Embed Size (px)

Citation preview

Accounting RoundupYear in Review — 2012

To our clients, colleagues, and other friends:

Welcome to the 2012 edition of Accounting Roundup: Year in Review. In 2012, the FASB and IASB continued their efforts to converge their various projects. There was also an increased international focus on regulatory and compliance topics such as ethics, professional competency, and professional skepticism. In the United States, the Private Company Council (PCC) was created earlier this year to improve the standard-setting process for private companies. And the SEC, in addition to releasing an order providing relief to filers affected by Hurricane Sandy, issued various final rules and guides.

The AICPA held its annual National Conference on Current SEC and PCAOB Developments in early December. During the conference, representatives from the SEC, PCAOB, FASB, IASB, and other organizations provided updates on new developments, regulations, and current priorities. For more information about the conference, see Deloitte’s December 11, 2012, Heads Up.

Accounting Roundup: Year in Review summarizes final guidance that affects reporting and disclosures for the coming reporting season. With the exception of guidance issued in December, proposed guidance, such as exposure drafts and invitations to comment, is not included. Please see our 2012 monthly and quarterly issues of Accounting Roundup for more information about these documents.

In addition, note that in this year-end edition, an asterisk in the article title denotes events that occurred in December or that were not addressed in previous 2012 issues of Accounting Roundup, including updates to previously reported topics. Events without asterisks were covered in those previous issues.

As usual, click any title in the table of contents to go directly to the article. For additional information about a topic, click the hyperlinks, which are blue. Further details are also on the Web sites of the accounting standard setters and regulators, including the FASB, GASB, SEC, PCAOB, AICPA, and IASB.

So what will be the focus for 2013? The FASB expects to publish final standards on revenue, consolidation, investment companies, presentation of comprehensive income, and the liquidation basis of accounting, while the IASB expects to publish final standards on hedge accounting in addition to completing joint projects with the FASB. Also watch for additional standard-setting activities from the PCC. We encourage you to keep up to date on the actions of the regulators and standard setters during 2013 through our Accounting Roundup series, EITF Snapshot series, Heads Up articles, and Dbriefs webcasts.

We hope that Accounting Roundup: Year in Review will be helpful to you this financial reporting season. As always, we welcome your feedback. Please send questions and comments to [email protected].

Happy New Year,

Deloitte & Touche LLP

Edited by Magnus Orrell and Jiaojiao Tian-Lee, Deloitte & Touche LLP

ContentsAccounting Developments 1

Bank Accounting 1OCC Publishes Update to BAAS 1

OCC Issues Bulletin on TDRs 1

Codification 1FASB Issues ASUs to Amend Codification 1

Disclosure 1FASB and CAQ Issue Summary of Observations From Two Forums on Disclosure Effectiveness* 1

EITF Activity 2FASB Issues Three ASUs Related to Recent EITF Consensuses 2

FASAC 2Four New Members Appointed to the Financial Accounting Standards Advisory Council* 2

Financial Instruments: Classification and Measurement 2FASB Tentatively Decides to Draft Proposed ASU on Classification and Measurement of Financial Instruments* 2

Financial Instruments: Credit Losses 3FASB Issues Proposed ASU on Accounting for Credit Losses on Financial Instruments* 3

Financial Instruments: Repurchase Agreements 3FASB Makes Tentative Decision on Held-to-Maturity Classification of Securities Transferred Under Held-to-Maturity

Repurchase Agreements* 3

Health Care and Continuing Care 3FASB Issues ASU on Refundable Advance Fees for Continuing Care Communities 3

AICPA Issues TPA on Accounting for Costs Incurred During ICD-10 Implementation 3

Intangible Assets 4FASB Issues ASU on Testing Indefinite-Lived Intangible Assets for Impairment 4

iii

iv

Accounting RoundupYear in Review — 2012

Investment Companies 4FASB Makes Tentative Decision About Scope of Guidance on Investment Companies* 4

Liquidation Basis of Accounting 4FASB Continues Deliberations of Liquidation Basis of Accounting* 4

Presentation of Other Comprehensive Income 5FASB Redeliberates Reclassification Adjustment Proposals* 5

Private Companies 5PCC Holds Inaugural Meeting and Identifies Four Topics for Future Consideration* 5

FAF Issues Final Report on Establishment of Private Company Council 5

Reporting Discontinued Operations 5FASB Makes Various Tentative Decisions Related to Discontinued Operations* 5

Revenue 6FASB and IASB Continue Redeliberating Revenue Exposure Draft* 6

XBRL 6FASB Releases 2012 U.S. GAAP Financial Reporting XBRL Taxonomy 6

IFRS Foundation Publishes 2012 IFRS Taxonomy 6

International 6IASB Issues Statement on Future Work Plan* 6

IASB Publishes Three EDs for Public Comment* 7

IASB Issues Guidance on Investment Entities 7

IASB Makes Editorial Corrections to IFRSs 7

IASB Issues Amendments to Consolidation Guidance 8

IASB Publishes Four Q&As on IFRS for SMEs 8

IASB Finalizes Amendments to IFRSs as Part of Annual Improvements Project 8

IASB Issues Amendments to IFRS 1 8

IFRS Foundation Publishes 2013 IFRS “Blue Book”* 8

Auditing Developments 9

AICPA 9AICPA Issues SOP on Reporting Under Global Investment Performance Standards 9

AICPA Issues Auditing Standard on Going Concern 9

AICPA Issues Practice Aid Related to Audits of Employee Benefit Plans 9

ASB Issues Guidance to Help Auditors Apply Clarified Auditing Standards 9

ASB Issues SAS 125 as Part of Clarity Project 9

CAQ 10CAQ Releases Guide Summarizing PCAOB Inspection Process 10

Auditor Evaluation Tool for Audit Committees Released 10

CAQ Issues Practice Aid on Communications With Audit Committees 10

SEC Staff Reminds Auditors of Foreign Private Issuers About Audit Report Requirements Under IFRSs 10

v

Accounting RoundupYear in Review — 2012

IIA 10IIA Issues Revisions to Internal Audit Standards 10

PCAOB 11SEC Approves PCAOB Auditing Standard 16* 11

PCAOB Releases Inspection Report on Audits of Internal Control Over Financial Reporting* 11

PCAOB Issues Audit Practice Alert on Professional Skepticism* 11

International 11IAASB Issues Standard on Review Engagements 11

IAASB Issues New Standard on Assurance on Greenhouse Gas Statements 11

IAASB Issues Revised Standard on Using the Work of Internal Auditors 11

IAASB Issues Revised Standard on Compilations 12

IAESB Releases Revised Standard on Assessment of Professional Competence 12

IAESB Issues Revised Standard on Continuing Professional Development 12

IESBA Releases Q&As on Implementing Code of Ethics 12

IFAC Releases Revisions to Policy Position Paper 2 12

IAASB Staff Issues Q&A Document on Professional Skepticism 12

Governmental Accounting and Auditing Developments 13

FASAB 13FASAB Issues Statement on Funds From Dedicated Collections 13

FASAB Issues Statement on Deferred Maintenance and Repairs 13

GASB 13Six New Members Appointed to the Governmental Accounting Standards Advisory Council* 13

GASB Posts New Pension Standards to Its Web Site 14

GASB Issues Two Statements 14

GASB Expands and Revises User Guide on Local-Government Finances 14

OMB 14OMB Issues 2012 Edition of OMB Circular A-133: Compliance Supplement 14

International 14IFAC Issues Paper on Public-Sector Financial Management Transparency and Accountability 14

Regulatory and Compliance Developments 15

SEC 15Paul A. Beswick Appointed as SEC Chief Accountant* 15

SEC and Justice Department Release FCPA Guide 15

SEC Issues Final Rule on Risk Management and Operations of Clearing Agencies 15

SEC Updates EDGAR Filer Manual 15

SEC Issues New FAQs on Title I of the JOBS Act 16

SEC Issues Risk Alert Related to Compliance With Municipal Securities Rules 16

SEC Issues Final Rule on Disclosing Payments Made by Issuers Engaged in Resource Extraction 16

SEC Issues Final Rule on Conflict Minerals 16

New Disclosure Requirement for Issuers Engaged in Sanctionable Activities With Iran and Syria* 17

vi

Accounting RoundupYear in Review — 2012

SEC Issues Small-Entity Compliance Guide on Listing Standards for Compensation Committees 17

SEC’s Observations Regarding Disclosures of Smaller Financial Institutions 17

SEC Sends Sample Letter to Financial Institutions About Prospectus Supplements and Structured Note Offerings 17

JOBS Act Signed Into Law to Ease Access to Investment Capital 18

SEC Issues Guidance on Disclosures About European Sovereign Debt Exposures 18

SEC Issues Final Rule on Mine Safety Disclosure Requirements 18

COSO 19COSO Issues White Paper on Risk Assessment 19

International 19IFAC Issues Policy Position Paper on Effective Governance, Risk Management, and Internal Control* 19

Basel Committee Issues Revised Securitization Framework for Public Comment* 19

Basel Committee Issues New Regulatory Capital Disclosure Requirements 19

IOSCO and CPSS Issues Disclosure Framework and Assessment Methodology for Financial Market Infrastructures* 19

IOSCO Publishes Principles for Ongoing Disclosures About Asset-Backed Securities 20

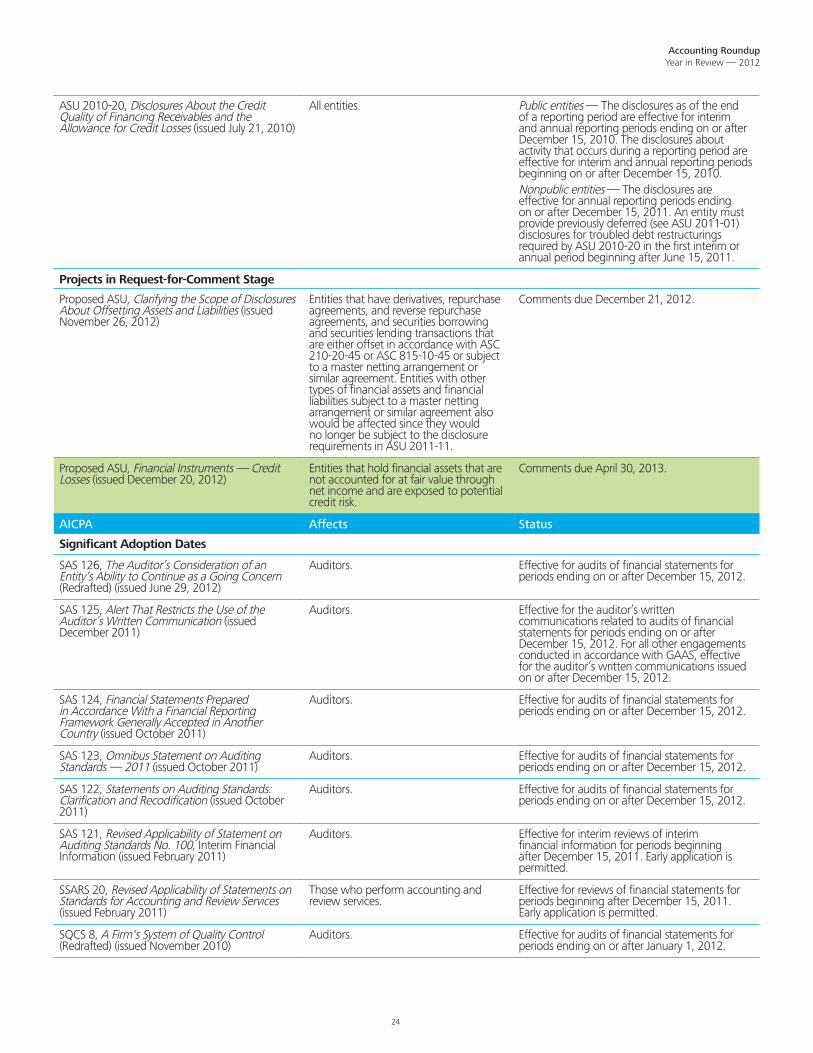

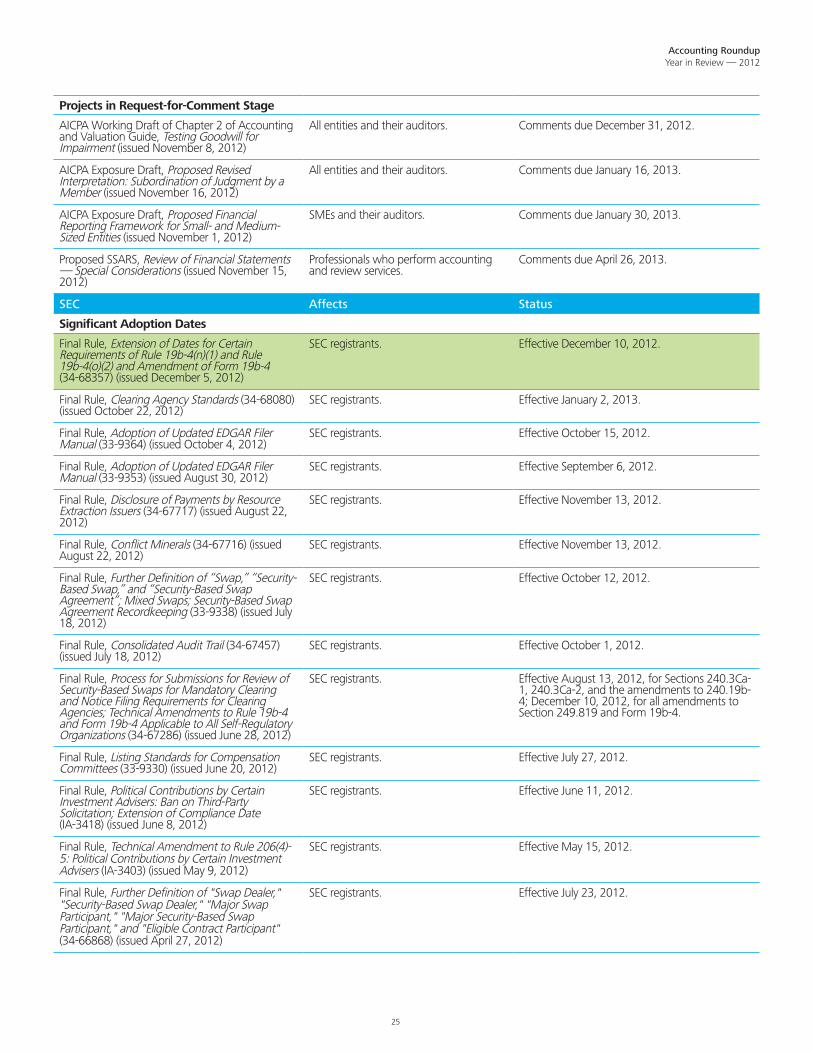

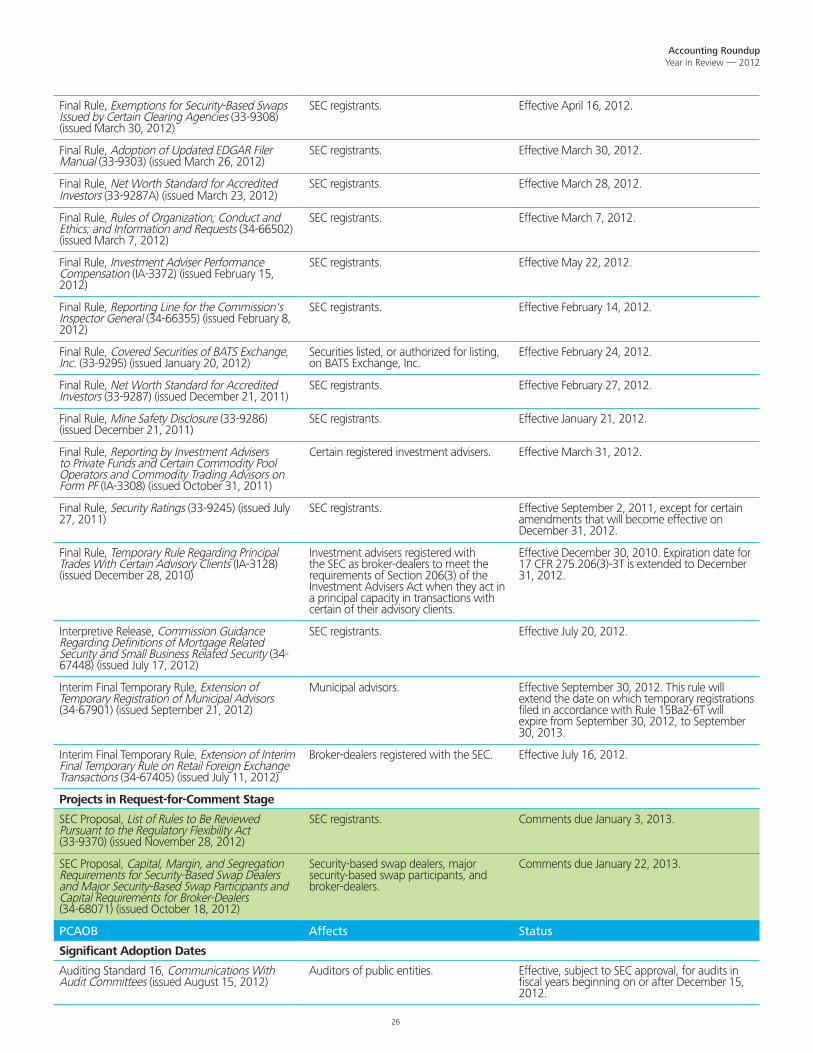

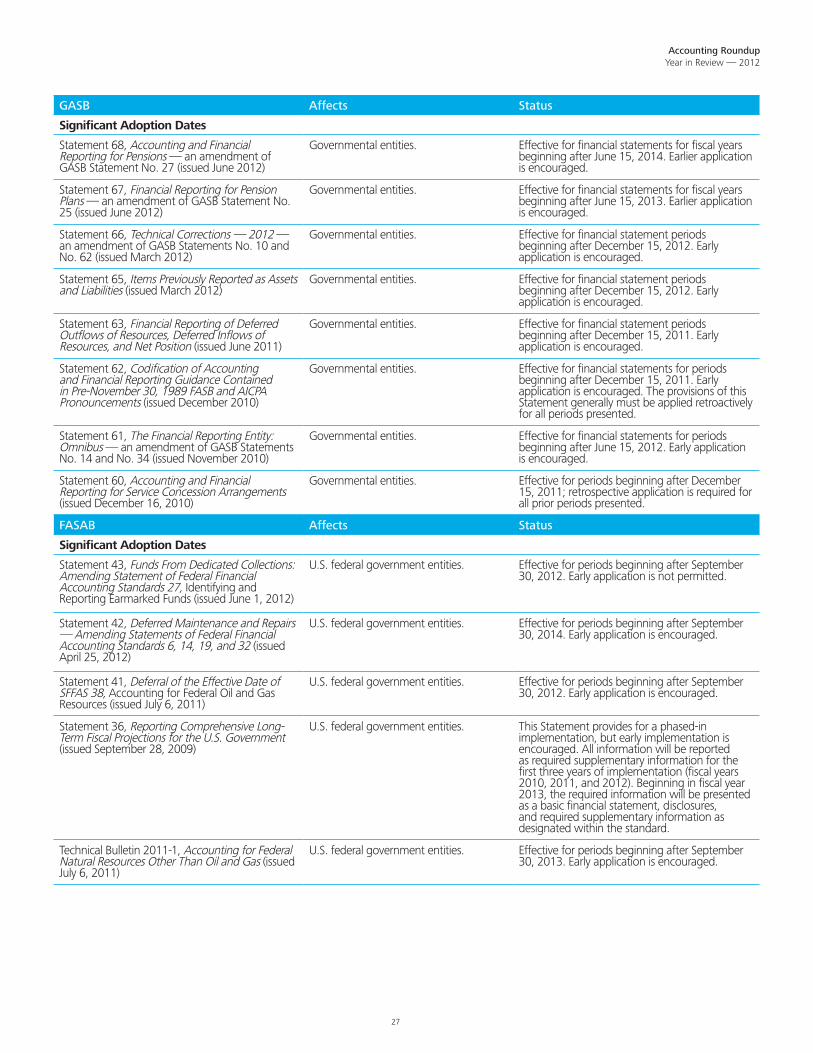

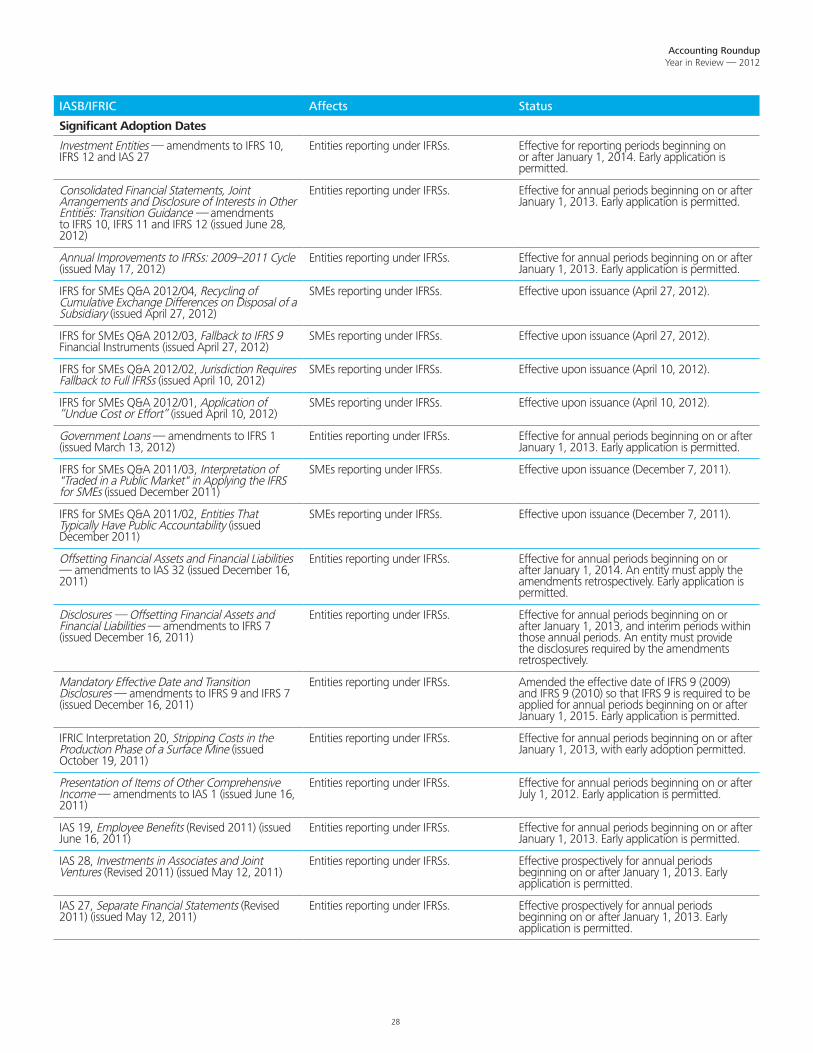

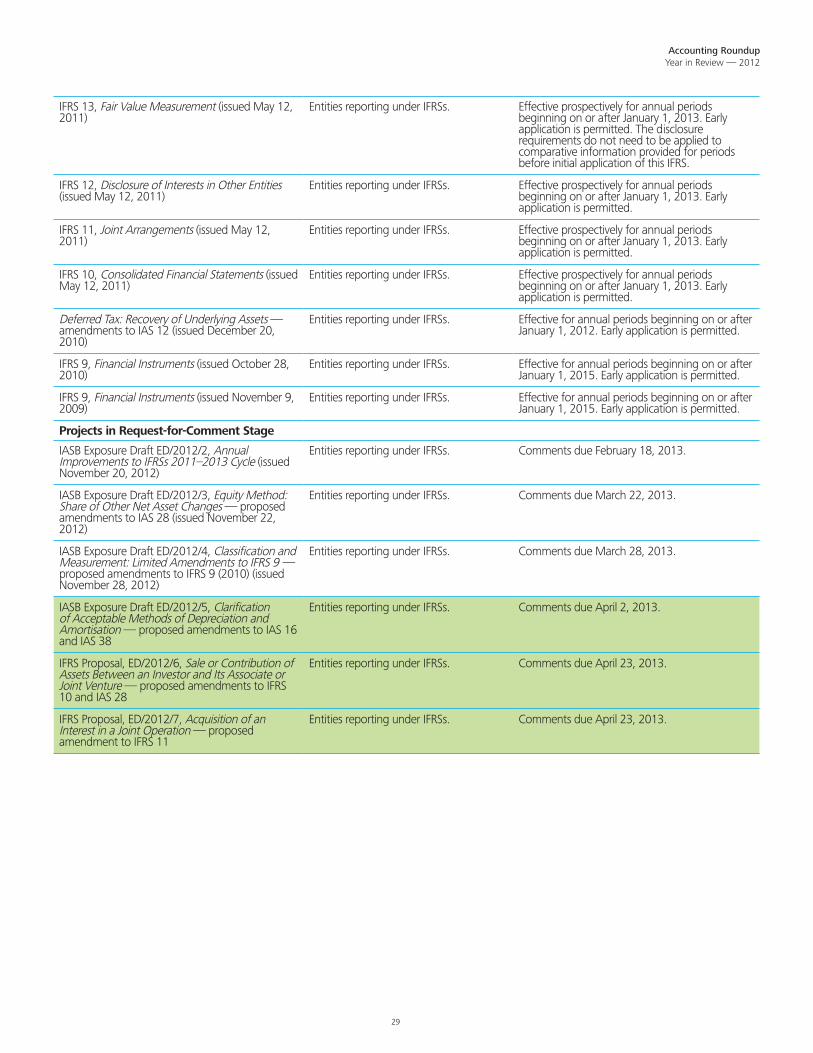

Appendix A: Significant Adoption Dates and Deadlines 21

Appendix B: Glossary of Standards 30

Appendix C: Abbreviations 33

1

Accounting RoundupYear in Review — 2012

Accounting Developments

Bank Accounting

OCC Publishes Update to BAAS

Affects: National banks and federal savings associations.

Summary: On July 25, 2012, the OCC’s Office of the Chief Accountant released an update to its BAAS, which provides the OCC’s views on various accounting-related topics that apply to banks and federal savings associations. This update includes new Q&As on TDRs, nonaccrual accounting, and insurance claims, among other items.

Other Resources: For more information, see the press release on the OCC’s Web site. •OCC Issues Bulletin on TDRs

Affects: National banks and federal savings associations.

Summary: On April 5, 2012, the OCC released a bulletin for national banks and federal savings associations (collectively, “banks“) that addresses “many inquiries received from bankers and examiners on the accounting and reporting requirements“ for TDRs, particularly loan renewals and extensions of substandard commercial loans. The bulletin reminded banks of the TDR guidance in the FASB’s ASU 2011-02. In addition, the OCC pointed banks to the FFIEC’s supplemental call report instructions for additional guidance on TDRs, including on how to apply the ASU. •

Codification

FASB Issues ASUs to Amend Codification

Affects: All entities.

Summary: On October 1, 2012, the FASB issued ASU 2012-04, which makes certain technical corrections (i.e., relatively minor corrections and clarifications) and “conforming fair value amendments“ to the FASB Accounting Standards Codification. The amendments affect various ASC topics and apply to all reporting entities within the scope of those topics. For more information, see Deloitte’s October 5, 2012, Heads Up.

In addition, on August 27, 2012, the FASB issued ASU 2012-03, which amends a number of SEC sections in the FASB Accounting Standards Codification as a result of (1) the issuance of SAB 114, (2) the issuance of SEC Final Rule 33-9250, and (3) corrections related to ASU 2010-22. •

Disclosure

FASB and CAQ Issue Summary of Observations From Two Forums on Disclosure Effectiveness*

Affects: All entities.

Summary: On December 12, 2012, the FASB and CAQ issued a summary of observations based on two disclosure effectiveness forums they hosted in October 2012. A wide range of financial statement users participated and provided comments on various disclosure-related topics.

Other Resources: For more information, see the press release on the FASB’s Web site. •

2

Accounting RoundupYear in Review — 2012

EITF Activity

FASB Issues Three ASUs Related to Recent EITF Consensuses

Affects: All entities.

Summary: In October 2012, the FASB issued ASUs related to three EITF consensuses reached earlier this year. The three final ASUs and related EITF Issues are as follows:

• ASU 2012-07, Accounting for Fair Value Information That Arises After the Measurement Date and Its Inclusion in the Impairment Analysis of Unamortized Film Costs (EITF Issue 12-E).

• ASU 2012-06, Subsequent Accounting for an Indemnification Asset Recognized at the Acquisition Date as a Result of a Government-Assisted Acquisition of a Financial Institution (EITF Issue 12-C).

• ASU 2012-05, Not-for-Profit Entities: Classification of the Sale Proceeds of Donated Financial Assets in the Statement of Cash Flows (EITF Issue 12-A).

Next Steps: The effective dates for the final ASUs are as follows:

• ASU 2012-07: For SEC filers, impairment tests performed on or after December 15, 2012. For all other entities, impairment tests performed on or after December 15, 2013. Early adoption is permitted.

• ASU 2012-06: Fiscal years, and interim periods within those years, beginning on or after December 15, 2012. Early adoption is permitted.

• ASU 2012-05: Fiscal years, and interim periods within those years, beginning after June 15, 2013. Early adoption is permitted.

Other Resources: Deloitte’s September 2012 EITF Snapshot. •FASAC

Four New Members Appointed to the Financial Accounting Standards Advisory Council*

Affects: All entities.

Summary: On December 4, 2012, four new members were appointed to the FASAC for a one-year term beginning on January 1, 2013. Further, the terms of the 30 current members were renewed for an additional year.

Other Resources: For more information, see the press release on the FAF’s Web site. •Financial Instruments: Classification and Measurement

FASB Tentatively Decides to Draft Proposed ASU on Classification and Measurement of Financial Instruments*

Affects: All entities.

Summary: At its December 12, 2012, meeting, the FASB tentatively agreed to have the staff draft a proposed ASU on classification and measurement of financial instruments. The comment period for the ASU will be “the longer of (1) 90 days from the exposure date of the proposed Update or (2) April 30, 2013.“

Next Steps: The FASB expects to issue the ED in the first quarter of 2013.

Other Resources: For more information, see the project page on the FASB’s Web site. •

3

Accounting RoundupYear in Review — 2012

Financial Instruments: Credit Losses

FASB Issues Proposed ASU on Accounting for Credit Losses on Financial Instruments*

Affects: All entities.

Summary: On December 20, 2012, the FASB issued an ED of a proposed ASU on accounting for credit losses on financial instruments. The ED “proposes a new accounting model intended to require more timely recognition of credit losses, while also providing additional transparency about credit risk.“

Next Steps: Comments on the proposed ASU are due by April 30, 2013.

Other Resources: Deloitte’s December 21, 2012, Heads Up. Also see the press release on the FASB’s Web site. •Financial Instruments: Repurchase Agreements

FASB Makes Tentative Decision on Held-to-Maturity Classification of Securities Transferred Under Held-to-Maturity Repurchase Agreements*

Affects: All entities.

Summary: At its December 12, 2012, meeting, the FASB tentatively decided that “a transfer of a held-to-maturity debt security in a repurchase-to-maturity agreement accounted for as a secured borrowing would not contradict the transferor’s stated intent to hold the security to maturity and, therefore, would not call into question the transferor’s intent to hold other debt securities to maturity.“

Next Steps: The FASB expects to issue a proposed ASU on this topic in the first quarter of 2013.

Other Resources: For more information, see the project page on the FASB’s Web site. •Health Care and Continuing Care

FASB Issues ASU on Refundable Advance Fees for Continuing Care Communities

Affects: Continuing care retirement communities (CCRCs).

Summary: On July 24, 2012, the FASB issued ASU 2012-01, which clarifies that an advance fee from a CCRC resident should be classified as deferred revenue if (1) the contract stipulates that this advance fee must be repaid when a room is reoccupied by a future resident and (2) the refundable amount is “limited to the proceeds from reoccupancy.“ If the refundable amount is not limited to the proceeds from reoccupancy, the advance fee must be reported as a liability.

Next Steps: For public entities, including conduit bond obligors, the ASU is effective for fiscal periods beginning after December 15, 2012. For nonpublic entities, the ASU is effective for fiscal periods beginning after December 15, 2013. Early adoption is permitted. •

AICPA Issues TPA on Accounting for Costs Incurred During ICD-10 Implementation

Affects: Health care entities.

Summary: On July 18, 2012, the AICPA published a TPA addressing how health care entities should account for costs incurred as a result of the transition from the ninth edition of the World Health Organization’s International Classification of Diseases (ICD-9) coding system to the tenth edition (ICD-10).

The transition from ICD-9 to ICD-10 is mandatory, and entities are expected to incur significant costs in complying with the new requirements.

Other Resources: Deloitte’s June 2012 Health Care Providers Spotlight. •

4

Accounting RoundupYear in Review — 2012

Intangible Assets

FASB Issues ASU on Testing Indefinite-Lived Intangible Assets for Impairment

Affects: All entities.

Summary: On July 27, 2012, the FASB issued ASU 2012-02, which amends the guidance in ASC 350-30 on testing indefinite-lived intangible assets, other than goodwill, for impairment. The FASB issued the ASU in response to feedback on ASU 2011-08, which amended the goodwill impairment testing requirements by allowing an entity to perform a qualitative impairment assessment before proceeding to the two- step impairment test. Similarly, under ASU 2012-02, an entity testing an indefinite-lived intangible asset for impairment has the option of performing a qualitative assessment before calculating the fair value of the asset. Although ASU 2012-02 revises the examples of events and circumstances that an entity should consider in interim periods, it does not revise the requirements to test indefinite-lived intangible assets (1) annually for impairment and (2) between annual tests if there is a change in events or circumstances.

Next Steps: ASU 2012-02 is effective for annual and interim impairment tests performed for fiscal years beginning after September 15, 2012. Early adoption is permitted.

Other Resources: Deloitte’s July 27, 2012, Heads Up. Also see the press release on the FASB’s Web site. •Investment Companies

FASB Makes Tentative Decision About Scope of Guidance on Investment Companies*

Affects: All entities.

Summary: At its December 12, 2012, meeting, the FASB tentatively decided to retain the guidance from ASC 946 that excludes real estate investment trusts, including those related to mortgages, from the scope of the guidance the Board is currently working on.

Next Steps: The FASB will continue to deliberate its guidance on investment companies and expects to issue a final standard on this topic in early 2013.

Other Resources: For more information, see the project page on the FASB’s Web site. •Liquidation Basis of Accounting

FASB Continues Deliberations of Liquidation Basis of Accounting*

Affects: All entities.

Summary: At its December 12, 2012, meeting, the Board tentatively decided “to clarify that liquidation would be considered imminent when a plan of liquidation is approved by or imposed on the entity by those with the power to do so. The Board also decided that all entities would be subject to the proposed guidance provided the entity’s liquidation was not as planned at inception.“

The Board also tentatively decided to further clarify the application of the liquidation basis of accounting to measurement of assets and liabilities.

Other Resources: For more information, see the project page on the FASB’s Web site. •

5

Accounting RoundupYear in Review — 2012

Presentation of Comprehensive Income

FASB Redeliberates Reclassification Adjustment Proposals*

Affects: All entities.

Summary: At its December 19, 2012, meeting, the FASB reaffirmed tentative decisions about reclassification adjustments that the Board made at its November meeting, including that the proposal is effective for reporting periods beginning after December 15, 2012, for public entities and December 15, 2013, for nonpublic entities. The Board also tentatively decided that an entity is not required to present the reclassification from accumulated other comprehensive income into net income on the face of the financial statements. However, an entity should present the aggregated tax effect of this reclassification.

Next Steps: The FASB expects to issue a final ASU on this topic in the first quarter of 2013.

Other Resources: For more information, see the project page on the FASB’s Web site. •Private Companies

PCC Holds Inaugural Meeting and Identifies Four Topics for Future Consideration*

Affects: Private companies.

Summary: At its inaugural meeting on December 6, 2012, the PCC discussed four topics that constituents expressed concerns about, instructing the FASB staff to develop a research memorandum to evaluate the topics for future consideration. The four topics are (1) consolidation, (2) “plain vanilla“ interest rate swaps, (3) income taxes, and (4) recognition and measurement of intangible assets (other than goodwill) acquired in a business combination.

Other Resources: For more information, see the press release on the FAF’s Web site. •FAF Issues Final Report on Establishment of Private Company Council

Affects: Private companies.

Summary: On May 23, 2012, the board of trustees of the FAF, the FASB’s parent organization, approved the formation of the PCC, which is tasked with improving the accounting standard-setting process for private companies. The two main responsibilities of the FAF will be to (1) determine whether exceptions or modifications to existing nongovernmental U.S. GAAP would benefit end users of private-company financial statements and (2) advise the FASB on how private-company accounting matters on the FASB’s technical agenda should be treated.

Further, on May 30, 2012, the FAF issued its final report on the formation of the PCC. The report summarizes the background of and key events leading to the establishment of the PCC, key matters considered by the FAF trustees when forming the PCC, details on comments the FAF received during its outreach on private-company standard setting, and an overview of the PCC’s responsibilities and operating procedures.

Other Resources: For more information, see the press release on the FAF’s Web site. •Reporting Discontinued Operations

FASB Makes Various Tentative Decisions Related to Discontinued Operations*

Affects: All entities.

Summary: At its December 12, 2012, meeting, the FASB reaffirmed its previous tentative decisions to propose disclosure requirements for (1) discontinued operations for public and nonpublic entities and (2) disposals of individually material components of an entity for public entities. Further, the Board tentatively decided to propose certain disclosure requirements for (1) noncontrolling interests in discontinued operations, (2) disposals of long-lived assets that are not components of an entity, and (3) continuing involvement and continuing cash flows.

Next Steps: The Board directed the staff to draft an ED on this topic for a 150-day comment period.

Other Resources: For more information, see the project page on the FASB’s Web site. •

6

Accounting RoundupYear in Review — 2012

Revenue

FASB and IASB Continue Redeliberating Revenue Exposure Draft*

Affects: All entities.

Summary: At their December 17, 2012, joint meeting, the FASB and IASB tentatively decided to retain the proposals in their November 2011 ED related to the costs of obtaining a contract and the residual approach to estimating the stand-alone selling price of a good or service; however, the boards tentatively decided to incorporate certain clarifications and refinements related to the residual approach into the final standard. In addition, the boards tentatively decided not to amend the proposed guidance on allocating the transaction price or accounting for contract acquisition costs for specific types of bundled arrangements. Rather, the general constraint guidance, as amended at the boards’ November 2012 meeting, would apply to all arrangements involving variable consideration.

Next Steps: The boards expect to issue final standards on revenue in early 2013.

Other Resources: For more information, see the project page on the FASB’s Web site. •XBRL

FASB Releases 2012 U.S. GAAP Financial Reporting XBRL Taxonomy

Affects: All entities.

Summary: On January 18, 2012, the FASB announced the publication of the 2012 U.S. GAAP Financial Reporting XBRL Taxonomy, which the SEC adopted by issuing a final rule on March 27, 2012. The taxonomy reflects accounting standards issued during the past year as well as other corrections and improvements to the 2011 taxonomy. The FASB has also published related release notes and other guidance and supporting documents, including a summary of changes from the 2011 taxonomy.

Other Resources: For more information, see the press release on the FASB’s Web site, the FASB guidance and supporting materials, and the SEC 2012 taxonomy release notes. •

IFRS Foundation Publishes 2012 IFRS Taxonomy

Affects: Entities reporting under IFRSs.

Summary: On March 30, 2012, the IFRS Foundation released the 2012 IFRS Taxonomy. The taxonomy is a translation of IFRSs into XBRL and is consistent with IFRSs as issued by the IASB as of January 1, 2012. The release contains XBRL tags for all IFRS disclosure requirements.

Other Resources: For more information, see the press release on the IASB’s Web site. •International

IASB Issues Statement on Future Work Plan*

Affects: Entities reporting under IFRSs.

Summary: On December 18, 2012, the IASB issued a feedback statement to discuss its future work plan related to its strategic priorities as well as potential improvements and efficiencies. The statement is being issued in response to hundreds of comment letters received from the public. Five broad themes were addressed in the statement.

Other Resources: For more information, see the project update on the IASB’s Web site. •

7

Accounting RoundupYear in Review — 2012

IASB Publishes Three EDs for Public Comment*

Affects: Entities reporting under IFRSs.

Summary: In December 2012, the IASB published the following three EDs:

• Acquisition of an Interest in a Joint Operation — proposed amendment to IFRS 11 (ED/2012/7).

• Sale or Contribution of Assets Between an Investor and Its Associate or Joint Venture — proposed amendments to IFRS 10 and IAS 28 (ED/2012/6).

• Clarification of Acceptable Methods of Depreciation and Amortisation — proposed amendments to IAS 16 and IAS 38 (ED/2012/5).

Next Steps: Comments on ED/2012/7 and ED/2012/6 are due by April 23, 2013. Comments on ED/2012/5 are due by April 2, 2013.

Other Resources: For more information, see the project updates news summary on the IASB’s Web site. •IASB Issues Guidance on Investment Entities

Affects: Entities reporting under IFRSs.

Summary: On October 31, 2012, the IASB published a final standard on investment entities, which amends IFRS 10, IFRS 12, and IAS 27 and introduces the concept of an investment entity in IFRSs. The amendments establish an exception to IFRS 10’s general consolidation principle for investment entities, requiring them to “measure particular subsidiaries at fair value through profit or loss, rather than consolidate them.“ In addition, the amendments outline required disclosures for reporting entities that meet the definition of an investment entity.

Next Steps: The amendments are effective for reporting periods beginning on or after January 1, 2014. Early adoption is permitted.

Other Resources: For more information, see the press release on the IASB’s Web site. •IASB Makes Editorial Corrections to IFRSs

Affects: Entities reporting under IFRSs.

Summary: On July 31, 2012, the IASB published editorial corrections (e.g., correction of spelling errors and grammatical mistakes) to the following pronouncements:

• IFRS 5, Non-current Assets Held for Sale and Discontinued Operations (issued March 2004).

• IFRS 7, Financial Instruments: Disclosures (issued August 2005).

• IFRS 10, Consolidated Financial Statements (issued May 2011).

• IFRS 11, Joint Arrangements (issued May 2011).

• IFRS 13, Fair Value Measurement (issued May 2011).

• IAS 19, Employee Benefits (issued June 2011).

• IAS 27, Separate Financial Statements (issued May 2011).

• Mandatory Effective Date of IFRS 9 and Transition Disclosures — amendments to IFRS 9 and IFRS 7 (issued December 2011).

• Annual Improvements 2009–2011 Cycle (issued May 2012).

Other Resources: For more information, see the press release on the IASB’s Web site. •

8

Accounting RoundupYear in Review — 2012

IASB Issues Amendments to Consolidation Guidance

Affects: Entities reporting under IFRSs.

Summary: On June 28, 2012, the IASB issued amendments to the transition guidance in IFRS 10, IFRS 11, and IFRS 12. The amendments would provide entities with transition relief from certain of the requirements in the three IFRSs (e.g., by “limiting the requirement to provide adjusted comparative information to only the preceding comparative period“).

Other Resources: For more information, see the press release on the IASB’s Web site. •IASB Publishes Four Q&As on IFRS for SMEs

Affects: SMEs reporting under IFRSs.

Summary: In April 2012, the IASB’s SMEIG issued four new Q&As:

• Recycling of Cumulative Exchange Differences on Disposal of a Subsidiary.

• Fallback to IFRS 9 Financial Instruments.

• Jurisdiction Requires Fallback to Full IFRSs.

• Application of ’Undue Cost or Effort.’

Other Resources: For more information, see the IFRS for SMEs update page on the IASB’s Web site. •IASB Finalizes Amendments to IFRSs as Part of Annual Improvements Project

Affects: Entities reporting under IFRSs.

Summary: In May 2012, the IASB finalized amendments to five IFRSs addressed during the project’s 2009–2011 cycle. The purpose of the annual improvements project is to make nonurgent changes, including clarifications and narrow-scope modifications, to multiple IFRSs in one convenient location rather than in separate documents.

Other Resources: For more information, see the press release on the IASB’s Web site. •IASB Issues Amendments to IFRS 1

Affects: Entities reporting under IFRSs.

Summary: On March 13, 2012, the IASB issued amendments to IFRS 1. The amendments exempt first-time IFRS adopters from full retrospective application of IFRSs when accounting, upon transition, for loans received from governments at a below-market rate of interest.

Next Steps: The amendments will be effective for annual periods beginning on or after January 1, 2013. Early adoption is permitted.

Other Resources: For more information, see the press release on the IASB’s Web site. •IFRS Foundation Publishes 2013 IFRS “Blue Book“*

Affects: Entities reporting under IFRSs.

Summary: In December 2012, the IFRS Foundation published its “blue book,“ 2013 International Financial Reporting Standards Consolidated Without Early Application, which contains all IFRS pronouncements that an entity must apply as of January 1, 2013.

Other Resources: For more information, see the description on Deloitte’s IASPlus Web site. •

9

Accounting RoundupYear in Review — 2012

Auditing Developments

AICPA

AICPA Issues SOP on Reporting Under Global Investment Performance Standards

Affects: Auditors of entities reporting under global investment performance standards.

Summary: In October, the ASB of the AICPA issued SOP 12-1, which supersedes the guidance in SOP 06-1 on examining and reporting on “aspects of an investment firm’s compliance with Global Investment Performance Standards.“ •

AICPA Issues Auditing Standard on Going Concern

Affects: Auditors that perform audits in accordance with U.S. GAAS.

Summary: In June 2012, the AICPA released SAS 126, which provides guidance on an auditor’s responsibility for evaluating “whether there is substantial doubt about the entity’s ability to continue as a going concern.“ SAS 126 applies to audits of all financial statements except those based on the assumption of liquidation, whether by dissolution, bankruptcy, or other processes.

Next Steps: SAS 126 is effective for audits of financial statements for periods ending on or after December 15, 2012. •AICPA Issues Practice Aid Related to Audits of Employee Benefit Plans

Affects: Auditors of employee benefit plans that use a service organization.

Summary: On March 26, 2012, the AICPA issued a practice aid that provides auditors with guidance on auditing the financial statements of an employee benefit plan that uses a service organization. •

ASB Issues Guidance to Help Auditors Apply Clarified Auditing Standards

Affects: Auditors that perform audits in accordance with U.S. GAAS.

Summary: In the third quarter of 2012, the AICPA published the following two practice aids to help auditors apply the ASB’s clarified auditing standards:

• Summary of Clarified Reporting Standards — Summarizes the content of and relationships between three clarified sections of U.S. auditing standards: AU-C Sections 700, 705, and 706.

• Clarified Auditing Standards — Learning and Implementation Plan — Provides an eight-step approach to help auditors understand the clarified standards, train their staff to effectively and efficiently implement them, and communicate with clients about the standards’ consequences.

Next Steps: The clarified auditing standards are effective for calendar-year 2012 audits.

Other Resources: For more information about the AICPA’s Clarity Project, see the AICPA’s Web site. •ASB Issues SAS 125 as Part of Clarity Project

Affects: Auditors that perform audits in accordance with U.S. GAAS.

Summary: In late December 2011, the ASB issued SAS 125 as part of its Clarity Project (i.e., the AICPA’s effort to improve understanding of and compliance with U.S. GAAS). SAS 125 “addresses the auditor’s responsibility, when required or the auditor decides, to include in the auditor’s report or other written communication issued by the auditor in connection with an engagement conducted in accordance with GAAS language that restricts the use of the auditor’s written communication.“

Next Steps: SAS 125 is effective for audits of financial statements for periods ending on or after December 15, 2012.

Other Resources: For more information, see the summary of SAS 125 on the AICPA’s Web site. •

10

Accounting RoundupYear in Review — 2012

CAQ

CAQ Releases Guide Summarizing PCAOB Inspection Process

Affects: Public entities and their auditors.

Summary: On November 6, 2012, the CAQ released a guide “that provides a high-level overview of the PCAOB’s process for inspecting public company auditing firms.“ The guide includes discussion of “selecting and reviewing audits for conformance to audit standards, and the assessment of a firm’s audit quality control program.“

Other Resources: For more information, see the press release on the CAQ’s Web site. •Auditor Evaluation Tool for Audit Committees Released

Affects: All entities.

Summary: On October 15, 2012, a group of leading governance organizations released an 11-page tool to help audit committees evaluate their external auditor as part of the annual reappointment process.

Other Resources: Deloitte’s October 19, 2012, Heads Up. Also see the press release on the CAQ’s Web site. •CAQ Issues Practice Aid on Communications With Audit Committees

Affects: All entities.

Summary: On October 10, 2012, the CAQ issued a practice aid that encourages auditors to “proactively communicate in a timely, forthright and robust manner“ with audit committees and outlines several items that auditors should consider when establishing their communication plan.

Other Resources: For more information, see the press release on the CAQ’s Web site. •SEC Staff Reminds Auditors of Foreign Private Issuers About Audit Report Requirements Under IFRSs

Affects: Foreign private issuers and their auditors.

Summary: On March 19, 2012, the CAQ issued an alert that discusses a recent SEC staff communication to the IPTF. In that communication, the SEC staff reminded auditors of FPIs filing under IFRSs that they are required, in accordance with Item 17(c) of Form 20-F, to “unreservedly and explicitly [state] an opinion on whether the financial statements comply with IFRS as issued by the IASB.“ •

IIA

IIA Issues Revisions to Internal Audit Standards

Affects: All entities.

Summary: On October 8, 2012, the IIA published revisions to its International Standards for the Professional Practice of Internal Auditing to “help internal audit focus on timely risks, stay aligned with exemplary practices, and maintain the appropriate stature.“ The revisions primarily focus on:

• “Clarifying the responsibilities of internal auditors, the chief audit executive (CAE), and the internal audit activity for conforming with the Standards.“

• “Increasing focus on the Quality Assurance and Improvement Program requirements and clarifying ways in which conformance may be achieved.“

• “Clarifying the CAE’s role in communicating unacceptable risk.“

• “Explicitly requiring timely adjustments to the internal audit plan.“

• “Ensuring the audit plan covers risks to achieving strategic objectives.“

• “Adding more examples of what constitutes ’functional reporting to the board.’“

• “Adding the definitions of ’overall opinion’ and ’engagement opinion’ to the Glossary, as well as changing the definition of ’board.’“

Other Resources: For more information, see the press release on the IIA’s Web site. •

11

Accounting RoundupYear in Review — 2012

PCAOB

SEC Approves PCAOB Auditing Standard 16*

Affects: Auditors.

Summary: On December 17, 2012, the SEC issued an order approving PCAOB Auditing Standard 16, which provides guidance on communications with audit committees.

Next Steps: Auditing Standard 16 applies to audits of fiscal years beginning on or after December 15, 2012. •PCAOB Releases Inspection Report on Audits of Internal Control Over Financial Reporting*

Affects: Auditors.

Summary: On December 10, 2012, the PCAOB released a report on the ICFR auditing deficiencies of eight accounting firms that the PCAOB inspected during 2010.

Other Resources: For more information, see the press release on the PCAOB’s Web site. •PCAOB Issues Audit Practice Alert on Professional Skepticism*

Affects: Auditors.

Summary: On December 4, 2012, the PCAOB issued a staff audit practice alert that reminds auditors about the importance of exercising professional skepticism during an audit.

Other Resources: For more information, see the press release on the PCAOB’s Web site. •International

IAASB Issues Standard on Review Engagements

Affects: Professional accountants.

Summary: On September 27, 2012, the IAASB issued ISRE 2400, which contains requirements for professional accountants who perform reviews of an entity’s financial statements. The objective of ISRE 2400 is “to enhance the quality and consistency of engagements to review historical financial statements.“

Next Steps: ISRE 2400 is effective for financial statement reviews for periods ending on or after December 31, 2013.

Other Resources: For more information, see the At a Glance summary document on IFAC’s Web site. •IAASB Issues New Standard on Assurance on Greenhouse Gas Statements

Affects: Practitioners that perform assurance procedures related to greenhouse gas statements.

Summary: On June 6, 2012, the IAASB issued ISAE 3410 to address “an increasingly relevant global assurance service in support of reliable emissions reporting, whether for regulatory compliance purposes or undertaken on a voluntary basis to inform investors, consumers, and others.“

Other Resources: For more information, see the press release on IFAC’s Web site. •IAASB Issues Revised Standard on Using the Work of Internal Auditors

Affects: Auditors that perform audits in accordance with ISAs.

Summary: On March 23, 2012, the IAASB issued ISA 610 (Revised), which addresses “the external auditor’s responsibilities if using the work of the internal audit function in obtaining audit evidence.“ Related changes have been made to ISA 315 (Revised), which “deals with the auditor’s responsibility to identify and assess the risks of material misstatement in the financial statements, through understanding the entity and its environment, including the entity’s internal control.“

Next Steps: ISA 610 (Revised) and ISA 315 (Revised) are effective for audits of financial statements for periods ending on or after December 15, 2013.

Other Resources: For more information, see the press release on IFAC’s Web site. •

12

Accounting RoundupYear in Review — 2012

IAASB Issues Revised Standard on Compilations

Affects: Compilation engagements.

Summary: On March 16, 2012, the IAASB issued ISRS 4410 (Revised), which “deals with the practitioner’s responsibilities when engaged to assist management with the preparation and presentation of historical financial information without obtaining any assurance on that information, and to report on the engagement in accordance with this ISRS.“ ISRS 4410 (Revised) also “expands the traditional compilation engagement report“ to clarify the auditor’s “contribution to the compiled financial information presented by management, and the key features of a compilation engagement.“

Next Steps: ISRS 4410 (Revised) is effective for compilation reports dated on or after July 1, 2013.

Other Resources: For more information, see the press release on IFAC’s Web site. •IAESB Releases Revised Standard on Assessment of Professional Competence

Affects: IFAC member bodies.

Summary: On November 16, 2012, the IAESB published a revised version of IES 6, which provides guidance on assessing, on the basis of certain principles and verifiable evidence, the competence of aspiring professional accountants.

Next Steps: IES 6 will become effective on July 1, 2015. •IAESB Issues Revised Standard on Continuing Professional Development

Affects: Professional accountants.

Summary: On July 23, 2012, the IAESB published a revised version of IES 7, which amends the continuing professional development requirements for professional accountants. The clarified standard represents the first of eight IESs that the IAESB plans to release over the next 18 months.

Next Steps: The revised standard will become effective on January 1, 2014.

Other Resources: For more information, see the press release on the IAESB’s Web site. •IESBA Releases Q&As on Implementing Code of Ethics

Affects: All entities and their auditors.

Summary: On November 7, 2012, the IESBA released new Q&As on adopting and implementing the IESBA’s Code of Ethics for Professional Accountants. Topics discussed in the new Q&As include materiality, partner rotation, public interest entities, and network firms.

Other Resources: For more information, see the press release on IFAC’s Web site. •IFAC Releases Revisions to Policy Position Paper 2

Affects: Auditors of SMEs.

Summary: On March 16, 2012, IFAC issued a revised version of Policy Position Paper 2. Originally issued in 2008, the paper “discusses the public interest considerations relevant to the application of ISAs for audits of [SMEs].“ The revisions include updated references to (1) clarified ISAs, (2) “other standards that the IAASB has issued and that are relevant to small and medium practitioners,“ and (3) “tools and guidance made available to practitioners by IFAC and the IAASB.“

Other Resources: For more information, see the press release on IFAC’s Web site. •IAASB Staff Issues Q&A Document on Professional Skepticism

Affects: Auditors.

Summary: On February 29, 2012, the IAASB issued a Q&A document on the importance of exercising professional skepticism in audits of financial statements.

Other Resources: For more information, see the press release on IFAC’s Web site. •

13

Accounting RoundupYear in Review — 2012

Governmental Accounting and Auditing Developments

FASAB

FASAB Issues Statement on Funds From Dedicated Collections

Affects: Federal government entities.

Summary: On June 1, 2012, the FASAB issued Statement 43, which amends the guidance in FASAB Statement 27. The amendments include:

• Changing the term “earmarked funds“ to “funds from dedicated collections.“

• Permitting entities to provide either consolidated or combined data on funds from dedicated collections.

• Allowing certain component entities to report on funds from dedicated collections for amounts related to the statement of changes in net position in a note rather than on the face of the statement.

Next Steps: Statement 43 is effective for periods beginning after September 30, 2012. Early application is not permitted.

Other Resources: For more information, see the press release on the FASAB’s Web site. •FASAB Issues Statement on Deferred Maintenance and Repairs

Affects: Federal government entities.

Summary: On April 25, 2012, the FASAB issued Statement 42, which amends the requirements in Statement 6 on deferred maintenance and repairs and makes certain conforming amendments to other standards. Specifically, Statement 42 would:

• Supersede Statement 6’s “definitions, measurement and reporting requirements for deferred maintenance and repairs.“

• Rescind Statement 14’s previous amendments to Statement 6.

• Amend Statement 32 to incorporate the revised definitions and eliminate certain other requirements.

Next Steps: Statement 42 is effective for periods beginning after September 30, 2014. Early application is encouraged.

Other Resources: For more information, see the press release on the FASAB’s Web site. •GASB

Six New Members Appointed to the Governmental Accounting Standards Advisory Council*

Affects: Governmental entities.

Summary: On December 4, 2012, six new members were appointed to the GASAC for two-year terms beginning on January 1, 2013. Further, 10 current members were also reappointed for two-year terms.

Other Resources: For more information, see the press release on the FAF’s Web site. •

14

Accounting RoundupYear in Review — 2012

GASB Posts New Pension Standards to Its Web Site

Affects: Governmental entities.

Summary: In August 2012, the GASB posted to its Web site two standards that it had approved for issuance in late June 2012:

• Statement 67 — Supersedes Statement 25 and provides revised financial reporting requirements for pension plan reporting entities.

• Statement 68 — Supersedes Statement 27 and provides revised financial reporting requirements for governments that provide pension benefits to their employees.

Next Steps: Statement 67 is effective for fiscal years beginning after June 15, 2013. Statement 68 is effective for fiscal years beginning after June 15, 2014. Earlier application of both Statement 67 and Statement 68 is encouraged. The related implementation guidance is expected to be issued in June 2013. •

GASB Issues Two Statements

Affects: Governmental entities.

Summary: On April 2, 2012, the GASB issued two Statements:

• Statement 65, which “clarifies the appropriate reporting of deferred outflows of resources and deferred inflows of resources to ensure consistency in financial reporting“ and is effective for periods beginning after December 15, 2012. Early adoption is encouraged.

• Statement 66, which resolves “conflicting accounting and financial reporting guidance that could diminish the consistency of financial reporting“ and is effective for periods beginning after December 15, 2012. Early adoption is encouraged.

Other Resources: For more information, see the press release on the GASB’s Web site. •GASB Expands and Revises User Guide on Local-Government Finances

Affects: Governmental entities.

Summary: On February 15, 2012, the GASB announced the release of the second edition of What You Should Know About Your Local Government’s Finances: A Guide to Financial Statements. This publication is intended for taxpayers, elected representatives, and others who may be using local-government financial statements.

Other Resources: For more information, see the press release on the GASB’s Web site. •OMB

OMB Issues 2012 Edition of OMB Circular A-133: Compliance Supplement

Affects: Governmental entities and their auditors.

Summary: The OMB has released the 2012 edition of OMB Circular A-133: Compliance Supplement, which contains guidance for auditors performing audits under the Single Audit Act and Circular A-133. The supplement provides information on the “objectives, procedures, and compliance requirements [of such audits] as well as audit objectives and suggested audit procedures for determining compliance with [those] requirements.“ •

International

IFAC Issues Paper on Public-Sector Financial Management Transparency and Accountability

Affects: Governmental entities.

Summary: On March 19, 2012, IFAC released Policy Position Paper 4, which discusses its view that governments need to provide “clear and comprehensive information regarding the financial consequences of economic, political, and social decisions.“

Other Resources: For more information, see the press release on IFAC’s Web site. •

15

Accounting RoundupYear in Review — 2012

Regulatory and Compliance Developments

SEC

Paul A. Beswick Appointed as SEC Chief Accountant*

Affects: SEC registrants.

Summary: On December 21, 2012, Paul A. Beswick was appointed chief accountant of the SEC after serving as acting chief accountant for the past several months. Mr. Beswick will replace James L. Kroeker, who left the Commission in July.

Other Resources: For more information, see the press release on the SEC’s Web site. •SEC and Justice Department Release FCPA Guide

Affects: Entities conducting business abroad.

Summary: On November 14, 2012, the SEC and the Department of Justice released a guide that contains a detailed analysis of the Foreign Corrupt Practices Act (FCPA) as well as a close examination of the approach that the two organizations employ for FCPA enforcement.

Other Resources: For more information, see the press release on the SEC’s Web site. •SEC Issues Final Rule on Risk Management and Operations of Clearing Agencies

Affects: SEC registrants.

Summary: On October 22, 2012, the SEC issued a final rule on the risk management and operations of clearing agencies. The rule requires clearing agencies to “establish, implement, maintain and enforce written policies and procedures reasonably designed to:

• Measure [their] credit exposures to [their] participants at least once a day.

• Use margin requirements to limit [their] credit exposures to participants using risk-based models and parameters, to be reviewed at least monthly.

• Maintain sufficient financial resources to withstand, at a minimum, a default by the participant family to which [they have] the largest exposure in extreme but plausible market conditions (and a default by the two participant families to which [they have] the largest exposures for security-based swap clearing agencies).

• Provide for an annual model validation by a qualified person who is free from influence from the persons responsible for the development or operation of the models being validated.“

Next Steps: The final rule will become effective on January 2, 2013.

Other Resources: For more information, see the press release on the SEC’s Web site. •SEC Updates EDGAR Filer Manual

Affects: SEC registrants.

Summary: On October 4, 2012, the SEC published a final rule that would amend its EDGAR Filer Manual to:

• “Support public dissemination of previously submitted draft registration statements either under the JOBS Act or the Division of Corporation Finance’s foreign private issuer policy.“

• “Support PDF as an official filing format for submission type 40-33 and 40-33/A.“

• “Support changes in the beneficiary account and receiver American Bank Association number and name for fee payments made for filings.“

• “Allow a future period date up to the next business date for Form 8-K.“

The final rule became effective on October 15, 2012. •

16

Accounting RoundupYear in Review — 2012

SEC Issues New FAQs on Title I of the JOBS Act

Affects: SEC registrants.

Summary: On September 28, 2012, the SEC issued 13 new Q&As related to the implementation of Title I of the JOBS Act. The new Q&As address the submission of draft financial statements and the definition of an EGC, among other items.

Other Resources: For more information, see the SEC’s Web site. •SEC Issues Risk Alert Related to Compliance With Municipal Securities Rules

Affects: SEC registrants.

Summary: On August 31, 2012, the SEC issued a risk alert that highlights the SEC’s concerns regarding compliance with the MSRB’s rules against “pay-to-play“ practices (i.e., campaign contributions made by municipal securities dealers to public officers of municipal securities issuers). The alert reminds firms of their obligations under the MSRB’s rules, discusses recent examination findings regarding compliance with these rules, and highlights practices that some firms are using in their compliance efforts.

Other Resources: For more information, see the press release on the SEC’s Web site. •SEC Issues Final Rule on Disclosing Payments Made by Issuers Engaged in Resource Extraction

Affects: SEC registrants engaged in resource extraction.

Summary: On August 22, 2012, the SEC issued a final rule implementing Section 1504 of the Dodd-Frank Wall Street Reform and Consumer Protection Act. Under Section 1504, issuers that are (1) required to file an annual report with the SEC and (2) engaged in commercial resource extraction of oil, natural gas, and minerals must disclose certain payments made to the federal government or foreign national or subnational governments. Domestic issuers (including smaller reporting companies), foreign issuers, their subsidiaries, and other entities controlled by such extractive issuers are subject to the final rule´s disclosure requirements. The final rule requires extractive issuers to annually file with the SEC a newly created Form SD that would include, as an electronically tagged (XBRL) exhibit, the required payment information.

Next Steps: Extractive issuers must file Form SD with the SEC no later than 150 days after their fiscal year-end and must comply with the final rule´s disclosure provisions for fiscal years ending after September 30, 2013. For an extractive issuer whose fiscal year began before September 30, 2013, disclosures in the first report will need to include only those payments made after September 30, 2013, to the end of the issuer´s fiscal year.

Other Resources: Deloitte’s September 27, 2012, Heads Up. •SEC Issues Final Rule on Conflict Minerals

Affects: SEC registrants.

Summary: On August 22, 2012, the SEC narrowly approved issuance of a long-awaited final rule implementing Section 1502 of the Dodd-Frank Act. Section 1502 requires issuers to annually disclose a description of the measures employed to “exercise due diligence on the source and chain of custody of such conflict minerals“ that originate from the Democratic Republic of Congo (DRC) and adjoining countries.

Under the final rule, all SEC registrants must assess whether they use conflict minerals and whether such conflict minerals are “necessary to the functionality or production“ of either (1) products they manufacture or (2) products that they have contracted to third parties for manufacture. If these conditions are met, registrants must conduct a reasonable country-of-origin inquiry to determine the source of the conflict minerals. The rule also requires registrants to perform, when applicable, reasonable due diligence to classify their conflict minerals as (1) DRC conflict free, (2) not been found to be DRC conflict free, or (3) DRC conflict undeterminable. Each classification has different reporting requirements. Registrants must file a newly created Form SD with the SEC on a calendar-year basis (regardless of their fiscal year-ends) beginning with the first calendar year ending December 31, 2013. Form SD is due on May 31, 2014 (and on May 31 each year thereafter).

Other Resources: Deloitte’s September 11, 2012, Heads Up. •

17

Accounting RoundupYear in Review — 2012

New Disclosure Requirement for Issuers Engaged in Sanctionable Activities With Iran and Syria*

Affects: SEC registrants.

Summary: On August 10, 2012, President Obama signed into law the Iran Threat Reduction and Syria Human Rights Act of 2012 (the “Act“). One of the Act’s provisions is to amend Section 13 of the Securities Exchange Act of 1934 to require issuers to disclose information about any instance in which they or their affiliates engaged in “sanctionable activities“ (i.e., activities prohibited by the Act) with Iran or Syria.

Issuers that have engaged in sanctionable activities must disclose the following information in their annual or quarterly filings with the SEC:

• The nature and extent of the activity.

• The gross revenues and profits, if any, that are attributable to the activity.

• Whether the issuer intends to continue the activity.

The new disclosure requirement is effective for quarterly and annual reports that an issuer is required to file with the SEC on or after February 6, 2013.

Further, on December 4, 2012, the SEC issued new C&DIs (e.g., Questions 147.01–.07) addressing various implementation issues associated with the new disclosure requirements. •

SEC Issues Small-Entity Compliance Guide on Listing Standards for Compensation Committees

Affects: SEC registrants.

Summary: On July 12, 2012, the SEC staff issued a small-entity compliance guide that provides interpretive guidance on implementing Section 10C of the Securities and Exchange Act of 1934. Specifically, the guide addresses (1) disclosure requirements related to compensation consultant conflicts of interest and (2) the requirement that securities exchanges establish minimum listing standards related to issuers’ compensation committees. The guide also covers which entities would be subject to the new requirements. •

SEC’s Observations Regarding Disclosures of Smaller Financial Institutions

Affects: SEC registrants.

Summary: On April 20, 2012, the SEC’s Division of Corporation Finance issued CF Disclosure Guidance: Topic No. 5, a summary of observations that the SEC staff has made regarding MD&A and accounting policy disclosures provided by smaller financial institutions. •

SEC Sends Sample Letter to Financial Institutions About Prospectus Supplements and Structured Note Offerings

Affects: SEC registrants.

Summary: On April 13, 2012, the Office of Capital Markets Trends in the SEC’s Division of Corporation Finance sent a sample letter to certain financial institutions highlighting ways in which issuers can improve their disclosures about structured note offerings. Although the letter primarily addresses prospectus supplements, it also discusses certain topics applicable to filings under the Securities Exchange Act of 1934. Topics addressed in the sample letter include disclosures related to:

• Product names, pricing, and value.

• Use of proceeds and reasons for offerings.

• Plan of distribution.

• Liquidity and credit risk.

• Tax consequences.

• Exhibit filing requirements. •

18

Accounting RoundupYear in Review — 2012

JOBS Act Signed Into Law to Ease Access to Investment Capital

Affects: SEC registrants.

Summary: On April 5, 2012, President Obama signed into law the JOBS Act. The primary objective of the JOBS Act is to “increase American job creation and economic growth by improving access to the public capital markets for emerging growth companies.“ The JOBS Act addresses “crowdfunding“ transactions and shareholder limits and, specifically for EGCs, would change such items as financial statement and selected financial data requirements, attestation requirements for ICFR, and the period in which new and revised accounting standards are adopted.

Title I of the JOBS Act changes the Securities Act of 1933 to allow an EGC to provide a confidential-draft initial public offering registration statement to the SEC staff for review before its public filing (i.e., the SEC is prohibited from disclosing the information being reviewed).

As a result, the SEC staff announced on May 11, 2012, that it has implemented a secure e-mail system that allows EGCs and eligible FPIs to submit a draft registration statement to the SEC staff. The staff can then provide these entities with confidential review comments. This announcement replaces the staff’s April 5, 2012, announcement. Detailed instructions for the submission process are available on the SEC’s Web site.

Further, on May 3, 2012, the SEC staff posted to its Web site additional FAQs about the JOBS Act. Many of the FAQs address implementation of the JOBS Act’s provisions by EGCs. Topics discussed include the following:

• Determining whether an issuer qualifies for EGC status.

• Understanding how certain provisions of the JOBS Act interact with existing SEC rules and regulations related to smaller reporting companies, issuers of asset-backed securities, and FPIs.

• Applying certain of the financial reporting and disclosure accommodations available to EGCs (e.g., deferral of the adoption of new and revised accounting standards).

Other Resources: Deloitte’s April 2, 2012 (updated May 8, 2012), Heads Up. •SEC Issues Guidance on Disclosures About European Sovereign Debt Exposures

Affects: SEC registrants.

Summary: On January 6, 2012, the staff of the SEC’s Division of Corporation Finance issued CF Disclosure Guidance Topic 4, which indicates that registrants need to improve disclosures about their holdings of eurozone sovereign debt. This guidance is being issued in response to the continued uncertainties associated with such debt and the staff’s observation that registrants have sometimes provided inconsistent disclosures regarding the nature and extent of their debt exposures.

Other Resources: Deloitte’s January 9, 2012, Financial Reporting Alert. •SEC Issues Final Rule on Mine Safety Disclosure Requirements

Affects: SEC registrants.

Summary: On December 21, 2011, the SEC issued a final rule on mine safety disclosures that completes the Commission’s required rulemaking under Section 1503 of the Dodd-Frank Act. The final rule is based on the safety and health requirements under the Federal Mine Safety and Health Act of 1977 and requires registrants (including FPIs) to periodically disclose mine safety violations and related information, regardless of materiality. Under the new rule, registrants “that are operators, or that have a subsidiary that is an operator, of a coal or other mine located in the U.S.“ would be required to disclose, in their periodic reports to the SEC, “health and safety violations, orders and citations, related assessments and legal actions, and mining-related fatalities.“

The final rule became effective on January 27, 2012.

Other Resources: For more information, see the press release on the SEC’s Web site. •

19

Accounting RoundupYear in Review — 2012

COSO

COSO Issues White Paper on Risk Assessment

Affects: All entities.

Summary: On October 26, 2012, COSO issued a white paper that outlines best practices for an entity’s risk assessment procedures. The white paper “represents another in a series of papers published by COSO aimed at helping organizations move up the maturity curve in their ongoing development of a robust ERM program.“

Other Resources: For more information, see the press release on COSO’s Web site. •International

IFAC Issues Policy Position Paper on Effective Governance, Risk Management, and Internal Control*

Affects: All entities.

Summary: On December 13, 2012, IFAC issued Policy Position Paper 7, which discusses effective governance, risk management, and internal control. IFAC states that it “believes that establishing an integrated and effective system of governance, risk management, and internal control is desirable for all types of organizations and can make an invaluable contribution to achieving sustained organizational success.“

Other Resources: For more information, see the At a Glance summary document on IFAC’s Web site. •Basel Committee Issues Revised Securitization Framework for Public Comment*

Affects: Banking entities.

Summary: On December 18, 2012, the Basel Committee published proposed revisions to its securitization framework for public comment.

Next Steps: Comments on the proposed revisions are due by March 15, 2013.

Other Resources: For more information, see the press release on the BIS’s Web site. •Basel Committee Issues New Regulatory Capital Disclosure Requirements

Affects: Banking entities.

Summary: The Basel Committee on Banking Supervision has released a final rule that establishes new regulatory capital disclosure requirements for banking entities. The objective of the new disclosure requirements is to “improve consistency and ease of use of disclosures relating to the composition of regulatory capital, and to mitigate the risk of inconsistent formats undermining the objective of enhanced disclosure.“ To achieve this objective, the final rule requires banking entities to use a common template to report their capital positions.

Next Steps: National authorities are expected to incorporate the rule’s disclosure requirements by no later than June 30, 2013. Subject to such incorporation, banks would be required to comply with most of the disclosure requirements from the date of publication of their first set of financial statements on or after June 30, 2013.

Other Resources: For more information, see the press release on the BIS’s Web site. •IOSCO and CPSS Issue Disclosure Framework and Assessment Methodology for Financial Market Infrastructures* Affects: Financial market infrastructures (FMIs).

Summary: On December 14, 2012, IOSCO and the CPSS issued a set of principles that promotes the provision of more objective, comparable, and transparent information by FMIs.

Other Resources: For more information, see the press release on the BIS’s Web site. •

20

Accounting RoundupYear in Review — 2012

IOSCO Publishes Principles for Ongoing Disclosures About Asset-Backed Securities

Affects: Securities regulators.

Summary: On November 27, 2012, IOSCO published a final report that contains guidance on ongoing disclosures that securities regulators may require about offerings and listings of asset-backed securities.

Other Resources: For more information, see the press release on IOSCO’s Web site. •

21

Accounting RoundupYear in Review — 2012

Appendix A: Significant Adoption Dates and Deadlines

The chart below indicates significant adoption dates and deadline dates for the FASB, EITF, AICPA, SEC, PCAOB, GASB, FASAB, and international standards. Content recently added or revised is highlighted in green.

FASB/EITF Affects Status

Significant Adoption Dates

ASU 2012-07, Accounting for Fair Value Information That Arises After the Measurement Date and Its Inclusion in the Impairment Analysis of Unamortized Film Costs — a consensus of the FASB Emerging Issues Task Force (issued October 24, 2012)

Entities that perform impairment assessments of unamortized film costs.

For SEC filers, effective for impairment assessments performed on or after December 15, 2012. For all other entities, effective for impairment assessments performed on or after December 15, 2013. The amendments resulting from this Issue should be applied prospectively.Early application is permitted, including for impairment assessments performed as of a date before October 24, 2012, if, for SEC filers, the entity’s financial statements for the most recent annual or interim period have not yet been issued or, for all other entities, have not yet been made available for issuance.

ASU 2012-06, Subsequent Accounting for an Indemnification Asset Recognized at the Acquisition Date as a Result of a Government-Assisted Acquisition of a Financial Institution — a consensus of the FASB Emerging Issues Task Force (issued October 23, 2012)

Entities that recognize an indemnification asset as a result of a government-assisted acquisition of a financial institution.

Effective for fiscal years, and interim periods within those years, beginning on or after December 15, 2012. Early adoption is permitted.Entities should apply the ASU prospectively to any new indemnification assets acquired after the adoption date and to indemnification assets existing as of the adoption date that arise from a government-assisted acquisition of a financial institution.

ASU 2012-05, Not-for-Profit Entities: Classification of the Sale Proceeds of Donated Financial Assets in the Statement of Cash Flows — a consensus of the FASB Emerging Issues Task Force (issued October 22, 2012)

Entities within the scope of ASC 958 that accept donated financial assets.

Effective prospectively for fiscal years, and interim periods within those years, beginning after June 15, 2013. Retrospective application to all prior periods presented upon the date of adoption is permitted. Early adoption from the beginning of the fiscal year of adoption is permitted. For fiscal years beginning before October 22, 2012, early adoption is permitted only if a not-for-profit entity’s financial statements for those fiscal years and interim periods within those years have not yet been made available for issuance.

ASU 2012-04, Technical Corrections and Improvements (issued October 1, 2012)

All entities. Effective upon issuance, except for amendments that are subject to transition guidance, which will be effective for fiscal periods beginning after December 15, 2012, for public entities and fiscal periods beginning after December 15, 2013, for nonpublic entities.

ASU 2012-03, Technical Amendments and Corrections to SEC Sections (issued August 27, 2012)

All entities. Effective upon issuance.

ASU 2012-02, Testing Indefinite-Lived Intangible Assets for Impairment (issued July 27, 2012)

Entities, both public and nonpublic, that have indefinite-lived intangible assets, other than goodwill, reported in their financial statements.

Effective for annual and interim impairment tests performed for fiscal years beginning after September 15, 2012. Early adoption is permitted, including for annual and interim impairment tests performed as of a date before July 27, 2012, if a public entity's financial statements for the most recent annual or interim period have not yet been issued or, for nonpublic entities, have not yet been made available for issuance.

22

Accounting RoundupYear in Review — 2012

ASU 2012-01, Continuing Care Retirement Communities — Refundable Advance Fees (issued July 24, 2012)

Continuing care retirement communities that have resident contracts that provide for a payment of a refundable advance fee upon reoccupancy of that unit by a subsequent resident.

Public entities — Effective for fiscal periods beginning after December 15, 2012.Nonpublic entities — Effective for fiscal periods beginning after December 15, 2013. For both public and nonpublic entities, early adoption is permitted. The amendments should be applied retrospectively by recording a cumulative-effect adjustment to opening retained earnings (or unrestricted net assets) as of the beginning of the earliest period presented.

ASU 2011-12, Deferral of the Effective Date for Amendments to the Presentation of Reclassifications of Items Out of Accumulated Other Comprehensive Income in Accounting Standards Update No. 2011-05 (issued December 23, 2011)

Entities that report items of other comprehensive income.

Public entities — Effective for fiscal years, and interim periods within those years, beginning after December 15, 2011.Nonpublic entities — Effective for fiscal years ending after December 15, 2012, and interim and annual periods thereafter.For both public and nonpublic entities, early adoption is permitted and transition disclosures are not required. In addition, the ASU must be applied retrospectively to all periods presented.

ASU 2011-11, Disclosures About Offsetting Assets and Liabilities (issued December 16, 2011)

Entities that have financial instruments and derivative instruments that are either (1) offset in accordance with either ASC 210-20-45 or ASC 815-10-45 or (2) subject to an enforceable master netting arrangement or similar agreement.

An entity is required to apply the amendments for annual reporting periods beginning on or after January 1, 2013, and interim periods within those annual periods. An entity should provide the disclosures required by those amendments retrospectively for all comparative periods presented.

ASU 2011-10, Derecognition of in Substance Real Estate — a Scope Clarification — a consensus of the FASB Emerging Issues Task Force (issued December 14, 2011)

Entities that cease to have a controlling financial interest (as described in ASC 810-10) in a subsidiary that is in-substance real estate as a result of default on the subsidiary’s nonrecourse debt.

Public entities — Effective for fiscal years, and interim periods within those years, beginning on or after June 15, 2012. Nonpublic entities — Effective for fiscal years ending after December 15, 2013, and interim and annual periods thereafter. Early adoption is permitted.

ASU 2011-09, Disclosures About an Employer's Participation in a Multiemployer Plan (issued September 21, 2011)

Nongovernmental reporting entities that participate in multiemployer plans. While the majority of the amendments in this ASU apply only to multiemployer pension plans, there also are amendments that require changes in disclosures for multiemployer plans that provide postretirement benefits other than pensions as defined in the Master Glossary of the FASB Accounting Standards Codification.

Public entities — Effective for annual periods for fiscal years ending after December 15, 2011, with early adoption permitted. Nonpublic entities — Effective for annual periods for fiscal years ending after December 15, 2012, with early adoption permitted. The amendments should be applied retrospectively for all prior periods presented.

ASU 2011-08, Testing Goodwill for Impairment (issued September 15, 2011)

Entities, both public and nonpublic, that have goodwill reported in their financial statements.

Effective for annual and interim goodwill impairment tests performed for fiscal years beginning after December 15, 2011. Early adoption is permitted, including for annual and interim goodwill impairment tests performed as of a date before September 15, 2011, if an entity’s financial statements for the most recent annual or interim period have not yet been issued or, for nonpublic entities, have not yet been made available for issuance.

ASU 2011-07, Presentation and Disclosure of Patient Service Revenue, Provision for Bad Debts, and the Allowance for Doubtful Accounts for Certain Health Care Entities — a consensus of the FASB Emerging Issues Task Force (issued July 25, 2011)

Health care organizations. Public entities — Effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2011, with early adoption permitted. Nonpublic entities — Effective for the first annual period ending after December 15, 2012, and interim and annual periods thereafter, with early adoption permitted. The amendments to the presentation of the provision for bad debts related to patient service revenue in the statement of operations should be applied retrospectively to all prior periods presented. The disclosures required by this ASU should be provided for the period of adoption and subsequent reporting periods.

23

Accounting RoundupYear in Review — 2012

ASU 2011-06, Fees Paid to the Federal Government by Health Insurers — a consensus of the FASB Emerging Issues Task Force (issued July 21, 2011)

Reporting entities that are subject to the fee imposed on health insurers mandated by the Patient Protection and Affordable Care Act, as amended by the Health Care and Education Reconciliation Act.

Effective for calendar years beginning after December 31, 2013, when the fee initially becomes effective.

ASU 2011-05, Presentation of Comprehensive Income (issued June 16, 2011)

Entities that report items of other comprehensive income.