Embed Size (px)

Citation preview

Acct 310 Accounting ReviewPart I

Rick Hayes, Ph.D., CPACalifornia State University L.A.

2

Accounting Analysis...

Analyze the effect of business transactions on the basic accounting equation:

Assets = Liabilities + Stockholders’ Equity

Must always balance.

3

Transaction AnalysisTransaction Analysis

• Two or more items can be affectedTwo or more items can be affected• Example: purchase computer for Example: purchase computer for

$10,000 by paying $6,000 in cash and $10,000 by paying $6,000 in cash and signing a note for $4,000signing a note for $4,000

4

Event 1 – Investment of Cash Event 1 – Investment of Cash by Stockholdersby Stockholders

Oct. 1 - Owner invested $10,000 Oct. 1 - Owner invested $10,000 Cash in business in exchange for Cash in business in exchange for $10,000 of Sierra Corporation $10,000 of Sierra Corporation Common StockCommon Stock

5

Event 2 – Note Issued in Exchange Event 2 – Note Issued in Exchange for Cashfor Cash

Oct. 1 – Sierra issued a 3-month, Oct. 1 – Sierra issued a 3-month, 12%, $5,000 Note Payable to Castle 12%, $5,000 Note Payable to Castle Bank in exchange for cash.Bank in exchange for cash.

6

Event 3 – Purchase of Office Event 3 – Purchase of Office Equipment for CashEquipment for Cash

Oct. 2 – Sierra acquired office Oct. 2 – Sierra acquired office equipment by paying $5,000 cash to equipment by paying $5,000 cash to Superior Sales CoSuperior Sales Co..

7

Event 4 – Receipt of Cash in Advance Event 4 – Receipt of Cash in Advance from Customerfrom Customer

Oct. 2 – Sierra received a $1,200 Oct. 2 – Sierra received a $1,200 cash advance from R. Knox, a cash advance from R. Knox, a client.client.

8

Event 5 – Services Rendered for Event 5 – Services Rendered for CashCash

Oct. 3 – Sierra received $10,000 in Oct. 3 – Sierra received $10,000 in cash from Copa Co. for advertising cash from Copa Co. for advertising services performedservices performed

9

Event 5 –Event 5 – Services Rendered, Services Rendered, WHAT IFWHAT IF these were performed “on account”?these were performed “on account”?

Later, when $10,000 is collected from Later, when $10,000 is collected from customer…customer…

10

11

Examples

12

Total the Entries to Each Side

If the greater sum is on the left, the account has a Debit Balance

Total Debits Total Credits

TITLE

Debit Credit

13

Total the Entries to Each Side

If the greater sum is on the right, the account has a Credit Balance

Total Debits Total Credits

TITLE

Debit Credit

14

Summary of TransactionsSummary of Transactions

Assets =Assets = Liabilities + EquityLiabilities + Equity

15

Normal Normal Balances for Assets and Liabilitiesfor Assets and Liabilities

16

Normal Balances for Stockholders’ Equity

17

Normal Balances for Expenses and Revenues

18

Expansion of Basic Equation

19

ReviewReview

What is the normal balance for the What is the normal balance for the following accounts?following accounts?

CashCash

Service RevenueService Revenue

Accounts ReceivableAccounts Receivable

Accounts PayableAccounts Payable

Common StockCommon Stock

Salaries ExpenseSalaries Expense

DebitDebit

CreditCredit

DebitDebit

CreditCredit

CreditCredit

DebitDebit

20

ReviewReview

What is the normal balance for the What is the normal balance for the following accounts?following accounts?

DividendsDividends

Unearned RevenusUnearned Revenus

Taxes PayableTaxes Payable

BuildingBuilding

Prepaid InsurancePrepaid Insurance

Rent ExpenseRent Expense

DebitDebit

DebitDebit

CreditCredit

CreditCredit

DebitDebit

DebitDebit

Date Debit Credit

GENERAL JOURNAL

Account Titles and Explanations

2007 Oct. 1 Cash 10,000 Common Stock 10,000 (Invested cash in business) 1 Cash 5,000

Notes Payable 5,000 (Issued 3-month, 12% note payable for cash) 2 Office Equipment 5,000 Cash 5,000 (Purchased office equipment for cash)

22

The General Ledger

23

The General Ledger

GENERAL JOURNALAccount Titles and Explanations

2007 Oct. 1 Cash 10,000 Common Stock 10,000

BalanceAcct 1010 Account CASH

Date

Acct 3010 Account COMMON STOCKDate Balance

debit

debit

credit

credit

debit

debit

credit

credit

ref

ref

Posting Entries

GENERAL JOURNAL

Account Titles and Explanations

2007 Oct. 1 Cash 10,000 Common Stock 10,000

BalanceAcct 1010 Account CASH

Date

Acct 3010 Account COMMON STOCKDate Balance

debit

debit

credit

credit

debit

debit

credit

credit

ref

ref

Oct 1

Oct 1

gj 1

gj 1

10,000 10,000

10,00010,000

Posting Entries

Posting Entries

GENERAL JOURNAL

Account Titles and Explanations

2007 Oct. 1 Cash 10,000 Common Stock 10,000

BalanceAcct 1010 Account CASH

Date

Acct 3010 Account COMMON STOCKDate Balance

debit

debit

credit

credit

debit

debit

credit

credit

ref

ref

Oct 1

Oct 1

gj 1

gj 1

10,000 10,000

10,00010,000

27

Trial Balance

A list of all the accounts and their balances at a given time.

It serves to prove the mathematical equality of debits and credits after posting.

It aids in the preparation of financial statements.

11 8

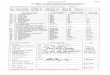

Sierra CorporationTrial Balance

October 31, 2007

Debit Credit Cash $15,200Advertising Supplies 2,500Prepaid Insurance 600Office Equipment 5,000Notes Payable $ 5,000Accounts Payable 2,500Unearned Service Revenue 1,200Common Stock 10,000Dividends 500Service Revenue 10,000Salaries Expense 4,000Rent Expense 900 $28,700 $28,700