Embed Size (px)

Citation preview

ACN 1 4 6 0 3 5 6 9 0

2 0 1 5 A N N U A L R E P O R T

For the year ended 30 June 2015

For

per

sona

l use

onl

y

1

C O R P O R A T E D I R E C T O R Y

DIRECTORS Executive Chairman Dato Soo Kok Lim Executive Director Datuk Siew Swan Ong Chief Executive Officer/Director Mr Brent Butler Non-Executive Director Mr Raymond Browning Non-Executive Director Mr Andrew Kwa PRINCIPAL PLACE OF BUSINESS AND REGISTERED OFFICE Level 1, Office F 1139 Hay Street WEST PERTH WA 6005 Telephone: (61 8) 9321 0715 Facsimile: (61 8) 9321 0721 Email: [email protected] Website: www.audalia.com.au SHARE REGISTRY Advanced Share Registry Limited 110 Stirling Highway NEDLANDS WA 6009 PO Box 1156 NEDLANDS WA 6909 Telephone: (61 8) 9389 8033 Facsimile: (61 8) 9262 3723 AUDITOR BDO Audit (WA) Pty Ltd 38 Station Street SUBIACO WA 6008

COMPANY SECRETARY Ms Karen Logan STOCK EXCHANGE ASX Limited Level 40, Central Park 152-158 St George’s Terrace Perth WA 6000 ASX Code: ACP BANKER National Australia Bank 1/1238 Hay Street WEST PERTH WA 6005

For

per

sona

l use

onl

y

2

C O N T E N T S

PAGE

Corporate Directory 1

Review of Activities 3

Directors' Report 7

Financial Report 19

Directors’ Declaration 44

Independent Auditor’s Report 45

Auditor’s Independence Declaration 47

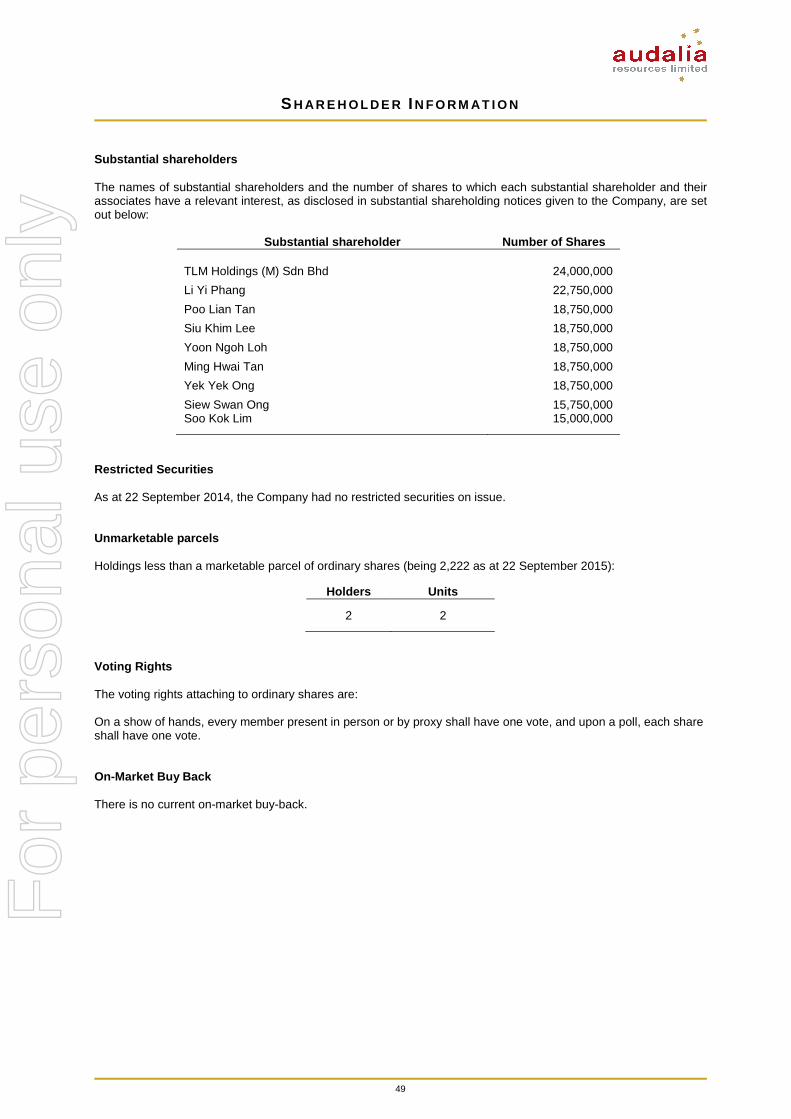

Shareholder Information 48

Summary of Tenements 50

For

per

sona

l use

onl

y

3

R E V I E W O F A C T I V I T I E S

Audalia Resources Limited (ASX: ACP) is pleased to present its annual report for the year ended 30 June 2015 to shareholders and provide some insight into the advancement the Company has made in its activities to date and progress that it expects to make going forward. OVERVIEW MEDCALF PROJECT The Medcalf Project is located 470km east-southeast of Perth. The Medcalf Project comprises five exploration licences and eight prospecting licences, with a total area covering approximately 25 km2. An application for a mining lease covering 80% of the area of the granted licences is pending. The Medcalf Project lies in the southern end of the Archaean Lake Johnston greenstone belt. This greenstone belt is a narrow, north-northwest trending belt approximately 110km in length. It is located near the south margin of the Yilgarn Craton, midway between the southern ends of the Norseman-Wiluna and the Forrestania-Southern Cross greenstone belts (see Figure 1). Previous work carried out by numerous holders of the tenements over the last 40 years includes exploration for nickel, titanium/vanadium, platinum group metals (PGM) and gold. The primary vandiferous titanomagnetite mineralisation occurs within the pyroxenite zone between the basal peridotite and upper gabbro zones of the sill. The lateritic weathering of this sill has removed much of the silica, calcium and magnesium in solution thus resulting in residual concentrations of iron, titanium and vanadium oxides. This secondary enrichment potentially hosts economic ore.

Figure 1: Medcalf Project location map Activities conducted during the year During the 2015 financial year, the Company continued to undertake metallurgical test works to determine the likely processing method and recoveries for the project. With the engagement of a South African consulting group known to have expertise in vanadium, significant improvements in vanadium recovery were achieved, including metallurgical recovery of 62%. Subsequently, further test work on 50kg run of mine composite sample of ore was commission and completed in a specialised metallurgical laboratory in Germany to independently confirm test work completed in South Africa. The outcome of the test work in Germany confirmed results achieved in South Africa.

For

per

sona

l use

onl

y

4

R E V I E W O F A C T I V I T I E S

The metallurgical South African Phase 1 and 2 test work results returned encouraging vanadium recoveries that could support the potential for a viable mining operation for the Medcalf Project, and underpins Audalia’s intention to continue development work and undertake a comprehensive prefeasibility study (PFS). On 18 August 2014, the Company announced a significant upgrade in the JORC 2012 resource classification for its Medcalf Project, with 72% of the vanadium deposit now reporting to the higher Indicated category as follows:

• Indicated Resources of 23.0Mt at 0.47% V2O5 • Inferred Resources of 8.8Mt at 0.40% V2O5 • for a total resource of 31.8Mt at 0.45% V2O5.

Figure 2: Geological map of the Medcalf deposit wit h drill collars and resource outline This compares to the maiden Inferred Resource of 28.5 Mt at 0.50% V2O5 announced in 2013. This new resource equates to contained vanadium pentoxide contents of approximately 108,000 tonnes in the Indicated category and 35,000 tonnes in the Inferred category. During the December 2014 quarter, an Engineering consultant was engaged to complete a review of all test work completed to date and make recommendations as to the next phase of test work. The Company supported in favour of a bench scale metallurgical test work programme in the June 2015 quarter which established a base line to commence work in developing a preliminary flow sheet to drive process development and design. The results of this work will be incorporated into the PFS study that has now commenced. Concurrently with the study, Audalia commenced work in other areas with assessing haul road access, water and power logistics. Following engagement with various stakeholders, the Company withdrew its application for miscellaneous licence L63/68 and investigated alternative options for haul road access from the Medcalf Project site. A drill core programme was designed to extract further samples for the metallurgical test work in order to define the metallurgical characteristics of the ore body to a PFS standard and confirm the optimal process flow sheets. The programme of works for the drill core programme was granted subsequent to balance date.

For

per

sona

l use

onl

y

5

R E V I E W O F A C T I V I T I E S

During the year, Audalia the Company completed the following flora and fauna surveys:

1. Level 1 spring season flora and fauna survey for the proposed haul road (ML63/68); 2. Level 2 spring and autumn season flora surveys over the mining lease application M63/656 3. Spring and autumn season targeted searches up to a 20km radius from Medcalf for flora of conservation

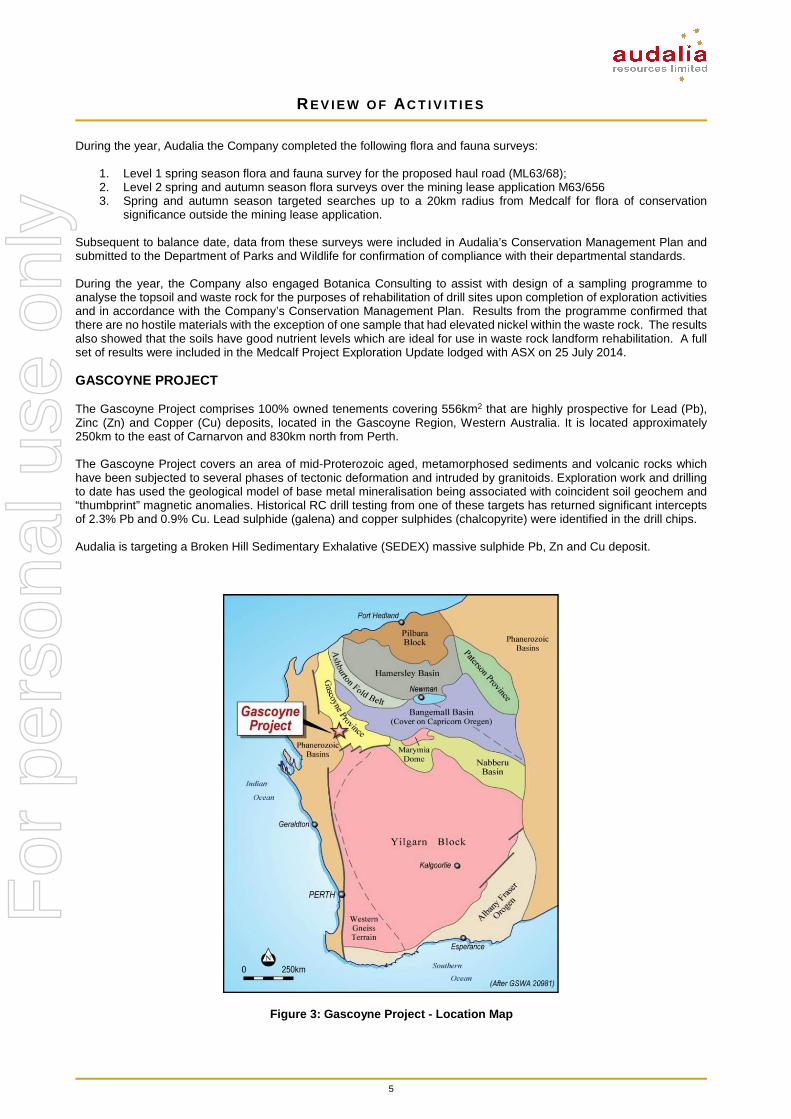

significance outside the mining lease application. Subsequent to balance date, data from these surveys were included in Audalia’s Conservation Management Plan and submitted to the Department of Parks and Wildlife for confirmation of compliance with their departmental standards. During the year, the Company also engaged Botanica Consulting to assist with design of a sampling programme to analyse the topsoil and waste rock for the purposes of rehabilitation of drill sites upon completion of exploration activities and in accordance with the Company’s Conservation Management Plan. Results from the programme confirmed that there are no hostile materials with the exception of one sample that had elevated nickel within the waste rock. The results also showed that the soils have good nutrient levels which are ideal for use in waste rock landform rehabilitation. A full set of results were included in the Medcalf Project Exploration Update lodged with ASX on 25 July 2014. GASCOYNE PROJECT The Gascoyne Project comprises 100% owned tenements covering 556km2 that are highly prospective for Lead (Pb), Zinc (Zn) and Copper (Cu) deposits, located in the Gascoyne Region, Western Australia. It is located approximately 250km to the east of Carnarvon and 830km north from Perth. The Gascoyne Project covers an area of mid-Proterozoic aged, metamorphosed sediments and volcanic rocks which have been subjected to several phases of tectonic deformation and intruded by granitoids. Exploration work and drilling to date has used the geological model of base metal mineralisation being associated with coincident soil geochem and “thumbprint” magnetic anomalies. Historical RC drill testing from one of these targets has returned significant intercepts of 2.3% Pb and 0.9% Cu. Lead sulphide (galena) and copper sulphides (chalcopyrite) were identified in the drill chips. Audalia is targeting a Broken Hill Sedimentary Exhalative (SEDEX) massive sulphide Pb, Zn and Cu deposit.

Figure 3: Gascoyne Project - Location Map

For

per

sona

l use

onl

y

6

R E V I E W O F A C T I V I T I E S

Activities conducted during the year A reconnaissance rockchip and trap-site stream sediment sampling program was carried out in August 2014 over all the tenements. Sixteen minus 80 mesh follow-up stream sediment samples were collected from two catchments to more closely define the source of the lead anomalies generated from the previous field programme during June 2014. Best result obtained was 171ppm lead. Six minus 3mm trap-site 2kg trap-site stream sediment samples were collected over a previous gold anomaly. Best result obtained was 4.63ppb gold. Sixty two rockchip samples were collected mostly from ironstones or ironstone quartz veins from Banded Iron Formations (BIFs) that have been mapped and traced along a total strike length of 25km and outcrop over a north-south distance of 30km and an east-west distance of 19km. A full listing of results were included in the Gascoyne Project Exploration Update lodged with ASX on 16 September 2014. In October and November 2014, the Company carried out a reconnaissance rockchip sampling programme and aeromagnetic/radiometric survey over all the tenements. The exploration results were released to ASX on 28 January 2015. The results indicated further work is warranted on the BIF particularly around rockchip CW978 that has elevated copper, lead, zinc and manganese values. Future work at the Gascoyne Project should include diamond drilling in order to understand the stratigraphy and mineralisation at depth. In June 2014, the Company submitted an application for exploration licence E09/2102 covering 70 graticular blocks that adjoin the existing Gascoyne Project tenements. After entering into a heritage agreement with the Gnulli People on 14 July 2015, the application was granted by the Department of Mines and Petroleum on 15 July 2015. Audalia now has contiguous tenements that increased the prospective ground area from 337km2 to 556km2. The Gascoyne Project remains prospective for targeting a Broken Hill Sedimentary Exhalative (SEDEX) massive sulphide, Pb, Zn and Cu deposit. CORPORATE The Company secured short term loan of $700,000 in August 2014 for the purpose of supplementing its existing working capital. Given the short term nature of the loan, the Company entered into subscription agreements with sophisticated investors in September 2014 to raise $1.5 million by way of placement (Placement ). The Placement was completed in two tranches, $750,000 in November 2014 and $750,000 in February 2015. The short-term loan of $700,000 was repaid in March 2015. Subsequent to completion of the Placement, the Company successfully secured a loan of $4,000,000 in March 2015 to commence a pre-feasibility study on its flagship Medcalf Project. Audalia appointed Mr Brent Butler as Chief Executive Officer (CEO) of the Company with effect from 14 April 2015. Mr Butler has served as a non-executive director of Audalia since before the Company’s admission to the official list of ASX in July 2011. Mr Butler also continues to serve as a director of Audalia. GOVERNANCE The Board of Directors is responsible for the operational and financial performance of the Company, including its corporate governance. The Company believes that the adoption of good corporate governance adds value to stakeholders and enhances investor confidence. Audalia’s corporate governance statement is available on the Company’s website, in a section titled ‘Corporate Governance’: www.audalia.com.au/corporate/corporate-governance/. Competent Person’s Statement The information in this report that relates to Exploration Results is based on information compiled by Mr Brent Butler, who is a member of the Australasian Institute of Mining and Metallurgy. Mr Butler is a consultant geologist with 31 years’ experience as a geologist. Mr Butler has sufficient experience which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2012 edition of the ‘Australasian Code for Reporting of Exploration results, Mineral Resources and Ore Reserves’ (JORC Code). Mr Butler consents to the inclusion in the report of the matters based on his information in the form and context in which it appears.

For

per

sona

l use

onl

y

7

D I R E C T O R S ’ R E P O R T

The Directors present their report together with the financial statements of Audalia Resources Limited (the Company) for the year ended 30 June 2015. DIRECTORS The Directors of the Company at any time during or since the end of the financial year are: Dato Soo Kok Lim Executive Chairman – Age 46, appointed: 9 October 2010 Dato Lim is a graduate in Law with Honours from The University of Kent in Canterbury, England in 1989. In 1990, he obtained the degree of Utter Barrister Gray’s Inn, England. He was called to the Bar in Malaysia in 1991. After a brief career in a local law firm in Kuala Lumpur, he established his own practice in 1993 and operated it until 1999. He was appointed a Commissioner for Oaths by the Chief Justice of Malaysia in 1999. Dato Lim is also a Notary Public appointed by the Attorney General of Malaysia. He is also currently a director of a number of companies listed on Bursa Malaysia (formerly known as the Kuala Lumpur Stock Exchange). Dato Lim is actively involved with the management of significant family investments in property development, hotel management and other commercial interests. He has substantial business and legal experience in investments in Malaysia, Australia, China and other South East Asian countries. Datuk Siew Swan Ong Executive Director – Age 43, appointed: 9 October 2010 Datuk Ong is an advocate & solicitor with more than 16 years of experience including managing his legal practice in Malaysia. He is a graduate in law from Bond University, Australia. He provides legal advice to a wide range of clients including clients in the mining industry in Malaysia and Indonesia. He has extensive knowledge of the mining industry in Malaysia having been involved as legal counsel in joint ventures and acquisition of mining transactions and dispute resolution between clients and State Governments. Datuk Ong has served as a director and company secretary on several companies in Malaysia and Hong Kong. Mr Brent Butler Chief Executive Officer and Director – Age 55, appointed: 16 February 2011 Mr Butler is a geologist with over 30 years’ experience in the resource industry. He has a geology degree from Otago University and is a member of the Australasian Institute of Mining and Metallurgy. Mr Butler is also a Fellow of the Society of Geology (USA) and a member of Prospectors Development of Canada. He is currently the President and CEO of Superior Mining International Corporation, Director of Redhill Resources Corp and Managing Director of its Australian subsidiary. He has significant international exploration and mining experience in the gold industry, having worked in the United States, Brazil, Chile, Argentina, Africa and Australia. Mr Raymond Browning Non-Executive Director – Age 44, appointed: 3 September 2015 Mr Browning is a qualified mechanical engineer with extensive operational and project experience in the mining industry. He spent 18 years as a specialist designer, supplier and installer of specialised underground mining equipment in the Southern African mining industry. Mr Browning progressed through the ranks to the position of Managing Director of the company following a successful acquisition and merger. During this time he gained extensive experience in business development and management, including international corporate governance. More recently, Mr Browning assisted in various specialist consulting roles with small and large Western Australian companies providing engineering and project management services. Mr Andrew Kwa Non-Executive Director – Age 63, appointed: 11 October 2011 Mr Kwa has a bachelor of Computer Science degree from Teesside University in the UK. He worked as a Systems Analyst and IT Consultant for several years both in Malaysia and in Australia. Mr Kwa has extensive financial and project management experience. He is currently a consultant in a substantial property development in Western Australia.

For

per

sona

l use

onl

y

8

D I R E C T O R S ’ R E P O R T

COMPANY SECRETARY Ms Karen Logan Appointed: 27 August 2010 Ms Logan is a Chartered Secretary with over 11 years’ experience in assisting small to medium capitalised ASX-listed and unlisted companies with compliance, governance, financial reporting, capital raising, merger and acquisition, and IPO matters. She is an Associate of the Institute of Chartered Secretaries and Administrators, a Fellow of the Financial Services Institute of Australasia and a Graduate Member of the Australian Institute of Company Directors. Ms Logan is presently the principal of a consulting firm and secretary of a number of ASX-listed companies, providing corporate and accounting services to those clients. DIRECTORSHIPS IN OTHER LISTED ENTITIES Directorships of other listed entities held by directors of the Company during the last 3 years immediately before the end of the financial year are as follows:

Period of directorship Director Company From To

Dato Soo Kok Lim Not Applicable - - Datuk Siew Swan Ong Not Applicable - - Mr Brent Butler Redhill Resources Corp.

Superior Mining International Corporation Siburan Resources Limited

2006 2011 2009

Present Present

21 August 2012 Mr Raymond Browning Not Applicable Mr Andrew Kwa Global Gold Holdings Ltd 2008 Present

DIRECTORS’ INTERESTS

The relevant interests of each director in the securities of the Company at the date of this report are as follows:

Director Shares Options

Dato Soo Kok Lim 16,140,000 - Datuk Siew Swan Ong 16,900,000 - Mr Brent Butler 530,000 (1) - Mr Raymond Browning (appointed 3 Sept 2015) - - Mr Andrew Kwa 250,000 -

(1) Mr Butler may be granted up to 4 million Shares upon the achievement of certain milestones. Any grant of the

shares will be subject to the Company obtaining all shareholder and regulatory approvals required. Refer to Note 17 for further details of this proposed share based payment.

DIRECTORS’ MEETINGS The number of directors’ meetings and the number of meetings attended by each of the directors of the Company during the financial year are:

Board Meetings Audit and Risk Committee Meetings

Nomination and Remuneration Committee Meetings

Director Held Attended Held Attended Held Attended

Dato Soo Kok Lim 13 13 2 2 N/A N/A Datuk Siew Swan Ong 13 13 N/A N/A 1 1 Mr Brent Butler 13 13 2 2 1 0 Mr Andrew Kwa 13 12 2 2 1 1

Committee membership As at the date of the report, the Company had a Nomination and Remuneration Committee and an Audit and Risk Committee of the Board of Directors.

For

per

sona

l use

onl

y

9

D I R E C T O R S ’ R E P O R T

Members acting on the committees of the Board during the financial year were:

Nomination and Remuneration Committee Audit and Risk Committee

Mr Brent Butler (Chairman) Mr Brent Butler (Chairman) Mr Andrew Kwa Mr Andrew Kwa Datuk Siew Swan Ong Dato Soo Kok Lim

PRINCIPAL ACTIVITY The principal activity of the Company during the financial year was mineral exploration. OPERATING AND FINANCIAL REVIEW Operating review Information regarding operating activities undertaken by the Company during the year is contained in the section entitled Review of Activities in this Annual Report. Financial review The Company incurred a loss of $1,022,458 after income tax for the financial year (2014: loss of $402,942). This net loss after tax included $ 269,317 of share based payment expenses recognised in equity and issued to the CEO. As at 30 June 2015, the Company had net assets of $3,659,919 (30 June 2014: $2,921,293), including cash and cash equivalents of $2,660,781 (30 June 2014: $350,396). During the year, Audalia raised $1.5 million by way of placement via two tranches, receiving $750,000 in November 2014 and $750,000 in February 2015. The Company also secured additional funding of $4 million in March 2015 by way of loan facilities. The Audit Report issued by the Company’s auditor, contains an “Emphasis of Matter” paragraph in relation to the Company’s ability to continue as a “going concern”. The Board of Directors considers it appropriate to prepare the Company’s 2015 Annual Report on a going concern basis as there are reasonable grounds to believe that the Company will be able to pay its debts as and when they become due and payable. These include the Company’s ability to modify expenditure outlays, if required. The directors also continue to consider opportunities to source further funding to supplement its existing working capital and fund its ongoing exploration work. Further details are set out in Note 1 to the Financial Statements. SIGNIFICANT CHANGES IN THE STATE OF AFFAIRS Significant changes in the state of affairs of the Company during the financial year were as follows:

� Contributed equity increased by $1,491,767 (from $4,093,968 to $5,585,735 after costs) as a result of share placements in November 2014 and February 2015. Details of changes in contributed equity are disclosed in Note 15(a) to the financial statements.

� Net cash received from the increase in contributed equity was used principally to repay the short-term working

capital loan of $700,000 and fund ongoing exploration work at the Company’s Medcalf and Gascoyne Projects.

� In March 2015, the Company successfully secured loan facilities totalling $4,000,000 to commence its pre-feasibility study on its flagship Medcalf Project. As at 30 June 2015, Audalia had drawn down on $3,000,000 of the facilities. Details of the loan facilities are disclosed in Note 14 to the financial statements.

There were no other significant changes in the state of affairs of the Company during the financial year. Total shares on issue at 30 June 2015 are 234,160,001. RESULTS The Company incurred a loss of $ 1,022,458 (2014: loss of $402,942) after income tax for the financial year.

For

per

sona

l use

onl

y

10

D I R E C T O R S ’ R E P O R T

LIKELY DEVELOPMENTS The Company will continue to pursue its principal activity of mineral exploration and continue to review and assess other acquisition and joint venture opportunities in the resource sector. Specifically, Audalia is seeking to advance the PFS at the flagship Medcalf Project. Planned exploration and activities The Company’s near term objectives include: Medcalf Project

o Sign a definitive agreement with the Ngadju People; o Advance work on haul road and logistics, water and power options for the project; o Complete PFS level metallurgical test work; o Complete the PFS; o Upgrade the Mineral Resource to the Ores Reserve category; o Complete metallurgical drill core programme; o Continue targeted searches for flora of conservation significance.

Gascoyne Project

o Complete sampling programme at the recently granted exploration licence E09/2102 to bring the level of geological understanding in line with the rest of the tenement package;

o Design and implement a drill programme. MINERAL RESOURCES STATEMENT The Company has a 100% equity interest in mineral resource estimate at its Medcalf Project, which is located 470km east of Perth. At 30 June 2015, the Medcalf Project’s mineral resource estimate stood at 31.8 Mt at 0.45% V2O5 for contained vanadium pentoxide contents of approximately 108,000 tonnes in the Indicated category and 35,000 tonnes in the Inferred category. This mineral resource estimate was prepared in accordance with the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves 2012 Edition (JORC 2012). The Company announced a significant upgrade in the JORC 2012 resource classification for its Medcalf Project to the market on 18 August 2014. This upgrade followed revision of the geological and mineralisation modelling in conjunction with updated and ongoing metallurgical extraction testwork. This compares to the maiden Inferred Resource of 28.5 Mt at 0.50% V2O5 for 142,862 tonnes contained vanadium pentoxide as announced in 2013 and included in the 2014 Annual Report. The ‘Checklist of Assessment and Reporting Criteria’ was also provided with the technical report in line with the guidelines of the JORC Code (2012). The mineral resource has been interpolated within geological wireframe the using a 0.20% V205 lower cut and is tabulated below.

Mineral Resources for the Medcalf Deposit - JORC 2012 Resource Category Tonnes V 2O5 (%) TiO2 (%) Cut-off

V2O5 (%) Measured - Indicated 23.0 0.47 8.5 0.2 Inferred 8.8 0.40 8.1 0.2 TOTAL 31.8 0.45 8.4 0.2

The Company’s independent mineral resource estimates were developed by Ravensgate. Governance arrangements and internal controls Mineral resources are estimated by suitably qualified independent consultants to Audalia in accordance with the requirements of the JORC Code, using industry standards and consultants’ internal guidelines for the estimation and reporting of mineral resources. The mineral resource estimates included in the Company’s 2015 Annual Report are reviewed by a suitably qualified competent person.

For

per

sona

l use

onl

y

11

D I R E C T O R S ’ R E P O R T

Competent Person’s Statement The information in this report that relates to the Mineral Resource for the Medcalf Project is based on information compiled by Stephen Hyland, who is a Principal Consultant of Ravensgate. Mr Hyland is a Fellow of the Australasian Institute of Mining and Metallurgy. Mr Hyland has had sufficient experience that is relevant to the style of mineralisation, type of deposit under consideration and to the activity being undertaken to qualify as a Competent Person as defined in the 2012 edition of the Australasian Code for Reporting of Exploration, Results, Mineral Resource and Ore Reserves (JORC Code 2012). Mr Hyland consents to the inclusion in the report of the matters based on this information in the form and context in which it appears. DIVIDENDS No dividend has been declared or paid by the Company to the date of this report. ENVIRONMENTAL REGULATION The Company’s exploration and mining activities are governed by a range of environmental legislation and regulations including the National Greenhouse and Energy Report Act 2007 and Mining Act 1978. As the Company is still in the development phase of its interests in exploration projects, Audalia is not yet subject to the public reporting requirements of environmental legislation and regulations. To the best of the directors’ knowledge, the Company has adequate systems in place to ensure compliance with the requirements of the applicable environmental legislation and is not aware of any breach of those requirements during the financial year and up to the date of the Directors’ Report. EVENTS SUBSEQUENT TO REPORTING DATE Other than the negotiation on the 25 September 2015 for the extension of repayment date of its loan facilities of A$4 million from 20 March 2016 to 20 March 2017, there has not arisen in the interval between the end of the financial year and the date of this report any item, transaction or event of a material and unusual nature likely, in the opinion of the directors, to affect significantly the operations of the Company, the results of those operations, or the state of affairs of the Company in future financial years. REMUNERATION REPORT (AUDITED) The Remuneration Report, which has been audited, outlines the key management personnel remuneration arrangements for the Company, in accordance with the requirements of the Corporations Act 2001 and its regulations. For the purposes of this report, key management personnel of the Company are defined as those persons having authority and responsibility for planning, directing and controlling the major activities of the Company, directly or indirectly, including any director (whether executive or otherwise) of the Company. In this report, the term “executive” refers to the executive directors of the Company. (a) Key management personnel

The following were key management personnel of the Company at any time during the year and unless otherwise indicated were KMP for the entire year:

Name Position held

Dato Soo Kok Lim Executive Chairman Datuk Siew Swan Ong Executive Director Mr Brent Butler Chief Executive Officer and Director Mr Andrew Kwa Non-Executive Director

(b) Remuneration governance The Nomination and Remuneration Committee of the Board of Directors of the Company is responsible for determining and reviewing remuneration policies for the directors and executives. If necessary, the Nomination and Remuneration Committee obtains independent advice on the appropriateness of remuneration packages given trends in comparable companies and in accordance with the objectives of the Company.

For

per

sona

l use

onl

y

12

D I R E C T O R S ’ R E P O R T

Further information on the Nomination and Remuneration Committee’s role, responsibilities and membership is set out in the Company’s corporate governance statement which can be found on the Company’s website, in a section titled ‘Corporate Governance’: www.audalia.com.au/corporate/corporate-governance/. (c) Use of remuneration consultants The Nomination and Remuneration Committee did not engage the services of a remuneration consultant during the year. (d) Remuneration policies and framework (i) Principles of remuneration The remuneration structures explained below are competitively set to attract, motivate and retain suitably qualified and experienced candidates, reward the achievement of strategic objectives and achieve the broader outcome of creation of value for shareholders. The remuneration structures take into account:

o the capability and experience of the key management personnel;

o the key management personnel’s ability to control the achievement of strategic objectives;

o the Company’s performance including: � the growth in share price; and � the amount of incentives within each key management person’s compensation.

Given the evaluation and developmental nature of the Company’s principal activity, the overall level of compensation does not have regard to the earnings of the Company. (ii) Remuneration structure In accordance with best practice corporate governance, the structure of non-executive directors’ remuneration is clearly distinguished from that of executives. (e) Non-executive director remuneration The Constitution and the ASX Listing Rules specify that the aggregate remuneration of non-executive directors shall be determined from time to time by a general meeting. The aggregate remuneration for all non-executive directors, last voted upon by shareholders at the 2011 General Meeting, is not to exceed $300,000 per annum. Directors’ fees cover all main board activities and membership of committees. Non-executive directors do not receive any retirement benefits, other than statutory superannuation, nor do they receive any performance related compensation. Level of non-executive directors’ fees is as follows:

Name From 4 July 2014 July 2011

to 3 July 2014

Mr Andrew Kwa $25,000 $20,000

Mr Brent Butler1 $30,000 $20,000

1. Mr Brent Butler was appointed Chief Executive Officer on 14 April 2015. His remuneration as an executive director is disclosed in section (i) of this Remuneration Report. Mr Butler continues to receive this director’s fee in addition to his remuneration as an executive director of the Company.

(f) Executive remuneration Remuneration for executives is set out in employment and consultancy agreements. Details of the agreements with the Executive Chairman, Executive Director and Chief Executive Officer are provided below. Executive directors may receive performance related compensation but do not receive any retirement benefits, other than statutory superannuation. (i) Fixed remuneration Fixed remuneration consists of base compensation (which is calculated on a total cost basis and includes any FBT charges related to employee benefits including motor vehicles) as well as employer contributions to superannuation funds. Fixed remuneration is reviewed annually by the Nomination and Remuneration Committee. As described in (h), as it is not possible to evaluate the Company’s financial performance using generally accepted measures such as profitability or total shareholder returns, remuneration considerations will have regard to achievement of strategic objectives, service criteria and growth in share price.

For

per

sona

l use

onl

y

13

D I R E C T O R S ’ R E P O R T

(f) Executive remuneration (continued) As noted above, the Nomination and Remuneration Committee has access to external advice independent of management, if required. (ii) Short-term incentive The Company has not set any short-term incentives (STI) for key management personnel. (iii) Long-term incentive Long-term incentives (LTI) may be provided to key management personnel in the form of options over ordinary shares of the Company, ordinary shares or other equity-settled remuneration. LTI are considered to promote continuity of employment and provide additional incentive to recipients to increase shareholder wealth. LTI may generally only be issued to directors subject to approval by shareholders in general meeting. During the year, the CEO participated in LTI in the form of equity-settled remuneration which may be granted subject to fulfilment of certain performance conditions and the Company obtaining all necessary regulatory approvals. Further details are set out in (l) of this Remuneration Report. The Company has a policy that prohibits employees and directors of the Company from entering into transactions that operate or are intended to operate to limit the economic risk or are designed or intended to hedge exposure to unvested Company securities. This includes entering into arrangements to hedge their exposure to LTI granted as part of their remuneration package. This policy may be enforced by requesting employees and directors to confirm compliance. (g) Voting and comments made at the Company’s 2014 A nnual General Meeting The Remuneration Report for the 2014 financial year received positive shareholder support at the 2014 AGM with a vote of 100% in favour. The Company did not receive any specific feedback at the AGM or throughout the year on its remuneration practices. (h) Consequences of performance on shareholder weal th In considering the Company’s performance and benefits for shareholder wealth, the Directors have regard to the following indices in respect of the current financial period:

2015 2 2014 1 2013 2012 Net loss for the year $1,022,458 $402,942 $288,724 $393,303 Change in share price $0.10 ($0.125) $0.04 $0.01 Share price at beginning of the period $0.13 $0.25 $0.21 $0.20 Share price at end of the period $0.23 $0.13 $0.25 $0.21 Loss per share 0.44 cents 0.23 cents 0.36 cents 0.49 cents

1. The Company issued a total of 150,000,000 shares during the 2014 financial year, on 27 September 2013 (12,000,000) and 12

November 2013 (138,000,000). 2. The Company issued a total of 4,000,000 shares during the 2015 financial year, on 14 November 2014 (2,000,000) and 26 February

2015 (2,000,000). Due to the Company currently being in an exploration and evaluation phase, the Company’s earnings are not considered to be a principal performance indicator. However, the overall level of key management personnel remuneration takes into account the achievement of strategic objectives, service criteria and growth in share price. The overall level of key management personnel remuneration takes into account the performance of the Company since the Company’s incorporation on 27 August 2010. As a result, remuneration was not paid to directors or executives until the Company was admitted to the Official List of ASX in July 2011. Since then until the start of the 2015 financial year, the level of remuneration had remained unchanged, other than the increase or decrease in remuneration levels due to the appointment of key management personnel. Given the Company’s increasing level of activities, the achievement of milestones since incorporation in 2010, levels of both non-executive and executive remuneration increased with effect from 4 July 2014, as disclosed in this Remuneration Report. The aggregate remuneration for non-executive directors has remained unchanged since voted upon by shareholders in January 2011. (i) Employment and Consultancy Agreements The Company has entered into employment agreements with its Executive Chairman and Executive Director. The employment agreements outline the components of remuneration paid to the executives and are reviewed on an annual basis.

For

per

sona

l use

onl

y

14

D I R E C T O R S ’ R E P O R T

(i) Employment and Consultancy Agreements (continued ) Dato Soo Kok Lim, Executive Chairman, has an employment agreement effective from 4 July 2011 with the Company (EC Employment Agreement ). The EC Employment Agreement specifies the duties and obligations to be fulfilled by the Executive Chairman. The initial term of the EC Employment Agreement was 2 years but it has been renewed for a further term of 3 years with effect from 4 July 2014. Annual salary for Dato Lim for the initial period was $20,000 per annum (exclusive of statutory superannuation) and from 4 July 2014, $80,000 per annum (exclusive of statutory superannuation) under the EC Employment Agreement. Either Dato Lim or Audalia may terminate the agreement at any time by giving three month’s written notice to the other. Dato Lim has no entitlement to termination payment should he terminate the agreement by written notice. Audalia may, by giving written notice to Dato Lim, immediately terminate the agreement should a number of specified occurrences happen, including a serious breach of the agreement or serious misconduct. Dato Lim has no entitlement to termination payment in the event of removal for misconduct. Datuk Siew Swan Ong, Executive Director, has an employment agreement effective from 4 July 2011 with the Company (ED Employment Agreement ). The ED Employment Agreement specifies the duties and obligations to be fulfilled by the Executive Director. The initial term of the ED Employment Agreement was 2 years but it has been renewed for a further term of 3 years with effect from 4 July 2014. Annual salary for Datuk Ong for the initial period was $20,000 per annum (exclusive of statutory superannuation) and from 4 July 2014, $80,000 per annum (exclusive of statutory superannuation) under the ED Employment Agreement. Either Datuk Ong or Audalia may terminate the agreement at any time by giving three month’s written notice to the other. Datuk Ong has no entitlement to termination payment should he terminate the agreement by written notice. Audalia may, by giving written notice to Datuk Ong, immediately terminate the agreement should a number of specified occurrences happen, including a serious breach of the agreement or serious misconduct. Datuk Ong has no entitlement to termination payment in the event of removal for misconduct. Mr Butler, CEO, has consultancy agreement effective from 14 April 2015 with the Company (CEO Consultancy Agreement ). The CEO Consultancy Agreement specifies the duties and obligations to be fulfilled by the CEO. The initial term of the CEO Consultancy Agreement is 2 years with an option to further extend under mutually agreed terms between the Company and Mr Butler. The annual fee for Mr Butler is $120,000 per annum (exclusive of GST) under the CEO Consultancy Agreement. Subject to the Company obtaining all shareholder and regulatory approvals that may be required, Mr Butler will be issued with the following fully paid ordinary shares (Shares ) in the Company upon the successful achievement of the agreed milestones:

o 2,000,000 Shares upon the Company granting of Mining Lease Application M63/656; and o 2,000,000 Shares upon the completion and receipt of the pre-feasibility report on the Medcalf Project.

Each of the tranches of Shares will be held in escrow for a period of 2 years from their respective dates of issue. Further details are set out in (l) of this Remuneration Report. Either Mr Butler or Audalia may terminate the agreement at any time by giving three month’s written notice to the other. Audalia may, by giving written notice to Mr Butler, immediately terminate the agreement should a number of specified occurrences happen, including a serious breach of the agreement or serious misconduct. Mr Butler has no entitlement to termination payment in the event of removal for misconduct. Refer to Note 19 for details on the financial impact in future periods resulting from firm commitments arising from non-cancellable contracts for services with directors. (j) Link between remuneration and performance The Nomination and Remuneration Committee determines the Company’s remuneration policy and structure to ensure it aligns with the Company’s needs and meet remuneration principles set out in (d). Remuneration is not linked to performance using generally accepted measures such as profitability or total shareholder returns but linked to achievement of strategic objectives or service criteria aimed at advancing the goals set out to achieve project outcomes which the Board believes aligns with creation of positive shareholder value. F

or p

erso

nal u

se o

nly

15

D I R E C T O R S ’ R E P O R T

(k) Remuneration expense of key management personne l

Details of the nature and amount of each major element of the remuneration of each key management person of the Company are:

Fixed Remuneration

Variable Remuneration

SHORT-TERM EMPLOYEE BENEFITS

POST-EMPLOYMENT BENEFITS

LONG-TERM BENEFITS

LONG-TERM BENEFITS

Salary & fees $

Superannuation benefits

$

Annual and Long Service

Leave $

Share based payments

$ Total

$ Directors

Non-executive Mr A Kwa 2015 22,831 2,169 - - 25,000 2014 18,307 1,693 - - 20,000 Executive Dato S K Lim 2015 80,000 7,600 25,853 - 113,453 2014 20,000 1,850 1,766 - 23,616 Datuk S S Ong 2015 80,000 7,600 25,853 - 113,453 2014 20,000 1,850 1,766 - 23,616 Mr B Butler 2015 55,000 - - 269,317 324,317 2014 20,000 - - - 20,000

Total 2015 237,831 17,369 51,706 269,317 576,223

2014 78,307 5,393 3,532 - 87,232 Reconciliation of Share based payments held by key management personnel:

Balance at 1 July 2014 (number)

Initial measurement

date ** (number)

Vested

(number)

Forfeited

(number)

Balance at 30 June 2015

Vested (number)

Balance at 30 June 2015

Unvested (number)

Executive Mr B Butler 2015 - 4,000,000 - - - 4,000,000 2014 - - - - - - **The issue of Shares is subject to shareholder approval, which will be considered by shareholders at the 2015 Annual General Meeting. However, under the Accounting Standard AASB 2, the Company is required to recognise the expense over the period in which the employee rendered the services. (l) Share-based remuneration Share based payment compensation benefits are provided to the CEO under the Consultant Agreement. Shares will be granted on fulfilment of performance hurdles, and the issue of which is subject to shareholder approval. Upon vesting, each right automatically converts into one ordinary share. Fair value of rights is determined with reference to the share price at the date of commencement of services and recognised over the period from commencement of the service contract to when milestones are expected to be achieved. Assessment of the likelihood of milestones being achieved is subject to the Board’s assessment of operational considerations at the time of valuation and revised at each reporting date.

For

per

sona

l use

onl

y

16

D I R E C T O R S ’ R E P O R T

(l) Share-based remuneration (continued) The following table sets out the terms and conditions of CEO’s Share based remuneration:

Agreement commencement

(term)

Right to shares

(Number)

Conditions for grant of shares

Ordinary shares on

fulfilment of conditions (Number)

14 April 2015 (2 years)

2,000,000

Hurdle 1

Grant of mining lease application M63/656

2,000,000

14 April 2015 (2 years)

2,000,000

Hurdle 2

Completion and receipt of the pre-feasibility report on the Medcalf Project

2,000,000

Fair value of Share based remuneration

The assessed fair value based on initial measurement date (agreement date) of an underlying share was $0.225 (being market price at date of agreement) and the corresponding number of shares that can be issued under the agreement is 4,000,000 shares. The fair value is therefore $900,000. These are the valuation inputs of CEO Share based remuneration (considered to be level 3):

Initial measurement

date

Expected expiry date (a)

Fair Value

($)

Balance at start of the year

(Number)

Expected to be

granted on fulfilment of hurdles (Number)

Cancelled (Number)

Converted during the

year (Number)

Balance at end of the year

(Number)

Fair Value at initial

measurement date ($)

14 April 2015 30 Nov 2015 0.225 - 2,000,000 - - - 450,000 14 April 2015 31 Jan 2016 0.225 - 2,000,000 - - - 450,000 Total - 4,000,000 - - - 900,000 (a) Based on management’s assessment of the likelihood of milestones being achieved, at the date of this Annual Report.

(m) Equity instruments held by key management person nel The number of ordinary fully paid shares in the Company held directly and indirectly by directors and other key management personnel, and any movements during the period are set out below:

Balance at 1 July 2014

Received as remuneration

Options Exercised

Net Changes Other

Balance at 30 June 2015

Directors

Non-Executive Mr A Kwa 250,000 - - - 250,000

Executive Dato S K Lim 16,140,000 - - - 16,140,000 Datuk S S Ong 16,900,000 - - - 16,900,000 Mr B Butler 530,000 - - - 530,000 Mr B Butler (subject to conditions) - 4,000,000** - - 4,000,000

** Under Mr Butler’s Consultancy Agreement, entitlement to 4,000,000 fully paid ordinary shares subject to achievement of performance conditions, and subject to shareholder approval, refer (l). No shares have been granted as at the date of report. ‘Net changes other’ relate to shares sold or acquired during the financial year. (n) Loans to key management personnel There were no loans to key management personnel during the year.

For

per

sona

l use

onl

y

17

D I R E C T O R S ’ R E P O R T

(o) Other transactions with key management personne l There were no other transactions with key management personnel and related parties during the year other than reported below. A number of key management persons, or their related parties, hold positions in other entities that result in them having control or significant influence over the financial or operating policies of those entities. The terms and conditions of those transactions were no more favourable than those available, or which might reasonably be expected to be available, on similar transactions to unrelated entities on an arm’s length basis.

The aggregate amounts recognised during the year relating to key management personnel and their related parties were as follows:

Transactions value year

ended 30 June Balance outstanding

as at 30 June Director / Executive Transaction

2015 $

2014 $

2015 $

2014 $

Mr B Butler1 Consultancy fees 191,000 115,000 4,303 Nil

Notes in relation to the table of related party transactions

1. A company associated with Mr Butler, World Technical Services Group Pty Ltd, provided consulting services in

connection with the Company’s exploration projects. Terms for such services were based on market rates, and amounts were payable on a monthly basis.

This concludes the Remuneration Report, which has been audited. OPTIONS Unissued shares under option At the date of this report, there were no unissued ordinary shares of the Company under option. No options have been granted since the end of the previous financial year. INDEMNIFICATION AND INSURANCE OF OFFICERS

Indemnification

The Company has agreed to indemnify the current directors and company secretary of the Company against all liabilities to another person (other than the Company or a related body corporate) that may arise from their position as directors of the Company, except where the liability arises out of conduct involving a lack of good faith. The agreement stipulates that the Company will meet the full amount of any such liabilities, including costs and expenses.

Insurance

The Company paid a premium, during the year in respect of a director and officer liability insurance policy, insuring the directors of the Company, the company secretary, and executive officers of the Company against a liability incurred as such a director, secretary or executive officer to the extent permitted by the Corporations Act 2001. The directors have not included details of the nature of the liabilities covered or the amount of the premium paid in respect of the director’s and officers’ liability and legal expenses’ insurance contracts as such disclosure is prohibited under the terms of the contract.

INDEMNIFICATION AND INSURANCE OF AUDITORS

The Company has not, during or since the financial year, indemnified or agreed to indemnify the auditor of the Company or any related entity against liability incurred by the auditor.

During the financial year, the Company has not paid a premium in respect of a contract to insure the auditor of the Company or any related entity.

For

per

sona

l use

onl

y

18

D I R E C T O R S ’ R E P O R T

PROCEEDINGS ON BEHALF OF THE COMPANY

No person has applied to the Court under section 237 of the Corporations Act 2001 for leave to bring proceedings on behalf of the Company, or to intervene in any proceedings to which the Company is a party for the purposes of taking responsibility on behalf of the Company for all or part of those proceedings. NON-AUDIT SERVICES

The following non-audit services were provided by BDO Corporate Tax (WA) Pty Ltd, a company associated with the Company's auditor, BDO Audit (WA) Pty Ltd. The Directors are satisfied that the provision of non-audit services is compatible with the general standard of independence for auditors imposed by the Corporations Act 2001. The nature and scope of each type of non-audit service provided means that auditor independence was not compromised. BDO Corporate Tax (WA) Pty Ltd and BDO Corporate Finance (WA) Pty Ltd received or is due to receive the following amounts for the provision of non-audit services:

2015 $

2014 $

BDO Corporate Finance (WA) Pty Ltd Corporate Finance services 12,240 - BDO Corporate Tax (WA) Pty Ltd Tax compliance services 31,162 37,715

OFFICERS OF THE COMPANY WHO ARE FORMER AUDIT PARTNERS OF BDO AUDIT (WA) PTY LTD

There are no officers of the Company who are former audit partners of BDO Audit (WA) Pty Ltd. AUDITOR’S INDEPENDENCE DECLARATION

The auditor’s independence declaration is set out on page 47 and forms part of the Directors’ Report. AUDITOR

BDO Audit (WA) Pty Ltd continues in office in accordance with section 327 of the Corporations Act 2001. Dated at Perth, Western Australia this 29th day of September 2015. Signed in accordance with a resolution of the directors: Dato Soo Kok Lim Executive Chairman

For

per

sona

l use

onl

y

19

ST A T E M E N T O F P R O F I T O R L O S S A N D OT H E R C O M P R E H E N S I V E I N C O M E for the year ended 30 June 2015

Note

2015 $

2014 $

Revenue from Continuing Operations Revenue 4 18,381 14,064 Exploration expenditure write off 11 (1,359) Corporate and administrative expenses 5 (770,163) (417,006) Share based payment expense 17 (269,317) -

Loss before income tax (1,022,458) (402,942) Income tax expense 6 - -

Net loss after income tax for the year (1,022,458) (402,942) Other comprehensive income Items that will not be reclassified to profit or loss - - Items that may be reclassified subsequently to profit or loss - - Other comprehensive income for the year, net of tax - -

Total comprehensive loss for the year attributable to the owners of the Company (1,022,458) (402,942) Loss per share attributable to the owners of the Company Basic loss per share (cents) 20 (0.44) (0.23)

Diluted loss per share is not shown as all potential ordinary shares on issue would decrease the loss per share and are thus not considered dilutive.

The Statement of Profit or Loss and Other Comprehensive Income is to be read in conjunction with the accompanying notes.

For

per

sona

l use

onl

y

20

ST A T E M E N T O F F I N A N C I A L P O S I T I O N as at 30 June 2015

Note

2015 $

2014 $

CURRENT ASSETS Cash and cash equivalents 7 2,660,781 350,396 Trade and other receivables 8 51,054 9,362 Other current assets 9 21,110 18,696

Total Current Assets 2,732,945 378,454 NON-CURRENT ASSETS Trade and other receivables 8 - 17,875 Property, Plant & Equipment 10 40,737 15,081 Exploration and evaluation assets 11 4,444,000 2,711,384

Total Non-Current Assets 4,484,737 2,744,340

TOTAL ASSETS 7,217,682 3,122,794

CURRENT LIABILITIES Trade and other payables 12 495,539 190,385 Employee benefit obligations 13 14,092 4,114 Borrowings 14 3,000,000 -

Total Current Liabilities 3,509,631 194,499

NON-CURRENT LIABILITIES

Employee benefit obligations 13 48,132 7,002

Total Non -Current Liabilities 48,132 7,002

TOTAL LIABILITIES 3,557,763 201,501

NET ASSETS

3,659,919 2,921,293

EQUITY Contributed equity 15 5,585,735 4,093,968 Reserves 16 279,317 10,000 Accumulated losses 18 (2,205,133) (1,182,675)

TOTAL EQUITY

3,659,919 2,921,293

The Statement of Financial Position is to be read in conjunction with the accompanying notes.

For

per

sona

l use

onl

y

21

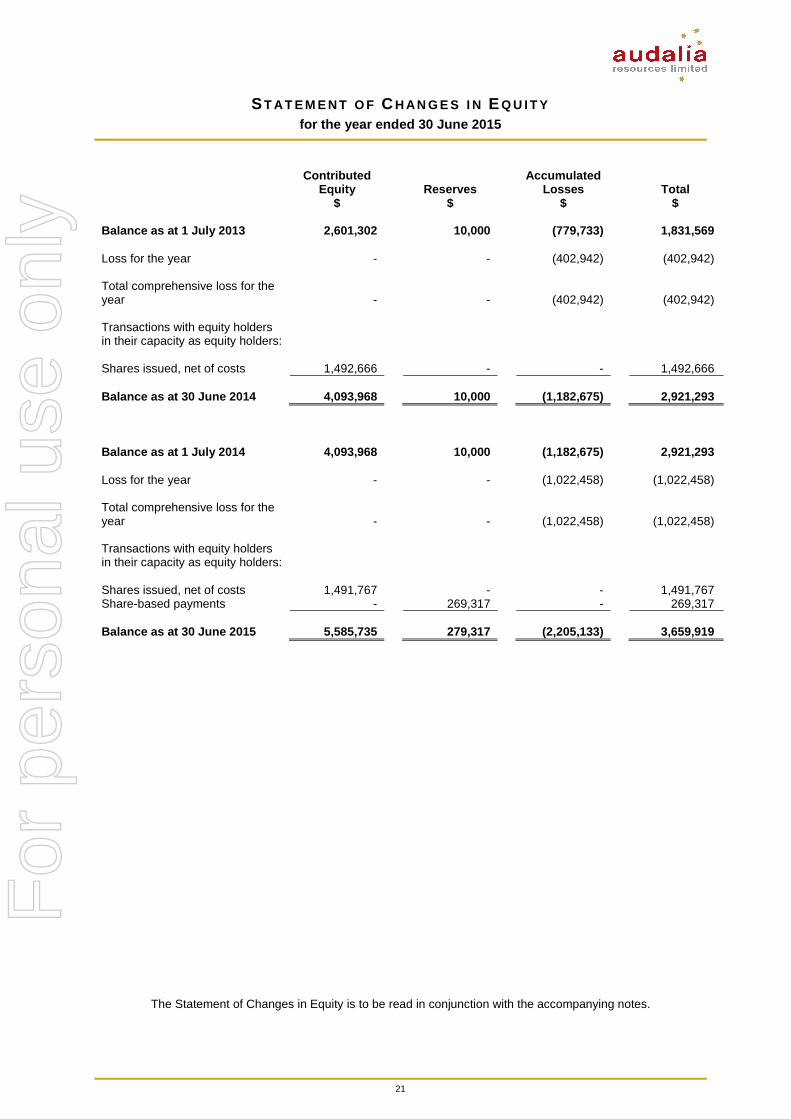

ST A T E M E N T O F C H A N G E S I N E Q U I T Y for the year ended 30 June 2015

Contributed Equity

$ Reserves

$

Accumulated Losses

$ Total

$ Balance as at 1 July 2013 2,601,302 10,000 (779,733) 1,831,569 Loss for the year - - (402,942) (402,942) Total comprehensive loss for the year - -

(402,942) (402,942)

Transactions with equity holders in their capacity as equity holders:

Shares issued, net of costs 1,492,666 - - 1,492,666

Balance as at 30 June 2014 4,093,968 10,000 (1,182,675) 2,921,293

Balance as at 1 July 2014 4,093,968 10,000 (1,182,675) 2,921,293 Loss for the year - - (1,022,458) (1,022,458) Total comprehensive loss for the year - -

(1,022,458) (1,022,458)

Transactions with equity holders in their capacity as equity holders:

Shares issued, net of costs 1,491,767 - - 1,491,767 Share-based payments - 269,317 - 269,317

Balance as at 30 June 2015 5,585,735 279,317 (2,205,133) 3,659,919

The Statement of Changes in Equity is to be read in conjunction with the accompanying notes.

For

per

sona

l use

onl

y

22

ST A T E M E N T O F C A S H F L O W S for the year ended 30 June 2015

Note 2015

$ 2014

$

Cash flows from operating activities

Payments to suppliers and employees (inclusive of GST) (483,046) (378,349) Interest received 16,214 14,528 Interest paid (33,139) (9,644)

Net cash (outflows) from operating activities 23 (499,971) (373,464) Cash flows from investing activities

Payments for acquisition of property plant and equipment (32,121) (15,904) Payments for exploration and evaluation assets – capitalised costs (1,649,290) (1,455,881) Proceeds from R&D incentive for exploration and evaluation - 203,923

Net cash (outflows) from investing activities (1,681,411) (1,267,862) Cash flows from financing activities

Proceeds from borrowings 3,700,000 500,000 Repayment of borrowings (700,000) (500,000) Proceeds from issue of shares 15 1,500,000 1,500,000 Payment for share issue costs (8,233) (7,334)

Net cash inflows from financing activities 4,491,767 1,492,666 Net increase/(decrease) in cash held 2,310,385 (148,661) Cash and cash equivalents at 1 July 2014 350,396 499,057

Cash and cash equivalents at 30 June 2015 7 2,660,781 350,396

The Statement of Cash Flows is to be read in conjunction with the accompanying notes.

For

per

sona

l use

onl

y

23

N O T E S T O T H E F I N A N C I A L S T A T E M E N T S for the year ended 30 June 2015

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES The financial report of Audalia Resources Limited (the Company or Audalia ) for the financial year ended 30 June 2015 was authorised for issue in accordance with a resolution of directors on 29 September 2015.

The Company is a public company limited by shares incorporated and domiciled in Australia whose shares are traded on the Australian Securities Exchange.

The nature of the operations and principal activities of the Company are described in the Review of Activities. (a) Basis of preparation

The principle accounting policies adopted for the preparation of financial statements are set out below. These accounting policies have been applied consistently to all periods presented and have been consistently applied by the Company to all the years presented unless otherwise stated.

(i) Statement of compliance

These general purpose financial statements have been prepared in accordance with the requirements of the Corporations Act 2001, Australian Accounting Standards and Interpretations issued by the Australian Accounting Standards Board and the Corporations Act 2001. Audalia is a for profit entity for the purpose of preparing the financial statements.

The financial statements of the Company also comply with the International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB ).

(ii) Basis of measurement

The financial statements are prepared on the accruals basis and the historical cost basis except for financial assets and liabilities measured at fair value. The financial statements are presented in Australian dollars and all values are rounded to the nearest dollar unless otherwise stated.

(iii) Going concern

At 30 June 2015, the Company had net assets of $3,659,919 (30 June 2014: $2,921,293), including $2,660,781 (30 June 2014: $350,396) in cash and cash equivalents. At 30 June 2015, the Company had incurred a net loss after tax of $1,022,458 (2014: $402,942) and net operating cash outflows of $499,971 (2014: $373,464) for the year ended 30 June 2015 and the Company continues to incur expenditure in developing and exploring its tenements, drawing on its cash balances.

The financial report has been prepared on a going concern basis, which assumes continuity of normal business activities and the realisation of assets and the settlement of liabilities in the ordinary course of business. The Directors consider there are reasonable grounds to believe that the Company will be able to continue as a going concern after consideration of the following factors:

• The Company has access to the use of cash reserves of $2,660,781 as at 30 June 2015 (2014: $350,396).

• The Company has access to a further $1,000,000 under its loan facilities as at the date of this report.

• The Company has the ability to adjust its exploration expenditure subject to results of its exploration activities.

• Subsequent to reporting date, in July 2015 the Company received $395,259 research and development (R&D) incentive.

The Company continues to advance the development work at the Medcalf Project and progress the ongoing exploration activities at the Gascoyne Project. Although Audalia has a strong cash position, the Company will need to complete further capital raisings to continue to develop and explore its tenements as planned. The directors anticipate the support of its major shareholders and lenders and are confident in the Company’s ability to raise an appropriate level of funding to execute its development plan and continue its exploration activities. This was demonstrated by the extension of the repayment date of the Loan Facilities of $4 million from 20 March 2016 to 20 March 2017 on 25 September 2015. Should the Company be unable to raise sufficient capital when required, there is a material uncertainty which may cast significant doubt as to whether the Group will continue as a going concern and, therefore, whether it will realise its assets and extinguish its liabilities in the normal course of business and at the amounts stated in the financial report. The financial statements do not include any adjustments relating to the recoverability and classification of asset carrying amounts or the amounts of liabilities that might result should the company be unable to continue as a going concern and meet its debts as and when they fall due.

For

per

sona

l use

onl

y

24

N O T E S T O T H E F I N A N C I A L S T A T E M E N T S for the year ended 30 June 2015

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued ) (iv) Significant accounting judgements, estimates and assumptions

The preparation of the financial statements requires management to make judgements, estimates and assumptions that affect the reported amounts in the financial statements. Management continually evaluates its judgements and estimates in relation to assets, liabilities, contingent liabilities, revenue and expenses. Management bases its judgements and estimates on historical experience and on other various factors it believes to be reasonable under the circumstances, the result of which form the basis of the carrying values of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates. Revisions to accounting estimates are recognised in the period in which the estimate is revised and in any future periods affected. In particular, information about significant areas of estimation uncertainty and critical judgements in applying accounting policies that have the most significant effect on the amount recognised in the financial statements are outlined below:

Exploration and evaluation expenditure

The write-off and carrying forward of exploration acquisition costs is based on an assessment of an area of interest’s viability and/or the existence of economically recoverable reserves with information available at the time of preparing this report. Information may come to light in subsequent periods which requires the asset to be impaired or written down for which the director has no control. Deferred taxation

Deferred tax assets in respect of tax losses have not been brought to account as it is not considered probable that future taxable profits will be available against which they could be utilised. Valuation of share based remuneration

Assessment of the fair value of share based payment not traded in an active market is determined using a valuation technique which includes selecting appropriate inputs and assumptions available at the time of valuation. The Company has made an assessment of:

(a) the period over which the value will be recorded (recognise) – this is the period over which the services provided by the executive are received by the Company up to the point where the Company expects the executive to achieve the performance hurdles;

(b) the probability of the hurdles being met (vesting) –the likelihood of the hurdles being met. This is an operational assessment taking into account the current progress of the executive against the hurdle requirements and the final intention of the Company to issue the shares. This probability assessment is based on the best available information at the time of the estimate and will be revised at each reporting date

(b) Segment reporting An operating segment is a component of an entity that engages in business activities from which it may earn revenues and incur expenses, whose operating results are regularly reviewed by the entity's chief operating decision maker to make decisions about resources to be allocated to the segment and assess its performance and for which discrete financial information is available. This includes start-up operations which are yet to earn revenues. Management will also consider other factors in determining operating segments such as the level of segment information presented to the Board of Directors. Operating segments have been identified based on the information provided to the chief operating decision makers, being the Board of Directors. (c) Impairment of non-financial assets Goodwill and intangible assets that have an indefinite useful life are not subject to amortisation and are tested annually for impairment, or more frequently if events or changes in circumstances indicate that they might be impaired. Other assets are tested for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognised for the amount by which the asset’s carrying amount exceeds its recoverable amount. The recoverable amount is the higher of an asset’s fair value less costs to sell and value in use. For the purposes of assessing impairment, assets are grouped at the lowest levels for which there are separately identifiable cash flows which are largely independent of the cash inflows from other assets or groups of assets (cash-generating units). Non-financial assets other than goodwill that suffered an impairment are reviewed for possible reversal of the impairment at the end of each reporting period.

For

per

sona

l use

onl

y

25

N O T E S T O T H E F I N A N C I A L S T A T E M E N T S

for the year ended 30 June 2015

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) (d) Cash and cash equivalents Cash and cash equivalents in the statement of financial position comprise cash at bank and in hand and short-term deposits with an original maturity of three months or less that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value. For the purposes of the Statement of Cash Flows, cash and cash equivalents consist of cash and cash equivalents as defined above. (e) Trade and other receivables Trade receivables are recognised initially at fair value and subsequently at amortised cost less any impairment losses recognised. Collectability of trade receivables is reviewed on an ongoing basis. An allowance account (provision for impairment of trade receivables) is used when there is objective evidence that the Company will not be able to collect all amounts due.

(f) Exploration and evaluation expenditure Exploration, evaluation and development expenditure incurred is accumulated in respect of each identifiable area of interest. These costs are only carried forward to the extent that they are expected to be recouped through the successful development of the area or where activities in the area have not yet reached a stage that permits reasonable assessment of the existence of economically recoverable reserves. Where there are research and development costs recouped through government incentives in relation to exploration and evaluation, these are netted against the carrying value of capitalised expenditure incurred in respect of the identifiable project or area of interest where practicable. Events may occur or information may come to hand after the issue of this report which may materially alter the carrying value of this asset. Accumulated costs in relation to an abandoned area are written off in full against profit in the year in which the decision to abandon the area is made. When production commences, the accumulated costs for the relevant area of interest are amortised over the life of the area according to the rate of depletion of the economically recoverable reserves. A regular review is undertaken of each area of interest to determine the appropriateness of continuing to carry forward costs in relation to that area of interest. Costs of site restoration are provided over the life of the facility from when exploration commences and are included in the costs of that stage. Site restoration costs include the dismantling and removal of mining plant, equipment and building structures, waste removal, and rehabilitation of the site in accordance with clauses of the mining permits. Such costs are determined using estimates of future costs, current legal requirements and technology on an undiscounted basis. Any changes in the estimates for the costs are accounted on a prospective basis. In determining the costs of site restoration, there is uncertainty regarding the nature and extent of the restoration due to community expectations and future legislation. Accordingly the costs are determined on the basis that the restoration will be completed within one year of abandoning the site. (g) Trade and other payables Liabilities are recognised for amounts to be paid in the future for goods or services received, whether or not billed to the Company. Trade accounts payable are normally settled within 60 days. They are recognised initially at their fair value and subsequently measured at amortised cost using the effective interest method. (h) Borrowings Borrowings are initially recognised at fair value, net of transaction costs incurred. Borrowings are subsequently measured at amortised cost. Any difference between proceeds (net of transaction costs) and the redemption amount is recognised in profit and loss over the period of borrowings using the effective interest method. Borrowings are removed from the statement of financial position when the obligation specified in the contract is discharged, cancelled or expired. The difference between the carrying amount of a financial liability that has been extinguished or transferred to another party and the consideration paid, including any non-cash asset transferred or liabilities assumed, is recognised in profit and loss as other income or finance costs. Borrowings are classified as current liabilities unless the Company has an unconditional right to defer the settlement of the liability for at least 12 months after the reporting period. (i) Employee benefits Liabilities for wages and salaries including non-monetary benefits and accumulating sick leave that are expected to be settled wholly within 12 months after the end of the period in which the employees render the related services are recognised in respect of employee’s services up to the end of the reporting period and are measured at the amounts expected to be paid when the liabilities are settled. The liabilities are presented as current employee benefit obligations in the statement of financial position.

For

per

sona

l use

onl

y

26

N O T E S T O T H E F I N A N C I A L S T A T E M E N T S

for the year ended 30 June 2015

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) (i) Employee benefits (continued) Liabilities for long service leave and annual leave are not expected to be settled wholly within 12 months after the end of the period in which the employees render the related service. They are measured as present value of expected future payments to be made in respect of services provided by employees up to the end of the reporting period. Re-measurements as a result of adjustments and changes are recognised in profit and loss. The obligations are presented as current liabilities in the statement of financial position if the Company does not have an unconditional right to defer settlement for at least 12 months after the reporting period, regardless of when the actual settlement is expected to occur. (j) Share based payments Share based compensation benefits are provided to a key management personnel and a consultant. Information relating to the share based payments are set out in Note 17. Fair value of share based payments are recognised as an expense with a corresponding increase in equity. The total amount to be expensed is determined by reference to the fair value of rights determined with reference to the share price at the date of commencement of services and recognised over the period from commencement of the service contract to when milestones are expected to be achieved. Assessment of the likelihood of milestones being achieved is subject to the Board’s assessment of operational considerations at the time of valuation and revised at each reporting date. (k) Contributed equity

Ordinary shares are classified as equity. Incremental costs directly attributable to the issue of new shares are shown in equity as a deduction, net of tax, from the proceeds.

(l) Revenue recognition Revenue is measured at fair value of consideration received or receivable. Revenue is recognised to the extent that it is probable that the economic benefits will flow to the Company and can be reliably measured. Amounts disclosed as revenue represent interest received. Interest income is recognised as it accrues. (m) Leases Operating lease payments are recognised as an expense in the Statement of Profit or Loss and Other Comprehensive Income on a straight-line basis over the lease term. (n) Income tax Deferred income tax is provided on all temporary differences at the reporting date between the tax bases of assets and liabilities and their carrying amounts for financial reporting purposes. Deferred income tax liabilities are recognised for all taxable temporary differences:

(a) except where the deferred income tax liability arises from the initial recognition of an asset or liability in a transaction that is not a business combination and, at the time of the transaction, affects neither the accounting profit nor taxable profit or loss; and

(b) in respect of taxable temporary differences associated with investments in subsidiaries, associates and interests in joint ventures, except where the timing of the reversal of the temporary differences can be controlled and it is probable that the temporary differences will not reverse in the foreseeable future.

Deferred income tax assets are recognised for all deductible temporary differences, carry-forward of unused tax assets and unused tax losses, to the extent that it is probable that taxable profit will be available against which the deductible temporary differences, and the carry-forward of unused tax assets and unused tax losses can be utilised:

(a) except where the deferred income tax asset relating to the deductible temporary difference arises from the initial recognition of an asset or liability in a transaction that is not a business combination and, at the time of the transaction, affects neither the accounting profit nor taxable profit or loss; and

(b) in respect of deductible temporary differences associated with investments in subsidiaries, associates and interests in joint ventures, deferred tax assets are only recognised to the extent that it is probable that the temporary differences will reverse in the foreseeable future and taxable profit will be available against which the temporary differences can be utilised.

For

per

sona

l use

onl

y

27

N O T E S T O T H E F I N A N C I A L S T A T E M E N T S

for the year ended 30 June 2015

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued ) (n) Income tax (continued) The carrying amount of deferred income tax assets is reviewed at each reporting date and reduced to the extent that it is no longer probable that sufficient taxable profit will be available to allow all or part of the deferred income tax asset to be utilised. Deferred income tax assets and liabilities are measured at the tax rates that are expected to apply to the year when the asset is realised or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted at the reporting date. Income taxes relating to items recognised directly in equity are recognised in equity and not in the income statement. The Company has unused tax losses. However, no deferred tax balances have been recognised, as it is considered that asset recognition criteria have not been met at this time. (o) Goods and services tax (“GST”) Revenues, expenses and assets are recognised net of the amount of GST except:

� When the GST incurred on a purchase of goods and services is not recoverable from the taxation authority, in which case the GST is recognised as part of the cost of acquisition of the asset or as part of the expense item as applicable.