Embed Size (px)

Citation preview

Accounting for Foreign Currency

Publication Date: September 2020

Accounting for Foreign Currency

Copyright © 2020 by

DELTACPE LLC

All rights reserved. No part of this course may be reproduced in any form or by any means, without permission in

writing from the publisher.

The author is not engaged by this text or any accompanying lecture or electronic media in the rendering of legal,

tax, accounting, or similar professional services. While the legal, tax, and accounting issues discussed in this

material have been reviewed with sources believed to be reliable, concepts discussed can be affected by changes

in the law or in the interpretation of such laws since this text was printed. For that reason, the accuracy and

completeness of this information and the author's opinions based thereon cannot be guaranteed. In addition,

state or local tax laws and procedural rules may have a material impact on the general discussion. As a result, the

strategies suggested may not be suitable for every individual. Before taking any action, all references and citations

should be checked and updated accordingly.

This publication is designed to provide accurate and authoritative information in regard to the subject matter

covered. It is sold with the understanding that the publisher is not engaged in rendering legal, accounting, or other

professional service. If legal advice or other expert advice is required, the services of a competent professional

person should be sought.

—-From a Declaration of Principles jointly adopted by a committee of the American Bar Association and a

Committee of Publishers and Associations.

Course Description

In today’s modern economy, the growth of foreign operations is continuing upward and the number of companies

with foreign operations has expanded. For example, a company often operates in different economic and currency

environments to stay competitive in the global marketplace. Thus, it must have a process for reporting foreign

currency balances to address several financial reporting issues, such as determining functional currencies,

accounting for foreign currency transactions, and translating its foreign entity’s financial statements. ASC 830

Foreign Currency Matters provides guidance for transactions denominated in a foreign currency, and for

operations undertaken in a foreign currency environment. This course covers key aspects of the guidance and

includes specific examples to illustrate its application. Relevant references to and excerpts from ASC 830 are

discussed throughout the course.

Field of Study Accounting

Level of Knowledge Intermediate

Prerequisite None

Advanced Preparation None

Learning Objectives

After completing this section, you should be able to:

1. Recognize key areas of guidance in ASC 830 Foreign Currency Matters

2. Identify steps to remeasure foreign currency transactions to the functional currency

3. Identify steps to translate foreign currency financial statements to the reporting currency

Table of Contents

I. Basic Principles of ASC 830 .................................................................................. 1

A. Scope and Scope Exceptions ........................................................................................... 1

B. The Accounting Model for Foreign Currency Matters ...................................................... 2

Example 1: The Translation Process of Foreign Currency Transactions and Financial Statements ............4

II. Determine the Functional Currency ................................................................... 5

A. General Rules ................................................................................................................. 5

B. Classes of Foreign Operations ......................................................................................... 6

C. Factors in Determining the Functional Currency .............................................................. 8

Example 2: Determination of the Functional Currency ...............................................................................9

D. Highly Inflationary Environment ................................................................................... 10

Example 3: Determination of Highly Inflation ......................................................................................... 10

E. Change in the Functional Currency ................................................................................ 11

Example 4: Change in Functional Currency ............................................................................................. 12

Example 5: Functional Currency Changes Because the Economy is No Longer Highly Inflationary ........ 13

The SEC’s View on Changes in Functional Currency................................................................................. 14

Review Questions – Section 1 .............................................................................. 16

III. Remeasure Foreign Currency Transactions to the Functional Currency ........... 17

A. General Rules ............................................................................................................... 17

Example 6: Remeasurement Requirements ............................................................................................. 17

B. Selection of Exchange Rates for Remeasurement .......................................................... 18

Monetary Accounts ........................................................................................................................... 18

Nonmonetary Accounts ..................................................................................................................... 18

C. Transaction Gains or Losses .......................................................................................... 20

Example 7: Determining Transaction Gains or Losses ............................................................................. 20

D. Foreign Currency Transactions ...................................................................................... 22

1. Property, Plant and Equipment .................................................................................................. 22

Example 8: Depreciation of Fixed Assets ................................................................................................. 22

2. Inventories.................................................................................................................................. 23

Example 9: Write-down of Inventory Measured Using FIFO ................................................................... 23

3. Debt ............................................................................................................................................ 24

4. Debt and Equity Securities ......................................................................................................... 25

Trading Debt Securities ............................................................................................................................... 26

Available-for-Sale Debt Securities ............................................................................................................... 26

Held-to-Maturity Debt Securities ................................................................................................................ 26

Equity Securities .......................................................................................................................................... 27

5. Foreign Currency Leases ............................................................................................................ 27

Lessee Accounting ....................................................................................................................................... 27

Lessor Accounting ........................................................................................................................................ 28

Comprehensive Illustration: Remeasurement of Foreign Currency Transactions to the

Functional Currency .......................................................................................................... 29

1. Accounts Receivable................................................................................................................... 29

2. Inventory .................................................................................................................................... 30

3. Held-to-Maturity Debt Securities ............................................................................................... 31

4. Foreign Subsidiary Accounts ...................................................................................................... 33

Review Questions – Section 2 .............................................................................. 34

IV. Translate Foreign Currency Financial Statements............................................ 36

A. General Rules ............................................................................................................... 36

B. Selection of Exchange Rates for Translation .................................................................. 37

Example 10: Exchange Rate When Exchangeability is Lacking Temporarily ........................................... 38

1. Balance Sheet ............................................................................................................................. 39

2. Income Statement ...................................................................................................................... 39

3. Cash Flow Statement.................................................................................................................. 39

C. Translation Adjustments ............................................................................................... 39

Example 11: Reporting Gains or Losses ................................................................................................... 40

D. Highly Inflationary Environment ................................................................................... 40

E. Derecognition ............................................................................................................... 42

1. Disposition of a Foreign Entity ................................................................................................... 42

Example 12: Reporting Translation Adjustments .................................................................................... 43

2. Partial Sale of Ownership Interest ............................................................................................. 44

Example 13: Partial Sale of Ownership Interest ...................................................................................... 45

Release of Cumulative Translation Adjustment Decision Tree ................................................................... 46

3. Cumulative Translation Adjustment in Impairment Assessment .............................................. 47

Example 14: Impairment Assessment ...................................................................................................... 47

Comprehensive Illustration: Translation of Foreign Entity Financial Statements ................ 48

V. Other Matters ................................................................................................. 51

A. Intercompany Profits .................................................................................................... 51

Example 15: Elimination of Intercompany Profits ................................................................................... 51

B. Hedging ........................................................................................................................ 52

C. Disclosures .................................................................................................................... 54

1. Aggregate Transaction Gains or Losses ...................................................................................... 54

2. Cumulative Translation Adjustments ......................................................................................... 54

3. Exchange Rate Changes .............................................................................................................. 54

4. Footnote Disclosure ................................................................................................................... 55

5. Excluding a Foreign Entity from Financial Statements ............................................................... 56

The SEC’s View on Disclosures, if the U.S. Dollar is Not the Reporting Currency ..................................... 56

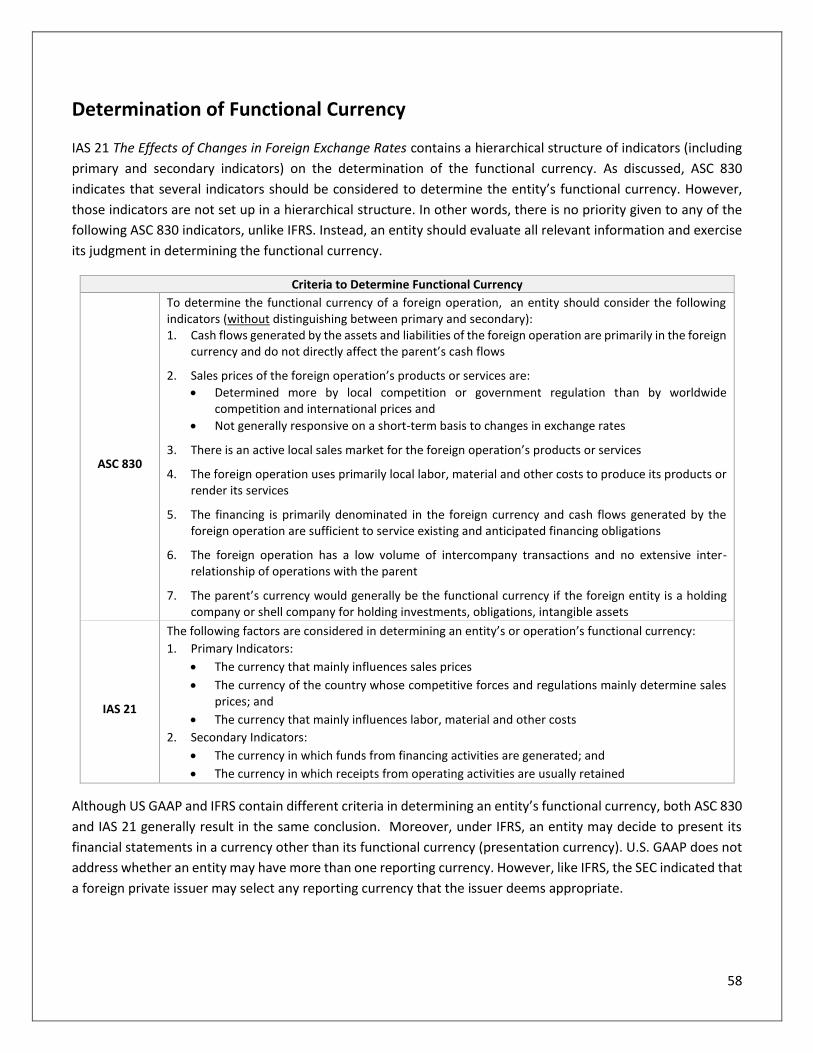

D. Difference between U.S. GAAP and IFRS ....................................................................... 57

Determination of Functional Currency .............................................................................................. 58

Highly Inflationary Economy .............................................................................................................. 59

Review Questions – Section 3 .............................................................................. 60

Glossary ............................................................................................................... 61

Index ................................................................................................................... 63

Review Question Answers ................................................................................... 64

Review Questions − Section 1 ........................................................................................... 64

Review Questions − Section 2 ........................................................................................... 65

Review Questions − Section 3 ........................................................................................... 68

1

I. Basic Principles of ASC 830

A. Scope and Scope Exceptions

Financial statements are intended to effectively communicate financial information about the performance,

financial position, and cash flows of a reporting entity to investors and creditors and other parties. Thus, the

financial statements of separate entities within a reporting entity, which may exist and operate in different

economic and currency environments, are consolidated and presented as though they were the financial

statements of a single reporting entity. That is, the reporting entity must prepare financial statements in a single

reporting currency. If the foreign statements have any accounts expressed in a currency other than their own,

they have to be converted into the foreign statement's currency prior to translation into U.S. dollars or any other

reporting currency.

According to ASC 830, a reporting entity is an entity or group whose financial statements are being referred to.

Those financial statements reflect any of 1) the financial statements of one or more foreign operations by

combination, consolidation, or equity accounting 2) foreign currency transactions. Reporting currency is the

currency in which an entity prepares its financial statements

ASC 830 Foreign Currency Matters (formerly FAS 52 Foreign Currency Translation) provides accounting and

reporting requirements for converting transactions and financial statements from a foreign currency to the

reporting currency. ASC 830 applies to the financial statements of ALL entities prepared in conformity with U.S.

generally accepted accounting principles (GAAP), whether the U.S. dollar or a foreign currency is the reporting

currency. That is, a foreign entity may report in its local currency in conformity with U.S. GAAP. For example, a

Chinese entity whose reporting currency is the Chinese yuan but reports in conformity with U.S. GAAP should

follow the requirements of ASC 830.

According to ASC 830, a foreign entity is an operation (for example, subsidiary, division, branch, joint venture, and

so forth) whose financial statements are both: 1) prepared in a currency other than the reporting currency of the

reporting entity 2) combined or consolidated with or accounted for on the equity basis in the financial statements

of the reporting entity.

ASC 830-10-15-3 specifies that ASC 830 applies to:

✓ Foreign currency transactions, including imports and exports denominated in a currency other than the

company's functional currency.

✓ Foreign currency financial statements of divisions, branches, and other investees included in the financial

statements of a U.S. company by consolidation, combination, or the equity method.

2

According to ASC 830, an entity's functional currency is the currency of the primary economic environment in

which the entity operates; normally, that is the currency of the environment in which an entity primarily generates

and expends cash.

ASC 830-10-15-7 indicates that ASC 830 does NOT apply to the translation of financial statements for purposes

other than consolidation, combination, or the equity method. For example, it does not cover translation of the

financial statements of a reporting entity from its reporting currency into another currency for the convenience

of readers accustomed to that other currency. ASC 830-20-15-2(a) also states that ASC 830 does NOT apply to

transactions involving derivative instruments. The derivatives guidance is codified in ASC 815 Derivatives and

Hedging.

B. The Accounting Model for Foreign Currency Matters

It is important to know that before applying ASC 830, a foreign entity's financial statements must be prepared in

accordance with GAAP. ASC 830 requires two accounting tasks for reporting foreign currency balances:

1. Foreign currency remeasurement: This is the process of expressing transactions denominated in a foreign

currency in its functional currency.

2. Foreign currency translation: This is the process of converting a foreign entity’s functional currency

financial statements into the reporting currency for preparing the reporting entity's (consolidated)

financial statements.

The following diagram illustrates the two distinct processes:

As shown in the example above, a U.S.-based conglomerate has a subsidiary in Norway that keeps its books and

records using the krone (Kr) (its local currency). But its primary operations involve Eurozone entities. Accordingly,

to prepare the consolidated financial statements, the parent first must remeasure all unsettled transactions of

the subsidiary from kroner to functional currency (euros). It then must translate those remeasured amounts into

reporting currency (U.S. dollars).

A key distinction between remeasurement and translation is:

U.S.

Reporting currency

(consolidated statements)

$

Eurozone

Functional currency

€

Norway

Local currency

(books of the subsidiary)

Kr

Step 1:

Remeasurement

Step 2:

Translation

3

• Transaction gains or losses, changes in functional currency amounts resulting from the remeasurement

process, are recognized in the income statement (net income from continuing operations) in the period

in which the exchange rate changes (affecting earnings).

• Translation adjustments, changes resulting from the process of converting financial statements from the

entity's functional currency into the reporting currency, are included in other comprehensive income

(affecting equity).

According to ASC 830, the exchange rate is the ratio between a unit of one currency and the amount of another

currency for which that unit can be exchanged at a particular time.

The following table summarizes the difference between remeasurement and translation.

Foreign currency

remeasurement

The process of expressing transactions

denominated in a foreign currency in its

functional currency.

Cash flow

consequence

Affects

earnings

Foreign currency

translation

The process of expressing in the reporting

currency of the enterprise those amounts that

are denominated or measured in a different

currency

No cash flow

consequence

Affects

equity

It is presumed under ASC 830 that the reporting currency for a company is U.S. dollars; however, it is possible that

the reporting currency may be other than U.S. dollars.

The objectives of remeasurement and translation are to:

✓ Provide information that is generally compatible with the expected economic effects of a rate change on

an entity's cash flows and equity; and

✓ Reflect in consolidated statements the financial results and relationships as measured in its functional

currency.

The key steps in accomplishing the objectives include:

Determine the functional currency: An essential purpose in translating foreign currency is to preserve the

financial performance and relationships expressed in the foreign currency. This is achieved by using the foreign

entity's functional currency.

Details are discussed in the “Determine the Functional Currency” chapter.

Determine the functional currency

Remeasure foreign currency transactions to the functional currency

Translate foreign currency financial

statements

4

Remeasure foreign currency transactions: Once the functional currency of an entity is identified, transactions

denominated in a currency other than its functional currency should be measured in the functional currency.

Details are discussed in the “Remeasure Foreign Currency Transactions” chapter.

Translate foreign currency financial statements: After the remeasurement process is complete, the financial

statements stated in the functional currency should be translated to the reporting currency via the current rate

method.

Details are discussed in the “Translate Foreign Currency Financial Statements” chapter.

Since the FASB released its initial guidance on foreign currency in 1981, there have been very few amendments

within ASC 830.

Example 1: The Translation Process of Foreign Currency Transactions and Financial Statements

Smith Corp., a U.S. company, has a Mexican subsidiary, PETRO, whose records are maintained in Mexican pesos.

However, due to other factors, the functional currency for the subsidiary is actually Canadian dollars. The accounts

of PETRO must be remeasured into Canadian dollars before the financial statements are then translated into the

reporting entity's currency (in this case, U.S. dollars). An ensuing translation gain or loss from Mexican pesos to

Canadian dollars is included in the remeasured net income.

However, if PETRO’s functional currency was instead the Mexican peso, there is only a need to translate to the

reporting currency (U.S. dollars).

Finally, if PETRO's functional currency was the same as that of the reporting entity, Smith, remeasurement is only

from the Mexican peso to the reporting currency (U.S. dollars).

5

II. Determine the Functional

Currency “The assets, liabilities, and operations of a foreign entity must be measured using the functional currency of that

entity.”

ASC 830-10-45-2

A. General Rules

The FASB believes that the most meaningful measurement unit for the assets, liabilities, and operations of an

entity is the currency in which it primarily conducts its business, assuming that currency has reasonable stability.

Thus, ASC 830-10-45-2 requires that the assets, liabilities, and operations of a foreign entity be measured in the

functional currency of that entity.

A reporting entity must determine the functional currency of each foreign entity (distinct and separable operation)

included in its consolidated financial statements. The choice of functional currency often depends on the

relationship between the reporting entity (parent) and foreign operation (subsidiary). However, if the currency of

the primary economic environment is highly inflationary, the parent's reporting currency should be adopted.

The functional currency should not change unless there are significant changes in economic facts and

circumstances. Changes in the functional currency should be reported prospectively from the date of change.

Therefore, previously issued financial statements are NOT restated for a change in the functional currency.

This chapter addresses the following key principles of determining the functional currency:

✓ Classes of Foreign Operations

✓ Factors in Determining the Functional Currency

✓ Highly Inflationary Environment

✓ Change in the Functional Currency

6

B. Classes of Foreign Operations

For purposes of determining functional currency, ASC 830-10-45-4 divides foreign operations into two broad

classes:

1. Self-contained and integrated within a particular country or economic environment: If a foreign

subsidiary's activities are situated within one country, are basically self-contained, and do not rely on the

parent's economic environment, the subsidiary's functional currency is the currency of the country in

which it is located. For example, if a U.S. company has a foreign subsidiary in France that is an independent

entity and received cash and incurred expenses in euros, the euro is the functional currency.

2. Direct and integral component or extension of the parent entity’s operations: If the foreign subsidiary's

daily activities are a direct and important element of the parent's operations and environment, the

parent's currency will be the functional currency. In other words, the day-to-day operations are

dependent on the economic environment of the parent’s currency, and the changes in the foreign entity’s

individual assets and liabilities impact directly on the cash flows of the parent entity in the parent’s

currency. For example:

− Significant assets may be acquired from the parent entity or otherwise by expending dollars

− The sale of assets may generate dollars that are available to the parent

− Financing is primarily by the parent or otherwise from dollar sources

An entity may have more than one distinct and separable operation (e.g., branch, division). If those operations

are conducted in different economic settings, they may have different functional currencies. For example:

• A foreign entity might have one operation that sells parent-entity-produced products and another

operation that manufactures and sells foreign-entity-produced products. If they are conducted in

different economic environments, those two operations might have different functional currencies.

• A single subsidiary of a financial institution might have relatively self-contained and integrated operations

in each of several different countries.

According to ASC 830-10-55-6, in those circumstances, each operation may be considered to be an entity, and,

based on the facts and circumstances, each operation might have a different functional currency. PwC believes

that an entity should demonstrate all of the following characteristics to conclude that an operation within an

entity is distinct and separable.

7

Characteristics of a Distinct and Separable Operation

Operation is distinct and separable Operation is not distinct and separable

Separate operations

Operations are managed independently and

can be separated, both operationally and

for financial reporting purposes, from the

reporting entity’s other operations

Operations are not managed independently

or cannot be separated, either

operationally or for financial reporting

purposes, from the reporting entity’s other

operations

Assets and liabilities

Assets and liabilities of the operation can be

separated from those of the reporting

entity’s other operations and relate directly

to the operation’s activities

Assets and liabilities of the operation

cannot be separated from those of the

reporting entity’s other operations, the

operation holds only certain assets and

liabilities (e.g., receivables and inventory),

or they hold assets and liabilities that relate

directly to a reporting entity’s other

operations

Financial statements

A meaningful set of all-inclusive financial

statements could be routinely prepared for

the operation

The operation cannot produce financial

statements or produces a limited set of

financial statements

Source: PwC, Foreign currency, June 2019

The different operating and economic characteristics of various types of foreign operations will be distinguished

in their accounting. FAS 52 states that:

• The economic effects of an exchange rate change on an operation that is relatively self-contained and

integrated within a foreign country relate to the net investment in that operation. Translation

adjustments that arise from consolidating that foreign operation do NOT impact cash flows and are NOT

included in net income.

• The economic effects of an exchange rate change on a foreign operation that is an extension of the

parent's domestic operations relate to individual assets and liabilities and impact the parent's cash flows

directly. Accordingly, the exchange gains and losses in such an operation are included in net income.

• Contracts, transactions, or balances that are, in fact, effective hedges of foreign exchange risk will be

accounted for as hedges without regard to their form.

8

C. Factors in Determining the Functional Currency

It is important to determine the functional currency because remeasurement and translation are both based on

the functional currency of the entity. An entity’s functional currency is usually the currency of the primary

economic environment in which the entity operates. According to ASC 830-10-45-6, the functional currency of an

entity is, in principle, a matter of fact. In some cases, the facts will clearly identify the functional currency; in other

cases, they will not. For example, if a foreign entity conducts significant amounts of business in two or more

currencies, the functional currency might not be clearly identifiable. In those instances, the economic facts and

circumstances of a particular foreign operation should be assessed in relation to the stated objectives for foreign

currency translation.

When an entity carries out major operations in more than one currency, management must determine which

currency to use as the functional currency. ASC 830-10-55-5 provides the following economic factors that should

be considered individually and collectively when determining a foreign operation’s functional currency:

Indicator

Foreign Subsidiary’s Currency as

Functional Currency

Parent’s Currency as Functional

Currency

Cash Flow

Cash flows related to the foreign entity’s

assets and liabilities are primarily in the

foreign currency and do not directly affect

the parent entity’s cash flows.

Cash flows related to the foreign entity’s

assets and liabilities directly affect the

parent’s cash flows currently and are

readily available for remittance to the

parent entity.

Selling Price

Selling prices arise from local factors such

as competition and government law

rather than exchange rates.

Selling prices are influenced by

international factors such as worldwide

competition and international prices.

Sales Market There is a strong local sales market. The sales market is primarily in the

parent's country.

Expenses

Manufacturing costs or services are

typically incurred locally and denominated

in foreign currency.

Manufacturing and service costs are

mostly component costs obtained from

the parent's country.

Financing

Financing is secured locally and

denominated in local currency. Funds

obtained are adequate to meet debt

obligations.

Financing is mainly provided by the

parent or denominated in the parent’s

currency.

Intercompany

Transactions

Intercompany transactions are few. There

is no major interrelationship between the

parent and the foreign entity.

Intercompany transactions are high. A

substantial interrelationship exists

between the parent and foreign entity.

9

Example 2: Determination of the Functional Currency

MAX Corp. is a U.S. company that uses the U.S. dollar as its reporting currency. Sino is a wholly-owned subsidiary

of MAX located in China, which functions as a manufacturing facility of MAX.

Consider the following facts regarding Sino:

• MAX manufactures parts for one of its products at a facility in the U.S., packages the parts, and ships them

to Sino for assembly.

• Sino has a manufacturing facility in Guangzhou, China. This facility receives the parts from MAX. Sino’s

employees assemble the parts into the final product. They also test them to ensure that the quality of the

product meets MAX’s standards.

• Sino then ships the completed product back to MAX for sale to customers.

• The local currency of Sino is the yuan.

• MAX funds the expenses of Sino each month, plus a small margin.

What is the functional currency of Sino?

Solution:

According to ASC 830-10-45-4, when a foreign subsidiary is a direct and integral component or extension of the

parent entity’s operations, the parent's currency will be the functional currency. That is, the foreign subsidiary's

daily activities are a direct and important element of the parent's operations and environment.

Sino is a direct and integral extension of USA Corp’s operations because Sino’s assembly is considered a direct and

important element of MAX’s operations. Besides, Sino’s manufacturing costs are mostly component costs

obtained from MAX. Finally, Sino cannot operate without financing from MAX. Therefore, the functional currency

of Sino is the U.S. dollar, the reporting currency of its parent, MAX.

10

D. Highly Inflationary Environment

According to ASC 830-10-45-11, a highly inflationary economy is one that has cumulative inflation of

approximately 100% or more over a 3-year period. A currency in a highly inflationary environment is not

considered stable enough to serve as a functional currency and the more stable currency of the reporting parent

is to be used instead. In other words, the financial statements of a foreign entity in a highly inflationary economy

must be remeasured as if the functional currency were the reporting currency.

The International Monetary Fund of Washington, D.C. publishes information about the international inflation

rates.

ASC 830-10-45-12 explains that the determination of a highly inflationary economy must begin by calculating the

cumulative inflation rate for the three years that precede the beginning of the reporting period, including interim

reporting periods:

• If that calculation results in a cumulative inflation rate in excess of 100%, the economy is considered highly

inflationary in all instances. In other words, the inflation rate must be increasing at an average rate of

about 26% per year for three consecutive years, given compounding. Projections cannot be used to

overcome the presumption that an economy is highly inflationary.

• if that calculation results in the cumulative rate being less than 100%, historical inflation rate trends

(increasing or decreasing) and other pertinent economic factors should be considered to determine

whether such information suggests that classification of the economy as highly inflationary is appropriate.

The definition of a highly inflationary economy is necessarily an arbitrary decision. In some instances, the trend of

inflation might be as important as the absolute rate. The definition of a highly inflationary economy should be

applied with judgment.

The following example illustrates the application of ASC 830-10-45-12.

Example 3: Determination of Highly Inflation

ASC 830-10-55-23

The following Cases illustrate the application of 830-10-45-12:

• Case A: The cumulative 3-year inflation rate exceeds 100%

• Case B: The cumulative 3-year inflation rate drops below 100% but no evidence suggests that drop is other

than temporary.

• Case C: The cumulative 3-year inflation rate drops below 100% after having spiked above 100%.

Case A: Cumulative 3-Year Inflation Rate Exceeds 100%

ASC 830-10-55-24

11

Country A’s economy at the beginning of 20X9 continues to be classified as highly inflationary because the

cumulative 3-year rate is in excess of 100% (see the following table). The recent trend of declining inflation rates

should not be extrapolated to project future rates to overcome the classification that results from the calculation.

Fiscal Year X1 X2 X3 X4 X5 X6 X7 X8

Annual inflation rate 9% 8% 12% 17% 33% 52% 30% 15%

Cumulative three-year rate (a) 32% 42% 74% 137% 163% 127%

(a) Amounts are calculated as a compounded three-year inflation rate.

Case B: Cumulative 3-Year Inflation Rate Drops Below 100%

ASC 830-10-55-25

Country B’s economy at the beginning of 20X9 should continue to be classified as highly inflationary even though

the cumulative 3-year rate is less than 100% (see the following table) because there is no evidence to suggest that

the drop below the 100% cumulative rate is other than temporary and the annual rate of inflation during the

preceding 8 years has been high.

Fiscal Year X1 X2 X3 X4 X5 X6 X7 X8

Annual inflation rate 15% 28% 46% 41% 35% 29% 23% 21%

Cumulative three-year rate (a) 115% 164% 178% 146% 114% 92%

(a) Amounts are calculated as a compounded three-year inflation rate.

Case C: Cumulative 3-Year Inflation Rate Drops Below 100% After Spike

ASC 830-10-55-26

Country C’s economy at the beginning of 20X9 should no longer be classified as highly inflationary because the

cumulative 3-year rate is less than 100% (see the following table) and the historical inflation rates suggest that

the prior classification resulted from an isolated spike in the annual inflation rate.

Fiscal Year X1 X2 X3 X4 X5 X6 X7 X8

Annual inflation rate 5% 6% 4% 7% 12% 55% 18% 6%

Cumulative three-year rate (a) 16% 18% 25% 86% 105% 94%

(a) Amounts are calculated as a compounded three-year inflation rate.

E. Change in the Functional Currency

There should be consistent use of the functional currency unless significant economic changes required a change.

ASC 830 does not provide guidance on identifying significant changes in economic facts and circumstances.

However, changes in economic facts or circumstances that are considered significant are rare. E&Y identified the

following examples that may necessitate the functional currency to change:

12

✓ A foreign entity that sells only parent-produced products assumes all manufacturing functions itself.

✓ A foreign entity that sells its products only to its parent establishes a significant local sales market for

those products.

✓ The currency mix of the revenue for a given foreign entity changes.

✓ An entity with predominantly USD-based revenue changes to predominantly euro-based revenue due to

the shift in targeted consumer groups.

Moreover, when a country experiences high rates of inflation, ASC 830-10-45-11 requires a change in functional

currency (a functional currency other than the reporting currency). That is, the parent's reporting currency should

be adopted. As an example, in a highly inflationary economy, any assets recently acquired at higher prices due to

inflation will appear significantly larger than assets purchased only a few years prior.

Example 4: Change in Functional Currency

A&E, located in Mexico, is a wholly-owned subsidiary of Johnson Corp. The U.S. dollar is Johnson’s functional

currency and A&E has previously identified the peso as its functional currency. The functional currency was

identified because A&E’s sales and purchases were denominated primarily in peso, as were all of its labor costs.

During the second quarter, A&E’s operations began to change. A&E’s sales decreased due to a loss of some sizable

contracts while Johnson’s sales increased due to new significant contracts. To meet its sales orders, Johnson began

using A&E’s manufacturing facilities. A&E shut down its sales department since it will no longer need to generate

its own sales and more than 70% will originate from Johnson’s operations. Johnson has built a new facility to

produce the materials needed. As of the end of the fiscal year, A&E began receiving all materials from Johnson

instead of from suppliers.

Based on the changes in A&E’s business, it expects cash inflows and outflows, except for wages, primarily to be

denominated in U.S. dollars. A&E’s functional currency may have changed because of the following significant

changes in economic facts and circumstances:

• The currency of revenues has changed from the peso to primarily the US dollar. This change does not

seem to be short-term as the sales department was closed down.

• The currency of cash outflows for materials has changed to the US dollar. As Johnson has built a new

facility to produce these materials, this change does not seem to be short-term either.

• The position of A&E’s operations within Johnson’s overall operating strategy has changed, from a

relatively self-contained operating entity to an extension of Johnson’s manufacturing operation.

As discussed, once a determination of the functional currency is made, that decision should be consistently used

for each foreign entity unless significant changes in economic facts and circumstances indicate clearly that the

functional currency has changed. Changes resulting from economic factors (e.g. inflation) should not be

considered a change in accounting principles. Thus, previously issued financial statements should NOT be restated

for any change in the functional currency in accordance with ASC 830-10-45-7. In other words, a change in the

13

functional currency is treated as a change in estimate. Such change is accounted for on a prospective basis (only

over current and future years).

In general, entities should follow these requirements for a change in functional currency:

1. Change from reporting currency to foreign currency: ASC 830-10-45-9 indicates that the adjustment

attributable to a currency-rate translation of nonmonetary assets as of the date of the change should be

reported in other comprehensive income.

ASC 830-10-45-9 does NOT apply to circumstances in which the functional currency changes from the

reporting currency to a foreign currency because the economy is no longer highly inflationary. Instead, ASC

830-10-45-15 should be followed.

2. Change from foreign currency to reporting currency: ASC 830-10-45-10 indicates that translation

adjustments for prior periods should NOT be removed from equity.

The translated amounts for nonmonetary assets at the end of the prior period become the accounting

basis for those assets in the period of the change and subsequent periods. This guidance should be used

also to account for a change in functional currency from the foreign currency to the reporting currency

when an economy becomes highly inflationary.

A change in accounting estimate is accounted for on a prospective basis (only over current and future years.) It

should NOT be accounted for by restating or retrospectively adjusting amounts reported in financial statements

of prior periods or by reporting pro forma amounts for prior periods.

As discussed, ASC 830-10-45-15 specifically applies to functional currency changes from the reporting currency to

a foreign currency due to a change in an inflationary economy. When an entity’s subsidiary’s functional currency

changes from the reporting currency back to the local currency because the economy ceases to be considered

highly inflationary, the entity should restate the functional currency accounting bases of nonmonetary assets and

liabilities at the date of the change as follows:

✓ The reporting currency amounts at the date of change should be translated into the local currency at

current exchange rates.

✓ The translated amounts should become the new functional currency accounting basis for the

nonmonetary assets and liabilities

ASC 830 provides the following example to illustrate the application of ASC 830-10-45-15.

Example 5: Functional Currency Changes Because the Economy is No Longer Highly Inflationary

ASC 830-10-55-13

A foreign subsidiary of a U.S. entity operating in a highly inflationary economy purchased equipment with a 10-

year useful life for 100,000 local currency (LC) on January 1, 20X1. The exchange rate on the purchase date was

LC 10 to USD 1, so the U.S. dollar equivalent cost was USD 10,000. On December 31, 20X5, the equipment has a

net book value on the subsidiary’s local books of LC 50,000 (original cost of LC 100,000 less accumulated

14

depreciation of LC 50,000) and the current exchange rate is LC 75 to the U.S. dollar. In the U.S. parent’s financial

statements, annual depreciation expense of USD 1,000 has been reported for each of the past 5 years, and on

December 31, 20X5, the equipment is reported at USD 5,000 (foreign currency basis measured at the historical

exchange rate).

ASC 830-10-55-14

As of the beginning of 20X6, the economy of the subsidiary ceases to be considered highly inflationary. Under

paragraph 830-10-45-15, a new functional currency accounting basis for the equipment would be established as

of January 1, 20X6, by translating the reporting currency amount of USD 5,000 into the functional currency at the

current exchange rate of LC 75 to the U.S. dollar. The new functional currency accounting basis at the date of

change would be LC 375,000. For U.S. reporting purposes, the new functional currency accounting basis and

related depreciation would subsequently be translated into U.S. dollars at current and average exchange rates,

respectively.

The Securities and Exchange Commission (SEC) indicates that registrants with foreign operations in economies

that have recently experienced economic turmoil should evaluate whether significant changes in economic facts

and circumstances have occurred that warrant reconsideration of their functional currencies.

The SEC also noted that ASC 830 does not prescribe specific disclosures about a change in functional currency.

However, the SEC believes that disclosures in the financial statements and MD&A may be necessary to permit an

investor to understand the foreign operations and their impact on the registrant's results of operations, liquidity,

and cash flows.

Details of the SEC’s view on changes in functional currency are addressed below.

The SEC’s View on Changes in Functional Currency

Excerpt from the SEC publication Division of Corporation Finance: Frequently Requested Accounting and Financial

Reporting Interpretations and Guidance

D. Changes in Functional Currency

FASB Statement No. 52, Foreign Currency Translation [ASC 830], requires the assets, liabilities, and operations of

a foreign operation to be measured using the functional currency of that foreign operation. The functional

currency is the currency of the primary economic environment in which the entity operates, normally the currency

in which the operation generates and expends cash. Appendix A to SFAS 52 provides guidance for determination

of the functional currency. Once the functional currency has been determined, SFAS 52 requires that

determination to be used consistently unless significant changes in economic facts and circumstances indicate

clearly that the functional currency has changed.

Registrants with foreign operations in economies that have recently experienced economic turmoil should

evaluate whether significant changes in economic facts and circumstances have occurred that warrant

reconsideration of their functional currencies. Registrants with foreign operations in economies that have adopted

15

the Euro currency should make similar evaluations. Determination of the functional currency is also required when

the economy in which a foreign operation is located ceases to be highly inflationary.

The staff would expect a registrant's analysis to focus on factors that affect the specific foreign operation's cash

flows. For example, problems in an Asian economy could cause local currency cash flow sources to severely

diminish for a self-contained foreign operation and clearly indicate a different primary currency. Conversely, these

problems generally would not indicate a change in functional currency for a foreign operation that is an integral

component or extension of the parent company's operations. The staff generally will be skeptical that currency

exchange rate fluctuations alone would cause a self-contained foreign operation to become an extension of the

parent company. Remeasurement of assets and results using the registrant's reporting currency in lieu of

determining the functional currency is appropriate only when the foreign operations are in a highly inflationary

economy as defined by SFAS 52.

SFAS 52 does not prescribe specific disclosures about a change in functional currency. However, the staff believes

that disclosures in the financial statements and MD&A may be necessary to permit an investor to understand the

foreign operations and their impact on the registrant's results of operations, liquidity, and cash flows. Registrants

should consider the need to disclose the nature and timing of the change, the actual and reasonably likely effects

of the change, and economic facts and circumstances that led management to conclude that the change was

appropriate. The effects of those underlying economic facts and circumstances on the registrant's business should

also be discussed in MD&A.

16

Review Questions – Section 1 1. In preparing consolidated financial statements of a U.S. parent company with a foreign subsidiary, what is the

foreign subsidiary's functional currency?

A. The currency in which the subsidiary maintains its accounting records

B. The currency of the country in which the subsidiary is located

C. The currency of the country in which the parent is located

D. The currency of the environment in which the subsidiary primarily generates and expends cash

2. What is the currency in which the parent company prepares its financial statements?

A. The functional currency

B. The reporting currency

C. The historical currency

D. The base currency

3. The economic effects of a change in foreign exchange rates on a relatively self-contained and integrated

operation within a foreign country relate to the net investment by the reporting enterprise in that operation.

What can be said about the translation adjustments that arise from the consolidation of that operation?

A. They directly affect cash flows but should not be reflected in income

B. They directly affect cash flows and should be reflected in income

C. They do not directly affect cash flows and should not be reflected in income

D. They do not directly affect cash flows but should be reflected in income

4. Which of the following is considered a highly inflationary environment?

A. A cumulative inflation rate of 100% or more over a three-year period

B. A cumulative inflation rate of 50% per year over a five-year period

C. A cumulative inflation rate of 25% per year over a four-year period

D. A cumulative inflation rate of 15% per year over a two-year period

17

III. Remeasure Foreign Currency

Transactions to the Functional Currency “If an entity’s books of record are not maintained in its functional currency, remeasurement into the functional

currency is required. That remeasurement is required before translation into the reporting currency.”

ASC 830-10-45-17

A. General Rules

Common foreign currency transactions denominated in a currency other than the entity’s functional currency

arise when a reporting entity:

1. Buys or sells on credit goods or services whose prices are denominated in foreign currency,

2. Borrows or lends funds and the amounts payable or receivable are denominated in foreign currency,

3. Is a party to an unperformed forward exchange contract,

4. Acquires or disposes of assets denominated in foreign currency, or

5. Incurs or settles liabilities.

For example, foreign currency transactions may result in receivables or payables fixed in the amount of foreign

currency to be received or paid. If books and records of a foreign entity are not maintained in the functional

currency, foreign currency transactions must be remeasured into the functional currency. For example, the U.S.

dollar has been designated as the functional currency for a Mexican subsidiary, but books and records at the

subsidiary are recorded using the Mexican peso. In this case, remeasurement is required since the subsidiary’s

book of records is maintained in peso instead of its functional currency (U.S. dollar).

The objective of the remeasurement process is to generate the same result as if the entity's books and records had

been kept in the functional currency. To achieve the objective, ASC 830-10-45-17 requires entities to account for

its monetary and nonmonetary assets and liabilities that are not denominated in the functional currency. ASC 830-

20-30-1 states that at the date a foreign currency transaction is recognized, each asset, liability, revenue, expense,

gain, or loss arising from the transaction should be measured initially in the functional currency of the recording

entity using the current exchange rate.

If exchangeability between two currencies is temporarily lacking at the transaction date or balance sheet date,

ASC 830-20-30-2 requires the use of the first subsequent rate at which exchanges could be made. If the lack of

exchangeability is other than temporary, the propriety of consolidating, combining, or accounting for the foreign

operation by the equity method should be carefully considered.

Example 6: Remeasurement Requirements

Johnson Corp. is a U.S. company. Johnson’s functional currency is the U.S. dollar.

18

Johnson borrows 3,000,000 Swiss francs from a bank in Switzerland in the form of a note payable bearing interest

at 8% per annum. This is a foreign currency transaction entered into by Johnson resulting in recognition of

monetary assets and liabilities denominated in a foreign currency (cash, note payable, and interest payable).

Therefore, remeasurement is required.

B. Selection of Exchange Rates for Remeasurement

Monetary Accounts

Monetary accounts are remeasured at the current exchange rate. Monetary accounts include assets and liabilities

whose amounts are fixed or determinable without reference to future prices of specific goods or services.

Examples include cash, short- or long-term accounts receivable and notes receivable in cash, short- or long-term

accounts payable and notes payable in cash, and inventories carried at market, and marketable securities carried

at fair value.

At each balance sheet date, balances related to monetary assets and liabilities should be remeasured to reflect

the current exchange rate. This measurement gives rise to foreign currency transaction gains or losses; the

increase or decrease in expected functional currency cash flows. For example, if the exchange rate changes

between the date of a purchase or sale and the time of actual payment or receipt, a foreign exchange transaction

gain or loss arises.

Details about transaction gains or losses are discussed in the “Transaction Gains or Losses” section.

Nonmonetary Accounts

Nonmonetary accounts should be remeasured using historical exchange rates (i.e. the exchange rate at the date

of the nonmonetary account originated). Nonmonetary accounts include assets and liabilities other than

monetary ones. The economic significance of nonmonetary accounts depends heavily on the value of specific

goods and services. According to ASC 255 Changing Prices, nonmonetary assets include all of the following:

✓ Goods held primarily for resale or assets held primarily for direct use in providing services for the

business of the entity

✓ Claims to cash in amounts dependent on future prices of specific goods or services

✓ Residual rights such as goodwill or equity interests

Nonmonetary liabilities include both of the following:

✓ Obligations to furnish goods or services in quantities that are fixed or determinable without reference

to changes in prices.

✓ Obligations to pay cash in amounts dependent on future prices of specific goods or services.

19

Examples include inventories, investments in common stocks, property, plant and equipment, and liabilities for

rent collected in advance.

It is important to note that nonmonetary assets and liabilities are NOT subsequently remeasured. Once purchased

or incurred, nonmonetary assets and liabilities are recorded in the functional currency of the purchaser. Likewise,

amounts recognized in the income statement related to nonmonetary assets and liabilities (e.g. cost of goods sold,

depreciation) are accounted for in the functional currency of the purchaser.

ASC 830-10-45-18 lists the following common balance sheet and income statement accounts that should be

remeasured using historical exchange rates.

Accounts to Be Remeasured Using Historical Exchange Rates

• Equity securities without readily determinable

fair values accounted for in accordance with

paragraph 321-10-35-2. The historical rate to

be used shall be the exchange rate as of the

later of the acquisition date or the most recent

date on which the equity security was adjusted

to fair value in accordance with paragraphs

321-10-35-2 through 35-3, if applicable

(Amended by ASU 2019-04 Codification

Improvements to Topic 326, Financial

Instruments—Credit Losses, Topic 815,

Derivatives and Hedging, and Topic 825,

Financial Instruments)

• Inventories carried at cost

• Prepaid expenses such as insurance,

advertising, and rent

• Property, plant, and equipment

• Accumulated depreciation on property, plant,

and equipment

• Patents, trademarks, licenses, and formulas

• Goodwill

• Other intangible assets

• Deferred charges and credits, except deferred

income taxes and policy acquisition costs for life

insurance companies

• Deferred income

• Common stock

• Preferred stock carried at issuance price

• Examples of revenues and expenses related to

nonmonetary items:

− Cost of goods sold

− Depreciation of property, plant, and

equipment

− Amortization of intangible items such as

goodwill, patents, licenses, etc.

− Amortization of deferred charges or credits

except for deferred income taxes and

policy acquisition costs for life insurance

companies

20

C. Transaction Gains or Losses

Transaction gains or losses should be included in the income statement (net income from continuing operations)

for the period in which the exchange rate changes. This accounting treatment was adopted because transaction

gains or losses on remeasurement affect functional currency cash flows.

However, ASC 830-20-35-3 requires that transaction gains or losses on the following foreign currency transactions

should NOT be included in determining net income. Instead, they should be reported in the same manner as

translation adjustments (reported in other comprehensive income):

1. Foreign currency transactions engaged in net investment hedges in a foreign entity, beginning as of the

designation date. A foreign currency transaction is deemed a hedge of an identifiable foreign currency

commitment provided BOTH of the following two conditions exist:

✓ The foreign currency commitment is firm; and

✓ The foreign currency transaction is intended as a hedge.

A net investment hedge protects against adverse movement of exchange rates impacting any foreign

currency exposure. A foreign currency hedge can, for example, involve either fair value or cash flow

hedges in foreign currency or a net investment in a foreign business activity when there is concern over

the impact that a devaluation of a foreign currency would have on the entity’s investment in an overseas

subsidiary.

Details about foreign currency hedge are discussed in the “Hedging” section.

2. Intra-entity foreign currency transactions that are of a long-term investment nature (settlement is not

planned or anticipated in the foreseeable future), when the entities to the transactions are consolidated,

combined, or accounted for under the equity method in the reporting company's financial statements.

Reporting requirements of translation adjustments are discussed in the “Translation Adjustments” section.

Example 7: Determining Transaction Gains or Losses

Example 7-1

On September 14, 20X2, ABC Company bought goods from an unaffiliated foreign company for 30,000 units of the

foreign company's local currency. On that date, the spot rate was $.57. ABC paid the bill in full on March 27, 20X3,

when the spot rate was $.64. The spot rate was $.68 on December 31, 20X2. ABC should report as a foreign

currency transaction loss $3,300 in its income statement for the year ended December 31, 20X2, calculated as

follows:

Liability—12/31/20X2: 30,000 × $.68 $20,400

Liability—9/14/20X2: 30,000 × $.57 17,100

Foreign currency transaction loss at 12/31/20X2: 30,000 × $.11 $ 3,300

21

Example 7-2

On September 1, a U.S. company bought foreign goods requiring payment in euros (EUR) in 30 days after their

receipt. The title to the merchandise passed on November 15. The goods were still in transit on November 30, the

fiscal year-end. The exchange rates were:

September 1: USD 1 = EUR 2.2

November 15: USD 1 = EUR 2.0

November 30: USD 1 = EUR 2.1

The transaction was recorded on November 15, when title to the merchandise passed, and was recorded at an

exchange rate of USD 1 = EUR 2.0 (i.e., it would cost $.5 to buy one euro). On November 30, the exchange rate

increased to 2.1 euros (it would cost less than $.5 to buy one euro). Because the dollar equivalent of the liability

declined from November 15 to November 30, it gave rise to a gain included in income from continuing operations.

Example 7-3

An exchange gain or loss takes place when the exchange rate changes between the purchase and payment dates.

Merchandise is purchased for 300,000 euros. The exchange rate is 3 euros to 1 U.S. dollar. The journal entry is:

Purchases $100,000

Accounts payable $100,000

300,000 euros/3 = $100,000

When the goods are paid for, the exchange rate is 3.5 euros to 1 U.S. dollar. The journal entry is:

Accounts payable $100,000

Cash $85,714

Foreign exchange gain 14,286

300,000 euros/3.5 = $85,714

The $85,714, using an exchange rate of 3.5 to 1, can buy 300,000 euros. The transaction gain is the difference

between the cash required of $85,714 and the initial liability of $100,000.

Example 7-4

Klemer Corporation bought merchandise for 240,000 pesos when the exchange rate was 12 pesos to a dollar. The

journal entry expressed in dollars follows:

Purchases $20,000

Accounts payable $20,000

When the merchandise is paid for, the exchange rate changes to 15:1. The journal entry in dollars is:

Accounts payable $20,000

Cash $18,667

22

Foreign exchange gain $ 1,333

At a 15:1 exchange rate, $18,667 can buy 240,000 pesos. The difference between $18,667 and the initial

liability of $20,000 represents a foreign exchange gain. If payment is made when the exchange rate is below 12

pesos to a dollar, a foreign exchange loss would arise.

D. Foreign Currency Transactions

1. Property, Plant and Equipment

Property, plant and equipment whose values change substantially over time are considered nonmonetary assets.

When property, plant and equipment are acquired in a foreign currency, they should be recorded in the functional

currency using the exchange rate on the date of purchase. They should NOT be subsequently remeasured for

changes in exchange rates during the period they are held.

The entity should perform the impairment evaluation using its functional currency. Impairment testing may result

in a functional currency impairment or a reversal of local currency impairments. That is, when an entity keeps its

books and records in a currency other than its functional currency (local currency), it is possible that an asset is

not impaired for its local currency books, but is impaired for its functional currency financial statements (or vice

versa). In this case, an entity should either record or reverse impairment charges to produce its functional currency

financial statements.

Example 8: Depreciation of Fixed Assets

TEX Corp. is a U.S. company with a U.S. dollar functional currency. ViTa is a foreign entity of TEX located in

Switzerland. ViTa keeps its books and records in the local currency, Swiss franc (CHF). However, management

determined its functional currency is the euro (EUR).

ViTa purchased machinery for CHF 600,000 on January 1, 20X5 when the exchange rate was EUR 1.2 = CHF 1. The

machinery has a useful life of five years.

How should ViTa account for annual depreciation expense in the currency of its books and records, Swiss franc,

and its functional currency (EUR)?

Solution:

ViTa should record the machinery using the exchange rate in effect at the date of purchase.

CHF 600,000 × [1.2 EUR / 1 CHF] = EUR 720,000.

ViTa should also calculate annual depreciation using the exchange rate in effect on the date of purchase. The

following table shows the calculation of the annual depreciation expense.

23

CHF EUR

Purchase price CHF 600,000 EUR 720,000

Useful life 5 years 5 years

Annual depreciation 120,000 144,000

Changes in exchange rates subsequent to the purchase of the machinery do NOT affect depreciation or the

carrying amount of the machinery in the functional currency financial statements.

2. Inventories

Inventory measured using the subsequent measurement guidance in ASC 330-10 in an entity’s books of record

that are maintained in a foreign currency requires special application of ASC 830.

ASC 830-10-55-8 requires that inventories carried at cost in the books of record in another currency should be

first remeasured to cost in the functional currency using historical exchange rates. Then, the historical cost in the

functional currency should be evaluated for impairment under the subsequent measurement guidance using the

functional currency, which may require a write-down in the functional currency statements even though no write-

down has been made in the books of record maintained in another currency. Similarly, a write-down in the books

of record may need to be reversed if the application of the subsequent measurement guidance in the functional

currency does not require a write-down. If inventory has been written down to market in the functional currency

statements, that functional currency amount should continue to be the carrying amount in the functional currency

financial statements until the inventory is sold or a further write-down is necessary. That is, the write-down should

not be reversed until the inventory is sold.

ASC 830-10-55-9 states that an inventory write-down may occur if the value of the currency in which the books of

record are maintained has declined in relation to the functional currency between the date the inventory was

acquired and the date of the balance sheet. However, such a write-down may not be necessary. For example, a

write-down may not be necessary for inventory measured using the first-in, first-out (FIFO) methodology if the

net realizable value expressed in the local currency has increased sufficiently so that net realizable value exceeds

its historical cost measured in the functional currency.

ASC 830 provides the following example to illustrate the application of ASC 830-10-55-9 (Amended by ASU 2015-

11 Inventory).

Example 9: Write-down of Inventory Measured Using FIFO

ASC 830-10-55-15

The following cases illustrate the remeasurement of inventory that is measured using FIFO and is not recorded in

the functional currency:

a. Historical cost in functional currency exceeds net realizable value in functional currency (Case A)

b. Net realizable value in functional currency exceeds historical cost in functional currency (Case B)

24

ASC 830-10-55-16

Cases A and B share all of the following assumptions:

a. BR is the currency in which the books of record are maintained.

b. FC is the functional currency.

c. When the rate is BR 1 = FC 2.40, a foreign subsidiary of a U.S. entity purchases a unit of inventory at a cost

of BR 500 (measured in functional currency, FC 1,200).

d. At the foreign subsidiary’s balance sheet date, the current rate is BR 1 = FC 2.00.

Case A: Historical Cost in Functional Currency Exceeds Net Realizable Value in Functional Currency

ASC 830-10-55-18

Assume the net realizable value of the unit of inventory is BR 560 (measured in functional currency, FC 1,120).

Because net realizable value as measured in the functional currency (FC 1,120) is less than historical cost as

measured in the functional currency (FC 1,200), an inventory write-down of FC 80 is required in the functional

currency financial statements.

Case B: Net Realizable Value in Functional Currency Exceeds Historical Cost in Functional Currency

ASC 830-10-55-19

Assume the net realizable value at the foreign subsidiary’s balance sheet date is BR 620. Because net realizable

value as measured in the functional currency (BR 620 x FC 2.00 = FC 1,240) exceeds historical cost as measured in

the functional currency (BR 500 x FC 2.40 = FC 1,200), an inventory write-down is not required in the functional

currency financial statements.

3. Debt

When a debt is denominated in a currency other than its functional currency, it should initially be measured using

the exchange rate in effect at the issuance date. Because a debt is a monetary liability, the debt balance is

remeasured in the functional currency each reporting date using the exchange rate in effect at the reporting date.

Debt premium, discount, and debt issuance costs should be included in the balance measured in the reporting

entity’s functional currency since they are part of the carrying amount of the debt. By measuring the premium,

discount, and issuance costs at current exchange rates, an entity ensures that a level of effective yield in the

foreign currency is maintained.

ASC 830 does not identify the rates at which amortization of the discounts or premiums should be reported in the

income statement. However, PwC believes that it is acceptable to record amortization for a period using the

average spot rate for that period since the amortization is occurring throughout the period.

25

An exchange of debt instruments between or a modification of a debt instrument resulting in more than a 10%

change in cash flows is treated as an extinguishment and issuance of new debt (the 10% test). When a debt

instrument is modified such that the currency of the debt changes, the change in currency should be included in

the cash flows as part of the 10% test. To convert the cash flows on the new debt into the currency of the original

debt, PwC identifies two acceptable methods:

1. Use the spot rate in effect at the debt modification date, or

2. Use the forward rates corresponding to the payment date of each cash flow (e.g. interest payment and

principal).

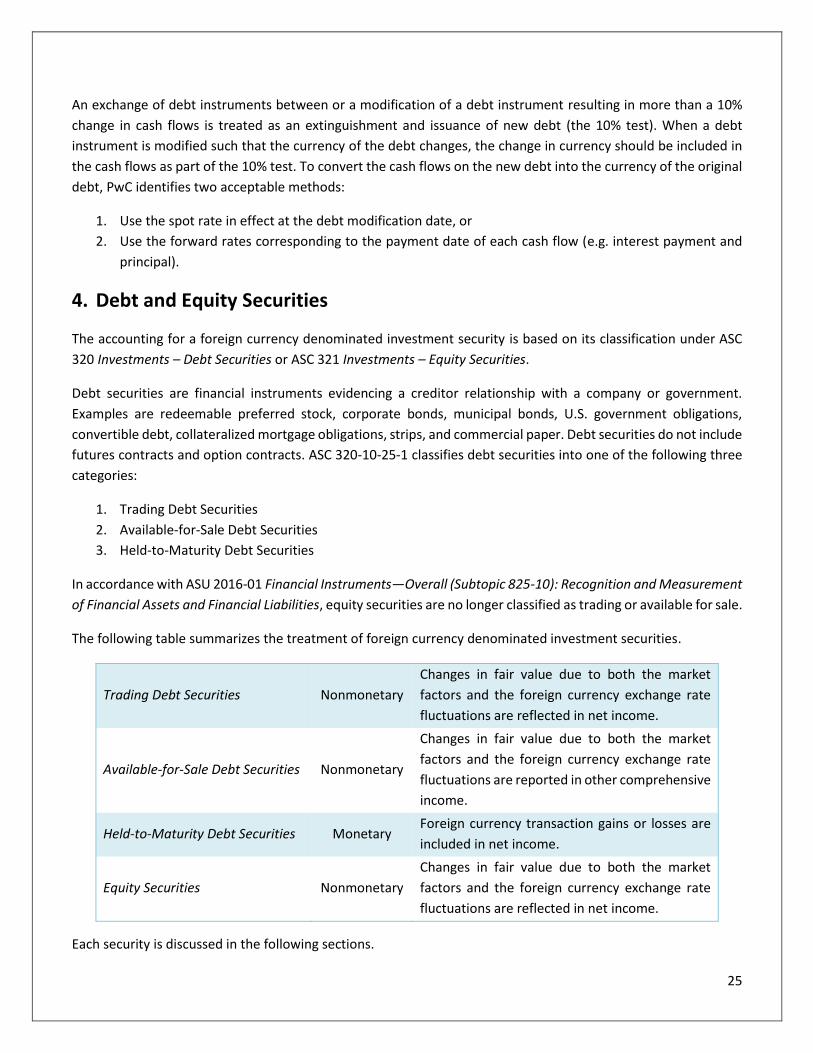

4. Debt and Equity Securities

The accounting for a foreign currency denominated investment security is based on its classification under ASC

320 Investments – Debt Securities or ASC 321 Investments – Equity Securities.

Debt securities are financial instruments evidencing a creditor relationship with a company or government.

Examples are redeemable preferred stock, corporate bonds, municipal bonds, U.S. government obligations,

convertible debt, collateralized mortgage obligations, strips, and commercial paper. Debt securities do not include

futures contracts and option contracts. ASC 320-10-25-1 classifies debt securities into one of the following three

categories:

1. Trading Debt Securities

2. Available-for-Sale Debt Securities

3. Held-to-Maturity Debt Securities

In accordance with ASU 2016-01 Financial Instruments—Overall (Subtopic 825-10): Recognition and Measurement

of Financial Assets and Financial Liabilities, equity securities are no longer classified as trading or available for sale.

The following table summarizes the treatment of foreign currency denominated investment securities.

Trading Debt Securities Nonmonetary

Changes in fair value due to both the market

factors and the foreign currency exchange rate

fluctuations are reflected in net income.

Available-for-Sale Debt Securities Nonmonetary

Changes in fair value due to both the market

factors and the foreign currency exchange rate

fluctuations are reported in other comprehensive

income.

Held-to-Maturity Debt Securities Monetary Foreign currency transaction gains or losses are

included in net income.

Equity Securities Nonmonetary

Changes in fair value due to both the market

factors and the foreign currency exchange rate

fluctuations are reflected in net income.

Each security is discussed in the following sections.

26

Trading Debt Securities

Trading debt securities (not classified as held-to-maturity) are bought and held primarily for sale in the near term

(usually three months or less). Trading debt securities are considered nonmonetary assets since the amount

received depends on the future prices of specific goods or services. Thus, these debt securities do NOT give rise

to transaction gains and losses. However, trading debt securities should be subsequently measured at fair value,

with changes in fair value (including changes in market price and foreign currency exchange rates) reflected in net

income (presented separately in the income statement).

Available-for-Sale Debt Securities

Available-for-sale debt securities are not held for short-term profits, nor are they to be held to maturity.

Therefore, they are in between trading and held-to-maturity classifications. In other words, investments in debt

securities not classified as trading debt securities or as held-to-maturity debt securities should be classified as

available-for-sale debt securities.

Available-for-sale debt securities are considered nonmonetary assets since the amount received depends on

future prices of specific goods or services. Thus, these debt securities do NOT give rise to transaction gains and

losses. However, according to ASC 830-20-35-6, the entire change in the fair value of foreign currency

denominated available-for-sale debt securities due to both the market factors (e.g. interest rate, credit risk) and

the foreign currency exchange rate fluctuations should be reported in other comprehensive income.

Upon the adoption of ASU 2016-13 Financial Instruments—Credit Losses (Topic 326): Measurement of Credit

Losses on Financial Instruments, the change in the fair value of foreign currency denominated available-for-sale

debt securities, excluding the amount recorded in the allowance for credit losses, should be reported in other

comprehensive income.