Embed Size (px)

Citation preview

ACG6295

Please do not leave the classroom while class is in session.

ACG6295

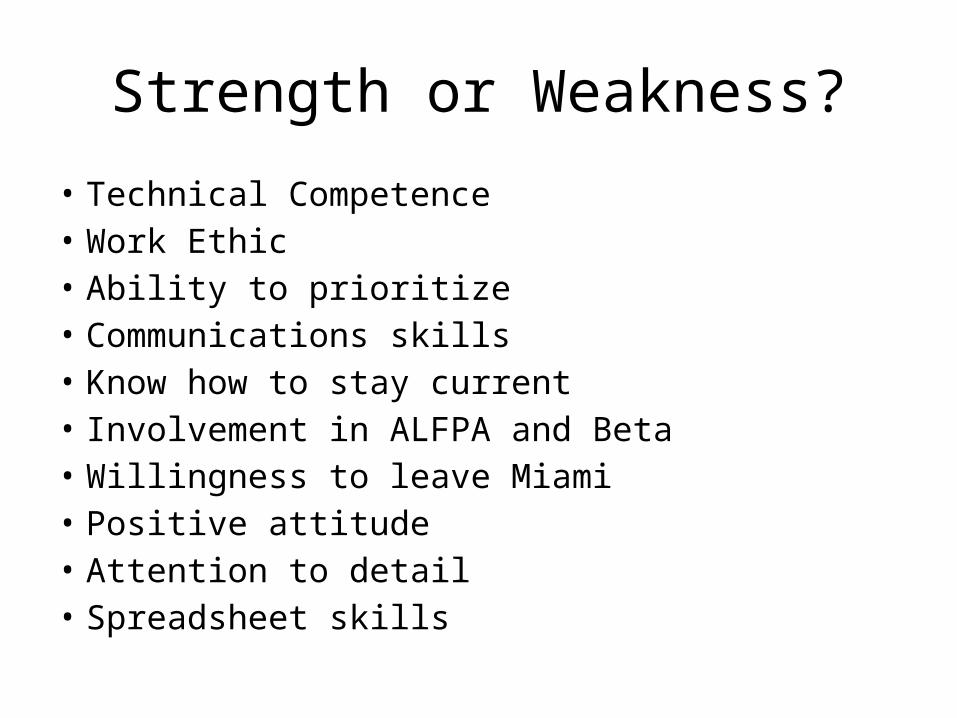

Interviewed 50 partners in Miami and asked

What are the strengths and weaknesses of the average FIU

MACC graduate?

Strength or Weakness?

• Technical Competence• Work Ethic• Ability to prioritize• Communications skills• Know how to stay current• Involvement in ALFPA and Beta• Willingness to leave Miami• Positive attitude• Attention to detail• Spreadsheet skills

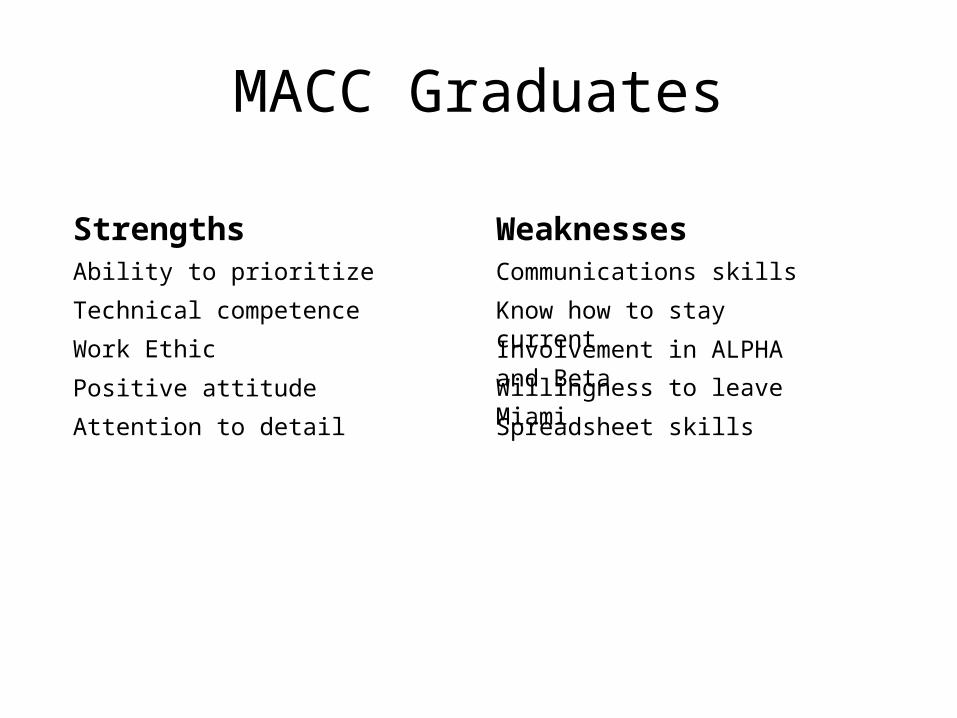

MACC Graduates

Strengths WeaknessesAbility to prioritize

Technical competence

Work Ethic

Positive attitude

Communications skills

Know how to stay current

Involvement in ALPHA and Beta

Willingness to leave Miami

Spreadsheet skillsAttention to detail

We will address currency and communications

• The objectives of this course include:– Evaluate current Exposure Drafts related to

financial reporting and explain, if fully implemented, why they will affect financial transparency.

– Explain and interpret changes to the Codification.– Assess the decision usefulness of technical

pronouncements under consideration for adoption.

– Communicate technically advanced information

Financial Reporting• Our perspective is external financial reporting using

financial statements prepared under US GAAP• The primary objective of external financial reporting

under US GAAP is to provide information that is useful to investors, creditors and others in making future decisions

• We prepare the statements such that a reasonably educated consumer exercising due diligence will understand them

• We should also consider the transparency of the information we provide in the financial statements

6

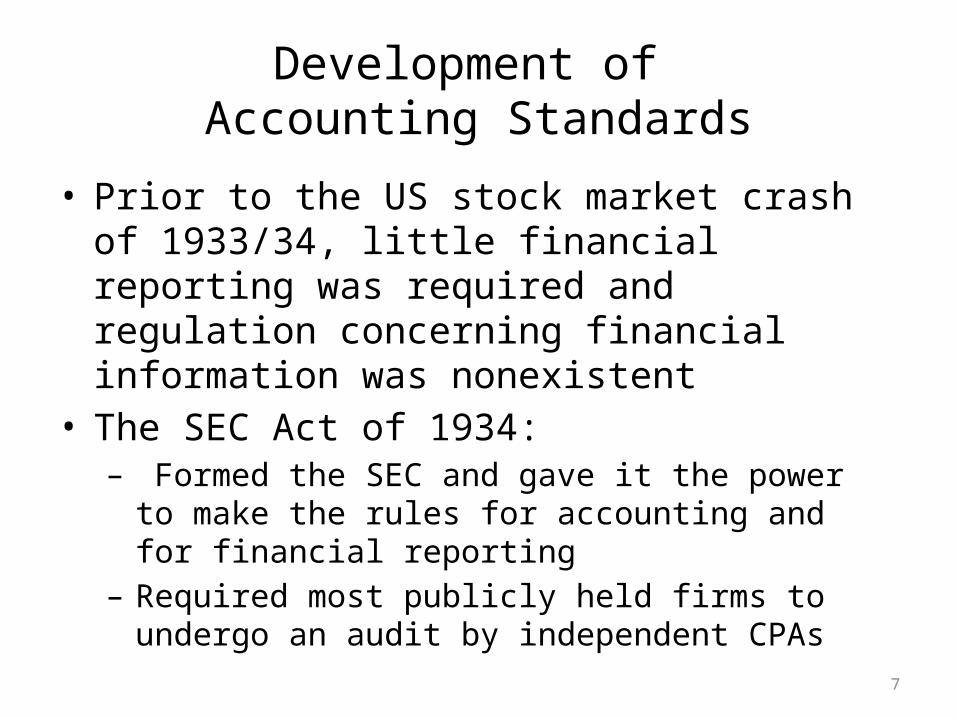

Development of Accounting Standards

• Prior to the US stock market crash of 1933/34, little financial reporting was required and regulation concerning financial information was nonexistent

• The SEC Act of 1934:– Formed the SEC and gave it the power to make the rules

for accounting and for financial reporting– Required most publicly held firms to undergo an audit by

independent CPAs

7

Who Sets the Standards?

• The SEC (a public sector entity) delegated rule making authority to the AICPA (a private sector entity). – AICPA formed subcommittees called Committee on

Accounting Procedure (CAP) and later Accounting Principles Board (APB) to write standards

– When accounting issues became too complex for a part time committee, the Financial Accounting Standards Board (FASB) was established

– The SEC maintains enforcement and provides Staff Accounting Bulletins that interpret FASB standards

8

Who Sets the Standards?

• Accounting standards are written in the private sector, but the SEC provides public oversight for the standards– FASB, with SEC oversight, writes the standards for external

financial reporting– The SEC identifies areas in which additional information is

needed and may request additional information from registrants

– The SEC also sets standards for registrant filings such as the 10K, 10Q, and others

• If individual firms submit statements with “irregularities”, SEC issues deficiency letter with issues that must be resolved

9

Who Sets the Standards?

• In summary, many groups have been involved in writing and interpreting standards– FASB, its governmental group GASB, and its Emerging Issues

Task Force (EITF)– AICPA created a group called the Accounting Standards

Executive Committee (AcSEC) to ensure a voice in the process. They also provide information about regulatory matters ( http://www.aicpa.org/sarbanes/index.asp ) and CPA licensure

– SEC provides oversight (http://www.sec.gov/about/offices/oca.htm)

– Congress provides political pressure when FASB makes unpopular rulings

10

11

US Generally Accepted Accounting Principles (GAAP)

• “GAAP” is a technical term that encompasses the conventions, rules, and procedures necessary to define accepted accounting practice at a particular time

• It includes not only broad guidelines of general application, but also detailed practices and procedures. Those conventions, rules, and procedures provide a standard by which to measure financial presentations

• GAAP is presented as a hierarchy of guidance.

• Sometimes, the guidance from one source contradicts guidance from another source.

12

FAS 162 – Issued May, 2008• The sources of accounting principles that are generally accepted are

categorized in descending order of authority as defined by Financial Accounting Standard (FAS) 162: – Category A

• Statements of Financial Accounting Standards (FAS) and Interpretations (FIN)

• AICPA Accounting Research Bulletins (ARB) and Accounting Principles Board (APB) Opinions that are not superseded by action of the FASB

• Derivatives Implementation Group Issues (DIG)• FASB Staff Positions (FSP)• U.S. Securities and Exchange Commission Staff Accounting

Bulletins (SAB)

13

FAS 162 - continued• The sources of accounting principles that are generally

accepted are categorised in descending order of authority as

follows: – Category B

• FASB Technical Bulletins • AICPA Industry Audit and Accounting Guides *• AICPA Statements of Position * * If cleared by the FASB

14

FAS 162 - continued– Category C

• AICPA Accounting Standards Executive Committee Practice Bulletins that have been cleared by the FASB and

• Consensus positions of the FASB Emerging Issues Task Force (EITF)– often deal with issues not explicitly covered elsewhere

15

FAS 162

– Category D• Implementation guides (Q&As) published by the FASB staff• AICPA accounting interpretations• Practices that are widely recognised and prevalent either

generally or in the industry

16

17

Applying the Hierarchy Before July 1, 2009

• Compliance with category A items is mandatory

• Auditors may not express an unqualified opinion if there is a material departure from category A

• If a treatment is not specified in category A proceed to categories B, C, or D using the treatment specified by the source in the highest category

• If a prescribed treatment in category B, C, or D is relevant to the circumstances, that treatment must be followed unless there is justification that another treatment is generally accepted

Applying Guidance after July 1, 2009

• Confusion about the hierarchy, along with the presumed convergence of US GAAP and International Financial Accounting Standards (IFRS) led to a new system

• FASB has codified all guidance.

18

www.fasb.org

19

Sign in to access the Codification

• Look for the link to the Codification on the right hand side of the page (blue arrow on prior slide)

• Click for free student access to the Codification.

20

You should then see:

21

Click on “Academic User”

• We provide you with free access to the Codification only while you are a student.

• Your user name is: • Your password is:

22

You will see:

23

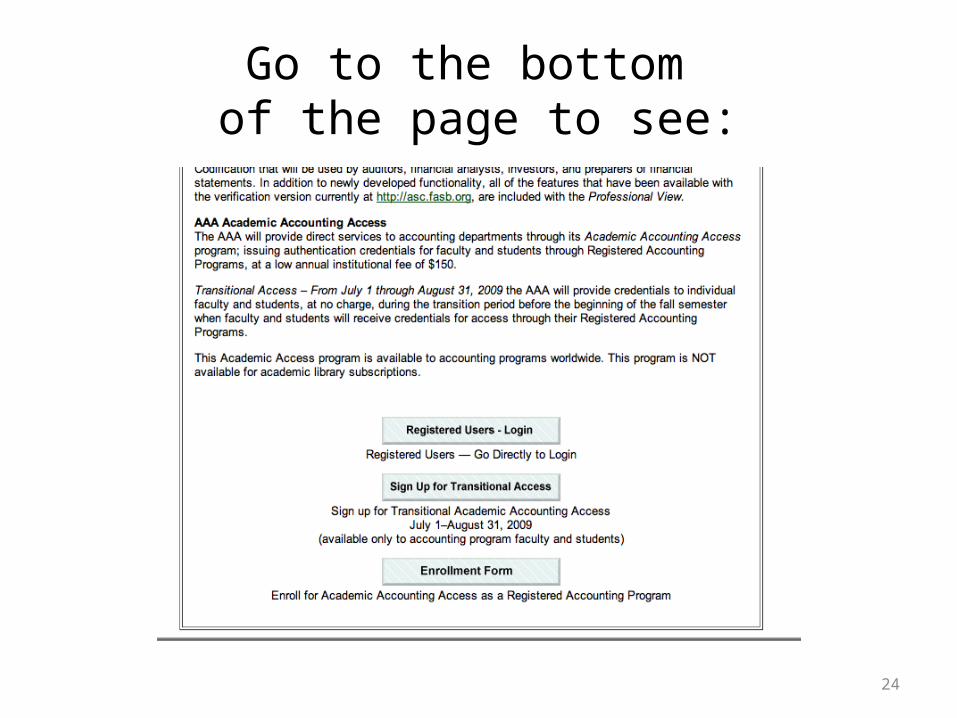

Go to the bottom of the page to see:

24

Click on Registered User to see:

25

User Name and Password

• Your user name is: AAA52091• Your password is: FvLxvv9• Click on the link for the Codification. You will

then see the screen on the next slide.

26

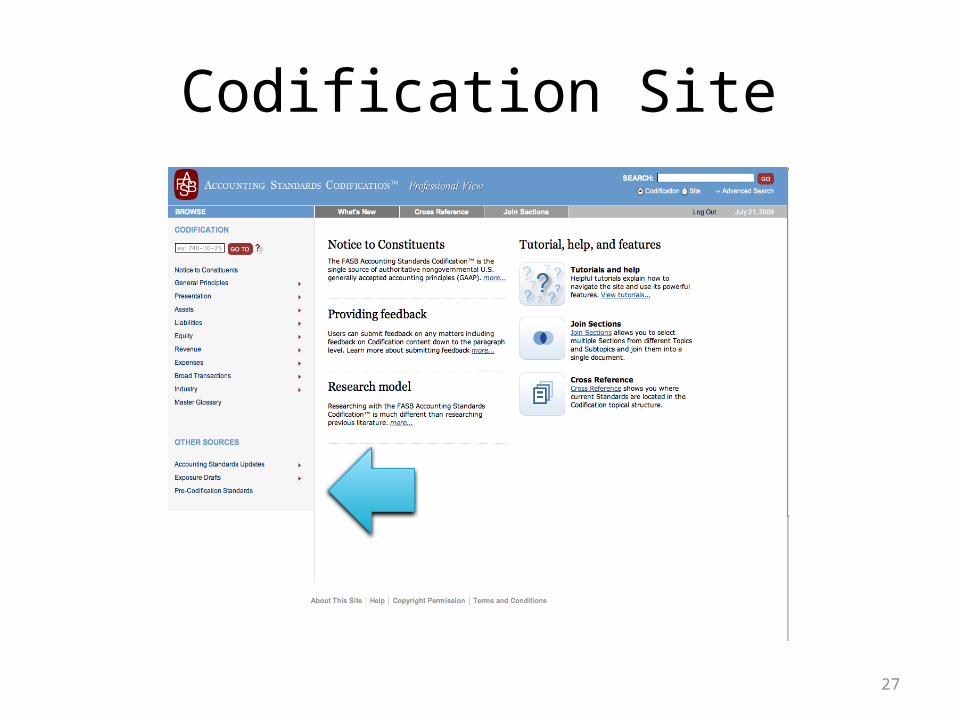

Codification Site

27

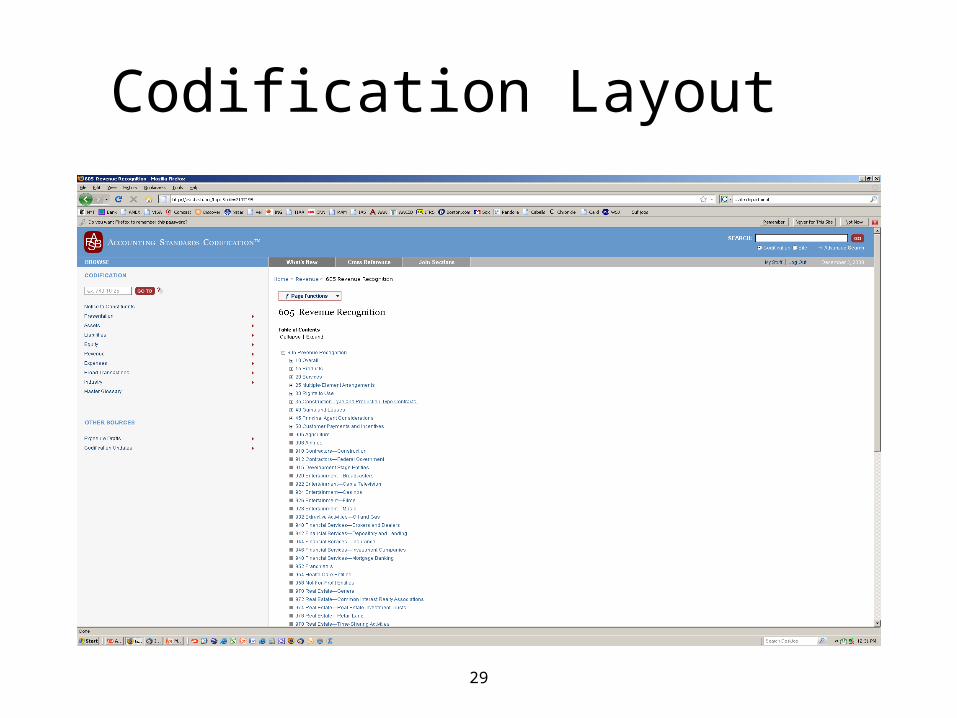

Navigating the Codification

• Look at the list on the left side of the page• This is the navigation panel for all US GAAP

authoritative guidance• Go to Revenue Recognition, Codification

section 605

28

Codification Layout

29

Expanded Layout

30

Referencing US GAAP

• Your text, your professors and your employers will probably use some mix of the old way of referencing (i.e., FAS 133) and the Codification method of referencing

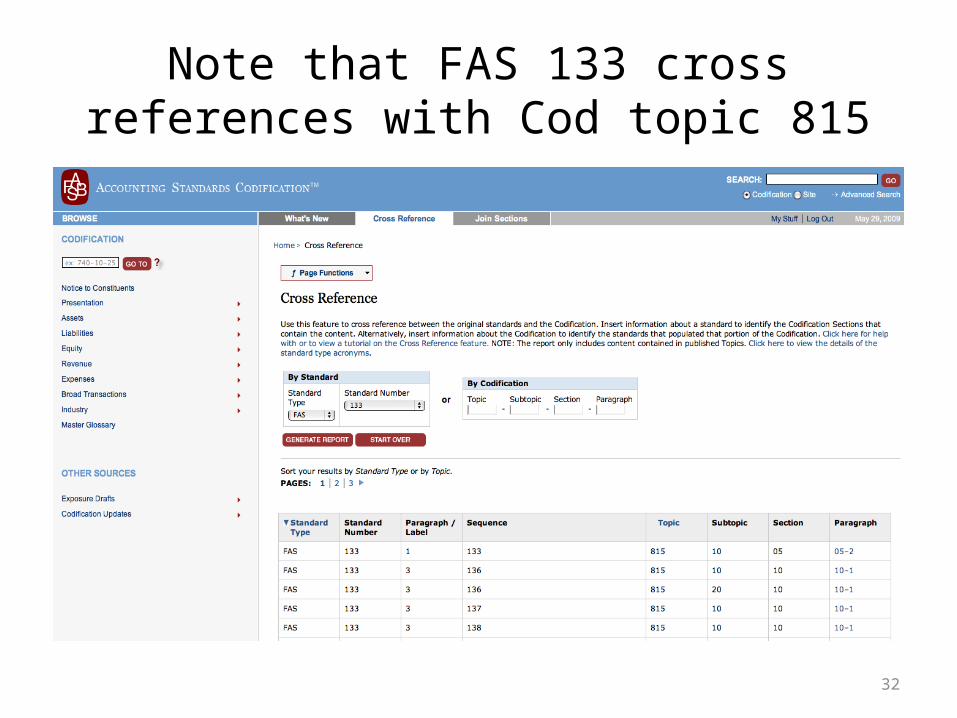

• You can cross reference by using the cross reference tool on the codification site

31

Note that FAS 133 cross references with Cod topic 815

32

33

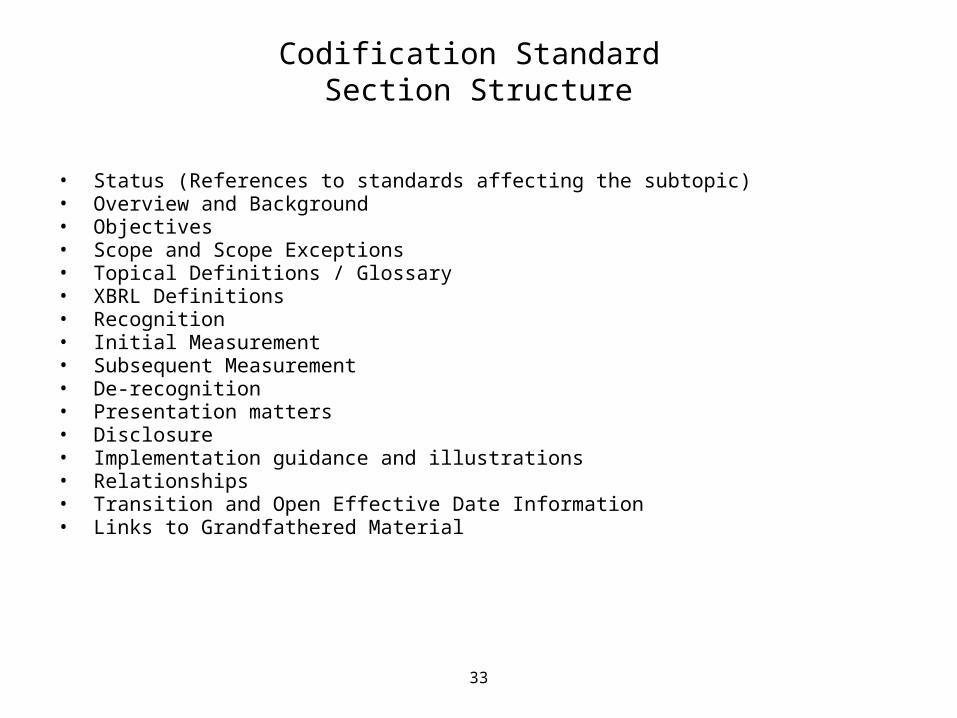

Codification Standard Section Structure

• Status (References to standards affecting the subtopic)• Overview and Background• Objectives• Scope and Scope Exceptions• Topical Definitions / Glossary• XBRL Definitions• Recognition • Initial Measurement • Subsequent Measurement • De-recognition • Presentation matters• Disclosure• Implementation guidance and illustrations• Relationships • Transition and Open Effective Date Information• Links to Grandfathered Material

34

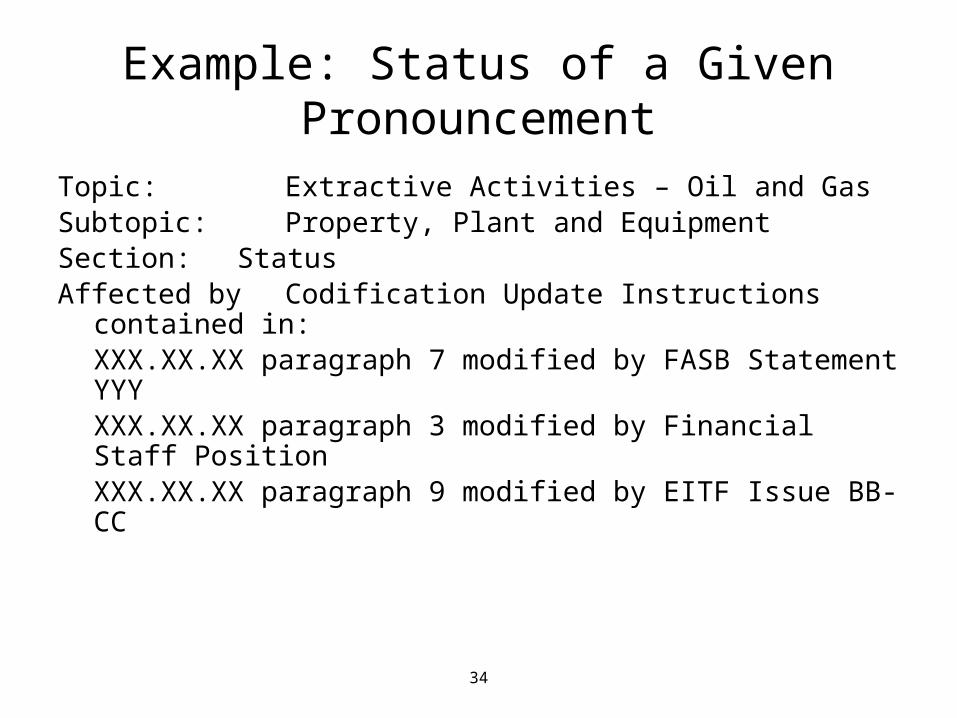

Example: Status of a Given Pronouncement

Topic: Extractive Activities – Oil and GasSubtopic: Property, Plant and EquipmentSection: StatusAffected by Codification Update Instructions contained in:

XXX.XX.XX paragraph 7 modified by FASB Statement YYY XXX.XX.XX paragraph 3 modified by Financial Staff PositionXXX.XX.XX paragraph 9 modified by EITF Issue BB-CC

35

Overview and Background• Overview and background will contain material generally considered

useful to a user in understanding typical situations required by the standard.

• Example from Oil and Gas topic:

• This Subtopic establishes standards of financial accounting and reporting for the oil and gas producing activities of a business entity. Those activities involve the acquisition of mineral interest in properties, exploration (including prospecting), development, and production of crude oil, including condensate and natural gas liquids, and natural gas.

36

Objectives

• The Objectives section will state the high-level objectives that the subtopic is trying to accomplish or attain.

37

Scope and Scope Exceptions

• Below is an illustrative structure of a Scope section of the Overall subtopic of Extractive Activities — Oil and Gas:

• Overall guidance: “The Subtopics within Extractive Activities—Oil and Gas Topic provide incremental industry guidance for the entities defined in the Scope Section. Entities within the scope of this industry shall also apply the applicable standards not included in this Topic.”

• Entity-based scope: “This Topic applies only to entities with oil and gas producing activities.”

• Transactions: This will several types of transactions that are excluded from the scope of this topic.

38

Topical Definitions / Glossary

• This section contains a definition of the terms specific to the topic and would include the definitions of words like: proved oil and gas reserves, reservoir, field, service well, and others.

• The goal is to have one glossary for all of the codification

39

XBRL – Extensible Business Reporting Language

• XBRL taxonomy announced 2008.– A system of data tags, to enable the viewer to

rearrange, summarize financial data in alternative formats.

• Interactive XBRL viewer:– www.sec.gov/xbrl

40

Recognition

• Recognition generally addresses when a transaction is recorded

• Cod 932-360-25-4 is an example of recognition.

• “An enterprise’s oil and gas producing activities involve certain special types of assets. Costs of those assets shall be capitalized when incurred…”

41

Initial Measurement

• Initial Measurement addresses the criteria and amounts used to measure a particular item at date of recognition (tells us how much is recognized).

• Section 310-10-30-2 exemplifies initial measurement… “when a note is received solely for cash and no other right or privilege is exchanged, it is presumed to have a present value at issuance measured by the cash proceeds exchanged.”

42

Subsequent Measurement • Subsequent Measurement relates almost exclusively to assets,

liabilities, and equity. It addresses the criteria and amounts used to measure a particular asset, liability or equity item subsequent to the date of recognition (e.g., impairment, FMV changes, depreciation, amortization, etc.).

• 360-10-35 states: “The Subsequent Measurement Section provides guidance on an entity’s subsequent measurement and subsequent recognition of an item. Situations that may result in subsequent changes to carrying amount include impairment, fair value adjustments, depreciation and amortization, and so forth.”

43

Derecognition

• De-recognition relates almost exclusively to assets, liabilities, and equity. It addresses: (1) the criteria, (2) the basis to be relieved (i.e., dollar amount), and (3) the timing to be used when derecognizing a particular asset, liability or equity item for purposes of determining gain or loss, if any

44

Presentation

• This section will include presentation matters related to the subtopic. Some examples include: – Specific balance sheet classification requirements

for a derivative – Specific cash flow requirements for stock

compensation – Specific effect on EPS related to stock

compensation guidance

45

Disclosure

• Disclosure includes specific disclosure requirements for a subtopic, but excludes general disclosure requirements.

• Readers will be referred to other sections of the codification for relevant disclosure guidance for related subtopics.

46

Implementation guidance and illustrations

• This section will contain implementation guidance and illustrations of the standards.

• The primary sources for the implementation guidance and illustrations section include: – (1) Implementation guidance and illustrations contained in

appendices of various standards, – (2) FASB Staff Question & Answer documents, – (3) FASB Staff Positions, and – (4) EITF Abstracts.

47

Relationships

• Relationships include references to other subtopics that may contain guidance related to the subtopic.

• This section is intended to provide a simple reference to the relevant sections and will not include a complete description of the relationship.

48

Transition and Open Effective Date Information

• This section is intended to contain guidance and references to paragraphs within the subtopic that have open transition guidance.

• Modified paragraphs will appear in the relevant section of the codification with some form of emphasis (e.g., boxed).

49

Links to Grandfathered Materials

• Grandfathered material will contain descriptions, references, and transition periods for grandfathered standards.

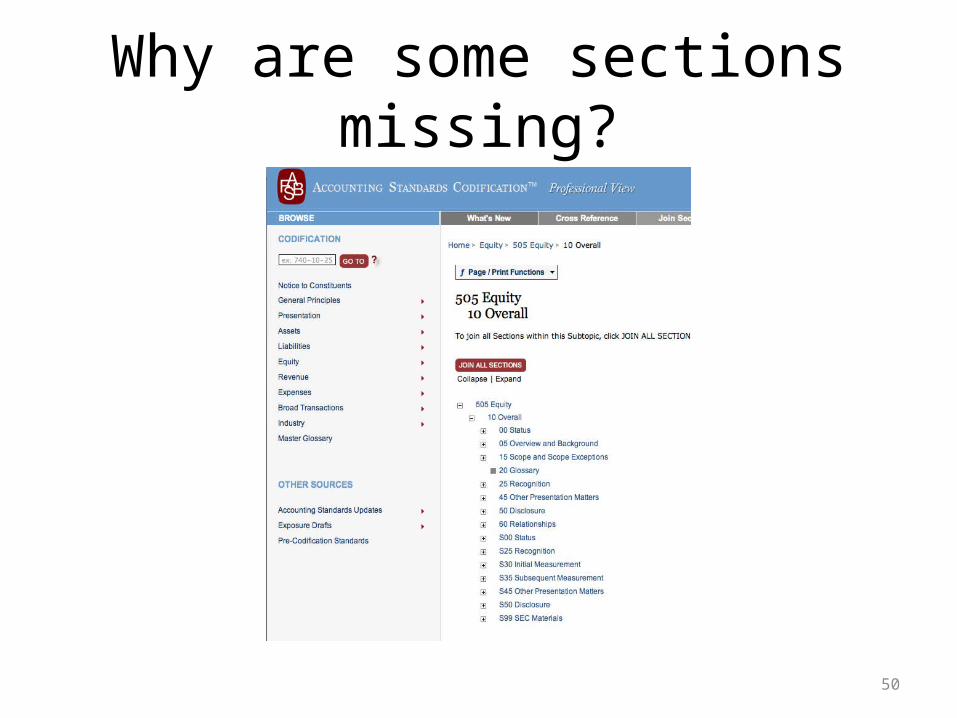

Why are some sections missing?

50

Why is there no Implementation Guidance for Equity?

• Codification authors did not write new GAAP.• Since there was no Implementation Guidance

under the standards-based system, there is none under the Codification.

51

What about convergence with IFRS?

• IFRS does not follow the Codification system. References in IFRS are much like the old system under GAAP.

• While many standards are virtually identical, FASB and IASB have yet to agree on how converged standards will be referenced.

52

53

GAAP Hierarchy in IFRS (IAS 8)

• If there is no specific guidance in a Standard or Interpretation, an enterprise should: – apply by analogy other Standards that deal with similar or related

issues – apply the definitions and criteria set out in the IASB Framework– apply pronouncements of national standard setters and accepted

industry practices, providing that these are consistent with other Standards, other Interpretations, and the Conceptual Framework

– Entities may use any GAAP that has a Conceptual Framework consistent with IFRS

FASB’s Due Process Procedure

• Topic added to FASB’s agenda– Issues may arise from EITF, Financial Accounting Standards

Advisory Council (FASB), Research Staff of FASB, SEC, industry or other groups

• Task force and FASB researchers write a discussion memorandum that is then released to the public

• Hearings are held• Task force revises and prepares an exposure draft• Hearings are held

54

FASB’s Due Process Procedure

• Task force evaluates and revises as necessary• Full FASB board (7 full-time members serving

5-year terms) votes on draft. • If 4 of 7 approve, a Standards Statement is

issued• Process can take years….

55

We will focus on Exposure Drafts

• For each topic we address this term, you will focus on financial transparency and whether it is enhanced or diminished by the proposed accounting guidance.

• For example, next class, I will give a presentation on the Leasing exposure draft and we will discuss whether the draft, if fully implemented, will enhance or diminish transparency and why

What is financial transparency?

• After banking crisis, much talk of financial transparency

• Reforms were proposed that would increase transparency

• Is there a common definition?

Transparent financial reports

• “… are clear, accurate reports that reflect the economic substance of transactions in a straightforward manner, even in times of great uncertainty.” [McEwen, 2009]

• Transparent reports are useful in making decisions.

Examples?

• Would publishing an aging schedule of receivables enhance transparency?

• Why?• Would forcing off balance sheet debt onto the

balance sheet enhance transparency?• If the disclosure already is in the footnotes,

why would adding it to the balance sheet enhance transparency?

Presentations

• Summary of the General Topic Area• Treatment under Current GAAP• Treatment if Exposure Draft fully adopted• Summary of Major Differences• The Effect on Financial Transparency if

Exposure Draft fully adopted – focus on why

Presentation requirements for presenters

• Presenters are required to turn in a PowerPoint presentation

• Assume that you are explaining the new guidance to a client

• Dress professionally for your clients• Be ready to answer questions and to engage your

clients in a discussion• Provide examples. • Cite your sources.• Introduce yourself.

Presentation requirements for clients

• Write a one-page, three paragraph paper on how the exposure draft, if fully implemented, will affect transparency.

• Paragraph one should introduce the topic.• The second paragraph should summarize the major

differences between the old and new guidance• The last paragraph should state your ideas about

whether transparency will be enhanced or diminished and why.

Teamwork

• Is encouraged…• Except for the one-page write up.• Discuss as much as you wish with your team,

but write your own paper.• Use turnitin.com to submit the paper• The similarity index cannot exceed 20%