Embed Size (px)

Citation preview

© ICAEW 2016

ACA SKILLS DEVELOPMENT GRIDS 2017

© ICAEW 2016 2

CONTENTS

ACA OVERVIEW ............................................................................................................................ 3

Skills progression through the ACA qualification ............................................................................. 5

Professional Level ........................................................................................................................... 6

Audit and Assurance ....................................................................................................................... 6

Business Strategy ......................................................................................................................... 11

Financial Accounting and Reporting .............................................................................................. 14

Financial Management .................................................................................................................. 16

Tax Compliance ............................................................................................................................ 18

Business Planning ........................................................................................................................ 21

Advanced Level ............................................................................................................................ 26

Corporate Reporting ..................................................................................................................... 26

Strategic Business Management ................................................................................................... 28

Case Study ................................................................................................................................... 32

© ICAEW 2016 3

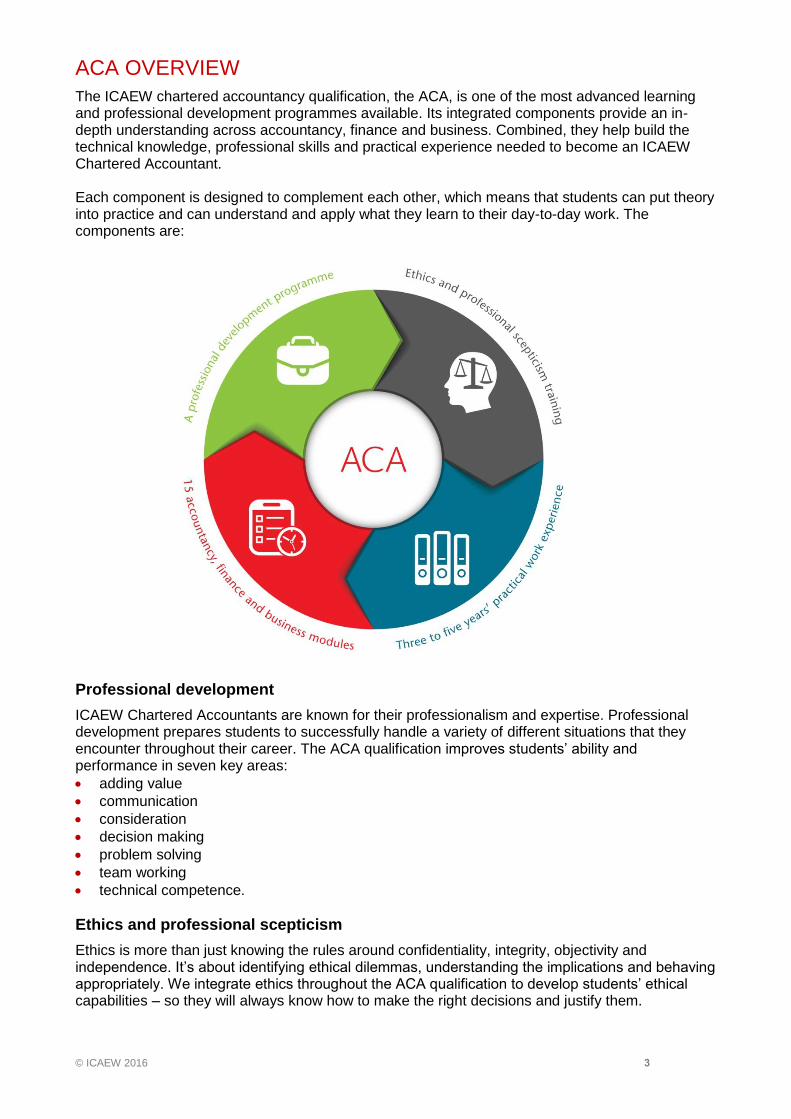

ACA OVERVIEW

The ICAEW chartered accountancy qualification, the ACA, is one of the most advanced learning and professional development programmes available. Its integrated components provide an in-depth understanding across accountancy, finance and business. Combined, they help build the technical knowledge, professional skills and practical experience needed to become an ICAEW Chartered Accountant. Each component is designed to complement each other, which means that students can put theory into practice and can understand and apply what they learn to their day-to-day work. The components are:

Professional development

ICAEW Chartered Accountants are known for their professionalism and expertise. Professional development prepares students to successfully handle a variety of different situations that they encounter throughout their career. The ACA qualification improves students’ ability and performance in seven key areas:

adding value

communication

consideration

decision making

problem solving

team working

technical competence.

Ethics and professional scepticism

Ethics is more than just knowing the rules around confidentiality, integrity, objectivity and independence. It’s about identifying ethical dilemmas, understanding the implications and behaving appropriately. We integrate ethics throughout the ACA qualification to develop students’ ethical capabilities – so they will always know how to make the right decisions and justify them.

© ICAEW 2016 4

Three to five years’ practical work experience

Practical work experience is done as part of a training agreement with an authorised training employer or principal. Students need to complete 450 days, which normally takes between three and five years. The knowledge, skills and experience they gain as part of their training agreement are invaluable, giving them the opportunity to put what they’re learning into practice. Experience can be completed in at least one of the following six categories:

Accounting

Audit and assurance (audit is not compulsory)

Financial management

Information technology

Insolvency

Taxation.

15 accountancy, finance and business modules

Students gain in-depth knowledge across a broad range of topics in accountancy, finance and business. The modules are designed to complement their practical work experience, so they constantly progress through the qualification. There are 15 modules over three levels – Certificate, Professional and Advanced. The modules can be taken in any order with the exception of the Case Study which has to be attempted last. Students must pass every exam (or receive credit).

Certificate Level

There are six modules that introduce the fundamentals of accountancy, finance and business. They each have a 1.5 hour computer-based exam, a 55% pass mark, and can be sat throughout the year at an ICAEW-approved test centre. Students may be eligible for credit for some modules if they have studied accounting, finance, law or business at degree level or through another professional qualification. These six modules are also available as a stand-alone certificate, the ICAEW Certificate in Finance, Accounting and Business (ICAEW CFAB). Students studying for this certificate will only complete these six modules. On successful completion, the ICAEW CFAB can be used as a stepping stone to studying the ACA qualification.

© ICAEW 2016 5

Professional Level

The next six modules build on the fundamentals and test students’ understanding and ability to use technical knowledge in real-life scenarios. Each module is 2.5 hours long, except the Financial Accounting and Reporting exam which is 3 hours long. The pass mark for each exam is 55%. The modules can be taken in March, June, September and December. Please note, the Business Planning alternative modules for banking and insurance are available at the June, September and December sittings. Prescribed texts are permitted for Audit and Assurance, Finance Accounting and Reporting and Tax Compliance, with open books permitted for the Business Planning exams. The Professional Level modules are flexible and can be taken in any order to fit with a student’s day-to-day work. The Business Planning and Business Strategy modules in particular help students to progress to the Advanced Level. Alternative modules are available for the Business Planning and Financial Accounting and Reporting modules:

in addition to Business Planning: Taxation, Business Planning: Banking and Business Planning: Insurance modules are available (see page 20); and

students can study the financial reporting framework most beneficial to their employer and clients and can choose either UK GAAP or IFRS when studying towards the Financial Accounting and Reporting module (see page 13).

An employer or principal will guide their students on the modules which are right for them. If a student is studying the ACA independently, they should consider their future ambitions when selecting which modules to sit. Please note that computer-based exams will be introduced for some Professional Level modules in 2017, visit the exam resources area of our website to find out more, icaew.com/exams

Advanced Level

The Corporate Reporting and Strategic Business Management modules test students’ understanding and strategic decision making at a senior level. They present real-life scenarios, with increased complexity and implications from the Professional Level modules. Both exams are 3.5 hours long and have a 50% pass mark. The Case Study tests all the knowledge, skills and experience gained so far. It presents a complex business issue which challenges students’ ability to problem solve, identify the ethical implications and provide an effective solution. The exam is 4 hours long and also has a 50% pass mark. The Advanced Level exams can be taken in July and November. They are fully open book, so they replicate a real-life scenario where all the resources are at their fingertips. Please note that students will not be able to attempt the Case Study until they have taken (or received credit for) all of the other ACA modules. Students also need to be in their final year of their training agreement.

Skills development grid

This document presents the skills assessed alongside technical knowledge for Professional and Advanced Level modules. The skills should be read with the syllabus and learning outcomes, and the relevant technical knowledge grid for each module. The link between work experience and the exams will be made explicit through the professional development framework and the skills development grids. Students should use the professional development framework and skills development grids to ensure success in their exams and

© ICAEW 2016 6

workplace. For each skills area, there is a description of the specific skills that are assessed, and how these skills are assessed.

© ICAEW 2015 7

SKILLS PROGRESSION THROUGH THE ACA QUALIFICATION

Assessed skills Certificate Level Professional Level

Advanced Level

Corporate Reporting and Strategic Business

Management

Case Study

Assimilating and using information

Understanding the subject matter and identifying issues

Specific issues Simple scenarios Complex scenarios Unstructured complex business scenarios

Accessing, evaluating and managing information

Information/data as provided Single information source provided

Multiple information sources provided

Multiple information sources including own research

Using technical knowledge and professional experience

Highly structured application of non-integrated knowledge

Structured application of integrated and non-integrated knowledge

Structured application of integrated and non-integrated knowledge and experience

Unstructured application of integrated knowledge and experience

Structuring problems and solutions

Using analytical tools Specified tools Specified tools Tools inferred by nature of problem

Unspecified tools

Analysing and evaluating problems

Highly specified tasks Specified integrated and non-integrated problems

Specified integrated and non-integrated problems

Defined output but unspecified problems

Applying judgement

Assessing quality of information

Objective testing Specified in simple scenario Specified in complex scenario Underlying requirement within complex scenario

Assessing options and priorities including ethical issues

Options given Options included in simple scenario

Options included in complex scenario

Balanced judgement of priorities and risks in unstructured scenario

Considering other perspectives Not assessed Possible alternative provided Alternative(s) provided Alternatives identified using professional experience

Conclusions, recommendations and communication

Drawing conclusions and making recommendations

Not assessed Specified conclusions and recommendations in simple scenarios

Specified conclusions and recommendations in complex scenarios

Conclusions and recommendations supported by own evidence

Presenting data and written work

Prescribed exam format Exam requirements, including some professional presentation

Short written professional presentations

Professional report with appendices

© ICAEW 2015 8

PROFESSIONAL LEVEL

AUDIT AND ASSURANCE

From the March 2017 exam session onwards, the Audit and Assurance module will be examined as a computer-based exam. A paper-based exam for this module will no longer be available. Find out more at icaew.com/exams

Assimilating and using information

Assessed skills

Reading and understanding subject matter.

Accessing, evaluating and managing information provided in a few defined sources.

Framing questions that clarify information or identify gaps in knowledge.

Operating to a brief in structured situations.

Explaining the nature of ethics and its significance in the business environment.

Understanding the public interest and social responsibility.

Understanding the importance of contributing to the profession.

Appreciating the ethos and culture of the accountancy profession.

Understanding the role of the professional accountant within the public interest, practice and business contexts and the regulatory structure of the profession.

Understanding the importance of ethical behaviour to a professional and the reasons for the adoption of ethical codes by professions acting in the public interest.

Understanding the pressures on professional ethical behaviour, including the interaction between professional ethics and the law and other value systems.

How skills are assessed

Questions will contain both structured and unstructured detail that candidates have to

understand.

Requirements will include demonstrating an understanding of:

the regulatory, professional and ethical issues relevant to accepting, carrying out and managing assurance engagements; and

how quality assurance processes mitigate risks.

Structuring problems and solutions

Assessed skills

Understanding data and information given: identifying and understanding issues arising in straightforward scenarios.

Using the data and information given: understanding requirements, analysing data and information to support the requirement.

Drawing upon technical and professional knowledge learnt to analyse issues.

Understanding the workings of, and controls within, an organisational framework.

Applying knowledge from different technical areas: analysing problems that combine technical skills in a single disciplinary environment.

Using new concepts: evaluating new ideas and concepts.

Appreciating the ethical dimensions of situations, problems and proposals.

Identifying and selecting appropriate courses of action using an ethical framework.

Financial data analysis: performing the required calculations; explaining or stating the issues.

Financial statement analysis: performing the required analytical process, explaining or stating the issues.

Identifying and explaining the consequence of unethical behaviour.

© ICAEW 2016 9

Identifying and using relevant up to date content of International and ICAEW Code of Ethics and FRC Ethical Standards.

Recognising ethical issues arising from situations likely to be encountered by chartered accountants; identifying possible courses of action to resolve them.

How skills are assessed

Requirements will include planning assurance engagements in accordance with the terms of

engagement and appropriate standards, taking account of:

managing audit and other assurance engagements;

reliance on controls;

reliance on the work of internal audit or other experts;

reliance on the work of another auditor;

extent of tests of control and of substantive procedures, including analytical procedures

use of analytical procedures to identify the risk of misstatement; and

number, timing, staffing and location of assurance visits.

Applying judgement

Assessed skills

Applying discrimination: identifying the relevant/reasonable in data and evidence; recognising varying quality in data or evidence.

Relating parts and wholes: discerning particular issues as part of wholes.

Demonstrating an understanding of different perspectives (eg social, political, economic): analysing and interpreting problems and situations from a given stance.

Change management (appreciating the impacts/effects of change): considering and evaluating the effects of a given future scenario.

Assessing/applying materiality: understanding the concept of materiality.

Applying a sceptical and critical approach in a given straightforward situation.

Appreciating when more expert help is required in a given straightforward situation.

Exercising ethical judgement in a given straightforward situation.

Developing arguments, having first appreciated the perspective of all other parties.

Conducting critiques: critically reviewing a statement, argument or position.

How skills are assessed

Candidates will be required to identify significant business or audit risks from a given scenario, explain their impact on the financial statements, and finally recommend audit procedures to mitigate the risk of a material error. Requirements will test the ability of candidates to filter those issues which are more relevant than others in a given scenario. Candidates' ability to distinguish the quality of data or evidence will be tested in two potential ways. (i) Candidates will need to distinguish between data generated from within an organisation and that generated by a third party, the latter being less susceptible to management bias; and (ii) candidates will need to appreciate the effect on the quality of evidence that bias caused by specific factors can have eg, where profits are used to determine a bonus payment to be made to the company’s management. Question requirements will include the need to identify the impact of specific economic and political factors on a set of financial statements eg, in the context of dealing with customers or suppliers from overseas that (i) political instability may cause problems which prevent the customer or supplier from trading, ultimately leading to going concern issues for the audited entity; and (ii) economic factors may cause exchange rate fluctuations leading to the risk of misstated balances in the financial statements.

© ICAEW 2016 10

Candidates will be expected to evaluate the effect of uncertain future events when describing the procedures to be performed in carrying out an examination of a company’s financial forecasts. Question requirements will include the need to assess the materiality of a particular matter (eg, an unadjusted error) in the context of a set of financial statements. This assessment should then inform the candidate’s judgement as to whether or not to modify the opinion given in a statutory audit report. Candidates are required to exercise ethical judgement in a variety of different scenarios, including:

judging the potential independence risks involved in accepting or continuing an audit engagement, and the procedures to mitigate those risks; and

consideration of the required steps upon the discovery of fraud/money laundering.

Candidates are expected to display the ability to present a structured argument to a client eg, in situations where management is questioning the extent of audit work performed.

Conclusions, recommendations and communication

Assessed skills

Using technical knowledge to support reasoning and conclusions.

Decision making: using relevant quantitative approaches in decision analysis.

Identifying the best explanation, solution or steps against defined criteria in a given straightforward situation.

Formulating opinions, reservations, advice, recommendations, plans, solutions, options and risks including business implications in a given straightforward situation.

Preparing, describing, outlining the advice, report, notes required in a given straightforward situation.

Presenting a basic or routine memorandum or briefing note in writing in a clear and concise style.

How skills are assessed

Requirements will include:

advising on the regulatory, professional and ethical issues in carrying out an assurance engagement;

concluding and reporting on assurance engagements, including determining whether to a modified report with or without a modified opinion/conclusion; and

identifying weaknesses in financial information systems, their potential consequences and recommendations for improvement.

© ICAEW 2016 11

BUSINESS STRATEGY

Assimilating and using information

Assessed skills

Reading and understanding subject matter.

Accessing, evaluating and managing information provided in a few defined sources.

Framing questions that clarify information or identify gaps in knowledge.

Operating to a brief in structured situations.

Explaining the nature of ethics and its significance in the business environment.

Understanding the public interest and social responsibility.

Understanding the pressures on professional ethical behaviour, including the interaction between professional ethics and the law, regulations and other value systems.

How skills are assessed

The majority of written test questions will require candidates to absorb and understand both structured and unstructured material.

Requirements will include:

understanding key information from the scenario provided;

understanding the context of the scenario in terms of type of business, industry and wider context;

recognising key ethical issues for an accountant undertaking work in accounting and reporting; and

recognising specific issues that may arise in the context of the situation described.

Structuring problems and solutions

Assessed skills

Understanding data and information given: identifying and understanding issues arising in straightforward scenarios.

Using the data and information given: understanding requirements, analysing data and information to support the requirement.

Drawing upon technical and professional knowledge learnt to analyse issues.

Understanding the workings of, and controls within, an organisational framework.

Applying knowledge from different technical areas: analysing problems that combine technical skills in a single disciplinary environment.

Using new concepts: evaluating new ideas and concepts.

Appreciating the ethical dimensions of situations, problems and proposals.

Identifying and selecting appropriate courses of action using an ethical framework.

Financial data analysis: performing the required calculations; explaining or stating the issues.

How skills are assessed

Questions will be scenario-based (on occasions based on actual situations in the real world). These will require candidates to apply technical knowledge to practical situations and analyse information (including quantitative analysis) to support sound decision making

Candidates will be required to:

identify and use information to define key business issues;

demonstrate understanding of the business, its strategy, industry and wider context.

demonstrate the impact of ethics on the objectives and methods of an organisation;

identify the ethical implications of strategic proposals;

© ICAEW 2016 12

demonstrate relevant technical knowledge;

perform appropriate analysis of numerical data and demonstrate an understanding of what is relevant; and

use data analysis to develop and illustrate an answer.

Applying Judgement

Assessed skills

Applying discrimination: identifying the relevant/reasonable in data and evidence; recognising varying quality in data or evidence.

Relating parts and wholes: discerning particular issues as part of wholes.

Sensitivity analysis: demonstrating an understanding of sensitivities to change: calculating a range of outputs for given inputs.

Demonstrating an understanding of different perspectives (eg social, political, economic): analysing and interpreting problems and situations from a given stance.

Change management (appreciating the impacts/effects of change): considering and evaluating the effects of a given future scenario.

Applying a sceptical and critical approach in a given straightforward situation.

Exercising ethical judgement in a given straightforward situation.

Developing arguments, having first appreciated the perspective of all other parties.

Conducting critiques: critically reviewing a statement, argument or position.

How skills are assessed

Questions will require candidates to use their understanding and interpretation of the information, together with the results of any analysis, to provide a reasoned argument and as a means of developing conclusions and recommendations.

Candidates will be required to:

evaluate the impact of a business proposal on an entity;

assess the reliability, accuracy and limitations of any analysis performed;

be able to produce arguments integrating numerical and descriptive analysis;

prioritise the issues facing an entity;

identify links and relationships between different issues affecting an entity and use these to establish priorities;

evaluate options for an organisation, taking into account its stakeholders, objectives, priorities, available resources and ethical obligations; and

provide reasons for the rejection of alternatives.

Conclusions, recommendations, and communication

Assessed Skills

Using technical knowledge to support reasoning and conclusions.

Decision making: using relevant quantitative approaches in decision analysis.

Identifying the best explanation, solution or steps against defined criteria in a given straightforward situation.

Formulating opinions, reservations, advice, recommendations, plans, solutions, options and risks including business implications in a given straightforward situation.

Preparing, describing, outlining the advice, report or notes required in a given straightforward situation.

Presenting a basic or routine memorandum or briefing note in writing in a clear and concise style.

Combining cognitive and behavioural skills to communicate to specialists and non-specialists.

© ICAEW 2016 13

How skills are assessed

The provision of advice to managers and others will be central to most questions.

Candidates may be required to:

draw realistic conclusions from an analysis of data and the information provided;

prepare a report or memorandum structured according to the requirements of the scenario, with appropriate context;

provide reasoned advice based on an understanding of the business and the relevant scenario, including an assessment of possible alternatives;

recommend suitable courses of action in a given situation; and

identify risks and outline reservations about the advice.

© ICAEW 2016 14

FINANCIAL ACCOUNTING AND REPORTING

From March 2017, alternative financial reporting modules will be introduced to the Financial Accounting and Reporting module. Students can choose between two different contexts, either UK GAAP or IFRS. This means that students can study the financial reporting framework most beneficial to their employer and clients. The learning materials for this module will continue to cover the fundamental differences between UK GAAP and IFRS. This will ensure that alongside a detailed understanding of a student’s chosen framework, they will also develop an awareness of the other framework. Whether students choose the UK GAAP or IFRS version of Financial Accounting and Reporting, the issues and scenarios in both exams will be the same. Students will be expected to respond to the exam questions using their selected financial reporting framework. Students will need to sit one version of the Financial Accounting and Reporting module. They are advised to speak to their employer or principal to determine which version is right for them. If a student is studying the ACA independently, they should consider their future ambitions when selecting which modules to sit. In addition to the introduction of alternative financial reporting modules, please note that from the September 2017 exam session onwards, the Financial Accounting and Reporting module will be examined as a computer-based exam. A paper-based exam for this module will no longer be available. Find out more at icaew.com/exams

Assimilating and using information

Assessed skills

Reading and understanding subject matter.

Accessing, evaluating and managing information provided in a few defined sources.

Framing questions that clarify information or identify gaps in knowledge.

Operating to a brief in structured situations.

Explaining the nature of ethics and its significance in the business environment.

Understanding the public interest and social responsibility.

Appreciating the ethos and culture of the accountancy profession.

Understanding the role of the professional accountant within the public interest, practice and business contexts and the regulatory structure of the profession.

Understanding the pressures on professional ethical behaviour, including the interaction between professional ethics and the law and other value systems.

How skills are assessed

Questions will contain both structured and unstructured detail in scenarios that candidates have to read, assimilate and understand.

Requirements will include:

explaining the contribution and inherent limitations of financial statements;

applying elements of the IASB conceptual framework for financial reporting;

recognising key ethical issues for an accountant undertaking work in accounting and reporting; and

recognising specific issues that may arise in the context of the situation described.

Structuring problems and solutions

Assessed skills

© ICAEW 2016 15

Understanding data and information given: identifying and understanding issues arising in straightforward scenarios.

Using the data and information given: understanding requirements, analysing data and information to support the requirement.

Drawing upon technical and professional knowledge learnt to analyse issues.

Applying knowledge from different technical areas: analysing problems that combine technical skills in a single disciplinary environment.

Using new concepts: evaluating new ideas and concepts.

Identifying and using relevant content of IFAC and ICAEW Code of Ethics.

Recognising ethical issues arising from situations likely to be encountered by trainee chartered accountants; identifying possible courses of action to resolve them.

How skills are assessed

Requirements will include:

applying elements of the IASB conceptual framework for financial reporting;

applying knowledge of financial reporting standards;

preparing and presenting financial statements from accounting data in conformity with IFRS for single entities, whether organised in corporate or in other forms and entities requiring consolidated financial statements;

explaining the principal differences between IFRS and UK GAAP; and

identifying ethical issues and using ethical codes to formulate solutions.

Applying judgement

Assessed skills

Understanding data and information given to reach the correct financial reporting judgement.

Drawing upon technical and professional knowledge learnt to analyse issues.

Exercising ethical judgement in a given straightforward situation.

How skills are assessed

Candidates will be required to explain accounting and reporting concepts based on their judgements in non-technical language to non-financial managers.

Conclusions, recommendations and communication

Assessed skills

Preparing, describing, outlining the advice, report, notes required in a given straightforward situation.

Presenting a basic or routine memorandum or briefing note in writing in a clear and concise style.

How skills are assessed

Candidates will be required to explain accounting and reporting concepts in non-technical language to non-financial managers.

© ICAEW 2016 16

FINANCIAL MANAGEMENT

Please note that from the September 2017exam session onwards, the Financial Management module will be examined as a computer-based exam. A paper-based exam for this module will no longer be available. Find out more at icaew.com/exams

Assimilating and using information

Assessed skills

Reading and understanding subject matter.

Accessing, evaluating and managing information provided in a few defined sources.

Framing questions that clarify information or identify gaps in knowledge.

Operating to a brief in structured situations.

How skills are assessed

The majority of written test questions will require candidates to absorb and understand both structured and unstructured material. Candidates will often be required to give recommendations based on their understanding and interpretation of the information provided, supported by explanation of the reasoning behind and implications of their recommendations. Quantitative calculations will often form part of the analysis and be a means of supporting conclusions and recommendations.

Structuring problems and solutions

Assessed skills

Understanding data and information given: identifying and understanding issues arising in straight forward scenarios.

Using the data and information given: understanding requirements, analysing data and information to support the requirement.

Drawing upon technical and professional knowledge learnt to analyse issues.

Applying knowledge from different technical areas: analysing problems that combine technical skills in a single disciplinary environment.

Using new concepts: evaluating new ideas and concepts.

Financial data analysis: performing the required calculations; explaining or stating the issues.

How skills are assessed

The majority of written test questions will be scenario-based (on occasions based on actual situations in the real world), requiring candidates to assimilate significant amounts of information, to analyse it (including quantitative analysis) in a way that demonstrates relevant technical knowledge and to draw and support appropriate conclusions Quantitative analysis will form a major part of questions requiring candidates to apply technical knowledge to practical situations in order to make accurate calculations and to support sound decision-making.

Applying judgement

Assessed skills

Applying discrimination: identifying the relevant/reasonable in data and evidence; recognising varying quality in data or evidence.

Relating parts and wholes: discerning particular issues as part of wholes.

© ICAEW 2016 17

Sensitivity analysis: demonstrating an understanding of sensitivities to change: calculating a range of outputs for given inputs.

Applying a sceptical and critical approach in a given straightforward situation.

Appreciating when more expert help is required in a given straightforward situation.

Developing arguments, having first appreciated the perspective of all other parties.

Conducting critiques: critically reviewing a statement, argument or position.

How skills are assessed

In written test questions candidates will be required make sense of relatively large volumes of data, making judgments on the relevance of data for use in subsequent calculations and discussions. Even largely quantitative questions will invariably have elements in which candidates will be required to reflect on their calculations and the methodology employed and to identify and discuss the implications of calculations.

Candidates will often be required to make and justify judgements based on earlier calculations.

Conclusions, recommendations and communication

Assessed skills

Using technical knowledge to support reasoning and conclusions.

Decision-making: using relevant quantitative approaches in decision analysis.

Identifying the best explanation, solution or steps against defined criteria in a given straightforward situation.

Formulating opinions, reservations, advice, recommendations, plans, solutions, options and risks including business implications in a given straightforward situation.

Preparing, describing, outlining the advice, report, notes required in a given straightforward situation.

Presenting a basic or routine memorandum or briefing note in writing in a clear and concise style.

Combining cognitive and behavioural skills to communicate to specialists and non-specialists.

How skills are assessed

Candidates will often be required in written test questions to recommend suitable courses of action in a given situation (financing decisions, dividend decisions, investment appraisal decisions). Such advice has often to be incorporated within a ‘business report’ format, addressing both the strengths and weaknesses of any recommendations and/or reasons for the rejection of alternatives. The provision of advice to managers and others will be central to most written test questions.

© ICAEW 2016 18

TAX COMPLIANCE

Please note that from the March 2017 exam session onwards, the Tax Compliance module will be examined as a computer-based exam. A paper-based exam for this module will no longer be available. Find out more at icaew.com/exams

Assimilating and using information

Assessed skills

Reading and understanding subject matter.

Accessing, evaluating and managing information provided in a few defined sources.

Framing questions that clarify information or identify gaps in knowledge.

Operating to a brief in structured situations.

How skills are assessed

Questions will contain both structured and unstructured detail in scenarios that candidates have to read, assimilate and understand. The information will be presented in a business context, with varying technical complexity. Information may need to be assimilated from various sources within the question. Some issues may need to be deduced by inference or analysis. Candidates may be required to explain the implications of proposed transactions in any of the following ways:

calculation of tax liabilities and reliefs available;

written description of tax treatments;

explanation of tax treatments in light of unstructured information relating to individuals, partnerships or companies;

description of the availability and values of tax reliefs within the context of numerical questions;

explanation of alternative tax treatments; and

explanation of ethical issues within given scenarios.

All of these skills will be assessed in the context of:

ethics and law

capital taxes

income tax

national insurance contributions

corporation tax

VAT and stamp taxes.

Structuring problems and solutions

Assessed skills

Understanding data and information given: identifying and understanding issues arising in straightforward scenarios.

Using the data and information given: understanding requirements, analysing data and information to support the requirement.

Drawing upon technical and professional knowledge learnt to analyse issues.

Applying knowledge from different technical areas: analysing problems that combine technical skills in a single disciplinary environment.

Using new concepts: evaluating new ideas and concepts.

Appreciating the ethical dimensions of situations, problems and proposals.

Identifying and selecting appropriate courses of action using an ethical framework.

© ICAEW 2016 19

Financial data analysis: performing the required calculations; explaining or stating the issues.

Identifying and explaining the consequence of unethical behaviour.

Identifying and using relevant up to date content of the IFAC and ICAEW Codes of Ethics.

Recognising legal and ethical issues arising from situations likely to be encountered by trainee chartered accountants; identifying possible courses of action to resolve them.

How skills are assessed

Candidates may be required to:

calculate tax liabilities from a given scenario;

demonstrate relevant technical knowledge;

perform relevant, accurate calculations in a logically structured way;

identify different business entities and their tax status (eg, company, sole trader, partnerships), and understand the tax implications thereof;

integrate verbal descriptions with calculations;

use calculations to illustrate an answer; and

provide relevant legal and ethical information in the context of a tax scenario.

Applying judgement

Assessed skills

Applying discrimination: identifying the relevant/reasonable in data and evidence; recognising varying quality in data or evidence.

Relating parts and wholes: discerning particular issues as part of wholes.

Sensitivity analysis: demonstrating an understanding of sensitivities to change; calculating a range of outputs for given inputs.

Appreciating when more expert help is required in a given straightforward situation.

Exercising ethical judgement in a given straightforward situation.

Conducting critiques: critically reviewing a statement, argument or position.

How skills are assessed

Candidates may be asked to critically evaluate the quality, completeness and integrity of

information put forward by tax payers.

Candidates may be required to assess the legality of options and the consequences of various courses of action with regard to:

new client procedures;

HMRC errors;

money laundering; and

tax avoidance and evasion.

Conclusions, recommendations and communication

Assessed skills

Using technical knowledge to support reasoning and conclusions.

Decision making: using relevant quantitative approaches in decision analysis.

Identifying the best explanation, solution or steps against defined criteria in a given straightforward situation.

Formulating opinions, reservations, advice, recommendations, plans, solutions, options and risks including business implications in a given straightforward situation.

Preparing, describing and outlining clearly the advice, report notes required in a given straightforward situation.

How skills are assessed

© ICAEW 2016 20

Candidates may be asked to analyse the implications of various courses of action out of a limited

set of prescribed options.

Candidates may be required to:

determine the tax implications of scenarios and proposals to provide alternative tax implications;

take a given set of circumstances and reach a reasoned conclusion; and

justify a conclusion made using knowledge of the existing tax regime.

Illustrative examples of this would be to reach conclusions on:

possible VAT treatments eg with regard to transactions involving land and buildings;

inheritance tax implications of a proposed lifetime transfer or a transfer on death;

the impact of residency status on income tax, capital gains tax or corporation tax; or

whether an individual is trading by applying the badges of trade to reach a reasoned conclusion.

This list is not exhaustive.

© ICAEW 2016 21

BUSINESS PLANNING

The Business Planning modules provide students with the opportunity to gain subject- and sector-specific knowledge while studying for the ACA. The suite of Business Planning modules are based on the same syllabus structure and skills frameworks, and will provide students with the opportunity to demonstrate their learning and use this in the context of taxation, banking or insurance. Students will sit one of the Business Planning modules. There are three to choose from – Business Planning: Taxation, Business Planning: Banking and Business Planning: Insurance. Students are advised to speak to their employer to determine which Business Planning module to take. If a student is studying the ACA independently, they should consider their future ambitions when selecting which modules to sit.

Assimilating and using information

Assessed skills

Reading and understanding subject matter in a given complex situation.

Accessing, evaluating and managing information provided in multiple sources.

Framing questions that clarify information or identify gaps in knowledge.

Operating to a brief in structured situations.

Explaining the nature of ethics and its significance in the business environment.

Understanding the public interest and corporate and social responsibility.

Understanding the importance of contributing to the profession.

Appreciating the ethos and culture of the accountancy profession.

Understanding the role of the professional accountant within the public interest, practice and business contexts and the regulatory structure of the profession.

Understanding the importance of ethical behaviour to a professional and the reasons for the adoption of ethical codes by professions acting in the public interest.

Understanding the pressures on professional ethical behaviour, including the interaction between professional ethics and the law and other value systems.

How skills are assessed

Questions will contain both structured and unstructured detail in scenarios that candidates have to read, assimilate and understand. The information will be presented in a business context, with varying technical complexity. Information may need to be assimilated from various sources within the question. Some issues may need to be deduced by inference or analysis. Scenarios may be based on both historic and future events. Candidates may be required to respond to instructions from different parties for example a line manager, a client request or from other senior personnel. The requests may be specific, or they may be more general requiring interpretation by the candidate.

© ICAEW 2016 22

Candidates may be required to:

Business Planning: Taxation Business Planning: Banking Business Planning: Insurance

assimilate information provided by internal and external sources;

identify and evaluate inconsistencies in information provided from multiple sources; and

recognise and explain key ethical issues for an accountant undertaking work in taxation.

recognise specific issues that may arise in the context of the situation described;

identify and evaluate inconsistencies in information provided from multiple sources; and

recognise and explain key ethical issues for an accountant undertaking work in banking.

recognise specific issues that may arise in the context of the situation described;

identify and evaluate inconsistencies in information provided from multiple sources; and

recognise and explain key ethical issues for an accountant undertaking work in insurance.

Structuring problems and solutions

Assessed skills

Understanding data and information given: identifying and understanding issues arising in given scenarios.

Using the data and information given: understanding requirements, analysing data and information to support the requirement.

Drawing upon technical and professional knowledge learnt to analyse issues.

Applying knowledge from different technical areas: identifying a range of solutions from problem analysis in a defined situation.

Using new concepts: evaluating new ideas and concepts.

Appreciating the ethical dimensions of situations, problems and proposals.

Identifying and selecting appropriate courses of action using an ethical framework.

Financial data analysis: performing the required calculations; explaining or stating the issues

Identifying and explaining the consequence of unethical behaviour.

Identifying and using relevant up to date content of the IFAC and ICAEW codes of ethics.

Recognising ethical issues arising from situations likely to be encountered by trainee chartered accountants; identifying and selecting appropriate resolutions to them in given complex situations.

How skills are assessed:

Candidates may be required to:

Business Planning: Taxation Business Planning: Banking Business Planning: Insurance

consider and calculate a range of appropriate tax treatments;

provide descriptive analysis and explanations;

integrate different taxes and jurisdictions;

evaluate taxation impact of a transaction;

integrate descriptions with calculations in a form appropriate for the user;

apply technical knowledge to perform relevant,

formulate, evaluate and implement accounting and reporting policies;

identify regulatory issues and requirements and consider appropriate responses where necessary;

integrate requirements of various international regulatory bodies and jurisdictions;

identify audit issues for a banking client and

formulate, evaluate and implement accounting and reporting policies;

identify regulatory issues and requirements and consider appropriate responses where necessary;

integrate requirements of various international regulatory bodies and jurisdictions;

identify audit issues for an insurance client and

© ICAEW 2016 23

accurate calculations in a logically structured way;

identify further information or clarifying existing arrangements with a client;

consider the impact of delaying or modifying future decisions; and

identify and explain ethical and legal issues.

suggest appropriate responses

integrate descriptions with calculations in a form appropriate for the user;

apply technical knowledge to perform relevant, accurate calculations in a logically structured way;

identify further information needed;

provide descriptive analysis and explanations; and

identify and explain ethical and legal issues.

suggest appropriate responses

integrate descriptions with calculations in a form appropriate for the user;

apply technical knowledge to perform relevant, accurate calculations in a logically structured way;

identify further information needed;

provide descriptive analysis and explanations; and

identify and explain ethical and legal issues.

Applying judgement

Assessed skills

Applying discrimination: filtering information provided in complex problems to identify critical factors, understanding that not all issues are clear cut.

Relating parts and wholes: discerning particular issues as part of wholes.

Sensitivity analysis: demonstrating an understanding of sensitivities to change, calculating a range of outputs for given inputs.

Demonstrating an understanding of different perspectives (eg, social, political, economic): analysing and interpreting problems and situations from alternative given stances.

Applying a sceptical and critical approach in a given complex situation.

Appreciating when more expert help is required in a given complex situation.

Exercising ethical judgement in a given complex situation with a range of alternative actions.

Developing arguments, having first appreciated the perspective of all other parties.

Conducting critiques: critically reviewing situations and problems. .

How skills are assessed:

Candidates may be asked to evaluate critically the quality, completeness and integrity of information in a given scenario. Judgement will be applied in the context of scenarios of varying complexity, involving calculations and the drawing of inferences from information provided.

Examples of how candidates may be required to apply their judgement include:

Business Planning: Taxation Business Planning: Banking Business Planning: Insurance

applying scepticism to the integrity of information provided in the scenario having regard to its source;

selecting between appropriate options;

identifying omissions in the information;

applying scepticism to the integrity of information provided in the scenario having regard to its source;

identifying omissions in the information;

evaluating inconsistencies in information;

applying scepticism to the integrity of information provided in the scenario having regard to its source;

identifying omissions in the information;

evaluating inconsistencies in information;

© ICAEW 2016 24

evaluating inconsistencies in information;

evaluating the effects of future events;

identifying key linkages between information provided in a scenario and possible tax treatments;

comparing the effects of a range of estimates, outcomes or tax treatments; and

exercising own ethical judgement in assessing the consequences of various courses of action.

exercising own ethical judgement in assessing the consequences of various courses of action;

evaluating the effects of future events;

assessing the materiality of errors; and

selecting between appropriate options.

exercising own ethical judgement in assessing the consequences of various courses of action;

evaluating the effects of future events;

assessing the materiality of errors; and

selecting between appropriate options.

Conclusions, recommendations, and communication

Assessed Skills

Using technical knowledge and professional experience to support reasoning and conclusions.

Decision making: assimilating data from different sources and data types in decision analysis.

Identifying the best explanation, solution or steps against defined criteria in a given complex situation.

Formulating opinions, reservations, advice, recommendations, plans, solutions, options and risks including business implications in a given complex situation.

Preparing, describing, outlining the advice, report notes required in a given complex situation.

Combining cognitive and behavioural skills to communicate clearly to a specialist or non-specialist audience.

How skills are assessed

Candidates may be required to:

Business Planning: Taxation Business Planning: Banking Business Planning: Insurance

determine the tax implications of scenarios and proposals to provide alternative recommendations to meet a given individual or corporate objective or goal;

formulate and recommend a reasoned conclusion from structured calculations;

justify a conclusion made using knowledge of the existing tax regime;

advise on the ethical considerations; and

formulate and recommend a reasoned conclusion from data, facts, calculations, judgements and own analysis;

advise on the ethical considerations; and

draw conclusions from data, facts, calculations, judgements and own analysis;

explain the limitations of conclusions or recommendations;

formulate and recommend a reasoned conclusion from data, facts, calculations, judgements and own analysis;

draw conclusions from data, facts, calculations, judgements and own analysis;

advise on the ethical considerations; and

explain the limitations of conclusions or recommendations;

© ICAEW 2016 25

explain the limitations of conclusions or recommendations.

identify key linkages; and

compare the effects of a range of estimates, and outcomes or financial treatments.

identify key linkages; and

compare the effects of a range of estimates, and outcomes or financial treatments.

Examples of how candidates may be required to present their recommendations are:

Business Planning: Taxation Business Planning: Banking Business Planning: Insurance

a report/memorandum in response to a specific technical or ethical issue and in accordance with client requirements;

a review of advice or proposed tax strategies making recommendations supported by calculations or analysis of tax issues identified; and

a justification of a specific recommended action when a variety of options are available.

a report/memorandum in response to a specific technical or ethical issue and in accordance with client requirements;

reasoned, practicable advice that is clear and concise, supported by calculations or analysis of issues identified; and

a justification of a specific recommended action when a variety of options are available.

a report/memorandum in response to a specific technical or ethical issue and in accordance with client requirements; and

reasoned, practicable advice that is clear and concise, supported by calculations or analysis of issues identified; and

a justification of a specific recommended action when a variety of options are available.

© ICAEW 2016 26

ADVANCED LEVEL

CORPORATE REPORTING

Assimilating and using information

Assessed skills

Understanding the subject matter in a practical situation.

Accessing, evaluating and managing information provided in multiple sources.

Framing questions that clarify information or identify gaps in knowledge.

Operating to a brief in structured situations.

Identifying elements of risk and uncertainty.

Explaining the nature of ethics and its significance in the business environment and understanding the importance of ethical behaviour in respect of the public interest, the accounting profession, the law and other value systems.

Understanding the importance of contributing to the profession and appreciating the ethos and culture of the accountancy profession.

Understanding the public interest and corporate responsibility.

How skills are assessed

Questions will contain both structured and unstructured details in scenarios of varying complexity with technical content and business context. Information may need to be assimilated from various sources within the question. Some issues may need to be deduced by inference or analysis. Different types of information may also need to be assimilated and synthesized to develop a coherent understanding. For example: qualitative and quantitative; market data and financial reporting information; internally generated and externally available information. Questions will require candidates to have a detailed knowledge and understanding of relevant regulations in financial reporting, auditing and ethics, which will need to be related to practical business scenarios and applied to any data provided. The data provided will focus on technical compliance and understanding. Candidates may be required to respond to instructions from a line manager, a client request or from other senior personnel. The requests may be specific, or they may be more general requiring interpretation and judgement to be applied by the candidate.

Examples of issues and tasks that candidates may be required to consider include:

evaluate the quality and relevance of information provided in the context of a particular assignment;

evaluate inconsistencies in information provided from multiple sources;

use different sources and types of evidence to confirm, or question, financial statement assertions applying professional scepticism; and

evaluate the ethical implications of making information available including confidentiality and transparency.

Structuring problems and solutions

Assessed skills

Understanding data and information given: identifying and understanding issues arising in given scenarios.

Using the data and information given: analysing data and information to support requirement.

© ICAEW 2016 27

Drawing upon technical and professional knowledge learnt to analyse issues.

Applying knowledge from different technical areas: analysing problems that combine technical skills in a single disciplinary environment and identifying a range of solutions.

Explaining, listing, drafting or stating briefly the issues or analysis.

Financial statement analysis: performing the required calculations and comparing and contrasting more than one element of the financial statements; explaining or stating the issues.

Using new concepts: evaluating new ideas and concepts.

Recognising ethical issues arising from situations likely to be encountered by ICAEW Chartered Accountants; identifying possible courses of action to resolve them; and appreciating the ethical dimensions of situations, problems and proposals.

Identifying and explaining the consequences of unethical behaviour.

Identifying and using relevant up to date content of IESBA and ICAEW codes of ethics.

Identifying and selecting appropriate courses of action using an ethical framework.

How skills are assessed

Candidates will be required to apply technical knowledge, analytical techniques and professional skills to resolve compliance and business issues that arise in the context of the preparation and evaluation of corporate reports and from providing audit services. Candidates will be required to structure problems and solutions in scenario based questions which may be presented in the following forms:

Mini case – in the context of auditing but with significant corporate reporting emphasis. This may be technical, compliance or interpretive (for example including analytical procedures).

Financial statement analysis – including technical aspects of corporate reporting.

Technical question on aspects of audit and corporate reporting (which may include assurance, internal audit).

Examples of the elements that candidates may be required to consider are:

Audit and Assurance

Business and inherent risks in complex scenarios.

The control environment.

Selective financial analysis in an auditing context.

Risk and control evaluation in the context of IT or e-business.

Design audit procedures as part of a structured response to assessed risks.

Professional scepticism in relation to audit evidence.

Consideration of appropriate corporate governance measures and structures.

Ethics

Ethical problems in reporting, assurance and business scenarios.

Relevance, importance and consequences of ethical issues.

Corporate reporting

Formulation, evaluation and implementation of accounting and reporting policies.

Measurement and recognition of assets and obligations on reported financial performance.

Impact and interaction of applicable accounting principles, bases and standards.

Appraisal of remuneration policies on reported performance.

Evaluation of reporting issues in relation to group scenarios and overseas activities.

Applying judgement

Assessed skills

Assessing arguments and considering evidence against set criteria.

Applying discrimination: filtering information provided to identify critical factors.

© ICAEW 2016 28

Relating parts and wholes: discerning particular issues within complex scenarios.

Demonstrating an understanding of sensitivities to change (sensitivity analysis): flexing a range of inputs and assessing the outcomes.

Demonstrating an understanding of different perspectives analysing and interpreting related problems and situations from alternative given stances.

Change management (appreciating the impacts/effects of change): considering and evaluating the effects of given alternative future scenarios.

Appreciating when more expert help is required.

Applying a sceptical and critical approach.

Conducting critiques: critically reviewing situations and problems.

Seeking opportunities to add value: thinking imaginatively in a business context.

Prioritising key issues.

Applying the concept of materiality.

Developing arguments, having first appreciated the perspective of other parties.

Exercising ethical judgement.

How skills are assessed

Candidates will be required to use technical knowledge and professional judgement to identify, explain and evaluate alternatives and to determine the appropriate solutions to compliance issues, giving due consideration to the needs of clients and other stakeholders. The commercial context and impact of recommendations and ethical issues will also need to be considered in making such judgements.

Judgement will be applied in the context of scenarios of varying complexity, involving calculations and the drawing of inferences from the information provided.

Candidates may be required to demonstrate judgement in the following ways:

selecting between technical choices;

filtering data to identify critical elements;

prioritising information, issues or tasks;

identifying omissions in the information;

evaluating inconsistencies in information;

distinguishing between the various qualities of the data provided;

evaluating the impact of economic and political factors;

evaluating the effects of known events;

evaluating the appropriateness of accounting policy choice and estimation selection;

evaluating options;

comparing the effects of a range of estimates, outcomes or financial treatments;

assessing the materiality of errors;

exercising ethical judgement;

identifying key linkages; and

drawing appropriate conclusions from data provided to satisfy specified objectives and assessing the materiality of errors and omissions.

Conclusions, recommendations and communication

Assessed skills

Using technical knowledge and evidence to support reasoning and conclusions.

Assimilating data from different sources, data types in making decisions.

Identifying the best explanation, solution or steps against defined criteria considering risk.

Identifying a range of solutions based on analysis and developing recommendations which combine different technical skills in a defined situation.

Formulating opinions, advice, recommendations, plans, solutions, options and reservations based on valid evidence.

© ICAEW 2016 29

Presenting analysis and recommendations in accordance with instructions.

Providing specified responses to a specialist or non-specialist audience.

How skills are assessed

Candidates may be required to draw conclusions in the following ways:

from data, facts, calculations, judgements and own analysis;

on complex assurance engagements;

by identifying weaknesses in financial information systems and their potential consequences;

by distinguishing between the qualities of data provided or other evidence generated; and

by developing risk management solutions in an audit and corporate reporting environment. Examples of how candidates may be required to present and communicate their recommendations include:

A report/memorandum in response to a specific technical issue and in accordance with client requirements.

Reasoned, practicable advice that is clear and concise, supported by calculations or analysis of technical/business issues identified.

Use judgement to select the most appropriate audit procedures in the context of risks identified.

Justifying a specific recommended action when a variety of options are available.

Candidates may be required to explain the limitations of their conclusions or recommendations.

© ICAEW 2016 30

STRATEGIC BUSINESS MANAGEMENT

Assimilating and using information

Assessed skills

Understanding the subject matter in a practical situation.

Accessing, evaluating and managing information provided from multiple sources.

Framing questions that clarify information or identify gaps in knowledge.

Operating to a brief in structured situations.

Explaining the nature of ethics and its significance in the business environment and understanding the importance of ethical behaviour in respect of the public interest, the accounting profession, the law and other value systems.

Understanding the importance of ethical behaviour to a professional accountant and the reasons for the adoption of ethical codes by professions acting in the public interest.

Understanding the importance of contributing to the profession, appreciating the ethos and culture of the accountancy profession and understanding the role of the professional accountant within the public interest, practice and business contexts and the regulatory structure of the profession.

Understanding the public interest and corporate responsibility.

How skills are assessed

Questions will contain both structured and unstructured details in scenarios of varying complexity and technical content. The scenarios will normally be forward looking, but past evidence and current circumstances will also be relevant. Information may need to be assimilated from various sources within the question. Some issues may embedded and need to be deduced by inference or analysis. Different types of information may also need to be assimilated and synthesized to develop a coherent understanding. For example: qualitative and quantitative; market data and financial reporting information; internally generated and externally available information. Questions will require candidates to have a detailed knowledge and understanding of relevant regulations, techniques and concepts in business management, finance, corporate reporting, assurance and ethics. This knowledge will need to be assimilated and applied in order to solve practical business problems, using any data and other information provided. The data provided may include both historic information and projections/forecasts. Candidates may be required to respond to instructions from a line manager, a client request or from other senior personnel. The requests may be specific, or they may be more general, requiring interpretation and judgement to be applied by the candidate. Examples of issues and tasks that candidates may be required to consider include:

evaluate the quality and relevance of information provided in the context of a particular assignment;

evaluate inconsistencies in information provided from multiple sources;

use different sources and types of evidence to confirm, or question, financial statement assertions applying professional scepticism;

extrapolate given information into the future based upon given or own assumptions; and

evaluate the ethical implications of making information available including confidentiality and transparency.

© ICAEW 2016 31

Structuring problems and solutions

Assessed skills

Understanding data and information given, structuring the information and identifying gaps.

Assimilating raw data to produce more meaningful information relevant in resolving a particular problem.

Explaining, listing, drafting or stating briefly the issues or analysis.

Data analysis:

structuring, transforming and analysing data provided (financial and non-financial) in order to enhance understanding of business issues and their underlying causes, and to enable conclusions to be drawn to support solutions to complex problems.

Financial statement analysis:

reviewing and evaluating a company’s financial statements by comparing and contrasting individual elements over time, or by comparison to a similar entity, in order to enhance understanding of the company’s performance and position, make projections and inform decision making.

Analysing and evaluating new and complex ideas within a defined situation.

Identifying the relevant technical knowledge and professional experience required to solve problems and generate solutions; including identification and evaluation of risks within the scenario.

Recognising ethical issues arising from situations likely to be encountered by ICAEW Chartered Accountants; identifying possible courses of action to resolve them and appreciating the ethical dimensions of situations, problems and proposals.

Approaching decision making using an ethical framework, including identifying and using IESBA and ICAEW Codes of Ethics.

How skills are assessed

Scenarios will be integrated to cover more than one technical discipline. Examples of issues and tasks that candidates may be required to consider include: Business management

Undertaking a critical assessment of key business issues.

Structuring market data and industry data from various sources.

Explaining and evaluating the strengths and weaknesses of an organisation or segments of an organisation.

Evaluating the impact of decisions on business strategy.

Evaluating the impact of financial strategy on business strategy. Finance

Undertaking valuations, where the information is incomplete, suspect or unsuitable.

Undertaking financial risk analysis and considering the management of financial risks.

Evaluating the impact of business strategy on financial strategy. Corporate reporting

Considering relevance and reliability of unstructured information.

Evaluating the impact and legitimacy of a range of financial reporting treatments.

Dealing with complex financial reporting information.

Impact of future events on financial statements.

Impact on financial statements of delaying or modifying business and financial decisions.

Evaluating business position, prospects and risks. Assurance

© ICAEW 2016 32

Understanding business and inherent risks in complex scenarios.

Evaluating the control environment.

Undertaking selective financial analysis.

Evaluating risk and control evaluation in the context of IT.

Undertaking assurance to support specific transactions (eg, due diligence).

Applying professional scepticism. Ethics

The structured application of ethical codes and structured application.

Identifying ethical problems in complex scenarios and structuring appropriate actions.

Applying judgement

Assessed skills

Assessing arguments and considering evidence against set criteria.

Applying discrimination: filtering information to identify critical factors.

Relating parts and wholes: discerning particular issues within complex scenarios.

Demonstrating an understanding of sensitivities to change (sensitivity analysis): flexing a range of inputs and assess the outcomes.

Demonstrating an understanding of different perspectives, analysing and interpreting related problems and situations from alternative given stances.

Change management (appreciating the impacts/effects of change): considering and evaluating the effects of given alternative future scenarios.

Appreciating when more expert help is required.

Applying professional scepticism and critical evaluation.

Conducting critiques: critically reviewing situations and problems.

Seeking opportunities to add value: thinking imaginatively in a business context.

Prioritising key issues to solve business and financial problems, leading to creative and realistic solutions.

Applying the concept of materiality, including drawing inferences about risk.

Appreciating the needs and perspectives of a range of stakeholders, including issues of corporate responsibility and sustainability.

Exercising ethical judgement.

Identifying a range of choices, selecting and justifying the most appropriate.

How skills are assessed

Judgement will be applied in the context of scenarios of varying complexity, which require the drawing of inferences and conclusions from prior qualitative and quantitative analysis, and other information, in order to solve problems and developing a solution, or alternative solutions. Examples of how candidates may be required to apply their judgement include:

selecting between technical choices;

filtering data to identify critical elements;

prioritising information, issues or tasks;

identifying omissions in the information provided;

evaluating inconsistencies in information;

distinguishing between the various qualities of the data provided;

evaluating the impact of business, financial and economic factors;

evaluating the effects of future events;

evaluating the appropriateness of accounting policy and estimation selection;

comparing the effects of a range of estimates, outcomes or financial treatments;

exercising ethical judgement;

identifying key linkages; and

© ICAEW 2016 33

drawing appropriate conclusions from data provided to satisfy specified objectives and assessing the materiality of errors and omissions.

Conclusions, recommendations and communication

Assessed skills

Using technical knowledge, evidence and analysis to provide reasoned conclusions and advice.

Making evidence-based recommendations which can be justified by reference to supporting data and other information.

Identifying the best explanation, solution or steps against defined criteria, considering risk and other specified objectives and constraints.

Identifying a range of solutions, based on analysis, and developing recommendations which combine different technical skills and business and financial awareness in a defined situation.

Formulating opinions, advice, plans, options and reservations based on valid prior analysis.

Presenting analysis and recommendations in accordance with instructions.

Providing specified responses to a specialist audience.

Communicating recommendations in a manner suitable for the intended recipients.

How skills are assessed

Examples of how candidates may be required to draw conclusions include:

from data, facts, calculations, judgements and own analysis;

on complex assurance engagements;

by identify weaknesses in financial information systems and their potential consequences;

by distinguishing between the qualities of data provided or other evidence generated;

by developing risk management solutions;

by making strategic decisions; and

by valuing a company or a financial instrument. Examples of how candidates may be required to present their recommendations include:

A report/memorandum in response to a specific technical or business issue and in accordance with client requirements.

Reasoned, practicable advice that is clear and concise, supported by calculations or analysis of technical or business issues identified.

Justifying a specific recommended action when a variety of options are available. Candidates may be required to explain the limitations of their conclusions or recommendations.

© ICAEW 2016 34

CASE STUDY

Assimilating and using information

Assessed skills

Understanding the subject matter.

Accessing, evaluating and managing data and information provided in multiple sources (some pre-disclosed) and from independent research plans.

Using technical knowledge and professional experience to assess interaction of information from different sources.

Framing questions that clarify information or identify gaps in knowledge.