Embed Size (px)

Citation preview

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

Achieving high productivity in the small Nordic welfare states

Vesa Vihriälä 11 June 2014

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

The Nordics have succeeded well • High GDP/capita combined with low income disparities;

the Nordics top many rankings of perceived quality of life (including OECD’s better life index)

• Particularly employment rates but also productivity levels have been high

• The key - mutually reinforcing - elements of the “Nordic model”: – Substantial public spending on human capital, innovation

support, safety nets; financed by high taxes – Trust, capacity to take risks, acceptance of structural change – High productivity, high employment => large tax base limiting the

pressure on tax rates – Fiscal prudence => space for fiscal stabilisation

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

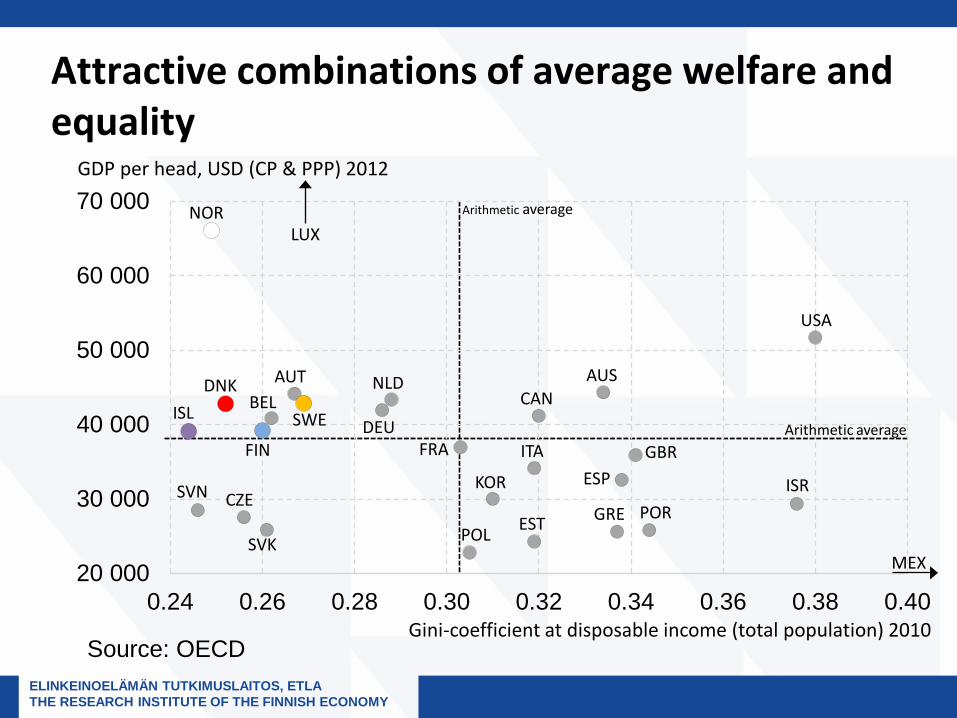

Attractive combinations of average welfare and equality

20 000

30 000

40 000

50 000

60 000

70 000

0.24 0.26 0.28 0.30 0.32 0.34 0.36 0.38 0.40

FIN

GDP per head, USD (CP & PPP) 2012

Gini-coefficient at disposable income (total population) 2010

CAN

ITA FRA

BEL

CZE

AUT

EST

NOR

NLD DNK

POL

USA

KOR

DEU

SVK

GBR ESP

SWE

MEX

ISR

AUS

SVN GRE POR

ISL

LUX Arithmetic average

Arithmetic average

Source: OECD

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

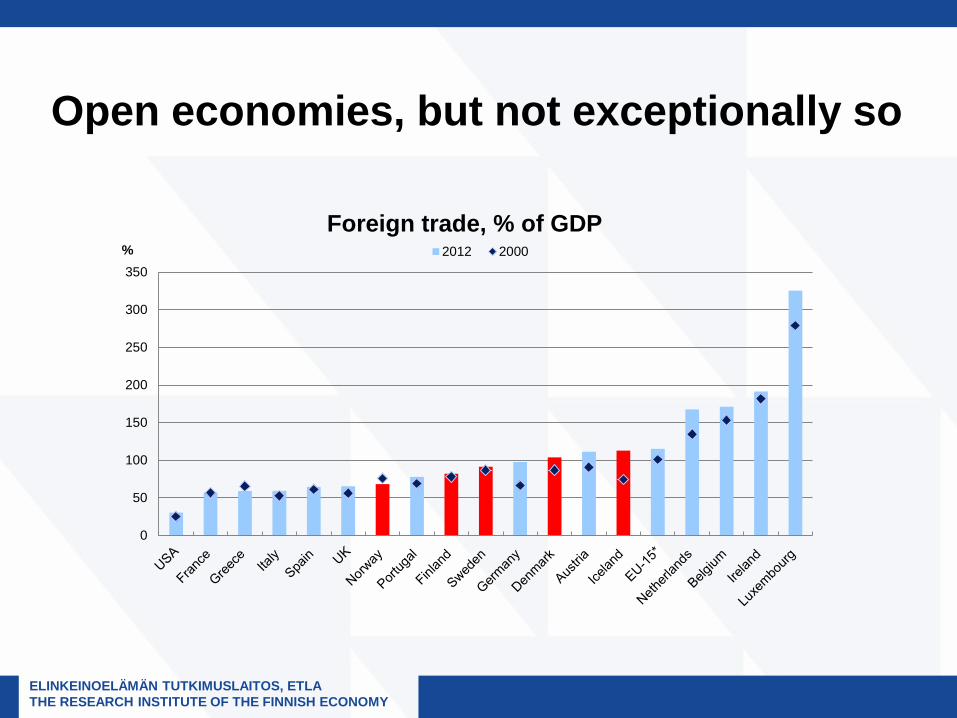

Open economies, but not exceptionally so

0

50

100

150

200

250

300

350%

Foreign trade, % of GDP 2012 2000

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

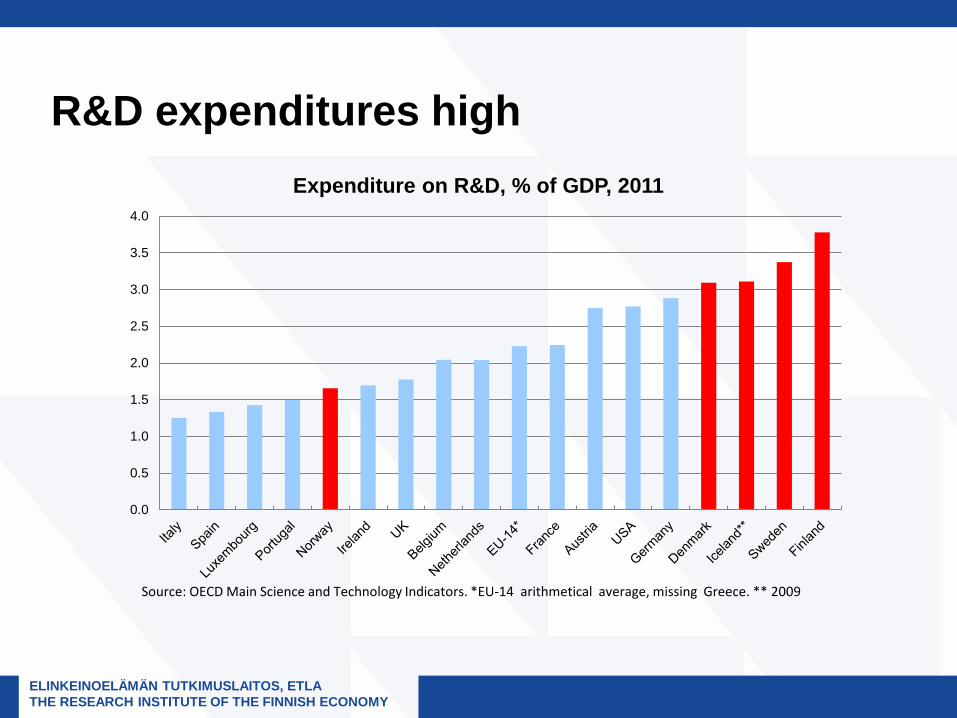

R&D expenditures high

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Expenditure on R&D, % of GDP, 2011

Source: OECD Main Science and Technology Indicators. *EU-14 arithmetical average, missing Greece. ** 2009

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

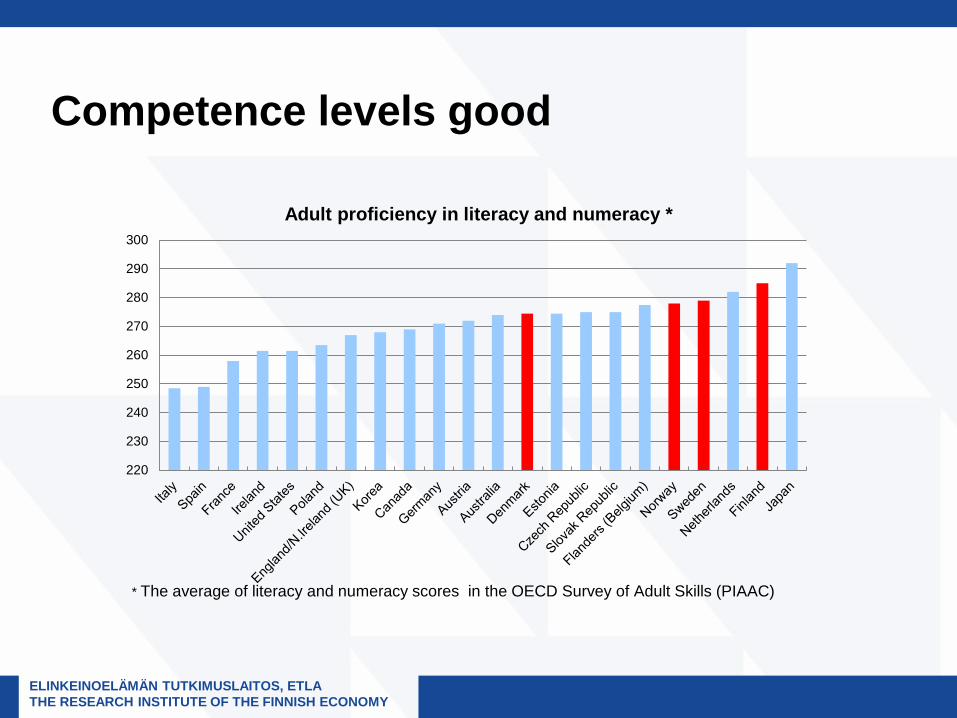

Competence levels good

220

230

240

250

260

270

280

290

300

Adult proficiency in literacy and numeracy *

* The average of literacy and numeracy scores in the OECD Survey of Adult Skills (PIAAC)

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

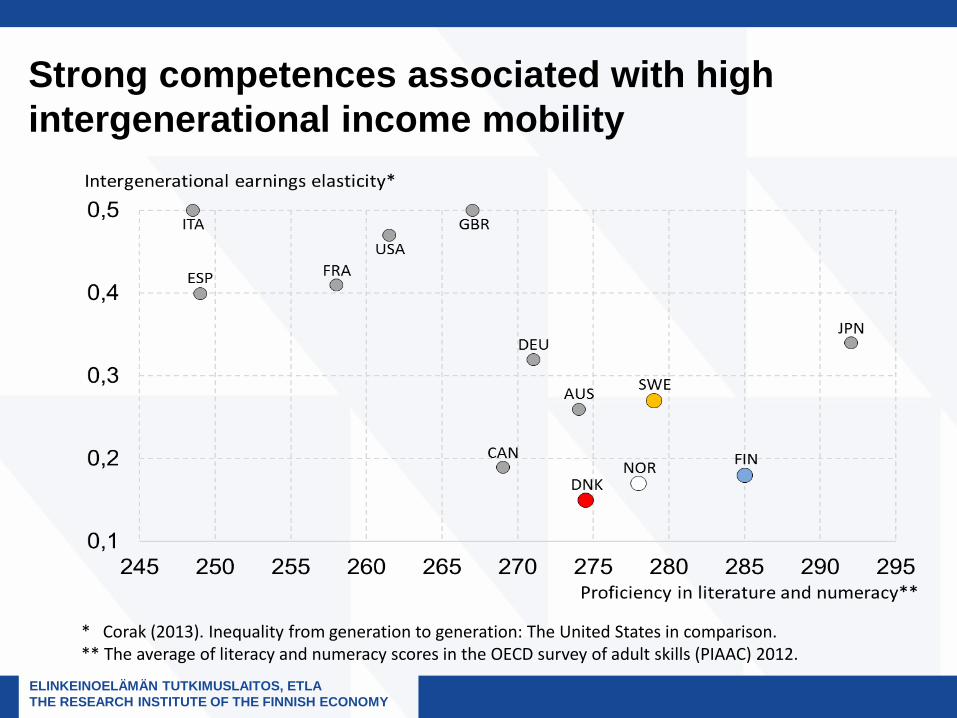

Strong competences associated with high intergenerational income mobility

* Corak (2013). Inequality from generation to generation: The United States in comparison. ** The average of literacy and numeracy scores in the OECD survey of adult skills (PIAAC) 2012.

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

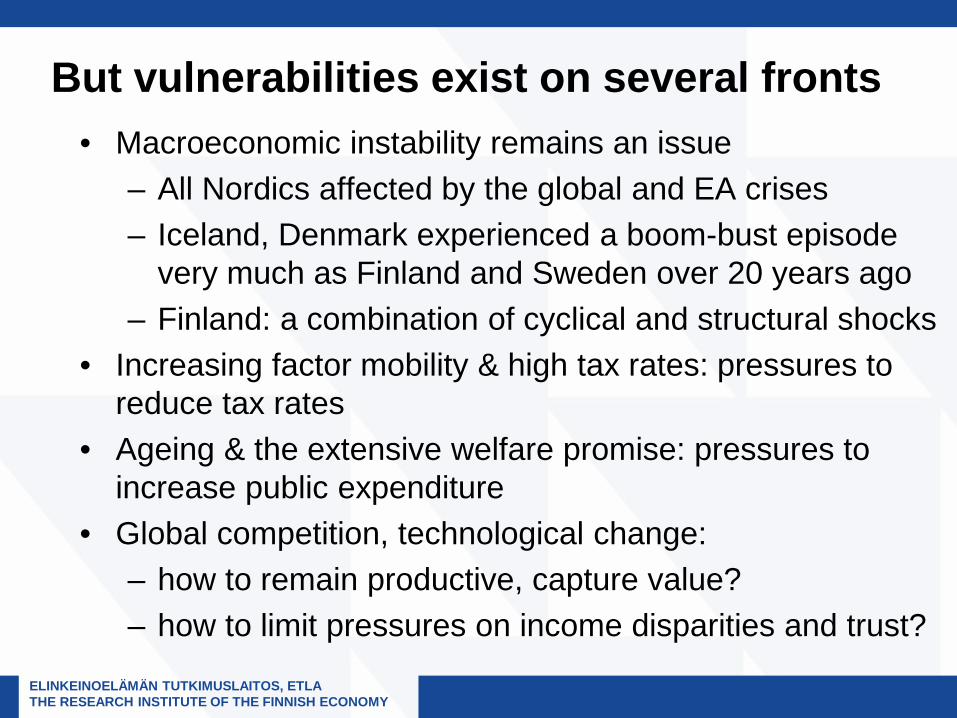

But vulnerabilities exist on several fronts • Macroeconomic instability remains an issue

– All Nordics affected by the global and EA crises – Iceland, Denmark experienced a boom-bust episode

very much as Finland and Sweden over 20 years ago – Finland: a combination of cyclical and structural shocks

• Increasing factor mobility & high tax rates: pressures to reduce tax rates

• Ageing & the extensive welfare promise: pressures to increase public expenditure

• Global competition, technological change: – how to remain productive, capture value? – how to limit pressures on income disparities and trust?

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

100

102

104

106

108

110

112

114

116

118

120

2005/1 2006/1 2007/1 2008/1 2009/1 2010/1 2011/1 2012/1 2013/1

Volu

me

inde

x, 2

005Q

1=10

0

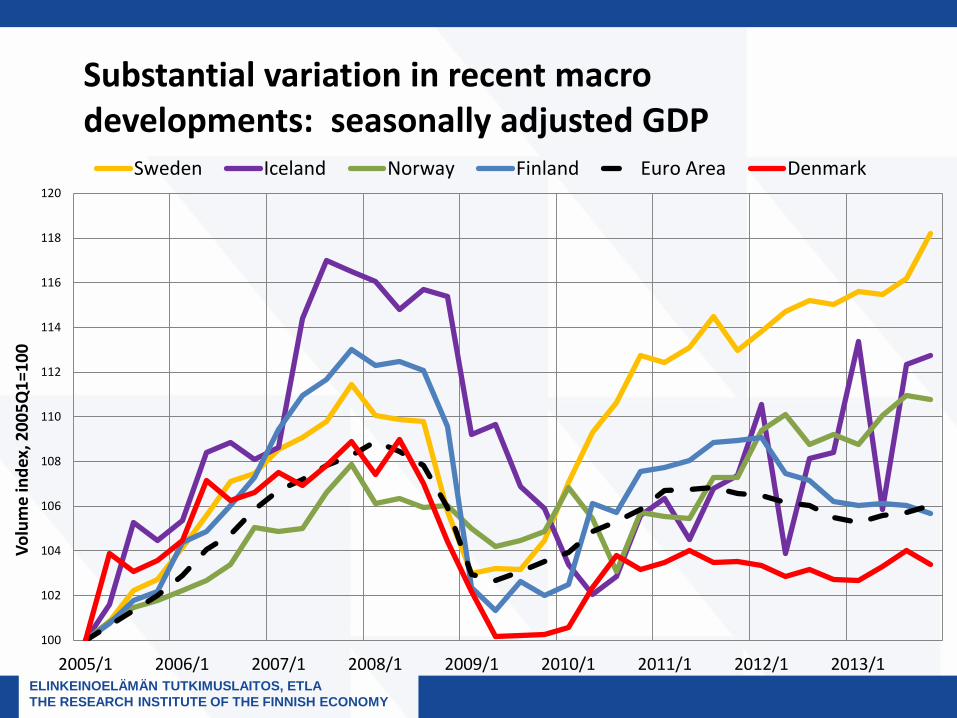

Substantial variation in recent macro developments: seasonally adjusted GDP

Sweden Iceland Norway Finland Euro Area Denmark

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

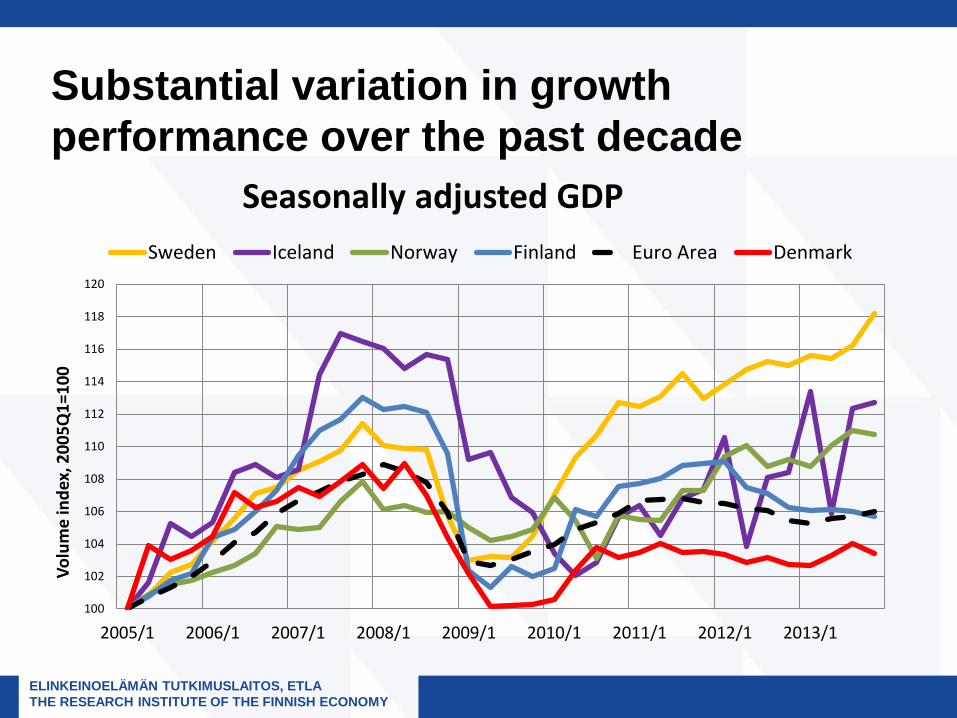

Substantial variation in growth performance over the past decade

100

102

104

106

108

110

112

114

116

118

120

2005/1 2006/1 2007/1 2008/1 2009/1 2010/1 2011/1 2012/1 2013/1

Volu

me

inde

x, 2

005Q

1=10

0

Seasonally adjusted GDP Sweden Iceland Norway Finland Euro Area Denmark

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

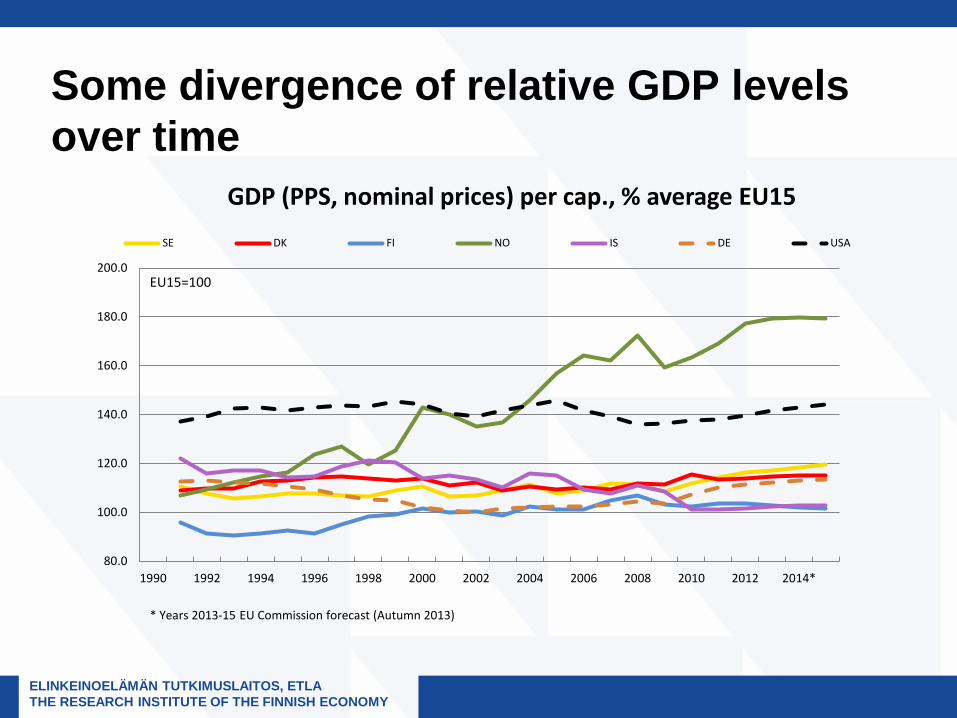

Some divergence of relative GDP levels over time

80.0

100.0

120.0

140.0

160.0

180.0

200.0

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014*

GDP (PPS, nominal prices) per cap., % average EU15 SE DK FI NO IS DE USA

* Years 2013-15 EU Commission forecast (Autumn 2013)

EU15=100

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

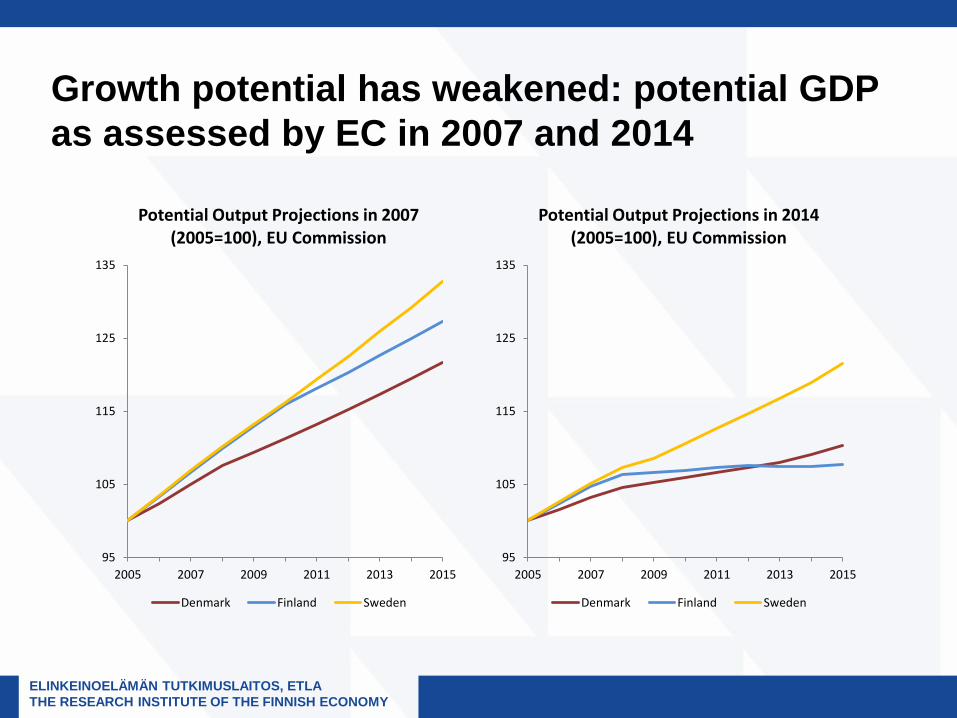

Growth potential has weakened: potential GDP as assessed by EC in 2007 and 2014

95

105

115

125

135

2005 2007 2009 2011 2013 2015

Potential Output Projections in 2007 (2005=100), EU Commission

Denmark Finland Sweden

95

105

115

125

135

2005 2007 2009 2011 2013 2015

Potential Output Projections in 2014 (2005=100), EU Commission

Denmark Finland Sweden

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

The Nordic approach to productivity • Openness to trade: making the most of

comparative advantage, embracing competition • Acceptance of “creative destruction”; little efforts to

save existing companies, “national champions” • Extensive public investments in human capital and

innovation • Red tape on businesses limited/moderate • Good infrastructure • Competitive corporate tax systems, dual income

taxation to spur capital formation

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

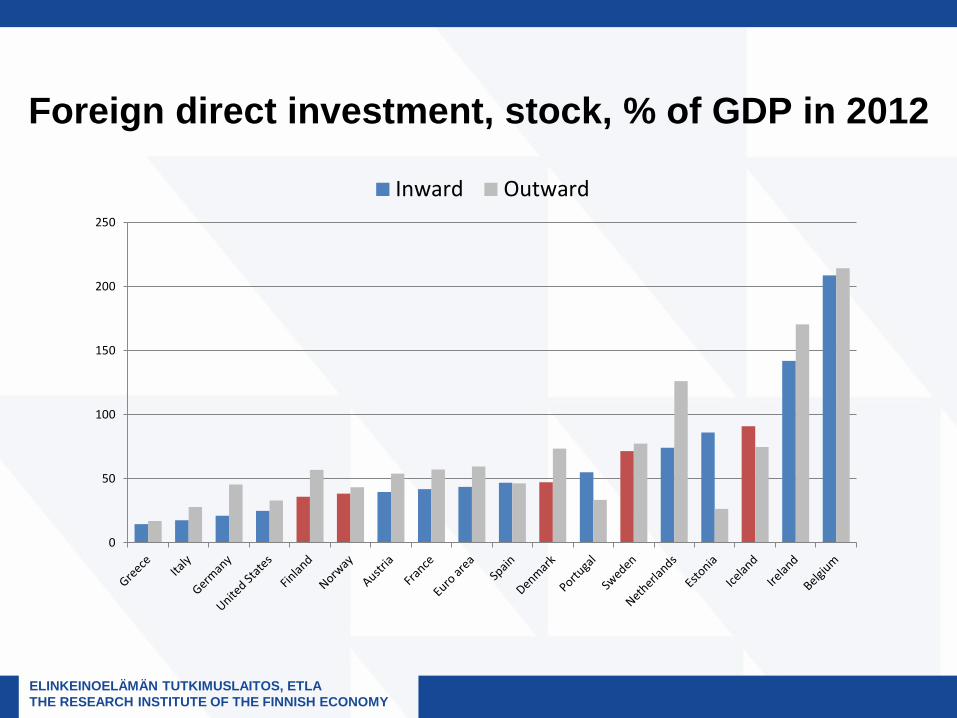

The approach is very much in line with the OECD recommendations. But is it delivering? • Total economy productivity has been reasonably good but

not at the top • Recent productivity growth has been more mediocre or

even weak • Considerable variation among the Nordics • All the Nordics have started to lag further behind the USA

in business sector productivity • The attractiveness of the Nordics as a destination of FDI

not at the top and varies across the countries – Level: FI, NO below average – Recent growth: FI, DEN below average

• Are the Nordics or some of them underperforming?

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

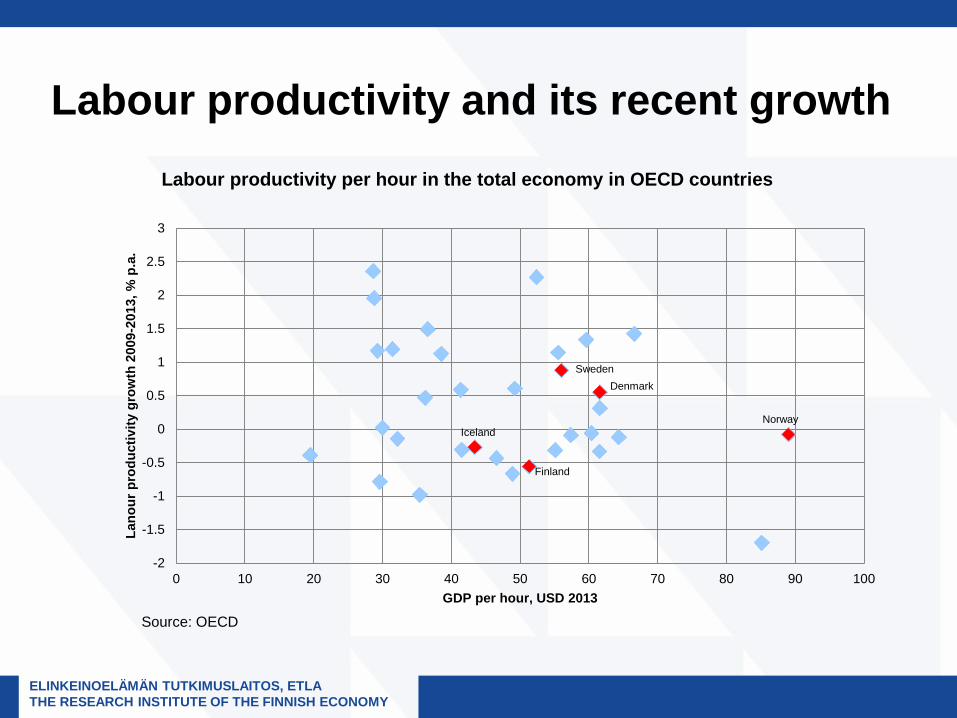

Labour productivity and its recent growth

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

3

0 10 20 30 40 50 60 70 80 90 100

Lano

ur p

rodu

ctiv

ity g

row

th 2

009-

2013

, % p

.a.

GDP per hour, USD 2013

Labour productivity per hour in the total economy in OECD countries

Denmark

Finland

Iceland Norway

Sweden

Source: OECD

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

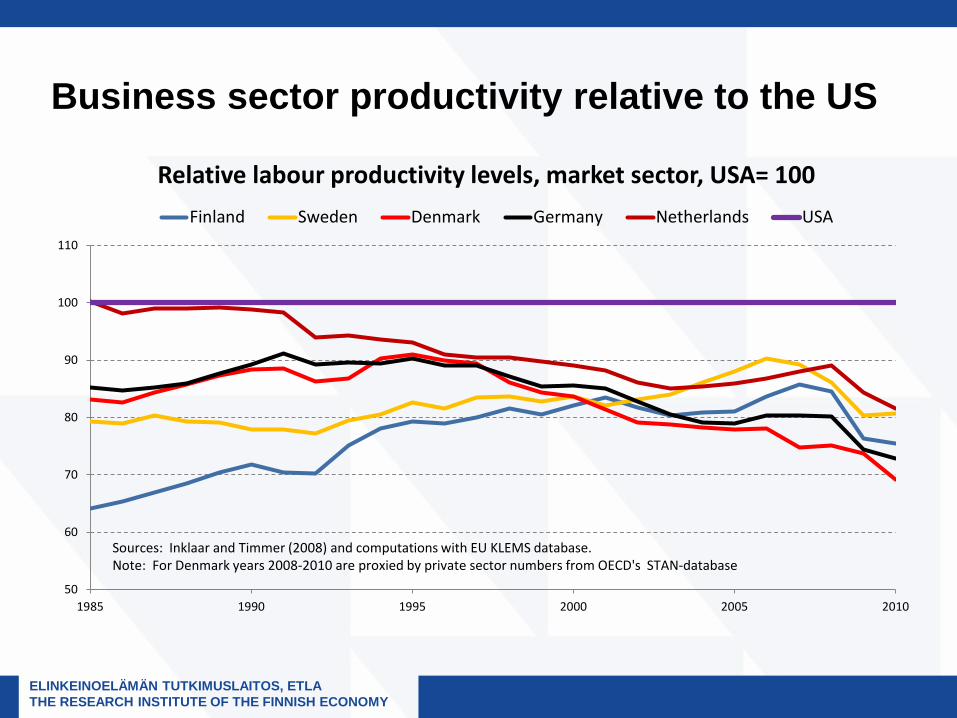

Business sector productivity relative to the US

50

60

70

80

90

100

110

1985 1990 1995 2000 2005 2010

Relative labour productivity levels, market sector, USA= 100 Finland Sweden Denmark Germany Netherlands USA

Sources: Inklaar and Timmer (2008) and computations with EU KLEMS database. Note: For Denmark years 2008-2010 are proxied by private sector numbers from OECD's STAN-database

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

Foreign direct investment, stock, % of GDP in 2012

0

50

100

150

200

250

Inward Outward

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

Potential problems 1. Are incentives for effort and risk-taking sufficient? 2. Can the Nordics keep and attract innovative talents? 3. Are the labour and product market institutions flexible

enough to facilitate structural change? 4. Can popular support for creative destruction be

maintained in the context of continued labour market polarisation and widening income/wealth disparities?

5. Can the Nordics cope with the innovation needs on a broad enough basis or are they forced to specialise in a way that makes them very vulnerable?

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

Incentives, attractiveness as entrepreneurial environment • The outcomes likely to depend on the “package”, rather than

individual elements • Taxes are not wholly out of line and in part compensated by

– Risk-sharing arrangements, efficient, non-corrupt administrations and public services, functioning infrastructure

– Also: liberal attitudes, lack of corruption, trust, general work ethics – Relative predictability of policy (consensus approach)

• Labour and product market flexibility neither best nor worst • Anyway, there are several margins on which to improve

– Improved efficiency of the public sector: less tax pressure – More robust and growth-friendly tax structures – Flexibility of wage formation, labour mobility

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

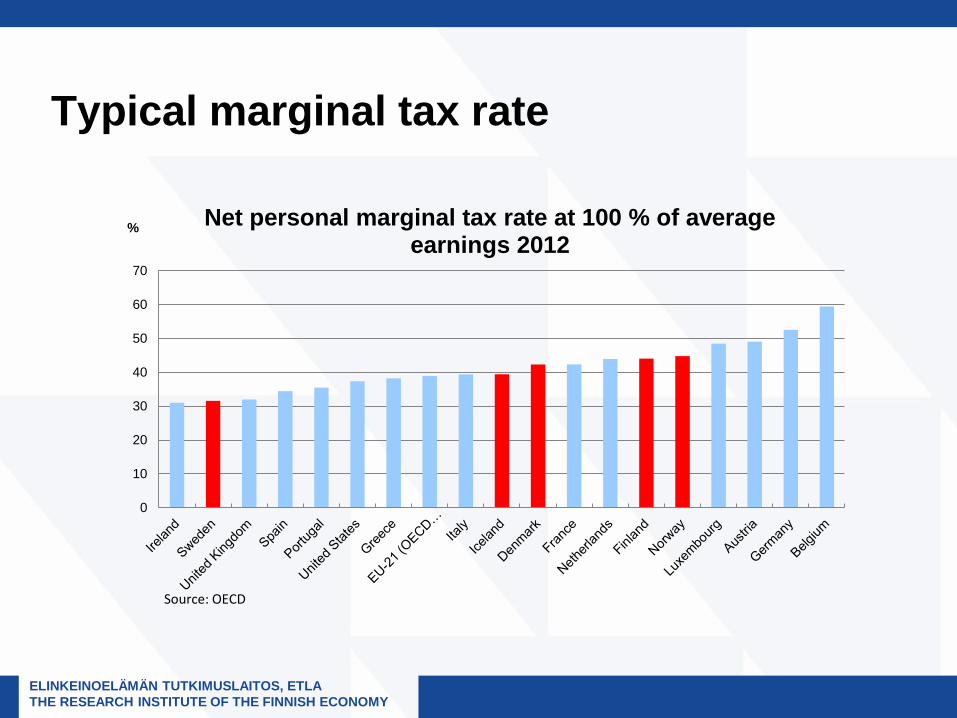

Typical marginal tax rate

0

10

20

30

40

50

60

70

% Net personal marginal tax rate at 100 % of average earnings 2012

Source: OECD

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

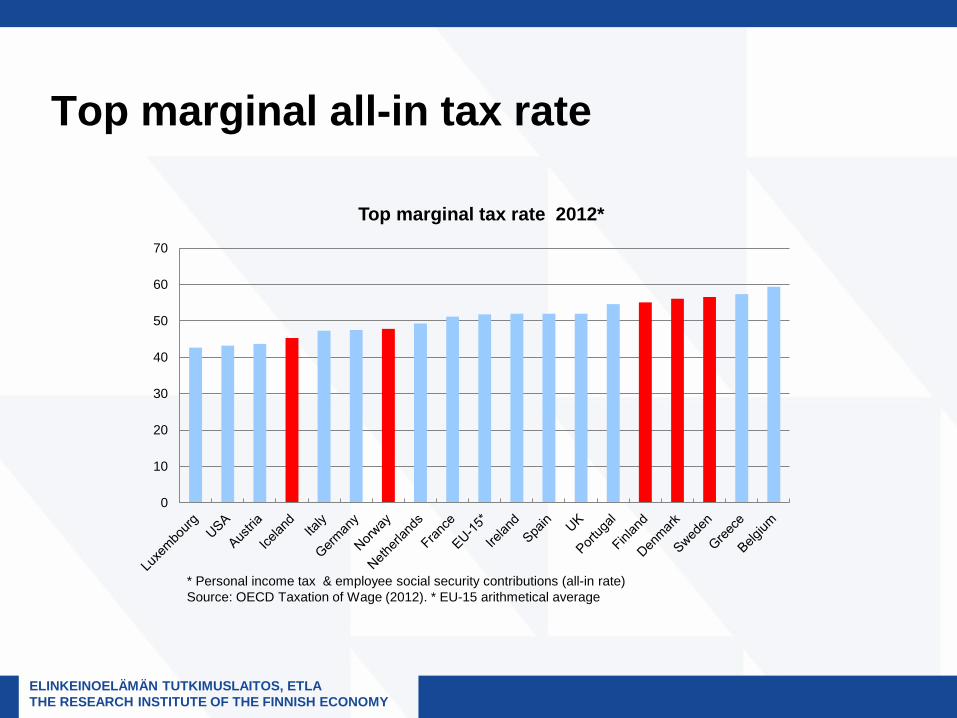

Top marginal all-in tax rate

0

10

20

30

40

50

60

70

Top marginal tax rate 2012*

* Personal income tax & employee social security contributions (all-in rate) Source: OECD Taxation of Wage (2012). * EU-15 arithmetical average

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

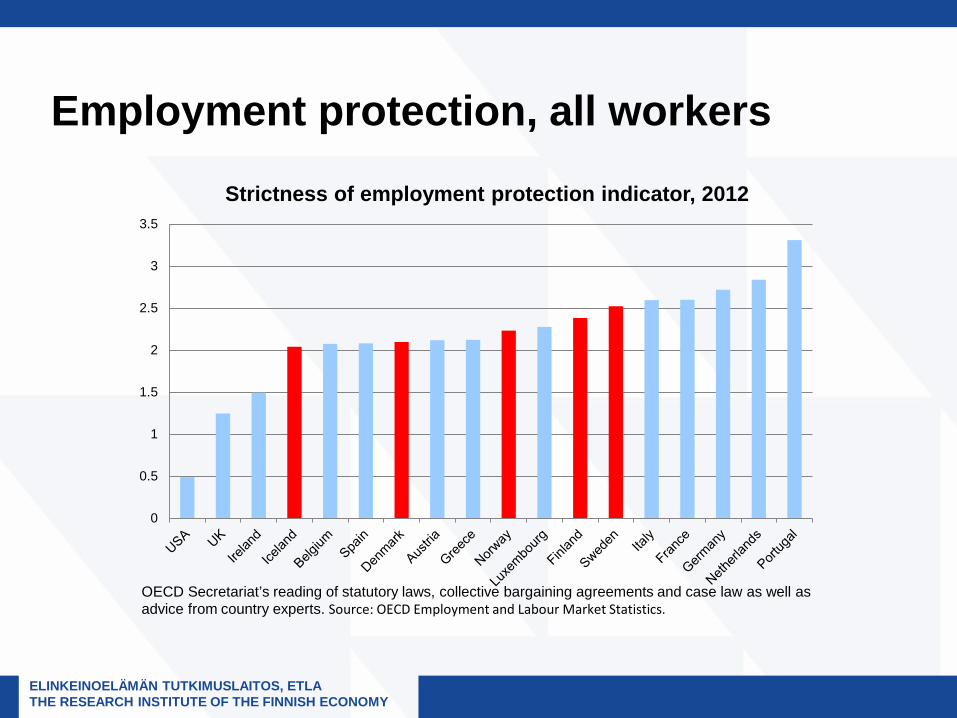

Employment protection, all workers

0

0.5

1

1.5

2

2.5

3

3.5

Strictness of employment protection indicator, 2012

OECD Secretariat’s reading of statutory laws, collective bargaining agreements and case law as well as advice from country experts. Source: OECD Employment and Labour Market Statistics.

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

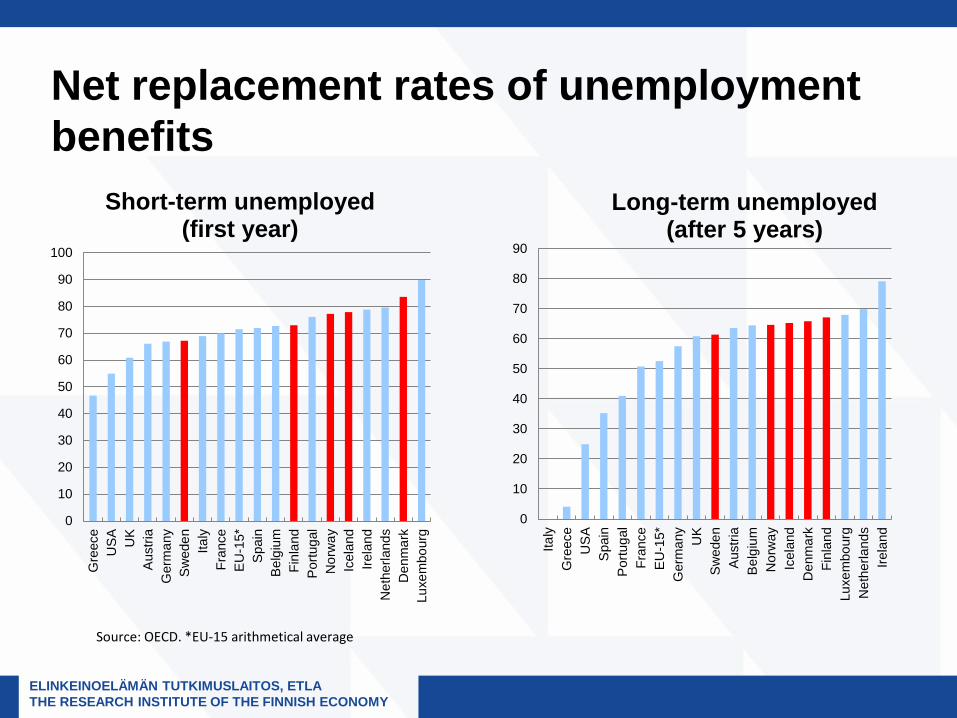

Net replacement rates of unemployment benefits

0

10

20

30

40

50

60

70

80

90

100

Gre

ece

US

AU

KA

ustri

aG

erm

any

Sw

eden

Italy

Fran

ceE

U-1

5*S

pain

Bel

gium

Finl

and

Por

tuga

lN

orw

ayIc

elan

dIre

land

Net

herla

nds

Den

mar

kLu

xem

bour

g

Short-term unemployed (first year)

0

10

20

30

40

50

60

70

80

90

Italy

Gre

ece

US

AS

pain

Por

tuga

lFr

ance

EU

-15*

Ger

man

yU

KS

wed

enA

ustri

aB

elgi

umN

orw

ayIc

elan

dD

enm

ark

Finl

and

Luxe

mbo

urg

Net

herla

nds

Irela

nd

Long-term unemployed (after 5 years)

Source: OECD. *EU-15 arithmetical average

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

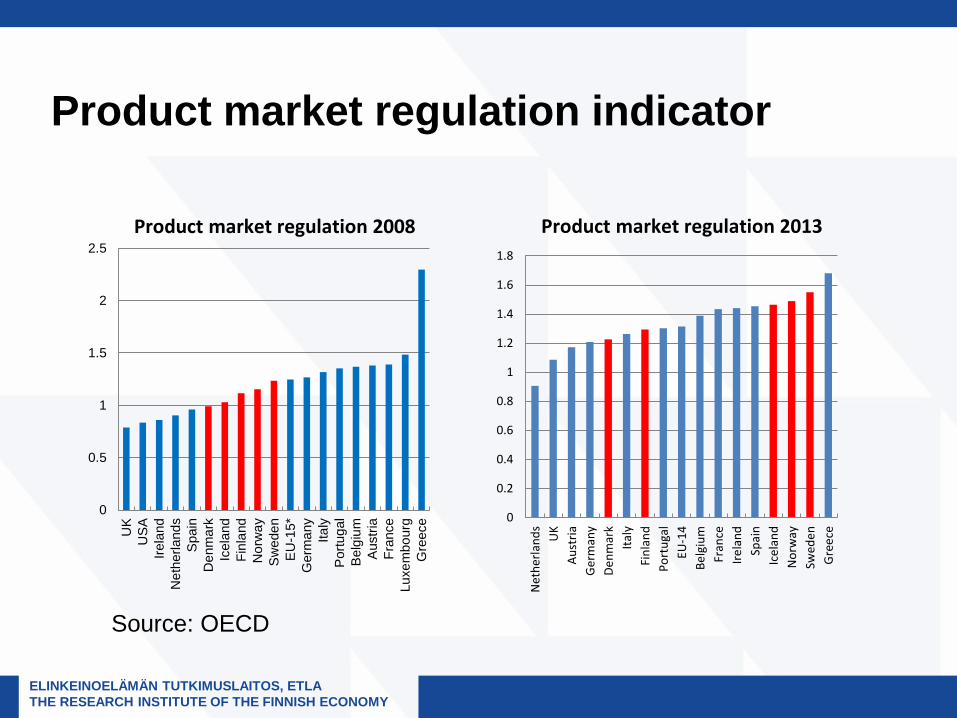

Product market regulation indicator

0

0.5

1

1.5

2

2.5

UK

US

AIre

land

Net

herla

nds

Spa

inD

enm

ark

Icel

and

Finl

and

Nor

way

Sw

eden

EU

-15*

Ger

man

yIta

lyP

ortu

gal

Bel

gium

Aus

tria

Fran

ceLu

xem

bour

gG

reec

e

Product market regulation 2008

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Net

herla

nds

UK

Aust

riaG

erm

any

Denm

ark

Italy

Finl

and

Port

ugal

EU-1

4Be

lgiu

mFr

ance

Irela

ndSp

ain

Icel

and

Nor

way

Swed

enG

reec

e

Product market regulation 2013

Source: OECD

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

Acceptance of structural change • Facilitating factors

– Good basic education, extensive adult education – Generous support for those in need of adjustment (incl. ALMP) – Experience of widely shared benefits of productivity-enhancing

structural change

• Potential fault lines going forward – Strong polarisation of the job market, income disparities – Persistent unemployment (particularly skilled)

• Useful policy responses – More efforts to competence building in general and in the early

years of life in particular – Evidence-based refining the flexicurity approach

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

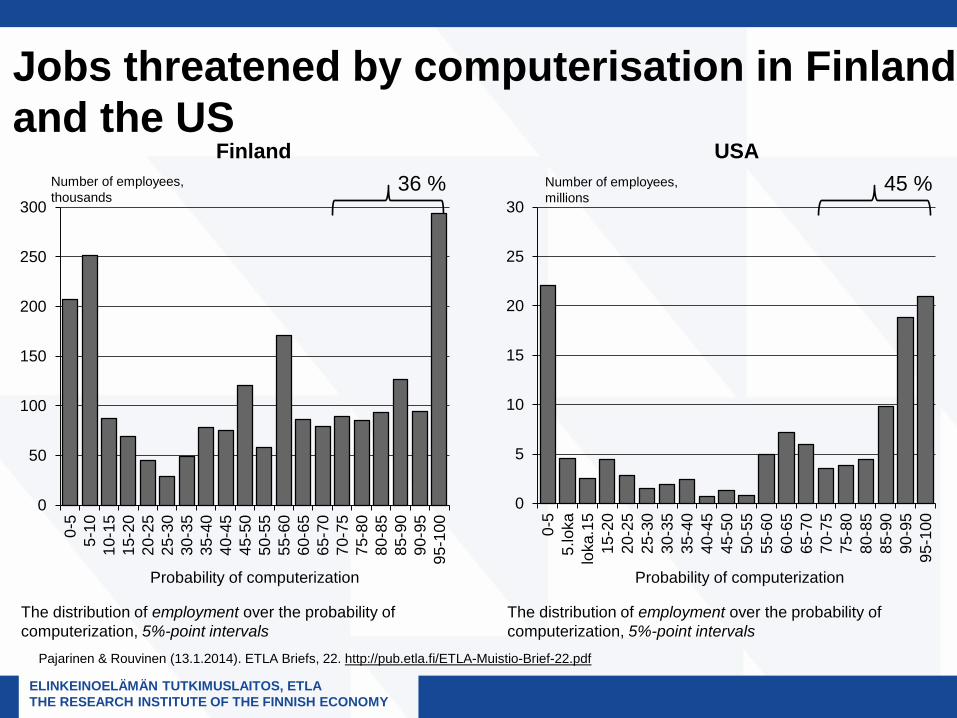

Jobs threatened by computerisation in Finland and the US

Pajarinen & Rouvinen (13.1.2014). ETLA Briefs, 22. http://pub.etla.fi/ETLA-Muistio-Brief-22.pdf

36 %

0

50

100

150

200

250

300

0-5

5-10

10-1

515

-20

20-2

525

-30

30-3

535

-40

40-4

545

-50

50-5

555

-60

60-6

565

-70

70-7

575

-80

80-8

585

-90

90-9

595

-100

The distribution of employment over the probability of computerization, 5%-point intervals

Finland 45 %

0

5

10

15

20

25

30

0-5

5.lo

kalo

ka.1

515

-20

20-2

525

-30

30-3

535

-40

40-4

545

-50

50-5

555

-60

60-6

565

-70

70-7

575

-80

80-8

585

-90

90-9

595

-100

The distribution of employment over the probability of computerization, 5%-point intervals

USA

Probability of computerization Probability of computerization

Number of employees, thousands

Number of employees, millions

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

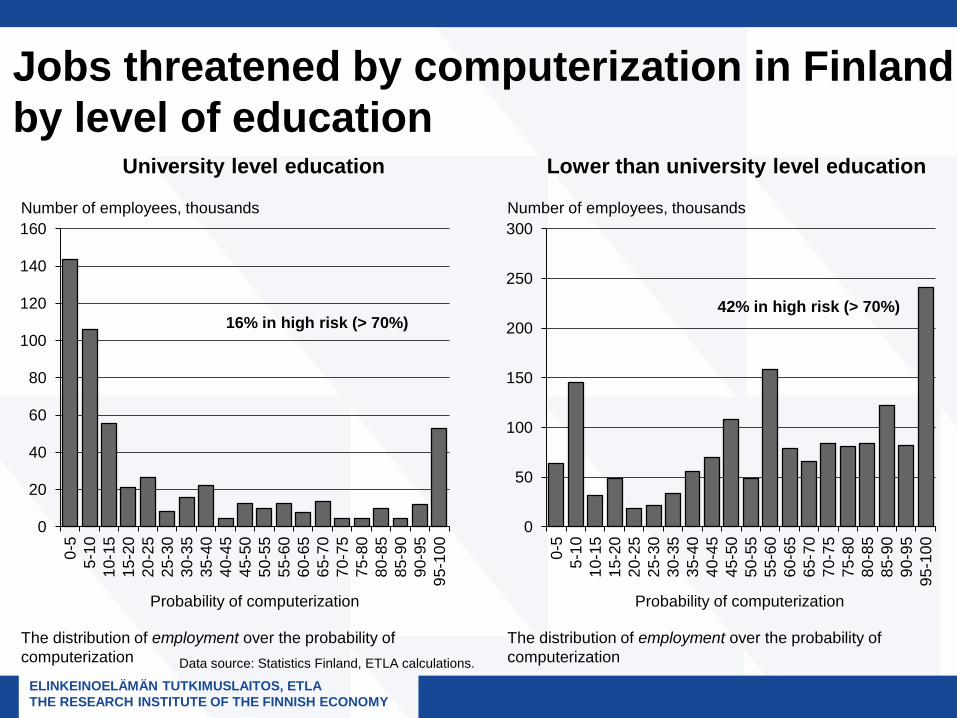

Jobs threatened by computerization in Finland by level of education

Data source: Statistics Finland, ETLA calculations.

0

20

40

60

80

100

120

140

160

0-5

5-10

10-1

515

-20

20-2

525

-30

30-3

535

-40

40-4

545

-50

50-5

555

-60

60-6

565

-70

70-7

575

-80

80-8

585

-90

90-9

595

-100

The distribution of employment over the probability of computerization

University level education

0

50

100

150

200

250

300

0-5

5-10

10-1

515

-20

20-2

525

-30

30-3

535

-40

40-4

545

-50

50-5

555

-60

60-6

565

-70

70-7

575

-80

80-8

585

-90

90-9

595

-100

The distribution of employment over the probability of computerization

Lower than university level education

Number of employees, thousands Number of employees, thousands

16% in high risk (> 70%) 42% in high risk (> 70%)

Probability of computerization Probability of computerization

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

The vulnerability of the small economies close to the technology frontier?

• Potential problem: small specialised economies could be vulnerable to radical disruptions in cutting-edge technology and strategic choices of multinationals – Example: Finland and Nokia

• Are the Nordics highly specialised? Yes and no • Are they dependent on a few large companies? Yes, but

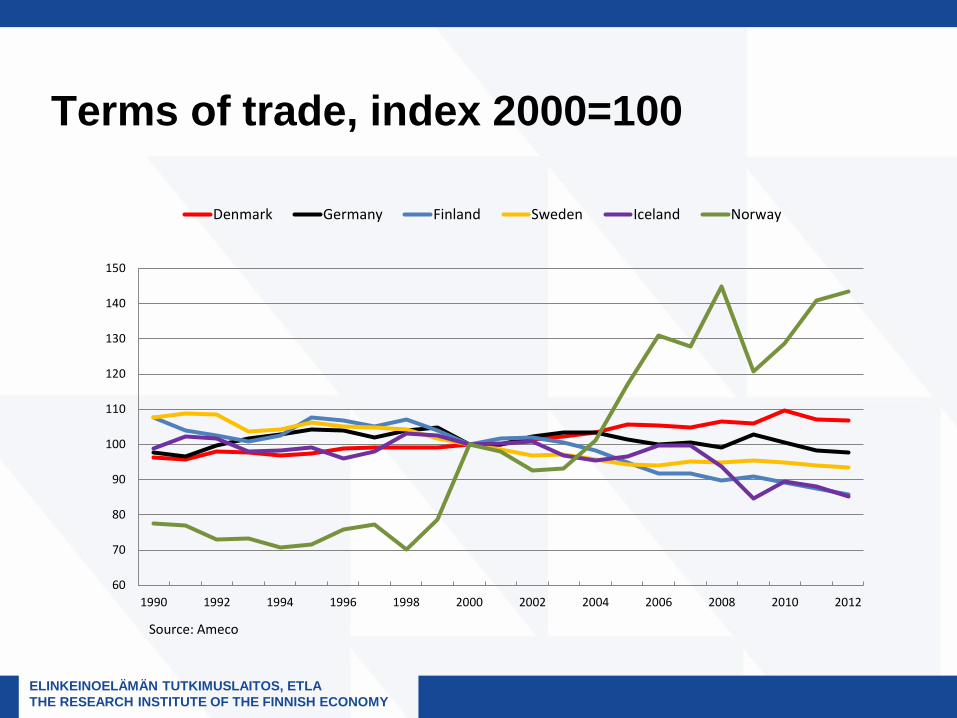

not in the same degree • Can a good terms of trade development compensate for

weak productivity growth? One should not trust that

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

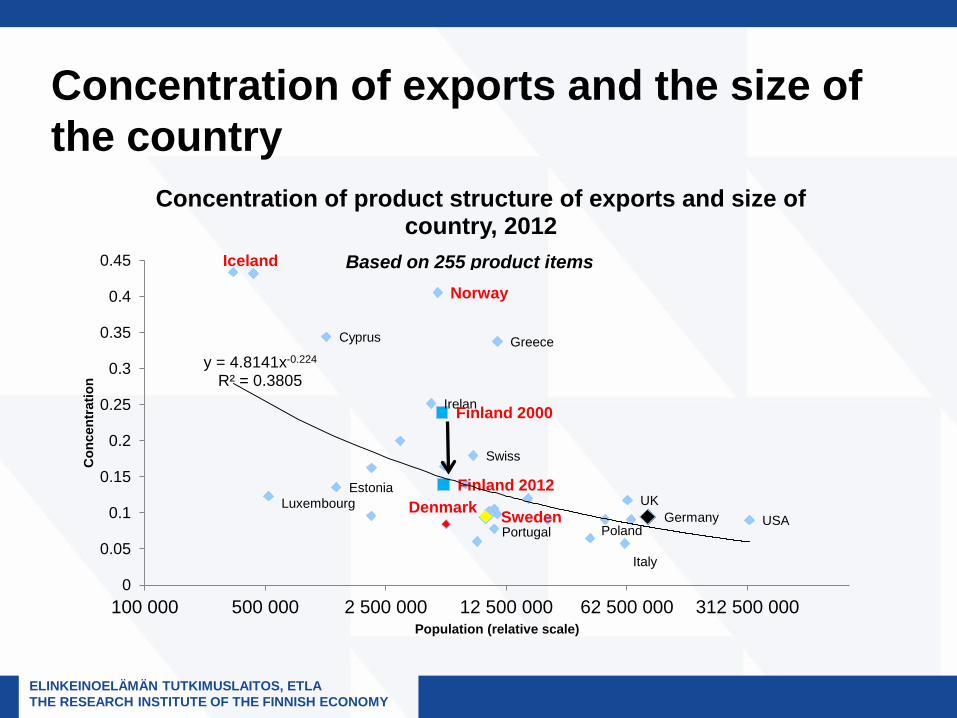

Concentration of exports and the size of the country

Cyprus

Denmark Estonia Finland 2012

Germany

Greece

Iceland

Irelan

Italy

Luxembourg

Norway

Poland Portugal Sweden

Swiss

UK USA

Finland 2000

y = 4.8141x-0.224 R² = 0.3805

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

100 000 500 000 2 500 000 12 500 000 62 500 000 312 500 000

Con

cent

ratio

n

Population (relative scale)

Concentration of product structure of exports and size of country, 2012

Based on 255 product items

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

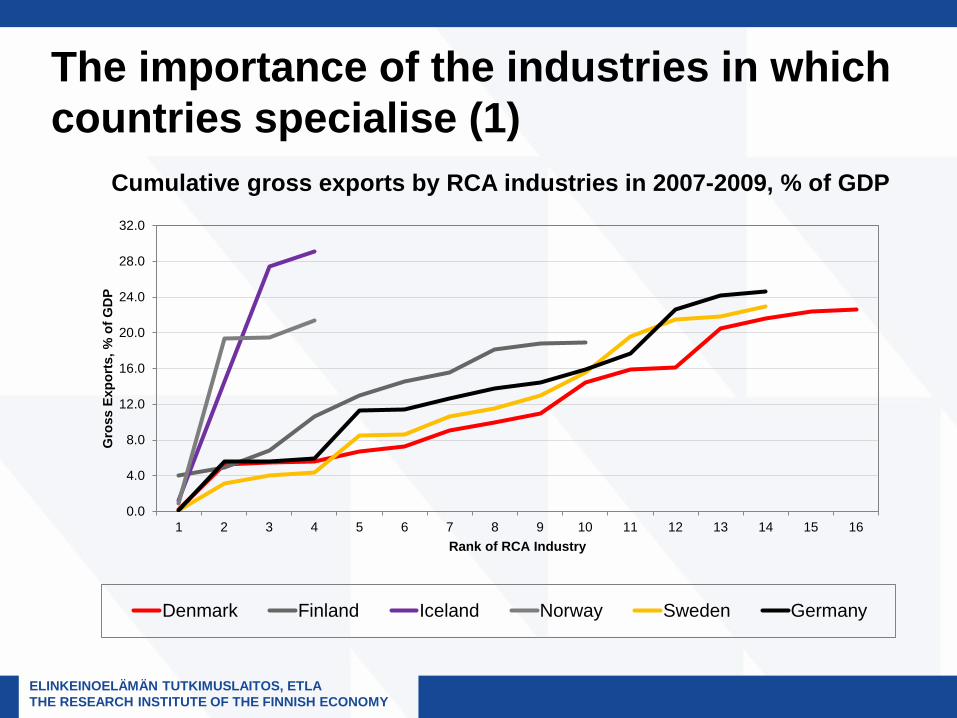

The importance of the industries in which countries specialise (1)

0.0

4.0

8.0

12.0

16.0

20.0

24.0

28.0

32.0

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Gro

ss E

xpor

ts, %

of G

DP

Rank of RCA Industry

Denmark Finland Iceland Norway Sweden Germany

Cumulative gross exports by RCA industries in 2007-2009, % of GDP

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

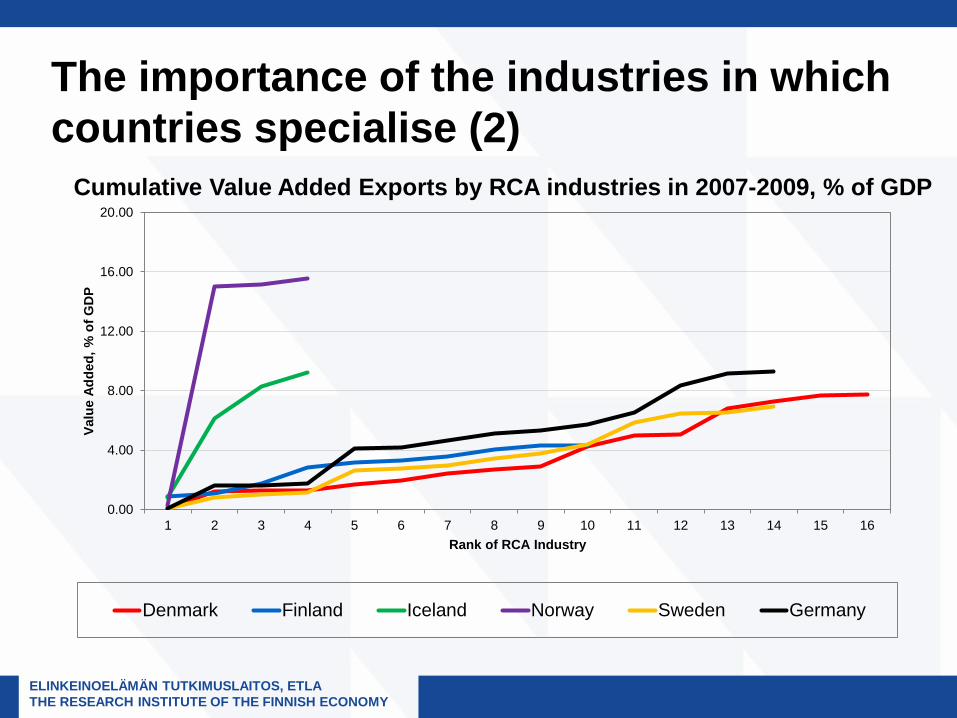

The importance of the industries in which countries specialise (2)

Cumulative Value Added Exports by RCA industries in 2007-2009, % of GDP

0.00

4.00

8.00

12.00

16.00

20.00

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Valu

e Ad

ded,

% o

f GD

P

Rank of RCA Industry

Denmark Finland Iceland Norway Sweden Germany

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

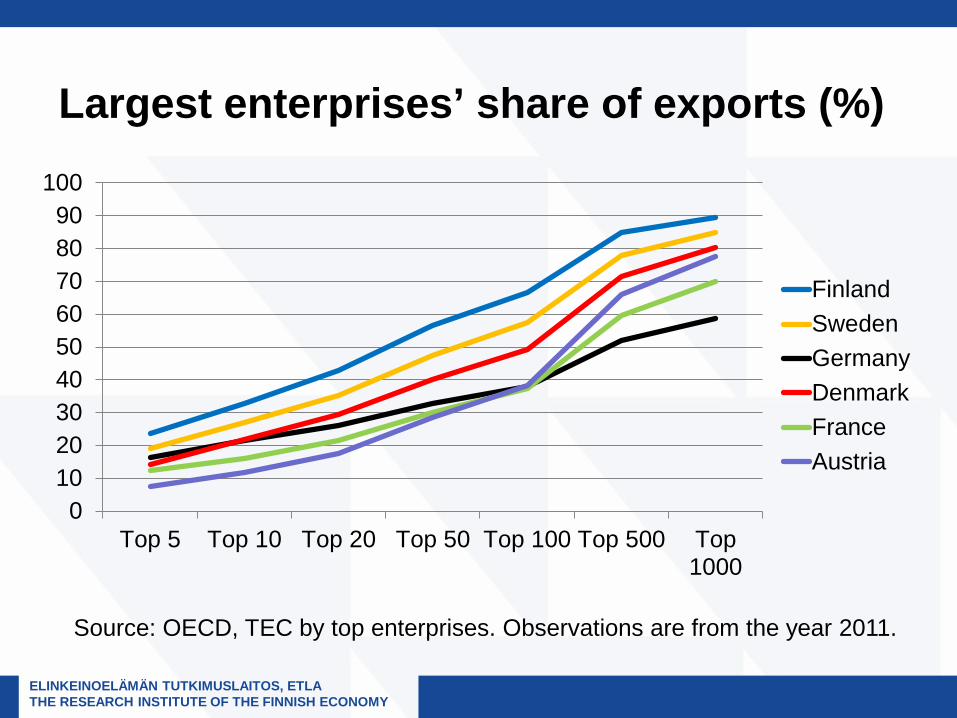

Largest enterprises’ share of exports (%)

0102030405060708090

100

Top 5 Top 10 Top 20 Top 50 Top 100 Top 500 Top1000

FinlandSwedenGermanyDenmarkFranceAustria

Source: OECD, TEC by top enterprises. Observations are from the year 2011.

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

Terms of trade, index 2000=100

60

70

80

90

100

110

120

130

140

150

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Denmark Germany Finland Sweden Iceland Norway

Source: Ameco

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

Ways to support innovation without taking excessive risks • Difficult to see a sensible alternative to a neutral policy

approach of not picking winners, emphasis on competition • Nevertheless some choices in the use of scarce public

resources necessary – Existing areas of strength have already passed a market test – Support development of general purpose technology rather than

very specific applications

• Support entrepreneurial ecosystems – Incubators, start-up programmes, cluster programmes – Development of domestic capital markets to provide an alternative

for foreign takeovers too early

• Co-operation between national funding agencies?

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

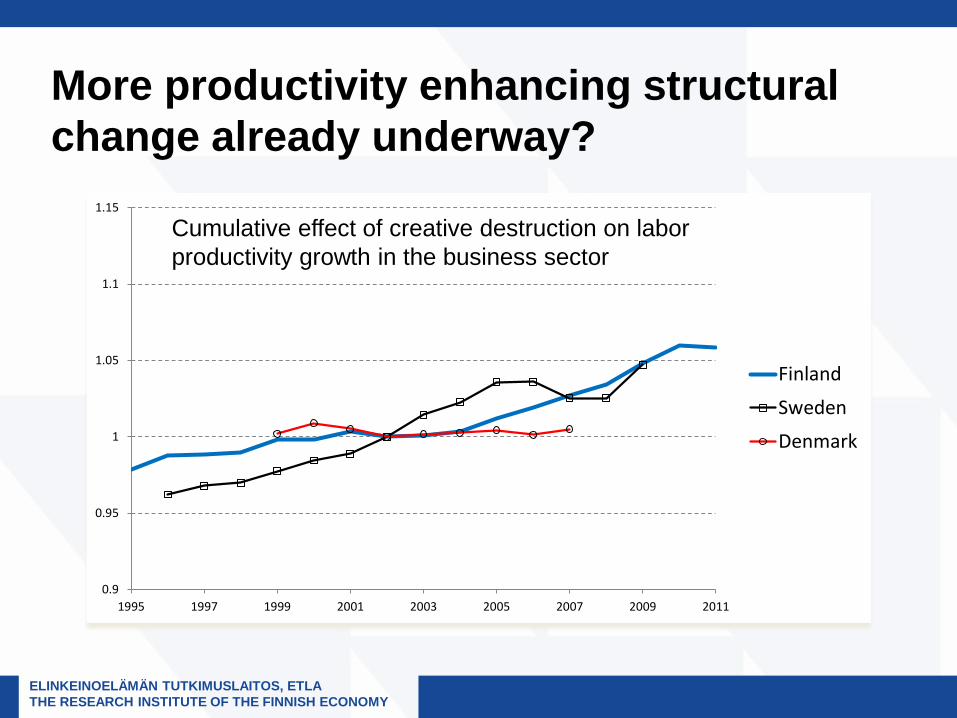

More productivity enhancing structural change already underway?

0.9

0.95

1

1.05

1.1

1.15

1995 1997 1999 2001 2003 2005 2007 2009 2011

Finland

Sweden

Denmark

Cumulative effect of creative destruction on labor productivity growth in the business sector

ELINKEINOELÄMÄN TUTKIMUSLAITOS, ETLA THE RESEARCH INSTITUTE OF THE FINNISH ECONOMY

Concluding remarks

• The Nordics’ point of departure to achieve high productivity is in many ways good

• But they have not performed recently quite as well as one might have expected and face challenges going forward

• There is potential to improve framework conditions • Key issue: maintenance of acceptance/support for

structural change to fully utilize the existing strengths