Embed Size (px)

Citation preview

CHAPTER TEN ACCOUNTING FOR FIXED ASSETS

Introduction An asset is a resource acquired for use in a business. A distinction is made in accounting between "current assets" and " "fixed assets". Current assets are those assets that form part of the working capital of a business. They are assets whose benefits are expected to be realized within one accounting period. They are replaced frequently or converted into cash during the course of trading and therefore they are short term in nature e.g. stock, prepayments, debtors, cash and bank. A fixed asset is an asset of a business intended for continuing use, rather than a short-term, temporary asset such as stocks. Fixed assets are assets acquired for use in the business and not for resale in the ordinary course of business. Their use value extends beyond one accounting period and therefore they are long-term in nature e.g. furniture, buildings, plant and machinery, motor vehicles, fittings etc. This chapter will present the accounting for fixed assets. This chapter covers the recognition, valuation and presentation of fixed assets and the provision of depreciation expense. Objectives: After studying this chapter you should be able to:

• Identify the various types of long term assets • Distinguish between capital and revenue expenditure • Identity the relevant cost of fixed assets. • Appreciate methods of estimating depreciation expense • Draw ledger accounts for fixed assets and depreciation • Account for disposal of assets • Draw schedule of fixed assets

Key Terms Assets: Resources acquired for use in the business e.g. stock, motor vehicles Tangible Assets: Assets with a physical existence land, buildings and machinery. Intangible Assets Assets without a physical existence e.g. goodwill, patent rights. Current Assets: Assets expected to be realised within one accounting period eg cash, debtors Fixed Assets: Fixed assets are assets acquired for use in the business and not for resale in the ordinary course of business.

Classification of Long-term assets Fixed assets can be classified in a company's balance sheet as intangible, tangible, or investments. Tangible fixed assets are those fixed assets with a physical existence e.g. Land and buildings, furniture and fitting, etc. Intangible fixed assets are those fixed assets without physical existence. Examples of intangible fixed assets include:

1. Goodwill; this is an asset created by a business over time through its location, reputation skills of workers etc.

2. Patent right and trademarks; legal right to a product or an art or device of production

Accounting for fixed assets Fixed assets are resources acquired for use over a long period of time. The benefits derived from the assets are enjoyed for more than one accounting period. For instance a Lorry acquired today may be used for a period of 10 years. The cost of fixed assets is treated differently from that of rent, electricity or salaries and wages. While the cost of rent, electricity, salaries and wages are charged to the profit and loss account (that is expensed) for the year in which they are incurred, the cost of a fixed asset is not, instead it is carried forward to the next accounting period (i.e. capitalised). Revenue expenditure and capital expenditure At this point it is important to draw the distinction between capital and revenue expenditure. Revenue expenditure is the expenditure whose benefits are enjoyed within one accounting period. The cost of such expenditure is charged to profit and loss account e.g. salaries and wages, rent, electricity etc. Capital expenditure is the expenditure whose benefits run beyond one accounting period, therefore the cost is not charged in the year in which it is incurred instead it is capitalized. Capitalization means that it is recognized as a balance available for use for the next year and subsequent years. Relevant cost of a fixed asset The amount that is recognised as the cost of a fixed asset in the books of accounts includes all amounts incurred to acquire the asset (either purchase cost or construction costs) and any amounts that can be directly attributed to bringing the asset into working condition. The cost of acquisition includes the purchase price (net of trade discounts and rebate), including import duties and non-refundable purchase taxes. Directly attributable costs may include:

- Delivery costs - Costs associated with acquiring the asset such as stamp duty and import duties - Costs of preparing the site for installation of the asset - Professional fees, such as legal fees and architects' fees

Note that general overhead costs or administration costs should not be included as part of the total costs of a fixed asset (e.g. the costs of the factory building in which the asset is kept or the cost of the maintenance team who keep the asset in good working condition). The cost of subsequent expenditure on a fixed asset will be added to the cost of the asset

provided that this expenditure enhances the benefits of the fixed asset or restores any benefits consumed. This means that major improvements or a major overhaul may be capitalised and included as part of the cost of the asset in the accounts. However, the costs of repairs or overhauls that are carried out simply to maintain existing performance will be treated as expenses of the accounting period in which the work is done, and charged in full as an expense in that period. Accounting for the use of fixed assets A fixed asset is used for a number of years. The benefits that a business obtains from a fixed asset extend over several years. By accepting that the life of a fixed asset is limited, the accounts of a business need to recognise the benefits of the fixed asset as it is "consumed" over several years. The cost must be allocated to the years in use. The process of allocating the cost of an asset to the years in use is known as depreciation. Depreciation may be seen as the amount of consumption of a fixed asset. Depreciation may be defined as “Loss of value of an asset or other reduction in the useful life of a tangible fixed asset whether arising from use, passage of time or obsolescence through either changes in technology or demand for goods and services produced by the asset”. Methods of estimating depreciation Depreciation, which is the allocation of the expense that reflects the "using up" of capital assets employed by the entity, is subject to a number of different calculation approaches. Conceptually, this allocation is done over the useful life of the asset in a "systematic and rational" manner. An asset may be seen as having a physical life and an economic life. Most fixed assets suffer physical deterioration through usage and the passage of time. Although care and maintenance may succeed in extending the physical life of an asset, typically it will, eventually, reach a condition where the benefits have been exhausted. However, a business may not wish to keep an asset until the end of its physical life. There may be a point when it becomes uneconomic to continue to use the asset even though there is still some physical life left. The economic life of the asset will be determined by such factors as technological progress and changes in demand. For purposes of calculating depreciation, it is the estimated economic life rather than the potential physical life of the fixed asset that is used. At the end of the useful life of a fixed asset the business will dispose it off and any amounts received from the disposal will represent its residual value. This, again, may be difficult to estimate in practice. However, an estimate has to be made. If it is unlikely to be a significant amount, a residual value of zero will be assumed. The cost of a fixed asset less its estimated residual value represents the total amount to be depreciated over its estimated useful life. In order to calculate the amount of depreciation that should be charged to earnings during any period of an asset’s useful life, the following information is needed:

i) The original cost or other original basis that was used to reflect the value of the asset at the time it was put into service.

ii) An estimate of the pattern of flow of benefits from the assets over the expected useful life.

iii) The salvage value of the asset, which is an estimate of what the asset will be worth at the end of its useful life.

As is noticed, the method of depreciation may vary from one asset to the other and also from one organisation to the other. The following are some of the popular deprecation methods:

1. Straight line method 2. Reducing balance method (Accelerated Depreciation method)

i) Fixed rate of reducing balance ii) Double-Declining Balance Method iii) Usage method iv) Sum of digits method v) Revaluation method.

STRAIGHT LINE METHOD This is a method that charges depreciation equally to all the years in use. The depreciation base (or depreciable amount) is evenly allocated over the lifetime of the asset, resulting in equal annual depreciation. Depreciable amount is cost of asset less residue value. The residue value is the resale value expected at the end of the assets useful life. Depreciation charge per year is given by: Cost of asset Estimated useful life (economic life) Example: XYZ limited acquired an item of motor vehicle at a cost of Ksh. 5,000,000. The estimated useful life of the asset is 5 years. XYZ uses straight-line method of charging depreciation. Required. i) Calculate the annual depreciation

ii) Suppose it is expected that the motor vehicle will be sold for Ksh. 1,000,000 at the end of its useful life. What will be the annual depreciation?

Suggested solution i) Depreciation = cost of assets = 5,000,000 = Ksh. 1,000,000 Estimated useful life 5 ii) Depreciation = Cost – residue value = 5,000,000 – 1,000,000 = Ksh 800,000 Estimated useful life 5

Note that Straight-line depreciation may be charged as a fixed percentage of cost i.e.

Depreciation rate = annual depreciation x 100 Cost of asset

Annual depreciation = Cost of asset x depreciation rate. Changes in depreciation in the straight-line method Depreciation under straight line depends on the estimate of useful life and residue value. This estimate may be found to be inappropriate after a number of years use. In such a case it is necessary to change depreciation charge accordingly. If there is a change in estimated useful life (with no residue value) , the new depreciation charge will be: New depreciation = Book value at time of change Remaining estimated useful life Example XYZ ltd bought an item of plant at a cost of sh. 5,000,000. Depreciation is charged on straight line with an estimated useful life of 10yrs. After 3 years of use, it is estimated that the asset will be used for a further 5 years only. Required: Compute the new depreciation charge per annum. Suggested solution (Yr 1 to 3) depreciation = cost = 5,000,000 = 500,000 Number of years 10 (AFTER 3RD YR) depreciation = 5,000,000 – (3 x 500,000) = 700,000 5 A change in estimated residue value is rare but if there is , the new depreciation charge will be: New depreciation = Book value at time of change-new estimated residue Remaining estimated useful life Advantages of straight line method 1 Easy to understand and simple to operate 2) It is frequently used in practice. 3) It requires little work for calculating depreciation amounts. 4) Constant annual charges, which ensures comparable cost charges.

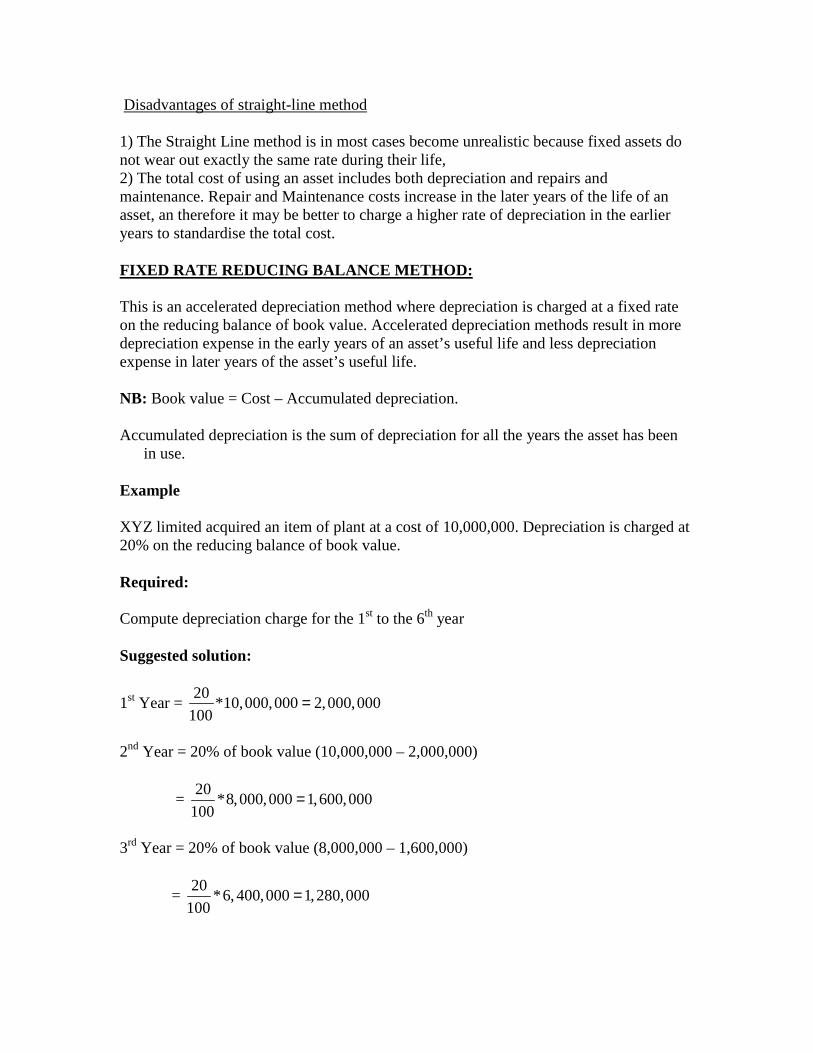

Disadvantages of straight-line method 1) The Straight Line method is in most cases become unrealistic because fixed assets do not wear out exactly the same rate during their life, 2) The total cost of using an asset includes both depreciation and repairs and maintenance. Repair and Maintenance costs increase in the later years of the life of an asset, an therefore it may be better to charge a higher rate of depreciation in the earlier years to standardise the total cost. FIXED RATE REDUCING BALANCE METHOD: This is an accelerated depreciation method where depreciation is charged at a fixed rate on the reducing balance of book value. Accelerated depreciation methods result in more depreciation expense in the early years of an asset’s useful life and less depreciation expense in later years of the asset’s useful life. NB: Book value = Cost – Accumulated depreciation. Accumulated depreciation is the sum of depreciation for all the years the asset has been

in use. Example XYZ limited acquired an item of plant at a cost of 10,000,000. Depreciation is charged at 20% on the reducing balance of book value. Required: Compute depreciation charge for the 1st to the 6th year Suggested solution:

1st Year = 20

*10,000,000 2,000,000100

=

2nd Year = 20% of book value (10,000,000 – 2,000,000)

= 20

*8,000,000 1,600,000100

=

3rd Year = 20% of book value (8,000,000 – 1,600,000)

= 20

*6,400,000 1,280,000100

=

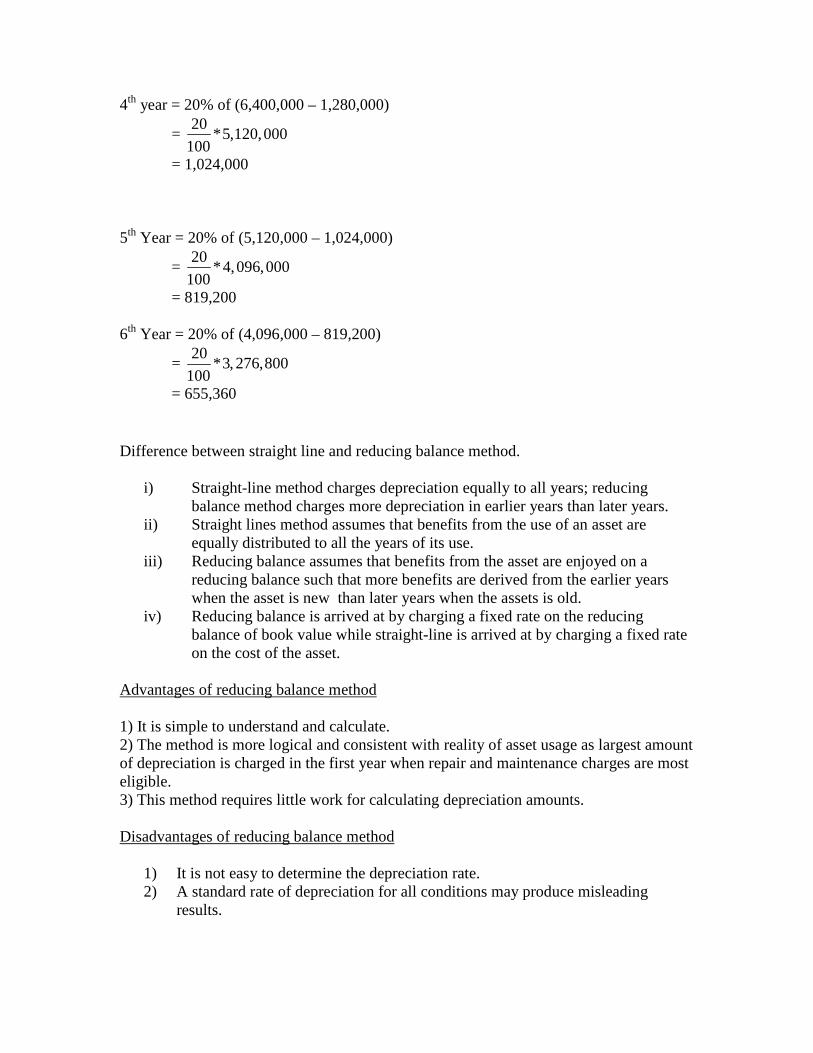

4th year = 20% of (6,400,000 – 1,280,000)

= 20

*5,120,000100

= 1,024,000 5th Year = 20% of (5,120,000 – 1,024,000)

= 20

*4,096,000100

= 819,200 6th Year = 20% of (4,096,000 – 819,200)

= 20

*3,276,800100

= 655,360

Difference between straight line and reducing balance method.

i) Straight-line method charges depreciation equally to all years; reducing balance method charges more depreciation in earlier years than later years.

ii) Straight lines method assumes that benefits from the use of an asset are equally distributed to all the years of its use.

iii) Reducing balance assumes that benefits from the asset are enjoyed on a reducing balance such that more benefits are derived from the earlier years when the asset is new than later years when the assets is old.

iv) Reducing balance is arrived at by charging a fixed rate on the reducing balance of book value while straight-line is arrived at by charging a fixed rate on the cost of the asset.

Advantages of reducing balance method 1) It is simple to understand and calculate. 2) The method is more logical and consistent with reality of asset usage as largest amount of depreciation is charged in the first year when repair and maintenance charges are most eligible. 3) This method requires little work for calculating depreciation amounts. Disadvantages of reducing balance method

1) It is not easy to determine the depreciation rate. 2) A standard rate of depreciation for all conditions may produce misleading

results.

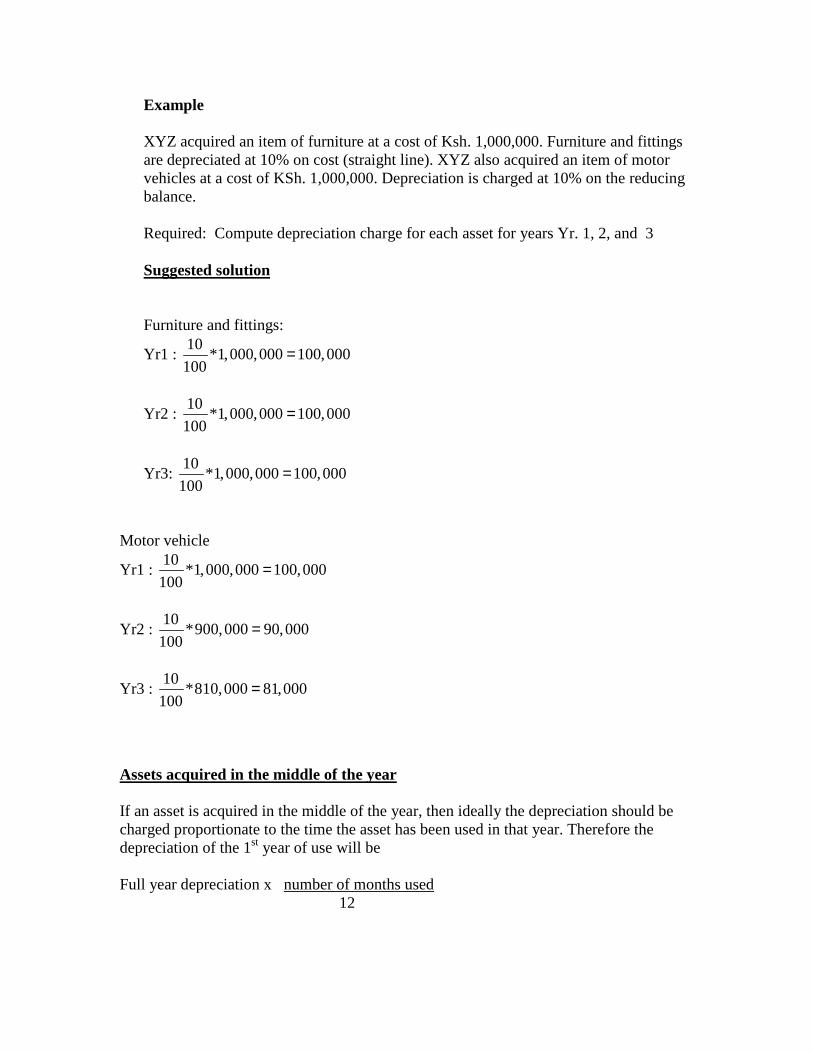

Example XYZ acquired an item of furniture at a cost of Ksh. 1,000,000. Furniture and fittings are depreciated at 10% on cost (straight line). XYZ also acquired an item of motor vehicles at a cost of KSh. 1,000,000. Depreciation is charged at 10% on the reducing balance. Required: Compute depreciation charge for each asset for years Yr. 1, 2, and 3 Suggested solution Furniture and fittings:

Yr1 : 10

*1,000,000 100,000100

=

Yr2 : 10

*1,000,000 100,000100

=

Yr3: 10

*1,000,000 100,000100

=

Motor vehicle

Yr1 : 10

*1,000,000 100,000100

=

Yr2 : 10

*900,000 90,000100

=

Yr3 : 10

*810,000 81,000100

=

Assets acquired in the middle of the year If an asset is acquired in the middle of the year, then ideally the depreciation should be charged proportionate to the time the asset has been used in that year. Therefore the depreciation of the 1st year of use will be Full year depreciation x number of months used 12

EXAMPLE On 30th June 2003, XYZ acquired a motor vehicle and furniture at a cost of 3,000,000 and 2,000,000 respectively. Motor vehicles are depreciated at 20% reducing balance while furniture is depreciated at 10% on cost. XYZ accounts are closed at 31st December. Required: compute depreciation charged for the year ended 31st December 2003

Motor vehicle depreciation = 6 20

* *3,000,000 300,00012 100

=

Furniture depreciation = 6 10

* *2,000,000 100,000120 100

=

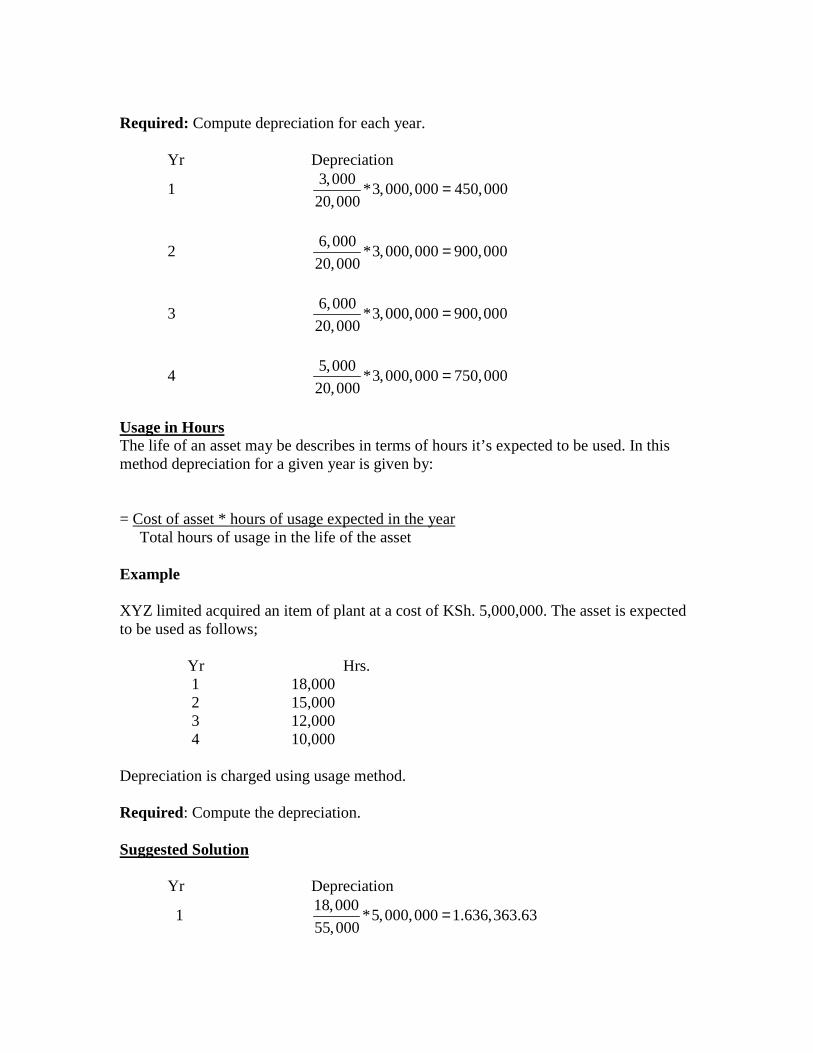

Rate of usage method This is a method of allocating depreciation cost based on the use of the asset. Useful life is in this case defined in terms of usage rather than years. The rate of usage method allocates depreciation expenses according to actual physical usage. Assets with an indefinite useful life but a limited productive capacity are good candidates for this method. The rate of usage method is particularly appropriate when the usage of a fixed asset varies greatly from year to year. Usage may be described in terms of either:

1.) Number of units expected to be produced. 2.) Number of hours of usage expected to run the asset life USAGE IN UNITS Under this method depreciation charge for a given year is: = Units expected to be produced in that year Total number of units in the asset life Example ABC limited acquired an item of plant and machinery at a cost of Ksh. 3,000,000. The item is expected to produce units as follows. YR UNITS

1 3,000 2 6,000 3 6,000 4 5,000

The asset is depreciated using the usage method.

Required: Compute depreciation for each year. Yr Depreciation

1 3,000

*3,000,000 450,00020,000

=

2 6,000

*3,000,000 900,00020,000

=

3 6,000

*3,000,000 900,00020,000

=

4 5,000

*3,000,000 750,00020,000

=

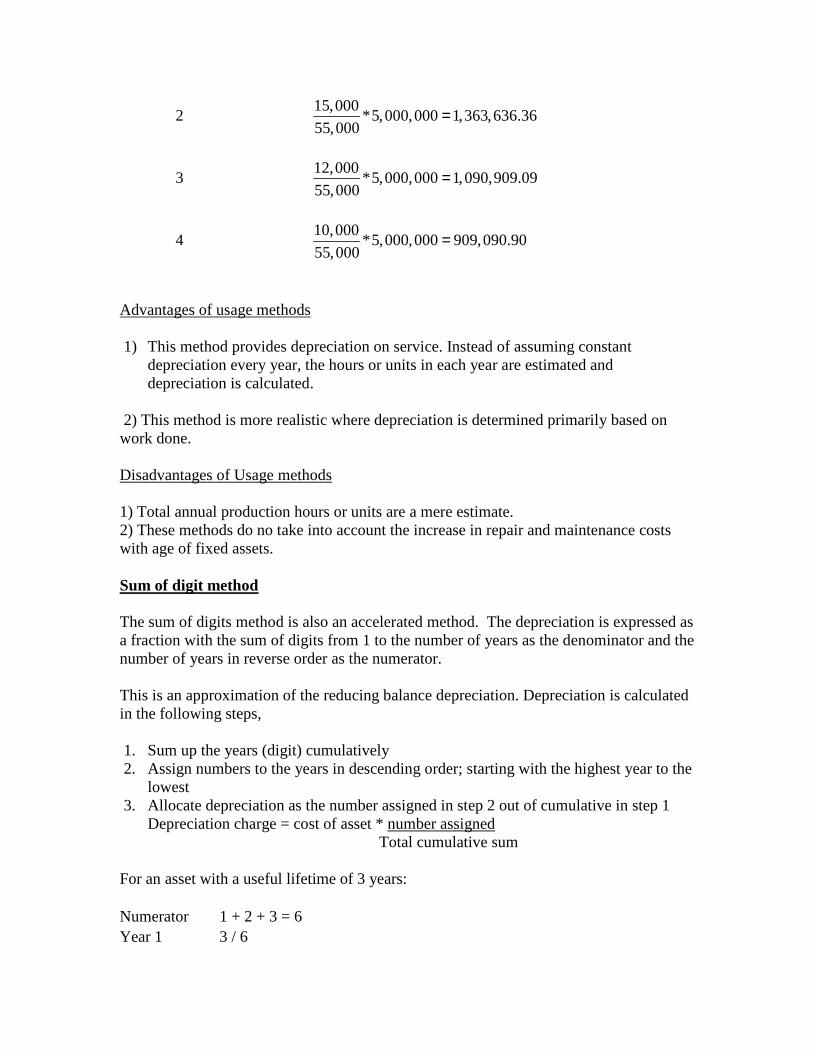

Usage in Hours The life of an asset may be describes in terms of hours it’s expected to be used. In this method depreciation for a given year is given by: = Cost of asset * hours of usage expected in the year Total hours of usage in the life of the asset Example XYZ limited acquired an item of plant at a cost of KSh. 5,000,000. The asset is expected to be used as follows; Yr Hrs.

1 18,000 2 15,000 3 12,000 4 10,000

Depreciation is charged using usage method. Required: Compute the depreciation. Suggested Solution Yr Depreciation

1 18,000

*5,000,000 1.636,363.6355,000

=

2 15,000

*5,000,000 1,363,636.3655,000

=

3 12,000

*5,000,000 1,090,909.0955,000

=

4 10,000

*5,000,000 909,090.9055,000

=

Advantages of usage methods 1) This method provides depreciation on service. Instead of assuming constant

depreciation every year, the hours or units in each year are estimated and depreciation is calculated.

2) This method is more realistic where depreciation is determined primarily based on work done. Disadvantages of Usage methods 1) Total annual production hours or units are a mere estimate. 2) These methods do no take into account the increase in repair and maintenance costs with age of fixed assets. Sum of digit method The sum of digits method is also an accelerated method. The depreciation is expressed as a fraction with the sum of digits from 1 to the number of years as the denominator and the number of years in reverse order as the numerator. This is an approximation of the reducing balance depreciation. Depreciation is calculated in the following steps, 1. Sum up the years (digit) cumulatively 2. Assign numbers to the years in descending order; starting with the highest year to the

lowest 3. Allocate depreciation as the number assigned in step 2 out of cumulative in step 1

Depreciation charge = cost of asset * number assigned Total cumulative sum

For an asset with a useful lifetime of 3 years: Numerator 1 + 2 + 3 = 6 Year 1 3 / 6

Year 2 2 / 6 Year 3 1 / 6 Example XYZ limited acquired an item of plant at a cost of KSh 5,000,000. The expected useful life of the asset is 4 years. Depreciation is charged using sum-of-digit method. Required: Compute depreciation charged for each of the years. Suggested solution

1. Sum of digit (years) = 1+2+3+4 = 10

2. 1st year depreciation = 4

*5,000,000 2,000,00010

=

2nd year depreciation =3

*5,000,000 1,500,00010

=

3rd year depreciation=- 2

*5,000,000 1,000,00010

=

4th year depreciation = 1

*5,000,000 500,00010

=

Advantages of Sum of digits Method

1) The effect of this method is to charge depreciation at a decreasing rate each year 2) This method provides for depreciation by means of different periodic rates. 3) It is a fast method of depreciating assets without use of too elaborate rates of

depreciation 4) It is a realistic method, particularly where assets have an immediate drop in value.

Disadvantage of Sum of digits Method

1) There may be no direct relation between deprecation rate and the flow of benefit from asset usage.

2) It still requires an estimate of useful life. Double-Declining Balance Method

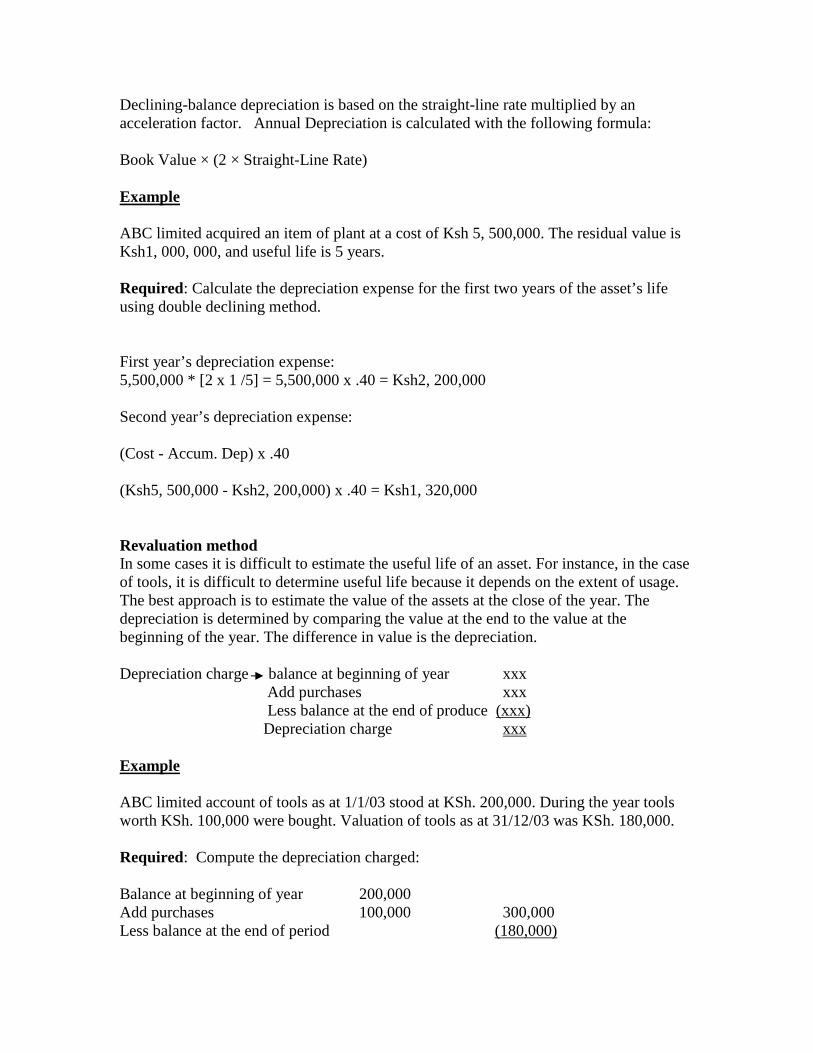

Declining-balance depreciation is based on the straight-line rate multiplied by an acceleration factor. Annual Depreciation is calculated with the following formula: Book Value × (2 × Straight-Line Rate) Example ABC limited acquired an item of plant at a cost of Ksh 5, 500,000. The residual value is Ksh1, 000, 000, and useful life is 5 years. Required: Calculate the depreciation expense for the first two years of the asset’s life using double declining method. First year’s depreciation expense: 5,500,000 * [2 x 1 /5] = 5,500,000 x .40 = Ksh2, 200,000 Second year’s depreciation expense: (Cost - Accum. Dep) x .40 (Ksh5, 500,000 - Ksh2, 200,000) x .40 = Ksh1, 320,000

Revaluation method In some cases it is difficult to estimate the useful life of an asset. For instance, in the case of tools, it is difficult to determine useful life because it depends on the extent of usage. The best approach is to estimate the value of the assets at the close of the year. The depreciation is determined by comparing the value at the end to the value at the beginning of the year. The difference in value is the depreciation. Depreciation charge balance at beginning of year xxx Add purchases xxx Less balance at the end of produce (xxx) Depreciation charge xxx Example ABC limited account of tools as at 1/1/03 stood at KSh. 200,000. During the year tools worth KSh. 100,000 were bought. Valuation of tools as at 31/12/03 was KSh. 180,000. Required: Compute the depreciation charged: Balance at beginning of year 200,000 Add purchases 100,000 300,000 Less balance at the end of period (180,000)

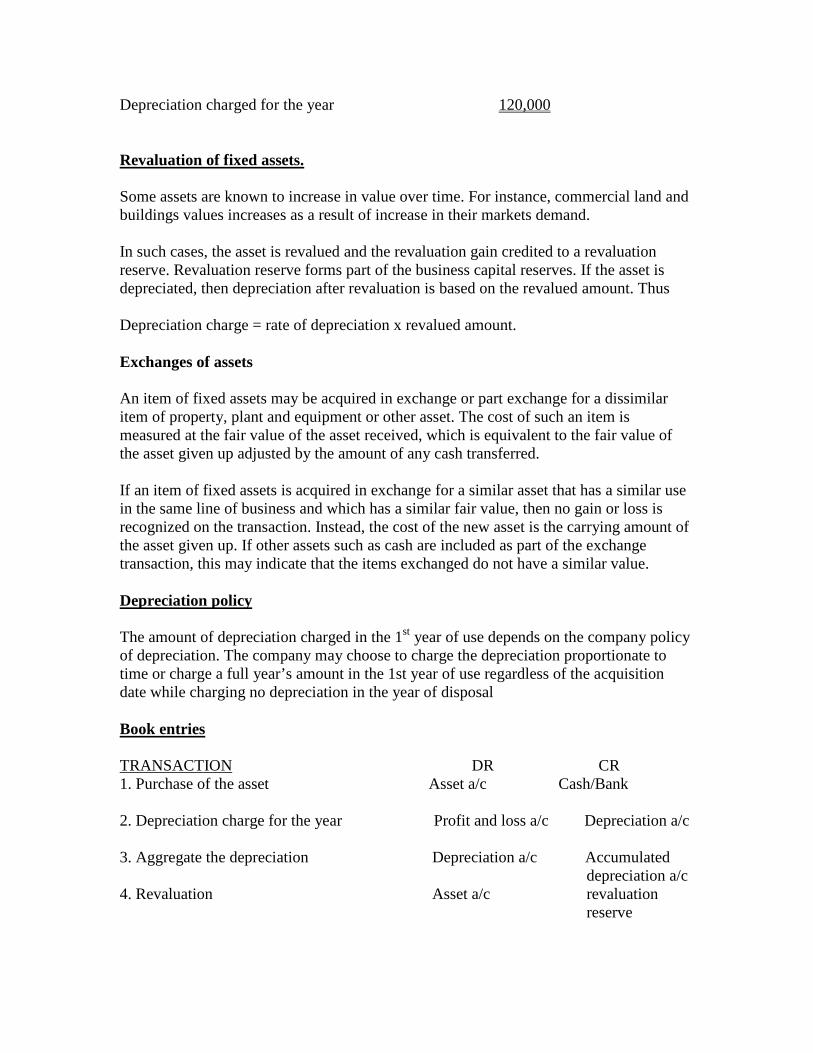

Depreciation charged for the year 120,000 Revaluation of fixed assets. Some assets are known to increase in value over time. For instance, commercial land and buildings values increases as a result of increase in their markets demand. In such cases, the asset is revalued and the revaluation gain credited to a revaluation reserve. Revaluation reserve forms part of the business capital reserves. If the asset is depreciated, then depreciation after revaluation is based on the revalued amount. Thus Depreciation charge = rate of depreciation x revalued amount. Exchanges of assets An item of fixed assets may be acquired in exchange or part exchange for a dissimilar item of property, plant and equipment or other asset. The cost of such an item is measured at the fair value of the asset received, which is equivalent to the fair value of the asset given up adjusted by the amount of any cash transferred. If an item of fixed assets is acquired in exchange for a similar asset that has a similar use in the same line of business and which has a similar fair value, then no gain or loss is recognized on the transaction. Instead, the cost of the new asset is the carrying amount of the asset given up. If other assets such as cash are included as part of the exchange transaction, this may indicate that the items exchanged do not have a similar value. Depreciation policy The amount of depreciation charged in the 1st year of use depends on the company policy of depreciation. The company may choose to charge the depreciation proportionate to time or charge a full year’s amount in the 1st year of use regardless of the acquisition date while charging no depreciation in the year of disposal Book entries TRANSACTION DR CR 1. Purchase of the asset Asset a/c Cash/Bank 2. Depreciation charge for the year Profit and loss a/c Depreciation a/c 3. Aggregate the depreciation Depreciation a/c Accumulated

depreciation a/c 4. Revaluation Asset a/c revaluation

reserve

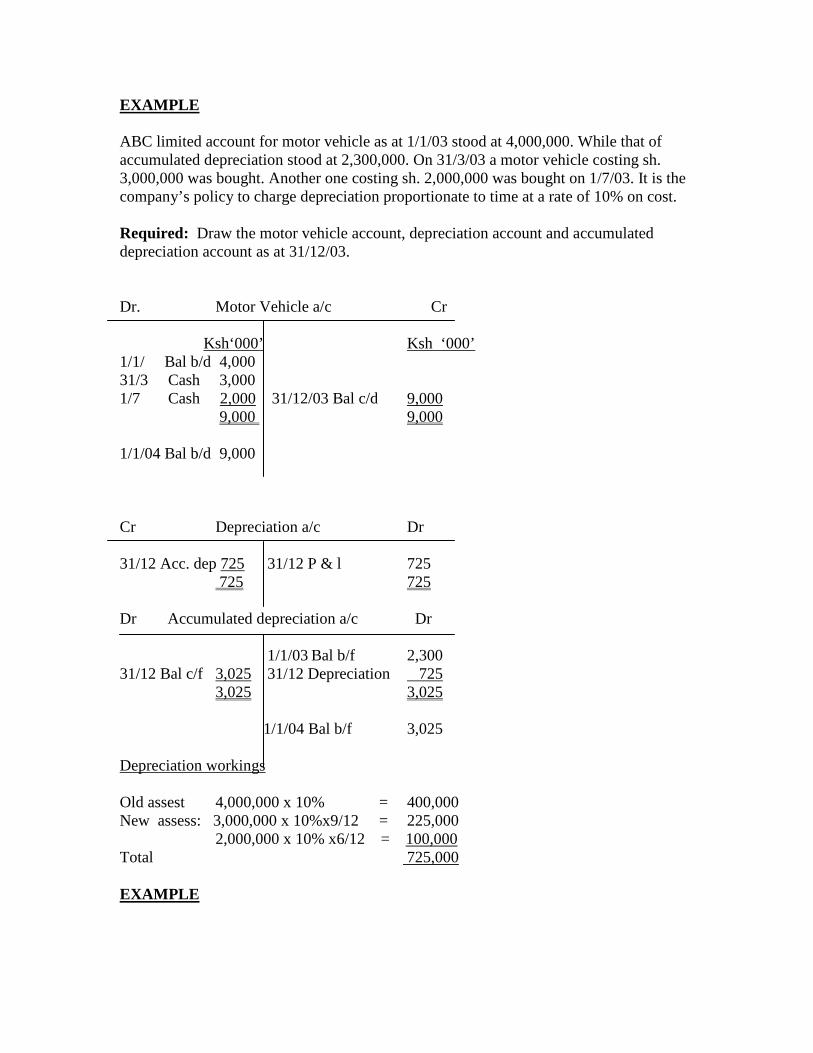

EXAMPLE ABC limited account for motor vehicle as at 1/1/03 stood at 4,000,000. While that of accumulated depreciation stood at 2,300,000. On 31/3/03 a motor vehicle costing sh. 3,000,000 was bought. Another one costing sh. 2,000,000 was bought on 1/7/03. It is the company’s policy to charge depreciation proportionate to time at a rate of 10% on cost. Required: Draw the motor vehicle account, depreciation account and accumulated depreciation account as at 31/12/03.

Dr. Motor Vehicle a/c Cr Ksh‘000’ Ksh ‘000’ 1/1/ Bal b/d 4,000 31/3 Cash 3,000 1/7 Cash 2,000 31/12/03 Bal c/d 9,000 9,000 9,000 1/1/04 Bal b/d 9,000 Cr Depreciation a/c Dr 31/12 Acc. dep 725 31/12 P & l 725 725 725 Dr Accumulated depreciation a/c Dr 1/1/03 Bal b/f 2,300 31/12 Bal c/f 3,025 31/12 Depreciation 725 3,025 3,025

1/1/04 Bal b/f 3,025

Depreciation workings Old assest 4,000,000 x 10% = 400,000 New assess: 3,000,000 x 10%x9/12 = 225,000

2,000,000 x 10% x6/12 = 100,000 Total 725,000 EXAMPLE

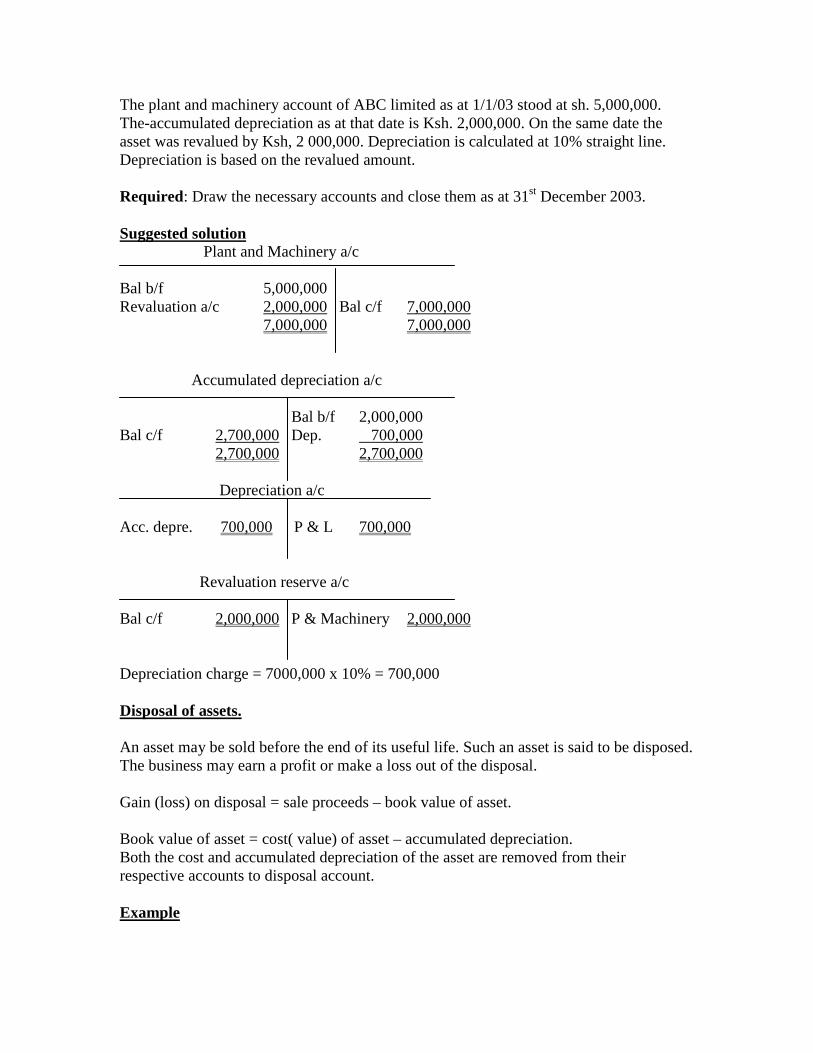

The plant and machinery account of ABC limited as at 1/1/03 stood at sh. 5,000,000. The-accumulated depreciation as at that date is Ksh. 2,000,000. On the same date the asset was revalued by Ksh, 2 000,000. Depreciation is calculated at 10% straight line. Depreciation is based on the revalued amount. Required: Draw the necessary accounts and close them as at 31st December 2003. Suggested solution Plant and Machinery a/c Bal b/f 5,000,000 Revaluation a/c 2,000,000 Bal c/f 7,000,000 7,000,000 7,000,000 Accumulated depreciation a/c Bal b/f 2,000,000 Bal c/f 2,700,000 Dep. 700,000 2,700,000 2,700,000 Depreciation a/c Acc. depre. 700,000 P & L 700,000 Revaluation reserve a/c Bal c/f 2,000,000 P & Machinery 2,000,000 Depreciation charge = 7000,000 x 10% = 700,000 Disposal of assets. An asset may be sold before the end of its useful life. Such an asset is said to be disposed. The business may earn a profit or make a loss out of the disposal. Gain (loss) on disposal = sale proceeds – book value of asset. Book value of asset = cost( value) of asset – accumulated depreciation. Both the cost and accumulated depreciation of the asset are removed from their respective accounts to disposal account. Example

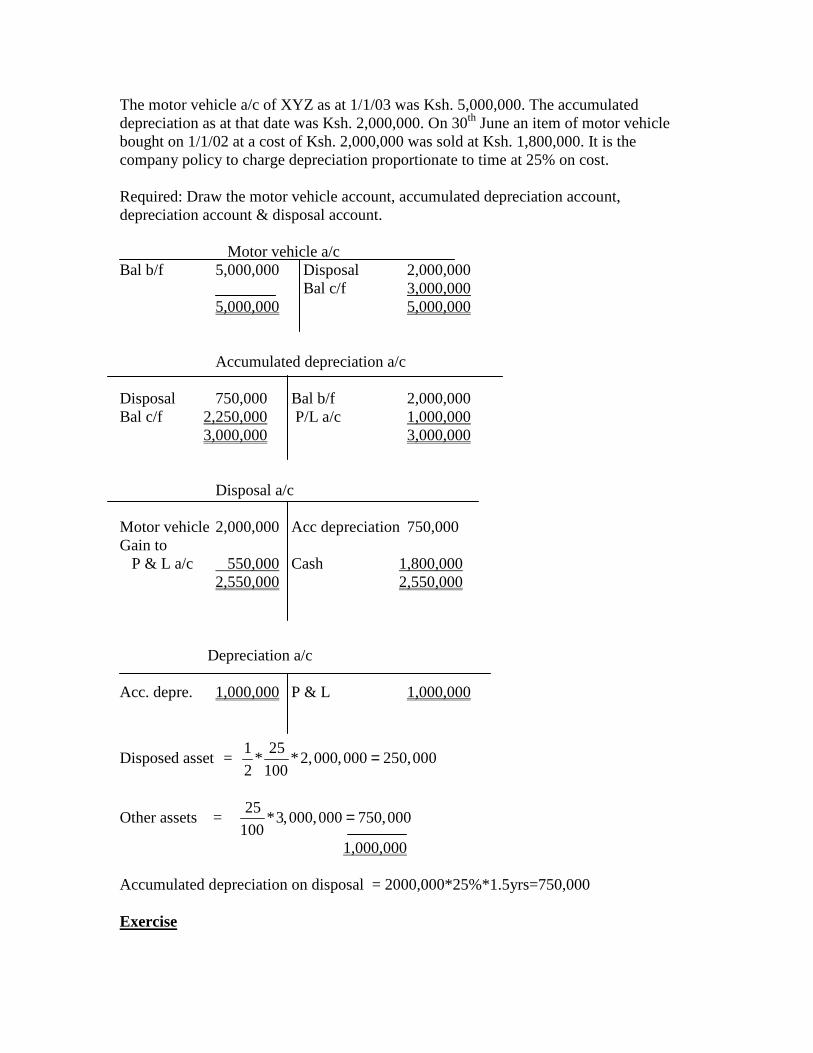

The motor vehicle a/c of XYZ as at 1/1/03 was Ksh. 5,000,000. The accumulated depreciation as at that date was Ksh. 2,000,000. On 30th June an item of motor vehicle bought on 1/1/02 at a cost of Ksh. 2,000,000 was sold at Ksh. 1,800,000. It is the company policy to charge depreciation proportionate to time at 25% on cost. Required: Draw the motor vehicle account, accumulated depreciation account, depreciation account & disposal account. Motor vehicle a/c Bal b/f 5,000,000 Disposal 2,000,000 Bal c/f 3,000,000 5,000,000 5,000,000 Accumulated depreciation a/c Disposal 750,000 Bal b/f 2,000,000 Bal c/f 2,250,000 P/L a/c 1,000,000 3,000,000 3,000,000 Disposal a/c Motor vehicle 2,000,000 Acc depreciation 750,000 Gain to P & L a/c 550,000 Cash 1,800,000 2,550,000 2,550,000 Depreciation a/c Acc. depre. 1,000,000 P & L 1,000,000

Disposed asset = 1 25

* *2,000,000 250,0002 100

=

Other assets = 25

*3,000,000 750,000100

=

1,000,000 Accumulated depreciation on disposal = 2000,000*25%*1.5yrs=750,000 Exercise

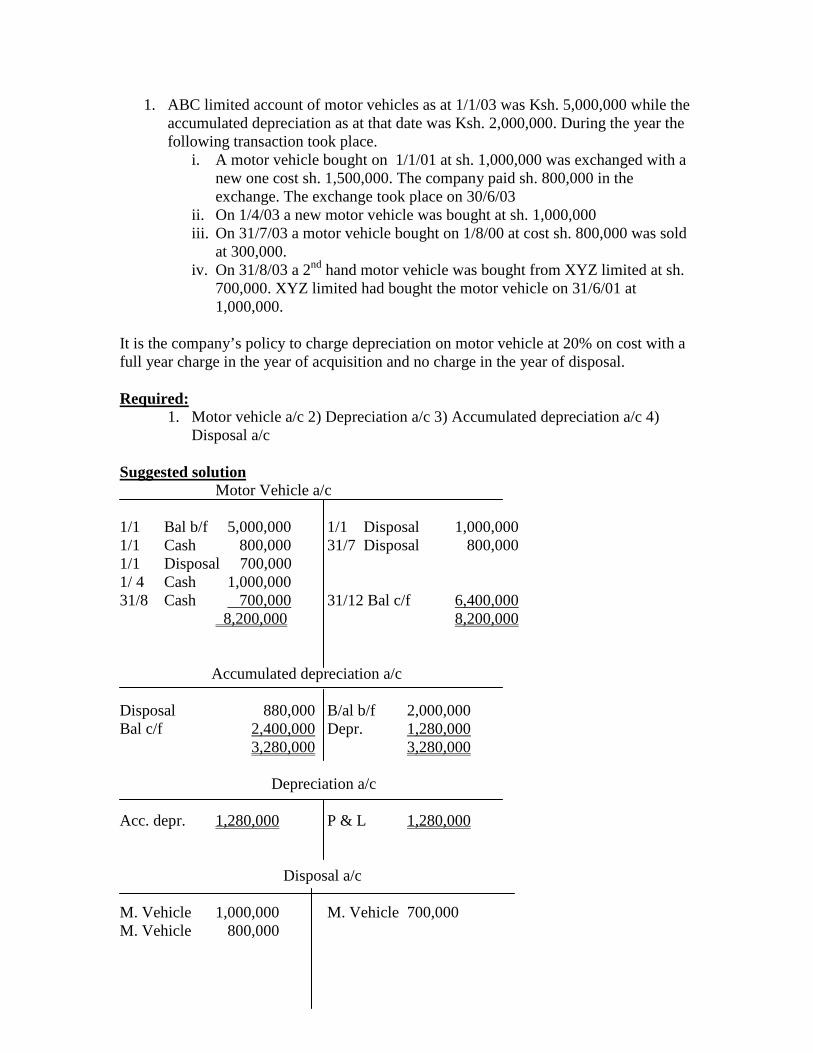

1. ABC limited account of motor vehicles as at 1/1/03 was Ksh. 5,000,000 while the accumulated depreciation as at that date was Ksh. 2,000,000. During the year the following transaction took place.

i. A motor vehicle bought on 1/1/01 at sh. 1,000,000 was exchanged with a new one cost sh. 1,500,000. The company paid sh. 800,000 in the exchange. The exchange took place on 30/6/03

ii. On 1/4/03 a new motor vehicle was bought at sh. 1,000,000 iii. On 31/7/03 a motor vehicle bought on 1/8/00 at cost sh. 800,000 was sold

at 300,000. iv. On 31/8/03 a 2nd hand motor vehicle was bought from XYZ limited at sh.

700,000. XYZ limited had bought the motor vehicle on 31/6/01 at 1,000,000.

It is the company’s policy to charge depreciation on motor vehicle at 20% on cost with a full year charge in the year of acquisition and no charge in the year of disposal. Required:

1. Motor vehicle a/c 2) Depreciation a/c 3) Accumulated depreciation a/c 4) Disposal a/c

Suggested solution Motor Vehicle a/c 1/1 Bal b/f 5,000,000 1/1 Disposal 1,000,000 1/1 Cash 800,000 31/7 Disposal 800,000 1/1 Disposal 700,000 1/ 4 Cash 1,000,000 31/8 Cash 700,000 31/12 Bal c/f 6,400,000 8,200,000 8,200,000 Accumulated depreciation a/c Disposal 880,000 B/al b/f 2,000,000 Bal c/f 2,400,000 Depr. 1,280,000 3,280,000 3,280,000

Depreciation a/c Acc. depr. 1,280,000 P & L 1,280,000 Disposal a/c M. Vehicle 1,000,000 M. Vehicle 700,000 M. Vehicle 800,000

Gain to Acc. depre 880,000 P & L a/c 80,000 Cash 300,000 1,880,000 1,880,000 Depreciation charge for the year: 20% * 6,400,000 = 1,280,000 Depreciation on disposals = 20% * 1,000,000 * 2 = 400,000 20% * 800,000 * 3 = 480,000 880,000 2. XYZ limited account of plant and machinery as at 1/1/03 stood at Ksh. 11,000,000

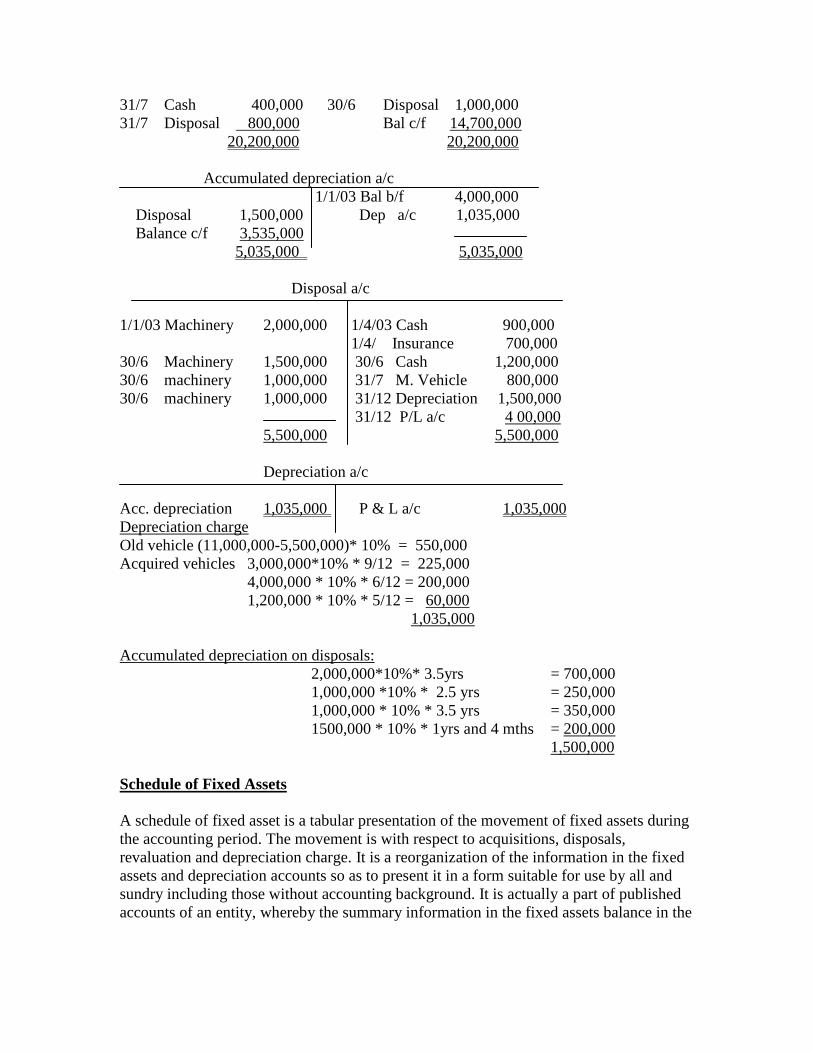

while the accumulated depreciation stood at Ksh. 4,000,000. It is the company’s policy to charge depreciation at 10% on cost pro-rata to time on all assets and no charge in the year of disposal. The following transactions took place:

Purchases: Date Item Amount 1/3/03 Machinery X 3,000,000 30/6/03 Machinery 4,000,000 Disposals: Date Item Orig.cost Sale proceeds Date of Purchase 1/4/03 Machinery A 2,000,000 900,000 30/6/99 30/6/03 Machinery B 1,500,000 1,200,000 1/9/01 Other transactions:

1. A machinery bought on 30/6/00 at 1,000,000 was completely damaged on 1/4/03. The insurance company paid sh. 700,000

2. A machinery bought on 30/6/99 at 1,000,000 was exchanged for a new one costing 1200,000 on 31/7/03. The company paid sh. 400,000 in the exchange.

Required: 1. Machinery a/c 2) Depreciation a/c 3) Accumulated depreciation a/c 4) Disposal

a/c Suggested Solution

Machine a/c 1/1/03 Bal b/f 11,000,000 1/4/ Disposal 2,000,000 1/3/03 Cash 3,000,000 30/6 Disposal 1,500,000 30/6 Cash 4,000,000 10/6 Disposal 1,000,000

31/7 Cash 400,000 30/6 Disposal 1,000,000 31/7 Disposal 800,000 Bal c/f 14,700,000 20,200,000 20,200,000 Accumulated depreciation a/c 1/1/03 Bal b/f 4,000,000 Disposal 1,500,000 Dep a/c 1,035,000 Balance c/f 3,535,000 5,035,000 5,035,000 Disposal a/c 1/1/03 Machinery 2,000,000 1/4/03 Cash 900,000 1/4/ Insurance 700,000 30/6 Machinery 1,500,000 30/6 Cash 1,200,000 30/6 machinery 1,000,000 31/7 M. Vehicle 800,000 30/6 machinery 1,000,000 31/12 Depreciation 1,500,000 31/12 P/L a/c 4 00,000 5,500,000 5,500,000 Depreciation a/c Acc. depreciation 1,035,000 P & L a/c 1,035,000 Depreciation charge Old vehicle (11,000,000-5,500,000)* 10% = 550,000 Acquired vehicles 3,000,000*10% * 9/12 = 225,000 4,000,000 * 10% * 6/12 = 200,000 1,200,000 * 10% * 5/12 = 60,000 1,035,000 Accumulated depreciation on disposals: 2,000,000*10%* 3.5yrs = 700,000 1,000,000 *10% * 2.5 yrs = 250,000 1,000,000 * 10% * 3.5 yrs = 350,000

1500,000 * 10% * 1yrs and 4 mths = 200,000 1,500,000 Schedule of Fixed Assets

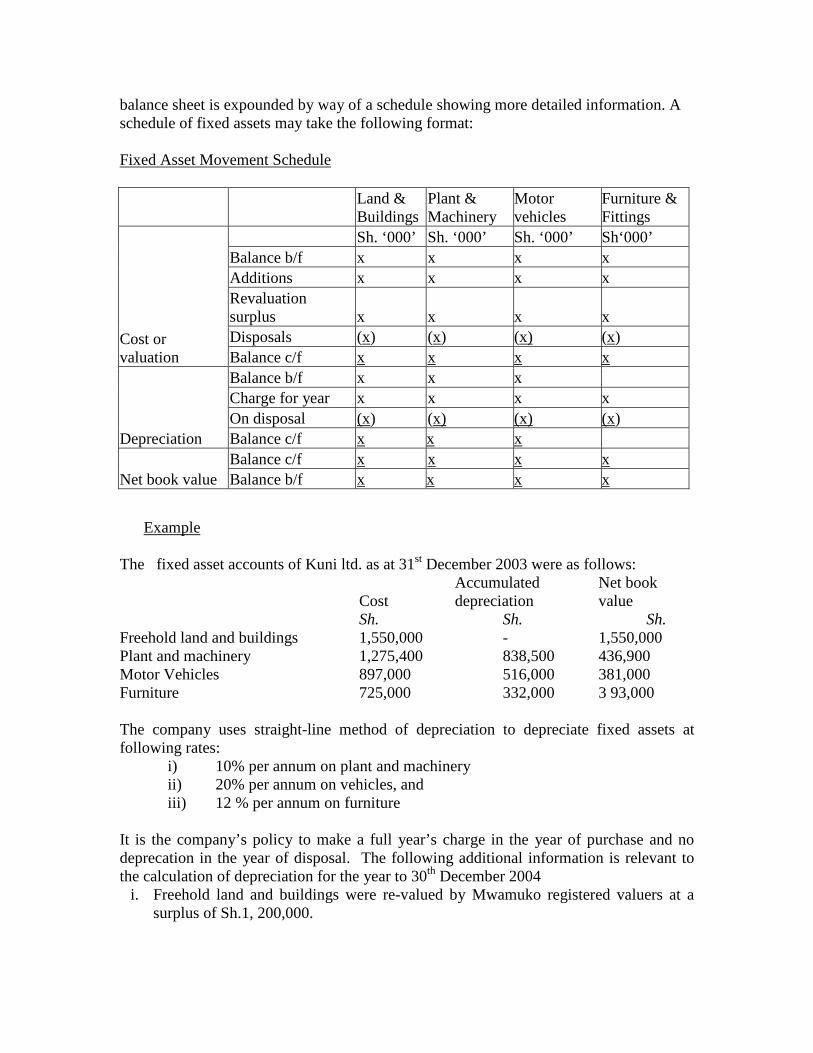

A schedule of fixed asset is a tabular presentation of the movement of fixed assets during the accounting period. The movement is with respect to acquisitions, disposals, revaluation and depreciation charge. It is a reorganization of the information in the fixed assets and depreciation accounts so as to present it in a form suitable for use by all and sundry including those without accounting background. It is actually a part of published accounts of an entity, whereby the summary information in the fixed assets balance in the

balance sheet is expounded by way of a schedule showing more detailed information. A schedule of fixed assets may take the following format: Fixed Asset Movement Schedule

Land & Buildings

Plant & Machinery

Motor vehicles

Furniture & Fittings

Cost or valuation

Sh. ‘000’ Sh. ‘000’ Sh. ‘000’ Sh‘000’ Balance b/f x x x x Additions x x x x Revaluation surplus x x x x Disposals (x) (x) (x) (x) Balance c/f x x x x

Depreciation

Balance b/f x x x Charge for year x x x x On disposal (x) (x) (x) (x) Balance c/f x x x

Net book value Balance c/f x x x x Balance b/f x x x x

Example The fixed asset accounts of Kuni ltd. as at 31st December 2003 were as follows: Accumulated Net book Cost depreciation value Sh. Sh. Sh. Freehold land and buildings 1,550,000 - 1,550,000 Plant and machinery 1,275,400 838,500 436,900 Motor Vehicles 897,000 516,000 381,000 Furniture 725,000 332,000 3 93,000 The company uses straight-line method of depreciation to depreciate fixed assets at following rates:

i) 10% per annum on plant and machinery ii) 20% per annum on vehicles, and iii) 12 % per annum on furniture

It is the company’s policy to make a full year’s charge in the year of purchase and no deprecation in the year of disposal. The following additional information is relevant to the calculation of depreciation for the year to 30th December 2004

i. Freehold land and buildings were re-valued by Mwamuko registered valuers at a surplus of Sh.1, 200,000.

ii. An item of Machinery bought on January 2000 for Sh350, 000 is now recognized to have a useful life of at least 20 years.

iii. A vehicle bought on 1st July 2000 for Sh.450, 000 was traded in at a value of Sh.240, 000 in part exchange for a new vehicle costing 600,000.

iv. Included with the furniture is an item which originally cost Sh.215, 000 and which is already fully depreciated and not expected to realise much from use or disposal.

v. An item of plant bought in 2001 at a cost of 500,000 is disposed in the year at 350,000.

Required: a) Prepare a schedule of fixed assets movements and balances for the year to 31st

December 2004. Suggested solution

Kuni ltd Schedule of Fixed assets

Land & Buildings

Plant & Machinery

Motor vehicles

Furniture & Fittings

Cost or valuation

Sh. ‘000’ Sh. ‘000’ Sh. ‘000’ Sh‘000’

Balance b/f 1,550,000 1,275,400 897,000 725,000

Additions 600,000 Revaluation Surplus 1,200,000 Disposals (500,000) (450,000) (215,000)

Balance c/f 2,750,000 775,400 1,047,000 510,000

Depreciation

Balance b/f 838,500 516,000 332,000

Charge for year 55,665 209,400 61,200

Disposal (150,000) (360,000)

(215,000)

Balance c/f 744,165 365,400 178,200

Net book value

Balance c/f 2,750,000 31,235 681,600 331,800

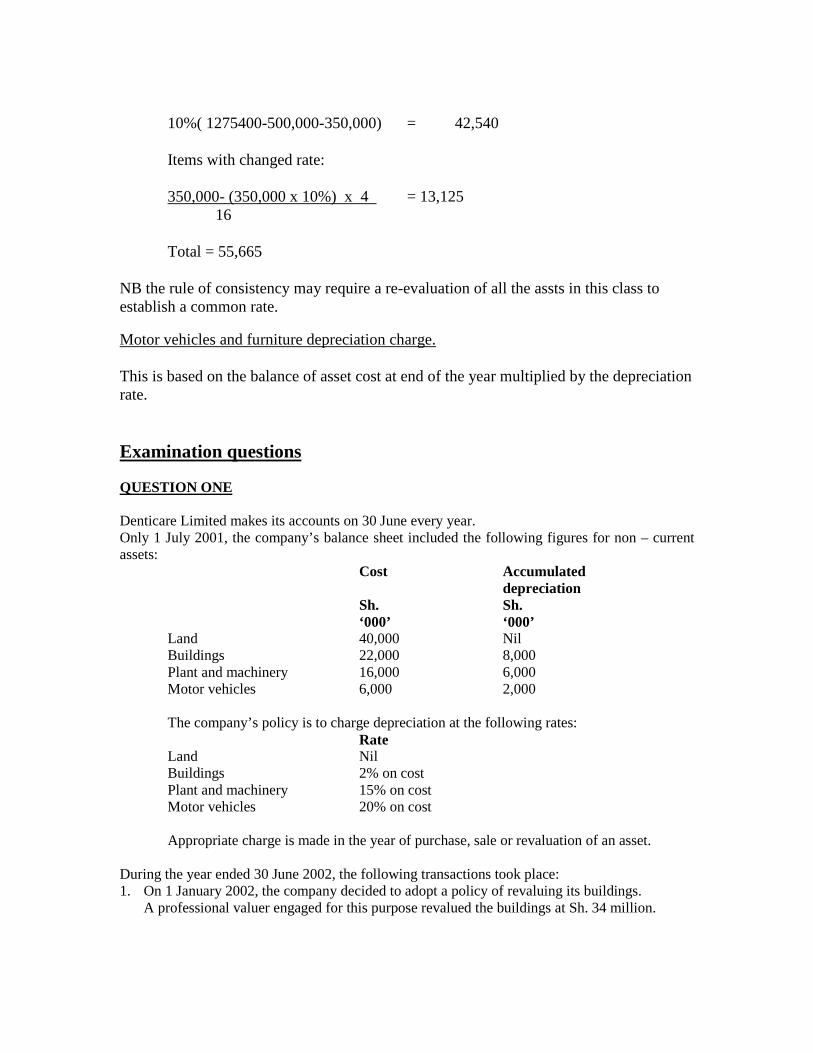

Balance b/f 1550000 436,900 381,000 393,000 Notice that the schedule of movement of fixed assets does not record the disposal proceeds of an asset. Workings: Plant and machinery depreciation: Items whose rate remains the same:

10%( 1275400-500,000-350,000) = 42,540

Items with changed rate:

350,000- (350,000 x 10%) x 4 = 13,125 16

Total = 55,665

NB the rule of consistency may require a re-evaluation of all the assts in this class to establish a common rate. Motor vehicles and furniture depreciation charge. This is based on the balance of asset cost at end of the year multiplied by the depreciation rate. Examination questions QUESTION ONE Denticare Limited makes its accounts on 30 June every year. Only 1 July 2001, the company’s balance sheet included the following figures for non – current assets:

Cost Accumulated depreciation

Sh. Sh. ‘000’ ‘000’

Land 40,000 Nil Buildings 22,000 8,000 Plant and machinery 16,000 6,000 Motor vehicles 6,000 2,000

The company’s policy is to charge depreciation at the following rates:

Rate Land Nil Buildings 2% on cost Plant and machinery 15% on cost Motor vehicles 20% on cost

Appropriate charge is made in the year of purchase, sale or revaluation of an asset.

During the year ended 30 June 2002, the following transactions took place: 1. On 1 January 2002, the company decided to adopt a policy of revaluing its buildings.

A professional valuer engaged for this purpose revalued the buildings at Sh. 34 million.

2. On 1 January 2002 a plant which had cost Sh. 3 million was sold for Sh. 500,000. Accumulated depreciation on this plant on 30 June 2001 amounted to Sh. 2.3 million. A new plant was then purchased at a cost of Sh. 4 million.

3. On 1 April 2002 a new motor vehicle was purchased for Sh. 300,000. Part of the purchase price was settled by exchanging another motor vehicle at an agreed value of Sh. 120,000. The balance of Sh. 180,000 was paid in cash. The vehicle which was given in part exchange had cost Sh. 200,000 and had a net book value of Sh. 100,000 as at 30 June 2001.

Required: (a) The following ledger accounts to record the above transactions (i) Buildings account (ii) Provision for depreciation: Buildings (iii) Plant and machinery account. (iv) Provision for depreciation: Plant and Machinery. (v) Motor vehicles account. (vi) Provision for depreciation: Motor vehicles. (9 marks) (b) Property, plant and equipment movement schedule for the year ended 30 June 2002.

(6 marks) (Total: 15 marks) Soluti0on Buildings Account Sh.”000” Sh.”000” Balance b/d 22,000 Revaluation 20,220 Balance c/f 42,220 42,220 42,220 Building depreciation accounts Sh.”000” Sh.”000” Balance b/f 8,000

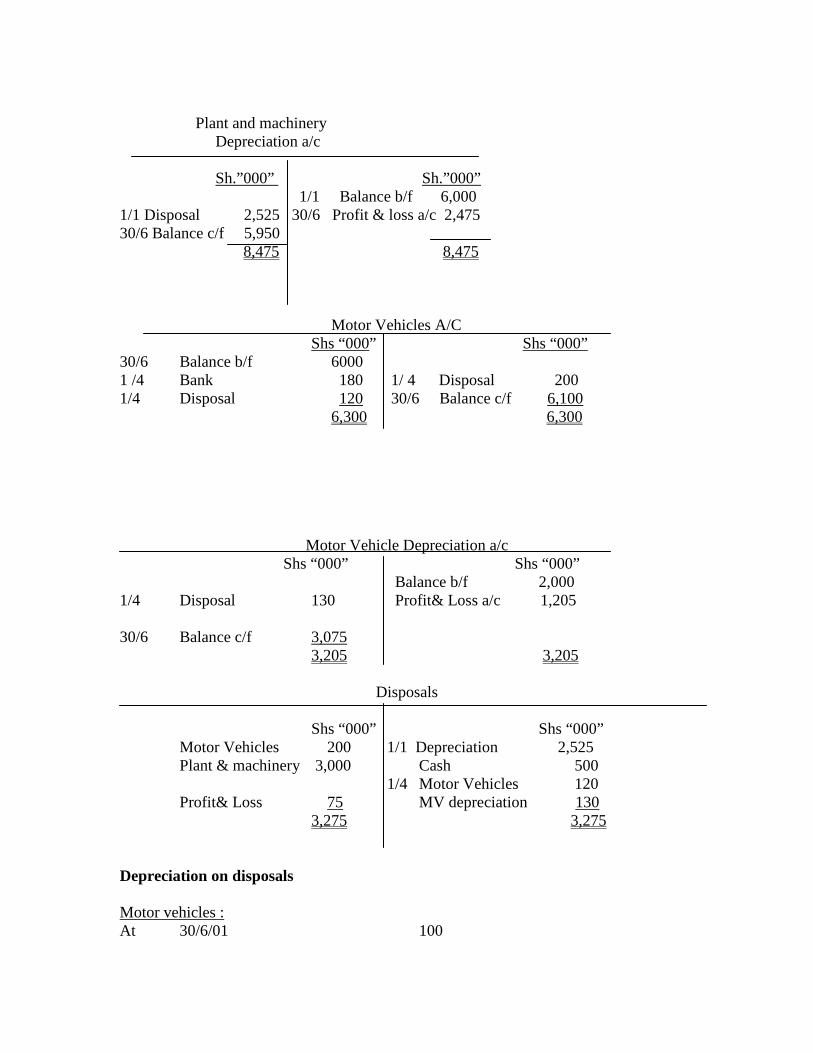

Profit loss a/c 8,22.2 Balance c/f 8,822.2 8,822.2 8,822.2 Plant & machinery a/c. Sh.”000” Sh.”000” 1/1 Disposal 3,000 Balance b/f 16,000 30/6 Balance c/f 17,000 1/1 bank 4,000 20,000 20,000

Plant and machinery

Depreciation a/c Sh.”000” Sh.”000” 1/1 Balance b/f 6,000 1/1 Disposal 2,525 30/6 Profit & loss a/c 2,475 30/6 Balance c/f 5,950 8,475 8,475 Motor Vehicles A/C Shs “000” Shs “000” 30/6 Balance b/f 6000 1 /4 Bank 180 1/ 4 Disposal 200 1/4 Disposal 120 30/6 Balance c/f 6,100 6,300 6,300

Motor Vehicle Depreciation a/c Shs “000” Shs “000” Balance b/f 2,000 1/4 Disposal 130 Profit& Loss a/c 1,205 30/6 Balance c/f 3,075 3,205 3,205

Disposals

Shs “000” Shs “000” Motor Vehicles 200 1/1 Depreciation 2,525 Plant & machinery 3,000 Cash 500 1/4 Motor Vehicles 120 Profit& Loss 75 MV depreciation 130 3,275 3,275 Depreciation on disposals Motor vehicles : At 30/6/01 100

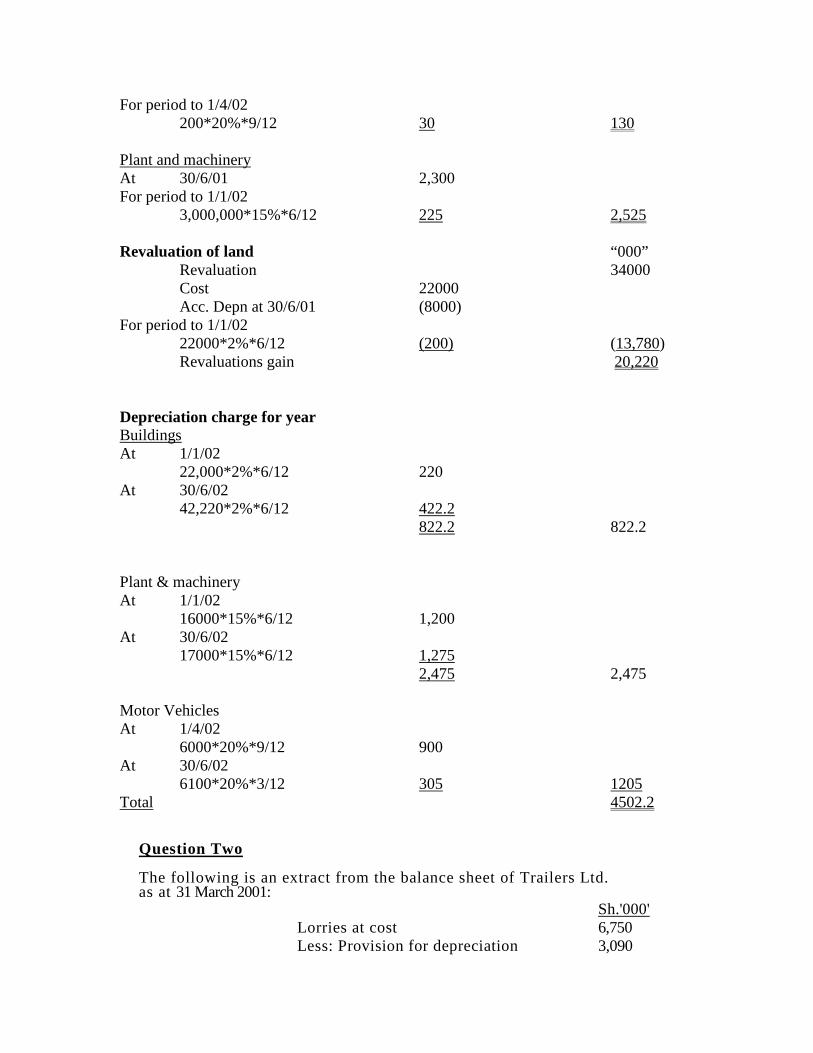

For period to 1/4/02 200*20%*9/12 30 130 Plant and machinery At 30/6/01 2,300 For period to 1/1/02 3,000,000*15%*6/12 225 2,525 Revaluation of land “000” Revaluation 34000 Cost 22000 Acc. Depn at 30/6/01 (8000) For period to 1/1/02 22000*2%*6/12 (200) (13,780) Revaluations gain 20,220 Depreciation charge for year Buildings At 1/1/02 22,000*2%*6/12 220 At 30/6/02 42,220*2%*6/12 422.2 822.2 822.2 Plant & machinery At 1/1/02 16000*15%*6/12 1,200 At 30/6/02 17000*15%*6/12 1,275 2,475 2,475 Motor Vehicles At 1/4/02 6000*20%*9/12 900 At 30/6/02 6100*20%*3/12 305 1205 Total 4502.2

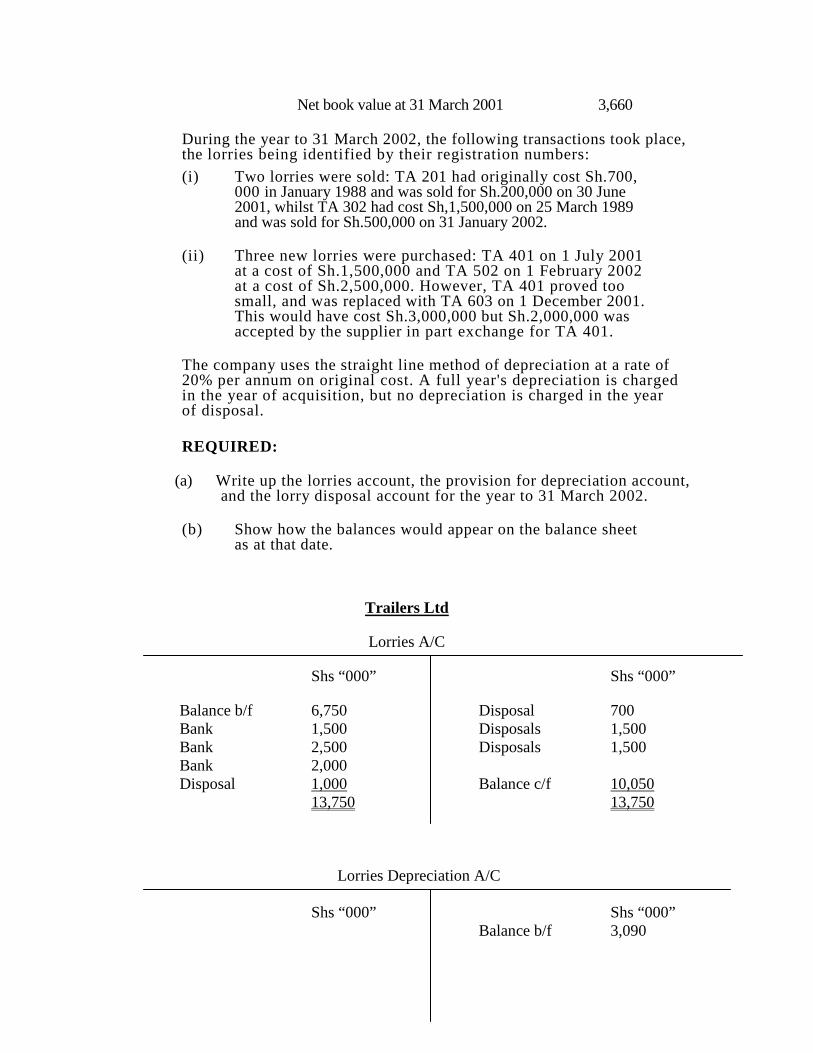

Question Two The following is an extract from the balance sheet of Trailers Ltd. as at 31 March 2001:

Sh.'000' Lorries at cost 6,750 Less: Provision for depreciation 3,090

Net book value at 31 March 2001 3,660

During the year to 31 March 2002, the following transactions took place, the lorries being identified by their registration numbers:

(i) Two lorries were sold: TA 201 had originally cost Sh.700, 000 in January 1988 and was sold for Sh.200,000 on 30 June 2001, whilst TA 302 had cost Sh,1,500,000 on 25 March 1989 and was sold for Sh.500,000 on 31 January 2002.

(ii) Three new lorries were purchased: TA 401 on 1 July 2001

at a cost of Sh.1,500,000 and TA 502 on 1 February 2002 at a cost of Sh.2,500,000. However, TA 401 proved too small, and was replaced with TA 603 on 1 December 2001. This would have cost Sh.3,000,000 but Sh.2,000,000 was accepted by the supplier in part exchange for TA 401.

The company uses the straight line method of depreciation at a rate of 20% per annum on original cost. A full year's depreciation is charged in the year of acquisition, but no depreciation is charged in the year of disposal.

REQUIRED:

(a) Write up the lorries account, the provision for depreciation account, and the lorry disposal account for the year to 31 March 2002.

(b) Show how the balances would appear on the balance sheet as at that date.

Trailers Ltd

Lorries A/C

Shs “000” Shs “000”

Balance b/f 6,750 Disposal 700 Bank 1,500 Disposals 1,500 Bank 2,500 Disposals 1,500 Bank 2,000 Disposal 1,000 Balance c/f 10,050 13,750 13,750

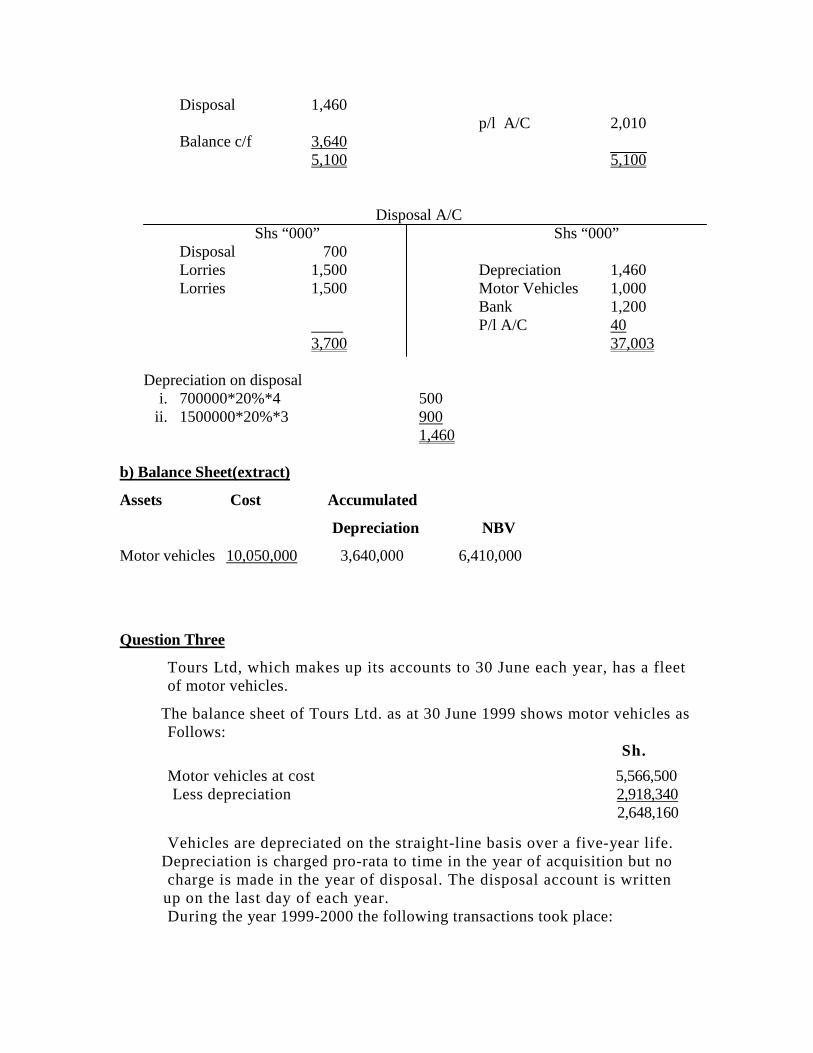

Lorries Depreciation A/C

Shs “000” Shs “000” Balance b/f 3,090

Disposal 1,460 p/l A/C 2,010 Balance c/f 3,640 5,100 5,100

Disposal A/C Shs “000” Shs “000”

Disposal 700 Lorries 1,500 Depreciation 1,460 Lorries 1,500 Motor Vehicles 1,000 Bank 1,200 P/l A/C 40 3,700 37,003 Depreciation on disposal

i. 700000*20%*4 500 ii. 1500000*20%*3 900

1,460

b) Balance Sheet(extract)

Assets Cost Accumulated

Depreciation NBV

Motor vehicles 10,050,000 3,640,000 6,410,000

Question Three

Tours Ltd, which makes up its accounts to 30 June each year, has a fleet of motor vehicles.

The balance sheet of Tours Ltd. as at 30 June 1999 shows motor vehicles as Follows: Sh.

Motor vehicles at cost 5,566,500 Less depreciation 2,918,340 2,648,160

Vehicles are depreciated on the straight-line basis over a five-year life. Depreciation is charged pro-rata to time in the year of acquisition but no charge is made in the year of disposal. The disposal account is written up on the last day of each year. During the year 1999-2000 the following transactions took place:

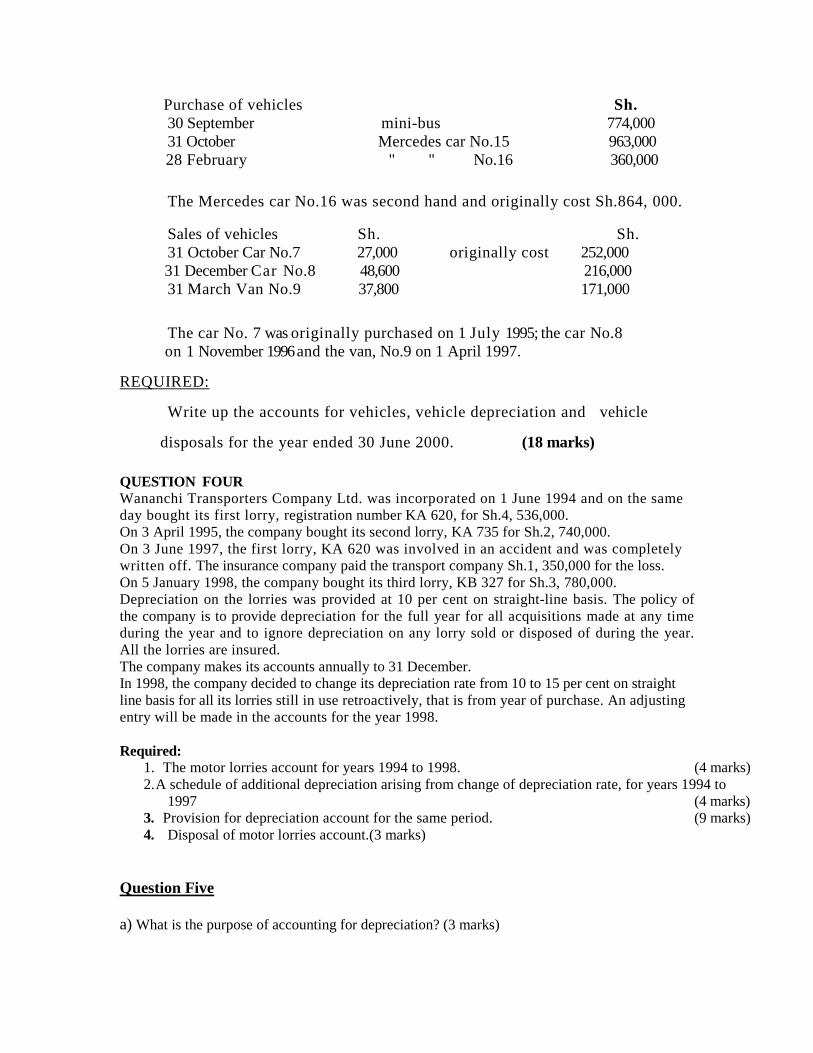

Purchase of vehicles Sh. 30 September mini-bus 774,000 31 October Mercedes car No.15 963,000

28 February " " No.16 360,000

The Mercedes car No.16 was second hand and originally cost Sh.864, 000.

Sales of vehicles Sh. Sh. 31 October Car No.7 27,000 originally cost 252,000

31 December Car No.8 48,600 216,000 31 March Van No.9 37,800 171,000

The car No. 7 was originally purchased on 1 July 1995; the car No.8 on 1 November 1996 and the van, No.9 on 1 April 1997.

REQUIRED:

Write up the accounts for vehicles, vehicle depreciation and vehicle

disposals for the year ended 30 June 2000. (18 marks)

QUESTION FOUR Wananchi Transporters Company Ltd. was incorporated on 1 June 1994 and on the same day bought its first lorry, registration number KA 620, for Sh.4, 536,000. On 3 April 1995, the company bought its second lorry, KA 735 for Sh.2, 740,000. On 3 June 1997, the first lorry, KA 620 was involved in an accident and was completely written off. The insurance company paid the transport company Sh.1, 350,000 for the loss. On 5 January 1998, the company bought its third lorry, KB 327 for Sh.3, 780,000. Depreciation on the lorries was provided at 10 per cent on straight-line basis. The policy of the company is to provide depreciation for the full year for all acquisitions made at any time during the year and to ignore depreciation on any lorry sold or disposed of during the year. All the lorries are insured. The company makes its accounts annually to 31 December. In 1998, the company decided to change its depreciation rate from 10 to 15 per cent on straight line basis for all its lorries still in use retroactively, that is from year of purchase. An adjusting entry will be made in the accounts for the year 1998. Required:

1. The motor lorries account for years 1994 to 1998. (4 marks) 2. A schedule of additional depreciation arising from change of depreciation rate, for years 1994 to

1997 (4 marks) 3. Provision for depreciation account for the same period. (9 marks) 4. Disposal of motor lorries account.(3 marks)

Question Five a) What is the purpose of accounting for depreciation? (3 marks)

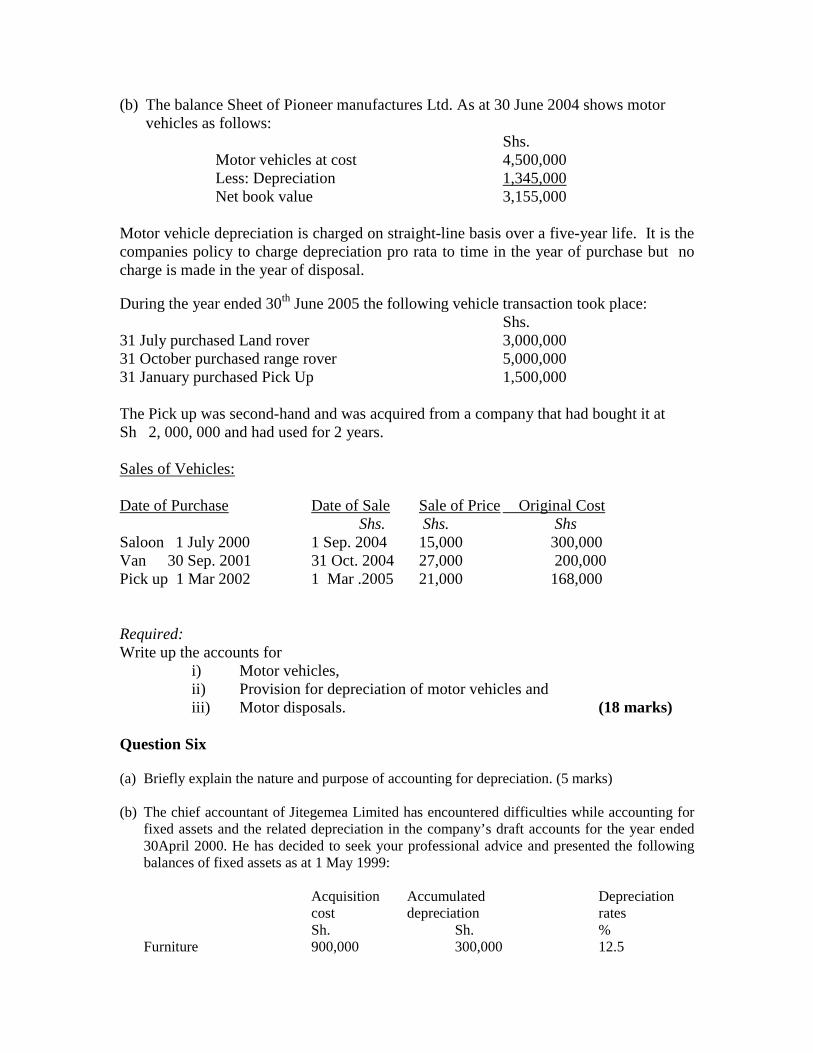

(b) The balance Sheet of Pioneer manufactures Ltd. As at 30 June 2004 shows motor vehicles as follows:

Shs. Motor vehicles at cost 4,500,000 Less: Depreciation 1,345,000 Net book value 3,155,000

Motor vehicle depreciation is charged on straight-line basis over a five-year life. It is the companies policy to charge depreciation pro rata to time in the year of purchase but no charge is made in the year of disposal. During the year ended 30th June 2005 the following vehicle transaction took place: Shs. 31 July purchased Land rover 3,000,000 31 October purchased range rover 5,000,000 31 January purchased Pick Up 1,500,000 The Pick up was second-hand and was acquired from a company that had bought it at Sh 2, 000, 000 and had used for 2 years. Sales of Vehicles: Date of Purchase Date of Sale Sale of Price Original Cost Shs. Shs. Shs Saloon 1 July 2000 1 Sep. 2004 15,000 300,000 Van 30 Sep. 2001 31 Oct. 2004 27,000 200,000 Pick up 1 Mar 2002 1 Mar .2005 21,000 168,000 Required: Write up the accounts for

i) Motor vehicles, ii) Provision for depreciation of motor vehicles and iii) Motor disposals. (18 marks)

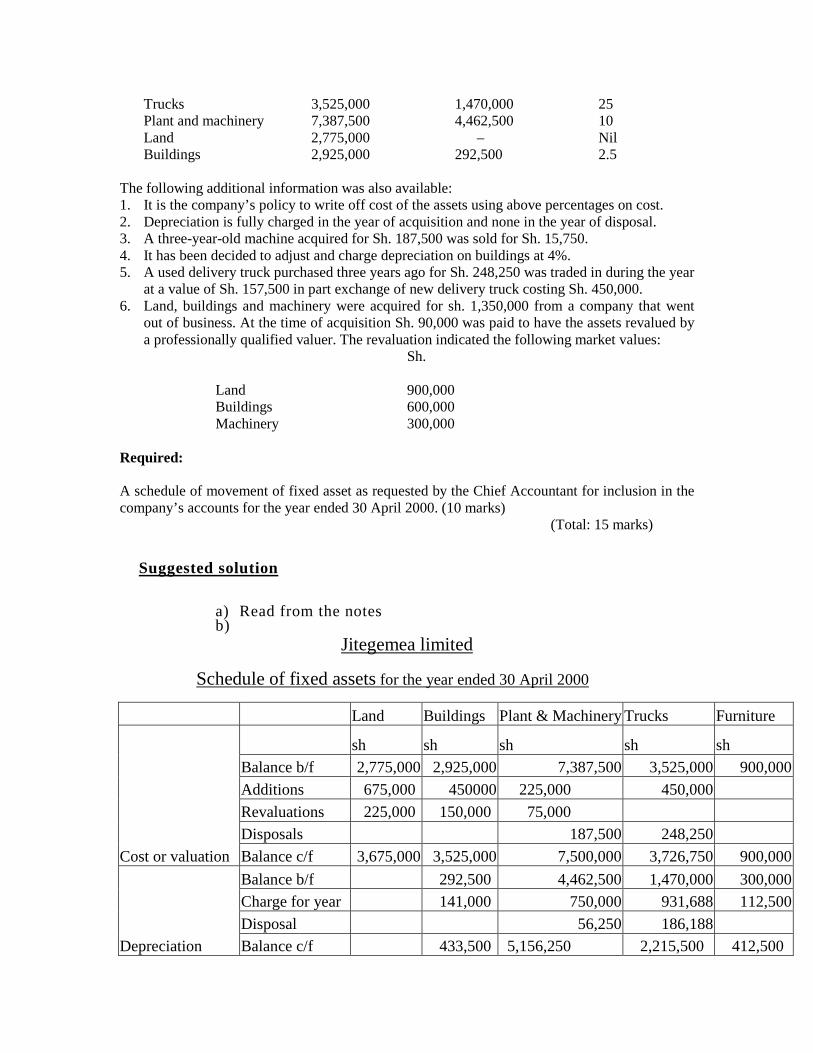

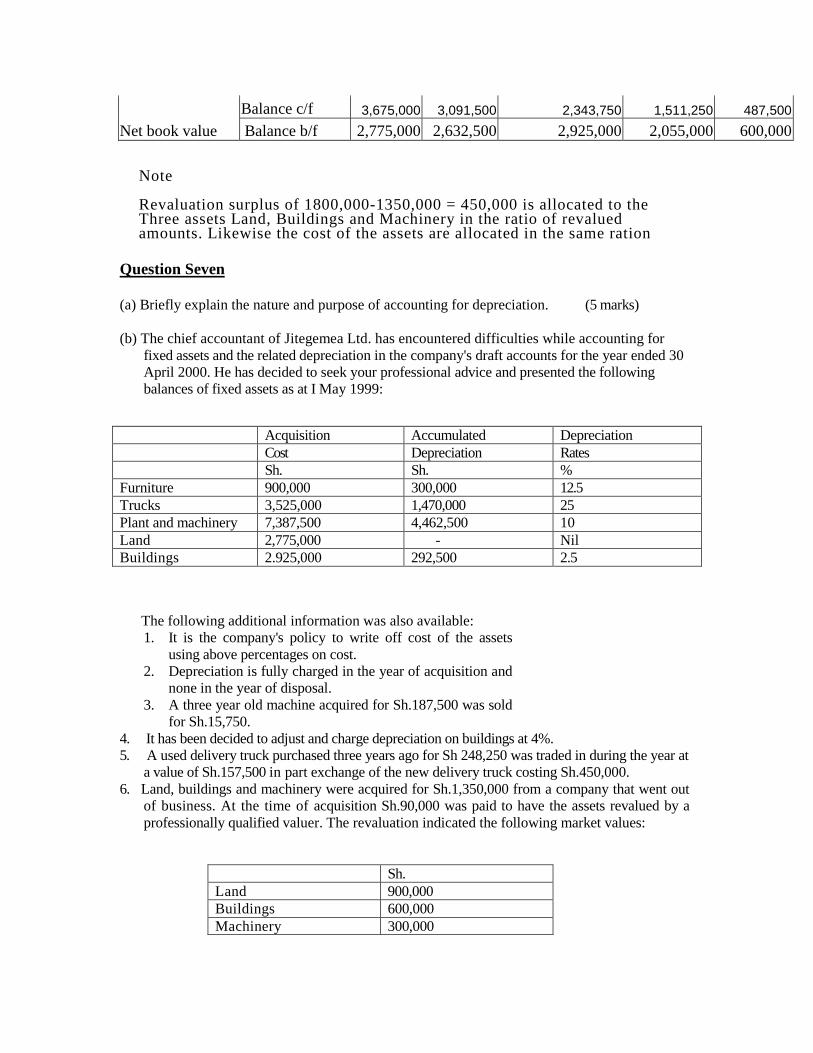

Question Six (a) Briefly explain the nature and purpose of accounting for depreciation. (5 marks) (b) The chief accountant of Jitegemea Limited has encountered difficulties while accounting for

fixed assets and the related depreciation in the company’s draft accounts for the year ended 30April 2000. He has decided to seek your professional advice and presented the following balances of fixed assets as at 1 May 1999:

Acquisition Accumulated Depreciation cost depreciation rates Sh. Sh. %

Furniture 900,000 300,000 12.5

Trucks 3,525,000 1,470,000 25 Plant and machinery 7,387,500 4,462,500 10 Land 2,775,000 – Nil Buildings 2,925,000 292,500 2.5

The following additional information was also available: 1. It is the company’s policy to write off cost of the assets using above percentages on cost. 2. Depreciation is fully charged in the year of acquisition and none in the year of disposal. 3. A three-year-old machine acquired for Sh. 187,500 was sold for Sh. 15,750. 4. It has been decided to adjust and charge depreciation on buildings at 4%. 5. A used delivery truck purchased three years ago for Sh. 248,250 was traded in during the year

at a value of Sh. 157,500 in part exchange of new delivery truck costing Sh. 450,000. 6. Land, buildings and machinery were acquired for sh. 1,350,000 from a company that went

out of business. At the time of acquisition Sh. 90,000 was paid to have the assets revalued by a professionally qualified valuer. The revaluation indicated the following market values:

Sh.

Land 900,000 Buildings 600,000 Machinery 300,000

Required: A schedule of movement of fixed asset as requested by the Chief Accountant for inclusion in the company’s accounts for the year ended 30 April 2000. (10 marks)

(Total: 15 marks) Suggested solution

a) Read from the notes b)

Jitegemea limited

Schedule of fixed assets for the year ended 30 April 2000 Land Buildings Plant & Machinery Trucks Furniture

Cost or valuation

sh sh sh sh sh Balance b/f 2,775,000 2,925,000 7,387,500 3,525,000 900,000

Additions 675,000 450000 225,000 450,000

Revaluations 225,000 150,000 75,000 Disposals 187,500 248,250

Balance c/f 3,675,000 3,525,000 7,500,000 3,726,750 900,000

Depreciation

Balance b/f 292,500 4,462,500 1,470,000 300,000 Charge for year 141,000 750,000 931,688 112,500

Disposal 56,250 186,188 Balance c/f 433,500 5,156,250 2,215,500 412,500

Net book value Balance c/f 3,675,000 3,091,500 2,343,750 1,511,250 487,500

Balance b/f 2,775,000 2,632,500 2,925,000 2,055,000 600,000 Note Revaluation surplus of 1800,000-1350,000 = 450,000 is allocated to the Three assets Land, Buildings and Machinery in the ratio of revalued amounts. Likewise the cost of the assets are allocated in the same ration

Question Seven (a) Briefly explain the nature and purpose of accounting for depreciation. (5 marks) (b) The chief accountant of Jitegemea Ltd. has encountered difficulties while accounting for

fixed assets and the related depreciation in the company's draft accounts for the year ended 30 April 2000. He has decided to seek your professional advice and presented the following balances of fixed assets as at I May 1999:

Acquisition Accumulated Depreciation Cost Depreciation Rates Sh. Sh. % Furniture 900,000 300,000 12.5 Trucks 3,525,000 1,470,000 25 Plant and machinery 7,387,500 4,462,500 10 Land 2,775,000 - Nil Buildings 2.925,000 292,500 2.5

The following additional information was also available: 1. It is the company's policy to write off cost of the assets

using above percentages on cost. 2. Depreciation is fully charged in the year of acquisition and

none in the year of disposal. 3. A three year old machine acquired for Sh.187,500 was sold

for Sh.15,750. 4. It has been decided to adjust and charge depreciation on buildings at 4%. 5. A used delivery truck purchased three years ago for Sh 248,250 was traded in during the year at

a value of Sh.157,500 in part exchange of the new delivery truck costing Sh.450,000. 6. Land, buildings and machinery were acquired for Sh.1,350,000 from a company that went out

of business. At the time of acquisition Sh.90,000 was paid to have the assets revalued by a professionally qualified valuer. The revaluation indicated the following market values:

Sh. Land 900,000 Buildings 600,000 Machinery 300,000

Required:

A schedule of movement of fixed assets as requested by the Chief Accountant for inclusion in the company's accounts for the year ended 30 April 2000. (10 marks) (Total:15 marks)

Question Eight At 1st January 2004 the fixed asset balances of Kipevu Ltd. comprised the following:

Cost Depreciation NBV Shs Shs Shs.

Freehold land & building 2,284,000 – 2,284,000 Plant and Machinery 2,340,000 1,260,400 1,079,600 Vehicles 1,260,000 768,000 492,000 Equipment The company uses straight-line method of depreciation as follows:

i) 10% per annum for plant and Machinery ii) 20% per annum for vehicles.

It is the company’s policy to make a deprecation charge proportionate to the time of usage of the asset. The following additional information is provided. (i) An item of machinery bought on 1st July 2000 for Sh. 336,000 was sold on 1st

may 2004 at sh 200,000. (ii) It has been decided to charge depreciation on freehold buildings at 2.5 % per

annum. The buildings represent Sh. 1,284, 000 of the Sh. 2,284,000 and were all completed in 1st July 2000

(iii) A new machine costing shilling 350,000 was bought on 31st august 2004. (iv) A vehicle purchased in 1st may 2001 for Sh. 420,000 was traded in at a value of

Sh. 244,000 in part exchange for a new vehicle costing Sh. 600,000 on 1st January 2004.

(v) Included with the machinery is an item, which originally cost Sh. 450,000 and which is already, fully depreciated but not expected to yield any material amount on either use or resale.

(vi) A second machine costing shillings 450,000 on 30/6/2004 was bought from Adede ltd who had used it for 3 years and had bought it at sh 600,000.

Required: (a) Prepare a schedule of fixed asset movement for the year to 31st December 2004.

Kipevu ltd

Schedule of fixed assets for the year to 31st December 2004

Land Buildings Plant & Machinery Motor vehicles

Cost or valuation

Sh Sh Sh. Sh.

Balance b/f 1,000,000 1,284,000 2,340,000 1,260,000

Additions 800000 600,000 Disposals 786,000 420,000

Balance c/f 1,000,000 1,284,000 2,354,000 1,440,000

Depreciation

Balance b/f 1,260,400 768,000

Charge for year 144,450 200,767 288,000

Disposal 578,800 224,000 Balance c/f 144,450 729,767 765,000

Net book value Balance c/f 1,000,000 1,139,550 1,471,633 608,000 Balance b/f 1,000,000 1,284,000 1,079,600 492,000

Workings Disposal depreciation (1) Machines

i. 336000*10%*3 & 10/12 128,800 ii. 450,000 (Fully depreciated) 450,000

578,800 (2) Motor vehicles 120,000*20%*2 & 8/12 224,000 Depreciation charge: (1) Buildings Charge to reserves (retrospective) 2.5%*1284000*3.5yrs 112,350 Charge to Profit & Loss a/c 2.5%*1284000 32,100 144,450 (2) Plant & machinery Disposed 336000*10%*4/12 11,200 Old Machine (2,340,000-786,000) * 10% 155,400 Additions

i. 350000*10%*4/12 11,667 ii. 450000*10%*6/12 22,500

200,767 (3) Motor vehicles:

i. (1,260,000-420,000)*0.2 168,000

ii. 600,000*0.2 120,000 288,000