Embed Size (px)

Citation preview

Accounting for income taxes: hot topics and developments

14 May 2013

Eighth Annual Domestic Tax Conference2

Disclaimer

► Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited located in the US.

► This presentation is ©2013 Ernst & Young LLP. All rights reserved. No part of this document may be reproduced, transmitted or otherwise distributed in any form or by any means, electronic or mechanical, including by photocopying, facsimile transmission, recording, rekeying or using any information storage and retrieval system, without written permission from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material herein is prohibited and is in violation of US and international law. Ernst & Young and its member firms expressly disclaim any liability in connection with use of this presentation or its contents by any third party.

► The views expressed by panelists in this session are not necessarily those of Ernst & Young LLP.

Eighth Annual Domestic Tax Conference3

Circular 230 disclaimer

► Any US tax advice contained herein was not intended or written to be used, and cannot be used, for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code or applicable state or local tax law provisions.

► These slides are for educational purposes only and are not intended, and should not be relied upon, as accounting advice.

Eighth Annual Domestic Tax Conference4

Today's presenters

Angela Evans (moderator)Brian FoleyKathy FordJoan Schumaker

Eighth Annual Domestic Tax Conference5

Today’s agenda

► Legislation and other developments► Accounting standards update► Tax accounting challenges► Regulatory focus on income taxes ► Auditing environment

Eighth Annual Domestic Tax Conference6

Legislative environment

Governments look for ways to increase revenues in a myriad of ways:►Base broadening►Incentive packages to increase number of taxpayers►Voluntary disclosure programs

Eighth Annual Domestic Tax Conference7

2012 was an active year for legislation

►Tax legislation in 2012:► Approximately 18 states passed new legislation► Over 25 countries passed new legislation

►Major themes in 2012:► State tax apportionment changes► New tax regimes► Transfer pricing legislation► Use of net operating losses► Limits on interest deductibility► Corporate tax rate changes

Eighth Annual Domestic Tax Conference8

Significant 2012 legislation examples

► State tax apportionment changes – Arizona, Virginia, Louisiana, Nebraska, Pennsylvania

► New tax regimes - Australia mining tax, France distribution tax, Spain capital gain tax on foreign investments, UK North Sea drilling

► Transfer pricing legislation – Australia, Brazil, Colombia, Panama, Peru

► Use of net operating losses – Denmark, France, Latvia, Spain

► Limits on interest deductibility – Belgium, Dominican Republic, France, Netherlands, Spain, Brazil, Russia, Sweden

► Corporate tax rate changes – Chile, Colombia, Mexico, Slovenia, Sweden, Vietnam

► General Anti-Avoidance Regulations – India, Peru

Eighth Annual Domestic Tax Conference9

2013 legislative developments – examples

►American Taxpayer Relief Act – enacted 2 January 2013► Extension of 2011 expired tax provisions, such as:

► Research and experimentation tax credit► Subpart F exception for active financing income► Controlled foreign corporation look through provision for Subpart F► Renewable energy tax credits► Incentives for biodiesel and renewable diesel► New markets tax credit► Work opportunity tax credit

► All provisions extended through December 31, 2013

Eighth Annual Domestic Tax Conference10

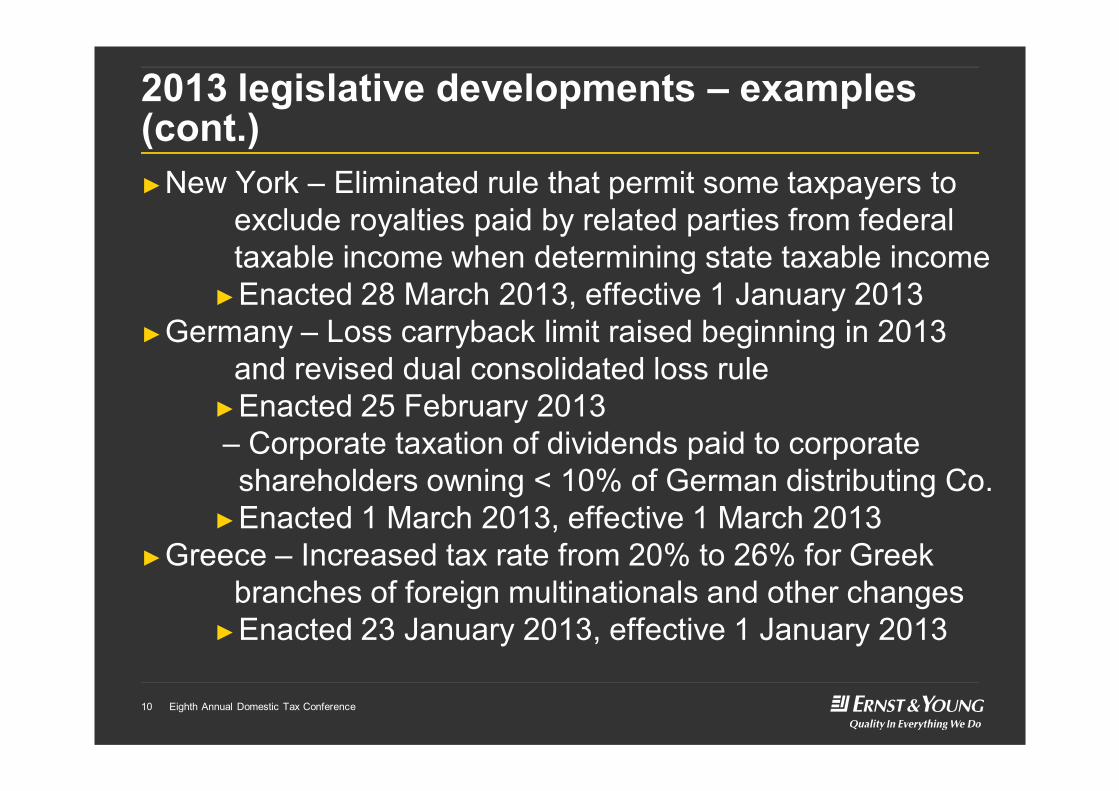

2013 legislative developments – examples (cont.)►New York – Eliminated rule that permit some taxpayers to

exclude royalties paid by related parties from federal taxable income when determining state taxable income

►Enacted 28 March 2013, effective 1 January 2013►Germany – Loss carryback limit raised beginning in 2013

and revised dual consolidated loss rule ►Enacted 25 February 2013– Corporate taxation of dividends paid to corporate shareholders owning < 10% of German distributing Co.

►Enacted 1 March 2013, effective 1 March 2013►Greece – Increased tax rate from 20% to 26% for Greek

branches of foreign multinationals and other changes►Enacted 23 January 2013, effective 1 January 2013

Eighth Annual Domestic Tax Conference11

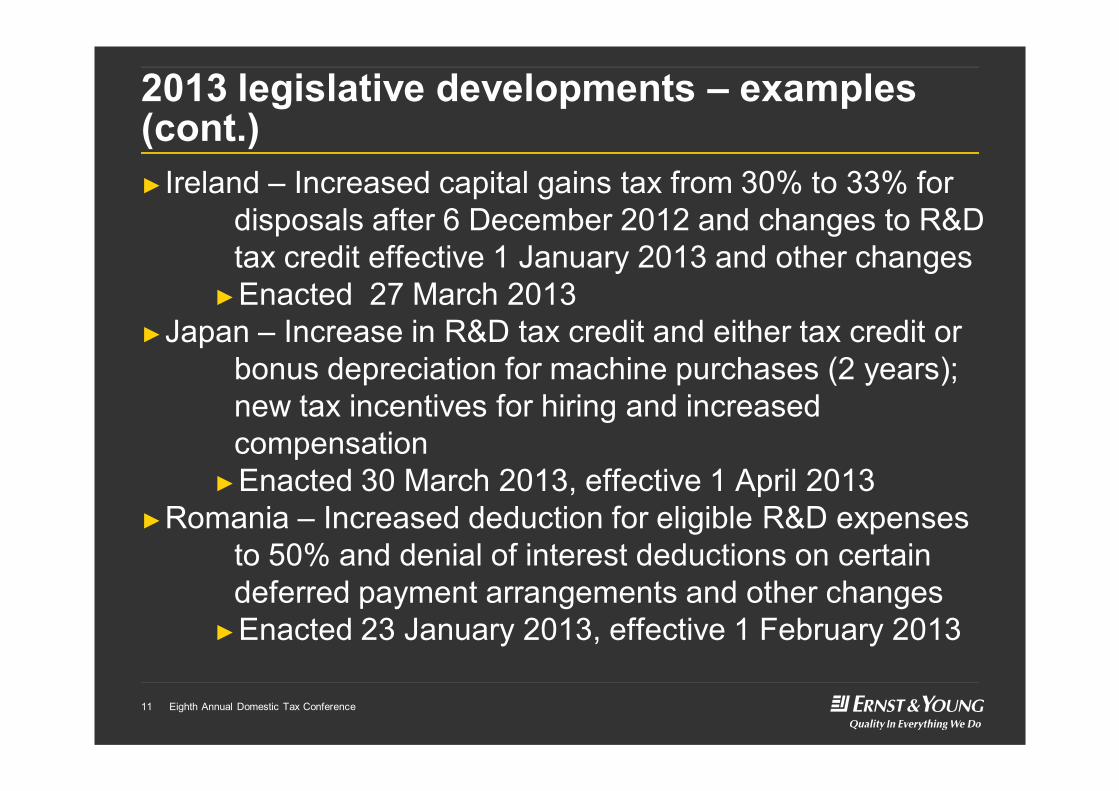

2013 legislative developments – examples (cont.)►Ireland – Increased capital gains tax from 30% to 33% for

disposals after 6 December 2012 and changes to R&D tax credit effective 1 January 2013 and other changes

►Enacted 27 March 2013►Japan – Increase in R&D tax credit and either tax credit or

bonus depreciation for machine purchases (2 years); new tax incentives for hiring and increased compensation

►Enacted 30 March 2013, effective 1 April 2013►Romania – Increased deduction for eligible R&D expenses

to 50% and denial of interest deductions on certain deferred payment arrangements and other changes

►Enacted 23 January 2013, effective 1 February 2013

Eighth Annual Domestic Tax Conference12

Changes in tax laws or ratesTax accounting considerations

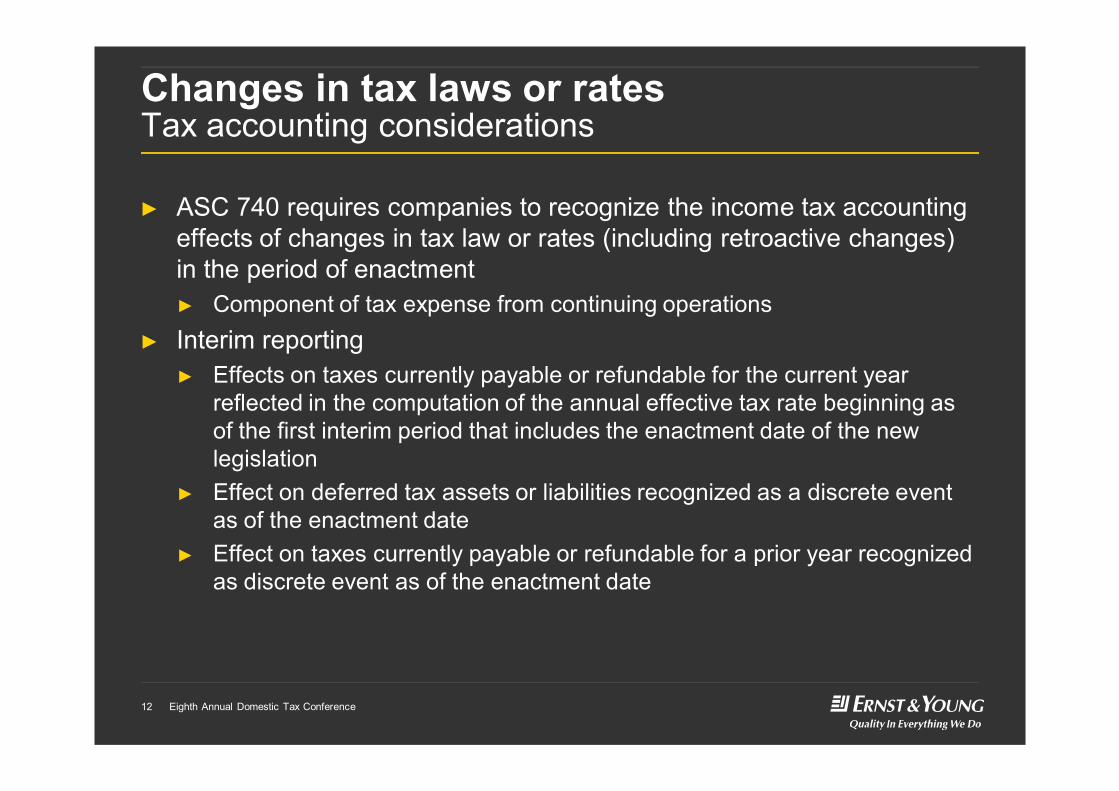

► ASC 740 requires companies to recognize the income tax accounting effects of changes in tax law or rates (including retroactive changes) in the period of enactment► Component of tax expense from continuing operations

► Interim reporting► Effects on taxes currently payable or refundable for the current year

reflected in the computation of the annual effective tax rate beginning as of the first interim period that includes the enactment date of the new legislation

► Effect on deferred tax assets or liabilities recognized as a discrete event as of the enactment date

► Effect on taxes currently payable or refundable for a prior year recognized as discrete event as of the enactment date

Eighth Annual Domestic Tax Conference13

► ASC 855, Subsequent Events► If a nonrecognized subsequent event is material to the results of

operations or financial position, disclose:► The nature of the event► An estimate of its financial effect► Pro forma information as if change in law occurred as of the balance

sheet date

Changes in tax laws or rates Tax accounting considerations

Eighth Annual Domestic Tax Conference14

Tangible property regulations

► Amended temporary regulations issued 14 December 2012 delaying effective date to tax years beginning on or after 1 January 2014

► Final regulations anticipated summer of 2013► Notice 2012-73 allows taxpayers to elect to early-adopt

the temporary regulations, or the final regulations, for tax years beginning on or after 1 January 2012

Eighth Annual Domestic Tax Conference15

U.S. and state court decisions – examples

► CBS Corporation v. U.S. (May 2012)► Companies that sold assets at a gain that generated Foreign Sales

Corporation (FSC) commissions may restore a portion of the basis of the underlying assets and decrease the amount of gain on sale

► Bank of NY Mellon v. Commissioner (February 2013)► Structured Trust Advantaged Repackaged Securities (STARS)

transaction lacked economic substance and are disregarded for tax purposes; taxpayer is not entitled to foreign tax credits, a foreign tax deduction or foreign-source income treatment

► Consolidated Edison v. U.S. (January 2013)► Federal Circuit held expense deductions were from abusive lease

in lease out (LILO) transaction and are disallowed based on substance over form

Eighth Annual Domestic Tax Conference16

U.S. and state court decisions – examples (cont.)► Gillette v. Franchise Tax Board (October 2012)

► Court of Appeals held that taxpayer should be allowed to elect to apply the state codified apportionment or Multistate Tax Compact

Eighth Annual Domestic Tax Conference17

Uncertain tax positionsChanges in judgment► Changes in judgment that result in the subsequent

recognition, derecognition or changes in measurement of a tax position that was previously recognized in a prior annual period► Consider at each reporting date ► To be based on new information versus simply changing an

interpretation or evaluation of previous information

► Reporting considerations► Change in judgment of a tax position that was taken in a prior

annual period (including any interest and penalties)► Discrete event recognized in earnings in the period (interim or annual)

in which the change occurs► Change in judgment related to a tax position taken in prior interim

period of the current year is accounted for pursuant to interim reporting guidance of ASC 740

Eighth Annual Domestic Tax Conference18

Tax legislation pending and not yet enacted under US GAAP ─ example

► UK proposed corporate tax rate reduction► Currently enacted tax rate for US GAAP purposes► 23%, beginning on 1 April 2013

► 2013 U.K. Budget delivered 20 March 2013► 21% rate beginning 1 April 2014 and further proposed

reduction to 20% beginning 1 April 2015► Royal Assent required for enactment under US

GAAP► Expected July 2013

Eighth Annual Domestic Tax Conference19

Legislative proposals Obama administration fiscal 2014 budget

► Budget issued 10 April 2013 calls for revenue-neutral business tax reserve fund

► Unspecified lower tax rate offset by tax subsidy reforms► R&E tax credit and Work Opportunity Tax Credit (WOTC)

made permanent► Eliminate tax deduction for expenses to move overseas► New tax credit for costs to relocate manufacturing to U.S.► New manufacturing communities tax credit► Tax mark-to-market on derivative contracts► Eliminate LIFO and oil and gas tax preferences► Reform treatment of insurance industry and products► International tax provisions (same as last year)► Insurance provisions

Eighth Annual Domestic Tax Conference20

Legislative proposals Obama administration fiscal 2014 budget (cont.)

► Other business tax proposals to be considered outside of tax reform, include► Tax carried interests as ordinary income► Tax accrued market discount currently► Use average basis for all identical shares of portfolio

stock with long-term holding period► Other changes

► Does not address tax extenders

Eighth Annual Domestic Tax Conference21

Today’s agenda

► Legislation and other developments► Accounting standards update► Tax accounting challenges► Regulatory focus on income taxes ► Auditing environment

Eighth Annual Domestic Tax Conference22

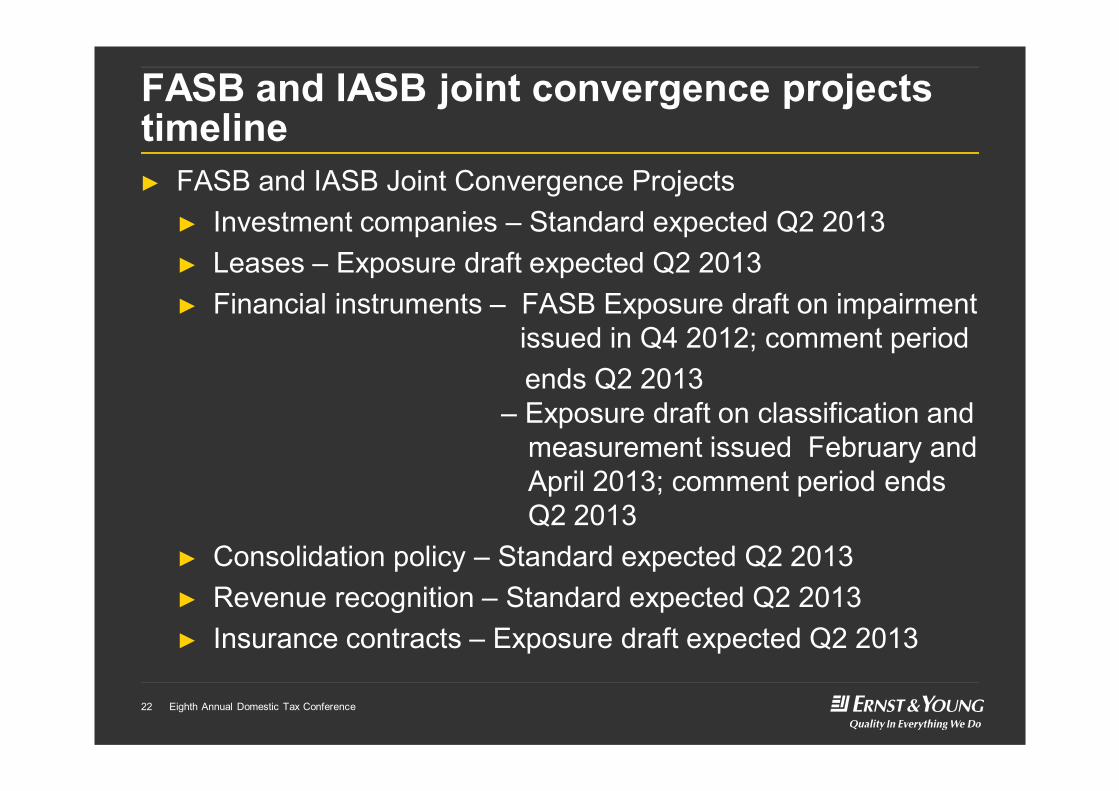

FASB and IASB joint convergence projects timeline► FASB and IASB Joint Convergence Projects

► Investment companies – Standard expected Q2 2013► Leases – Exposure draft expected Q2 2013► Financial instruments – FASB Exposure draft on impairment

issued in Q4 2012; comment periodends Q2 2013

– Exposure draft on classification and measurement issued February and April 2013; comment period ends Q2 2013

► Consolidation policy – Standard expected Q2 2013► Revenue recognition – Standard expected Q2 2013► Insurance contracts – Exposure draft expected Q2 2013

Eighth Annual Domestic Tax Conference23

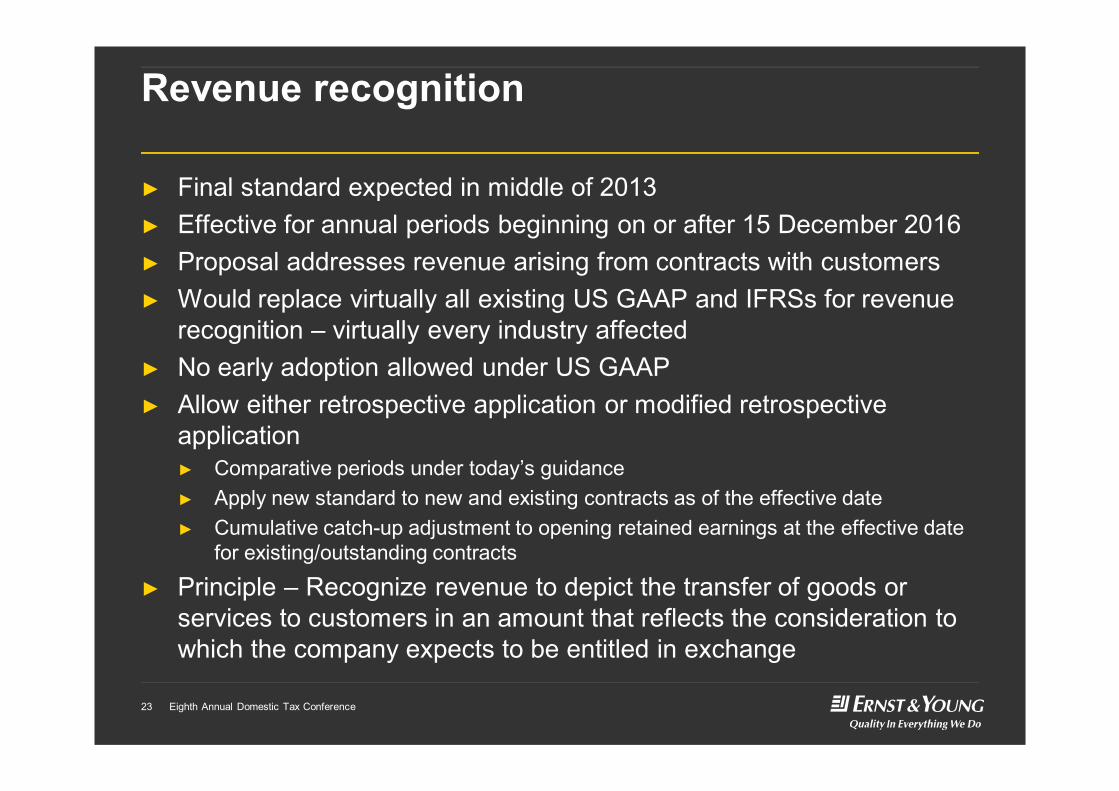

Revenue recognition

► Final standard expected in middle of 2013► Effective for annual periods beginning on or after 15 December 2016► Proposal addresses revenue arising from contracts with customers► Would replace virtually all existing US GAAP and IFRSs for revenue

recognition – virtually every industry affected► No early adoption allowed under US GAAP► Allow either retrospective application or modified retrospective

application ► Comparative periods under today’s guidance► Apply new standard to new and existing contracts as of the effective date► Cumulative catch-up adjustment to opening retained earnings at the effective date

for existing/outstanding contracts

► Principle – Recognize revenue to depict the transfer of goods or services to customers in an amount that reflects the consideration to which the company expects to be entitled in exchange

Eighth Annual Domestic Tax Conference24

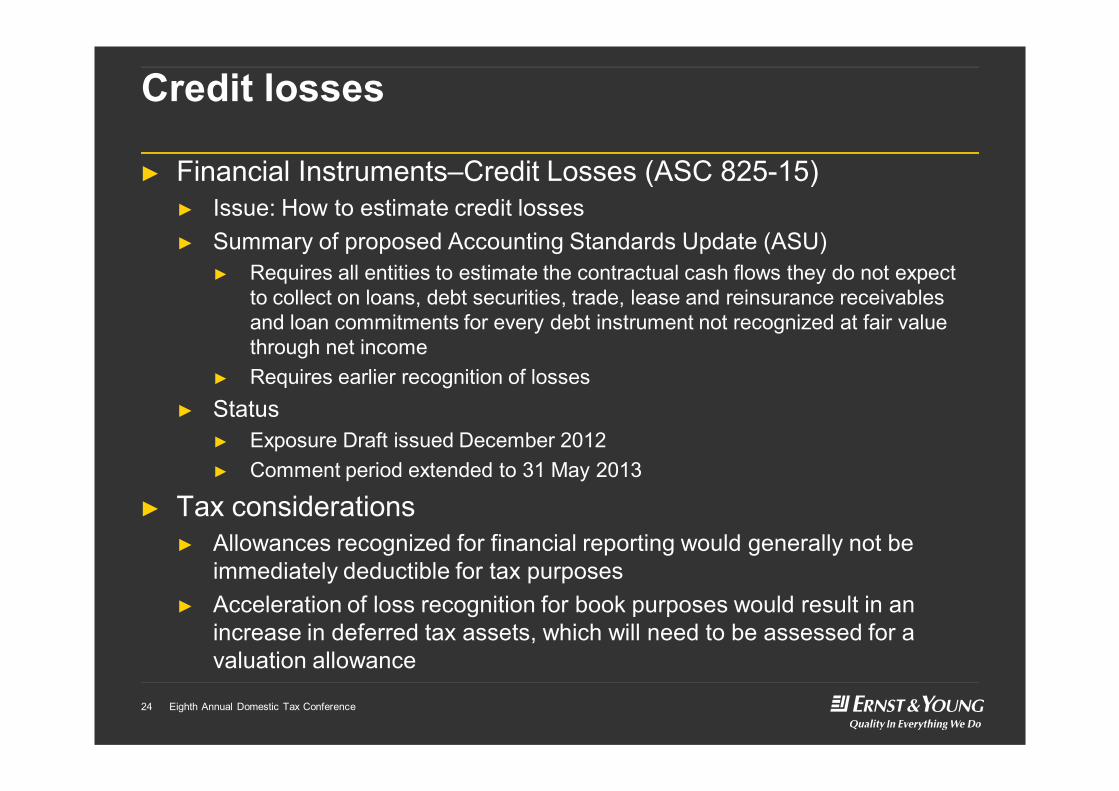

Credit losses

► Financial Instruments–Credit Losses (ASC 825-15)► Issue: How to estimate credit losses► Summary of proposed Accounting Standards Update (ASU)

► Requires all entities to estimate the contractual cash flows they do not expect to collect on loans, debt securities, trade, lease and reinsurance receivables and loan commitments for every debt instrument not recognized at fair value through net income

► Requires earlier recognition of losses ► Status

► Exposure Draft issued December 2012► Comment period extended to 31 May 2013

► Tax considerations► Allowances recognized for financial reporting would generally not be

immediately deductible for tax purposes► Acceleration of loss recognition for book purposes would result in an

increase in deferred tax assets, which will need to be assessed for a valuation allowance

Eighth Annual Domestic Tax Conference25

EITF 13-B Low Income Housing Credits

► Issue 13-B – Accounting for Investments in Qualified Affordable Housing Projects► Issue : How to account for limited partnership investment in a qualified

affordable housing project► Summary of proposed Accounting Standards Update (ASU)

► Ease conditions in ASC 323-740-25-1 to use the effective yield method (i.e., recognizing the entity’s portion of both the Low Income Housing Tax Credits (LIHTC) and the earnings or losses of the LIHTC investment net as a component of income taxes attributable to continuing operations)

► Accounting policy to use effective yield method if new proposed conditions are met

► Status► Proposed ASU issued 17 April 2013► Comment deadline 17 June 2013

► Effective date - TBD► Proposed transition

► Retrospective application► Early adoption would be permitted – Only upon issuance of final standard

► Other► Comments requested on expansion to other tax benefit/credit investments

Eighth Annual Domestic Tax Conference26

EITF 13-C Presentation of a liability for an unrecognized tax benefit ► Issue 13-C - Presentation of a liability for an unrecognized tax benefit (UTB) when

a net operating loss (NOL) or tax credit carryforward exists► Issue - How to present the liability for an UTB when an NOL or tax credit

carryforward exists(i.e., gross or net balance sheet presentation)

► Summary of proposed Accounting Standards Update (ASU) guidance► An UTB would be presented as a reduction of a deferred tax asset (DTA)

when settlement in this manner is available under the tax law (i.e., net presentation)

► Status► Proposed ASU was issued 21 February 2013► Comment deadline ended 22 April 2013

► Effective date – TBD► Proposed transition

► Retrospective application► Early adoption is permitted – Only upon issuance of final standard

Eighth Annual Domestic Tax Conference27

Financial Accounting Foundation Review of ASC 740► The Financial Accounting Foundation (FAF) announced during

February a post-implementation review of FAS 109, issued in 1992► Reasons cited

► Complex for stakeholders to understand► A number of constituents and the FASB advisory groups have

indicated this is an area that can be improved► Income tax accounting is source of deficiencies, errors and

restatements► Post-implementation review process

► Obtain stakeholder input► Comments and surveys not available to the public► Timetable for report

► Longer-term implications uncertain

Eighth Annual Domestic Tax Conference28

Today’s agenda

► Legislation and other developments► Accounting standards update► Tax accounting challenges► Regulatory focus on income taxes ► Auditing environment

Eighth Annual Domestic Tax Conference29

Income tax accounting restatements

While specific causes vary, a significant portion of recent restatements related to income taxes fall into the following categories:►Inappropriate evaluation of the realizability of deferred tax

assets (DTAs)►Incorrect identification or calculation of tax basis, resulting

in inappropriate measurement of deferred tax assets and liabilities

►Income tax accounting errors associated with intercompany transactions

►Incorrect application of intra-period allocation rules►Improper accounting for outside basis differences

Eighth Annual Domestic Tax Conference30

Income tax accounting restatementsRealizability of deferred tax assets

►Restatements generally occurred due to errors in assessing the four sources of taxable income

►Examples include:►Inappropriately considering a projection of future taxable

income to be a tax planning strategy►Evaluating deferred tax assets for realizability on a net

vs. gross basis►Inappropriate consideration of taxable temporary

differences (e.g., taxable temporary differences related to indefinite-lived intangibles) as a source of future taxable income

Eighth Annual Domestic Tax Conference31

Income tax accounting restatementsTax basis

►Maintaining a detailed and accurate record of the tax basis of all assets and liabilities, including those without a book basis, is an essential starting point in accounting for income taxes

►Restatements have been caused by not properly identifying a tax basis or attribute or not appropriately recording and tracking the tax basis or attribute in subsequent periods ─ Requires technical understanding of tax law

► Often for multiple taxing jurisdictions

► May be simple or complex

Eighth Annual Domestic Tax Conference32

Income tax accounting restatementsIntercompany transfers

► Exception to general provisions in ASC 740

► Assets are sometimes sold at a profit between affiliated entities that are consolidated for financial reporting purposes, but file separate income tax returns► Seller’s separate books generally reflect profit or loss on sale and related

income tax effect of that profit or loss► Buyer’s separate books (and tax basis) generally reflect the assets at the

intercompany transfer price► Consolidation entries that eliminate intercompany profit also will eliminate

the related tax expense (benefit)► Record any income taxes paid by the seller as a prepaid tax

►Restatements have been caused by failure to track intercompany transactions and related income tax effects

Eighth Annual Domestic Tax Conference33

Income tax accounting restatementsIntra-period allocation

►Restatements have been caused by failure to allocate income tax expense correctly in accordance with the intra-period allocation rules

►Examples include:► Failure to apply the exception in ASC 740-20-45-7

► Failure to consider interaction of exception in ASC 740-20-45-7 with the interim reporting rules in calculating the EAETR

► Inappropriate “backward tracing” to prior annual periods of effects of changes in deferreds and related valuation allowances

Eighth Annual Domestic Tax Conference34

Income tax accounting restatementsOutside basis differences

►The ASC 740-30 (indefinite reinvestment) exception for undistributed earnings of foreign subsidiaries and foreign corporate joint ventures does not apply to 50% or less owned investees that are not corporate joint ventures as defined by ASC 323

►Restatements have been caused by companies inappropriately applying the indefinite reinvestment assertion to foreign equity method investments and by failure to consider certain sub-part F activities of these investments

Eighth Annual Domestic Tax Conference35

Today’s agenda

► Legislation and other developments► Accounting standards update► Tax accounting challenges► Regulatory focus on income taxes ► Auditing environment

Eighth Annual Domestic Tax Conference36

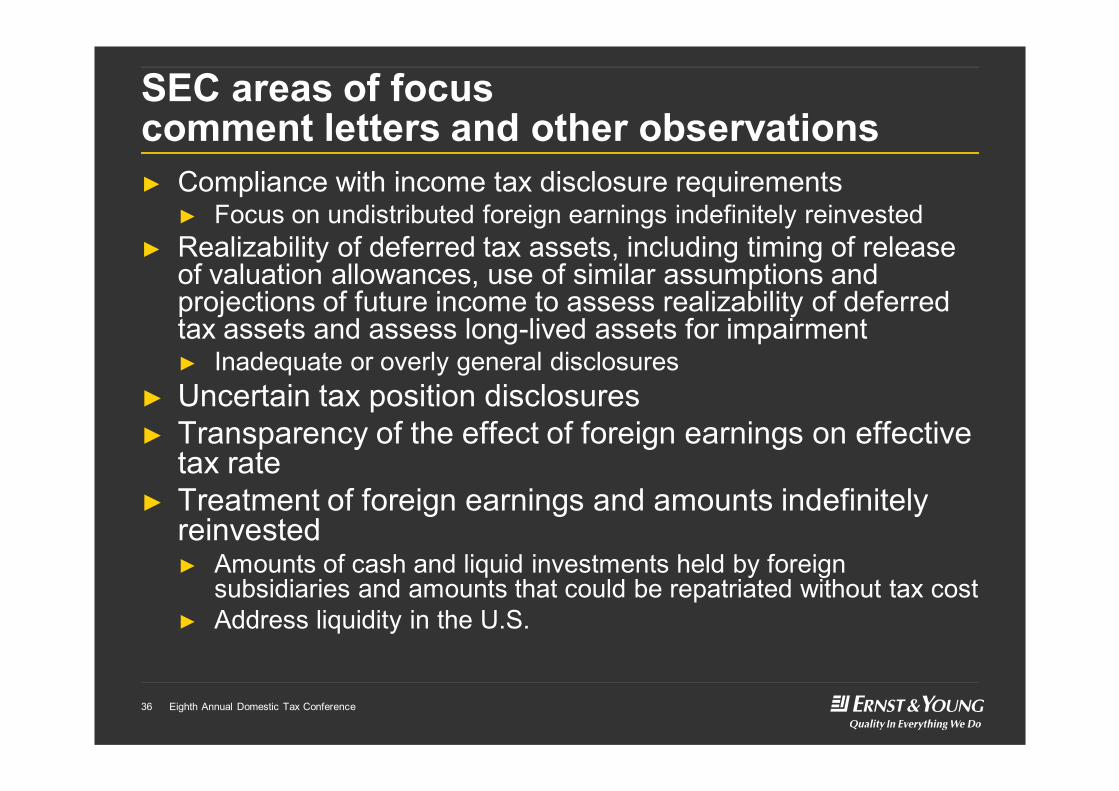

SEC areas of focuscomment letters and other observations► Compliance with income tax disclosure requirements

► Focus on undistributed foreign earnings indefinitely reinvested ► Realizability of deferred tax assets, including timing of release

of valuation allowances, use of similar assumptions and projections of future income to assess realizability of deferred tax assets and assess long-lived assets for impairment ► Inadequate or overly general disclosures

► Uncertain tax position disclosures► Transparency of the effect of foreign earnings on effective

tax rate► Treatment of foreign earnings and amounts indefinitely

reinvested► Amounts of cash and liquid investments held by foreign

subsidiaries and amounts that could be repatriated without tax cost► Address liquidity in the U.S.

Eighth Annual Domestic Tax Conference37

Today’s agenda

► Legislation and other developments► Accounting standards update► Tax accounting challenges► Regulatory focus on income taxes ► Auditing environment

Eighth Annual Domestic Tax Conference38

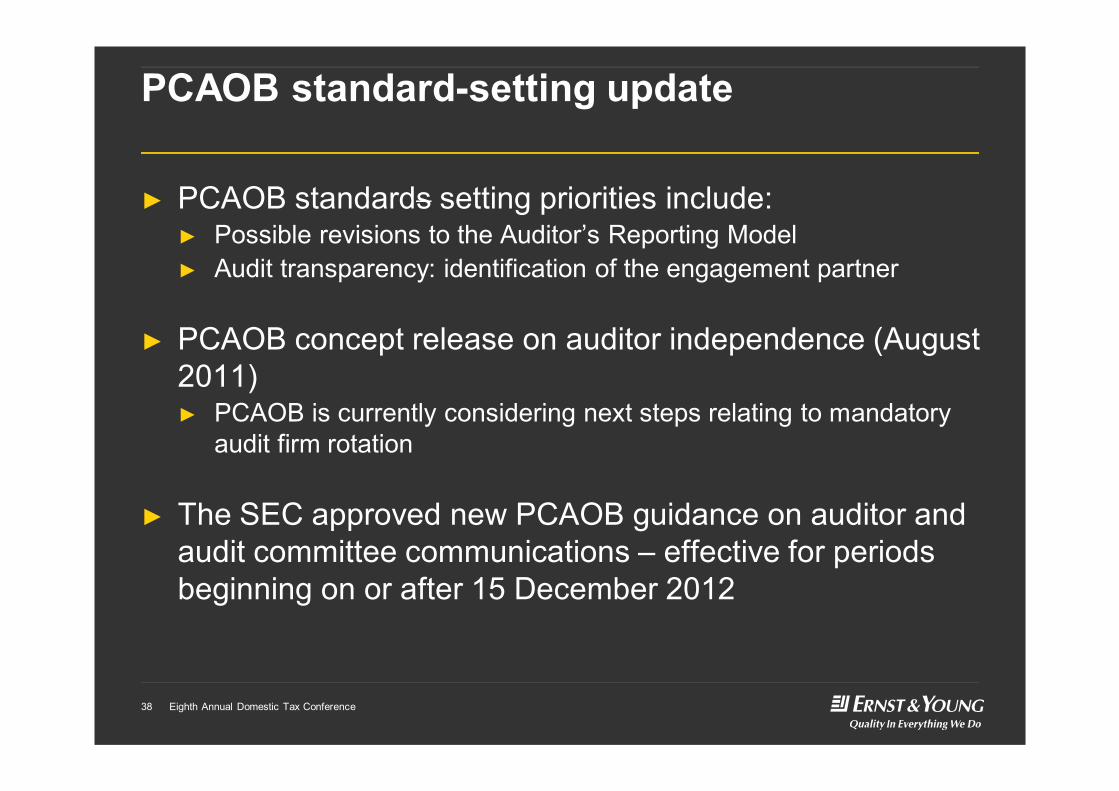

PCAOB standard-setting update

► PCAOB standards setting priorities include:► Possible revisions to the Auditor’s Reporting Model► Audit transparency: identification of the engagement partner

► PCAOB concept release on auditor independence (August 2011) ► PCAOB is currently considering next steps relating to mandatory

audit firm rotation

► The SEC approved new PCAOB guidance on auditor and audit committee communications – effective for periods beginning on or after 15 December 2012

Eighth Annual Domestic Tax Conference39

European developments on audit policy

► Netherlands audit changes approved December 2012► Mandatory audit rotation after 8 years effective 1 January 2016

► Applies to public interest entities (PIEs) ► Netherlands-based entities with securities listed on EU exchange

► Two-year cooling off period► Ban on non-audit services for “organizations of public interest”

► Significant restrictions on providing non-audit services to audit clients came into effect 1 January 2013 (2 year grandfather clause for services in contract at 31 December 2012)

► UK Financial Reporting Council changes to UK Corporate Governance Code issued September 2012► FTSE 350 companies should put external audit contract out to

tender at least every 10 years► Transition generally upon next change in audit partner

Thanks for participating