Embed Size (px)

DESCRIPTION

single and output costing

Citation preview

SINGEL OR OUTPUT COSTING

MEANING :-

Single or output costing is employed in case of industries where the production is uniform and a continued affair,

(i) The units of production are identical; and(ii) The cost units are physical and natural.

The system is, therefore, most commonly used in case of industries like breweries, brickworks, quarries, dairies, cement works, sugar mills, paper mills etc. In all these industries, there is a natural cost unit such as a tonne of coal or cement or sugar a lb. of paper, a gallon of milk etc.

Under this system, an analysis of the different elements of expenditure is made so as to find out the factory cost, office cost and total cost. The per unit cost can be arrived at after dividing the total expenditure by the quantity produced. The expenditure can be classified at regular intervals e.g. monthly, quarterly or half-yearly. A statement of cost or a cost sheet is made out which throws light on every aspect of cost. Comparative figures of a preceding period are also provided in the cost statement so as to enable the management in assessing the progress of the business. Sometimes, in place of the figures of the preceding period, the budgeted figures are given which enable management to know the extent to which the targets have been achieved.

FEATURES OF SINGEL OR OUTPUT COSTING :-

i. Average unit cost computation – an average cost per unit is calculated by dividing the total cost incurred in a period by the periods output

ii. Single product involved -in the case of output costing only a single product or a number of grades of the product is involved.

iii. Work in progress is ignored – the work in progress is not considered at the time of ascertainment of cost as it does not vary from period to period.

iv. Applicable to non continuous manufacturing process industries – this method of costing is suitable for industries where the manufacturing process is not continuous.

WHAT IS COST ? :-

Cost refers to the expenditure incurred in producing a productand rendering a service

It is expressed from the producer or manufacturer’s view point

Cost ascertainment is based on uniform principles and techniques. Hence cost is objectively and ( not subjectively)determined.

Costs are the necessary expenditures that must be made in order to run a business. Every factor of production has a cost associated with it: labour, fixed assets, and capital, for example. The cost of labour used in the production of goods and services is measured in terms of wages.

The cost of a fixed asset used in production is measured in terms of

depreciation. The cost of capital used to purchase fixed assets is measured in terms of the interest expense associated with raising the capital.

Businesses are vitally interested in measuring their costs. Many types of costs are observable and easily quantifiable. In such cases there is a direct relationship between cost of input and quantity of output. Other types of costs must be estimated or allocated. That is, the relationship between costs of input and units of output may not be directly observable or quantifiable. In the delivery of professional services, for example, the quality of the output is usually more significant that the quantity, and output cannot simply be measured in terms of the number of patients treated or students taught. In such instances where qualitative factors play an important role in measuring output, there is no direct relationship between costs incurred and output achieved.

Cost represents the amount of expenditure (actual or notional) incurred on or attributable to a given thing. It represents the resources that have been or must be sacrificed to attain a particular objective

ELEMENTS OF COST :-

There are 4 main elements of cost :-

1. Material –

The substance from which a product is made is known as material. It may be in a raw or a manufactured state. It can be direct as well as indirect.

a. Direct Material :

The material which becomes an integral part of a finished product and which can be conveniently assigned to specific physical unit is termed as direct material. Following are some of the examples of direct material:

All material or components specifically purchased, produced or requisitioned from stores.

Primary packing material (e.g., carton, wrapping, cardboard, boxes etc.)

Purchased or partly produced components

Direct material is also described as process material, prime cost material ,production material, stores material, constructional material etc.

b. Indirect Material :

The material which is used for purposes ancillary to the business and which cannot be conveniently assigned to specific physical units is termed as indirect material. Consumable stores, oil and waste, printing and stationery material etc. are some of the examples of indirect material. Indirect material may be used in the factory, office or the selling and distribution divisions.

2. Labour –

For conversion of materials into finished goods, human effort is needed and such human effort is called labour. Labour can be direct as well as indirect.

a. Direct Labour:

The labour which actively and directly takes part in the production of a particular commodity is called direct labour. Direct labour costs are, therefore, specifically and conveniently traceable to specific products. Direct labour can also be described as process labour, productive labour, operating labour, etc.

b. Indirect Labour:

The labour employed for the purpose of carrying out tasks incidental to goods produced or services provided, is indirect labour. Such labour does not alter the construction, composition or condition of the product. It cannot be practically traced to specific units of output. Wages of storekeepers, foremen, timekeepers, directors’ fees, salaries of salesmen etc, are examples of indirect labour costs. Indirect labour may relate to the factory, the office or the selling and distribution divisions.

3. Expenses-

Expenses may be direct or indirect.

a. Direct Expenses:

These are the expenses that can be directly, conveniently and wholly allocated to specific cost centres or cost units. Examples of such expenses are as follows:

Hire of some special machinery required for a particular contract. Cost of defective work incurred in connection with a particular job or contract etc . Direct expenses are sometimes also described as chargeable expenses.

b. Indirect Expenses:

These are the expenses that cannot be directly, conveniently and wholly allocated to cost centres or cost units. Examples of such expenses are rent, lighting, insurance charges etc.

4. Overhead-

The term overhead includes indirect material ,indirect labour and indirect expenses. Thus, all indirect costs are over heads. A manufacturing organization can broadly be divided into the following three divisions:

a. Factory Overheads:

They include the following things:

Indirect material used in a factory such as lubricants, oil, consumable stores etc. Indirect labour such as gate keeper, time keeper, works manager salary etc. Indirect expenses such as factory rent, factory insurance, factory lighting etc.

b. Office and Administration Overheads:

They include the following things:

Indirect materials used in an office such as printing and stationery material, brooms and dusters etc.

Indirect labour such as salaries payable to office manager, office accountant, clerks, etc. Indirect expenses such as rent, insurance, lighting of the office.

c. Selling and Distribution Overheads :

They include the following things:

Indirect materials used such as packing material, printing and stationery material etc. Indirect labour such as salaries of salesmen and sales manager etc. Indirect expenses such as rent, insurance, advertising expenses etc.

COMPONENTS OF OUTPUT COSTS :-

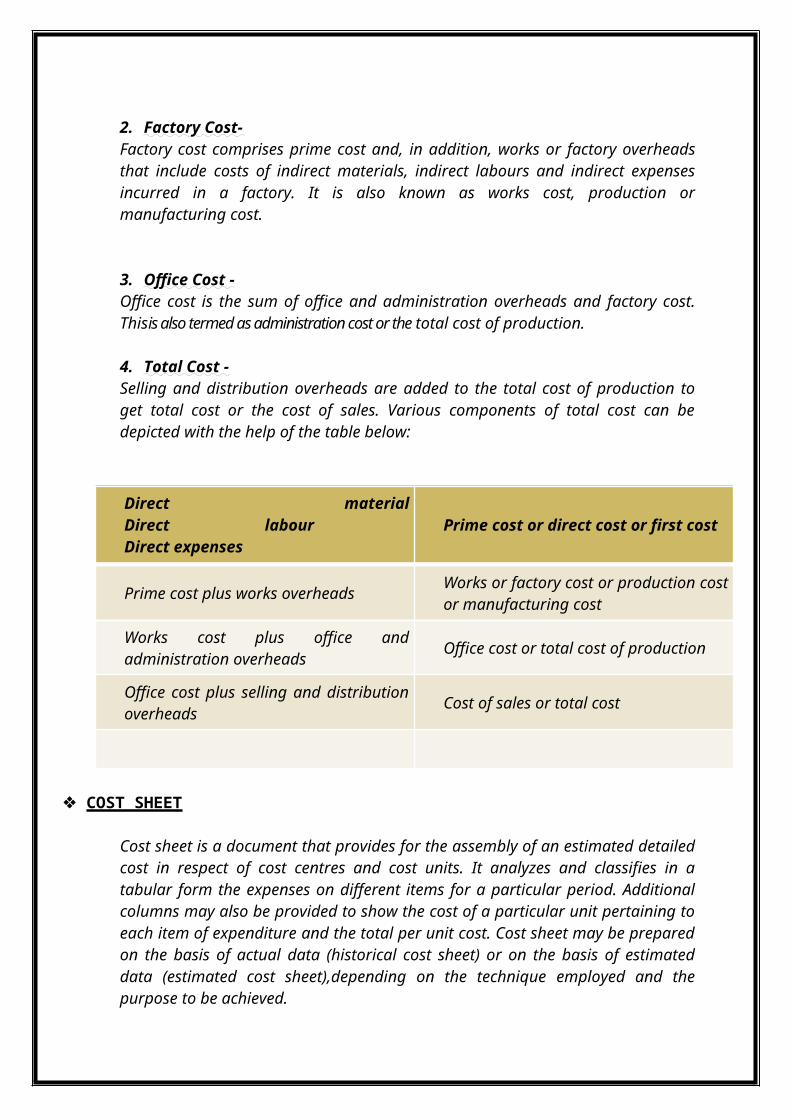

1. Prime Cost- Prime cost consists of costs of direct materials, direct labours and direct expenses. It is also known as basic, first or flat cost.

2. Factory Cost- Factory cost comprises prime cost and, in addition, works or factory overheads that include costs of indirect materials, indirect labours and indirect expenses incurred in a factory. It is also known as works cost, production or manufacturing cost.

3. Office Cost - Office cost is the sum of office and administration overheads and factory cost. Thisis also termed as administration cost or the total cost of production.

4. Total Cost - Selling and distribution overheads are added to the total cost of production to get total cost or the cost of sales. Various components of total cost can be depicted with the help of the table below:

Direct materialDirect labour Direct expenses

Prime cost or direct cost or first cost

Prime cost plus works overheadsWorks or factory cost or production cost or manufacturing cost

Works cost plus office and administration overheads

Office cost or total cost of production

Office cost plus selling and distribution overheads

Cost of sales or total cost

COST SHEET

Cost sheet is a document that provides for the assembly of an estimated detailed cost in respect of cost centres and cost units. It analyzes and classifies in a tabular form the expenses on different items for a particular period. Additional columns may also be provided to show the cost of a particular unit pertaining to each item of expenditure and the total per unit cost. Cost sheet may be prepared on the basis of actual data (historical cost sheet) or on the basis of estimated data (estimated cost sheet),depending on the technique employed and the purpose to be achieved.

Cost sheet is a document which provides for the assembly of the estimated detailed cost in respect of a cost centre or a cost unit. It analyses and classifies in a tabular form the expenses on different items for a particular period. Additional columns may also be provided to show the cost per unit pertaining to each item of expenditure and the total per

unit cost. Variations of stock are also recorded and proper adjustments made to arrive at the correct figures of raw materials consumed and the cost of goods sold.

Cost sheet may also depict data for the preceding period alongwith the data for the present period so as to have a quick appraisal of trends and tendencies in a cost sheet for a comparative study. It may also be prepared for making inter-firm comparison by including cost data of different firms. Such a single statement will facilitate inter-firm comparison of costs for taking decision about the policy formulation in the event of market competitions.

Cost sheet may be prepared on the basis of actual data or on the basis of estimated data depending on the technique of costing employed and the purpose to be achieved.

TYPES OF COST SHEET :-

1) Historical Cost Sheet: Such a cost sheet is prepared periodically after the costs have been incurred. The period may be a year, half-year, a quarter or a month. Actual costs are compiled and presented through such a cost statement. Comparisons can be made and decisions taken for cost control effectively if statements are prepared frequently.

2) Estimated Cost Sheet: Such a cost sheet is prepared before the actual commencement of production. The estimating process is repeated at regular intervals. Estimated cost sheets may be prepared on a half-yearly, quarterly or monthly basis. The estimated costs are compared with the actual costs every time whenever estimates are prepared so that costs can be controlled effectively since the ultimate aim of adoption of estimated costing technique is effective cost control. Costs are predetermined having regard to the present conditions and the circumstances likely to prevail in future, besides the past performances.

Ascertain of future costs and making comparisons with past records help the management in fixing up the selling prices of the products. Several important decisions can be taken by the management regarding profit planning, production and marketing strategy etc.

Estimation of different elements of cost has to be carefully made. Direct material cost is generally estimated on the basis of per unit cost of a preceding period subject to any fluctuations in market prices for estimated output of the future period. A similar pattern is adopted for estimating direct labour cost taking into account any proposed increase in wage rates. Overheads are estimated on the basis of past experience and current trends and then absorbed on a suitable basis.

Computation of profit :- To find the profit on each item one can subtract the cost of the product from the sale price of the item through which we gat the profit we earned.

PRODUCTION ACCOUNT :

A cost sheet is a document showing detailed costs of a product , service centre or unit. In case the items of finished goods inventories , sales , profit are also included in the cost sheet, it is called as a production or output statement. The same information can be presented in the form of an ordinary t shape account. Production account may be defined a an account giving the cost of production ,sales and profit made during a particular period.

,TREATMENT OF STOCK AND SCRAP :-

Stock & scrap materials requires a special treatment whilw preparing a cost sheet. there are discussed below:-

(I) Treatment Of Stock -

Stock may be of raw materials, of finished goods, or of work-in-progress.

(i) Stock of raw materials: With the help of stock of raw materials at the beginning and at the end of any accounting period, value of raw materials consumed is calculated. In the total amount of raw materials purchased, the stock at the beginning is added and closing stock is subtracted to arrive at the value of raw materials consumed.

Stock of raw materials may be valued at according to any of the methods discussed in the materials, e.g. FIFO, LIFO, average etc.

Example: From the following calculate the value of raw materials consumed:

Value of raw materials consumed:

$ 50,000 + $ 10,000 – $ 8000 = $ 52,000

(ii) Stock of finished goods: In the cost of production relating to a particular commodity or unit of production, the opening stock of finished goods is added and closing stock subtracted to find out the cost of production of goods sold.

Stock of finished goods is generally valued at the total cost of production: The selling and distribution overheads are charged on units sold and not on units produced and, therefore, the value of stock at the end takes into account the total production costs. The current cost is considered while valuing closing stock on the assumption that the stocks are being disposed off on first in first out basis; thus the last year’s stocks are over and whatever remains is out of the current year’s lot of production.

(iii) Stock of work-in-progress: Work-in-progress means units which are not yet complete but on which work has been done. Thus, it represents goods which are in the process of manufacturing. Generally, such goods bear a proportionate part of factory overheads besides raw materials and direct wages and, therefore, opening stock of work-in-progress is taken into consideration in the cost sheet while computing the works cost of goods manufactured during the year. Some concerns, however, follow the practice of valuing stock of work-in-

progress at prime cost. In such a case the stock of work-in-progress should be taken note of while calculating the prime cost.

The practice of valuing work-in-progress at prime cost does not seem to be very correct because after all some works expenses have been incurred on such goods. “The accountants cost hand book” edited by Professor I. Dickey also states. “The value of work-in-progress consists of direct material, direct labour and manufacturing overheads accumulated to the stage of completion reached at the end of a period.” Thus, the factory overheads should be generally included in the valuation of work-in-progress.

TREATMENT OF SCRAP :-

Scrap is a left over or residue after a product has been manufactured. The remnant of material resulting after producing the product is scrap. Thus, the residue of raw material incidentally realized in course of manufacturing goods is called scrap. Low quality raw material or abnormal size of raw material gives scrap material. Faulty or wrong product designing, substandard or unsuitable raw material, abnormal machine operation etc are the main causes of scraps. Thus a correct product design helps check scrap.The leftovers of the coconut hair oil are fibres and the outer shield. Therefore, the fibres and the outer shield of a coconut are scrap since they have to be sold at a nominal value. A hard and thin outer cover of a tree known as bark, end pieces of timber, sawdust, curly pieces of the surface of timber called shavings are scrap of a timber mill.

ACCOUNTING TREATMENT OF SCRAP :-

Nominal sales price realized out of negligible scrap is treated as other income in cost account.

A scrap account is opened with the full amount of the scrap of the process or job if such a scrap value is significant.

Process account or job account is given credit by the value of scrap. The scrap account is closed by the balance either of profit or loss to the profit or loss account.

Net sales value of scrap after deduction of selling and distribution costs is deducted either from the overhead amount or from the material cost.

Deduction out of overheads is made to adjust the overhead ratio if scrap is not possible to identify in relation to a process or a job.

TREATMENT FOR SPOILED AND DEFECTIVE WORK :-

In the case of spoilage, the first requirement is to know the nature and cause of the spoiled units.

The second requirement, the accounting problem is to record the cost of spoiled units and to

accumulate spoilage costs and report them to responsible personnel for corrective actions.Attaining the degree of materials and machine precision and the perfection of labour performance necessary to eliminate spoiled units entirely would involve costs far in excess of a normal or tolerable level of spoilage. If spoilage is normal and happens at any time and at any stage of the productive process, its cost should be treated as factory overhead, included in the predetermined factory overhead rate, and prorated overall production of a period. If, on the other hand, normal spoilage is caused by exacting specifications, difficult processing, or other unusual and unexpected factors, the spoilage cost should be charged to that order. In either cause, the cost of abnormal spoilage should be charged to factory overhead.

DIFFERENCE BETWEEN COST SHEET & PRODUCTION ACCOUNT

1. Cost sheet is made just for showing total cost of production but production account is just like trading and profit and loss account and it shows total cost and total net profit from producing specific units of production.

2. Production Account follows the rules of double entry system but cost sheet does not follow the rules of double entry system.

3. Production Account has four parts two. The first part shows prime cost, second part shows cost of goods manufacturing, third part shows gross profit and fourth part shows net profit. Cost Sheet presents the elements of costs in a classified manner and the cost ascertained at different states such as prime cost; works cost; cost of production; cost of goods sold; cost of sales and total cost.

4. With the help of Production Account, we can not prepare tenders or quotations because it shows historical detail regarding production of units. But estimated cost sheets can be prepared on the basis of actual cost sheets and these are useful for preparing tenders or quotations.

JOB COSTING

MEANING

Job costing involves the accumulation of the costs of materials, labor, and overhead for a specific job. This approach is an excellent tool for tracing specific costs to individual jobs and examining them to see if the costs can be reduced in later jobs. An alternative use is to see if any excess costs incurred can be billed to a customer.

Job costing is used to accumulate costs at a small-unit level. For example, job costing is appropriate for deriving the cost of constructing a custom machine, designing a software program, constructing a building, or manufacturing a small batch of products.

Job costing involves the following accounting activities:

Materials -It accumulates the cost of components and then assigns these costs to a product or project once the components are used.

Labour- Employees charge their time to specific jobs, which are then assigned to the jobs based on the labour cost of the employees.

Overhead-It accumulates overhead costs in cost pools, and then allocates these costs to jobs.

Job costing results in discrete “buckets” of information about each job that the cost accountant can review to see if it really should be assigned to that job. If there are many jobs currently in progress, there is a strong chance that costs will be incorrectly assigned, but the very nature of the job costing system makes it highly auditable.

If a job is expected to run for a long period of time, then the cost accountant can periodically compare the costs accumulated in the bucket for that job to its budget, and give management advance warning if costs appear to be running ahead of projections. This gives management time to either get costs under control over the remainder of the project, or possibly to approach the customer about a billing increase to cover some or all of the cost overrun.

Job costing demands a considerable amount of costing precision if costs are to be reimbursed by customers (as is the case in a cost-plus contract, where the customer pays all costs incurred, plus a profit). In such cases, the cost accountant must carefully review the costs assigned to each job before releasing it to the billing staff, which creates a customer invoice. This can cause long hours for the cost accountant at the end of a job, since the company controller will want to issue an invoice as soon as possible.

FEATURES :-

The Job Costing may be defines as "in job costing, costs are collected and accumulated according to jobs, contracts, products or work orders. Each job is treated as a separate entity for the purpose of costing. The material and labour costs are complied through the respective abstracts and overheads are charged on pre-determined basis to arrive at the total cost."

Some of the important features of this method of costing are given below:

(1) Works or production are undertaken against the order of customers.

(2) Production is not as a continuous process because each job is accepted by work order basis not for stock or future sales.

(3) Each job is treated as a separate entity for the purpose of costing.

(4) There is no uniformity in the flow of production because of different production process.

(5) Costs are collected and accumulated after the completion of each job or products in order to find out profit or loss on each job.

(6) The jobs differ from each other requiring separate work in progress maintained for each job.

PRE-REQUISITES FOR JOB COSTING :-

In order to ensure the successful application of Job Costing method, it is essential to consider the following pre-requisites :

(1) A sound production planning and controlling system.

(2) An appropriate time booking and time keeping system to avoid idle time.

(3) Maintenance of necessary records with regard to job tickets, work order, operation tickets, bills of materials and tools requirements etc.

(4) Appropriate methods of overhead apportionment and absorption rate.

(5) Effective designing and scheduling of production.

PROCEDURE :-

1. Job order number: Every order received is allotted a certain number from a running list maintained for this purpose. Every order or job will be known by its number throughout its production process in the factory.

2. Production / job order: A production / job order is a written order issued to the manufacturing department to proceed with a job. It is issued by the production planning department on receipt of a job order to the foreman of the relevant department. Instructions to the costing department to collect particulars of costs on execution of the job are also issued simultaneously. The production order is prepared with sufficient copies for all the departmental managers or foreman who will be required to take any part in the production.

3. Bills of materials: The production and planning department also prepares a list of materials and stores required for the completion of the job. A copy is also sent to the concerned foreman with the production order which serves as an authority to him for collecting the materials and stores mentioned from the storekeeper. On the same pattern a list of tools required is also prepared.

4. Job cost card: Job cost card or job cost sheet is the most important document used in the job costing system. A separate card or cost sheet is maintained for each job in which all expenses regarding materials, labour and overheads are recorded directly from costing records. The method of finding out the cost of these elements in respect of a particular order is as follows.

a) Materials: The information regarding cost of materials or stores used for a particular job order can be obtained from materials or stores requisition slips. In case of large job orders, materials abstracts can be prepared for finding out the total value of materials issued to different jobs.

b) Labour: The cost of labour incurred on each job can be ascertained with the help of time and job cards. In case of a large number of jobs, preparation of wages abstract may considerably help in computing the amount paid as wages for completion of specific jobs. Wages paid for indirect labour will constitute an item of factory overheads.

c) Overheads: Every job will be charged with amount of overheads determined on the basis of the method selected for allocation of overheads. Normally on the basis of past results an overhead rate is determined and each job is charged for overheads at the pre-determined rate.

Profit or loss on a job can also be found out by preparing a job account. The job account is debited with all expenses incurred on the job and is credited with the job price. The difference of the two sides will be the profit or loss made or suffered on the job.

1. Work-in-process: The account is maintained in the cost ledger and it represents the jobs under production. The account may be maintained in any of the following two ways depending upon the requirements of the business:

a) A composite work-in-process account for the entire factory.b) A composite work-in-process account for every department. For example, if

the factory has three departments A, B and C, a work-in-process for each of these three departments will be opened.

The work-in-process account is periodically debited with all costs direct and indirect incurred in execution of the jobs. At intervals of month or so a summary of completed jobs is prepared and the work-in-process account is credited with the cost of completed jobs. In case work-in-progress account for each department of the factory has been opened, it will be necessary to find out the cost of completed jobs regarding each department. The balance in work-in-process account at any time represents the cost of jobs not yet completed.

2. Job ticket: In order to provide information regarding the progress of each job at each operation, generally a job ticket is issued by the production control department. The

ticket contains detachable portions for different operations. The job ticket is useful for both production control and costing departments. On completion of an operation, the relevant portion of ticket is detached and sent to production control department. This enables production control department in keeping production schedule up-to-date. On the basis of detached portion a departmental summary of production can be prepared which is very useful for costing purposes. Moreover, the amount of work-in-process as shown by the cost ledger can be checked by listing the ticket number of jobs in process in any department and valuing this list.

3. Progress advice: The foreman of a department may be required to send periodically a statement regarding the stage of completion of each job to ensure completion of jobs by scheduled dates. Such a note is called “progress advice”.

JOB COSTING EXAMPLE :-

Mayur engineering co. engaged in job work has completed all the jobs in hand on 30th dec. 2009 except job no. 447. The cost sheet on 30th ,Dec. 2009 showed direct material and direct labour cost of Rs. 40,000 and Rs. 30,000 respectively as having being incurred on job no. 447. The cost incurred by the business on 30st dec. 2009, the last date of the accounting year were as follows :

Direct material Rs. 2000

Direct labour Rs. 8000

Indirect labour Rs. 2000

Misc.Factory overhead Rs. 3000

The company follows the practice to make job absorbed factory overheads on the basis of 120% of direct labour cost. Prepare a composite job cost sheet for job 447 showing analytical computation.

ADVANTAGES OF JOB COSTING:

1. Job costing enables the management to identify spoiled and defective work in respect to particular production orders, departments or groups of workers and hence the management can fix up responsibility for inefficiency.

2. Management can determine the trends in costs and compare the operating efficiency of men and machines in each cost centre. It can also determine the completion cost of each job.

3. It enables the preparation of estimates of costs of jobs before production.4. It enables comparison of estimated costs with actual costs as the costs are analysed

on the basis of costs, services and production.5. It makes available to the management a complete file of production orders which

contains valuable statistics on cost.6. It enables ascertainment of profit or loss on each job immediately after their

completion.7. It enables the management to identify unprofitable jobs.8. In case of cost plus contracts, job costing enables to provide precise quotations.9. It helps in production planning.10. It facilitates fixation of selling price.

LIMITATIONS OF JOB COSTING:

1. Job costing involves a lot of clerical work in identifying materials, labour and overheads with specific jobs and departments.

2. Management cannot evaluate precisely the operating efficiency of men and machines.3. Since costs ascertained and compiled are historical costs, they are not of much utility

to the management.4. It does not apply budgetary control to important cost elements such as labour,

materials and overheads.5. Job costs over any period of time cannot be compared if major economic changes

take place in between.6. It is expensive to operate and errors are possible due to increased clerical work.

BATCH COSTING MEANING

Batch costing is a modified form of job costing. While job costing is concerned with costing of jobs that are executed against specific orders of the customers, batch costing is used where articles are manufactured in definite batches. The articles are usually kept in stock for selling to customers on demand. The term batch refers to the lot in which the articles are to be manufactured. Whenever a particular product is required, one unit of such product is not produced but a lot of say 500 or 1000 units of such product are produced. It is therefore also known as “Lot Costing”. This method of costing is used in case of pharmaceutical or drug industries, ready-made garment factories, industries manufacturing component parts of radio sets, television sets, watches, etc.

The costing procedure for batch costing is similar to that under job costing except with the difference that a batch becomes the cost unit instead of a job. Separate job cost sheets are maintained for each batch of products. Each batch is allotted a number. Material requisitions are prepared batchwise, the direct labour is engaged batchwise and the overheads are also recovered batchwise. Cost per unit is ascertained by dividing the total cost of a batch by number of items produced in that batch. Ordinary principles of inventory control are used. Production orders are issued only when the stock of finished goods reaches the ordering level. In case the batches are repetitive, the costing work is much simplified.

Two typical situations in which batch costing would be used are:

where a customer orders a quantity of identical items; or where an internal manufacturing order is raised for a batch of identical parts.

In general the procedures for costing batches are very similar to costing jobs. The batch would be treated as a job during manufacture. On completion of the batch the cost per unit can be calculated by dividing the total batch cost by the number of good units produced.

Examples of products that are best accounted for cost through batch costing include:

Production of engineering components Radios/television sets Medicine Footwear Clothing manufacturer

The costs included in the batch cost are direct costs of material, labour and direct expenses plus overheads absorbed into the batch.

Since in batch costing production is done in batches and each batch consists of a number of units, the determination of optimum quantity to constitute an economical batch is all the more important. Such a quantity can be fixed on the basis of same formulae and principles as are applicable to economic order quantity of materials.

In Batch Costing, a lot of similar units which comprise the batch may be used as a cost unit for ascertainment of cost. Separate Cost Sheet is maintained for each batch by assigning a batch number. Cost per unit of product is determined by dividing the total cost of a batch by the number of units of that batch. Batch costing is used in number drug industries, ready made garment industries, electronic components manufacture, TV sets, radio etc.

FEATURES OF BATCH COSTING

Cost are collected batch wise. A batch number is allocated to each batch and cost are accumulated for each batch.

1. Products of identical nature- item which are produced in a batch are identical or similar in nature.

2. Conventional group – it is possible to classify them into conventional group for the purpose of costing.

DETERMINATION OF ECONOMIC BATCH QUANTITY (EBQ) :-

Determination of economic batch lot is the important work in batch costing. The two types of costs involved in batch costing are (1) Set up cost and (2) Carrying cost.

If the batch size is increased. set up cost per unit will come down and the carrying cost will increase. It the batch size is reduced. set up cost per unit will increase and the carrying cost will come down. Economic Batch Quantity will balance these two opposing costs.

Economic Batch Quantity = 2U x P

S

Where:

U = Annual demand

P = Setting up and order placing costs per batch

S = Storage or inventory carrying over cost per unit per annum

FORMULA FOR COST PER UNIT:-

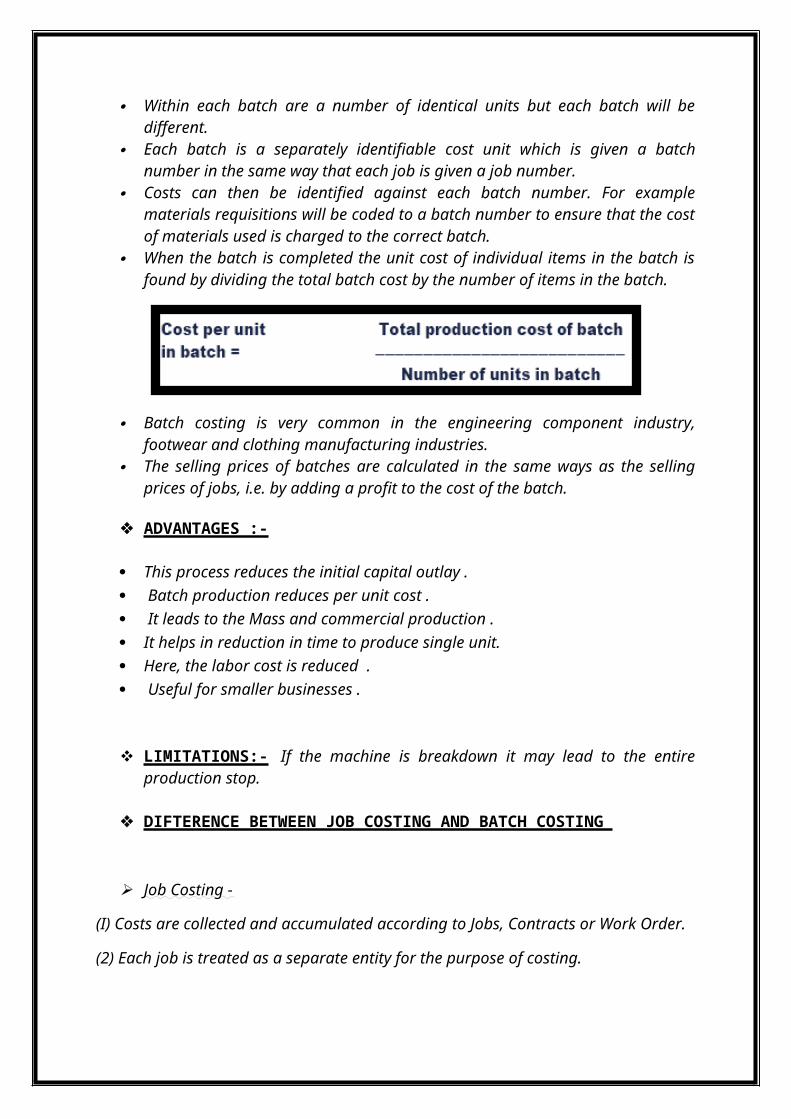

Within each batch are a number of identical units but each batch will be different. Each batch is a separately identifiable cost unit which is given a batch number in the

same way that each job is given a job number. Costs can then be identified against each batch number. For example materials

requisitions will be coded to a batch number to ensure that the cost of materials used is charged to the correct batch.

When the batch is completed the unit cost of individual items in the batch is found by dividing the total batch cost by the number of items in the batch.

Batch costing is very common in the engineering component industry, footwear and clothing manufacturing industries.

The selling prices of batches are calculated in the same ways as the selling prices of jobs, i.e. by adding a profit to the cost of the batch.

ADVANTAGES :-

This process reduces the initial capital outlay . Batch production reduces per unit cost . It leads to the Mass and commercial production . It helps in reduction in time to produce single unit. Here, the labor cost is reduced . Useful for smaller businesses .

LIMITATIONS:- If the machine is breakdown it may lead to the entire production stop.

DIFTERENCE BETWEEN JOB COSTING AND BATCH COSTING

Job Costing -

(I) Costs are collected and accumulated according to Jobs, Contracts or Work Order.

(2) Each job is treated as a separate entity for the purpose of costing.

(3) The materials and labour costs are complied through the respective abstracts and overheads are charged on predetermined basis.

(4) Costs are found out at the stage of completion of the job.

(5) Job costing is used in Printing, Furniture making, Ship Building etc.

Batch Costing -

(I) Lot of similar units which comprise the batch may be used as a cost unit for ascertainment of cost.

(2) Separate cost sheet is maintained for each batch by assigning a batch number.

(3) Separate cost sheet is maintained for each batch by assigning a batch manner.

(4) Cost per unit of product is determined by dividing the total cost of a batch by the number of units of that batch.

(5) Batch costing is used in drug industries, ready- made garments, T.V. sets, Radio's and Electronic Components Manufacture.

CONTRACT COSTINGMEANING :-

Contract Costing is a special type of job costing where the unit of cost is a single contract.

Contract itself is a cost centre and is executed under the customer's specifications.

Contract Costing is defined by the I C M A Terminology as "that form of specific order costing which applies where work is undertaken to customer's special requirements and each order is of long duration. The work is usually of constructional nature."

Contract Costing is also termed as ''Terminal Costing."

The principles of job costing are applicable to contract costing and is used by such concerns of builders, public works contractors, constructional and mechanical engineering firms and ship builders etc. who undertake work on a contract basis.

SPECIAL FEATURES OF CONTRACT COSTING

The following are the special features of Contract Costing:

(1) The cost unit is a specific contract.

(2) Each contract takes a long time to complete.

(3) The work being of a constructional nature, the same is executed at customer's site, as per his specifications.

(4) Bulk of the materials purchased and delivered direct to the contract site or obtained from the central stores through the requisition slips.

(5) Generally specific portions of the contract are given to sub-contractors.

(6) Most of costs which are normally treated as indirect can be identified specifically with a particular contract and are charged to it as direct costs.

(7) Overheads constitute only a very small proportion of the cost of the contract. However, indirect costs consist mainly of administrative cost of the central office.

492 A Textbook of Financial Cost and Management Accounting

(8) Scale of operations and cost control becomes difficult due to theft of materials, labour time utilization, pilferages etc.

(9) The pay roll is prepared either at the site or at a central administrative office.

CONTRACT PROCEDURE :-

In contract costing, costs are allocated, collected and accumulated according to the contract works. Each contract is treated as a separate entity in which each contract account may be maintained separately or in general ledger itself for the purpose of costing and cost control. The following are the costing procedure for different costs relating to the important expenses:

(1) Materials:

(A) Contract Account is debited with the following transactions relating to materials :

Bulk of materials are purchased for a specific contract from suppliers. Materials obtained from contractor's central stores through the requisition slips. Materials transferred from one contract to another contract. Value of materials remaining unutilized on site during the accounting year.

(B) Contract Account is credited with the following transactions relating to materials:

Materials returned under Materials Return Note. Sale of materials at site on account of some extraneous reasons. Materials transferred to other contracts. Materials stolen or destroyed by fire. On completion, if a part of materials received from the stores are returned.

(C) Any profit or loss on materials account is transferred to the Profit and Loss Account:

Sale price is different from the cost price. Resulting from the sale of materials at site. Resulting from the materials stolen or destroyed by fire. Labour: In the case of contract costing, all labours engaged at site and the salaries

and wages paid to the labour and workers are treated as direct labour cost is debited to Contract Account.

Direct Expenses: Most of the expenses like electricity, insurance telephone, postage, sub-contracts, Architect's fees etc. can also be treated as direct cost is debited to Contract Account.

Overhead Cost: In the case of contract costing overheads incurred only an insignificant part of the total cost of contract account. The nature office and administrative expenses of a particular contract may be apportioned on suitable basis.

Plant and Machinery: For use of plant and machinery in a particular contract, the treatment of plant costs in any of the two ways:

Where a plant has been specially purchased for a particular contract and will be exhausted at site Contract Account should be debited with the cost of the plant. On completion of the contract the residual or written down value as shown by the Plant Ledger will be credited "to the Contract Account.

When the plant and machinery are required to the contract site only for a shorter period, the contract account should be debited with the notional amount of depreciation based on some estimates be charged to Contract Account.

Sub-Contracts : Sub-Contracts refer to some portions of the specified work connected with the main contract, to be done by the sub-contractor. For example, the work of painting, special flooring, steel work etc. may be given to the sub-contractors. Usually sub-contract has been undertaken on cost-plus basis and the cost of such sub-contract should be treated as a direct charge and is debited to Contract Account.

Work Certified : In the case of the small contracts which are completed within the shorter period, the contractor pays the contract price on the completion of the contract. In the case of contracts of long duration. the contract agreement provides interim payment to the contractor. It is done on the basis of certificates issued by the contractor Surveyor, Architect or Engineer. At the same time Contractor usually does not pay to the full value of the work certified. A portion of amount say 20% or 30% thereof shall be retained by the Contractor. The money so retained is called as "Retention Money." This retention money is intended to ensure that the contractor to complete the work as scheduled and according to specifications. Money retained could also be used for imposing penalties for faulty or delayed work. This amount will be settled on completion of the contract.

Work Uncertified : If the progress of a work is unsatisfactory or the work has not reached the stipulated stage, though certain work is completed, such work does not qualify for a certificate by the Contractor’s Architect or Surveyor is termed as "Work Uncertified." It is valued at cost and credited to Contract Account and debited to Work in Progress Account.

Work in Progress: Work in progress includes the amount of work .certified and the amount of work uncertified. The work in progress account will appear on the asset side of the balance sheet. The amount of cash received from the contractor and reserve for contingencies will be deducted out of this amount.

TREATMENT OF PROFITS OR LOSS ON CONTRACTS A/C :-

The accounting treatment of profits or loss of contracts in the following stages :

(A) Profit or Loss on incomplete contracts -

To determine the profits to be taken to Profit and Loss Account. in the case of incomplete contracts, the following situations may arise :

(i) Completion of Contract is Less than 25% : In this case no profit should be taken to Profit and Loss Account.

(ii) Completion of Contract is upto 25% or more but Less than 50% : In this case one-third of the notional profit, reduced in the ratio of cash received to work certified, should be transferred to Profit and Loss Account. It can be expressed as :

1 Cash Received -- x Notional Profit x ------ 3 Work Certified

(iii) Completion of Contract is upto 50% or more but Less than 90% : In this case two-third of the notional profit reduced by proportion of cash received to work certified is transferred to Profit and Loss Account. The equation is

(iv) Completion of Contract is upto 90% or more than 90%, i.e., it is nearing completion: In this case the profit to be taken to Profit and Loss Account is determined by determining the estimated profit and using anyone of the following formula :

Contract price :-

i. Escalation Clause: This clause is often provided in contracts as safeguard against any likely changes in price or utilization of material and labour. Such a clause in a contract would provide that in the event of a specified contingency happening, the contract price would be suitably enhanced by an agreed formula or factor. This clause is particularly necessary where the prices of a certain raw material are likely to rise. where labour rates are anticipated to increase, or where the quantity of material and labour hours cannot be assessed properly or estimated unless the job has progressed sufficiently.

ii. Cost-Plus Contract: These contracts provide for the payment by the contractee of the actual cost of manufacturing plus a stipulated profit. The profit to be added to the cost may be a fixed amount or it may be a stipulated percentage of cost. These contracts are generally entered into when at the time of undertaking of a work, it is not possible to estimate it's cost with reasonable accuracy due to unstable condition of material. labour etc. or when the work is spread over a long period of time and prices of materials. rates of labour etc. are liable to fluctuate.

(B) Profits or Loss on Completed Contracts :-

When a contract is completed, the overall profit or loss on the contract is transferred to the Profit and Loss Account.

ADVANTAGES OF CONTRACT COSTING:-

The total cost is determined at the beginning of the contract, and not negotiable by either party at the end or during the time the work is completed.

Time & Materials (T&M) whereby the total cost is charged according to the actual number of hours work (time) and the cost of the equipment used (materials).

The contractor can show exactly what the customer is paying for.

If the job takes longer than expected, they are not tied to the previously agreed price which could not account for un-seen circumstances.

DISADVANTAGES OF CONTRACT COSTING:-

It is a time consuming process

It is very Expensive

It creates lots of clerical work.

PROCESS COSTING

MEANING :-

Process costing is a form of operations costing which is used where standardized homogeneous goods are produced. This costing method is used in industries like chemicals, textiles, steel, rubber, sugar, shoes, petrol etc. Process costing is also used in the assembly type of industries also. It is assumed in process costing that the average cost presents the cost per unit. Cost of production during a particular period is divided by the number of units produced during that period to arrive at the cost per unit.

Process costing is a method of costing under which all costs are accumulated for each stage of production or process, and the cost per unit of product is ascertained at each stage of production by dividing the cost of each process by the normal output of that process.

FEATURES OF PROCESS COSTING:- i. The production is continuous.

ii. The product is homogeneous.iii. The process is standardized.iv. Output of one process become raw material of another process.v. The output of the last process is transferred to finished stock .

vi. Costs are collected process-wise.vii. Both direct and indirect costs are accumulated in each process.

viii. If there is a stock of semi-finished goods, it is expressed in terms of equalling unitsix. The total cost of each process is divided by the normal output of that process to find

out cost per unit of that process.

PROCESSING DEPARTMENTS :-

A processing department is an organizational unit where work is performed on a product and where materials, labor, or overhead costs are added to the product. For example, a Nalley’s potato chip factory might have three processing departments—one for preparing potatoes, one for cooking, and one for inspecting and packaging. A brick factory might have two processing departments—one for mixing and molding clay into brick form and one for firing the molded brick. Some products and services may go through a number of processing departments, while others may go through only one or two. Regardless of the number of processing departments, they all have two essential features. First, the activity in the processing department is performed uniformly on all of the units passing through it. Second, the output of the processing department is homogeneous; in other words, all of the units produced are identical.

COSTING PROCEDURE :-

For each process an individual process account is prepared. Each process of production is treated as a distinct cost centre.

Items on the Debit side of Process A/c. Each process account is debited with – a) Cost of materials used in that process.

b) Cost of labour incurred in that process.

c) Direct expenses incurred in that process.

d) Overheads charged to that process on some pre determined.

e) Cost of ratification of normal defectives.

f) Cost of abnormal gain (if any arises in that process)

Items on the Credit side:

Each process account is credited with a) Scrap value of Normal Loss (if any) occurs in that process. b) Cost of Abnormal Loss (if any occurs in that process)

Cost of Process: The cost of the output of the process (Total Cost less Sales value of scrap) is transferred to the next process. The cost of each process is thus made up to cost brought forward from the previous process and net cost of material, labour and overhead added in that process after reducing the sales value of scrap. The net cost of the finished process is transferred to the finished goods account. The net cost is divided by the number of units produced to determine the average cost per unit in that process.

Process Losses:

In many process, some loss is inevitable. Certain production techniques are of such a nature that some loss is inherent to the production. Wastages of material, evaporation of material is un avoidable in some process. But sometimes the Losses are also occurring due to negligence

of Labourer, poor quality raw material, poor technology etc. These are normally called as avoidable losses. Basically process losses are classified into two categories

(a) Normal Loss

(b) Abnormal Loss

1. Normal Loss: Normal loss is an unavoidable loss which occurs due to the inherent nature of the materials and production process under normal conditions. It is normally estimated on the basis of past experience of the industry. It may be in the form of normal wastage, normal scrap, normal spoilage, and normal defectiveness. It may occur at any time of the process. No of units of normal loss: Input x Expected percentage of Normal Loss. The cost of normal loss is a process. If the normal loss units can be sold as a crap then the sale value is credited with process account. If some rectification is required before the sale of the normal loss, then debit that cost in the process account. After adjusting the normal loss the cost per unit is calculates with the help of the following formula:

Cost of good unit: Total cost increased – Sale Value of Scrap Input – Normal Loss units

2. Abnormal Loss: Any loss caused by unexpected abnormal conditions such as plant breakdown, substandard material, carelessness, accident etc. such losses are in excess of pre-determined normal losses. This loss is basically avoidable. Thus abnormal losses arrive when actual losses are more than expected losses. The units of abnormal losses in calculated as under:

Abnormal Losses = Actual Loss – Normal Loss The value of abnormal loss is done with the help of following formula: Value of Abnormal Loss: Total Cost increase – Scrap Value of normal Loss x Units of abnormal loss Input units – Normal Loss Units 6 Abnormal Process loss should not be allowed to affect the cost of production as it is caused by abnormal (or) unexpected conditions. Such loss representing the cost of materials, labour and overhead charges called abnormal loss account. The sales value of the abnormal loss is credited to Abnormal Loss Account and the balance is written off to costing P & L A/c.

SIMILARITIES BETWEEN JOB-ORDER AND PROCESS COSTING :-

Much of what you learned in the previous chapter about costing and cost flows applies equally well to process costing in this chapter. We are not throwing out all that we have learned about costing and starting from “scratch” with a whole new system. The similarities between job-order and process costing can be summarized as follows:

1. Both systems have the same basic purposes—to assign material, labor, and manufacturing overhead costs to products and to provide a mechanism for computing unit product costs.

2. Both systems use the same basic manufacturing accounts, including Manufacturing Overhead, Raw Materials, Work in Process, and Finished Goods.

3. The flow of costs through the manufacturing accounts is basically the same in both systems. As can be seen from this comparison, much of the knowledge that you have already acquired about costing is applicable to a process costing system. Our task now is to refine and extend your knowledge to process costing.

DIFFERENCES BETWEEN JOB-ORDER AND PROCESS COSTING :-

There are three differences between job-order and process costing. First, process costing is used when a company produces a continuous flow of units that are indistinguishable from one another. Job-order costing is used when a company produces many different jobs that have unique production requirements. Second, under process costing, it makes no sense to try to identify materials, labor, and overhead costs with a particular customer order (as we did with job-order costing) because each order is just one of many that are filled from a continuous flow of virtually identical units from the production line. Accordingly, process costing accumulates costs by department (rather than by order) and assigns these costs uniformly to all units that pass through the department during a period. Job cost sheets (which we used for job-order costing) are not used to accumulate costs. Third, process costing systems compute unit costs by department. This differs from job-order costing where unit costs are computed by job on the job cost sheet.

ADVANTAGES OF PROCESS COSTING:

1. Costs are be computed periodically at the end of a particular period

2. It is simple and involves less clerical work that job costing

3. It is easy to allocate the expenses to processes in order to have accurate costs.

4. Use of standard costing systems in very effective in process costing situations.

5. Process costing helps in preparation of tender, quotations 6. Since cost data is available for each process, operation and department, good managerial control is possible.

LIMITATIONS: 1. Cost obtained at each process is only historical cost and are not very useful for

effective control.2. Process costing is based on average cost method, which is not that suitable for

performance analysis, evaluation and managerial control.3. Work-in-progress is generally done on estimated basis which leads to inaccuracy in

total cost calculations.4. The computation of average cost is more difficult in those cases where more than

one type of products is manufactured and a division of the cost element is necessary. 5. Where different products arise in the same process and common costs are prorated to

various costs units. Such individual products costs may be taken as only approximation and hence not reliable.

OPERATING OR SERVICE COSTING

MEANING:-

The Chartered Institute of Management Accountants (CIMA), London defines “operating

cost” as “the cost of providing a service. “Services performed may be internal or external.

Services are termed as internal where they have to be performed on inter-departmental basis

in the factory itself, e.g. supplying of power, gas or electricity from factory’s own power-

house, catering from the factory’s canteen; supplying steam raised from the boiler house,

repairing necessary items by the repair and maintenance department etc. Services are termed

as external when they have to be provided to outside parties. Such concerns are service

undertakings, e.g. transport corporations carrying loads of goods or human beings;

electricity companies generating electricity or power; hospitals serving patients or carrying

out operations; canteens serving meals or dishes of different varieties etc. The method

employed to find out the cost of rendering a service, either internal or external, is serving

cost or operating cost.

Operating costing is just a variant of unit or output costing. The method of computing

operating cost is very simple the expenses of operating a service for a particular period are

grouped under suitable headings and their total is divided by the number of service unit for

the same period, and thus cost per unit of service is obtained. The cost for a future period

may be estimated on the basis of estimated service units and the estimated costs. This will

help in fixing the price to be charged for the service units and the estimated cost. Thus, the

principle involved under operating costing is the same as under unit costing but they differ in

the manner in which costing information have to be collected and allocated to cost units. The

data about expenses are to be classified according to their nature of variability and

moreover, the unit of cost maybe simple or composite.

FEATURES :-

The undertaking which adopts service costing does not produce any tangible goods. These undertakings render unique services to their customers.

The expenses are divided into fixed and variable cost . Such a classification is necessary to ascertain the cost of service and the unit cost of service.

The cost unit may be simple or composite. The examples of simple cost units are cost per unit in electricity supply , cost per litre in water supply, cost per meal in canteen etc.

Similarly cost per passenger kilo-meters in transport cost per patient-day in hospital, cost per room-day in hotel etc. are the examples of composite cost unit.

Total cost are averaged over the total amount of service rendered.

Costs are usually computed period-wise. However, in the case of utilization of vehicles, use of road-rollers etc., the costs are computed order wise.

Service costing can be used for service performed internally or externally.

Documents like the daily log sheet, cost sheet etc. are used for the collection of cost data.

DETERMINATION OF UNIT OF COST :-

A proper unit of cost must be selected, in order to ascertain the cost per unit of service

provided. The selection of proper unit is a difficult task and it depends upon the nature of

work and the purpose for which cost has to be computed. The unit may be simple as under

unit costing e.g., per bed in case of hospitals, per 1000 litres in case of water work, per child

in case of schools, per km. of road maintained in case of road maintenance undertaking, per

cup of tea or per dish in case of canteen service etc. But in certain cases, a composite unit of

cost is used, e.g., per passenger-kilometre in case of bus companies, which means the cost of

carrying one passenger for one kilometre. Similarly, cost per quintal kilometre in case of

motor transport means cost of carrying the load of one quintal for one kilometre. For

electricity supply undertakings, the unit of cost may be kilowatt- hour which signifies the cost

of one kilowatt of electricity generated during an hour.

COLLECTION OF COSTING DATA :-

After determining the unit of cost to which the total expenditure to be allocated, the process

of collecting the necessary data about costs of operating the services is carried out. The data

after collection are classified under fixed and variable heads so that greater control can be

exercised over cost. In whatever quantum the service is rendered, fixed cost shall not change

and the management should concentrate over such costs. The expenses which vary according

to a change in the operating level are grouped separately and sometimes such expenses are

placed in sub-groups like maintenance charges and running expenses so as to have a better

idea about the cost structure. Costing in some specified undertaking has been explained in

detail in the following pages.

i. Transport Costing :-

To find out the cost of carrying goods or passenger for a distance for a suitable costing

records should be maintained. Firstly, a Log Book should be supplied to the vehicle driver

who should maintain it regularly. A daily log report or sheet should be filled in by the driver

of the vehicle giving necessary details about the journeys or trips made. Secondly, a vehicle

cost sheet and performance statement should be prepared by the costing department showing

details about the total and the unit cost.

Log Sheet serves as the basis for cost accounting and control. Idleness of vehicles, under-

utilisation of capacity by low burdening or over-utilisation by extra loading, duplication of

trips etc. are avoided if a proper system of checks is enforced through daily log reports.

The data may be compiled from the daily reports and cost summary and performance

statement prepared. For preparing a cost sheet, the costs may be sub-divided under following

heads:

1. Fixed or standing charges. Whether the vehicle is in operation or not such costs shall

have to be incurred. Examples of such costs are insurance premium, road tax, licence

fees, rent of the garage etc. Interest on capital if charged should be included under

this head.

2. Maintenance charges. They are in the nature of semi-variable expenses, e.g. repair

and maintenance of vehicles, cost of tyres and tubes, cost of their retreading, over

hauling of vehicles, painting, etc.

3. Running Charges. They are incurred when the vehicle is in operation and they vary

with the variation in the level of operation and thus in fact they are variable costs.

Examples of such costs are petrol, oil, grease, part of wages of drivers and

conductors etc.

Depreciation is a semi-variable item which depending upon the method of charging

depreciation may be included under fixed or running charges.

In order to make a comparative assessment it may be beneficial to compare the figures of the

current period with those of the previous period. This will help in judging the operating

efficiency of the current period.

ii. Power House Costing :-

Power-house operating cost statement may be prepared after accumulating data about the

costs of producing the steam and the costs of generating the electricity. The unit of cost for

production of steam may be ‘per lb’. And for generation of electricity ‘per kilowatt’. A

composite unit of cost may be used i.e. the kilowatt-hour. The cost of producing steam shall

include the raw material costs, e.g. coal, water softeners etc. , labour costs e.g. wages paid

for stocking and coal handling; and overhead costs e.g. storage costs, costs of supervision,

repairs and maintenance; depreciation etc. Besides the cost of steam which shall be used for

generation e.g. wages of the operators and other overhead costs as for production of steam.

For controlling the costs, figures, for a particular period may be compared with the figures

for a previous period and cumulative costs may also be calculated.

iii. Canteen Costing :-

The expenditure incurred for serving meals or dishes of different varieties may be grouped

under various head like provisions, labour, services, consumable stores and miscellaneous

items. An estimate will have to be prepared for the number of persons to be catered each day

and the choice of their dishes. The fixation of price for main meals and for subsidiary items is

a difficult task because of difficulty in appropriating the overhead costs to different items,

some being served frequently and some rather irregularly. However, the cost per meal can be

calculated on a general basis by assembling the cost data and then allocating it to the meals

served during a period.

A cost statement may also provide information about the subsidy received, if any, from any

agency and the revenue from sales etc. so as to show the net operating profit or loss.

ADVANTAGES OF SERVICE AND OPERATING COSTING :-

a) Intangibility

The nature of the service (as opposed to a product) is nonphysical.

A service company will have no inventory of completed services and minimal to moderate inventories of supplies. Thus, a service company does not emphasize accounting for the cost of inventories.

b. Inseparability

Customers are involved in the production of a service because the production and consumption of a service occur almost simultaneously.

Differences in customers affect service companies more than manufacturing firms. Costs are accounted for by customer type.

Service quality is often evaluated based on how the service is presented to the customer.

c. Heterogeneity of labor

There are greater chances for variations in the performance of services than there are for the production of a product.

Service companies recognize the differences in labor. Thus, the continuous measurement of productivity and quality of a service company becomes very important.

d. Perishability

Services cannot be inventoried but must be consumed when performed.

Service benefits expire quickly. There is no inventory.

A standardized system is needed to handle repeat customers.

DISADVANTAGES OF SERVICE AND OPERATING COSTING :-

More time consuming to collect data Cost of buying, implementing and maintaining activity based system Lots of clerical work.

CONCLUSION:-

Cost accounting is the process of collecting and interpreting information to determine how an organization earns and uses funds. There are multiple advantages to using cost accounting, since it provides vastly more actionable information than the financial statements produced through financial accounting. Here are the key advantages of cost accounting to consider:

Cost object analysis. Revenues and expenses can be clustered by cost object, such as by product, product line, and distribution channel, to determine which ones are profitable or require further support.

Discovers causes. An effective cost accountant not only locates problems within a company, but also drills down through the data to determine the exact cause of the issue, and also recommends solutions to management.

Trend analysis. Costs can be tracked on a trend line to discover expense surges that may be indicative of long-term trends.

Modeling. Costs can be modeled at different activity levels. For example, if management is contemplating the addition of a second shift, cost accounting can be used to derive the additional costs associated with that shift.

Acquisitions. The cost structures of possible acquisition candidates can be examined to see if costs can be pruned in some areas, thereby justifying the cost of the acquisition.

Project billings. If a company is billing a customer based on costs incurred, cost accounting can be used to accumulate costs by project and roll this information into customer billings.

Budget compliance. Actual costs incurred can be compared to budgeted or standard costs, to see if any part of a business is spending more than expected.

Capacity. The ability of a business to support increased sales levels can be examined by exploring the amount of its excess capacity. Conversely, equipment that is idle can be sold off, thereby reducing the asset base of the organization.

Inventory valuation. The cost accountant is usually tasked with accumulating the cost of inventory for financial reporting purposes. This includes charging direct labor to inventory, as well as allocating factory overhead to inventory.