Embed Size (px)

Citation preview

Level 2, 53 Blackall Street

Barton ACT 2600

02 6260 3733

www.regionalaustralia.org.au

Access to Finance Growing SMEs in regional Western Australia

June 2015

Access to Finance, June 2015 P a g e | i

Access to Finance, June 2015 P a g e | ii

The Regional Australia Institute

Independent and informed by both research and ongoing dialogue with the community, the

Regional Australia Institute (RAI) develops policy and advocates for change to build a stronger

economy and better quality of life in regional Australia – for the benefit of all Australians.

Disclaimer and Copyright

This research report translates and analyses findings of research to enable an informed public

discussion of regional issues in Australia. It is intended to assist people to think about their

perspectives, assumptions and understanding of regional issues. No responsibility is accepted

by RAI Limited, its Board or its funders for decisions made by others based on the information

presented in this publication.

Unless otherwise specified, the contents of this report remain the property of the Regional

Australia Institute. Reproduction for non-commercial purposes with attribution of authorship is

permitted.

RAI Research and Policy

Project researchers: Annemarie Ashton-Wyatt, Senior Researcher

Chrissy Peters, Research Assistant

Project supervisor: Jack Archer, Deputy Chief Executive Officer

Contributing to analysis, editorial and review:

Su McCluskey, Chief Executive Officer All RAI research is informed by the expertise of the RAI Research Advisory Committee. Members in 2014/15 are:

Professor Sandra Harding, James Cook University (Chair)

Professor Andrew Beer, University of Adelaide

Professor Graeme Hugo, University of Adelaide

Professor John Tomaney, University College of London

Tim Shackleton, Director, Virtual Health, and Director, Regional Australia Institute

Su McCluskey, Chief Executive Officer, Regional Australia Institute

Access to Finance, June 2015 P a g e | iii

Research Partnership Structure

Executive Reference Group:

Tim Shackleton, Regional Development Council of Western Australia

Mike Rowe, Department of Regional Development, Western Australia

Su McCluskey, Regional Australia Institute

Project Steering Committee:

Ken King, Pilbara Development Commission (until February 2015) (Chair)

Bruce Manning, Great Southern Development Commission

Grant Arthur, Wheatbelt Development Commission

Richard Hancock, Pilbara Development Commission

John Acres, Department of Regional Development

Denis O’Donovan, Department of Regional Development

Jack Archer, Regional Australia Institute

Acknowledgements

The RAI thanks the following people and organisations who have contributed information,

feedback and ideas during the development of this report:

Steven Münchenberg, Australian Bankers’ Association

John Stamolis, Australian Bankers’ Association

Collin Brady, Bendigo Bank

Russell Pritchard, Great Southern Development Commission

John Burn, Many Rivers Microfinance Limited

Catherine Lim, Many Rivers Microfinance Limited

Claudia Rayne, Many Rivers Microfinance Limited

Busselton Chamber of Commerce and Industry

Access to Finance, June 2015 P a g e | iv

Table of Contents

Executive Summary ...................................................................................................................................... v

Profiting from Potential: Access to Finance and SMEs in Regional Western Australia .................. 1

SMEs in Regional Western Australia ....................................................................................................... 3

The Economic Environment for SMEs in Western Australia ............................................................. 5

Investigating Access to Finance ................................................................................................................ 9

Types of Finance .................................................................................................................................. 10

Access to Finance for Australian SMEs ............................................................................................. 11

Factors Contributing to Access to Finance ........................................................................................ 12

Bank Lending ............................................................................................................................................. 15

Postcode Lending Systems .................................................................................................................. 22

Proximity to Financial Institutions ....................................................................................................... 23

Importance of the Business Relationship ........................................................................................... 29

Case Study 1: Bendigo Bank and Mobile Lending in Regional Areas ........................................... 30

Non-Bank Lending .................................................................................................................................... 32

Business Credit ...................................................................................................................................... 32

Venture Capital and Angel Investment ............................................................................................ 33

Case Study 2: Angel Investment in Regional Business in Western Australia ................................ 35

Other Non-Bank Lending .................................................................................................................... 36

Case Study 3: Many Rivers Microfinance .......................................................................................... 38

The Importance of Non-Bank Funding for Enabling Innovation ................................................... 40

Conclusion ................................................................................................................................................... 41

Appendix A: Lists of Figures and Tables .............................................................................................. 43

Contacts and Further Information .......................................................................................................... 44

References and End Notes ...................................................................................................................... 45

Access to Finance, June 2015 P a g e | v

Executive Summary

The perception that poor access to finance is a constraint on local business and regional

growth is a long-standing feature of the regional development discussion in Australia.

The Regional Australia Institute (RAI) has consulted with regional groups, banks and other

stakeholders, to investigate the financing environment for small and medium enterprises (SMEs)

in regional Western Australia.

Overall, it is clear that regional SMEs in Western Australia face many of the same constraints

on access to finance that have been identified for SMEs nationally. Reviews, such as the recent

Financial System Inquiry, draw attention to some of the challenges in assessing the worth of

SMEs and understanding the variation across different industries or geographical areas.

The RAI analysis finds limited evidence to suggest that additional, widespread access to

finance issues exist for regional SMEs in Western Australia. Instead, regional businesses usually

have many of the factors associated with successful access to finance. These factors include

good availability of collateral, sufficient size of employment or turnover, a well-established

trading history or credit record, good financial literacy, and being in industries which are well-

understood by banks.

There is a high rate of successful access to finance in regional Western Australia. This is most

likely due to the dominance of the agriculture sector, with land assets that can be used as

collateral for lending. Good availability of industry-specific data and agri-business lending

specialists helps to inform decision-making in financial institutions. This makes it more likely that

applications will be successful where the individual business case is also strong.

Other SMEs in regional Western Australia, such as those in the mining and manufacturing

sectors, have utilised different pathways to access finance in recent times. The mining industry

is a high user of equity finance, which is sought through capital markets or joint venture

agreements. Similarly, manufacturing SMEs may be able to secure debt-funding using supply

contracts to larger companies as collateral.

Continued access to capital for SMEs in each of these industries is important for regional

Western Australia’s economy, particularly given the capital intensity and need for continual

investment in some sectors.

Despite the generally strong picture across regional Western Australia, there is evidence that

some regional SMEs may face difficulties in accessing finance, particularly when compared to

similar businesses in metropolitan areas. These SMEs are more likely to be in industries where

their collateral is based on ideas or activities, such as the knowledge sector or the services

delivery sector. The growth of knowledge-based industries and service industries in regional

areas is important, as these are growing markets within the Australian economy.

Access to Finance, June 2015 P a g e | vi

Barriers preventing viable businesses from accessing finance often reflect the thinner markets

and limited information on the performance of similar business in regional Western Australia.

Each of these factors helps banks to assess the business income growth potential and identify

any potential risks for lending. SMEs with higher risk profiles due to a lack of available data

are likely to face increased costs when borrowing from financial institutions or may even be

unable to secure finance, despite being a sound and viable business.

The RAI’s investigation into access to finance revealed that bank finance is the most commonly

used means of funding for regional SMEs, but the use of non-bank finance is growing. While

leasing and debt-financing facilities are currently the most commonly used forms of non-bank

finance, market potential is growing in other pathways.

New forms of finance available to regional SMEs include online avenues to venture capital

and angel investment, crowd funding, peer to peer lending, and guarantor loan schemes.

These finance options may offer more potential to fund growth for SMEs in regional areas,

particularly for business start-ups or for knowledge-based and service-delivery businesses.

At present, non-bank forms of finance are more readily available in Perth or other Australian

capital cities, but are relatively rare in regional Western Australia. However, many types of

non-bank finance are now being delivered completely through online portals, which enables

wider regional access.

While there is certainly no case for substantial government intervention in this area, some

measured policy responses may be usefully considered to support improved access to finance

for regional SMEs:

Improved data about regional business and business performance will increase the

understanding of regional potential and help to reduce the risks of banks or others

rejecting applications from good businesses;

Strategies to build business confidence will be vital for supporting the growth of SMEs

in regional communities and encouraging banks to invest in regional business;

Improving availability of supports for regional businesses to improve their financial

literacy skills; and

Building greater awareness of non-bank lending options, and encouraging

engagement with entrepreneurial regional business. Growth in the scale and frequency

of equity funding through angel networks or venture capital could help to increase the

dynamism and sophistication of regional finance in Western Australia.

These strategies will be vital to offset the challenges of the slowdown in the resources sector,

and also to grow the knowledge and service sectors which are under-represented in regional

areas. Investing in the growth and capacity of SMEs will help to broaden local economic

capacity in the longer term and help to reduce many communities vulnerability to changes in

external markets.

Access to Finance, June 2015 P a g e | 1

Profiting from Potential: Access to Finance and

SMEs in Regional Western Australia

Small to medium enterprises (SMEs) have been identified as a major driver of economic

growth in Australia, as they are a substantial source of both employment and innovation.1

An active and profitable local business sector adds diversity to many regional economies.

It also provides services to meet the needs of local populations and industry.

Businesses need access to finance in order to grow, whether through expansion of production

capacity, entry into new markets, or new business start-ups. Difficulties in accessing finance are

considered to have inhibited the growth of SMEs across the Asia-Pacific region.2 Banks in

Australia have indicated that loan application decline rates are more than twice as high for

business start-ups compared to established businesses.3 This presents a substantial barrier to

growth, which may be particularly to the disadvantage of business in regional areas.

The global financial crisis (GFC) in 2008 led to a general tightening of bank lending criteria

and requirements for greater capital and liquidity, under the Basel III Agreement, which has

created flow-on effects across the world’s economies.4 In Australia, some of the effects of the

GFC are reduced business confidence and a more restricted lending market.

The Basel lll Agreement came into effect in Australia at the start of 2014. Prior to this, bank-

imposed restrictions, such as reduced loan to valuation ratios, had already made credit harder

to obtain and also more expensive. These factors, combined with a soft economic environment,

has led to a business focus on consolidation and survival rather than growth, which further

inhibits economic recovery.5

In Australia, businesses have been obtaining funds needed for survival through non-bank

sources, profit reinvestment, or sale of assets rather than through finance applications.6 While

this may be suitable for survival in challenging economic times, such strategies are unlikely to

realise the level of capital required to foster business growth.

Bank loans have been perceived as less desirable in recent years, despite low interest rates,

due to perceptions that the Australian economy is facing tough times ahead. Fears about the

potential for future interest rate rises are heightened for small business owners, as they also

have concerns that high debt levels with banks may limit their autonomy over the future of the

business.7

Financial commentators have noted that a general deterioration in trust in the relationships

between business and the banks seems to be inhibiting economic growth.8

Access to Finance, June 2015 P a g e | 2

“Growth in the Australian economy will not only be largely determined by the

willingness of businesses to borrow but by banks being prepared to lend to them.

Both sides are likely to show considerable caution in the current economic

environment. Banks will also need to improve their relationship with business — as

shown by the much lower satisfaction levels when compared to their retail customers

— if they are going to retain and attract good business customers.”9

Evidence of this deterioration includes small business continuing to having very low satisfaction

rates with the big four banks, due to increased fees and charges, and the introduction of

centralised operating models which are perceived to reduce understanding of business needs

and strengths at a local level.10

Technological advances have also changed the way that businesses access finance. While

automated application procedures for finance may enable easier access for businesses without

a local bank branch, it may also result in exclusion due to poor recognition of asymmetric

information across different sectors or regions.11 Asymmetry of information12, alongside

volatility of revenue and higher levels of default risk, is also a factor in the higher cost of

finance for many SMEs.13

Despite the challenging economic times, regional SMEs in Australia may be better placed for

growth than metropolitan SMEs. Recent research indicates that 69 per cent of SMEs in regional

centres are optimistic about potential growth in their business, compared to 65 per cent of

capital city SMEs and 57 per cent of rural SMEs.14

This paper investigates whether access to finance is more challenging for regional businesses

compared to metropolitan businesses in Western Australia. It also seeks to identify any factors

associated with access to finance which may promote the growth of regions by enabling the

development of new or expanded SMEs.

Regional SMEs in different

industries all need access to

finance to grow, but some may

have easier access than others

Knowledge-based Service-based

Agriculture-based Mining/manufacturing based

Access to Finance, June 2015 P a g e | 3

SMEs in Regional Western Australia

SMEs can be defined by number of employees or by size of annual turnover.15 The Australian

Bureau of Statistics (ABS) defines a small business as having less than 20 employees, and a

medium-sized business as having 20 or more employees but less than 200 employees.16 Small

business finance in Australia is defined by the Reserve Bank of Australia (RBA) as loans of

under $2 million.17

SMEs are important sources of employment in many regional areas, and are often found in

labour intensive industries, such as food services.18 SMEs are most common in agriculture and

are less common in those businesses requiring very large capital investment, such as mining or

manufacturing.19

Regional areas in Western Australia had almost 56,000 SMEs as at June 2012, which is

approximately 25 per cent of all Western Australian SMEs.20 These SMEs were most likely to

be in the agriculture, forestry and fishing industry, followed by the construction industry, and

then the rental, hiring and real estate services industry (Figure 1).

Figure 1: SMEs in Western Australia to June 2012 by regional or metropolitan location 21

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Perc

ent

ag

e

Regional Metropolitan

Access to Finance, June 2015 P a g e | 4

Over two thirds of all SMEs in Western Australia are sole person operations with no

employees. Despite this, SMEs in regional areas were more likely to have employees than

those in the Perth metropolitan area (39 per cent of all regional SMEs compared to 36 per

cent of Perth SMEs).22 This is similar to the national level for SMEs, which sits at 39 per cent.

The SME group identified as having the highest likelihood of growth is a business with one to

four employees (Figure 2).23 There were 12,399 SMEs of this size in regional Western

Australia, which is approximately 22 per cent of all regional SMEs.24

Regional SMEs are also highly engaged in adopting new business practices enabled through

technology. Research indicates small businesses in regional Western Australia were more likely

to generate a proportion of their income through online sales compared to small businesses in

the Perth metropolitan area.25

Figure 2: Key characteristics of SMEs in Western Australia 26

Access to Finance, June 2015 P a g e | 5

The Economic Environment for SMEs in Western Australia

The economic environment affects how SMEs do business. Growth in a business depends on the

opportunities available, its capacity to realise those opportunities, and the conditions of the

general economic environment, particularly those affecting business income and access to

finance.

Managing periods of economic uncertainty has been identified as a key priority for many

businesses in Western Australia.27 SMEs in Western Australia have been impacted by

economic events in both external and local markets, such as shifts in resources and commodities

markets, changes in government spending patterns, tightening lending markets, and low levels

of consumer confidence.

SMEs in different industries and/or regions will experience different levels of impact. This can

be due to a higher level of exposure to the external changes, but also reflect the level of

resilience within the business itself.

The Impact of Changes in External Markets

SMEs in regions with a high level of dependence upon single industries have more sensitivity to

changes in external markets. They can experience high demand for their goods and services

when economic conditions are positive, and may need access to finance to quickly grow their

capacity and capitalise on available opportunities.

SMEs can also lose vital sources of income when corrections or slowdowns occur in external

markets. Some may need access to finance to survive a period of lower business income while

new markets or opportunities to diversify are identified.

Slowdowns can also present vital opportunities for SMEs to invest in development of the

business. New goods, services, or market opportunities may have been identified during a

period of peak demand, but not acted upon. While some businesses may have reserves of

capital to invest in research and development, others will need access to finance to bring a

longer term growth strategy to fruition.

An example of how changes in external markets can impact on small business is evident in the

flow on impacts in the Goldfields-Esperance region from changes in the gold price. Gold is a

large export earner for the region; the value of mining and mineral production was over

$9 billion in 2012-13.28 Since early 2013, a lower price trend, combined with fluctuations in

the value of the Australian dollar, has substantially affected the profit margin for gold

producers.

Access to Finance, June 2015 P a g e | 6

Mining companies’ responses to lowering commodity prices can include strategies such as

stock-piling of ore, reduced production rates, workforce redundancies, and reductions in

discretionary or capital expenditure.29 This creates flow-on effects in local economies, as

changes in larger companies’ expenditure on wages and goods or services will have direct

impacts on local SMEs who depend upon these sources for business income.

Changes in external markets require a shift in business focus for SMEs from growth strategies

to survival strategies. If the downturn is prolonged, local SMEs may then make reductions in

staffing, which then contributes to higher local unemployment. Evidence of this type of impact

can be seen in the Goldfields-Esperance regional economy, where unemployment rates in

LGAs with high gold mining activity have increased during a period of relatively low gold

prices (Figure 3).

As employment markets contract in the region, two flow-on effects on population mobility will

likely become evident:

A slowing of inward migration; and

An increase in outward migration.

One of the first indicators of such trends is slowing of demand for rental accommodation,

leading to higher vacancy rates and lower rents. Median rental rates in Kalgoorlie-Boulder

declined by 15.4 per cent between September 2013 and September 2014.30

Higher rates of outward migration and lower inward migration can reduce the revenue

opportunities for SMEs due to the smaller size of the local market. This can create further stress

on cash flow, forcing additional reduction in business overheads if not offset by new business

growth.

This situation will create challenges for many SMEs in the region in the 2014-15 financial year

and beyond. SMEs which are highly dependent upon revenue from the regional resources

sector will be particularly affected. Owners and operators of any SMEs experiencing a

slowdown in revenue will need to adapt to survive and grow their business through

diversification.

Consultation with local business owners in Kalgoorlie highlighted an important issue in

managing slowdowns in the resources industry. While they may have to cut business

expenditure to survive, too much reduction in capacity would inhibit their ability to react to the

potential resurgence in business when commodity markets cycle upwards again. Therefore,

retention of staff during slower periods was a priority for many business owners.

Access to Finance, June 2015 P a g e | 7

Figure 3: Smoothed unemployment rates in LGAs with high employment in gold mining for the Goldfields/Esperance region31

The identification of new external markets outside of the region or new products/services for

inside the region will be fundamental to economic growth. Slower local market conditions can

also offer the opportunity for SMEs to invest time into developing new products, methods or

services which have been identified, but not acted upon because of the priority need to meet

the high levels of demand during the boom time.

SMEs Growing Through New Market Opportunities

A number of positive trends are also evident in the Western Australian economy. The

slowdown in the resources sector is easing some pressures on labour and input costs which can

provide an advantage to SMEs in other industries. New market opportunities are also

emerging in other areas, such as the knowledge sector, tourism, and agribusiness, which may

create opportunities for SMEs in Western Australia to grow.32

The latest survey of business expectations indicated the following positive trends for SME

business growth in Western Australia:33

Labour scarcity which constricted the growth of some SMEs during the resources boom

has eased making recruitment less difficult;

Staff retention has also become easier for SMEs;

0

2

4

6

8

10

12

14

Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14

Kalgoorlie/Boulder (C) Laverton (S) Leonora (S) Menzies (S) Ngaanyatjarraku (S)

Unemployment starts to rise as the gold price declinestarts in April/May 2013

Unemployment starts to plateau at 13 per cent

Access to Finance, June 2015 P a g e | 8

Wages costs have decreased;

Non-wages production input costs remained stable or eased in many sectors;

Business operating conditions generally improved, despite continued falls in sales

activity; and

Capital expenditure growth was more likely in the services sector than other industries.

Other signs of positive economic conditions in Western Australia include a 2.6 per cent

increase in lending activity in the six months to September 2014, and a 2.7 per cent increase

in building approvals in the quarter ending September 2014.34 This likely indicates that

growth is occurring in areas unaffected by shifts in the resources sector. Highest growth in

median sale prices over the 12 months to September 2014 occurred in the Busselton,

Mandurah-Murray, Albany, and Bunbury urban areas.

Access to finance was a top three issue for 16 per cent of businesses surveyed in Western

Australia.35 This indicates that some SMEs in Western Australia continue to need access to

funds to take advantage of growth opportunities, to develop greater capacity to respond to

changing markets, and to invest in innovation.

New market

opportunities are

emerging in regional

Western Australia

Tourism

Knowledge

Agri-business

Access to Finance, June 2015 P a g e | 9

Investigating Access to Finance

SMEs usually need access to capital funds or other sources of finance to enable growth to

occur. Research indicates that SMEs tend to use different sources of finance depending on the

needs of the business. The different business needs vary across the business lifetime and may

include:

Capital for business start-up;

Flexible access to finance for ongoing cash flow management;

Finance to enable the growth of business (i.e. to meet increased demand, to take advantage of new business opportunities, or to diversify into new markets);

Investment to enable development of the business and its workforce; and

Funds to enable survival of the business due to changes in internal or external business environments.36

While some businesses may simply not be a viable prospect for finance, economic growth is

impaired when good businesses are unable to access the finance they need for growth. There

is evidence that access to finance is mostly impaired for younger and smaller businesses, and

high growth businesses, which are all perceived to be a higher financial risk under post-GFC

assessment practices.37

While it is easy to measure the use of financial services, it is less easy to measure whether all

businesses have equal access.38 Some businesses are an unviable proposition for finance,

others may be excluded from access due to factors of market imbalance.39 Such imbalances

and gaps are hard to measure. Unsuccessful finance applications will not fully reflect levels of

exclusion, as barriers can also work as a deterrent to others, who may decide not to apply in

the first place.

The issue for regional businesses is whether their geographical location is a factor enabling or

inhibiting access to finance, or are barriers due to other factors such as type of industry, size

of business, financial literacy, or availability of documentation? Access to finance for SMEs is

especially important in Western Australia, due to the need to encourage economic growth and

diversify local and regional economies following the slowdown of the resources sector.

The growth of regional SMEs will be an important contributor to the long term expansion of

regional cities in Western Australia. This is important as Western Australia (like Queensland

and the Northern Territory) faces development challenges from a comparatively low density

of population across very large geographic areas. SMEs will also be essential to widening the

base of local economies in smaller settlements, particularly where those economies have a high

level of vulnerability to changes in external markets.

Access to Finance, June 2015 P a g e | 10

Types of Finance

Types of finance available to businesses for funding growth can be classified in three

categories: capital funding, grants funding and debt finance. Different types of funding within

these categories are available from different sources:

Capital funding exchanges a stake or share in the business for an injection of funds.

Investors received a share in business profits, and the capital investment is a tangible

asset that can be sold. Providers of capital funding may be informal (such as family or

friends) or through formal sources (e.g. angel investment, venture capital lenders,

investment banks, or securities exchanges).

Grants funding may be sourced from government or philanthropic sources. The funds

are tied to agreed terms and conditions, but do not create a debt to be repaid or

require any security. Grants are usually tied to a contractual set of obligations or

progress towards an agreed outcome.

Debt finance creates an obligation on the business to repay the amount of loaned

finance, plus an amount of interest and/or other fees and charges. Such finance

includes:

o Business loans from banks and other financial institutions for a fixed amount to

be repaid over a specified term. Such loans are often secured against other

assets (e.g. real estate or personal property) but may be unsecured or subject

to a guarantor arrangement (where another party agrees to pay the debt in

the case of default);

o Debt finance raised against unpaid invoices, which are used as a tradeable

asset for the business and can improve cash-flow;

o Lease agreements for equipment or vehicles through financial services or

vendor finance arrangements; and

o Flexible or ongoing debt-finance, such as trade or store accounts, credit cards,

or overdraft facilities.

Industries may vary in their use of the different types or sources of finance. The agriculture

industry, for example, would be likely to use debt finance secured against property, as land is

a core commodity in agriculture. In contrast, the mining industry tends to use equity finance

through joint ventures and funds raised in capital markets. Research and development,

particularly for medical, ICT, and technology industries, has a higher use of grant funding.

In 2013, the Australian small businesses most likely to have sought external finance were in the

agriculture, forestry and fishing industry and the transport and warehousing industry.40 The

small businesses least likely to have sought external finance were in the rental, hiring and real

estate industry and the retail trade industry.41

Access to Finance, June 2015 P a g e | 11

Access to Finance for Australian SMEs

Different surveys of business in Australia conducted in 2012 and 2013 reveal variable levels

of concern about access to finance; from 11 per cent 42 to 23 per cent of SMEs.43 In each case

access to finance was of more concern to those SMEs with existing plans for growth over the

next year.

Recent research in Australia indicates approximately half of all small businesses with turnover

of less than $5 million do not have access to any source of formal finance beyond a credit

card (Table 2).44 Furthermore, almost a third have no source of bank finance at all.45

The use of banking products is not homogenous across all types of industry. Research in

Australia indicates that agriculture, transport, mining and accommodation/food services are

the four highest users of financial products.46 The communications, health,

arts/culture/recreation, and education industries were the lowest users of financial products.47

As regional areas in Australia tend to be dominated by agricultural, mining and tourism

industries, this may mean that access to finance is even more important for growth in regional

economies. This is reflected in the data as small businesses in regional areas do have a higher

proportion of usage for financial services, with 78 per cent compared to 67 per cent in

metropolitan areas.48

Table 1 Estimated access to finance for small business in Australia

Finance type Estimated percentage of small businesses in

Australia using this product

Credit cards 51%

Lease finance 35%

Overdraft 28%

Long term loans 15%

Property mortgage 14%

Line of credit 9%

Data source: Australian Bankers Association and Council of Small Business Australia (2013)49

Access to Finance, June 2015 P a g e | 12

Factors Contributing to Access to Finance

Both macro and micro forces contribute to variable levels of access to finance. International

trends can include world economic factors, reduced supply or increased cost in wholesale

markets and changing perceptions of risk.

Macro factors also work at a national level of influence, including government economic

policies, and the level of competitiveness in the domestic banking environment. Lending

policies, business strategies and the use of new technology may also change the lending

environment within individual financial institutions. Different lending environments affect both

the funds available and the selection of customers who obtain access to them.

At the micro level, businesses vary in their level of viability for expansion, the potential risk for

non-return of investment, and financial literacy of the business owners. Some businesses are

simply not a viable option for investors, but overall economic growth is inhibited when viable

businesses cannot access the funds they need for expansion at a reasonable level of cost.

For SMEs in Western Australia, the macroeconomic forces associated with the resources

slowdown may increase perceptions of risk for lending funds to support SME expansion. This

comes at a time when regional SME expansion is most needed, particularly to diversify the

smaller or more resource-dependent regional economies. This could present a potential barrier

to regional development in Western Australia.

Changes in Supply and Demand

Lenders of finance are concerned with achieving the optimum return on funds loaned and the

relative level of risk involved in making the loan.50 When the demand for credit availability

exceeds the supply of funds available for loan, financial institutions will use interest rates,

collateral requirements, lending criteria and quantity restraints as a means of controlling the

flow of finance and limiting their level of exposure in the marketplace.51

International research by the Asian Development Bank and the OECD notes that ongoing gaps

between supply and demand for finance, particularly for SMEs, requires a broadening of the

finance model from traditional bank finance pathways to include non-banking sources of funds

and capital markets.52 53

International research also reveals that access to finance for business improves with a higher

level of competitiveness in the banking sector within a country.54 Places with a few very large

banks tended to have higher rates and more restrictive lending criteria, which worked to

restrict access to finance for smaller businesses.55

Access to Finance, June 2015 P a g e | 13

Risk Assessment and Lending Policies

Lending policies and practices of lending institutions shape access to finance. Risk assessment is

a necessary factor in containing the costs of finance. International research consistently finds

that the likelihood of obtaining finance increases for businesses with higher turnover, more

employees, and a longer history of operation.56 57 International research also finds that access

to finance is easier for those with substantial existing wealth in income and/or assets.58

Despite this, lending criteria and assessments of relative risk are not consistent across all banks

and lending institutions. Adverse selection occurs when these filtering processes inadvertently

reduce the number of low risk businesses and increase the number of high risk businesses in the

pool of potential loan recipients.59 In other words, groups of businesses or industries may be

disadvantaged if they are located in geographic spaces or industry sectors where banks

perceive it is harder to weed out the high risk applicants from low risk applicants.60

It is likely that this is occurring in regional and rural access to finance. Effectively, the thinner

markets and lower levels of data available on regions makes it harder for banks and lending

institutions to easily and fairly compare apples with apples. Comparisons to the denser

markets of metropolitan Perth would likely result in a negative assessment of SMEs in regional

Western Australia, simply due to the smaller size of markets in many regions and variations in

population density. Furthermore, SMEs in the remote and very remote regions of Western

Australia would face substantial disadvantage under such a system.

Such a system would require SMEs to work harder to bypass standard lending policy barriers

and assessment processes. They would need to engage directly with assessors to convince them

of the value and potential of their business and growth plans. It is likely that this process works

as a substantial disincentive to SMEs in many regional areas and industry sectors in Western

Australia from even applying for finance.

Essentially, the lack of available information on regional areas creates a market failure which

may need to be redressed through policy action to improve data availability on regional

areas. In this case, the public good created by enabling greater financial growth in regions

works to offset the cost of collecting more data to help potential lenders better understand the

potential that exists within regional markets for different industry types.

Financial Literacy

Education is a big factor in improving the chances of success in business, and this is recognised

by lenders. Studies in the USA indicate that people with a higher level of education tend to

have better communication and planning skills, which may contribute to higher success rates in

obtaining access to finance.61 These studies have found a strong, positive relationship between

education and entrepreneurship, where both the numbers of entrepreneurs and the level of

business success are higher.

Access to Finance, June 2015 P a g e | 14

Business planning is an important factor in successful identification of financial needs and in

successfully obtaining funds. Business plans provide a rational, verifiable case for growth

prospects for the SME. They provide financial institutions with insight into the strengths of the

business and detail how the growth of the business will be achieved. SMEs with better business

plans are more likely to be successful because they reduce the level of risk assessed by the

bank. SMEs with incomplete information are more likely to be assessed as being a higher risk

of default.

Financial literacy is also important as a demand generator as it improves awareness of

available sources of finance.62 SMEs need to educate themselves on the types of products

offered by different lenders and find the best match for their business needs. Yet, there is also

a role for government and the private sector in supporting the development of financial

literacy skills in regional areas, particularly through the expansion of business incubation and

start-ups support services which are mostly limited to the Perth metropolitan area at present.

Research in Australia reveals that while 68 per cent of SMEs surveyed in 2012 in Australia

had prepared a business plan, only 42 per cent did so on an annual basis.63 Businesses with

more employees were more likely to complete a formal business plan.64 This is identified as an

area needing improvement, as higher financial literacy is associated with better success in

business and in higher success rates for obtaining access to finance.

Reducing perceptions of risk improves access to finance and lowers the cost of lending

Business plans

Evidence on the business history

Evidence on the

market potential

Access to Finance, June 2015 P a g e | 15

Bank Lending

Small businesses in Australia overwhelmingly use bank finance rather than non-banking

sources. Research identifies that 90 per cent of all small business using finance only use bank

sources, three per cent only use non-bank sources, and seven per cent use a mix of non-bank

and bank sources for finance needs.65

Research in Australia is consistent with international findings which indicates a strong, positive

relationship between likelihood of obtaining finance and SME attributes, such as the size of

turnover, number of employees, and the length of time a business has been operating.66

Businesses which are bigger or older have a lower risk profile, due to their skills base,

established assets, and trading relationships. Effectively, this inhibits growth in regions, as new

or small businesses can be an important source of employment growth in regional communities.

Evidence presented to the Senate Economics References Committee 2010 Inquiry into Access of

Small Business to Finance stated that centralisation of lending processes by financial institutions

had led to circumstances where some regional branches were unable to assess or approve

loans, which was considered to be a substantial barrier in access to finance.67

While the final report of the Financial System Inquiry (FSI) did not detail issues of regional

finance, the interim report identified a number of factors that contributed to a differential

level of access to finance for SMEs in Australia compared to other users (i.e. large businesses

and personal finance applicants):

Costs of borrowing are usually higher for SMEs, reflecting asymmetric information

barriers and higher levels of risk;

High collateral requirements can lead to businesses with the best collateral getting

finance, rather than SMEs with better business prospects;

SMEs may bear an unfair level of burden from banking regulation, such as non-

monetary default clauses in loan contracts;

The $1 million loan threshold for defining retail (lower cost and regulation

requirements) from corporate loans (higher costs and banking regulation requirements)

acts as a disincentive for growth of SMEs; and

SMEs face substantial barriers in raising funds directly from capital markets. 68

However, neither the final nor the interim FSI report find any evidence of reductions in the

supply of funds potentially available for loan to SMEs from financial institutions.69 The FSI

noted that while the rural sector was certainly affected by other trends in access to finance,

there was no evidence of any significant issues related specifically to rural finance.70

The final report of the FSI did note the disadvantage to small business created by the

tightening of trade credit (wholesale money) markets in the post-GFC period.71 The FSI makes

a number of recommendations to improve access to finance for SMEs in Australia including:

Access to Finance, June 2015 P a g e | 16

The reform of regulation currently inhibiting small business from seeking finance for

start-ups and innovations through innovative sources of finance, particularly crowd-

funding;

The extension of unfair contract protections to include small business, preventing

discriminatory practices in loan contracts; and

Improved sharing of credit data and the use of personal credit history to inform

lending to reduce barriers for new business and smaller businesses. 72

Research by the Australian Bankers’ Association (ABA) indicates that issues regarding access to

finance affects 11 per cent of small businesses in Australia.73 There is some variation between

states, ranging from nine per cent of small businesses in South Australia/Northern Territory to

12 per cent in Queensland. In Western Australia, 90 per cent of small businesses stated that

access to finance or capacity to finance further growth was not an issue for the business

(Figure 4).

Figure 4: Variation in importance of access to finance by state or territory 74

0

1

2

3

4

5

6

7

8

NSW/ACT VIC/TAS QLD WA SA/NT

Perc

ent

ag

e

Access to Finance' or 'Capacity to Finance Further Growth in the Business' is one of the issues facing their business(Business has a loan)

Access to Finance' or 'Capacity to Finance Further Growth in the Business' is one of the issues facing theirbusinesse (Business has no loan, but may have credit card)

Access to Finance, June 2015 P a g e | 17

Interestingly, businesses with an existing loan were more likely to identify access to finance or

capacity to finance further growth in the business as a problem than businesses with no loan

(Figure 4). This pattern was consistent across all states and territories, but least variation

between the groups occurred in Western Australia. This may reflect the fact that some small

businesses may have capital reserves or cash flow sufficient to meet needs for growth. Some

small businesses may also have no plans for expansion, and therefore have no need for

additional finance.

There is a very small trend for access to finance to be less important for businesses in regional

areas compared to businesses in metropolitan areas (Figure 5). This is evident across all

categories of existing loan or credit card use. This may be related for the tendency for

agriculture to have better access to finance, and the dominance of agriculture for SMEs in

regional areas. Further exploration of this trend would be informative.

Figure 5: Variation in importance of access to finance for small businesses by existing credit use and location

0

2

4

6

8

10

12

14

Metropolitanbusinesses withexisting loans

Regionalbusinesses withexisting loans

Metropolitanbusinesses withcredit card only

Regionalbusinesses withcredit card only

Metropolitanbusinesses with no

credit card orloan

Regionalbusinesses with no

credit card orloan

Perc

ent

ag

e

Metropolitan businesses with existing loans Regional businesses with existing loans

Metropolitan businesses with credit card only Regional businesses with credit card only

Metropolitan businesses with no credit card or loan Regional businesses with no credit card or loan

Access to Finance, June 2015 P a g e | 18

Businesses with an existing loan were no more likely to identify access to finance or capacity

to finance further growth in the business as a problem than businesses with no loan in the

subset of data for small businesses in Western Australia (Figure 6). Data limitations prevented

analysis of this sub-set at a regional/metropolitan level.

Overall consideration of this data indicates no evidence of widespread disadvantage to

regional small business owners compared to metropolitan small business owners. However, this

data does not assess any impact of barriers preventing small business start-ups or assess any

factors contributing to the failure of businesses due to difficulties in accessing finance. It also

does not assess any difference between the accessibility of finance for businesses in large

regional centres compared to the accessibility for small businesses in small or remote regional

areas. Further research in each of these areas, incorporating new data collection or analysis

of non-publicly available data on current bank lending patterns, would likely prove to be

highly beneficial.

Literature searching of other international and Australian research suggests that factors such as

industry, age of business, size of business and access to collateral may be stronger factors

than simply a regional or metropolitan address. Still, further research is recommended in this

area to fully resolve this issue, particularly given the relatively recent changes in technology,

banking practices and global economic conditions, which may be impacting upon access to

finance and capacity of small business to achieve growth.

Figure 6: Variation in importance of access to finance for small businesses by existing credit use for businesses in Western Australia

0

10

20

30

40

50

60

70

80

90

100

WA businesses with existingloans

WA businesses with credit cardonly

WA businesses with no creditcard or loan

Perc

ent

ag

e

'Access to Finance' or 'Capacity to Finance Further Growth in the Business' is one of the issuesfacing their business

'Access to Finance' or 'Capacity to Finance Further Growth in the Business' is NOT one of theissues facing their business

Access to Finance, June 2015 P a g e | 19

The ABA has provided the RAI with additional detail on their previously published research, to

help identify the differences between metropolitan and regional small businesses use of

finance. This data is drawn from DBM Consultancy surveys of over 20,000 businesses in

Australia.75

1. Use of business lending products by small businesses is higher in regional areas compared to metropolitan areas.

When credit cards are included, 78 per cent of regional small businesses have a business

lending product, but this drops to 62 per cent when credit cards are excluded from

consideration (Figure 7). This reflects the number of SMEs whose credit card is their only

financial product. Only 22 per cent of all small businesses in regional Australia do not

have any lending product, compared to 33 per cent of metropolitan small businesses.

Figure 7: Comparison of metropolitan and regional small business use of business lending products 76

0

10

20

30

40

50

60

70

80

90

Uses a business lendingproduct, including use of

credit cards

Uses a business lendingproduct, not including use

of credit cards

Does not use businesslending product at all

Does not use a businesslending product other

than a credit card

Perc

ent

ag

e

Metropolitan small businesses in Australia Regional small businesses in Australia

All small businesses in Australia

Access to Finance, June 2015 P a g e | 20

2. Small businesses in regional areas are more likely to have a bigger loan than small businesses in metropolitan areas.

Small businesses in regional areas have a higher proportion of loans in every category

from $50,000 upwards (Figure 8). This pattern is consistent for small businesses with and

without credit cards being included for consideration.

Figure 8: Comparison of metropolitan and regional small business amount of loan 77

0

5

10

15

20

25

More than$0 butunder

$10,000

$10,000 toless than$50,000

$50,000 toless than

$100,000

$100,000to less than$500,000

$500,000to less than

$1M

$1M to lessthan $2M

$2M to lessthan $5M

$5M ormore

Perc

ent

ag

e

Loan amount

Metropolitan small businesses (incl credit card) Regional small businesses (incl credit card)

Metropolitan small businesses (no credit card) Regional small businesses (no credit card)

All small businesses in Australia (incl credit card) All small businesses in Australia (no credit card)

Access to Finance, June 2015 P a g e | 21

3. There are few differences between small businesses in regional areas compared to metropolitan areas for the amount of loan outstanding.

Regional areas have a higher proportion of loan outstanding values in only three out of

eight categories (Figure 9). As indicated in the preceding graphs, regional small businesses

do have a higher proportion of activity in each category of loan above $50,000, but this

does not translate into corresponding levels of outstanding debt. This could reflect

variations in rates of repayment or longer timelines since loan establishment (i.e. older

loans tend to have more of the capital amount repaid).

In contrast, regional small businesses also have twice the level of representation in the

$5 million or more outstanding debt category compared to metropolitan small businesses.

This level of difference is greater than Figure 8 previously, where rates of participation in

this category were equal. This indicates that regional small businesses may be slower to

repay very high loans or that these loans are more recently established with little capital

reduction.

Figure 9: Comparison of metropolitan and regional small business amount of loan outstanding

0

5

10

15

20

25

30

35

More than$0 butunder

$10,000

$10,000 toless than$50,000

$50,000 toless than

$100,000

$100,000to less than$500,000

$500,000to less than

$1M

$1M to lessthan $2M

$2M to lessthan $5M

$5M ormore

Perc

ent

ag

e

Loan outstanding

Metropolitan small businesses (incl credit card) Regional small businesses (incl credit card)

Metropolitan small businesses (no credit card) Regional small businesses (no credit card)

All small businesses in Australia (incl credit card) All small businesses in Australia (no credit card)

Access to Finance, June 2015 P a g e | 22

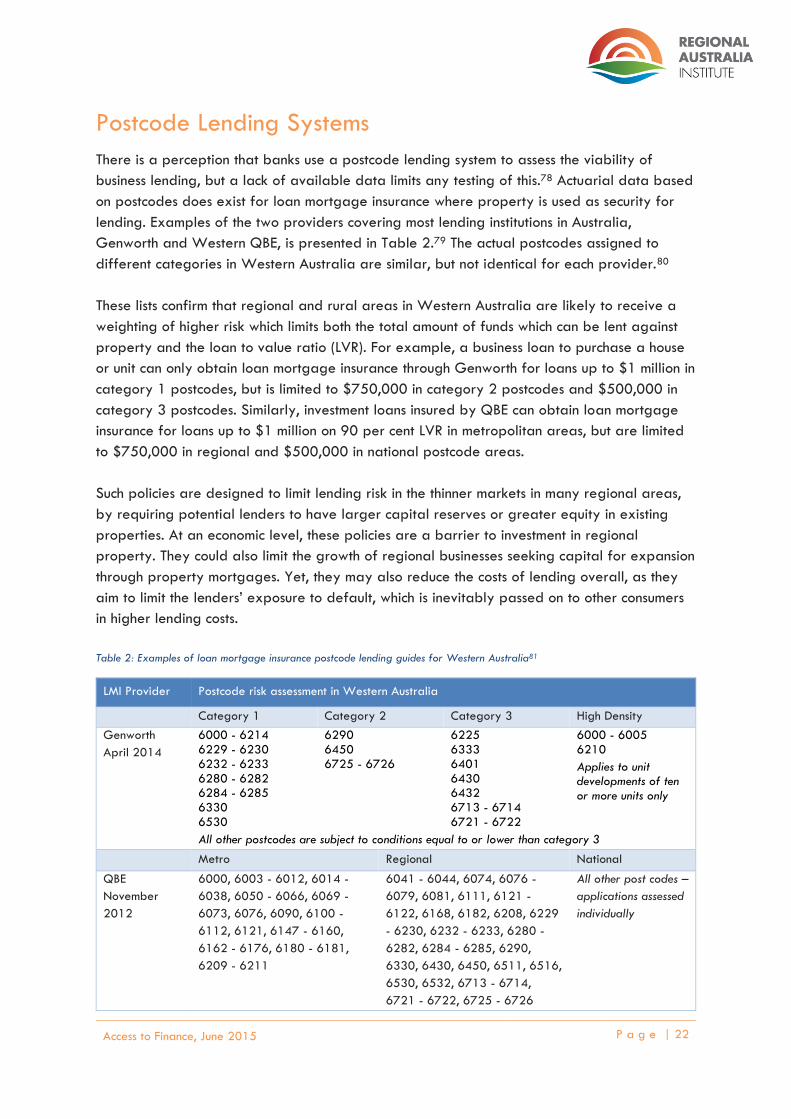

Postcode Lending Systems

There is a perception that banks use a postcode lending system to assess the viability of

business lending, but a lack of available data limits any testing of this.78 Actuarial data based

on postcodes does exist for loan mortgage insurance where property is used as security for

lending. Examples of the two providers covering most lending institutions in Australia,

Genworth and Western QBE, is presented in Table 2.79 The actual postcodes assigned to

different categories in Western Australia are similar, but not identical for each provider.80

These lists confirm that regional and rural areas in Western Australia are likely to receive a

weighting of higher risk which limits both the total amount of funds which can be lent against

property and the loan to value ratio (LVR). For example, a business loan to purchase a house

or unit can only obtain loan mortgage insurance through Genworth for loans up to $1 million in

category 1 postcodes, but is limited to $750,000 in category 2 postcodes and $500,000 in

category 3 postcodes. Similarly, investment loans insured by QBE can obtain loan mortgage

insurance for loans up to $1 million on 90 per cent LVR in metropolitan areas, but are limited

to $750,000 in regional and $500,000 in national postcode areas.

Such policies are designed to limit lending risk in the thinner markets in many regional areas,

by requiring potential lenders to have larger capital reserves or greater equity in existing

properties. At an economic level, these policies are a barrier to investment in regional

property. They could also limit the growth of regional businesses seeking capital for expansion

through property mortgages. Yet, they may also reduce the costs of lending overall, as they

aim to limit the lenders’ exposure to default, which is inevitably passed on to other consumers

in higher lending costs.

Table 2: Examples of loan mortgage insurance postcode lending guides for Western Australia81

LMI Provider Postcode risk assessment in Western Australia

Category 1 Category 2 Category 3 High Density

Genworth

April 2014

6000 - 6214 6229 - 6230 6232 - 6233 6280 - 6282 6284 - 6285 6330 6530

6290 6450 6725 - 6726

6225 6333 6401 6430 6432 6713 - 6714 6721 - 6722

6000 - 6005 6210

Applies to unit developments of ten or more units only

All other postcodes are subject to conditions equal to or lower than category 3

Metro Regional National

QBE

November

2012

6000, 6003 - 6012, 6014 -

6038, 6050 - 6066, 6069 -

6073, 6076, 6090, 6100 -

6112, 6121, 6147 - 6160,

6162 - 6176, 6180 - 6181,

6209 - 6211

6041 - 6044, 6074, 6076 -

6079, 6081, 6111, 6121 -

6122, 6168, 6182, 6208, 6229

- 6230, 6232 - 6233, 6280 -

6282, 6284 - 6285, 6290,

6330, 6430, 6450, 6511, 6516,

6530, 6532, 6713 - 6714,

6721 - 6722, 6725 - 6726

All other post codes –

applications assessed

individually

Access to Finance, June 2015 P a g e | 23

Proximity to Financial Institutions

Access to banking and financial services using local branches was historically important for

improving competitiveness and meeting the service needs of residential and business

populations. Many rural and regional communities reported substantial negative impacts on

communities and business due to the closure of bank branches, which reached a peak with

14 per cent of all regional bank branches in Australia closing between 1993 and 1996.82

The number of financial institutions in a local government area (LGA) is now closely associated

with population density in regional Western Australia, with a high positive correlation of 0.89.

The greatest concentrations of financial institutions occur in the highly populated regional

service centres of Bunbury, Mandurah, Geraldton, Busselton, Kalgoorlie-Boulder and Albany

(Figure 10).

Figure 10: Number of financial institutions and usual resident population in regional Western Australia in 2011 83

-5

0

5

10

15

20

25

30

35

0 10000 20000 30000 40000 50000 60000 70000 80000

Num

ber

of

fina

ncia

l in

stitut

ions

in

LGA

Population

Bunbury

Greater GeraldtonMandurah

Busselton

Kalgoorlie/Boulder

Albany

HarveyEsperanceChittering

RoebourneMurray

Serpentine-Jarrahdale

Access to Finance, June 2015 P a g e | 24

Proximity to financial institutions has essentially become a proxy measure for the density and

complexity of the local economy, rather than an effective measure of access to finance. The

presence of financial institutions is relevant to competitiveness because it is an indicator of

when a location has reached the level of economic development that makes it commercially

viable to support one or a number of banks or other financial institutions.

Technological improvements have substantially changed the delivery of banking and financial

services, and this will require new means of measurement. Telephone and internet-based

banking and lending services are now commonplace across the industry. Accordingly, the

regional marketplace is no longer restricted to the big four banks and small, local credit

unions.

Technology offers the means to lessen the effect of spatial proximity as a driver of business

growth in regional communities. Yet, it may also be that other service providers, such as

Australia Post and Bendigo Bank mobile services, have moved in at a local level to meet the

need for financial services provision in regional communities.

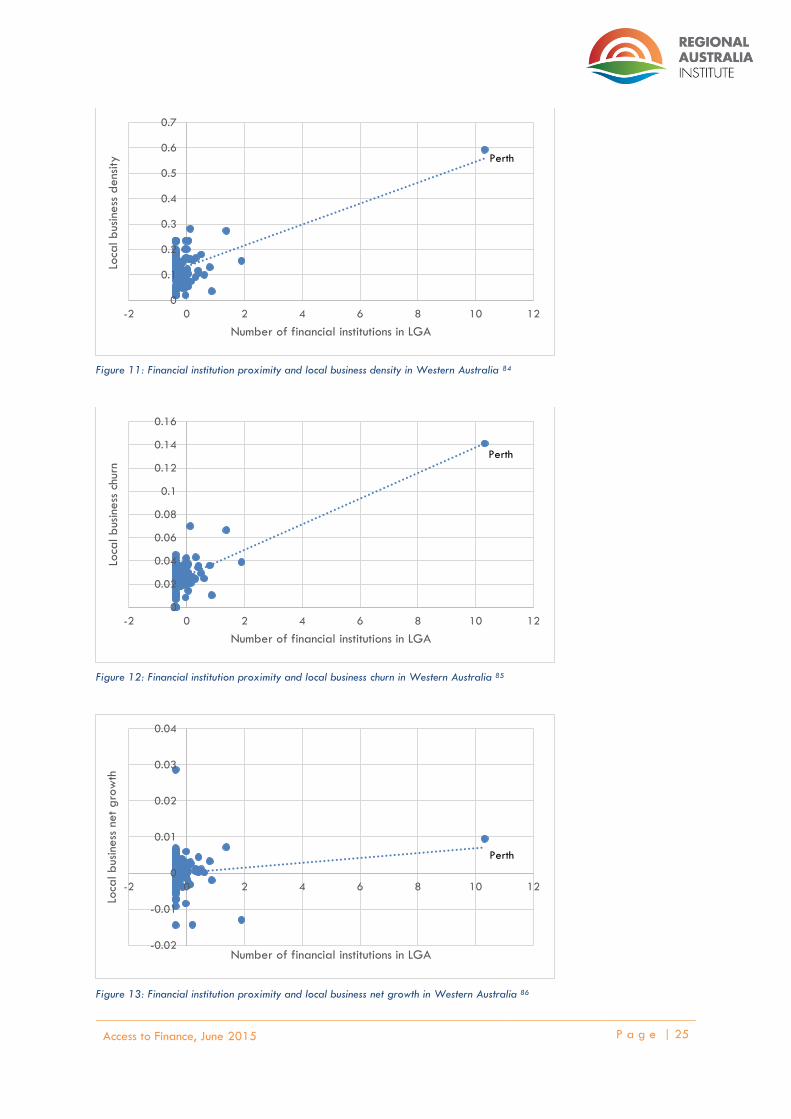

Analysis of all LGAs in Western Australia reveals a strongly Perth-centric pattern in access to

financial institutions. This reflects the high population density in the State capital, but also the

general trend for financial services to congregate within a central business district location.

At the whole of State comparison, there is a moderate positive correlation (0.56) between

access to financial institutions and local business density. There is also a high positive

correlation (0.73) between access to financial institutions and the rate of local business churn

(entries plus exits) which indicates a high degree of mobility in the local business market. In

contrast, there is only a slight correlation (0.14) between access to financial institutions and net

local business growth.

The reason for these figures is evident in scatter analysis, where it is clear that the heavy

concentration of financial institutions and local businesses in the City of Perth LGA is creating a

very strong outlier effect which drags the trend line in an upward direction (Figures 11 to 13).

This means that these trends reflect factors of population density rather than business growth,

as population is strongly associated with the distribution of financial institutions. When

population is controlled for, there is little to no evidence of a relationship between the density

of financial institutions and growth in local business. This tells us that regional businesses do not

necessary need to be in close proximity to a financial institution premises to obtain services.

Access to Finance, June 2015 P a g e | 25

Figure 11: Financial institution proximity and local business density in Western Australia 84

Figure 12: Financial institution proximity and local business churn in Western Australia 85

Figure 13: Financial institution proximity and local business net growth in Western Australia 86

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

-2 0 2 4 6 8 10 12

Loca

l b

usin

ess

dens

ity

Number of financial institutions in LGA

Perth

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

-2 0 2 4 6 8 10 12

Loca

l b

usin

ess

chu

rn

Number of financial institutions in LGA

Perth

-0.02

-0.01

0

0.01

0.02

0.03

0.04

-2 0 2 4 6 8 10 12

Loca

l b

usin

ess

net g

row

th

Number of financial institutions in LGA

Perth

Access to Finance, June 2015 P a g e | 26

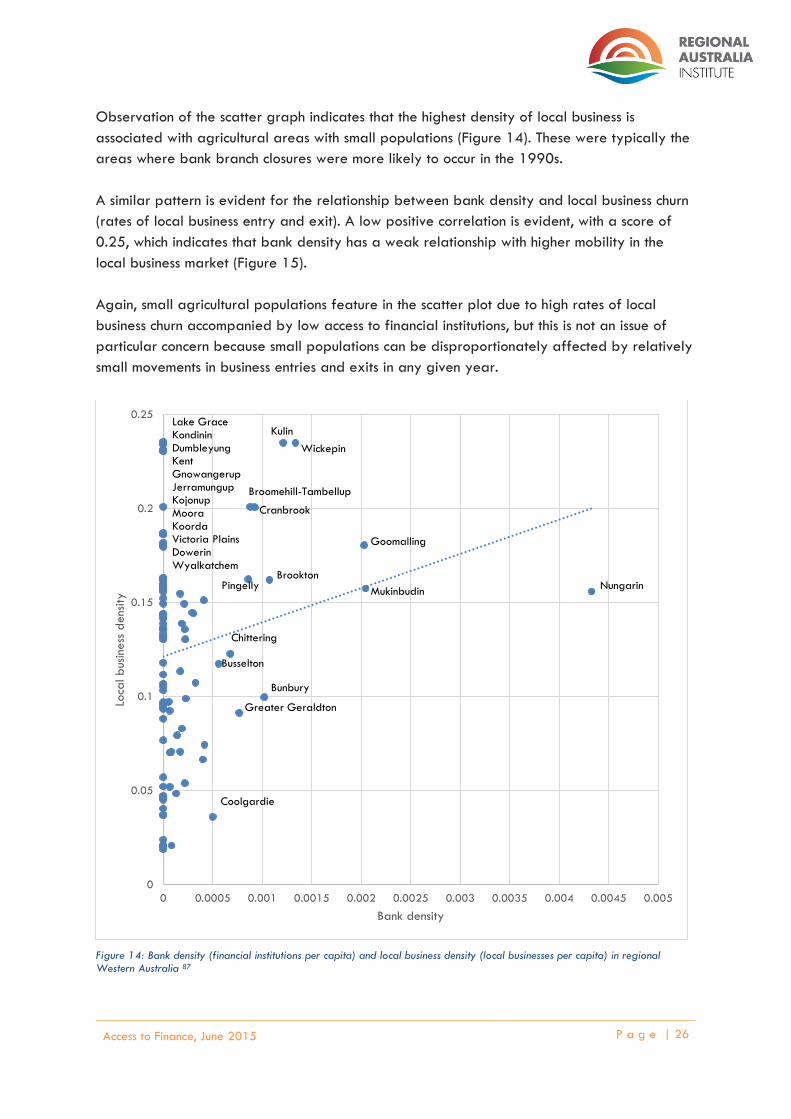

Observation of the scatter graph indicates that the highest density of local business is

associated with agricultural areas with small populations (Figure 14). These were typically the

areas where bank branch closures were more likely to occur in the 1990s.

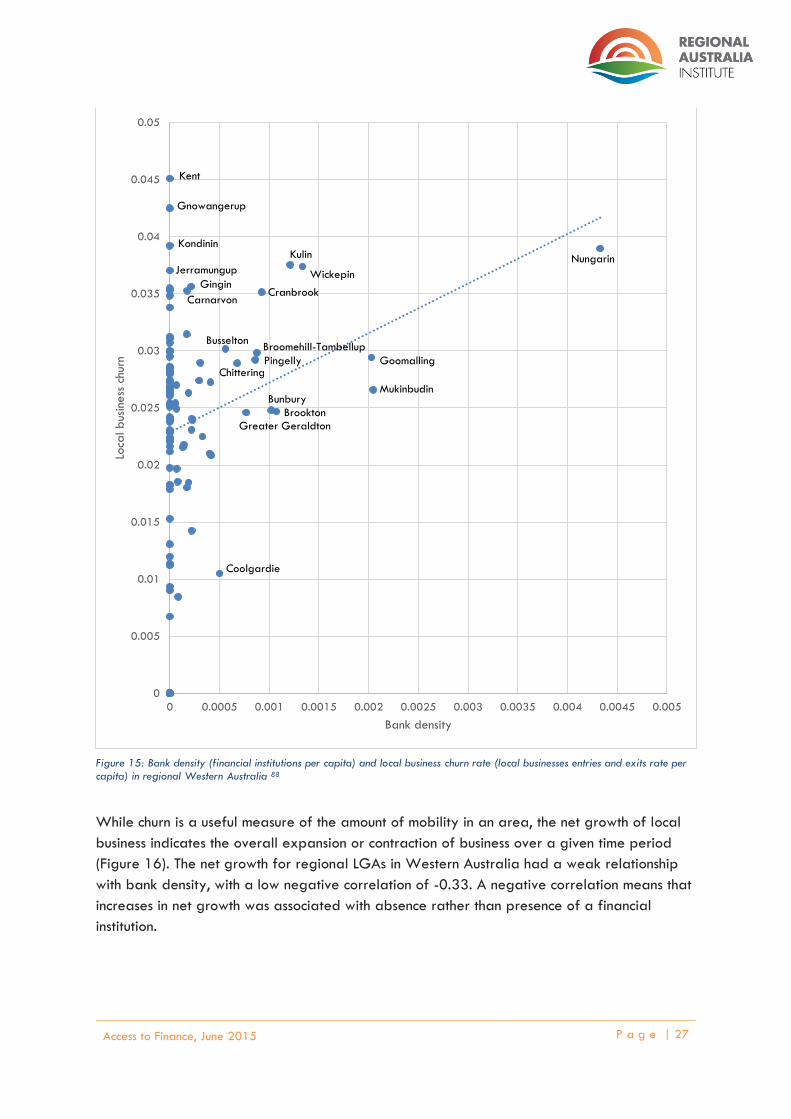

A similar pattern is evident for the relationship between bank density and local business churn

(rates of local business entry and exit). A low positive correlation is evident, with a score of

0.25, which indicates that bank density has a weak relationship with higher mobility in the

local business market (Figure 15).

Again, small agricultural populations feature in the scatter plot due to high rates of local

business churn accompanied by low access to financial institutions, but this is not an issue of

particular concern because small populations can be disproportionately affected by relatively

small movements in business entries and exits in any given year.

Figure 14: Bank density (financial institutions per capita) and local business density (local businesses per capita) in regional Western Australia 87

0

0.05

0.1

0.15

0.2

0.25

0 0.0005 0.001 0.0015 0.002 0.0025 0.003 0.0035 0.004 0.0045 0.005

Loca

l b

usin

ess

dens

ity

Bank density

Lake GraceKondininDumbleyungKentGnowangerupJerramungupKojonupMooraKoordaVictoria PlainsDowerinWyalkatchem

Kulin

Wickepin

Broomehill-Tambellup

Cranbrook

Goomalling

PingellyBrookton

MukinbudinNungarin

Chittering

Busselton

Bunbury

Greater Geraldton

Coolgardie

Access to Finance, June 2015 P a g e | 27

Figure 15: Bank density (financial institutions per capita) and local business churn rate (local businesses entries and exits rate per capita) in regional Western Australia 88

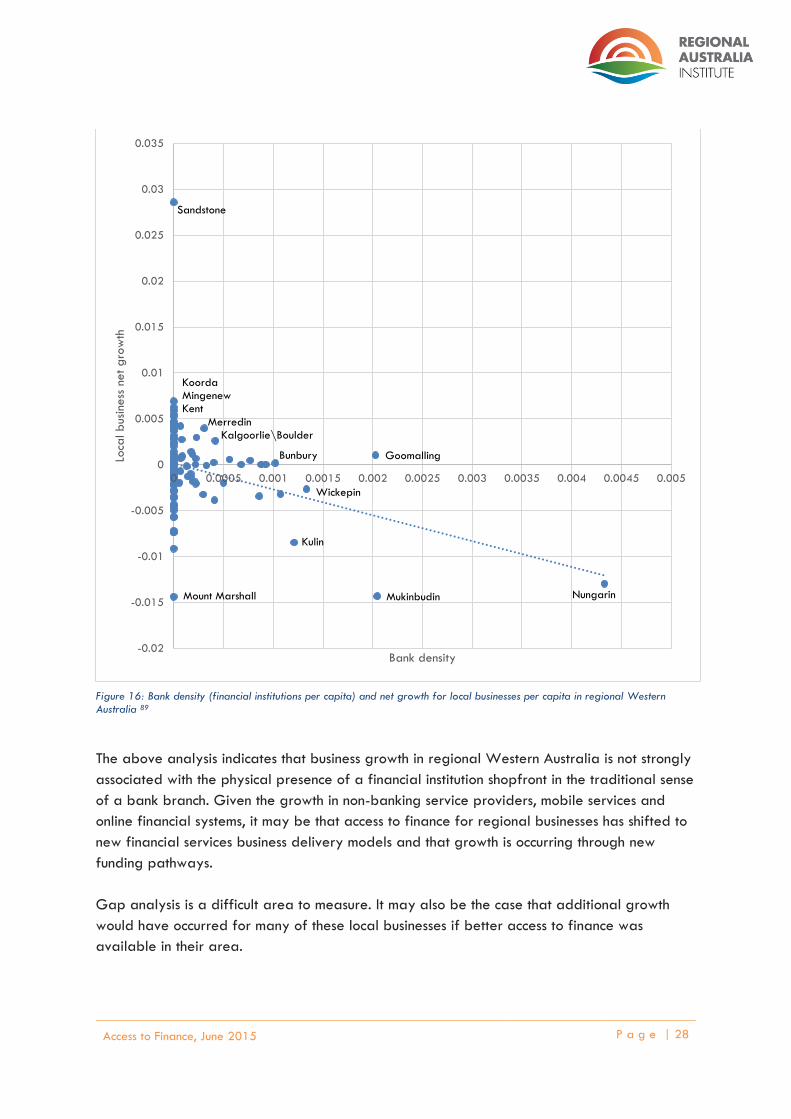

While churn is a useful measure of the amount of mobility in an area, the net growth of local

business indicates the overall expansion or contraction of business over a given time period

(Figure 16). The net growth for regional LGAs in Western Australia had a weak relationship

with bank density, with a low negative correlation of -0.33. A negative correlation means that

increases in net growth was associated with absence rather than presence of a financial

institution.

0

0.005

0.01

0.015

0.02

0.025

0.03

0.035

0.04

0.045

0.05

0 0.0005 0.001 0.0015 0.002 0.0025 0.003 0.0035 0.004 0.0045 0.005

Loca

l b

usin

ess

chu

rn

Bank density

Kent

Gnowangerup

Kondinin

Jerramungup

Gingin

CarnarvonCranbrook

Wickepin

Kulin Nungarin

BusseltonBroomehill-Tambellup

PingellyChittering

Goomalling

Mukinbudin

Brookton

Bunbury

Greater Geraldton

Coolgardie

Access to Finance, June 2015 P a g e | 28

Figure 16: Bank density (financial institutions per capita) and net growth for local businesses per capita in regional Western Australia 89

The above analysis indicates that business growth in regional Western Australia is not strongly

associated with the physical presence of a financial institution shopfront in the traditional sense

of a bank branch. Given the growth in non-banking service providers, mobile services and

online financial systems, it may be that access to finance for regional businesses has shifted to

new financial services business delivery models and that growth is occurring through new

funding pathways.

Gap analysis is a difficult area to measure. It may also be the case that additional growth

would have occurred for many of these local businesses if better access to finance was

available in their area.

-0.02

-0.015

-0.01

-0.005

0

0.005

0.01

0.015

0.02

0.025

0.03

0.035

0 0.0005 0.001 0.0015 0.002 0.0025 0.003 0.0035 0.004 0.0045 0.005

Loca

l b

usin

ess

net g

row

th

Bank density

Sandstone

KoordaMingenewKent

MerredinKalgoorlie\Boulder

GoomallingBunbury

Wickepin

Kulin

Mount Marshall Mukinbudin Nungarin

Access to Finance, June 2015 P a g e | 29

Importance of the Business Relationship

Evidence in Australia suggests that business relationships with financial institutions are seen as

more important by micro businesses and small businesses than for medium and large

businesses.90 Yet, less than two per cent of the 984 businesses in one recent research sample

indicated that they attended a branch for consultations regarding loans or other financial

products and services.91

A fundamental shift has occurred towards the use of online banking facilities by both business

and individuals in Australia. Tools such as internet banking and electronic payment transfers,

such as PAYPAL and EFTPOS systems, have almost completely displaced the petty cash and

business chequebook systems of the past. The growth of electronic banking systems have been

used as a rationale for the reduction in need for the high street bank branches that used to

feature in every small town in Australia.

Yet, this created a gap in the market as effective lending practices still required a business

relationship between the customer and the lending institution to enable effective assessment of

every application that did not fit the pro forma profile of the perfect applicant. This has seen

many banks steadily reduce their frontline business staff and lose a share of the lending

market to the small, community banks with micro branches and networks of mobile lenders who

have stepped in to meet the continuing demand from SMEs.

Relationships between lenders and business are important and productive. International

research indicates that relationship banking increases the competitive advantage of small

businesses access to finance, providing both a higher success rate for applications and

reduced costs for the borrower (e.g. waived or reduced fees and lower interest rates).92 The

greater local knowledge and networks available to community based banks are associated

with successful finance relationships with small business.93 In recognition of this, some banks in

Australia are now pursuing an expansion strategy to redress this situation.94

The establishment and rapid growth of the Bendigo Bank is testament to the value of business

and personal banking markets in regional Australia. The following case study examines the

role of Bendigo Bank as a provider of financial services to SMEs in regional Western

Australia.

Access to Finance, June 2015 P a g e | 30

Case Study 1: Bendigo Bank and Mobile Lending in

Regional Areas

Bendigo Bank established its Community Bank program in 1998. This program was initiated in

response to the closure of 29 per cent of Australia’s bank branches by other banks between

1993 and 2000. These closures left many regional businesses and communities without access

to any branch banking facilities.

Bendigo Bank with its affiliates, the Community Bank and the Rural Bank, offer banking to those

in regional Australia, with products and services specific to the needs of individuals and

businesses in these areas.95 A Community Bank is a locally owned and operated company

which functions as a franchise of Bendigo Bank.96 It is set up by local communities to meet their

needs and helps keep local capital in the region, but is supported by the Bendigo Bank

infrastructure and services systems.

The Rural Bank is a fully owned subsidiary of Bendigo Bank and provides specialist banking

services to regional Australia from assistance for large agribusinesses to personal money

management for small rural producers and SMEs.97 Products and services offered through

Rural Bank are easy to access through affiliate relationships with Elders Rural Services

agencies. In Western Australia, the Bendigo Bank operates predominantly in regional areas

(Figure 17).

Figure 17: Bendigo Bank regional presence98

Bendigo Bank at a Glance

Bendigo Bank in Australia:

Is a top 60 listed company on the Australian Stock Exchange;

Has over 90,000 shareholders; and

Has 1.5 million customers.

In Western Australia:

Bendigo Bank has 54 affiliated branches, including 40 Community Bank Branches in

regional Western Australia;

53 per cent of the 302 staff in Western Australia operate in regional areas; and

From 1999 to 2015 the Community Bank Branches in Western Australia have

invested $15.7 million back into their local communities.

Access to Finance, June 2015 P a g e | 31

Benefits for SMEs

Bendigo Bank’s expansion was enabled by the gap in the market for regional specific banking

and business options resulting from the withdrawal of the ‘big four’ banks99 from regional

Australia. Bendigo Bank and its affiliates are driven by a philosophy of active engagement

with regional communities, as well as offering financial services for businesses in regional

areas. This increases commercial confidence and facilitates local economic development.

Banks that are run by locals or that have a specific focus on regional Australia allow for

specialised understanding of the needs of and issues facing local business. They also have a

greater flexibility to offer tailor-made programs and solutions. These factors both facilitate

access to finance for regional SMEs.

Financial products can also be developed that better meet the needs of regional SMEs. For

example, long-term and short-term financing options that consider the often unpredictable and

cyclic nature of regional life. Such options allow regional businesses to forward plan, enable

growth and have the flexibility to adapt to short term changes in external markets. The

development of a more responsive financial system aims to improve the understanding of

regional businesses to achieve long term sustainability and help grow more economically

stable communities.

The Rural Bank specifically aims to develop a more nuanced and detailed understanding of

regional businesses through its Relationship Managers. These are people with farming

expertise who can visit their clients on site to enhance their understanding of each particular

business. This allows the bank to more accurately assess the merits and risks of each business

and offer access to services that better meet individual business needs and capacity.

Relationship banking helps to reduce the risk profile for the lender, but also improves

knowledge spillover as the Relationship Manager builds a network through the local

community, potentially creating more opportunities for economic growth. Furthermore, this

knowledge spillover supports the growth of local knowledge by providing access to external

expertise in Bendigo Bank, and, in turn, informs the Bank’s understanding of regional financial

needs.

Access to Finance, June 2015 P a g e | 32

Non-Bank Lending