Embed Size (px)

Citation preview

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 1/25

Accounting conservatism andstock pricing: an analysis based

on China’s split-stock reformSong Zhu

School of Economics and Business Administration, Beijing Normal University, Beijing, China, and

Donglin XiaSchool of Economics and Management, Tsinghua University, Beijing, China

Abstract

Purpose – China’s securities market is growing gradually as well as the investors, analysts,intermediates and regulation authorities. Accounting earnings is a key determinant among the factorsinfluencing stock prices, which even overreacts to earnings. Split-stock reform (all-circulation reform) inChina provides a chance for investors to revaluate the stock prices. The purpose of this paper is toinvestigate the market reaction during the reform from the perspective of accounting conservatism.

Design/methodology/approach – Using the data of companies completing the split-stock reform,this paper empirically investigates how the accounting conservatism influences the market reactionaround re-open day after the reform.

Findings – Accounting information plays its role on stock pricing through the reform of split-stockreform in the China securities market, evident in the significantly positive relation between the proxiesof accounting conservatism and cumulative abnormal returns for one day, three days, ten days and 30days around re-open day after the reform. Also, the profitability of listed firms in the past will furtherimprove the positive relation between conservatism and market reaction.

Originality/value – There is ample theoretical work on stock pricing of accounting conservatism butempirical work is scarce, so this paper provides more evidence forthe role of stock pricingof accountingconservatism, especially in emerging markets. Second, current research on accounting conservatism inChina is focusing on whether conservatism exists and how the conservatism varies; this paper furtherextends the research field of conservatism from the pricing perspective. Third, researches based on thedeterminants of stock compensation and market reaction on stock reform lack theoretical analysis, whilethis paper provides a theory basis for the market reaction during the stock reform.

Keywords China, Securities markets, Stock prices

Paper type Research paper

1. IntroductionAccounting conservatism implies that measurement errors tend to underestimate the

earnings and netassets.If two estimates of earnings or assets to be received or paid in thefuture are approximately equally likely, then conservatism dictates that the lessoptimistic one be used (Statement of Financial Accounting Concepts No. 2, FinancialAccounting Standard Board, FASB). Conservatism indicates the inter-influence amongthe contractual parties (Watts, 2003; Ball et al., 2003) and determines how the profit isdistributed among those contractual parties (Ahmed et al., 2002; Francis et al., 2004;Ahmend and Duellaman, 2007; LaFond and Watts, 2008). Both the Financial AccountingConcepts of FASB and the Chinese General Accepted Accounting Principle (GAAP)

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/2040-8749.htm

Accountingconservatism

23

Received 2 August 2010Revised 12 October 2010

Accepted 1 November 2010

Nankai Business Review

International

Vol. 2 No. 1, 2011

pp. 23-47

q Emerald Group Publishing Limited

2040-8749

DOI 10.1108/20408741111113484

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 2/25

consider accounting conservatism as one of the important information qualities. So howdoes the accounting conservatism affect the efficiency of market, the effectivenessof firm operation and the economic decision of investors? This issue is the importantone for investors and standard setting authorities and is the basis of researches on

conservatism.In this paper, we investigate the valuation effect of accounting conservatism in the

context of China’s split-share structure reform[1]. Using the data of companiescompletingthe split-share structure reform, we find thataccounting information plays itsrole throughout the reform. The market recognizes the role of accounting conservatismon stock pricing, evidently shown by the significantly positive relationship betweenconservatism proxies and cumulative abnormal returns (CARs) for one day, three days,ten days and 30 days around re-open day after the reform. Also, the profitability of listedfirms in the past will further improve the positive relation between conservatism andmarket reaction. All in all, accounting conservatism has significant influence on stockpricing, affecting the decision making and expectation of investors.

Theoretical works on the valuation effect of accounting conservatism have been donefor many years (Ohlson, 1995; Feltham and Ohlson, 1996; Penman and Zhang, 2002;Watts, 2003); however, there has been little empirical work (Li, 2007; Balachandran andMohanram, 2008; Kim and Pevzner, 2010). Therefore, first, our work provides moreevidence of the role of accounting conservatism on stock pricing. Also, our work looks atthe situation of China, a typical emerging market, supplementing the research carriedout in the USA. Second, current researches on accounting conservatism in Chinaare focusing on whether conservatism exists and how the conservatism varies (Xia andZhu, 2009; Chen et al., 2010), whereas our work further extends the research field of conservatism from the perspective of stock pricing. Third, research based on thedeterminants of stock compensation and market reaction for the split-share structurereform in China are lack of theoretical analysis, while our work provides more theory

basis for the market reaction during the stock reform.Section 2 introduces the characteristics of stock valuation and development of Chinasecurities market, and then we elaborate China’s split-share structure reform issuein Section 3. Section 4 gives our hypothesis. Empirical analysis is in Section 6 andSection 7 concludes our paper.

2. The characteristics of stock valuation and development of Chinasecurities marketThe development of China’s A-share stock market has three evident seedtimes(Liang, 2003). The first phase is before 1995 – since the set up of the Shanghai Exchangeon November 26, 1990, the early stock market had developed slowly. The distinctcharacteristics are small size of market scale and the increasing conflict between stock

supply and demand. The development of the market is under the process of blindness.The second phase is from 1995 to 1998. During this phase, when the number of listedcompanies doubled, the securities market expanded with great speed. While this periodwas a time highly regulated by the authority, when the price-earning (PE) ratio is undercontrolled by less than 15 times in initial public offering (IPO), contrast with that after IPOby one sixth. The third phase is after 1998. Since 1998, the securities market had striddento a standard phase. However, China’s securities market is an emerging market of lessthan 20 years; an unsound and normative securities system cannot supervise and guide

NBRI2,1

24

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 3/25

the behaviors of speculators and investors. Though the stock market was foundedin 1990, the official security law, “The Security Law of People of Republic of China”,was not implemented until July 1, 1997. As the judicial/law system and relatedregulations are rapidly developing, it still cannot meet the need of constructing an efficient

capital market. Regarding the enforcement aspect, China’s securities market still hassome problems, especially those illegal affairs without restrictive punishment. On theother hand, the number of canonical institutional investors is few and the number of small investors is large, leading to the deficiency of investor structure. This deficiencyresults in a lack of stability in the market, providing conditions for minority institutionalspeculators to manipulate thestock price viatheir advantages of capitals and information.The speculation atmosphere is severe in the market, investors including the institutionalinvestors intend to prefer the short-term trading, and some institutional investors evenmanipulate the trend of stock price. In addition, the consulting organizations, whichshould play as an intermediary to speed up the information delivery, however, prick upthe information asymmetry in the securities market, further promoting the short-termtrading (Tian, 2003; Tang, 2003; Tan, 2003). Stock turnover ratio in China’s securitiesmarket, in Shanghai or Shenzhen, is much higher than that in foreign capital markets.From 1992 to 2000, the turnover ratioin A-share stock market wasfour times a year; someindividual stock is even turned over higher to 100-200 times. Whilethis PE ratioin foreignmarkets is usually around 15 times, in China’s A-share market, the average level isabove 30, for some individual stock it is hundreds of times, even thousands of times(Tian, 2003).

Information promotes the market to the equilibrium. When information conveyssignals to some investors, changing their prior belief about the stock price, themarket will make corresponding adjustments (Grossman and Stigliz, 1976). Accountingearnings is the most popular information receiving the attentions of investors,and earnings information in annual and periodical reports guides the “intrinsic value”

of stocks and is most valuable. Therefore, disclosure of earnings information has themost influence on the behavior of investors. The unexpected earnings and sign of stockCAR are positively related; the abnormal return (AR) during the announcements periodis positively related with the unexpected earnings (Chen et al., 1999). Also, during theearnings announcement period, there exists an abnormal turnover phenomenon, and theinformation is probably released ahead of schedule (Chen and Chen, 2001). Informationis released in advance when significant events happen, such as the earnings’ fiercelyfluctuation, high seasoned offerings, significant investment, ownership transferringand so on. In China’s securities market, manipulation of stock price by the insiders withinformation advantage is severe. Wire-pullers with the inside information can purchasestock in advantage of their capital dominance before the release of information and sellout those stocks or continuously drive up the price after the release. Manipulation by the

bankers aggravates the quality of accounting information disclosure (Chen and Qin,2003). In other words, stock price can hardly reflect the fundamental value of firms if it ismanipulated by the bankers. Manipulation by the bankers leads to the over-fluctuationof stock prices. The market is pervaded with the atmosphere of speculation. Investorsincluding the institutional investors tend to prefer the short-term trading, and someinstitutional investors even manipulate the stock price (Zhang and Chen, 2001).

The heavy speculative atmosphere in China’s securities market leads to bubbles instock prices. In 2001, economists, like Jinglian Wu, had a fierce debate about the stock

Accountingconservatism

25

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 4/25

bubble in China’s securities market. Fureng Dong suggests that if PE ratio is compared,this ratio in China is much lower than that in Japan, where the PE rate is higher to80 times, even 100 times. PE ratio in China seems to be high, but it is still reasonable.First, since China’s securities market is still in its young phase, and supply of stock

cannot meet the demand, this results in high stock prices. Second, stocks in China are notall circular, only one-third of those stocks can be traded in the open market[2], thus theprice seems to perform well and is high. Xiaonian Xu suggests that it is not realistic tofind a reasonable PE ratio in the world. Considering the current situation in China’ssecurities market, investors should admit that the PE ratio seems to be overvalued.Weiying Zhang proposes that some listed companies are deficient, manipulating theiraccounting records and suffering loses. But why do the investors still pay much moneyfor their stocks? It is evident that there exits some bubbles. Considering this, he supportsthe judgement of Jinglian Wu. Economists represented by Jinglian Wu suggest that PEratio of, for example, 60 times is so high that the growth of the economy in any countrycannot sustain such a high PE ratio.

These comments and qualitative analysis by economists about the bubbles in China’ssecurities market is explanatory to some extent; however, it is not enough. Though theempirical research is a few and almost indirectly test to ascertain the bubble, those cangive quantitative support for existence of bubbles. Researchers investigate whether dataare meeting the certain characteristics and conditions of bubbles, exemplified by theauto regression test in Zhou (1998) and Zhou and Zhang (1999). Li (2005) directlyinvestigates the 13 years’ time series characteristics of the Shenzhen index from October1992 to June 2005, starting with a description of the trend behavior of certainty bubbletheory model. His results show that this model can explain the stock movementpreferably, supporting the existence of bubbles in China’s securities market. Debatesamong economists and the evidence in empirical research indicate bubbles in the marketand the stock prices are overvalued.

3. China’s split-stock reformBubbles in the securities market, over speculation and kinds of adverse behaviors toinvestors are related to the phenomenon of ownership separation (not all-circulation of stocks) to some extent, such as the high premium phenomenon in IPOs (Liu and Li, 2000;Du et al., 2001), and the corporate governance problems related with the largestshareholders, including related party transactions (Chen and Wang, 2005), embezzlingthe listed companies (Li et al., 2004; Zhang and Xu, 2005; Ma et al., 2005), tunneling cashdividends (Yuan, 1999; Lv and Zhou, 2005) and changing the use of capital raised (Zhangand Zhai, 2005). Ownership separation means that not all stocks can be traded in thepublic market, which is disadvantageous for shareholders whose stocks cannot betraded freely. These shareholders and management with un-circular stocks cannot

achieve benefit of stock appreciations in the public market; on the other hand,shareholders with circular stocks, and even the market, have no power to force thecontrolling shareholders and management to make decisions beneficial to small circularshareholders because they have less voting rights. Therefore, those controllingshareholders and management do not care about the market price of their stocks, andwhat they want are embezzlement and tunneling from those minorities. Current marketvaluation in China’s securities market is severely distorted due to the ownershipseparation (Ba, 2005).

NBRI2,1

26

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 5/25

As an attempt to solve the ownership separation problem, the State Departmentissued “Regulations on Decreasing State Ownership to Raise the Fund for SocialSecurity” in June, 2001 (State Council of China, 2001). However, this guide wasvehemently opposed by the market, represented by the dramatic drop-off in prices for all

stocks. Four months later, on October 22, 2001, China Securities Regulation Committee(CSRC) announced that it had ceased to implement the fifth term in “Regulations onDecreasing State Ownership to Raise the Fund for Social Security” (State Council of China, 2001), and it would publicly collect proposals of decreasing the state ownershipin listed companies and investigate the proper solutions to complete this reform. On

June 23, 2002, the State Department announced that it would cease implementing theterm of decreasing the state ownership in the “Regulations on Decreasing StateOwnership to Raise the Fund for Social Security” (State Council of China, 2001) exceptfor those companies listed abroad. Hence, the policy of decreasing state ownership wassuspended officially. In early February 2004, the State Department issued the “The StateDepartments’ Opinions about the Stable Development and Opening Reform of CapitalMarket” (State Council of China, 2004), pointing out definitely that “solve the separation

of ownership stably and affirmatively”. On April 29, 2005, CSRC issued “Notice aboutthe Issues related with the Ownership Separation Reform Experiment” (CSRC, 2005)in the allowance of the State Department, indicating the start-up of experiments of ownership separation reform (split-stock reform).

On May 9, 2005, four listed companies, including Tsinghua Tongfang, SanyiZhonggong, Zijiang qiye and Jinniu Energy, were on the first tentative list to initial theall-circulation reform. On September 12, the first list was announced including 40 listedfirms. From then on, all listed companies in China’s A-share market were beginning tolaunch the all-circulation reform and that thing was even put on the official agenda to befinished in 2006.

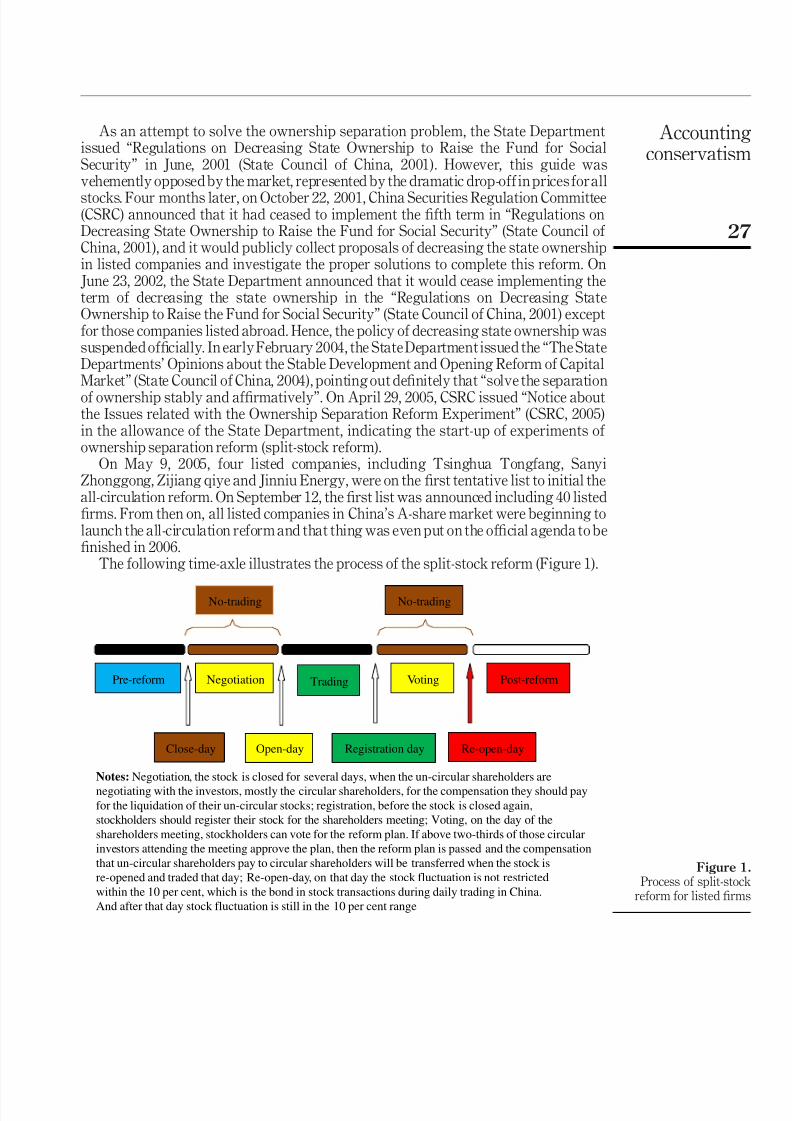

The following time-axle illustrates the process of the split-stock reform (Figure 1).

Figure 1.Process of split-stock

reform for listed firms

Pre-reform

Close-day

Negotiation Trading Voting Post-reform

Open-day Registration day Re-open-day

No-trading No-trading

Notes: Negotiation, the stock is closed for several days, when the un-circular shareholders are

negotiating with the investors, mostly the circular shareholders, for the compensation they should pay

for the liquidation of their un-circular stocks; registration, before the stock is closed again,

stockholders should register their stock for the shareholders meeting; Voting, on the day of the

shareholders meeting, stockholders can vote for the reform plan. If above two-thirds of those circular

investors attending the meeting approve the plan, then the reform plan is passed and the compensation

that un-circular shareholders pay to circular shareholders will be transferred when the stock is

re-opened and traded that day; Re-open-day, on that day the stock fluctuation is not restricted

within the 10 per cent, which is the bond in stock transactions during daily trading in China.

And after that day stock fluctuation is still in the 10 per cent range

Accountingconservatism

27

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 6/25

While the listed firms are beginning to launch the split-stock reform, the stock is closedfor several days when the un-circular shareholders are negotiating with the investors,mostly the circular shareholders, for the compensations they should pay for the right of the liquidation of their un-circular stocks. After they decide the compensation and the

reform plan, the stock is re-opened and investors can trade the stock in the market. Sincein the reform plan, it will announce the time of the shareholders’ meeting, during whichthe reform plan will be voted on. Before the stock is closed again, stockholders shouldregister their stocks for the shareholders meeting, and then on the day of theshareholders’ meeting, they can vote for the reform plan. If above two-thirds of thosecircular investors who attend the meeting agree with the plan, the reform plan is passedand the compensation that un-circular shareholders pay to circular shareholders will betransferred when the stock is re-opened and traded that day. On that day, the stockfluctuation is not restricted within the 20 per cent boundary upward and downward,which is the bond in stock transactions during daily trading in China. After that day,stock fluctuation is still in the 20 per cent range.

Why do the un-circular shareholders pay compensation to the circular-shareholders?

Because shares of un-circular shareholders are not allowed to circular in the secondmarket before the reform (due to some complicated historical reasons), and if they wanttheir shares to be circular in the market, they are required to compensate for the circularshareholders with their shares, or cash, or other means, to exchange for the circularright of their shares after the reform. When the compensation plan is accepted by thecircular shareholders, which is approved in the formal shareholders’ meeting, thenshares that are not circular before the reform are going to be traded freely in the secondmarket[3]. In practice, almost all the un-circular shareholders compensate for thecircular investors with their stock, cash or other means for the liquidation rights of theun-circular stocks.

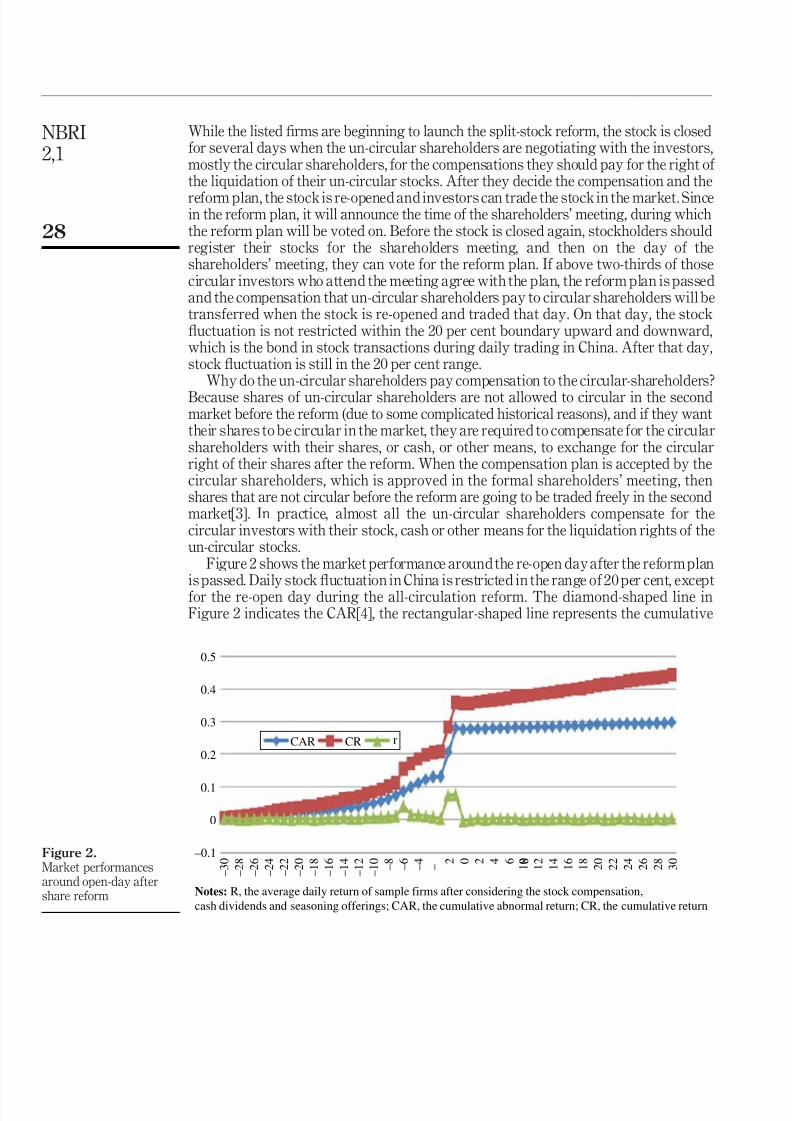

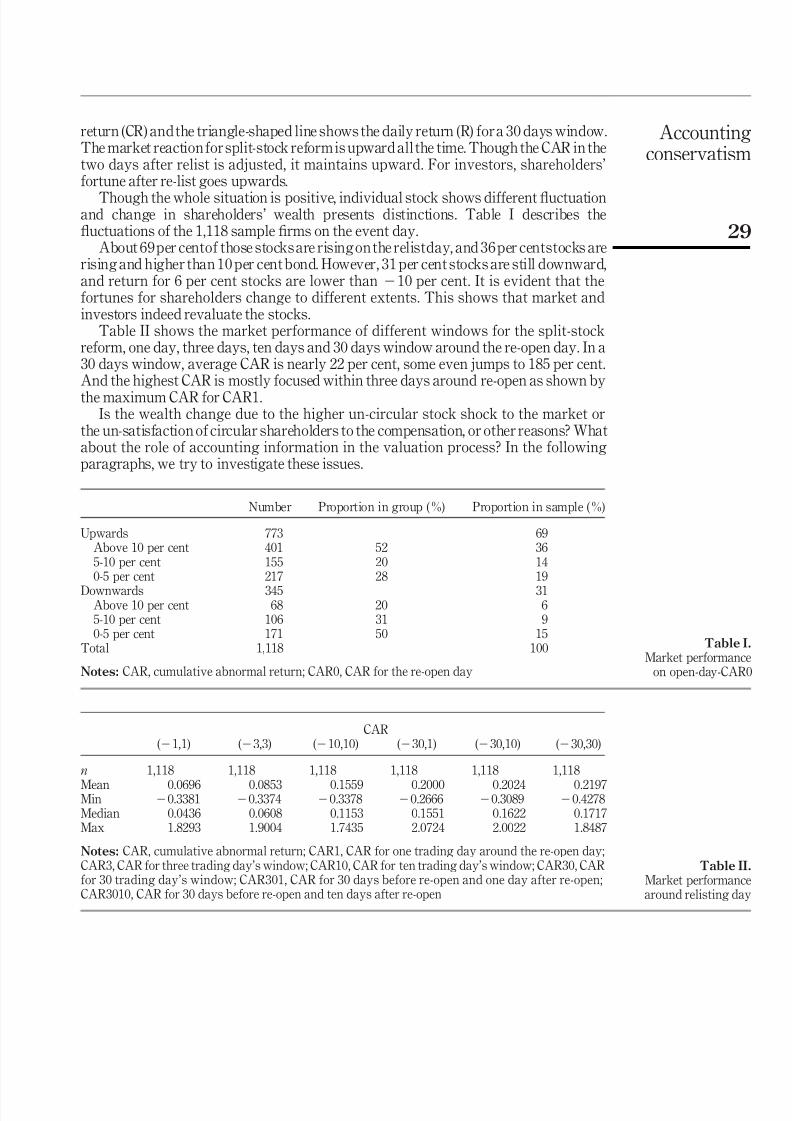

Figure 2 shows the market performance around the re-open day after the reform planis passed. Daily stock fluctuation in China is restricted in the range of 20 per cent, exceptfor the re-open day during the all-circulation reform. The diamond-shaped line inFigure 2 indicates the CAR[4], the rectangular-shaped line represents the cumulative

Figure 2.Market performancesaround open-day aftershare reform

0.5

0.4

0.3

0.2

0.1

0

–0.1

– 3 0

– 2 8

– 2 6

– 2 4

– 2 2

– 2 0

– 1 8

– 1 6

– 1 4

– 1 2

– 1 0

– 8

CAR CR r

– 6

– 4

– 2 0 2 4 6 8

1 0

1 2

1 4

1 6

1 8

2 0

2 2

2 4

2 6

2 8

3 0

Notes: R, the average daily return of sample firms after considering the stock compensation,

cash dividends and seasoning offerings; CAR, the cumulative abnormal return; CR, the cumulative return

NBRI2,1

28

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 7/25

return (CR) and the triangle-shaped line shows the daily return (R) for a 30 days window.The market reaction for split-stock reform is upward all the time. Though the CAR in thetwo days after relist is adjusted, it maintains upward. For investors, shareholders’fortune after re-list goes upwards.

Though the whole situation is positive, individual stock shows different fluctuationand change in shareholders’ wealth presents distinctions. Table I describes thefluctuations of the 1,118 sample firms on the event day.

About 69 per centof those stocks are rising on the relistday, and 36 per centstocks arerising and higher than 10 per cent bond. However, 31 per cent stocks are still downward,and return for 6 per cent stocks are lower than 210 per cent. It is evident that thefortunes for shareholders change to different extents. This shows that market andinvestors indeed revaluate the stocks.

Table II shows the market performance of different windows for the split-stockreform, one day, three days, ten days and 30 days window around the re-open day. In a30 days window, average CAR is nearly 22 per cent, some even jumps to 185 per cent.And the highest CAR is mostly focused within three days around re-open as shown by

the maximum CAR for CAR1.Is the wealth change due to the higher un-circular stock shock to the market or

the un-satisfaction of circular shareholders to the compensation, or other reasons? Whatabout the role of accounting information in the valuation process? In the followingparagraphs, we try to investigate these issues.

Number Proportion in group (%) Proportion in sample (%)

Upwards 773 69Above 10 per cent 401 52 365-10 per cent 155 20 140-5 per cent 217 28 19

Downwards 345 31Above 10 per cent 68 20 65-10 per cent 106 31 90-5 per cent 171 50 15

Total 1,118 100

Notes: CAR, cumulative abnormal return; CAR0, CAR for the re-open day

Table I.Market performance

on open-day-CAR0

CAR( 21,1) ( 23,3) ( 210,10) ( 230,1) ( 230,10) ( 230,30)

n 1,118 1,118 1,118 1,118 1,118 1,118

Mean 0.0696 0.0853 0.1559 0.2000 0.2024 0.2197Min 20.3381 20.3374 20.3378 20.2666 20.3089 20.4278Median 0.0436 0.0608 0.1153 0.1551 0.1622 0.1717Max 1.8293 1.9004 1.7435 2.0724 2.0022 1.8487

Notes: CAR, cumulative abnormal return; CAR1, CAR for one trading day around the re-open day;CAR3, CAR for three trading day’s window; CAR10, CAR for ten trading day’s window; CAR30, CARfor 30 trading day’s window; CAR301, CAR for 30 days before re-open and one day after re-open;CAR3010, CAR for 30 days before re-open and ten days after re-open

Table II.Market performancearound relisting day

Accountingconservatism

29

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 8/25

4. Theory and hypothesisQuality of earnings is the focus of analyzing the relation between accountinginformation, particularly accounting earnings, and market reactions. Quality of accounting earnings is affected by many factors, one of which is the principle of

conservatism. Commentators sometimes claim that the practice of conservatism inaccounting produces higher quality earnings. Conservatism yields lower earnings, theysay, and so prima facie these conservative earnings are of high quality. Feltham andOhlson’s (1995) valuation framework predicts a positive association between thevaluation multiple on operation assets and the accounting conservatism. The relationbetween operating assets and operating accruals provides the basis for Feltham andOhlson’s (1995) further prediction of a positive association between the responsecoefficient to operating accruals and the accounting conservatism. Stober (1996) andAhmed et al. (2000) present evidence that the valuation multiple on operating assets isincreasing in conservatism. Hence, by investigating the relation between conservatismand the differential response to operating accruals, Mason (2004) extends the findings of Stober (1996) and Ahmed et al. (2000) and provides additional evidence on the agreementof the Feltham and Ohlson (1995) framework. When firms are partitioned onconservatism, evidence is generally consistent with Feltham and Ohlson’s (1995)prediction that as conservatism increases so does the magnitude of the responsecoefficient on operating accruals. Balachandran and Mohanram (2008) find no negativeimpact of un-conditional conservatism on value-relevance of earnings. Greaterconservatism results in a stronger market response to the accounting numbers.Specifically, to the extent that conservatism reduces perceived variance of futureexpected cash flows (because conservatism makes estimates of such cash flows morereliable), the market should reward more conservative firms with higher valuationmultiples (Kim and Pevzner. 2010). Following Balachandran and Mohanram (2008),Li (2007) shows that un-conditional conservatism reduces uncertainty in analyst

forecasts. While Kim and Pevzner (2010) find that higher current conditionalconservatism is associated with lower probability of future bad news, proxy by missinganalyst forecasts, earnings decreases and dividend decreases. They also find weakevidence that the stock market reacts stronger (weaker) to good (bad) earnings news of more conditionally conservative firms, providing additional evidence that conditionalconservatism affects stock prices. Therefore, both conditional conservatism andun-conditional conservatism can improve the value relevance and information contentsof financial reporting, and the market will reward more conservative firms with highervaluation multiples. Actually, the market reaction to conservatism is due to the currentthe future higher expected earnings.

GAAP requires firms to recognize revenue only if recognition standards are satisfied,namely, reliably measured and matched with costs, which results in un-recognition of

positive net present value projects and lower earnings. Moreover, accounting standardson measurement and recognition, like the expense of R&D, makes the book value lowerthan the market value (Feltham and Ohlson, 1995). However, it can be expected thatfuture earning price will exceed the expected return, which means conservatismaccounting will lead to higher profitability. Ohlson (2009) suggests that with growthbeing expected, it follows that the firm’s price is at a premium relative to book values andcapitalized forward earnings. In other words, growth and conservative accounting arethe two sides of the same coin. Easton (2009) also suggests that more growth is expected

NBRI2,1

30

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 9/25

in future accounting earnings to complete the “correction” for conservatism. Therefore,the influence of conservative accounting on stock pricing is exhibited on the will“correction” for future accounting performance.

Before 2005, about 60 per cent of the stock of listed firms cannot be traded freely on

the stock market which leads to the indifference of management and controllingshareholders for the stock price since they cannot cash their benefits through the stockexchange and price appreciation. Due to the un-circular of all stocks in the Chinesesecurities market, the market valuation is wholly distorted (Ba, 2005). Therefore, theinitiative for the stock reform is to solve the great agency issue of listed firms andimprove the performance and valuation. Once the stocks are circular in the market,the interests of management and controlling shareholders will be closely related with themarket value of the firm and then they will take more considerations of the consequencesof their decisions and behavior on the stock price. For the eon of all circular, the stockmarket will be more powerful and minority shareholders can give higher pressureson management and controlling shareholders through “voting with feet”. Thus, the

“tunneling” behaviors will be less and agency problems will be reduced, leading toimproved performance and the market value will properly reflect the value of the firm.Regulation authorities, investors and other institutions all give high expectations for thesplit-stock reform and hope the governance of listed firms will be improved with thesame applying to performance and growth. Investors will re-evaluate the stock based onthe past accounting information. While the past profitability is the basis for futurepricing, higher past earnings will predict the future to some extent and past growth alsoreflects this perspective. Firms with conservative reporting in the past will releasemore reserve and achieve higher growth (Ohlson, 2009), namely future earnings willshow higher growth to “correct” the conservatism (Easton, 2009). Therefore, thisexpectation indicates higher growth and better accounting performance, leading tohigher investors’ wealth.

On the other hand, in 2005, the Ministry of Finance Peoples’ Republic of China issued22 Exposure Draft of Proposed Accounting Standards which brings the fair valuemeasurement, including the consolidation, investment real estate, donation and subsidy,assets impairment, annuity, recognition and measurement of financial instruments,financial assets transfer and arbitrage. In February 2006, the Ministry of FinancePeoples’ Republic of China officially issued the new Chinese GAAP and required thelisted firms to follow the new GAAP. Fair value measurement changes the pastvaluation model which is based on historical cost and would correct the underestimate of earnings and firm value. Moreover, firms can recognize future expected benefits in theircurrent financial statements for some conditions. For example, the gain from fair valuecan increase the current earnings and net assets to a great extent. Therefore, firms with

conservative reporting in the past will show higher accounting performance under fairvalue measurement, and the market reaction will be much stronger. Overall, wehypothesise that:

H1. The more conservative of accounting information, the better marketperformance of listed companies around share reform re-open day.

H2. Better accounting earnings will improve the positive relation betweenconservatism and market performance around share reform re-open day.

Accountingconservatism

31

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 10/25

5. Variables and data5.1 VariablesThe dependent variables are CAR around re-open day (after allowing for the dividends,

offerings and compensation for the reform) under naı̈ve model that AR is calculated as

the daily return minus the average return on market portfolio. In order to examinedifferent time windows, we calculate the CAR0 on the re-open day, CAR1 for one tradingday around the re-open day and CAR3, CAR10, CAR30 for three, ten and 30 trading dayswindow around the re-open day. CAR301 means CAR for 30 days before re-open and oneday after re-open; CAR3010 means CAR for 30 days before re-open and ten days afterre-open. CAR301 and CAR3010 are used to analyze the variations before re-open day.In order to minimize the influence of outliers, we winsorize the top and bottom 1 per centof CARs.

Accounting information includes accounting conservatism and the profitabilityproxy. Conservative accounting will lead to negative accruals, the bigger the amount,the more conservative is the accounting information (Givoly and Hayn, 2000), so we use

three years cumulative accruals to proxy for the conservatism, as Ahmend andDuellaman (2007), Qiang (2007) and Xia and Zhu (2009). Accruals are equal to net incomeminus cash flow from operation then divided by total asset. Since many firms useextraordinary items to manipulate their earnings in China, we also use the net income

before extraordinary items to compute the accruals. Thus, CumAcc1 is three yearscumulative accruals using net income; CumAcc2 is three years cumulativeaccruals using net income before extraordinary items to compute the accruals.To explain the results more easily, we multiply the cumulative accruals by 21,Conserv1 ¼ 2CumAcc1 and Conserv2 ¼ 2CumAcc2; therefore, the larger the proxy,namely Conserv1 and Conserv2, the more conservative is the accounting information(Givoly and Hayn, 2000; Ahmend and Duellaman, 2007; Xia and Zhu, 2009). In order tominimize the influence of outliers, we winsorize the top and bottom 1 per cent of theconservatism measures[5]. We use the conservatism measure at the prior year sinceinvestors’ decision is based on the past information.

Profitability is proxy by the average return on equity (ROE) for the past three years,where the ROE equals to net income divided by the equity at the end of period. We alsouse the volatility of the past earnings as a robust test, which is equal to the standarddeviation of ROE (SDROE) for the past three years. Since the growth and conservativeaccounting are the two sides of the same coin (Ohlson, 2009), we also control for thegrowth effect when considering the influence of conservatism on future performancerevision by using the average revenue growth rate of the past three years (Grow).

Ownership reform is a key step for the healthy development of the China securitiesmarket. It is designed to solve the severe agency problem between large shareholders,

the controlling shareholders and the minority shareholders or the circular shareholders.Agency problems must have to be solved more effectively and firms are operating moreefficiently after the reform. Special treatment (ST) companies are problematic due to theprior worse performance and corporate governance with greater agency problems; thus,the market will consider that those companies will be improved to a greater extent andtheir values will go up. Then, the market will give more approbates for reforms by thosecompanies; thus, we use a dummy variable (ST) to control. ST is a dummy variable,1 indicates the firm is “ST” for the prior year before reform, and 0 otherwise.

NBRI2,1

32

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 11/25

Before the all-circulation reform, only about one-third of the stocks of Chinese listedcompanies are circular, leading to the overvaluation of stock price. If all the stocks arecirculated, this will give a big shock to the market and return for stocks will dropsignificantly. From the supply and demand perspective, bigger supply will

significantly shock the equilibrium under the demand does not change significantly.We use the ratio of un-circular stock to proxy for this shock, and the ratio is theun-circular stock to total stock in the prior year before reform (Unliquid).

In the reform plan, some firms even propose management stock incentives plans.Since managers of listed firms are low paid in China and compensations are not linkedto stock price, more expropriation conducts are found before the reform andmanagement do not care for the stock price. To alleviate this problem and give moreincentive for management, some firms propose the stock incentive plans and it is sureto receive more attention and welcomed by the circular shareholders. Thus, we alsocontrol for the influence of stock incentive plan, using a dummy variable (incentive),1 means the reform plan includes a management incentive plan, and 0 otherwise.

The compensation from un-circular shareholders to the circular shareholders for theliquidate right of their stock may significantly influence the market performance and thereturn. The higher the compensation rate, the more stock compensation circularshareholders will receive. The higher proportion of circular stock which brings biggershock to the market, the lower wealth circular shareholders will benefits and the returnfor all stocks. To control for the compensation effects, we use the compensation byun-circular shareholders to circular shareholders computed as the stock compensation,which is from Wind Database (Compen). Circular shareholders should vote for theproposal or the reform plan; if they accept the plan, then they will get the compensationsupplied by un-circular shareholders. The participation ratio and the approval ratioshow their attention and satisfactions for the plan. If they do not care for the shareholdermeeting and are not satisfied with the plan, the market will reflect their emotion. We use

the participation ratio (Ltcy) and the approval ratio (Ltzc) to proxy for their emotions.All-circulation reform receives positive appraisals from many fields and investors

give high expectations to the compensation rate from the un-circular shareholders.But in the atmosphere of speculation, institutional investors and other investors maytake this chance for arbitrage and speculation. From the proposal of the reform plan tothe completion, the longer the time span, the more opportunity for speculation andmanipulation. Further, the longer time span, the more problems listed companies mayencounter during the reform or have done in their prior operation. Therefore, the timespan may influence the market performance. We use the time span (Time) from theapproval day, when CRSC approve the reform plan proposed by listed companies, to there-list day.

Some listed companies issue other types of stocks, like B-share, H-share or S-share.

But in the process of all-circulation reform, foreign investors do notparticipate. They canspeculate if there exist arbitrage chances. Further, those companies use the internationalaccounting standard or US GAAP, the accounting information may be somewhatdifferent from those only issues A-share. Hence, we add a dummy variable to control,OtherSec, 1 indicates firms that also issue other type of shares, and 0 otherwise. We alsocontrol for the size effect and leverage effect in the return regressions: the nature log formof asset at the end of prior year before reform (Size) to proxy the size and total debtratio (Lev) to proxy the leverage. Further, some industries are heavily speculated

Accountingconservatism

33

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 12/25

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 13/25

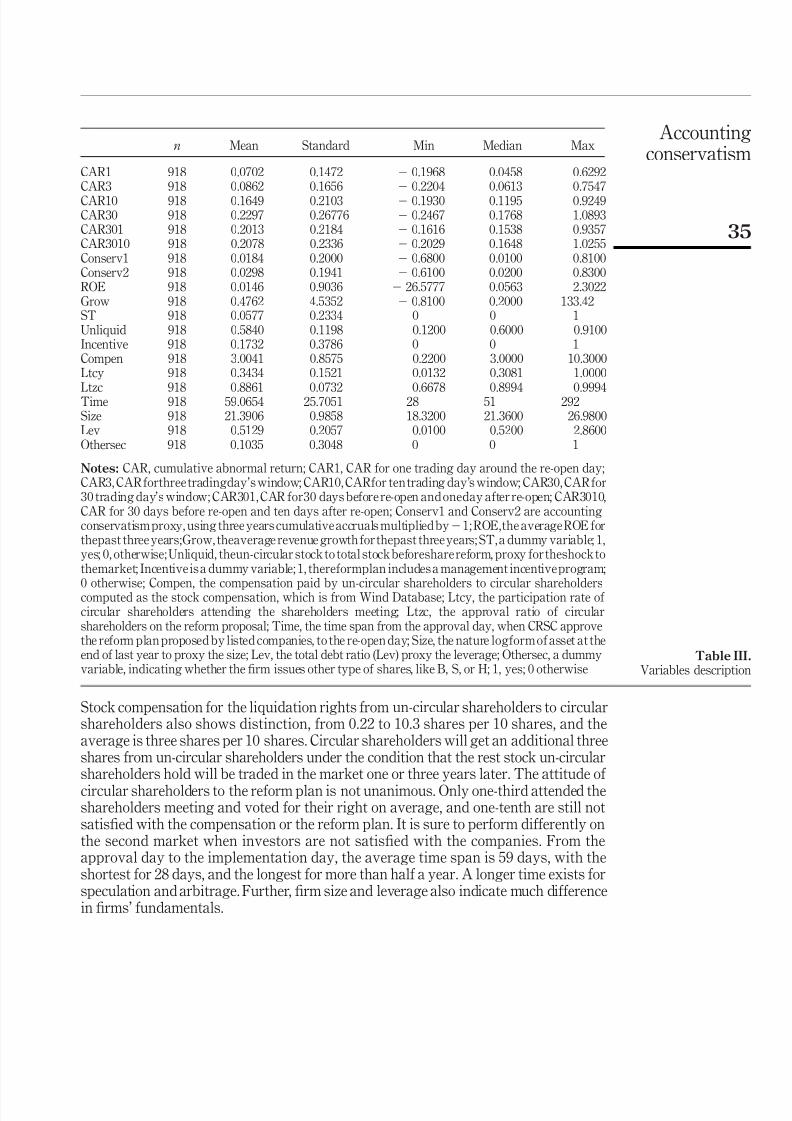

Stock compensation for the liquidation rights from un-circular shareholders to circularshareholders also shows distinction, from 0.22 to 10.3 shares per 10 shares, and theaverage is three shares per 10 shares. Circular shareholders will get an additional threeshares from un-circular shareholders under the condition that the rest stock un-circularshareholders hold will be traded in the market one or three years later. The attitude of

circular shareholders to the reform plan is not unanimous. Only one-third attended theshareholders meeting and voted for their right on average, and one-tenth are still notsatisfied with the compensation or the reform plan. It is sure to perform differently onthe second market when investors are not satisfied with the companies. From theapproval day to the implementation day, the average time span is 59 days, with theshortest for 28 days, and the longest for more than half a year. A longer time exists forspeculation and arbitrage. Further, firm size and leverage also indicate much differencein firms’ fundamentals.

n Mean Standard Min Median Max

CAR1 918 0.0702 0.1472 2 0.1968 0.0458 0.6292CAR3 918 0.0862 0.1656 2 0.2204 0.0613 0.7547

CAR10 918 0.1649 0.21032

0.1930 0.1195 0.9249CAR30 918 0.2297 0.26776 2 0.2467 0.1768 1.0893CAR301 918 0.2013 0.2184 2 0.1616 0.1538 0.9357CAR3010 918 0.2078 0.2336 2 0.2029 0.1648 1.0255Conserv1 918 0.0184 0.2000 2 0.6800 0.0100 0.8100Conserv2 918 0.0298 0.1941 2 0.6100 0.0200 0.8300ROE 918 0.0146 0.9036 2 26.5777 0.0563 2.3022Grow 918 0.4762 4.5352 2 0.8100 0.2000 133.42ST 918 0.0577 0.2334 0 0 1Unliquid 918 0.5840 0.1198 0.1200 0.6000 0.9100Incentive 918 0.1732 0.3786 0 0 1Compen 918 3.0041 0.8575 0.2200 3.0000 10.3000Ltcy 918 0.3434 0.1521 0.0132 0.3081 1.0000

Ltzc 918 0.8861 0.0732 0.6678 0.8994 0.9994Time 918 59.0654 25.7051 28 51 292Size 918 21.3906 0.9858 18.3200 21.3600 26.9800Lev 918 0.5129 0.2057 0.0100 0.5200 2.8600Othersec 918 0.1035 0.3048 0 0 1

Notes: CAR, cumulative abnormal return; CAR1, CAR for one trading day around the re-open day;CAR3, CAR forthree tradingday’s window; CAR10, CARfor ten trading day’s window; CAR30, CAR for30 trading day’s window; CAR301, CAR for30 days before re-open and oneday after re-open; CAR3010,CAR for 30 days before re-open and ten days after re-open; Conserv1 and Conserv2 are accountingconservatism proxy, using three years cumulative accruals multiplied by21; ROE,the average ROE forthepast three years;Grow, theaverage revenue growth for thepast three years; ST, a dummy variable; 1,yes; 0, otherwise; Unliquid, theun-circular stock to total stock beforeshare reform, proxy for theshock tothemarket; Incentive is a dummy variable; 1, thereformplan includes a management incentive program;

0 otherwise; Compen, the compensation paid by un-circular shareholders to circular shareholderscomputed as the stock compensation, which is from Wind Database; Ltcy, the participation rate of circular shareholders attending the shareholders meeting; Ltzc, the approval ratio of circularshareholders on the reform proposal; Time, the time span from the approval day, when CRSC approvethe reform plan proposed by listed companies, to the re-open day; Size, the nature logform of asset at theend of last year to proxy the size; Lev, the total debt ratio (Lev) proxy the leverage; Othersec, a dummyvariable, indicating whether the firm issues other type of shares, like B, S, or H; 1, yes; 0 otherwise

Table III.Variables description

Accountingconservatism

35

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 14/25

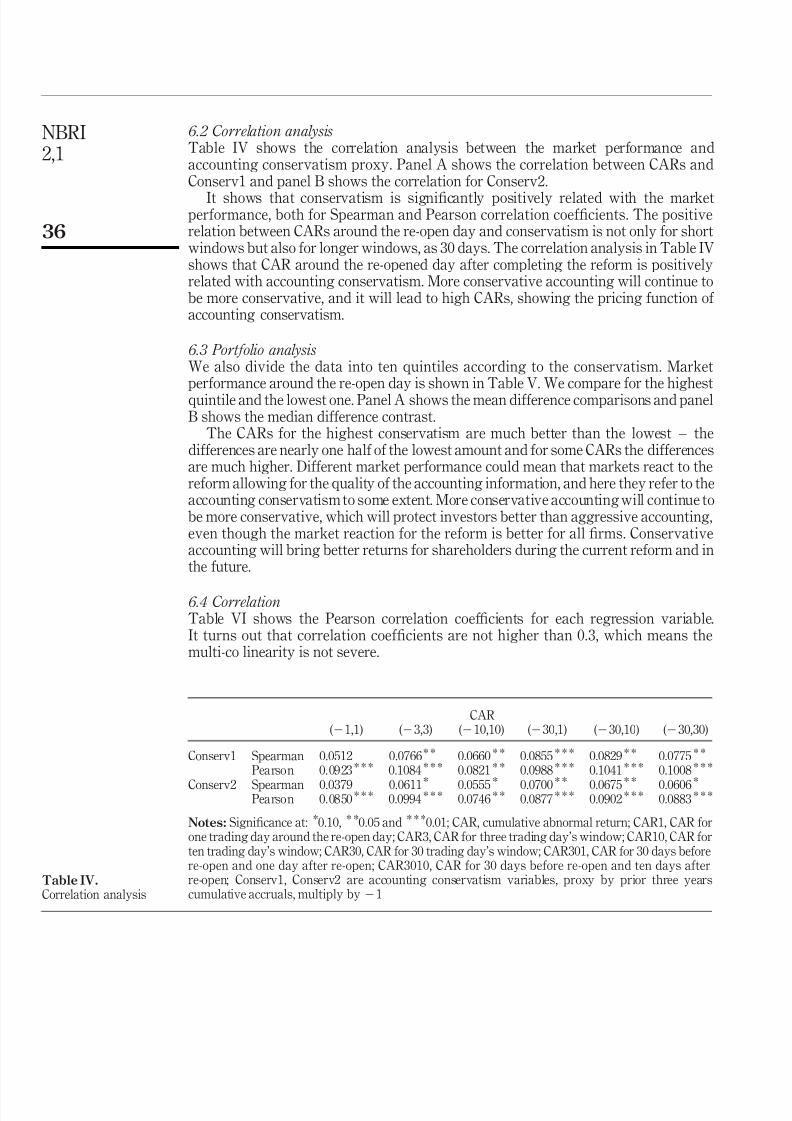

6.2 Correlation analysisTable IV shows the correlation analysis between the market performance andaccounting conservatism proxy. Panel A shows the correlation between CARs andConserv1 and panel B shows the correlation for Conserv2.

It shows that conservatism is significantly positively related with the marketperformance, both for Spearman and Pearson correlation coefficients. The positiverelation between CARs around the re-open day and conservatism is not only for shortwindows but also for longer windows, as 30 days. The correlation analysis in Table IVshows that CAR around the re-opened day after completing the reform is positivelyrelated with accounting conservatism. More conservative accounting will continue tobe more conservative, and it will lead to high CARs, showing the pricing function of accounting conservatism.

6.3 Portfolio analysisWe also divide the data into ten quintiles according to the conservatism. Marketperformance around the re-open day is shown in Table V. We compare for the highestquintile and the lowest one. Panel A shows the mean difference comparisons and panelB shows the median difference contrast.

The CARs for the highest conservatism are much better than the lowest – thedifferences are nearly one half of the lowest amount and for some CARs the differencesare much higher. Different market performance could mean that markets react to thereform allowing for the quality of the accounting information, and here they refer to theaccounting conservatism to some extent. More conservative accounting will continue tobe more conservative, which will protect investors better than aggressive accounting,even though the market reaction for the reform is better for all firms. Conservativeaccounting will bring better returns for shareholders during the current reform and inthe future.

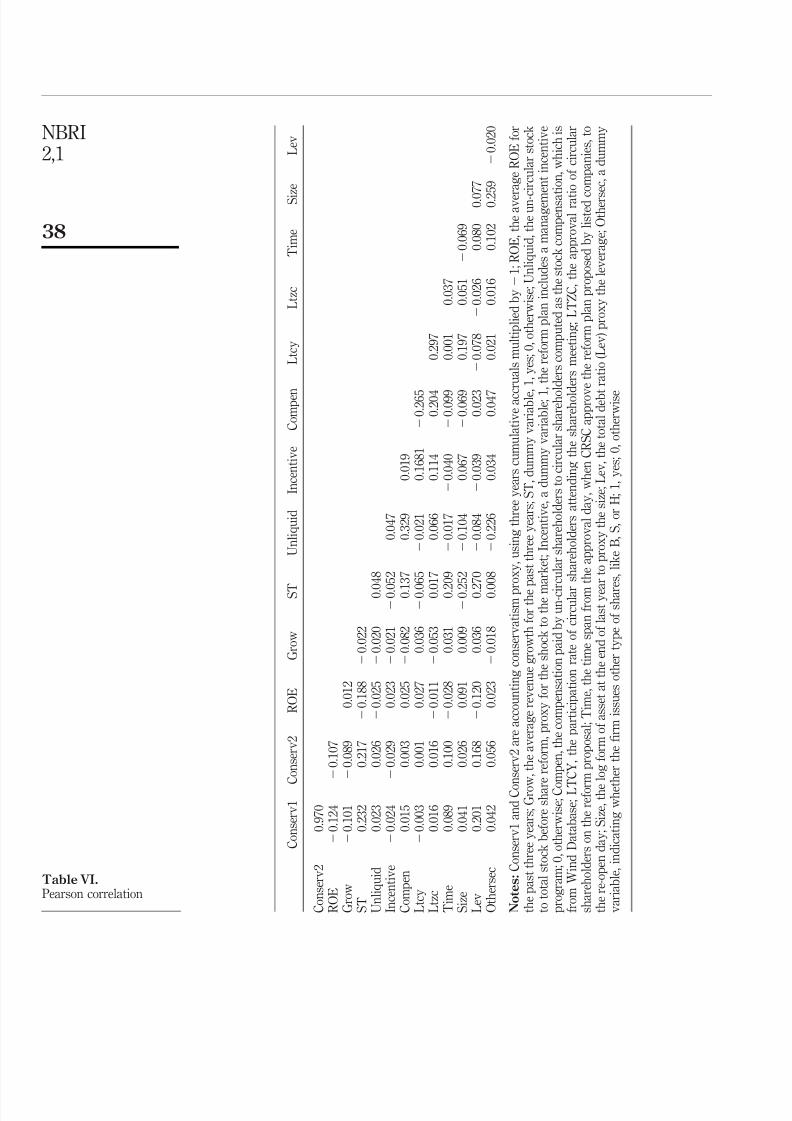

6.4 CorrelationTable VI shows the Pearson correlation coefficients for each regression variable.It turns out that correlation coefficients are not higher than 0.3, which means themulti-co linearity is not severe.

CAR( 21,1) ( 23,3) ( 210,10) ( 230,1) ( 230,10) ( 230,30)

Conserv1 Spearman 0.0512 0.0766 * * 0.0660 * * 0.0855 * * * 0.0829 * * 0.0775 * *

Pearson 0.0923 * * * 0.1084 * * * 0.0821 * * 0.0988 * * * 0.1041 * * * 0.1008 * * *

Conserv2 Spearman 0.0379 0.0611 * 0.0555 * 0.0700 * * 0.0675 * * 0.0606 *Pearson 0.0850 * * * 0.0994 * * * 0.0746 * * 0.0877 * * * 0.0902 * * * 0.0883 * * *

Notes: Significance at: *0.10, * *0.05 and * * *0.01; CAR, cumulative abnormal return; CAR1, CAR forone trading day around the re-open day; CAR3, CAR for three trading day’s window; CAR10, CAR forten trading day’s window; CAR30, CAR for 30 trading day’s window; CAR301, CAR for 30 days beforere-open and one day after re-open; CAR3010, CAR for 30 days before re-open and ten days afterre-open; Conserv1, Conserv2 are accounting conservatism variables, proxy by prior three yearscumulative accruals, multiply by 21

Table IV.Correlation analysis

NBRI2,1

36

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 15/25

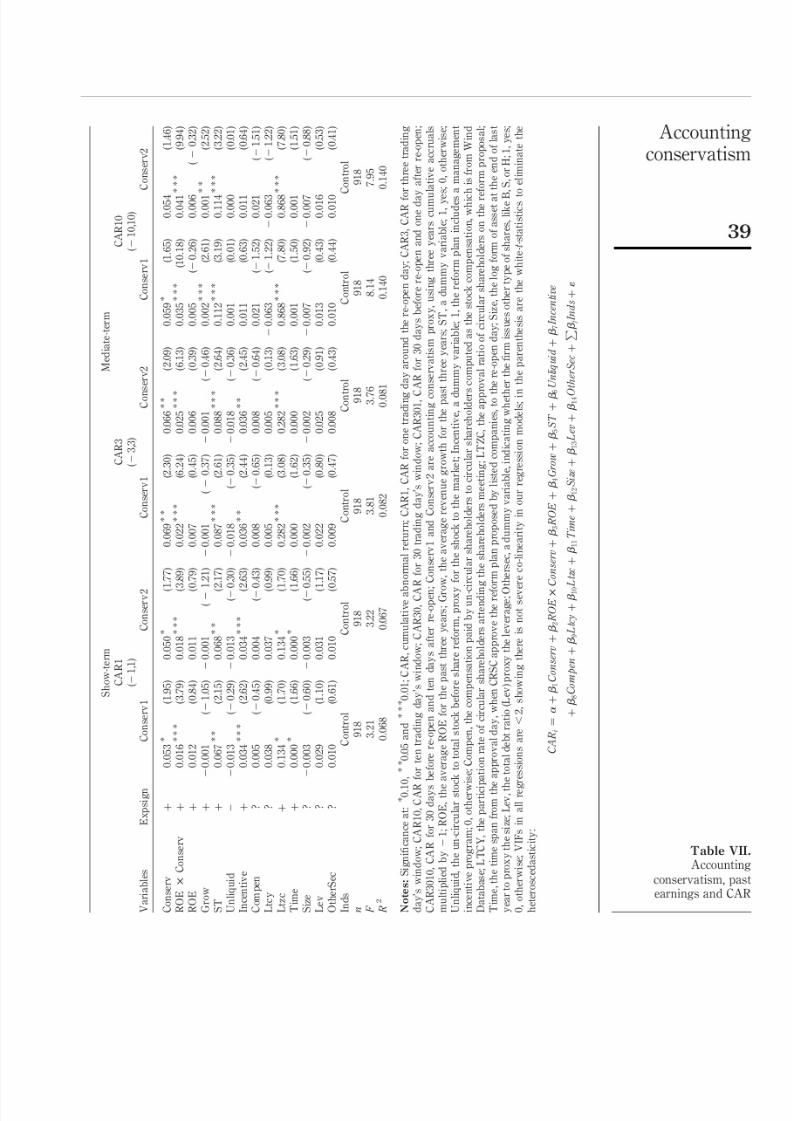

6.5 Regress analysisTable VII investigates the relation between the market performance and the accountingconservatism around the re-open day in split-stock reform for short and mediatewindows. The first two columns show the regressions for a short window, one dayaround the re-open day, using two conservatism proxies. The middle two columns arefor three days window, and the last two columns are for ten days window.

For all these windows, Conserv1, the first proxy for accounting conservatism, issignificantly positively related with CARs in all regressions. Conserv2 and CARs are also

positively related, significant in 0.10 levels, though not significantly in ten days window.Thus, generally speaking, the positive relation between accounting conservatism andCAR around the reform day indicates the role of conservatism in stock pricing, whichmeans that investors will predict the future of firms based on the past conservatism of financial reports, more conservative reporting will release more reserve in the future andachieve higher growth (Ohlson, 2009) and thus future earnings will show higher growthto “correct” the conservatism (Easton, 2009). Moreover, accounting performance for firmswith conservative reporting will be further improved under the fair value measure; thus,the market willbe more positive to the earningsincrease. H1 is supported. Coefficients forcross-term of profitability and conservatism, ROE £ Conserv, are all positive andsignificant at 0.01 levels, which means better past performance will improve the positiverelation between market reaction and conservative reporting. H2 is supported.

Coefficients for ROE are not significant, and it may be because the market tends tocare more about the future profitability reserve and growth potential. Coefficient forGrow is significant in regression for CAR10 but not significant for other windows.The ST group is significantly distinguished from the non-ST group – the former gainsmore during the reform. ST firms may have server agency problems, and after thereform, all-circulation phenomenon will bring more pressure from the market to themanagement, alleviating the agency cost and bringing in more benefits for largeshareholders and circular shareholders. The rate of un-circular stock does not have

CAR( 21,1) ( 23,3) ( 210,10) ( 230,1) ( 230,10) ( 230,30)

Panel A – mean test

Portfolio – highest 0.1046 0.1361 0.2259 0.2743 0.2890 0.3074Portfolio – lowest 0.0733 0.0798 0.1705 0.1786 0.1936 0.2085Difference 0.0313 0.0564 0.0554 0.0956 0.0954 0.0989t 1.3351 * 2.1499 * * 1.6643 * * 2.8457 * * * 2.5342 * * * 2.3439 * *

Panel B – median test Portfolio – highest 0.0718 0.0963 0.1849 0.2349 0.2377 0.2554Portfolio – lowest 0.0602 0.0491 0.1255 0.1324 0.1252 0.1512Difference 0.0116 0.0472 0.0595 0.1025 0.1125 0.1042Mann-Whitney Z 0.491 1.888 * 1.774 * 3.039 * * * 2.720 * * * 2.444 * * *

Notes: Significance at: *0.10, * *0.05 and * * *0.01; CAR, cumulative abnormal return; CAR1, CAR forone trading day around the re-open day; CAR3, CAR for three trading day’s window; CAR10, CAR forten trading day’s window; CAR30, CAR for 30 trading day’s window; CAR301, CAR for 30 days beforere-open and one day after re-open; CAR3010, CAR for 30 days before re-open and ten days after

re-open; we divide the data into ten quintiles according to the conservatism; highest, highestconservatism; lowest, the lowest group in conservatism

Table V.Portfolio strategy

Accountingconservatism

37

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 16/25

C o n s e r v 1

C o n s e r v 2

R O E

G r o w

S T

U n l i q u i d

I n c e n t i v e

C o m p e n

L t c y

L t z c

T i m e

S i z e

L e v

C o n s e r v 2

0 . 9 7 0

R O E

2 0 . 1 2 4

2 0 . 1 0 7

G r o w

2 0 . 1 0 1

2 0 . 0 8 9

0 . 0 1 2

S T

0 . 2 3 2

0 . 2 1 7

2 0 . 1 8 8

2 0 . 0 2 2

U n l i q u i d

0 . 0 2 3

0 . 0 2 6

2 0 . 0 2 5

2 0 . 0 2 0

0 . 0

4 8

I n c e n t i v e

2 0 . 0 2 4

2

0 . 0 2 9

0 . 0 2 3

2 0 . 0 2 1

2 0 . 0

5 2

0 . 0 4 7

C o m p e n

0 . 0 1 5

0 . 0 0 3

0 . 0 2 5

2 0 . 0 8 2

0 . 1

3 7

0 . 3 2 9

0 . 0 1 9

L t c y

2 0 . 0 0 3

0 . 0 0 1

0 . 0 2 7

0 . 0 3 6

2 0 . 0

6 5

2

0 . 0 2 1

0 . 1 6 8 1

2 0 . 2 6 5

L t z c

0 . 0 1 6

0 . 0 1 6

2 0 . 0 1 1

2 0 . 0 5 3

0 . 0

1 7

0 . 0 6 6

0 . 1 1 4

0 . 2 0 4

0 . 2 9 7

T i m e

0 . 0 8 9

0 . 1 0 0

2 0 . 0 2 8

0 . 0 3 1

0 . 2

0 9

2

0 . 0 1 7

2 0 . 0 4 0

2 0 . 0 9 9

0 . 0 0 1

0 . 0 3 7

S i z e

0 . 0 4 1

0 . 0 2 6

0 . 0 9 1

0 . 0 0 9

2 0 . 2

5 2

2

0 . 1 0 4

0 . 0 6 7

2 0 . 0 6 9

0 . 1 9 7

0 . 0 5 1

2 0 . 0 6 9

L e v

0 . 2 0 1

0 . 1 6 8

2 0 . 1 2 0

0 . 0 3 6

0 . 2

7 0

2

0 . 0 8 4

2 0 . 0 3 9

0 . 0 2 3

2 0 . 0 7 8

2 0 . 0 2 6

0 . 0 8 0

0 . 0 7 7

O t h e r s e c

0 . 0 4 2

0 . 0 5 6

0 . 0 2 3

2 0 . 0 1 8

0 . 0

0 8

2

0 . 2 2 6

0 . 0 3 4

0 . 0 4 7

0 . 0 2 1

0 . 0 1 6

0 . 1 0 2

0 . 2 5 9

2 0 . 0 2 0

N o t e s : C o n s e r v 1 a n d C o n s e r v 2 a r e a c c o u n t i n g c o n s e r v a t i s m p r o x y , u s i n g t h r e e y e a r s c u m u l a t i v e a c c

r u a l s m u l t i p l i e d b y 2 1 ; R O E , t h e a v e r a g e R O E f o r

t h e p a s t t h r e e y e a r s ; G r o w

, t h e a v e r a g e r e v e n u e g r o w t h f o r t h e p a s t t h r e e y e a r s ; S T , d u m m y v a r i a b l e , 1 , y e s ; 0 , o t h e r w i s e ; U n l i q u i d , t h e u n - c

i r c u l a r s t o c k

t o t o t a l s t o c k b e f o r e s h a r e r e f o r m , p r o x y f o r t h e s h o c k t o t h e m

a r k e t ; I n c e n t i v e , a d u m m y v a r i a b l e ; 1 , t h e r e f o r m p l a n i n c l u d e s a m a n a g e m

e n t i n c e n t i v e

p r o g r a m ; 0 , o t h e r w i s e ; C o

m p e n , t h e c o m p e n s a t i o n p a i d b y u n - c i r c u l a r s h a r e h o l d e r s t o c i r c u l a r s h a r e h o l d e r s c o m p u t e d a s t h e s t o c k c o m p e n s a t i o n , w h i c h i s

f r o m W i n d D a t a b a s e ; L T

C Y , t h e p a r t i c i p a t i o n r a t e o f c i r c u l a r

s h a r e h o l d e r s a t t e n d i n g t h e s h a r e h o l d

e r s m e e t i n g ; L T Z C , t h e a p p r o v a l r a t i o o f c i r c u l a r

s h a r e h o l d e r s o n t h e r e f o r m p r o p o s a l ; T i m e , t h e t i m e s p a n f r o m

t h e a p p r o v a l d a y , w h e n C R S C a p p r o v

e t h e r e f o r m p l a n p r o p o s e d b y l i s t e d c

o m p a n i e s , t o

t h e r e - o p e n d a y ; S i z e , t h e

l o g f o r m o f a s s e t a t t h e e n d o f l a s t y e a

r t o p r o x y t h e s i z e ; L e v , t h e t o t a l d e b t

r a t i o ( L e v ) p r o x y t h e l e v e r a g e ; O t h e r s

e c , a d u m m y

v a r i a b l e , i n d i c a t i n g w h e t h e r t h e fi r m i s s u e s o t h e r t y p e o f s h a r e s , l i k e B , S , o r H ; 1 , y e s ; 0 , o t h e r w i s e

Table VI.Pearson correlation

NBRI2,1

38

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 17/25

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 18/25

a significant negative influence to the market as a huge shock from the supplyperspective. This does not mean that the shock to market does exist; we suggest that atthe very beginning, investors have not realized the huge shock to the market, and their

attentions are focusedon the reformitself.Whether the reformplan includes an incentive

for management shows their perspective of the future. Incentive programs will giveinvestors more confidence in the future, since management will be stimulated and theirinterest will be connected with circular investors; therefore, those firms will performbetter. The stock compensation supplied by un-circular shareholders to circularshareholders is not significantly related to market performance. Maybe this effect is alsoreflected in their satisfaction with the reform proposal.

Participation of circular shareholders in the shareholders meetings does not havemuch influence on the CAR, while their satisfactions indeed affect the performance andthe market will reflect their emotion. The more they are satisfied, the better the marketwill reflect it, evident in the significantly positive relation between Ltzc and CARs. Thelonger the time span for the reform, the more opportunity to manipulate and speculate,

thus significantly influence the market performance after relist. Results show asignificantly positive relation between the time span and CAR1, but under mediatewindow, this relation does not hold anymore.

The size effect and leverage effect do not have significant influence on CARs during

the reform. And firms issuing other types of shares, like B, S or H, also do not exhibitdistinctions in market performance during the reform.

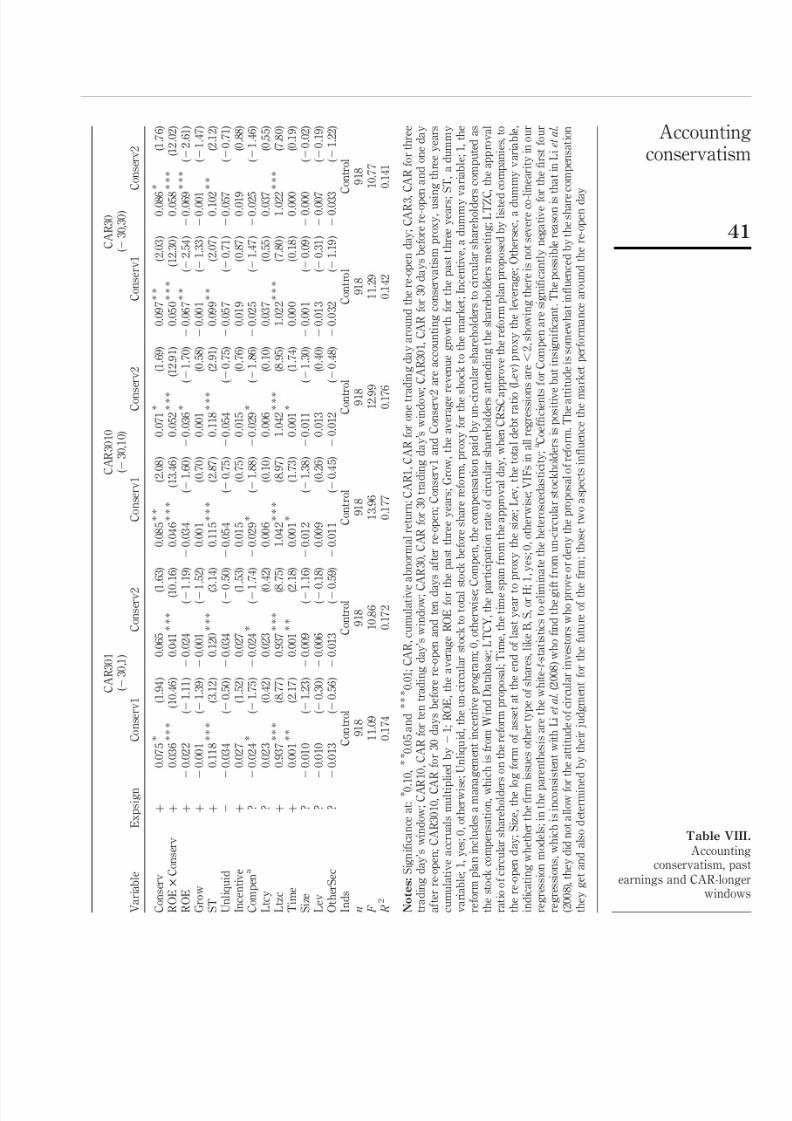

How about the relation in a longer window? Does accounting conservatism still havea role in stock pricing for long window around the re-open day? Table VIII shows theresult for a longer window, 30 days around the reform completion day. The first twocolumns show the CAR for 30 days before re-open and 1 day after re-open. The middletwo columns give the results for 30 days before re-open and 1 day after re-open. The lasttwo columns investigate a longer window, 30 days around the re-open day.

CAR301, CAR3010 and CAR30 are all significantly positively related withconservatism measure (Conserv), consistent with results for short-term windows inTable VI. H1 is further supported. Coefficients for ROE £ Conserv are also positiveand significant in 0.01 levels, meaning higher past profitability will improve thepositive relation between conservatism and market valuation, supporting H2 .

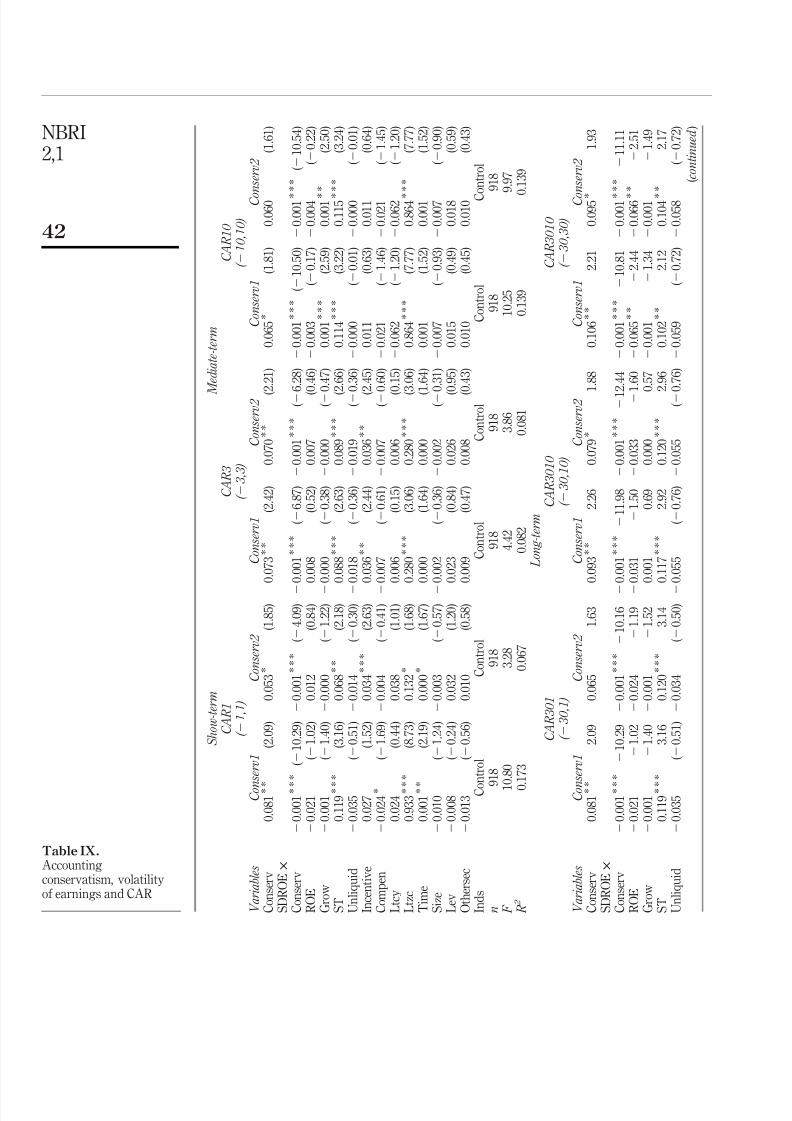

Table IX shows the regression results for the volatility of past earnings instead of earnings level, and for different windows and two conservatism measures. Coefficientsfor Conserv are still significantly positive, except for Conserv2 in CAR10 and CAR301,showing that past conservatism will be “corrected” during the reform and marketreaction is much stronger, supporting H1.

Coefficients for the cross-term of earnings’ volatility and conservatism,

SDROE £ Conserv, all significantly negative, meaning that the more volatile of the pastearnings will predict lower persistence in their profitability and will lower the positiverelation between conservatism and market action. On the other hand, it means morepersistence of accounting earnings will improve the positive relation, still supporting H2 .

Moreover, we also add more controlling variables, such as the characteristics of ultimate shareholders (the control right, the divergence of cash flow right and controlright, the nature of ultimate shareholders), the characteristics of the board and themanagement ownership. The results are basically the same[6].

NBRI2,1

40

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 19/25

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 20/25

S h o w - t e r m

M

e d i a t e - t e r m

C A R 1

C A R 3

C A R 1 0

( 2 1 , 1 )

( 2 3 , 3 )

( 2 1 0 , 1 0 )

V a r i a b l e s

C o n s e r v 1

C o n s e r v 2

C o n s e r v 1

C o n s e r v 2

C o n s e r v 1

C o n s e r v 2

C o n s e r v

0 . 0 8 1 * *

( 2 . 0 9 )

0 . 0 5 3 *

( 1 . 8 5 )

0 . 0 7 3 * *

( 2 . 4 2 )

0 . 0 7 0 * *

( 2 . 2 1 )

0 . 0 6 5 *

( 1 . 8 1 )

0 . 0 6 0

( 1 . 6 1 )

S D R O E £

C o n s e r v

2 0 . 0 0 1 * *

*

( 2 1 0 . 2 9 ) 2 0 . 0 0 1 * * *

( 2 4 . 0 9 ) 2

0 . 0 0 1 * * *

( 2 6 . 8 7 ) 2 0 . 0 0 1 * * *

( 2 6 . 2 8 ) 2 0 . 0 0 1 * * *

( 2 1 0 . 5 0 ) 2 0 . 0 0 1 * * *

( 2 1 0 . 5 4 )

R O E

2 0 . 0 2 1

( 2 1 . 0 2 )

0 . 0 1 2

( 0 . 8 4 )

0 . 0 0 8

( 0 . 5 2 )

0 . 0 0 7

( 0 . 4 6 ) 2 0 . 0 0 3

( 2 0 . 1 7 ) 2 0 . 0 0 4

( 2 0 . 2 2 )

G r o w

2 0 . 0 0 1

( 2 1 . 4 0 ) 2 0 . 0 0 0

( 2 1 . 2 2 ) 2

0 . 0 0 0

( 2 0 . 3 8 ) 2 0 . 0 0 0

( 2 0 . 4 7 )

0 . 0 0 1 * * *

( 2 . 5 9 )

0 . 0 0 1 * *

( 2 . 5 0 )

S T

0 . 1 1 9 * *

*

( 3 . 1 6 )

0 . 0 6 8 * *

( 2 . 1 8 )

0 . 0 8 8 * * *

( 2 . 6 3 )

0 . 0 8 9 * * *

( 2 . 6 6 )

0 . 1 1 4 * * *

( 3 . 2 2 )

0 . 1 1 5 * * *

( 3 . 2 4 )

U n l i q u i d

2 0 . 0 3 5

( 2 0 . 5 1 ) 2 0 . 0 1 4

( 2 0 . 3 0 ) 2

0 . 0 1 8

( 2 0 . 3 6 ) 2 0 . 0 1 9

( 2 0 . 3 6 ) 2 0 . 0 0 0

( 2 0 . 0 1 ) 2 0 . 0 0 0

( 2 0 . 0 1 )

I n c e n t i v e

0 . 0 2 7

( 1 . 5 2 )

0 . 0 3 4 * * *

( 2 . 6 3 )

0 . 0 3 6 * *

( 2 . 4 4 )

0 . 0 3 6 * *

( 2 . 4 5 )

0 . 0 1 1

( 0 . 6 3 )

0 . 0 1 1

( 0 . 6 4 )

C o m p e n

2 0 . 0 2 4 *

( 2 1 . 6 9 ) 2 0 . 0 0 4

( 2 0 . 4 1 ) 2

0 . 0 0 7

( 2 0 . 6 1 ) 2 0 . 0 0 7

( 2 0 . 6 0 ) 2 0 . 0 2 1

( 2 1 . 4 6 ) 2 0 . 0 2 1

( 2 1 . 4 5 )

L t c y

0 . 0 2 4

( 0 . 4 4 )

0 . 0 3 8

( 1 . 0 1 )

0 . 0 0 6

( 0 . 1 5 )

0 . 0 0 6

( 0 . 1 5 ) 2 0 . 0 6 2

( 2 1 . 2 0 ) 2 0 . 0 6 2

( 2 1 . 2 0 )

L t z c

0 . 9 3 3 * *

*

( 8 . 7 3 )

0 . 1 3 2 *

( 1 . 6 8 )

0 . 2 8 0 * * *

( 3 . 0 6 )

0 . 2 8 0 * * *

( 3 . 0 6 )

0 . 8 6 4 * * *

( 7 . 7 7 )

0 . 8 6 4 * * *

( 7 . 7 7 )

T i m e

0 . 0 0 1 * *

( 2 . 1 9 )

0 . 0 0 0 *

( 1 . 6 7 )

0 . 0 0 0

( 1 . 6 4 )

0 . 0 0 0

( 1 . 6 4 )

0 . 0 0 1

( 1 . 5 2 )

0 . 0 0 1

( 1 . 5 2 )

S i z e

2 0 . 0 1 0

( 2 1 . 2 4 ) 2 0 . 0 0 3

( 2 0 . 5 7 ) 2

0 . 0 0 2

( 2 0 . 3 6 ) 2 0 . 0 0 2

( 2 0 . 3 1 ) 2 0 . 0 0 7

( 2 0 . 9 3 ) 2 0 . 0 0 7

( 2 0 . 9 0 )

L e v

2 0 . 0 0 8

( 2 0 . 2 4 )

0 . 0 3 2

( 1 . 2 0 )

0 . 0 2 3

( 0 . 8 4 )

0 . 0 2 6

( 0 . 9 5 )

0 . 0 1 5

( 0 . 4 9 )

0 . 0 1 8

( 0 . 5 9 )

O t h e r s e c

2 0 . 0 1 3

( 2 0 . 5 6 )

0 . 0 1 0

( 0 . 5 8 )

0 . 0 0 9

( 0 . 4 7 )

0 . 0 0 8

( 0 . 4 3 )

0 . 0 1 0

( 0 . 4 5 )

0 . 0 1 0

( 0 . 4 3 )

I n d s

C o n t r o l

C o n t r o l

C o n t r o l

C o n t r o l

C o n t r o l

C o n t r o l

n

9

1 8

9 1 8

9 1 8

9 1 8

9 1 8

9 1 8

F

1 0 . 8 0

3 . 2 8

4 . 4 2

3 . 8 6

1 0 . 2 5

9 . 9 7

R 2

0 . 1 7 3

0 . 0 6 7

0 . 0 8 2

0 . 0 8 1

0 . 1 3 9

0 . 1 3 9

L o n g - t e r m

C A R 3 0 1

C A R 3 0 1 0

C A R 3 0 1 0

( 2 3 0 , 1 )

( 2 3 0 , 1 0 )

( 2 3 0 , 3 0 )

V a r i a b l e s

C o n s e r v 1

C o n s e r v 2

C o n s e r v 1

C o n s e r v 2

C o n s e r v 1

C o n s e r v 2

C o n s e r v

0 . 0 8 1 * *

2 . 0 9

0 . 0 6 5

1 . 6 3

0 . 0 9 3 * *

2 . 2 6

0 . 0 7 9 *

1 . 8 8

0 . 1 0 6 * *

2 . 2 1

0 . 0 9 5 *

1 . 9 3

S D R O E £

C o n s e r v

2 0 . 0 0 1 * *

*

2 1 0 . 2 9

2 0 . 0 0 1 * * *

2 1 0 . 1 6 2

0 . 0 0 1 * * *

2 1 1 . 9 8

2 0 . 0 0 1 * * *

2 1 2 . 4 4

2 0 . 0 0 1 * * *

2 1 0 . 8 1

2 0 . 0 0 1 * * *

2 1 1 . 1 1

R O E

2 0 . 0 2 1

2 1 . 0 2

2 0 . 0 2 4

2 1 . 1 9 2

0 . 0 3 1

2 1 . 5 0

2 0 . 0 3 3

2 1 . 6 0

2 0 . 0 6 5 * *

2 2 . 4 4

2 0 . 0 6 6 * *

2 2 . 5 1

G r o w

2 0 . 0 0 1

2 1 . 4 0

2 0 . 0 0 1

2 1 . 5 2

0 . 0 0 1

0 . 6 9

0 . 0 0 0

0 . 5 7

2 0 . 0 0 1

2 1 . 3 4

2 0 . 0 0 1

2 1 . 4 9

S T

0 . 1 1 9 * *

*

3 . 1 6

0 . 1 2 0 * * *

3 . 1 4

0 . 1 1 7 * * *

2 . 9 2

0 . 1 2 0 * * *

2 . 9 6

0 . 1 0 2 * *

2 . 1 2

0 . 1 0 4 * *

2 . 1 7

U n l i q u i d

2 0 . 0 3 5

( 2 0 . 5 1 ) 2 0 . 0 3 4

( 2 0 . 5 0 ) 2

0 . 0 5 5

( 2 0 . 7 6 ) 2 0 . 0 5 5

( 2 0 . 7 6 ) 2 0 . 0 5 9

( 2 0 . 7 2 ) 2 0 . 0 5 8

( 2 0 . 7 2 )

( c o n t i n u e d )

Table IX.Accountingconservatism, volatilityof earnings and CAR

NBRI2,1

42

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 21/25

I n c e n t i v e

0 . 0 2 7

( 1 . 5 2 )

0 . 0 2 7

( 1 . 5 3 )

0 . 0 1 4

( 0 . 7 5 )

0 . 0 1 5

( 0 . 7 5 )

0 . 0 1 9

( 0 . 8 7 )

0 . 0 1 9

( 0 . 8 7 )

C o m p e n

2 0 . 0 2 4 *

( 2 1 . 6 9 ) 2 0 . 0 2 4 *

( 2 1 . 7 4 ) 2

0 . 0 2 8 *

( 2 1 . 8 0 ) 2 0 . 0 2 8 *

( 2 1 . 8 0 ) 2 0 . 0 2 4

( 2 1 . 4 0 ) 2 0 . 0 2 4

( 2 1 . 4 0 )

L t c y

0 . 0 2 4

( 0 . 4 4 )

0 . 0 2 3

( 0 . 4 2 )

0 . 0 0 7

( 0 . 1 3 )

0 . 0 0 8

( 0 . 1 3 )

0 . 0 3 8

( 0 . 5 7 )

0 . 0 3 9

( 0 . 5 8 )

L t z c

0 . 9 3 3 * *

*

( 8 . 7 3 )

0 . 9 3 7 * * *

( 8 . 7 5 )

1 . 0 3 7 * * *

( 8 . 9 3 )

1 . 0 3 8 * * *

( 8 . 9 2 )

1 . 0 1 7 * * *

( 7 . 7 6 )

1 . 0 1 7 * * *

( 7 . 7 6 )

T i m e

0 . 0 0 1 * *

( 2 . 1 9 )

0 . 0 0 1 * *

( 2 . 1 8 )

0 . 0 0 1 *

( 1 . 7 5 )

0 . 0 0 1 *

( 1 . 7 6 )

0 . 0 0 0

( 0 . 2 0 )

0 . 0 0 0

( 0 . 2 0 )

S i z e

2 0 . 0 1 0

( 2 1 . 2 4 ) 2 0 . 0 0 9

( 2 1 . 1 6 ) 2

0 . 0 1 2

( 2 1 . 4 0 ) 2 0 . 0 1 1

( 2 1 . 3 4 ) 2 0 . 0 0 1

( 2 0 . 1 0 ) 2 0 . 0 0 1

( 2 0 . 0 5 )

L e v

2 0 . 0 0 8

( 2 0 . 2 4 ) 2 0 . 0 0 6

( 2 0 . 1 8 )

0 . 0 1 1

( 0 . 3 3 )

0 . 0 1 6

( 0 . 4 9 ) 2 0 . 0 1 0

( 2 0 . 2 5 ) 2 0 . 0 0 4

( 2 0 . 1 1 )

O t h e r s e c

2 0 . 0 1 3

( 2 0 . 5 6 ) 2 0 . 0 1 3

( 2 0 . 5 9 ) 2

0 . 0 1 1

( 2 0 . 4 5 ) 2 0 . 0 1 1

( 2 0 . 4 6 ) 2 0 . 0 3 2

( 2 1 . 1 8 ) 2 0 . 0 3 3

( 2 1 . 2 0 )

I n d s

C o n t r o l

C o n t r o l

C o n t r o l

C o n t r o l

C o n t r o l

C o n t r o l

n

9

1 8

9 1 8

9 1 8

9 1 8

9 1 8

9 1 8

F

1 0 . 8 0

1 0 . 8 6

1 2 . 3 5

1 3 . 2 5

1 0 . 8 8

1 1 . 0 5

R 2

0 . 1 7 3

0 . 1 7 2

0 . 1 7 7

0 . 1 7 6

0 . 1 4 1

0 . 1 4 1

N o t e s : S i g n i fi c a n c e a t : *

0 . 1 0 ,

* * 0 . 0 5 a n d * * * 0 . 0 1 ; C A R , c u m u

l a t i v e a b n o r m a l r e t u r n ; C A R 1 , C A R f

o r o n e t r a d i n g d a y a r o u n d t h e r e - o p e n d a y ; C A R 3 ,

C A R f o r t h r e e t r a d i n g d a

y ’ s w i n d o w ; C A R 1 0 , C A R f o r t e n t r a d i n g d a y ’ s w i n d o w ; C A R 3 0 , C A R f o r 3 0 t r a d i n g d a y ’ s w i n d o w ; C A R 3 0 1 , C A R

f o r 3 0 d a y s

b e f o r e r e - o p e n a n d o n e d a y a f t e r r e - o p e n ; C A R 3 0 1 0 , C A R f o r 3 0 d a y s b e f o r e r e - o p e n a n d t e n d a y s a f t e r r e - o p e n ; C o n s e r v 1 a n d C o n s e r v 2 a r

e a c c o u n t i n g

c o n s e r v a t i s m p r o x y , u s i n

g t h r e e y e a r s c u m u l a t i v e a c c r u a l s m u l t i p l i e d b y 2 1 ; S D R O E , t h e s t a n d a r d d e v i a t i o n o f t h e a v e r a g e ; R O E , t h e p a s t t h r e e y e a r s ;

G r o w , t h e a v e r a g e r e v e n u

e g r o w t h f o r t h e p a s t t h r e e y e a r s ; S T , a d u m m y v a r i a b l e ; 1 , y e s ; 0 , o t h e r w i s e ; U n l i q u i d , t h e u n - c i r c u l a r s t o c k t o t o t a l s t o c k b e f o r e

s h a r e r e f o r m , p r o x y f o r t h

e s h o c k t o t h e m a r k e t ; I n c e n t i v e , a d u m m y v a r i a b l e ; 1 , t h e r e f o r m p l a n i n c l u d e s a m a n a g e m e n t i n c e n t i v e p r o g r a m ;

0 , o t h e r w i s e ;

C o m p e n , t h e c o m p e n s a t i o

n p a i d b y u n - c i r c u l a r s h a r e h o l d e r s t o c i r c u l a r s h a r e h o l d e r s c o m p u t e d a s t h e s t o c k c o m p e n s a t i o n , w h i c h i s f r o m W i n d D a t a b a s e ;

L T C Y , t h e p a r t i c i p a t i o n r

a t e o f c i r c u l a r s h a r e h o l d e r s a t t e n d i n g t h e s h a r e h o l d e r s m e e t i n g ; L T Z C , t h e a p p r o v a l r a t i o o f c i r c u l a r s h a r e h o l d e r s o n t h e r e f o r m

p r o p o s a l ; T i m e , t h e t i m e s p a n f r o m t h e a p p r o v a l d a y , w h e n C R S

C a p p r o v e t h e r e f o r m p l a n p r o p o s e d b

y l i s t e d c o m p a n i e s , t o t h e r e - o p e n d a y ; S i z e , t h e l o g

f o r m o f a s s e t a t t h e e n d o f l a s t y e a r t o p r o x y t h e s i z e ; L e v , t h e t o t a l d e b t r a t i o ( L e v ) p r o x y t h e l e v e r a g e ; O t h e r s e c , a d u m m y v a r i a b l e , i n d i c a t i n g

w h e t h e r t h e

fi r m i s s u e s o t h e r t y p e o f s

h a r e s , l i k e B , S , o r H ; 1 , y e s ; 0 , o t h e r w i s

e ; V I F s i n a l l r e g r e s s i o n s a r e ,

2 , s h o w

i n g t h e r e i s n o t s e v e r e c o - l i n e a r i t y i n o u r r e g r e s s i o n

m o d e l s ; i n t h e p a r e n t h e s i s a r e t h e w h i t e - t - s t a t i s t i c s t o e l i m i n a t e t h e h e t e r o s c e d a s t i c i t y :

C A

R i ¼

a

þ

b 1

C o n s e r v þ

b 2

S D R O E £ C

o n s e r v þ

b 3

R O E þ

b 4

G r o w þ

b 5

S T

þ

b 6

U n l i q u i d þ

b 7

I n c e n t i v e

þ

b 8

C o m p e n þ

b 9

L t c y þ

b 1 0 L t z c þ

b 1 1

T i m e þ

b 1 2

S i z e þ

b 1 3

L e v þ

b 1 4

O t h e r S e c þ

P b j I n d s þ

1

Table IX.

Accountingconservatism

43

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 22/25

7. ConclusionChina’s securities market is facing fierce revolutions; numerous listed companies arelaunching their reform that all stocks, including some un-circular stocks, will be tradedin the market. What influence does the reform bring to the market and stock price? How

does the market evaluate the reform of each listed company, and does accountinginformation have any influence?

Using the data of companies completing the split-stock reform, we find thataccounting information plays its role through the reform in China’s securities market.The market recognizes the role of accounting conservatism, evident in the significantlypositive relation between the proxies of accounting conservatism and the CARs for oneday, three days, ten days and 30 days around re-open day after the reform. Also, theprofitability of listed firms in the past will further improve the positive relation betweenconservatism and market reaction. In all, accounting conservatism really has muchinfluence in the stock pricing, affecting the decision making and expectation of investors.

Notes1. It is also called all-circulation reform, split-share reform or ownership separation reform.

2. In China, on average, one-third stocks of listed companies are traded at the market quotedprices in the open capital market. In contrast, the other two-thirds are traded at the bookvalue in another closed market with much restriction.

3. Actually, those stock which are not circular before the reform cannot be traded freelyimmediately after the reform, they often have a buffering period, one to three years. Afterone to three years, they can be traded in the open market. The different buffering period isdetermined in the reform plan.

4. CAR is the cumulative abnormal return around the re-open day under naı̈ve model that ARis calculated as the daily return minus the average return on market portfolio.

5. We do not use the Cscore as Khan and Watts (2009) and the M/B ratio as conservatism, sinceduring 2001 to 2006, the Chinese stock market was declining monotonously for theregulation policy; however, the accounting performance, both ROE and cash flow, is arising.Market movement is not matched with operation, which is somewhat contradicted with theessential of Basu (1997) and Khan and Watts (2009) measures. The anther reason is that bothBasu (1997) and Khan and Watts (2009) measures are actually the conditional conservatism(Beaver and Ryan, 2005), which is only a part of conservatism. M/B is much noisy asconservatism due to the market efficiency.

6. To be succinct, we do not show regression results.

References

Ahmed, A.S. and Duellman, S. (2007), “Accounting conservatism and board of directorcharacteristics: an empirical analysis”, Journal of Accounting and Economics, Vol. 43,pp. 411-37.

Ahmed, A.S., Morton, R.M. and Schaefer, T.F. (2000), “Accounting conservatism and thevaluation of accounting numbers: evidence of the Feltham-Ohlson (1996) model”, Journal of Accounting, Auditing and Finance, Vol. 15, pp. 271-91.

Ahmed, A.S., Billings, B.K., Morton, R.M. and Stanford-Harris, M. (2002), “The role of accountingconservatism in mitigating bondholder-shareholder conflicts over dividend policy and inreducing debt costs”, The Accounting Review, Vol. 77, pp. 867-90.

NBRI2,1

44

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 23/25

Ba, S.S. (2005), “Ownership separation reform – what system will we buy?”, China Economy,

Vol. 309, pp. 26-7 (in Chinese).

Balachandran, S. and Mohanram, P. (2008), “Is the decline in the value relevance of accounting

driven by increased conservatism?”, working paper, Columbia University, New York, NY.

Ball, R., Robin, A. and Wu, J. (2003), “Incentives vs. standards: properties of accounting income in

four East Asian countries”, Journal of Accounting and Economics, Vol. 36, pp. 235-70.

Basu, S. (1997), “The conservatism principle and the asymmetric timeliness of earnings”, Journal of Accounting and Economics, Vol. 24, pp. 3-37.

Beaver, W.H. and Ryan, S.G. (2005), “Conditional and unconditional conservatism: concepts andmodeling”, Review of Accounting Studies, Vol. 10, pp. 269-309.

Chen, X. and Chen, S.Y. (2001), “Research on the reaction of stock trading volume to the annualfinancial reporting”, Journal of Financial Research, Vol. 7, pp. 98-105 (in Chinese).

Chen, X. and Qin, Y.H. (2003), “The banker and the quality of information disclosure”, Management World , Vol. 3, pp. 28-35 (in Chinese).

Chen, X. and Wang, K. (2005), “Related party transactions, corporate governance and state

ownership reform”, Economic Research Journal , Vol. 4, pp. 77-86 (in Chinese).

Chen, X., Chen, X.Y. and Liu, Z. (1999), “Research on the usefulness of financial statement”, Economic Research Journal , Vol. 6, pp. 21-6 (in Chinese).

Chen, H., Chen, J., Lobo, G. and Wang, Y. (2010), “Association between borrower and lenderstate ownership and accounting conservatism”, working paper, University of Houston,Houston, TX.

CSRC (2005), Notice About the Issues Related with the Ownership Separation Reform Experiment ,The State Department of P.R.C., Beijing (in Chinese).

Du, X., Liang, H.J. and Song, F.M. (2001), “Empirical investigation of initial returns of China’sA-share IPOs”, Journal of Management Science in China, Vol. 8, pp. 55-61 (in Chinese).

Easton, P. (2009), “Discussion of accounting data and value: the basic results”, Contemporary

Accounting Research, Vol. 26, pp. 261-72.

Feltham, J. and Ohlson, J. (1995), “Valuation and clean surplus accounting for operating and

financial activities”, Contemporary Accounting Research, Vol. 2, pp. 689-731.

Feltham, J. and Ohlson, J. (1996), “Uncertainty resolution and the theory of depreciationmeasurement”, Journal of Accounting Research, Vol. 34, pp. 209-34.

Francis, J., LaFond, R., Olsson, P. and Schipper, K. (2004), “Costs of equity and earningsattributes”, The Accounting Review, Vol. 79, pp. 967-1010.

Givoly, D. and Hayn, C. (2000), “The changing time-series properties of earnings, cash flows andaccruals: has financial reporting become more conservative?”, Journal of Accounting and

Economics, Vol. 29, pp. 287-320.

Grossman, S.J. and Stigliz, J. (1976), “Informational and competitive price system”,

American Economic Review, Vol. 66, pp. 246-54.Khan, M. and Watts, R.L. (2009), “Estimation and empirical properties of a firm-year measure of

accounting conservatism”, Journal of Accounting & Economics, Vol. 48, pp. 132-50.

Kim, B.H. and Pevzner, M. (2010), “Conditional accounting conservatism and future negativesurprises: an empirical investigation”, Journal of Accounting & Public Policy, Vol. 29,pp. 311-29.

LaFond, R. and Watts, R. (2008), “The information role of conservatism”, The Accounting Review,Vol. 83, pp. 447-78.

Accountingconservatism

45

8/2/2019 Accounting Conservatism

http://slidepdf.com/reader/full/accounting-conservatism 24/25

Li, J. (2007), “Accounting conservatism, information uncertainty and analysts’ forecasts”,working paper, Columbia University, New York, NY.

Li, J., Liao, L. and Shen, H.B. (2008), “An inelastic demand curve for stocks: evidence from China’ssplit-share structure reform”, working paper, Tsinghua University, Beijing.

Li, Z.G. (2005), “Empirical research on the bubble in China securities market”, working paper,Degrees of Doctor of Economics, Tsinghua University, Beijing (in Chinese).

Li, Z.Q., Sun, Z. and Wang, Z.W. (2004), “Tunneling and ownership structure: evidence from thelending of controlling shareholder”, Accounting Research, Vol. 12, pp. 3-13 (in Chinese).

Liang, H.J. (2003), “Research on the characteristics of A-share market and the separation of capitals between IPO market and trading market”, Degrees of Doctor of Economics,Tsinghua University, Beijing (in Chinese).