Embed Size (px)

Citation preview

Activity Based Costing ProjectActivity Based Costing Project 2003 - 2005 2003 - 2005

Executive SummaryExecutive Summary

Activity Based Costing ProjectActivity Based Costing Project 2003 - 2005 2003 - 2005

Executive SummaryExecutive Summary

USQ Student Enrolments 2004

USQ Delivery Channels

On CampusIndividualDistributed

Learning Centres

Standard DE Off Shore

Primarily Online On ShoreWide Bay SpringfieldToowoomba

IndividualOff Campus

Channel

On CampusChannel

Distributed Learning Centre

Channel

50% 4% 3% 23% 0% 17% 3%

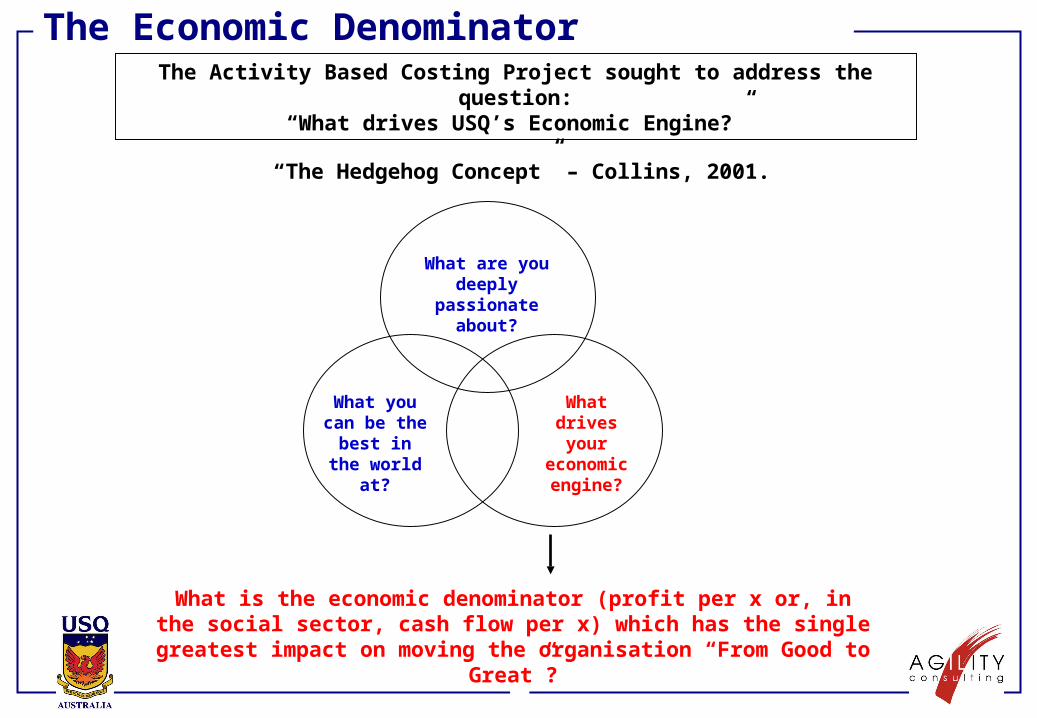

The Economic DenominatorThe Activity Based Costing Project sought to address the question:

“What drives USQ’s Economic Engine?”

What are you deeply passionate

about?

What you can be the best in the world at?

What is the economic denominator (profit per x or, in the social sector, cash flow per x) which has the single greatest impact on moving the organisation

“From Good to Great”?

What drives your

economic engine?

“The Hedgehog Concept” – Collins, 2001.

MethodologyABC attempts to link the inputs of the University (people, premises, technology and consumables) with the outputs teaching courses and programs and research. A typical cost architecture and model data sources are shown below.

FacultiesFaculties

RESOURCES ACTIVITIES COST OBJECTS

AcademicSupport

AcademicSupport

AdministrationSupport

AdministrationSupport

MarketingMarketing

Research SupportResearch Support

SupportingStudent

SupportingStudent

ResearchingResearching

Enrolling StudentsEnrolling Students

Providing LibraryServices

Providing LibraryServices

ACC 1100ACC 1100

SCC1123SCC1123

Courses

B. BusB. Bus

B. ScB. Sc

B. ArtsB. Arts

M. BusM. Bus

M. ScM. Sc

M. IBM. IB

Programs

Research

InternationalOnshore

InternationalOnshore

InternationalOffshore

InternationalOffshore

DomesticHECS

DomesticHECS

DomesticFee PayingDomestic

Fee Paying

Students

LibraryLibrary

Finance, IT, HRFinance, IT, HR

Providing CorporateServices

Providing CorporateServices

Liaising with Students

Liaising with Students

TimeSurveys

Floorspace / Timetabling

Systems

GrantsGrants

PublicationsPublications

HRD CompletionsHRD Completions

BusinessSustainingBusiness

Sustaining

Leadership

Govern

Strategy

Compliance

FinancialSystems

PayrollSystem

FacilitiesFacilities

Preparing Lectures

Delivering Lectures

Assessing Students

Preparing Lectures

Delivering Lectures

Assessing Students

Preparing Lectures

Delivering Lectures

Assessing Students

Preparing Lectures

Delivering Lectures

Assessing Students

Preparing LecturesPreparing Lectures

Delivering LecturesDelivering Lectures

Assessing StudentsAssessing Students

StudentRecordsSystem

TimetablingSystem

Delivery Modes

Model Demonstration Resource Costs are assigned to Activities based on statistical drivers. The cost of Academic Salaries, for example, is assigned to activities based on Salary Weighted Time Survey results as shown below.

The USQ cumulative “Course Contribution Cliff” is shown below. The courses on the left are the most profitable with the courses on the right being the least profitable.

0

5

10

15

20

25

30

$M

537 Courses 528 Courses

$10M in value is eroded by 200 courses

$10M in value is eroded by 200 courses

2003 Results: Course Contribution Cliff

The contribution from teaching from each of the Faculties is shown below. The size of the bubble represents the number of enrolments. Faculties below the x-axis are providing a negative contribution.

2003 Results by Faculty

Key:

2,000 20,000Enrolments Enrolments

Key:

2,000 20,000Enrolments Enrolments

-2

0

2

4

6

8

0 10 20 30 40

Revenue ($M)

Co

ntr

ibu

tio

n (

$M) Faculty of Arts

Faculty of Business

Faculty of Education

Faculty of Engineering andSurveying

Faculty of Sciences

Contribution Margin = 15%

The contribution from teaching from each of the modes is shown below. The size of the Bubble represents the number of enrolments. Modes below the x-axis are providing a negative contribution.

2003 Results by Delivery Mode

Key:

2,000 20,000Enrolments Enrolments

Key:

2,000 20,000Enrolments Enrolments

-8

-4

0

4

8

12

(20) 0 20 40 60

Revenue ($M)

Co

ntr

ibu

tio

n (

$M)

Educational Partners - Off Shore

Educational Partners - On Shore

Off Campus - On-Line

Off Campus - Standard

On Campus - Toowoomba

On Campus - Wide Bay

Contribution Margin = 15%

(500)

(400)

(300)

(200)

(100)

0

100

200

300

400

(500) 0 500 1,000 1,500 2,000 2,500 3,000

Bretten

Canterbury

Informatics - Malaysia

Informatics - Singapore

Kangda College

SALO

Segi Group

STI - Shanghai

STI - Taiwan

ZUCC

Other

Educational partner results are shown below. The size of the bubble represents the number of enrolments. Partners below the x-axis are providing a negative contribution.

Revenue ($000)

Co

ntr

ibu

tio

n (

$000

)

20%

10%

(10%)

(20%)(30%)

Target Contribution Margin - 15%

Break Even

(40%)

45Partners Key:

250 2000Enrolments Enrolments

Key:

250 2000Enrolments Enrolments

2003 Results by Educational Partner

Note: Construction of this level of detail from the ABC Model result requires further analysis outside of the model.

Note: Construction of this level of detail from the ABC Model result requires further analysis outside of the model.

Performance Management

The EconomicDenominator

The EconomicDenominator

DepartmentContribution

DepartmentContribution

CourseLevel

Management

CourseLevel

Management

For USQ the economic denominator is the“Course Contribution Margin”

Course contribution targets will be set for each Faculty/ Department

A framework is being developed to address possiblecourse /program rationalization

EducationalPartners

EducationalPartners USQ has changed its Learning Management System

for online delivery and is now investigating an open source/open standards based approach

Performance Management (cont’d)

An Educational Partner Model is being developed addressing such issues as:

• Pricing model;• Standard Contract; and• “Partner non-performance” escape clauses

The University is in the process of setting targets for all output groups (Teaching, Research, Commercial, Community, etc).

University ExampleTotal Revenue $130M

Revenue from Teaching $110M

Return @ 5% = Net Profit $6M

Add: Investment in Research $10M

Add: Strategic Projects $8M

Required Contribution From Teaching $24M

Baseline Teaching Margin = 22% (24/110 100)

Course contribution is the Economic Denominator. Well structured programs with a reasonable sized student cohort deliver a 30% - 40% Contribution Margin

The Economic Denominator

With course contribution as the economic denominator, USQ is committed to reducing the number of courses which provide a negative contribution, thus “Trimming the Tail off the Whale”.

0

5

10

15

20

25

30

$M

537 Courses 528 Courses

The Economic Denominator

Model Utilisation and Enhancement

•The Activity Based Costing Model is a journey, not a destination

•Current enhancements include: Calculating program contribution; Deployment of model reporting and analysis; Data collection of time surveys online

•Data is to be refreshed annually

•The use of the ABC Model for budgetary allocation purposes is via the Budget Management Committee, which is chaired by the VC