Embed Size (px)

Citation preview

ACCA P1

Governance, Risk and Ethics

2

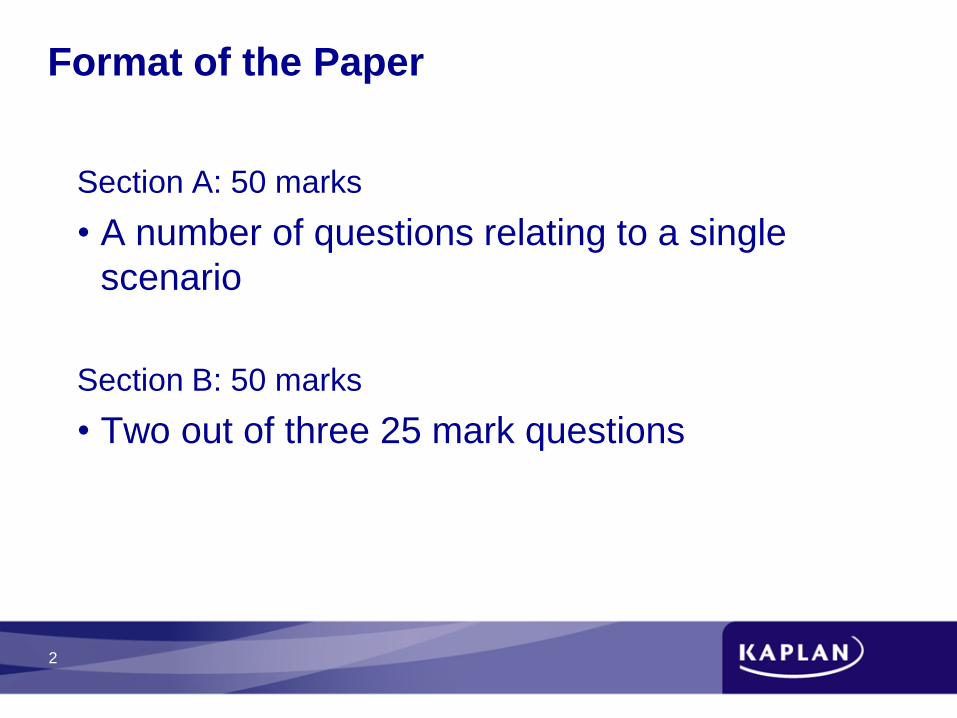

Format of the Paper

Section A: 50 marks

• A number of questions relating to a single

scenario

Section B: 50 marks

• Two out of three 25 mark questions

3

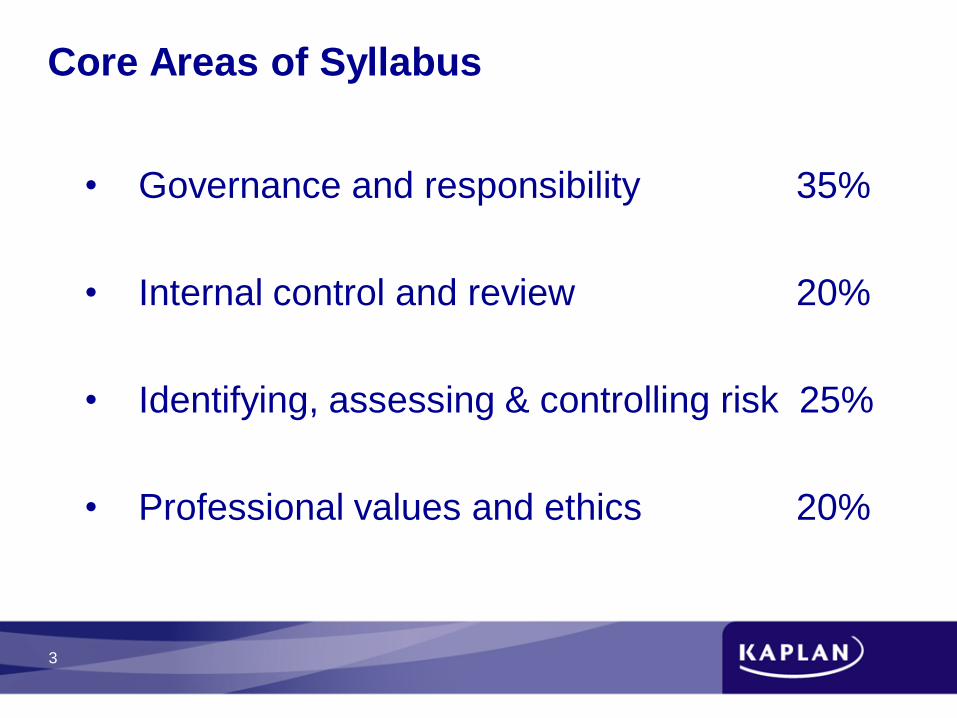

Core Areas of Syllabus

• Governance and responsibility 35%

• Internal control and review 20%

• Identifying, assessing & controlling risk 25%

• Professional values and ethics 20%

4

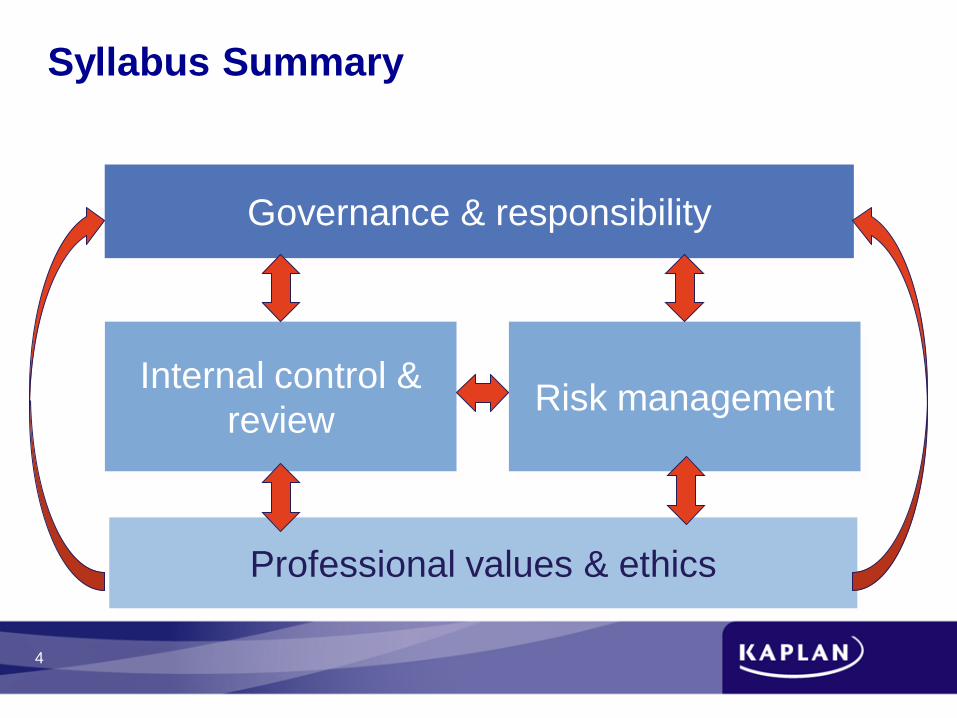

Syllabus Summary

Governance & responsibility

Professional values & ethics

Risk management Internal control &

review

5

1 Chapter Theory of governance

6

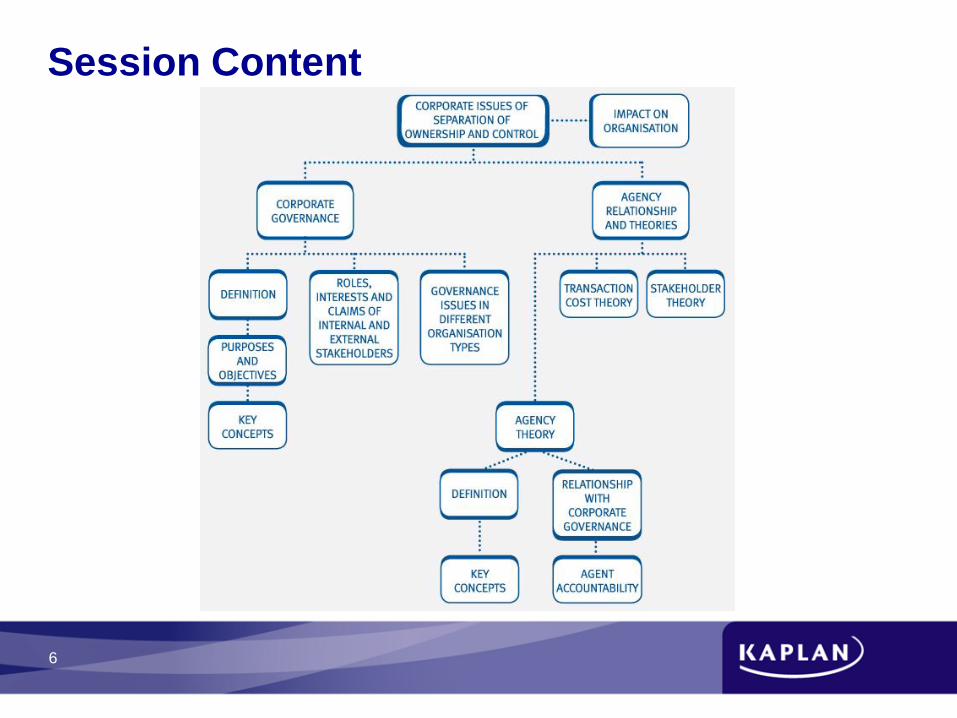

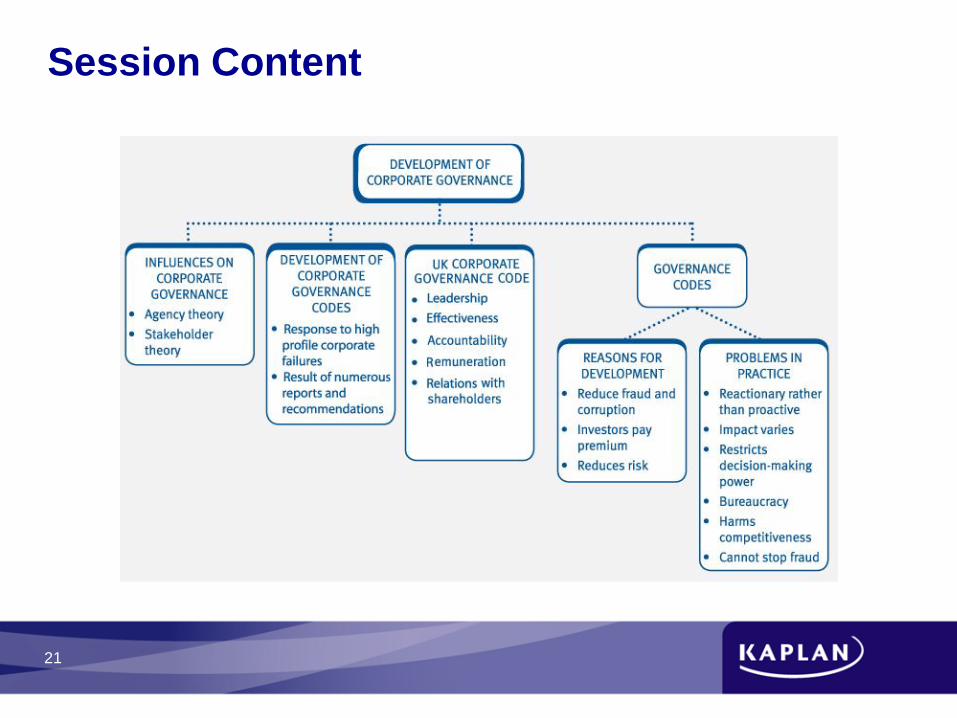

Session Content

7

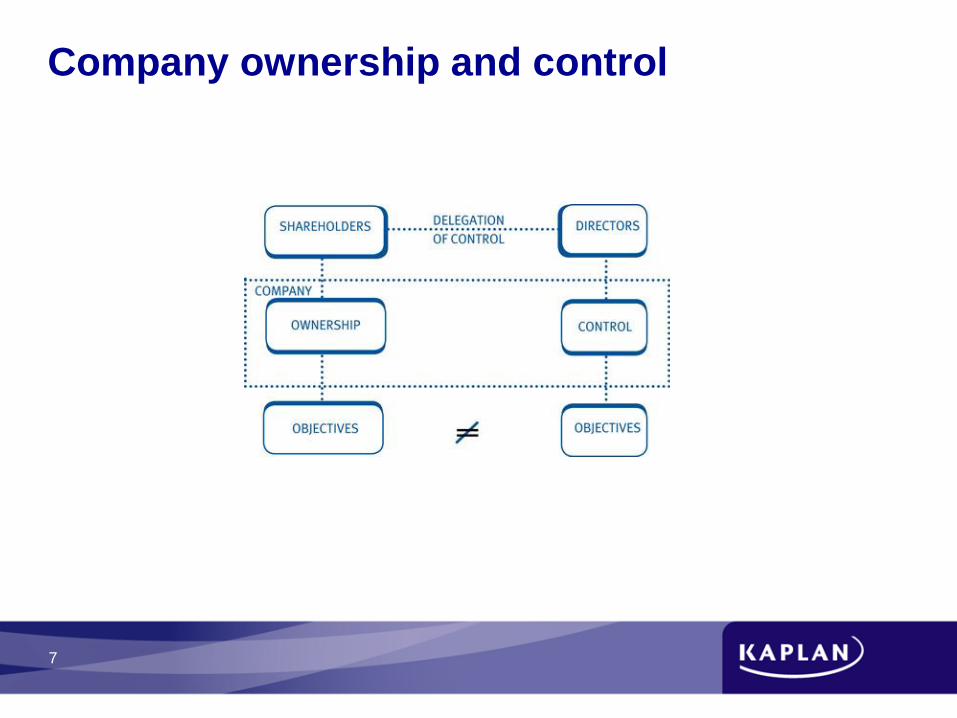

Company ownership and control

8

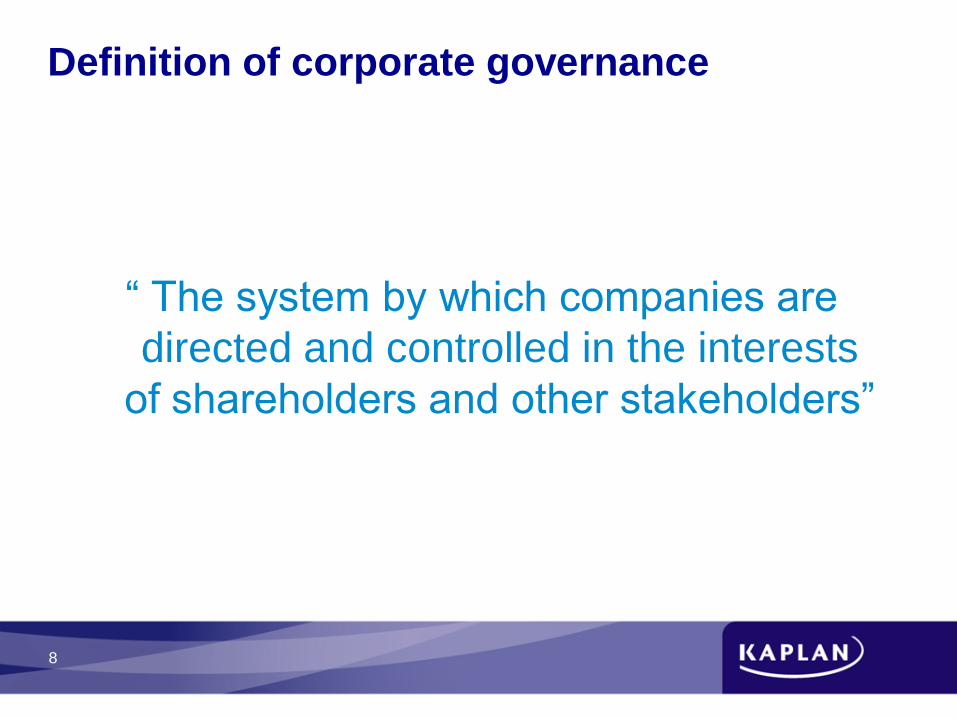

Definition of corporate governance

“ The system by which companies are

directed and controlled in the interests

of shareholders and other stakeholders”

9

Key concepts

• Fairness

• Openness / transparency

• Independence

• Probity / honesty

• Responsibility

• Accountability

• Reputation

• Judgement

• Integrity

10

Operational areas affected by corporate

governance

11

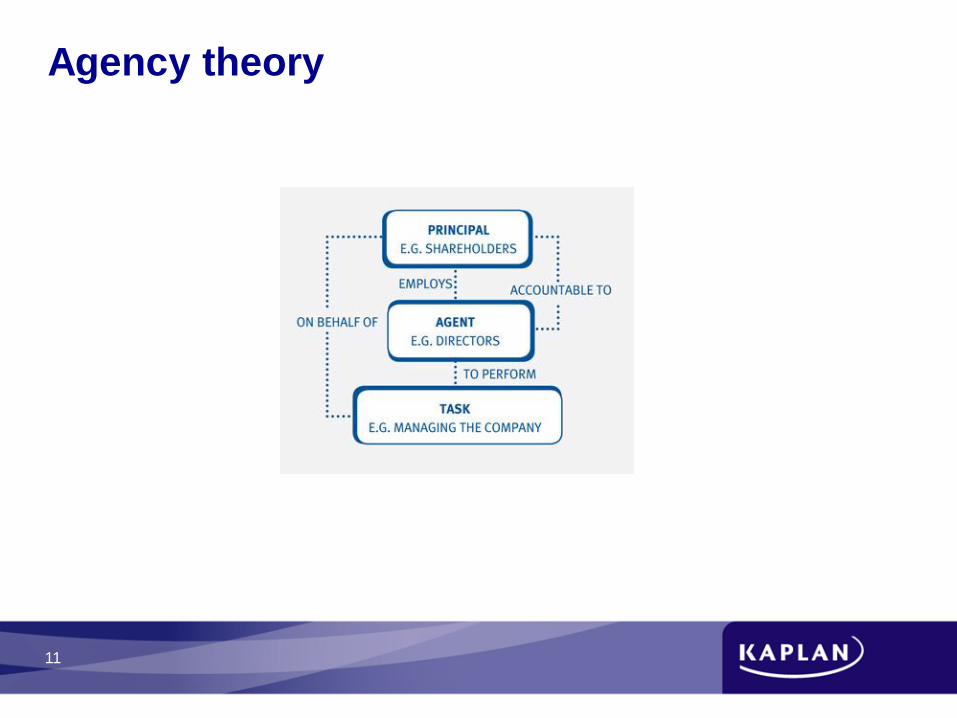

Agency theory

12

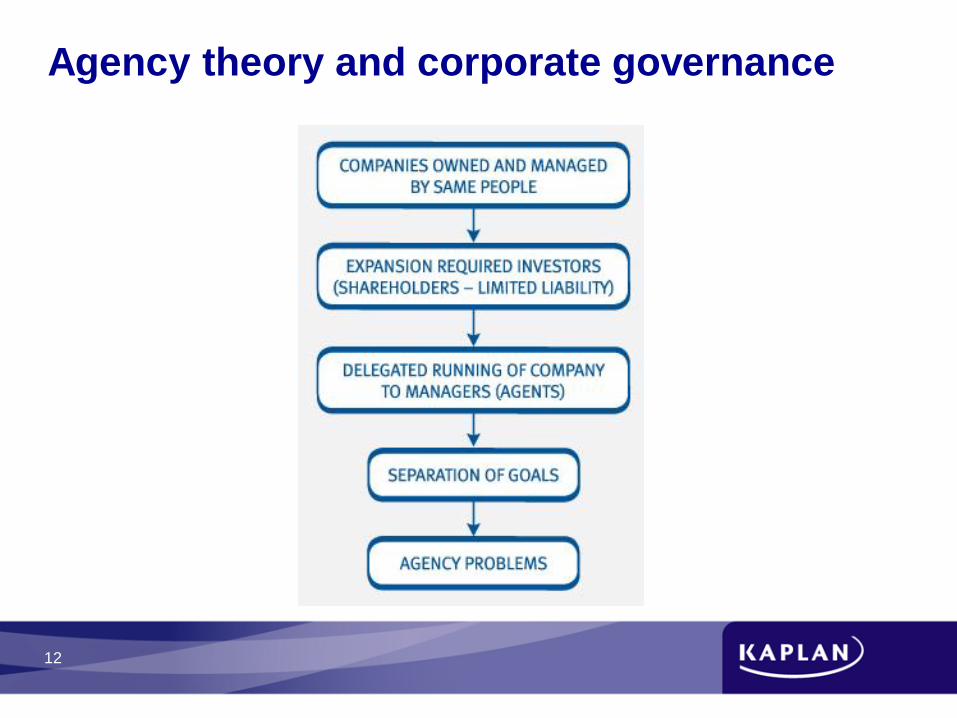

Agency theory and corporate governance

13

Key concepts of agency theory

• Agent employed by principal

• Agency = relationship

• Agency costs

• Accountability

• Fiduciary responsibility

• Stakeholders

• Objectives

14

Cost of agency relationships

Examples include:

• Incentive schemes for directors

• Providing and reviewing data

• Meetings

• Accepting higher risks

• Monitoring behaviour

• Residual loss

15

Agency problem resolution measures

• Meeting – Principal/key investors

• Voting at AGM

• Resolutions at AGM

• Accepting takeovers

• Divestment of shares

16

Agency accountability

• Act in shareholders’ interests

• Provide good information

• Operate within legal structure

17

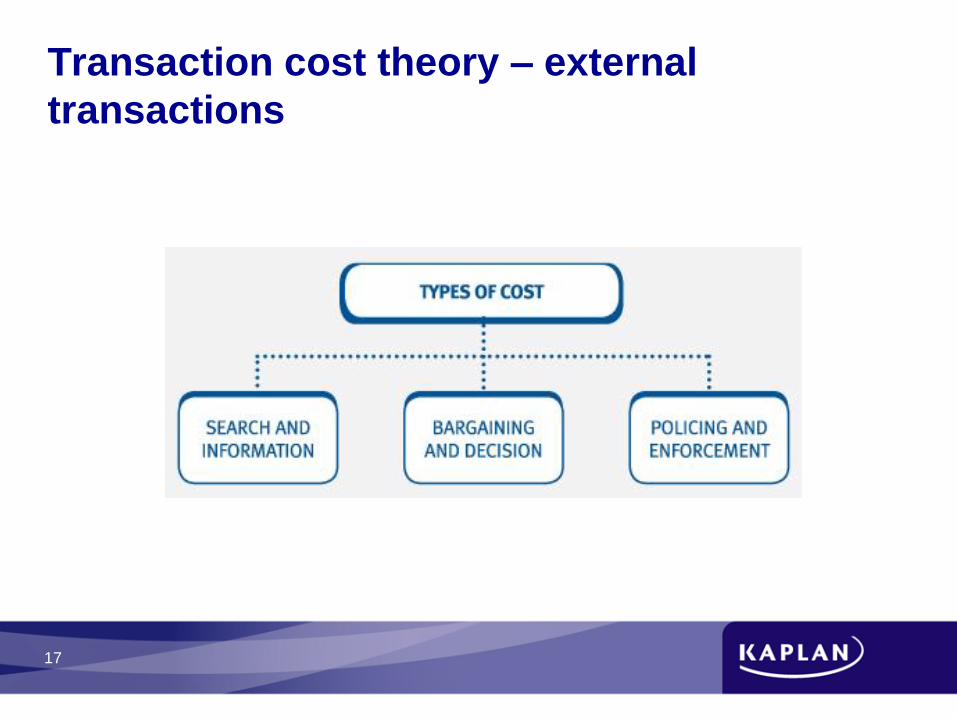

Transaction cost theory – external

transactions

18

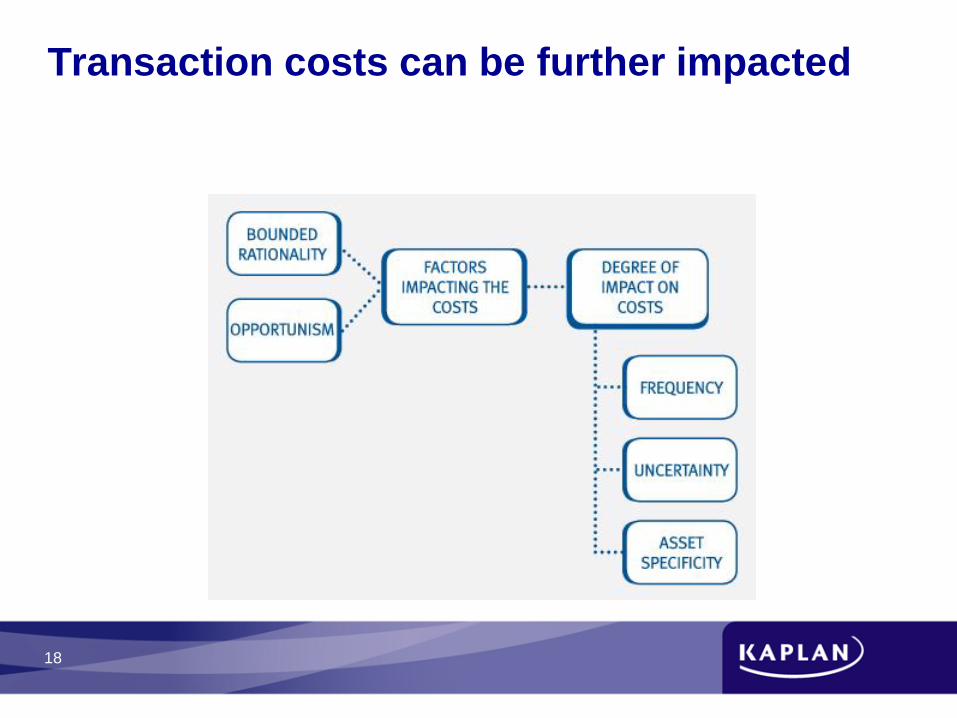

Transaction costs can be further impacted

19

Stakeholder theory

20

2 Chapter Development of corporate governance

21

Session Content

22

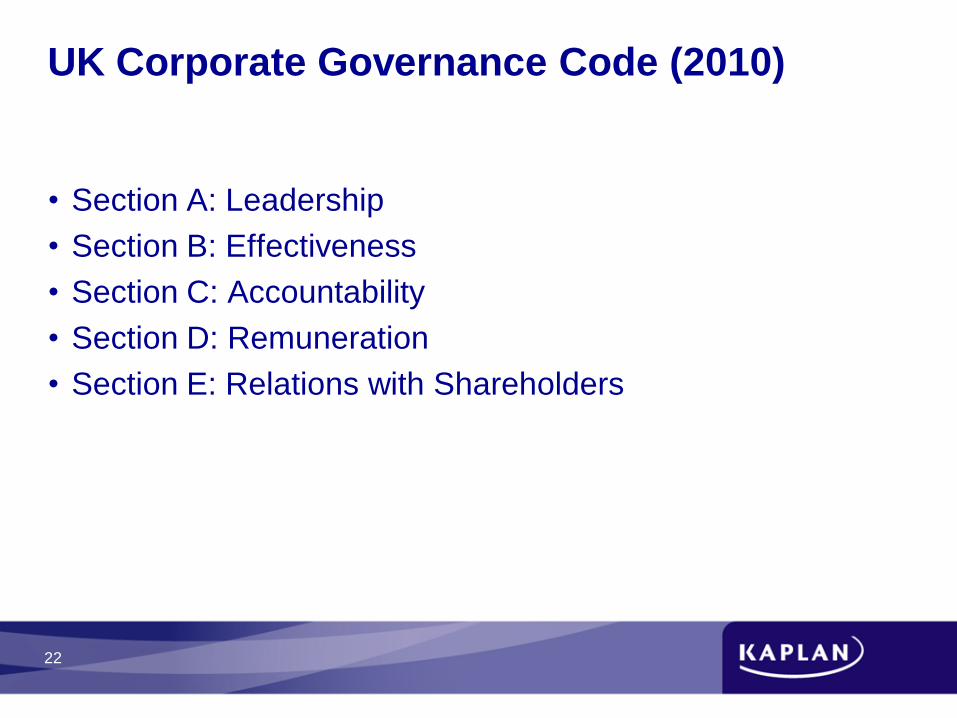

UK Corporate Governance Code (2010)

• Section A: Leadership

• Section B: Effectiveness

• Section C: Accountability

• Section D: Remuneration

• Section E: Relations with Shareholders

23

Reasons for developing a governance code

• Reduce fraud / corruption

• Poor governance = poor performance

• Investors will pay a premium

• Decision factor for institutional investors

• Reduces risk

24

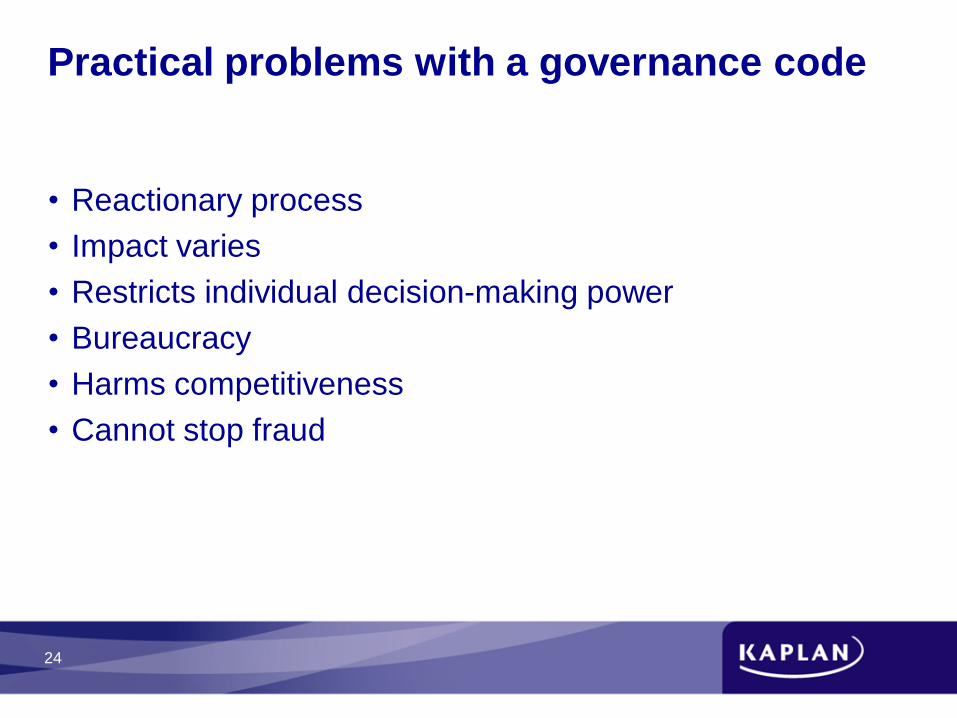

Practical problems with a governance code

• Reactionary process

• Impact varies

• Restricts individual decision-making power

• Bureaucracy

• Harms competitiveness

• Cannot stop fraud