Embed Size (px)

DESCRIPTION

Accounting

Citation preview

102. 5-2 (Q5-2) (a) Explain how an increase in financialleverage can increase a company's ROE. (b) Given thepotentially positive relation between financial leverageand ROE, why don't we see companies with 100%financial leverage (entirely non-owner financed)?

ROE is the sum of return on assets (ROA) and the return that resultsfrom the effective use of financial leverage (ROFL). Increasingleverage increases ROE as long as ROA exceeds the after-taxinterest rate. Financial leverage is also related to risk: the risk ofpotential bankruptcy and the risk of increased variability of profits.Companies

98. Accounting for Disposal of a LTA 1. Record Depreciation Expense up to disposal date2. Record any cash received at the time of disposal3. Remove asset and any accumulated depreciation from the balancesheet.4. Record a Gain or Loss

14. Accounts Receivable Turnover (Sales Revenue/ Ave. Accounts Receivable)

28. Adjusting LIFO COGS to FIFO (IS) FIFO COGS = LIFO COGS - current period change in LIFO reserve

29. Adjusting LIFO inventory to FIFO (BS) FIFO Inventory = LIFO inventory +LIFO Reserve

72. Amortization The reduction of the discount over the life of the bond. Amortizationcauses the effective interest expense to be greater than the periodiccash interest payments based on the coupon rate.

100. Analyzing and Computing Accrued Interest on Notes.Compute any interest accrued for each of the followingnotes payable owed by Penman,Inc. as of December 31,2013 (use a 365-day year):-Lender--Issue Dt--Principal--Coupon Rate (%)--Term(days)-------------------------------------------------------------------------Nissim...........11/21/13.............18,000.....10.....................120Klein..............12/13/13............14,000......9......................90Bildersee.......12/19/13.............16,000.....12.....................60

Nissim40 days between 11/21/2013 and 12/31/2013(18,000 x .10) x (40/365)= $197.26-Klein18 days between 12/13/2013 and 12/31/2013(14,000 x .09) x (18/365) = $62.14-Bildersee12 days between 12/19/2013 and 12/31/2013(16,000 x .12) x (12/365) = $63.12-Added together they total: $322.52

125. Analyzing and Reporting Financial Statement Effects ofBond Transactions. On January 1, 2014, Hutton Corp. issued $300,000 for 15-year, 11% bonds payable for $377,814, yielding an effectiveinterest rate of 8%. Interest is payable semiannually onJune 30 and December 31. a. Show computations to confirm the issue price of$377,814. b. Prepare journal entries to record the bond issuance,semiannual interest payment and premium amortizationon June 30, 2014, and semiannual interest payment andpremium amortization on December 31, 2014. Use theeffective interest rate. c. Post the journal entries from part b to their respectiveT-accounts. d. Record each of the transactions from part b in thefinancial statement effects template.

16. Asset Turnover (Sales Revenue/Ave. Total Assets); ability to generate sales for agiven level of assets

31. Average Cost COGS and inventory are priced on the average cost of itemsavailable during the period

AccountingStudy online at quizlet.com/_i89th

70. Balance Sheet Effects - Bonds Issued at aDiscount

When a bond is sold at a discount, Cash (A) Increases, and Net Liabilities Increase.They are recorded at the amount of the proceeds received (NOT face value): BondPayable (L) at face value less Bond Discount (XL). The Bond Discount (XL) isamortized each period until it reaches 0, and the total liability of the bond has beenremoved from the balance sheet.

73. Balance Sheet Effects - Bonds Issued at aPremium

When a bond is sold at a premium, Cash (A) Increases (amount received will equalbond payable plus premium), and Net Liabilities Increase: Bond Payable (L) at facevalue plus Bond Premium (L).

69. Balance Sheet Effects - Bonds Issued atPar

When Bonds are issued at Par, Cash (A) is increased and Bonds Payable (L) isincreased by the face value.

40. Basic Issues of Inventory Accounting &Reporting

what physical goods should be included; what costs should be related to inventory;what cost assumption should be used

78. Bond Book Value The net liability remaining on the balance sheet.

60. Bond Premium When a bond's coupon rate (issued rate driven by issuing firm) is greater than themarket rate (driven by supply and demand). Bonds that sell at a premium are desirableto investors.

57. Bond Price The bond price equals the present value of the expected cash flows to the bondholder.

58. Bondholder cash flows Periodic Interest Payments - Equal payments are periodic intervals, called annuities.Single Payment - The face (principle) amount of the bond at maturity.

124. Bushman, Inc. issues $500,000 of 9%bonds that pay interest semiannually andmature in 10 years. Compute the bondissue price assuming that the bonds'market rate is: a. 8% per year compoundedsemiannually. b. 10% per year compoundedsemiannually

96. Can a company generate a Goodwill asset No. Goodwill is an asset that is acquired and transferred to the acquirer's balance sheetwhen all assets have been accounted for and there is residual value.

89. Capitalize or Expense - Paid $1,200 forroutine maintenance of machinery

Expense.

93. Capitalize or Expense - Paid $1,600 torefurbish a machine, thereby extendingits useful life

Capitalize. The useful life is extended

91. Capitalize or Expense - Paid $2,000 toequip the production line with newinstruments that measure quality

Capitalize. The new equipment enhances the assembly line.

90. Capitalize or Expense - Paid $5,400 torent equipment for two years

Capitalize. It improves operations. Recognize rental expense over the next two years.

92. Capitalize or Expense - Paid $20,000 torepair the roof on the building

Expense.This is routine maintenance of the building, unless it extends the building's useful life

94. Capitalize or Expense - Purchased apatent for $5,000

Capitalize. This is a purchased intangible asset

1. Challenges of Ratio Analysis 1.what measure of earnings to use 2.how changes in the accounting, acquisitions, willchange value 3.identifying comparable companies 4.understanding calculation ofratios 5.understand limitations of accouting-ambiguities, accounting methods

23. Common Size Financial Statements standardize the various line items in financial statements so thet can be comparedacross many companies

121. Computing and Recording Depletion Expense. In 2013, Eldenburg Mining Company purchased land for $7,200,000 that had anatural resource reserve estimated to be 500,000 tons. Development and roadconstruction costs on the land were $420,000, and a building was constructed ata cost of $50,000. When the natural resources are completely extracted, the landhas an estimated residual value of $1,200,000. In addition, the cost to restorethe property to comply with environmental regulations is estimated to be$800,000. Production in 2013 and 2014 was 60,000 tons and 85,000 tons,respectively. a. Compute the depletion charge for 2013 and 2014. (You should includedepreciation on the building, if any, as part of the depletion charge.) b. Prepare a journal entry to record each year's depletion expense as determinedin part a.

122. Computing Depreciation and Accounting for a Change of Estimate. In January 2013, Rankine Company paid $8,500,000 for land and a building. Anappraisal estimated that the land had a fair market value of $2,500,000 and thebuilding was worth $6,000,000. Rankine estimated that the useful life of thebuilding was 30 years, with no residual value. a. Calculate annual depreciation expense using the straight-line method.

a. Straight-line: $6,000,000 / 30 =$200,000 per year each year.

120. Computing Depreciation, Asset Book Value, and Gain or Loss on Asset Sale. Sloan Company uses its own executive charter plane that originally cost$800,000. It has recorded straight-line depreciation on the plane for six fullyears, with an $80,000 expected salvage value at the end of its estimated 10-yearuseful life. Sloan disposes of the plan at the end of the sixth year. a. At the disposal date, what is the (1) cumulative depreciation expense and (2)net book value of the plane? b. Prepare a journal entry to record the disposal of the plane assuming that thesales price is 1. Cash equal to the book value of the plane 2. $195,000 cash 3. $600,000 cash

127. Computing Present Values of Single Amounts and Annuities. Refer to Tables 2 and 3 in Appendix A near the end of the book to compute thepresent value for each of the following amounts: a. $90,000 received 10 years hence if the annual interest rate is 1. 8% compounded annually 2. 8% compounded semiannually b. $1,000 received at the end of each year for the next 8 years if money is worth10% per year compounded annually. c. $600 received at the end of each six months for the next 15 years if the interestrate is 8% per year compounded semiannually. d. $500,000 inheritance 10 years hence if money is worth 10% per yearcompounded annually.

55. Coupon Rate (Contract or Stated Rate) The coupon rate of interest is stated in thebond contract. It is used to compute thedollar amount of (semiannual) interestpayments that are paid to bond holdersduring the life of the bond issue.Fixed prior to issuance and remains sothroughout the life of the bond.

63. Coupon Rate < Market Rate Bond sells at a discount (below facevalue)

62. Coupon Rate = Market Rate Bond sells at Par Value (at face value)

61. Coupon Rate > Market Rate Bond sells at a premium (above facevalue)

9. Current Ratio (Current Assets / Current Liabilities)

4. Debt to Equity (Total Liabilities/Shareholders Equity)

47. Depletion the process of allocating (recording as anexpense) the cost of natural resources over theperiod of use

97. Depreciation and Long Term Assets (LTA) All long term assets (LTA) are depreciated exceptfor Land.

104. Describe the concept of asset turnover. What does the concept mean andwhy is it so important to understanding the interpreting financialperformance?

Asset turnover measures the amount of revenuevolume compared with the investment in an asset.Generally speaking, we want turnover to be higherrather than lower. Turnover measures productivityand an important company objective is to makeassets as productive as possible.

45. Disposal fo Asset After fully depreciated - record cash received assalvage value, remove asset and accum.Depreciation from balance sheet, record gain(loss) on sale

19. Earnings Before Interest (EBI) (net income + (interest expense x (1-tax rate))

64. Effective Cost of Debt When a bond sells for Par, the cost to the issuingcompany is the cash interest paid.When a bond sells at a discount, the issuer'seffective costs are two: The cash interest paid, andthe discount that occurred.

68. Effective Cost of Debt - 2 Reflected in the issuer's Income statement in theincome statement as an expense.

67. Effective Interest Rate The effective interest rate always equals themarket rate.

65. Effects of a Discount Bond The discount is the difference between the facevalue (par) and the lower issue price. It is a costthat must be reflected in the issuer's incomestatement as an expense.The effective cost of a discount bond is greaterthan if the bond sells at face value (par)

66. Effects of a Premium Bond When a bond is sold at a premium, the issuer'seffective costs are: the cash interest paid, and acost reduction due to the premium received. Thisultimately is reflected on the Balance Sheet as areduction of interest expense. The effective cost ofa premium bond is less than if the bond sold atface value (par).

117. Equipment costing $130,000 is expected to have a residual value of$10,000 at the end of its six-year useful life. The equipment is metered sothat the number of units processed is counted. The equipment isdesigned to process 1,000,000 units in its lifetime. In 2013 and 2014, theequipment processed 180,000 units and 140,000 units respectively.Calculate the depreciation expense for 2013 and 2014 using the straight-line method.

Straight-line: ($130,000 - $10,000)/ 6 years =$20,000 for both 2013 and 2014.

111. Even though it may not reflect their physical flow of goods, why mightcompanies adopt last-in, first-out inventory costing in periods whencosts are consistently rising?

A significant tax benefit results from using LIFOwhen costs are consistently rising. LIFO resultsin lower pretax income and, therefore, lower taxespayable, than other inventory costing methods.

101. Explain in general terms the concept of return on investment.Why is this concept important in the analysis of financialperformance?

Return on investment measures profitability in relation to theamount of investment that has been made in the business.

33. FIFO First In First Out; assumes company sells goos in the order theywere purchased; COGS contains earliest items purchased;ending inventory contains the latest items purchased

11. Financial Leverage use of debt to fund assets of the firm - if firm can earn an aftertax rate of ROA that exceeds the after tax cost of debt funding,the common shareholders benefit

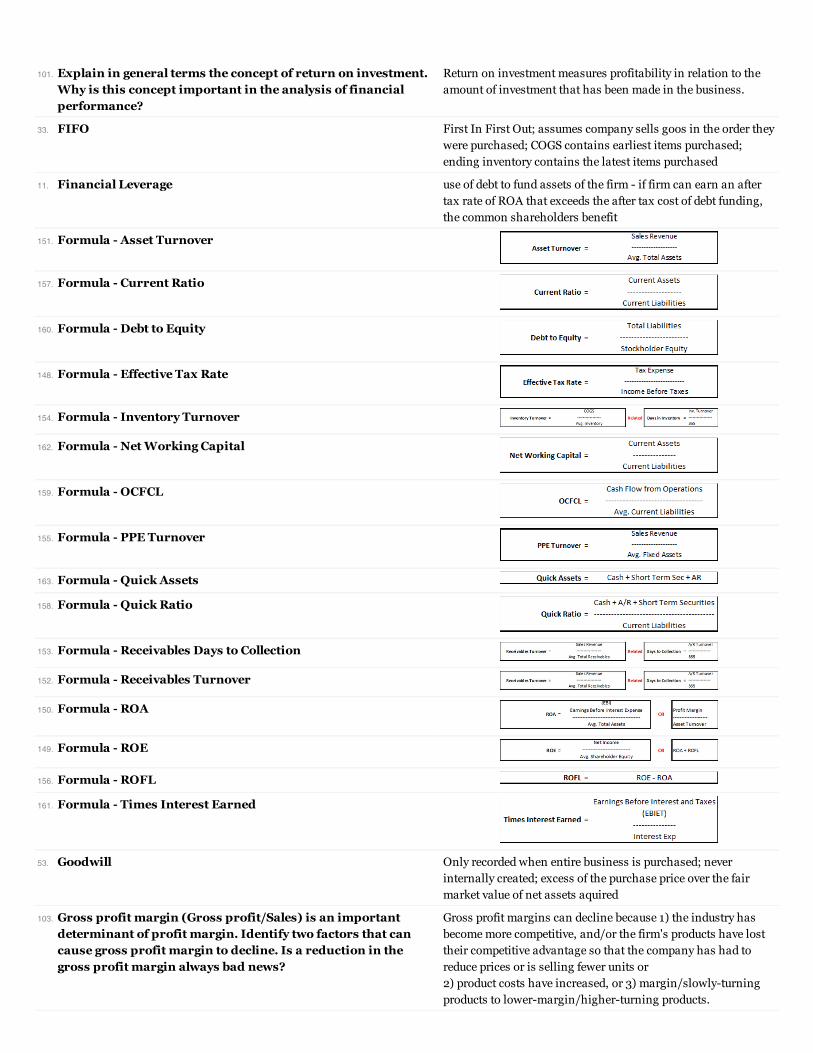

151. Formula - Asset Turnover

157. Formula - Current Ratio

160. Formula - Debt to Equity

148. Formula - Effective Tax Rate

154. Formula - Inventory Turnover

162. Formula - Net Working Capital

159. Formula - OCFCL

155. Formula - PPE Turnover

163. Formula - Quick Assets

158. Formula - Quick Ratio

153. Formula - Receivables Days to Collection

152. Formula - Receivables Turnover

150. Formula - ROA

149. Formula - ROE

156. Formula - ROFL

161. Formula - Times Interest Earned

53. Goodwill Only recorded when entire business is purchased; neverinternally created; excess of the purchase price over the fairmarket value of net assets aquired

103. Gross profit margin (Gross profit/Sales) is an importantdeterminant of profit margin. Identify two factors that cancause gross profit margin to decline. Is a reduction in thegross profit margin always bad news?

Gross profit margins can decline because 1) the industry hasbecome more competitive, and/or the firm's products have losttheir competitive advantage so that the company has had toreduce prices or is selling fewer units or 2) product costs have increased, or 3) margin/slowly-turningproducts to lower-margin/higher-turning products.

113. How is the LIFO reserve related tounrealized holding gains?

The LIFO reserve represents the difference between the historical, LIFO cost of inventoryand its current cost. This disparity between the book value and the current value representsa gain from holding the inventory that has not yet been recognized in income or in equity anunrealized holding gain.

82. How should a company treat achange in an asset's estimated usefullife or residualvalue?

When a change occurs in the estimate of an asset's useful life or its salvage value, therevision of depreciation expense is handled by depreciating the current undepreciated costof the asset (original cost - accumulated depreciation) using the revised assumptions ofremaining useful life and salvage value.

115. How should companies account forcosts, such as improvements, whichare incurred after an asset isacquired?

Betterment or improvement costs should be capitalized if the outlay enhances the usefulnessof the asset or extends the asset's useful life beyond original expectations. As would be thecase with any cost, an immaterial amount should be expensed as incurred.

79. How should companies account forcosts, such as maintenance orimprovements, which are incurredafter an asset is acquired?

Routine maintenance costs that are expensed. Improvement costs should be capitalized ifthey enhance the usefulness of the asset or extends the asset's useful life beyond originalexpectations.

114. How should companies account forcosts, such as maintenance, whichare incurred after an asset isacquired?

Routine maintenance costs that are necessary to realize the full benefits of ownership of theasset should be expensed.

123. How should premium and discountnon-bonds payable be presented inthe balance sheet?

Bonds payable is presented in the balance sheet net of any discount or plus any premium.

140. If a business had a net loss for theyear, under what circumstanceswould the statement of cash flowsshow a positive net cash flow fromoperating activities?

The statement of cash flows will show a positive net cash flow from operating activities ifoperating cash receipts exceed operating cash payments. This could happen, for example, ifnoncash expenses (such as depreciation and amortization) exceed the net loss. It wouldalso happen if operating cash receipts exceed sales by more than the loss or if operatingcash payments are less than accrual expenses by more than the loss (or some combinationof these events).

110. If inventory costs are rising, whichinventory costing method—first-in,first-out; last-in, first-out; or averagecost—yields the greatest cash flowassuming that method is used for taxpurposes.

Last-in, first-out

108. If inventory costs are rising, whichinventory costing method—first-in,first-out; last-in, first-out; or averagecost—yields the largest endinginventory?

First-in, first-out

109. If inventory costs are rising, whichinventory costing method—first-in,first-out; last-in, first-out; or averagecost—yields the largest net income?

First-in, first-out

106. If inventory costs are rising, whichinventory costing method—first-in,first-out; last-in, first-out; or averagecost—yields the lowest ending

Last-in, first-out

107. If inventory costs are rising, whichinventory costing method—first-in,first-out; last-in, first-out; or averagecost—yields the lowest net income?

Last-in, first-out

46. Impairment The write-off when some or all of the book value of an asset is not recoverable

131. In which of the three activity categories of a statement ofcash flows would each of the following items appear? Is it acash inflow or outflow: Cash collection on loans.

Investing; inflow

132. In which of the three activity categories of a statement ofcash flows would each of the following items appear? Is it acash inflow or outflow: Cash dividends paid

Financing; outflow

133. In which of the three activity categories of a statement ofcash flows would each of the following items appear? Is it acash inflow or outflow: Cash dividends received

Operating (direct method, not shown separately under indirectmethod); inflow

136. In which of the three activity categories of a statement ofcash flows would each of the following items appear? Is it acash inflow or outflow: Cash interest paid.

Operating (direct method, not shown separately under indirectmethod); outflow.

137. In which of the three activity categories of a statement ofcash flows would each of the following items appear? Is it acash inflow or outflow: Cash interest received

Operating (direct method, not shown separately under indirectmethod); inflow.

134. In which of the three activity categories of a statement ofcash flows would each of the following items appear? Is it acash inflow or outflow: Cash proceeds from issuing stock.

Financing; inflow.

130. In which of the three activity categories of a statement ofcash flows would each of the following items appear? Is it acash inflow or outflow: Cash purchase of equipment

Investing; outflow

135. In which of the three activity categories of a statement ofcash flows would each of the following items appear? Is it acash inflow or outflow: Cash receipts from customers

Operating (direct method, not shown separately under indirectmethod); inflow

76. Income Statement Effects - Bonds Issued at a Premium The amount of interest reported on the income statement isalways equal to the Bond Payable net of discount or premium atthe beginning of the period multiplied the market rate at time ofissue.Interest = Beginning Net Bond Payable x Market Rate at IssuanceA Bond premium yields a reduction in interest expense on theincome statement.

52. Indefinate Life Intangibles no foreseeable limit on the time asset is expected to provide cashflows; all must be periodically evaluated for impairment

143. Indicate whether the cash flow relates to an operatingactivity, an investing activity, or a financing activity:Acquisition of plant assets for cash.

Cash flow from an investing activity.

145. Indicate whether the cash flow relates to an operatingactivity, an investing activity, or a financing activity: Bondspayable issued for cash.

Cash flow from a financing activity.

141. Indicate whether the cash flow relates to an operatingactivity, an investing activity, or a financing activity: Cashreceipts from customers for services rendered.

Cash flow from an operating activity.

146. Indicate whether the cash flow relates to an operatingactivity, an investing activity, or a financing activity:Payment of cash dividends declared in previous year.

Cash flow from a financing activity

144. Indicate whether the cash flow relates to an operatingactivity, an investing activity, or a financing activity:Payment of income taxes.

Cash flow from an operating activity.

147. Indicate whether the cash flow relates to an operatingactivity, an investing activity, or a financing activity:Purchase of short-term investments (not cash equivalents)for cash.

Cash flow from an investing activity.

142. Indicate whether the cash flow relates to an operatingactivity, an investing activity, or a financing activity: Saleof long-term investments for cash.

Cash flow from an investing activity.

49. Intangible Assets no physical existance, not financial instruments; recorded at fairvalue of consideration or value received, includes costs to makeready for use

50. Internally Created Intangibles Generally expensed; only capitalize direct cots incurred in obtainingthe intangible, such as legal fees

13. Inventory Turnover (COGS/Ave. Inventory), remember 365/inventory turnover = # daysitems remain in inventory

32. LIFO Last In First Out; assumes company always sells the most recentitems purchased; ending inventory contains the oldest itemspurchased

30. LIFO Conformity Rule if using LIFO for tax purpose, must also use LIFO for financialreporting purposes

27. LIFO Liquidation When inventory levels valued at older proces are sold and thoseolder prices flow through COGS; can distort reported income(unrealistically low COGS and high net income)

51. Limited Life Intangibles amortize to expense over expected useful life, reflect pattern of use, ifnot use straight-line

43. Long Term Assets Tangible and Intangible - PP&E, Natural Resources, Trademarks,Patents, Goodwill

95. Long Term Assets (LTA) TangiblePP&ENatural Resources

IntangibleTrademarksGoodwillPatents

54. Long Term Liabilities probably future sacrifices of economic benefits arising from presentobligations that are not payable within a year or the operating cycleof the company, whichever is longer

26. Lower of Cost or Market Rule rule for writing down the recorded value of inventory whos marketvalue has declined below cost. Cost in historical costand marketrefers to current cost to replace

35. Manufacturer Product Costs 1. direct material costs 2. direct labor costs 3.manufacturingoverhead costs

56. Market (Yield) Rate The market rate is the interest rate that investors expect to earn onthe investment for this debt security. This rate is used to price thebond issue.This rate fluctuates based on supply and demand in the market.

36. Merchandiser Product Costs 1.aquisition cost 2. freight charges 3.sales taxes and insurance4.labor & other costs due to processing at time of sale

6. Operating Cash Flows to Current Liabilities (Cash Flow from Operations / Ave. Current Liabilities)

59. Par value When a bond is issued at Par, the Market Rate (drives investmentyield) and Coupon Rate (drives interest payments) are identical.

12. PP&E Turnover (Sales Revenue/Ave. Fixed Assets)

2. Price - Earnings Ratio (market price per share / annual earnings)realtionship between afirms financial performance and the firms stock price

37. Product Costs costs directly connected with bringing thegoods to the buyers place of business andconverting such goods to a saleablecondition

17. Profit Margin (EBI/Sales Revenue); ability to controlexpenses relative to sales

24. Purpose of Financial Statement Analysis present financial information in a formatthat facilitates the analysis andinterpretation of a company'sperformance

7. Quick Current Assets (Cash + Short Term Securities + AccountsReceivable)

8. Quick Ratio (Quick Current Assets / CurrentLiabilities)

22. Ratio Analysis calculating relationship of incomestatement items with balance sheet items;ROE=Income/Eqity;ROA=Income/Assets

99. Record a Gain or Loss Gain (loss) = Sale Proceeds - Book Valueof Asset

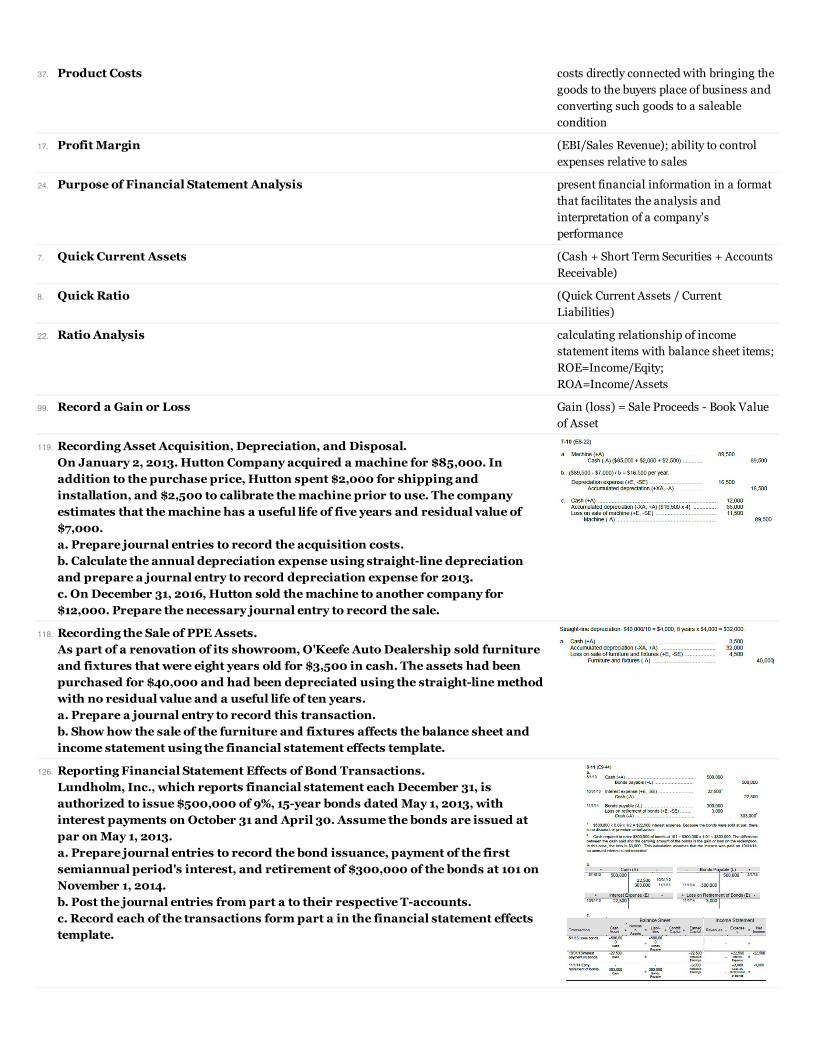

119. Recording Asset Acquisition, Depreciation, and Disposal. On January 2, 2013. Hutton Company acquired a machine for $85,000. Inaddition to the purchase price, Hutton spent $2,000 for shipping andinstallation, and $2,500 to calibrate the machine prior to use. The companyestimates that the machine has a useful life of five years and residual value of$7,000. a. Prepare journal entries to record the acquisition costs. b. Calculate the annual depreciation expense using straight-line depreciationand prepare a journal entry to record depreciation expense for 2013. c. On December 31, 2016, Hutton sold the machine to another company for$12,000. Prepare the necessary journal entry to record the sale.

118. Recording the Sale of PPE Assets. As part of a renovation of its showroom, O'Keefe Auto Dealership sold furnitureand fixtures that were eight years old for $3,500 in cash. The assets had beenpurchased for $40,000 and had been depreciated using the straight-line methodwith no residual value and a useful life of ten years. a. Prepare a journal entry to record this transaction. b. Show how the sale of the furniture and fixtures affects the balance sheet andincome statement using the financial statement effects template.

126. Reporting Financial Statement Effects of Bond Transactions. Lundholm, Inc., which reports financial statement each December 31, isauthorized to issue $500,000 of 9%, 15-year bonds dated May 1, 2013, withinterest payments on October 31 and April 30. Assume the bonds are issued atpar on May 1, 2013. a. Prepare journal entries to record the bond issuance, payment of the firstsemiannual period's interest, and retirement of $300,000 of the bonds at 101 onNovember 1, 2014. b. Post the journal entries from part a to their respective T-accounts. c. Record each of the transactions form part a in the financial statement effectstemplate.

25. Reporting Inventory Information Calculating relationship of income statement items with balance sheet items;ROE=Income/Eqity; ROA=Income/Assets

77. Repurchasing Bonds Companies may exercise a call provisions (if in the bond contract), or bondscan be repurchased on the open market by the issuing firm prior to the bondreaching maturity. When a company repurchases the bond, they must book again or loss and retire the bond:Gain or Loss on Bond Retirement = Book Value - Repurchase PaymentRecorded as regular income.

20. Return on Assets (EBI/Average Total Assets); measures company performance using assets togenerate net income independent of how the company financed the assets

21. Return on Equity (Net Income/Ave. Shareholders' Equity); measuers performance of usingfinancing assets to generate net income for common shareholders

18. ROA = ? X ? (Profit Margin x Asset Turnover)

10. ROFL (ROE - ROA), remember ROE=ROA+ROFL; the effect of financial leverage on acompany's ROE

85. Sale of a Long-Term Asset 1. Determined by the difference between the asset's book value and the saleproceeds. a. Sales proceeds in excess of book values create gainsb. Sales proceeds less than book values cause losses.

5. Solvency ability to meet debt payments including interest and the repayment of principal

44. Straight Line Depreciation ((Total Asset Value - Salvage Price)/Useful Life of Asset)

39. Three Major Cost Assumptions for Inventory FIFO, LIFO, Average cost (weighted average of inventory)

3. Time Interest Earned (EBIT/Interest Expense)

15. To Improve ROA... 1.improve your profit margin 2.improve asset turnover **Use ratio analysis tofigure out which one an entity may be focused on

71. Transaction - Bonds Issued at a Discount If the Bond has a face value of $100,000 and the discount is $6,733, then theTransaction is recorded as such: Cash (A) 93,267, Bond Payable (L) 100,000,Bond Discount (XL) -6,733

74. Transaction - Bonds Issued at a Premium Cash (A) 107,325, Bond Payable (L) 100,000, Bond Premium (L) 7,325

41. Two Categories of Businesses with Inventory merchandising business who purchase goods ready to sell; manufacturingbusiness who produce goods that are then sold to merchandisers

48. Units of Production Method ((total cost-residual value)/estimated total units of resource available); (unitsextracted x cost per unit)

129. What are the three major types of activitiesclassified on a statement of cash flows? Give anexample of a cash inflow and cash outflow ineach classification.

Operating activities Inflow: Cash received from customers Outflow: Cash paid to suppliers .Investing activities Inflow: Sale of equipment Outflow: Purchase of stocks and bonds Financing activities .Inflow: Issuance of common stock Outflow: Payment of dividends

42. What can be Classified as Inventory items held for sale; items in process of production or sale; goods used in theproduction of goods to be sold (raw material goods)

84. What factors determine the gain or loss fromthe sale of a long-term operating asset?

1. Depreciation rate 2. Salvage values used to compute depreciation expense3. Accumulated depreciation and the net book value of the asset4. Selling price

112. What is a LIFO reserve? The "LIFO reserve" is the difference between the cost of inventory determined using the last-in, first-out(LIFO) method and the cost determined using another method (either FIFO or average cost).

88. What is meant by anintangible asset with an"indefinite life"?

The useful life is long and cannot be determined with any reasonable degree of accuracy.

128. What is the definition ofcash equivalents? Givethree examples of cashequivalents.

Cash equivalents are short-term, highly liquid investments that firms acquire with temporarily idle cashto earn interest on these excess funds. To qualify as a cash equivalent, an investment must (1) be easilyconvertible into a known cash amount and (2) be close enough to maturity so that its market value is notsensitive to interest rate changes (generally, investments with initial maturities of three months or less).Three examples of cash equivalents are Treasury bills, commercial paper, and money market funds.

139. What is the differencebetween the directmethod and the indirectmethod of presenting netcash flow from operatingactivities?

The direct method presents the net cash flow from operating activities by showing the major categories ofoperating cash receipts and cash payments (such as cash received from customers, cash paid toemployees and suppliers, cash paid for interest, and cash paid for income taxes). The indirect (orreconciliation) method, in contrast, presents the net cash flow from operating activities by applying aseries of adjustments to the accrual net income to convert it to a cash basis.

81. What is the effect ofcapitalized interest onthe income statement infuture periods?

An increase in periodic depreciation expense and reduced net income.

116. What is the effect ofcapitalized interest onthe income statement inthe period that an asset isconstructed?

Capitalizing interest costs as part of the cost of constructing an asset reduces interest expense, andincreases net income during the construction period.

80. What is the effect ofcapitalized interest onthe income statement inthe period that an asset isconstructed?

Capitalizing interest costs reduces interest expense, and increases net income during the constructionperiod.

86. What is the properaccounting treatment forresearch anddevelopment costs?

R&D costs must be expensed under GAAP unless they have alternative future uses.

Outputs from costs related to R&D activities are uncertain and there are, therefore, no expected cash flowsagainst which to match any future depreciation expense.

34. What Makes Up the CostFlow Assumption

1.what prices should be assigned to the goods that have been sold 2.what prices should be assigned to thegoods that remain in inventory

38. When Should a CompanyRecord Inventory

when it obtains legal title to the good; must consider goods in transit, special arrangements, sales returns

87. Which intangible assetscan be Amortized?

Intangible assets that have a useful life that is limited and can be easily estimated can be amortized.

83. Which period(s)—past,present, or future—isaffected by a change in anassets estimated usefullife?

Present and future periods are affected by such revisions. Depreciation expense calculated and reported inpast periods is not revised.

138. Why are noncashinvesting andfinancingtransactionsdisclosed assupplementalinformation to astatement of cashflows?

Noncash investing and financing transactions are disclosed as supplemental information to a statement of cashflows because a secondary objective of cash flow reporting is to present information about investing andfinancing activities. Noncash investing and financing transactions, generally, affect future cash flows. Issuingbonds payable to acquire equipment, for example, requires future cash payments for interest and principal on thebonds. On the other hand, converting bonds payable into common stock eliminates future cash payments relatedto the bonds. Knowledge of these types of events, therefore, should be helpful to users of cash flow data who wishto assess a firm's future cash flows.

105. Why is itimportant todisaggregate ROAinto profit margin(PM) and assetturnover (AT)?

Companies must manage both the income statement and the balance sheet in order to maximize ROA.

75. Zero Coupon Bond A bond which has no explicit coupon rate, and is issued at a deep discount. The bond price is the present value ofthe principle payment at maturity. A 4 year zero coupon bond with a face value of $100,000 and a market rate of6% would sell for $78,941 with a discount of $21,059.