Embed Size (px)

Citation preview

Accounting From A to ZAdvanced AccountingSt Louis / April 2007

Presenter: Kathleen Graw

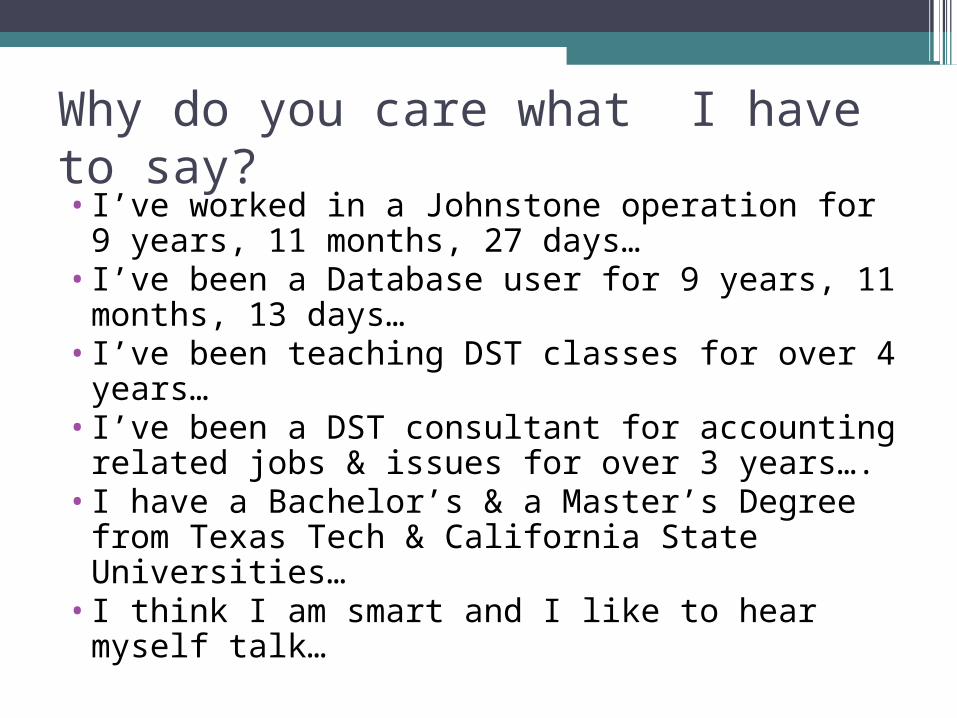

Why do you care what I have to say?• I’ve worked in a Johnstone operation for 9

years, 11 months, 27 days…• I’ve been a Database user for 9 years, 11

months, 13 days…• I’ve been teaching DST classes for over 4

years…• I’ve been a DST consultant for accounting

related jobs & issues for over 3 years….• I have a Bachelor’s & a Master’s Degree from

Texas Tech & California State Universities…• I think I am smart and I like to hear myself

talk…

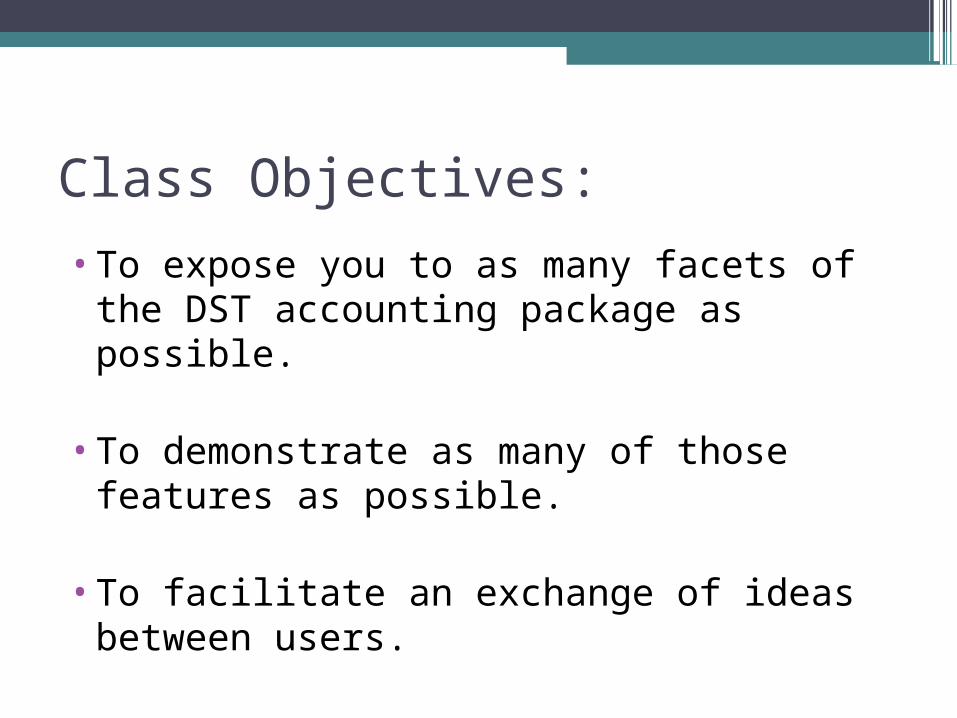

Class Objectives:

•To expose you to as many facets of the DST accounting package as possible.

•To demonstrate as many of those features as possible.

•To facilitate an exchange of ideas between users.

Ground Rules:• PLEASE ask questions – I don’t mind being

interrupted.

• NO question is stupid.

• Please keep questions relevant to the group as a whole.

• “Can it be done” versus “Should it be done”?

• MY way isn’t the ONLY way.

Kathleen’s Silver Rule:

The system is really hard to break – not much that you can do that we can’t undo

with a Journal Entry, Programmer’s Magic or

some fast thinking!

Class Structure:

-We have A LOT of ground to cover and FOUR hours just SEEMS like a long

time.

-Tried to give you as many screenshots as I could to cut down on your note taking.

-One break at halfway point (15 minutes)

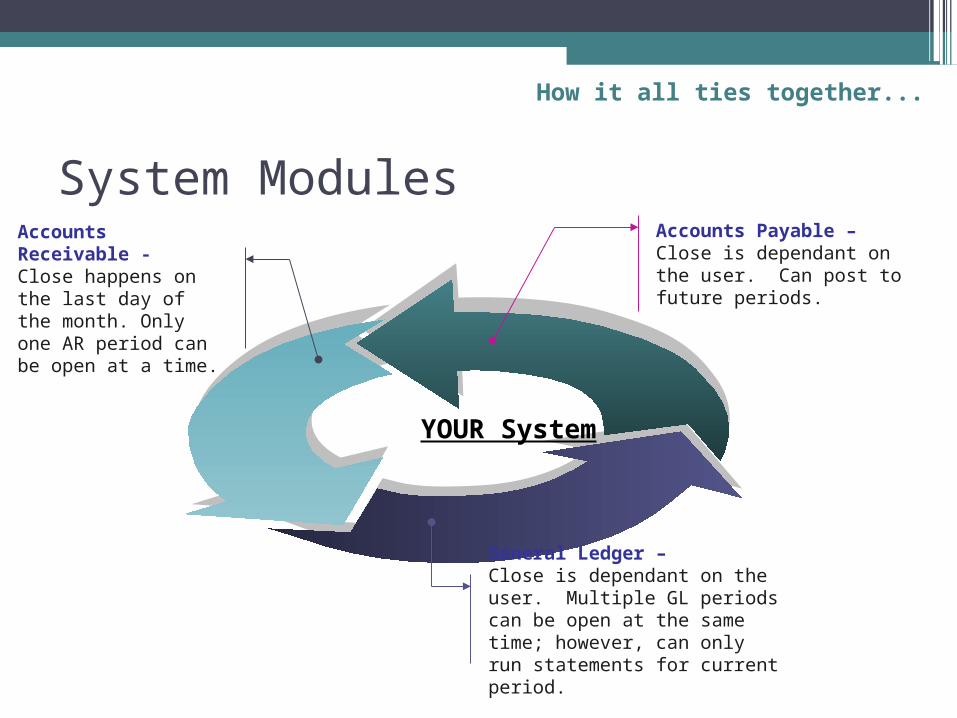

System Modules

YOUR System

Accounts Payable – Close is dependant on the user. Can post to future periods.

General Ledger –Close is dependant on the user. Multiple GL periods can be open at the same time; however, can only run statements for current period.

Accounts Receivable -Close happens on the last day of the month. Only one AR period can be open at a time.

How it all ties together...

Men 13

Helpful tidbits

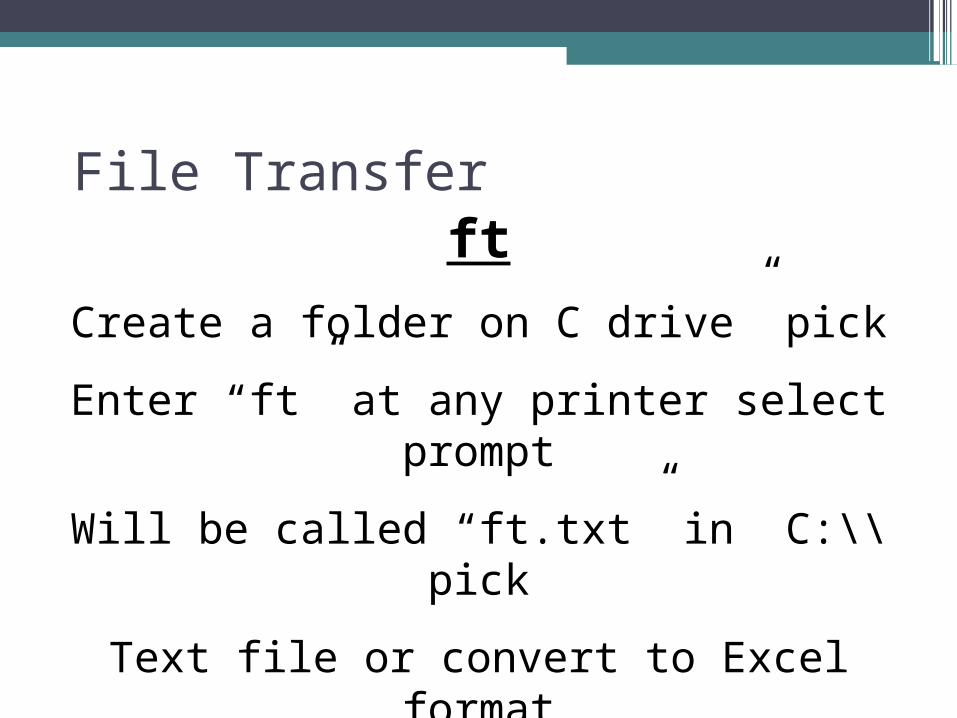

ft

Create a folder on C drive” pick

Enter “ft” at any printer select prompt

Will be called “ft.txt” in C:\\pick

Text file or convert to Excel format

File Transfer

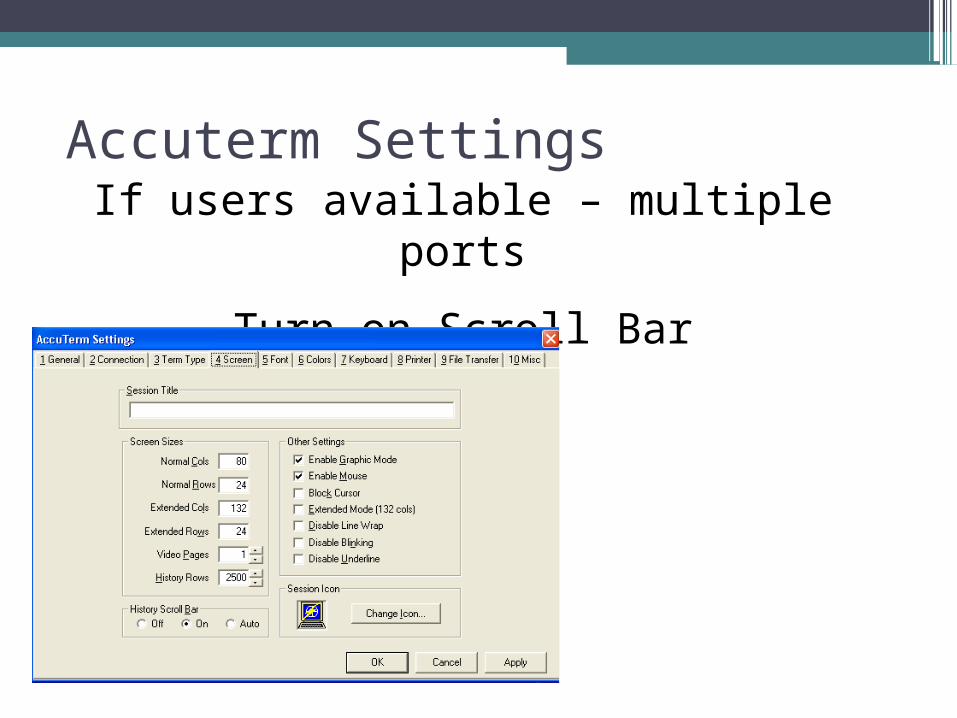

If users available – multiple ports

Turn on Scroll Bar

Accuterm Settings

Service Charges Menu 4.3

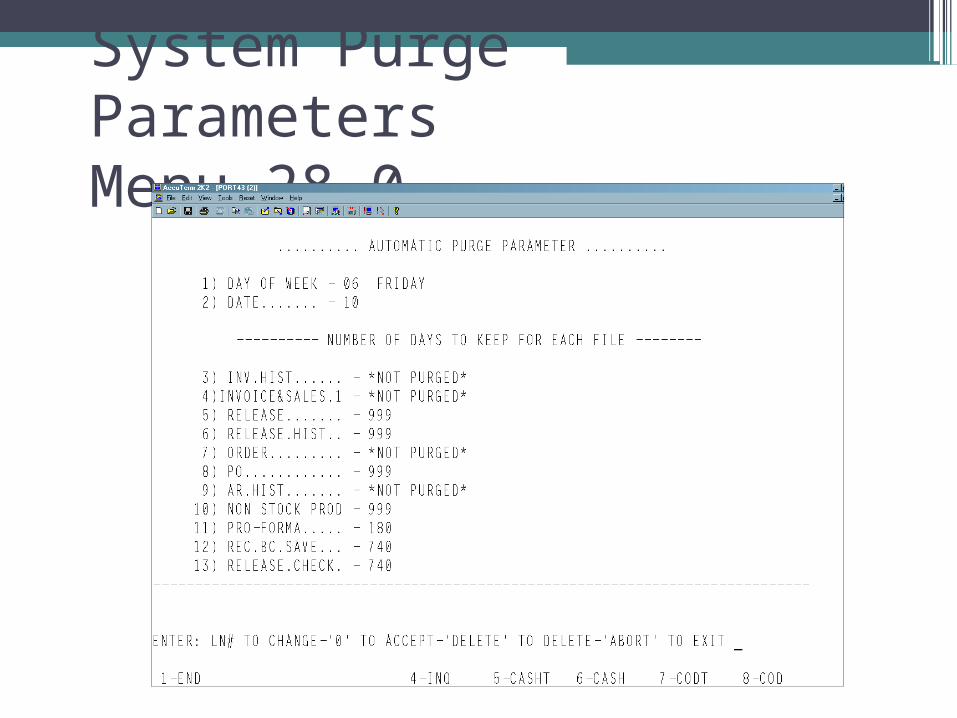

System Purge Parameters Menu 28.0

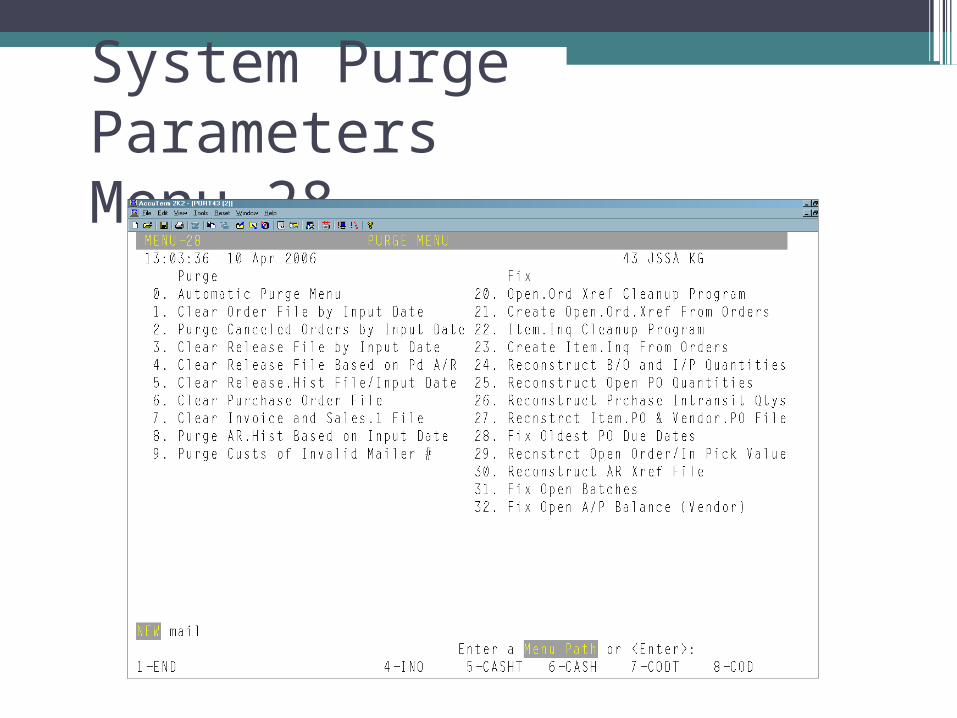

System Purge Parameters Menu 28.0

System Purge Parameters Menu 28.

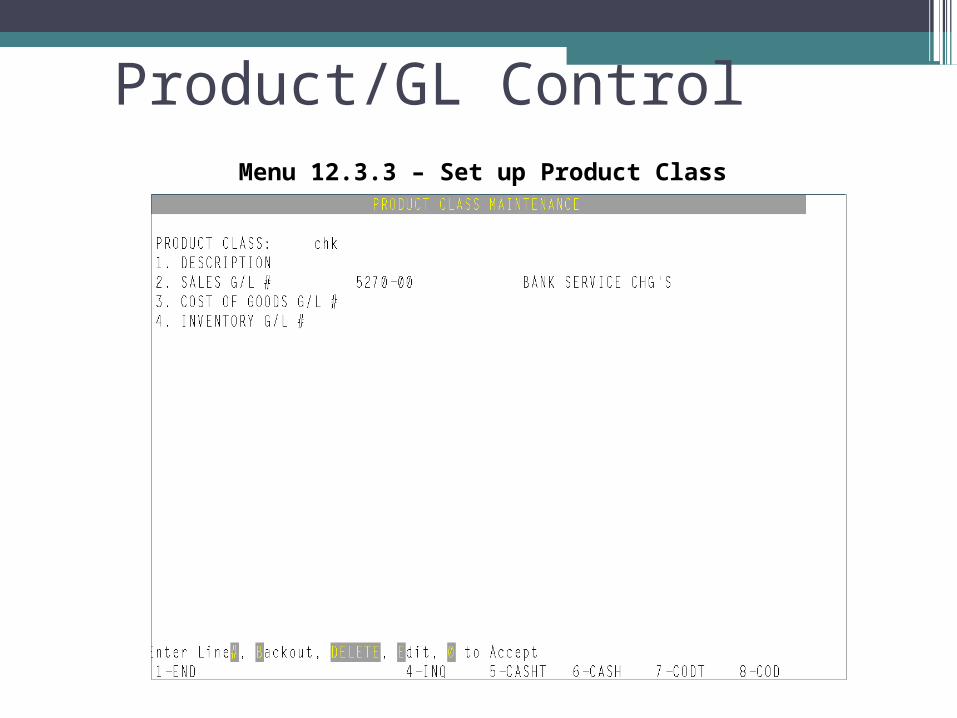

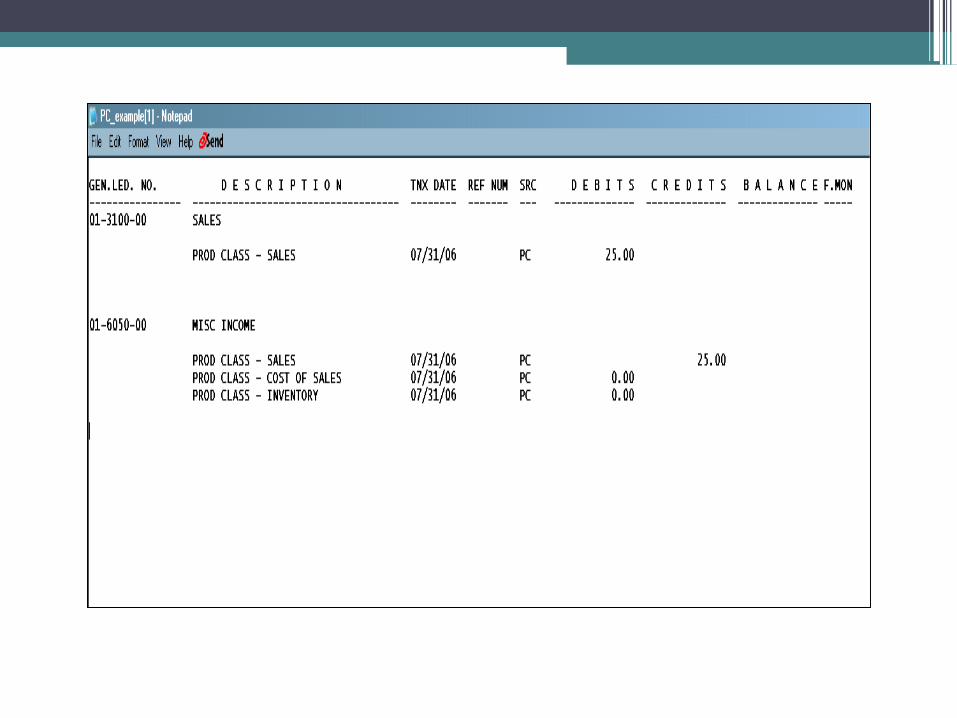

Product/GL ControlMenu 12.3.3 – Set up Product Class

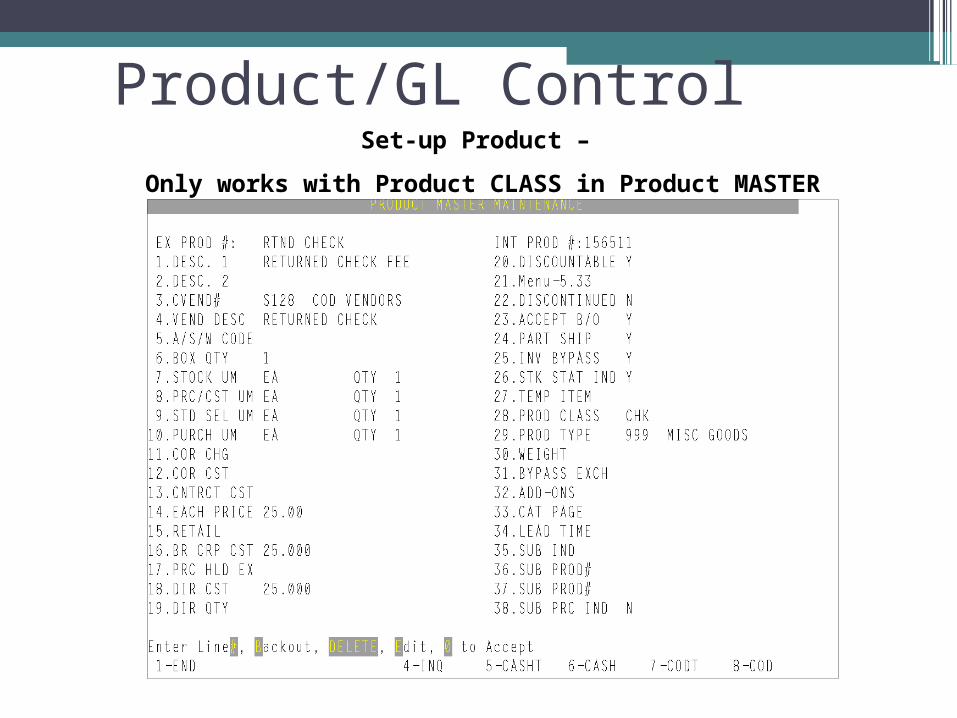

Product/GL ControlSet-up Product –

Only works with Product CLASS in Product MASTER

Men 13

Parameters

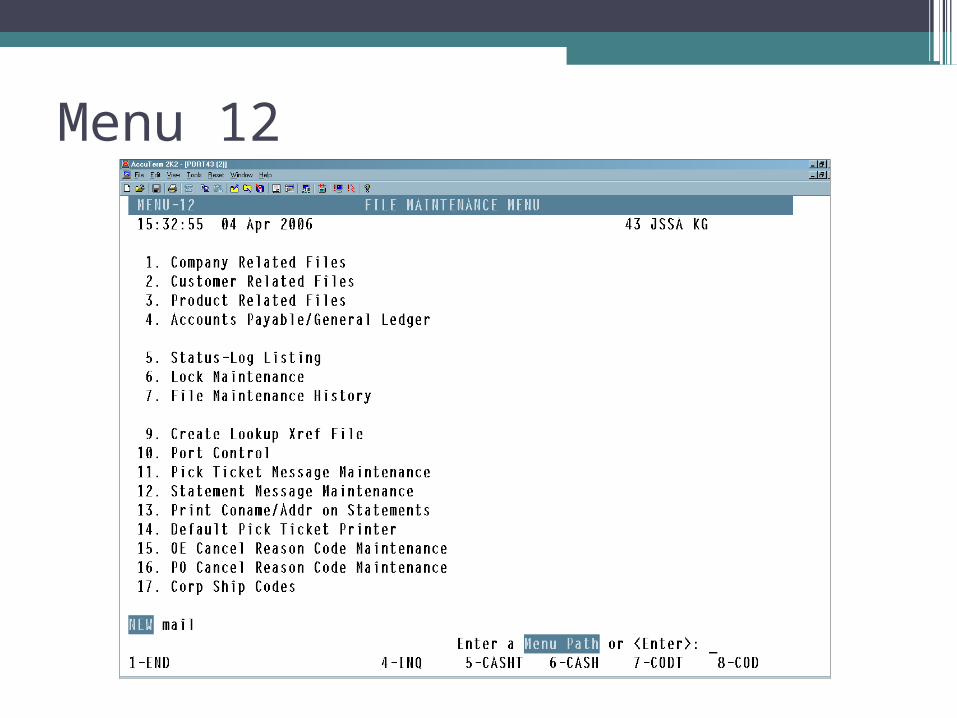

Menu 12

Menu Path Focus

Menu 12

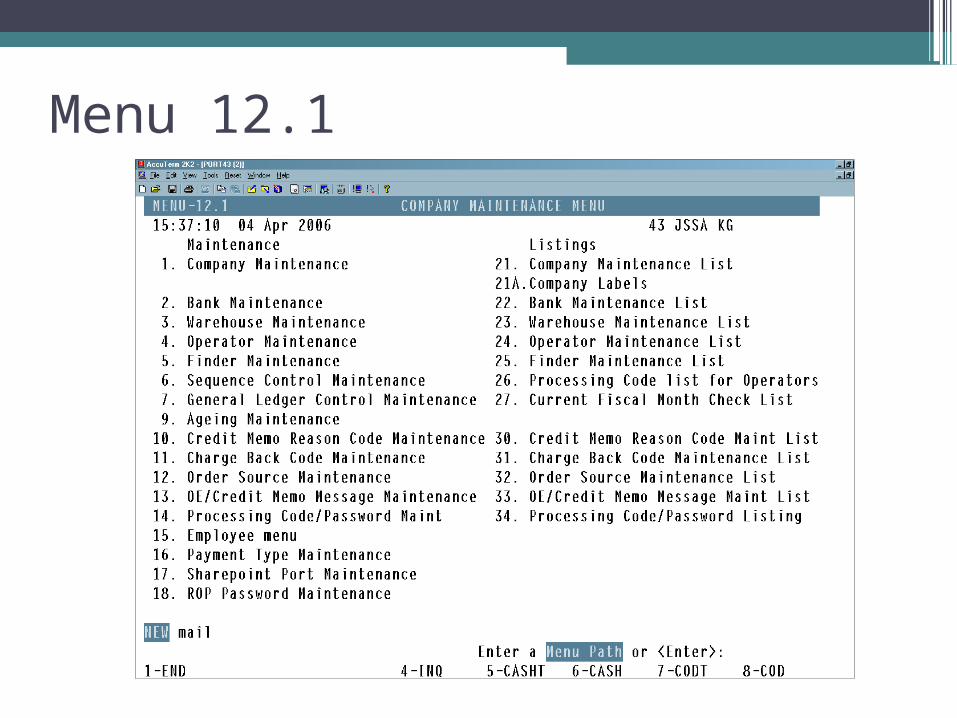

Menu 12.1

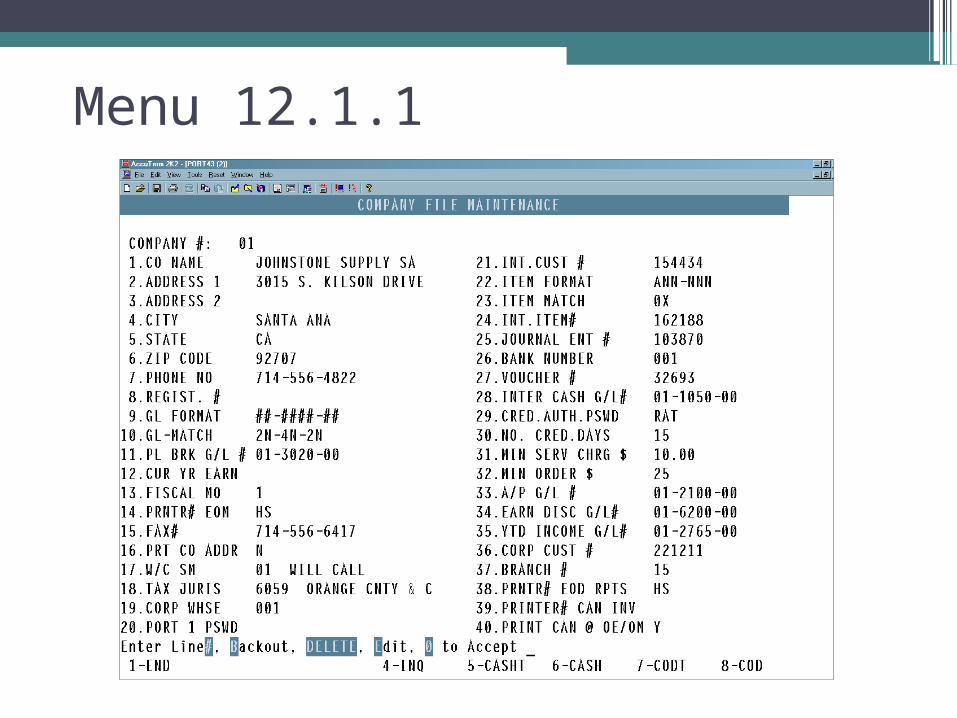

Menu 12.1.1

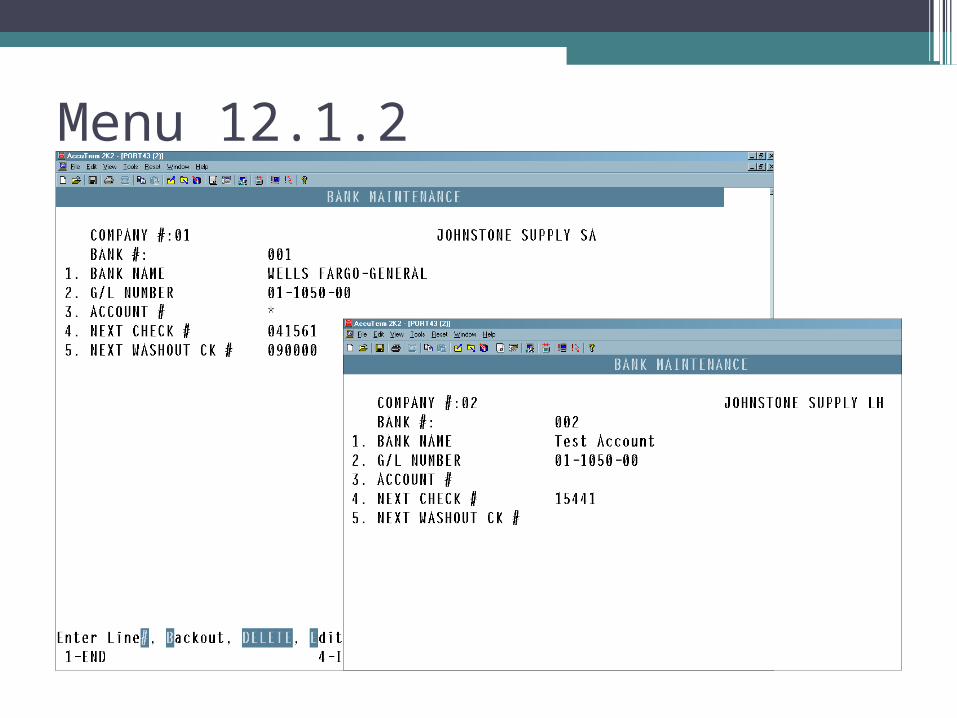

Menu 12.1.2Menu 12.1.2

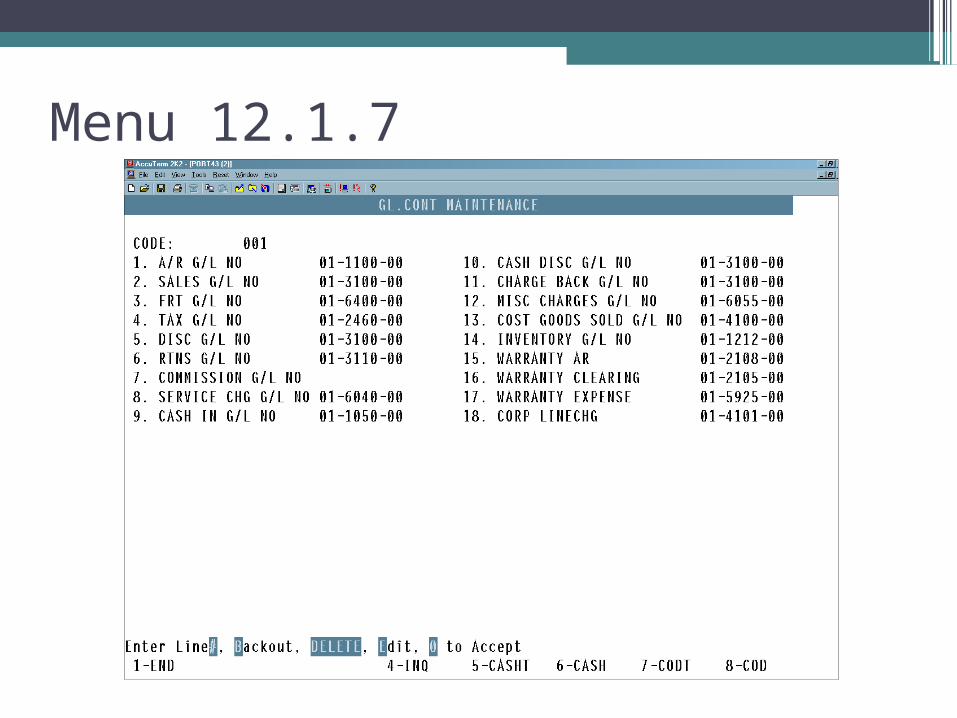

Menu 12.1.7

Nashvill

e, April 2006

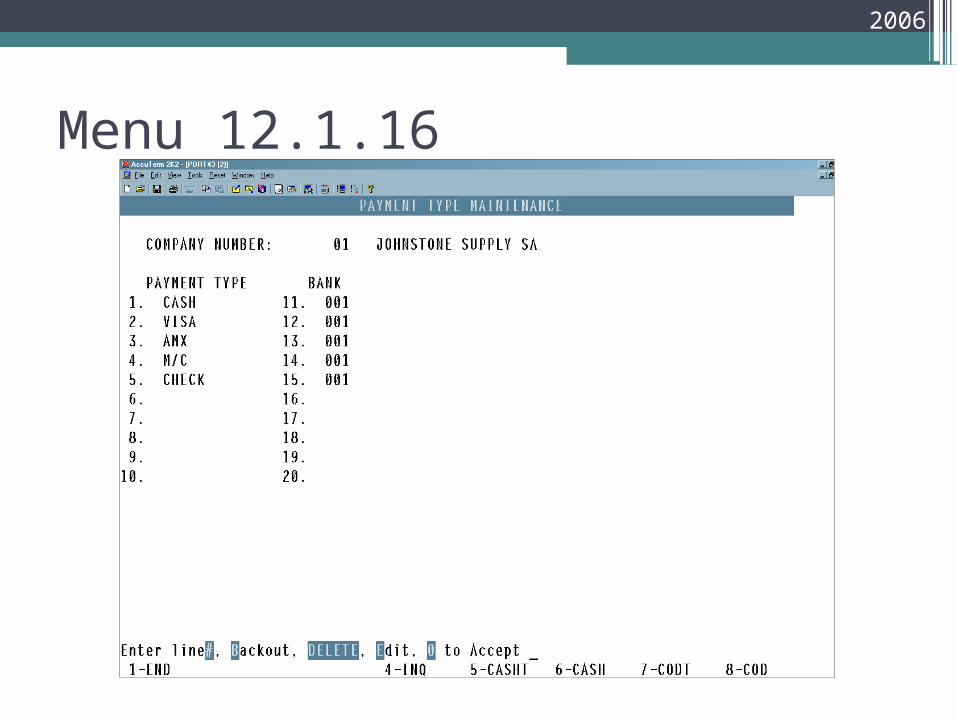

Menu 12.1.16

Menu 12.2

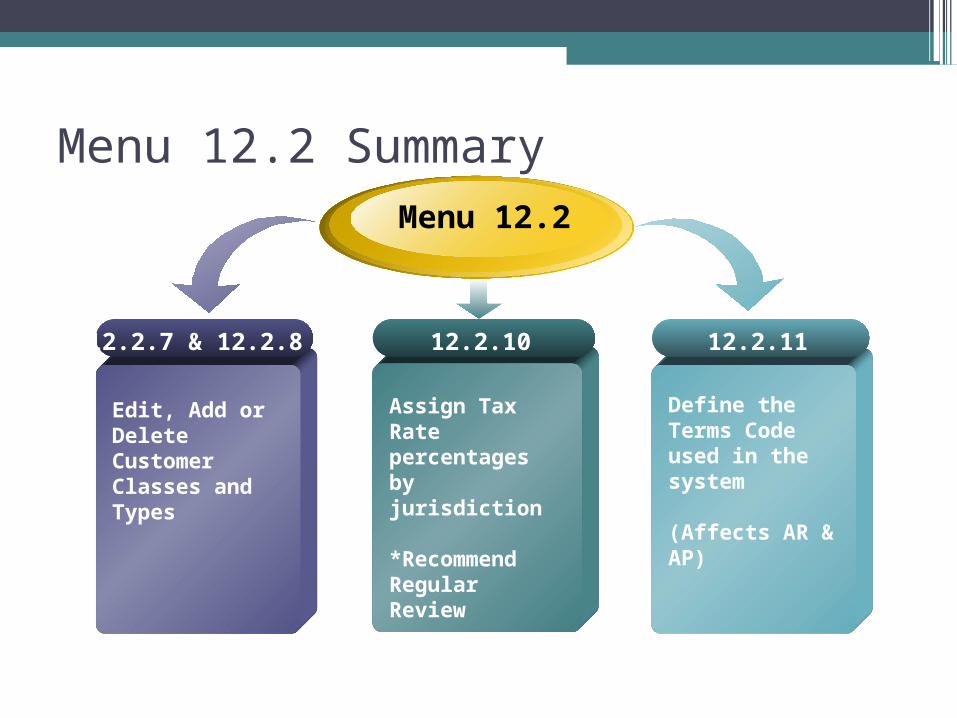

Menu 12.2 Summary

12.2.7 & 12.2.8

Edit, Add or Delete Customer Classes and Types

Assign Tax Rate percentages by jurisdiction

*Recommend Regular Review

12.2.10

Define the Terms Code used in the system

(Affects AR & AP)

12.2.11

Menu 12.2

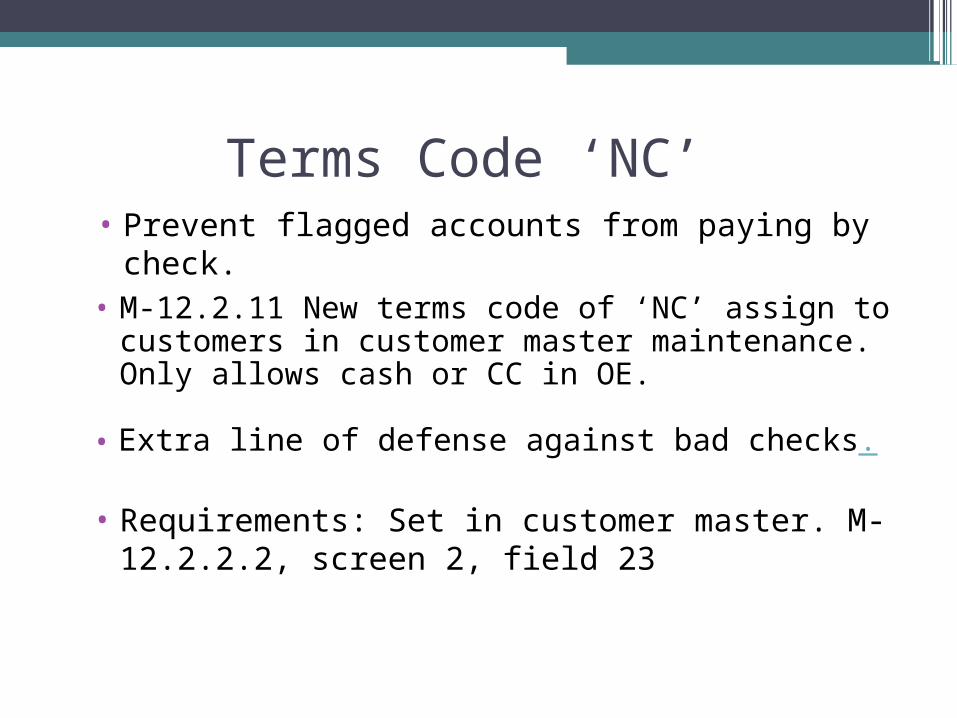

Terms Code ‘NC’

• M-12.2.11 New terms code of ‘NC’ assign to customers in customer master maintenance. Only allows cash or CC in OE.

• Prevent flagged accounts from paying by check.

• Requirements: Set in customer master. M-12.2.2.2, screen 2, field 23

• Extra line of defense against bad checks.

Neat Trick – 12.2.21

Menu 12.3

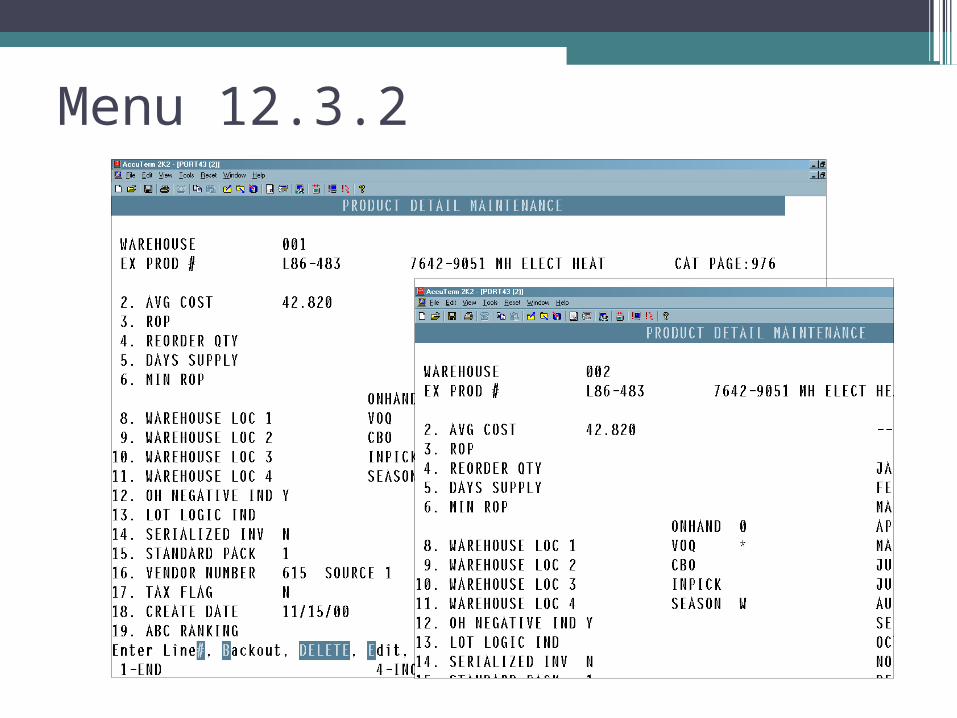

Menu 12.3.2

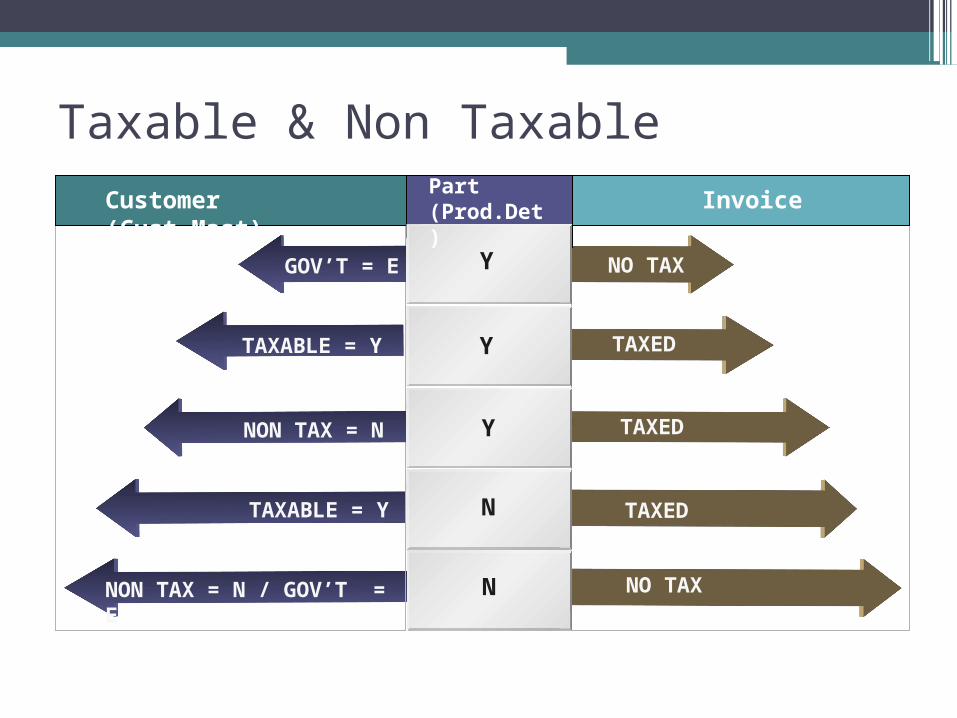

Taxable & Non Taxable

Customer (Cust.Mast)

Invoice

GOV’T = E

TAXABLE = Y

NON TAX = N

TAXABLE = Y

NO TAX

TAXED

TAXED

TAXED

Part (Prod.Det)

Y

Y

Y

N

NNON TAX = N / GOV’T = E

NO TAX

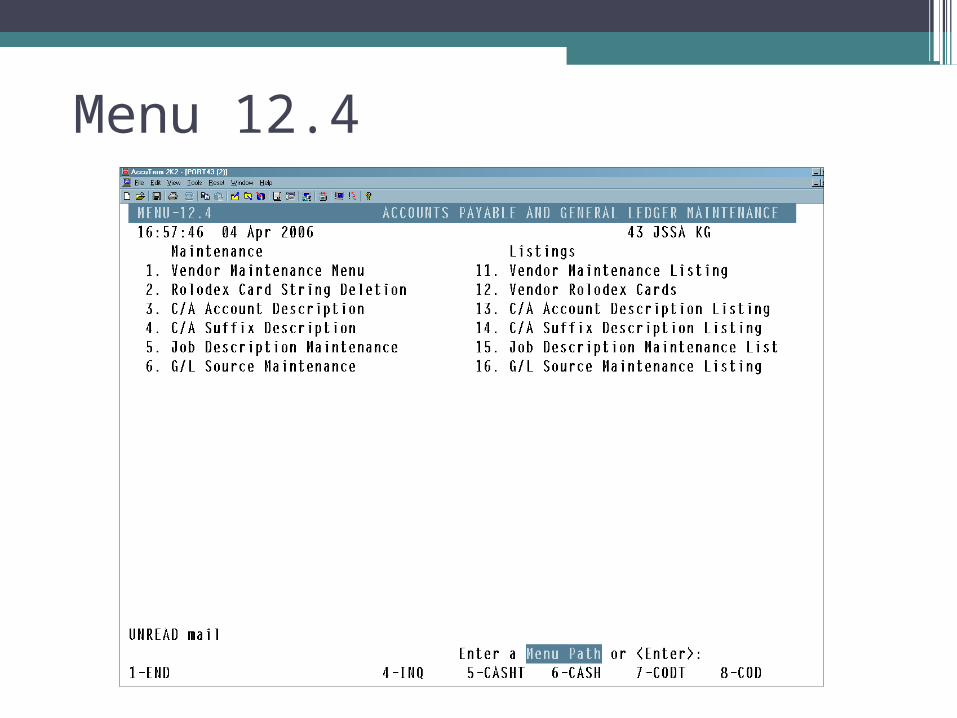

Menu 12.4

Menu 12.4

•Chart of Accounts – ▫12.4.3 – Create /Change GL

Account▫12.4.13 – Print out listing

Menu 12.7 - Demonstration

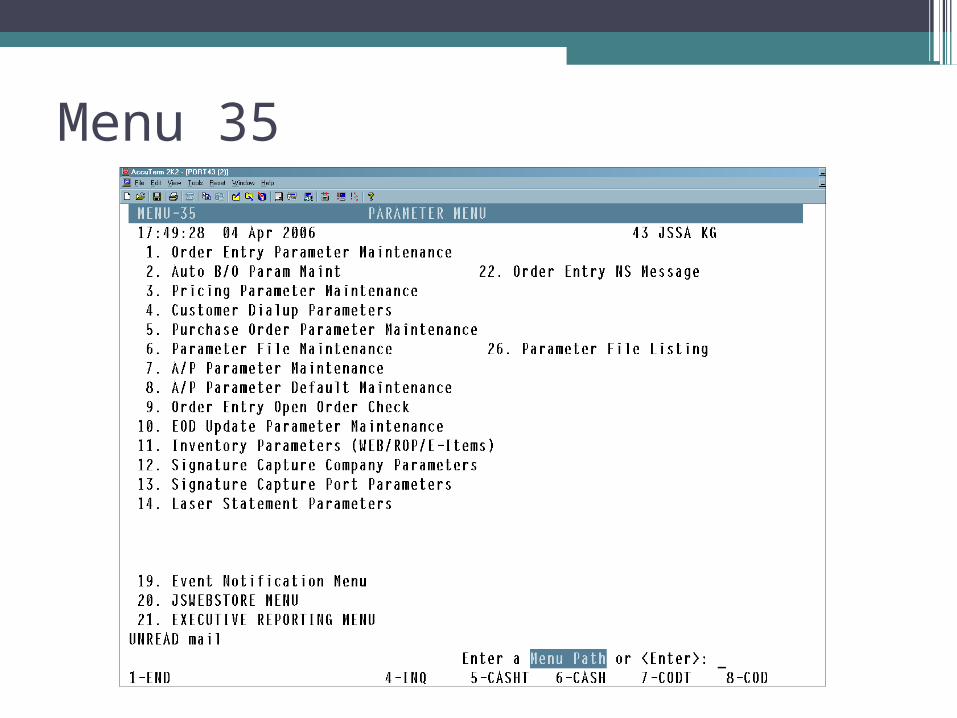

Menu 35

Menu Path Focus

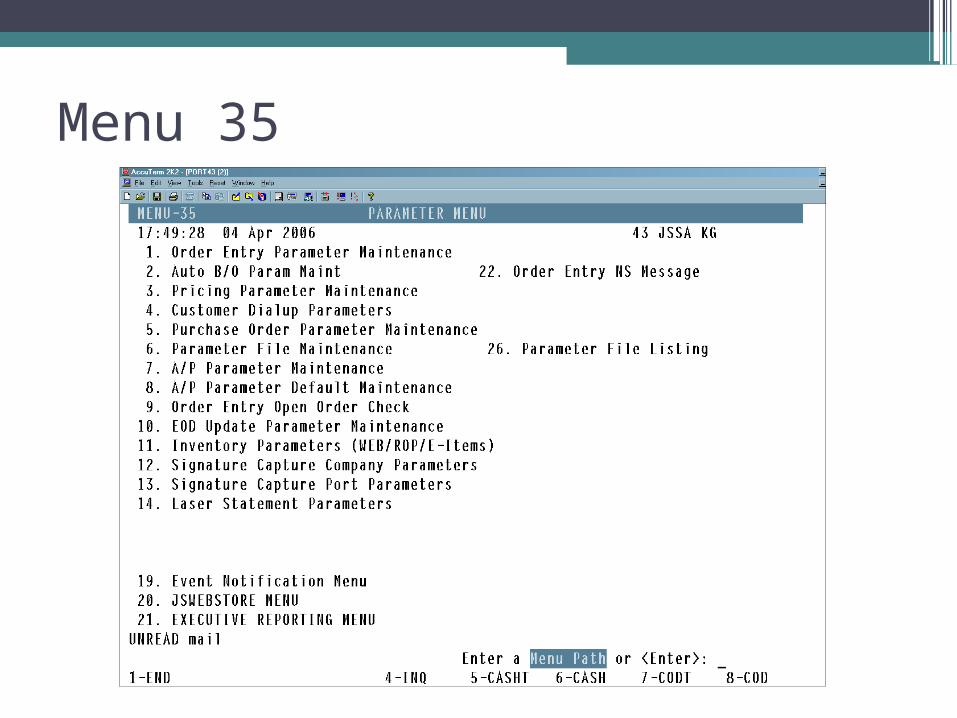

Menu 35

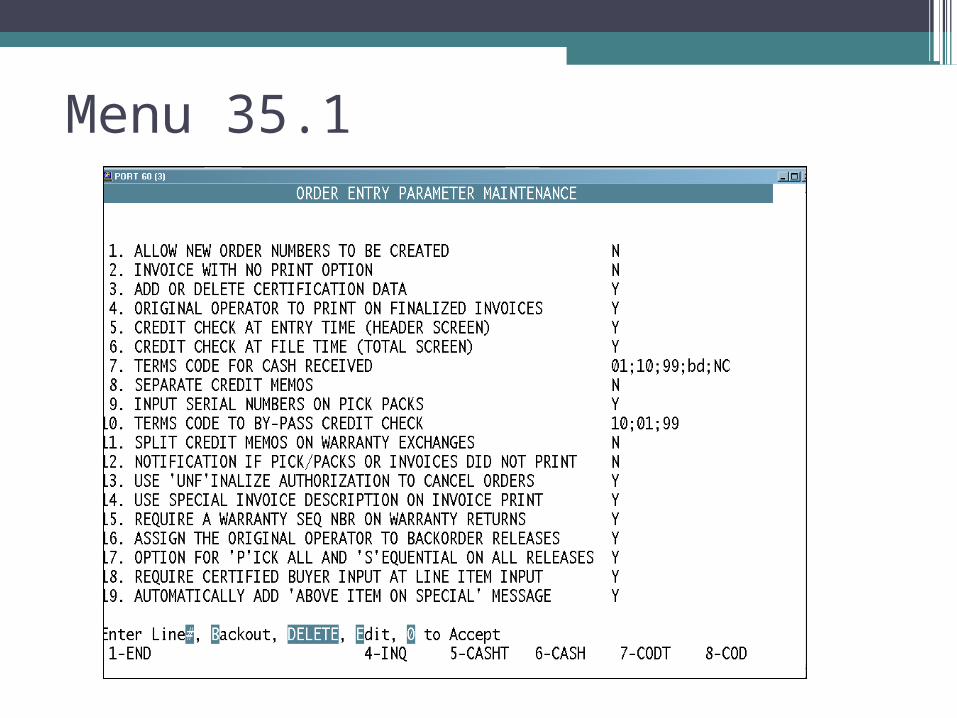

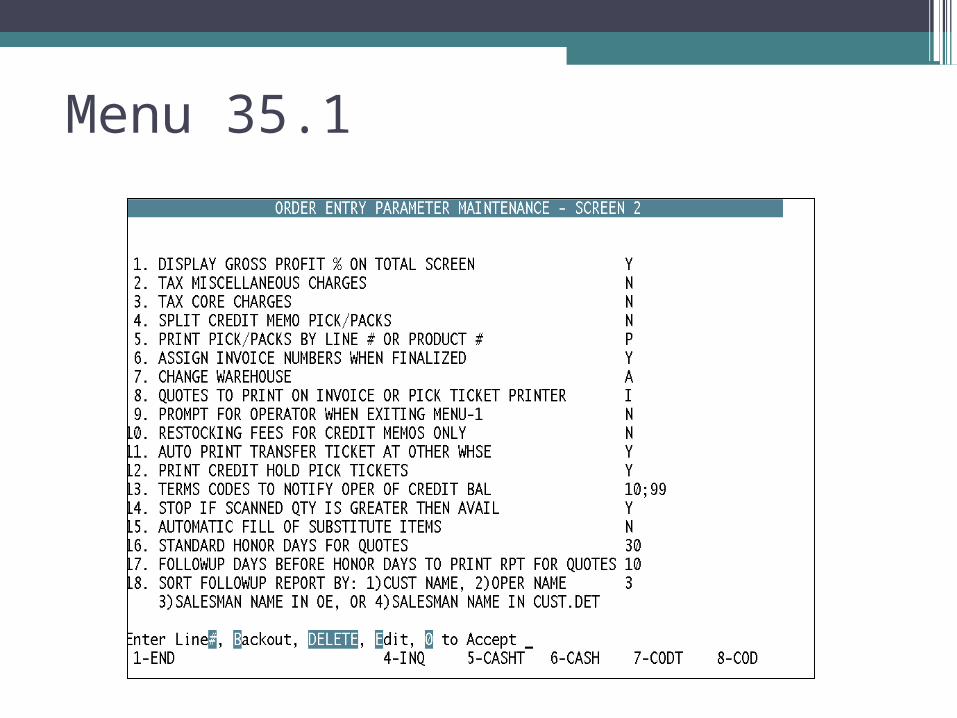

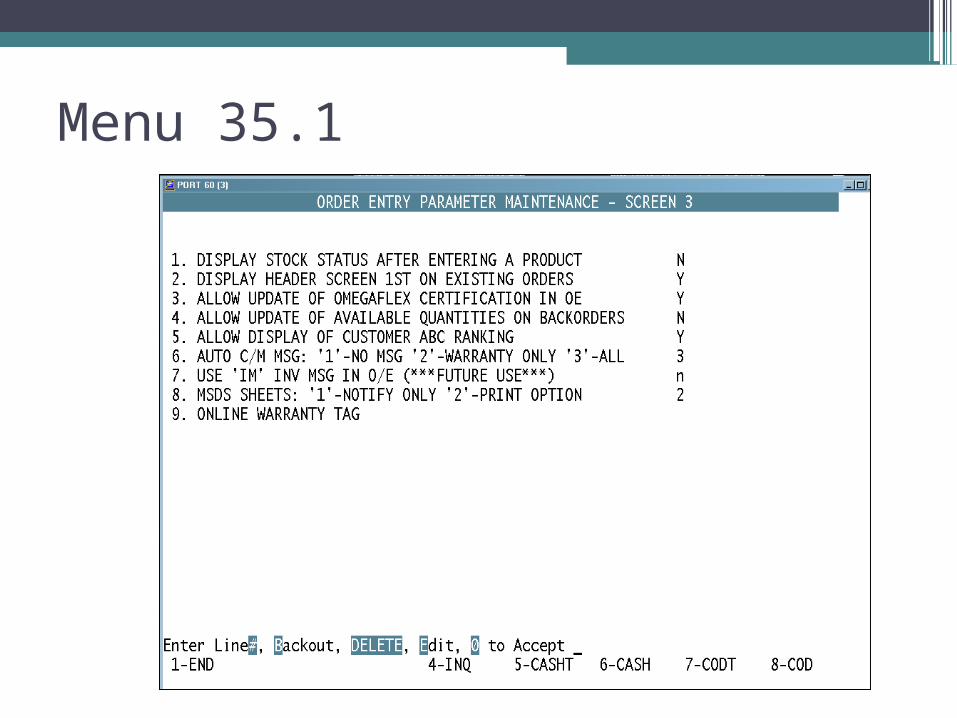

Menu 35.1

Menu 35.1

Menu 35.1

Menu 35

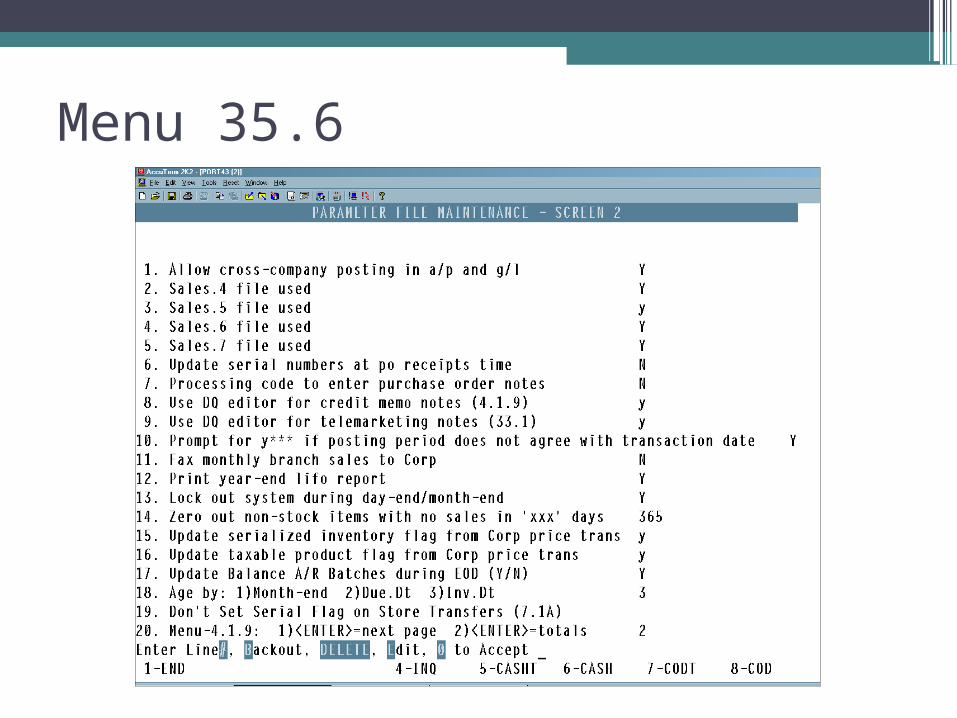

Menu 35.6

Menu 35.6

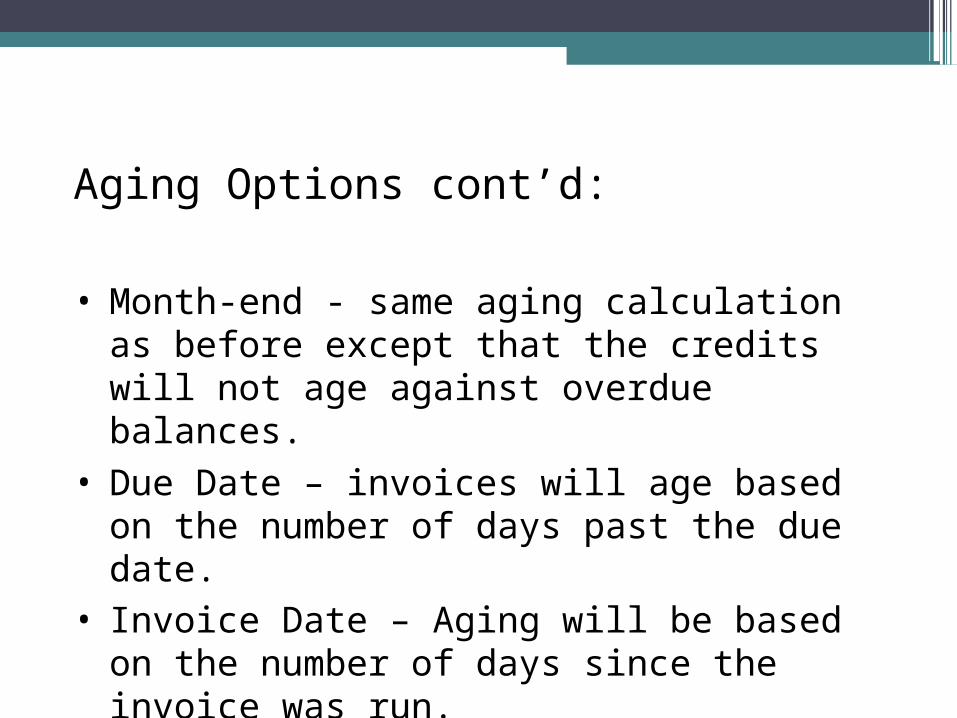

Aging Options

•M-35.6, Screen 2 field 18 Set the parameter, run through eod, see how it works.

• AR Aging options for system to age based on month-end, due date, or invoice date.

• Find the AR aging method that works best for how you do your business.

Aging Options cont’d:

• Month-end - same aging calculation as before except that the credits will not age against overdue balances.

• Due Date – invoices will age based on the number of days past the due date.

• Invoice Date – Aging will be based on the number of days since the invoice was run.

• Secret Option #4

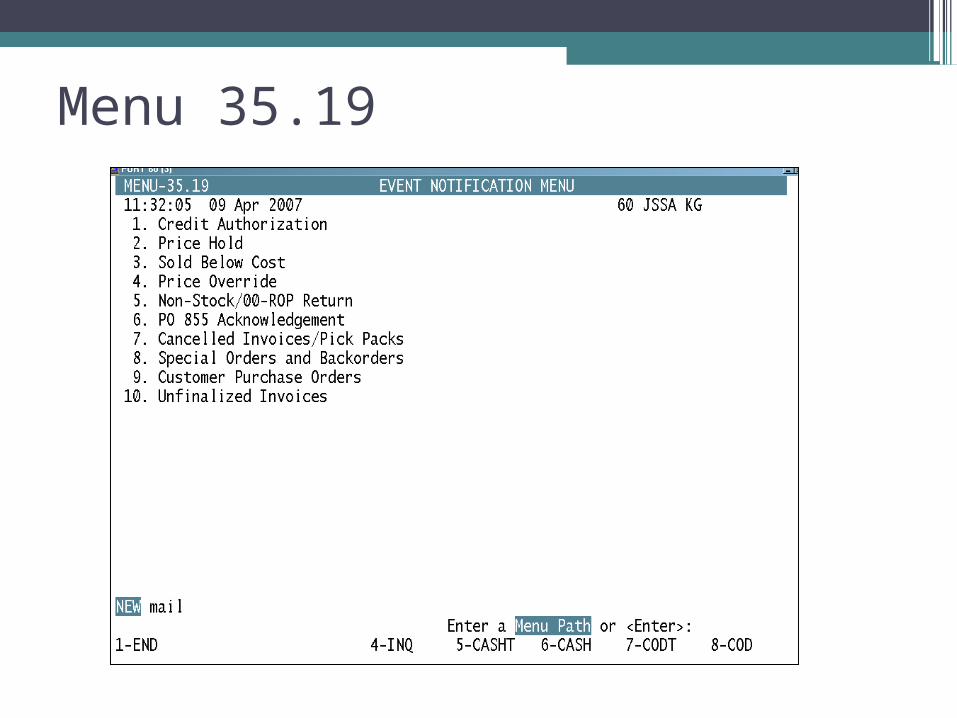

Menu 35.19

Demonstration

Questions?

Menu 13

Menu Path Focus

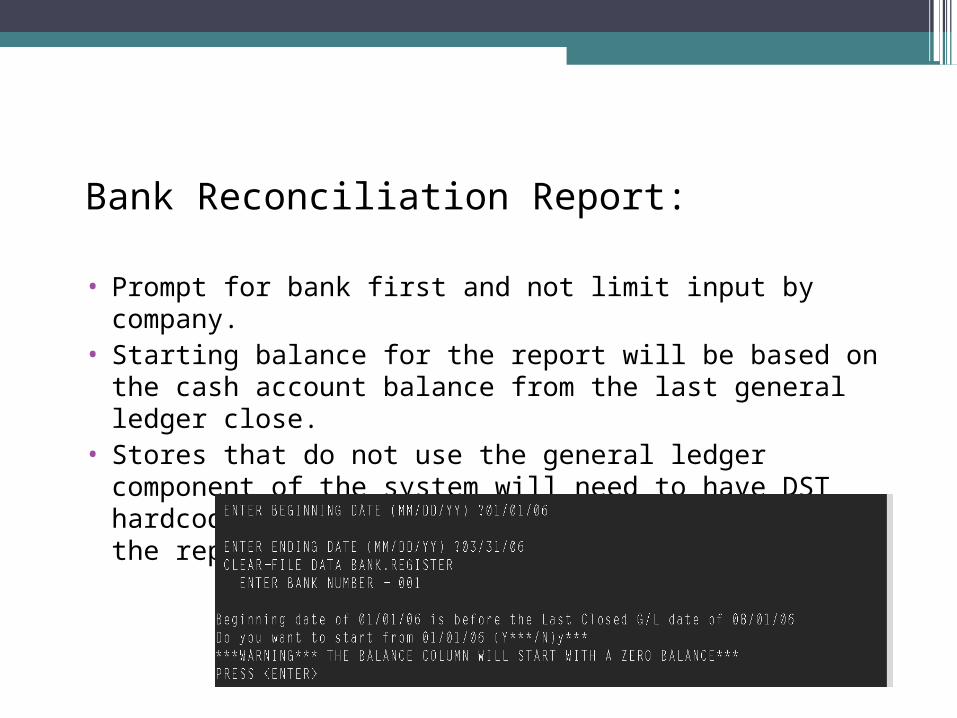

Bank Reconciliation Report:

• Prompt for bank first and not limit input by company.• Starting balance for the report will be based on the cash

account balance from the last general ledger close. • Stores that do not use the general ledger component of

the system will need to have DST hardcode their January 1 balance each year and the report will populate from there.

Demonstration

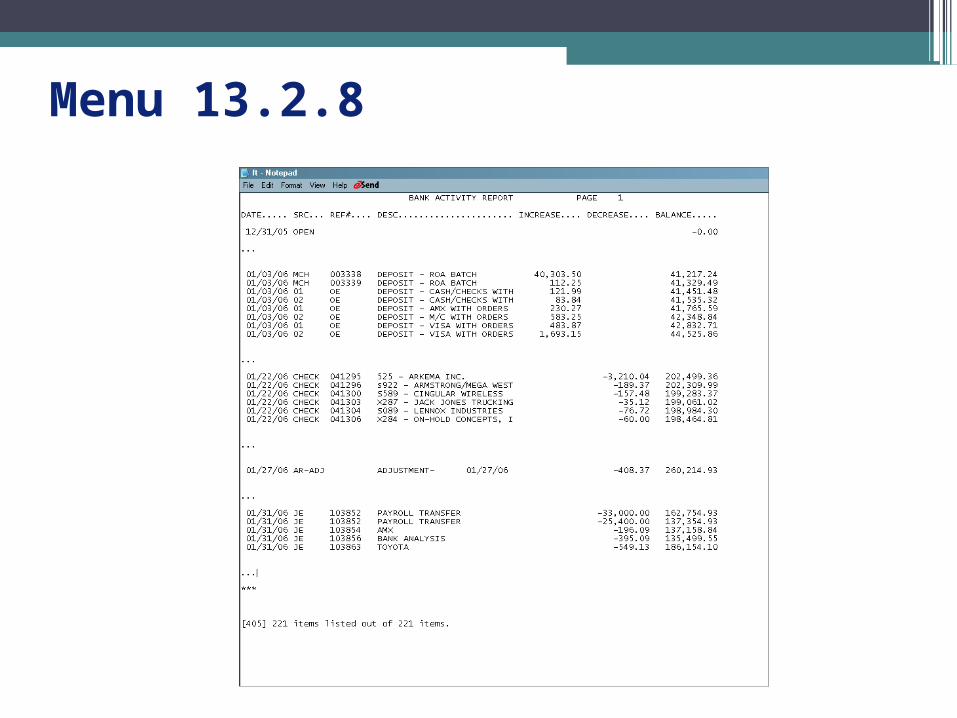

Menu 13.2.8

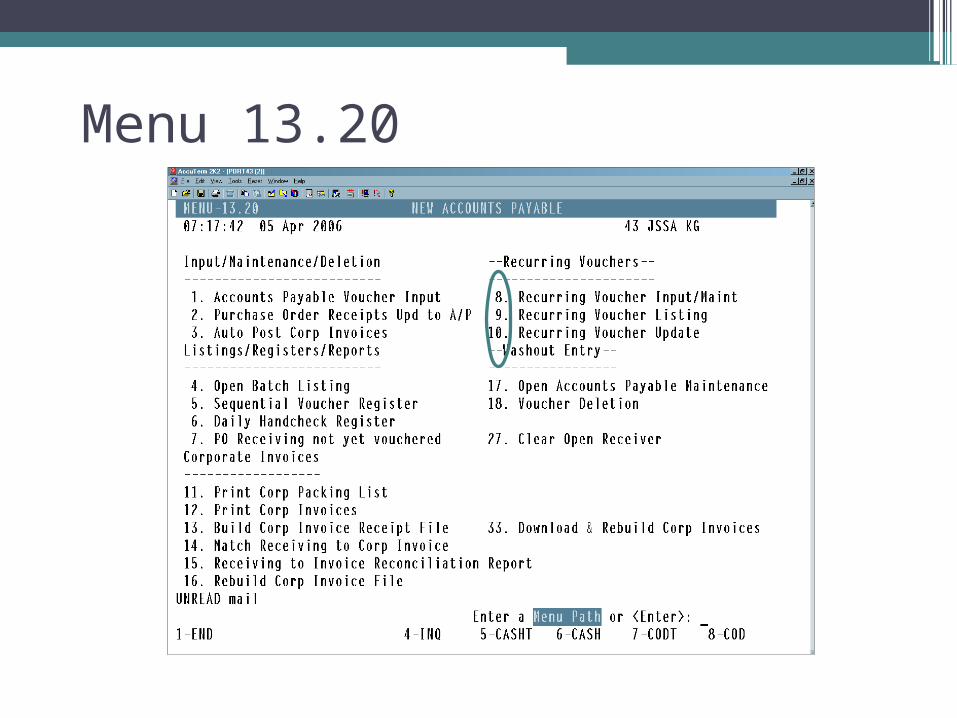

Menu 13.20

Demonstration

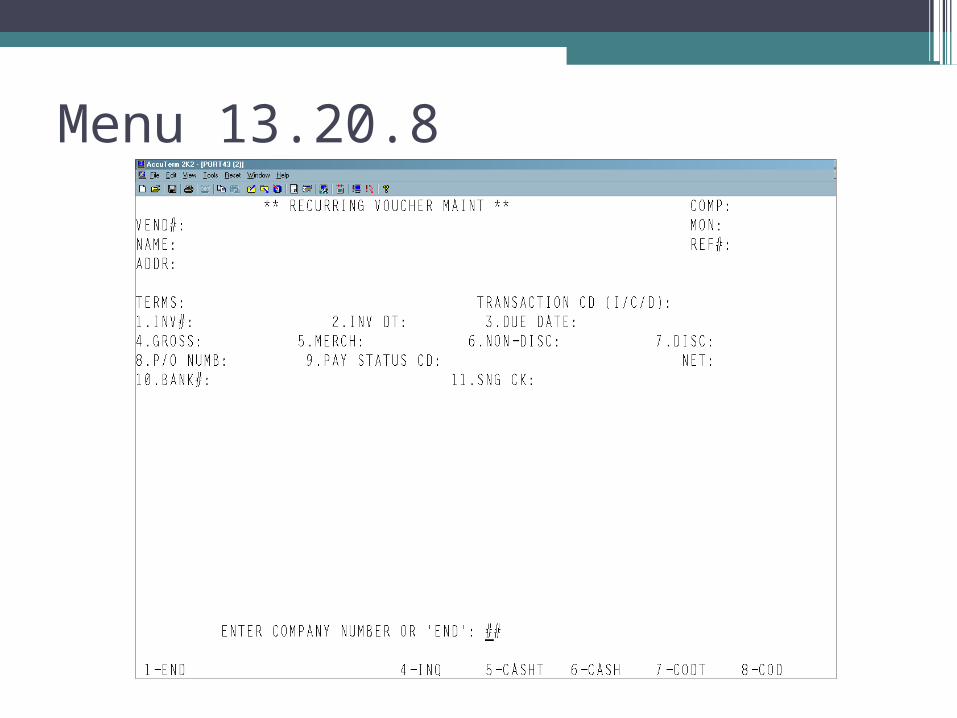

Menu 13.20.8

Reoccurring Vouchers

Enter vouchers in 13.20.8

Listing 13.20.9 (Monthly)

Update 13.20.10 (Monthly)

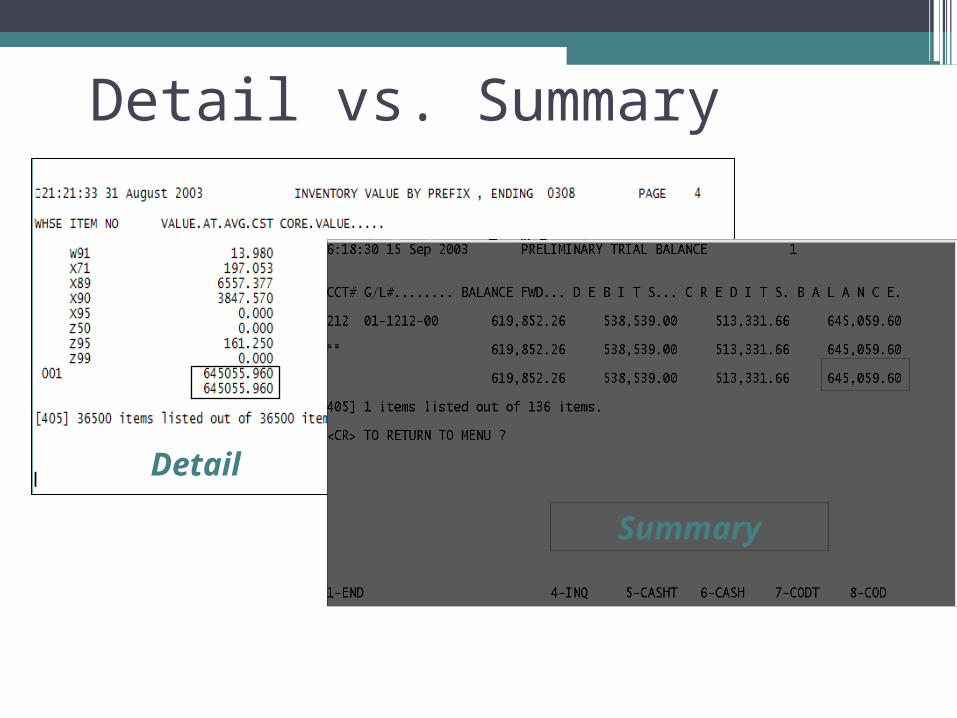

Inventory Valuation

Detail

Summary

Detail vs. Summary

Impact Inventory (Detail)? YES NOStock Adjustments XReceive in Inventory XVoucher/Accounts Payable XMonth End Journal Entries X

Detail

General Ledger Implications

Impact Inventory (Summary)? YES NOStock Adjustments XReceive in Inventory XVoucher/Accounts Payable XMonth End Journal Entries X

Summary

General Ledger Implications

How to balance your inventory…

NO easy solution, but it can happen with:

TimeEffort

Attention to detail

Monthly Reconciling

EOM Journal Entries

Average Cost

Pieces to Valuing Inventory

Time & Effort

Potential Problems:

• 1) Product has been received but not yet vouchered into the Accounts Payable system - Inventory value is updated at receiving time (i.e. as soon as the on-hand increases due to a PO receipt). However, the G/L Inventory is not updated until the vendor invoice has been vouchered and the Inventory G/L account debited for the amount of the merchandise received.

• 2) Inventory adjustments have not been properly entered into the General Ledger via a Journal Entry - The Daily Inventory Transaction Audit Report that runs with each Day End lists all inventory adjustments that have been made for the day. These adjustments directly affect the product on-hand quantity and consequently the inventory value. A journal entry must be made to the Inventory G/L account for all inventory adjustments made throughout the month to properly reflect these changes in the General Ledger inventory value.

Potential Problems (cont’d):

• 3) The difference between the PO receipt cost and the vendor-invoiced cost does not agree - It is necessary to properly record any differences between the product cost at PO receiving time and the actual cost invoiced from the vendor.

• 4) Incorrect use of the Warranty System…vendor credits do not match credits issued through the warranty claim - When closing warranty claims, vouchers should be expensed only to the Warranty A/R account. Also, when issuing vendor credits, the actual credit amount from the vendor should be used.

• 5) Incorrect or non-posting of the Inventory Buyback. The Buybacks (rotational or annual) reduces on-hand (and subsequently inventory value). It is therefore necessary to make a journal entry to reflect this change in the G/L inventory value.

Potential Problems (cont’d):

• 6) Incorrect or non-posting of the Physical Inventory variance - The Physical Inventory process updates on-hand (and subsequently inventory value) at the time the inventory is updated. It is therefore necessary to make a journal entry to reflect this change in the G/L inventory value.

• 7) PO Receipts posting of items not carried as inventory - Products such as C99 and Z95 items should have then Inventory Bypass flag set to ‘Y’es to avoid updating their on-hand (and subsequently inventory) values. Also, these items should not be received, as their on-hand value should always remain at zero.

Potential Problems (cont’d):

• 8) Failure to utilize 13.20.2 Purchase Order Receipts Update to A/P to record vendor invoices and cost changes - 13.20.2 is the only supported process by which stores, whose desire is to balance Inventory Value to General Inventory, can ensure that what is being entered into the inventory system via PO receipts posting matches that which is entered into the A/P system and subsequently the General Ledger. Care must be taken to match all PO receipts to vendor invoices, with reconciliation and cost discrepancies entered through the Purchase Order Receipts Update to A/P process (13.20.2).

Average Cost Calculation

Menu 13.20.2

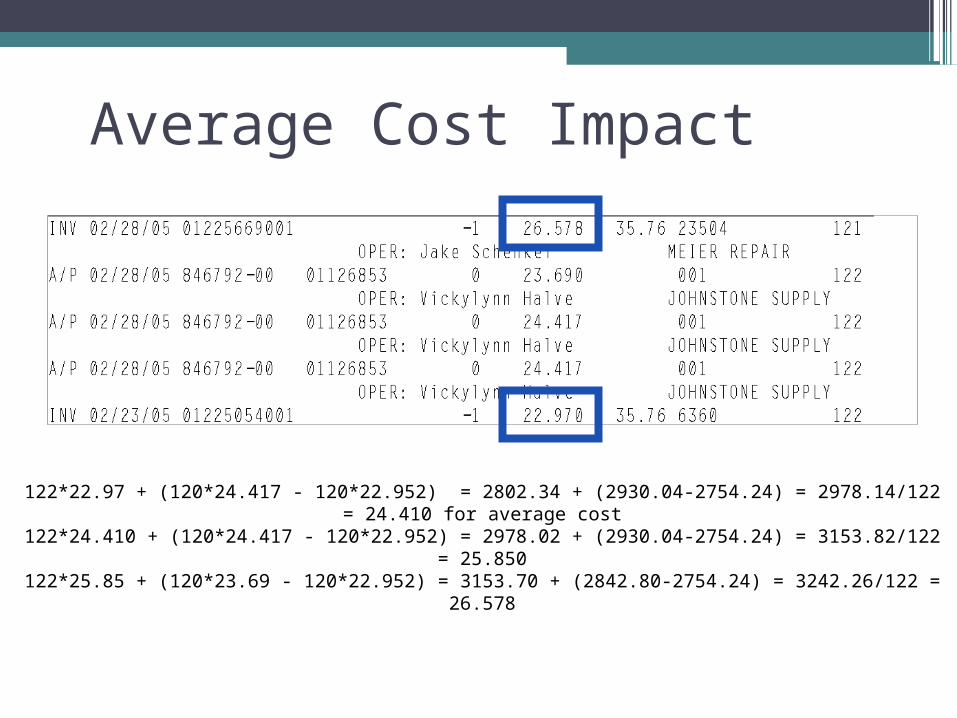

Average Cost Impact

BUT

Average Cost Impact

122*22.97 + (120*24.417 - 120*22.952) = 2802.34 + (2930.04-2754.24) = 2978.14/122 = 24.410 for average cost

122*24.410 + (120*24.417 - 120*22.952) = 2978.02 + (2930.04-2754.24) = 3153.82/122 = 25.850122*25.85 + (120*23.69 - 120*22.952) = 3153.70 + (2842.80-2754.24) = 3242.26/122 = 26.578

Questions?

Inventory Valuation

$$

Quantity on Hand

Purchase Price Variance (PPV)

Average Cost

Calculation

Step OneStep One Step TwoStep Two End ResultEnd Result

QOH x Average

Cost

New Average

Cost

Diff. on Inv v. PO

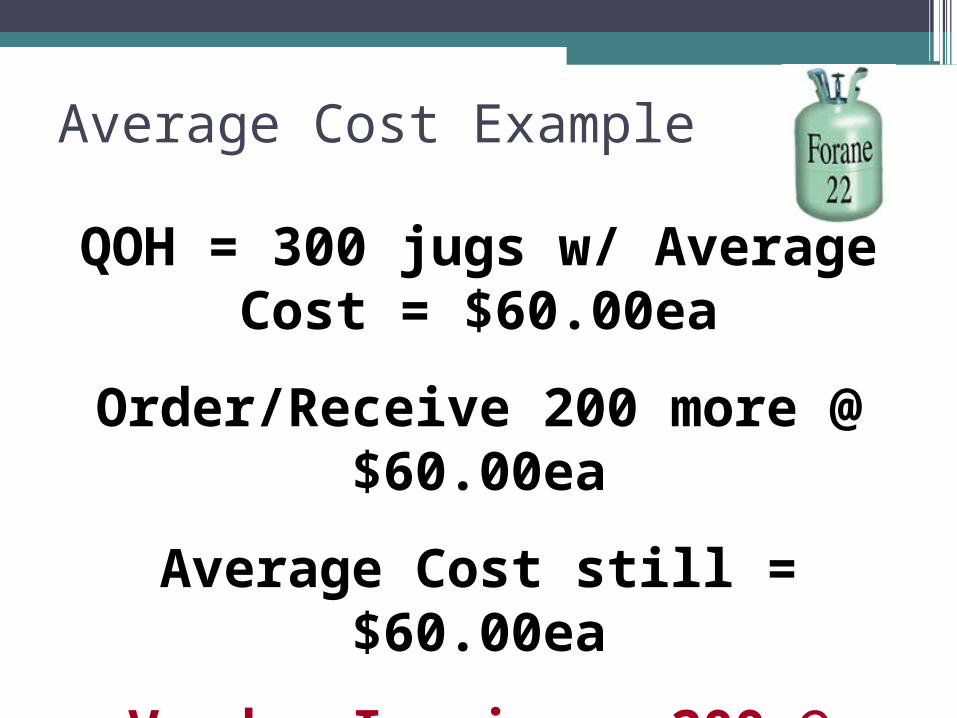

QOH = 300 jugs w/ Average Cost = $60.00ea

Order/Receive 200 more @ $60.00ea

Average Cost still = $60.00ea

Vendor Invoice = 200 @ $70.00ea

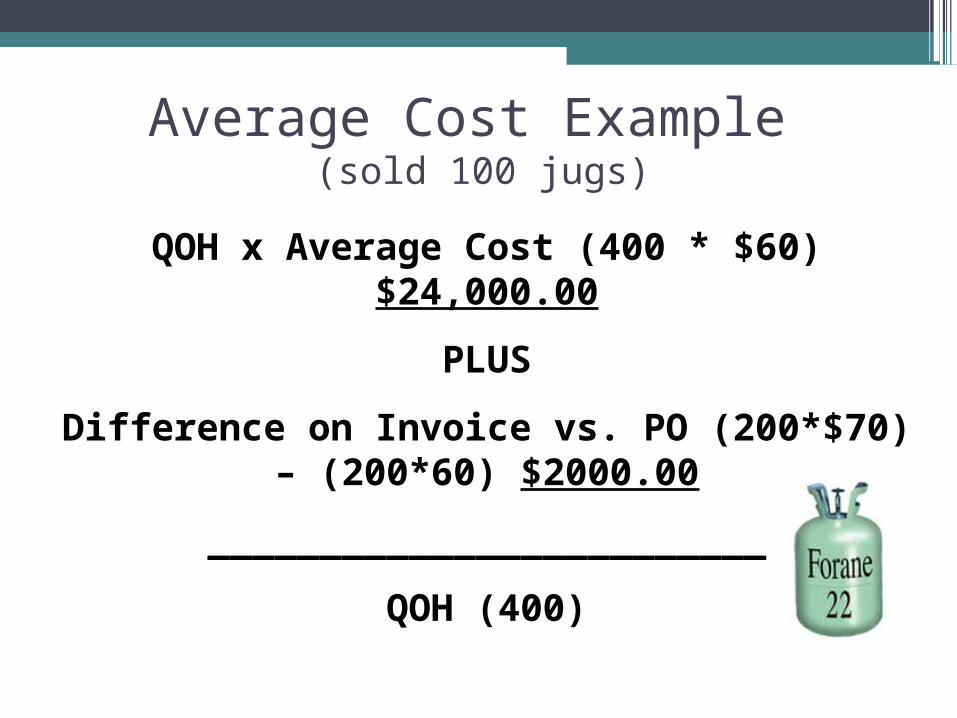

Average Cost Example

QOH x Average Cost (400 * $60) $24,000.00

PLUS

Difference on Invoice vs. PO (200*$70) – (200*60) $2000.00

_________________________

QOH (400)

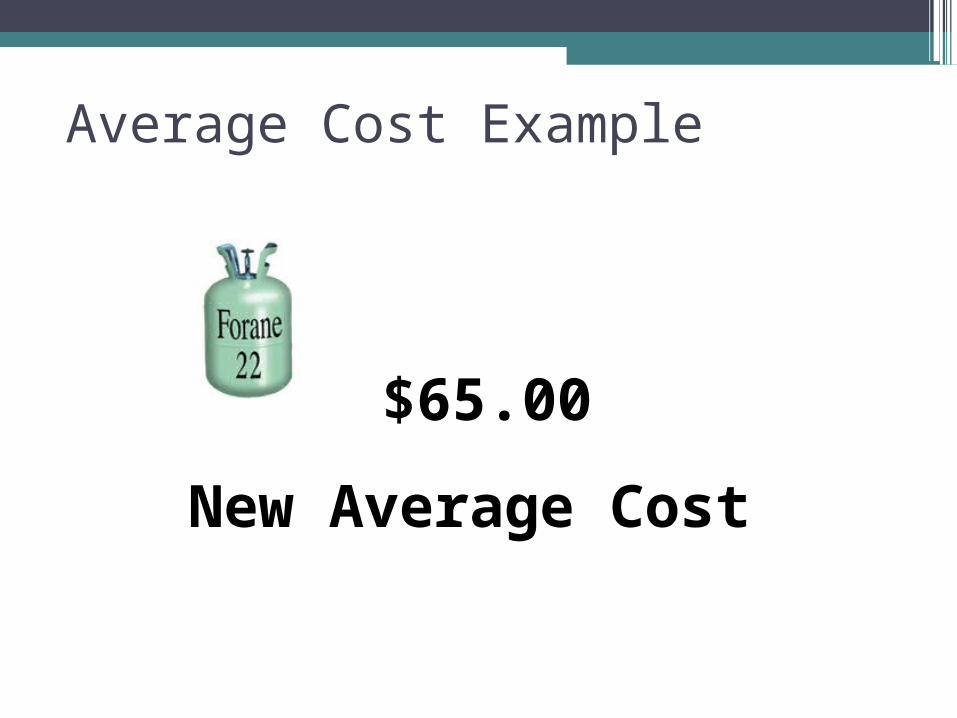

Average Cost Example (sold 100 jugs)

$65.00

New Average Cost

Average Cost Example

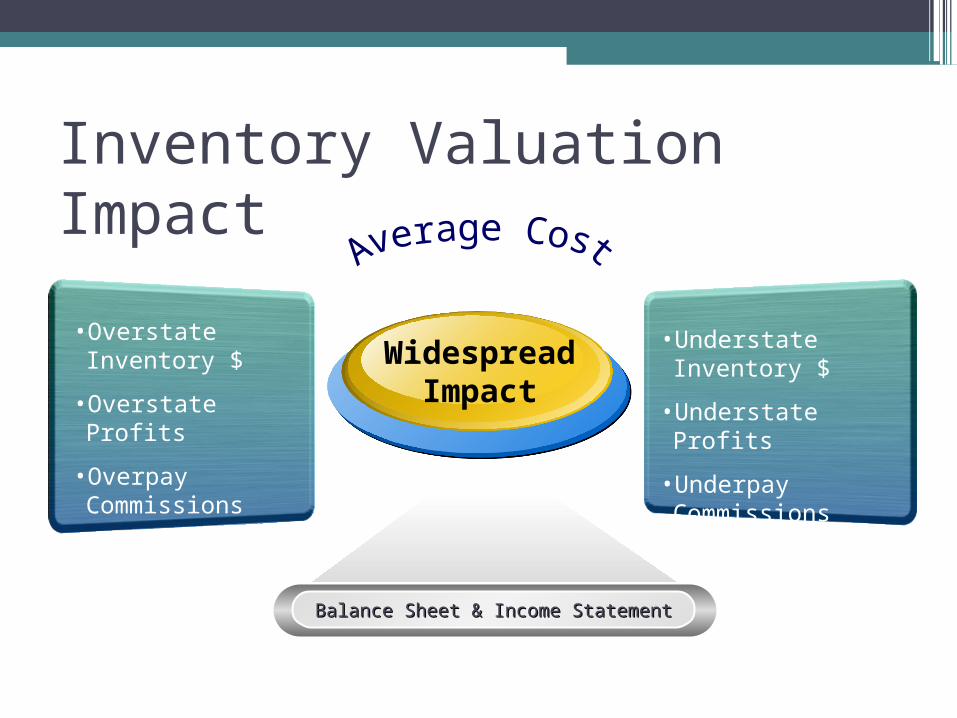

Balance Sheet & Income StatementBalance Sheet & Income Statement

Inventory Valuation Impact

• Overstate Inventory $

• Overstate Profits

• Overpay Commissions

• Understate Inventory $

• Understate Profits

• Underpay Commissions

WidespreadImpact

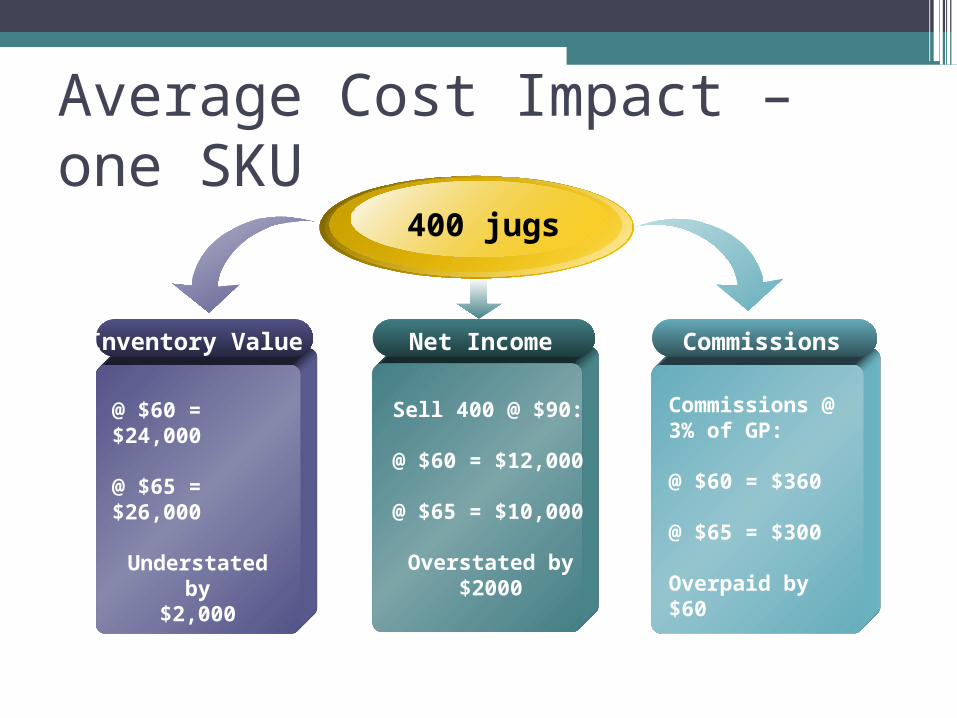

Average Cost Impact – one SKU

Inventory Value

@ $60 = $24,000

@ $65 = $26,000

Understated by$2,000

Sell 400 @ $90:

@ $60 = $12,000

@ $65 = $10,000

Overstated by$2000

Net Income

Commissions @ 3% of GP:

@ $60 = $360

@ $65 = $300

Overpaid by $60

Commissions

400 jugs

Average Cost Impact

Inventory Value

Devalued your Company by understating

your inventory.

Paying taxes on income that you

didn’t really realize.

Net Income

Paid out more to sales people than

you needed to and inaccurately

reduced your bottom line & affected cash

flow.

Commissions

Bad Avg. Cost

Accurate reflection of Gross Profit by month

Accurate reflection of Gross Profit by part

Accurate reflection of Net Income

No large inventory adjustments at year end

Better handle on inventory value and turns

Average Cost reflects true cost

Average Cost Impact

Questions?

EOM Inventory Procedures

Use Menu 13.20.2 and 13.20.3

Run Menu 13.20.7 at month end and use for reversing Journal Entry

Inventory XXXXX Inv. Accr XXXXX

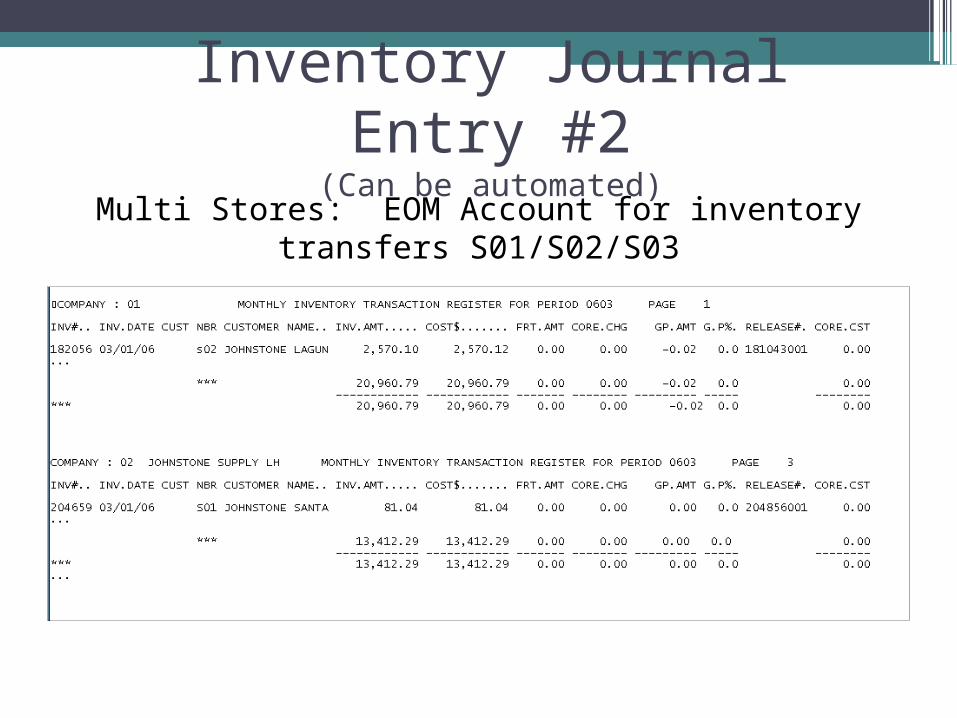

Inventory Journal Entry #1

Multi Stores: EOM Account for inventory transfers S01/S02/S03

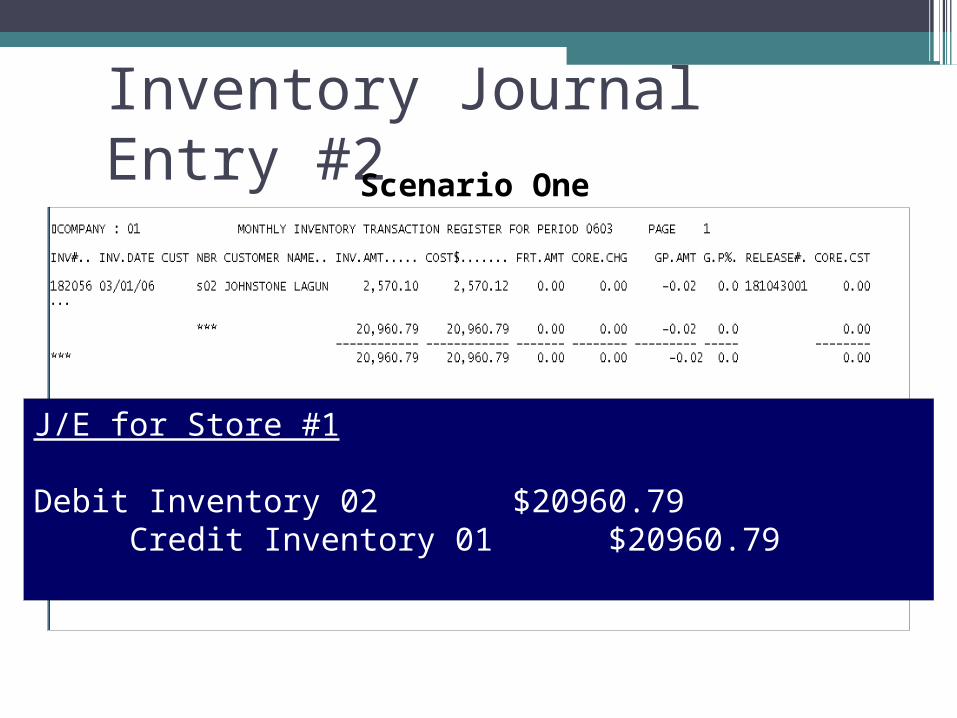

Inventory Journal Entry #2(Can be automated)

J/E for Store #1

Debit Inventory 02 $20960.79 Credit Inventory 01 $20960.79

Inventory Journal Entry #2Scenario One

Inventory Journal Entry #2Scenario Two

J/E for Store #1

Debit Inventory 02 $20960.79 Credit Intercompany 02 $20960.79Debit Intercompany 01 $20960.79 Credit Inventory 01 $20960.79

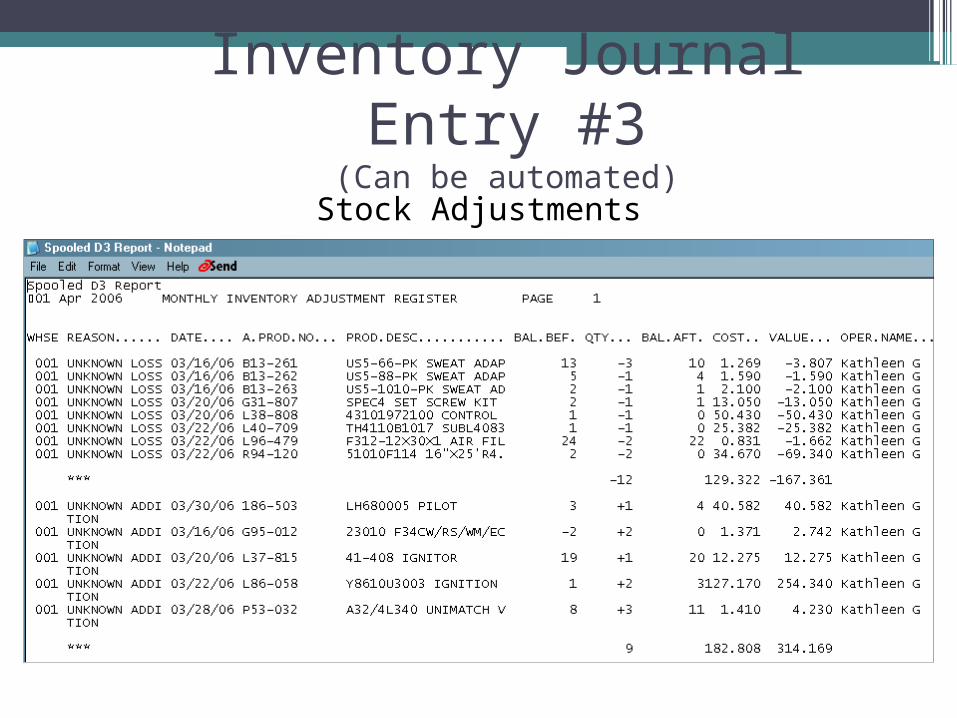

Stock Adjustments

Inventory Journal Entry #3(Can be automated)

Questions?

Men 13

Inventory Processes

Reopening Receivers

If you do it – have to reopen the first & only receiver on the PO

OR

It can throw out your AP/GL Reconciliation

** Doesn’t work with Dropship POs

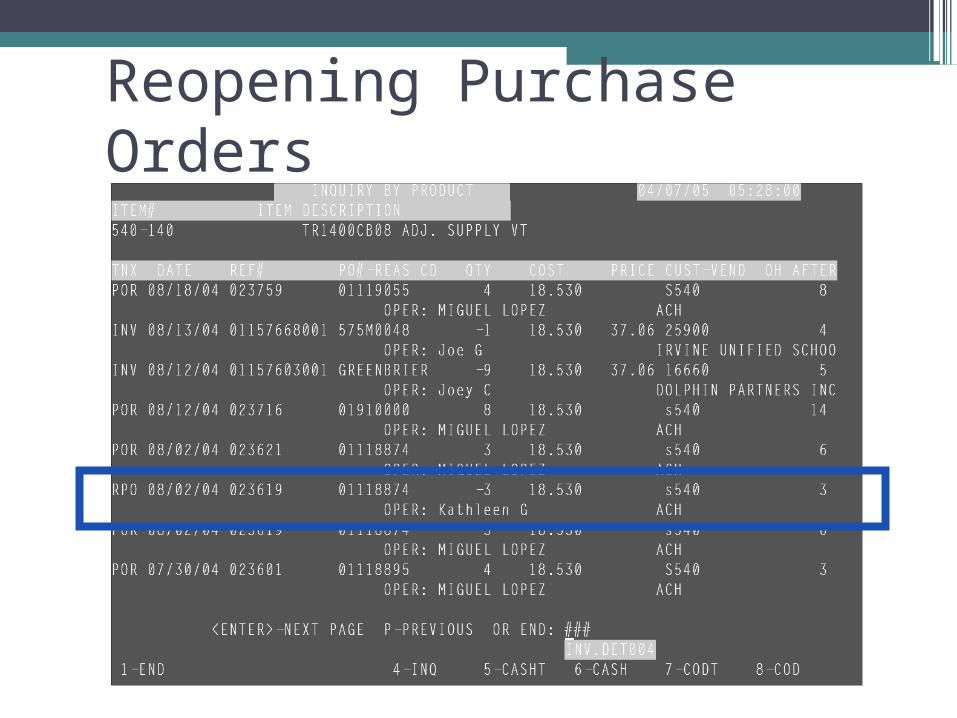

Reopening Purchase Orders

Reopening Purchase Orders

Physical Inventory

Be sure to make note of the final variance amount that you update since you will need to make the journal entry on the books to balance the detail to the summary.

You debit/credit inventory and an income statement account with this variance amount.

Buyback•Corp is set up as customer 00000. Field 17 (Inv.sfer) in 12.2.2.3 is set to "1." This is so that the invoices will not show on the Invoice and Credit Memo Register and will not figure in the Gross Profit Report.

•Menu 19.7a &7b are updated so that these transactions can be seen in the inventory history.

•Also, A/R is not created and the G/L is not automatically updated.

•Since the General Ledger is not automatically updated, you have to do a journal entry to relieve inventory. We credit inventory and debit “buyback expense”. Then when we get the credit in from Corp, we credit buyback expense. The difference left in the account and gives us an idea of what expense we incurred (write off of dead inventory) as a result of the buyback.

Buyback

•The sales analysis files are not updated so they do not show up in sales. This is important since we don't want to pay 1% to Corp on the buyback sales. **An additional note along those same lines: the report that you get off at the end of the day that shows the invoices to customer 0000 at sell price. So using the report, figure out the average cost per invoice by using the sell and the GP figures. This is the number that you want to relieve inventory by (with journal entry).

•There may be multiple invoices for the buyback. It usually doesn't happen on just one invoice. Usually all the invoices for the buyback are generated the same day; however, if not, just make sure to stay in contact with the warehouse so that you know whenever an invoice is generated.

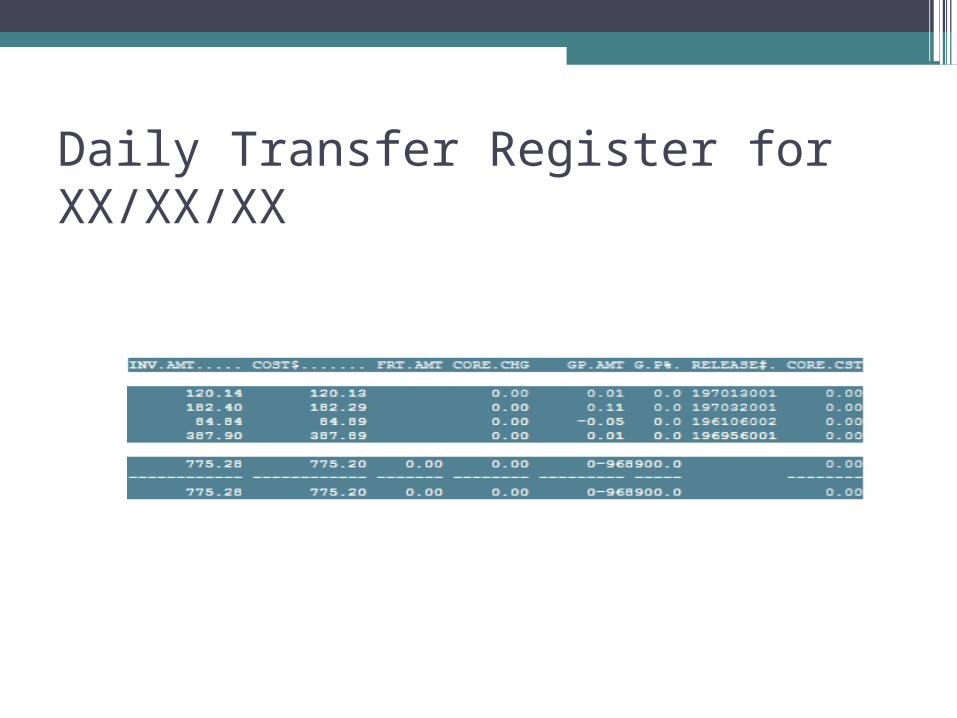

Daily Transfer Register for XX/XX/XX

Men 13

Warranty

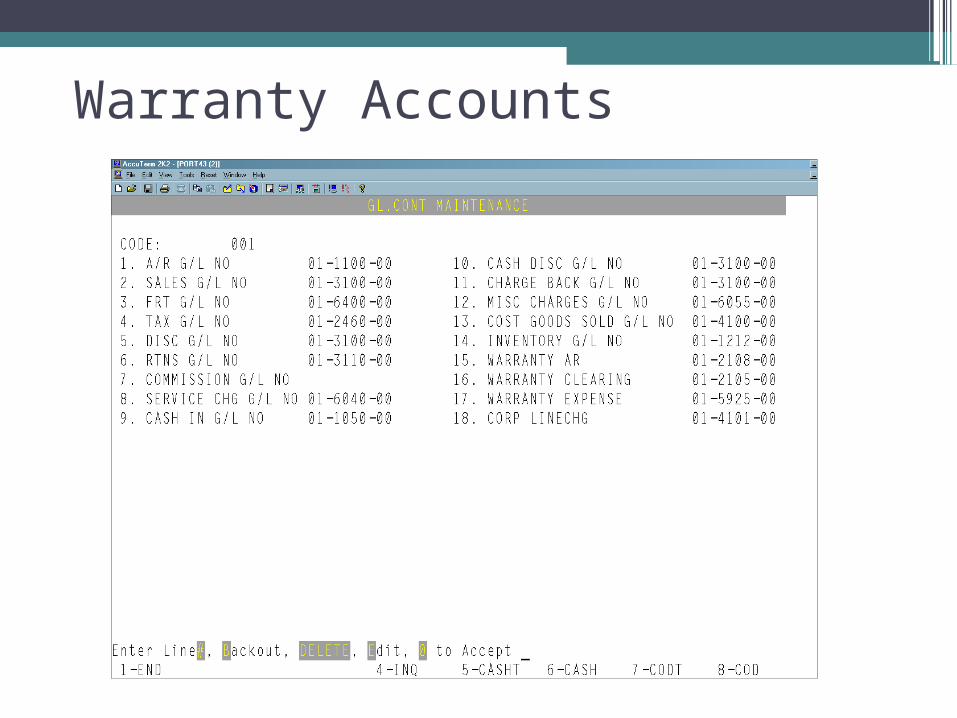

Warranty Accounts

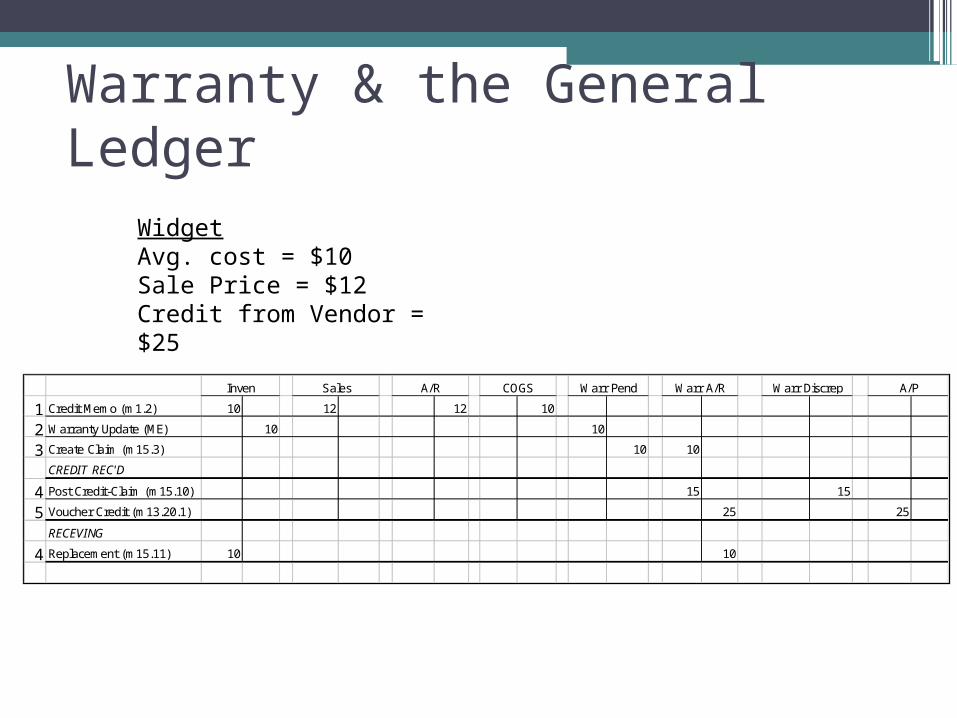

1 Credit Memo (m1.2) 10 12 12 10

2 Warranty Update (ME) 10 10

3 Create Claim (m15.3) 10 10

CREDIT REC'D

4 Post Credit-Claim (m15.10) 15 15

5 Voucher Credit (m13.20.1) 25 25

RECEVING

4 Replacement (m15.11) 10 10

Inven Sales A/R COGS Warr Pend Warr A/R Warr Discrep A/P

WidgetAvg. cost = $10Sale Price = $12Credit from Vendor = $25

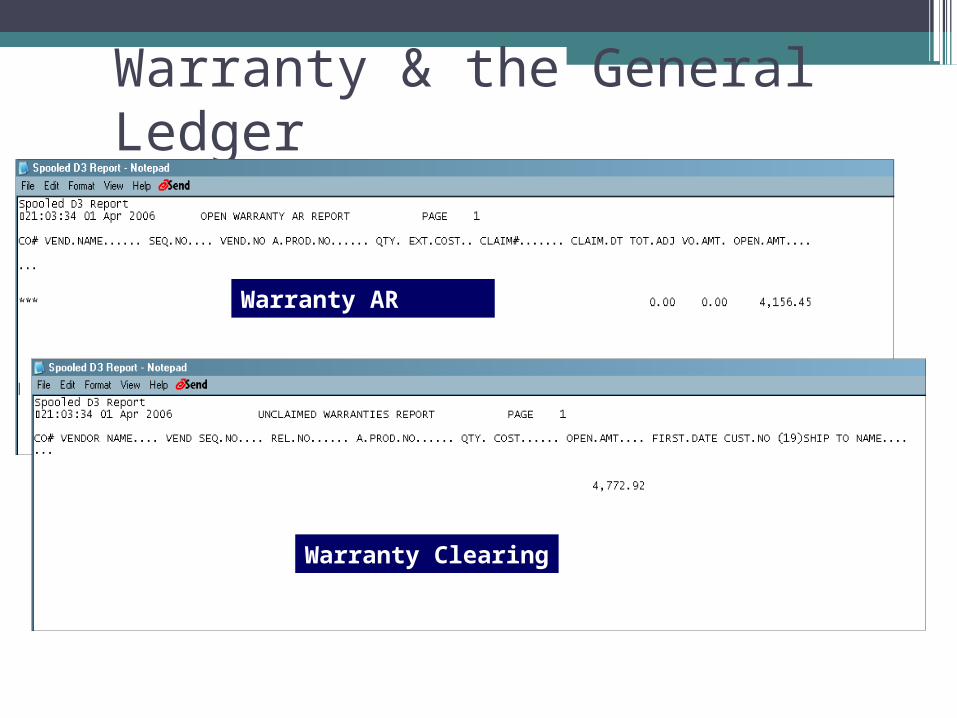

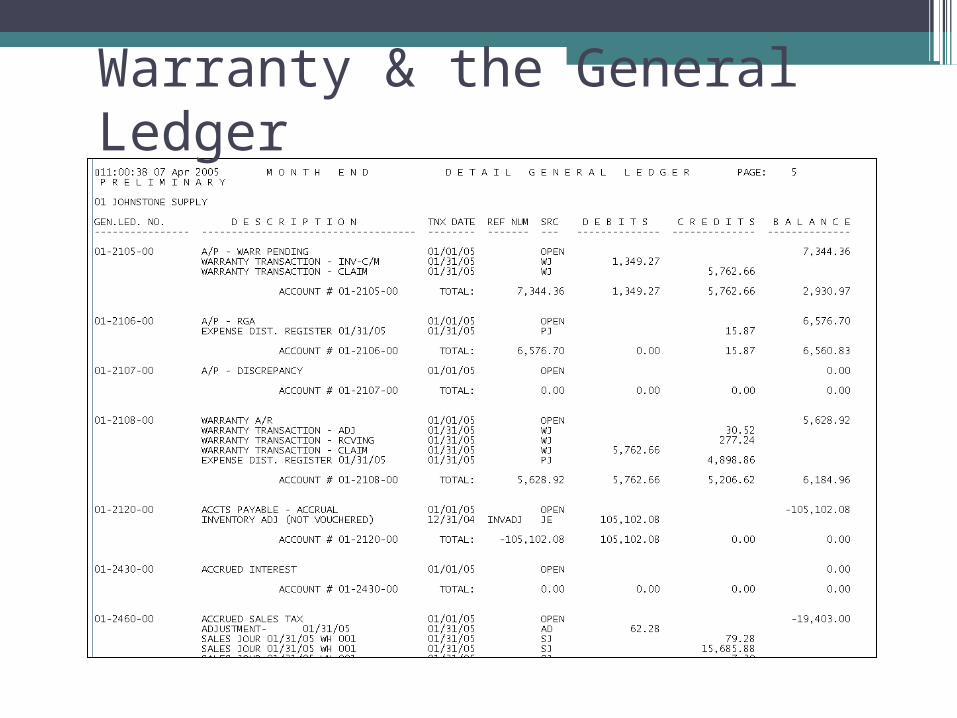

Warranty & the General Ledger

Warranty Reconciling

EOM Balancing

•Unclaimed Warranties•Claimed Warranties – AR

•Inventory?

Warranty & the General Ledger

Warranty AR

Warranty Clearing

Warranty & the General Ledger

Men 13

Sales Tax

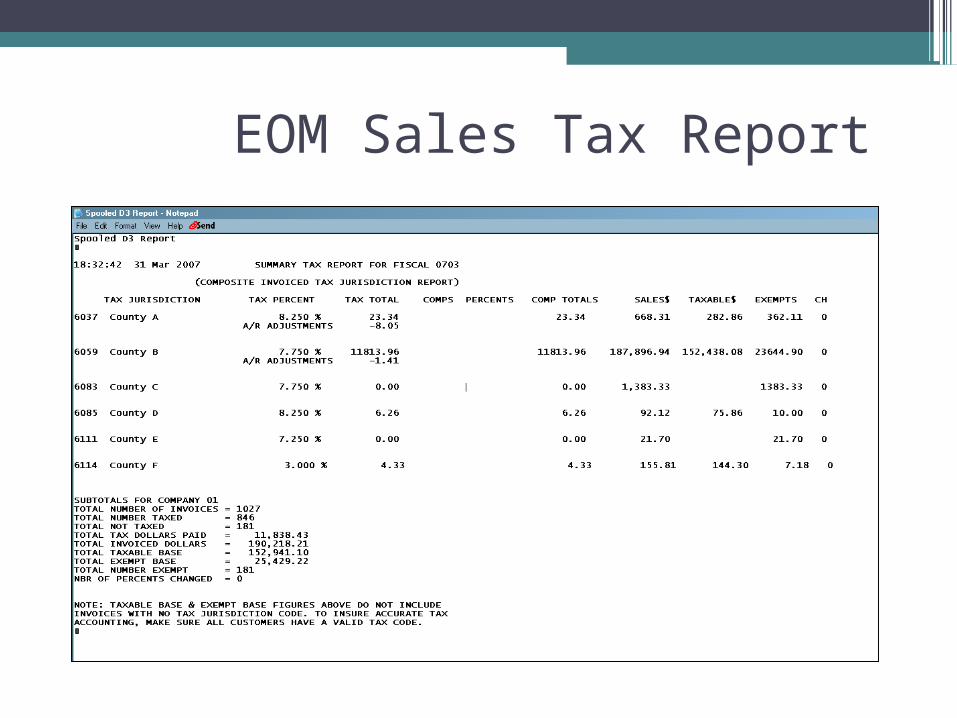

EOM Sales Tax Report

Men 13

Excise Tax

Discussion

Men 13

General Ledger

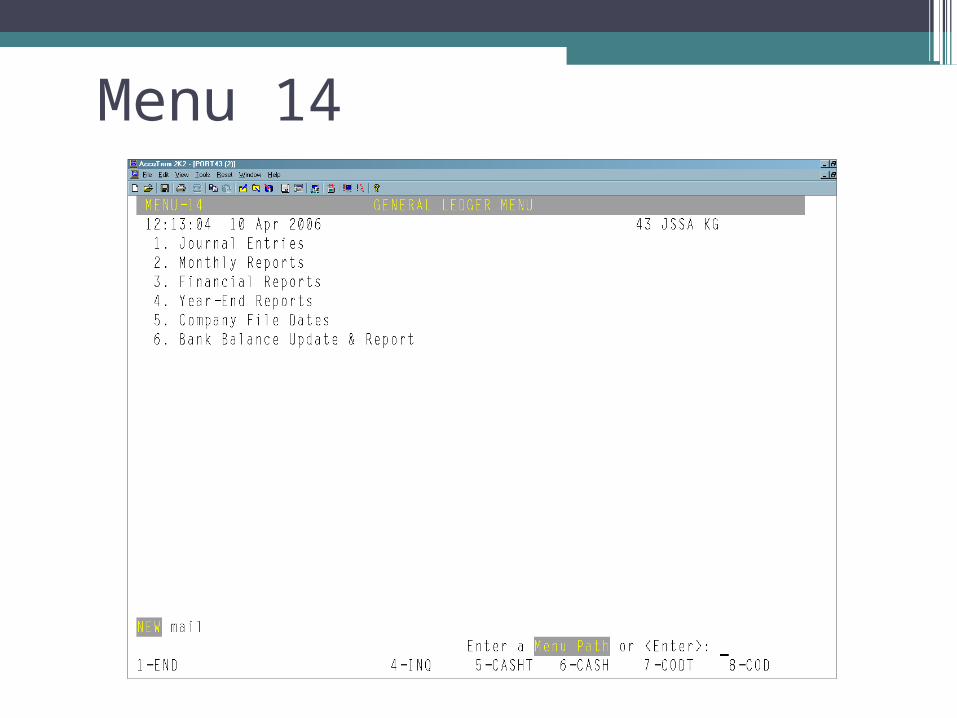

Menu 14

14.1.1 (for each company) (Menu 12.4.3)

Add to financial statements

Setting up a GL account

Demonstration

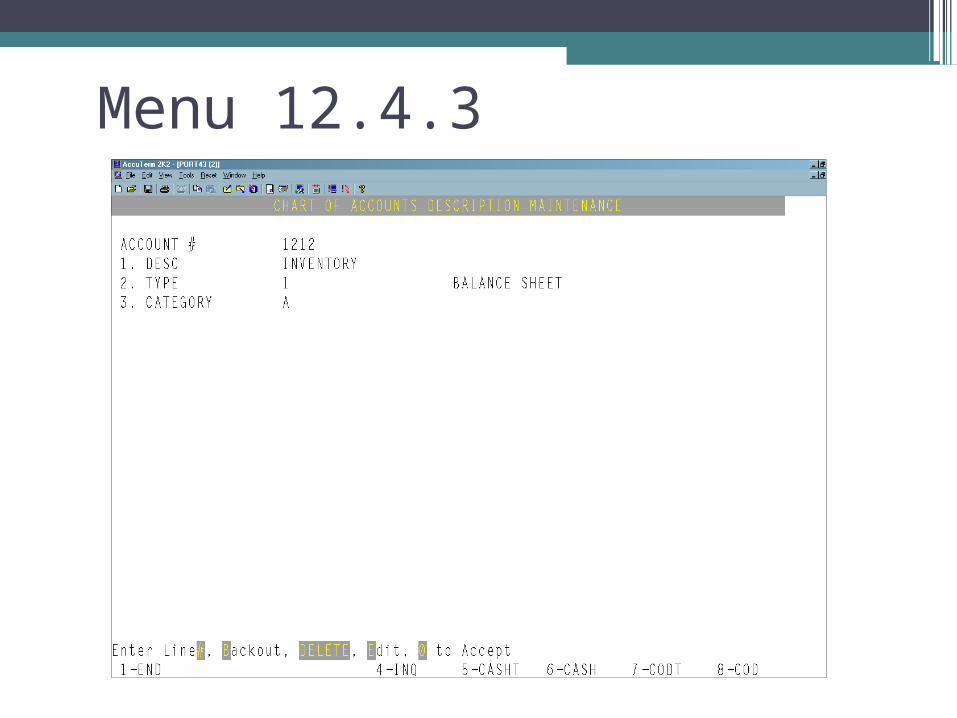

Menu 12.4.3

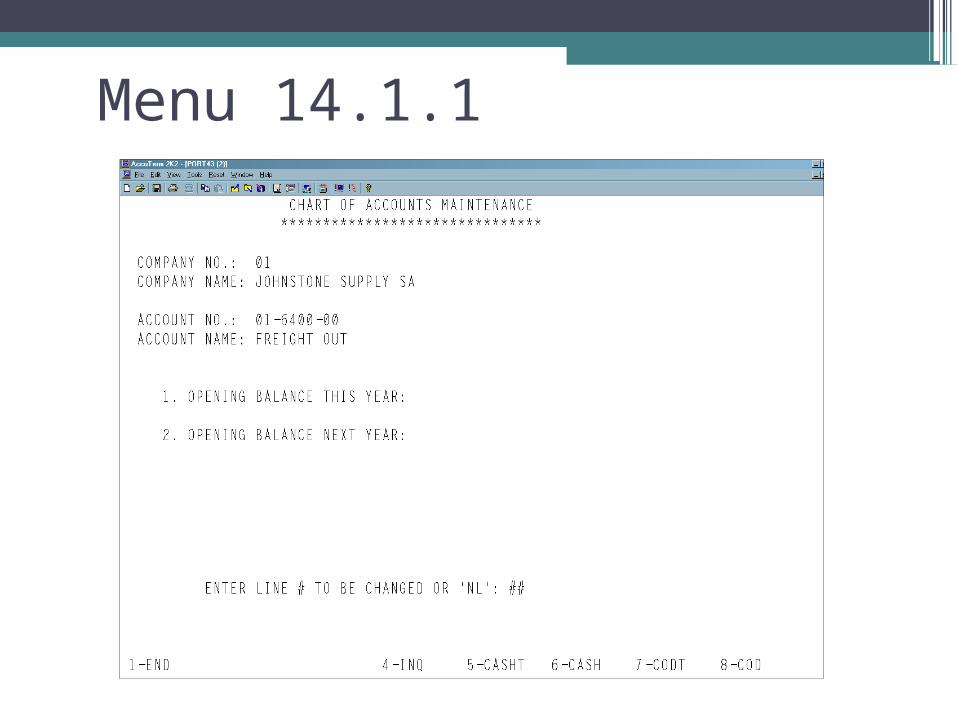

Menu 14.1.1

Setting up Financial Statements

Menu 14.1

Journal Entries

1. Enter JE 14.1.3 or 14.1.4

2. Print & Review JE 14.1.13 & 14.1.14

3. Update Trial Balance 14.2.4

Demonstration

Menu 14.1.3

Reoccurring Journal Entries

Enter JE 14.1.5

Review JE 14.1.15

Update JE 14.1.16

Update Trial Balance 14.2.4

Demonstration

Menu 14.5

Menu 14.2

Menu 14.3

REAL TIME GENERALLEDGER!!!

*Have to run 14.2.4 first*AR & AP periods have to be

current

Upgrade Suggestions

Discussion Topics

Handling of Tanks

R22 Pricing

AP process, paper trail, filing

Session Evaluations