Embed Size (px)

Citation preview

Accounting for Convertible

Instruments

James Barker

Michael Mueller

Mark Bolton

Magnus Orrell

July 31, 2007

Financial Reporting Presents:

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Agenda

• Flashback to 1st Convertibles Dbriefs

• Let’s Meet Ms. Host

• Let’s Meet Mr. Conventional

• Let’s Meet Mr. ―Not-So‖ Conventional

• What’s left…

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Learning Objectives

At the end of the webcast, participants should have

an understanding of

• how the host contract of a convertible instrument

is determined

• when a convertible instrument qualifies as

―conventional‖ – impact on EITF 00-19 analysis

• the 8 factors in paragraphs 12-32 of EITF 00-19.

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Keep in Mind

• This webcast does not provide official Deloitte &

Touche LLP interpretative accounting guidance.

• Don’t expect this webcast to turn you into a convertibles

expert.

• Remember, the Convertibles Dbriefs are designed to

build on each other.

• If you haven’t yet had the opportunity to view the

previous webcast, you are out of luck…just joking, you

can retrieve the webcast (see last slide).

• Seriously, try to have some fun with this stuff

because, otherwise, you’ll look like this guy…

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Polling Question #1

Did you attend the previous webcast?

•Yes

•No

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Flashback to 1st Convertibles Dbriefs

Back then (1969)…

Convertible into a fixed

# of shares

Standard antidilution

provisions

If-converted method

Convertible Debt

1

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Flashback to 1st Convertibles Dbriefs

…Today (2007)

Contingently

convertible

Conversion spread

settled in net shares,

principal settled in

cash

Non-standard

antidilution provisions

Treasury stock method

Instrument C

2

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Flashback to 1st Convertibles Dbriefs

CONVERTIBLES – Accounting Challenges

Attractiveness of Convertibles

Issuer: Low cost financing

Investor: Upside potential

Product Complexity

Too many form-driven rules in too many

places in GAAP

# of Restatements

Accounting Complexity

CoCos, Instrument C, Instrument X,

other features to minimize EPS/

economic dilution…

3

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Flashback to 1st Convertibles Dbriefs

… Need to identify embedded derivatives and

evaluate them for separation under FAS 133

… Need to determine host contract and recognize

that it might change

… Need to determine accounting

for host contract and separated embedded

derivatives

… Need to determine EPS impact

Complex because…

Initially and

Subsequently

!

4

Copyright © 2007 Deloitte Development LLC. All rights reserved.

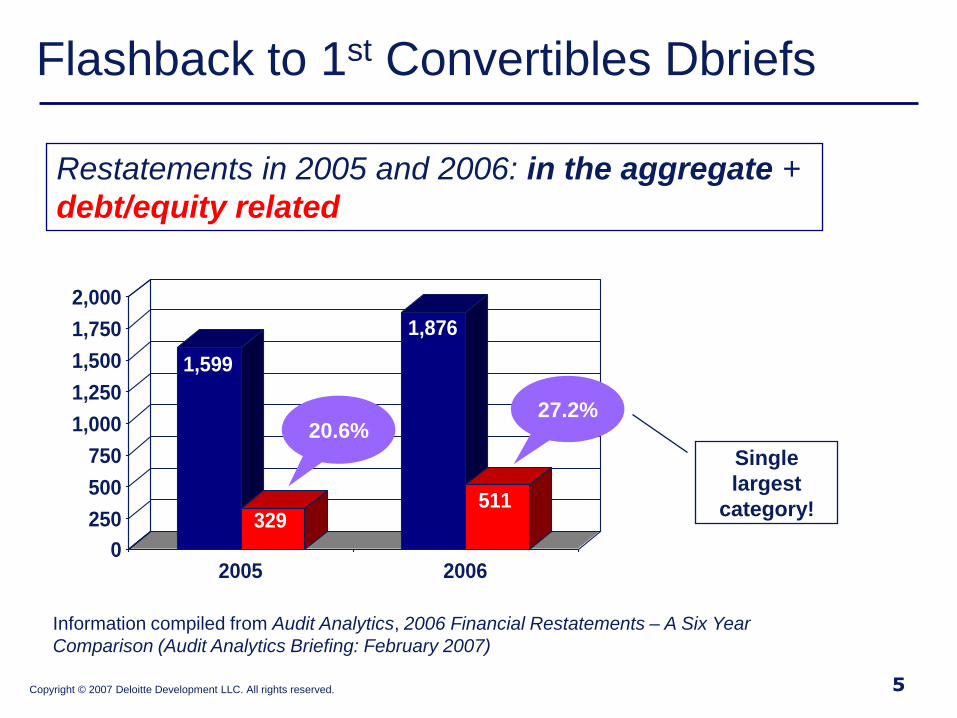

Flashback to 1st Convertibles Dbriefs

Information compiled from Audit Analytics, 2006 Financial Restatements – A Six Year

Comparison (Audit Analytics Briefing: February 2007)

1,599

329

1,876

511

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2005 2006

Restatements in 2005 and 2006: in the aggregate +

debt/equity related

27.2%20.6%

5

Single

largest

category!

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Flashback to 1st Convertibles Dbriefs

12a: Not clearly and closely related to host contract?

12b: Hybrid = Not marked to market under other GAAP?

12c: If freestanding, derivative?

6a: Underlying, notional?

6b: Small initial net investment?

6c: Net settleable?

11a: Qualify for Scope Exception?

EITF 01-6: Indexed to Issuer’s Own Stock?

EITF 00-19: Classified in Equity?

Does the conversion option in a convertible instrument

require bifurcation from the host contract?

6

Copyright © 2007 Deloitte Development LLC. All rights reserved.

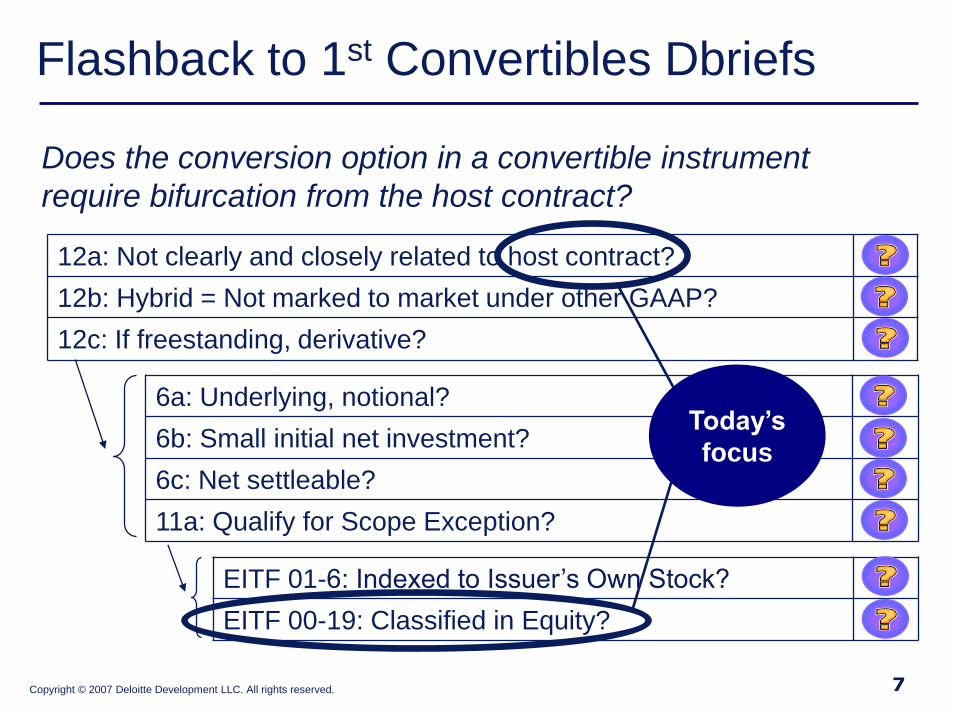

Flashback to 1st Convertibles Dbriefs

12a: Not clearly and closely related to host contract?

12b: Hybrid = Not marked to market under other GAAP?

12c: If freestanding, derivative?

6a: Underlying, notional?

6b: Small initial net investment?

6c: Net settleable?

11a: Qualify for Scope Exception?

EITF 01-6: Indexed to Issuer’s Own Stock?

EITF 00-19: Classified in Equity?

Does the conversion option in a convertible instrument

require bifurcation from the host contract?

7

Today’s

focus

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Polling Question #2

Test question: What are the accounting implications

of applying SFAS 133 to the conversion option?

•Income statement volatility for the issuer

•Higher interest expense on the debt

•Valuation challenges

•All of the above

•Don't know/Not applicable

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Ms. Host

8

Before we say “hi” to Ms.

Host, let’s go back to the

host discussion in 1st

Dbriefs…

Copyright © 2007 Deloitte Development LLC. All rights reserved.

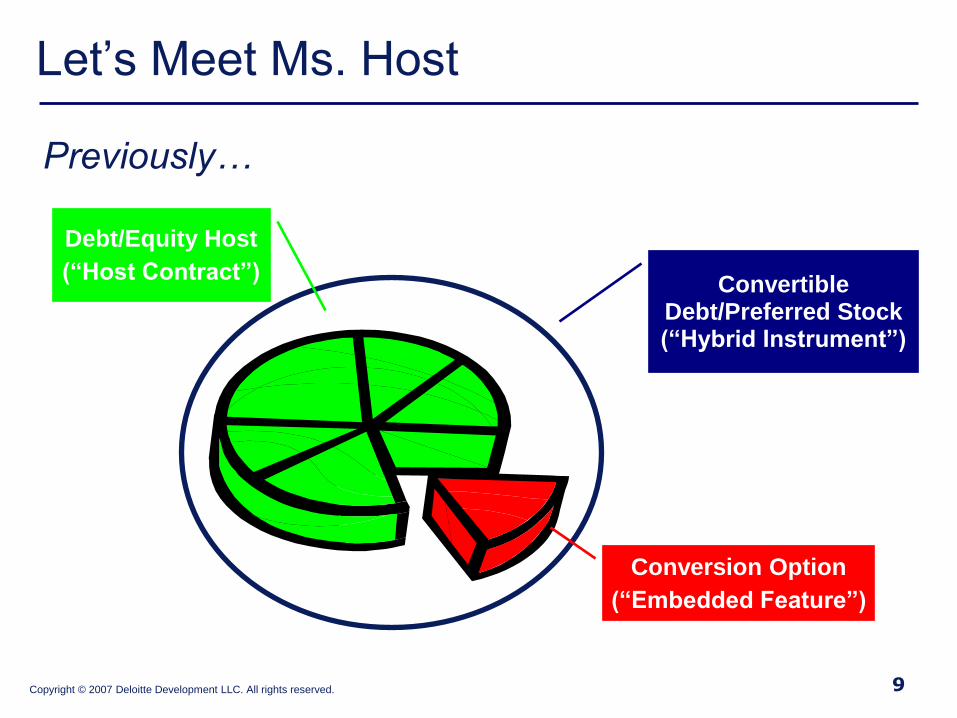

Let’s Meet Ms. Host

Debt/Equity Host

(“Host Contract”)

Previously…

Conversion Option

(“Embedded Feature”)

Convertible Debt/Preferred Stock (“Hybrid Instrument”)

9

Copyright © 2007 Deloitte Development LLC. All rights reserved.

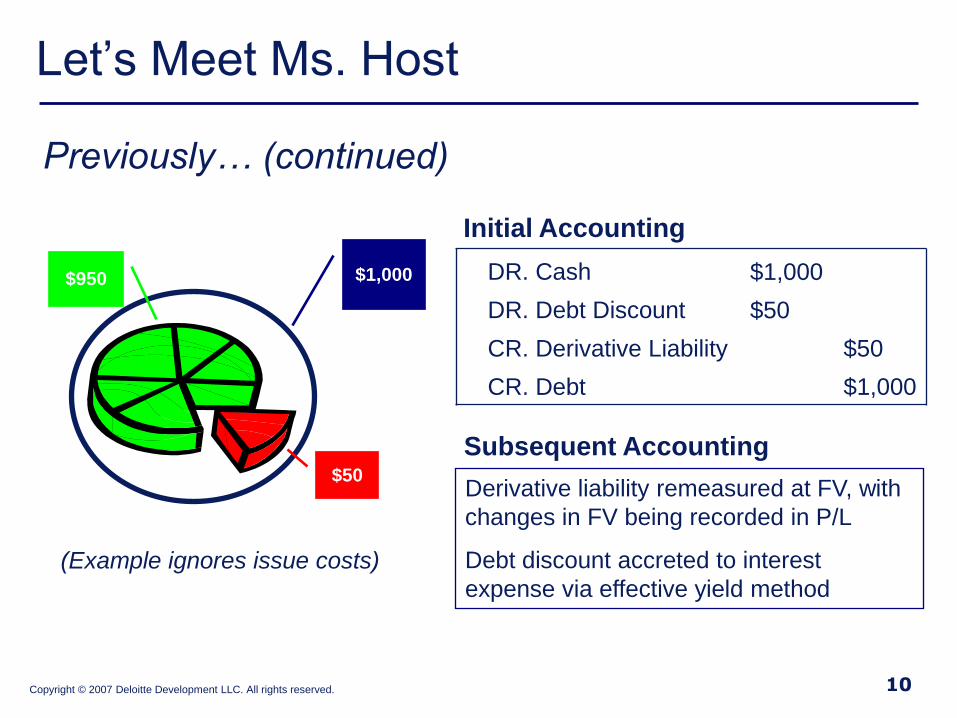

Let’s Meet Ms. Host

Previously… (continued)

$950

$50

$1,000

10

DR. Cash $1,000

DR. Debt Discount $50

CR. Derivative Liability $50

CR. Debt $1,000

Initial Accounting

Derivative liability remeasured at FV, with

changes in FV being recorded in P/L

Debt discount accreted to interest

expense via effective yield method

Subsequent Accounting

(Example ignores issue costs)

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Ms. Host

Guiding principle: Does the host contract encompass a residual interest in the issuing entity (para. 60 of FAS 133)?

Equity Host Debt Host

Yes No

EITF Topic D-109:

Consider ALL

substantive terms

of the convertible!

11

Copyright © 2007 Deloitte Development LLC. All rights reserved.

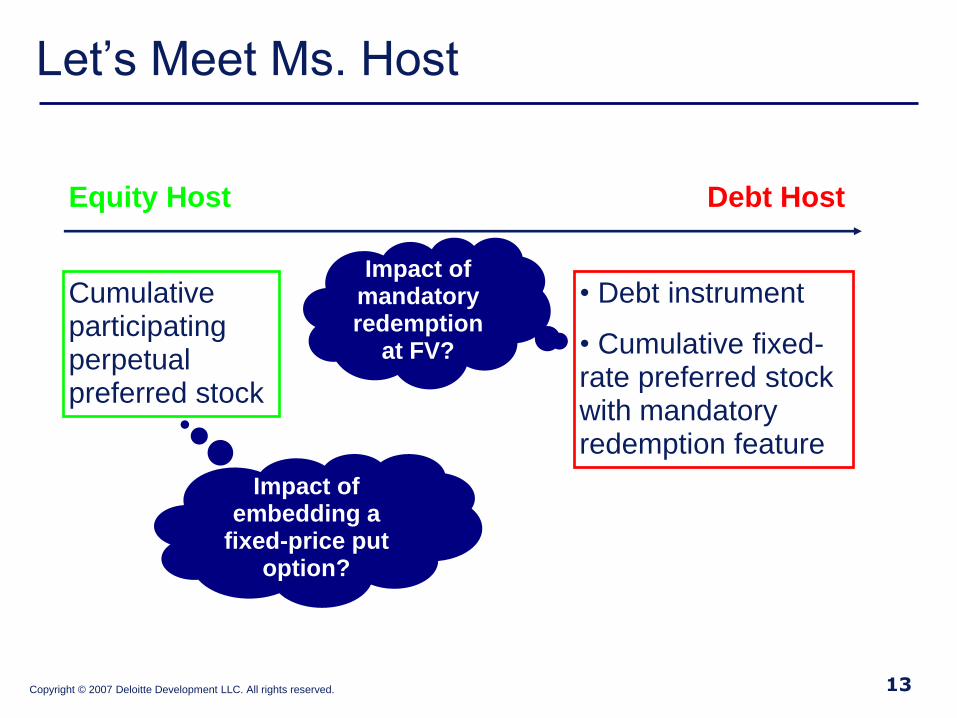

Let’s Meet Ms. Host

• Debt instrument

• Cumulative fixed-rate preferred stock with mandatory redemption feature

Cumulative participating perpetual preferred stock

Equity Host Debt Host

12

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Ms. Host

• Debt instrument

• Cumulative fixed-rate preferred stock with mandatory redemption feature

Cumulative participating perpetual preferred stock

Equity Host Debt Host

Impact of embedding a

fixed-price put option?

Impact of mandatory redemption

at FV?

13

Copyright © 2007 Deloitte Development LLC. All rights reserved.

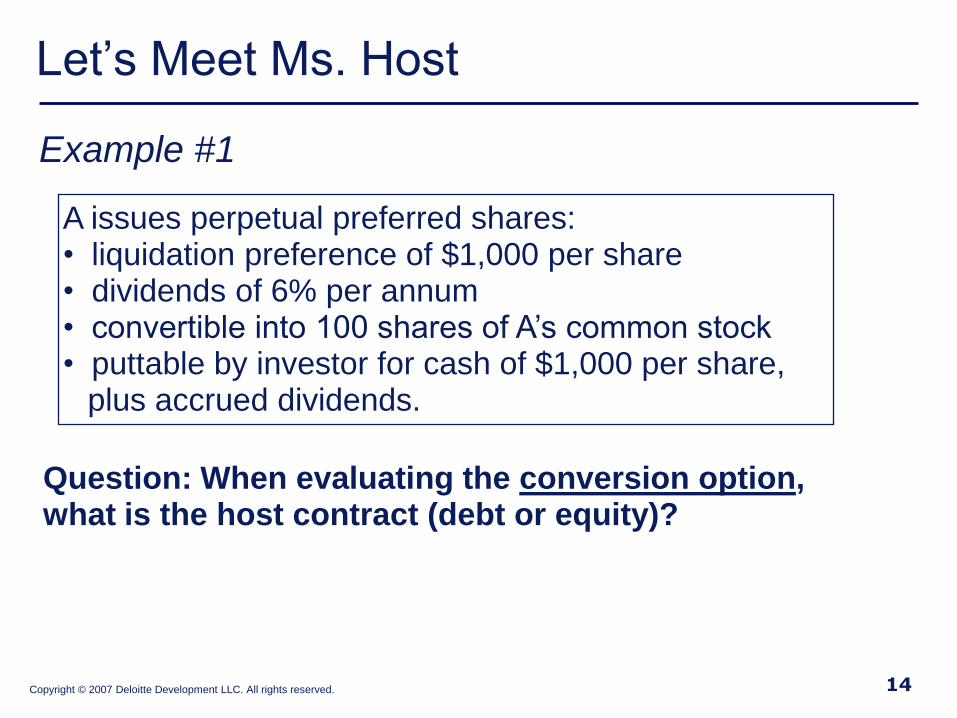

Let’s Meet Ms. Host

Example #1

A issues perpetual preferred shares:• liquidation preference of $1,000 per share• dividends of 6% per annum• convertible into 100 shares of A’s common stock• puttable by investor for cash of $1,000 per share,

plus accrued dividends.

Question: When evaluating the conversion option, what is the host contract (debt or equity)?

14

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Ms. Host

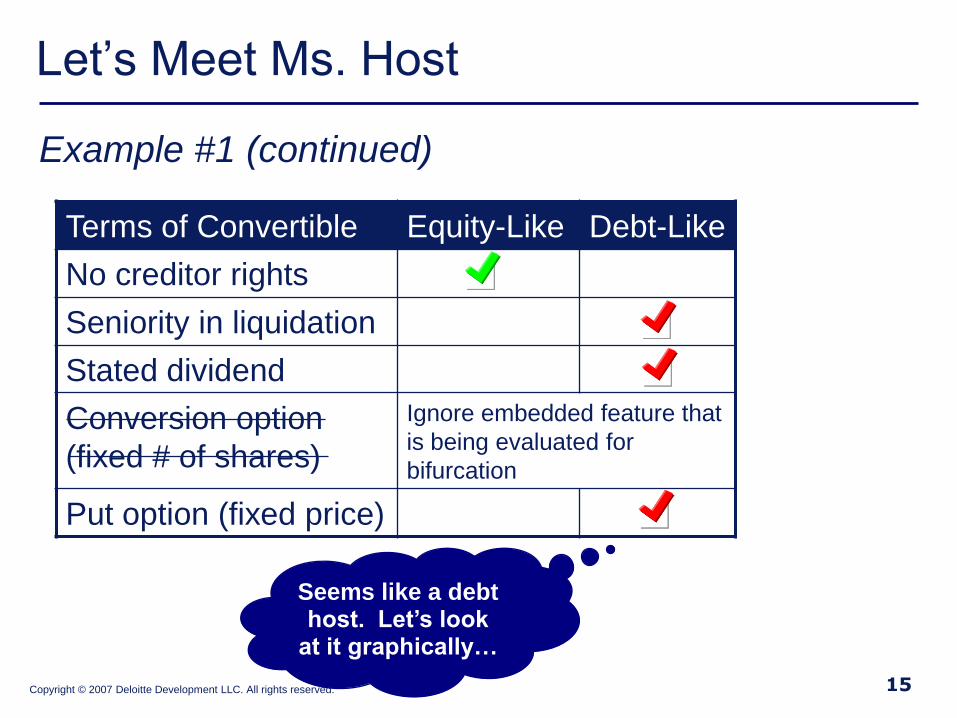

Example #1 (continued)

Terms of Convertible Equity-Like Debt-Like

No creditor rights

Seniority in liquidation

Stated dividend

Conversion option

(fixed # of shares)

Ignore embedded feature that

is being evaluated for

bifurcation

Put option (fixed price)

15

Seems like a debt host. Let’s look

at it graphically…

Copyright © 2007 Deloitte Development LLC. All rights reserved.

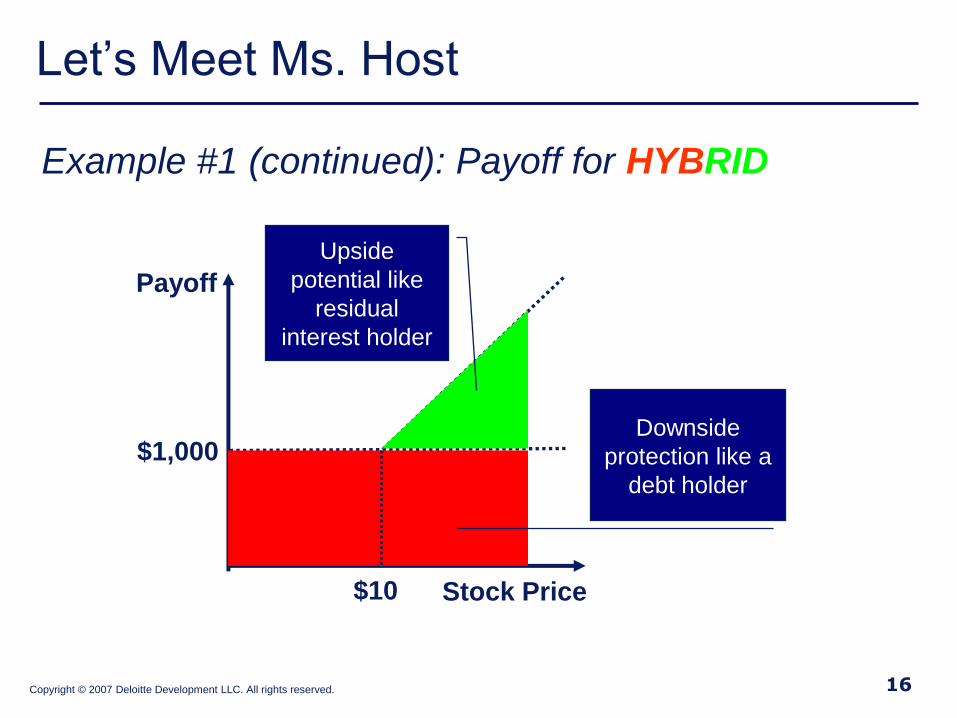

Let’s Meet Ms. Host

Example #1 (continued): Payoff for HYBRID

$10

$1,000

Stock Price

Payoff

Downside

protection like a

debt holder

Upside

potential like

residual

interest holder

16

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Ms. Host

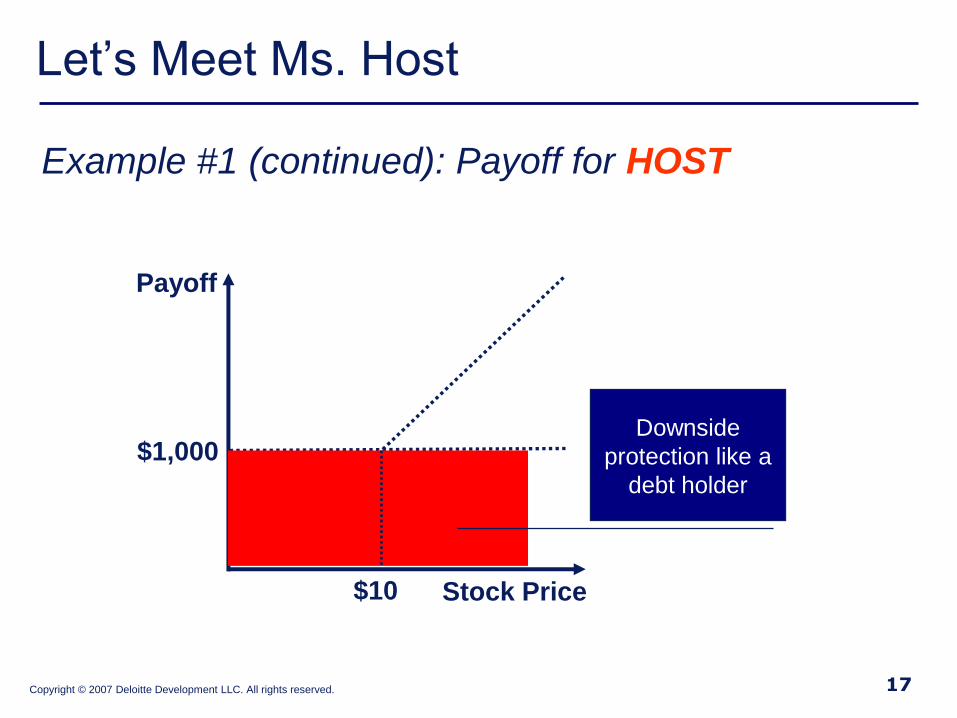

Example #1 (continued): Payoff for HOST

$10

$1,000

Stock Price

Payoff

Downside

protection like a

debt holder

17

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Ms. Host

Example #1 (continued)

A issues perpetual preferred shares:• liquidation preference of $1,000 per share• dividends of 6% per annum• convertible into 100 shares of A’s common stock• puttable by investor for cash of $1,000 per share,

plus accrued dividends.

Answer: DEBT HOST as embedded put at a fixed $ amount provides for downside protection, which is more debt-like.

18

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Ms. Host

Example #2

A issues perpetual preferred shares:• liquidation preference of $1,000 per share• dividends of 6% per annum• convertible into 100 shares of A’s common stock• puttable by investor for cash of $1,000 per share,

plus accrued dividends.

Question: When evaluating the put option, what is the host contract (debt or equity)?

Let’s say

hi to Ms.

Host!

19

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Ms. Host

Example #2 (continued)

Terms of Convertible Equity-Like Debt-Like

No creditor rights

Seniority in liquidation

Stated dividend

Conversion option

(fixed # of shares)

Put option (fixed price) Ignore embedded feature that

is being evaluated for

bifurcation

20

Copyright © 2007 Deloitte Development LLC. All rights reserved.

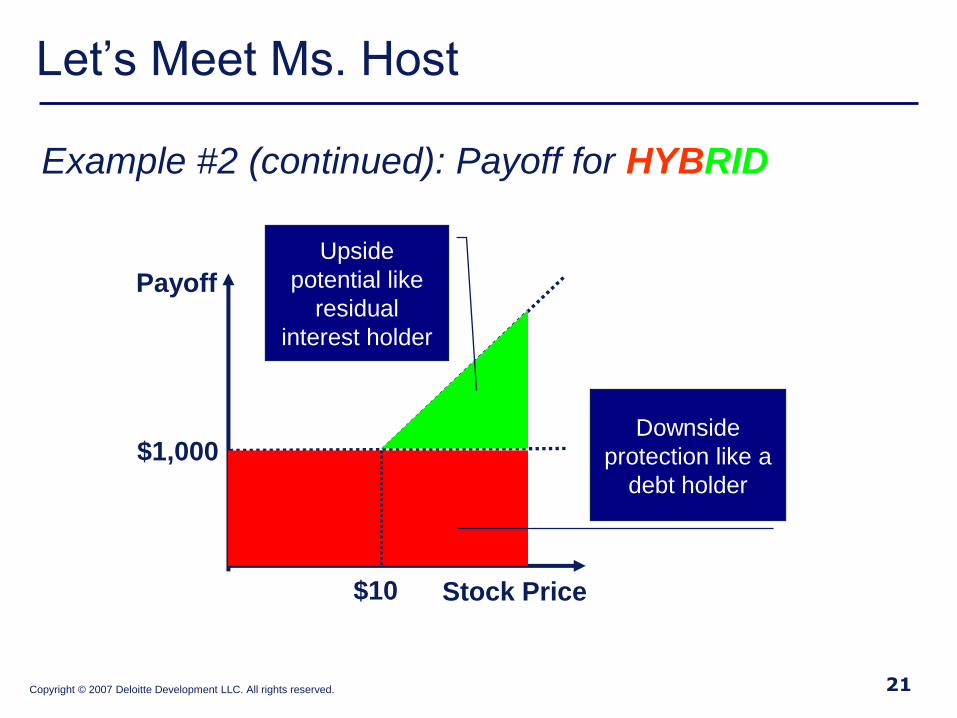

Let’s Meet Ms. Host

Example #2 (continued): Payoff for HYBRID

$10

$1,000

Stock Price

Payoff

Downside

protection like a

debt holder

Upside

potential like

residual

interest holder

21

Copyright © 2007 Deloitte Development LLC. All rights reserved.

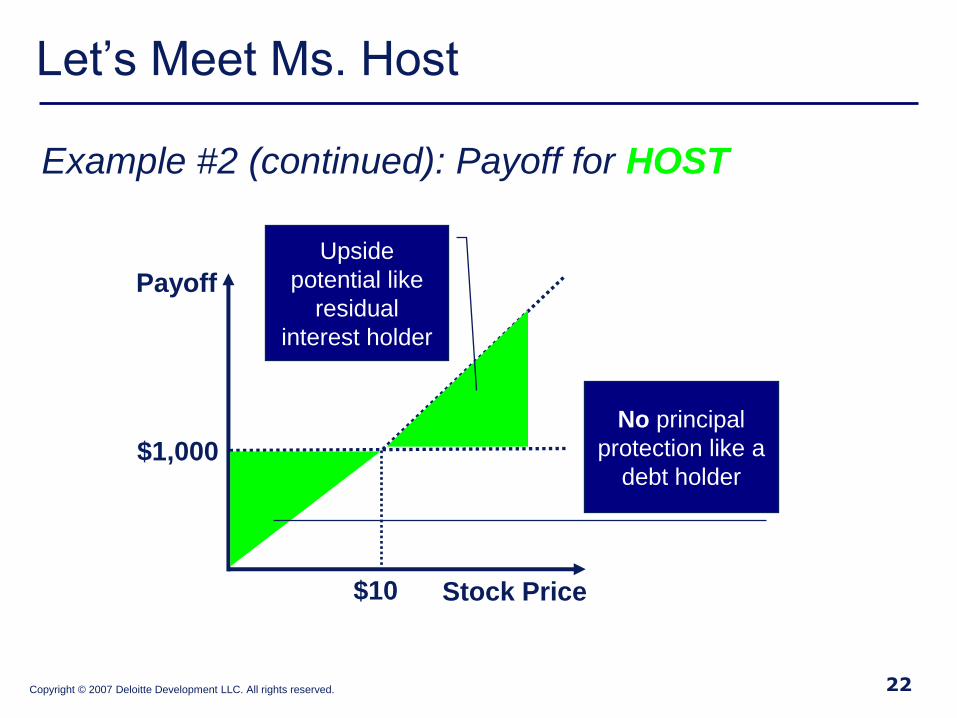

Let’s Meet Ms. Host

Example #2 (continued): Payoff for HOST

$10

$1,000

Stock Price

Payoff

Upside

potential like

residual

interest holder

22

No principal

protection like a

debt holder

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Ms. Host

Example #2 (continued)

A issues perpetual preferred shares:• liquidation preference of $1,000 per share• dividends of 6% per annum• convertible into 100 shares of A’s common stock• puttable by investor for cash of $1,000 per share,

plus accrued dividends.

Answer: EQUITY HOST as absent the fixed-price put, the economic profile of the preferred stock is more akin to that of a residual interest holder.

23

Copyright © 2007 Deloitte Development LLC. All rights reserved. 24

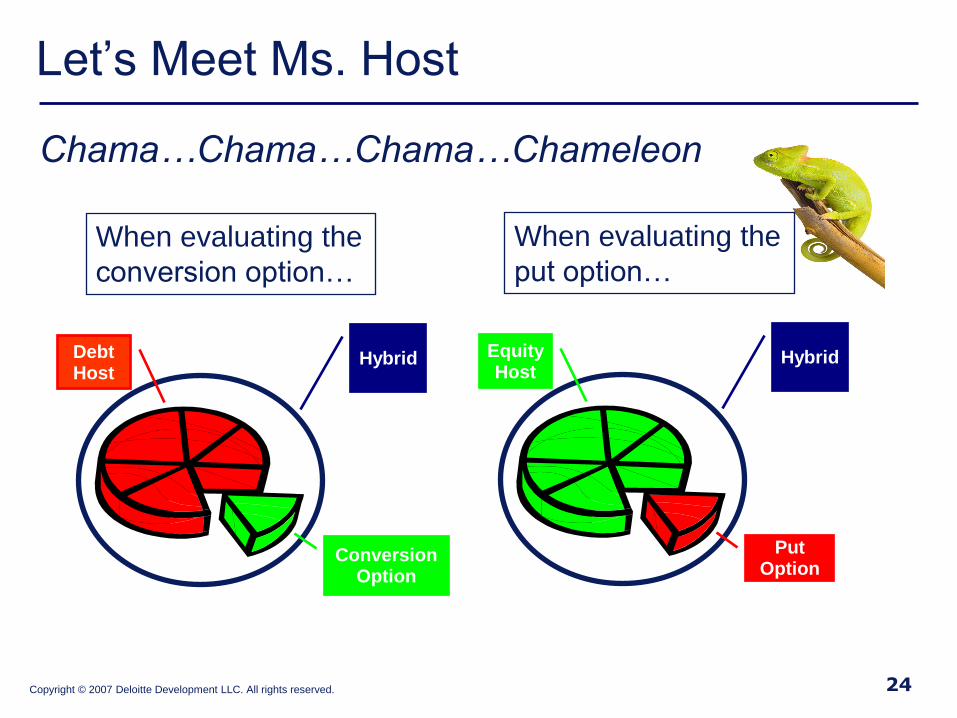

When evaluating the

conversion option…

Equity Host

Put Option

HybridDebt Host

Conversion Option

Hybrid

When evaluating the

put option…

Chama…Chama…Chama…Chameleon

Let’s Meet Ms. Host

Copyright © 2007 Deloitte Development LLC. All rights reserved. 25

To be clear: The Chameleon host approach is one of the acceptable approaches in EITF Topic D-109.

Let’s Meet Ms. Host

The ―clean-host‖ approach is no longer acceptable under EITF Topic D-109.

Remember: Consider all substantive terms of the convertible (absent the embedded feature being evaluated for bifurcation)!

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Polling Question #3

Test Question - Fill in the missing word:

The Chameleon host approach considers all substantive terms of a convertible, _________ the embedded feature that is being evaluated for bifurcation under FAS 133.

• Including

• Excluding

• Don’t know

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Mr. Conventional

26

Let’s see why he is so

popular…

Copyright © 2007 Deloitte Development LLC. All rights reserved.

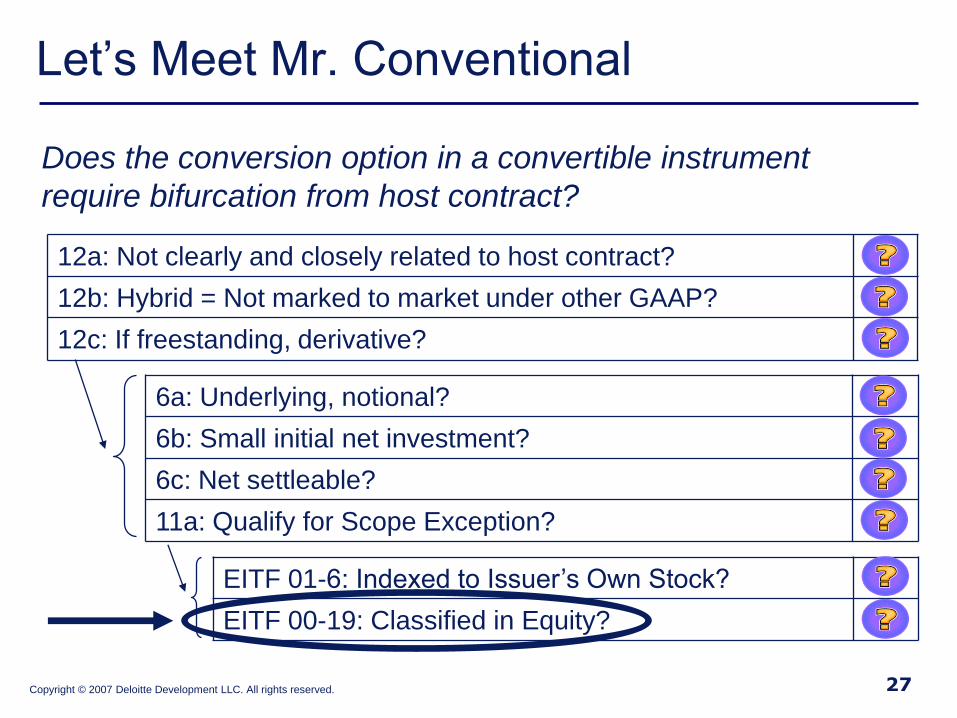

Let’s Meet Mr. Conventional

12a: Not clearly and closely related to host contract?

12b: Hybrid = Not marked to market under other GAAP?

12c: If freestanding, derivative?

6a: Underlying, notional?

6b: Small initial net investment?

6c: Net settleable?

11a: Qualify for Scope Exception?

EITF 01-6: Indexed to Issuer’s Own Stock?

EITF 00-19: Classified in Equity?

Does the conversion option in a convertible instrument

require bifurcation from host contract?

27

Copyright © 2007 Deloitte Development LLC. All rights reserved.

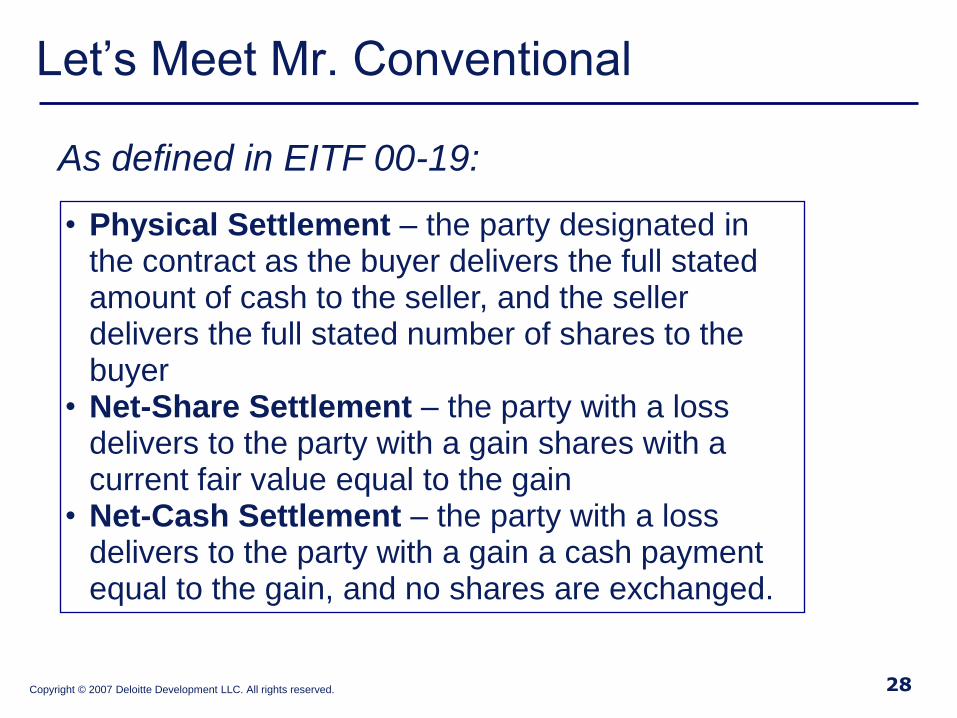

Let’s Meet Mr. Conventional

As defined in EITF 00-19:

• Physical Settlement – the party designated in the contract as the buyer delivers the full stated amount of cash to the seller, and the seller delivers the full stated number of shares to the buyer

• Net-Share Settlement – the party with a loss delivers to the party with a gain shares with a current fair value equal to the gain

• Net-Cash Settlement – the party with a loss delivers to the party with a gain a cash payment equal to the gain, and no shares are exchanged.

28

Copyright © 2007 Deloitte Development LLC. All rights reserved.

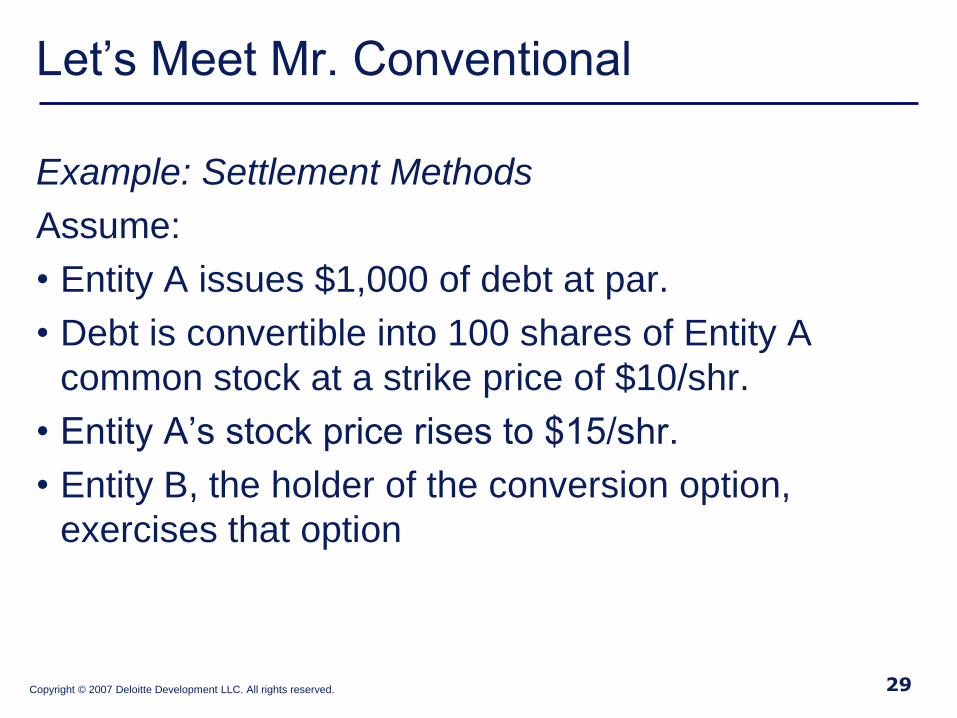

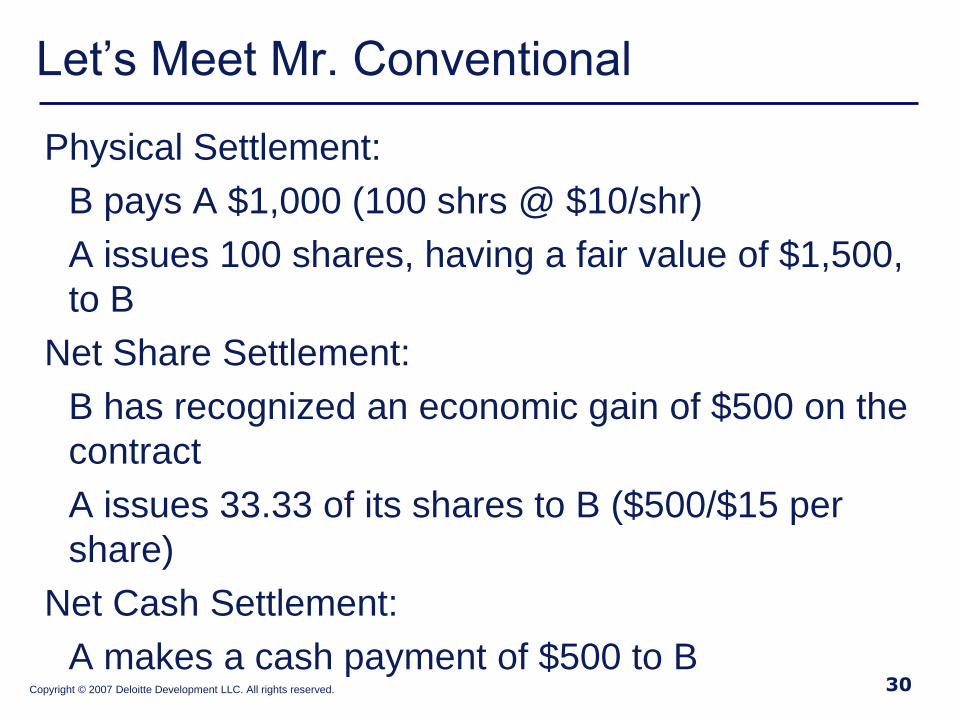

Let’s Meet Mr. Conventional

Example: Settlement Methods

Assume:

• Entity A issues $1,000 of debt at par.

• Debt is convertible into 100 shares of Entity A

common stock at a strike price of $10/shr.

• Entity A’s stock price rises to $15/shr.

• Entity B, the holder of the conversion option,

exercises that option

29

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Mr. Conventional

Physical Settlement:

B pays A $1,000 (100 shrs @ $10/shr)

A issues 100 shares, having a fair value of $1,500,

to B

Net Share Settlement:

B has recognized an economic gain of $500 on the

contract

A issues 33.33 of its shares to B ($500/$15 per

share)

Net Cash Settlement:

A makes a cash payment of $500 to B 30

Copyright © 2007 Deloitte Development LLC. All rights reserved.

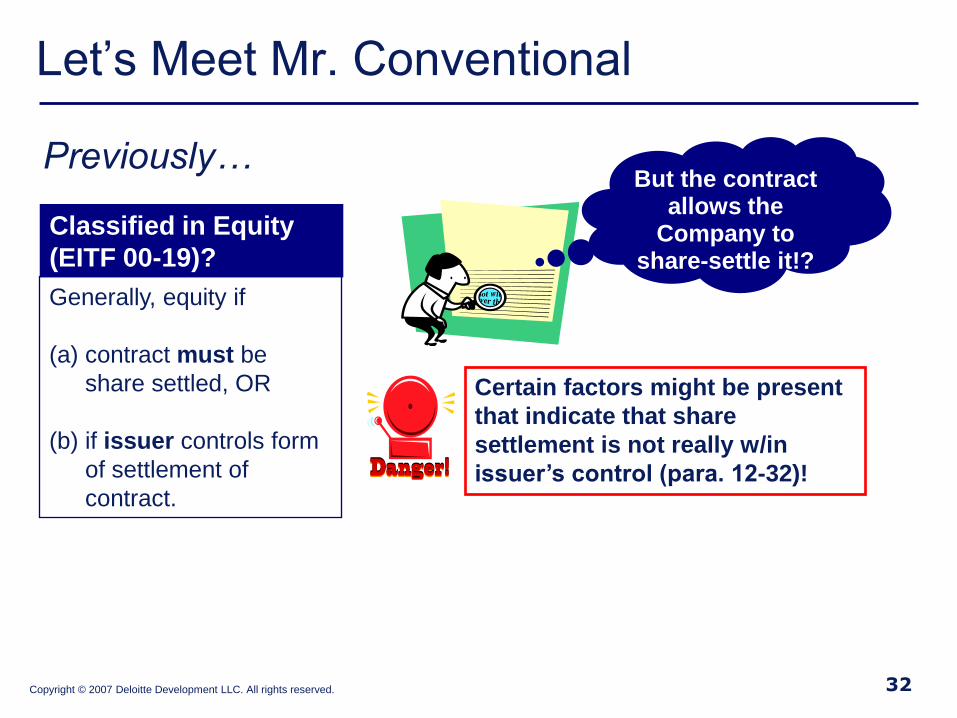

Let’s Meet Mr. Conventional

31

Classified in Equity

(EITF 00-19)?

Generally, equity if

(a) contract must be

share settled, OR

(b) if issuer controls form

of settlement of

contract.

Previously…

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Mr. Conventional

32

Classified in Equity

(EITF 00-19)?

Generally, equity if

(a) contract must be

share settled, OR

(b) if issuer controls form

of settlement of

contract.

Certain factors might be present

that indicate that share

settlement is not really w/in

issuer’s control (para. 12-32)!

But the contract allows the

Company to share-settle it!?

Previously…

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Mr. Conventional

33

Classified in Equity

(EITF 00-19)?

Generally, equity if

(a) contract must be

share settled, OR

(b) if issuer controls form

of settlement of

contract.

Certain factors might be present

that indicate that share

settlement is not really w/in

issuer’s control (para. 12-32)!

But the contract allows the

Company to share-settle it!?

Previously…

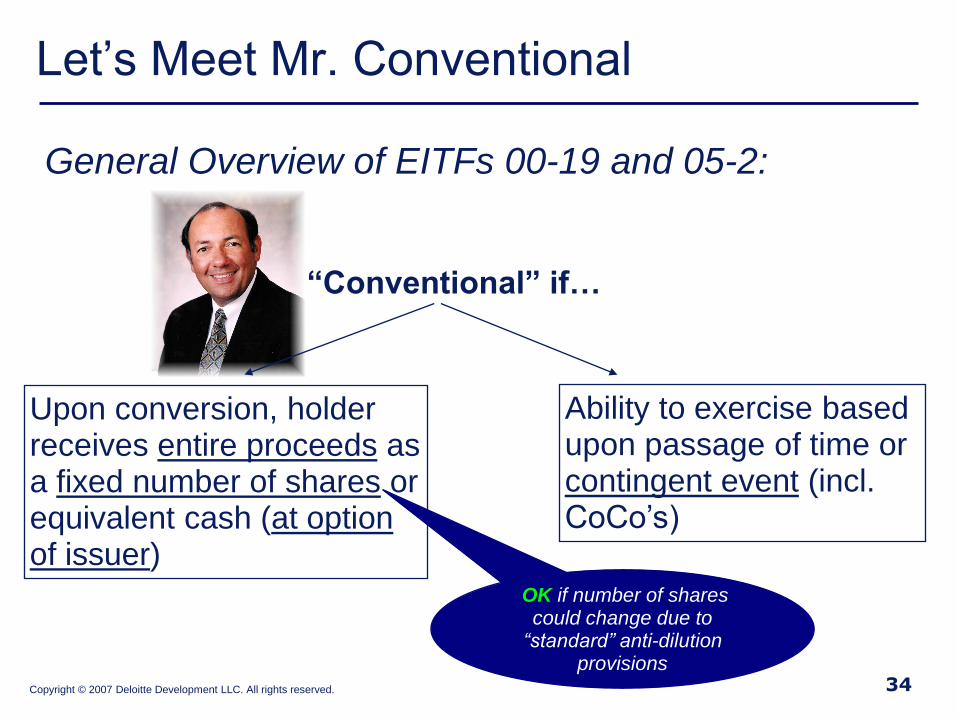

BUT: If convertible instrument qualifies as

CONVENTIONAL, those factors would not apply

to an otherwise share-settlable contract (see

EITF 05-2 for what qualifies as ―conventional‖).

Copyright © 2007 Deloitte Development LLC. All rights reserved. 34

Let’s Meet Mr. Conventional

Upon conversion, holder receives entire proceeds as a fixed number of shares or equivalent cash (at option of issuer)

Ability to exercise based upon passage of time or contingent event (incl. CoCo’s)

General Overview of EITFs 00-19 and 05-2:

“Conventional” if…

OK if number of shares could change due to

“standard” anti-dilution provisions

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Mr. Conventional

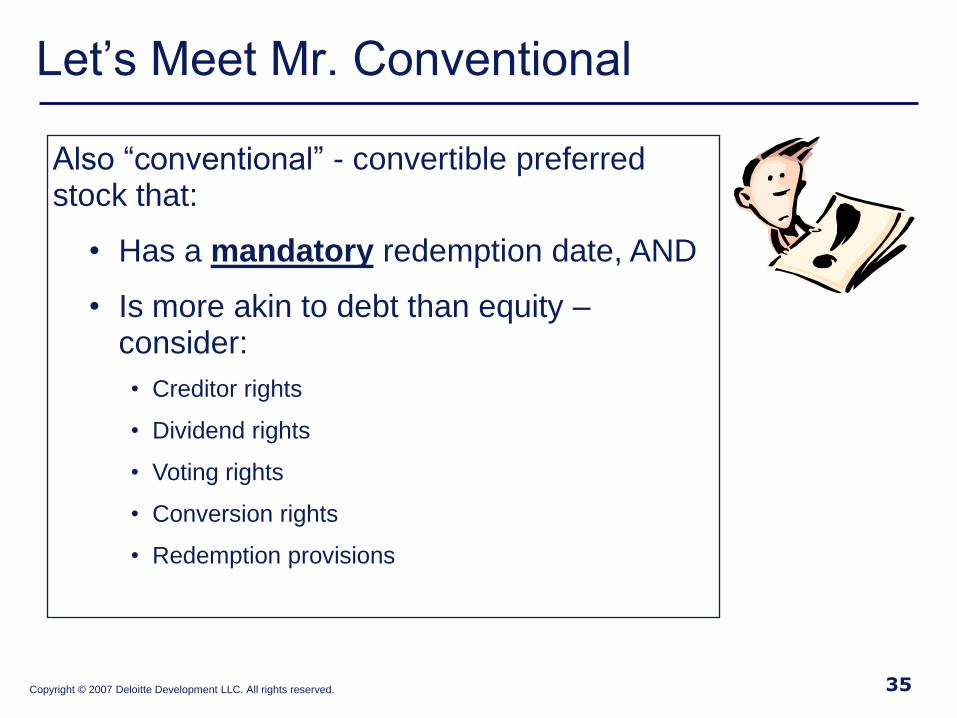

Also ―conventional‖ - convertible preferred stock that:

• Has a mandatory redemption date, AND

• Is more akin to debt than equity –consider:

• Creditor rights

• Dividend rights

• Voting rights

• Conversion rights

• Redemption provisions

35

Copyright © 2007 Deloitte Development LLC. All rights reserved.

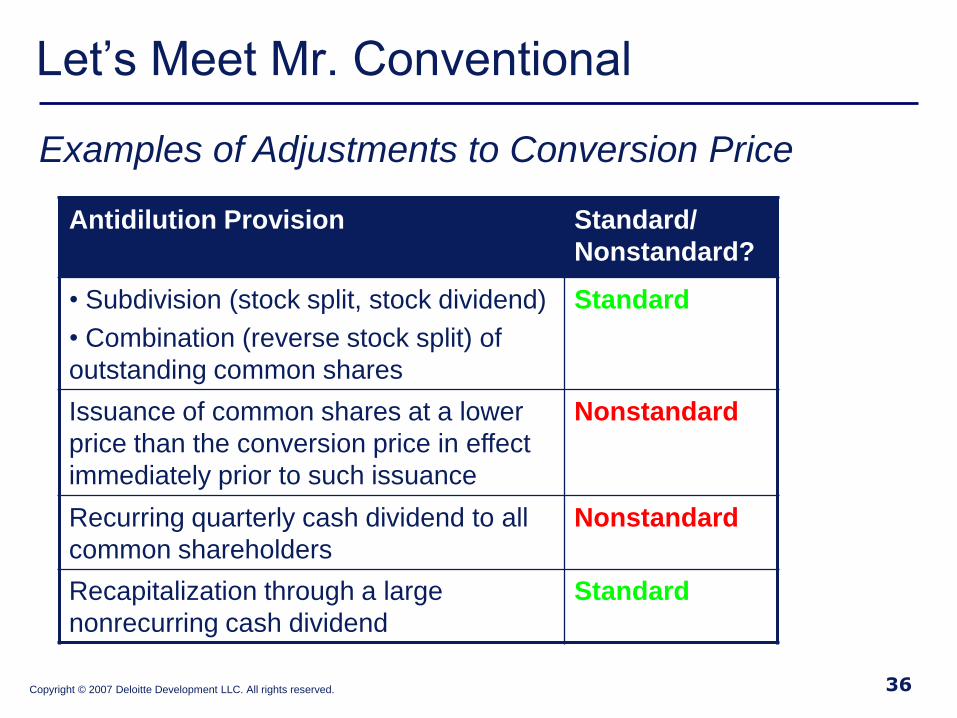

Let’s Meet Mr. Conventional

Examples of Adjustments to Conversion Price

Antidilution Provision Standard/

Nonstandard?

• Subdivision (stock split, stock dividend)

• Combination (reverse stock split) of

outstanding common shares

Standard

Issuance of common shares at a lower

price than the conversion price in effect

immediately prior to such issuance

Nonstandard

Recurring quarterly cash dividend to all

common shareholders

Nonstandard

Recapitalization through a large

nonrecurring cash dividend

Standard

36

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Mr. ―Not-So‖ Conventional

37

Let’s see why he loses the

popularity contest against

Mr. Conventional…

Copyright © 2007 Deloitte Development LLC. All rights reserved.

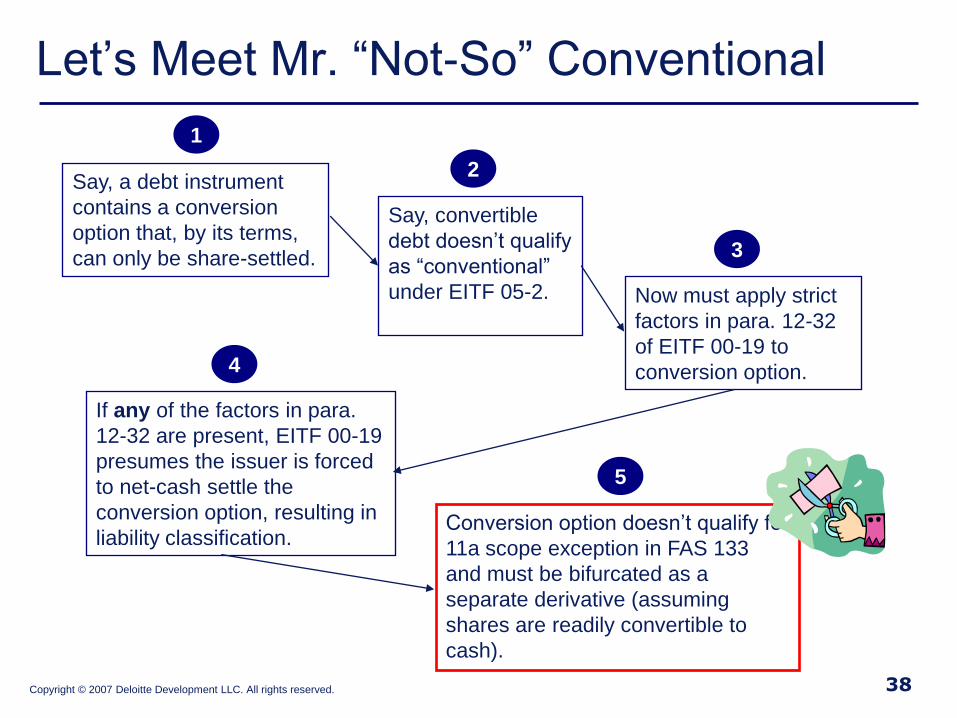

Let’s Meet Mr. ―Not-So‖ Conventional

Say, a debt instrument

contains a conversion

option that, by its terms,

can only be share-settled.

Now must apply strict

factors in para. 12-32

of EITF 00-19 to

conversion option.

Say, convertible

debt doesn’t qualify

as ―conventional‖

under EITF 05-2.

If any of the factors in para.

12-32 are present, EITF 00-19

presumes the issuer is forced

to net-cash settle the

conversion option, resulting in

liability classification.Conversion option doesn’t qualify for

11a scope exception in FAS 133

and must be bifurcated as a

separate derivative (assuming

shares are readily convertible to

cash).

38

1

2

3

4

5

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Polling Question #4

Test question: ―Instrument C‖ qualifies as conventional convertible debt.

(Reminder: ―Instrument C‖ requires cash settlement for the accreted value of the debt and permits the issuer to settle the conversion spread in either cash or shares.)

• True

• False

• Don’t Know/Not Applicable

Copyright © 2007 Deloitte Development LLC. All rights reserved.

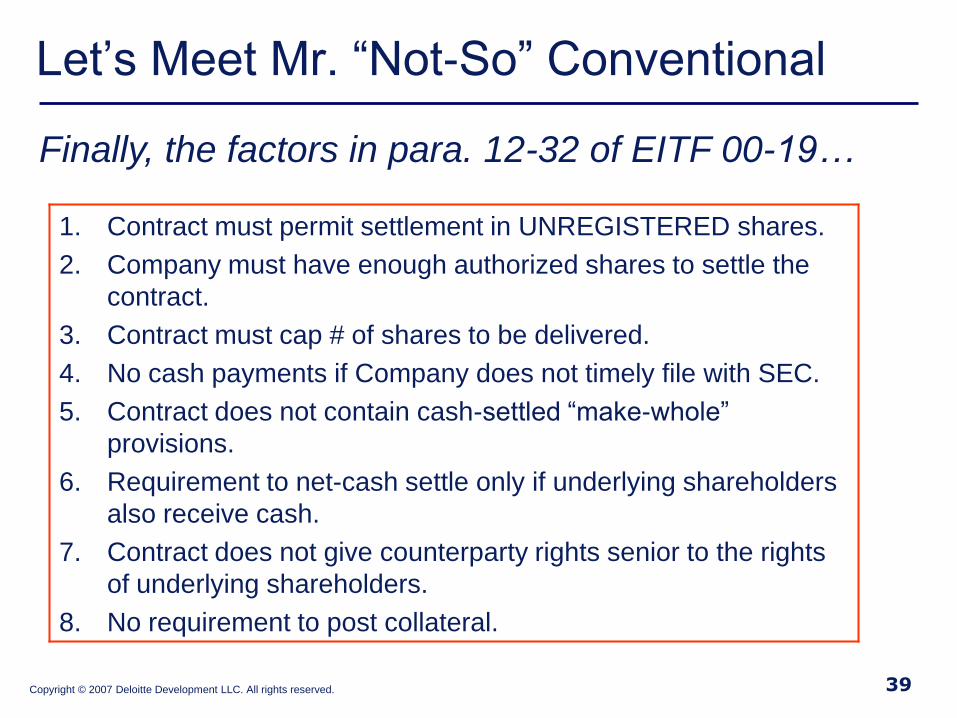

Let’s Meet Mr. ―Not-So‖ Conventional

1. Contract must permit settlement in UNREGISTERED shares.

2. Company must have enough authorized shares to settle the

contract.

3. Contract must cap # of shares to be delivered.

4. No cash payments if Company does not timely file with SEC.

5. Contract does not contain cash-settled ―make-whole‖

provisions.

6. Requirement to net-cash settle only if underlying shareholders

also receive cash.

7. Contract does not give counterparty rights senior to the rights

of underlying shareholders.

8. No requirement to post collateral.

Finally, the factors in para. 12-32 of EITF 00-19…

39

Copyright © 2007 Deloitte Development LLC. All rights reserved.

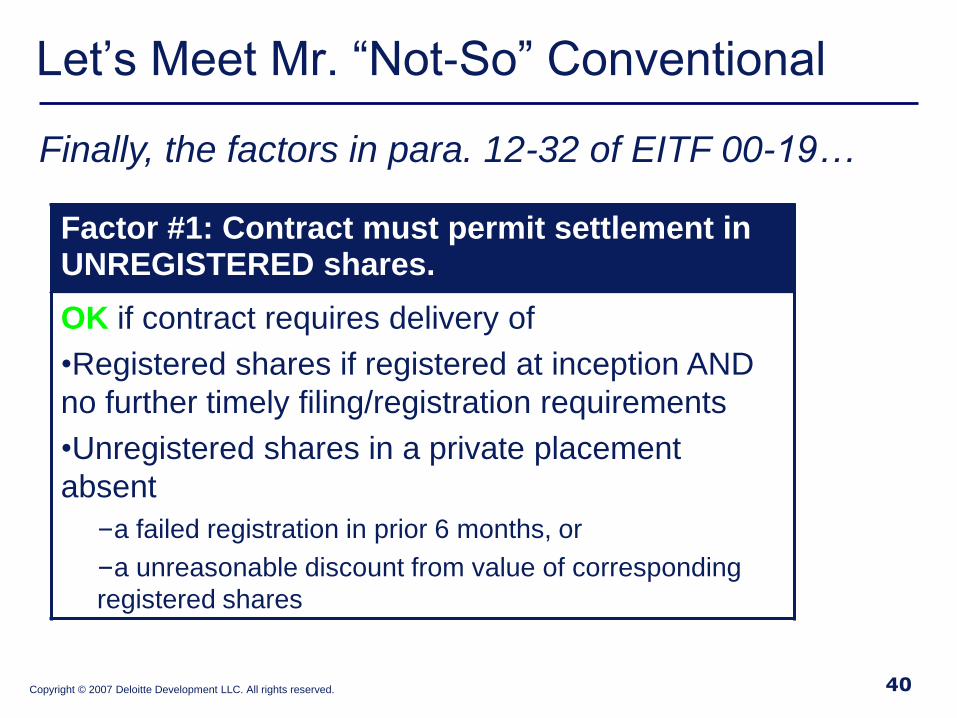

Let’s Meet Mr. ―Not-So‖ Conventional

Factor #1: Contract must permit settlement in UNREGISTERED shares.

OK if contract requires delivery of

•Registered shares if registered at inception AND

no further timely filing/registration requirements

•Unregistered shares in a private placement

absent

–a failed registration in prior 6 months, or

–a unreasonable discount from value of corresponding

registered shares

Finally, the factors in para. 12-32 of EITF 00-19…

40

Copyright © 2007 Deloitte Development LLC. All rights reserved.

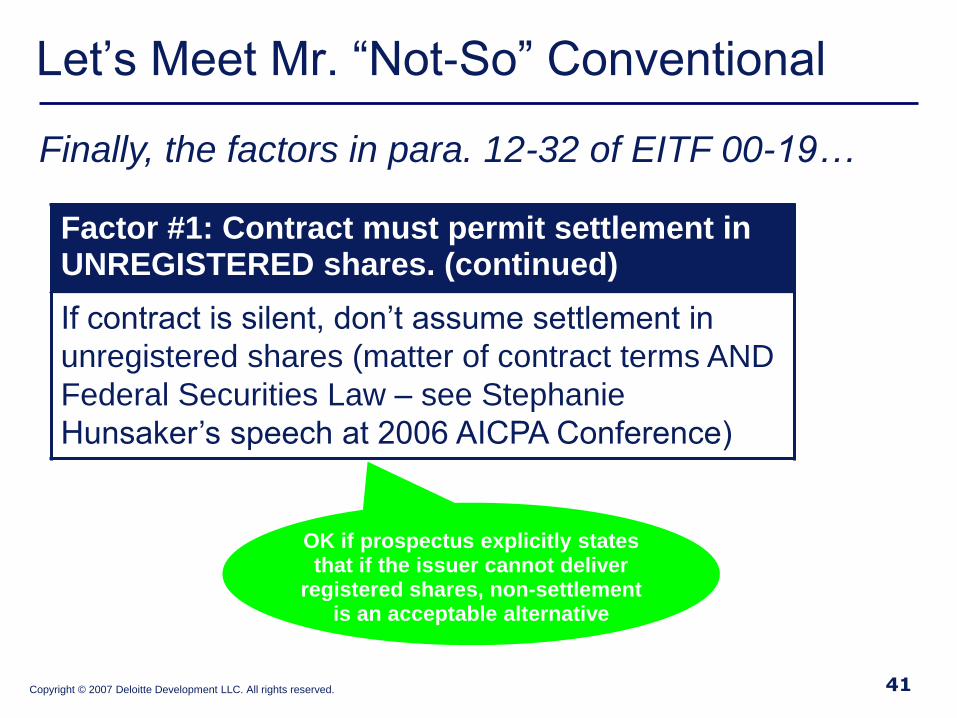

Let’s Meet Mr. ―Not-So‖ Conventional

Factor #1: Contract must permit settlement in UNREGISTERED shares. (continued)

If contract is silent, don’t assume settlement in

unregistered shares (matter of contract terms AND

Federal Securities Law – see Stephanie

Hunsaker’s speech at 2006 AICPA Conference)

Finally, the factors in para. 12-32 of EITF 00-19…

OK if prospectus explicitly states that if the issuer cannot deliver

registered shares, non-settlement is an acceptable alternative

41

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Mr. ―Not-So‖ Conventional

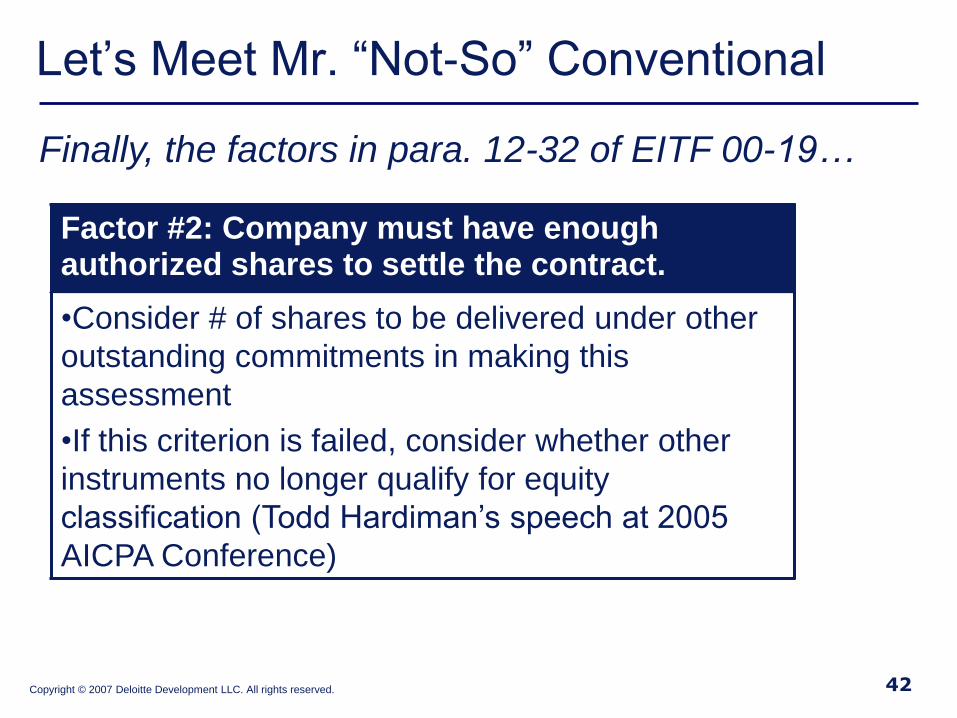

Factor #2: Company must have enough authorized shares to settle the contract.

•Consider # of shares to be delivered under other

outstanding commitments in making this

assessment

•If this criterion is failed, consider whether other

instruments no longer qualify for equity

classification (Todd Hardiman’s speech at 2005

AICPA Conference)

Finally, the factors in para. 12-32 of EITF 00-19…

42

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Mr. ―Not-So‖ Conventional

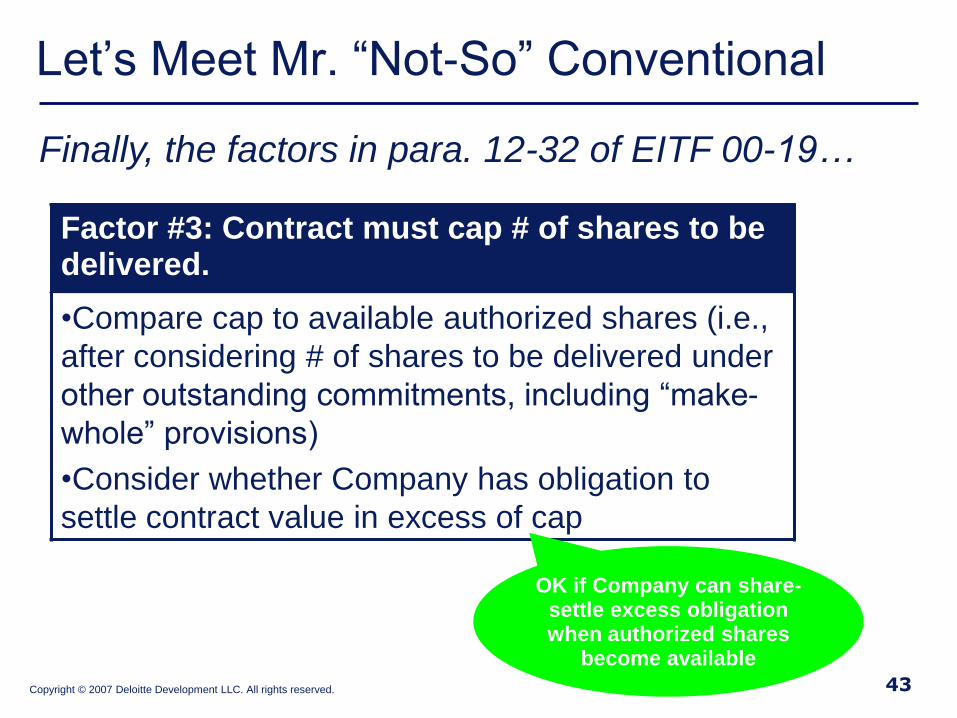

Factor #3: Contract must cap # of shares to be delivered.

•Compare cap to available authorized shares (i.e.,

after considering # of shares to be delivered under

other outstanding commitments, including ―make-

whole‖ provisions)

•Consider whether Company has obligation to

settle contract value in excess of cap

Finally, the factors in para. 12-32 of EITF 00-19…

OK if Company can share-settle excess obligation when authorized shares

become available

43

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Polling Question #5

Is Mr. Conventional looking better to you?

• Yes

• No

• Don’t Know/Not Applicable

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Mr. ―Not-So‖ Conventional

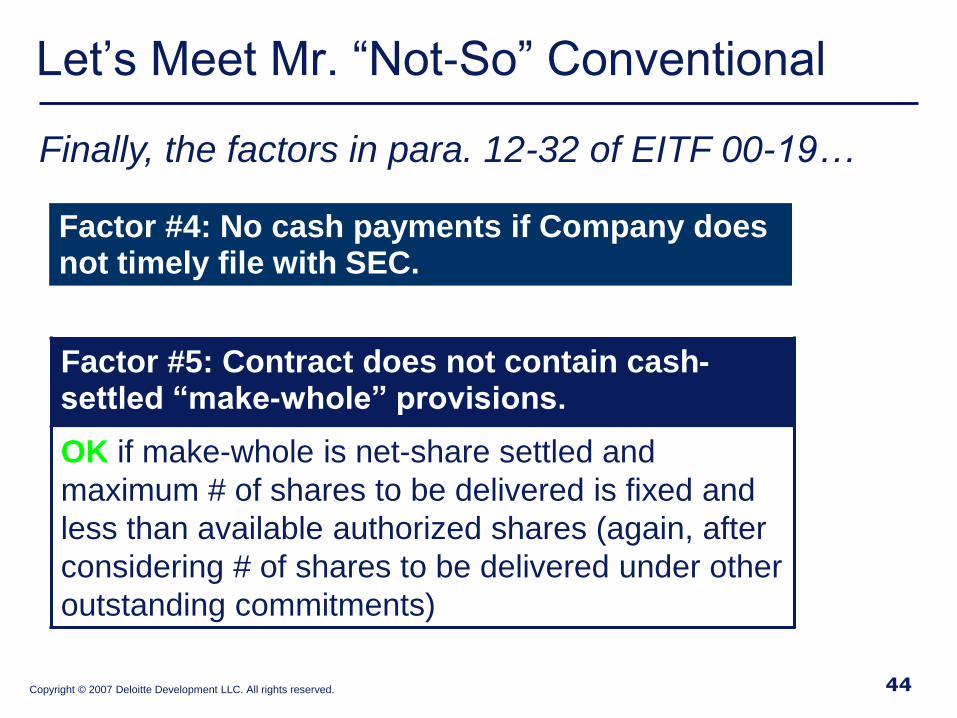

Factor #5: Contract does not contain cash-settled “make-whole” provisions.

OK if make-whole is net-share settled and

maximum # of shares to be delivered is fixed and

less than available authorized shares (again, after

considering # of shares to be delivered under other

outstanding commitments)

Finally, the factors in para. 12-32 of EITF 00-19…

Factor #4: No cash payments if Company does not timely file with SEC.

44

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Mr. ―Not-So‖ Conventional

Factor #6: Requirement to net-cash settle only if underlying shareholders also receive cash.

OK (i.e., contract would still be considered to be

indexed to stock of purchaser) if, upon change-in

control, contract holder and shareholders all were

to receive the same stock of acquirer

Finally, the factors in para. 12-32 of EITF 00-19…

Factor #7: Contract does not give counterparty rights senior to the rights of underlying shareholders.

45

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Mr. ―Not-So‖ Conventional

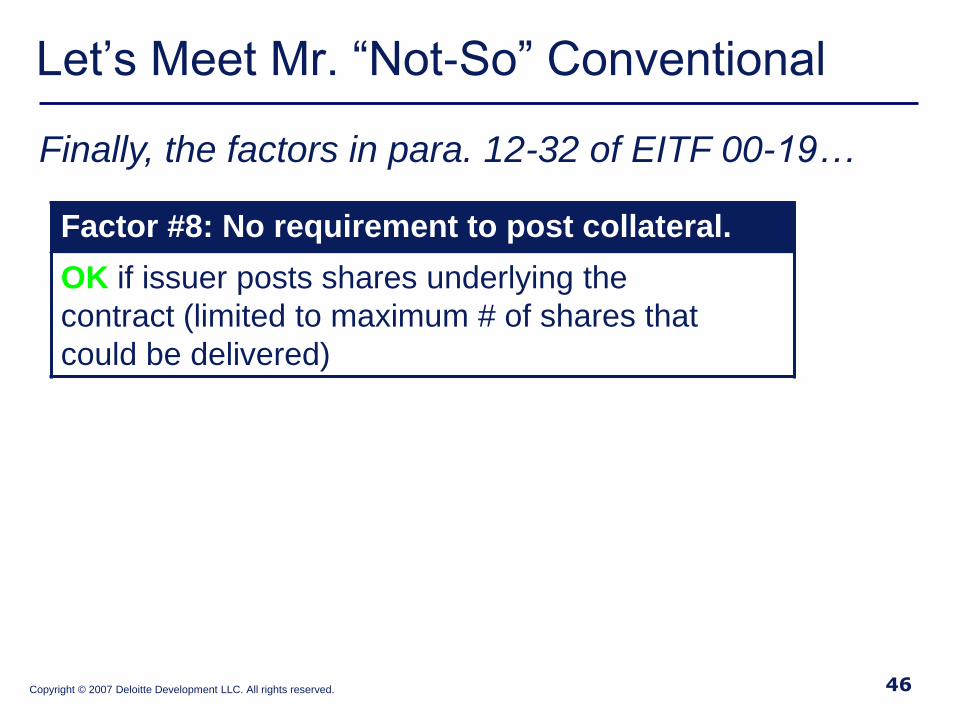

Factor #8: No requirement to post collateral.

OK if issuer posts shares underlying the

contract (limited to maximum # of shares that

could be delivered)

Finally, the factors in para. 12-32 of EITF 00-19…

46

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Mr. ―Not-So‖ Conventional

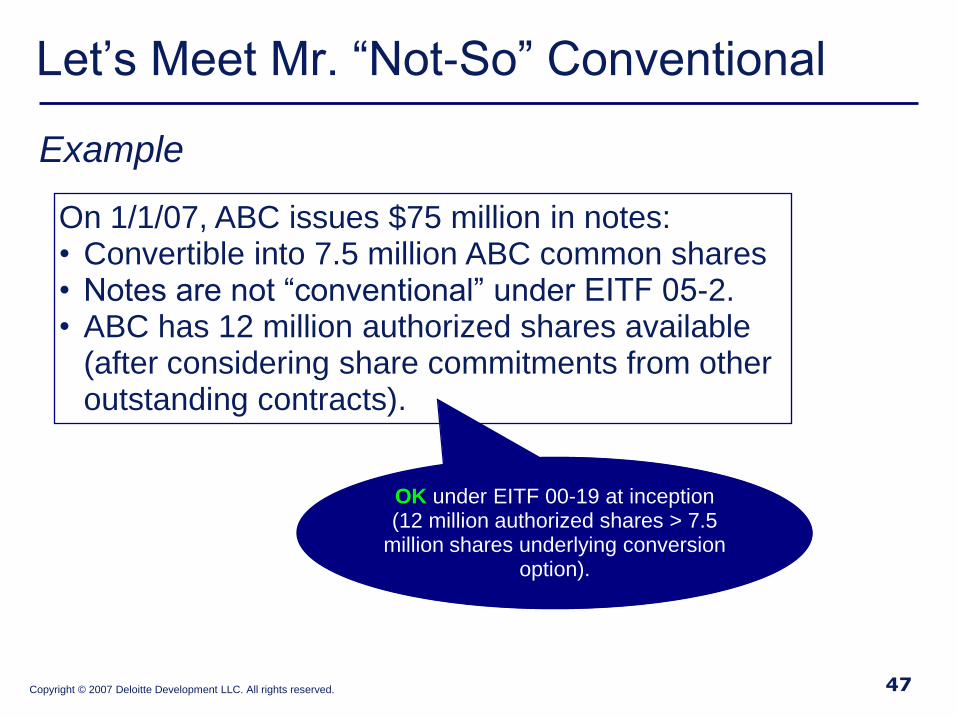

Example

On 1/1/07, ABC issues $75 million in notes: • Convertible into 7.5 million ABC common shares• Notes are not ―conventional‖ under EITF 05-2.• ABC has 12 million authorized shares available

(after considering share commitments from other outstanding contracts).

47

OK under EITF 00-19 at inception(12 million authorized shares > 7.5

million shares underlying conversion option).

Copyright © 2007 Deloitte Development LLC. All rights reserved.

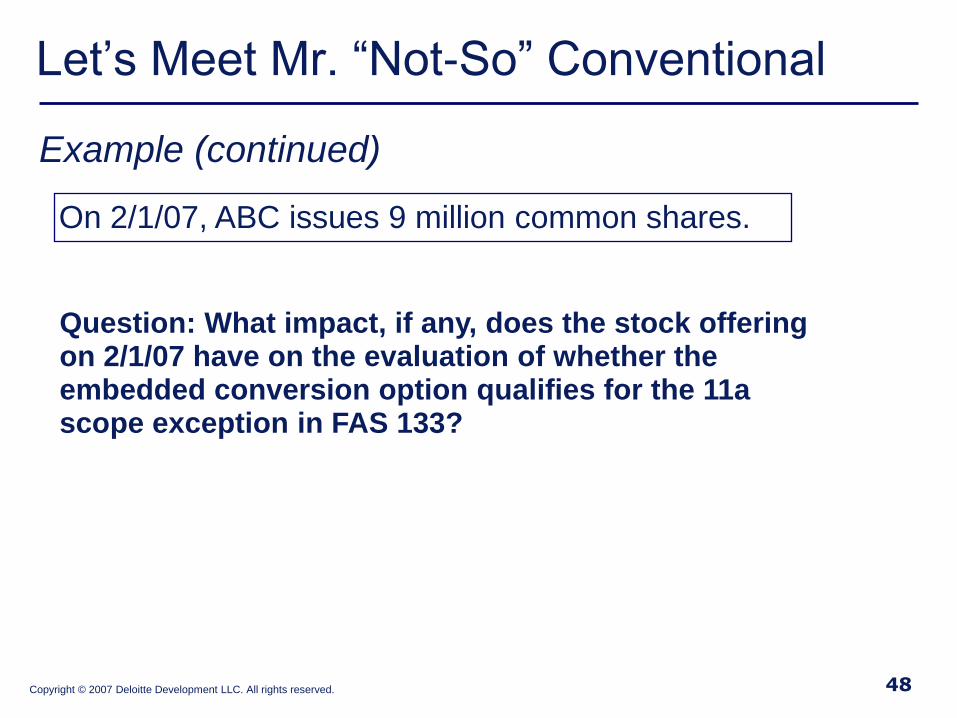

Let’s Meet Mr. ―Not-So‖ Conventional

Example (continued)

On 2/1/07, ABC issues 9 million common shares.

48

Question: What impact, if any, does the stock offering on 2/1/07 have on the evaluation of whether the embedded conversion option qualifies for the 11a scope exception in FAS 133?

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Let’s Meet Mr. ―Not-So‖ Conventional

# of authorized shares available 12,000,000

# of shares issued in seasoned offering 9,000,000

# of authorized shares remaining 3,000,000

# of shares underlying conversion option 7,500,000

# of excess underlying shares 4,500,000

translated in aggregate face value of notes $45,000,000

Example (continued)

49

Answer: As of 2/1/07, conversion option embedded in $45 million of notes would no longer qualify for the 11(a) scope exception in FAS 133 (fails Factor #2 in EITF 00-19).

Copyright © 2007 Deloitte Development LLC. All rights reserved.

The Contest

50

Being conventional involves

less maintenance…in

accounting terms, less work

because:

Now we know why Mr. Conventional is so popular…

• Don’t have to analyze

factors in para. 12-32 of

EITF 00-19

• Don’t need a law degree to

figure out whether issuer

can settle in unregistered

shares

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Polling Question #6

Test question: A conversion option is net-cash settleable upon a change of control. Equity or liability under EITF 00-19?

• Liability

• Equity

• Not enough facts

• Don’t know

Copyright © 2007 Deloitte Development LLC. All rights reserved.

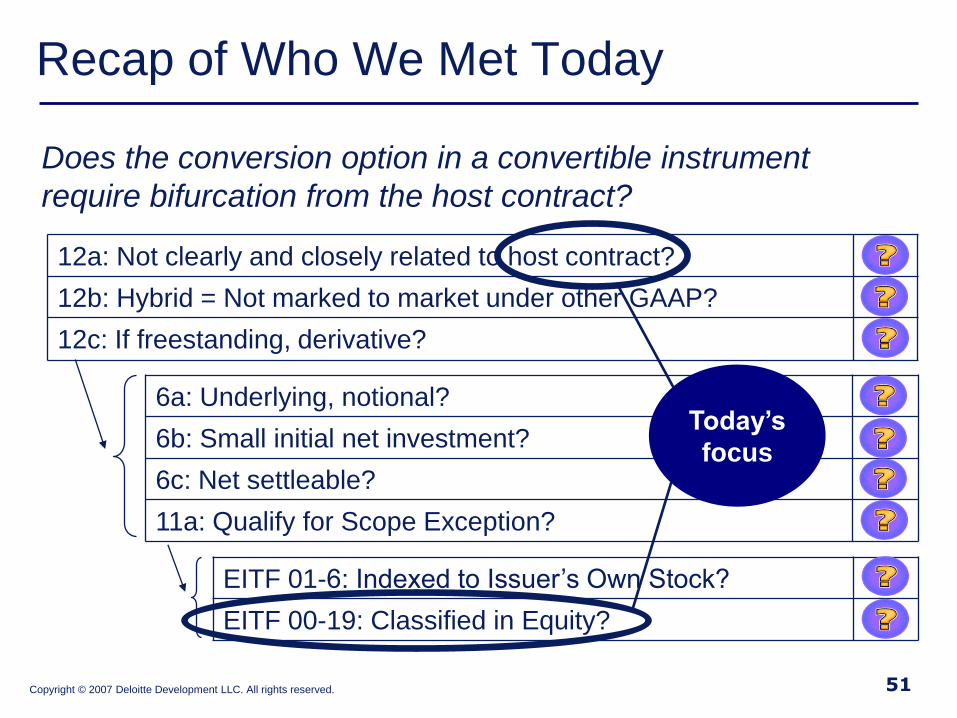

Recap of Who We Met Today

12a: Not clearly and closely related to host contract?

12b: Hybrid = Not marked to market under other GAAP?

12c: If freestanding, derivative?

6a: Underlying, notional?

6b: Small initial net investment?

6c: Net settleable?

11a: Qualify for Scope Exception?

EITF 01-6: Indexed to Issuer’s Own Stock?

EITF 00-19: Classified in Equity?

Does the conversion option in a convertible instrument

require bifurcation from the host contract?

51

Today’s

focus

Copyright © 2007 Deloitte Development LLC. All rights reserved.

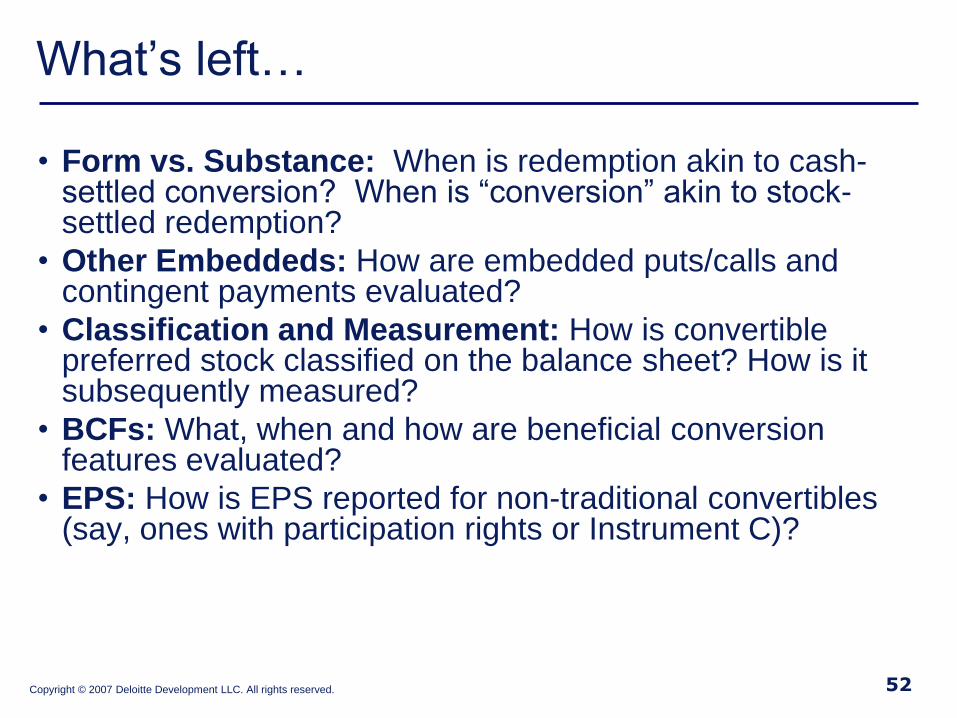

What’s left…

• Form vs. Substance: When is redemption akin to cash-settled conversion? When is ―conversion‖ akin to stock-settled redemption?

• Other Embeddeds: How are embedded puts/calls and contingent payments evaluated?

• Classification and Measurement: How is convertible preferred stock classified on the balance sheet? How is it subsequently measured?

• BCFs: What, when and how are beneficial conversion features evaluated?

• EPS: How is EPS reported for non-traditional convertibles (say, ones with participation rights or Instrument C)?

52

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Questions?

53

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Join us August 16th at 2 PM ET

as our Financial Reporting group

presents:

FIN 46(R): An Overview of

Consolidations

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Thank you for joining

today’s webcast.

To request CPE credit,

click the link below.

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Contact info

James Barker [email protected]

Michael Mueller [email protected]

Mark Bolton [email protected]

Magnus Orrell [email protected]

Copyright © 2007 Deloitte Development LLC. All rights reserved.

Other Resources at www.Deloitte.com

•To locate webcasts, click on the Dbriefs Webcast link at www.deloitte.com. You can find archived webcasts located under “Webcast Archives; Financial Executives”.•To locate other publications, such as Heads Up and Accounting Roundup, visit the “Assurance Newsletters” page on www.deloitte.com.

Copyright © 2007 Deloitte Development LLC. All rights reserved.

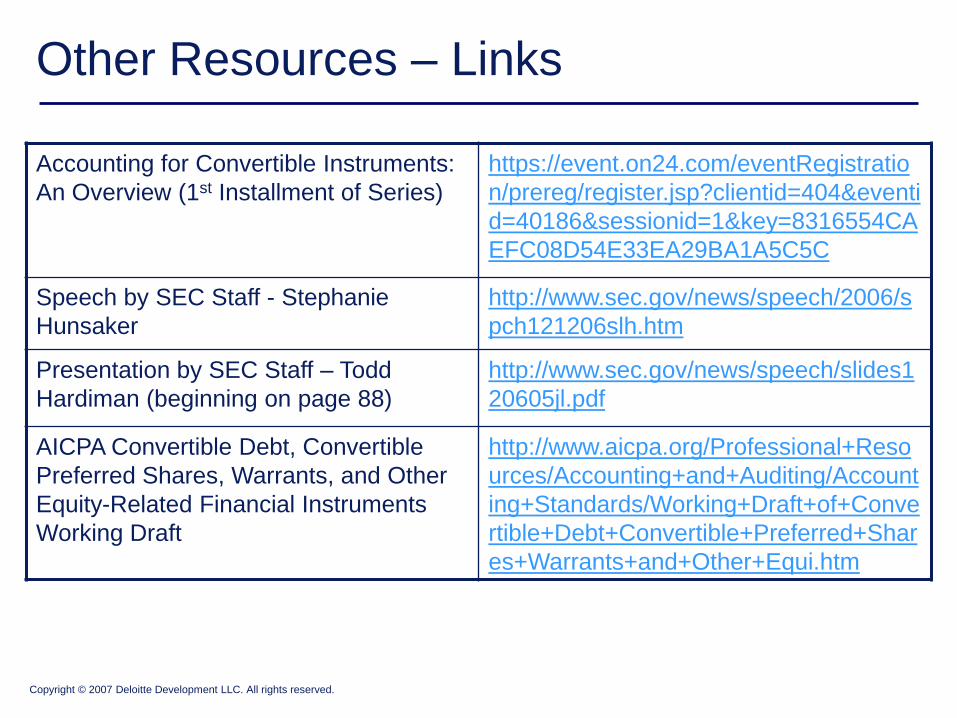

Other Resources – Links

Accounting for Convertible Instruments:

An Overview (1st Installment of Series)

https://event.on24.com/eventRegistratio

n/prereg/register.jsp?clientid=404&eventi

d=40186&sessionid=1&key=8316554CA

EFC08D54E33EA29BA1A5C5C

Speech by SEC Staff - Stephanie

Hunsaker

http://www.sec.gov/news/speech/2006/s

pch121206slh.htm

Presentation by SEC Staff – Todd

Hardiman (beginning on page 88)

http://www.sec.gov/news/speech/slides1

20605jl.pdf

AICPA Convertible Debt, Convertible

Preferred Shares, Warrants, and Other

Equity-Related Financial Instruments

Working Draft

http://www.aicpa.org/Professional+Reso

urces/Accounting+and+Auditing/Account

ing+Standards/Working+Draft+of+Conve

rtible+Debt+Convertible+Preferred+Shar

es+Warrants+and+Other+Equi.htm

Copyright © 2007 Deloitte Development LLC. All rights reserved.

The information contained in this publication is for general purposes only and is not

intended, and should not be construed, as legal, accounting, or tax advice or

opinion provided by Deloitte & Touche to the reader. This material may not be

applicable or suitable for, the reader’s specific circumstances of needs. Therefore,

the information should not be used as a substitute for consultation with professional

accounting, tax, or other competent advisors. Please contact a local Deloitte &

Touche professional before taking any action based upon this information.

Copyright © 2007 Deloitte Development LLC. All rights reserved.

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu, a Swiss Verein, its member firms, and their respective subsidiaries and affiliates. Deloitte

Touche Tohmatsu is an organization of member firms around the world devoted to excellence in providing professional services and advice, focused

on client service through a global strategy executed locally in nearly 140 countries. With access to the deep intellectual capital of approximately

150,000 people worldwide, Deloitte delivers services in four professional areas — audit, tax, consulting, and financial advisory services — and serves

more than 80 percent of the world’s largest companies, as well as large national enterprises, public institutions, locally important clients, and

successful, fast-growing global companies. Services are not provided by the Deloitte Touche Tohmatsu Verein, and, for regulatory and other reasons,

certain member firms do not provide services in all four professional areas.

As a Swiss Verein (association), neither Deloitte Touche Tohmatsu nor any of its member firms has any liability for each other’s acts or omissions.

Each of the member firms is a separate and independent legal entity operating under the names ―Deloitte,‖ ―Deloitte & Touche,‖ ―Deloitte Touche

Tohmatsu,‖ or other related names.

In the United States, Deloitte & Touche USA LLP is the U.S. member firm of Deloitte Touche Tohmatsu and services are provided by the subsidiaries

of Deloitte & Touche USA LLP (Deloitte & Touche LLP, Deloitte Consulting LLP, Deloitte Financial Advisory Services LLP, Deloitte Tax LLP, and their

subsidiaries), and not by Deloitte & Touche USA LLP. The subsidiaries of the U.S. member firm are among the nation’s leading professional services

firms, providing audit, tax, consulting, and financial advisory services through nearly 40,000 people in more than 90 cities. Known as employers of

choice for innovative human resources programs, they are dedicated to helping their clients and their people excel. For more information, please visit

the U.S. member firm’s Web site at www.deloitte.com

Copyright © 2007 Deloitte Development LLC. All rights reserved.

A member firm ofDeloitte Touche Tohmatsu