iii) It may lead to reduction in overall profit of the company. (iv) It leads to complications associated with transfer pricing problems. (v) It becomes difficult to precisely identify suitable profit centres.

1 ME29 / Prime /Final

ISCA

Number of Pages : 2 Total Marks: 100 Number of questions: 7 Time Allowed: 3 Hrs

Question No.1 is compulsory. Answer any four questions from the remaining

1 (a) “The move towards more automated financial statements has had an impact in the way auditors carry out their work”- explain

(10 Marks)

(b) “There are many reasons why organisations fail to meet the systems development objective”-Explain

(10 Marks)

2 (a) What are the causes for errors and bugs in softwares? (10 Marks)

(b) What role is Information Systems Audit policy expected to play in ensuring information

security? What the objectives are of IS Audit (10 Marks)

3(a) Explain the 8 phases of BCP plan formulation in brief

(10 Marks)

(b) Explain the three broad types of information required by executives (5 Marks)

(c) Explain as 5 data integrity controls in brief.

(5 Marks)

4 (a) Explain in detail the role of IS Auditor in audit of logical access controls (10 Marks)

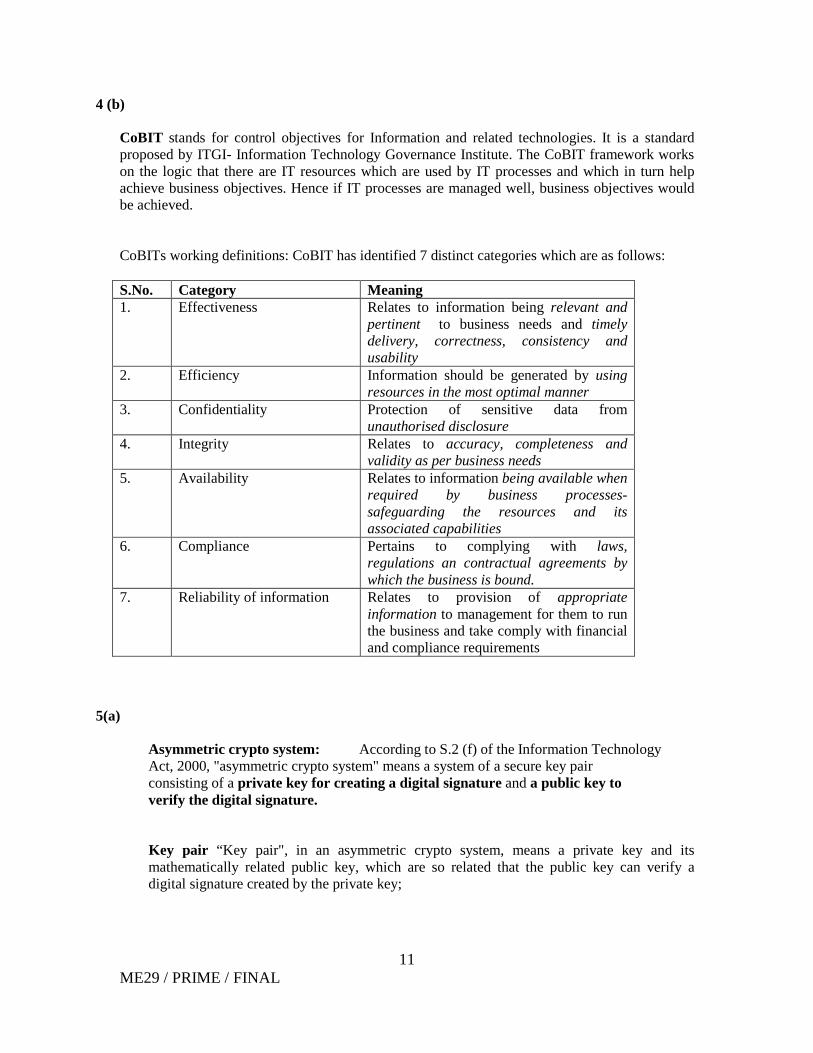

(b) Explain CoBIT. What is its working definition?

(10 Marks)

5 (a) Explain the terms: Asymmetric crypto systems, Key pair, Digital signature as per the IT Act, 2000

(10 Marks) (b) “The benefits accruing to business enterprise by implementing an ERP are unlimited”- explain

(10 Marks)

6 (a) What are the pre-requisites of an effective MIS (10 Marks)

2 ME29 / Prime /Final

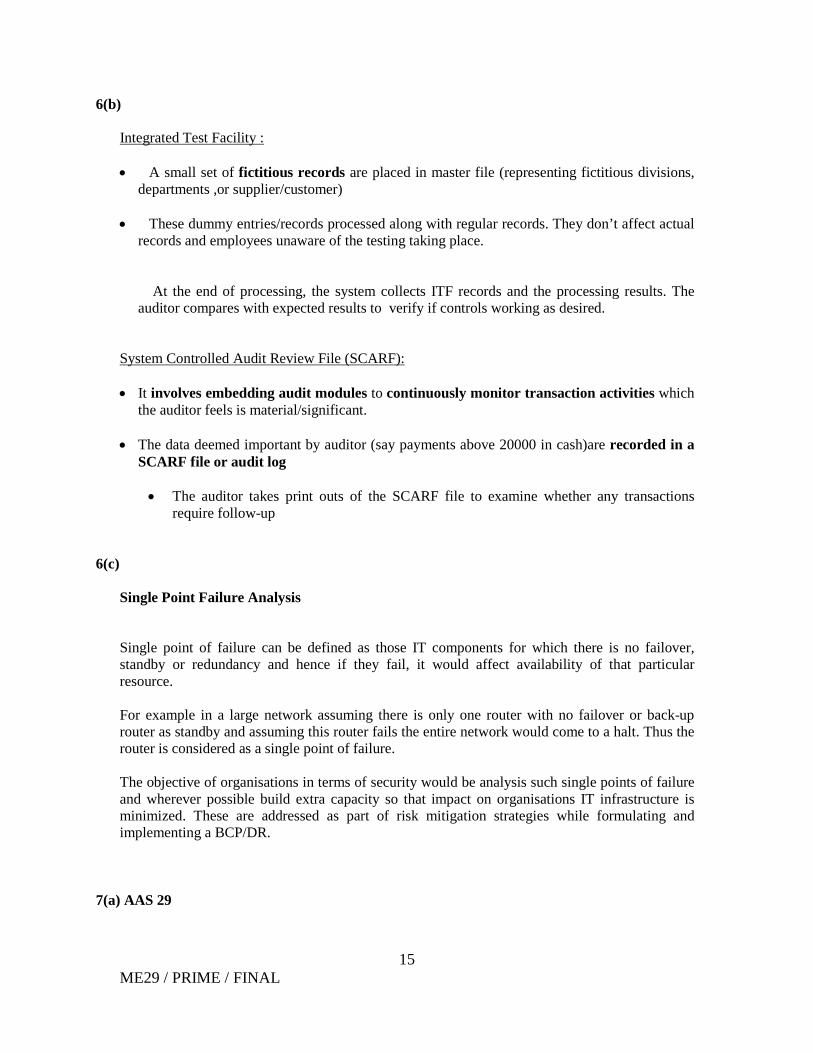

(b) Explain in brief the meaning of ITF and SCARF (5 Marks)

(c) Explain the term single point failure analysis

(5 Marks)

7 Write short notes on the following:

(a) AAS 29 (b) Bio-Metric devices (c) Systematic and un-systematic risk (d) Residuary Risk

(4 x 5 Marks = 20 Marks)

1 ME29 / PRIME / FINAL

PRIME ACADEMY

29TH SESSION MODEL EXAM

INFORMATION SYSTEMS CONTROL AND AUDIT - NEW SYLLABUS

SUGGESTED ANSWERS

1 (a) As organizations move towards computerization of their business processes (Information

Systems), the internal control mechanisms and audit processes also undergo a change. While the control objectives (purpose to be achieved by implementing a control) in a computerised environment may remain same as in manual environment, the manner in which controls are implement may be different. For example internal controls as known in manual environment (i.e. non computerized environment) like physical verification of documents or two people authorizing high value payments by signing the vouchers etc. may not work in a computerised environment. These may be replaced by online authorisation process etc. The impact of IS on audit process can be classified into: 1. Change in audit trail and audit evidence (i.e. moving towards digital evidence) 2. Change in internal control environment 3. High probability for unconventional errors and frauds (i.e. cyber crimes) 4. Change in audit procedures 1. Change in audit trail and audit evidence While in manual environment audit trails were easily visible and traceable, in computerised environment the audit trails are fragmented and difficult to trace. For example a payment voucher manually generated provides sufficient audit trail. If the same payment is made through say electronic clearing system or net banking, audit trails are not very visible and difficult for the auditor to trace. This is called as digital evidence. Issues relating to digital evidence are: a. Data Retention Policy: Depending on the data retention policy of and organisation, past transactions may or may not be readily available for verification on the system. They may have to be retrieved on demand. Also the data stored on the system may require specific software to interpret the data and may be as easy as auditing from a printed document. b. Direct data entry or lack of physical input documents: Many transaction processing systems work under the direct entry mode wherein data is input into the system directly without any supporting documents- for example ATM transactions which affects account balances but has no input documents. c. Lack of visible audit trail or short retention period of audit trails: Some organisations retain audit trails only for a short period of time- thus auditors may have to modify his audit approach suitably to look for compensating controls d. Reduction in printed outputs : As printed outputs are declining, audits may have to be carried out directly on data on the system through a separate access mechanism.

2 ME29 / PRIME / FINAL

e. Automated or system generated transactions: Certain transactions are system generated- for example if safety stock and re-order limits are set in an ERP, on reaching a particular stocking quantity, the ERP system may generate an automated purchase order and even email it to the supplier/vendor. Such transactions have no human intervention for authorisation and hence no judgment thereby increasing the chances of errors. f. Legal Issues: In contracts and payments which are concluded online, territorial jurisdiction issues arise as regards place of origination, taxation, dispute resolution etc. For example for an online purchase of goods, the buyer may be located in one state, the web site may be located in a server in another state or country, the goods may be shipped from a different location and payment may be credited online with a Bank in another country. In such a transaction, fixing the jurisdiction for say a dispute is quite difficult. Similarly admissibility of digital evidence-i.e whether it is good evidence or not- in a court of law is a challenge and is in very nascent stages.

Integrity and competency of personnel

2. Change in internal control environment Some of the basic internal controls in an organisation pertain to :

Segregation of duties in order to ensure that a single person cannot put through a transaction end to end.

Maker-checker or authorisation procedures Control over documents Access restrictions over assets and records (ex: cash as an asset can be accessed only by

authorised personnel) Overall control and supervision by the management

While the need for the above mentioned controls are there even in a computerised environment, the methodology of implementing the controls may be different. For example: a. Segregation of duties: In manual environment the auditor was concerned with say whether the maintenance of cash function was segregated from the physical verification of cash function. Similar control in computerised environment would be segregation within IT Department- say systems administration function should be segregated from computer operator function. In computerized environment proper segregation of duties is essential since a risk arises if one employee or group of employees are aware of the complete data flow and process logic. b. Centralization of data and application programs: Predominantly most organisations choose to centralize their data and programs in a single server or servers in one location. For example all the program and customer data of a Bank is located in one location called as the Data Centre. This is in contrast to a manual environment where data was stored in distributed locations (say at various branches). While centralization helps in operational efficiency, the impact of a threat is far greater since there is concentration at one place. For example if the data centre fails or is hacked, entire operations would come to a stand still.

3 ME29 / PRIME / FINAL

c. Access Controls: While in manual environment access control was predominantly physical access control (like door locks, security guard etc.) in computerised environment the access controls are predominantly logical access controls (like passwords, PIN etc.). 3. High probability for unconventional errors and frauds (i.e cyber crimes) a. Triggered transactions or system generated transactions: As discussed in earlier paragraphs, system generated transactions are difficult to trace and audit and it requires knowledge about the program functioning. b. Systematic errors : Computers are programmed to do transactions in a consistent manner- i.e. same inputs with the same application software would generate same outputs every time. Thus correct input and correct processing would always lead to correct output. While correct input with wrong processing would always lead to wrong output. For example one error in payroll software can lead to all net salary values for the month being calculated erroneously. Thus the impact is wide spread and needs to be corrected at the source rather than at the transaction level.

• Developers and users watch as to which projects are getting senior manager attention. They would shift focus from projects they feel is not getting the required attention of top management.

4. Change in audit procedures Since most of the audit evidence required to form an opinion is system based, manual audit procedures may not prove to be effective in a computerised environment. For example use of audit tools like ACL, IDEA may be required to query data and obtain sufficient evidence from a computerised environment.

1(b) Some reasons which can be attributed for failure of systems development objective are:

1. Lack of senior management effort and involvement:

• Also it is the top management which commits resources to the projects and

controls its progress.

2. Shifting user needs (called as scope creep- due to lack of software baselining)

• User requirements for information systems keep changing. More changes imply more requests for systems development and more development projects.

• Also if changes occur during development effort, there would be no baseline

and developers find it very difficult to provide for every change request.

4 ME29 / PRIME / FINAL

Ex: Say a accounts software is in the process of development. A user request comes asking for additional report generation not stated in earlier requirement specification. When this development is being done another user may come with further requests and so on, there is no end to it.

3. Development of unstructured or strategic systems.

• The requirements, specification and objectives of strategic systems are

difficult to define and hence it would be difficult to determine if development effort is successful or not.(Ex: Expert Systems)

4. New technologies

• When management tries to leverage new technology to its competitive advantage, it may face a problem that personnel are not familiar with the technology.

Ex: An organisation may want to achieve good results by implementing an ERP package, but may face a problem if users’ do not know how to use the package.

5. Lack of standard project management and systems development

methodologies.

• Lack of formal project management methodologies makes it difficult to stick to time schedules/budget schedules.

6. Over-worked or under-trained development efforts.

• Systems development team is over-worked due to constant requests

• Most of the company’s do not invest in employee training and hence the

employees are not up-date on current technologies.

7. Resistance to change

• Any development effort is countered by resistance to change.

• If employees perceive that as a result of business process re-engineering their power position will be affected or that there may be “down-sizing/retrenchment” they will work against the development effort.

8. Lack of user participation

• If users are not involved in the development efforts, they may not feel

responsible for the success of the projects. Also there may be resistance to change.

• Hence user involvement is critical to the success of the project.

5 ME29 / PRIME / FINAL

9. Inadequate testing and user training.

• If new systems are not tested properly, they may not meet the business objectives. Also it may give rise to control risks.

End user training on the new system is critical since any system is as effective as the user who uses it.

2(a) i. Errors associated with specifications/requirements: Specifications form the basis for software development. Following conditions associated with specifications give rise to errors:

a. Specifications are not documented b. Specifications are not comprehensive c. Constant change in specifications (shift in baseline/requirements)-lack of proper

communication to the development team ii. Errors associated with design: Design is the stage wherein the specifications are converted into a format understood by programmers. Following conditions associated with design give rise to errors:

a. Improper design b. Constant change in design c. Improper/lack of communication

iii. Errors associated with programming (i.e writing of codes) These are errors which creep in while the programmer is involved in the coding- i.e converting the design into a software program by writing lines of codes/instructions. Following conditions associated with design give rise to errors:

a. Complexity of the program logic b. Lack of or poor documentation c. Time and cost pressures associated with delivery schedules (i.e need to deliver the

software within a short span of time due to cost, time or business pressures) d. Programmers quality

Programming errors may be traced to poor specifications or poor testing processes.

6 ME29 / PRIME / FINAL

2(b) The purpose of the Audit policy is to provide the guidelines to the audit team to conduct an audit on IT infrastructure. The IS Audit policy should lay out the objective and the scope of the Policy. An IS Audit is conducted to :

a. Safeguard IS Assets b. Maintain data integrity c. Maintain effectiveness d. Maintain efficiency e. Comply with organizational policies

It lays down the responsibility of the audit. The policy also describes the frequency and authority to whom reporting is to be done Scope of IS Audit The scope of IS Audit is to assess the efficiency and effectiveness of the system of internal controls and the level of performance of IS. The purpose of IS Audit is to provide a reasonable assurance to the management as to whether IS will help achieve business objectives. Scope of IS Audit would include:

a. Data security b. Application software controls c. Technological controls d. Facilities or infrastructure based controls e. People or organizational structure controls

Items to be examined by IS Auditor would include:

a. IT mission statement and agreed goals and objectives b. The risk assessment and containment measures adopted in order to understand the

methodology adopted by management to address risk c. IT strategy plan and its monitoring mechanism (since this decides the long term focus

of the organization) d. IT Budgets and supervisions on it variations/deviations e. IT Usage Policy, IT protection policy and their monitoring and compliance f. How contracts are approved? How are service levels agreed with service provider

monitored to ensure they are in line with SLA? g. Procedure adopted for critical system acquisition h. Impact of Internet and other external connectivity on risk to IT set-up i. Prior audit, quality review reports , reports on self-assessments done on controls-

whether issues raised therein have been resolved on time j. BCP , Testing thereof k. Level of compliance with legal and regulatory requirements

7 ME29 / PRIME / FINAL

What should an IS Audit Policy do:

• Lays down the responsibility of the audit • IS Auditors should be independent of the activities they audit in order to maintain

objectivity • Lays down periodicity of reporting and authority to whom they should report • Describe the minimum qualification required to conduct the audit. • Provide a format for Non-disclosure agreement or secrecy agreement which IS

Auditor should sign prior to commencement of the audit (as he would be privy to a lot of sensitive data)

• The policy should define the extent of testing to be done as part of planning, compliance testing and substantive testing.

• A documented audit program would be developed to include: o Procedure for collecting, analysing and interpreting audit evidence o Objectives of audit o Scope, nature and extent of testing warranted o Identification of technical aspects,risks,processes and transactions to be

examined • Policy to define to whom and when audit results are to be reported • Access required for Auditors to carry out the audit will be specified • Areas for compliance testing would be identified • Whenever weaknesses are noticed as part of compliance testing, substantive testing

would be carried out • Define audit working papers to be maintained and their formats (either paper based

or automated working papers)

3(a) Eight Phases of Business Continuity Plan formulation and implementation are:

i. Plan initiation or pre-plan activity ii. Vulnerability/Control Assessment and basic definition of what the Plan should

address iii. Business Impact Analysis (BIA) iv. Detailed plan definitions v. Plan development/formulation vi. Test Program for the plan vii. Plan maintenance program viii. Testing and implementation of the plan

(Each of the above 8 phases to be explained in brief)

8 ME29 / PRIME / FINAL

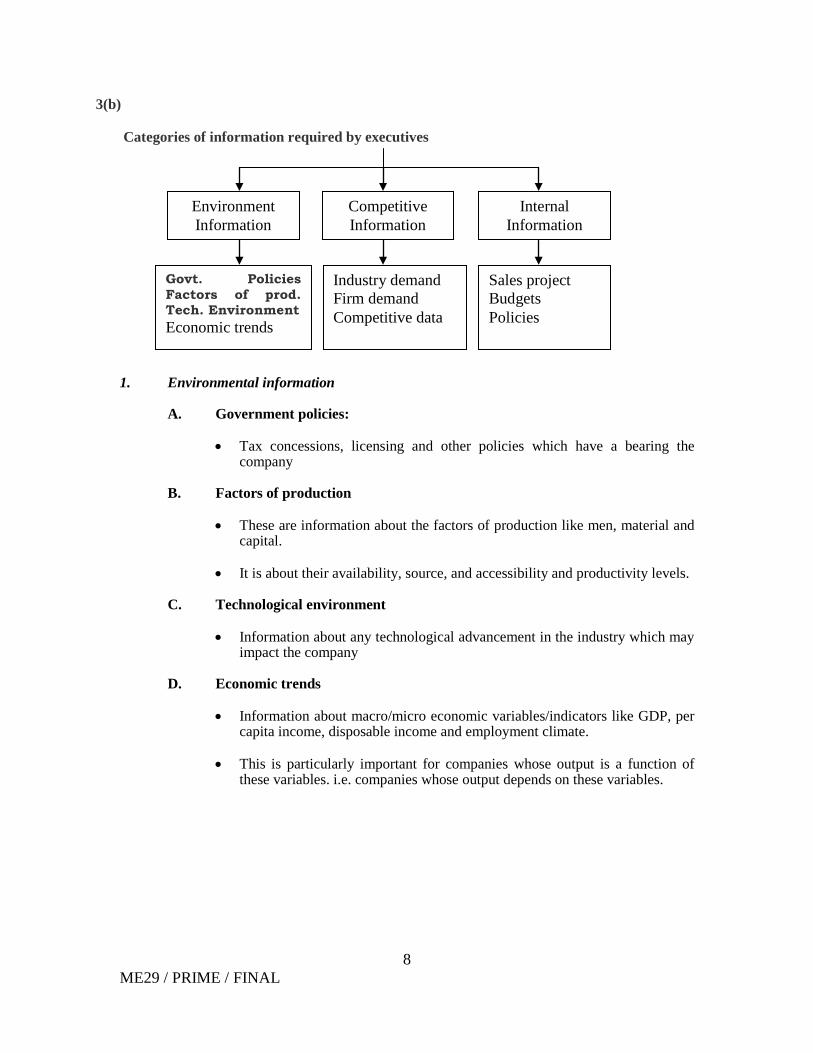

3(b)

Categories of information required by executives

1. Environmental information

A. Government policies:

• Tax concessions, licensing and other policies which have a bearing the company

B. Factors of production

• These are information about the factors of production like men, material and capital.

• It is about their availability, source, and accessibility and productivity levels.

C. Technological environment

• Information about any technological advancement in the industry which may impact the company

D. Economic trends

• Information about macro/micro economic variables/indicators like GDP, per

capita income, disposable income and employment climate.

• This is particularly important for companies whose output is a function of these variables. i.e. companies whose output depends on these variables.

Environment Information

Competitive Information

Internal Information

Govt. Policies Factors of prod. Tech. Environment Economic trends

Industry demand Firm demand Competitive data

Sales project Budgets Policies

9 ME29 / PRIME / FINAL

2. Competitive information

A. Industry demand Demand forecast for the product of the industry in which the company is

operating.

B. Demand of products of the company

• Assessing the demand for the company’s product in the market

• Assessing the capacity of the company to meet such demand

C. Competitive data This is data about competitive firms so as to forecast and plan to achieve the

forecast.

3. Internal information

• These are information generated internally like sales forecast, budgets/plans and organizational policies that are used to organise activities of the company and allocate the same to work groups.

• Internal information is also used to exercise control function over the functional areas

like marketing, finance and manufacturing.

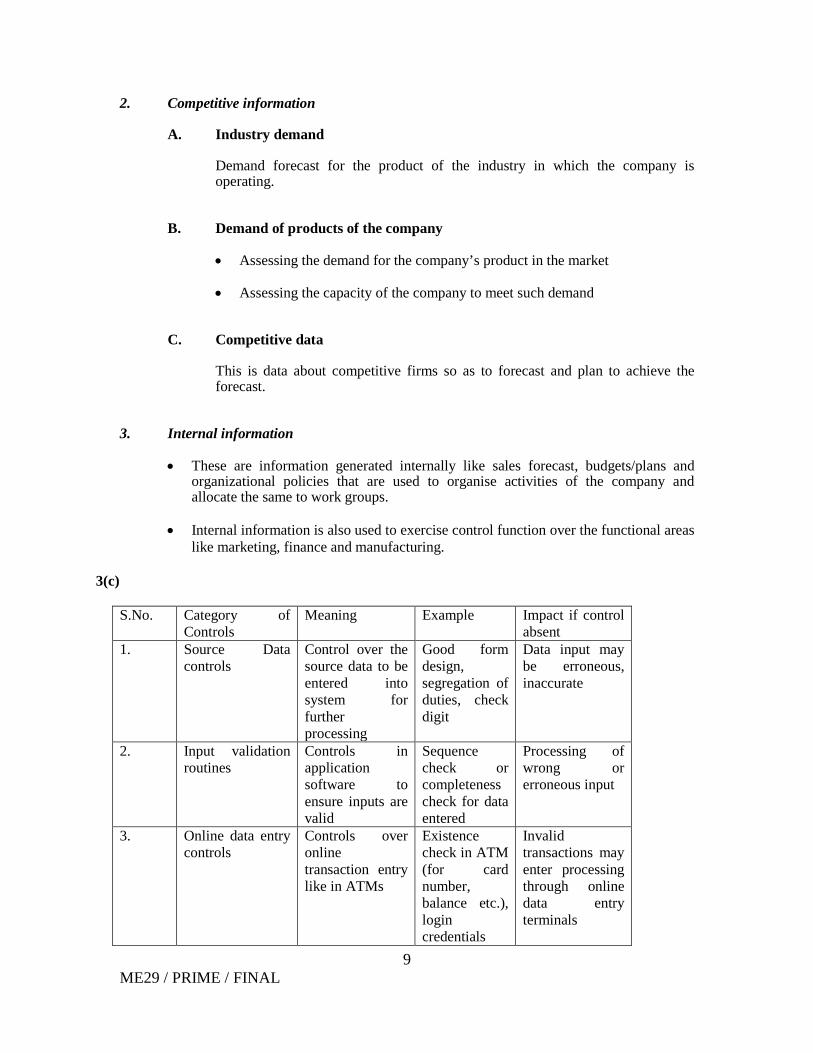

3(c) S.No. Category of

Controls Meaning Example Impact if control

absent 1. Source Data

controls Control over the source data to be entered into system for further processing

Good form design, segregation of duties, check digit

Data input may be erroneous, inaccurate

2. Input validation routines

Controls in application software to ensure inputs are valid

Sequence check or completeness check for data entered

Processing of wrong or erroneous input

3. Online data entry controls

Controls over online transaction entry like in ATMs

Existence check in ATM (for card number, balance etc.), login credentials

Invalid transactions may enter processing through online data entry terminals

10 ME29 / PRIME / FINAL

like user-id and password

4. Data Processing and storage controls

Controls in application software to ensure that data processing happens correctly and processed data is stored securely.

Monitoring of data entry by data control personnel, reconciliation of system updates with control accounts, exception reports

Updates to master files may be inaccurate or incomplete

5. Output controls Controls to ensure that outputs generated are accurate, reach only the authorised personnel and are protected from unauthorised access

Visual review of computer outputs, secure storage and distribution of outputs

Incomplete output or improper distribution of output

6. Data Transmission controls

Controls over data in transit over networks and in removable media

Network monitoring, alternate routing etc.

Unauthorised access to data in transmission or network failures

4(a) As part of IS Audit, we may be required to audit logical access controls at operating system level, application level, database level or network level. The broad methodology of audit would be as follows: Understand how access list has been configured Verify as to how changes are made to the access list and who is authorised to make the

changes (usually done by system/security administrator) Map the users in the access list with the attendance or HR records to verify if all users are

current users Verify the user access creation process- whether the privileges provided to various users

are backed by proper authorisation from respective departments (sample user creation forms)

Verify whether resigned/transferred employees have bee appropriately reflected in the access list

11 ME29 / PRIME / FINAL

4 (b) CoBIT stands for control objectives for Information and related technologies. It is a standard proposed by ITGI- Information Technology Governance Institute. The CoBIT framework works on the logic that there are IT resources which are used by IT processes and which in turn help achieve business objectives. Hence if IT processes are managed well, business objectives would be achieved. CoBITs working definitions: CoBIT has identified 7 distinct categories which are as follows: S.No. Category Meaning 1. Effectiveness Relates to information being relevant and

pertinent to business needs and timely delivery, correctness, consistency and usability

2. Efficiency Information should be generated by using resources in the most optimal manner

3. Confidentiality Protection of sensitive data from unauthorised disclosure

4. Integrity Relates to accuracy, completeness and validity as per business needs

5. Availability Relates to information being available when required by business processes- safeguarding the resources and its associated capabilities

6. Compliance Pertains to complying with laws, regulations an contractual agreements by which the business is bound.

7. Reliability of information Relates to provision of appropriate information to management for them to run the business and take comply with financial and compliance requirements

5(a)

Asymmetric crypto system: According to S.2 (f) of the Information Technology Act, 2000, "asymmetric crypto system" means a system of a secure key pair consisting of a private key for creating a digital signature and a public key to verify the digital signature.

Key pair “Key pair", in an asymmetric crypto system, means a private key and its mathematically related public key, which are so related that the public key can verify a digital signature created by the private key;

12 ME29 / PRIME / FINAL

Digital Signature As per S.2 (p) of the IT Act, 2000 “digital signature" means authentication of any electronic record by a subscriber by means of an electronic method or procedure in accordance with the provisions of section 3.

5(b)

Benefits of ERP

i. Gives accounts payable person increased control over invoicing/payments- hence increase their productivity.

ii. Reduces paper documents- provides on-line formats for entry and retrieval of information

iii. Improves timeliness of information

iv. Greater accuracy, detailed contents, better presentation

v. Improved cost control

vi. Effective monitoring & quicker problem solving

vii. Helps achieve competitive advantage

viii. Provides uniform customer database for all applications

ix. Improves information access and management x. Supports multiple currencies, variety of tax structures etc- hence suitable for

international operations.

6(a) PRE-REQUISITES OF AN EFFECTIVE MIS : The following are the essentials for an effective MIS

1. Database

2. Qualified systems and management staff

3. Top management support

4. Control and maintenance of MIS

5. Evaluation of MIS 1. Database

Meaning : “Super-File” that consolidates data records stored in many data files (Ex : Sales data files, purchase data files, payroll data files combine to form the database)

13 ME29 / PRIME / FINAL

• Data in data base organised in such a manner that

⇒ Access to data improved (querying is easy)

⇒ Redundancy and duplication is decreased

• Data base divided into major information subsets needed to meet business functionality

Ex. Customer file/ vendor file/ inventory file- each sub-system uses same data and information kept in same file.

Characteristics of data base • User oriented

• Available to authorised persons only (i.e. on “need to know” and “need to do basis”)

• Common data source for all users

• Controlled by separate authority, separate software called Data base administrator, Data Administrator and Database management systems

2. Qualified systems and management staff

• MIS should be manned by quality officers who are experts in their fields and understand views of fellow officers

• Comprise of two categories of officers:

Expertise in own field and capable of understanding management concepts to appreciate problems understand process of decision making & info. requirement of planning and control

Management knowledge and concepts & operations of computer- hence can work along side Sys. Experts.

Systems & computer experts Management experts

14 ME29 / PRIME / FINAL

3. Top management support

• MIS to be effective requires full support of top-management

• If top management support is absent then subordinates become lethargic and disinterested

• Top management support is also critical since resources required for MIS implementation is committed by them

How to obtain top management support?

• Officers should present all facts

• Clearly state the benefits of implementing MIS

• Hence change the attitude of management and get full support 4. Control & maintenance of MIS

Control

• Refers to process of ensuring that MIS is operating as it was designed to operate

• Users sometimes create short-cuts to circumvent the system. They may develop own procedures and methods and hence the effectiveness of MIS decreases. Management should build in checks to counter such activities.

Maintenance

• Refers to improvements and fine tuning of the MIS to ensure that it continues meet management needs

• Every change procedure should be properly documented (called as “change management”)

5. Evaluation of MIS

• Evaluating MIS & taking appropriate action to meet future information requirements

• Evaluation should consider :-

Whether system flexible enough to cope with expected and unexpected information requirements of the future

Feedback from users and designers about capabilities and deficiencies of the

system

Support/ appraisal of appropriate authority about steps to be taken to maintain effectiveness of MIS

15 ME29 / PRIME / FINAL

6(b)

• A small set of fictitious records are placed in master file (representing fictitious divisions, departments ,or supplier/customer)

Integrated Test Facility :

• These dummy entries/records processed along with regular records. They don’t affect actual

records and employees unaware of the testing taking place.

At the end of processing, the system collects ITF records and the processing results. The auditor compares with expected results to verify if controls working as desired.

• It involves embedding audit modules to continuously monitor transaction activities which the auditor feels is material/significant.

System Controlled Audit Review File (SCARF):

• The data deemed important by auditor (say payments above 20000 in cash)are recorded in a

SCARF file or audit log • The auditor takes print outs of the SCARF file to examine whether any transactions

require follow-up

6(c) Single Point Failure Analysis Single point of failure can be defined as those IT components for which there is no failover, standby or redundancy and hence if they fail, it would affect availability of that particular resource. For example in a large network assuming there is only one router with no failover or back-up router as standby and assuming this router fails the entire network would come to a halt. Thus the router is considered as a single point of failure. The objective of organisations in terms of security would be analysis such single points of failure and wherever possible build extra capacity so that impact on organisations IT infrastructure is minimized. These are addressed as part of risk mitigation strategies while formulating and implementing a BCP/DR.

7(a) AAS 29

16 ME29 / PRIME / FINAL

AAS 29 has been issued by the ICAI establishes procedures to be followed when audit related to accounting is carried out in a computer information system (CIS) environment- i.e accounting data and processes are system based. The said standard requires the auditor to evaluate the risks of a computerised environment so that his audit objectives can be suitably framed. The other aspects covered in the said standard are:

• Auditor is responsible for gaining sufficient understanding and assurance on the adequacy of accounting and internal controls in a CIS environment

• Design audit procedures based on above analysis after considering the potential impact of controls and audit risk

• The extent to which CIS is used for recording, compiling and analysing accounting information

• The system of internal controls which work towards achieving authorised, complete, accurate and valid processing

• Impact of CIS on audit trail- its completeness and reliability • Requires auditor to have sufficient knowledge of the CIS and possess appropriate skills to

plan, supervise and direct an audit in an CIS environment

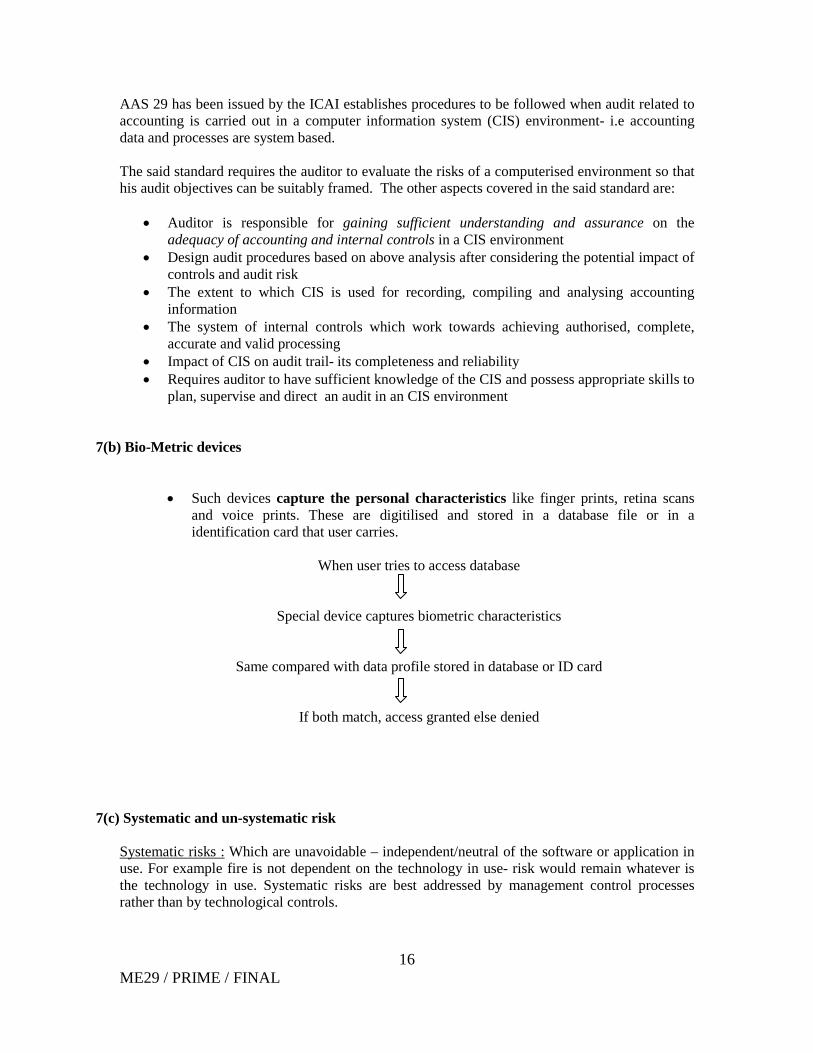

7(b) Bio-Metric devices

• Such devices capture the personal characteristics like finger prints, retina scans and voice prints. These are digitilised and stored in a database file or in a identification card that user carries.

When user tries to access database

Special device captures biometric characteristics

Same compared with data profile stored in database or ID card

If both match, access granted else denied

7(c) Systematic and un-systematic risk

Systematic risks : Which are unavoidable – independent/neutral of the software or application in use. For example fire is not dependent on the technology in use- risk would remain whatever is the technology in use. Systematic risks are best addressed by management control processes rather than by technological controls.

17 ME29 / PRIME / FINAL

Unsystematic risk: Peculiar/specific to a particular technology or software- can be mitigated using better technology or infrastructure. Example: Risk of network performance degradation due to increase in network traffic- can be reduced by better investment in IT Infrastructure- say a high band-width network. The decision that the management needs to take is whether the extra or additional cost involved is warranted- i.e whether it is willing to pay the price to reduce the risk.

7(d) Residuary Risk

Residuary Risk: Refers to that risk which exists even after application of controls. This risk can be managed but not eliminated. Organisations should maintain residuary risk within acceptable limits and accept it. For example even after having an anti-virus software there is a small chance of a virus attack due to say a new strain of virus. This cannot be eliminated and managements have to accept this as residuary risk.

ME29 / Prime / Final

1

TTLS

Number of Pages : 5 Total Marks: 100 Number of questions: 6 Time Allowed: 3 Hrs

Answer all questions All workings should form part of Answers

1. (a) Modern Ltd. is engaged in the manufacture and sale of textiles. Its net profit

for the year ending 31.3.2009 after debit/credit of the following items to the Profit and Loss Account was Rs.75, 00,000:

Payment to two employees of Rs.2, 50,000 each in connection with their

voluntary retirement. Fringe benefit tax paid Rs.1, 00,000. Charges of Rs.2, 00,000 paid for the advertisement in souvenir published

by a Political Party registered with the Election Commission of India. Retrenchment compensation paid to employees of one of the units closed

down during the year Rs.10, 00,000. Capital expenditure incurred for the purpose of promoting family planning

amongst its employees Rs.3, 00,000. Banking cash transaction tax paid Rs.10, 000. Interest paid under section 234B for short payment of advance tax

pertaining to the assessment year 2008-09 Rs.1, 10,000. Loss incurred in transactions of purchase and sale of shares of various

companies Rs.3, 00,000. Compensation received from supplier for delay in supply of raw materials

Rs.1, 00,000. Dividend received from a foreign company Rs.2, 00,000. The total sales of Modern Ltd. for the year was Rs.30 crores out of which

export sales amounted to Rs.10 crores.

Compute the total income of Modern Ltd. for the assessment year 2009-10.

Furnish explanations for the treatment of the various items given above. (12 Marks)

(b) Ranjan Ltd., made a provision on 31.3.05 of Rs.85,500 against a bill of

supplier of raw material by charging the amount to profit and loss account and claimed deduction thereof while computing the income chargeable to tax for A.Y. 2005-06. The amount of Rs.40, 000 not paid to the party till 31.3.09 was paid in cash on 11.6.09. The Assessing Officer issued show cause notice to the company to rectify the computation of income for the A.Y. 2005-06 on account of payment made in cash on 11.6.09.Can Assessing Officer do so?

(4 Marks)

ME29 / Prime / Final

2

(c) A co-operative society engaged in the business of banking seeks your opinion in the matter of eligibility of deduction u/s 80P on the following items of income earned by it during the year ending 31.3.2009:

(i) Interest on investment in Government securities made out of statutory

reserves (ii) Hire charges of safe deposit lockers

(4 Marks)

2. (a) Discuss the correctness or otherwise of the following statements

(i) Income deemed to accrue or arise in India to a non-resident by way of interest, royalty and fees for technical services is to be taxed irrespective of territorial nexus.

(ii) The power of the Settlement Commission to grant immunity from prosecution has now been restricted.

(iii) Section 2(14) of the Act excludes all items of movable property which are held for personal use of the assessee or any member of his family.

(iv) The Appellate Tribunal is empowered to grant indefinite stay for the demand disputed in appeals before it.

(4 X 3 = 12 Marks) (b) Mr.Nathan, a non-resident, operates an aircraft between Singapore and

Chennai. He received the following amounts in the course of the business of operation of aircraft during the year ending 31.3.2009:

(i) Rs.2 crores in India on account of carriage of passengers from Chennai. (ii) Rs.1 crore in India on account of carriage of goods from Chennai. (iii) Rs.3 crores in India on account of carriage of passengers from Singapore. (v) Rs.1 crore in Singapore on account of carriage of passengers from

Chennai.

The total expenditure incurred by Mr.Nathan for the purposes of the business during the year ending 31.3.2009 was Rs.6.75 crores.Compute the income of Mr.Nathan chargeable to tax in India under the head “Profits and gains of business or profession” for the assessment year 2009-10

(4 Marks)

3. (a) Explain the method for determining the amount of expenditure in relation to income not includible in total income

(5 Marks) (b) Asaan Cellular Ltd., to provide telecom services in Mumbai, obtained a

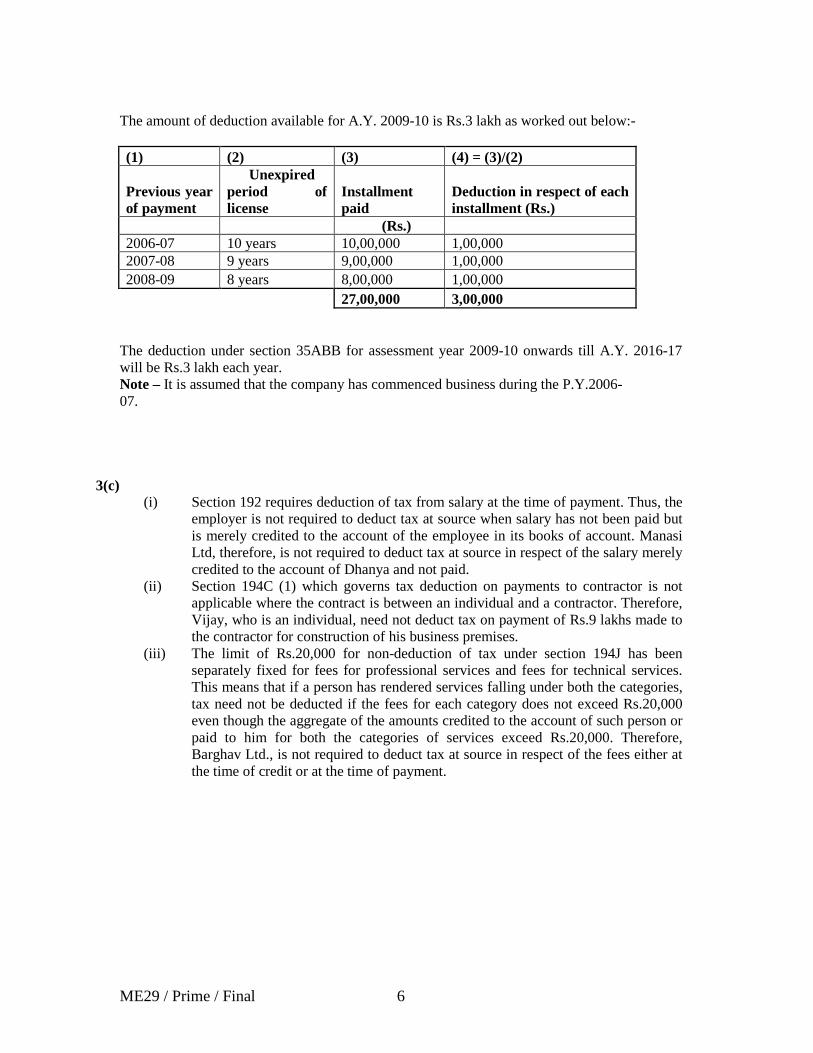

licence on 11.4.2006 for a period of 10 years ending on 31.3.2016 against a fee of Rs.27 lacs to be paid in 3 installments of Rs.10 lacs, 9 lacs and 8 lacs by April, 2006, April, 2007 and April, 2008 respectively. Explain how the payment made for licence fee shall be dealt with under the Income-tax Act, 1961 and work out the amount, if any, deductible in this respect out of income chargeable to tax for Assessment.Year. 2009-10 and subsequent years.

(5 Marks)

ME29 / Prime / Final

3

(c) Examine the obligation of the person responsible for paying the income to deduct tax at source and indicate the due date for payment of such tax, wherever applicable, in respect of the following items

(i) Manasi Ltd., the employer, credited salary due for the financial year 2008-09 amounting to Rs.2,40,000 to the account of Dhanya, an employee, in its books of account on 31.3.2009. Q has not furnished any information about his income/loss from any other head or proof of investments/payments qualifying for deduction under section 80C.

(ii) Vijay, an individual whose total sales in business during the year ending

31.3.2009 was Rs.1.20 crores, paid Rs.9 lakhs by cheque on 1.1.2009 to a contractor, for construction of his business premises, in full and final settlement. No amount was credited earlier to the account of the contractor in the books of Vijay.

(iii) Bhargav Ltd. credited Rs.18,000 towards fees for professional services and

Rs.12,000 towards fees for technical services to the account of Harini in its books of account on 06.10.2008. The total sum of Rs.30,000 was paid by cheque to Harini on 18.12.2008

(3 X 2 = 6 Marks)

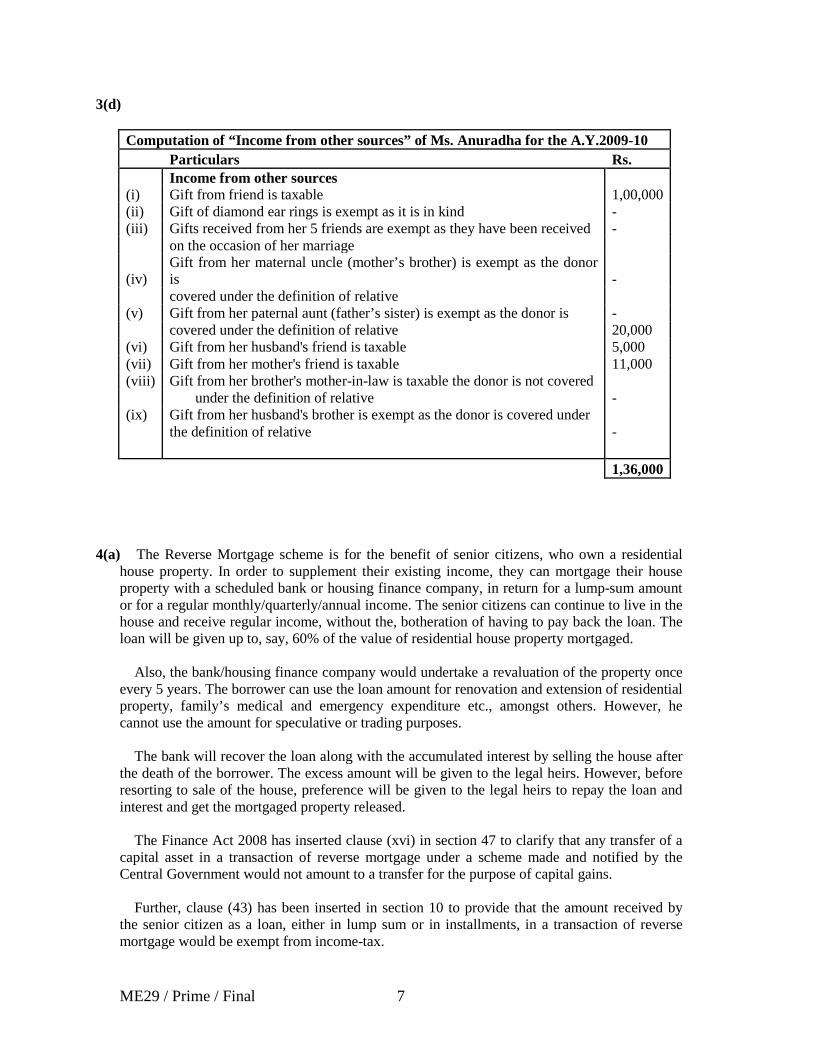

(d) Anuradha received the following gifts during the previous year 2008-09

(i) Gift of Rs.1, 00,000 on 14-4-2008 from her friend, Sneha. (ii) Gift of diamond ear rings worth Rs.2,10,000 on 15-5-2008 from her friend,

Geetha.135 (iii) Gifts of Rs.25, 000 each received from her 5 friends on the occasion of her

marriage on 5-6-2008. (iv) Gift of Rs.40, 000 on 24-7-2008 from her maternal uncle. (v) Gift of Rs.60, 000 on 26-8-2008 from her paternal aunt. (vi) Gift of Rs.20, 000 from her husband's friend on 1-9-2008. (vii) Gift of Rs.5, 000 on 2-10-2008 from her mother's friend. (viii) Gift of Rs.11, 000 on 5-11-2008 from her brother's mother-in-law. (ix) Gift of Rs.25, 000 from her husband's brother.

Compute her income chargeable to tax under the head “Income from other sources” for the Assessment Year 2009-10.

(6 Marks) 4. (a) What is meant by “Reverse Mortgage”? Discuss the tax implications of a

transaction of reverse mortgage. (4 Marks)

(b) Specify all those instances which are generally incorporated in Article 5(2) in

all DTA agreements to signify the presence of a permanent establishment (4 Marks)

ME29 / Prime / Final

4

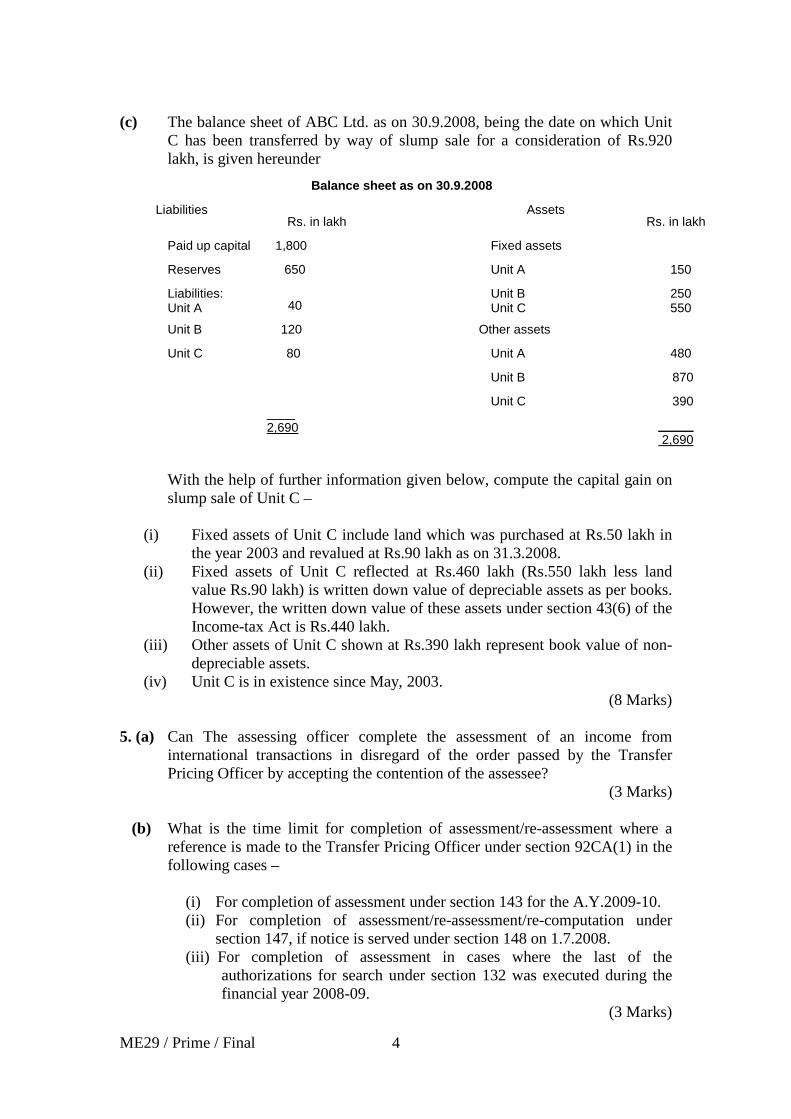

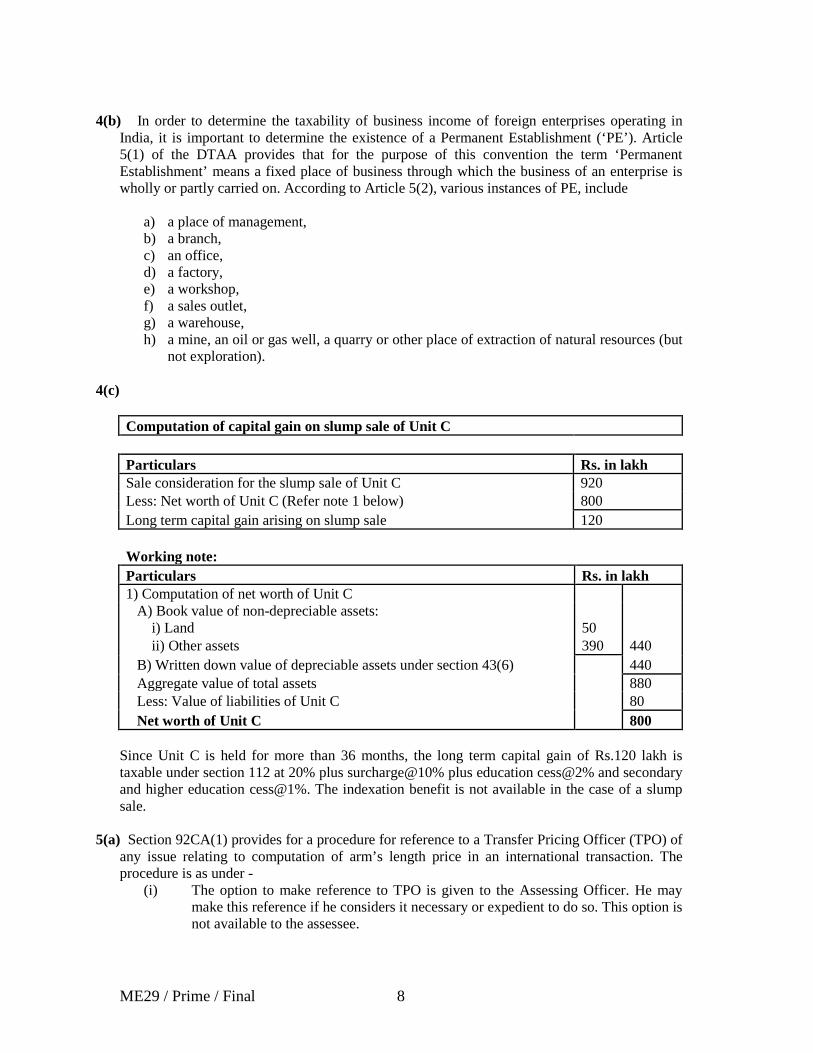

(c) The balance sheet of ABC Ltd. as on 30.9.2008, being the date on which Unit

C has been transferred by way of slump sale for a consideration of Rs.920 lakh, is given hereunder

With the help of further information given below, compute the capital gain on slump sale of Unit C –

(i) Fixed assets of Unit C include land which was purchased at Rs.50 lakh in the year 2003 and revalued at Rs.90 lakh as on 31.3.2008.

(ii) Fixed assets of Unit C reflected at Rs.460 lakh (Rs.550 lakh less land value Rs.90 lakh) is written down value of depreciable assets as per books. However, the written down value of these assets under section 43(6) of the Income-tax Act is Rs.440 lakh.

(iii) Other assets of Unit C shown at Rs.390 lakh represent book value of non-depreciable assets.

(iv) Unit C is in existence since May, 2003. (8 Marks)

5. (a) Can The assessing officer complete the assessment of an income from

international transactions in disregard of the order passed by the Transfer Pricing Officer by accepting the contention of the assessee?

(3 Marks) (b) What is the time limit for completion of assessment/re-assessment where a

reference is made to the Transfer Pricing Officer under section 92CA(1) in the following cases –

(i) For completion of assessment under section 143 for the A.Y.2009-10. (ii) For completion of assessment/re-assessment/re-computation under

section 147, if notice is served under section 148 on 1.7.2008. (iii) For completion of assessment in cases where the last of the

authorizations for search under section 132 was executed during the financial year 2008-09.

(3 Marks)

Balance sheet as on 30.9.2008 Liabilities Assets

Rs. in lakh Rs. in lakh Paid up capital 1,800 Fixed assets Reserves 650 Unit A 150 Liabilities: Unit A 40

Unit B Unit C

250 550

Unit B 120 Other assets Unit C 80 Unit A 480

Unit B 870 Unit C 390

_____ ____

2,690 2,690

ME29 / Prime / Final

5

(c) Write short notes on any two of the following

(i) Section 92A of the Income Tax Act (ii) Section 115JAA of the Income Tax Act (iii) Section 281B of the Income Tax Act (2 X 5 = 10 Marks)

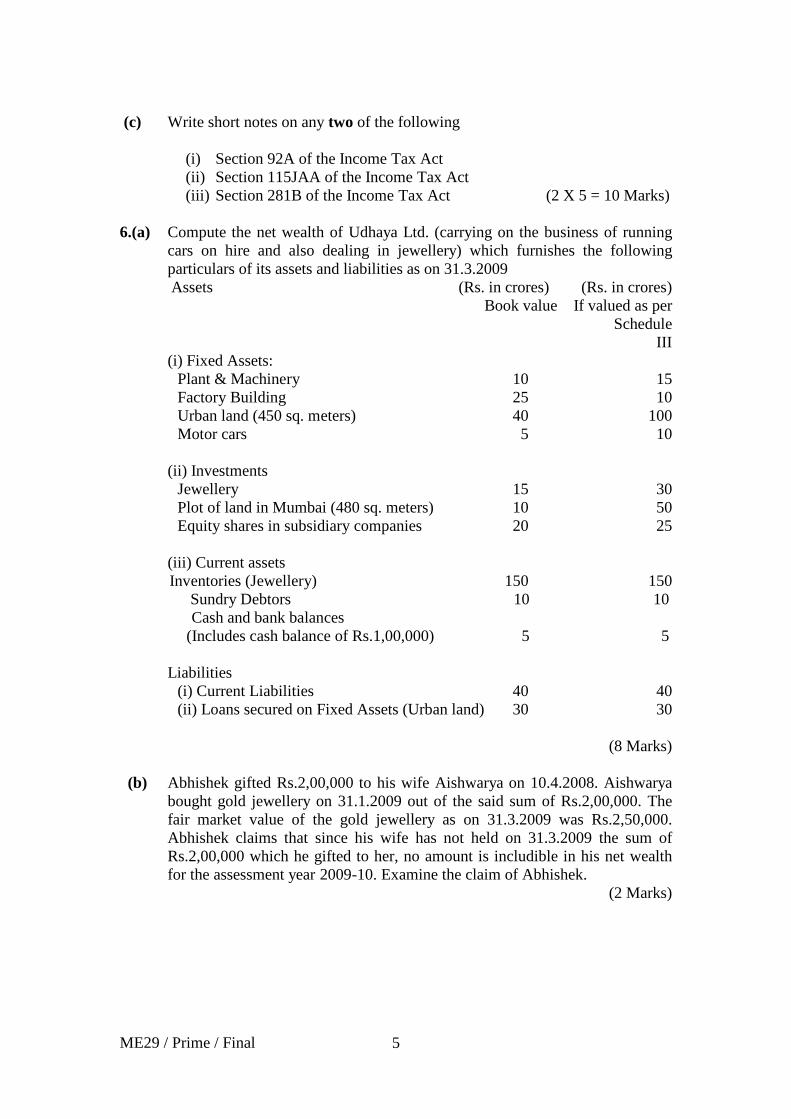

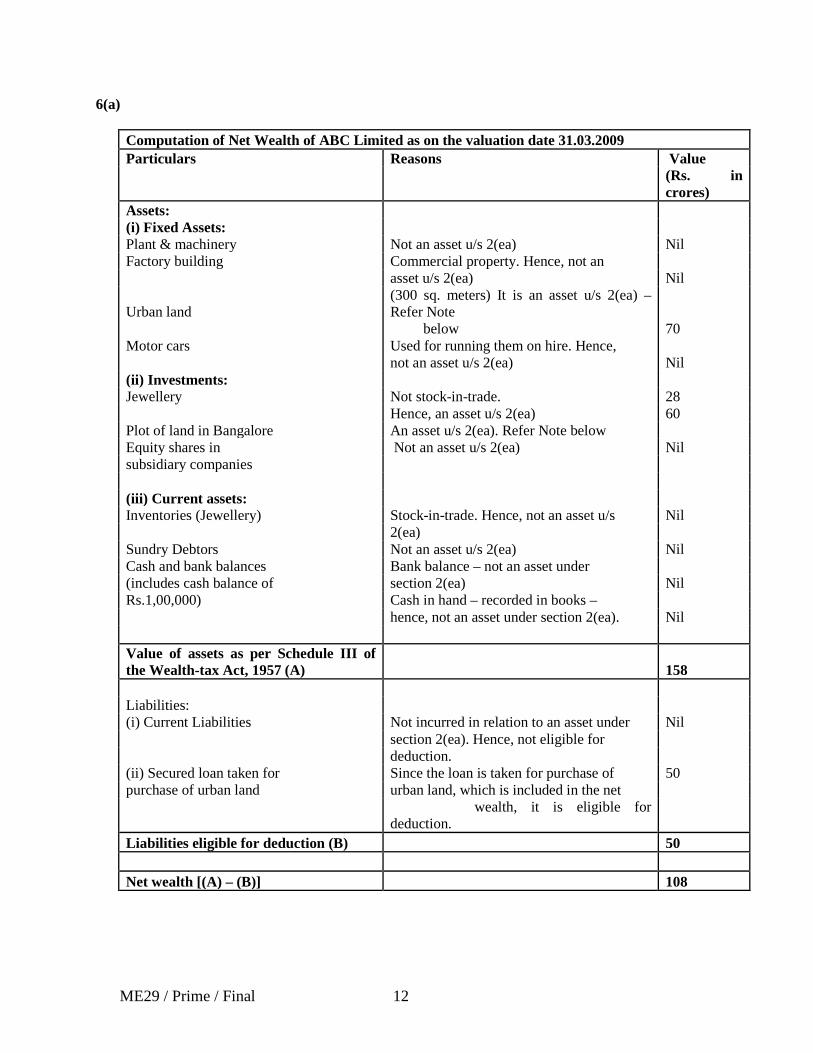

6.(a) Compute the net wealth of Udhaya Ltd. (carrying on the business of running

cars on hire and also dealing in jewellery) which furnishes the following particulars of its assets and liabilities as on 31.3.2009 Assets (Rs. in crores) (Rs. in crores)

Book value If valued as per Schedule

III (i) Fixed Assets:

Plant & Machinery 10 15 Factory Building 25 10

Urban land (450 sq. meters) 40 100 Motor cars 5 10

(ii) Investments

Jewellery 15 30 Plot of land in Mumbai (480 sq. meters) 10 50 Equity shares in subsidiary companies 20 25

(iii) Current assets Inventories (Jewellery) 150 150 Sundry Debtors 10 10 Cash and bank balances (Includes cash balance of Rs.1,00,000) 5 5

Liabilities

(i) Current Liabilities 40 40 (ii) Loans secured on Fixed Assets (Urban land) 30 30

(8 Marks)

(b) Abhishek gifted Rs.2,00,000 to his wife Aishwarya on 10.4.2008. Aishwarya

bought gold jewellery on 31.1.2009 out of the said sum of Rs.2,00,000. The fair market value of the gold jewellery as on 31.3.2009 was Rs.2,50,000. Abhishek claims that since his wife has not held on 31.3.2009 the sum of Rs.2,00,000 which he gifted to her, no amount is includible in his net wealth for the assessment year 2009-10. Examine the claim of Abhishek.

(2 Marks)

ME29 / Prime / Final 1

PRIME ACADEMY 29TH

Computation of total income of Modern Ltd. for the Assessment Year 2009-10

SESSION –MODEL EXAM DIRECT TAXES – NEW SYLLABUS

SUGGESTED ANSWERS

1(a)

Particulars Rs. Net profit as per Profit and Loss Account 75,00,000 Add: Inadmissible expenditure 4/5th of Rs.5,00,000 paid to employees on voluntary retirement [1/5th is 4,00,000 allowable as deduction u/s 35DDA] Fringe benefit tax u/s 40(a)(ic) 1,00,000 Advertisement charges of souvenir of political party u/s 37(2B) 2,00,000 4/5th of Rs.3,00,000, being capital expenditure incurred for promoting 2,40,000 family planning amongst employees [1/5th is allowable as deduction u/s 36(1)(ix)] Interest paid u/s 234B 1,10,000 Loss incurred in transactions of purchase and sale of shares considered 3,00,000 as speculation loss 88,50,000 Less: Dividend received from a foreign company considered under ‘Income from other sources’ 2,00,000 Business income 86,50,000 Income from other sources Dividend received from a foreign company 2,00,000 Gross total income 88,50,000 Less: Deduction u/s 80GGB 2,00,000 Total income 86,50,000

Explanations for the treatment of the various items in computing the total income of the company are furnished below -

(i) Section 35DDA provides for amortization of expenditure incurred under voluntary retirement scheme over a period of five years in equal installments. The company is, therefore, entitled to deduction of Rs.1,00,000, being one-fifth of the total sum of Rs.5,00,000 paid to the two employees in connection with their voluntary retirement for the relevant assessment year.

(ii) Fringe benefit tax paid is not allowable as deduction from business profits as per section 40(a)(i). Hence, fringe benefit tax paid by the company is not deductible.

(iii) Section 37(2B) prohibits allowance of any expenditure incurred by an assessee on

advertisement in any souvenir, brochure, pamphlet or the like published by a

ME29 / Prime / Final 2

political party. As such, advertisement charges paid in respect of souvenir published by a political party is not allowable as deduction from business profits of the company. However, under section 80GGB, expenditure incurred by an Indian company on advertisement in any publication, including a souvenir, by a political party is deemed to be a contribution of such amount to the political party and is, therefore, allowable as deduction in the hands of the company. It is logical to presume that Modern Ltd. is an Indian company.

(iv) Retrenchment compensation paid to employees at the time of closure of one of the units of the business is allowable as per the decision of the Allahabad High Court in CIT (Central) Kanpur vs. JK Cotton Spinning & Weaving Co. Ltd. (2005) 145 Taxman 591.

(v) Capital expenditure incurred for the purpose of promoting family planning amongst employees is deductible over a period of 5 years as per the first proviso to section 36(1)(ix). Hence, only Rs.60,000 is deductible in the current year in respect of such expenditure incurred by the company.

(vi) Banking cash transaction tax paid by the company is eligible for deduction in view of section 36(1)(xiii).

(vii) Interest paid for delayed payment of tax by the assessee is part and parcel of the liability to pay income-tax. When income-tax paid is itself not allowable as a deduction under section 40(a)(ii), the interest paid under section 234B cannot qualify for deduction. Thus, interest paid under section 234B is not deductible.

(viii) Loss of Rs.3 lakhs incurred by the company in dealing of shares constitutes speculation loss in view of the Explanation to section 73. In the absence of any speculative profit for the year, speculation loss is to be carried forward under section 73(2) for set off against speculation profits of subsequent assessment years. It can be carried forward for a maximum of 4 assessment years

(ix) Compensation received from supplier for delay in supplying the raw materials is a trading receipt.

(x) Dividend received from a foreign company in assessable under the head “Income from other sources”.

(xi) Deduction under section 80HHC in respect of profits from export business is not allowable for and from the assessment year 2005-06.

1(b) The proviso to section 40A(3) provides that where an allowance has been made in the

assessment for any year in respect of any liability for any expenditure incurred by the assessee and subsequently, during any previous year, the assessee makes any payment in respect of such liability in a sum exceeding Rs.20,000 otherwise than by an account payee cheque drawn on a bank or by an account payee bank draft, the allowance originally made shall be deemed to have been wrongly made and the Assessing Officer may re-compute the total income of the asssessee for the previous year in which such liability was incurred by making necessary amendment. The proviso to section 40A(3) is attracted in this case since the company has made a cash payment of Rs.40,000 in respect of a liability incurred and allowed in A.Y.2005-06. Accordingly, Rs.8000/-, being 20% of Rs.40,000, will be added in the computation of income for the A.Y.2005-06. The action of the Assessing Officer to issue show cause notice to rectify the computation of income for the A.Y.2005-06 is, therefore, correct.

ME29 / Prime / Final 3

1(c)

(i) Interest earned on investment in Government securities made out of statutory

reserves by a co-operative society engaged in banking business is eligible for deduction under section 80P as per the decision of the Supreme Court in CIT v. Karnataka State Co-operative Apex Bank (2001) 251 ITR 194. In this case, it was held that the placement of such funds being imperative for the purpose of carrying on banking business, the income therefrom would be income from the assessee’s business and there is nothing in section 80P which restricts the exemption to only income derived from working or circulating capital.

(ii) Provision of safe deposit lockers is part of the ordinary banking business. Income

from hiring of such lockers is income from banking business and, therefore, eligible for deduction under section 80P. Therefore, the society is entitled to deduction under section 80P in respect of hire charges of safe deposit lockers.

2(a)

(i) This statement is correct.The Supreme Court, in Ishikawajima-Harima Heavy Industries Ltd. v. Director of Income tax (2007) 288 ITR 408, observed that in order to tax the income of a non-resident assessee under section 9(1)(vii), relating to fee for technical services, the income sought to be taxed must have sufficient territorial nexus with India i.e. the fees paid for technical services provided by a non-resident cannot be taxed in India unless the services were utilized in India and rendered in India. However, the Finance Act, 2007 has now inserted an Explanation to section 9 with retrospective effect from 1.6.1976 to clarify that such income by way of interest, royalty or fee for technical services which is deemed to accrue or arise in India by virtue of clauses (v), (vi) and (vii) of section 9(1), shall be included in the total income of the non-resident, whether or not the non-resident has a residence or place of business or business connection in India.

(ii) This statement is correct. Under section 245H, the Settlement Commission may grant immunity from prosecution for any offence under the Indian Penal Code, Income-tax Act and any other Central Act. This power has now been restricted in respect of application made under section 245C on or after 1.6.2007. In respect of such cases, the Settlement Commission shall not grant immunity from prosecution for any offence under the Indian Penal Code or under any Central Act other than the Income-tax Act and Wealth-tax Act. However, in respect of applications pending as on 1.6.2007, the Settlement Commission has the power to grant immunity from prosecution for any offence under the Indian Penal Code and other Central Acts also.

(iii) Sub-clause (ii) of section 2(14) provides that all movable property including wearing apparel and furniture held for the personal use by the assessee or any member of his family dependent on him are not capital assets as per section 2(14). However, the following movable property held for the personal use by the assessee or any member of his family dependent on him are capital assets –

(a) jewellery (b) archaeological collections (c) drawings (d) paintings

ME29 / Prime / Final 4

(e) sculptures, or (f) any work of art