Embed Size (px)

Citation preview

85

PART 2, CHAPTER 1, COMPREHENSIVE ANALYSIS OF NIS-FOREX MARKET

Part 2

Activity in the NIS-Forex Market

86

BANK OF ISRAEL, CONTROLLER OF FOREIGN EXCHANGE, ANNUAL REPORT 2001

87

PART 2, CHAPTER 1, COMPREHENSIVE ANALYSIS OF NIS-FOREX MARKET

Activity in the NIS-Forex Market

Developments in the NIS-forex market in 2001 reflected the maturingof various processes in recent years. Since the middle of 1997, when theexchange-rate regime was eased, the rate has been set freely by marketforces. This development, which along with the contraction of the NIS-forex interest spread led to an increase in exchange-rate risk, acted inconcert with foreign-currency liberalization, globalization, andsolidification of the credibility of macroeconomic policy to make theNIS-forex market more efficient. Additional progress was made in 2001:trading volumes increased substantially, the market became deeper, anda new class of players—foreign financial institutions—made their debut.The exchange-rate changes in 2001 led in two directions with nosignificant trend, due to equilibrium among market forces that madecentral-bank intervention unnecessary. The market did experienceexternal and domestic shocks that, however, affected it for relativelyshort periods of time only.

The forces at work in the market in recent years will probably remainoperative in the near future and will allow the market to continue toperform soundly and without intervention—provided that the fiscal andeconomic policies not deviate from accepted international standards. On December 25, the key rate was lowered suddenly and surprisingly,in conjunction with the announcement of related measures in regard toliberalization and the exchange-rate band. The rate cut had a substantialimpact on the relative rate of return on assets, and immediately after itwas announced households began to generate demand for forex. Thisdemand lasted into January 2002 and caused the currency to depreciatesteeply. The business sector, by engaging in net sales of foreign currency,countered the exchange-rate trend—much as it had during previousshocks.

88

BANK OF ISRAEL, CONTROLLER OF FOREIGN EXCHANGE, ANNUAL REPORT 2001

Part 2 is divided into two chapters.Chapter 1 presents a comprehensive analysis of developments in the

NIS-forex market and attempts, by ex post argumentation, to draw aconnection between trends in the NIS exchange rate against the five-currency basket and changes in forex supply and demand by variousmarket sectors and those who affect them. (The framework of the analysisis described in the appendix at the end of this part of the report.) Theeffect of the December 25 rate cut on the NIS-forex market is analyzedseparately at the end of the chapter.

Chapter 2 reviews developments in main components of residents’portfolios of forex assets and liabilities and nonresidents’ portfolios inNIS.

89

PART 2, CHAPTER 1, COMPREHENSIVE ANALYSIS OF NIS-FOREX MARKET

Chapter 1

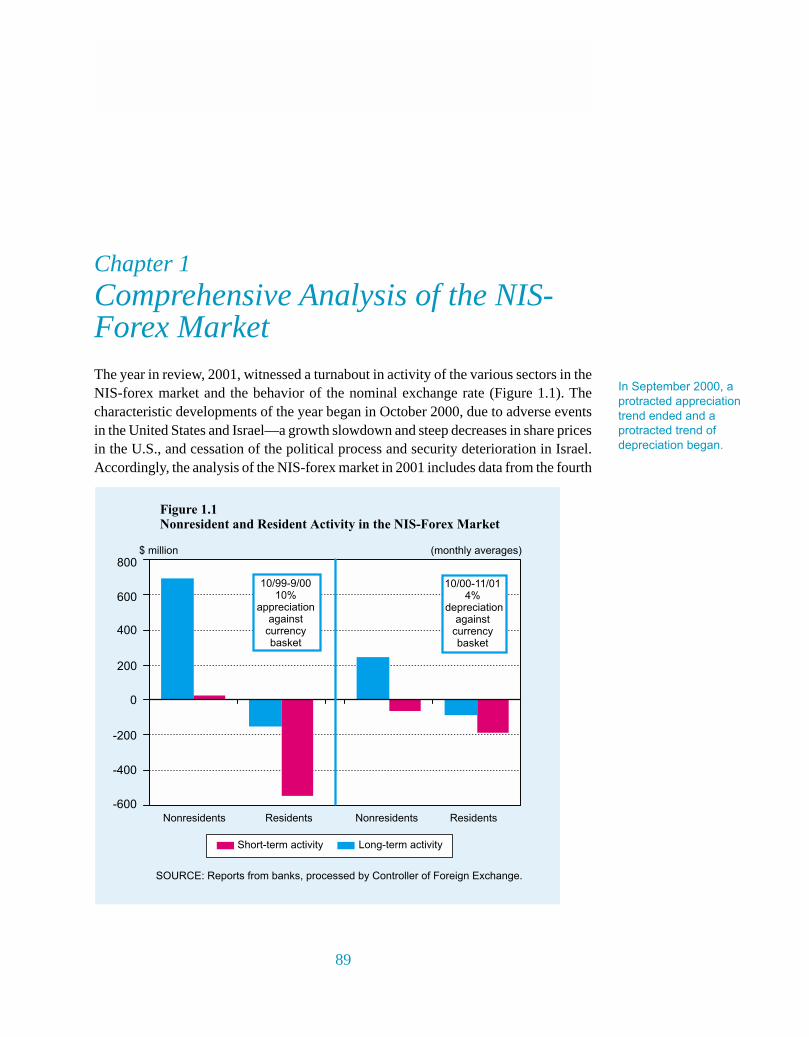

Comprehensive Analysis of the NIS-Forex MarketThe year in review, 2001, witnessed a turnabout in activity of the various sectors in theNIS-forex market and the behavior of the nominal exchange rate (Figure 1.1). Thecharacteristic developments of the year began in October 2000, due to adverse eventsin the United States and Israel—a growth slowdown and steep decreases in share pricesin the U.S., and cessation of the political process and security deterioration in Israel.Accordingly, the analysis of the NIS-forex market in 2001 includes data from the fourth

In September 2000, a

protracted appreciation

trend ended and a

protracted trend of

depreciation began.

90

BANK OF ISRAEL, CONTROLLER OF FOREIGN EXCHANGE, ANNUAL REPORT 2001

quarter of 2000 to November 2001 as the ‘survey period’ and those in the twelve monthspreceding October 2000 as the ‘comparison period.’

1. EXCHANGE-RATE DEVELOPMENTS

The NIS-forex market experienced a turnaround in October 2000, as protractedappreciation of the NIS against the five-currency basket during the comparison period(10 percent) was succeeded by depreciation. Despite several months of gravedevelopments in the U.S. and Israel, the depreciation of the NIS did not persist in thelong term; the cumulative depreciation against the basket during the survey period was4 percent amidst bidirectional volatility: External and domestic shocks in the markethad short-term effects only, as appreciation succeeded depreciation. The rather gentleresponse of the exchange rate in October 2000 and from then until November 2001stands out especially in comparison with the shocks that the market absorbed in previousyears. In 1998, for example, in the aftermath of an externality—a shock in theinternational financial markets, related to the crisis in Russia and the bailout of theLTCM hedging fund—the NIS lost 12 percent against the basket in October 1998 and20 percent in cumulative terms in August–October.

2. SECTORAL ACTIVITY IN THE NIS-FOREX MARKET

The transition from appreciation to moderate depreciation was occasioned by aperceptible change in the market behavior of nonresidents and residents. Since thesesectors were affected by different factors and considerations, their responses to theexchange-rate change led to a heterogeneity that contributed to market stability.

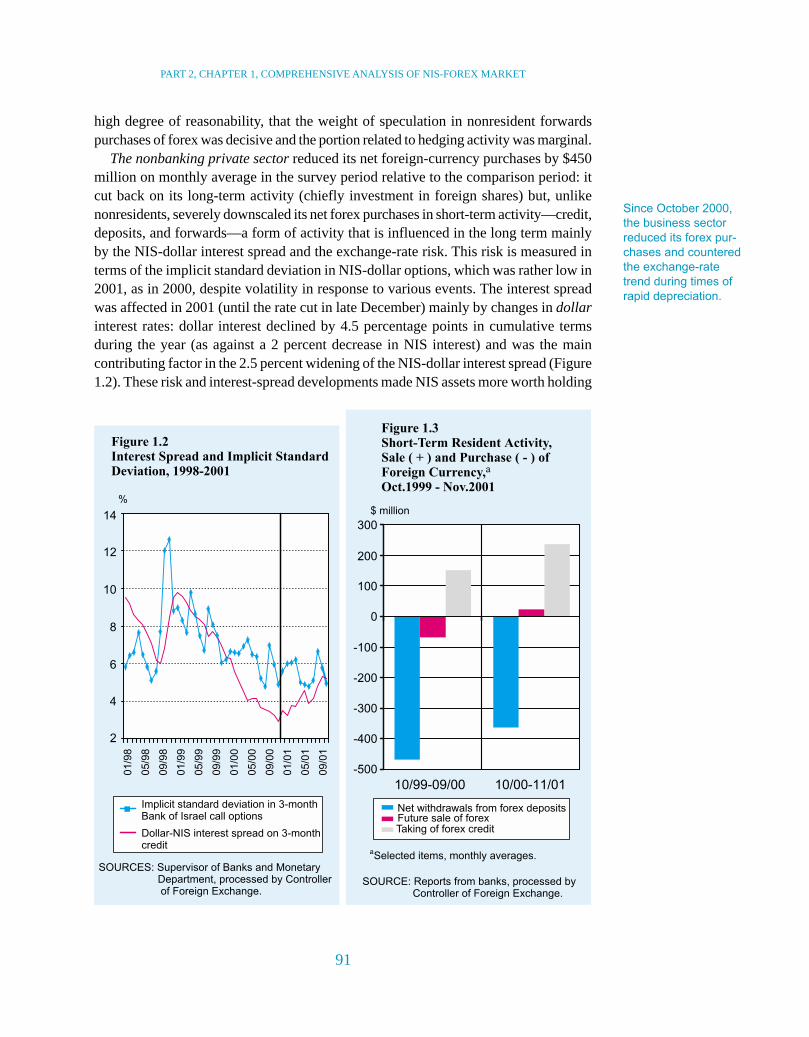

Nonresidents considerably reduced their long-term activity—investments in theshares of Israeli companies, an activity related to the economy’s underlying factors—during the survey period. These investments, an important component in the foreign-currency inflow in the comparison period, were affected mainly by the Nasdaq index,which reflects demand for high-tech products and affects Israeli companies’ assessmentsof the prospects of issuing in the American market. (These investments came to $258million on monthly average in the survey period as against $690 million on average inthe comparison period; see Table 1.1.) Concurrently, nonresidents became more activein vehicles related to short-term considerations of exchange-rate risk and interest spreads:they began to purchase forex by concluding forwards transactions and, for the firsttime, amassed a surplus of short-term NIS liabilities. Short-term forwards activity—which became possible due to the repeal of the restriction on forex-denominatedforwards for terms exceeding thirty days—also indicates that nonresidents becamemore sensitive to the implicit interest spread and exchange-rate risk that forwards carryby their very definition. This activity was apparently influenced by the decline in politicaland security conditions, which convinced nonresidents that the NIS was about todepreciate at a rate exceeding that implicit in the forward exchange rate derived fromthe interest spreads. Analysis of forwards activity during the year indicates, with a

Since October 2000,

nonresidents have

reduced their invest-

ments in Israeli

shares perceptibly

and increased their

activity in futures, due

to short-term

considerations.

91

PART 2, CHAPTER 1, COMPREHENSIVE ANALYSIS OF NIS-FOREX MARKET

high degree of reasonability, that the weight of speculation in nonresident forwardspurchases of forex was decisive and the portion related to hedging activity was marginal.

The nonbanking private sector reduced its net foreign-currency purchases by $450million on monthly average in the survey period relative to the comparison period: itcut back on its long-term activity (chiefly investment in foreign shares) but, unlikenonresidents, severely downscaled its net forex purchases in short-term activity—credit,deposits, and forwards—a form of activity that is influenced in the long term mainlyby the NIS-dollar interest spread and the exchange-rate risk. This risk is measured interms of the implicit standard deviation in NIS-dollar options, which was rather low in2001, as in 2000, despite volatility in response to various events. The interest spreadwas affected in 2001 (until the rate cut in late December) mainly by changes in dollarinterest rates: dollar interest declined by 4.5 percentage points in cumulative termsduring the year (as against a 2 percent decrease in NIS interest) and was the maincontributing factor in the 2.5 percent widening of the NIS-dollar interest spread (Figure1.2). These risk and interest-spread developments made NIS assets more worth holding

Since October 2000,

the business sector

reduced its forex pur-

chases and countered

the exchange-rate

trend during times of

rapid depreciation.

92

BANK OF ISRAEL, CONTROLLER OF FOREIGN EXCHANGE, ANNUAL REPORT 2001

in relative terms and prompted the business sector to downsize its accumulation ofshort-term forex assets (Figure 1.3). Indeed, this sector acquired $137 million in short-term assets during the survey period, in net monthly average terms, as against $550million in the comparison period.

The business sector also took more of its credit in forex and made more forwardssales, especially in months when nonresidents’ heightened demand generateddepreciation pressure.

The non-business sector contributed to the relative stability of the exchange rate byrefraining, in most months, from massive accumulation of foreign currency in deposits,which would have aggravated the depreciation. This is in contrast to the prior behaviorof this sector, e.g., in October 1998. However, this year, especially in the third quarter,the non-business sector bought $550 million by investing in mutual funds that specializein foreign-currency assets in Israel.

The banks, which since the second half of 1997 have served as market makers in theNIS-forex market and not only as intermediaries between the public and the Bank of

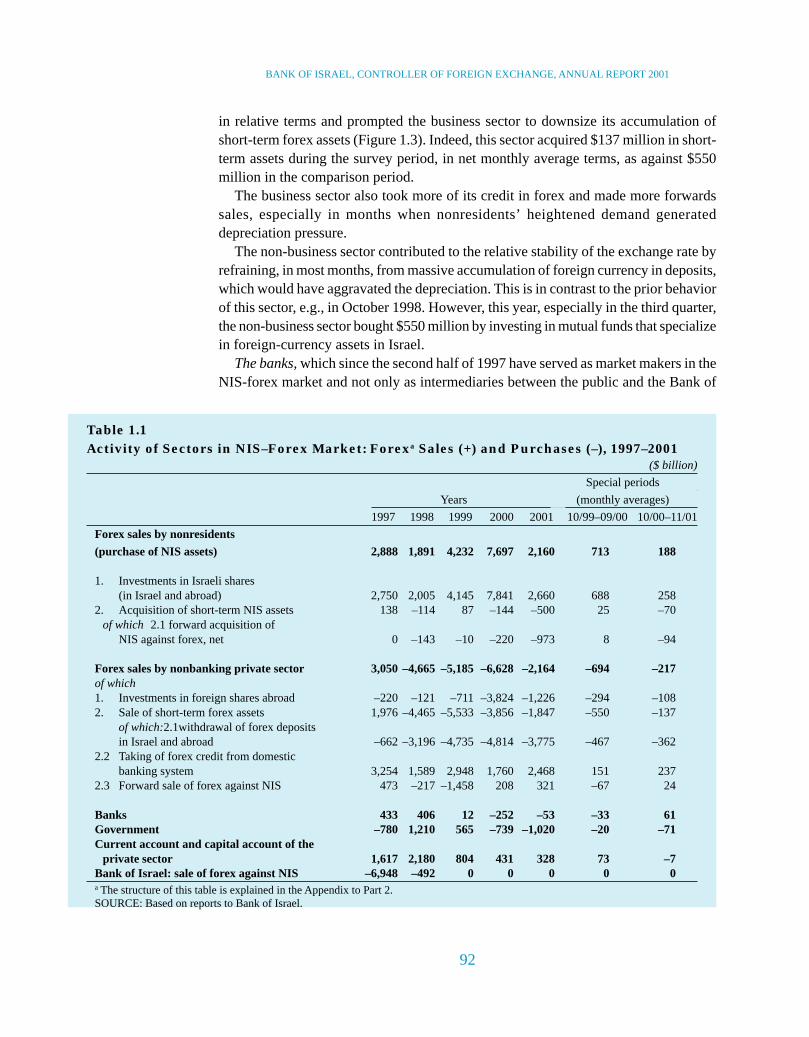

Table 1.1Activity of Sectors in NIS–Forex Market: Forexa Sales (+) and Purchases (–), 1997–2001

($ billion)

Special periods

Years (monthly averages)

1997 1998 1999 2000 2001 10/99–09/00 10/00–11/01

Forex sales by nonresidents

(purchase of NIS assets) 2,888 1,891 4,232 7,697 2,160 713 188

1. Investments in Israeli shares(in Israel and abroad) 2,750 2,005 4,145 7,841 2,660 688 258

2. Acquisition of short-term NIS assets 138 –114 87 –144 –500 25 –70of which 2.1 forward acquisition of

NIS against forex, net 0 –143 –10 –220 –973 8 –94

Forex sales by nonbanking private sector 3,050 –4,665 –5,185 –6,628 –2,164 –694 –217of which1. Investments in foreign shares abroad –220 –121 –711 –3,824 –1,226 –294 –1082. Sale of short-term forex assets 1,976 –4,465 –5,533 –3,856 –1,847 –550 –137

of which:2.1withdrawal of forex depositsin Israel and abroad –662 –3,196 –4,735 –4,814 –3,775 –467 –362

2.2 Taking of forex credit from domesticbanking system 3,254 1,589 2,948 1,760 2,468 151 237

2.3 Forward sale of forex against NIS 473 –217 –1,458 208 321 –67 24

Banks 433 406 12 –252 –53 –33 61Government –780 1,210 565 –739 –1,020 –20 –71Current account and capital account of the

private sector 1,617 2,180 804 431 328 73 –7Bank of Israel: sale of forex against NIS –6,948 –492 0 0 0 0 0a The structure of this table is explained in the Appendix to Part 2.SOURCE: Based on reports to Bank of Israel.

93

PART 2, CHAPTER 1, COMPREHENSIVE ANALYSIS OF NIS-FOREX MARKET

Israel, have been avoiding a long-term exchange-rate position in their activity in theforex market. However, at times when large changes occur in this market, the bankscreate limited positions by meeting demand for foreign currency and absorbing supplyin the course of their nostro activity amidst exchange-rate changes.

Three additional sectors are active in the market: the Government, the private sector(in the current and capital account), and the Bank of Israel. The Government had $0.9billion in net redemptions and non-rollover of forex-indexed Gilboa bonds in the courseof 2001. The private sector had a small positive balance in net activity in the currentaccount and capital account. The Bank of Israel did not intervene in foreign-currencytrading, in view of its policy in recent years to intervene only to defend the limits of theexchange-rate band.

In sum, the transition from appreciation in the comparison period to moderatedepreciation in the survey period originated in a decline in nonresident investments.The decline was influenced by the slump in demand for high-tech products and inshare prices in the U.S., and by nonresident demand for forex by means of forwards inview of uncertainty about the security situation.

The bidirectional volatility of the exchange rate during the survey period and themildness of the depreciation, despite the shocks and aforementioned behavior ofnonresidents, were occasioned by the moderate behavior of the nonbanking privatesector.

The persistence of market stability despite the shocks is traceable to an improvementin the underlying conditions of the NIS-forex market in recent years, which made themarket much less sensitive to shocks. The improvement was evident in various aspectsof market performance and macroeconomic policy, and its important contribution tomarket stability in the two years preceding October 2000 stems from the substantialcontraction of external financial vulnerability of the private sector—a vulnerabilityrelated to this sector’s forex and external activity. (See Part 1, Chapter 4.) Due to thisfactor, the market greeted the October 2000 shocks at a totally different point than itssituation on the eve of the shocks in October 1998.

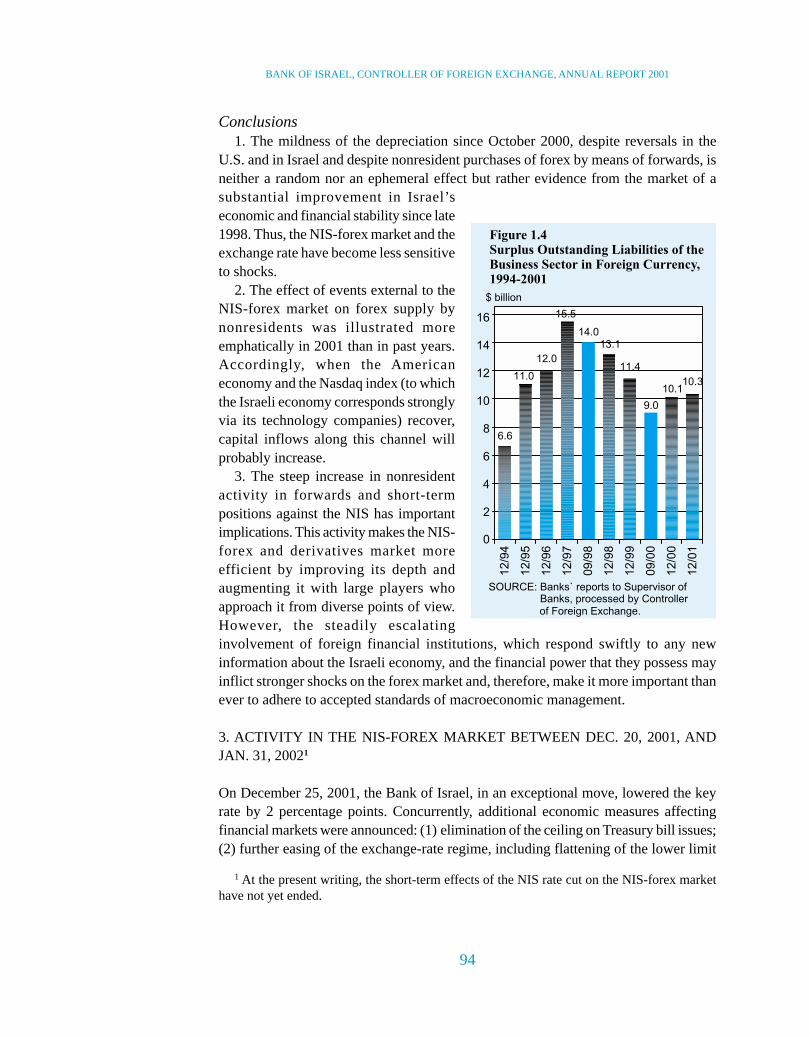

The decrease in vulnerability is evident in various indicators, most importantly thebusiness sector’s exposure to depreciation risk, measured by the surplus of its forexliability over its forex assets. This position contracted steadily from $14 billion to $9billion in the two-year period that began with the rapid depreciation in October 1998(Figure 1.4).

Another reason for greater stability in the NIS-forex market is an improvement invarious aspects of economic performance in the past two years. The main aspects arean improvement in the credibility of macroeconomic policy management, continuedenhancements of efficiency in the NIS-forex market, and the internalization of exchange-rate risk and the possibility of bidirectional volatility of the exchange rate. The last-mentioned improvement originates, among other things, in the Bank of Israel’s policyof non-intervention in trading since early 1998, even during the rapid depreciation thatoccurred at the end of that year.

The non-business sec-

tor contributed to ex-

change-rate stability in

2001 by refraining, in

most months, from

massive accumulation

of foreign currency in

deposits—in contrast

to its prior behavior.

The persistence of

market stability despite

the shocks is traceable

to an improvement in

the underlying con-

ditions of the NIS-forex

market in recent years,

which made the market

much less sensitive to

shocks.

94

BANK OF ISRAEL, CONTROLLER OF FOREIGN EXCHANGE, ANNUAL REPORT 2001

Conclusions1. The mildness of the depreciation since October 2000, despite reversals in the

U.S. and in Israel and despite nonresident purchases of forex by means of forwards, isneither a random nor an ephemeral effect but rather evidence from the market of asubstantial improvement in Israel’seconomic and financial stability since late1998. Thus, the NIS-forex market and theexchange rate have become less sensitiveto shocks.

2. The effect of events external to theNIS-forex market on forex supply bynonresidents was illustrated moreemphatically in 2001 than in past years.Accordingly, when the Americaneconomy and the Nasdaq index (to whichthe Israeli economy corresponds stronglyvia its technology companies) recover,capital inflows along this channel willprobably increase.

3. The steep increase in nonresidentactivity in forwards and short-termpositions against the NIS has importantimplications. This activity makes the NIS-forex and derivatives market moreefficient by improving its depth andaugmenting it with large players whoapproach it from diverse points of view.However, the steadily escalatinginvolvement of foreign financial institutions, which respond swiftly to any newinformation about the Israeli economy, and the financial power that they possess mayinflict stronger shocks on the forex market and, therefore, make it more important thanever to adhere to accepted standards of macroeconomic management.

3. ACTIVITY IN THE NIS-FOREX MARKET BETWEEN DEC. 20, 2001, ANDJAN. 31, 20021

On December 25, 2001, the Bank of Israel, in an exceptional move, lowered the keyrate by 2 percentage points. Concurrently, additional economic measures affectingfinancial markets were announced: (1) elimination of the ceiling on Treasury bill issues;(2) further easing of the exchange-rate regime, including flattening of the lower limit

1 At the present writing, the short-term effects of the NIS rate cut on the NIS-forex markethave not yet ended.

95

PART 2, CHAPTER 1, COMPREHENSIVE ANALYSIS OF NIS-FOREX MARKET

of the band and a 2 percentage point decrease so as to position it permanently at NIS 4.1against the currency basket; and (3) raising the permitted rate of institutional-investorinvestment in forex-denominated and external assets to 20 percent, and elimination ofthe restriction altogether as of January 1, 2003. The rate cut changed the relative returnon assets and the relative cost of NIS credit vs. forex credit perceptibly, and betweenthe time it was announced and January 31, 2002, the NIS exchange rate against thedollar and the currency basket depreciated by 8 percent in cumulative terms. The implicitstandard deviation in NIS-dollar options also climbed steeply to 7.5 percent duringthis time, as against 5 percent in the month preceding the rate cut.

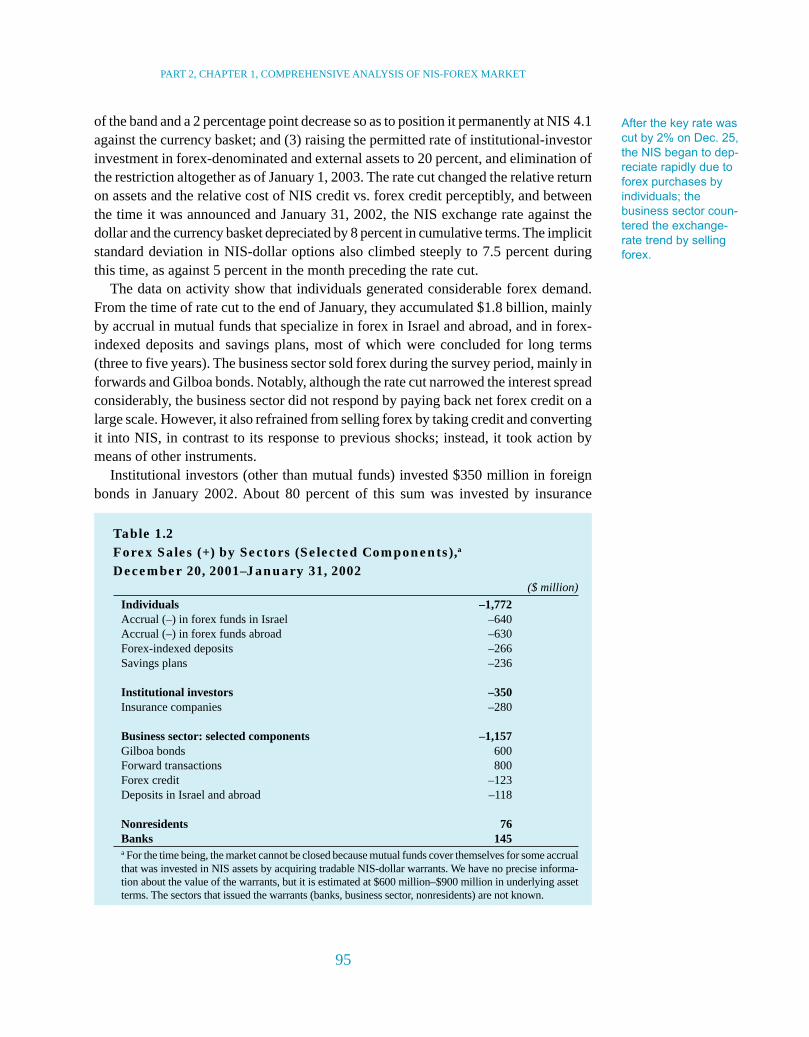

The data on activity show that individuals generated considerable forex demand.From the time of rate cut to the end of January, they accumulated $1.8 billion, mainlyby accrual in mutual funds that specialize in forex in Israel and abroad, and in forex-indexed deposits and savings plans, most of which were concluded for long terms(three to five years). The business sector sold forex during the survey period, mainly inforwards and Gilboa bonds. Notably, although the rate cut narrowed the interest spreadconsiderably, the business sector did not respond by paying back net forex credit on alarge scale. However, it also refrained from selling forex by taking credit and convertingit into NIS, in contrast to its response to previous shocks; instead, it took action bymeans of other instruments.

Institutional investors (other than mutual funds) invested $350 million in foreignbonds in January 2002. About 80 percent of this sum was invested by insurance

After the key rate was

cut by 2% on Dec. 25,

the NIS began to dep-

reciate rapidly due to

forex purchases by

individuals; the

business sector coun-

tered the exchange-

rate trend by selling

forex.

Table 1.2Forex Sales (+) by Sectors (Selected Components),a

December 20, 2001–January 31, 2002($ million)

Individuals –1,772Accrual (–) in forex funds in Israel –640Accrual (–) in forex funds abroad –630Forex-indexed deposits –266Savings plans –236

Institutional investors –350Insurance companies –280

Business sector: selected components –1,157Gilboa bonds 600Forward transactions 800Forex credit –123Deposits in Israel and abroad –118

Nonresidents 76Banks 145a For the time being, the market cannot be closed because mutual funds cover themselves for some accrualthat was invested in NIS assets by acquiring tradable NIS-dollar warrants. We have no precise informa-tion about the value of the warrants, but it is estimated at $600 million–$900 million in underlying assetterms. The sectors that issued the warrants (banks, business sector, nonresidents) are not known.

96

BANK OF ISRAEL, CONTROLLER OF FOREIGN EXCHANGE, ANNUAL REPORT 2001

companies that acquired government and corporate bonds in the euro market and theU.S. The pace of investment abroad accelerated due to falling interest rates and thehigher investment ceiling.

Nonresidents acquired $339 million in forwards in the first week after the rate cut.Afterwards, they sold small quantities of foreign currency during almost all of January.Their net activity in the market during the six weeks at issue was negligible. In January2002, however, nonresident trading volumes in the forex market increased, as did theshare of foreign financial institutions in total activity in NIS-dollar spot and forwardtransactions.

Notably, since the short-term effects of this development on activity in various sectorshave not yet ended, it is premature to analyze its effect on economic stability.

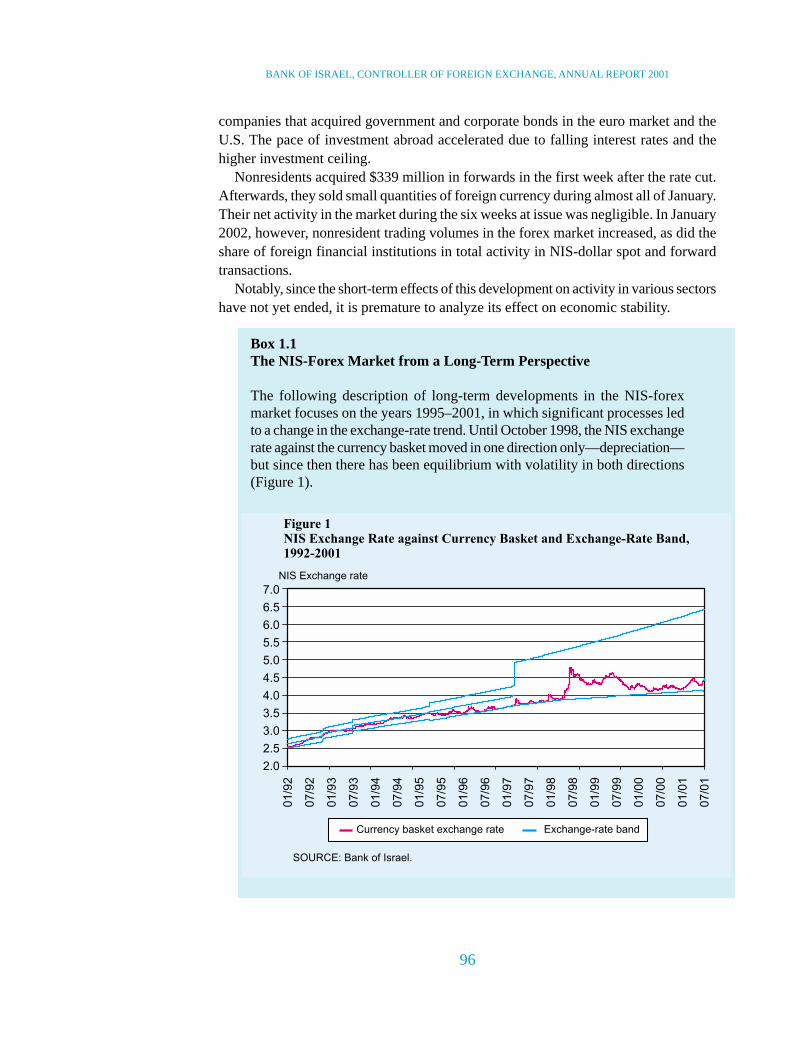

Box 1.1The NIS-Forex Market from a Long-Term Perspective

The following description of long-term developments in the NIS-forexmarket focuses on the years 1995–2001, in which significant processes ledto a change in the exchange-rate trend. Until October 1998, the NIS exchangerate against the currency basket moved in one direction only—depreciation—but since then there has been equilibrium with volatility in both directions(Figure 1).

97

PART 2, CHAPTER 1, COMPREHENSIVE ANALYSIS OF NIS-FOREX MARKET

Below we describe the main processes that caused this profoundchange, which reflects the transition to a more efficient market in whichthe exchange rate is set in response to market forces and without outsideintervention.

Developments in the NIS-forex market in 1995–2001 trace largely tothree factors: economic policy, global effects, and the consolidation ofIsrael’s comparative advantages. Economic policy affected the marketdirectly by liberalizing the forex rules, making the exchange-rate regimemore flexible, and halting intervention in forex trading as long as theexchange rate stayed within the band. It also had two indirect effects,manifested by the disinflationary monetary policy and a fiscal policythat is mindful of the overarching goal of lowering the budget deficit.The global effects on the NIS-forex market were reflected in greaterintegration among global financial markets, portability of capital andprivate investments in foreign markets, and greater demand for high-tech products. The consolidation of Israel’s comparative advantages,foremost in high-tech, made it possible to take advantage of opportunitiesto raise capital abroad.

During the survey period, these processes affected the NIS-forexmarket along four main paths of transmission: the NIS-forex interestspread, exchange-rate risk, the Nasdaq exchange, and Israel’s country

98

BANK OF ISRAEL, CONTROLLER OF FOREIGN EXCHANGE, ANNUAL REPORT 2001

rating. This led to changes in resident and nonresident activities in the marketand, consequently, to intervention or non-intervention by the Bank of Israelin the market and changes in the exchange rate trend.

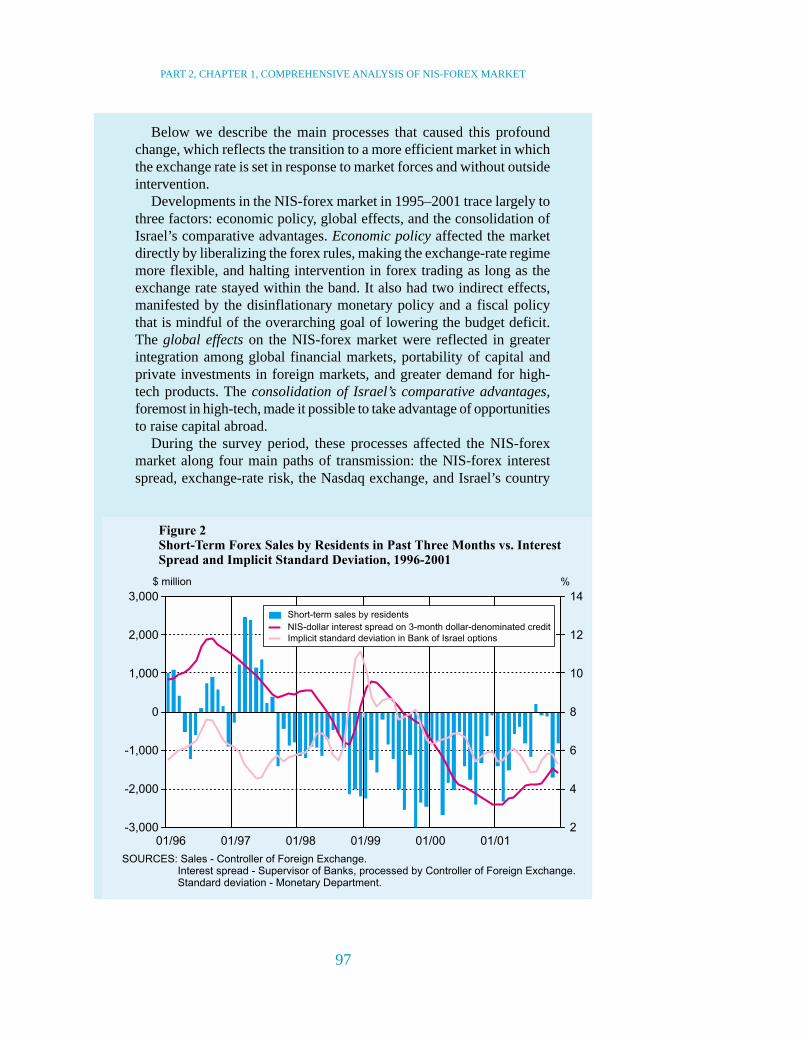

The nonbanking private sector sold forex in 1995–1997, perceptiblylowering its forex assets surplus and moving into a surplus of forex liabilities.This sector changed its behavior in the middle of 1997 and, since then, hasbeen buying forex, building up its forex asset surplus, and reducing itsexposure to depreciation risk. The change in behavior traces to two factorsacting in concert: an increase in the exchange-rate risk, due to the relaxationof the exchange-rate regime, and the narrowing of interest spreads, chieflydue to the lowering of NIS interest rates (Figure 2). This resident activityfocused mainly on short-term instruments (credit and deposits). Residentinvestments in foreign companies’ shares have been climbing in the pasttwo years, abetted by the liberalization and globalization processes.

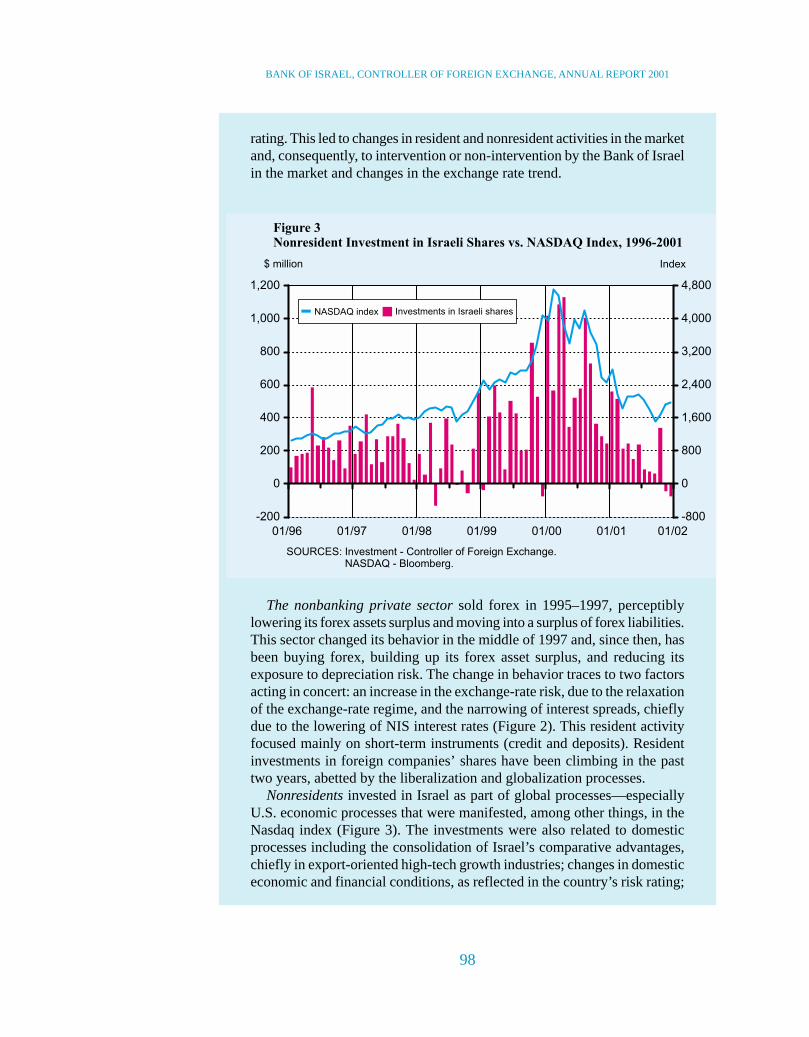

Nonresidents invested in Israel as part of global processes—especiallyU.S. economic processes that were manifested, among other things, in theNasdaq index (Figure 3). The investments were also related to domesticprocesses including the consolidation of Israel’s comparative advantages,chiefly in export-oriented high-tech growth industries; changes in domesticeconomic and financial conditions, as reflected in the country’s risk rating;

99

PART 2, CHAPTER 1, COMPREHENSIVE ANALYSIS OF NIS-FOREX MARKET

and geopolitical developments, foremost the peace process. These processesinfluenced nonresidents’ behavior both in 1999–2000, when investments rose,and in 1998 and 2001, when they declined.

The NIS-forex interest spread did not prompt nonresidents to invest in Israeluntil late 2000; until then, their investments focused on shares of Israelicompanies. Since the last quarter of 2000, nonresidents have also been takingactions for reasons related to the interest spread and exchange-rate risk, mainlyin short-term financial instruments (forwards).

Until early 1996, the Bank of Israel intervened in the NIS-forex marketdirectly. Since then, its intervention has been limited to defense of the limits ofthe exchange-rate band. Defense of the lower limit of the band became necessaryin late 1996 and in the first half and the last few days of 1997, when all sectorsof the economy sold forex that the central bank had to buy in order to preventthe exchange rate from slipping under the bottom of the band. After the middleof 1997, the private sector exhibited greater demand for forex and absorbed theescalating supply provided by nonresidents without central-bank intervention(except for several days at the end of that year).

The depreciation trend that persisted until the middle of 1998 was mainlythe result of the positive-slope exchange-rate band policy that forced the Bankof Israel, during some of that time, to absorb rather large quantities of foreigncurrency that reached the market. Since then, the exchange rate has been volatilein both directions and has shown no consistent trend, due to equilibrium amongmarket forces with no need for central-bank intervention. The transition fromde facto managed depreciation to a floating exchange rate shows how muchprogress the market has made due to the aforementioned processes and economicpolicies. If similar policies and international standards are applied in the future,market efficiency will continue to improve and the exchange rate will be setwith no need for intervention in trading.

100

BANK OF ISRAEL, CONTROLLER OF FOREIGN EXCHANGE, ANNUAL REPORT 2001