Embed Size (px)

Citation preview

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 1/50

Chapter3-1

CHAPTER 3

The Adjusting

Process

Accounting Principles, Eighth Edition

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 2/50

Chapter3-2

1. Explain the time period assumption.

2. Explain the accrual basis of accounting.

3. Explain the reasons for adjusting entries.

4. Identify the major types of adjusting entries.5. Prepare adjusting entries for deferrals.

6. Prepare adjusting entries for accruals.

7. Describe the nature and purpose of an adjustedtrial balance.

Study Objectives

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 3/50

Chapter3-3

Current Liabilities and Contingencies

Timing Issues

The Basics of

Adjusting

Entries

The Adjusted

Trial Balance and

Financial

Statements

Time period

assumption

Fiscal and

calendar years

Accrual- vs. cash-

basis accounting

Recognizing

revenues and

expenses

Types of adjusting

entries

Adjusting entries

for deferrals

Adjusting entries

for accruals

Summary of

journalizing and

posting

Preparing the

adjusted trial

balance

Preparing

financialstatements

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 4/50

Chapter3-4

Generally a month, a quarter, or a year.Fiscal year vs. calendar year

Also known as the ―Periodicity Assumption‖

Timing Issues

Accountants divide the economic life of abusiness into artificial time periods(Time Period Assumption).

LO 1 Explain the time period assumption.

Jan. Feb. Mar. Apr. Dec.. . . . .

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 5/50

Chapter3-5

The time period assumption states that:

a. revenue should be recognized in the accountingperiod in which it is earned.

b. expenses should be matched with revenues.

c. the economic life of a business can be dividedinto artificial time periods.

d. the fiscal year should correspond with thecalendar year.

Review

Timing Issues

LO 1 Explain the time period assumption.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 6/50

Chapter3-6

Accrual-Basis Accounting

Transactions recorded in the periods in which

the events occur

Revenues are recognized when earned, ratherthan when cash is received.

Expenses are recognized when incurred, ratherthan when paid.

Timing Issues

Accrual- vs. Cash-Basis Accounting

LO 2 Explain the accrual basis of accounting.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 7/50

Chapter3-7

Cash-Basis Accounting

Revenues are recognized when cash is received.

Expenses are recognized when cash is paid.

Cash-basis accounting is not in accordance withgenerally accepted accounting principles (GAAP).

Timing Issues

Accrual- vs. Cash-Basis Accounting

LO 2 Explain the accrual basis of accounting.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 8/50

Chapter3-8

Revenue Recognition Principle

Timing Issues

Recognizing Revenues and Expenses

LO 2 Explain the accrual basis of accounting.

Companies recognize

revenue in the accountingperiod in which it isearned.

In a service enterprise,revenue is considered tobe earned at the time theservice is performed.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 9/50

Chapter3-9

Matching Principle

Timing Issues

Recognizing Revenues and Expenses

LO 2 Explain the accrual basis of accounting.

Match expenses with

revenues in the periodwhen the company makesefforts to generatethose revenues.

“Let the expenses follow

the revenues.”

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 10/50

Chapter3-10

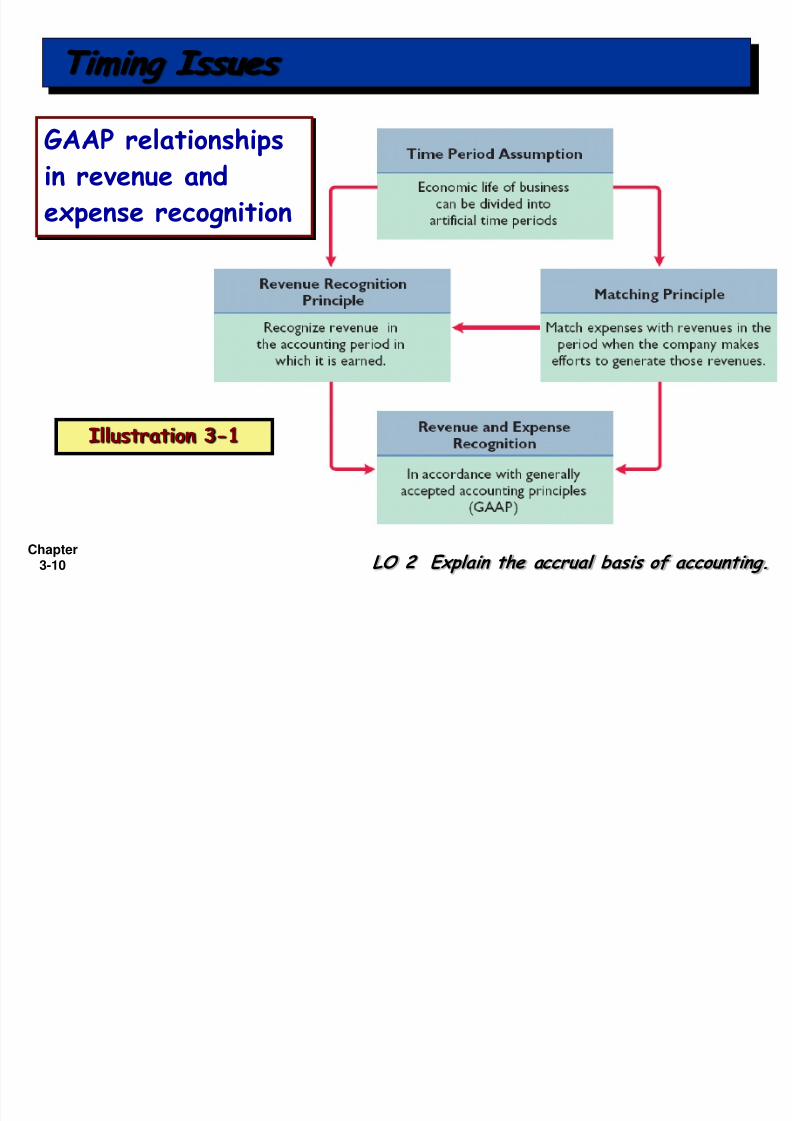

Timing Issues

LO 2 Explain the accrual basis of accounting.

GAAP relationshipsin revenue andexpense recognition

Illustration 3-1

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 11/50

Chapter3-11

One of the following statements about the accrual basisof accounting is false . That statement is:

a. Events that change a company’s financial

statements are recorded in the periods in whichthe events occur.

b. Revenue is recognized in the period in which it isearned.

c. This basis is in accord with generally acceptedaccounting principles.

d. Revenue is recorded only when cash is received, andexpense is recorded only when cash is paid.

Review

Timing Issues

LO 2 Explain the accrual basis of accounting.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 12/50

Chapter3-12

Adjusting entries make it possible to reportcorrect amounts on the balance sheet and onthe income statement.

A company must make adjusting entriesevery time it prepares financial statements.

The Basics of Adjusting Entries

LO 3 Explain the reasons for adjusting entries.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 13/50

Chapter3-13

Revenues - recorded in the period in whichthey are earned.

Expenses - recognized in the period in which

they are incurred.

Adjusting entries - needed to ensure that therevenue recognition and matching principles

are followed.

The Basics of Adjusting Entries

LO 3 Explain the reasons for adjusting entries.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 14/50

Chapter3-14

Adjusting entries are made to ensure that:

a. expenses are recognized in the period in which

they are incurred.b. revenues are recorded in the period in which

they are earned.

c. balance sheet and income statement accounts

have correct balances at the end of anaccounting period.

d. all of the above.

Review

Timing Issues

LO 3 Explain the reasons for adjusting entries.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 15/50

Chapter3-15

Types of Adjusting Entries

1. Prepaid Expenses. Expenses paid in cash andrecorded as assets beforethey are used or consumed.

Deferrals

3. Accrued Revenues. Revenues earned but not

yet received in cash orrecorded.

4. Accrued Expenses. Expenses incurred but not

yet paid in cash orrecorded.

2. Unearned Revenues. Revenues received in cash

and recorded as liabilitiesbefore they are earned.

Accruals

LO 4 Identify the major types of adjusting entries.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 16/50

Chapter3-16

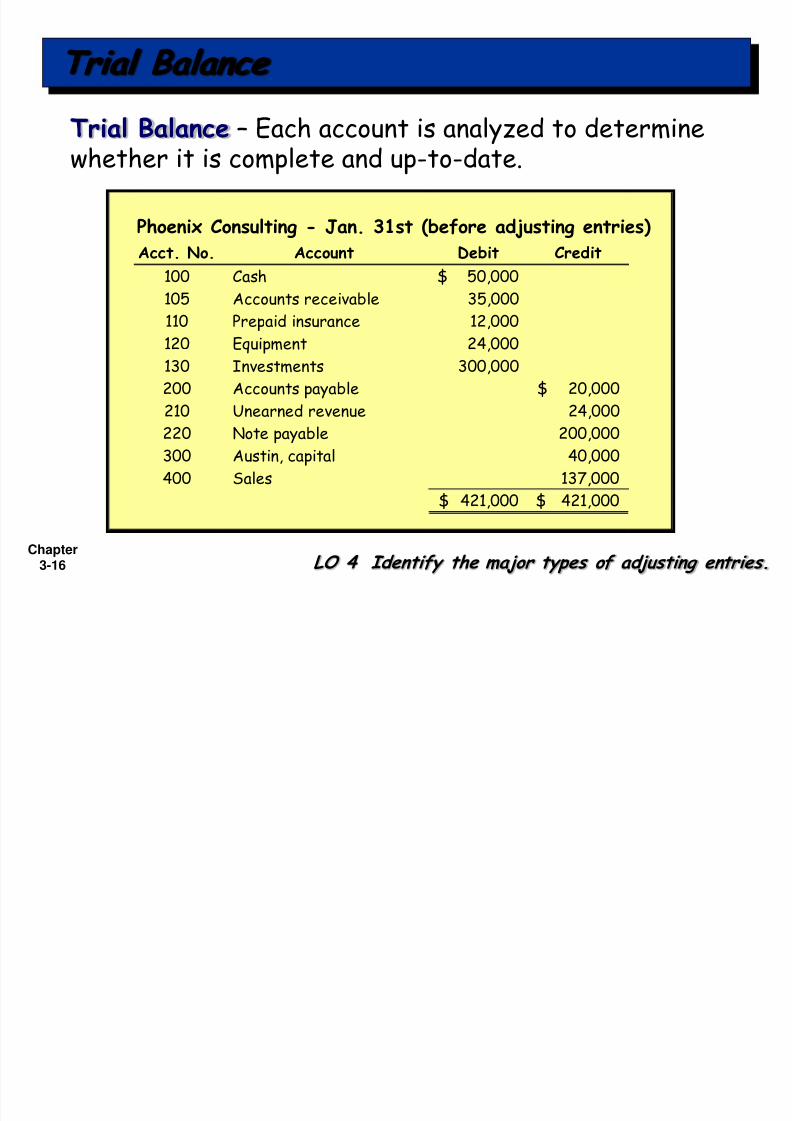

Trial Balance – Each account is analyzed to determinewhether it is complete and up-to-date.

Phoenix Consulting - Jan. 31st (before adjusting entries)

Acct. No. Account Debit Credit

100 Cash 50,000$105 Accounts receivable 35,000

110 Prepaid insurance 12,000

120 Equipment 24,000

130 Investments 300,000

200 Accounts payable 20,000$

210 Unearned revenue 24,000 220 Note payable 200,000

300 Austin, capital 40,000

400 Sales 137,000

421,000$ 421,000$

Trial Balance

LO 4 Identify the major types of adjusting entries.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 17/50

Chapter3-17

Deferrals are either:

Prepaid expenses or

Unearned revenues.

Adjusting Entries for Deferrals

LO 5 Prepare adjusting entries for deferrals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 18/50

Chapter3-18

Payment of cash, that is recorded as an asset becauseservice or benefit will be received in the future.

Adjusting Entries for “Prepaid Expenses”

insurance

suppliesadvertising

Cash Payment Expense RecordedBEFORE

LO 5 Prepare adjusting entries for deferrals.

rent

maintenance on equipmentfixed assets (depreciation)

Prepayments often occur in regard to:

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 19/50

Chapter3-19

Prepaid ExpensesCosts that expire either with the passage of timeor through use.

Adjusting entries (1) to record the expenses thatapply to the current accounting period, and (2) toshow the unexpired costs in the asset accounts.

Adjusting Entries for “Prepaid Expenses”

LO 5 Prepare adjusting entries for deferrals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 20/50

Chapter3-20

Adjusting Entries for “Prepaid Expenses”

LO 5 Prepare adjusting entries for deferrals.

Illustration 3-4Adjusting entries for prepaid expenses

Increases (debits) an expense account and

Decreases (credits) an asset account.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 21/50

Chapter3-21

Example (Insurance): On Jan. 1st

, Phoenix Consulting paid$12,000 for 12 months of insurance coverage. Show the journal entry to record the payment on Jan. 1st.

Cash 12,000

Prepaid insurance 12,000Jan. 1

Debit Credit

Prepaid Insurance

12,000 12,000

Debit Credit

Cash

Adjusting Entries for “Prepaid Expenses”

LO 5 Prepare adjusting entries for deferrals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 22/50

Chapter3-22

Example (Insurance): On Jan. 1st

, Phoenix Consulting paid$12,000 for 12 months of insurance coverage. Show theadjusting journal entry required at Jan. 31st.

Prepaid insurance 1,000

Insurance expense 1,000Jan. 31

Debit Credit

Prepaid Insurance

12,000 1,000

Debit Credit

Insurance expense

1,000

11,000

Adjusting Entries for “Prepaid Expenses”

LO 5 Prepare adjusting entries for deferrals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 23/50

Chapter3-23

Depreciation Buildings, equipment, and vehicles (long-livedassets) are recorded as assets, rather than anexpense, in the year acquired.

Companies report a portion of the cost of a long-lived asset as an expense (depreciation) duringeach period of the asset’s useful life (Matching

Principle).

Adjusting Entries for “Prepaid Expenses”

LO 5 Prepare adjusting entries for deferrals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 24/50

Chapter3-24

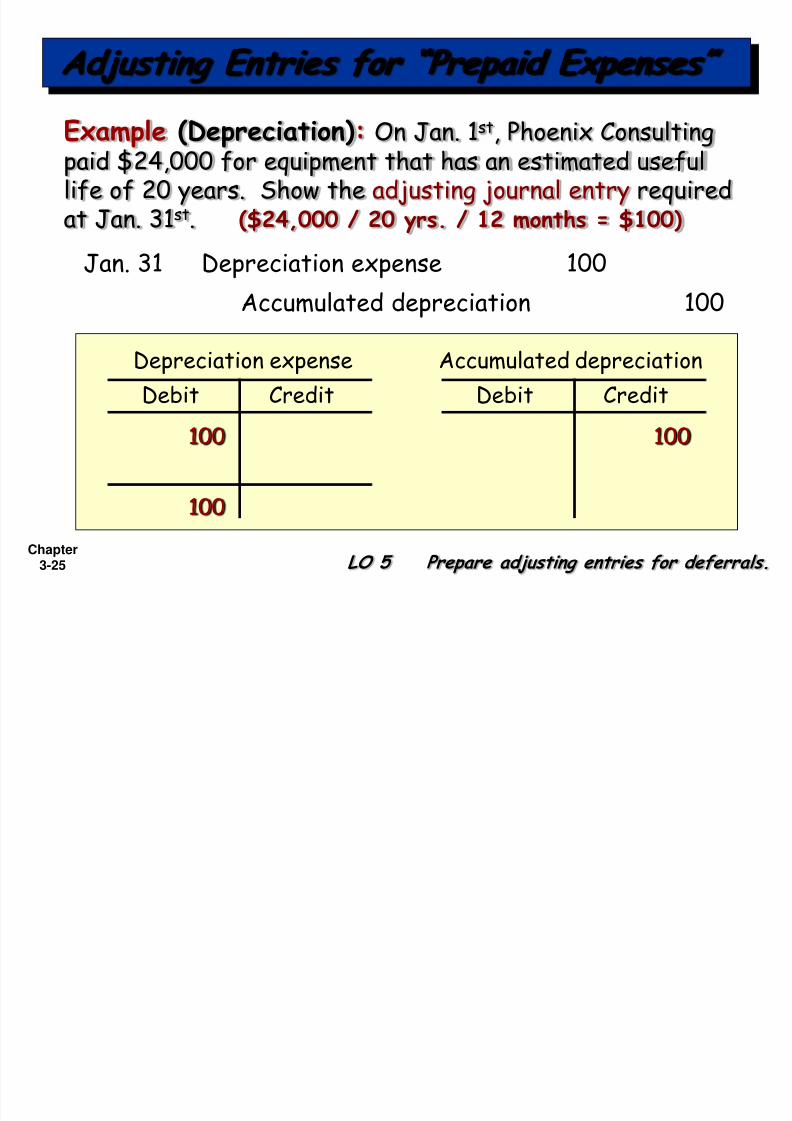

Example (Depreciation): On Jan. 1st

, Phoenix Consultingpaid $24,000 for equipment that has an estimated usefullife of 20 years. Show the journal entry to record thepurchase of the equipment on Jan. 1st.

Cash 24,000

Equipment 24,000Jan. 1

Debit Credit

Equipment

24,000 24,000

Debit Credit

Cash

Adjusting Entries for “Prepaid Expenses”

LO 5 Prepare adjusting entries for deferrals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 25/50

Chapter3-25

Example (Depreciation): On Jan. 1st

, Phoenix Consultingpaid $24,000 for equipment that has an estimated usefullife of 20 years. Show the adjusting journal entry requiredat Jan. 31st. ($24,000 / 20 yrs. / 12 months = $100)

Accumulated depreciation 100

Depreciation expense 100Jan. 31

Debit Credit

Depreciation expense

100 100

Debit Credit

Accumulated depreciation

100

Adjusting Entries for “Prepaid Expenses”

LO 5 Prepare adjusting entries for deferrals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 26/50

Chapter3-26

Depreciation (Statement Presentation) Accumulated Depreciation—is a contra assetaccount.

Appears just after the account it offsets(Equipment) on the balance sheet.

Adjusting Entries for “Prepaid Expenses”

LO 5 Prepare adjusting entries for deferrals.

Balance Sheet Jan. 31

AssetsEquipment 24,000

Accumulated Depreciation (100)

Net Equipment 23,900

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 27/50

Chapter3-27

Receipt of cash that is recorded as a liability becausethe revenue has not been earned.

Adjusting Entries for “Unearned Revenues”

rent

airline ticketsschool tuition

Cash Receipt Revenue RecordedBEFORE

magazine subscriptions

customer deposits

Unearned revenues often occur in regard to:

LO 5 Prepare adjusting entries for deferrals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 28/50

Chapter3-28

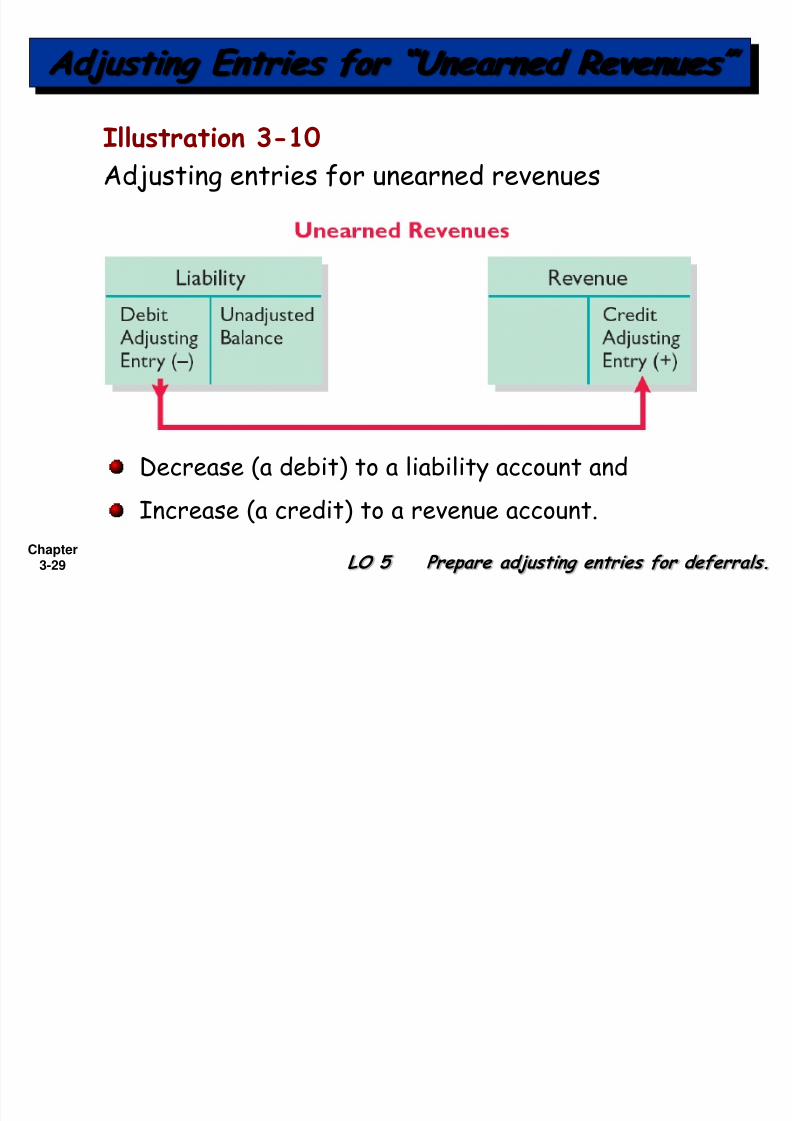

Unearned Revenues Company makes an adjusting entry to record therevenue that has been earned and to show the

liability that remains.The adjusting entry for unearned revenues resultsin a decrease (a debit) to a liability account and anincrease (a credit) to a revenue account.

LO 5 Prepare adjusting entries for deferrals.

Adjusting Entries for “Unearned Revenues”

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 29/50

Chapter3-29 LO 5 Prepare adjusting entries for deferrals.

Illustration 3-10Adjusting entries for unearned revenues

Decrease (a debit) to a liability account and

Increase (a credit) to a revenue account.

Adjusting Entries for “Unearned Revenues”

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 30/50

Chapter3-30

Example: On Jan. 1st

, Phoenix Consulting received $24,000from Arcadia High School for 3 months rent in advance.Show the journal entry to record the receipt on Jan. 1st.

Unearned rent revenue 24,000

Cash 24,000Jan. 1

Debit Credit

Cash

24,000 24,000

Debit Credit

Unearned Rent Revenue

Adjusting Entries for “Unearned Revenues”

LO 5 Prepare adjusting entries for deferrals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 31/50

Chapter3-31

Example: On Jan. 1st

, Phoenix Consulting received $24,000from Arcadia High School for 3 months rent in advance.Show the adjusting journal entry required on Jan. 31st.

Rent revenue 8,000

Unearned rent revenue 8,000Jan. 31

Debit Credit

Rent Revenue

8,000 24,000

Debit Credit

Unearned Rent Revenue

8,000

16,000

Adjusting Entries for “Unearned Revenues”

LO 5 Prepare adjusting entries for deferrals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 32/50

Chapter3-32

Made to record:

Revenues earned and

Expenses incurredin the current accounting period that have notbeen recognized through daily entries.

Adjusting Entries for Accruals

LO 6 Prepare adjusting entries for accruals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 33/50

Chapter3-33

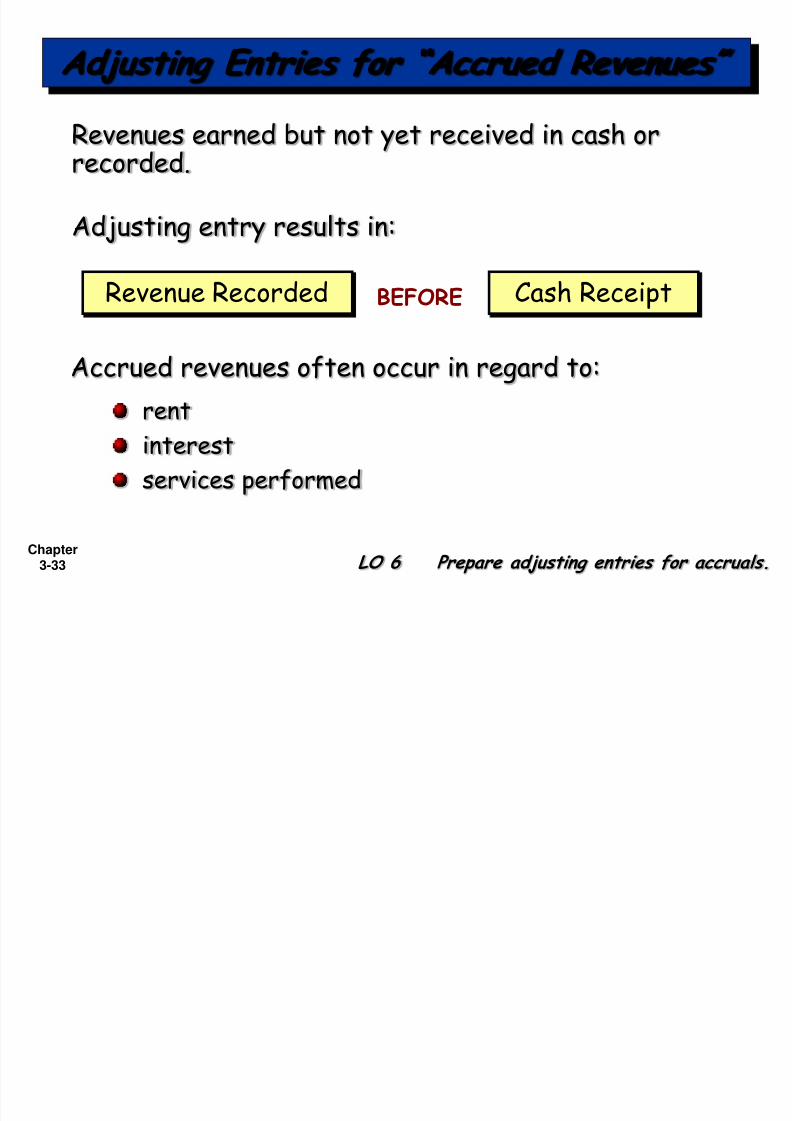

Revenues earned but not yet received in cash orrecorded.

Adjusting Entries for “Accrued Revenues”

rentinterest

services performed

BEFORE

Accrued revenues often occur in regard to:

Cash ReceiptRevenue Recorded

Adjusting entry results in:

LO 6 Prepare adjusting entries for accruals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 34/50

Chapter3-34

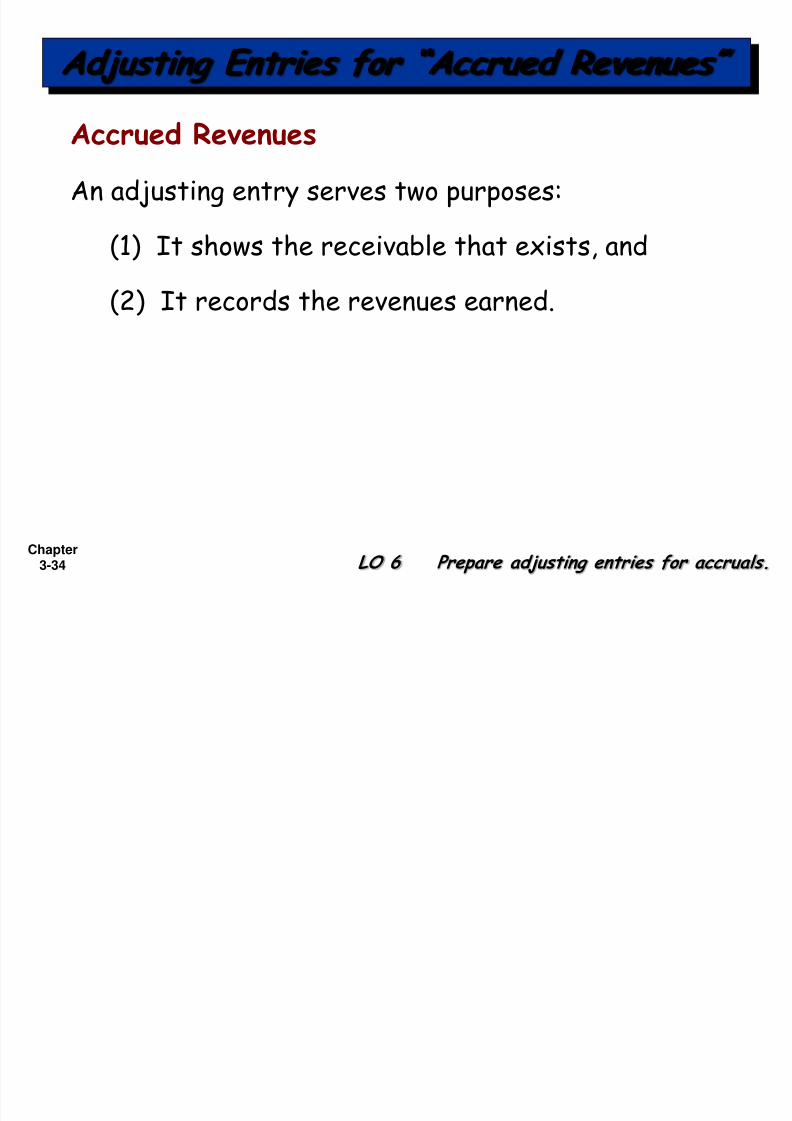

Accrued Revenues An adjusting entry serves two purposes:

(1) It shows the receivable that exists, and

(2) It records the revenues earned.

Adjusting Entries for “Accrued Revenues”

LO 6 Prepare adjusting entries for accruals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 35/50

Chapter3-35

Illustration 3-13Adjusting entries for accrued revenues

Increases (debits) an asset account and

Increases (credits) a revenue account.

LO 6 Prepare adjusting entries for accruals.

Adjusting Entries for “Accrued Revenues”

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 36/50

Chapter3-36

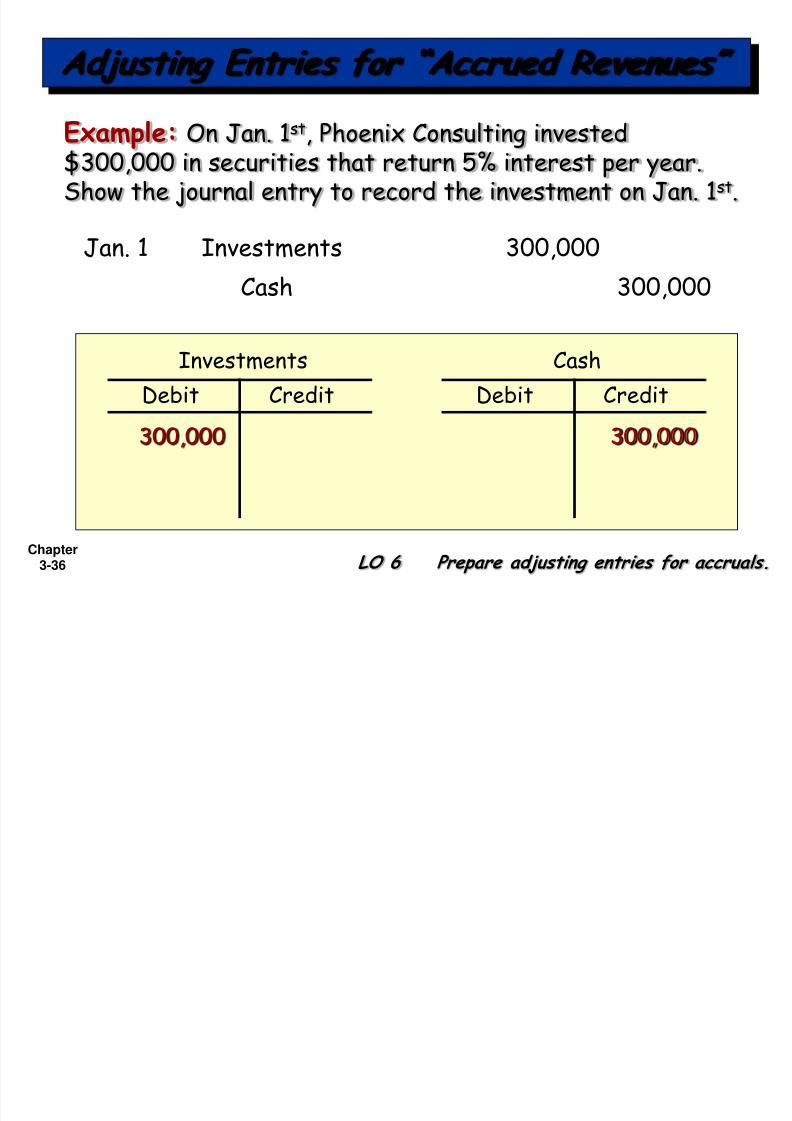

Example: On Jan. 1st

, Phoenix Consulting invested$300,000 in securities that return 5% interest per year.Show the journal entry to record the investment on Jan. 1st.

Cash 300,000

Investments 300,000Jan. 1

LO 6 Prepare adjusting entries for accruals.

Debit Credit

Investments

300,000 300,000

Debit Credit

Cash

Adjusting Entries for “Accrued Revenues”

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 37/50

Chapter3-37

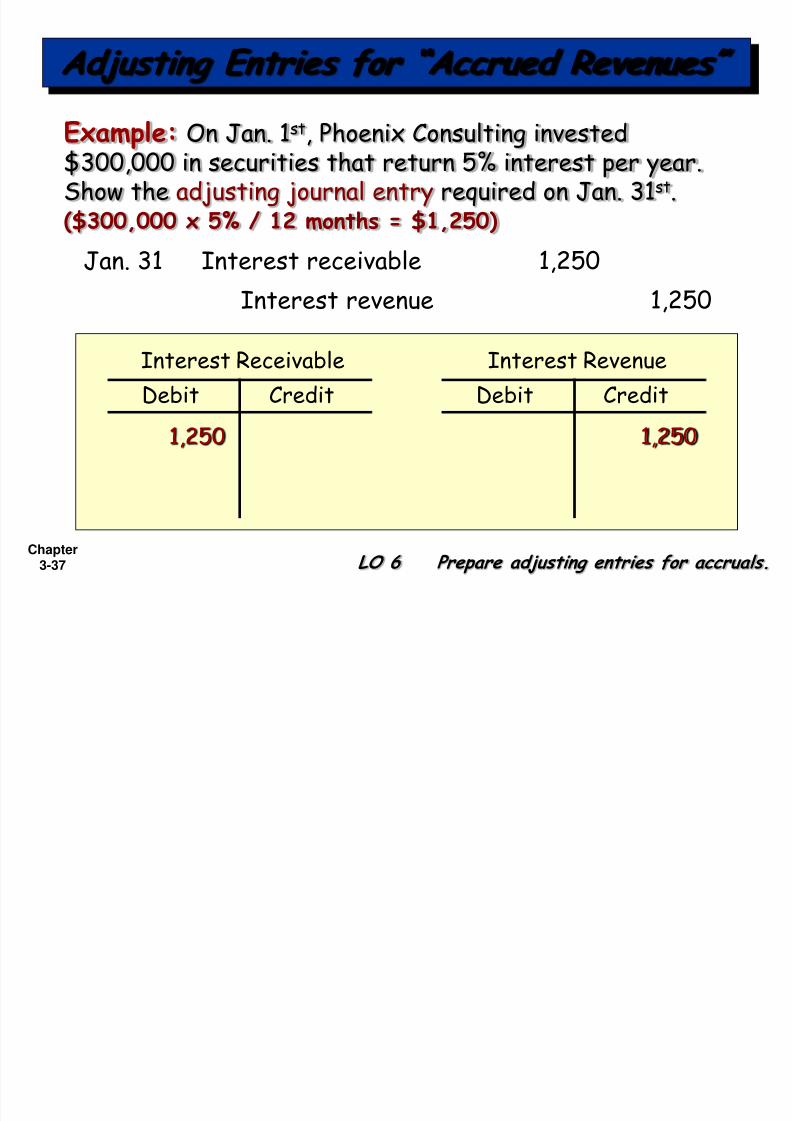

Example: On Jan. 1st

, Phoenix Consulting invested$300,000 in securities that return 5% interest per year.Show the adjusting journal entry required on Jan. 31st.($300,000 x 5% / 12 months = $1,250)

Interest revenue 1,250

Interest receivable 1,250Jan. 31

Debit Credit

Interest Receivable

1,250 1,250

Debit Credit

Interest Revenue

Adjusting Entries for “Accrued Revenues”

LO 6 Prepare adjusting entries for accruals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 38/50

Chapter3-38

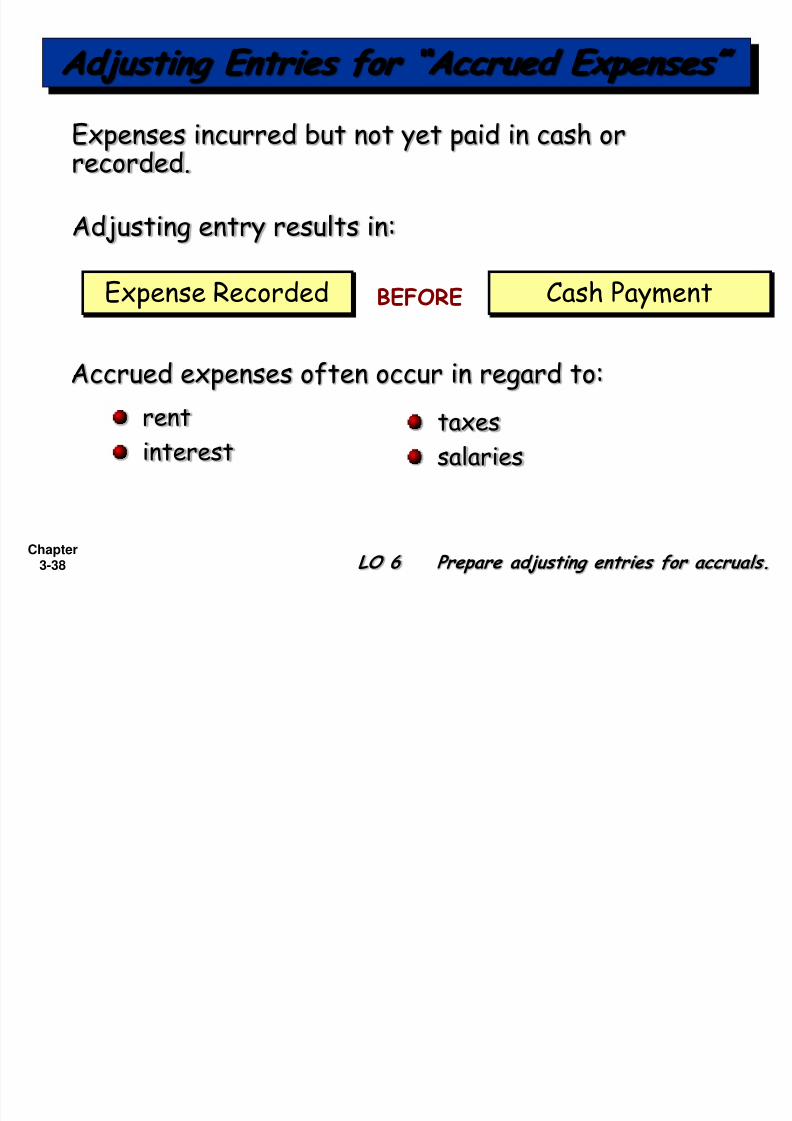

Expenses incurred but not yet paid in cash orrecorded.

Adjusting Entries for “Accrued Expenses”

rentinterest

BEFORE

Accrued expenses often occur in regard to:

Cash PaymentExpense Recorded

taxessalaries

Adjusting entry results in:

LO 6 Prepare adjusting entries for accruals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 39/50

Chapter3-39

Accrued Expenses An adjusting entry serves two purposes:

(1) It records the obligations, and

(2) It recognizes the expenses.

Adjusting Entries for “Accrued Expenses”

LO 6 Prepare adjusting entries for accruals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 40/50

Chapter3-40

Illustration 3-16Adjusting entries for accrued expenses

Increases (debits) an expense account and

Increases (credits) a liability account.

LO 6 Prepare adjusting entries for accruals.

Adjusting Entries for “Accrued Expenses”

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 41/50

Chapter3-41

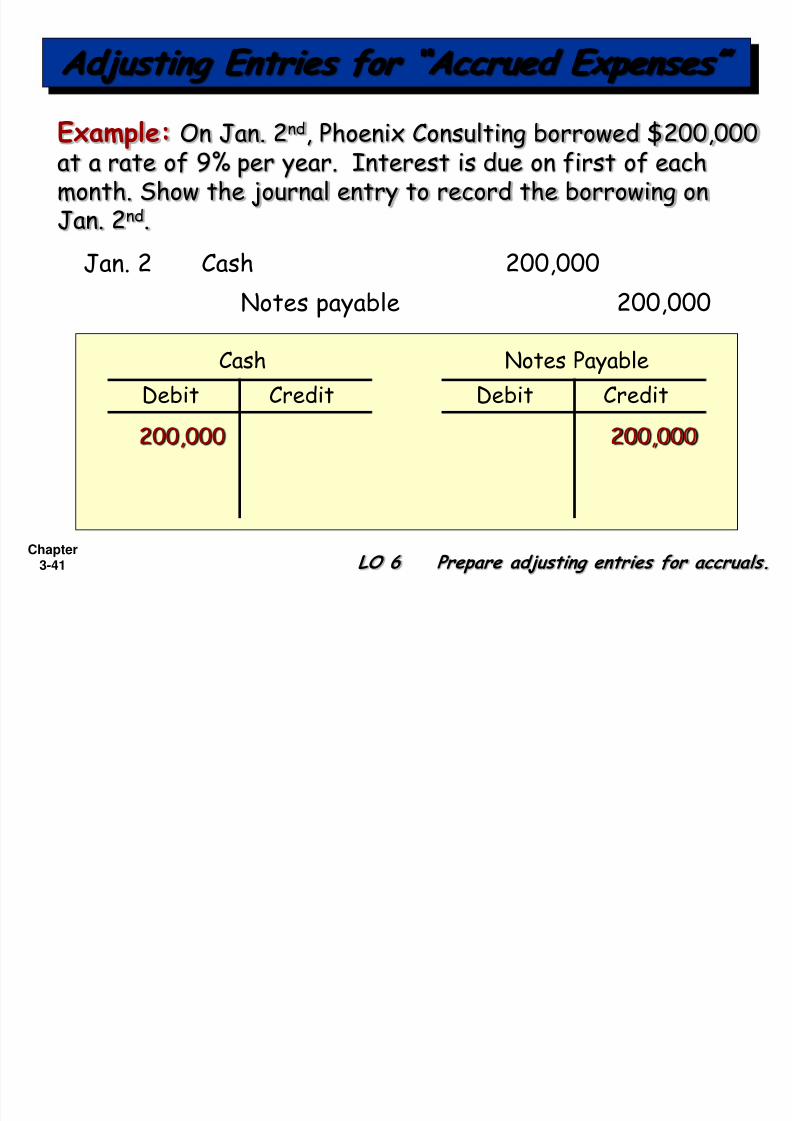

Notes payable 200,000

Cash 200,000Jan. 2

Debit Credit

Cash

200,000 200,000

Debit Credit

Notes Payable

Example: On Jan. 2nd

, Phoenix Consulting borrowed $200,000at a rate of 9% per year. Interest is due on first of eachmonth. Show the journal entry to record the borrowing onJan. 2nd.

Adjusting Entries for “Accrued Expenses”

LO 6 Prepare adjusting entries for accruals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 42/50

Chapter3-42

Example: On Jan. 2nd

, Phoenix Consulting borrowed $200,000at a rate of 9% per year. Interest is due on first of eachmonth. Show the adjusting journal entry required on Jan. 31st.($200,000 x 9% / 12 months = $1,500)

Interest payable 1,500

Interest expense 1,500Jan. 31

Debit Credit

Interest Expense

1,500 1,500

Debit Credit

Interest Payable

Adjusting Entries for “Accrued Expenses”

LO 6 Prepare adjusting entries for accruals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 43/50

Chapter3-43

Accrued Expenses An adjusting entry serves two purposes:

(1) It records the obligations, and

(2) it recognizes the expenses.

Adjusting Entries for “Accrued Expenses”

LO 6 Prepare adjusting entries for accruals.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 44/50

Chapter3-44

After all adjusting entries are journalized andposted the company prepares another trialbalance from the ledger accounts (Adjusted Trial

Balance).Its purpose is to prove the equality of debitbalances and credit balances in the ledger.

The Adjusted Trial Balance

LO 7 Describe the nature and purpose of an adjusted trial balance.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 45/50

Chapter3-45

Which of the following statements is incorrect

concerning the adjusted trial balance?

a. An adjusted trial balance proves the equality of the

total debit balances and the total credit balances inthe ledger after all adjustments are made.

b. The adjusted trial balance provides the primarybasis for the preparation of financial statements.

c. The adjusted trial balance lists the account balancessegregated by assets and liabilities.

d. The adjusted trial balance is prepared after theadjusting entries have been journalized and posted.

Review

Timing Issues

LO 7 Describe the nature and purpose of an adjusted trial balance.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 46/50

Chapter3-46

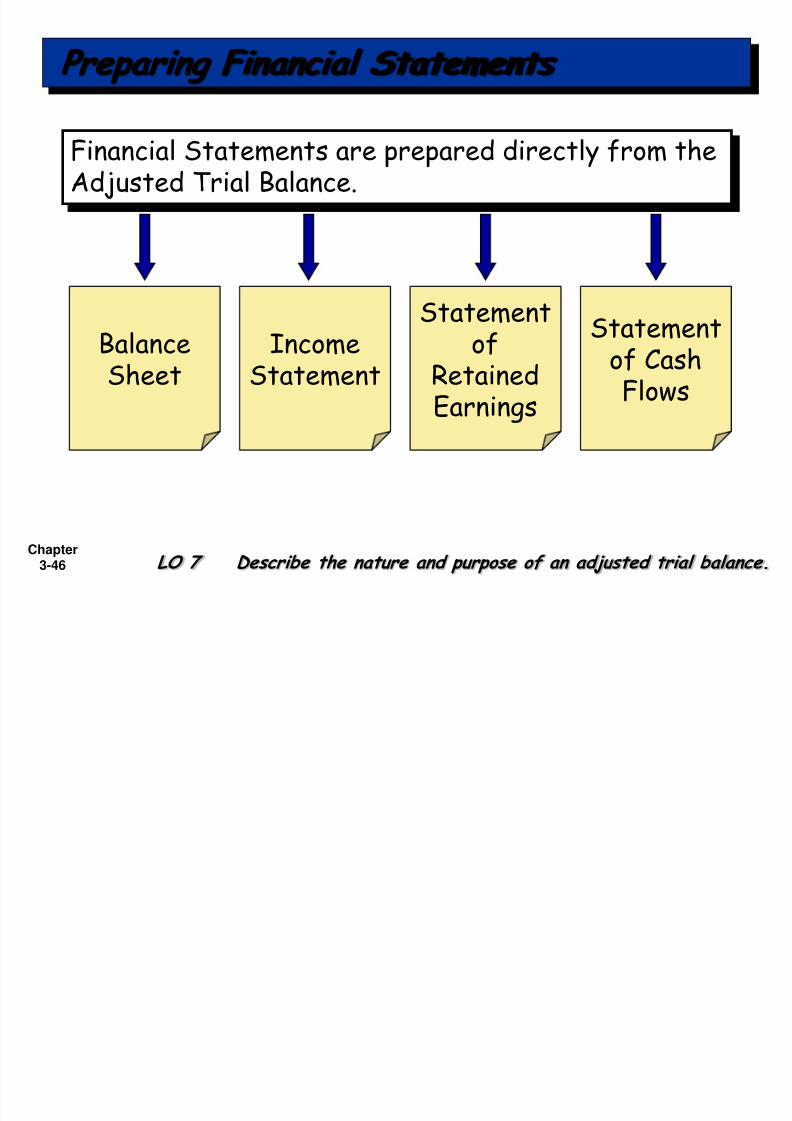

Financial Statements are prepared directly from theAdjusted Trial Balance.

BalanceSheet

IncomeStatement

Statementof CashFlows

Statementof

Retained

Earnings

Preparing Financial Statements

LO 7 Describe the nature and purpose of an adjusted trial balance.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 47/50

Chapter3-47

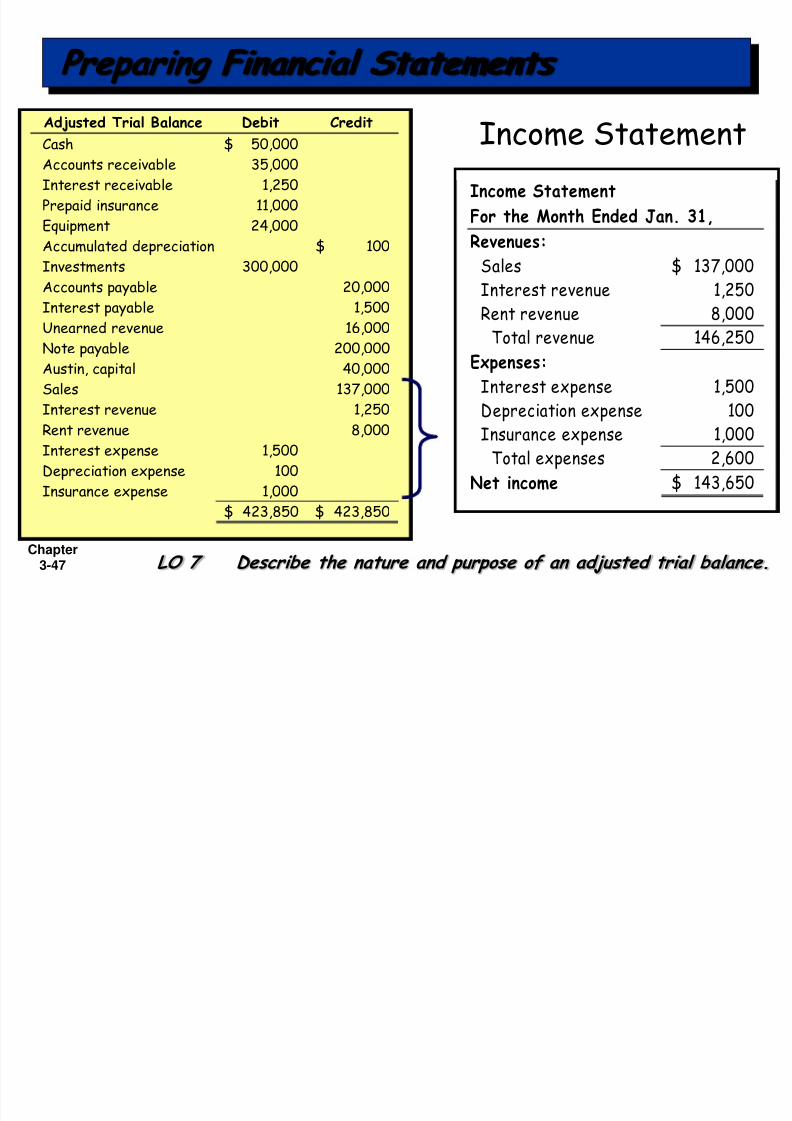

Income Statement

For the Month Ended Jan. 31,

Revenues:

Sales 137,000$

Interest revenue 1,250 Rent revenue 8,000

Total revenue 146,250

Expenses:

Interest expense 1,500 Depreciation expense 100 Insurance expense 1,000

Total expenses 2,600

Net income 143,650$

Income Statement

Preparing Financial Statements

LO 7 Describe the nature and purpose of an adjusted trial balance.

Adjusted Trial Balance Debit Credit

Cash 50,000$Accounts receivable 35,000

Interest receivable 1,250

Prepaid insurance 11,000

Equipment 24,000

Accumulated depreciation 100$

Investments 300,000

Accounts payable 20,000 Interest payable 1,500

Unearned revenue 16,000

Note payable 200,000

Austin, capital 40,000

Sales 137,000

Interest revenue 1,250

Rent revenue 8,000

Interest expense 1,500

Depreciation expense 100

Insurance expense 1,000

423,850$ 423,850$

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 48/50

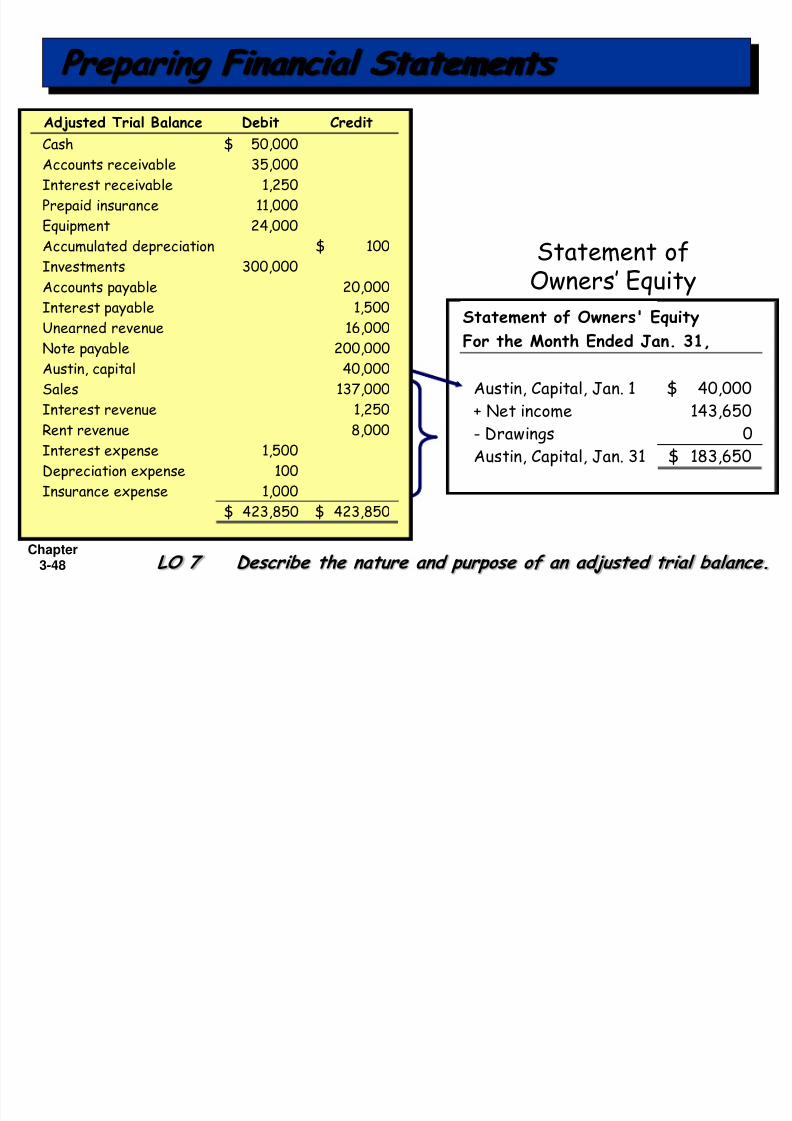

Chapter3-48

Statement of Owners' Equity

For the Month Ended Jan. 31,

Austin, Capital, Jan. 1 40,000$

+ Net income 143,650

- Drawings 0

Austin, Capital, Jan. 31 183,650$

Statement of

Owners’ Equity

Preparing Financial Statements

LO 7 Describe the nature and purpose of an adjusted trial balance.

Adjusted Trial Balance Debit Credit

Cash 50,000$Accounts receivable 35,000

Interest receivable 1,250

Prepaid insurance 11,000

Equipment 24,000

Accumulated depreciation 100$

Investments 300,000

Accounts payable 20,000 Interest payable 1,500

Unearned revenue 16,000

Note payable 200,000

Austin, capital 40,000

Sales 137,000

Interest revenue 1,250

Rent revenue 8,000

Interest expense 1,500

Depreciation expense 100

Insurance expense 1,000

423,850$ 423,850$

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 49/50

Chapter

3-49

Adjusted Trial Balance Debit Credit

Cash 50,000$Accounts receivable 35,000

Interest receivable 1,250

Prepaid insurance 11,000

Equipment 24,000

Accumulated depreciation 100$

Investments 300,000

Accounts payable 20,000 Interest payable 1,500

Unearned revenue 16,000

Note payable 200,000

Austin, capital 40,000

Sales 137,000

Interest revenue 1,250

Rent revenue 8,000

Interest expense 1,500

Depreciation expense 100

Insurance expense 1,000

423,850$ 423,850$

Balance Sheet Jan. 31

AssetsCash 50,000$Accounts receivable 35,000 Interest receivable 1,250 Prepaid insurance 11,000 Equipment 24,000

Accum. Depreciation (100) Investments 300,000

Total assets 421,150$

Liabilities & Owners' Equity

Accounts payable 20,000$Interst payable 1,500

Unearned revenue 16,000 Note payable 200,000 Austin, capital 183,650

Total liab. & equity 421,150$

Preparing Financial Statements

LO 7 Describe the nature and purpose of an adjusted trial balance.

8/3/2019 Accounting Principle Kieso 8e_Ch03

http://slidepdf.com/reader/full/accounting-principle-kieso-8ech03 50/50

Chapter

―Copyright © 2008 John Wiley & Sons, Inc. All rights reserved.Reproduction or translation of this work beyond that permittedin Section 117 of the 1976 United States Copyright Act withoutthe express written permission of the copyright owner isunlawful. Request for further information should be addressed

to the Permissions Department, John Wiley & Sons, Inc. Thepurchaser may make back-up copies for his/her own use onlyand not for distribution or resale. The Publisher assumes noresponsibility for errors, omissions, or damages, caused by theuse of these programs or from the use of the informationcontained herein.‖

Copyright