Embed Size (px)

Citation preview

Issued December 2015

Accounting Manual for Departments

Expenditure

Expenditure

Issued November 2016

Page 2

Chapter Content

1. Overview ....................................................................................................................................... 4

2. Key Learning Objectives ............................................................................................................... 4

3. Scope ............................................................................................................................................ 5

4. Expenditure ................................................................................................................................... 5

5. Recognition and Measurement of Expenditure ............................................................................ 7

5.1 General ............................................................................................................................... 7

5.2 Compensation of Employees ............................................................................................. 9

5.2.1 Salaries and wages ................................................................................................ 10

5.2.2 Social contributions ................................................................................................ 11

5.2.3 Members of Legislature salaries ............................................................................ 13

5.3 Goods and services .......................................................................................................... 15

5.3.1 Consultants, contractors and agency / outsourced services ................................. 16

5.3.2 Entertainment ......................................................................................................... 16

5.3.3 External audit fees ................................................................................................. 17

5.3.4 Capital assets less than R5,000 ............................................................................ 17

5.3.5 Consumables ......................................................................................................... 17

5.3.6 Inventory................................................................................................................. 18

5.3.7 Property payments ................................................................................................. 19

5.3.8 Travel and subsistence .......................................................................................... 20

5.4 Interest and rent on land .................................................................................................. 22

5.5 Payments for financial assets ........................................................................................... 24

5.6 Expenditure for capital assets .......................................................................................... 25

5.7 Transfers and subsidies ................................................................................................... 25

6. Disclosures ................................................................................................................................. 28

7. Summary of Key Principles......................................................................................................... 29

7.1 The types of expenditure the department would incur ..................................................... 29

Expenditure

Issued November 2016

Page 3

7.2 Recognition and measurement of expenditure ................................................................ 29

Expenditure

Issued November 2016

Page 4

1. Overview

The purpose of this Chapter is to provide an explanation on the different types of expenditure incurred by departments along with the accounting entries required to capture expenditure transactions in the Basic Accounting System (BAS).

The Office of the Accountant-General has compiled a Modified Cash Standard (MCS) and this manual serves as an application guide to the MCS which should be used by departments in the preparation of their financial statements.

Any reference to a “Chapter” in this document refers to the relevant chapter in the MCS and / or the corresponding chapter of the Accounting Manual.

Explanation of images used in the manual:

2. Key Learning Objectives

Understanding the different types of expenditure

Understanding the accounting entries for expenditure transactions

Definition

Take note

Management process and decision making

Example

Expenditure

Issued November 2016

Page 5

3. Scope

The Chapter on Expenditure in the MCS, and consequently this guide does not apply to:

The accounting requirements in respect of the secondary financial information for expenditure on capital assets. This is dealt with in the Chapter on Capital Assets. A department must also consider the provisions of that Chapter in order to correctly classify the type of asset acquired.

4. Expenditure

In the modified cash environment, expenditure is accounted for in the period in which the monies are paid and not in the period in which the underlying transaction or event that gives rise to the expenditure occurs. The management of expenditure must be directed at achieving economy, effectiveness and efficiency and avoiding unauthorised, irregular or fruitless and wasteful expenditure.

All functions and officials involved in the process of spending public funds must therefore ensure that:

a genuine requirement exists to expend funds on particular goods and services;

the expenditure is justified; and

funds are available.

The department’s service delivery mandate will drive the types of expenses it will incur. For example, departments whose service delivery mandate is to provide policy advice will spend a high portion of its budget on compensation of employees, whereas departments providing operational services will incur a wider range of expenses both of a current and a capital nature.

The main categories of expenditure for government departments are:

Compensation of employees;

Goods and services;

Interest and rent on land;

Transfers and subsidies;

Payments for financial assets - discussed in more detail in the Chapter on General Departmental Assets and Liabilities; and

Expenditure for capital assets - discussed in more detail in the Chapter on Capital Assets.

Expenses are decreases in economic benefits or service potential during the reporting period in the form of outflows or incurrences of liabilities that results in a decrease in net assets, other than those relating to capital distributions from net assets.

This means that expenditure is recognised when goods and/or services are received from parties. In the modified cash environment, payments are accounted for in the period in which the monies were paid and not in the period in which the underlying transaction or event occurred that gave rise to the expenditure.

Expenditure

Issued November 2016

Page 6

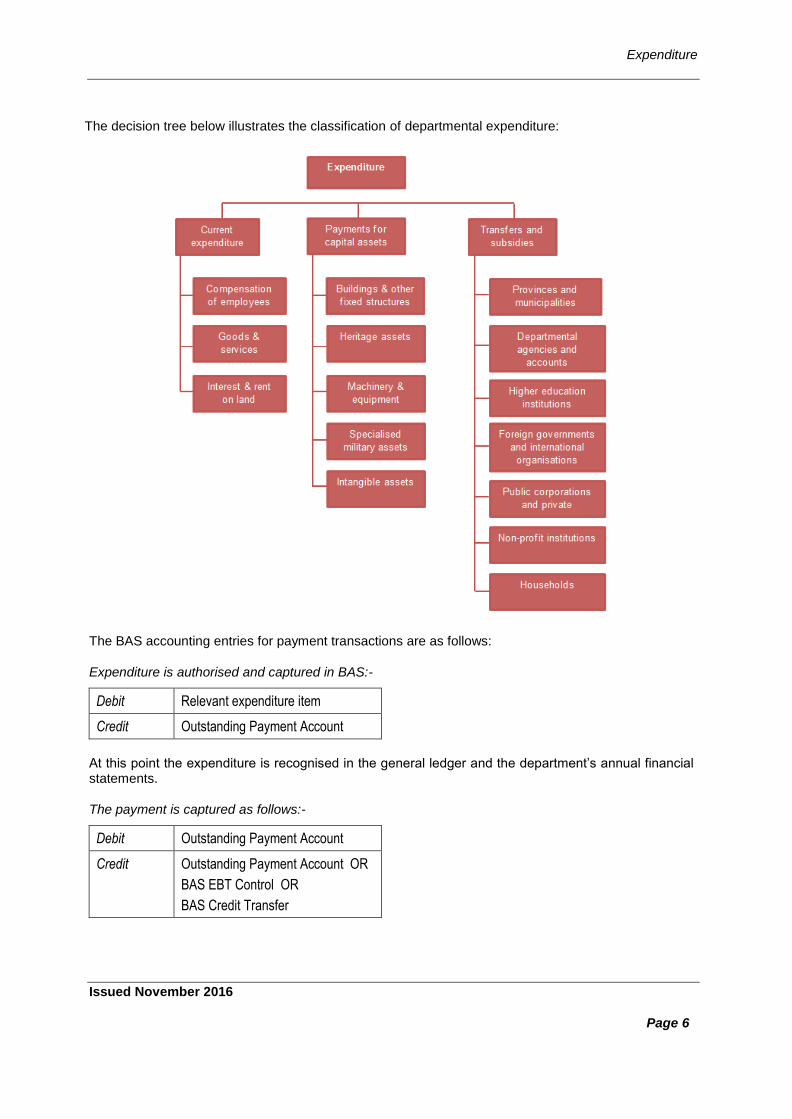

The decision tree below illustrates the classification of departmental expenditure:

The BAS accounting entries for payment transactions are as follows:

Expenditure is authorised and captured in BAS:-

Debit Relevant expenditure item

Credit Outstanding Payment Account

At this point the expenditure is recognised in the general ledger and the department’s annual financial statements.

The payment is captured as follows:-

Debit Outstanding Payment Account

Credit Outstanding Payment Account OR

BAS EBT Control OR

BAS Credit Transfer

Expenditure

Issued November 2016

Page 7

The interface on the bank statement:-

Debit Outstanding Payment Account OR

BAS EBT Control OR

BAS Credit Transfer

Credit Bank Account

Further discussion on the above can be found in the Chapter on The Standard Chart of Accounts and Systems.

5. Recognition and Measurement of Expenditure

5.1 General

A department recognises expenditure in the statement of financial performance on the date of payment.

For practical purposes, there is a rebuttable presumption that when a department authorises a payment on its system, the likelihood of this payment not occurring is remote and the department can recognise the expense. However, where there is evidence to the contrary, the department should make appropriate adjustments to ensure that expenses are recognised on the actual date that the cash outflow occurred.

Date of payment is the date on which the expenditure is authorised for payment on the system (but no later than the last day of the reporting period).

Note that there is a time lag between the authorisation for payment and the interface on the bank statement. At year-end the amount recognised as expenditure in the annual financial statements includes all purchases approved for payment by 31 March (even if the payment still needs to clear the bank account).

A rebuttable presumption means that something will be considered true (the presumption) until it is proven untrue (rebutted).

Expenditure

Issued November 2016

Page 8

Cash payments arising from transactions in a foreign currency should be recorded in South African Rand by applying to the foreign currency amount the spot exchange rate between South African Rand and the foreign currency at the date of the payment.

Expenditure is measured at the cash amount paid to settle the expenditure incurred.

Example: Recognition of expenditure

An invoice from a supplier for the purchase of goods or services is broken down as follows:

Invoice Impact on department

Cost of goods acquired

7,540.00 Amount recorded as the cost of goods acquired.

Note:

The trade discount is not recorded separately.

The cost of goods acquired includes the VAT levied by the supplier as a department is not a VAT vendor and cannot claim this amount from the Receiver. Thus the total expense is R8,279.82

Increase in expenditure resulting in a decrease in the surplus of the department

AND

Decrease in cash resources

Less: trade discount

(377.00)

Total excl VAT 7,263.00

VAT 1,016.82

Total incl. VAT 8,279.82

The payment to the supplier decreases the available cash resources and at the same time increases the costs of the department.

The above is reflected in the general ledger by:

Debit Relevant Goods and Services Expenditure Accounts

Credit Bank Account*

* This is the ultimate account; refer to the Chapter on The Standard Chart of Accounts and Systems for a further explanation on the credit leg of this transaction.

Expenditure

Issued November 2016

Page 9

5.2 Compensation of Employees

Example: Recognition of expenditure and accruals

An invoice received from the telephone company for the month of May is as follows:

Summary of account Impact on department

Balance brought forward

1,112.49

Payment(s) (1,112.49)

This invoice

(May 20x0)

1,219.42 Amount payable to the service provider

Recorded as ”Accruals” if unpaid

Rental 114.91

Usage 933.79

Subtotal 1,048.70

VAT 170.72

Total 1,219.42 Actual cost of line and calls made

When paid: Increase in expenditure resulting in a decrease in the surplus of the department.

Remove amount recorded as “Accruals “ in May

When the department pays the company in June 20x0 the impact on the general ledger is as follows:

Debit Relevant Goods and Services Expenditure Accounts

Credit Bank Account*

* This is the ultimate account; refer to the Chapter on The Standard Chart of Accounts and Systems for a further explanation on the credit leg of this transaction.

Compensation of employees comprise of most forms of consideration given by a department in exchange for services rendered by employees. It excludes payments made to employees as a re-imbursement of costs incurred on behalf of the employer (e.g. travel and subsistence expenditures).

Expenditure

Issued November 2016

Page 10

This is the largest spending item in the budget of government as more than a million public servants are paid via PERSAL on a monthly basis.

There are two main groupings within compensation of employees (also referred to as employee benefits), namely, “salaries and wages” and “social contributions”. Salary and wages comprise of amounts paid to the employees of a department including all payments made on their behalf such as PAYE / SITE and the employee’s contributions to pension and / or medical schemes. The social contributions category includes the employer’s contribution to the social insurance schemes to which the employee belongs.

Remember that only employee benefits paid to employees during the financial year are shown under “compensation of employees”. Employee benefits that have accrued to an employee, but have not yet been paid by year end are recorded in the “Employee Benefits” note to the financial statements. The recording and measurement of these liabilities are discussed in more detail in the Chapter on Provisions and Contingents.

5.2.1 Salaries and wages

Salaries and wages include the following payments:

Payments made to government employees at regular weekly or monthly intervals;

Remuneration to staff members employed on a contractual basis who are the government payroll and paid at regular intervals;

Supplementary allowances such as housing allowances;

Special allowances for overtime;

Special allowances for dangerous work;

Salaries and wages paid to employees away from work for short periods (such as leave pay); and

Performance bonuses.

Salaries and wages exclude the following payments:

Reimbursement of expenses incurred by employees for goods purchased to enable them to perform their duties e.g. tools, equipment and uniforms (classified as goods and services);

Reimbursement for relocation expenses e.g. when employees take up new positions of employment (classified as goods and services);

Travel and subsistence expenses e.g. per day and out-of-town allowances (classified as goods and services);

Purchases of services provided by non-government employees e.g. consultants and occasional workers (classified as goods and services);

Accounting For Transactions Related To The Government Employees Housing Scheme (GEHS)

Please refer to the instruction note issued by National Treasury on the OAG website.

Expenditure

Issued November 2016

Page 11

Social benefit allowances e.g. accidental injury, severance and pay for incapacity (classified as transfers to households); and

Allowances to dependents of employees are also categorised as social benefits (classified as transfers to households)

Compensation of employees includes most payments to government employees, except payments to government employees working on capital projects and where the department elects to capitalise these payments.

These specific payments are classified as capital expenditure and are recognised in the line item, “expenditure for capital assets” in the financial statement (refer to the Section on Expenditure on Capital Assets below).

Salaries and wages are further subdivided into smaller categories:

- Basic salary

- Performance awards

- Service based (benefit as determined by DPSA)

- Compensation/circumstantial

- Other non-pensionable allowances

- Periodic payments

5.2.2 Social contributions

Social contributions include employer contributions to social insurance schemes on behalf of its employees. Any contribution made by the employee is included under basic salary.

Social contributions are normally made on behalf of employees currently employed, but can also be paid on behalf of former employees.

Social contributions are further subdivided into smaller categories:

- Pension funds

- Provident funds

- Medical aid schemes

- Unemployment insurance funds

- Bargaining councils

- Official unions and associations

- Insurance

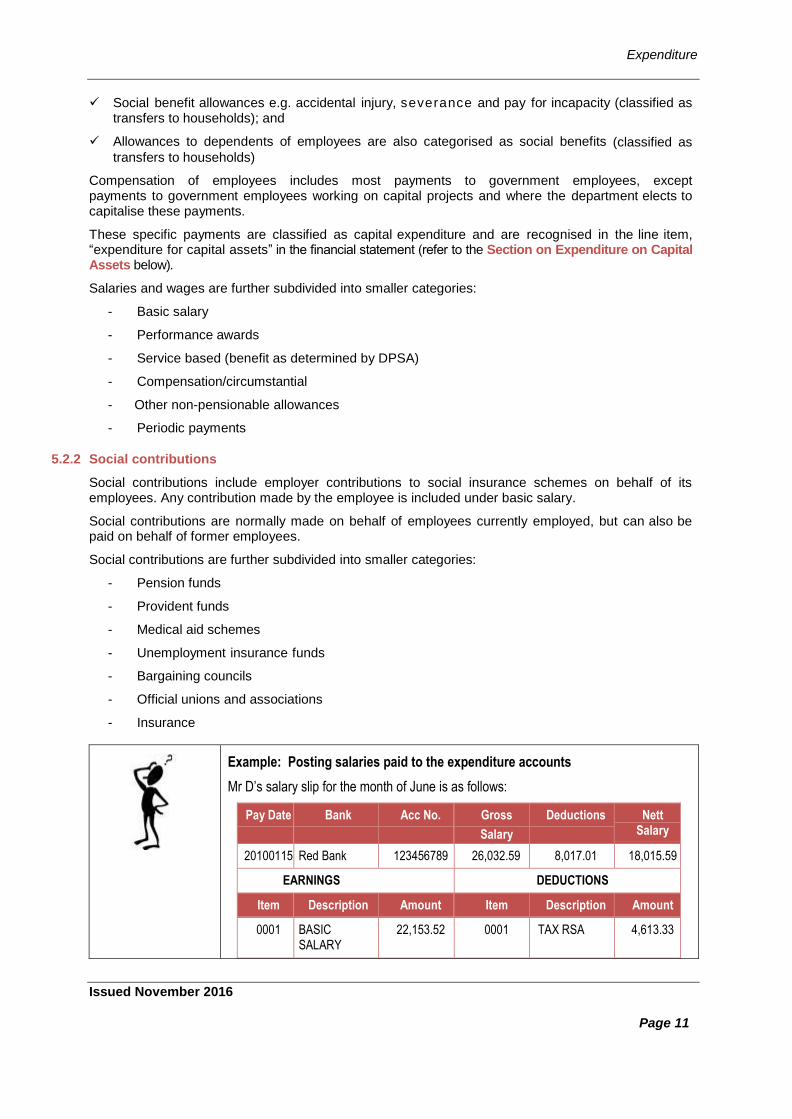

Example: Posting salaries paid to the expenditure accounts

Mr D’s salary slip for the month of June is as follows:

Pay Date Bank Acc No. Gross

Salary

Deductions Nett Salary

20100115 Red Bank 123456789 26,032.59 8,017.01 18,015.59

EARNINGS DEDUCTIONS

Item Description Amount Item Description Amount

0001 BASIC SALARY

22,153.52 0001 TAX RSA 4,613.33

Expenditure

Issued November 2016

Page 12

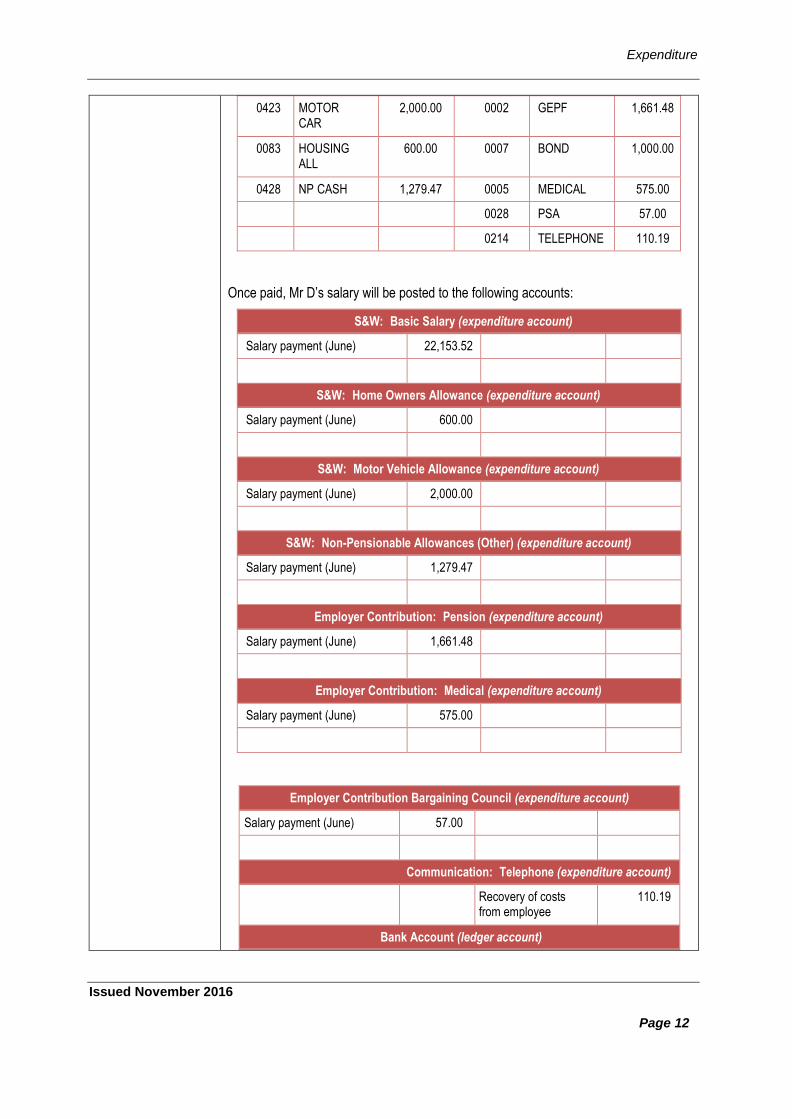

0423 MOTOR CAR

2,000.00 0002 GEPF 1,661.48

0083 HOUSING ALL

600.00 0007 BOND 1,000.00

0428 NP CASH 1,279.47 0005 MEDICAL 575.00

0028 PSA 57.00

0214 TELEPHONE 110.19

Once paid, Mr D’s salary will be posted to the following accounts:

S&W: Basic Salary (expenditure account)

Salary payment (June) 22,153.52

S&W: Home Owners Allowance (expenditure account)

Salary payment (June) 600.00

S&W: Motor Vehicle Allowance (expenditure account)

Salary payment (June) 2,000.00

S&W: Non-Pensionable Allowances (Other) (expenditure account)

Salary payment (June) 1,279.47

Employer Contribution: Pension (expenditure account)

Salary payment (June) 1,661.48

Employer Contribution: Medical (expenditure account)

Salary payment (June) 575.00

Employer Contribution Bargaining Council (expenditure account)

Salary payment (June) 57.00

Communication: Telephone (expenditure account)

Recovery of costs from employee

110.19

Bank Account (ledger account)

Expenditure

Issued November 2016

Page 13

5.2.3 Members of Legislature salaries

Since members of Legislatures are not “employees”, their remuneration should be disclosed separately.

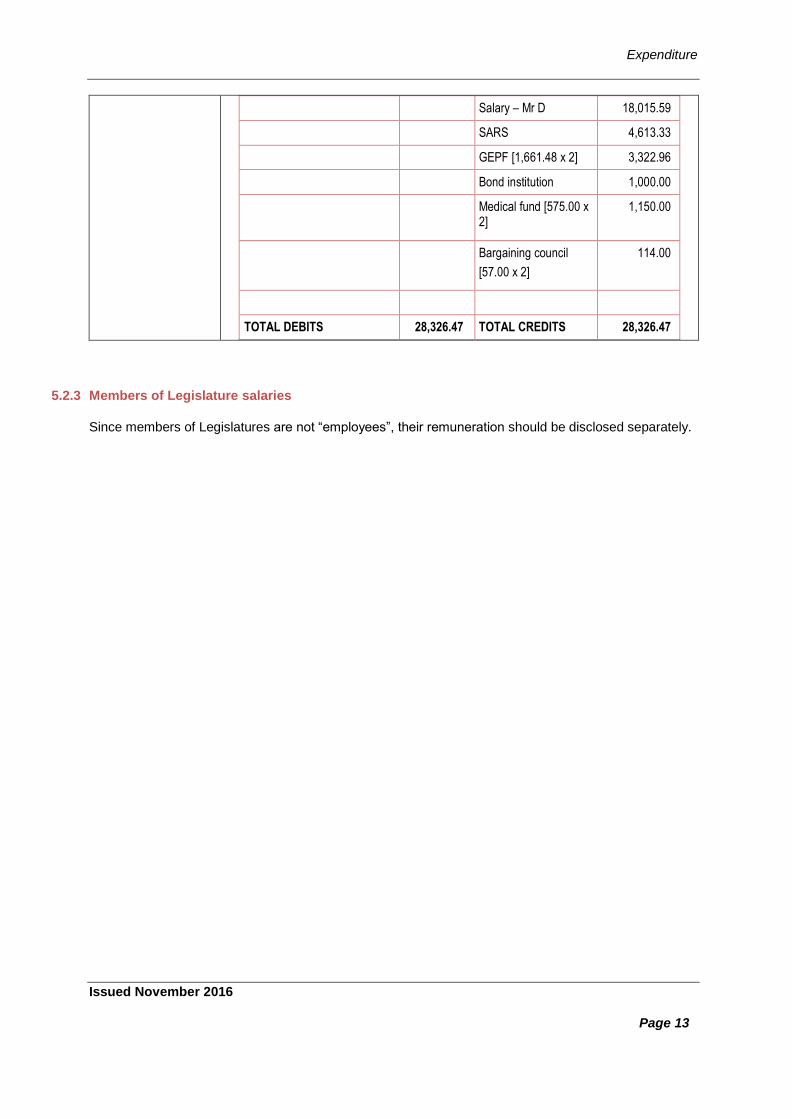

Salary – Mr D 18,015.59

SARS 4,613.33

GEPF [1,661.48 x 2] 3,322.96

Bond institution 1,000.00

Medical fund [575.00 x 2]

1,150.00

Bargaining council

[57.00 x 2]

114.00

TOTAL DEBITS 28,326.47 TOTAL CREDITS 28,326.47

Expenditure

Issued November 2016

Page 14

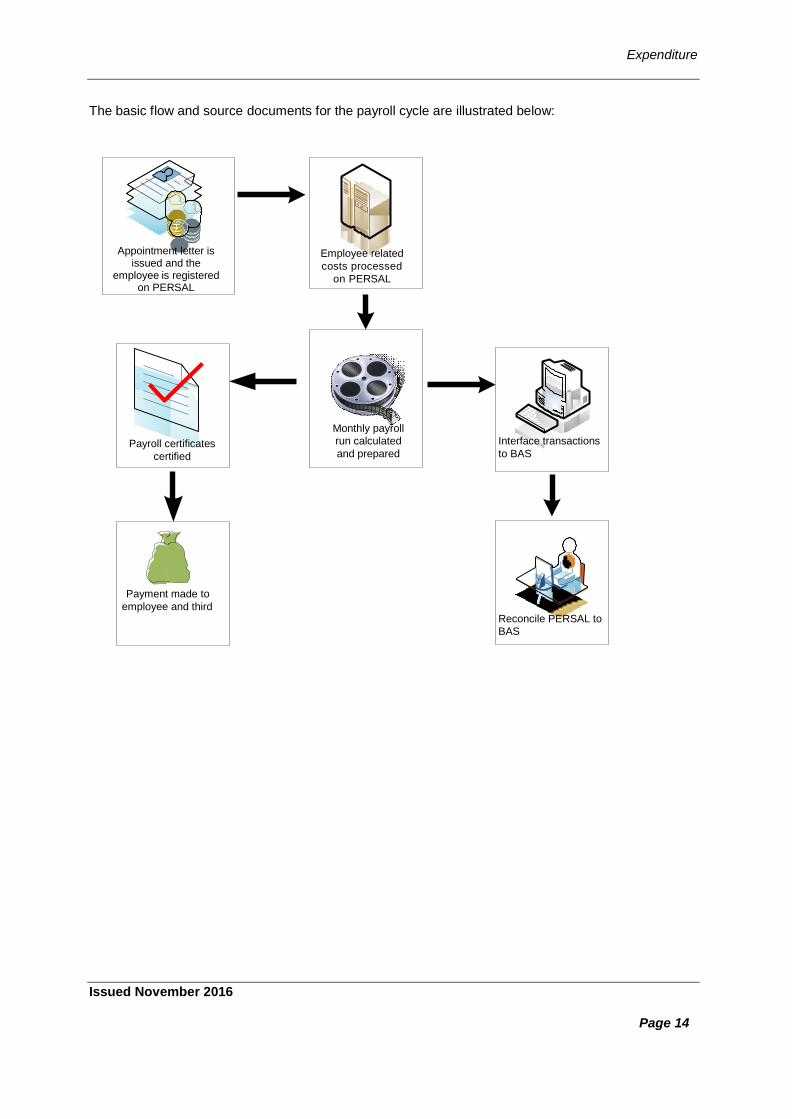

The basic flow and source documents for the payroll cycle are illustrated below:

Appointment letter is issued and the

employee is registered on PERSAL

Employee related

costs processed

on PERSAL

Payroll certificates

certified

Payment made to

employee and third

Monthly payroll

run calculated

and prepared

Interface transactions

to BAS

Reconcile PERSAL to

BAS

Expenditure

Issued November 2016

Page 15

Refer to the Chapter on The Standard Chart of Accounts and Systems for the accounting entries in BAS and PERSAL.

5.3 Goods and services

This category includes payments for all goods and services to be used by a department, excluding purchases of capital assets costing more than R5,000. Purchases of capital assets costing more than R5,000 fall under expenditure for capital assets. All capital assets to be used by a department and costing less than R5,000 are included here under goods and services

Payments for goods and services, to be used as input into a capital project carried out by government, are also excluded from goods and services. Such payments are classified as capitalised payments and are explained in more detail below under the Section on Expenditure on Capital Assets.

Goods and services include the following payments

Goods purchased for resale e.g. postcards for resale by government owned museums.

Goods purchased by government, but later transferred in kind to employees or other units.

Payments for use of buildings from other departments, for example Public Works.

Payments for research, design costs, bursaries to government employees and consultants’ fees.

Other examples of goods are: for example petrol, coal, small tools and equipment, stationery, foodstuff and electricity.

Other examples of services are: accommodation (hotels, etc.), restaurants, transport, communication, banking, business services, consultant fees, market research and staff training, as well as rental of buildings (not rental of land), other fixed structures, equipment and vehicles.

Reimbursements of:

o expenses incurred by employees on tools, equipment, uniforms and other items that are needed to enable them to carry out their work; uniform allowances if the employee is required to purchase a uniform required for use at work; and

o expenses incurred by employees when they take up new jobs or are required by their employer to move their homes, e.g. relocation expenses.

Goods and services in the statement of financial performance exclude the following payments

Payments for capital assets;

Payments for goods and services, to be used as input into a capital project executed by government;

Rent on land (*where it is not possible to distinguish the rent of land from the rent of buildings the total amount is included in goods and services – operating leases. Guidance on operating leases is in the Chapter on Leases);

Goods and services include payments for all goods and services to be used by a department, excluding purchases of capital assets.

Expenditure

Issued November 2016

Page 16

5.3.1 Consultants, contractors and agency / outsourced services

Consulting services refer to those specialist services and skills provided that are required for the achievement of a specific objective, with the aim of providing expert and professional advice on a time and material basis. It is unnecessary to maintain these skills in-house, since they are required on a once-off or temporary basis.

A consultant is a professional person appointed by the Public Service to provide technical and specialist advice or to assist with the design and implementation of projects / programmes. The legal status of this person can be an individual, a partnership, a corporation or a company.

The fact that a consultant is defined as a professional person implies that the consultant is professionally qualified. The provision of advice or service is in line with a contractual arrangement (usually commissioned on a project basis). Remuneration is usually based on an hourly fee or a fixed fee for a product / deliverable.

Contractors are required to provide services that are not the core business of the department. It is normally not cost effective to maintain these skills within the department. Contractors include costs associated with the use of contracted individuals or businesses on projects or tasks. Also note that it is common practice that the contractor provides all the materials required for the project - he/she tenders for the whole project including material required for the project.

Refer to the Chapter on Capital Assets for guidance on the capitalisation of consulting services to the cost of a capital project.

With regards to agency support and outsourced services, a department ordinarily has the capacity and expertise to carry out these services, but for some reason it is not utilising its own staff. The reasons might include temporary incapacity or the outsourcing of services to save costs, for example, cleaning, security and recruitment.

In evaluating the classification of such a transaction it should be established whether the service being procured could have been provided by the department itself. It could also be that the department ordinarily has the expertise to provide this service, but temporarily cannot do so or that in order to save costs, the work has been outsourced. If these requirement hold, the transaction should be classified as agency support / outsourced services.

5.3.2 Entertainment

This item includes entertainment expenditure incurred by members of the Senior Management Service (SMS) as well as Ministers and his/her office bearers in performance of their duties. Such expenditure includes, but is not limited to:

luncheon meetings held with colleagues, foreign delegations and/or other individuals in and outside the public sector; and

Purchase of dinner during authorised overtime

This item does not include, but is not limited to, spending on:

Gifts (including flowers) to individuals;

Private entertainment; and

Cleaning services contracted to service providers: classified as property payments or contractors

Only cleaning services related to properties such as office buildings etc. should be classified as property payments.

Expenditure

Issued November 2016

Page 17

Cost of meals claimed by individuals when away from home on official duty.

5.3.3 External audit fees

A distinction should be made between fees paid for the audit and fees paid for other services. Audits of departments are performed by the Auditor-General or by a firm of auditors on behalf of the Auditor-General. That firm may not render other services to the department, unless prior approval of the Auditor-General has been obtained. Accordingly any fees paid to audit firms would be for services other than the external audit and would be included under the heading of consultants and advisory services.

In the note, the following split regarding auditors’ remuneration should be shown:

Regularity audits

Performance audits

Investigations

Environmental audits

Computer audits

5.3.4 Capital assets less than R5,000

Capital assets less than R5,000 is measured per item / unit and not per payment. For example, a down payment of R4,000 on equipment of R10,000, will not be classified as capital assets less than R5,000 as there is still an outstanding amount of R6,000.

5.3.5 Consumables

Consumables are goods that normally meet the definition of inventory, but are not essential for satisfying the service delivery obligation of a department.

All capital assets purchased with a value of less than R5,000 each is recognised as expenditure under goods and services in the statement of financial performance in accordance with this chapter. The opposite applies to all capital assets purchased with a value of more than R5,000 each. These are recorded as capital assets in the statement of financial performance in accordance with the Chapter on Capital Assets.

If the department purchases 1,000 computers for R5,000 each the department should treat them as capital assets under the Chapter on Capital Assets and not as current expenditure under this chapter, whereas if the department purchases 1,000 computers for R4,999 each the department will treat them as current expenditure under this chapter.

Example: Consumables

Tea and coffee purchased by a provincial treasury for internal meetings purposes;

All stationery purchased by departments for internal use;

Memory sticks, DVD’s and other IT consumables;

Spare light bulbs for the lifts in an office building;

Milk used by employees;

Medicine in a first-aid kit for use by employees ;

Stationery used for administration of the department;

Expenditure

Issued November 2016

Page 18

5.3.6 Inventory

Inventories are assets:

in the form of materials or supplies to be consumed in the production process (for example, cement purchased by DPW when constructing a building); or

in the form of materials or supplies to be consumed or distributed in the rendering of services (for example, medication in the health sector environment, or animals procured and reared specifically to be consumed in the delivery of the department’s mandate such as, day old chicks bought and raised for slaughter and consumption in the short term, three weeks or three months even while harvesting eggs in between); or

held for sale or distribution in the ordinary course of operations (for example, furniture bought by the department of education for the schools ; or

in the process of production for sale or distribution (for example, work-in-progress when Human Settlement is construction RDP house to be distributed).

Inventory items are limited to those departments (called “Inventory Departments”) that must have inventory in order to deliver on their mandate. Should the inventory items not be needed for a department to deliver on their service delivery mandate, then those departments (called “Non-Inventory Departments”) are advised to use consumable items provided for in the Standard Chart of Accounts (SCOA).

Inventory versus consumables is largely covered by the mandate of the department and professional judgement. A department is either of the following:

“Inventory Department” - has inventory in order to deliver on their mandate

Consumable or “Non-Inventory Department”- the inventory items not needed for a department to deliver on their service delivery mandate

Cleaning materials used to clean office space;

Toilet paper bought in bulk – for use by employees of a department;

Sand, cement, bricks used by an internal maintenance unit for repairs to office space;

Uniforms for additional ad hoc security personnel e.g. at a Treasury;

Fertiliser e.g. for a garden surrounding office space

Refer to the AMD chapter on Inventory

Expenditure

Issued November 2016

Page 19

Further to the aspect of mandate, there may be indicator of materiality which are either qualitative, i.e. needed to comply with laws and regulations, or quantitative, where the cost of an item, may indicate the necessary level or control over an item.

Items such as the strategic importance of an item, or the level of care which needs to be exercised when managing an item, are considerations when determining whether an item needs to be considered as inventory or a consumable

5.3.7 Property payments

This category provides for all payments related to contractual (or otherwise) obligations contributing to the functionality of, for example buildings or land such as:

Gardening services;

Safety and security services;

Municipal services (which includes water, electricity, sewerage and waste / refuse removal); and

Payments for the maintenance, upgrade / addition or refurbishment / rehabilitation of property.

With regards to payments for the maintenance, upgrade / addition or refurbishment / rehabilitation of property:

These activities are executed as either own-account or outsourced projects. Outsourced projects are carried out by outside contractors and own-account projects by departments. If a department engages in an own-account maintenance / repairs, upgrade / additions and refurbishment / rehabilitation project, the Item segment is used to identify all inputs acquired i.e. compensation of employees (e.g. labour), and goods & services (e.g. inventory and equipment).

The Asset and Infrastructure segment on the other hand is used to identify the asset class and whether the project is ultimately classified as current or capital expenditure in the financial statements (refer to the Chapter on The Standard Chart of Accounts and Systems).

Irrespective of an item being inventory or consumable it is important that is managed and controlled. Departmental policies and procedures should address this.

The payments of rates and taxes to a municipality are not classified here. Rates and taxes are non-exchange transactions and are therefore recorded under “transfers and subsidies: provinces & municipalities”.

Maintenance and repairs include activities aimed at maintaining the capacity and effectiveness of an asset at its intended level. The maintenance action implies that the asset is restored to its original condition and there is no significant enhancement to its capacity or the value of the asset.

Upgrades and additions include activities aimed at improving the capacity and effectiveness of an asset above that of the intended purpose. The decision to renovate, reconstruct or enlarge an asset is a deliberate investment decision which may be

Expenditure

Issued November 2016

Page 20

5.3.8 Travel and subsistence

Travel and subsistence includes the payments for travel (either by way of land or air travel) within or outside South Africa for business purposes and subsistence for food and drink where the employee is required to stay at a location other than his/her permanent residence for one night or more within or outside South Africa. All payments with regards to travel and subsistence should be included under this item and a split between local and foreign travel and subsistence should be disclosed. All such payments should be processed through PERSAL.

undertaken at any time. It is not dictated by the condition of the asset, but rather in response to a change in demand and/or change in service requirements.

Rehabilitation and refurbishment include activities required due to neglect or unsatisfactory maintenance or degeneration of an asset. The action implies that the asset is restored to its original condition, enhancing the capacity and value of an existing asset that has become inoperative due to the deterioration of the asset.

Expenditure

Issued November 2016

Page 21

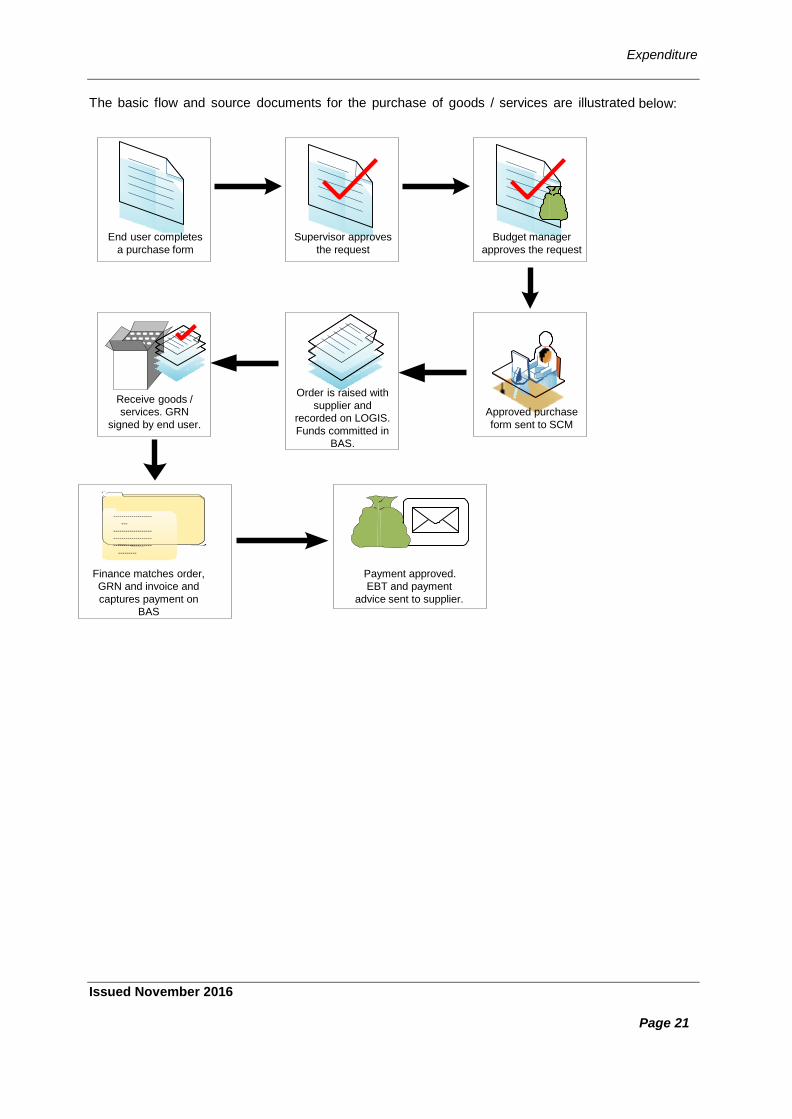

The basic flow and source documents for the purchase of goods / services are illustrated below:

End user completes

a purchase form

Supervisor approves

the request

Budget manager

approves the request

Receive goods /

services. GRN

signed by end user.

Order is raised with

supplier and

recorded on LOGIS.

Funds committed in

BAS.

Approved purchase

form sent to SCM

-------------------

---

-------------------

-------------------

-------------------

---------

Finance matches order,

GRN and invoice and

captures payment on

BAS

Payment approved.

EBT and payment

advice sent to supplier.

Expenditure

Issued November 2016

Page 22

5.4 Interest and rent on land

Interest includes the following payments:

Total value of interest payments where such payments are associated with debt, e.g. interest on borrowing and overdraft facilities.

Interest payments on bills and bonds issued by other government units.

Interest paid on overdue accounts.

Interest payments to local government on water and electricity accounts.

Interest on finance leases relating to public private partnerships (PPP).

Interest paid on Corporation for Public Deposit advances.

Rent on land includes the following payments:

Total value of payments due to the use of land owned by another party, including other government units.

Total value of payments due to use of sub-soil assets and other naturally occurring assets that are commercially exploitable such as virgin forests, game and fisheries. If it is impossible to distinguish between the rent of land and rental of the fixed structures erected thereupon, the whole amount, including the payment for use of land, is included in goods and services .

Interest includes the total value of interest payments. These are payments associated with debt, for example interest on borrowing and overdraft facilities. Interest payments on bills and bonds issued by other government units are also included here. Interest paid on overdue accounts should also be included under this item.

Rent on land includes the total value of payments due to the use of land owned by another party, including other government units.

Dealing with interest paid on Corporation for Public Deposit advances by provincial treasuries

When a provincial treasury requests an advance from the Corporation for Public Deposit (CPD), interest will be charged by the CPD. The provincial treasury has to determine which department is responsible for this request and the interest charged will be recovered from that department. However should the provincial treasury not be able to identify the responsible department, the provincial treasury has two options, namely:

To create a statutory vote for interest payment for the revenue fund. Funds should be appropriated for this; or

To fund the payment from the Paymaster General Account of the provincial treasury. In this case, approval that such interest is not fruitless and wasteful expenditure should be sought from the accounting officer or delegated official. Alternatively this should be covered in a departmental policy.

The interest cannot be a direct cost of the revenue fund.

Expenditure

Issued November 2016

Page 23

Note that all rent on land excludes rental for the use of buildings or other fixed structures. If it is not possible to distinguish between payment for the use of land and the fixed structures on it, the whole amount is recorded under goods and services as discussed in the Section on Goods and Services above.

Example: Interest

A provincial department of health purchases medicine from a supplier. It is policy to pay all suppliers within 30 days. In this instance the department takes 90 days to settle the account. Consequently the supplier charges interest of R150.

The accounting entry will be as follows:

Debit Credit

R R

INT PAID: Overdue Accounts 150

Bank Account* 150

*This is the ultimate account; refer to the Chapter on The Standard Chart of Accounts and Systems for a further explanation on the credit leg of this transaction.

This might attract Fruitless and Wasteful expenditure because expenditure was made in vain and would have been avoided had reasonable care been exercised

Example: Rent on land

The department of Defence rents a property that includes offices and a warehouse located outside Pretoria. The rent is made up of R50,000 for the fixed structures and R10,000 for the plot. The agreement is an operating lease.

The accounting entry for the rent of land will be as follows:

Debit Credit

R R

Rent on Land Account 10,000

Bank Account 10,000

The accounting entry for the rent of fixed structures will be as follows:

Debit Credit

R R

Goods and Services: Operating Leases 50,000

Bank Account 50,000

Expenditure

Issued November 2016

Page 24

5.5 Payments for financial assets

It is necessary to account for transactions associated with certain financial transactions in assets. This item consists mainly of transactions that create or increase a debtor’s outstanding account. Examples are where amounts are written off of debt that originated from irregular, fruitless and wasteful expenditure. Major categories should be grouped under each subheading and material items should be listed. In other words, major categories can be the total debts written off due to irregular expenditure, or due to unauthorised expenditure. Where there were specific material items within one of the categories, it should be disclosed additionally. For example:

“Included in the R5m debts written off due to irrecoverable fruitless and wasteful expenditure, is a specific item amounting to R4m that was written off as fruitless and wasteful expenditure as a result of……..”.

Payments for financial assets consist mainly of transactions that result in losses to the department such as the write-off of debt.

Example 4: Payments for financial assets

Department of Public Enterprises loans money to Eskom for the upgrading of its infrastructure. The amount loaned is R50 million, and no interest is charged. The accounting entry in the statement of financial performance, when the loan is extended will be as follows:

Debit Credit

R R

Extension of loans for policy purposes

(under “payments for financial assets”)

50,000,000

Bank Account* 50,000,000

The departments subsequently accounts for the loan in the statement of financial position as follows:

Debit Credit

R R

Loans (public corporations) : non-current assets

50,000,000

Loans (public corporations): recoverable capital

50,000,000

Any repayment from Eskom (e.g. R10,000,000) shall be recorded as follows:

Debit Credit

R R

Expenditure

Issued November 2016

Page 25

5.6 Expenditure for capital assets

Payments for capital assets include:

payments towards the cost of a new asset;

payments toward the cost of improvements to an existing capital asset;

payments for the use of an asset in terms of a finance lease arrangement;

Refer to Chapter on Capital Assets for more detail.

5.7 Transfers and subsidies

Examples of current transfers are:

Social security benefits paid to households

Fines

Penalties

Compulsory fees

Compensation for injuries or damages paid to another unit

Examples of capital transfers are:

Payments that are conditional on the recipient unit using the funds to acquire capital assets

Bank 10,000,000

Loans (public corporations) : non-current assets

10,000,000

Recording of the actual receipt

Debit Credit

R R

Loans (public corporations): recoverable capital

10,000,000

Departmental revenue – transactions in financial assets and liabilities, loans: public sector

10,000,000

The receipt is recorded as departmental revenue and subsequently paid over to the relevant revenue fund.

Transfers and subsidies include all “non-exchange” payments made by a department. A payment is “non-exchange” provided that the department does not receive anything directly in return for the transfer to the other party.

Both current and capital transfers are included in this item.

For more information on “exchange” and “non-exchange” refer to the Chapter on Revenue.

Expenditure

Issued November 2016

Page 26

Transfer to enterprises (publicly or privately owned) to cover large operating deficits accumulated over at least two years or to finance their cost of purchasing capital assets

Debt forgiveness extended to others

Capital taxes payable to other departments

Subsidies on production

Comprise all current, payments to businesses - both government and privately owned - on the basis of their level of production or quantity, or values of products produced, sold, imported or exported. Subsidies influence the level of production and/or pricing policies of the recipient.

Subsidies can be payable on specific products or on production in general. A subsidy on a product is a subsidy payable per unit of a good or service. The subsidy may be a specific amount of money per unit of quantity of a good or service, or it may be calculated ad valorem as a specified percentage of the price per unit. A subsidy may also be calculated as the difference between a specified target price and the market price actually paid by a buyer. A subsidy on a product usually becomes

payable when the good or service is produced, sold, exported, or imported. But it may also be payable

in other circumstances, such as when a good is transferred, leased, delivered, or used for own consumption or own capital formation.

Subsidies on production consist of subsidies that enterprises receive for engaging in production but that are not related to specific products. Included are subsidies on payroll or workforce, which are payable on the total wage or salary bill, the size of the total workforce, or the employment of particular types of person; subsidies to reduce pollution; and payments of interest on behalf of corporations.

Subsidies also include transfers to public corporations to compensate for losses they incur on their productive activities as a result of charging prices that are lower than their average costs of production because of deliberate government economic and social policy. If such losses have been accumulated over two or more years, however, the transfer is considered to be of a capital nature and classified as other transfers to public corporations and private enterprises.

Other transfers to public corporations and private enterprises

Consist of all capital transfers and those current transfers whose purpose is not to subsidise production. Most of these transfers are capital transfers; e.g. of this category include payments to corporations and enterprises to finance purchases of capital assets, to compensate them for damages to capital assets, and to cover large operating deficits accumulated for at least two years.

Transfers to municipalities

Include payment of rates and taxes. Property rates are levied by a municipality in terms of the Municipal Property Rates Act to pay for a wide range of public services, from the maintenance of roads and traffic control, to providing public parks, libraries, clinics, recreation centres and other similar services for the public. These services are for the benefit of the community as a whole and not an individual ratepayer. As such there is no direct link between the amounts paid by a ratepayer and the value of services received in return.

Transfers to households

Social benefits are current transfers to households, but not all transfers to households are included under this category. Included are the transfers made to households to protect them against

events that may adversely affect their social welfare; e.g. include the child support grant; payments

for medical, convalescent and dental care and home care. Social benefits also encompass the cost to provide free housing and housing below market prices.

Other transfers to households consist of all other transfers to households. All capital transfers to households are included here. This category also includes payments of bursaries (but excluding bursaries to government employees, which are recorded under goods and services), fines

Expenditure

Issued November 2016

Page 27

and penalties paid to households. It also includes compensation for injuries and damages caused by natural disasters or departments if paid to households.

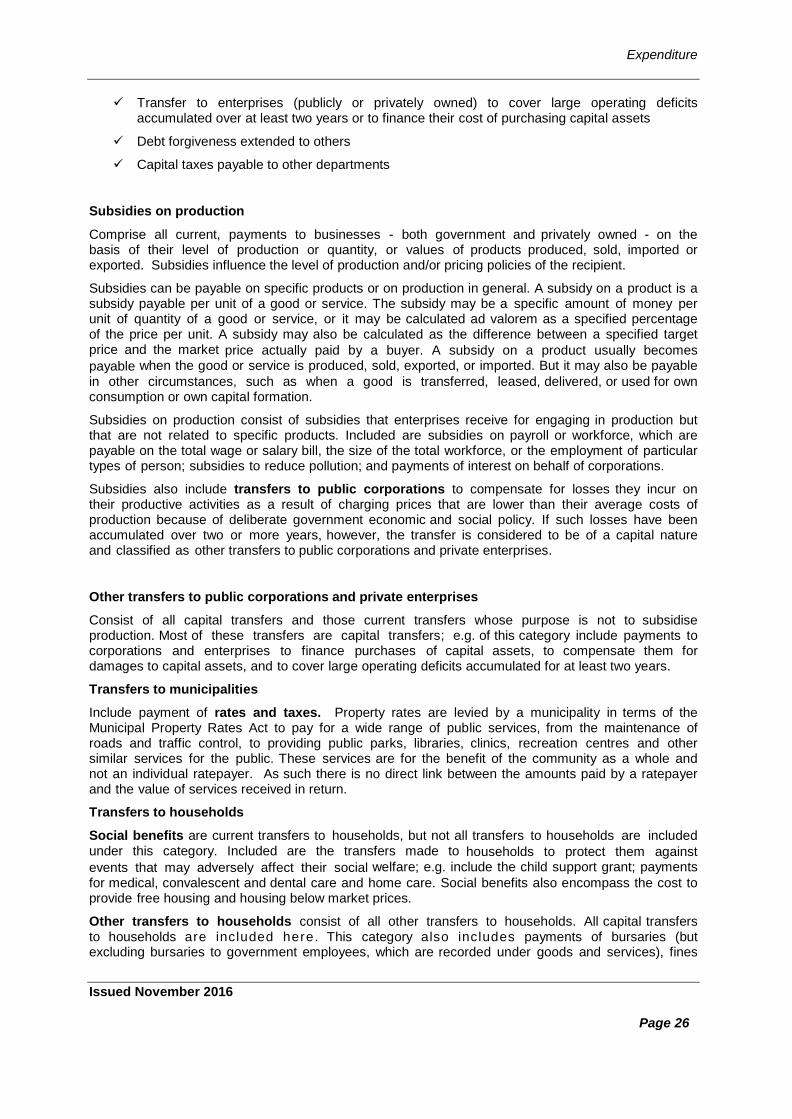

The basic flow and source documents for transfers and subsidies are illustrated below:

Receive

department’s

business plan with

budget etc

Obtain PFMA section 38 assurance

certificate

Complete request for

payment

Payment approved.

Payment advice

sent to department.

Supervisor approves

the request

Households are defined as small groups of persons who share the same living accommodation, pool some or all of their income and wealth, and consume certain types of goods and services.

Expenditure

Issued November 2016 Page 28

6. Disclosures

Refer to the Specimen Annual Financial Statements for the illustrated disclosure requirements.

Classification of expenditure in the financial statements

Expenditure is classified in the department’s budget and subsequently in the statement of financial performance according to the nature of the expense incurred. For example, the salary paid to an employee is classified as compensation of employees. The high level classification structure is prescribed in both the budget and financial reporting frameworks. Departments must exercise care to ensure that the planned and actual expenditure is correctly reflected in both the budget (appropriation Act) and the annual financial statements. Departures are only permitted when an alternative classification is more relevant.

Where a department determines that the classification of the expenditure is inconsistent with the nature thereof (e.g. money paid to the CSIR for a research paper budgeted under transfers and subsidies instead of goods and services), it must first correct the classification in the budget through the adjustment budget or virement process. Where neither option is available the department must reflect the expenditure correctly in the statement of financial performance and appropriation statement regardless of where the funds were appropriated.

As mentioned above, departures may arise albeit in limited circumstances for example, the conditional grant for the construction and provision of low cost housing must be classified as transfers and subsidies (further classified as transfers to households) in full. This was a specific policy position taken by the National Treasury to reflect the ultimate beneficiary of the funds rather than the intermediate use thereof.

Departments must consult the relevant treasury for guidance where there is uncertainty as to the appropriate classification of the expenditure.

Departments are required to disclose the unspent portion of funds transferred to certain beneficiaries in the Transfers and subsidies note. This disclosure only applies to transfers and subsidies made to the categories of transfer payments listed below where the funds are due back to the department at the end of the financial year:

· Provinces and municipalities; and

· Departmental agencies and accounts

The department should also indicate whether these amounts have been received by year-end or before the financial statements were authorised for issue.

In determining the amount to be disclosed, the department should also consider the amount that will be rolled over.

Expenditure

Issued November 2016 Page 29

7. Summary of Key Principles

This chapter provides a basic understanding of the types of expenditure a department is likely to incur and how the department should account for these transactions in its accounting records.

7.1 The types of expenditure the department would incur

The department is likely to incur the following expenditure:

1. Compensation of employees

2. Social contributions

3. Employee benefits

4. Goods and services

5. Interest and rent on land

6. Payments for financial assets

7. Expenditure on capital assets

8. Transfers and subsidies

7.2 Recognition and measurement of expenditure

A department recognises expenditure in the statement of financial performance on the date of payment.

Expenditure is measured at the cash amount paid to settle the expenditure incurred.

Compensation of employees note

The amounts included under the heading pension and medical are the employer’s contributions; any contribution made by the employee is included under basic salary.

The average number of employees should also be disclosed in the note. The number of individuals is determined on a full time equivalent basis at the beginning and the end of a financial year. The numbers reported here must agree with the numbers published elsewhere in the annual report.

Transfers and subsidies note

For this note the department should also complete Annexures to the financial statements which indicate the details of each transfer and subsidy paid.