Embed Size (px)

Citation preview

ADB Grant 0133-CAM: Public Financial Management in Rural Development

Ministries (Component 1)

Day 3: April 29, 2010Cash Management and Treasury Function

Budget Execution, Budget Execution, April 26 - 30, 2010April 26 - 30, 2010Budget Execution, Budget Execution, April 26 - 30, 2010April 26 - 30, 2010

ADB Grant No.0133-CAM/Component 1: PFMRD

Content

2

Session 3Cash Management and Treasury Function

1.Treasury function2.Cash management

- Petty cash advance- Advance payment- Direct payment

3.Management government bank account4.Financial plan forecasting

ADB Grant No.0133-CAM/Component 1: PFMRD 3

1. Treasury Function• Spending agencies must be provided with the funds

needed to implement the budget in a timely manner, and the cost of government borrowing must be minimized.

• Financial operations; accounting; and auditing and evaluation the Treasury function is to achieve the set of specific objectives mentioned above. It covers the following activities:– Cash management;– Management of government bank accounts;– Financial planning and forecasting of cash flows;– Public debt management;– Administration of foreign grants and counterpart funds from international aid;– Financial assets management.

ADB Grant No.0133-CAM/Component 1: PFMRD 4

1. Treasury Function (continued)

• Treasury Department focuses only on cash and debt management functions

• In a few countries, debt management is performed by an autonomous agency.

• In other countries, the Treasury Department performs budget execution controls execution reporting activities.

ADB Grant No.0133-CAM/Component 1: PFMRD 5

• In other countries, payments are processed by line ministries, but cash and bank accounts are controlled by the Treasury Department which is responsible for cash management.

• Therefore, issues related to whether accounting controls should be centralized or not. e.g. below should be distinguished from issues related to cash management:

1. Treasury Function (continued)

ADB Grant No.0133-CAM/Component 1: PFMRD 6

Limits of accounting controls– Many budget systems focus on accounting control to

ensure compliance This approach is insufficient. Accounting controls can prevent blatant cases of misuse of appropriations. However, whatever their organization, accounting controls do not prevent the accumulation of arrears since obligations are made upstream.

– They do not prevent the commitment of expenditures that are not authorized in the budget.

1. Treasury Function (continued)

ADB Grant No.0133-CAM/Component 1: PFMRD 7

Centralized external controls• Central payment systems ensure that accounting is done by a staff

of qualified accountants, and allow the central agencies to see to it that payments are appropriately documented and that every expenditure fits the purpose stated in the budget.

• In several countries, spending units maintain accounts with commercial banks and deal directly with their banks when making payments This has the advantage of avoiding delays in payment processing that are caused by ex-ante external controls in some countries.

• Spending units and the Ministry of Finance cannot monitor payment transactions, and idle balances are kept in the bank accounts of line ministries. External controls between the spending units and the commercial bank or centralized payment system would be a good way solving this problem.

1. Treasury Function (continued)

ADB Grant No.0133-CAM/Component 1: PFMRD 8

Note:• the treasury system suggest that treasuries would not

only scrutinize payments, but would also be responsible for compiling accounts. But such a step could widen the chasm between expenditure responsibility and the power of payment.

• Moreover, treasuries are no less resistant to political pressures than are the commercial banks.

• In countries that have poor governance and face arrears accumulation, centralized payment systems increase distortions in budget execution a central office have a wider range of opportunities to bargain invoice payments than the officers of line ministries or spending units. Supplier prioritization is therefore substituted for program prioritization.

1. Treasury Function (continued)

ADB Grant No.0133-CAM/Component 1: PFMRD 9

In Cambodia-Treasury function• Treasury is composed of all available credits held by

public accountants in the form of Cash on Hand and Deposits in one Current Account opened at NBC (Article 74 of sub-decree 82);

• Public institutions deposit their funds at the Treasury, unless waivers have been granted by the Minister of Finance (article 71, sub-decree 82);

• NBC shall be the sole depositary of the funds held by the Treasury’s direct accountants (article 78, sub-decree 82);

• State public accountants only are authorized to handle Treasury funds (article 72, sub-decree 82)

1. Treasury Function (continued)

ADB Grant No.0133-CAM/Component 1: PFMRD 10

In Cambodia-Treasury function (continued)

• Authorising officer and other state officers who do not have the capacity of public accountant cannot open an account in the banks or in public or private credit institions;

• Heads of PIUs which are financed by foreign aid may open an account to meet the needs of the projects under the terms set by the agreements signed with donors. The opening of these accounts by projects shall be subject to prior authorization of the Minister of Finance (article 73 and 77, sub-decree 82).

1. Treasury Function (continued)

ADB Grant No.0133-CAM/Component 1: PFMRD 11

In Cambodia-Treasury function (continued) • All flows of cash Cashable shares, deposit accounts,

current accounts and transactions concerning short-term receipt and debt payable account (article 68, sub-decree 82);

• Describe by nature for their entire amount and without any offsetting between them (article 69, sub-decree 82);

• Expenditures and revenues resulting from treasury operations are to be charged to budget account (article 69, sub-decree 82);

• Except for cash flows required by cash payments made to or releases made by accounting officers (article 80, sub-decree 82).

1. Treasury Function (continued)

ADB Grant No.0133-CAM/Component 1: PFMRD 12

In Cambodia-Treasury function (continued)

• Bodies and individuals who either pursuant to laws and regulations or in accordance with agreements, deposit treasury funds on a mandatory or optional basis or are authorized to carry out revenue or expenditure operations through treasury accountants;

• A authorization has been granted by the Minister of Finance, only one account per counterpart can be opened at the treasury (article 81, sub-decree 82);

• Treasury accountants maybe authorized by Minister of Finance to set up a special fund deposit service (article 83, sub-decree 82);

• Accounts opened at the treasury on behalf of counterparts shall not show any overdraft (article 84, sub-decree 82).

1. Treasury Function (continued)

ADB Grant No.0133-CAM/Component 1: PFMRD 13

2. Cash Management

- General (purpose and cash flows)- Petty cash advance- Advance payment- Direct payment

ADB Grant No.0133-CAM/Component 1: PFMRD 14

2. Cash ManagementPurpose:Controlling spending in the aggregate, implementing the budget

efficiently, minimizing of the cost of government borrowing, and maximizing the opportunity cost of resources. Control of cash is a key element in macroeconomic and budget

management. For efficient budget implementation, it is necessary to ensure

that claims will be paid according to the contract terms and that revenues are collected on time.

It is necessary to minimize transaction costs; and to borrow at the lowest interest rate or to generate additional cash by investing in revenue-yielding paper.

It is also necessary to avoid paying in advance and to track accurately the dates on which payments are due.

ADB Grant No.0133-CAM/Component 1: PFMRD 15

2. Cash ManagementNote: In developing countries• Governments often do not pay attention to issues related to cash

management. • Budget execution procedures and the management of cash flows

focus on compliance issues, while daily cash needs in are met at low cost by the Central Bank.

• Spending units are not concerned with borrowing costs.• Some countries have implemented reforms to make spending

agencies more responsible for cash, while maintaining instruments to ensure fiscal discipline. e.g. Philippines (see Box 26: Cash Management in Philippines, Chapter 8, ADB’s Managing Government Expenditure).

ADB Grant No.0133-CAM/Component 1: PFMRD 16

2. Cash ManagementCash Flows

i. Cash inflowsii. Cash outflowsiii.Payment methods

ADB Grant No.0133-CAM/Component 1: PFMRD 17

2. Cash ManagementCash Flows

i.i. Cash inflowsCash inflows

• Necessary to minimize the interval between the time when cash is received and the time it is available for carrying out expenditure programs.

• Collected revenues need to be processed promptly and made available for use.

• An appropriate system of penalties for taxpayers is also an important element in avoiding delays in revenue collection.

ADB Grant No.0133-CAM/Component 1: PFMRD 18

2. Cash Managementii.ii.Cash outflowsCash outflows

• Directly related to organizational arrangements for budget execution, can pose more difficulties than the control of cash inflows.

• It should not be confused with issues related to the distribution of responsibilities for accounting control and administration of the payment system.

• To ensure that there will be enough cash until the date payments are due and to minimize the costs of transactions, while keeping cash outflows compatible with cash inflows and fiscal constraints.

• The first condition for ensuring that cash outflows fit fiscal constraints is good budget preparation and budget implementation covering both cash and obligations.

• However, during budget implementation, cash outflows must also be regulated through cash plans to smooth cash outflows.

ADB Grant No.0133-CAM/Component 1: PFMRD 19

2. Cash Management

Payment methodPayment method• Affect the transaction costs of cash outflows. • Depending on the banking infrastructure and the nature of

expenditures, various payment methods may be considered (check, cash, electronic transfer, debit card, etc.).

• Modern methods of payment, for example, payment through electronic transfers instead of through checks or cash, allow the government to plan its cash flow more accurately, expedite payments, and simplify administrative and accounting procedures.

• However, whether one mode of payment is preferable to another depends on many factors, such as the degree of economic development of the country, the banking network, the status of computerization.

ADB Grant No.0133-CAM/Component 1: PFMRD 20

2. Cash Management

Payment methodPayment method (continued)(continued)• For payments within government (when an agency

provides services to another agency), a number of countries use non-payable checks, while others make book adjustments. Using non-payable checks has the advantage of avoiding delays in the preparation of accounts.

• In some aid-dependent countries non-payable checks are used to pay taxes related to imports financed with external aid, to avoid loopholes in the tax system created by duty-free imports.

ADB Grant No.0133-CAM/Component 1: PFMRD 21

2. Cash ManagementPetty Cash AdvanceNon program budget Urgent expenditures and minor item.

Equal /or Less than 1 Million Riel per payment sleep Revolving funds for at least 8 or 4 times per year - Initial

advance for 1:8 or 1:4 of 30% of total appropriate budget items, e.g. MAFF 2010: initial advance for 130 Million Riel; according to petty cash expenditure plan submit to MEF at the beginning of the fiscal year, (MEF Prakas 004, 25-Dec-09, page 14 of 18).

• Request for expenditure Prakas inter-ministerial to nominate custodian. Develop in detail of petty cash advance Petty cash liquidation by custodian, attached receipts voucher

and mandated.

ADB Grant No.0133-CAM/Component 1: PFMRD 22

2. Cash ManagementPetty Cash Advance (continued)• Request for expenditure

Custodian must be liquidated within 1 month, from the disbursement dated at Treasury.

Closing cash disbursement from Treasury on 10th of December, and deadline liquidation at Treasury on 29th December.

Process of Petty Cash Advance/Expenditure

National Treasury

Expenditure Units

Line Ministries’ Management

National Treasury

MEF’s Management

Financial Controller

Payment Processing

e.g. MAFF 2010:

130 Million Riel

ADB Grant No.0133-CAM/Component 1: PFMRD 24

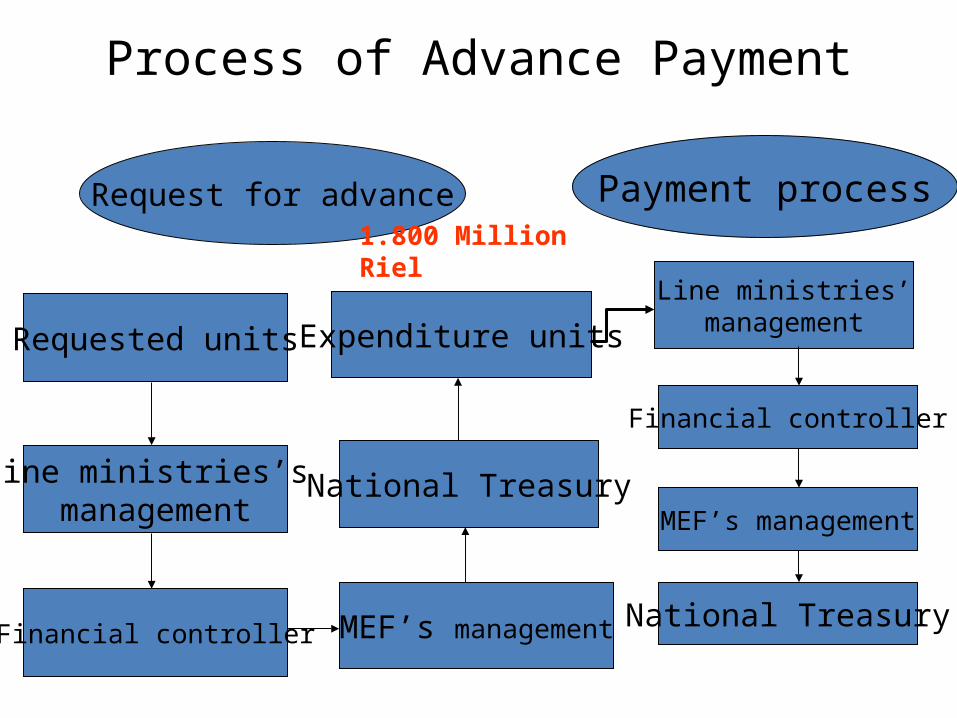

2. Cash ManagementAdvance PaymentProgram budget Urgent expenditures and larger item which

could not use petty cash fund. Revolving funds for at least 4 times per year - Initial advance

for 1:4 of total appropriate budget items, e.g. MAFF 2010: initial advance for 1.800 Million Riel; according to expenditure plan submit to MEF at the beginning of the fiscal year, (MEF Prakas 004, 25-Dec-09, page 14 of 18).

• Request for expenditure Line ministries request for advance. Expenditures plan Voucher and other relevant to expenditure Commitment letter

ADB Grant No.0133-CAM/Component 1: PFMRD 25

2. Cash ManagementAdvance Payment (continued)• Payment procedure

Request for payment Account statement and other receipt of actual

expenditure occurred Voucher and mandated Closing cash disbursement from Treasury on 19th of

November, and deadline liquidation at Treasury on 29th December.

In case of advance payment delay within the year, the balance shall be carried over for next year budget.

Process of Advance Payment

Requested units

Line ministries’s management

Financial controller

Request for advance Payment process

Expenditure units

Line ministries’management

Financial controller

MEF’s management

National Treasury

National Treasury

MEF’s management

1.800 Million Riel

ADB Grant No.0133-CAM/Component 1: PFMRD 27

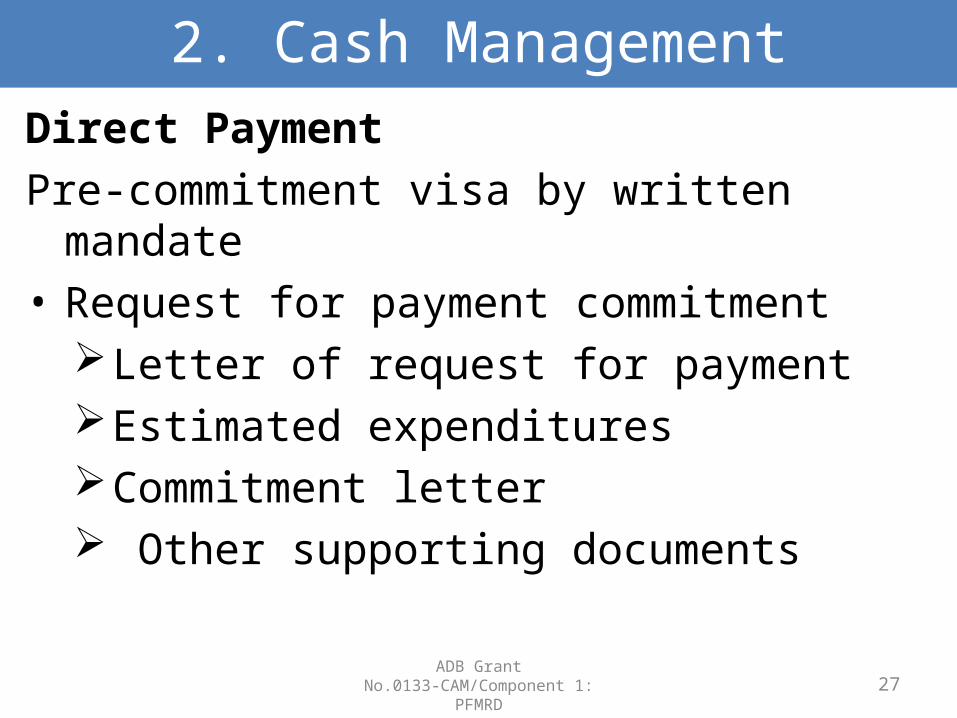

2. Cash ManagementDirect PaymentPre-commitment visa by written mandate• Request for payment commitment

Letter of request for paymentEstimated expendituresCommitment letter Other supporting documents

ADB Grant No.0133-CAM/Component 1: PFMRD 28

2. Cash ManagementDirect Payment• Public procurement procedural according to

the threshold (national budget and donor budget)e.g:

Threshold National Budget Donor Budget-SOP/PM

Canvassing Less than 20 M Riel Less than 500 US$

Quotation 20 M Riel-100 M Riel 500 US$ - 5 000 (without advertisement)

NCB 100 M Riel – 1 000 M Riel

ICB More than 1 000 M Riel

ADB Grant No.0133-CAM/Component 1: PFMRD 29

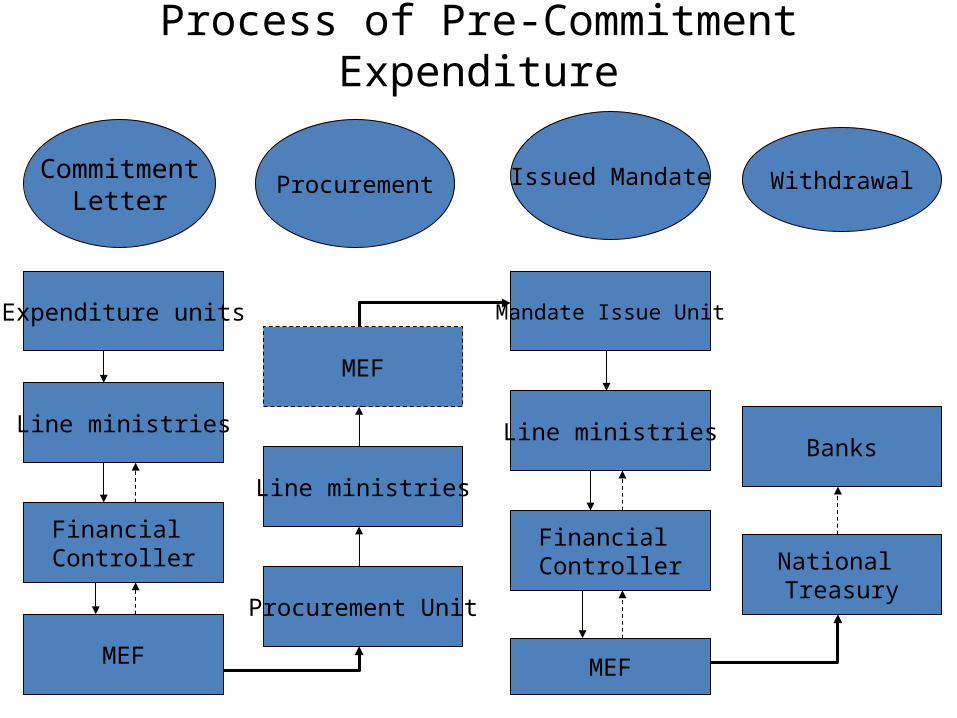

2. Cash ManagementDirect Payment• Contract award (national budget)

Bid evaluation for contract award must be equal or less than the committed expenditure

Mandating of expenditures according to the signed contract and supply/delivery minute

All mandates must submit to MEF before 25th December of each year

Process of Pre-Commitment Expenditure

CommitmentLetter

Procurement Issued Mandate Withdrawal

Expenditure units

Line ministries

Financial Controller

MEF

Line ministries

Procurement Unit

MEF

Mandate Issue Unit

Line ministries

Financial Controller

MEF

Banks

National Treasury

ADB Grant No.0133-CAM/Component 1: PFMRD 31

3. Management Government Bank AccountTax collection or expenditure payment, the Treasury

must be responsible for supervising all central government bank accounts, including any extra budgetary funds.

• When commercial banks are involved in revenue collection or expenditure payments, the banking arrangements must be negotiated and contracted by the Treasury.

• Treasury may have deposit accounts with commercial banks, which should be selected on a competitive basis to get higher-yielding terms

ADB Grant No.0133-CAM/Component 1: PFMRD 32

3. Management Government Bank AccountRelationship with the central bank in public

expenditure management.– Main cashier of the government– Government issuing, public debt management, intervention on

the secondary market for government securities, etc.– In many countries, the central banks provide the governments

with overdraft facilities. – More countries set stringent limits for government borrowing

from the Central Bank or forbid it.– From cash management, prohibiting borrowing from the

Central Bank requires an active policy of issuing government securities in the capital market and also intervening in the secondary market.

– Designated/Special accounts for donors funding

ADB Grant No.0133-CAM/Component 1: PFMRD 33

4. Financial Plan ForecastingFinancial planning and cash flow forecasts are needed

both to ensure that cash outflows are compatible with cash inflows and to prepare borrowing plans.

Cash planning must be done in advance and communicated to spending agencies to allow them to implement their budgets efficiently.

Financial planning includes the preparation of an annual cash plan and a budget implementation plan, monthly cash plans, and in-month forecasts.

ADB Grant No.0133-CAM/Component 1: PFMRD 34

4. Financial Plan Forecasting

In Cambodia• Annual Budget Law – appropriate budget

approved within December, then RGC issued Sub-decree on the budget appropriation and, MEF issued the Circular on the annual budget execution at ending of December. e.g. Budget Law 2010:– Sub-decree 227 RGC, dated 24-Dec-2009, on

Appropriation revenue budget for 2010– Sub-decree 228 RGC, dated 24-Dec-2009, on

Appropriation expenditure budget for 2010

ADB Grant No.0133-CAM/Component 1: PFMRD 35

4. Financial Plan Forecasting

In Cambodia (continue)– MEF issued circular No.004 MEF, dated 25-Dec-2010,

guideline on the implementation of budget law 2010

• Collection revenue: For rural ministries concerned to non-tax revenue (page 8-10 of 18, circular 004 above)

• Expenditure plan:– Program/non program budget, may request for

commitment of expenditures according to 3 larger items:

ADB Grant No.0133-CAM/Component 1: PFMRD 36

4. Financial Plan Forecasting

• Expenditure plan: (continue)1. Chapter 64 – Don’t need request for commitment,

except Ministry of Defense;2. Non procurement expenditure - Don’t need request

for commitment;3. Procurement expenditure – Must request for

commitment of expenditure (at least 6 month per time, or according to the procurement plan).

– All expenditures with non commitment, the authorizer may issues payment mandate attached of completed supporting documents.