Embed Size (px)

Citation preview

July 2013

MOSA Quartely Report – Issue 21Mobile Operator Strategies Analysis

Copyright © Maravedis Inc 2013.

CLIENT CONFIDENTIAL

Adaptive smart cells accelerating; first operator steps to LTE Advanced

2

MOSA stands for Mobile Operator Strategy Analysis. MOSA is the

ONLY exclusive Operator Tracking Service focusing on the leading

100 4G operator wirelessinfrastructure strategies

www.maravedis-bwa.com

Copyright © Maravedis Inc 2013.CLIENT CONFIDENTIAL

Copyright © Maravedis Inc 2012.

www.maravedis-bwa.com

Copyright © Maravedis Inc 2013.CLIENT CONFIDENTIAL

MOSA Coverage

Macro RAN Small Cells & WiFi Backhaul

Global SpectrumCore Network SWOT & Ranking

4

www.maravedis-bwa.com

Copyright © Maravedis Inc 2013.CLIENT CONFIDENTIAL

100 Operators CoveredIndia Aircel

India Bharti Airtel

China China Mobile

China China Telecom

China China Unicom

Taiwan Chunghwa Telecom

Hong Kong CSL Limited Japan EMOBILE Ltd

Taiwan FarEasTone

Philippines Globe Telecom

Japan KDDI

South Korea Korea Telecom(LTE)

South Korea LG U+

Malaysia Maxis Communications

Japan NTT DOCOMO

Australia Optus/vividwireless

Malaysia Packet One Networks (P1)

India Reliance Industries Limited

Singapore SingTel

South Korea SK Telecom.

Philippines Smart Communications

Japan SOFTBANK MOBILE

New Zealand Telecom New Zealand

Australia Telstra

India Tikona Digital Networks

Mexico America Móvil (Telcel)

Uruguay Antel

Colombia Claro

Chile Claro

Jamaica Digicel

Brazil Embratel / Telmex

Chile Entel

Venezuela MovilMax

Brazil Oi Brazil

Puero Rico Open Mobile

Brazil Sky Brazil

Argentina Telecom Argentina (Personal) Mexico Telefonica / Movistar Mexico

Colombia UNE Telecomunicaciones

Denmark 3

Poland Aero2 Group

France Bouygues Telecom

Finland Elisa

UK Everything Everywhere

Belgium KPN Group

Russia MegaFon

Russia MTS/Comstar

Sweden Net4Mobility

Germany O2 Germany

France Orange

Russia Rostelecom

France SFR

Portugal TDC

Sweden Tele2

Italy Telecom Italia

UK Telefonica O2

Spain Telefonica Spain

Austria Telekom Austria

Norway Telenor

Denmark TeliaSonera

Sweden Teliasonera

Norway Teliasonera

Portugal TMN

Austria T-Mobile Austria

Germany T-Mobile International AG

Turkey Turkcell

Russia Vimpelcom

Germany Vodafone Germany

Russia Yota

UAE Etisalat

Saudi Arabia Mobily

Namibia MTC Namibia

South Africa MTN

Saudi Arabia Saudi Telecom Company (STC)

South Africa Vodacom

Saudi Arabia ZAIN

USA AT&T

Canada Bell Canada

USA Clearwire USA

USA Dish Network

USA Leap Wireless

Canada Rogers Wireless

USA Sprint Nextel

Canada Telus Mobility

USA T-Mobile USA

USA Verizon Wireless

Malaysia DiGi

UK Telefonica O2

Qatar Ooredoo

Malaysia Celcom Axiata

Brazil Claro

Spain Vodafone

Spain Orange

Portugal Optimus

Czech Telefonica O2

Switzerland Swisscom

Italy 3 Italia

Italy Vodafone

Netherlands T-Mobile

Nigeria Airtel

Copyright © Maravedis Inc 2012.

www.maravedis-bwa.com

Copyright © Maravedis Inc 2013.CLIENT CONFIDENTIAL

MOSA Deliverables:

Infrastructure Profiles (PDF) Quarterly Reports (PPT)

Quarterly Master File (Excel)Briefings, Analyst Support

MOSA Matrix

• Top 100 4G operators analyzed against 10 key trends identified by MaRe for their impact on the 4G business case

• Small cells and HetNet

• Multiband LTE deployments including carrier aggregation

• TD-LTE and converged FD/TD-LTE

• Voice strategies including VoLTE

• LTE-Advanced deployment/contribution

• Cloud RAN

• Machine-to-machine services

• Advanced backhaul strategies

• Mobile cloud services

• Innovative applications including vertical markets

DRIVERS CHALLENGES SOLUTIONS

Structure of MOSA

July 2013

In each key topic area, gold standard operators selected

and analyzed in depth for their market leadership in the area. The business case and

prospects of others are assessed against the same

criteria.

Copyright © Maravedis Inc 2013.CLIENT CONFIDENTIAL

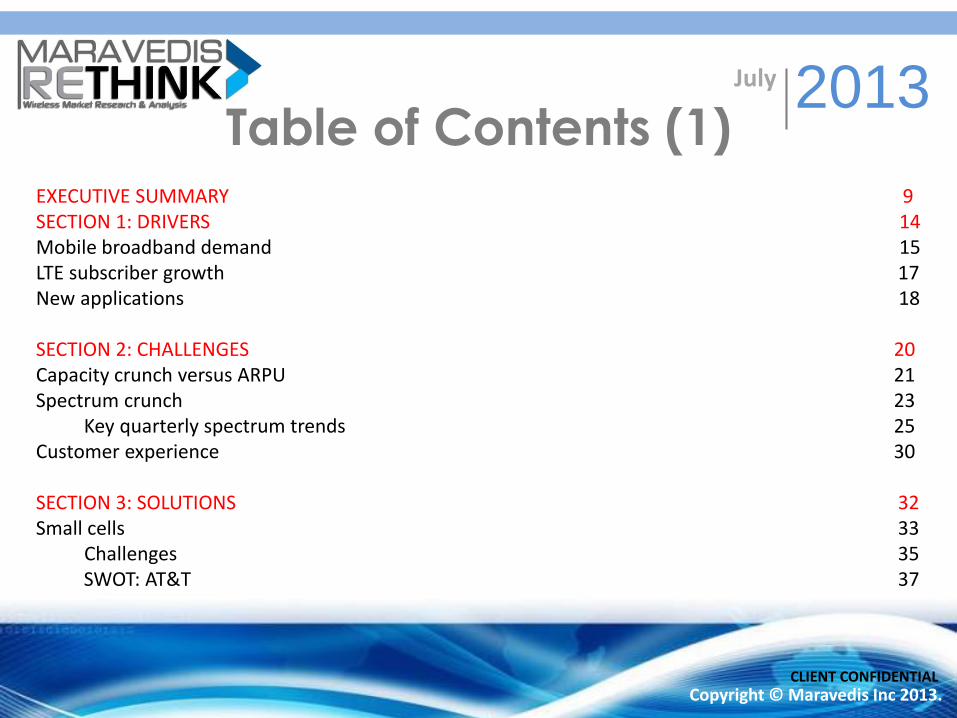

Table of Contents (1)July 2013

7Copyright © Maravedis Inc 2013.

CLIENT CONFIDENTIAL

EXECUTIVE SUMMARY 9SECTION 1: DRIVERS 14Mobile broadband demand 15LTE subscriber growth 17New applications 18

SECTION 2: CHALLENGES 20Capacity crunch versus ARPU 21Spectrum crunch 23

Key quarterly spectrum trends 25Customer experience 30

SECTION 3: SOLUTIONS 32Small cells 33

Challenges 35SWOT: AT&T 37

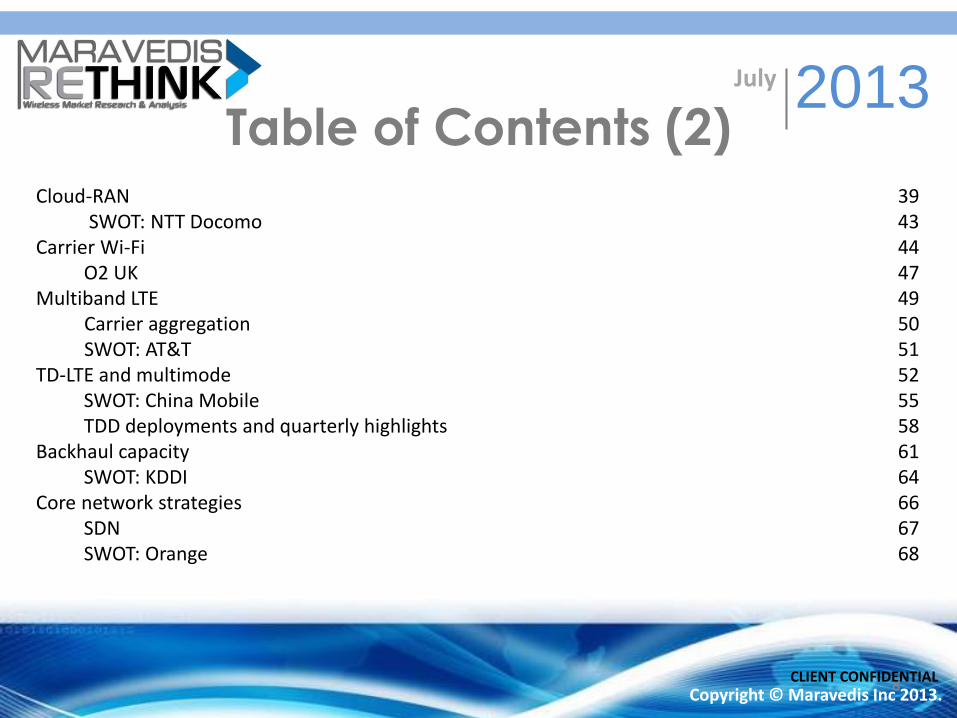

July 2013Table of Contents (2)

88Copyright © Maravedis Inc 2013.

CLIENT CONFIDENTIAL

Cloud-RAN 39SWOT: NTT Docomo 43

Carrier Wi-Fi 44O2 UK 47

Multiband LTE 49Carrier aggregation 50SWOT: AT&T 51

TD-LTE and multimode 52SWOT: China Mobile 55TDD deployments and quarterly highlights 58

Backhaul capacity 61SWOT: KDDI 64

Core network strategies 66SDN 67SWOT: Orange 68

July 2013Table of Contents (3)

99Copyright © Maravedis Inc 2013.

CLIENT CONFIDENTIAL

EDGE networking and optimization 69SWOT: Maxis 71

VoLTE and RCS 73SWOT: Telefonica 74

Progress to LTE-Advanced 75SWOT: SK Telecom 76

SECTION 4: TRENDS AND FORECASTS 78FDD-LTE trends and forecasts 79Regional LTE highlights of the quarter 80LTE subscriber trends 86LTE infrastructure contracts and trends 91WiMAX trends and forecast 934G subscriber forecast 96

July 2013

EXECUTIVE SUMMARYMobile Operator Strategy Analysis

10Copyright © Maravedis Inc 2013

CLIENT CONFIDENTIAL

Copyright © Maravedis Inc 2013.CLIENT CONFIDENTIAL

July 2013

At the heart of the Mobile Operator Strategy Analysis (MOSA) service is the MOSA Matrix. Thisassesses the Top 100 4G operators against the 10 key technology and business trends,identified by Maravedis-Rethink as critical for business success. For the second quarter of2013, the following operators were identified as leaders in these areas:

TRENDS OPERATOR

Small Cells AT&T

Distributed RAN/C-RAN NTT Docomo

Carrier Wi-Fi Telefonica O2 UK

Multiband LTE/carrier aggregation AT&T

TD-LTE and multimode China Mobile

Backhaul capacity KDDI

Innovative core strategies Orange

Optimization and edge networks Maxis

VoLTE and RCS Telefonica Group

Progress to LTE-Advanced SK Telecom

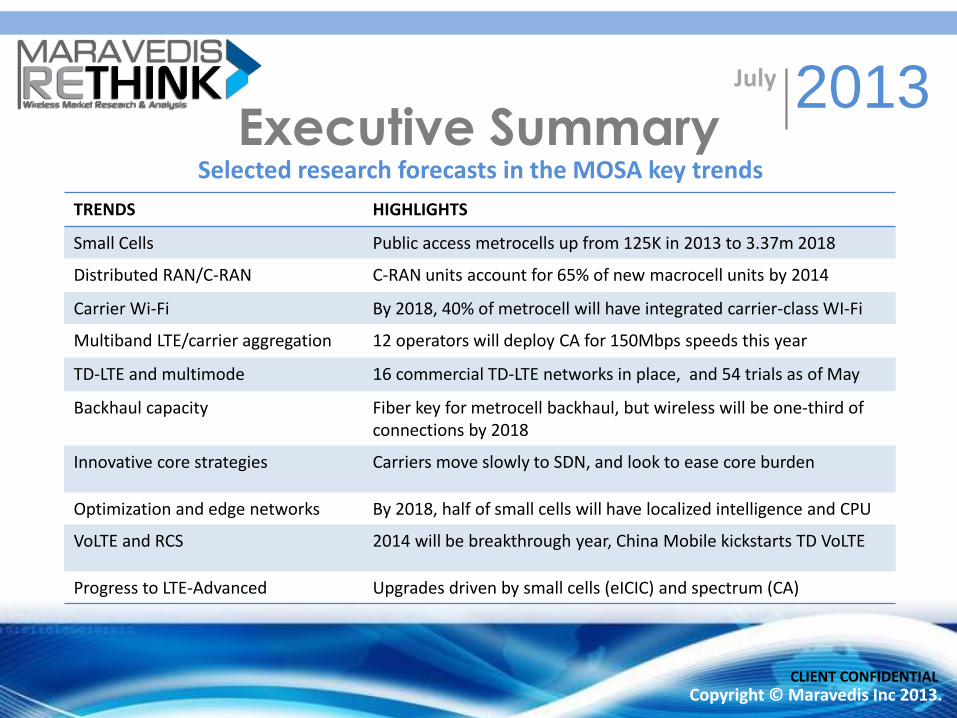

Executive Summary

Copyright © Maravedis Inc 2013.CLIENT CONFIDENTIAL

Selected research forecasts in the MOSA key trends

TRENDS HIGHLIGHTS

Small Cells Public access metrocells up from 125K in 2013 to 3.37m 2018

Distributed RAN/C-RAN C-RAN units account for 65% of new macrocell units by 2014

Carrier Wi-Fi By 2018, 40% of metrocell will have integrated carrier-class WI-Fi

Multiband LTE/carrier aggregation 12 operators will deploy CA for 150Mbps speeds this year

TD-LTE and multimode 16 commercial TD-LTE networks in place, and 54 trials as of May

Backhaul capacity Fiber key for metrocell backhaul, but wireless will be one-third of connections by 2018

Innovative core strategies Carriers move slowly to SDN, and look to ease core burden

Optimization and edge networks By 2018, half of small cells will have localized intelligence and CPU

VoLTE and RCS 2014 will be breakthrough year, China Mobile kickstarts TD VoLTE

Progress to LTE-Advanced Upgrades driven by small cells (eICIC) and spectrum (CA)

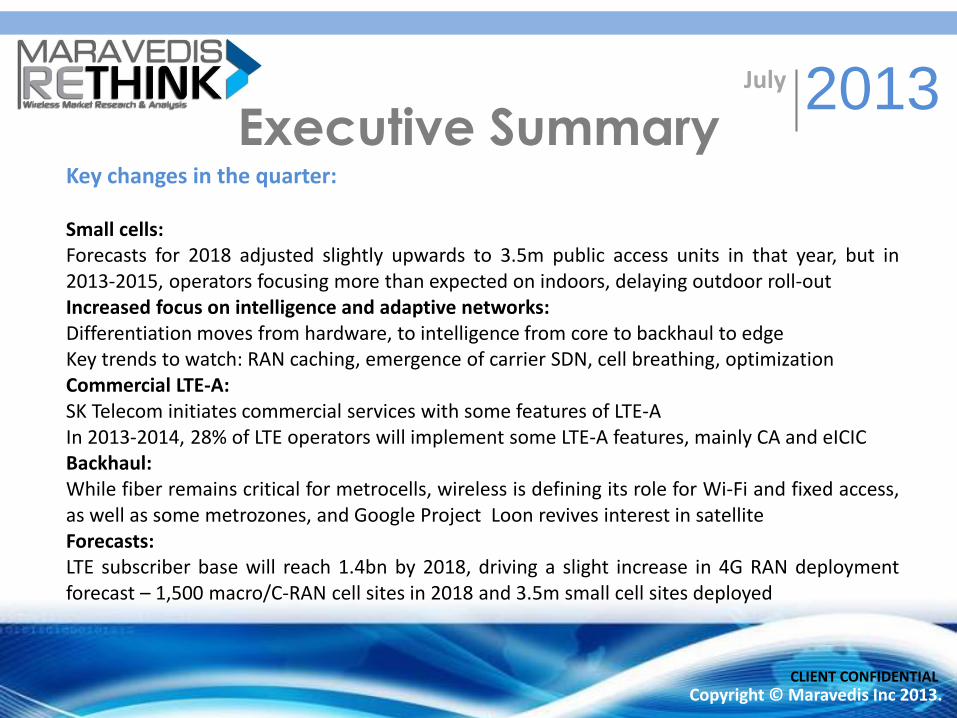

Executive SummaryJuly 2013

Key changes in the quarter:

Small cells:Forecasts for 2018 adjusted slightly upwards to 3.5m public access units in that year, but in2013-2015, operators focusing more than expected on indoors, delaying outdoor roll-outIncreased focus on intelligence and adaptive networks:Differentiation moves from hardware, to intelligence from core to backhaul to edgeKey trends to watch: RAN caching, emergence of carrier SDN, cell breathing, optimizationCommercial LTE-A:SK Telecom initiates commercial services with some features of LTE-AIn 2013-2014, 28% of LTE operators will implement some LTE-A features, mainly CA and eICICBackhaul:While fiber remains critical for metrocells, wireless is defining its role for Wi-Fi and fixed access,as well as some metrozones, and Google Project Loon revives interest in satelliteForecasts:LTE subscriber base will reach 1.4bn by 2018, driving a slight increase in 4G RAN deploymentforecast – 1,500 macro/C-RAN cell sites in 2018 and 3.5m small cell sites deployed

Executive SummaryJuly 2013

Copyright © Maravedis Inc 2013.CLIENT CONFIDENTIAL

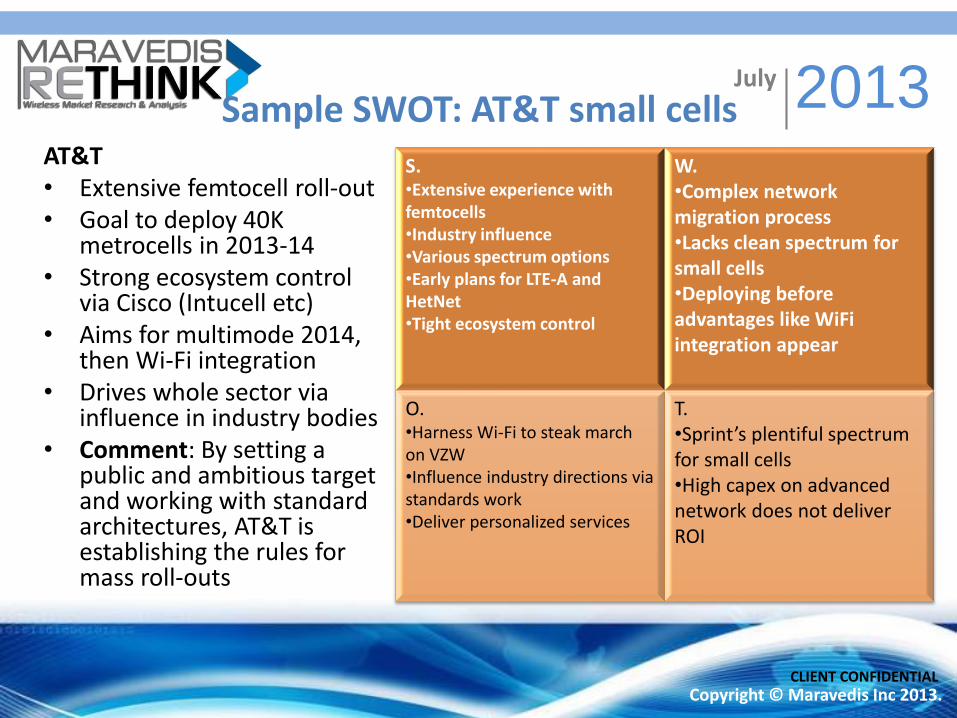

Sample SWOT: AT&T small cellsAT&T• Extensive femtocell roll-out• Goal to deploy 40K

metrocells in 2013-14• Strong ecosystem control

via Cisco (Intucell etc)• Aims for multimode 2014,

then Wi-Fi integration• Drives whole sector via

influence in industry bodies• Comment: By setting a

public and ambitious target and working with standard architectures, AT&T is establishing the rules for mass roll-outs

S.•Extensive experience with femtocells•Industry influence •Various spectrum options•Early plans for LTE-A and HetNet•Tight ecosystem control

W.•Complex network migration process•Lacks clean spectrum for small cells•Deploying before advantages like WiFiintegration appear

O.•Harness Wi-Fi to steak march on VZW•Influence industry directions via standards work•Deliver personalized services

T.•Sprint’s plentiful spectrum for small cells•High capex on advanced network does not deliver ROI

July 2013

Copyright © Maravedis Inc 2013.CLIENT CONFIDENTIAL

Sample forecastMetrocell backhaul

July 2013

Copyright © Maravedis Inc 2013.CLIENT CONFIDENTIAL

Source: Wireless Backhaul Market from an Intermodal Perspective, April 2013

Copyright © Maravedis Inc 2013.CLIENT CONFIDENTIAL

16

QUESTIONS?

June 2013

Adlane FellahCustomer Engagement

Maravedis-RethinkUS Land: +1(305) 865 1006

[email protected]@maravedis-bwa.com

![Microsoftdownload.microsoft.com/download/1/F/2/1F23AFFA-7CA9-452D... · Web view目的のオブジェクトが表示されます。4. [クリア] をクリックすると、元のオブジェクトの一覧に戻ります。](https://img.pdfslide.us/doc/110x75/5ff2bf1c44c4a75b94361d0a/web-view-ccffoeecoe4-f-ffffffe.jpg)

![11PPMI Program Outline E › p2m › seminar › aots › 11PPMI Program Outline _E_.pdfInfrastructure Construction and Plant Engineering [PPMI] 6 – 17 February 2012 ... coal gasification](https://img.pdfslide.us/doc/110x75/5ed5a79a740631020e41ceaf/11ppmi-program-outline-e-a-p2m-a-seminar-a-aots-a-11ppmi-program-outline.jpg)