Embed Size (px)

DESCRIPTION

Accelerating Growth and Development: The Contribution of an Integrated Manufacturing Strategy:. ACCOMPANYING DATA. Slow growth since 1994. Source: SARB QB. Increased integration into the global economy: General trend of lowering of tariffs. - PowerPoint PPT Presentation

Citation preview

Accelerating Growth and Development:

The Contribution of an Integrated

Manufacturing Strategy:

ACCOMPANYING DATA

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

Con

stan

t 199

5 R

mill

ions

Slow growth since 1994

Source: SARB QB

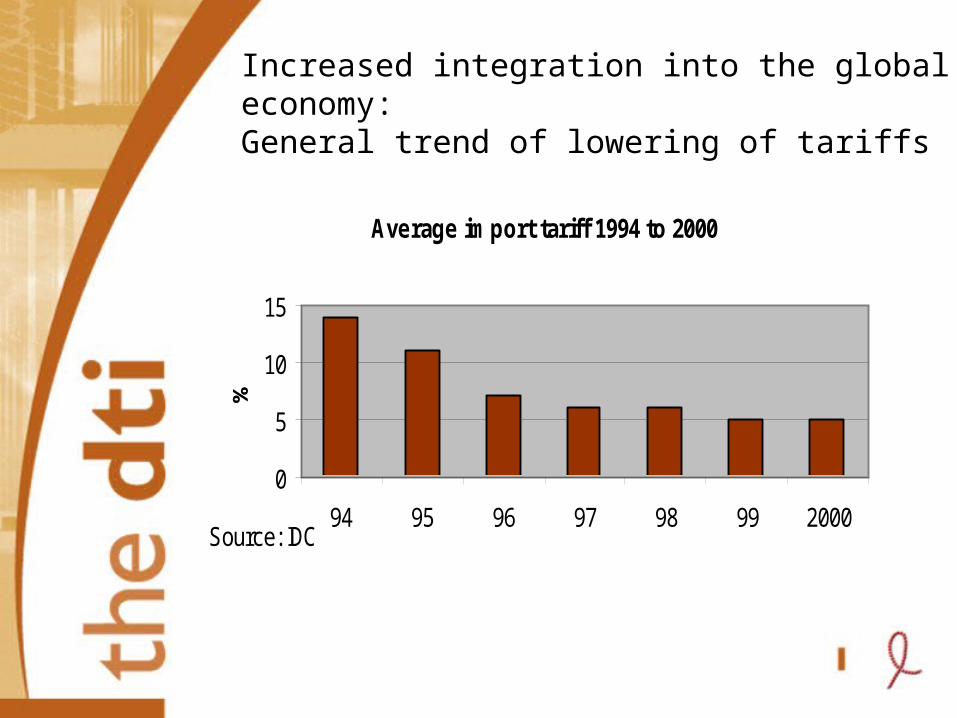

Increased integration into the global economy:General trend of lowering of tariffs

Average import tariff 1994 to 2000

0

5

10

15

94 95 96 97 98 99 2000

%

Source: IDC

Increased export orientation: significant export growth

60

80

100

120

140

160

180

200

19

90

=1

00

91 92 93 94 95 96 97 98 99 00 01

Total Excluding Metals & Minerals

Metals & Minerals

EXPORTS : Adjusted for nominaleffective exchange rate of the Rand

Increased share of manufacturing in export basket

Exports by stage of manufacturing, as % of total exports

Source: IDC

Exports Sectors, Jan - Sep 2001, R'000

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

Jan2001 Feb2001 Mar2001 Apr2001 May2001 Jun2001 Jul2001 Aug2001 Sep2001

R'00

0

Agro-Processing Clothing Automotives Furniture

Reduced vulnerability through diversification of export markets

Despite export growth, declining share in world trade

Source: WTO

0

20

40

60

80

100

120

1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

Inde

x 19

95=1

00

Falling Formal Sector Employment

Source: SARB QB

Increasing importance of informal sector

Formal (non-agricultural) and informal employment, '000

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

February 2000 September 2000 February 2001

Formal sector (excluding agriculture) Informal Sector

Source: Statistics South Africa

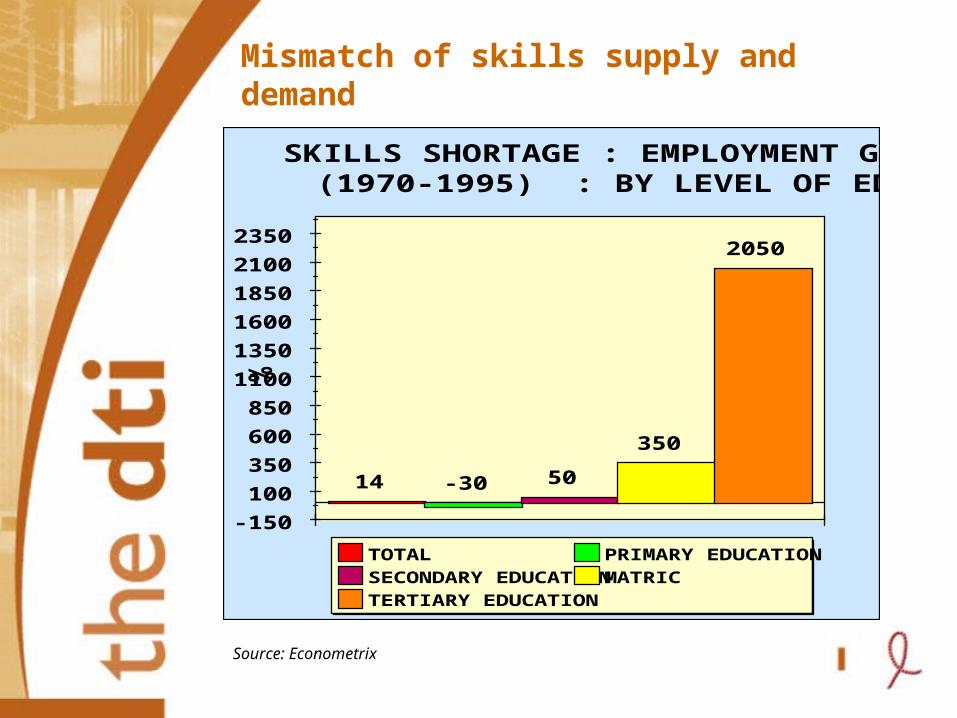

Mismatch of skills supply and demand

-150

100

350

600

850

1100

1350

1600

1850

2100

2350

%

14 -30 50

350

2050

TOTAL PRIMARY EDUCATION

SECONDARY EDUCATIONMATRIC

TERTIARY EDUCATION

SKILLS SHORTAGE : EMPLOYMENT GROWTH(1970-1995) : BY LEVEL OF EDUCATION

Source: Econometrix

Insufficient productive investment

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

1993 1994 1995 1996 1997 1998 1999 2000

General Government Public CorporationsPrivate Business Enterprises

Gross Fixed Capital FormationAt constant 1995 prices

Insufficient productive investment:

Portfolio inflows dominate long term capital inflows

Source: SARB QB

-40,000

-20,000

0

20,000

40,000

60,000

80,000

100,000

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

Direct Investment Portfolio Investment Other Investment

Foreign Capital Inflows Annual Figures

Insufficient Investment in R&D

R&D Intensity

00.5

11.5

22.5

3

Australia South Africa Malaysia Korea

Inte

nsity

Source: DACST

Source: World Bank

0

10

20

30

40

50

60

% participation in SMME sector

African Asian Coloured White

Sample from Greater Johannesburg Metro

Small enterprise development still racially unequal

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

African:42.9%

Coloured:30.3%

Indian:22.5%

White:10.1%

Total:37.0%

Female Male

Percentage Unemployment by Race and Gender

Source: Stats SA Labour Force Survey Feb 2001

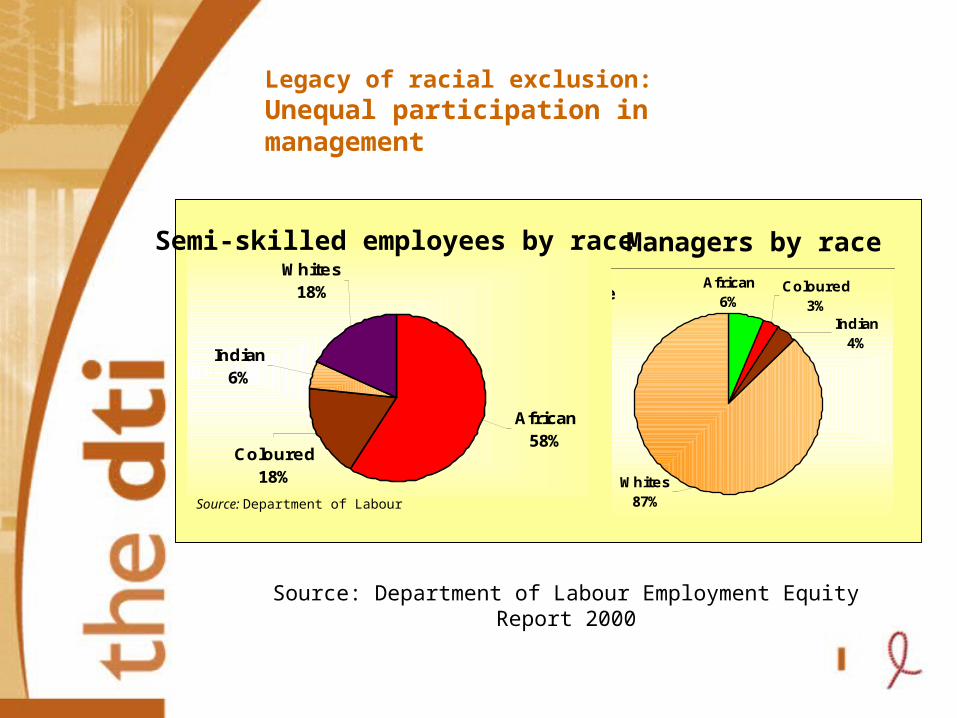

Continued racial inequalities in labour market

Legacy of racial exclusion:Unequal participation in management

Indian6%

Whites18%

Coloured18%

African58%

Semi-skilled employees by race Managers by race

Top Management Profile by Race Coloured3%

African6%

Indian4%

Whites87%Source: Department of Labour

Source: Department of Labour Employment Equity Report 2000

Insufficient improvement in quality of life

GDP Per Capita

12,000

12,500

13,000

13,500

14,000

14,500

15,000

15,500

16,000

16,500

17,000

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

Con

stan

t 199

5 R

mill

ions

Percentage of Households Living In Poverty, 1996

0%

10%

20%

30%

40%

50%

60%

Large regional disparities & high absolute poverty

Source: Statistics South Africa

Logistics costs: internationally uncompetitive

Total Waterfront Charges

0

200

400

600

800

1000

1200

1400

1600R

an

ds p

er

TE

U

Terminal Ancillary Port Authority

Source: Portnet, International Benchmarking - Waterfront 1995

Underdeveloped telecommunications infrastructure

Telephone mainlines (per 1,000 people), 1998

- 100.00 200.00 300.00 400.00 500.00 600.00

Egypt, Arab Rep.

Brazil

South Africa

Malaysia

Chile

Poland

Turkey

Czech Republic

Korea, Rep.

Australia

Source: World Development Indicators

Personal computers (per 1,000 people)

- 50 100 150 200 250 300 350 400 450

Egypt, Arab Rep.

Turkey

Brazil

Chile

Poland

South Africa

Malaysia

Czech Republic

Korea, Rep.

Australia

Investment in PC’s Slackening SA falling behind due to inequalities

Insufficient Science and Technology Skills

Tertiary Science Enrolment

0

10

20

30

Australia SouthAfrica

Malaysia Korea

Pe

rce

nta

ge

Source: DACST