Embed Size (px)

Citation preview

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Proprietary and confidential

ACA Compliance Playbook: The Two New Pay-or-Play Rules You

Must Follow to Avoid Up to $1.5 Million in Fines

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

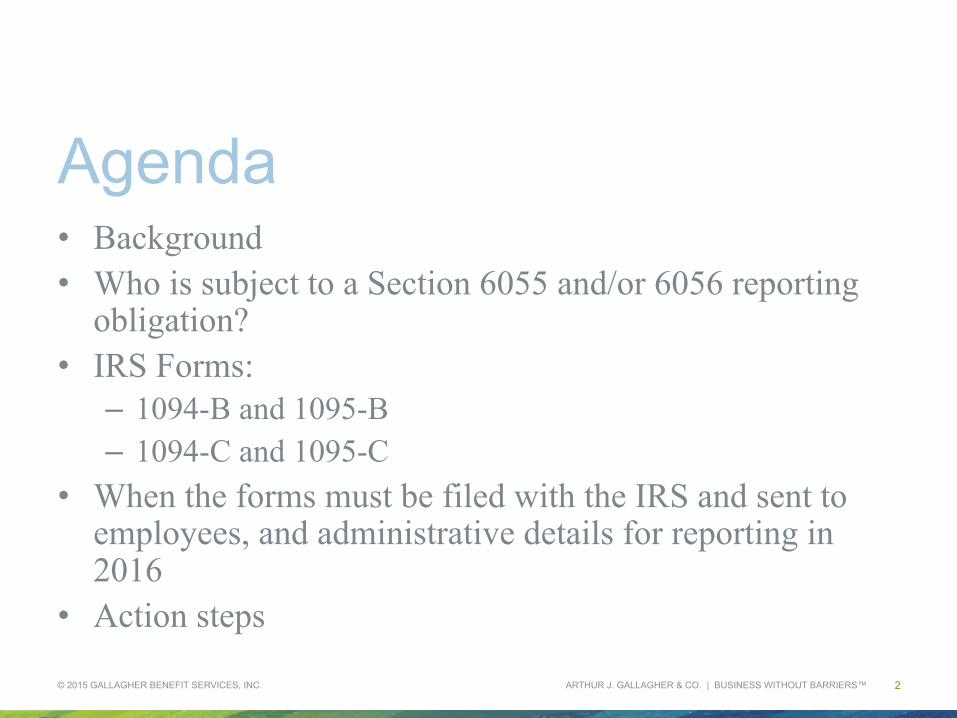

Agenda • Background • Who is subject to a Section 6055 and/or 6056 reporting

obligation? • IRS Forms:

– 1094-B and 1095-B – 1094-C and 1095-C

• When the forms must be filed with the IRS and sent to employees, and administrative details for reporting in 2016

• Action steps

© 2015 GALLAGHER BENEFIT SERVICES, INC. 2

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Background • PPACA created two significant IRS reporting obligations

that will commence in early 2016: – Internal Revenue Code Section 6055 requires insurers and

sponsors of self-insured plans to prepare annual reports regarding “minimum essential coverage” (“MEC”)

– Internal Revenue Code Section 6056 requires “applicable large employer” members (“ALE” members) to prepare annual reports regarding the coverage offered to their employees

© 2015 GALLAGHER BENEFIT SERVICES, INC. 3

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Who is Required to Report?

© 2015 GALLAGHER BENEFIT SERVICES, INC. 4

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Section 6055 (“MEC”) • Employers (of all sizes) who sponsor self-insured health

plans that provide minimum essential coverage to any individual during the calendar year are required to report under Section 6055. – What if we sponsor a fully-insured plan? Your health

insurance carrier will be responsible for Section 6055 reporting for that plan.

© 2015 GALLAGHER BENEFIT SERVICES, INC. 5

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

What is MEC? • Eligible employer-sponsored plans

– Both fully-insured and self-insured, regardless of employer size

– This does not include excepted benefits – This does include even “low cost” plans or plans that do

not provide minimum value – Reporting not required for coverage that supplements MEC

• Government-sponsored programs • Insured plans offered in the individual market or group

market

© 2015 GALLAGHER BENEFIT SERVICES, INC. 6

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Section 6056 (“ALE”) • Applicable large employer members (both fully-insured

and self-insured) must report information to the IRS about the health coverage, if any, that they offered to full-time employees

• Such ALE members must also report information about whether the coverage was affordable and whether coverage was offered to dependents

• Finally, this reporting is the mechanism in place for an employer to claim an exemption or delay in penalty exposure due to various forms of transitional relief

© 2015 GALLAGHER BENEFIT SERVICES, INC. 7

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Who is an ALE member? • Applicable large employers are those with 50 or more

full-time (FT) and full-time equivalent (FTE) employees • Status as applicable large employer is based on the entire

controlled group, but each ALE member reports separately for its employees

• NOTE: All ALE members remain subject to 6056 reporting for the 2015 calendar year, even if transitional relief delays their penalty exposure until later

© 2015 GALLAGHER BENEFIT SERVICES, INC. 8

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

ESR Penalties: A Refresher • Penalty for failing to offer coverage – 4980H(a)

– An employer must offer “minimum essential coverage” to 95% (70% for 2015) of its full-time employees and their dependent children up to age 26 or risk a penalty equal to (i) $2,080 (indexed), multiplied by (ii) the number of full-time employees minus 30 (80 for 2015)

– There is no requirement that the coverage be affordable or provide “minimum value” to avoid this penalty.

– But…

© 2015 GALLAGHER BENEFIT SERVICES, INC. 9

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

ESR Penalties: A Refresher • Penalty for failing to offer coverage which is both

affordable and provides minimum value – Section 4980H(b) – If the employer fails to offer coverage that is both

affordable and provides minimum value to a full-time employee, it can risk a penalty equal to $3,120 (indexed) per year for that employee

– Penalty can only be triggered if a full-time employee goes to the marketplace and receives premium tax assistance

© 2015 GALLAGHER BENEFIT SERVICES, INC. 10

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

IRS Forms

© 2015 GALLAGHER BENEFIT SERVICES, INC. 11

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Forms 1095-B and 1094-B • Used by plan sponsors of self-insured employer coverage

if the employer is not an applicable large employer member – In other words, this form is used by small, self-insured

employers – A Form 1095-B is provided to each “responsible

individual” – The Form 1094-B is the transmittal form

• Also used by insurance carriers for fully-insured coverage

© 2015 GALLAGHER BENEFIT SERVICES, INC. 12

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

1095-B: Parts I, II, and III

© 2015 GALLAGHER BENEFIT SERVICES, INC. 13

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

1095-B: Part IV

© 2015 GALLAGHER BENEFIT SERVICES, INC. 14

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Forms 1095-C and 1094-C • Used by applicable large employer members, regardless

of whether they are fully-insured or self-insured. – Employers that are fully-insured may leave part of the

Form 1095-C blank (the portion dealing with covered individuals)

• Keep in mind the rules for who is an ALE member – Even if transitional relief delays potential penalties, the

reporting obligation will apply for 2015

© 2015 GALLAGHER BENEFIT SERVICES, INC. 15

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

1095-C: Parts I and II

© 2015 GALLAGHER BENEFIT SERVICES, INC. 16

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

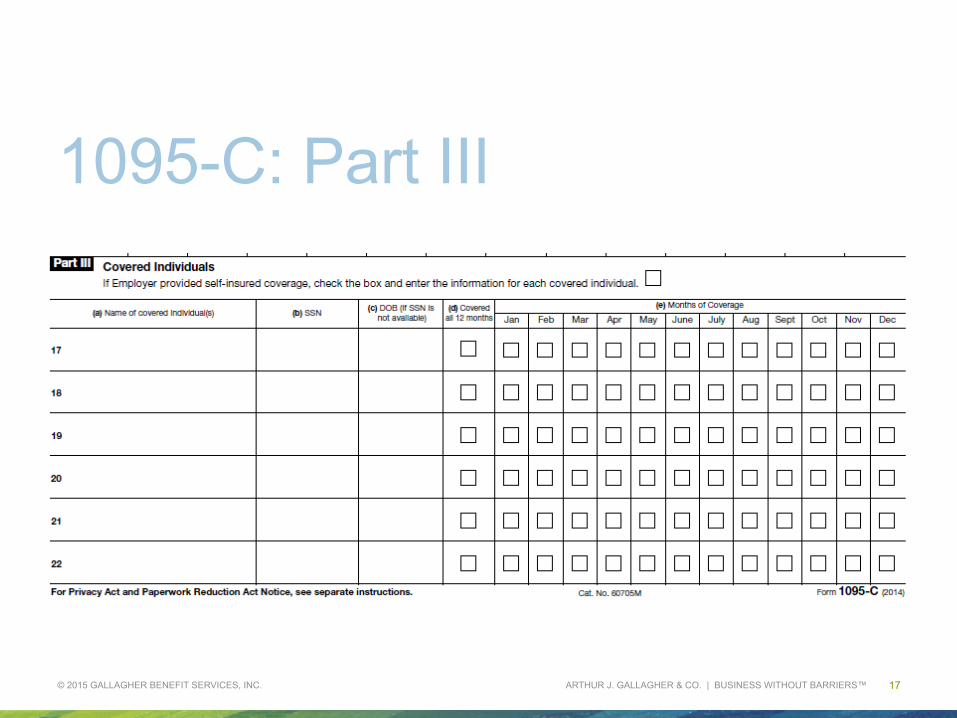

1095-C: Part III

© 2015 GALLAGHER BENEFIT SERVICES, INC. 17

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

1094-C: Part I

© 2015 GALLAGHER BENEFIT SERVICES, INC. 18

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Who Reports What? (Revisited)

© 2015 GALLAGHER BENEFIT SERVICES, INC. 19

Employer and Plan Type Type of Reporting Who Reports IRS Transmittal IRS Return Employee

Statement

Large employer* with fully insured group health plan

6055 Health insurance issuer or carrier 1094-‐B 1095-‐B 1095-‐B

6056 Employer 1094-‐C 1095-‐C, Parts I and II 1095-‐C, Parts I

and II (or alternaFve)

Large employer* with self-‐insured group health plan covering employees only

Combined 6055 and 6056 Employer 1094-‐C 1095-‐C 1095-‐C

Large employer* with self-‐insured group health plan covering employees and non-‐employees (e.g., directors, reFrees, or COBRA qualified beneficiaries)

Employees: Combined 6055 and

6056 Employer 1094-‐C 1095-‐C 1095-‐C

Non-‐employees employed for 1 or more months:

Combined 6055 and 6056

Employer 1094-‐C 1095-‐C 1095-‐C

Non-‐employees for all 12 months: 6055 Employer

1094-‐B or

1094-‐C**

1095-‐B or

1095-‐C, Part III**

1095-‐B or

1095-‐C, Part III**

* A large employer is an employer with 50 or more full-‐Fme and full-‐Fme equivalent employees. ** If using Form 1094-‐B as the transmiQal form, use Form 1095-‐B for the IRS return and employee statement. If using Form 1094-‐C for transmiQal, use Form 1095-‐C for the IRS return and employee statement.

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

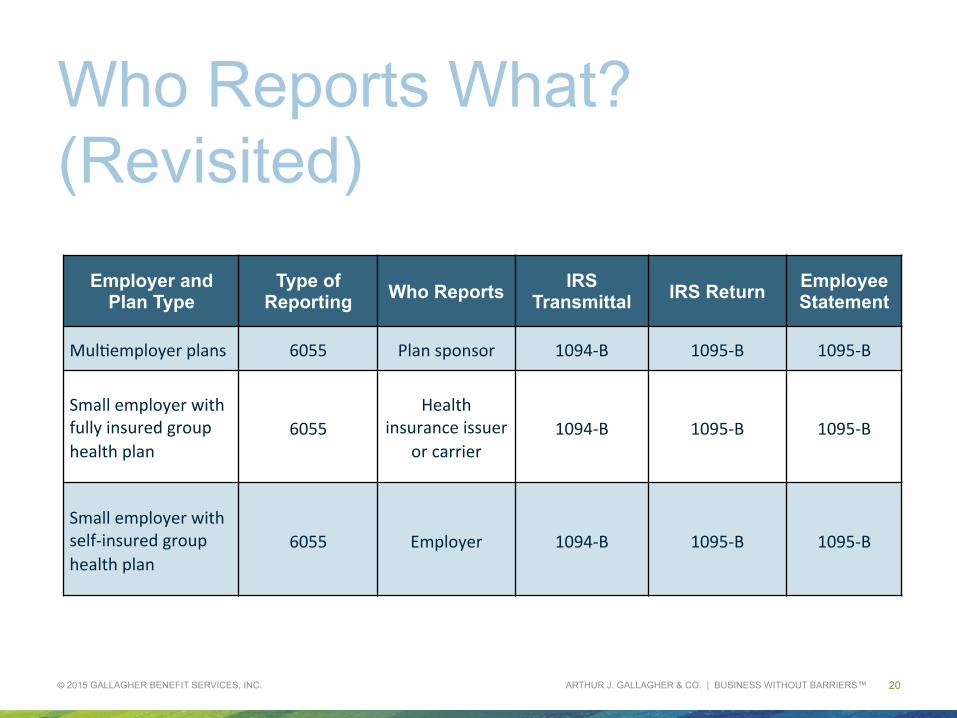

Who Reports What? (Revisited)

© 2015 GALLAGHER BENEFIT SERVICES, INC. 20

Employer and Plan Type

Type of Reporting Who Reports IRS

Transmittal IRS Return Employee Statement

MulFemployer plans 6055 Plan sponsor 1094-‐B 1095-‐B 1095-‐B

Small employer with fully insured group health plan

6055 Health

insurance issuer or carrier

1094-‐B 1095-‐B 1095-‐B

Small employer with self-‐insured group health plan

6055 Employer 1094-‐B 1095-‐B 1095-‐B

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Details and Deadlines

© 2015 GALLAGHER BENEFIT SERVICES, INC. 21

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Method of IRS Reporting • Mailing the forms to the IRS is permitted for employers

with fewer than 250 Forms 1095-B or 1095-C in a calendar year.

• Can I submit the reports electronically? – IRS encourages all employers to file their forms

electronically. – Employers that file at least 250 Forms 1095-B or 1095-C in

a calendar year are required to file electronically. Other employers may file electronically; but are not required to do so.

© 2015 GALLAGHER BENEFIT SERVICES, INC. 22

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Statements to Employees • How should I send out the statements?

– Mail – Electronically (if employee has consented to electronic) – Posting to a website (an employer must separately notify

the employee) – Employee can also request a paper copy

• Can we send out the employee statements with the Forms W-2? – Yes. Employers may include an employee’s statement with

his or her Form W-2 mailing.

© 2015 GALLAGHER BENEFIT SERVICES, INC. 23

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Separate Return and Statement Deadlines

Report/Disclosure Due date Form 1095-B to employees 1/31 of each year (2/1/16) Forms 1095-B and 1094-B to IRS 2/28 (or 3/31 if filed electronically*) Form 1095-C to employees 1/31 of each year (2/1/16) Forms 1095-C and 1094-C to IRS 2/28 (or 3/31 if filed electronically*)

© 2015 GALLAGHER BENEFIT SERVICES, INC. 24

* Must file electronically if provide 250 or more “returns”

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Penalties • Failure to timely file complete and accurate returns to the IRS, or

failure to timely furnish a correct statement to responsible individuals: – $100 per return with a maximum of $1,500,000 for a calendar year. – Penalties may be reduced if corrective action is taken within 30 days

and may even be waived if the failure to file timely or accurately is due to reasonable cause and not due to willful neglect.

• Penalty relief for reports filed in 2016 as long as “good faith” efforts to comply are made

• Important Note: the C series forms themselves will trigger penalties under employer shared responsibility rules, if you failed to offer coverage to a sufficient number of your full-time employees, or if the coverage you did offer was not affordable or did not provide minimum value

© 2015 GALLAGHER BENEFIT SERVICES, INC. 25

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Action Steps • Collect data during 2015

regarding: – Who is covered by MEC – Who are full-time

employees – Who was offered coverage – Was coverage affordable

• Consider vendor options for data aggregation and reporting

© 2015 GALLAGHER BENEFIT SERVICES, INC. 26

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Action Steps • Request Social Security

numbers for covered dependents

• Button-up compliance with employer shared responsibility rules

• Determine other controlled group and affiliated service group members

© 2015 GALLAGHER BENEFIT SERVICES, INC. 27

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Resources: ajghealthcarereform.com

© 2015 GALLAGHER BENEFIT SERVICES, INC. 28

ARTHUR J. GALLAGHER & CO. | BUSINESS WITHOUT BARRIERS™

Thank you!

The intent of this presenta8on is to provide you with general informa8on regarding the status of, and/or poten8al concerns related to, your current employee benefits issue. It does not necessarily fully address all your specific issues. It should not be construed as, nor is it intended to provide, legal or tax advice. Ques8ons regarding specific issues should be addressed by the your organiza8on's general counsel, tax advisor, or an aHorney who specializes in this prac8ce area.