Embed Size (px)

DESCRIPTION

analis

Citation preview

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 1/40

Mega Analytics:Consumer 2013-2015Mikhail Pershin

Head of Russian Retail Practice, Accenture

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 2/40

Copyright © 2013 Accenture All rights reserved. 2

To be covered

1. Factors influencingretail in Russia

2. Consumer:expectations &

preferences

4. Retail in Russia:segments dynamic

3. Retail in Russia:channels dynamic

Retail inRussia

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 3/40

Factors influencing retailin Russia

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 4/40

Copyright © 2013 Accenture All rights reserved. 4

Three major factors that will influence theRussian retail market in 2012-2015

Consumer

preferences

Competition

Legislation

• Tightening of government regulations for tobacco and alcohol product sales

• Active government regulation of e-commerce sales

• Possible legislation changes in retail trade - reducing of the dominance limitat the municipal level from 35% to 25%

• Revenues of Top-30 retailers in Russia were 14% of the total turnover in

2012, compared to 12% in 2011, while the share of grocery retailers hasincreased from 9% to 10% respectively

• There is a shortage of quality retail and warehouse premises

• Expansion of global e-commerce retail players onto the Russian market

• Consumers are becoming more and more focused on retailers’ promises: 83%are frustrated by failure to deliver on a promise

• E-commerce market continues to increase by 25-30% annually• Price and quality are still the most important factors for consumers, and the

main drivers for growth in private label sales, up to 29% annually

• Consumers are becoming more global and mobile: the volume of cross-bordershopping is growing by about 50% per year, and has now surpassed $15 billion

Source: Infoline, research by Accenture, news resources

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 5/40

Copyright © 2013 Accenture All rights reserved. 5

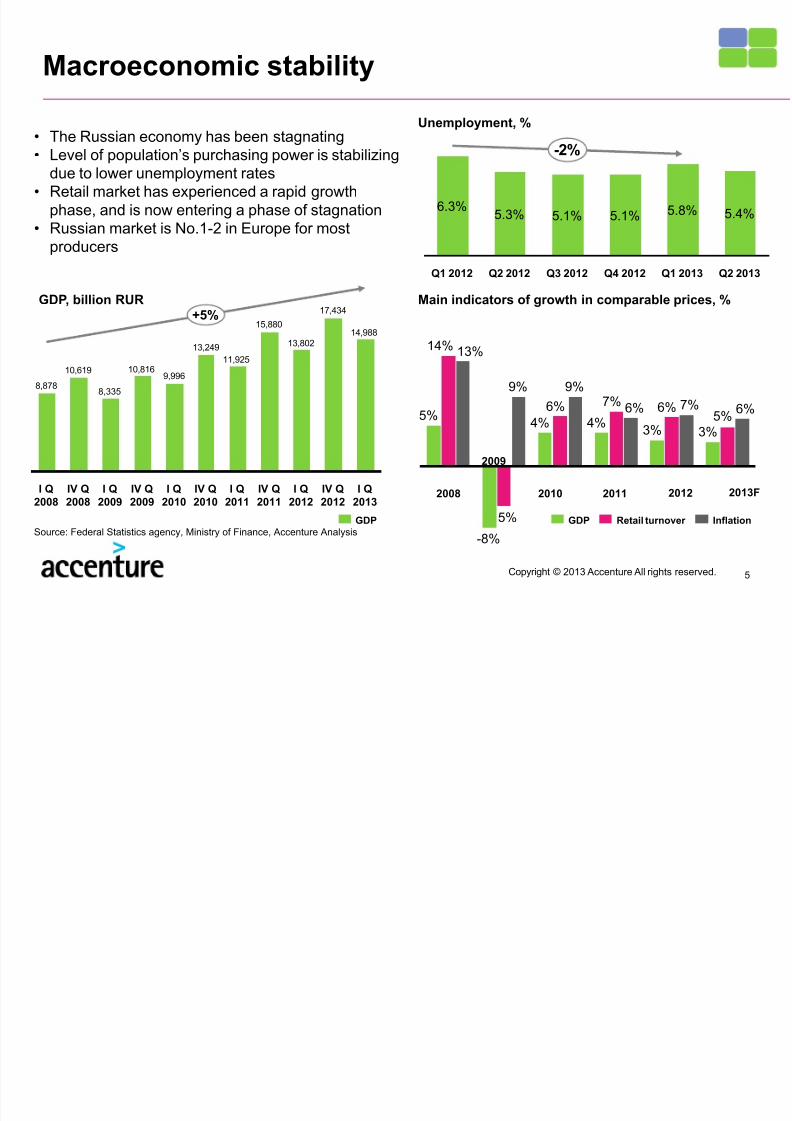

Macroeconomic stability

14,988

17,434

13,802

15,880

11,925

13,249

9,99610,816

8,335

10,619

8,878

+5%

I Q2013

IV Q2012

I Q2012

IV Q2011

I Q2011

IV Q2010

I Q2010

IV Q2009

I Q2009

IV Q2008

I Q2008

GDP

6%5%3%

7%6%

3%6%

7%

4%

9%

6%

4%

9%

5%

-8%

13%14%

5%

InflationRetail turnoverGDP

GDP, billion RUR Main indicators of growth in comparable prices, %

2008

2009

2010 2011 2012 2013F

-2%

Q2 2013

5.4%

Q1 2013

5.1% 5.8%

Q4 2012

5.1%

Q3 2012Q2 2012

5.3%

Q1 2012

6.3%

• The Russian economy has been stagnating• Level of population’s purchasing power is stabilizing

due to lower unemployment rates• Retail market has experienced a rapid growth

phase, and is now entering a phase of stagnation• Russian market is No.1-2 in Europe for most

producers

Source: Federal Statistics agency, Ministry of Finance, Accenture Analysis

Unemployment, %

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 6/40

Copyright © 2013 Accenture All rights reserved. 6

Russia now has a leading position in theEuropean retail market

• Thanks to enormous growth, as well as the

sheer size of the economy, Russia in 2012became the leader in retail turnover inEurope

• Ministry for Economic Development (MED)forecasts ~5-6% CAGR of retail turnover incomparable prices

2014F

+26%

23.8

+6%

55%

2015F

45%

47%

53%

2013F

22.6

54%

46%

2012

21.4

53%

47%

2011

19.1

52%

48%

2010

16.5

52%

48%

2009

14.6

55%51%

45%

49%

2006

25.2

8.7

13.9

55%

2007 2008

10.9

56%

44%

+14%

45%

Non-foodFood

Russian retail turnover, 2006-2015, trillion RUR

2011 2012 2013

Fact 16% 12% ?

MED forecast 5% 6.1% 5.2%

2014

5.2%(1 year prior period in comparableprices)

TOP-5 countries by retail turnover in2012, bln EURO

Russia 509.5

France 418.2

Germany 410.1

UK 377.6

Italy 253.1

Source: GFK, Federal Statistics Agency, MED forecast 2013-2015

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 7/40Copyright © 2013 Accenture All rights reserved. 7

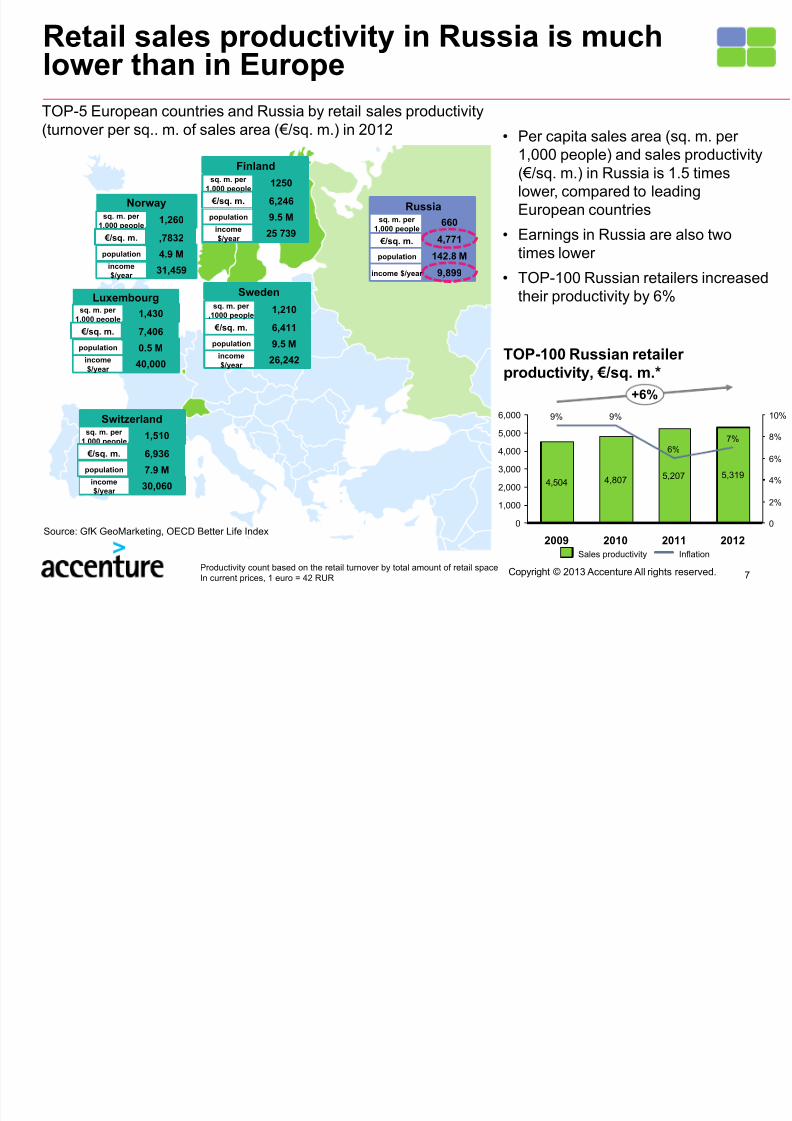

Retail sales productivity in Russia is muchlower than in Europe

4,504 4,807 5,207 5,319

0

1,000

2,000

3,000

4,000

5,000

6,000

8%

2%

4%

6%

+6%

2012

7%

2011

6%

2009

9% 9%

2010

0

10%

Norwaysq. m. per

1,000 people1,260

income

$/year31,459

population 4.9 M

Luxembourgsq. m. per

1,000 people1,430

income$/year

40,000

population 0.5 M

Switzerlandsq. m. per

1,000 people1,510

income$/year

30,060

population 7.9 M

€ /sq. m. ,7832

€ /sq. m. 7,406

€ /sq. m. 6,936

Swedensq. m. per

,1000 people1,210

income$/year

26,242

population 9.5 M

€ /sq. m. 6,411

Finlandsq. m. per

1,000 people1250

income$/year

25 739

population 9.5 M

€ /sq. m. 6,246Russia

sq. m. per1,000 people

660

income $/year 9,899

population 142.8 M

€ /sq. m. 4,771

TOP-5 European countries and Russia by retail sales productivity(turnover per sq.. m. of sales area ( €/sq. m.) in 2012

• Per capita sales area (sq. m. per1,000 people) and sales productivity( €/sq. m.) in Russia is 1.5 timeslower, compared to leadingEuropean countries

• Earnings in Russia are also twotimes lower

• TOP-100 Russian retailers increasedtheir productivity by 6%

TOP-100 Russian retailerproductivity, € /sq. m.*

Source: GfK GeoMarketing, OECD Better Life Index

Productivity count based on the retail turnover by total amount of retail spaceIn current prices, 1 euro = 42 RUR

InflationSales productivity

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 8/40

Consumer: expectations &preferences

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 9/409Copyright © 2013 Accenture All rights reserved.

Modern Russian Consumer – who is it?

493 RURI spend an average of onetrip to the store

Family

Security andWealth

Peace andJustice

30,245 RUR I received on average per month in 2013

43.5 K RURThe average amount currentpersonal loan/credit

The most important thing for me, and the importance of it is growing

Still important to me, but gradually their importance is decreasing

One of the most important words for me and over theyears their importance is growing

67%Consumers still love to goshopping and enjoy the shoppingprocess, but their volume is startingto decrease (fell by 1% comparedto 2011)

Source: Romir, FOM, Federal Statistics Agency, National Bureau of Credit Histories, GFK

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 10/40Copyright © 2013 Accenture All rights reserved. 10

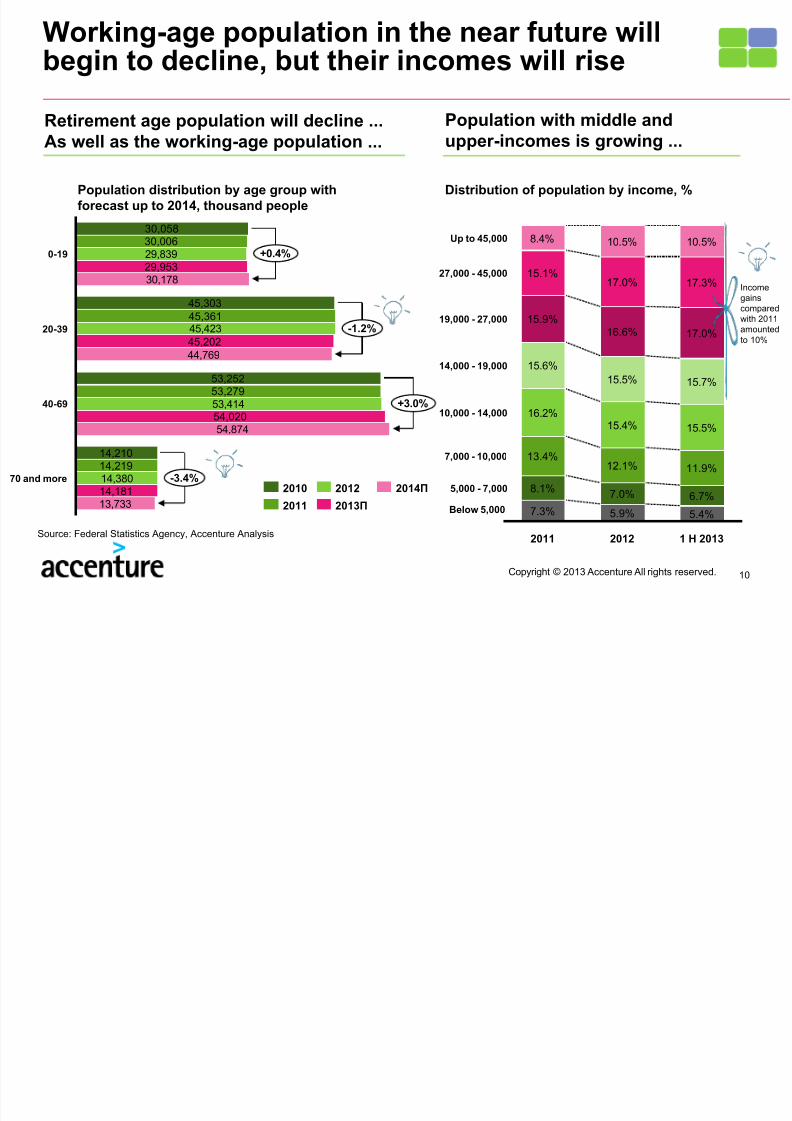

Working-age population in the near future willbegin to decline, but their incomes will rise

16.2%15.4% 15.5%

15.6%

15.5% 15.7%

8.4% 10.5% 10.5%

15.9%

15.1%

2012

17.0%

17.0%

5.9%

7.0%

12.1% 11.9%

16.6%

17.3%

2011

7.3%

8.1%

13.4%

Below 5,000

5,000 - 7,000

10,000 - 14,000

14,000 - 19,000

19,000 - 27,000

7,000 - 10,000

27,000 - 45,000

Up to 45,000

1 H 2013

5.4%

6.7%

Population with middle and

upper-incomes is growing ...

Distribution of population by income, %

Retirement age population will decline ...

As well as the working-age population ...

29,839

45,423

53,414

14,380

30,178

44,769

54,874

13,733

14,21914,210

-3.4%

+3.0%

-1.2%

+0.4%

14,181

45,36145,303

0-19

29,953

30,00630,058

40-69

54,020

70 and more

53,27953,252

20-39

45,202

2014П

2013П

2012

2011

2010

Population distribution by age group withforecast up to 2014, thousand people

Source: Federal Statistics Agency, Accenture Analysis

Incomegainscomparedwith 2011amountedto 10%

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 11/40Copyright © 2013 Accenture All rights reserved. 11

Income of Russian citizens is growing, but theywant to spend even more than they earn

30,245

26,62923,369

20,95218,63817,290

+14%

+12%

1 half2013

20122011201020092008

Average monthly income, RUR

1,922

1,534

1,7361,6191,588

1,252

316227

332270249181

Q2 2012Q1 2012

+27%

Q2 2013Q1 2013Q4 2012Q3 2012

Mortgage loansConsumer loans

Consumer and mortgage loans taken out during theperiod, billion RUR

11,72110,75410,478

10,0109,632

3,8663,8423,9233,8613,931

Q3 2012

1,2041,098

Q1 2012

1,046

+5%

Q1 2013

1,495

Q4 2012

1,337

Q2 2012

CashSecurititesSaving accounts

Accrued money savings, billion RUR

• Consumer income in 2013 has already grown by 14%

• Consumer loans have grown by 5% in Q2 2013compared to Q2 2012, and keep growing, mortgageloans have grown by 27%

• In 2013, consumers have increased savings, savingsaccounts have grown by 5%

• The volume of individuals with overdue loans in the Q22013 increased by 23%, compared to the same period

in 2012

Source: Federal Statistics agency, Accenture Analysis, Central Bank

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 12/40Copyright © 2013 Accenture All rights reserved. 12

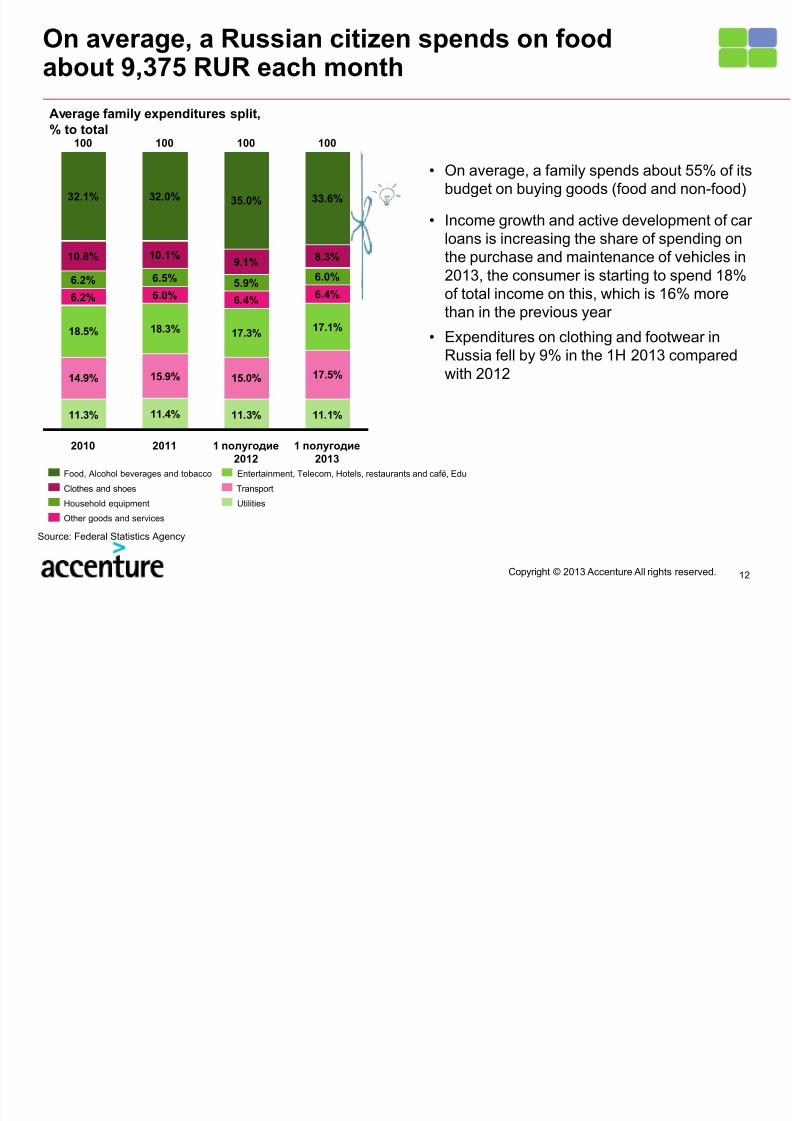

On average, a Russian citizen spends on foodabout 9,375 RUR each month

11.3% 11.4% 11.3% 11.1%

14.9% 15.9% 15.0% 17.5%

18.5% 18.3% 17.3% 17.1%

1 полугодие

2012

6.4%6.0%

8.3%

2011

35.0%

100

32.1%

1 полугодие

2013

5.9%

9.1%

6.2%

6.2%

100

10.8%

6.4%6.0%

10.1%

32.0%

6.5%

2010

100 100

33.6%

Utilities

Entertainment, Telecom, Hotels, restaurants and café, Edu

Other goods and services

Household equipment

Food, Alcohol beverages and tobacco

Clothes and shoes Transport

Average family expenditures split,% to total

Source: Federal Statistics Agency

• On average, a family spends about 55% of itsbudget on buying goods (food and non-food)

• Income growth and active development of carloans is increasing the share of spending onthe purchase and maintenance of vehicles in

2013, the consumer is starting to spend 18%of total income on this, which is 16% morethan in the previous year

• Expenditures on clothing and footwear inRussia fell by 9% in the 1H 2013 comparedwith 2012

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 13/4013Copyright © 2013 Accenture All rights reserved.

0

10

20

3040

50

60

70

80

Q2 2008

70.39%64.00%

71.59%

Q4 20102009

66.67%69.59%

Q4 2008 Q3 2011

66.86%

-6.61%

Q2 2012

Price is still the most important factor duringpurchase decisions for the consumer in Russia

Source: GFK Omnibus consumer habits

Responses to the questions:1. Price is the most important thing in making decision to buy2. I am willing to purchase essentials in several stores, if this will get me a better price and greater choice

Consumer is less ready to spend timesearching for the best deal*

0

10

20

3040

50

60

70

80

+12.38%

Q3 2011

65.55%

Q4 2010

69.90%

2009

72.46%

Q4 2008

70.15%

Q2 2008

73.67%

Q2 2012

66.03%

2007

72.13%

Price is the most important thing while buying goods*

While buying goods the most importantthing is the price*

% of those who agree % of those who agree

• 73.7% of consumers consider price as the most important thing in making decision to buy a good,with strong upward trend (growth rate of those who agreed is 12.4%)

• 66% of consumers are ready to spend additional time on searching for the best price and comparingprice in different places in order to make the best deal. This trend is declining, which can beexplained by the expansion of discounters and convenience stores.

I analyze the

price first

I won’t waste my

time looking for thelowest price

I am ready to try a new place for a better price*

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 14/4014Copyright © 2013 Accenture All rights reserved.

A lower price is more important to the consumerthan the communication with him, which cannot be saidabout the price

68%

28%4%

Neither Agree nor Disagree

Strongly Disagree – Disagree

Agree

32%28%

41%

50%37%

13%8%

54%

38%

The consumer is not willing to sacrificequality for price ...

The consumer is indifferent tocommunications with him ...

The buyer does not compare the price andthe assortment when making a choice ...

The level of service for the consumer isalmost as important as the quality *

* Response to the statement : I am willing to acceptlower levels of product quality, if it ensures I get thelowest price

* Response to the statement : I am willing to acceptlower frequency of communications, if it ensures Iget the lowest price

* Response to the statement : I am willing to acceptlower levels of customer service, if it ensures I getthe lowest price

* Response to the statement : I am willing to acceptlower levels of product ,if it ensures I get the lowestprice

Source: Accenture Consumer Pulse 2012

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 15/4015Copyright © 2013 Accenture All rights reserved.

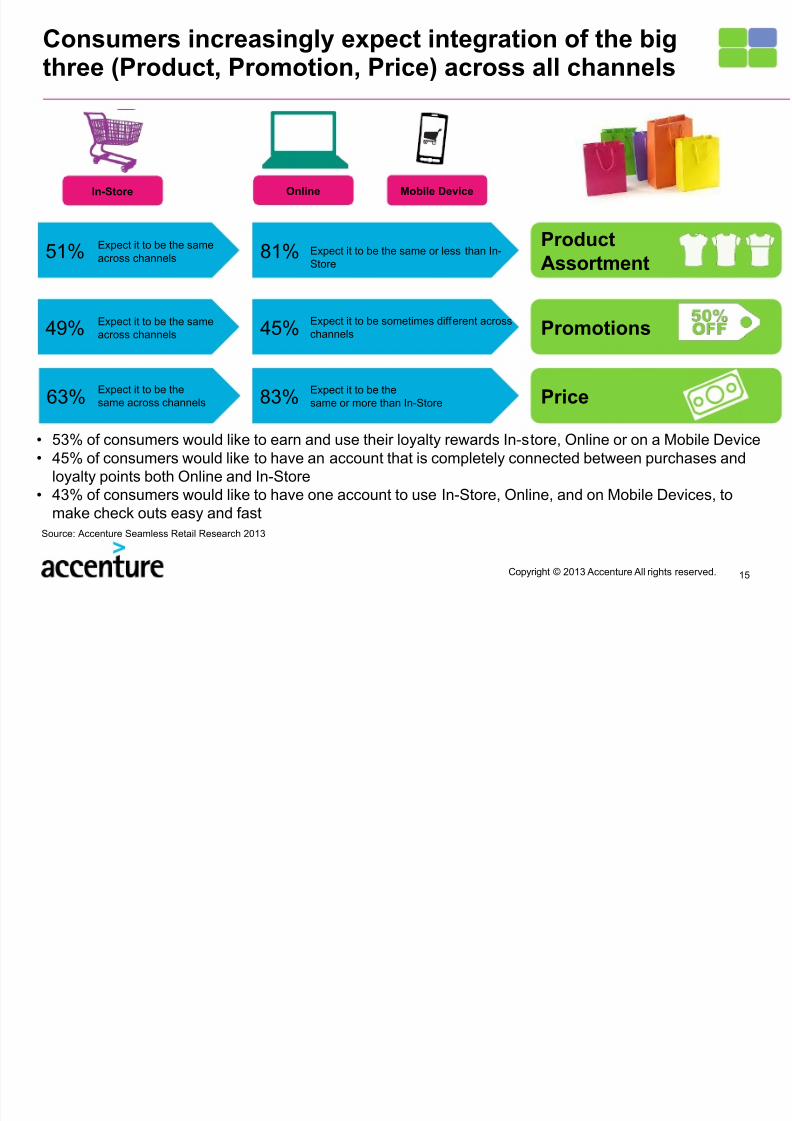

Consumers increasingly expect integration of the bigthree (Product, Promotion, Price) across all channels

In-Store Mobile DeviceOnline

ProductAssortment

Promotions

Price

51% 81%Expect it to be the sameacross channels

Expect it to be the same or less than In-Store

63% 83%Expect it to be thesame across channels

Expect it to be thesame or more than In-Store

49% 45%Expect it to be the sameacross channels

Expect it to be sometimes different acrosschannels

• 53% of consumers would like to earn and use their loyalty rewards In-store, Online or on a Mobile Device• 45% of consumers would like to have an account that is completely connected between purchases and

loyalty points both Online and In-Store• 43% of consumers would like to have one account to use In-Store, Online, and on Mobile Devices, to

make check outs easy and fastSource: Accenture Seamless Retail Research 2013

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 16/4016Copyright © 2013 Accenture All rights reserved.

Brand loyalty is still important, but it does notimply private labels do not have a bright future

98%

2%

Bulgaria Ukraine

99%

1%

Russia

89%

11%

Poland

82%

18%

CzechRepublic

79%

21%

Austria

73%

27%

National brandsPrivate labels

Share of private labels in Russia and Europe, %

Source: GFK, AC Nielsen Households Research Panel

0

20

40

60

80

100 -3%

Q2 2012

69%

Q3 2011

65%

Q4 2010

70%

2009

62%

Q4 2008

73%

Q2 2008

72%

2007

79%

2005

83%

Consumers prefer well-known brands to unknown

products*, % of those who agree

Brand-named goods are better than no-name goods

Response to the question:1. Well-known brand name goods are better than no-name goods

• Russian consumers have to constantly weigh their choice of brand versus private label. As wesee from the graph above, consumer preference for well-known brands is highly related to theeconomic conditions (lower during an economic downturn). Currently, the consumer would ratherchoose a well-known brand, and his/her intentions have become stronger during the last period

• 60% of respondents have already decided on the brand to buy before they come to the store• Despite strong adherence to well-known brands, Russians are ready to buy retailers’ private

labels as we can see from the growth of private labels turnover of 29.6% in 2012, compared to2011.

C till tl d f th i f ti

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 17/40

17Copyright © 2013 Accenture All rights reserved.

Consumers still mostly use word-of-mouth informationfrom family and friends, but with internet penetration,

online sources are growing in popularity

86% of consumers seek advice of theirrelatives and friends before making adecision to buy, 60% of these usually follow

this advice

Usage of information (% of consumers using the channel whilechoosing and making a purchase)

Usage of information sources varies withproduct category

Main info sources forsupermarkets

Main info sources for electronics Main info sources for apparel

?

21

23

31

Off line catalogues, leaflets

Word-of-mouth fromfamily and friends

Retailer corporate site

34

44

55

Search engines

Product comparison site

Retailer corporate site

29

34

37

Word-of-mouth fromfamily and friends

In store display or demo

Manufacturer corporate site

42

54

56

60

64

70

72

73

86

Online ads through banner ads,pop-up ads, etc.

Online ads in search enginesGoogle, Yandex, etc.

TV or radio ad

Online information from Social Media(Twitter, Facebook)

Print ads (newspaper, magazine)

In store information from sales peopleor displays

Corporate web site(company, brand or product website)

Online information from sources likeexpert review sites

Word-of-mouth informationfrom people I know

Source: 2012 Accenture Global Consumer Research Russia, Locata, GFK

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 18/40

18Copyright © 2013 Accenture All rights reserved.

Consumer expects retailers to deliver on theirpromise

83% of consumers feel frustrationwhen they do not get whatwas promised from acompany

78% of consumers will switchto another seller in suchcase

Source: Accenture Consumer Pulse

The consumer constantly monitors the company and its promises, and cares more about relations to his\her needs*

58%

47%

63%

83%

76%

74%

29%

47%

Promised one thing but delivered another

Employees are not knowledgeable or do not acknowledgeconsumer’s specific needs when considering a purchase

Company does not make it easy to do business with them

Unable to access information or buy a product/service usingmultiple channels

The company asks me the same questions or market s to me

the same offer againInconsistent offers through different channels when shopping

for the same product or service

The company is not using personal information to makeinteractions and offers more relevant

Inconsistent experience of treatment when using differentchannels

Responses to the question:1. For each of the following situations, please indicate the extent to which you personallyfind frustrating, and affect your buying choices?

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 19/40

19Copyright © 2013 Accenture All rights reserved.

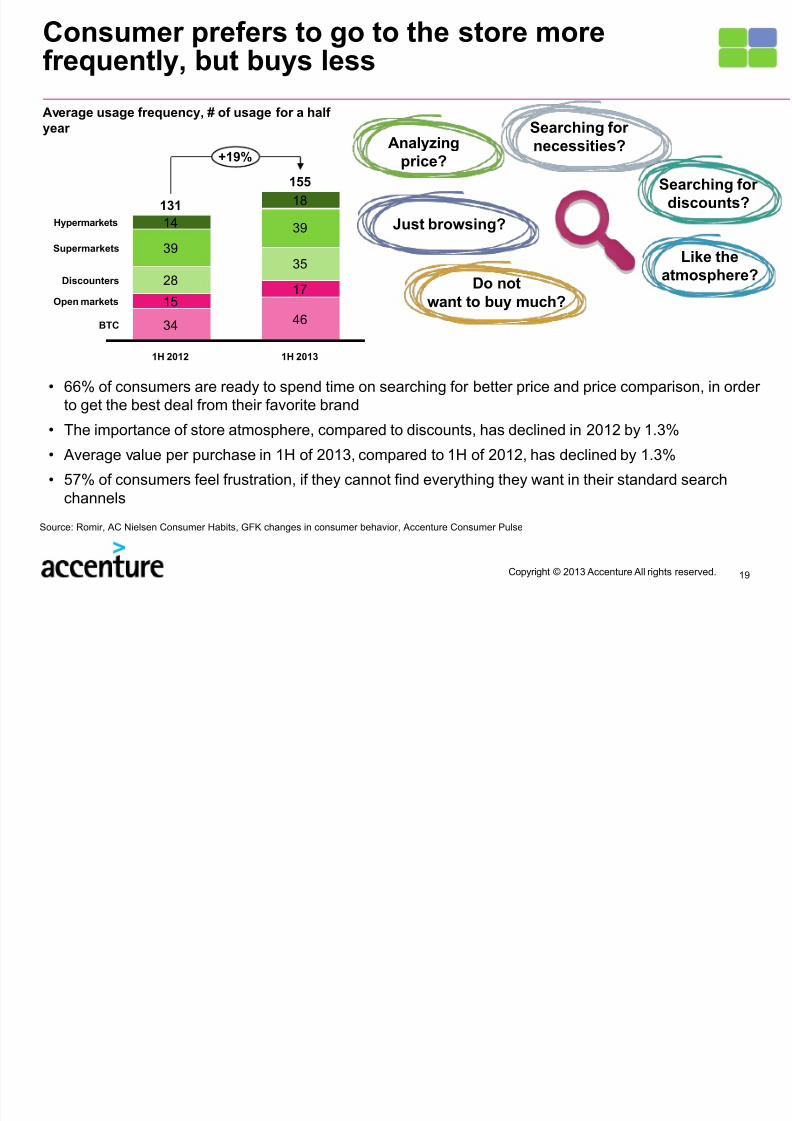

Consumer prefers to go to the store morefrequently, but buys less

34 46

28

35

39

39

Supermarkets

+19%

Hypermarkets

BTC

1H 2013

Open markets

155

Discounters17

18

1H 2012

131

15

14

Average usage frequency, # of usage for a halfyear

Source: Romir, AC Nielsen Consumer Habits, GFK changes in consumer behavior, Accenture Consumer Pulse

• 66% of consumers are ready to spend time on searching for better price and price comparison, in orderto get the best deal from their favorite brand

• The importance of store atmosphere, compared to discounts, has declined in 2012 by 1.3%

• Average value per purchase in 1H of 2013, compared to 1H of 2012, has declined by 1.3%

• 57% of consumers feel frustration, if they cannot find everything they want in their standard searchchannels

Do notwant to buy much?

Like the

atmosphere?

Analyzingprice?

Just browsing?

Searching fordiscounts?

Searching for

necessities?

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 20/40

20Copyright © 2013 Accenture All rights reserved.

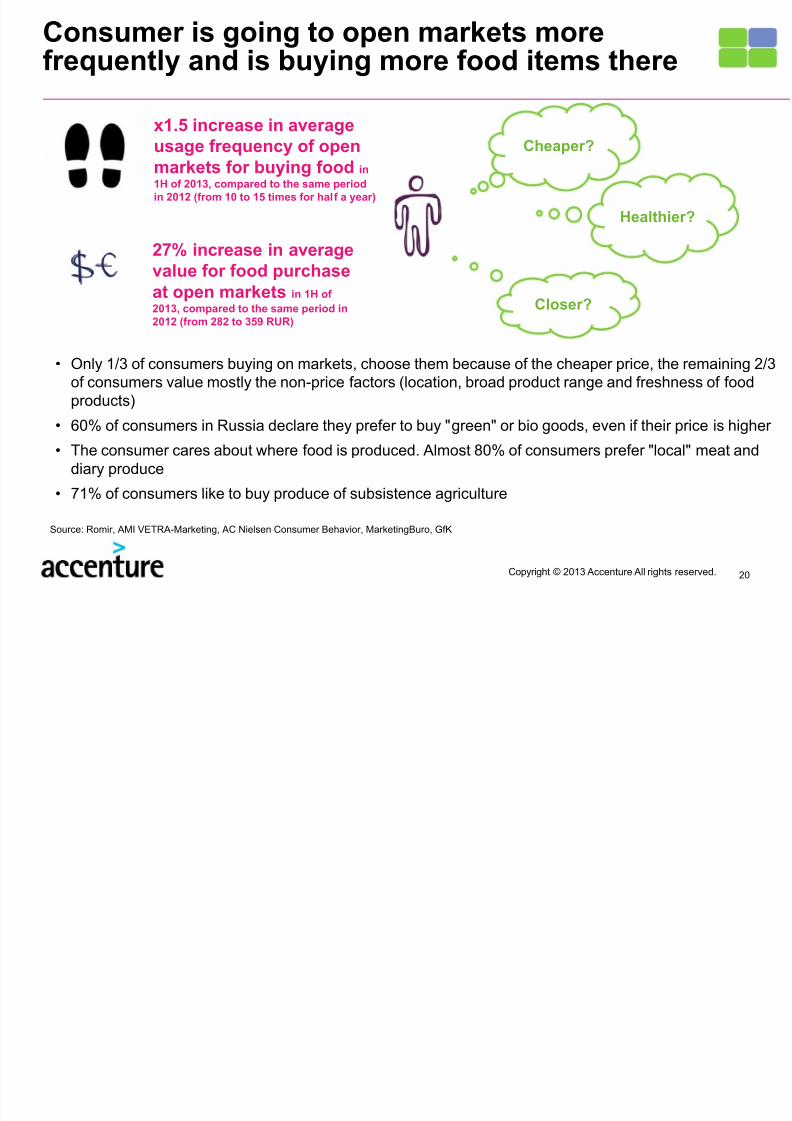

Consumer is going to open markets morefrequently and is buying more food items there

x1.5 increase in average

usage frequency of openmarkets for buying food in

1H of 2013, compared to the same periodin 2012 (from 10 to 15 times for half a year)

27% increase in average

value for food purchaseat open markets in 1H of

2013, compared to the same period in2012 (from 282 to 359 RUR)

Cheaper?

Healthier?

Closer?

• Only 1/3 of consumers buying on markets, choose them because of the cheaper price, the remaining 2/3of consumers value mostly the non-price factors (location, broad product range and freshness of foodproducts)

• 60% of consumers in Russia declare they prefer to buy "green" or bio goods, even if their price is higher

• The consumer cares about where food is produced. Almost 80% of consumers prefer "local" meat anddiary produce

• 71% of consumers like to buy produce of subsistence agriculture

Source: Romir, AMI VETRA-Marketing, AC Nielsen Consumer Behavior, MarketingBuro, GfK

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 21/40

21Copyright © 2013 Accenture All rights reserved.

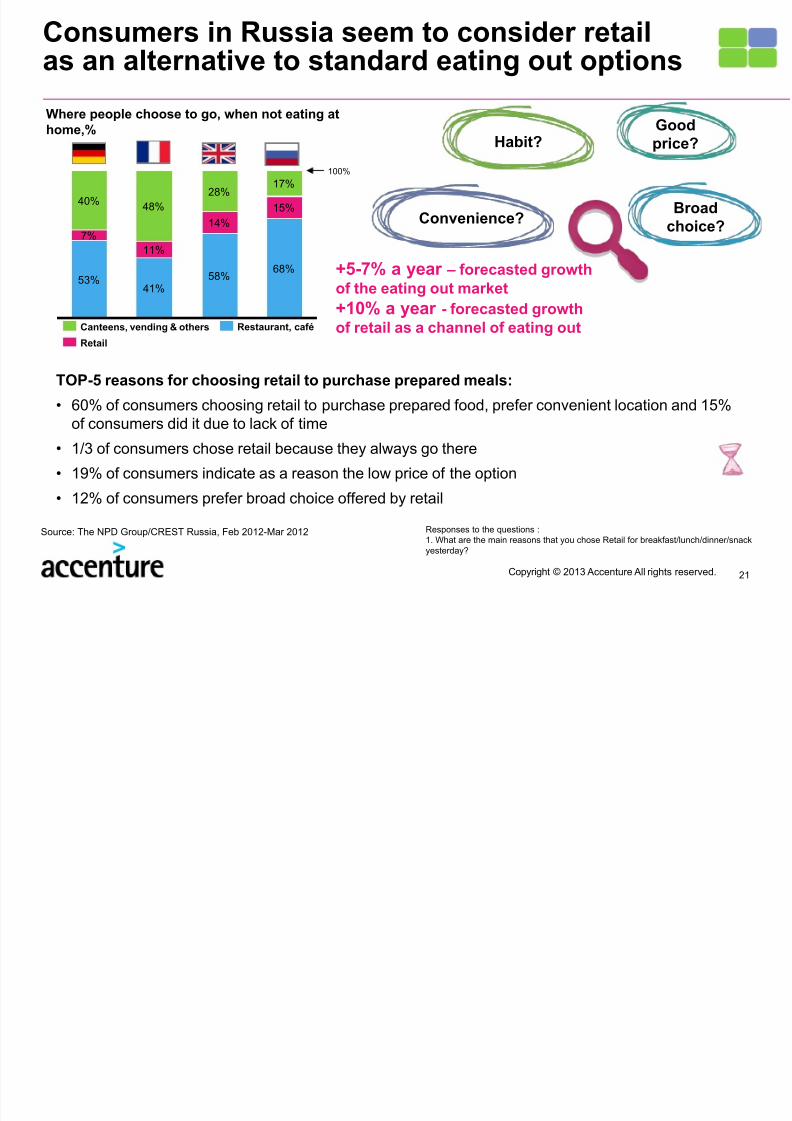

Consumers in Russia seem to consider retailas an alternative to standard eating out options

40%48%

28%17%

100%

68%

15%

58%

14%

41%

11%

53%

7%

Where people choose to go, when not eating athome,%

Broadchoice?

Habit?

Convenience?

Good

price?

Restaurant, café

Retail

Canteens, vending & others

TOP-5 reasons for choosing retail to purchase prepared meals:

• 60% of consumers choosing retail to purchase prepared food, prefer convenient location and 15%of consumers did it due to lack of time

• 1/3 of consumers chose retail because they always go there

• 19% of consumers indicate as a reason the low price of the option

• 12% of consumers prefer broad choice offered by retail

Source: The NPD Group/CREST Russia, Feb 2012-Mar 2012

+5-7% a year – forecasted growthof the eating out market

+10% a year - forecasted growthof retail as a channel of eating out

Responses to the questions :1. What are the main reasons that you chose Retail for breakfast/lunch/dinner/snackyesterday?

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 22/40

Retail in Russia:channels dynamic

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 23/40

Copyright © 2013 Accenture All rights reserved. 23

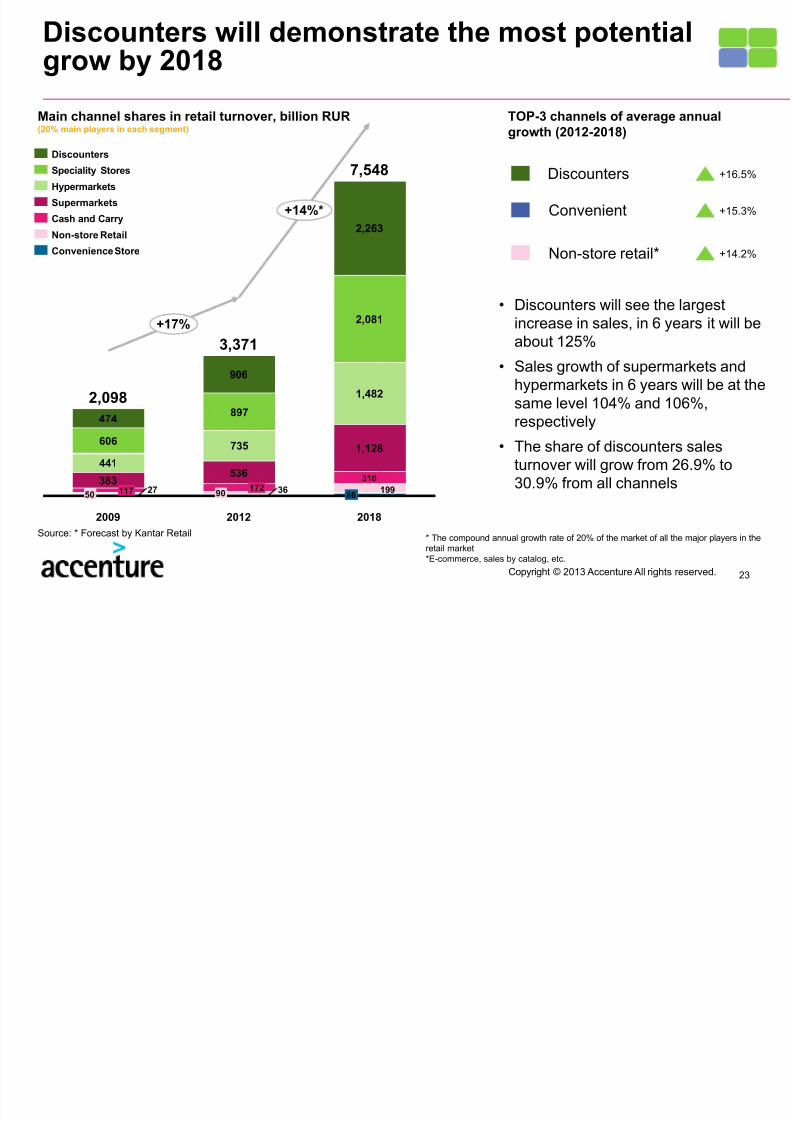

Discounters will demonstrate the most potentialgrow by 2018

Main channel shares in retail turnover, billion RUR(20% main players in each segment)

TOP-3 channels of average annualgrowth (2012-2018)

Discounters +16.5%

Convenient +15.3%

Non-store retail* +14.2%

• Discounters will see the largestincrease in sales, in 6 years it will beabout 125%

• Sales growth of supermarkets andhypermarkets in 6 years will be at thesame level 104% and 106%,

respectively

• The share of discounters salesturnover will grow from 26.9% to30.9% from all channels

Source: * Forecast by Kantar Retail

441

735606

897

3627 199

+14%*

+17%

2018

7,548

86

310

1,128

1,482

2,081

2,263

2012

3,371

90172

536

906

2009

2,098

50 117383

474

Convenience Store

Non-store Retail

Cash and Carry

Supermarkets

Hypermarkets

Speciality Stores

Discounters

* The compound annual growth rate of 20% of the market of all the major players in theretail market

*E-commerce, sales by catalog, etc.

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 24/40

Copyright © 2013 Accenture All rights reserved. 24

Hypermarkets have become the most fast-growing saleschannel in 1H 2013, thanks to rising average frequency

• Hypermarkets have become the most fast-growing channel in 1H 2013, due to rising penetration rate and

average usage frequency

• Modern retail is losing its share in the 1H of 2013, which is connected to rising popularity of open foodmarkets average usage frequency, and the greater variety of food offered there

• In 1H of 2013, average usage frequency of hypermarkets has increased with slightly decreasing averagevalue per purchase

Channel share in consumer expenditures and keydrivers in 1H 2013, %

Channel share

0.87%

-1.17%

# SKU

7.69%

-1.37%

Average valueper purchase

-4.63%

2.97%

Averagefrequency

22.90%

15.67%Traditional trade

Modern trade

Main indicators change in 1H 2013 to 1H 2012, %

Source: Romir

5.20%6.10%

4.00%

16.30%

3.00%

6.10%

9.30%

0

1

2

3

4

5

6

7

8

9

0 500 1,000 1,500 2,000

Average valueper purchase,RUR

DIY

1.20%Electronics

DrogeryClothing and footwear

E-commerce

Open markets

Discounter

13.80%

BTC

Supermarket

16.70%

Hypermarket

Averagefrequency,per month

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 25/40

25Copyright © 2013 Accenture All rights reserved.

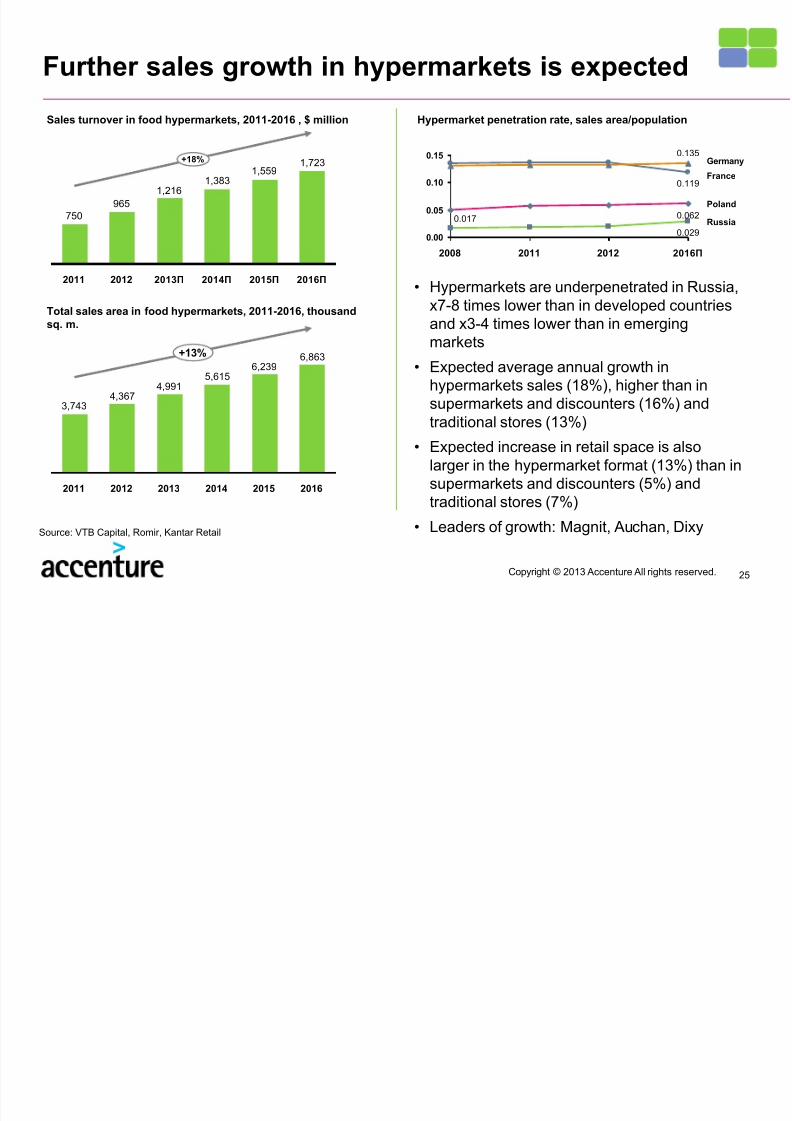

Further sales growth in hypermarkets is expected

• Hypermarkets are underpenetrated in Russia,x7-8 times lower than in developed countriesand x3-4 times lower than in emergingmarkets

• Expected average annual growth inhypermarkets sales (18%), higher than insupermarkets and discounters (16%) and

traditional stores (13%)

• Expected increase in retail space is alsolarger in the hypermarket format (13%) than insupermarkets and discounters (5%) andtraditional stores (7%)

• Leaders of growth: Magnit, Auchan, Dixy

Sales turnover in food hypermarkets, 2011-2016 , $ million

1,7231,559

1,3831,216

965

750

+18%

2016П 2015П 2014П 2013П 20122011

6,8636,239

5,6154,991

4,3673,743

+13%

201620152014201320122011

Total sales area in food hypermarkets, 2011-2016, thousandsq. m.

0.119

0.135

0.062

0.029

0.017

0.00

0.05

0.10

0.15Germany

Poland

Russia

France

2016П 201220112008

Hypermarket penetration rate, sales area/population

Source: VTB Capital, Romir, Kantar Retail

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 26/40

26Copyright © 2013 Accenture All rights reserved.

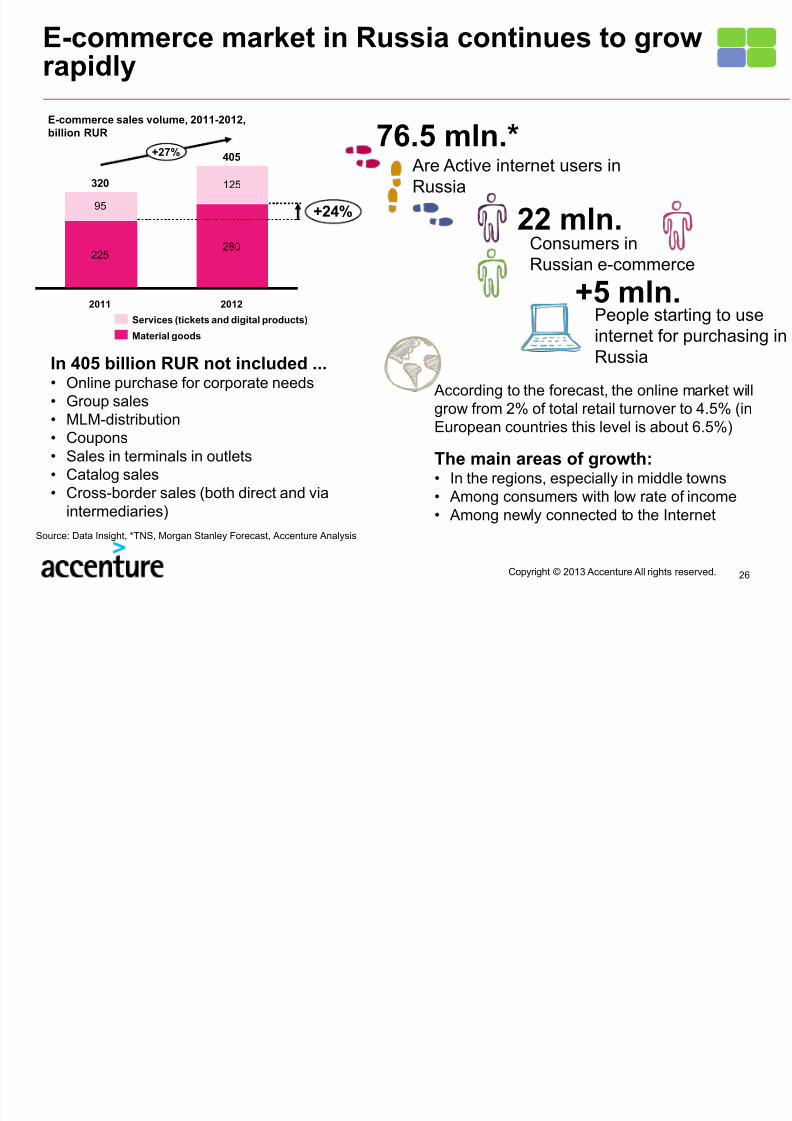

E-commerce market in Russia continues to growrapidly

95

125

+27% 405

+24%

2012

280

2011

320

225

Material goods

Services (tickets and digital products)

E-commerce sales volume, 2011-2012,billion RUR

In 405 billion RUR not included ...• Online purchase for corporate needs• Group sales

• MLM-distribution• Coupons• Sales in terminals in outlets• Catalog sales• Cross-border sales (both direct and via

intermediaries)

Source: Data Insight, *TNS, Morgan Stanley Forecast, Accenture Analysis

22 mln.Consumers inRussian e-commerce

+5 mln.People starting to useinternet for purchasing inRussia

The main areas of growth:• In the regions, especially in middle towns• Among consumers with low rate of income• Among newly connected to the Internet

According to the forecast, the online market willgrow from 2% of total retail turnover to 4.5% (inEuropean countries this level is about 6.5%)

76.5 mln.* Are Active internet users inRussia

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 27/40

Copyright © 2013 Accenture All rights reserved. 27

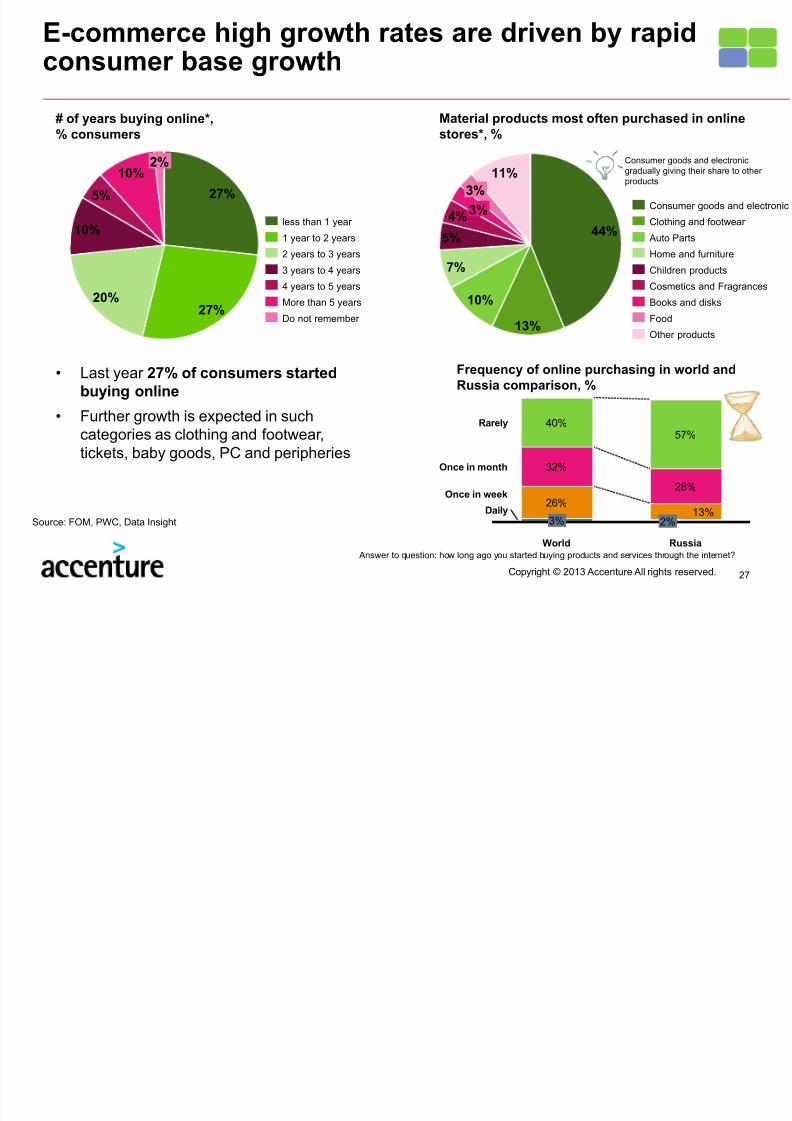

E-commerce high growth rates are driven by rapidconsumer base growth

20%27%

5%

2%

10%

10%

27%

4 years to 5 years

3 years to 4 years

Do not remember

2 years to 3 years

1 year to 2 years

More than 5 years

less than 1 year

# of years buying online*,% consumers

Answer to question: how long ago you started buying products and services through the internet?

Material products most often purchased in onlinestores*, %

Source: FOM, PWC, Data Insight

• Last year 27% of consumers startedbuying online

• Further growth is expected in suchcategories as clothing and footwear,tickets, baby goods, PC and peripheries

Frequency of online purchasing in world andRussia comparison, %

Daily

Rarely

Russia

2%

26%

3%13%

28%Once in week

57%

World

32%

40%

Once in month

7%

11%

10%

3%

3%4%

5%

13%

44%

Other products

Food

Books and disks

Cosmetics and Fragrances

Children products

Home and furniture

Auto Parts

Clothing and footwear

Consumer goods and electronic

Consumer goods and electronicgradually giving their share to otherproducts

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 28/40

28Copyright © 2013 Accenture All rights reserved.

Main e-commerce players are still representinga small part of entire e-commerce sales market

82%

18%

48% 52%

Remaining players

TOP-10 e-commerce stores

Level of e-commerce sales concentration, 2012

Russia USA

Market volume~$13 billion

Market volume~$184 billion

Source: Digital Guru, Data Insight, Accenture Analysis

• 5-8 million purchases (forpersonal use and not for resale)

during 2012• ~ 45 billion rubles of turnover(16% of sales of tangible goods)

• ~ 2 million consumers (10% oftotal)

• Purchases increase by morethan 50% in 2012

New global players on the Russian e-commercemarket :

Plans to double their performance in Russia

In the next 2.5 years, eBay plans to increase sales in Russiaby 4 times, and users by 6 times. Company turnover inRussia already has reached $400 million

Opened an office in RussiaCross-border shopping - thefastest growing and at the sametime the most unclear marketsegment

TOP-10 online stores turnover in 2012, $ billion/ year

188147150134

168231

187

493

297

774

211

947134

12768

286

115

290433

UtkonosKupiVip.ruOzonSvyaznoyExist.ruUlmart M.VideoBiglionSotmarketWilf-Berries

600

Holodilnik

2011

2012

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 29/40

Copyright © 2013 Accenture All rights reserved. 29

64

2

2

3

3

5

5

6

10

3

1

3

5

7

5

6

22

59

virtual bank card online

SMS

bank card upon receiving

internet banking

payment terminal

bank transfer in the bank

electronic money

bank card online

Cash upon receiving

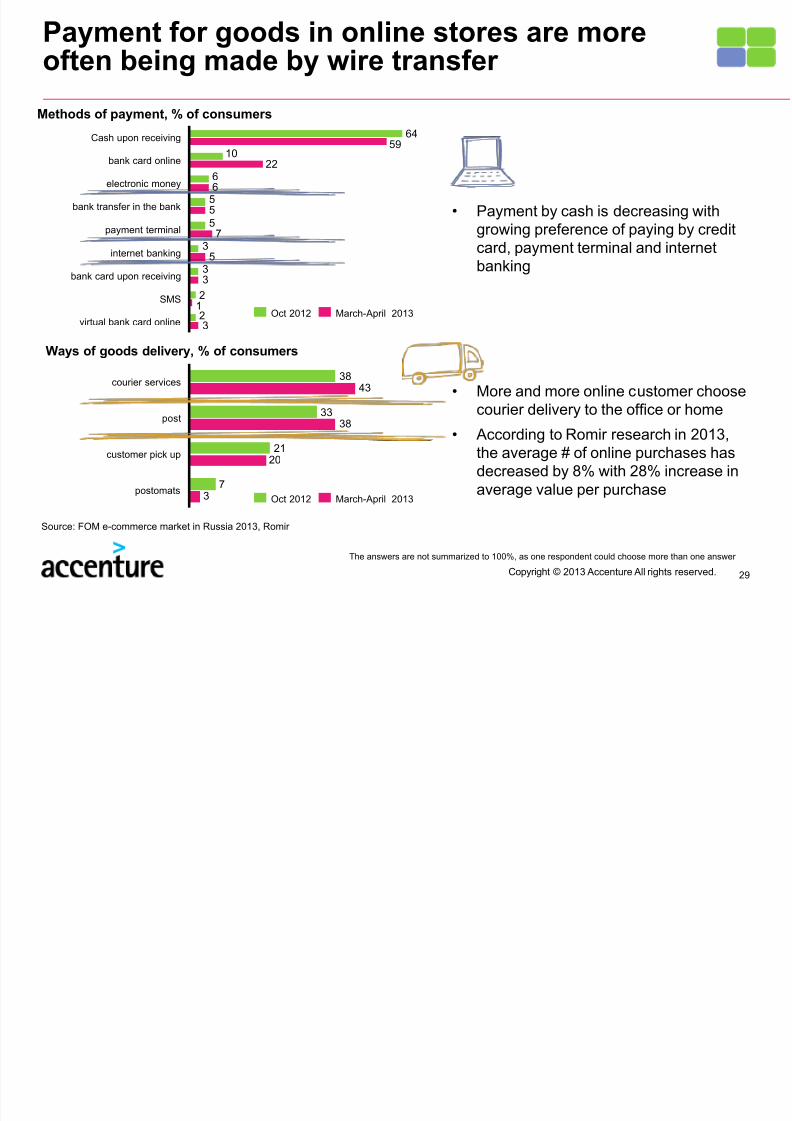

Payment for goods in online stores are moreoften being made by wire transfer

Methods of payment, % of consumers

March-April 2013Oct 2012

The answers are not summarized to 100%, as one respondent could choose more than one answer

• Payment by cash is decreasing withgrowing preference of paying by creditcard, payment terminal and internetbanking

• More and more online customer choosecourier delivery to the office or home

• According to Romir research in 2013,the average # of online purchases hasdecreased by 8% with 28% increase inaverage value per purchase

Ways of goods delivery, % of consumers

7

21

33

38

3

20

38

43

customer pick up

postomats

post

courier services

March-April 2013Oct 2012

Source: FOM e-commerce market in Russia 2013, Romir

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 30/40

Retail in Russia:segments dynamic

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 31/40

Copyright © 2013 Accenture All rights reserved. 31

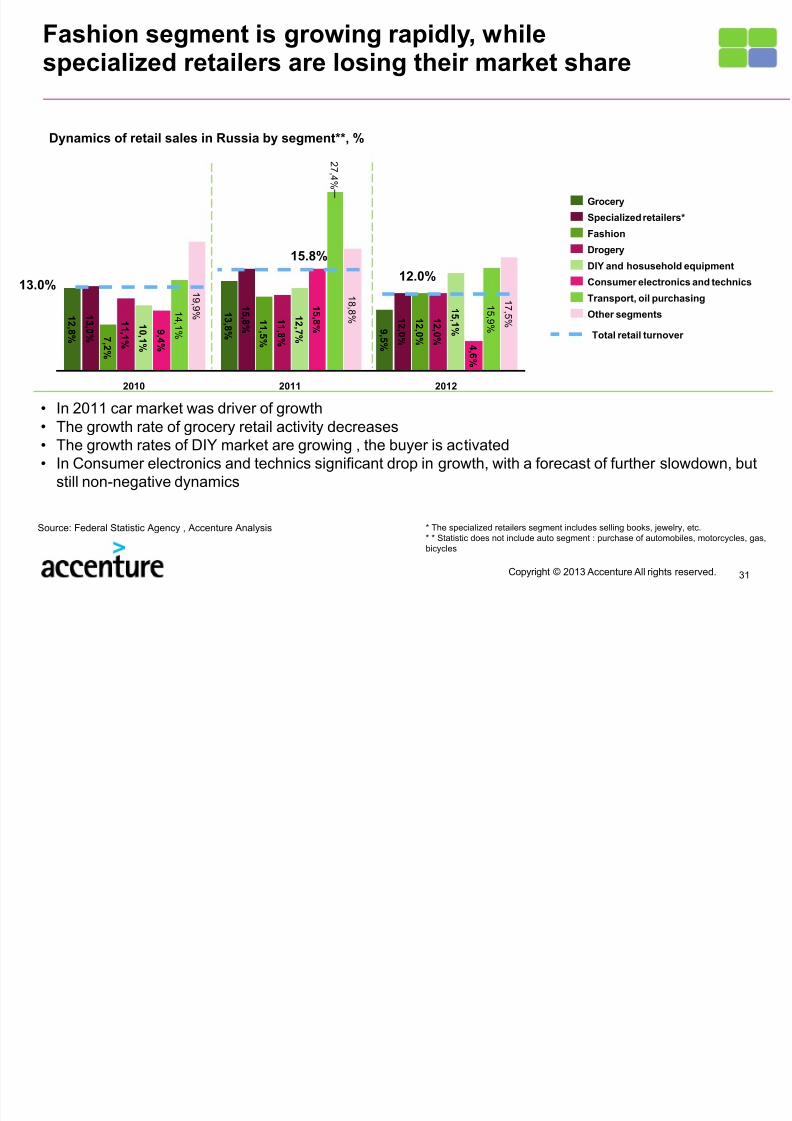

Fashion segment is growing rapidly, whilespecialized retailers are losing their market share

2012

1 7 , 5 %

1 5 , 9 %

4 , 6 %

1 5 ,1 %

1 2 , 0 %

1 2 , 0 %

1 2 , 0 %

9 , 5 %

2011

1 8 , 8 %

2 7 ,4 %

1 5 , 8 %

1 2 ,7 %

1 1 , 8 %

1 1 , 5 %

1 5 , 8 %

1 3 , 8 %

2010

1 9 , 9 %

1 4 ,1 %

9 ,4 %

1 0 ,1 %

1 1 ,1 %

7 ,2 %

1 3 , 0 %

1 2 , 8 %

Other segments

Transport, oil purchasing

Consumer electronics and technics

DIY and hosusehold equipment

Drogery

Fashion

Specialized retailers*

Grocery

Source: Federal Statistic Agency , Accenture Analysis

Dynamics of retail sales in Russia by segment**, %

• In 2011 car market was driver of growth• The growth rate of grocery retail activity decreases• The growth rates of DIY market are growing , the buyer is activated• In Consumer electronics and technics significant drop in growth, with a forecast of further slowdown, but

still non-negative dynamics

13.0%

15.8%

12.0%

Total retail turnover

* The specialized retailers segment includes selling books, jewelry, etc.* * Statistic does not include auto segment : purchase of automobiles, motorcycles, gas,bicycles

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 32/40

32Copyright © 2013 Accenture All rights reserved.

Grocery retail: the market growth rates of foodretail network are declining

The share and dynamics of grocery chains inthe total retail turnover, %

192022

14

23

34

42

0

5

10

15

20

25

30

35

40

45

0.03

0.10

0.00

0.04

0.05

0.06

0.07

0.08

0.09

0.01

0.02

2013П

14%

2012

15%

2011

12%

2006

11%

2010

13%

2009

13%

2008

15

11%

2007

14%

Share in retail turnover, % Growth rate, %

• The entire food market grew by 8.7% in2012, mainly due to inflation

• In retail turnover in 2012, the share offood retail chains is about 15%, 1 p.p.increase compared to 2011. But in 2013,1% decline is forecasted due to slowergrowth rates of 18-19%

• In the first half of 2013, the leader of foodretail has changed. The new leaderMagnit has overcome the X5 RetailGroup, not only by the number of stores,

but also by sales

Source: RBC Research, Romir

Decline in theshare by 1%

BillionRUR

DIY and Household retail: dynamic market share

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 33/40

33Copyright © 2013 Accenture All rights reserved.

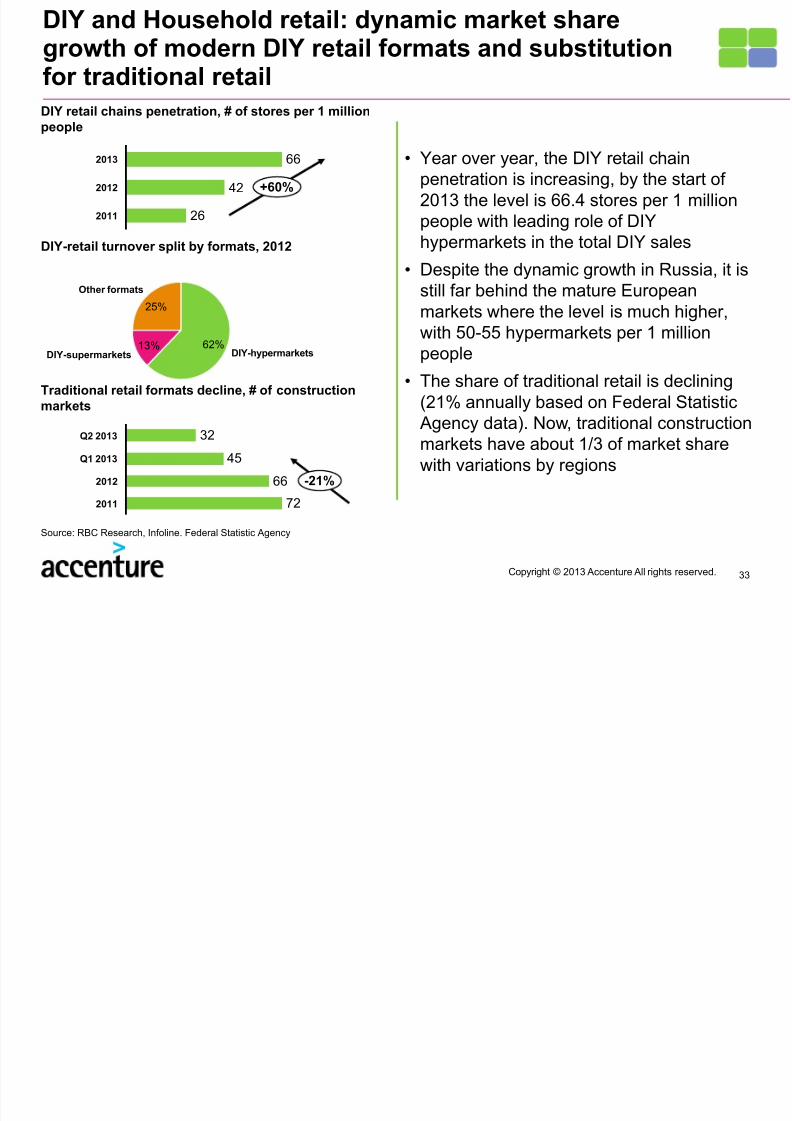

DIY and Household retail: dynamic market sharegrowth of modern DIY retail formats and substitutionfor traditional retailDIY retail chains penetration, # of stores per 1 millionpeople

• Year over year, the DIY retail chainpenetration is increasing, by the start of2013 the level is 66.4 stores per 1 millionpeople with leading role of DIYhypermarkets in the total DIY sales

• Despite the dynamic growth in Russia, it isstill far behind the mature Europeanmarkets where the level is much higher,with 50-55 hypermarkets per 1 millionpeople

• The share of traditional retail is declining(21% annually based on Federal Statistic

Agency data). Now, traditional constructionmarkets have about 1/3 of market sharewith variations by regions

DIY-hypermarkets

Other formats

13%

25%

DIY-supermarkets62%

26

42

66

2011

+60%2012

2013

DIY-retail turnover split by formats, 2012

72

66

45

32Q2 2013

2011

2012

Q1 2013

-21%

Traditional retail formats decline, # of constructionmarkets

Source: RBC Research, Infoline. Federal Statistic Agency

DIY d H h ld t il i t ti l DIY h i

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 34/40

34Copyright © 2013 Accenture All rights reserved.

DIY and Household retail: international DIY chainskeep their leading positions in the segment

Top-3 DIY retailers, sales, billion RUR, 2012

• TOP-3 retailers in 2012 are international chains:Leroy Merlin, OBI, Castorama

• But leading positions vary by regions

• The regional expansion of majority of DIY chains isslowing (Castorama, OBI, Home Center, K-Rauta,“Starik Khottabych", "СSuperStroy", etc.)

• DIY retail market keeps consolidating, thecompetition between Russian and global markets isrising

• DIY retail logistics function has grown in 2012, dueto new distribution centers construction, suppliesautomatization and logistics outsourcing

21

35

77

CastoramaOBILeroy Merlin

7

7

8

14

7

10

17

0

7

8

13

6

16

18

0

2

8

11

10

8

5

Severo-Zapadny

Central

Dalnevostochny

Sibirsky

Urals

Yuzhny

Privolzhsky

Castorama

OBI

Leroy Merlin

% of consumers visited TOP-3 retailers by regions,

1H of 2013

Source: RBC.Research, Federal Statistic Agency

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 35/40

35Copyright © 2013 Accenture All rights reserved.

Consumer Electronics: smartphone and tabletssales boost electronics segment growth

• Consumer Electronics and Technics becomes“stock exchange” item: you can easily check price,

price competition become lower and lower,consumer actively use Omni channel

• Structure of portable electronics sales activelychanging:

• In the first half of 2013 smartphone salesaccounted for 79% of mobile phone markets

• Smartphone sales in product terms exceedlaptop/netbook sales

• The highest growth rate is shown by tablet

PC market (239% compared to the previousperiod)

Source: Research by Evroset Company

7.35.12.91.1

10.410.511.413.4

1H 2013

76.0

1H 2012

53.5

1H 2011

32.6

1H 2010

14.2

Average price, ’000 RUR Sales, bln RUR#, bln

20.318.4

12.52.6

0.80.1

1H 2013

33.1

1H 2012

14.3

1H 2011

2.8

Average price, ’000 RUR Sales, bln RUR#, bln

Tablet market dynamics, 2011-2013

Smartphone market dynamics, 2010-2013

F hi t il th t ti l i i ll

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 36/40

36Copyright © 2013 Accenture All rights reserved.

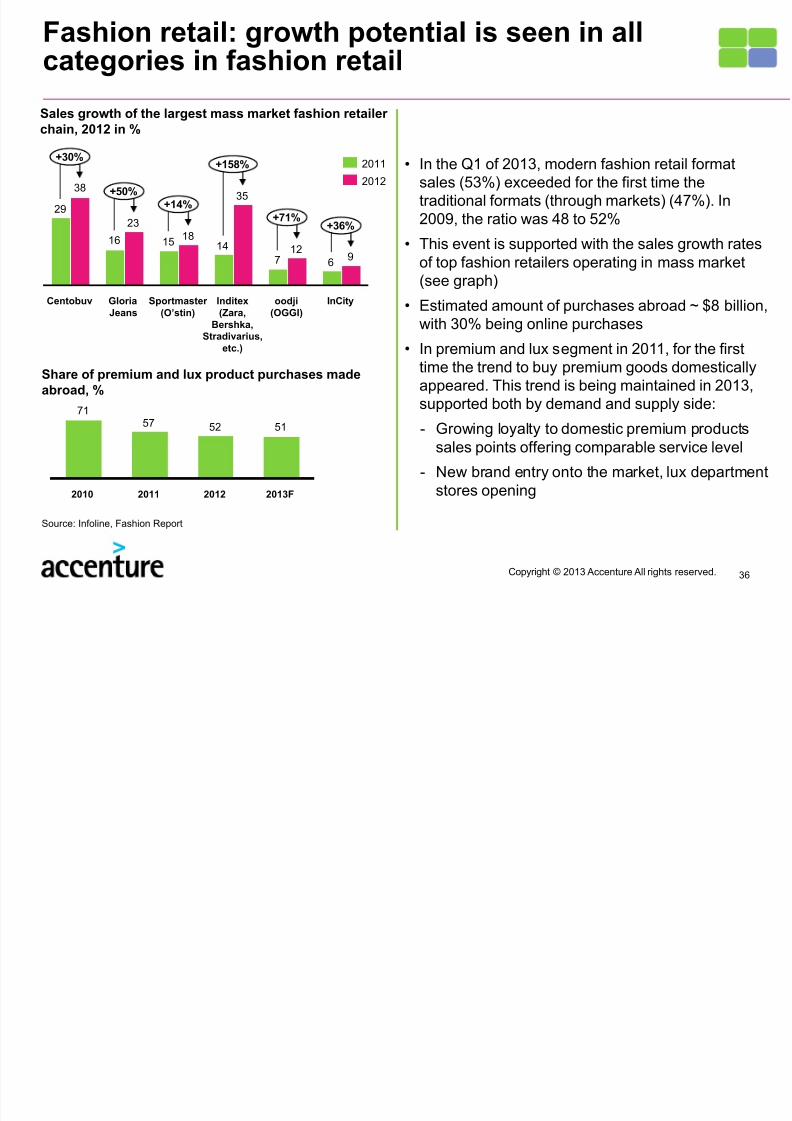

Fashion retail: growth potential is seen in allcategories in fashion retail

Share of premium and lux product purchases madeabroad, %

Sales growth of the largest mass market fashion retailerchain, 2012 in %

• In the Q1 of 2013, modern fashion retail formatsales (53%) exceeded for the first time thetraditional formats (through markets) (47%). In2009, the ratio was 48 to 52%

• This event is supported with the sales growth ratesof top fashion retailers operating in mass market

(see graph)• Estimated amount of purchases abroad ~ $8 billion,

with 30% being online purchases

• In premium and lux segment in 2011, for the firsttime the trend to buy premium goods domesticallyappeared. This trend is being maintained in 2013,supported both by demand and supply side:

- Growing loyalty to domestic premium productssales points offering comparable service level

- New brand entry onto the market, lux departmentstores opening

67

141516

29

912

35

18

23

38

Centobuv GloriaJeans

Sportmaster(O’stin)

+71%

+158%

+14%

+30%

Inditex(Zara,

Bershka,Stradivarius,

etc.)

+36%

+50%

InCityоodji

(OGGI)

2012

2011

515257

71

20112010 2013F2012

Source: Infoline, Fashion Report

D & Ph t il d t

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 37/40

37Copyright © 2013 Accenture All rights reserved.

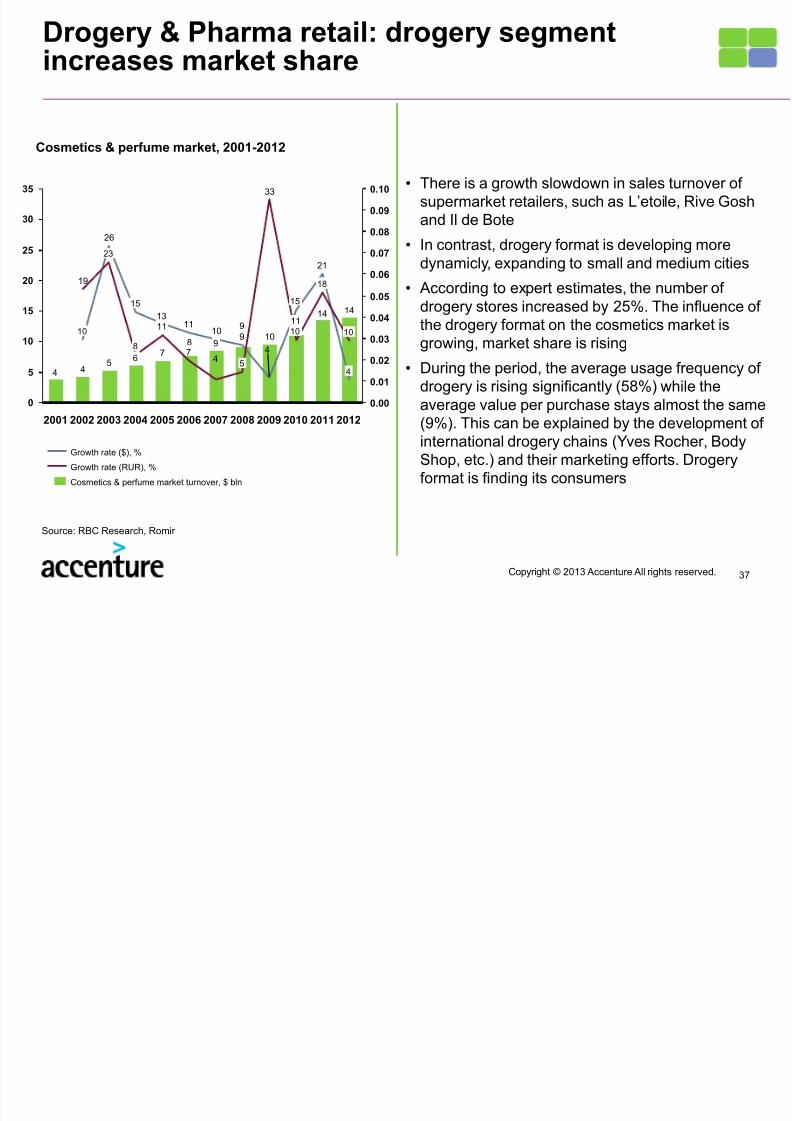

Drogery & Pharma retail: drogery segmentincreases market share

Cosmetics & perfume market, 2001-2012

• There is a growth slowdown in sales turnover ofsupermarket retailers, such as L’etoile, Rive Gosh

and Il de Bote

• In contrast, drogery format is developing moredynamicly, expanding to small and medium cities

• According to expert estimates, the number ofdrogery stores increased by 25%. The influence ofthe drogery format on the cosmetics market isgrowing, market share is rising

• During the period, the average usage frequency ofdrogery is rising significantly (58%) while theaverage value per purchase stays almost the same

(9%). This can be explained by the development ofinternational drogery chains (Yves Rocher, BodyShop, etc.) and their marketing efforts. Drogeryformat is finding its consumers

1414

10

9

8

7

544

21

4

910

1113

26

33

47

19

0

5

10

15

20

25

30

35 0.10

0.00

0.02

0.01

0.03

0.04

0.05

0.06

0.07

0.08

0.09

4

23

2002

10

2001 20122003

10

2011

18

2010

1110

15

20092008

5

2007

9

2005 2006

11

2004

6

8

15

Cosmetics & perfume market turnover, $ bln

Growth rate (RUR), %

Growth rate ($), %

Source: RBC Research, Romir

J l t il d t i i

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 38/40

38Copyright © 2013 Accenture All rights reserved.

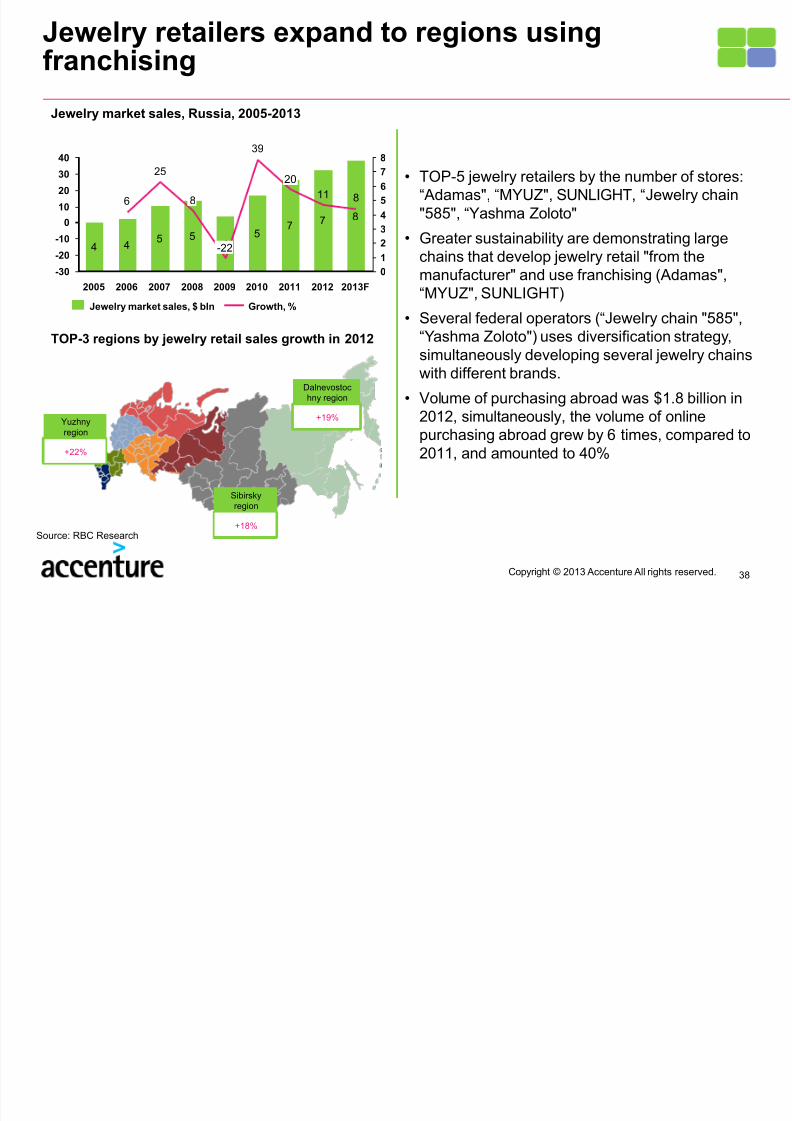

Jewelry retailers expand to regions usingfranchising

Jewelry market sales, Russia, 2005-2013

• TOP-5 jewelry retailers by the number of stores:“ Adamas", “MYUZ", SUNLIGHT, “Jewelry chain"585", “Yashma Zoloto"

• Greater sustainability are demonstrating largechains that develop jewelry retail "from the

manufacturer" and use franchising (Adamas",“MYUZ", SUNLIGHT)

• Several federal operators (“Jewelry chain "585",“Yashma Zoloto") uses diversification strategy,simultaneously developing several jewelry chainswith different brands.

• Volume of purchasing abroad was $1.8 billion in

2012, simultaneously, the volume of onlinepurchasing abroad grew by 6 times, compared to2011, and amounted to 40%

4 4 5 5

45

7 7 8

811

39

25

6

0

1

2

3

4

5

6

7

8

-30

-20

-10

0

10

20

30

40

2013F20122011

20

20102009

-22

2008

8

200720062005

Growth, %Jewelry market sales, $ bln

Dalnevostochny region

TOP-3 regions by jewelry retail sales growth in 2012

+19%Yuzhnyregion

+22%

Sibirskyregion

+18%Source: RBC Research

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 39/40

39Copyright © 2013 Accenture All rights reserved.

Three main facts to remember

• Market is in a stagnation phase, competition isescalating

• The middle class is growing, but is liking less theprocess of buying

• Service, quality, price

Summary

7/17/2019 Accenture Mega Analitics Consumer 2013 2015 English (1)

http://slidepdf.com/reader/full/accenture-mega-analitics-consumer-2013-2015-english-1 40/40

This document makes descriptive reference to trademarks that may be owned by others. The use of such trademarks herein is not an assertion of ownership ofsuch trademarks by Accenture and is not intended to represent or imply the existence of an association between Accenture and the lawful owners of suchtrademarks.

Copyright © 2013 Accenture. All rights reserved. Accenture, its logo, and High Performance Delivered are trademarks of Accent ure. This document is produced byconsultants at Accenture as general guidance. It is not intended to provide specific advice on your circumstances. If you require advice or further details on anymatters referred to, please contact your Accenture representative.

Thank you

Mikhail Pershin,Head of Russian Retail Practice, Accenture

www.accenture.com