Embed Size (px)

Citation preview

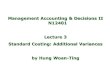

Long Ago

Before AS 19……

I want to buy this school bus will you lend me Rs. 5,00,000/- ?????

Ok what security you are giving against the money which I

lend

I don’t have security…. Please lend me money..

Don’t worry I have an idea

I will buy the bus and will give it to you on rental basis

You can use it for 5 years

Every year you have to pay me an installment of Rs.160000. and last with an additional amount of Rs. 5,000/- then you can own the bus

I agree to all your Terms n Conditions.

I will make payments as agreed and will use the Bus for 5 years.

Accounting Standard - 19

Accounting for Leases

Point of Discussions

1 •Applicability, Scope & Objective of AS 19

2 •Definitions & Lease Terms

3 •Classification of Lease

4 •Accounting for lease and its Disclosure requirements

5 •Sale and Lease Back Transactions

ApplicabilityEffective in respect of all assets leased on or after 1st April, 2001

Mandatory in nature

Prescribes appropriate Accounting Policies & Disclosures to lessor and lessee in relation to Finance & Operating Lease

lease agreements to explore for or use natural resources, such as oil, gas, timber, metals and other mineral rights

licensing agreements for items such as motion picture films, video recordings, plays, manuscripts, patents and copyrights

lease agreements to use lands.

Exclusions

Definition of Lease

A lease is an agreement whereby the lessor conveys to the lessee in return for a payment or series of payments the right to use an asset for an agreed period of time.

Owner/LesserTransfers the

right to use the asset

User/ Lessee

This AS applies to agreements that transfers the right to use assets even though substantial services by the lessor may be called for in connection with the operation or maintenance of such assets.

This AS does not apply to agreements that are contracts for services that do not transfer the right to use assets from one contacting party to the other.

Applicable

Not Applicable

Economic life of an Asset

Either

The period over which the asset is expected to be economically usable by one or more users

Or

The number of production or similar units expected to be obtained from the asset by one or more users

Useful life of a leased asset

Either

The period over which the leased asset is expected to be used by the Lessee

Or

The number of production or similar units expected to be obtained from the asset by the Lessee

Fair Value•The value at which the asset could be exchanged or a liability could be settled between knowledgeable, willing parties in an arm’s length transaction

Residual Value•Estimated fair value of the asset at the end of the lease term

Residual Value

Guaranteed Residual Value

Unguaranteed residual value

Guaranteed Residual Value (GRV)

In case of lessee

• Guaranteed by the lessee • By a party on behalf of the lessee

In case of Lessor

• Guaranteed by the lessee or• By a party on behalf of the lessee or• By an independent 3rd party who is financially capable of discharging the obligations under the guarantee

Minimum Lease Payments (MLP)Payments over the lease terms that the lessee is or can be required to

make, excluding Contingent Rent, Costs for services and taxes to be paid by and reimbursed to the lessor together with

In the case of Lessee, any GRV by or on behalf of lessee;

In the case of Lessor, Any GRV by or behalf of lesser or independent third party

It also includes the payments required to be made to exercise the Purchase Option (PO) if such option exists.

Minimum Lease Payments (MLP)

O It is the consideration under the lease contract.

MLP

LP + GRV

Contingent RentO It is that portion of the lease payments that

is not fixed in amount but is based on a factor other than just passage of time.

O Example : Percentage of sales

Interest rate implicit in the lease

It is the discount rate that at the inception of lease causes the aggregate present value of MLP and any URV to be equal to the fair value of the asset.

PV(MLP) PV(URV) FV

Lessee’s Incremental borrowing cost

It is the rate of interest the lessee would have to pay on a similar lease or, if that’s not determinable, the rate that, at the inception of the lease, the lessee would incur to borrow over a similar term, and with a similar security, the funds necessary to purchase the asset.

Gross Investment in the Lease

It is the aggregate of the minimum lease payments under a finance lease from the standpoint of the lessor and any unguaranteed residual value accruing to the lessor

MLP URV GI

Unearned Finance IncomeIt is the difference between Gross Investment in the lease and;O Present value of

O MLP from standpoint of lessorO Any URV accruing to the lessor, at the

interest rate implicit in the lease.

GI PV( GI)Unearned

finance income

Net InvestmentIt is the gross investment in the lease reduced by unearned finance income.

GIUnearned

finance income

Net Investment

PV( GI)Net

Investment

Definitions in other words

Unearned Finance income = GI - NI

NI = PV(GI)

NI = GI –[GI-PV(GI)]

NI = GI – Unearned Finance Income

Unearned Finance Income = GI – PV(GI)

Unearned Finance Income = GI – PV( MLP+URV)

GI = (LP + GRV) + URV

GI = MLP + URV

MLP=LP+GRV or MLP = LP + PO

RV=GRV+URV

Balance Outstanding

MLP Finance charge Principal Balance Outstanding

5,00,000

1,60,000

91,200

68,800 4,31,200

4,31,200

1,60,000

78,651

81,349 3,49,851

3,49,851

1,60,000

63,813

96,187 2,53,664

2,53,664

1,60,000

46,268

1,13,732 1,39,932

1,39,932

1,65,000

25,068

1,39,932 0

8,05,000

3,05,000

5,00,000

Classification of Lease

• Lease that transfers substantially all the risks and rewards incident to the ownership

Finance Lease

• Lease other than finance lease

Operating Lease

Basis for Classification

Risks

• Includes the possibilities of losses from idle capacity or Technological obsolescence and of variations in return due to changing economic conditions

Rewards

• Represents the expectation of profitable operation over the economic life of the asset and of gain from appreciation in value or realisation of residual value

Situations which would normally lead to a lease being classified as a finance lease;O The lease transfers ownership of the asset to the

lessee by the end of the lease termO The lessee has the option to purchase the asset at a

price lesser than fair value.O The lease term is for the major part of the economic

life of the asset even if title is not transferredO At the inception of the lease, Present value of the

MLP amounts to at least all of the fair value of the leased amount

O The asset is of a specialised nature such that only the lessee can use it without major modifications being made

O If on cancellation of the lease by the lessee, the consequent losses of lessor are borne by the lessee.

O Gains or losses from the fluctuation in the fair value of the residual fall to the lessee.

O The lessee can continue the lease for a secondary period at a rent which is substantially lower than market value.

Reclassification of leaseO Lease classification is made at the inception of the

leaseO If lessor and lessee agree to change the provision of

the lease terms other than by renewing it, in a manner that would have resulted in a different classification, the revised agreement is considered as a new agreement over its revised term.

O The change in estimates of the Economic life or of the residual value of the leased asset do not give rise to a new classification of the lease for accounting purposes.

Finance lease (Books of Lessee)

The discount rate is the interest rate implicit on the lease is this is practicable to determine, if not, the lessee’s incremental borrowing rate should be used.

The amount is equal to fair value of the leased asset or present value of the MLP from lessee’s view point, whichever is lower

At the inception, lessee recognises the lease as an asset and a liability

Finance lease give rise to a depreciation, it should be calculated in accordance with AS 6

Initial direct cost incurred specifically for the lease should be included in the amount recognised as an asset under the lease.

Finance charge is allocated over the lease term in such a way that it would produce constant rate of return on the principal balance

Each lease payments is apportioned between finance charge and reduction of the outstanding liability

Journal EntriesAt the inception of the lease

Leased Asset DR XXX

To Leased Liability XXX

When MLP is Paid

Interest or Finance Charge DR xxx

Lease Liability DR xxx

To Bank xxx

At the end of the FY

Depreciation DR Xxx

To Leased Asset Xxx

At the end of the lease Term

A. If the asset is purchased at GRV

Leased Liability DR XXX

To Bank xxx

B. If the asset is reverted back to the Lessor

Lease Liability DR xxx

To Asset xxx

DisclosureO Assets acquired under finance lease to be

segregated from the assets ownedO Net Carrying amount at the balance sheet

date of each class of assetsO Contingent rent recognised as an expenses

in the statement of profit and loss for the period

O A Reconciliation between the total of MLP’s at the balance sheet date and their PV’s

DisclosureO The total of MLP’s and their PV’s at the balance

sheet date for each of the following periods should be disclosed;O Not later than 1 yearO Later than 1 year and not later than 5 yearsO Later than 5 years

O Total future minimum sublease payments received under non cancellable subleases at the balance sheet date

O A General description of Lessee’s significant leasing arrangements.

Books of the Lessor

Any direct cost incurred at the inception of the lease may either be recognised immediately or allocated against the finance income over the lease term.

Lease rental receivable is treated as repayment of Principal (i.e. NI in lease) and a finance income to reimburse the lessor for its investment and services.

In case where no URV is expected to accrue to the lessor, the amounts of lease receivable recorded by the Lessor and the amount of lease liability recorded by the lessee are same.

NI = PV(MLP) + PV (URV), Discounting factor is the interest rate implicit on the lease

Recognises the asset given as a receivable at an amount equal to Net Investment in the lease

Journal Entries

At the inception of the lease

Leased Receivable DR XXX

To Leased Asset XXX

When MLP is Paid

Bank DR XXX

To Interest or Finance Income XXX

To Lease Receivable XXX

At the end of the lease Term

A. If the asset is purchased at GRV

Bank Account DR XXX

P & L account DR XXX

To Lease Receivable Account XXX

B. If the asset is reverted back to the lessor

Asset DR XXX

To Lease Receivable XXX

DisclosureO A reconciliation between the total GI and present value of the

MLP’s receivable at the balance sheet date, along with for each of the following periods;O Not later than 1 yearO Later than 1 year but Not later than 5 yearsO Later than 5 years

O Unearned finance incomeO UGV accruing to the benefit of the lessorO Accumulated provisions for uncollectible MLPs receivableO Contingent rents recognised in P& L Account for the periodO A general description of the significant leasing arrangement of

the lessorO Accounting policy adopted in respect of initial direct costs

Operating Lease (Books of Lessee)

Straight lining means the total lease rent will be averaged to three years i.e. Rs.30,000/- per year should be recognised in the P&L.

Example: Suppose an asset was taken on operating lease for a period of 3 years. The lease rent for three years was Rs. 15,000/-, 30,000/- and 45,000/- respectively.

Lease should be recognised as an expense in the statement of P& L on SLM basis over the lease term unless another systematic basis is more representative of the time pattern of the user’s benefit even if the payments are not on that basis.

DisclosureO Total of future MLP’s under non cancellable operating leases

for each of the following periods;O Not later than 1 yearO Later than 1 year and not later than 5 yearsO Later than 5 years

O Total of future minimum sublease payment expected to be received under non cancellable subleases at the balance sheet date.

O Lease payments recognised in the statement of P& L for the period with separate amounts for MLP’s and contingent rent.

O Sublease payments received or receivable recognisedO A general description of the lessee’s significant lease

arrangements

Books of Lessor

Depreciation of leased assets should be charged as per AS 6

Any direct cost incurred at the inception of the lease may either be recognised immediately or allocated against the finance income over the lease term.

Recognise the lease income statement of P& L on SLM basis over the lease term unless another systematic basis is more representative of the time pattern of the user’s benefit.

Record the leased asset as its fixed asset in the balance sheet

DisclosureO Gross carrying amount, accumulated

depreciation and accumulated impairment losses at the balance sheet date for each class of assets

O And all other disclosures that is applicable to Finance lease.

Sale and Lease back

Seller

BuyerLease

O The lease payments and the sale price are usually interdependent as they are negotiated as a package.

O The accounting treatment of a sale and leaseback transaction depends upon the type of lease involved.

O Accounting for sale and finance lease back is covered under para 48 and for sale and operating lease back is covered under para 50 & 52 of the AS.

Sales Proceeds

Carrying Amount (Book Value)

Excess/ Deficit

• To be deferred and amortised over the lease term in proportion to the depreciation of the leased asset

Para 50 & 52Carrying Amount

Treatment of P/L on Sale

when SP =<> FV

IF CA> FV , Record

Impairment Loss

Fair Value

Selling Price

Para 52 Para 50

Para 50 & 52O Para 50 compares the Selling Price with Fair

Value of the assetO Para 52 compares the Carrying amount in

the books with the fair value of the assetO One should always check for para 52

condition and then check for para 50 condition.

Para 52

Immediately recognised in the P & L

Loss= Carrying amount – Fair Value

Fair Value < Carrying Amount

Para 50

SP = FV, SP < FV, SP > FV

Para 50 Compares Selling price with Fair Value and the treatment of profit or loss depends upon whether

SP FV

Profit or Loss to be recognised immediately in the P & L

SP < FV

Profit

Recognise immediately in the P & L

Loss

If compensated by the future lease payments at below market price, defer and amortise in proportion to the lease payments

Loss

If not compensated recognise immediately.

SP > FV

Balance if any is recognised in P& L Immediately

Deferred and amortised over the period for which the asset is expected to be used

Excess of SP over FV

CA = 120

FV = 100 FV = 100

SP = 120

SP = 100

SP = 80Rs 20 Loss to be books immediately

20 Profit to be deferred

No P/L

Rs. 20 loss if compensated then Deferred

CA = 80

FV = 100

SP = 120

SP = 100

SP = 70

Profit 40, of Which 20 Deferred, and 20

recognised immediately

Profit 20 recognised Immediately

Rs. 10 loss if compensated then

Deferred, else recognised

immediately

Thank You