Embed Size (px)

Citation preview

Access to Financeand Economic Growthin Egypt

Access to

Finan

ce and

Econ

om

ic Gro

wth

in Eg

ypt

Middle East and North African Region

A Study Led By SAHAR NASR

A S

tud

y L

ed

By

SA

HA

R N

AS

R

This publication provides a comprehensive and informative analysis of a key policy issue facing Egypt and other developing countries-how to enhance appropriate access to finance in support of sustained

high economic growth and improved income distribution. The detailed and elegant evaluations of the key segments of the financial sector are supplemented by a holistic discussion that draws out the maininteractions, including the linkages to institutional reforms. The timely publication will be interest to a large number of policy makers, academics, development practitioners and financial market participants.”

Dr. Mohamed A. El-Erian, President and CEO of the Harvard Management Company, member of the faculty of the Harvard Business School, and Deputy Treasurer of Harvard University

Broadening the reach of the financial sector is the key to invigorating both economy and society. Ifmore small businesses can get access to the credit and other financial services they need to turn

initiative into employment and profitability, and if low income households can gain the economic securityoffered by an account at an intermediary, economic growth and social welfare will both be enhanced. This report takes a close look at the Egyptian financial system to see how outreach and access can beimproved. It is firmly based on recently collected statistics and it provides a comprehensive analysis withrecommendations. Recent government initiatives have already begun to transform the Egyptian financialsystem. Access to Finance and Growth in Egypt points the way to future success in lifting the system to the next level.”

Dr. Patrick Honohan, Senior Advisor, World Bank; and Professor of International Financial Economics and Development, Trinity College Dublin

Financial exclusion is likely to act as a “brake” on development as it retards economic growth and increases poverty and inequality. However, the access dimension of financial development has

often been overlooked, mostly because of serious data gaps on who has access to which financial services. Hence, empirical evidence that links broader access to financial services to outcomes has been verylimited, providing at best tentative guidance for public policy initiatives in this area. However, without inclusive financial systems, poor individuals and small enterprises need to rely on their personal wealthor internal resources to invest in their education, become entrepreneurs or take advantage of promising growth opportunities. Financial market imperfections—such s information and transactions costs—are likely to be especially binding on the talented poor and the micro and small enterprises, who lack collateral and credit histories.”

Asli Demirguc-Kunt, Senior Research Manager, Finance and Private Sector Development, Development Research Group (DECRG), World Bank

For Egypt, access to finance can radically transform peoples’ lives, promote entrepreneurship,help bridge the urban-rural income divide, alleviate poverty and improve individuals’ lifetime

economic and social prospects by integrating them into the market economy. In short, improved access to finance can be an engine of growth and structural transformation, if supported by other policies thatreduce barriers to competition, lower the cost of doing business and create incentives for moving out of the ‘informal sector’. For Egypt, where fewer than seven percent of households have a bank account, investments and policies that create and improve access to finance and its infrastructure, can breakdown economic and social barriers to economic growth and development. This well-researched report is an excellent guide and provides a practical tool-kit for economic and financial policy makers, banks andfinancial institutions seeking to improve Egypt’s financial infrastructure and access to finance.”

Dr. Nasser Saidi, Chief EconomistDubai International Financial Centre (DIFC)

“

“

“

“

41305

Introduction i

Access to Financeand Economic Growthin Egypt

Access to Finance and Economic Growth in Egyptii

Introduction iii

Access to Financeand Economic Growthin Egypt

Middle East and North African Region

A Study Led By SAHAR NASR

Access to Finance and Economic Growth in Egyptiv

Introduction v

Abbreviations and Acronyms viii

Foreword ix

Preface xi

Acknowledgments xiii

Executive Summary xvii

I. Introduction 1

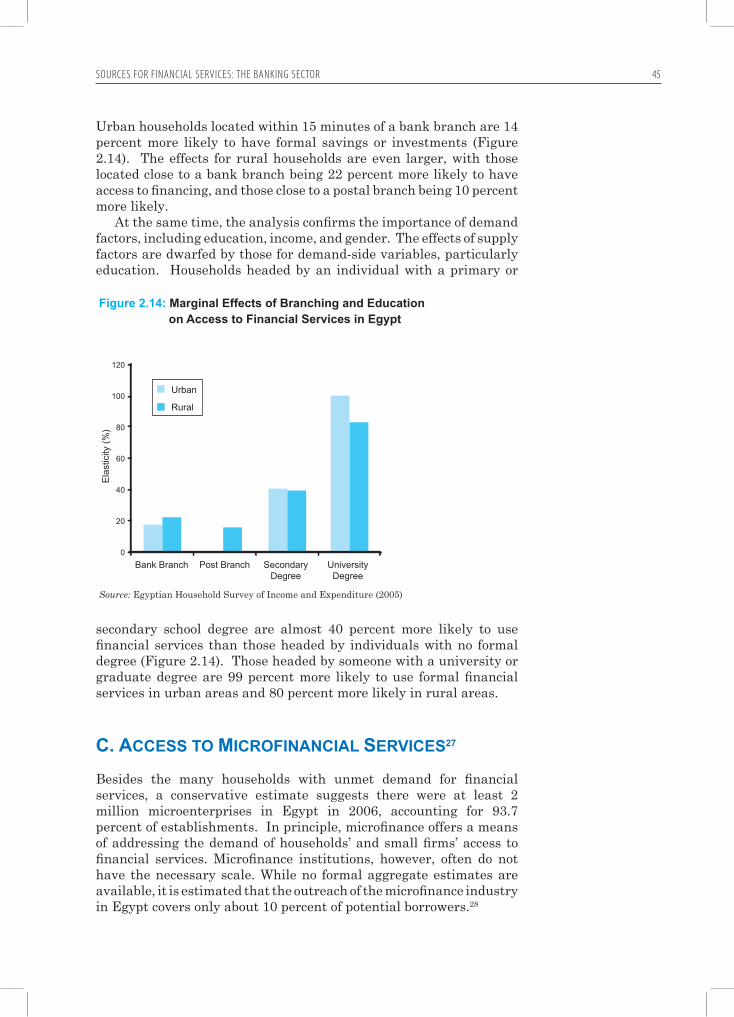

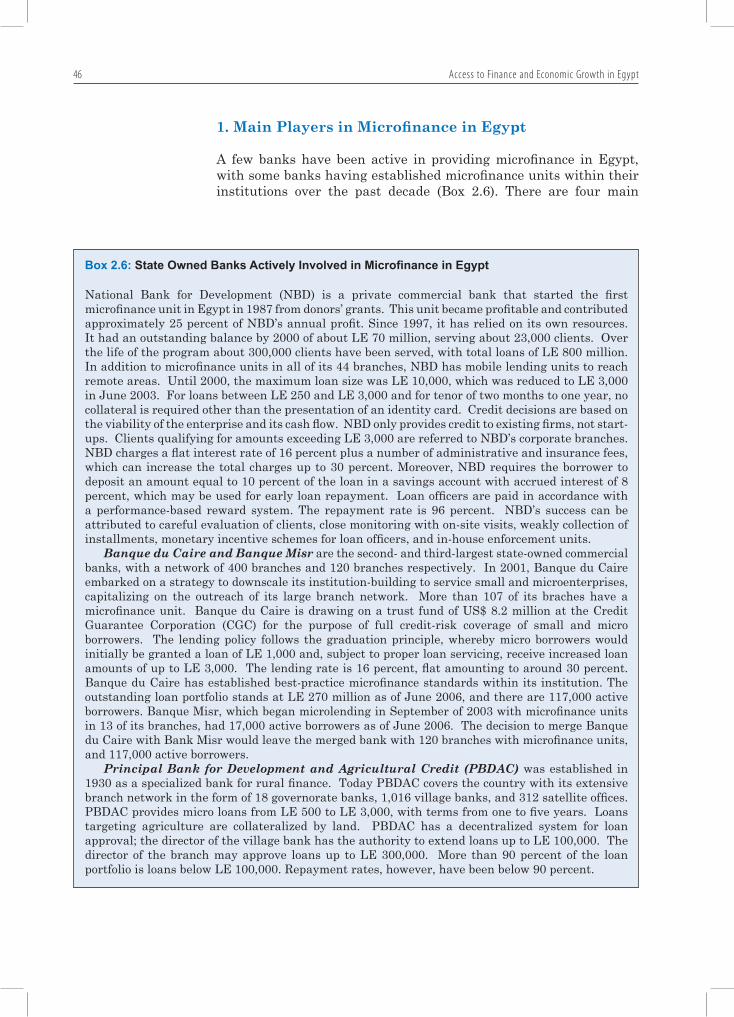

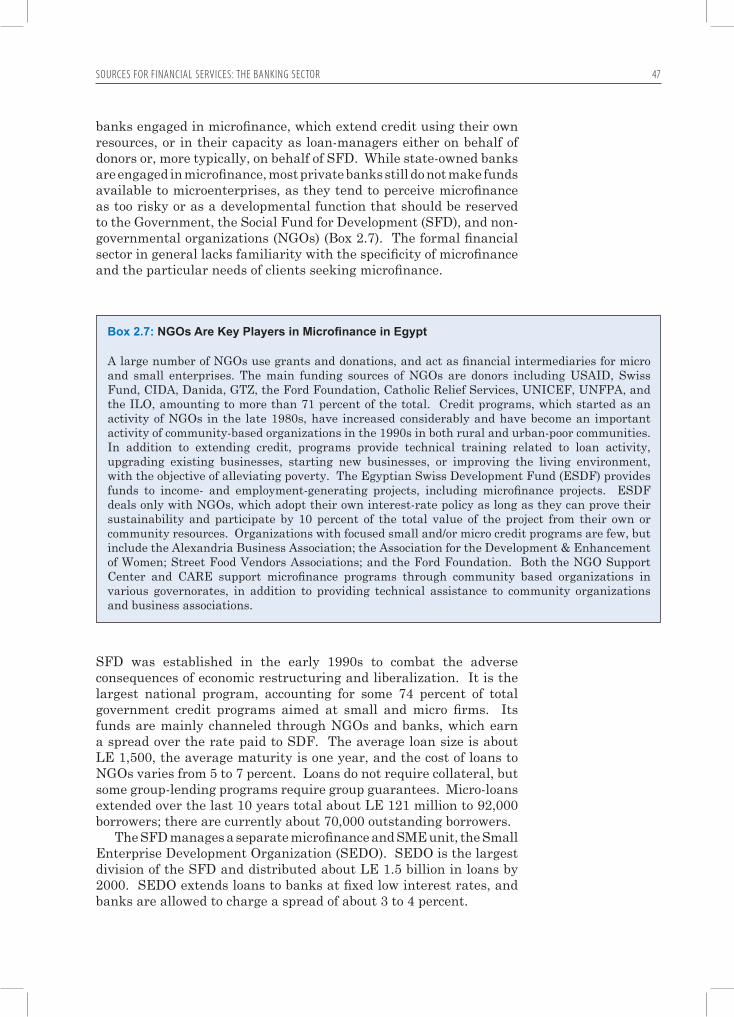

II. Sources for Financial Services: The Banking Sector 23A. Access to Bank Financial Services 23B. Factors behind Weaknesses in Supply of Banking Services 28C. Access to Microfinancial Services 45

III. Sources for Financial Services: Non-bank Financial Services 55A. Capital Markets 55B. Insurance and Contractual Savings 61C. Mortgage Finance 68D. Financial Leasing 73E. Factoring 76

IV. Institutional Environment 81A. Legal Framework 81B. Information Infrastructure–Credit Registry, Credit Bureau and Other Sources 86C. Financial Reporting Environment 89D. Financial Infrastructure 91

V.Expanding Access to Finance 95A. Enhancing the Role of the Banking Sector in Financial Intermediation 95B. Expanding the Postal System and Microfinance Institutions 101C. Promoting Capital Markets in the Access Agenda 105D. Contractual Savings Industry Potentials for Growth 107E. Developing the Mortgage Finance Market 113F. Increasing the Financial Leasing Industry’s Contributions to Access 115G. Developing the Factoring Industry 116H. Improving the Institutional Environment 117

Annexes 130Annex 1: Indicators For Assessing The Soundness And Performance 130 Of The Banking System Annex 2: Indicators For Assessing The Capital Market 135Annex 3: Indicators For Assessing The Insurance And Contractual Savings Sector 136

Bibliography 137

Contents

Access to Finance and Economic Growth in Egyptvi

Tables

Table 1.1: Main Macroeconomic Indicators in Egypt (2001-2006) 7Table 1.2: Business Environment in Egypt 9Table 1.3: Various Sources of Finance in Egypt, MENA, and the World 15Table 1.4: Household Use of Financial Services by Education Level in Egypt 17Table 1.5: Use of Finance by Employment Status of Head of Household in Egypt 18Table 2.1: Frequency Distribution of Private Sector Credit in Egypt 25Table 2.2: Share of Savings Accounts by Size of Deposits in Banks in Egypt 27Table 2.3: Local Currency Deposit Interest Rates in Egypt 27Table 2.4: Number of Credit and Debit Cards Issued in Egypt during 2005 28Table 2.5: Branching and ATM Presence, Cross-Country Comparisons 30Table 2.6: Earnings per Employee of Banks in Egypt 37Table 2.7: Expense Ratio of Banks in Egypt 37Table 2.8: Main Reasons for not Lending to SMEs in Egypt 40Table 2.9: Lending Rates for Local Currency of Banks Operating in Egypt 41Table 3.1: Compound Annual Growth Rate by Sub-Sector in Egypt 62Table 3.2: Statutory Investment Limits—Life Insurers in Egypt 63Table 3.3: Assets and Investments in Egypt 63Table 3.4: Insurance Investment Allocation in Egypt 65Table 3.5: Private Pension Investment Allocation in Egypt 66Table 3.6: Investment Approach of the Contractual Savings Industry 66Table 4.1: History of Public Credit Registry Database in Egypt 86Table 4.2: Negative Databases of CBE Credit Registry 87

Figures

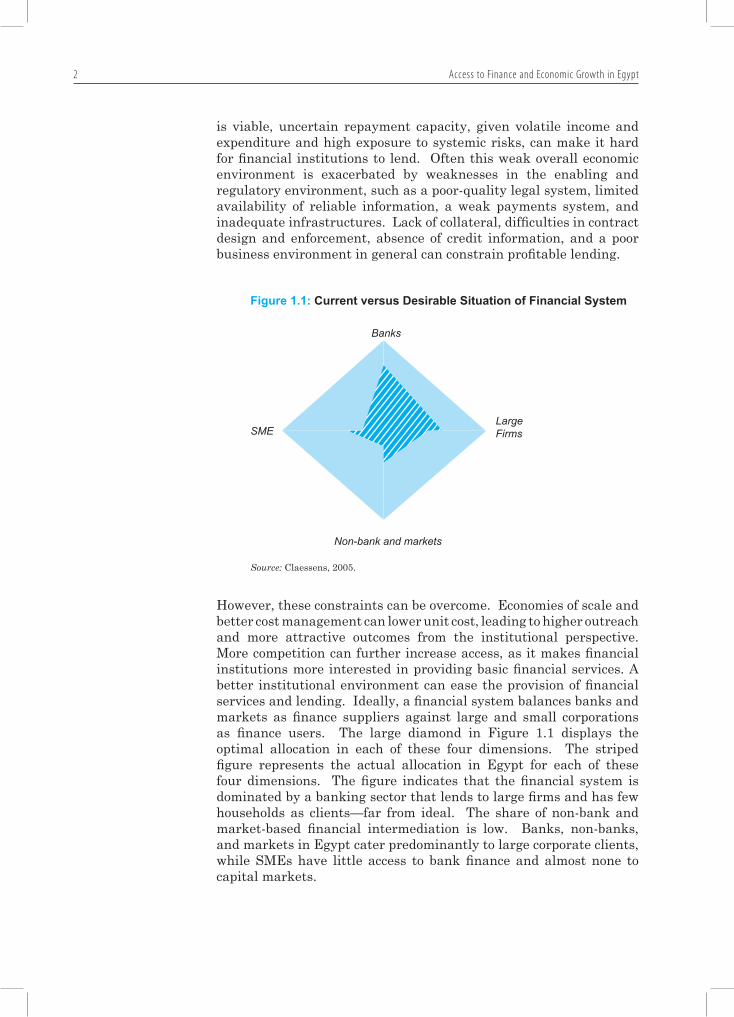

Figure 1.1: Current versus Desirable Situation of Financial System 2Figure 1.2: M2-to-GDP in Selected Countries across the World 8Figure 1.3: Private Sector Credit-to-GDP in Selected Emerging Economies 9Figure 1.4: Investment Climate Constraints in Egypt as Perceived by Businesses 15Figure 1.5: Percentage of Firms Currently with a Loan from a Financial Institution in Egypt 16Figure 1.6: Enterprises’ Access to Finance in Egypt and Selected MENA Countries 16Figure 1.7: Households’ Share in Access to Financial Services by Educational Attainment in Egypt 18Figure 2.1: Loans-to-Deposits Ratio in Egypt 24Figure 2.2: Loan-to-Deposit Ratio in Egypt 24Figure 2.3: Treasury Bills-to-Total Assets in Egypt 24Figure 2.4: Government Sector Loans-to-Total Loans in Egypt 25Figure 2.5: State-Owned Enterprises Loans-to-Total Loans in Egypt 25Figure 2.6: Credit Extended to Private Sector in Egypt 26Figure 2.7: State-Owned Banks’ Share of the Banking System Total Assets in Egypt 29Figure 2.8: Urban and Rural Branch Density by Bank Type in Egypt 31Figure 2.9: Equity-to-Assets Ratio of Banks in Egypt 33Figure 2.10: Distribution of Staff in the Egyptian Banking System 38Figure 2.11: Return on Assets of Egyptian Banks 39Figure 2.12: Return on Equity of Egyptian Banks 39Figure 2.13: Collateral Requirements as a Percent of Loan Values 41Figure 2.14: Marginal Effects of Branching and Education on Access to Financial Services in Egypt 45

Contents

Introduction vii

Figure 3.1: Equity Finance and Corporate Bonds as Sources of Investment Funding in Selected Emerging Economies 56Figure 3.2: Assessment of Enforcement in Egypt’s Capital Markets 60Figure 3.3: State-Owned Insurers’ Share of Insurance Assets in Egypt 63Figure 3.4: Funds under Management: Egypt and OECD 65Figure 3.5: Developments in Mortgage Loans in Egypt 71Figure 3.6: Volume and Number of Leasing Contracts in Egypt 74Figure 4.1: Legal Rights of Creditors in Egypt and Other Countries 82Figure 4.2: Cost to Create Collateral in Egypt and Other Countries 83Figure 4.3: Bankruptcy Costs and Time in Egypt, MENA Region and OECD 84Figure 4.4: Dominance of Collateral-Based Lending in Egypt 85Figure 5.1: Funds Build Up Under Five Percent Mandatory Pillar Option 111

Boxes

Box 1.1: Access to Finance as an Obstacle to Growth 5Box 1.2: Rationales for the Privatization of Banks 12Box 1.3: Egyptian Women’s Access to Finance 19Box 2.1: Egypt Post Offices 32Box 2.2: Status of Islamic Finance in Egypt 34Box 2.3: Bank Performance Analysis by Size and Ownership 35Box 2.4: Weaknesses in Corporate Governance in Egyptian State-Owned Banks 42Box 2.5: The Relative Importance of Demand and Supply Factors in Explaining Access 43Box 2.6: State-Owned Banks Actively Involved in Microfinance in Egypt 46Box 2.7: NGOs are Key Players in Microfinance in Egypt 47Box 3.1: Major Insurance and Pensions Investors in Egypt 67Box 3.2: The Government of Egypt’s Housing Finance Program for the Poor 69Box 3.3: The Egyptian Mortgage Refinance Company 70Box 4.1: Current Status of the Private Credit Bureau in Egypt 88Box 4.2: The Importance of Good Financial Reporting for Firm Financing 89Box 5.1: Lessons on Bank Restructuring from Other Countries 96Box 5.2: Subsidized Lending Schemes in Egypt 100Box 5.3: Lessons from Successful Postal Financial Systems: Case Studies from Brazil and China 102Box 5.4: International Evidence on Institutional Policies to Enhance Access 104

Contents

Access to Finance and Economic Growth in Egyptviii

ABBREVIATIONS AND ACRONYMS

ABS Asset-Backed SecuritiesAIM Alternative Investment MarketALM Asset and Liability ManagementAML/CTF Anti Money Laundering and Combating Terrorism FinancingATM Automatic Teller MachinesAUM Assets Under ManagementBRU Bank Restructuring UnitCAGR Compound Annual Growth RateCAPMAS Central Agency for Public Mobilization and StatisticsCASE Cairo and Alexandria Stock ExchangesCBE Central Bank of EgyptCCMAU Crown Company Monitoring Advisory UnitCFD Corporate Finance DivisionCGAP Consultative Group to Assist the PoorestCGC Credit Guarantee CompanyCIB Commercial International BankCIBOR Cairo Interbank Offer RateCIS Cooperative Insurance Society for Small EnterprisesCMA Capital Market AuthorityDB Defined BenefitsDC Defined ContributionEAB Egyptian American BankEAS Egyptian Accounting StandardsEEGC Egyptian Export Guarantee CompanyEFG Egyptian Financial GroupEISA Egyptian Insurance Supervisory AuthorityEMRC Egyptian Mortgage Refinance CompanyESDF Egyptian Swiss Development FundFCI Factors Chain InternationalFIRST Financial Sector Strengthening InitiativeFSAP Financial Sector Assessment ProgramFSS Financial Self-SufficiencyGAFI General Authority for Free Zones and InvestmentGATS General Agreement on Trade in ServicesGCC Gulf Cooperation CouncilGDP Gross Domestic ProductGDR Global Depository ReceiptGEM Gender Entrepreneurship MarketsGSF Guarantee and Subsidy FundHH HouseholdIAS International Accounting StandardsICA Investment Climate AssessmentICS Investment Climate SurveyICT Information and Communications TechnologiesIFG International Factoring Group

IFRS International Financial Reporting StandardsIFI Islamic Financial InstitutionsIFS Islamic Financial ServicesIIC Islamic Investment CompaniesIPOs Initial Public OfferingsKOSDAQ Korea Securities Dealers Automated QuotationLE Egyptian PoundM2 Broad MoneyMCSD Misr Clearing, Settlement and Central Depository CompanyMENA Middle East and North AfricaMFA Mortgage Finance AuthorityMFIs Microfinance InstitutionsMIB Misr International BankMIX Microfinance Information ExchangeMTPL Mandatory InsuranceNBFI Non-bank Financial institutionsNBD National Bank for DevelopmentNBE National Bank of EgyptNGO Non-governmental organizationNIB National Investment BankNPL Non-performing loansNPS National Payments SystemNSGB National Societe Generale BankOECD Organization for Economic Co-operation and DevelopmentOTC Over the counterPBDAC Principal Bank for Development and Agricultural CreditPML Primary mortgage lendingPSB Postal Savings BureauR&D Research and developmentRELC (Non-bank) real estate lending companies Repo Repurchase operationsROA Return on assetsROE Return on equityROSC-AA Report on Observance of Standards and Codes Accounting and AuditingRTGS Real-time gross settlementSEDO Small Enterprise Development OrganizationSFD Social Fund for DevelopmentSIF Social Insurance FundSME Small and Medium EnterpriseSOE State-Owned EnterprisesSRC Social Research CenterSRO Self-regulatory organizationTSX Toronto Stock ExchangeUS$ U.S. DollarsWBES World Business Environment SurveyWFE World Federation of Exchanges

Introduction ixContents

This report was initiated at the request of the Egyptian Government to get a better understanding of why, as found by the Investment Climate Assessment, only 17.4 percent of Egyptian firms operate inthe formal credit market. The report draws on surveys of firms, banksand households to determine why so few firms—and households—useformal financial markets for their investment and saving needs, andwhy banks and other financial institutions are reluctant to extendcredit, even in conditions of high liquidity.

The key findings are that: (i) significant public ownership of realand financial assets in Egypt has discouraged competition and thedevelopment of deep and well-regulated financial systems, includingnon-bank sources of financial services; (ii) a large fiscal deficit hasencouraged financial institutions, particularly publicly owned ones,to invest predominantly in risk and tax free government securities; banks, and publicly owned ones in particular, have little incentive to lend to other than state-owned enterprises and large private firms; and (iii) smaller private and foreign banks are more active inexpanding access to financial services by households and small andmedium enterprises (SMEs) due to their capacity to better assess risk and capture opportunities.

Improving access to financial services will require continuing theshift in the role of the government in the sector—away from asset ownership and towards creating an enabling environment for private (including foreign) financial service providers to innovate in providingservices to firms and households. Here, as the report indicates,the government has a critical role to play in ensuring a stable macroeconomic environment, lower deficit and public borrowing, goodsupervisory oversight, and adequate institutional infrastructure. A number of the issues raised in this report are already being addressed by the government under the financial sector reform program initiatedin November 2004.

The objective of this report is help the government with the design of the second generation of financial reforms aimed at increasing therole of the private sector in financial services provision, particularlyto SMEs and households, while strengthening risk management in financial institutions.

Foreword

Michael U. KleinVice President and Chief EconomistFinancial & Private Sector DevelopmentInternational Finance CorporationThe World Bank Group

Zoubida AllaouaSector ManagerFinance and Private Sector DevelopmentSocial and Economic Development GroupMiddle East and North Africa RegionThe World Bank

Emmanuel MbiDirectorEgypt, Yemen and Djibouti Country DepartmentThe World Bank

Access to Finance and Economic Growth in Egyptx

Introduction xi

In September 2004, the Financial Sector Reform Program was launched and endorsed by the Government of Egypt at the highest political level. The five pillars of the program are reforming the banking sector, restructuringthe insurance sector, deepening the capital markets, developing a well-functioning mortgage market, and activating other non-bank financialinstitutions and services. The program aims at improving the soundness of the financial sector and promoting an enabling environment for anefficient, competitive and agile financial system that serves Egypt’sdevelopment and growth objectives.

The Egyptian government and the Central Bank of Egypt have been keen on the effective implementation of this program, and significantprogress has already been made. Important achievements include, the turn around of the structure of the banking sector and the foreign exchange market as well as establishing a credible monetary policy framework, in addition to consolidating the banking sector, divestiture of the state-owned banks’ shares in the joint-venture banks, privatizing one of the four largest public banks, pursuing the restructuring of the remaining public financial intermediaries and building the supervisory capacity ofthe Central Bank.

Meanwhile, major reforms aiming at improving the regulatory framework and enhancing the soundness and effectiveness in financial intermediationof non-bank financial services, have been undertaken. These reforms havecontributed to the deepening of the capital market and enhancing its efficiencyand liquidity, restructuring and liberalizing the insurance sector, developing the mortgage market, and reviving the role of other non-bank financialservices and instruments, including leasing, factoring and securitization. This comprehensive reform program has been underpinned by capacity building of the supervisory authorities of all non-bank financial institutions.

The progress and pace of the Egyptian Financial Sector Reform Program have been commended at home and abroad. However, we are aware that we still have some way to go to fully reform the sector and address its main challenges; one of which is ensuring better access to financial services whichis imperative to economic growth and development. Improving access to finance allows businesses, especially small and medium enterprises, tocapitalize on their growth potential, operate on a larger scale and turn initiatives and ideas into employment opportunities. Moreover better and wider access to financial services by households at all income levelspositively impacts their economic and social welfare

The Government of Egypt will continue to foster efforts on facilitating access to financeinEgypt.Wehopethatthefindingsandrecommendationsofthis report would assist in the ongoing endeavors to meet this challenge.

Preface

Mahmoud MohieldinMinister of InvestmentMinistry of InvestmentEgypt

Farouk El OkdaGovernorCentral Bank of EgyptEgypt

Access to Finance and Economic Growth in Egyptxii

Introduction xiii

The Access to Finance and Growth in Egypt is a joint product of the Government of Egypt and the World Bank. The study was initiated by the Minister of Investment, H.E. Dr. Mahmoud Mohieldin, as a follow up to the Investment Climate Assessment, which had identified accessto finance as a main constraint to private-sector development; and H.E.Dr. Farouk El-Okda, Governor of the Central Bank of Egypt (CBE). This study was carried out under the joint leadership of Emmanuel Mbi, Country Director, and Zoubida Allaoua, Sector Manager in the Middle East and North Africa Region (MENA) of the World Bank. The study was led by Sahar Nasr, Senior Financial Economist in MENA, based on input from Stijn Claessens, Senior Adviser; Rodney Lester, Program Director, Financial Markets for Social Safety Net; David Scott, Adviser; Loïc Chiquier, Head, Housing Finance Practice; JaeHoon Yoo, Senior Securities Market Specialist; Robert J. Cull, Senior Economist; Luc Laeven, Senior Financial Economist from the Finance and Private Sector Development Vice Presidency; and Mohamed Yehia Abd El Karim, Financial Management Specialist; as well as Heba El Laithy, Senior Consultant; Bahaa Ali Eldin, Senior Legal Consultant; and Esen Ulgenerek, Consultant.

This access to finance study is based on the findings of five mainsurveys: the Investment Climate Survey (ICS) of 1,052 enterprises from the manufacturing sector that was carried out between October 7 and December 10, 2004 using the World Bank standard methodology; the ICS recall questionnaire of 300 enterprises that was carried out in June 2005; the individual banks survey undertaken between February and March 2006, supported by CBE, based on the core questionnaire provided by Asli Demirguc-Kunt, Senior Research Manager at the World Bank, to which 35 out of 45 banks operating in Egypt responded; the insurance survey, carried out under the leadership of the Ministry of Investment in March 2006 and to which 20 out of 21 insurance companies responded; and the National Household and Income Survey for the fiscal year 2005, which covered48,000 households in 1,500 communities. The first three surveys werecarried out by the Social Research Center (SRC) of the American University in Cairo, under the leadership of Dr. Hoda Rashad, and

Acknowledgments

Access to Finance and Economic Growth in Egyptxiv

coordinated by Dr. Ramadan Hamed; the fifth was undertaken bythe Central Agency for Public Mobilization and Statistics (CAPMAS) under the Ministry of State for Economic Development.

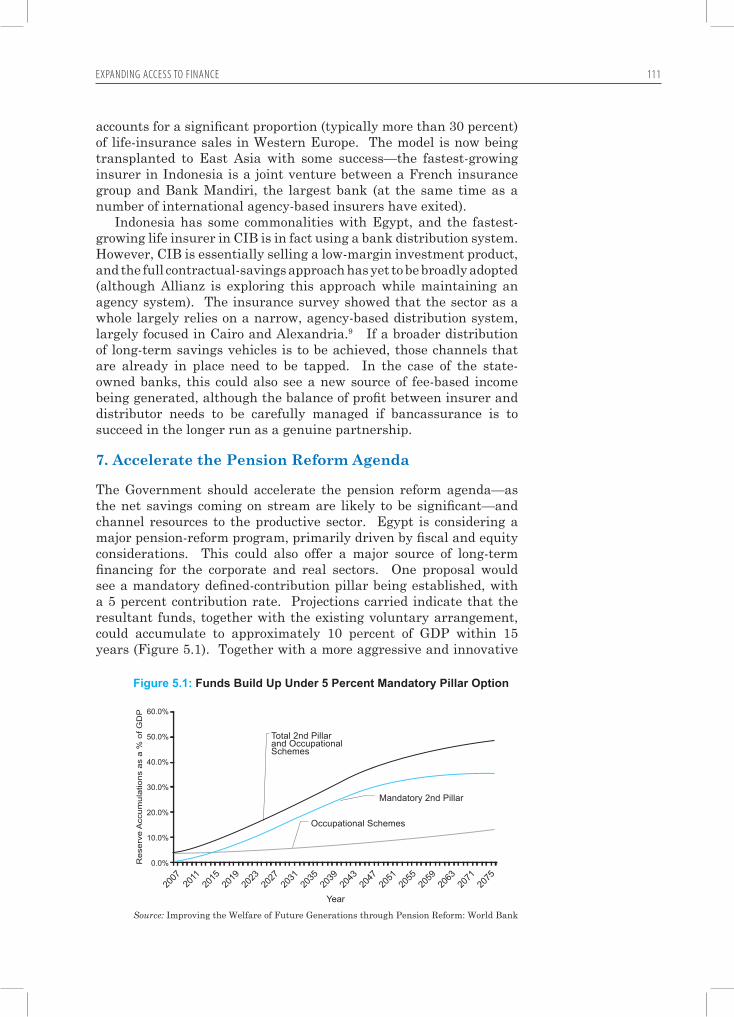

The development of the report entailed discussions with key policy makers and government counterparts, including, Tarek Amer, Deputy Governor; Tarek Kandil, Sub-Governor; Lobna Hilal, Assistant Sub-Governor; Mona Bassiouni, Assistant Sub-Governor; and Gamal Nigm, Assistant Sub-Governor. Valuable comments were received from Maged Shawki, Chairman of Cairo and Alexandria Stock Exchange (CASE); Hany Sarie El Din, Chairman of Capital Market Authority (CMA); Mahmoud Abdullah, Chairman of Egyptian Insurance Holding Company; Osama Saleh, Chairman of Mortgage Finance Authority (MFA); Ashraf El Kadi, Deputy Chairman of MFA; and Ziad Bahaa El Din, Chairman of General Authority for Investment and Free Zones (GAFI); as well as Abdel Hamid Ibrahim, Senior Advisor; Mona Zobaa, Advisor; and Ahmed Rostom, Economist in the Ministry of Investment.

Strong support was provided all along for the missions and various consultations during the preparation of this work. The team would like to thank in particular the Ministry of State for Economic Development; Ministry of Finance; Ministry of Foreign Trade and Industry; Social Fund for Development (SFD); Economic Research Forum (ERF); EFG Hermes; Syndicate of Commerce; Federation of Egyptian Industries; Egyptian Center for Economic Studies (ECES); Egyptian Businessmen Association; Institute of Banking and Finance; Misr Clearing, Settlement and Depository Company (MCSD); Egyptian Postal Authority; and Egyptian Society of Accountants and Auditors. Feedback was also provided by the private-sector community in a roundtable organized by the American Chamber of Commerce in Egypt coordinated by Hisham Fahmy, Executive Director. Partners who are actively involved in the financial sectorin Egypt, including USAID, European Commission (EU), and United Nations Development Program (UNDP), have made significantcontribution to this study.

Thoughtful comments from several World Bank colleagues and external reviewers are reflected in this study. The study benefitedimmensely from intensive reviews by Patrick Honohan, Senior Adviser; in addition to external reviewers Mohamed El Erian, President and CEO of Harvard Management Company; and Nasser Saidi, Director of Hawkamah Institute for Corporate Governance. Comments and contributions from several World Bank colleagues on an earlier draft have also been provided by Noritaka Akamatsu, Roberto Rocha and Ahmed Galal. The study also benefited from comments received fromGaiv Tata, S. Ramachandran, and Omer Karasapan. Valuable support was received from Marilou Jane D. Uy. World Bank, International Finance Corporation (IFC) and FIRST Initiative staff contributed to this study, including notably Bikki Randhawa; Carmen Niethammer; Isabella Segni; Jim Aziz, Jose Antonio Garcia Luna; Massimo

Acknowledgments

Introduction xv

Cirasino; Murat Sultanov; Peer Stein; Peter Sheerin; Robert Keppler; and Thomas Jacobs. Laila Abdel Kader provided extensive support with document preparation. Amira Fouad Zaky, Steve W. Wan Yan Lun, and Sydnella E. Kpundeh provided invaluable logistical support throughout the process. Editorial support was provided by Laura Goodin and print production including book design was undertaken by Magdy Nassif.

Early versions of this study have been presented and discussed at seminars and workshops in Cairo and Washington in which different stakeholders participated, including bank and non-bank financialinstitutions, private sector, civil society, donor agencies, academia, government officials, and the supervisory and regulatory bodies.Valuable comments received from these participants are reflected inthis final version. We would like to take this opportunity to thank allthe people in government, financial, donor, and academic communitieswho have provided their time, thoughts, and contributions to the team and to the study.

Acknowledgments

Access to Finance and Economic Growth in Egyptxvi

Introduction xvii

Access to finance is important for growth and economic development.Having an efficient financial system that can deliver essential servicescan make a huge contribution to a country’s economic development. Greater financial development increases growth, reduces economicvolatility, creates job opportunities and improves income distribution, as has been established by a large empirical literature. A well-functioning financial market plays a critical role in channeling fundsto their most productive uses, and allocates risks to those who can best bear them.

Getting the financial systems of developing countries to functionmore effectively in providing the full range of financial services isa task that will be well rewarded with economic growth. Where macroeconomic environment is sound, the efficient and prudentallocations of resources by the financial system makes it crucial forincreasing productivity, boosting economic development, enhancing equality of opportunity, and reducing poverty. Empirical evidence has shown that the financial systems in advanced economieshave contributed in an important way to the prosperity of those economies.

A well developed financial market comprise spectrum of well-functioning banks, and non-bank financial institutions. Banksprovide deposit and payments services, allocate resources, and monitor operations of firms. Equity markets provide financialleverage and ensure efficient allocation of resources. Well-developedcapital markets force banks to pay more attention to smaller firmsand households. Active domestic bond markets provide firms withlong-term domestic currency finance and ease credit crunch duringperiods of bank stress. Housing finance is important for householdsand provides an important asset for entrepreneurs. Successful leasing, factoring, and venture-capital markets provide financing andenhance an economy’s productivity.

The potential for financial development and growth in Egypt islarge as macro economic policies and overall business environment fundamentals are increasingly supportive. This is evident in accelerating economic growth, increased market confidence, strongcapital inflows, stability in the foreign exchange market, significantincrease in international reserves, and fall in inflation. The impact

Executive Summary

Greater financialdevelopment increases growth, reduces economic volatility and improves income distribution

The potential for financial developmentin Egypt is large as macro economic policies and overall business environment fundamentals are increasingly supportive

Executive Summar yxviii

of the broad range of structural reforms, particularly those affecting the investment climate, initiated by the government appointed in July 2004 is being reflected in the significant improvement in theinvestors’ perception of the business environment.

A cornerstone of the government’s comprehensive reform program is the Financial Sector Reform Program, endorsed in September 2004. The program aims at improving the soundness of the financialsector and fostering an enabling environment for the emergence of an efficient, increasingly private-led financial system that serves Egypt’sdevelopment and growth objectives. The program is underpinned by significant improvements in the legal, regulatory, and supervisoryframework across the bank and non-bank financial institutions, withthe aim of enhancing competition, improving financial intermediation,fostering more efficient mobilization of savings, and ensuring systemicsoundness. An integral component of the strategy is to promote the quality of information and market discipline by upgrading financialinstitutions’ accounting, auditing and reporting to international standards.

Significant progress has been made in the implementation ofthese financial sector reforms. Achievements include consolidatingthe banking sector, divesting the state-owned banks’ shares in the joint-venture banks, privatizing one state-owned bank, pursuing the restructuring of the remaining three state-owned commercial banks, and building the supervisory capacity at the central bank. For non-bank financial institutions, various reforms have been undertaken tofurther deepen the capital market, restructure the insurance sector, develop a well-functioning mortgage market, activate financial leasing,and factoring. However, such progress has not yet been reflected inimproved performance and enhanced financial intermediation.

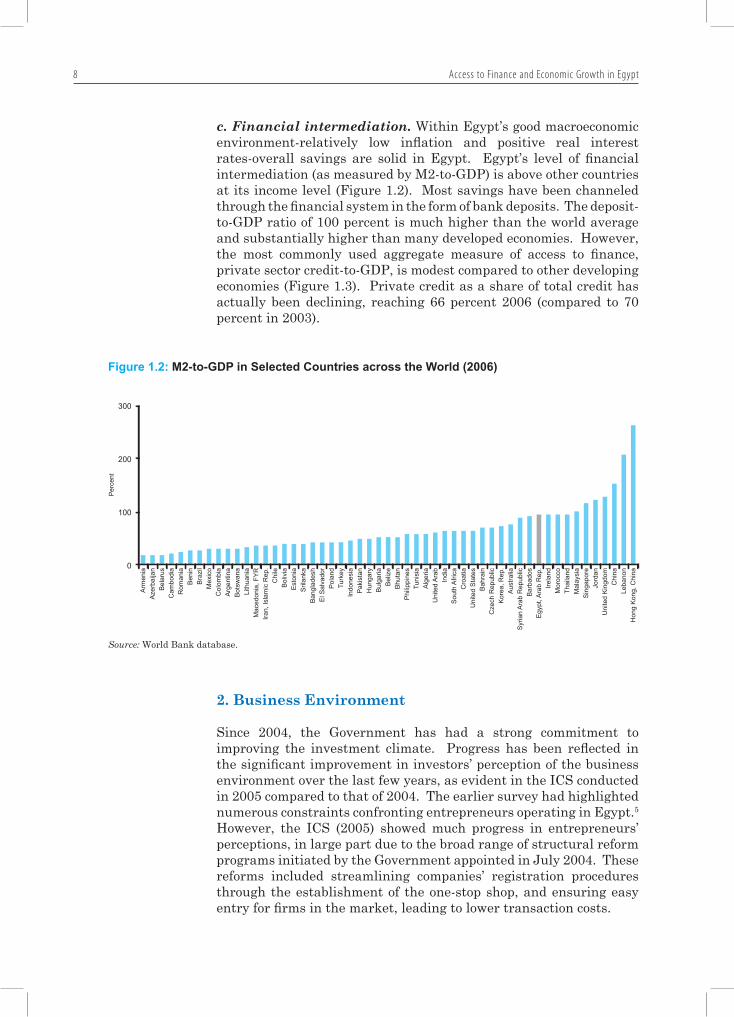

Various financial indicators put the Egyptian financial sectorat a moderate level in financial intermediation compared to otherdeveloping countries. Although mobilization of savings in Egypt is high by international standards, the banking sector is not intermediating efficiently. Most savings are channeled through the financial system asbank deposits, where the deposit-to-GDP ratio of 100 percent is much higher than the world average and substantially higher than many developed economies. However, little of it is channeled to the real, productive private sector and is mainly used to finance governmentdeficits or as loans extended to state-owned enterprises.

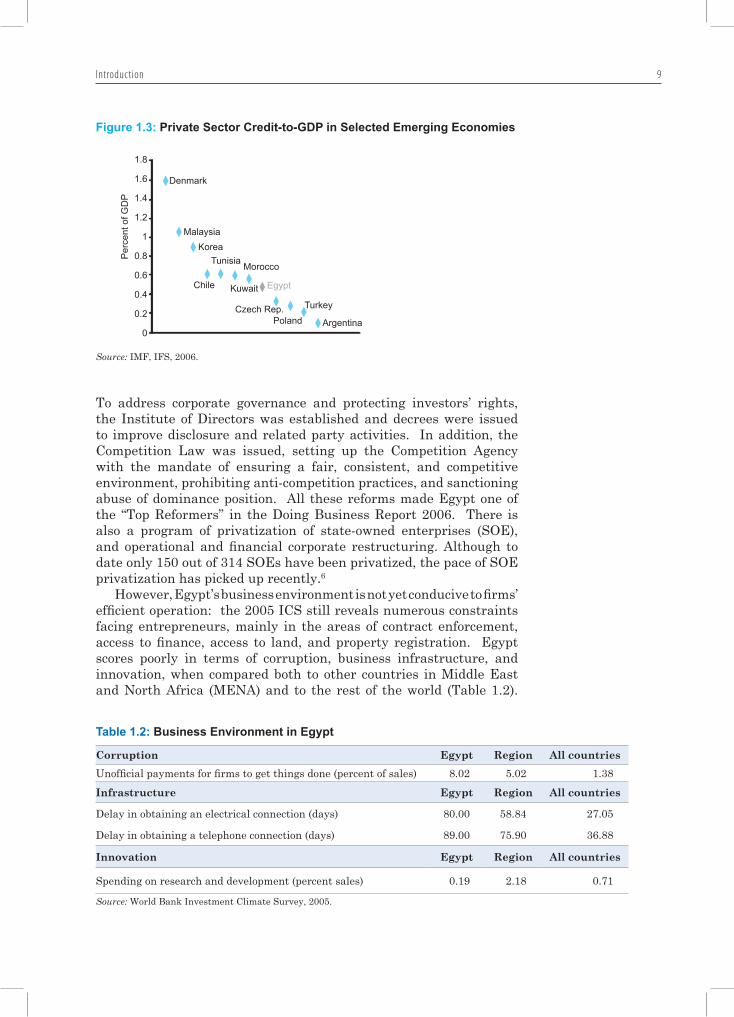

Private-sector credit to GDP in Egypt is modest compared to other developing economies. Private credit as a share of total credit has been declining, to reach 66 percent in 2006, compared to 70 percent in 2003. Importantly, the distribution of bank financing is uneven,with most loans going to large and well-established enterprises. Consequently, family-owned firms and small and medium enterprises(SMEs)—the majority of firms in Egypt—rely heavily on the informalmarket.

Formal financing, whether from banks or non-bank financialinstitutions, plays a limited role in financing enterprises, especially

This is largely due to the broad range of structural reforms initiated by the government since mid-2004, of which the “Financial Sector Reform Program” is a cornerstone

Significant progresshas been made in the implementation of the financial sector reformprogram

...however, this has not yet been translated to better performance and enhanced financialintermediation

Financial indicators still put the Egyptian financial sectorat a moderate level in financialintermediation

Executive Summar y xix

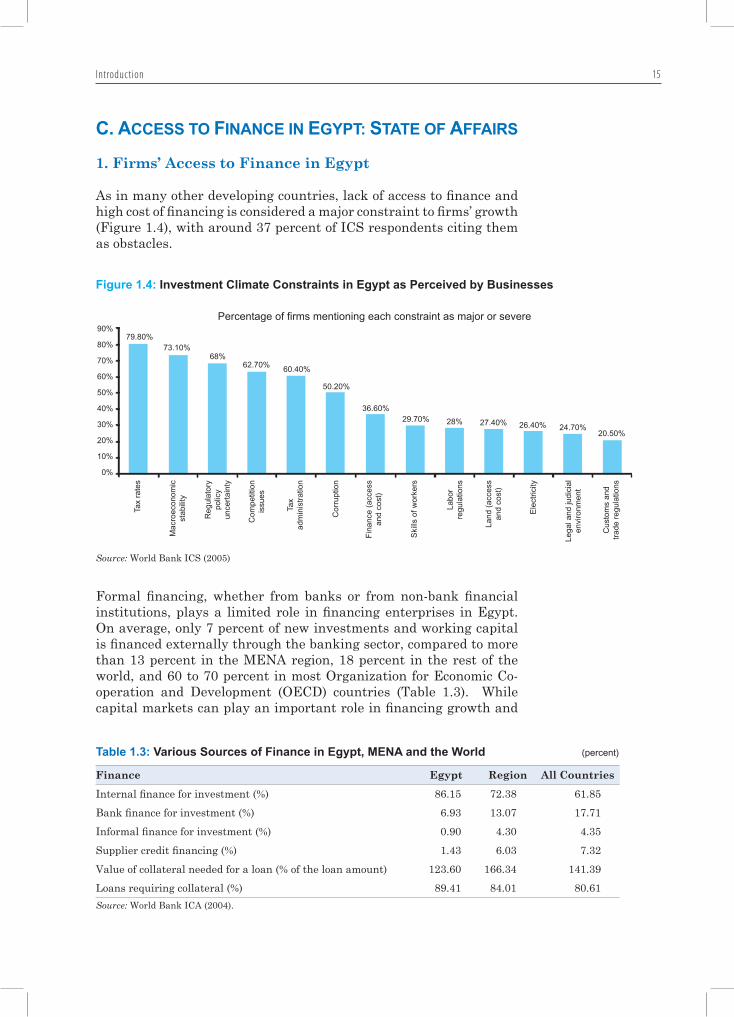

SMEs. More than 37 percent of the firms consider access and cost offinance major obstacles to growth. The large majority of Egyptianmanufacturers rely exclusively on their own funds; only 17.4 percent have access to finance from the financial sector. This is especiallystriking for small firms—only 13 percent have access to finance, asopposed to 36 percent for large firms. While the average for Egypt iscomparable to the other countries in the Middle East and North Africa (MENA), it is significantly below that in other developing countries.

Moreover, the financial sector plays a limited role in financingnew investments. On average, only 7 percent of new investments and working capital in Egypt is financed externally through thebanking sector, compared to more than 13 percent in MENA region, and 18 percent in the rest of the world. Banks often prefer to extend credit to large corporate clients and connected individuals that are considered less risky, while start-up companies remain financiallyconstrained. While the capital market can play an important role in financing growth and development, it only financed 3.8 percentof new investments in Egypt. The dependence on internal financeindicates that firms in Egypt are unable to take advantage of growthopportunities, with negative ramifications for overall economic andemployment growth.

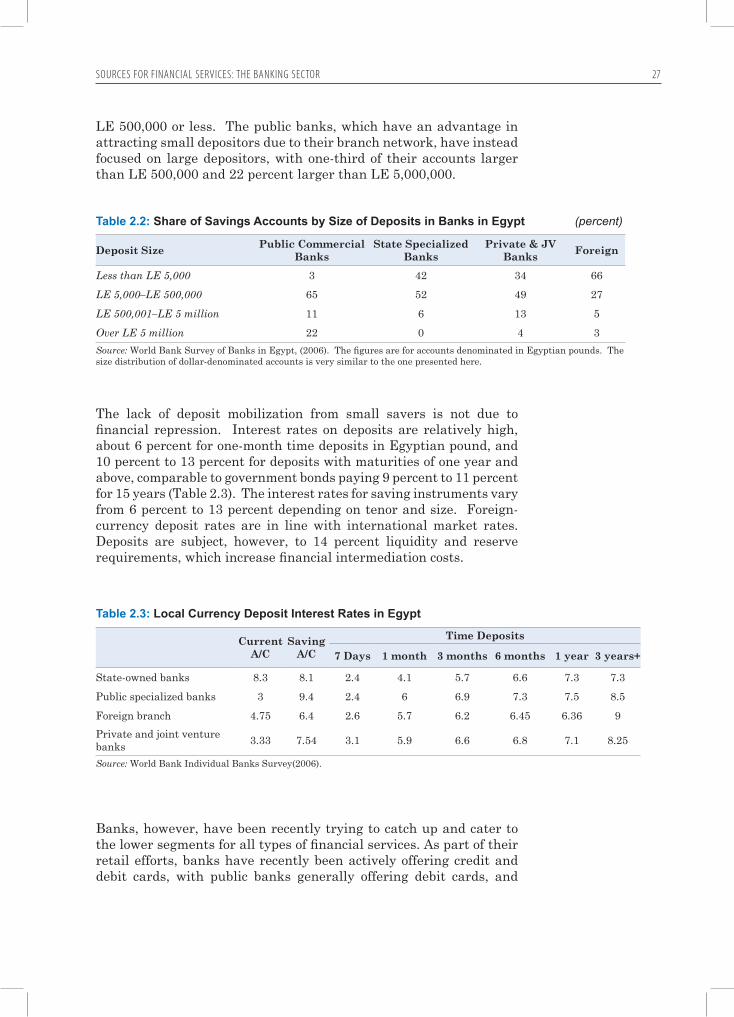

Incentives for small firms and households to use deposits andother financial services are poor. Minimum required deposit amountsare too high to enable the poorer segments of the population to access the banking system and tend to discourage the unbanked population to save through formal channels. The lack of deposit mobilization from small savers is not due to financial repression, as interest rateson deposits are relatively high. Although state-owned banks have a comparative advantage in attracting small depositors, with their huge branch network in governorates and villages, they have instead focused on large depositors, and extend very limited financial servicesto the relatively disadvantaged segments of society. Recently, however, banks have been trying to catch up and cater to small depositors for all types of financial services.

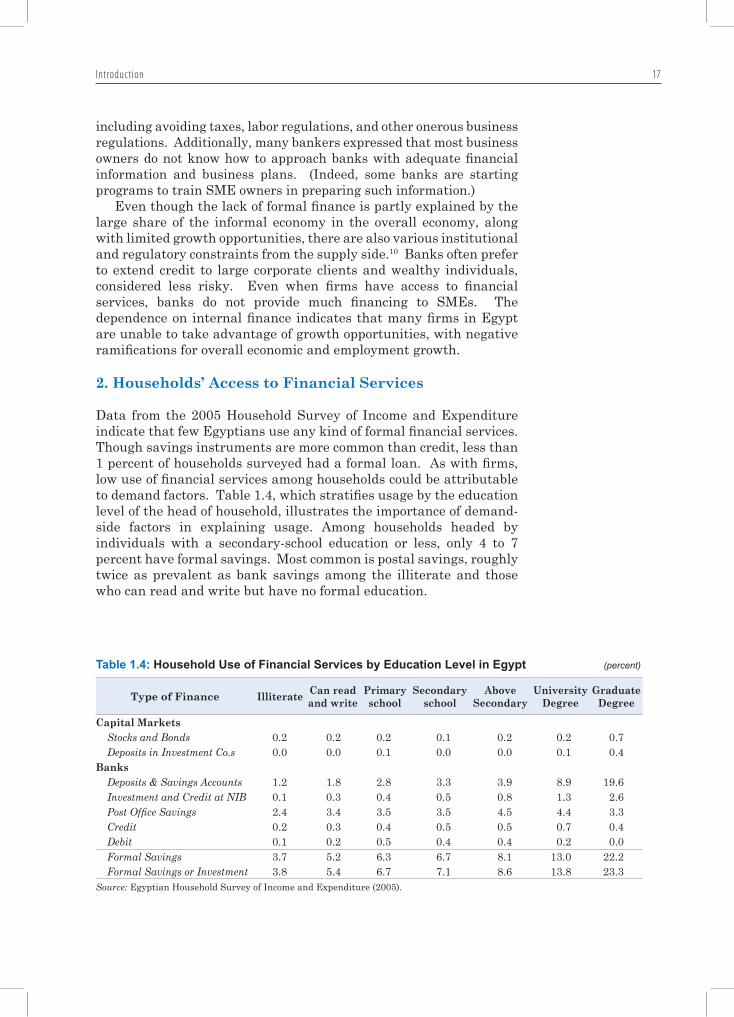

Few Egyptian households use any kind of formal financial services. Savings instruments are more common than credit, and the most common is postal savings, roughly twice as prevalent as bank savings among the illiterate and those who can read and write. Usage of financial services increases substantially with the level of educationof the head of the household. However, almost no households have formal credit or capital-market investments, where less than one percent of households surveyed had a formal loan.

Sources For Financial Services: The Banking Sector

Financial intermediation by the banking system that accounts for more than 60 percent of the financial system’s assets is weak byinternational standards. While savings are high and banks collect

Formal financing,whether from banks or non-bank financialinstitutions, plays a limited role in financing enterprises,especially SMEs

...this is especially striking for start-up enterprises that rely mainly on internal funds and retained earnings

Incentives for small firms and householdsto use deposits and other financialservices are poor

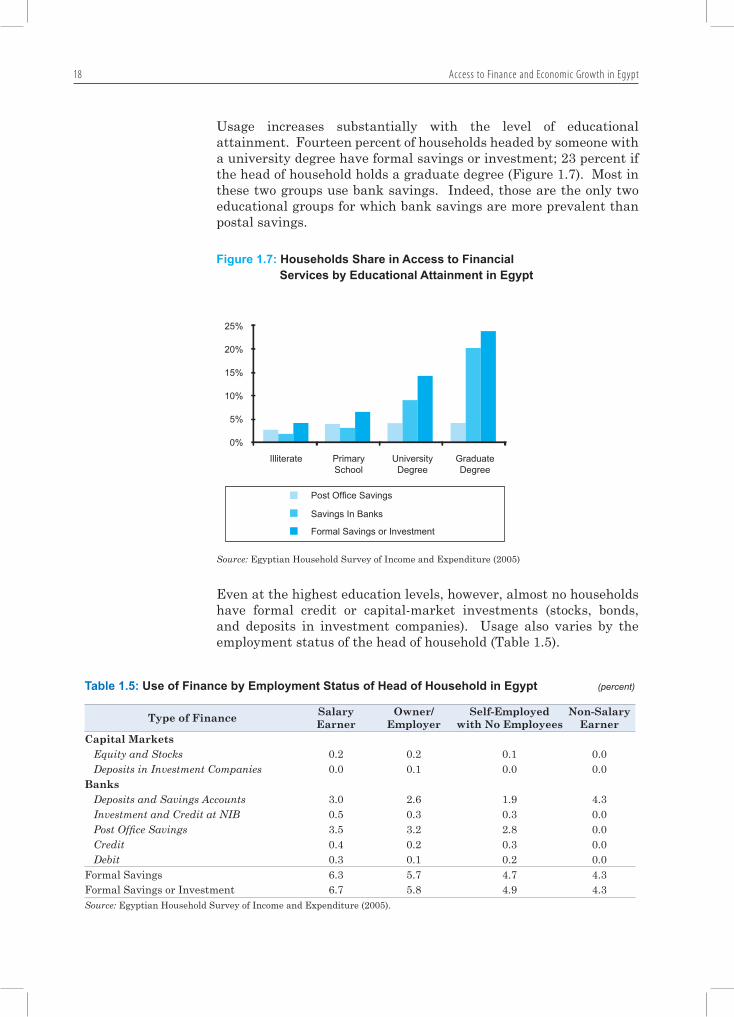

However, usage of financial servicesincreases substantially with the level of education of the head of the household

Executive Summar yxx

large deposits, amounting to about 100 percent of GDP, they actually lend little of these deposits. The loan-to-deposits ratio has been declining over the last few years to reach only 58 percent in June 2006, well below the world average of 86 percent, and much less than the level of intermediation in many developed economies, where typically credit exceeds deposits.

Only a small portion of the funds that are mobilized are lent to the productive sector, and even less to the private sector. Credit to the private sector was at 54 percent of GDP in 2006, similar to country comparators, yet half the OECD average. Credit to the private sector has sharply decreased over the past few years, as private credit as a share of total credit has been declining to reach 66 percent in 2006, compared to 70 percent in 2003. Furthermore, much of the lending extended to the private sector goes to a few large firms, with mostfirms, especially SMEs, receiving little financing.

Most of the funds that are mobilized financethebudgetdeficitandthepublic sector. Banks, particularly state-owned banks, are increasingly investing in treasury bills and government bonds, holding about 91 percent and 70 percent of the outstanding respectively as of June 2006. This reflects banks’ inefficiency in identifying profitable projects, as well as their cautious investment policies. Investing in treasury bills, in addition to being risk-free, is tax-exempted. Direct lending to the public sector–both the government and state-owned enterprises (SOEs)–has also increased in recent years. Lending to SOEs remains high for state-owned banks compared to private banks.

Access to Bank Financial Services

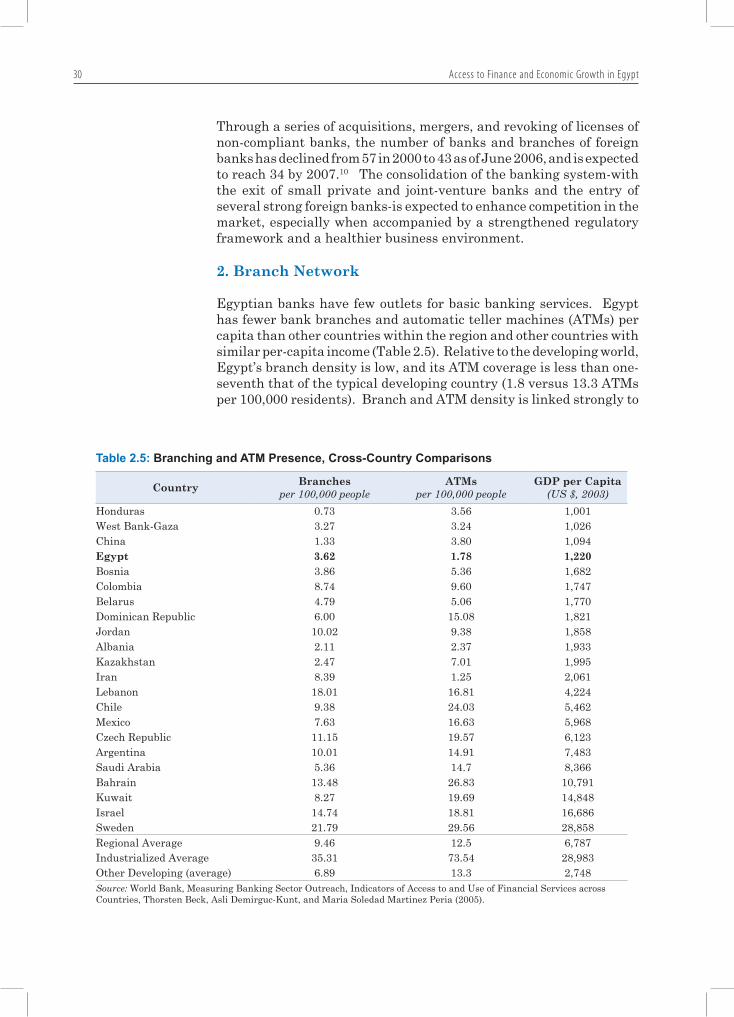

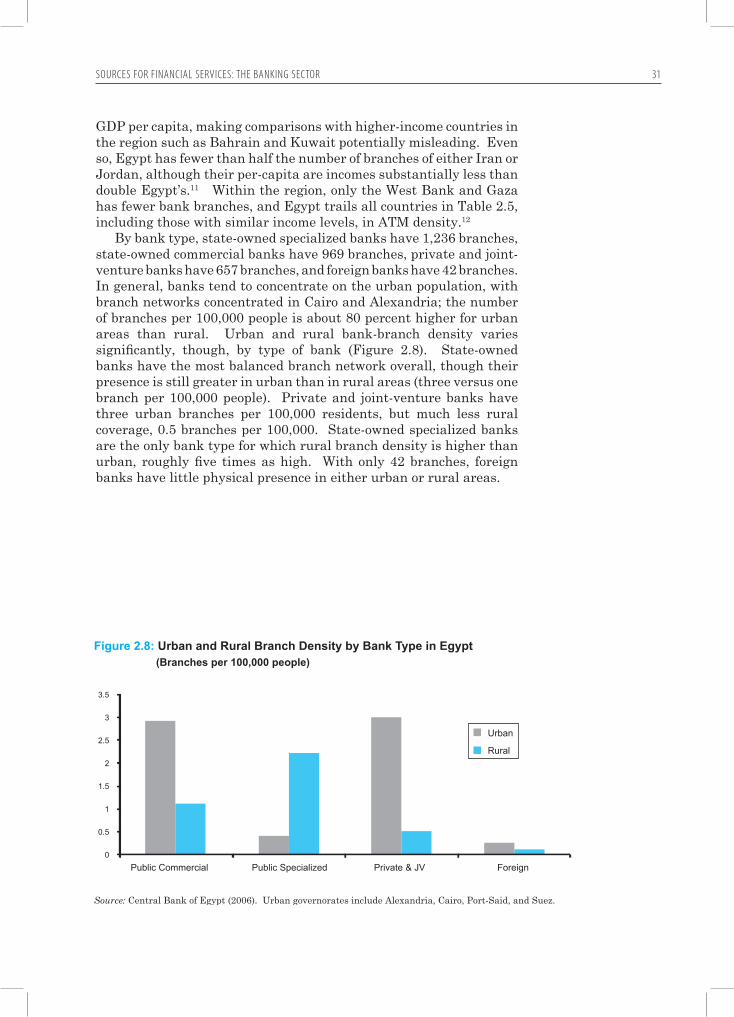

Relative to Egypt’s total population, banks have few outlets for basic banking services. Egypt has fewer bank branches and automatic teller machines (ATMs) per capita than countries with similar per-capita income. Relative to the developing world, Egypt’s branch density is low, and its ATM coverage is less than one-seventh that of the typical developing country. In general, banks tend to concentrate on the urban population. State-owned banks have the most balanced branch network overall, though their presence is still greater in urban than in rural areas. State-owned specialized banks are the only banks for which rural branch density is higher than urban. Private and joint-venture banks have much less rural coverage, while foreign banks have little physical presence in either urban or rural areas.

State-owned banks lend mainly to large corporations, while private, joint venture, and specialized state-owned banks, followed by foreign banks, are more active in lending to SMEs. Foreign banks also reach out more than other types of banks to retail clients, possibly taking advantage of their own superior credit-scoring skills. Large corporate-sector loans are as large as 70 percent of total loans for many banks, with SME lending accounting for only 20 percent, and retail lending only 10 percent of total loans. The distribution of loans is quite concentrated in Egypt, leaving the banking system suffering from a high concentration of credit risk and lack of diversification.

Financial intermediation by the banking system is weak by international standards

Most of the credit extended to private sector goes to a small number of large firms with mostfirms, especiallySMEs receiving little financing

Banks, especially state owned ones, increasingly invest in treasury bills and government bonds

Relative to Egypt’s total population, banks have few outlets for basic banking services

Executive Summar y xxi

Factors Behind Weaknesses in Supply of Banking Services

The poor quality of financial intermediation is reflected in hightransaction costs, large non-performing loans, and limited access for small firms and households to financial services. This could be partiallyattributed to the dominance of state-owned banks, compounded by the ongoing process of institutional and operational restructuring, as well as the new and relatively untested regulatory and supervisory framework.

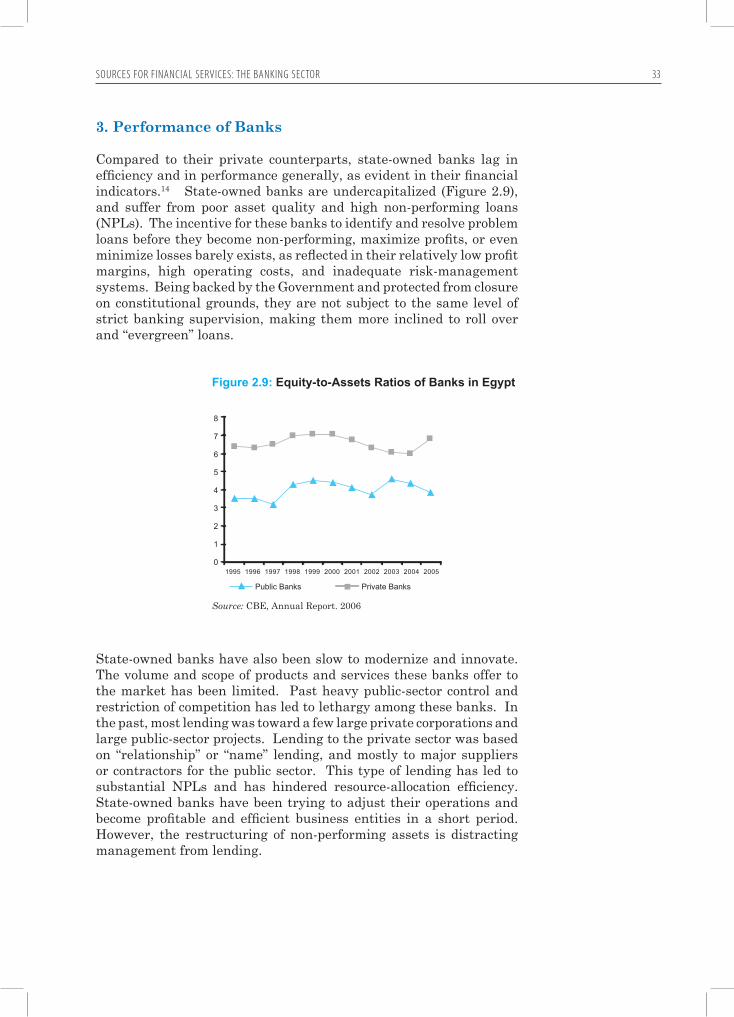

The banking sector is dominated by state-owned banks that lag in efficiency and generally in performance in financial intermediationcompared to their private counterparts. State-owned banks are undercapitalized, and suffer from poor asset quality and high levels of non-performing loans. There are no incentives for them to proactively identify problem loans, maximize profits, or even minimize losses, asreflected in their relatively low profit margins, high operating costs,and inadequate risk-management systems.

Importantly for access to financial services, state-owned banksare also slow to modernize and innovate, and the volume and scope of products and services they offer have been limited. Although new products are being introduced, most loan products are quite basic, generally straight lending with fixed interest rates. Fees andcommissions and treasury earnings are not significant sources ofrevenues, primarily because of a lack of product diversification. Banksare not offering hedging, forwards, factoring, or export receivables, discounting under letters of credits, and structured investment banking products. The recent increase in ATMs and credit/debit cards as well as retail lending suggest, however, that banks will see an increase in income from fees and commissions in the future.

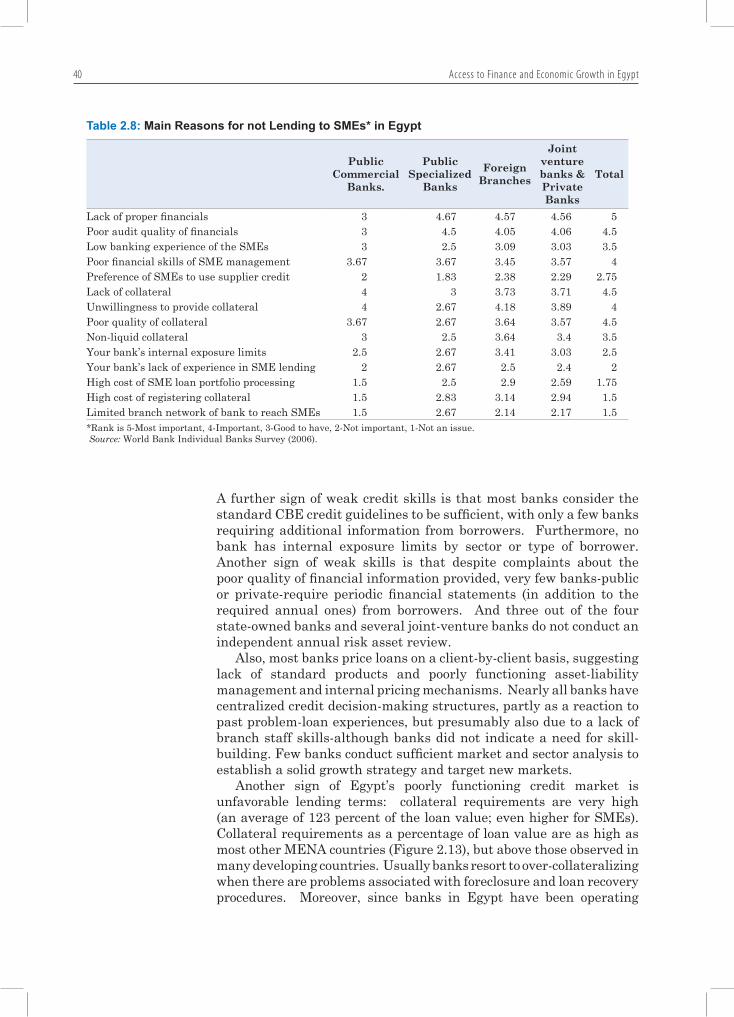

Skills to assess credit risk are generally weak, and the credit decision is centralized, especially in state-owned banks. A few banks have internal exposure limits by sector or types of borrowers, and require periodic financial statements from borrowers. A very limitednumber of banks conduct independent annual asset risk reviews, market and sector analysis sufficient to establish a solid strategyfor growth or to target new markets. Most banks are characterized by lack of standard products, poorly functioning asset-liability management, and internal pricing mechanisms. The restructuring of non-performing assets in the state-owned banks has distracted management from focusing on extending credit.

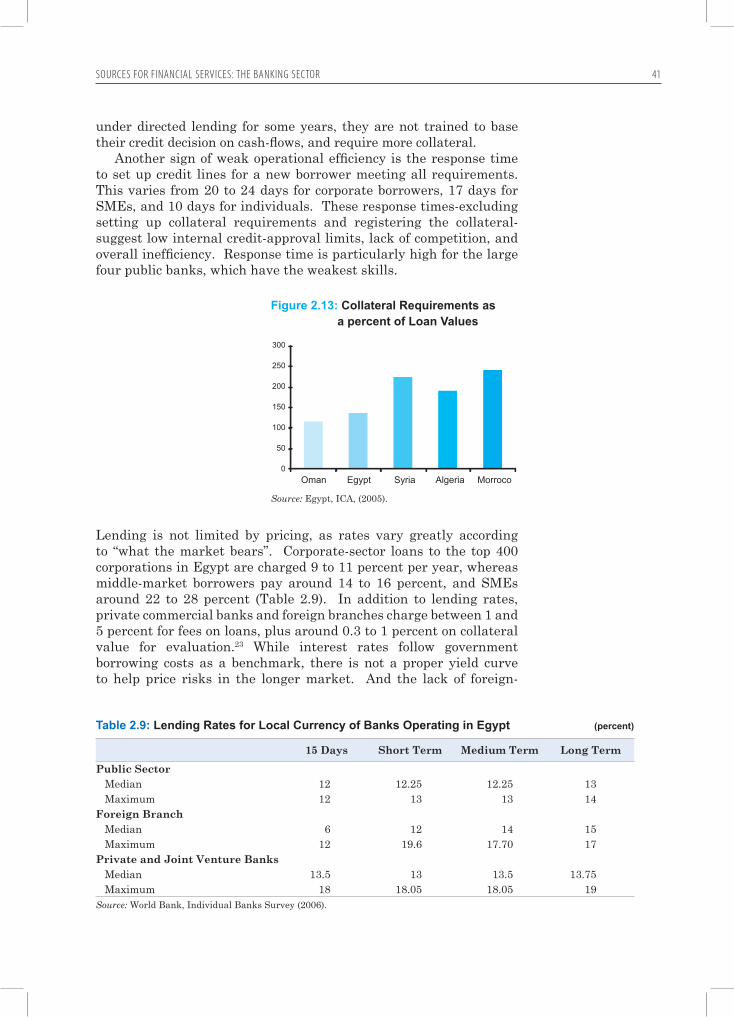

Another sign of a poorly functioning credit market is that lending terms are unfavorable, with very high collateral requirements. Usually banks resort to over-collateralizing when there are problems associated with foreclosure and loan-recovery procedures. Furthermore, since banks have been operating under directed lending for some years, they are not trained to base their credit decision on cash-flows, andthus require more collateral. Slow response times to set up credit lines–excluding the setting up of the collateral requirements and registering the collateral–suggest low internal credit-approval limits, lack of competition, and overall inefficiency.

State-owned banks, that dominate the banking system, lag in efficiencyand in financialintermediation compared to their private counterparts

...they are also slow to modernize and innovate, and the volume and scope of products and services they offer have been limited

Lending terms are unfavorable with very high collateral requirements, and slow response times to set up credit lines

Skills to assess credit risk are generally weak, and the credit decision is centralized

Executive Summar yxxii

While interest rates follow the government borrowing costs as a benchmark, there is no proper yield curve to help price risks in the longer market. The lack of foreign-currency hedging instruments leads banks to being overly cautious and charging high margins in foreign-currency lending. Spreads between lending and deposit interest rates are in general high, up to 10 percentage points. These high spreads reflect the need for high provisioning, andinefficiency due to overstaffing. The high spreads also show a supply-driven lending market, where banks take advantage of the lack of competition or collude in keeping spreads high. Only in lending to the large corporations do banks give evidence of much competition.

Moreover bigger banks (as measured by total operating income) and more highly capitalized banks extend relatively more loans. This suggests that there are economies of scale, arguing for increased consolidation of the banking sector in Egypt. At the same time, banks with relatively more deposits—the cheapest source of funding—tend to extend relatively fewer loans, independent of bank ownership. Investigations suggest that, not having to compete for deposits creates incentives for easy forms of financial intermediation, such as lendingto the government and large corporations. This analysis suggests that large private and foreign banks are best able to increase lending to the private sector in a sustainable manner in Egypt.

Overall, the banking sector reform program launched in late 2004 and changes in the business environment have rejuvenated banks. The institutional and operational restructuring of the state-owned commercial banks will further improve their efficiencyandprofitabilityover time. Banks are improving credit policies and procedures, while provisioning for past problem loans; upgrading their banking services; widening the range of lending products available to the non-corporate sector; and diversifying products as the regulatory framework adjusts to the new environment. The government is also making efforts to address state-owned banks’ non performing loans (NPLs), including a time-bound scheme with resources from privatization proceeds earmarked for its implementation.

The ongoing consolidation of the banking system with the exit of small private and joint-venture banks and the entry of several strong foreign banks is expected to enhance competition in the market. Such rapid consolidation will lead to opportunities to exploit economies of scale, lowering the cost of financial intermediation. The privatizationof Bank of Alexandria—the fourth largest state-owned bank—in late 2006 is considered a milestone in this comprehensive reform program. The progress in the implementation of the banking reform program has been evident in the slight improvements in the banking system performance and capacity to intermediate indicators.

...and there is not a proper yield curve to help price risks in the longer market

However, state-owned banks have recently been subject to institutional and operational restructuring

...and there has been slight improvements in banking system performance and capacity to intermediate

Executive Summar y xxiii

Sources For Financial Services:Non-bank Financial Services

Well-developed non-bank financial institutions can provide externalfinancing and help improve the risk and maturity profile ofcorporations’ external financing. Non-bank finance—capital markets,insurance, contractual savings, mortgage finance, financial leasing,and factoring can serve as an important source of finance for thereal sector. However, to date, these forms of external financing arerelatively underdeveloped in Egypt.

Non-bank financial institutions in Egypt face various obstacles,similar to those impeding efficient intermediation by the bankingsystem: the still-large role of the state, through ownership as well as tightly prescribed (investment) regulations; the lack of well-functioning and efficient means of registering and enforcing propertyrights, especially on collateral; and limited and poorly available information bases on potential clients and borrowers. Although there is progress, further streamlining and more market-based measures are needed.

Capital Markets

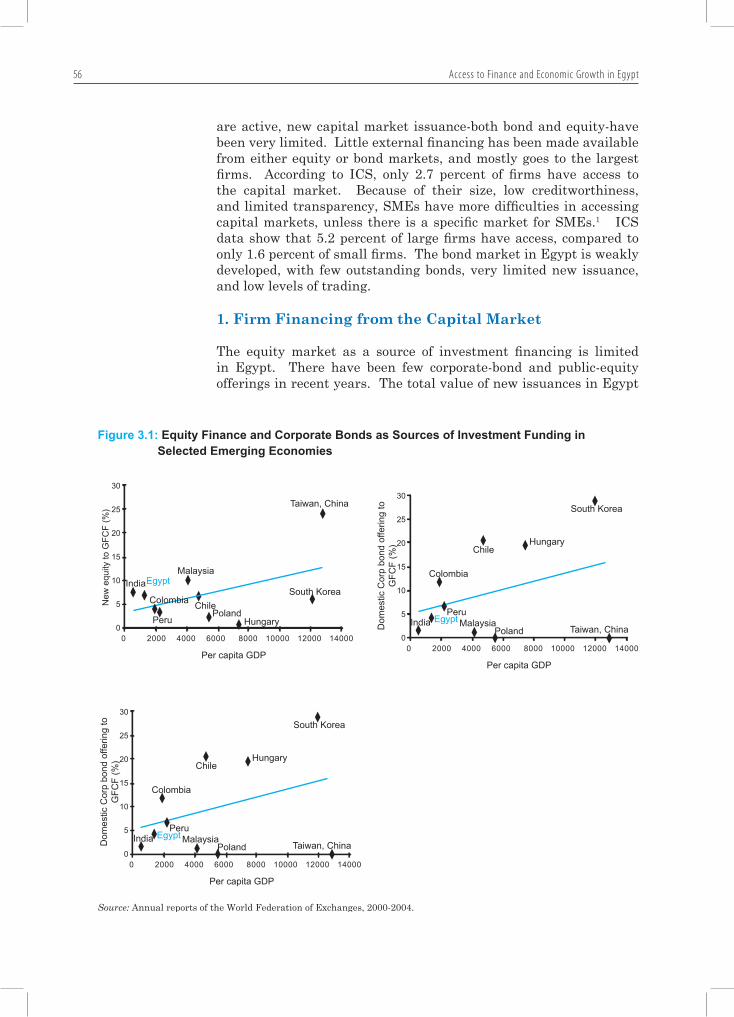

Although noteworthy strides have been made, the development of capital markets in Egypt remains below potential, especially in terms of primary markets. Egyptian firms’ access to long-term capital hasbeen hampered mainly by an inadequate legal framework, especially regarding new securities issuance; lack of active domestic financialinvestors; and a weak regulatory and supervisory framework. While the secondary capital markets are active, new capital market issuance–both bond and equity–have been very limited. The primary markets are much smaller than those of high-performing emerging markets. Little external financing has been made available for firmsfrom both equity or bond markets, and what is provided mostly goes to the largest firms. As elsewhere, stock exchanges mainly target large,blue-chip companies; because of their size, low creditworthiness, and limited transparency, SMEs have more difficulties in accessingcapital markets.

The securities market as a source of investment financing is limitedin Egypt. The private sector has made few corporate bond and public equity offerings in recent years. While there have been more equity issues than corporate bonds, many equity issues were public offerings or sales of government shares in large state-owned companies, which do not add to capital formation. Funds raised through corporate bonds were even less compared to equity financing. The corporate bondmarket is nascent and largely dominated by commercial banks, while access to international capital markets is limited to large enterprises and financial firms. No Eurobond has been issued by an Egyptiancompany to date.

Non-bank financialinstitutions are under developed, and face various obstacles similar to those impeding effective intermediation by the banking system

The developments of capital markets in Egypt remains below potential especially in terms of primary markets

The corporate bond market is nascent and largely dominated by commercial banks, while access to international capital markets is limited to large enterprises and financial firms

Executive Summar yxxiv

Insurance and Contractual Savings

Egypt’s insurance and contractual savings sector is small compared to the size of its economy. Since growth of contractual savings is typically linked to GDP per capita, with some low-income countries experiencing threshold effects, growth will take time. Still, Although penetration is higher than in other countries of the region, insurance and pension products have yet to gain broad public appeal. Only a small percentage of the working population participates in retirement plans. Furthermore, the sector does not yet do a good job of channeling resources to the private sector.

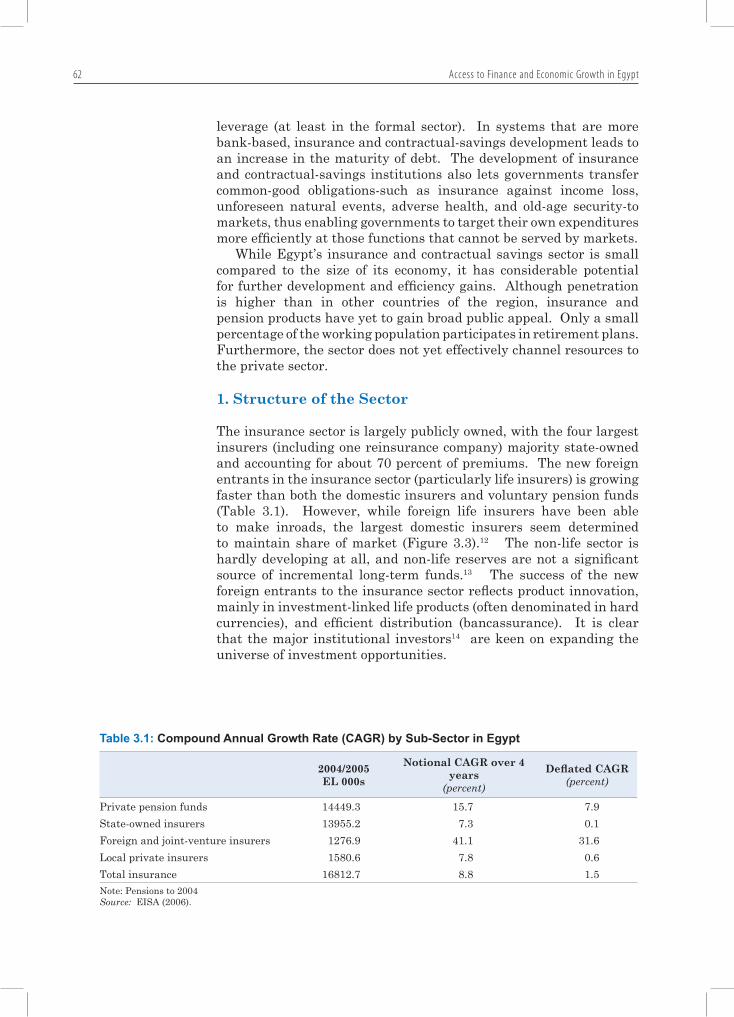

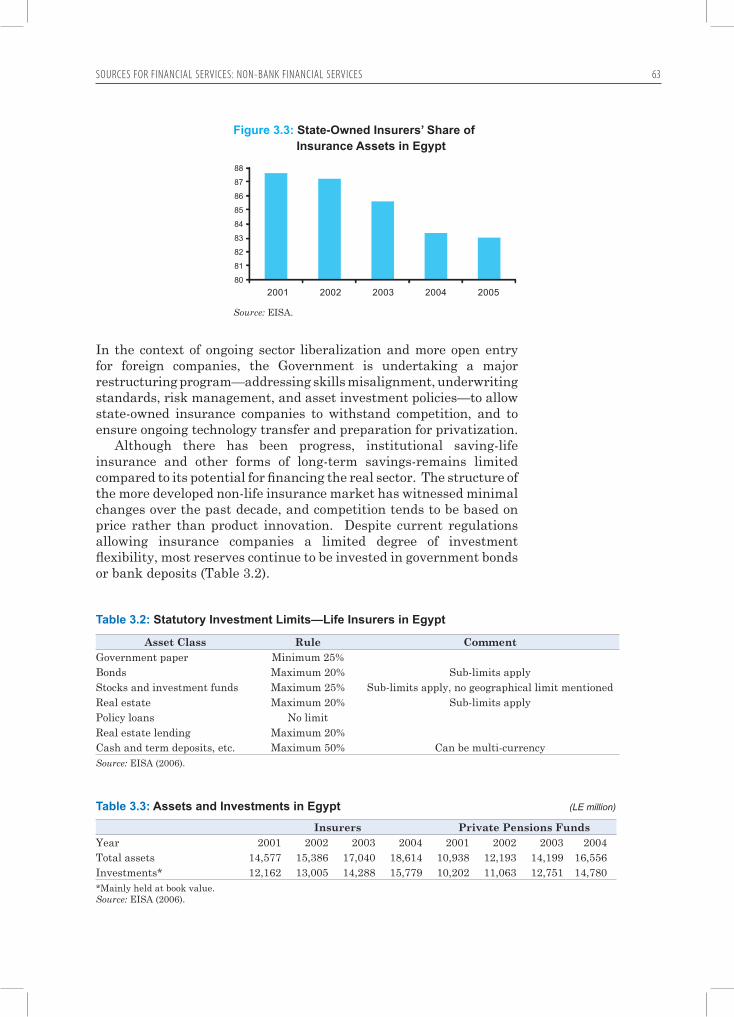

The insurance sector is largely publicly owned; however, more foreign insurers are entering the market. The four largest insurers (including one reinsurance company) are majority state-owned, accounting for about 70 percent of premiums. The new foreign entrants in the insurance sector (particularly life insurers) are growing faster than both the domestic insurers and voluntary pension funds. While foreign life insurers have been able to make inroads, the largest insurers seem determined to maintain market share. The non-life sector is hardly developing, and non-life reserves are very limited.

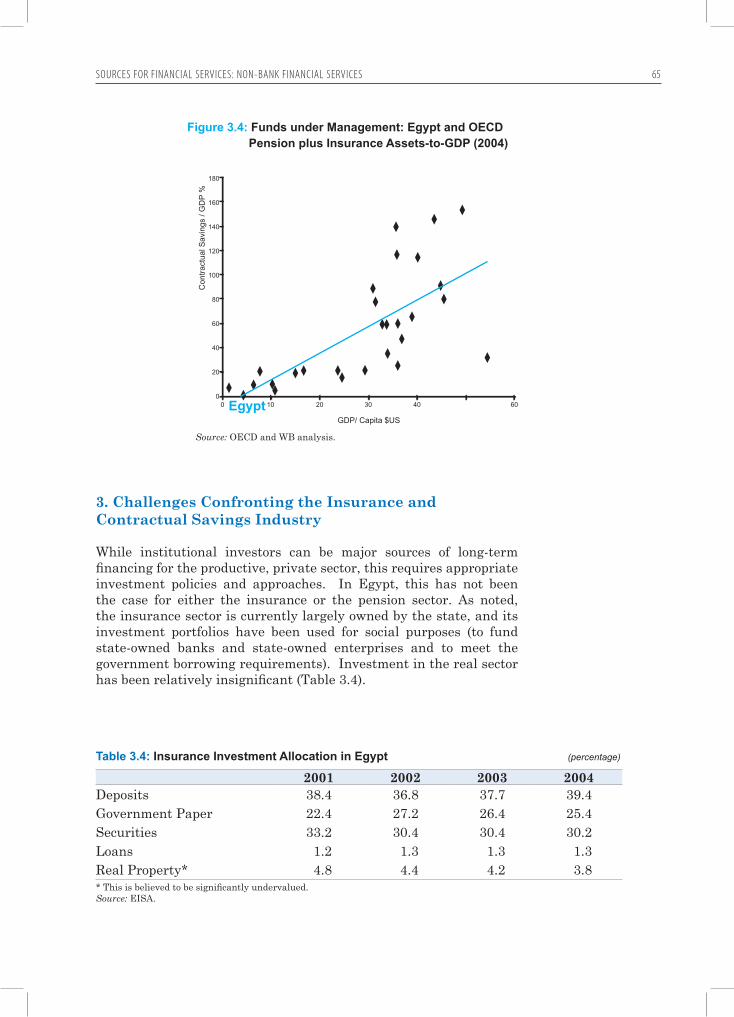

Institutional savings–life insurance and other forms of long-term savings–remain limited compared to their potential for financing thereal sector. The structure of the more developed non-life insurance market has changed marginally over the past decade, and competition tends to be based on price rather than product innovation. Importantly for access to financialservices,anddespitecurrentregulationsallowinginsurance companies a limited degree of investment flexibility,most reserves continue to be invested in government bonds or bank deposits. This underlines the need to develop a modern corporate-finance culture with up-to-date institutional investment skills. At thesame time, capital markets lack products suited to the insurance and contractual savings markets’ liability structures.

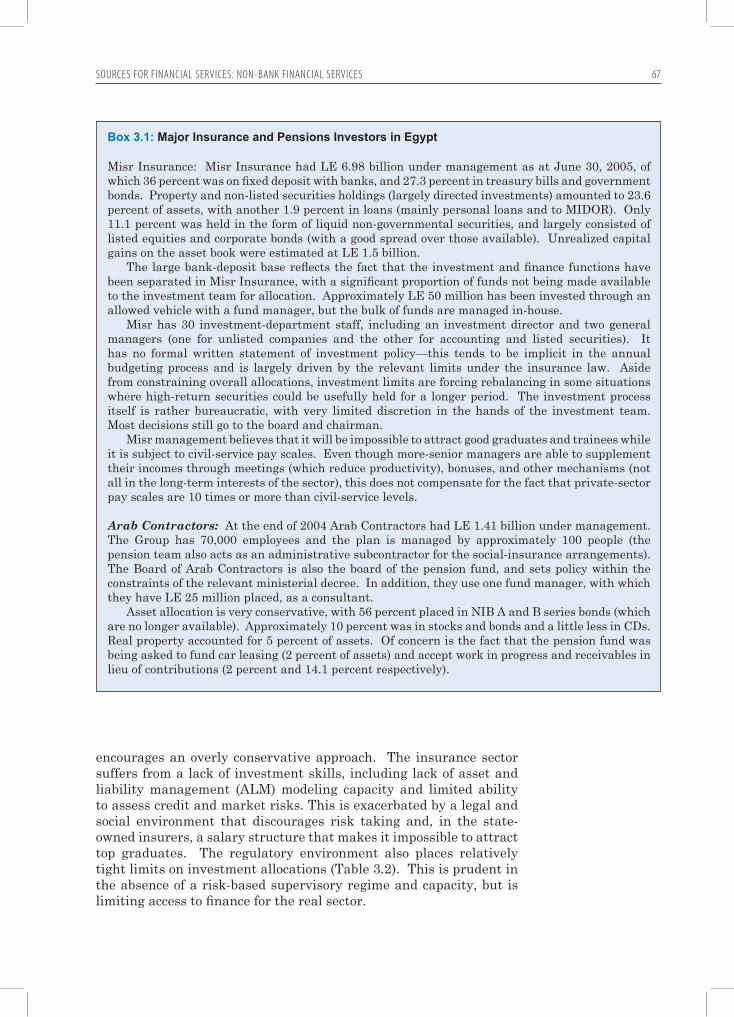

Dominated by state-ownership, the insurance sector’s investment portfolios have been used for social purposes, to fund state-owned banks and state-owned enterprises and to meet government borrowing requirements. Investment in the real sector has been relatively insignificant. The insurance sector suffers from a lack of investmentskills, including lack of asset and liability management modeling capacity and limited ability to assess credit and market risks. This is exacerbated by a legal and social environment that discourages risk taking and, in the state-owned insurers, a salary structure that makes it impossible to attract top graduates. The regulatory environment also places relatively tight limits on investment allocations, prudent in the absence of a risk-based supervisory regime and capacity, but limiting access to finance for the real sector.

Investment decisions by private pension funds—an essential component of the contractual savings scheme—show even lower intermediation to the real and private sectors than in the insurance sector. Private pension funds tend to be managed in-house, encouraging

Egypt’s insurance and contractual savings sector is small compared to the size of its economy

Institutional savings—life insurance and other forms of long-term savings—remain limited compared to their potential for financingthe real sector

Dominated by state-ownership, the insurance sector’s investment portfolios have been used for social purposes, to fund state-owned banks and state-owned enterprises and to meet government borrowing requirements

Executive Summar y xxv

an overly conservative approach. Larger funds have recently begun to experiment with the use of external investment managers. Aside from insurers and private pension funds, NIB is the major potential long-term investor in Egypt. NIB has generally not invested in the real or private sectors; its main role has been to intermediate funds from a public pension system. Its investments have been for social purposes, to fund state-owned banks and the government borrowing requirement, with negligible investment in the real sector. Altogether, as a consequence of limited development and poor asset allocation, insurance, pension, and other long-term institutional investors do not provide much financing to the productive sector.

However, in the context of ongoing sector liberalization and more open entry for foreign companies, the government is undertaking a major restructuring program—addressing skills misalignment, underwriting standards, risk management, and asset-investment policies—to allow state-owned insurance companies to withstand competition, ensure ongoing technology transfer, and prepare for privatization. Moreover, the success of the new foreign entrants reflects product innovation, mainly investment-linked life products,and efficient distribution. It is clear that the major institutionalinvestors are keen on expanding investment opportunities.

Mortgage Finance

Several constraints limit households’ access to long-term finance forhome ownership, and the consequent development of a mortgage market. These include limited access to long-term funding for primary lenders, cumbersome property registration procedures, inadequate collateral enforcement, lengthy court process, and untested foreclosure procedures; consequently, interest rates approximate those for unsecured lending. Another key challenge is the undeveloped regulatory framework for securitization to enhance the secondary mortgage market.

As a result, most commercial banks—state-owned and private—are extending loans to homebuyers, mostly as part of their retail activities or their lending to developers, by using collateral other than mortgage pledges. Although most banks are liquid, they are reluctant to extend mortgage loans, mainly because of maturity mismatches between short-term deposits and long-term mortgage loans, and lack of registered titles. There are currently few non-bank real estate lending companies extending mortgage loans.

Until a few years ago, only some individuals buying houses could obtain finance, but not in the form of mortgage loans. The most commonfinance arrangement was the deferred installment system where thedeveloper receives a down payment of around 10 to 25 percent of the purchase price, followed by installments over four to eight years, and the title is formally transferred when the last installment is paid. Under this system, purchasers pay a significantly higher interestrate than if they could obtain a loan secured on the property, and

However, in the context of ongoing sector liberalization and more open entry for foreign companies, the government is undertaking major restructuring of the insurance sector

Mortgage finance isconstrained by limited access to long-term funding, cumbersome property registration procedures, inadequate collateral enforcement, lengthy court process, and untested foreclosure procedures

Executive Summar yxxvi

short maturities require high repayments. The system also ties up the funds of developers, who would rather invest into new projects, and can be constrained by an adverse cycle of real estate markets. In general, it prevents many from entering the housing market, and is only a second-best to genuine residential mortgage markets.

Over the past few years, the government has made progress in developing an enabling environment for a modern residential-mortgage market. This includes setting the legal foundation and improving collateral enforcement and foreclosure procedures. The government has significantly reduced fees for property registration,alleviated bottlenecks in the new urban communities, and launched a systematic title adjudication, survey and registration process to modernize the property-registration system. The legal and institutional framework now also allows private-sector financialinstitutions to securitize mortgages.

Another major development has been the incorporation of the Egyptian Mortgage Refinance Company (EMRC), which will enablequalified mortgage lenders to access term refinancing for mortgageloans and better manage the risks of mortgage lending. EMRC will also offer banks a safe channel to lend excess funds to other credit institutions. The term finance that EMRC will provide to primarymortgage lenders will help them reduce the liquidity risk incurred in providing long-term housing loans. The EMRC is expected to improve access through competition in the mortgage market (by creating a funding source of non-depository lenders), promote the development of safe and sound mortgage credit standards, and spur the development of fixed-income securities markets. All these developments will helpshift most of the burden of housing finance from the governmentbudget and develop access to mortgage finance through financialmarkets.

Financial Leasing

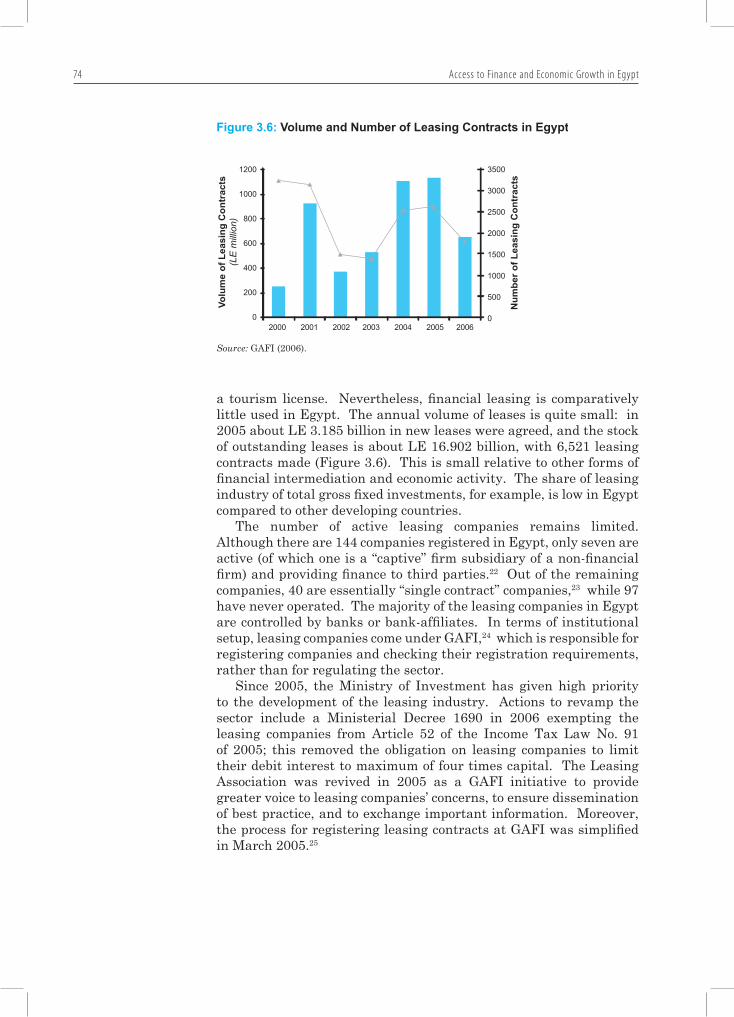

Financial leasing is comparatively little used in Egypt, and the annual volume of leases is quite small relative to other forms of financialintermediation and economic activity. There is a small stock of outstanding leases, and the number of leasing contracts and leasing companies is modest. Most leasing companies are controlled by banks or bank affiliates. The government has recently acted to develop thefinancial leasing industry, including exempting leasing companiesfrom stamp duty and removing obligations to limit debt interest to a maximum of four times their capital; eliminating restrictions on leasing companies lease of assets including land, cars, and tourism buses; and simplifying the contracts-registration process. The Leasing Association was revived in 2005 to provide a forum to voice to leasing companies’ concerns and to ensure dissemination of best practice.

In spite of these recent reforms, the development of the leasing industry is still hampered by an unsupportive institutional environment. One of the major impediments is the difficulty of

Over the past few years, the government has made progress in developing an enabling environment for a modern residential-mortgage market

The recent incorporation of the Egyptian Mortgage Refinance Companywill enable qualifiedmortgage lenders to access term refinancingfor mortgage loans and better manage the risks of mortgage lending

Financial leasing is comparatively little used, and the annual volume of leases is quite small

Executive Summar y xxvii

repossessing assets (due in part to the inadequate enforcement of ownership rights), as well as delays in the collection of overdue payments. Enforcement of court orders, especially for movable assets, is a major issue, and the costs associated with repossessions are very high. It is also difficult to sue defaulted clients for breach of contract,and the time to collect on a dishonored check is between one and fiveyears. Another impediment for the growth of the leasing industry, as for the financial system at large, is the unavailability of adequate andreliable credit information. The leasing industry is also constrained by the lack of long-term funding, and its relatively high cost when it is available. Together with poor market conditions, these factors have reduced leasing companies’ ability to seek clients, especially start-up enterprises.

Factoring

Factoring in Egypt is currently almost non-existent. Enterprises finance their accounts receivables through banks or from their ownsources, increasing their financing requirements. Like other non-bank financial institutions, factoring companies do not have accessto potential clients’ creditworthiness information, and are impeded by the inefficient legal mechanism for collection of receivables. Thegovernment has recently undertaken numerous reforms to foster the factoring industry, including amending the Executive Regulations of the Investment Law, setting the main rules and regulations governing factoring activities; licensing requirements; registration requirements and procedures; and establishing surveillance that includes financialadequacy, credit risk protection, disclosure, accounts receivable bookkeeping, and collection services. The amendments also facilitate the entry of factoring corporations.

Access to Microfinance Institutions and Postal System

The demand of household and small firms for microfinance is largelyunmet. A conservative estimate suggests that there are at least 2 million micro enterprises in Egypt as of June 2006, accounting for 93.7 percent of establishments. While no formal aggregate estimates are available, it is estimated that the outreach of the microfinanceindustry in Egypt covers only about 10 percent of potential borrowers. Microfinance institutions, however, often do not have the necessaryskills and scale. The recently endorsed National Strategy for Microfinance is expected to address the constraints to the developmentof the microfinance industry in Egypt.

Egypt Post plays a limited role in financial intermediation despiteits huge branch network of more than 3,600 branches, many of them in remote areas. It provides low-cost savings and transaction account services, supported by a centralized high-speed network linking all main offices. Only 600 are connected via DSL lines, and many do notoffer a full range of financial services. To date, Egypt Post cannot

...the financialleasing industry is still hampered by an unsupportive institutional environment

The demand of household and small firms for microfinanceis largely unmet

Egypt Post plays a limited role in financialintermediation despite its huge branch network

Factoring is almost non-existent in Egypt, enterprises financetheir accounts receivables through banks or from their own sources

Executive Summar yxxviii

exchange payments directly with other banks, but interoperability between its network and some inter-bank networks is under preparation.

INSTITUTIONAL ENVIRONMENT

Egypt does not have an enabling institutional infrastructure for a sound and efficient financial system. However, specific effortshave been exerted to improve the infrastructure and institutional environment for efficient intermediation include improving andstrengthening the legal, regulatory and supervisory framework, information infrastructure, financial reporting, the payments system,and entry and exit policies. Regulatory gaps are being filled, and newinstitutions are being created. The overall direction is promising, but it will take much more time to develop institutions, particularly in the judicial area, that facilitate easy access to financial services.

Legal Framework

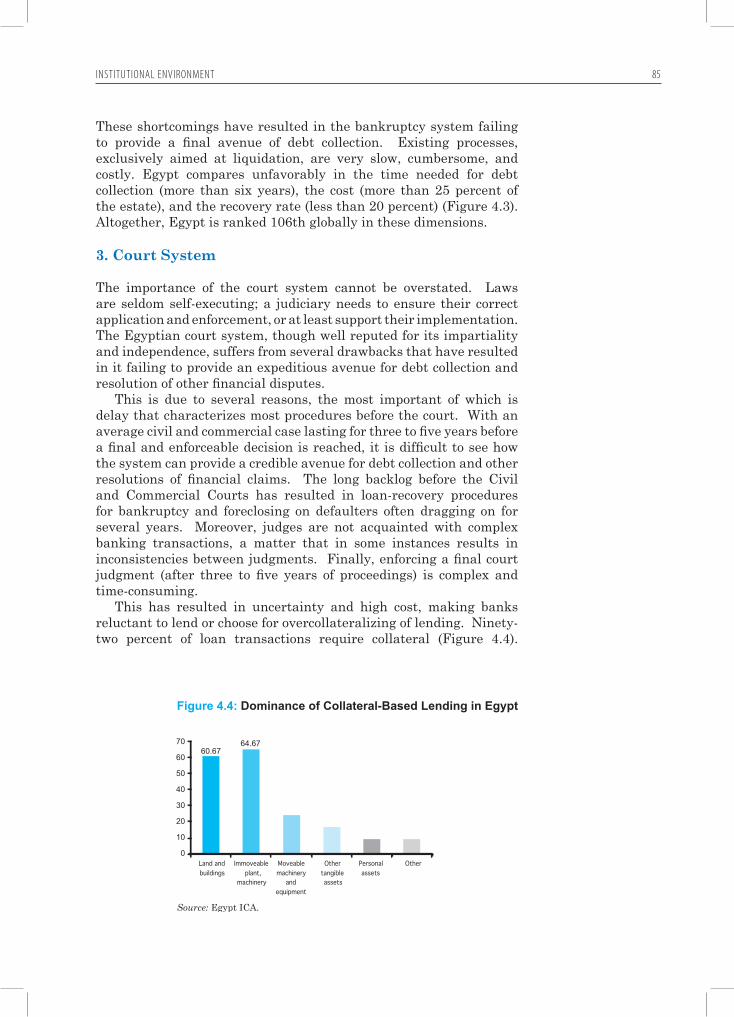

The prevailing legal framework in Egypt still constrains the cost and terms of finance. Some laws are poorly written, especiallythose regarding secured transactions, bankruptcy, and settlement of disputes. Moreover, the court system, though well reputed for its impartiality and independence, suffers from several drawbacks that keep it from helping expedite debt collection and resolve other financial disputes. This is due to several reasons, the most importantof which are backlog and delay; where loan recovery procedures for bankruptcy and foreclosing on defaulters can drag on for several years. There are no specialized courts for financial institutions, and nospecialized judges with adequate knowledge of financial market risks.Judges are often not acquainted with complex banking transactions and debts recovery of financial institutions, a matter that can resultin inconsistencies between courts’ judgments. Enforcing a final courtjudgment (after the three to five years needed to obtain it) is complexand time-consuming.

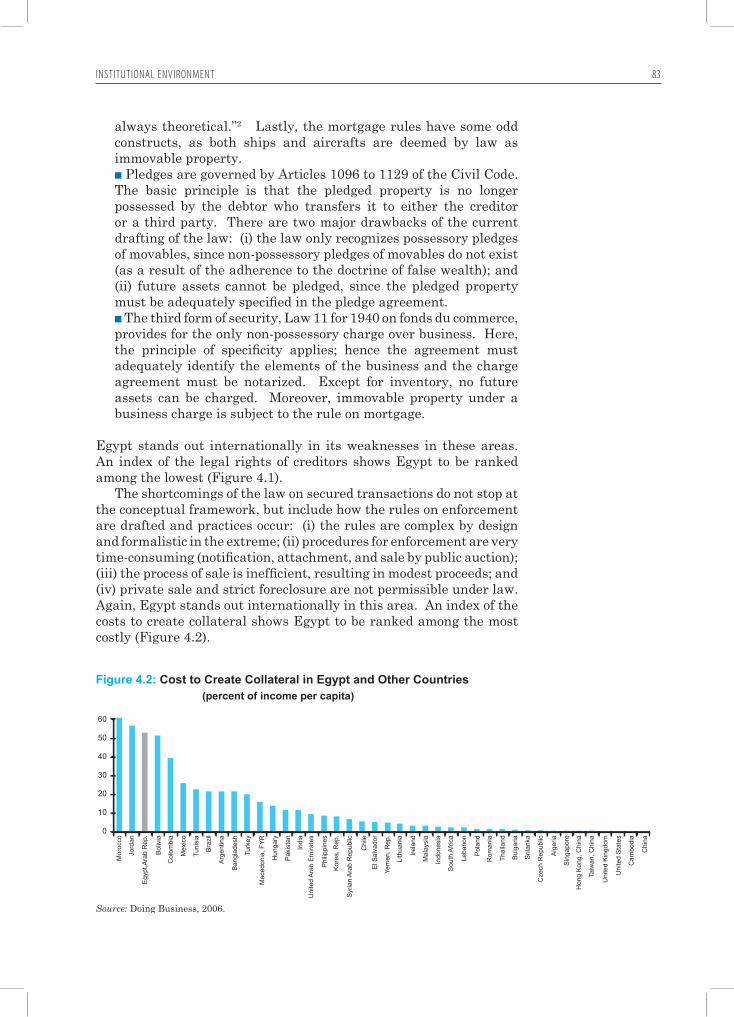

Collateral legislation is poorly enforced. Property-rights registration and titling issues make it difficult for firms, especially SMEs, to useland assets as collateral. Even when collateral is registered, there is no information on its value. This inadequate legal and judicial system has resulted in uncertainty and high cost, making banks reluctant to lend or choose for over collateralizing of lending. An index of the costs to create collateral shows Egypt to be ranked among the most costly.

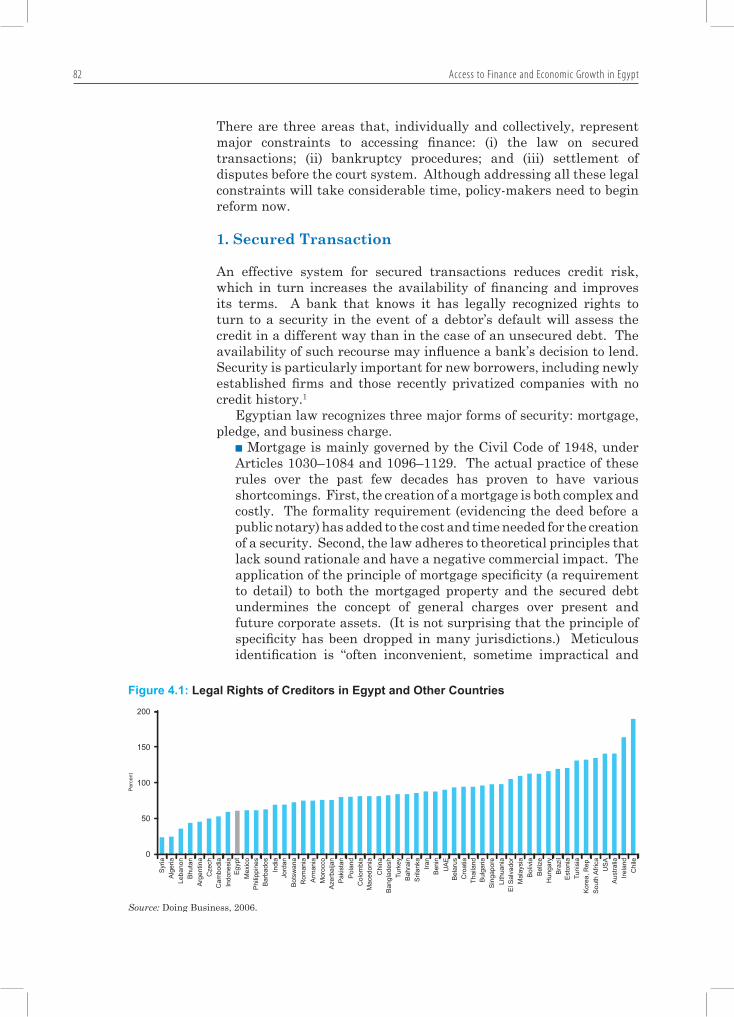

Shortcomings in rules for secured transactions have hindered access to finance. Egyptian law recognizes three major forms ofsecurity, mortgage, pledge, and business charge, which are governed by rules that have shown various shortcomings in actual practice. An index of creditors’ legal rights shows Egypt to be ranked among the lowest developing countries. The rules on enforcement are complex

Egypt does not have an enabling institutional infrastructure for a sound and efficientfinancial system

The prevailing legal framework in Egypt still constrains the cost and terms of finance

The poorly enforced collateral legislation, and the shortcomings in rules for secured transactions have hindered access to finance

Executive Summar y xxix

by design and formalistic in the extreme; procedures for enforcement are very time-consuming (notification, attachment, and sale by publicauction); the process of sale is inefficient, resulting in very modestproceeds; and private sale and strict foreclosure are not legal.

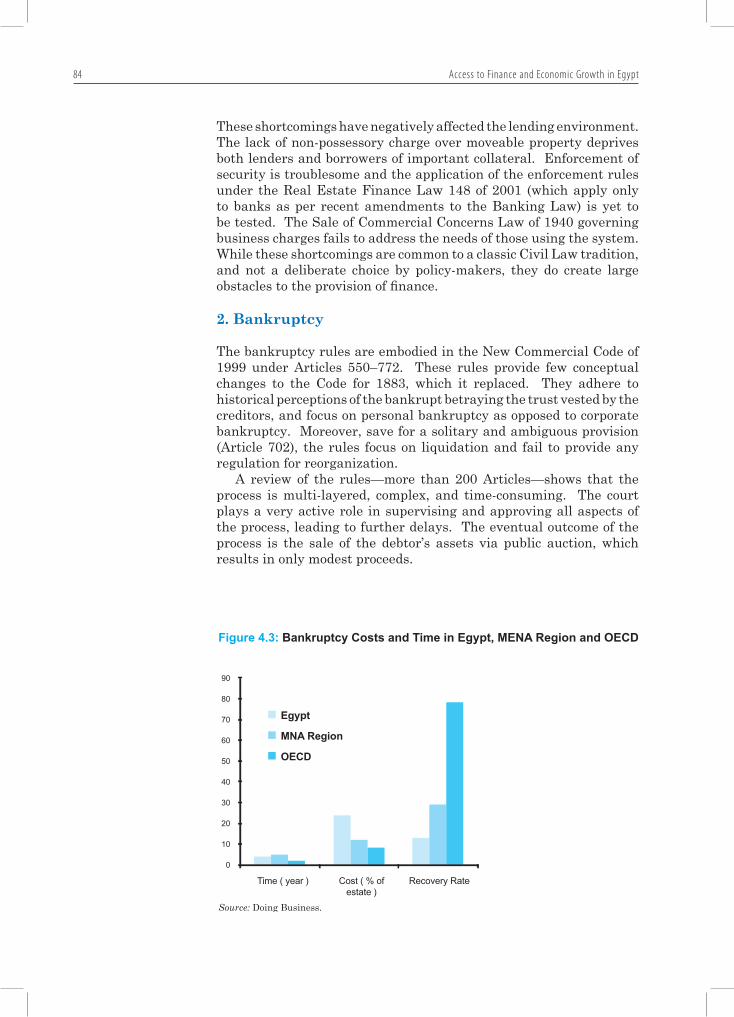

The bankruptcy rules adhere to historical perceptions of the bankrupt betraying creditors’ trust. The law focuses on personal bankruptcy, as opposed to corporate bankruptcy. Moreover, the rules rely on liquidation and fail to provide any regulation for reorganization, and the process is multi-layered, complex, and time-consuming. The court plays a very active role in supervising and approving all aspects of the process, leading to further delays. The eventual outcome which is the sale of the debtor’s assets via public auction, that results in very low proceeds. Internationally, Egypt compares unfavorably in terms of the time it takes (more than six years), the cost (more than 25 percent of the estate), and the recovery rate (less than 20 percent). Altogether, Egypt is ranked 106th globally in these dimensions.

Information Infrastructure—Credit Registry, Credit Bureau and Other Sources

Credit information in Egypt is inadequate and unreliable, and market information is poor. Bankers and firms have difficulty making soundcredit decisions due to lack of information on clients’ creditworthiness and sector-related statistics. The only source of credit information is the Public Credit Registry at the Central Bank of Egypt (CBE), which has until recently been accessible only by banks. However, a new strategy for expanding access to credit information and enhancing the information infrastructure is being implemented. Various legal, regulatory, and institutional reforms have allowed for establishing private credit bureaus and sharing credit information with non-bank financial institutions. This is expected to improve access tofinance, particularly for SMEs, as well as facilitate the developmentof independent leasing and mortgage finance companies. Theprivate credit bureau, ‘iScore’ is expected to improve the quality of information, decrease the cost of obtaining credit information, and hence the overall costs of intermediation.

Financial Reporting Environment

Another factor hampering access to finance in Egypt is the quality offinancial reporting. External users of corporate financial informationgenerally do not have enough confidence in the reliability of firms’financial statements to make their decisions, but rather rely on thecompany’s reputation, its major shareholders, and other qualitative factors. Despite progress in the setting of accounting and auditing standards, numerous deficiencies in Egypt’s current financialreporting environment still exist. There are recurring incidents of divergence between accounting standards as designed and as practiced. Investors are concerned about enforcement mechanisms and the regulatory framework for accounting and auditing

The bankruptcy rules adhere to historical perceptions of the bankrupt betraying creditors’ trust

There is a lack of information on clients’ creditworthiness and sector-related statistics

The quality of financialreporting is another factor hampering access to finance

Executive Summar yxxx

practitioners. The level of users’ confidence is further eroded by theperception that university education places insufficient emphasis onkeeping accounting curricula up to date. Small borrowers, especially, are overburdened with the high cost of maintaining appropriate accounting systems and the high cost of retaining qualified auditors. The resulting modest quality of corporate financial reporting leads toincreased risks to lenders and investors, and in turn higher costs for borrowers.

Related to the quality of financial reporting are deficiencies in theaccounting and auditing regulatory framework and its enforcement. There is no requirement for professional qualifying examination to practice auditing, no applicable peer-review practices through which auditors can provide cross-examination to each other’s working papers, and no supervisory body to monitor auditors’ working practices of auditors and enforce disciplinary actions violators. A company cannot appoint an audit firm, but rather appoints an individual partner ofa firm; as a result audit firms cannot be held liable. Various legaland institutional reforms undertaken so far to enhance accounting and auditing practices represent important interim arrangements. However, they will eventually need to be integrated under legislation that comprehensively regulates the profession.

Financial Infrastructure

Cash, cheques, and large-value inter-bank transfers are the basic means of making payments in Egypt. Cash is the major instrument for individuals, and cheques are primarily used for commercial transactions and some government payments. CBE operates the cheque-clearing system, and only one automated clearing house exists in Egypt. The CBE has led efforts to create a modernized payments-systems infrastructure to cover systems operations, policies and regulations, and oversight. To enhance efficiency, the maximumsettlement period has been reduced from five working days to at mosttwo; new instruments like direct debit have been added and payment cards have been introduced.

Nevertheless, there are challenges facing the payments system, including the legal framework covering payments and securities settlement systems, and the oversight function. Furthermore, although Egypt is one of the five top countries in terms of inflowsof remittances, there are currently no particular measures in place to control the liquidity and credit risks of cross-border transactions, or regulations specifying minimum service levels or minimum transparency requirements for international remittances or other types of cross-border payments. There is also no structured framework to improve the efficiency of remittance services.

Moreover there are deficiencies in theaccounting and auditing regulatory framework and its enforcement

Challenges facing the payments system, including the legal framework for the settlement system, and the oversight function, as well as the lack of mechanism to regulate cross-border transactions

The modest quality of corporate financialreporting leads to increased risks to lenders and investors, and in turn higher costs of borrowers

Executive Summar y xxxi

Entry and Exit Rules and Practices

The Egyptian financial system has suffered from significant entry andexit barriers. The banking system is subject to restrictive regulations such as special licenses and permits, which have prevented new entry and branch expansion, limiting competition. At the same time, banks in Egypt have not been allowed to fail. Weak banks were left to operate, while measures such as restructuring, merging or liquidation were not applied early enough. As a result, inefficient banks werekept operating and encouraged to indulge in high-risk activities, while sound banks were forced to subsidize them. However, as part of the reform program, the government has improved the rules and practices for entry and exit of banks and other financial institutions,which will ultimately increase the competitive landscape in Egypt.

Policy Recommendations

The speedy completion of the financial-sector reform program andthe restructuring of state-owned financial institutions are essentialto enhance access to financial services. Equally important isimproving the quality of the institutional environment and corporate governance. Enhancing the role of banks that have a huge branch network, of the postal system, and of microfinance institutions iscrucial for the access agenda. It is essential to improve and widen the availability of financial services in Egypt, especially for smallfirms and poor households, to enhance growth in the economy. Thesecurities issuance system; institutional investment deregulation; and the regulatory capacity and policy framework should be reformed to enhance the primary markets. Ultimately, the combination of financial restructuring and institutional reform will make Egypt’sfinancial sector more developed and efficient, leading it to providebetter-quality financial products and services, exhibiting a lower costof financial intermediation, and being more competitive.

The gains of better financial-sector development apply especiallyto small firms. Small firms that have proven their ability to surviveand grow in the marketplace can be important engines of innovation, job creation, and growth. Although both large and small firms needefficient access to financial products to remain competitive, smallfirms are typically much more growth-constrained by lack of finance.Small firms’ opportunities to develop into large, successful firms areinfluenced by a conducive overall investment climate—easy entryand exit, clearly established and protected property rights and good contract enforcement. Improving access to finance allows them tocapitalize on their growth opportunities, operate on a larger scale, and contribute more fully to economic growth.

The Egyptian financialsystem has suffered from significant entryand exit barriers as a result of which competition was limited and inefficientbanks were allowed to continue operating

The speedy completion of the financial sectorreform program and the restructuring of state-owned financial institutionsare essential to enhance financialintermediation

Improving small firmsaccess to finance allowsthem to capitalize on their growth opportunities, operate on a larger scale, and contribute more fully to economic growth

Executive Summar yxxxii

Enhancing the Role of the Banking Sector in Financial Intermediation

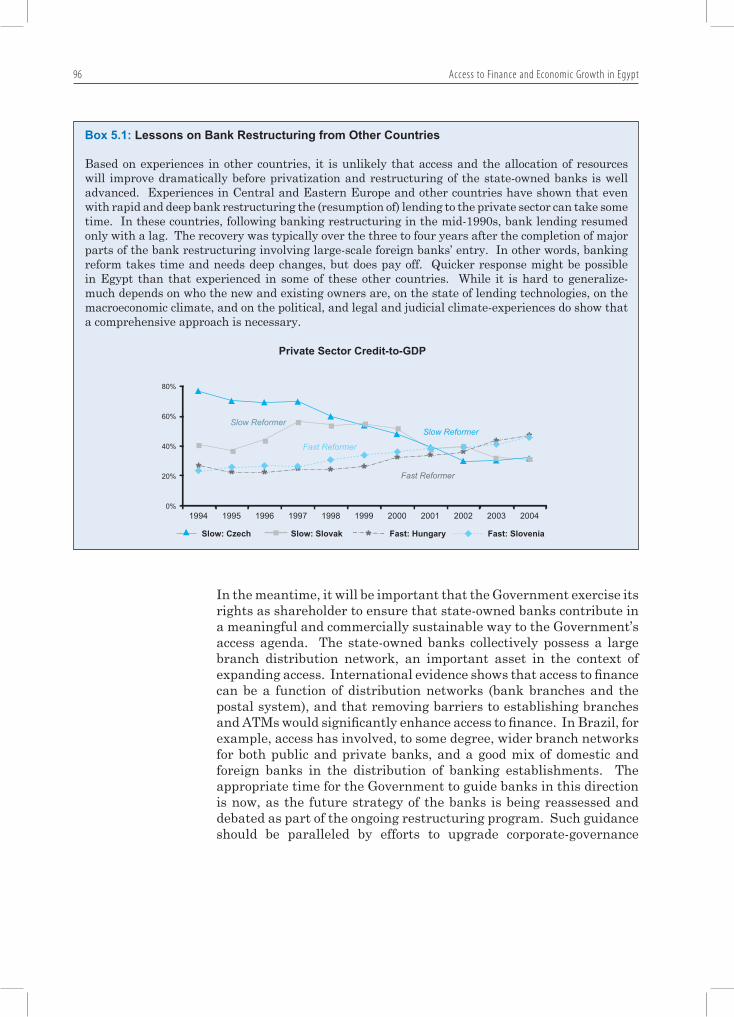

Restructuring the state-owned banks is important, not only for stability and reducing fiscal costs and contingent liabilities, butalso for access to finance. The government should also continuethe institutional restructuring of the state-owned banks that are likely to remain in public hands for some time, to assure they support a competitive market. Once the state-owned banks have been restructured and privatization is solidly underway, incentives for sound financial intermediation and a more competitive marketstructure will emerge. As private banks identify their comparative advantage and competitive niches, and as margins are squeezed in traditional markets, access to financial services for small firms andhouseholds can be expected to increase and the quality of financialservices enhanced. However, lessons from other countries suggest that reaping benefits of banking reform require a comprehensiveapproach. In depth restructuring of the state-owned banks will take time to be completely implemented, but does ultimately pay off.

Enhancing state-owned banks’ corporate governance is a vital step in the banking-sector reform agenda. It entails formulating quantifiable performance measures; specifying how the costsassociated with providing social-public services are to be covered; commissioning annual independent bank audits; and making an ongoing assessment of costs versus outcomes. The government should consider consolidating the responsibility for exercising ownership functions in the state-owned banks within a single ministry once the reform program is implemented. Sound corporate governance arrangements should clearly specify the respective responsibilities, authorities, and accountabilities of the owner, board, and executive management within a well-defined legal and institutionalinfrastructure.

It is crucial to fasten the role of specialized state-owned banks in financial intermediation, and make better use of their branchnetworks. This entails a comprehensive program for institutional, operational, and financial restructuring for these banks. Prior torestructuring these banks a formal assessment of their future is essential, including re-examining and clarifying their mandate in light of their current and prospective performance, considering whether any social and public policy objectives that remain valid can be met more cost-effectively by other means. An important context for such an assessment is a rethinking of the role of subsidized credit.