Embed Size (px)

Citation preview

Activist Investing:Impact on M&A February 2015

ACTIVIST INVESTING: IMPACT ON M&A Presented by The Deal in partnership with Toppan Vite CHANGE YOUR EXPERIENCE OF FINANCIAL PRINTING

“Some estimate that a company a week announces a sale as a result of activist

pressure,” said Gregg Feinstein, managing director of Houlihan Lokey and head of

the investment bank’s M&A group and activism practice.

A few activist investors, including Carl Icahn, Bill Ackman and Daniel Loeb, have

become bold-faced names in the business world. Their firms are training huge

financial arsenals on big-time targets like DuPont and EMC Corp. In early February,

Office Depot agreed to a merger with Staples, another ongoing effort by hedge

funds to pressure mergers or spin offs.

That pressure, as headlines attest, can yield results. Family Dollar Stores Inc.

shareholders voted Jan. 22 to merge with Dollar Tree Inc., the result of Icahn’s

successful prodding.

Other activists are pushing lesser-known companies, with market caps of

$500 million or less, to sell to better-heeled competitors.

In 2013, for example, Valeant Pharmaceuticals International Inc. paid $344 million

for Abaji Medical Products Inc. and $250 million for Solta Medical Inc. Activist

shareholders prodded both targets to sell.

Boards and management may also seek a sale on their own, preferring a buyer over

going through a bruising proxy battle they believe they would lose. Sometimes, the

Armed with more than $100 billion in capital and a tenacity to match, activist money managers have become an investment juggernaut. Their impact is indisputable. Their shareholder-value drumbeat has become a constant on Wall Street.That influence extends into the arena of mergers and

acquisitions. In ways both obvious and not, activist

hedge funds are forcing companies to put themselves

on the market, divest, spin off and split up.

2

ACTIVIST INVESTING: IMPACT ON M&A Presented by The Deal in partnership with Toppan Vite CHANGE YOUR EXPERIENCE OF FINANCIAL PRINTING

public isn’t even aware that a battle has ensued.

“Only about one out of four times when an activist goes and talks to a company is

there ever an announcement,” Feinstein said. “So you’ll see a split up of a company,

for example, and you hadn’t heard there was an activist involved behind the

scenes.”

Just how much M&A activity is attributable to activism is a matter of conjecture.

Some in the field suggested more than 25% of total deals are the result of activist

pressure, directly or indirectly.

Others said they believe the absolute numbers of activist-prodded deals are a

relatively small percentage of total M&A, but the dollar value is large, as some of the

biggest deals of the past two years have been driven by activists.

“The activist universe is just not big enough for us to be contributing to a major

amount of M&A,” said Glenn Welling, who heads activist hedge fund Engaged

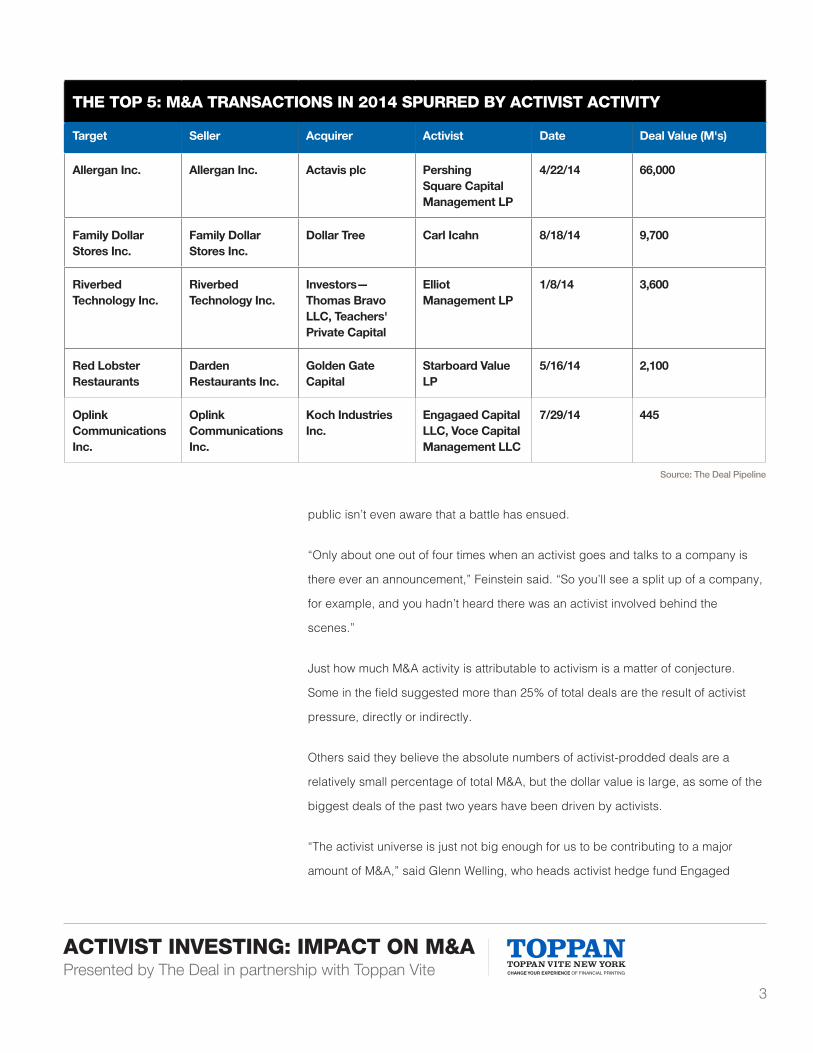

THE TOP 5: M&A TRANSACTIONS IN 2014 SPURRED BY ACTIVIST ACTIVITY

Target Seller Acquirer Activist Date Deal Value (M's)

Allergan Inc. Allergan Inc. Actavis plc Pershing Square Capital Management LP

4/22/14 66,000

Family Dollar Stores Inc.

Family Dollar Stores Inc.

Dollar Tree Carl Icahn 8/18/14 9,700

Riverbed Technology Inc.

Riverbed Technology Inc.

Investors—Thomas Bravo LLC, Teachers' Private Capital

Elliot Management LP

1/8/14 3,600

Red Lobster Restaurants

Darden Restaurants Inc.

Golden Gate Capital

Starboard Value LP

5/16/14 2,100

Oplink Communications Inc.

Oplink Communications Inc.

Koch Industries Inc.

Engagaed Capital LLC, Voce Capital Management LLC

7/29/14 445

Source: The Deal Pipeline

3

ACTIVIST INVESTING: IMPACT ON M&A Presented by The Deal in partnership with Toppan Vite CHANGE YOUR EXPERIENCE OF FINANCIAL PRINTING

Capital LLC. But “if you look across most of the successful activists’ books, over the

last few years we’ve all had situations that resulted in transactions.”

This much is known: More institutional investors are pouring ever-bigger amounts of

money into activist investing and that, at the very least, helps prime a surge in M&A

activity. According to Hedge Fund Research Inc., activist hedge funds held $120

billion at the end of 2014. That war chest almost doubled in two years and is nearly

four times the amount held by activist hedge funds at the end of 2008, according to

Hedge Fund Research data.

The five largest activist hedge funds hold about 40% of that total, according to a

report last year by the research firm Preqin. Elliott International and Cevian Capital

top that list.

Activism has gone mainstream. Institutional investors now include the likes of

California State Teachers Retirement System, also known as CalSTRS. “It used to

be somewhat considered a black art,” said J. Daniel Plants, who heads activist

hedge fund Voce Capital Management LLC. “There’s clearly been an awakening, a

recognition that these strategies get results.”

Even their total assets under management, as rapidly rising as they are, may

undervalue what activists can achieve through pressuring boards and management

to divest and sell. “Their collective impact is much greater than their assets would

indicate,” said investment managers at the Fiduciary Group in a position paper late

last year.

The activist’s playbook is fairly straightforward: Build up a stake in a publicly traded

company, often one with management and board deficiencies and a stock price

that lags its competitors, and then demand responses that can unlock value for the

shareholders. That proposed action includes everything from cost cutting to cash

dividends. A sale of part of the company itself is definitely part of the mix.

Activism “is a growth vehicle for M&A, and it takes on many forms,” said Steve

Wolosky, who chairs the activist and equity investment practice at New York law firm

Olshan Frome Wolosky LLP. “It’s a major catalyst for M&A.”

“Only about one out

of four times when an

activist goes and talks

to a company is there

ever an announcement.”

Gregg Feinstein, managing director of Houlihan Lokey and head of the investment bank’s M&A group and activism practice

4

ACTIVIST INVESTING: IMPACT ON M&A Presented by The Deal in partnership with Toppan Vite CHANGE YOUR EXPERIENCE OF FINANCIAL PRINTING

All signs point to continued activist-prompted deals.

“The age of activism is in the early innings,” Feinstein said. “Activism is here to

stay as a tool for shareholders to express their views more frequently and through

different venues. The assets in activist hedge funds have gone up so much, the

capital will be deployed over time.”

As activists gain traction, a new cadre of legal and financial advisers has joined

in the fray. They are assisting activist investors with strategies and with leads on

potential corporate acquirers. And they are counseling corporate targets in this new

age of shareholder activism with different advice than before. Unlike in years past,

when advisers girded their clients for lengthy sieges, the message now is, whenever

possible, to avoid long and costly activist battles.

“The advisers of today are saying, ‘Look, engage in the activists, listen to the

activists. These expensive fights take you away from running your business, it

distracts you, it consumes company resources and the risk of alienating investors is

simply not the way to go,’ ” said Paul Kessler, who heads Bristol Capital Advisors, a

Los Angeles-based activist hedge fund.

There are two important caveats about activism and the deal environment. First,

activists are usually on only one side of the M&A ledger. They are focused on the

sale of companies and divisions; they rarely advocate acquisitions.

“In terms of being buyers for companies, [activist-led deals] are few and far

between,” Wolosky said, although he hastened to add that may change in the years

ahead, something he termed “the public side of private equity.” Others added that

activist hedge funds may begin to team up with corporations for hostile takeovers,

something Ackman, for one, has toyed with.

Secondly, activism may contribute to a robust M&A market, but it doesn’t necessarily

lead. Rather, it follows. 2014 was a banner M&A year, the biggest in more than a

decade. Activists generated some of those deals. However, the basic ingredients

for that robust deal environment are low interest rates, flush corporate coffers and

booming stock markets. Activists take advantage of these elements; they don’t

“The advisers of today

are saying, ‘Look,

engage in the activists,

listen to the activists.

These expensive fights

take you away from

running your business,

it distracts you, it

consumes company

resources and the risk

of alienating investors

is simply not the way

to go.’ ”

Paul Kessler, Bristol Capital Advisors

5

ACTIVIST INVESTING: IMPACT ON M&A Presented by The Deal in partnership with Toppan Vite CHANGE YOUR EXPERIENCE OF FINANCIAL PRINTING

create them.

Not all activist pressure results in company break ups, either. Take, for example,

the highly publicized, 18 month battle between Peltz and PepsiCo. Nelson Peltz has

demanded that PepsiCo spin off its snack division.

In mid-January, however, PepsiCo announced that William Johnson, the former CEO

of H.J. Heinz Co. and an adviser to Peltz’s Trian Capital, would, in March, become

an independent director. In the announcement, Peltz was quoted as saying that he

supports Pepsi CEO Indra Nooyi’s “commitment to operational excellence,” a signal

that the breakup fight may be over, at least for now.

Private equity may be a huge force when it comes to the M&A market in general,

but to date, at least, these financial sponsors are rarely in on activist-spurred deals.

There are good reasons why: Strategic acquirers can afford to pay more because

these deals can create cost-saving synergies for them.

There are also instances of unintended consequences. One of the most talked of

examples of recent activist-led M&A involved the $2.1 billion sale in July 2014 by

Darden Restaurants Inc. of its Red Lobster chain to private equity firm Golden Gate

Capital. Activist investors led by Starboard Value and Barington Capital Group

had pushed hard for Darden to spin off Red Lobster, Olive Garden and LongHorn

Steakhouse, while retaining other brands and splitting off real estate assets into a

separate company. Instead, the Darden board agreed to a management plan

that, without shareholder approval, sold Red Lobster with its real estate attached.

Golden Gate Capital immediately sold off that real estate for $1.5 billion to American

Realty Capital Properties Inc. in a sale-leaseback, gaining the restaurant chain for

just $600 million.

Infuriated, Starboard Value and smaller hedge fund Barington Capital Group

mounted a successful proxy campaign to throw out the entire Darden board. CEO

and chairman Clarence Otis lost his job in the process.

“It was a game changer,” Kessler said of the bruising battle, although one of the

hedge fund advisers admitted that in the case of Darden, the pressure backfired.

“The activist has been

the instigator in a sense

to show where the

value really lies. And

once that’s shown to

the public, and more

importantly to the other

players in a specific

sector, M&A seems

to be a likely follow

through.”

Paul Kessler, Bristol Capital Advisors

6

ACTIVIST INVESTING: IMPACT ON M&A Presented by The Deal in partnership with Toppan Vite CHANGE YOUR EXPERIENCE OF FINANCIAL PRINTING

Setbacks and limitations aside, activists have demonstrated enormous strength and

perseverance when it comes to compelling a corporate sale.

“The activist has been the instigator in a sense to show where the value really lies,”

Kessler said. “And once that’s shown to the public, and more importantly to the

other players in a specific sector, M&A seems to be a likely follow through.”

Some recent deals combine many of those elements. Take the case of Oplink

Communications Inc. That publicly traded optical components manufacturer had a

strong cash flow and plenty of cash. However, the Fremont, Calif.-based company

formed a new venture called Oplink Connected, a plug-and-play home security

system that management said it hoped would compete with Google Nest. Instead,

Oplink Connected lost money and drained capital.

Activist funds Voce Capital and Engaged Capital targeted the company with

demands that Oplink shut down its connected security division and that the

company return cash to shareholders. After Oplink rebuffed both, the activists

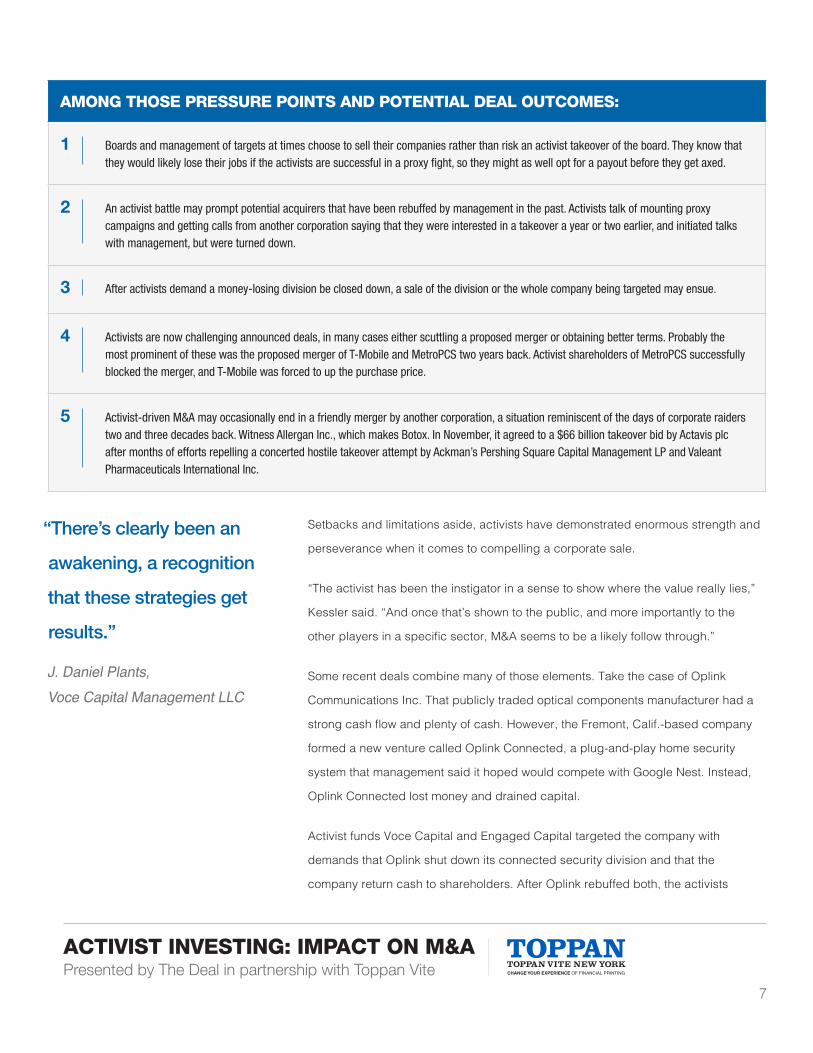

AMONG THOSE PRESSURE POINTS AND POTENTIAL DEAL OUTCOMES:

1 Boards and management of targets at times choose to sell their companies rather than risk an activist takeover of the board. They know that they would likely lose their jobs if the activists are successful in a proxy fight, so they might as well opt for a payout before they get axed.

2 An activist battle may prompt potential acquirers that have been rebuffed by management in the past. Activists talk of mounting proxy campaigns and getting calls from another corporation saying that they were interested in a takeover a year or two earlier, and initiated talks with management, but were turned down.

3 After activists demand a money-losing division be closed down, a sale of the division or the whole company being targeted may ensue.

4 Activists are now challenging announced deals, in many cases either scuttling a proposed merger or obtaining better terms. Probably the most prominent of these was the proposed merger of T-Mobile and MetroPCS two years back. Activist shareholders of MetroPCS successfully blocked the merger, and T-Mobile was forced to up the purchase price.

5 Activist-driven M&A may occasionally end in a friendly merger by another corporation, a situation reminiscent of the days of corporate raiders two and three decades back. Witness Allergan Inc., which makes Botox. In November, it agreed to a $66 billion takeover bid by Actavis plc after months of efforts repelling a concerted hostile takeover attempt by Ackman’s Pershing Square Capital Management LP and Valeant Pharmaceuticals International Inc.

“There’s clearly been an

awakening, a recognition

that these strategies get

results.”

J. Daniel Plants, Voce Capital Management LLC

7

ACTIVIST INVESTING: IMPACT ON M&A Presented by The Deal in partnership with Toppan Vite CHANGE YOUR EXPERIENCE OF FINANCIAL PRINTING

mounted a proxy battle. Three months later, a subsidiary of Koch Industries

announced it would acquire Oplink for $445 million in cash, a 14% premium over the

last trade, but almost 50% higher than when the hedge funds began building their

stakes.

It’s a great outcome for everyone,” Plants said. “They made a rational calculation.

They’d rather sell the company than have the ‘barbarians at the gate’ and have to sit

around the table with us. This is the third time our portfolio companies have made

the decision to sell under similar circumstances, and that’s fine with us.”

The activist-related M&A activity often belies common perception that activist hedge

funds are only interested in short-term gain. A study by Preqin last year indicated

that activists keep shares longer than other hedge funds do. According to Welling,

an activist campaign takes anywhere from two to four years. Not only must the

hedge fund itself persevere, but its limited partners must buy into what Welling calls

“patient capital.”

In addition, if activists actually do get on the board, they can’t trade stock in the

company they’re trying to help.

That combination of fortitude and patience may actually serve to limit activist-led

deals in the years ahead.

“Activism on the cheap, noncommittal activism isn’t going to be able to continue

to get results in a way that really effectuates change,” Plants added. “Very few

investors have the skills and the wherewithal to go all the way with a proxy contest,

particularly if it involves the investor joining the board.”

So saying, activist hedge fund managers see more deals in the months and years

ahead.

“In terms of activists still pushing for sales, divestitures and pieces of businesses,

and for boards saying, ‘This is a better solution for us than being thrown out at an

annual meeting,’ I just look at our portfolio of businesses, and I see no shortage of

opportunities over the next two or three years,” Welling concluded. n

“In terms of activists

still pushing for sales,

divestitures and pieces

of businesses,

and for boards saying,

‘This is a better solution

for us than being

thrown out at an

annual meeting,’ I just

look at our portfolio of

businesses, and I see

no shortage of

opportunities over the

next two or three years.”

Glenn Welling, Engaged Capital LLC

8

ACTIVIST INVESTING: IMPACT ON M&A Presented by The Deal in partnership with Toppan Vite

Toppan Vite, a leader in financial printing, is part of the Toppan

Printing Group, the world’s largest printing group, headquartered

in Tokyo with approximately US$18 billion in annual sales.

Our expanding U.S. operations deliver a hassle-free experience

for mission-critical content for capital markets transactions,

financial reporting and regulatory compliance filings, investment

companies and insurance providers.

Toppan Vite has been a pioneer and trusted partner in the

financial markets for three decades, serving the financial, legal

and corporate communities with meticulous, responsive service

and unparalleled local market expertise and capabilities.

Contact: Sarah Reilly, Marketing Manager

Office: (201) 518-9715

Email: [email protected]

Customer Service: [email protected]

Website: toppanvite.com/us

Connect: LinkedinBlogTwitter

CHANGE YOUR EXPERIENCE OF FINANCIAL PRINTING

9

OF FINANCIAL PRINTINGCHANGE YOUR EXPERIENCE

Hassle-FreeSpeed to MarketAny Deal, Any Size

us.toppanvite.com

New York I New Jersey I London I Hong Kong I Singapore I Tokyo

Telephone : 212.596.7747 Email : [email protected] head.