Embed Size (px)

Citation preview

ABU DHABI REAL ESTATE MARKET OVERVIEW

Q3 2015

REAL ESTATE SERVICES

CONTENTSDemand Drivers 4

Macro Trends 6

Residential Sector 8

Project in Focus 16

Office Sector 18

Retail Sector 22

Hospitality Sector 24

Definitions & Methodology 28

Contact Information 29

Supply - Photo Gallery 30

Development Location Map 32

REPORT HIGHLIGHTS Residential

Property values in the residential market have remained stable in Q3, reflecting low transaction volumes in the secondary market.

The low transaction volumes are a product of three factors:-

1) Weaker investor sentiment due to the impact of lower oil revenues which has seen a period of price stagnation in Abu Dhabi and prices falling in Dubai.

2) A lack of availability of good stock, as owners remain unmotivated to sell in the current market, with many enjoying healthy rental yields.

3) The increase in off-plan investment opportunities offering attractive payment plan terms is diverting some liquidity into this segment of the market.

There is evidence that rents may be approaching their ceiling level at the top end of the market demonstrated by modest growth of only 1% in the last 3 months despite a low level of vacancy and new supply in the high-end/luxury sectors. Developments in this segment have experienced year on year growth of between 7 to 10% hence many tenants are still facing sizeable increases at lease renewal.

Office

The commercial office market remains subdued and has seen low leasing activity during the last quarter. Although demand has declined, particularly from the government sector, this has been balanced by a lack of new supply entering the market, which has resulted in marginal rental increases of between 1-3%.

There are a number of office developments which are close to entering the market, including the ADIB HQ Tower 2 situated on Airport Road, Maryha Tower on Maryha Island, developed by Al Hilal Bank and the Al Qudra HQ at Khalifa Park, which together will add approximately 60,000 sqm of net leasable space.

Retail Sector

The retail sector has witnessed no major supply entering the market in Q3 with the majority of new supply comprising ancillary “street retail” on Abu Dhabi Island and mainland. This in turn is allowing the retail malls to focus on increasing their foot-falls by attracting tourists and residents in an increasingly competitive environment.

Retail rents across Abu Dhabi malls have remained stable during Q3 2015, although some mall tenants are requesting rental reductions at lease renewal, driven falling revenues witnessed by small retail stores during Q3 2015.

Hospitality Sector

Growth in guest arrivals into Abu Dhabi (up by 22% in Q2 2015 vs. Q2 2014), driven mainly by growth in tourists from China (68%), US (30%), Philipines (29%) and KSA (27%).

The hospitality sector is gearing up for the opening of Lourve Abu Dhabi, which is expected to increase the number of tourist arrivals into Abu Dhabi.

One of the aims of this report is to aid with improving market transparency by basing our analysis wherever possible on primary transactional evidence derived from our own managed portfolio and from the analysis of our sales and home financing activities. We believe that this adds credibility to the analysis and we hope provides confidence in its reliability.

MPM PROPERTIES FACTS AND FIGURES FOREWORD ADIB Real Estate Services comprises a comprehensive real estate banking and advisory platform providing the full range of professional services from a single provider. Our services include:-

�� Real estate financing�� Strategic development advisory�� Investment advisory�� Asset management�� Project management

�� Valuation�� Agency�� Market research�� Property management�� Facilities management

RENTAL INDEX | ABU DHABI REAL ESTATE MARKET OVERVIEWQ3 2015

2

RENTAL INDEX | ABU DHABI REAL ESTATE MARKET OVERVIEW Q3 2015

3

DEMAND DRIVERS – Q3 2015

GOVERNMENT INITIATIVES �� In line with the directives of President His

Highness Sheikh Khalifa bin Zayed Al Nahyan and His Highness Sheikh Mohamed bin Zayed Al Nahyan, Crown Prince of Abu Dhabi, Deputy Supreme Commander of the UAE Armed Forces and Chairman of Abu Dhabi Executive Council, new housing loans worth AED2,404 billion for 1,202 beneficiaries have been approved in the Emirate of Abu Dhabi

�� According to the World Economic Forum’s Global Competitiveness Index, UAE has moved to 17th position from 37th position in 2007 as the most competitive nation in the world,

placing it firmly in the ranks of the world’s elite innovation-based economies

�� The UAE will introduce new labour reforms aimed at tightening oversight of employment agreements for the millions of temporary migrant workers who make up the bulk of the country’s workforce. The reforms are being implemented through three decrees that will take effect on January 1. Three new labour rules issued by the Ministry of Labour include ministry-approved contracts, conditions for terminating employees and labour permits to work for new employers

TOURISM INITIATIVES�� The Ministry of Interior has launched a 90 days visit visas

accessed, either via the ministry website www.moi.gov.ae or its smartphone app

�� 26 events spread across eight-months have been announced by The Abu Dhabi Tourism and Culture Authority around the capital, in the Liwa desert and in Al Ain. The Abu Dhabi Classics season will

run until May next year and includes performances by well-known names in western and eastern classical music under the theme Music and Poetry, exploring how the genres blend

�� Under the patronage of Sheikh Mansour bin Zayed, Deputy Prime Minister and Minister of Presidential Affairs, Abu Dhabi is to host Red Bull X-Fighters World Tour finale on October 30

KEY EVENTS�� Ramadan and Eid Festival

7th July – 28th July

�� Eid al-Adha Exhibition 10th September – 21st September

�� Abu Dhabi International Hunting and Equestrian Exhibition (ADIHEX) - 9th – 12th September

�� Abu Dhabi Summer Season 11th June – 5th September

�� Louvre Abu Dhabi Stories 21st June – 30th August at Manarat Al Saadiyat

OIL & GAS�� The Shah gas project, which is being developed

by Al Hosn company to tap sour gas in the Western region of Abu Dhabi has reached its full capacity. Al Hosn is a 60-40 joint venture between Abu Dhabi National Oil Company (Adnoc) and Occidental Petroleum (Oxy)

from the US with total investment estimated to be around $10 billion (Dh36.7 billion). The Shah gas project located about 210 kilometers south-west of Abu Dhabi is expected to contribute significantly to the energy needs of the UAE for over 30 years

REAL ESTATE AND CONSTRUCTION - CREATING JOBS�� Reem Mall, ($1 billion project) is on target to complete by mid-

2018 after Abu Dhabi’s Urban Planning Council (UPC) granted approval for its concept plan. The mall is being developed by Kuwait’s National Real Estate Company alongside the United Projects for Aviation Services Company (Upac). Upac, through its subsidiary Al Arfaj Real Estate, is investing up to $224 million in the project which will compose 2 million sq.ft. of space including 450 stores, and 85 food and beverage outlets

�� Bloom Properties, the Abu Dhabi-based developer, owned by the Abu Dhabi conglomerate National Holding, launched Soho Square,

comprising 10-storeys with 302 homes ranging from studios to three-bedroom apartments, town houses and penthouses as well as shops and offices next to New York University’s Saadiyat campus

�� Gulf Related is about to begin construction on Al Maryah Central, a 2.3 million square foot super-regional shopping center. Australian contractor Brookfield Multiplex was awarded a $425 million contract to build the Al Maryah Central mall in Abu Dhabi

FREEZONES SIGNING UP NEW TENANTS; FORMING KEY ALLIANCES

�� Abu Dhabi Ports has signed a standard Musataha agreement (SMA) with Al Gharbia Pipe Company to open a new pipe manufacturing facility at Khalifa Industrial Zone Abu Dhabi (Kizad). The agreement will see Al Gharbia Pipe Company invest a projected total of AED 1.1 billion, with their new facility requiring a plot size of 200,000 square metres. Al Gharbia Pipe Company, a joint venture between Senaat, one of the largest industrial holding companies in the UAE, and two of Japan’s leading steel firms, JFE Steel Corporation and Marubeni-Itochu Steel Inc. (MISI), expects the facility to be completed by March 2018. The plant will employ over 370 staff and is expected to produce 240,000 tons of steel pipe a year

�� Abu Dhabi Ports signed a standard Musataha agreement (SMA) with Al Mazroui International Cargo Company (MICCO) to establish a new Logistics Business Centre at Khalifa Industrial Zone Abu Dhabi (Kizad). MICCO’s new Centre will be built in three phases and will cater to MICCO’s temperature controlled storage facilities, bulk storage through open yards, distribution services, and a service centre for their trucking fleet. The first phase will see MICCO, a leading freight contracting company in the UAE and one of the oldest logistics service providers in Abu Dhabi, invest an initial AED 35 million. Their new facility, requiring a plot size of 30,000 square metres, is expected to be ready by Q4 2016 and fully operational by January 2017

4 5

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ3 2015 | DEMAND DRIVERS REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q3 2015 | DEMAND DRIVERS

ABU DHABI REAL GDP FORECAST 2014-2018

Source: DED

0%

1%

2%

3%

4%

5%

6%

2013 Avg. 2014-2018

5.2% 5.5%

MACRO TRENDS

REAL GDP GROWTH RATE 2014-2018

Source: DED

0% 3% 6% 9% 12% 15%

Wholesale and retail trade; repairof motor vehicles and motorcycles

Accommodation and foodservice activities

Manufacturing

Transportation and storageand communications

Financial and insurance activities

6.8%

10.0%

10.0%

11.1%

15.0%

Dubai realty index Abu Dhabi realty index

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Ju

l-0

7

Ju

l-0

8

Ju

l-0

9

Ju

l-10

Ju

l-11

Ju

l-12

Ju

l-13

Ju

l-14

Jan

-15

Sep

t-15

0

5,000

10,000

15,000

20,000

Abu Dhabi MurbanCrude Oil

Gold Abu Dhabi Stock Market Index

Dubai Stock Index

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Sep

t-15

0

50

100

150

200

250

300

350

New Business Licences Business Licence Renewals

10,000

5,000

15,000

20,000

Q

1 20

10

Q2 2

010

Q

3 2

010

Q

4 2

010

Q1

20

11

Q2 2

011

Q

3 2

011

Q

4 2

011

Q1

20

12

Q2 2

012

Q

3 2

012

Q

4 2

012

Q1

20

13

Q2 2

013

Q

3 2

013

Q

4 2

013

Q1

20

14

Q2 2

014

Q

3 2

014

Q

4 2

014

Q1

20

15Q

2 2

015

Shorooq Abdulla Al ZaabiHead, Development Indicators

& Future Studies Division

Abu Dhabi Department of Economic Development

CPI Rental Contribution to CPI

Jan

20

12

Ju

l 20

12

Jan

20

13

Ju

l 20

13

Jan

20

14

Ju

l 20

14

Jan

20

15

Ju

l 20

15A

ug

20

15

80

100

120

Source: DED

Source: DEDSource: DED

Source: SCAD and MPM Properties Research

Source: Bloomberg and MPM Properties Research

CPI vs RENTAL CONTRIBUTION TO CPI

REALTY STOCK INDEX ABU DHABI vs DUBAI

REAL GDP GROWTH RATE 2014-2018

ABU DHABI CITY - BUSINESS LICENCE NUMBERS

ABU DHABI REAL GDP FORECAST 2014-2018

STOCK MARKET vs OIL vs GOLD

50

60

70

80

Q2 2

015

Q1

20

15Q

4 2

014

Q3

20

14Q

2 2

014

Q1

20

14Q

4 2

013

Q3

20

13Q

2 2

013

Q1

20

13Q

4 2

012

Q3

20

12Q

2 2

012

Q1

20

12Q

4 2

011

Q3

20

11Q

2 2

011

Q1

20

11Q

4 2

010

Q3

20

10Q

2 2

010

Q1

20

10

100

150

200

Q1

20

10Q

2 2

010

Q3

20

10Q

4 2

010

Q1

20

11Q

2 2

011

Q3

20

11Q

4 2

011

Q1

20

12Q

2 2

012

Q3

20

12Q

4 2

012

Q1

20

13Q

2 2

013

Q3

20

13Q

4 2

013

Q1

20

14Q

2 2

014

Q3

20

14Q

4 2

014

Q1

20

15Q

2 2

015

CONSUMER CONFIDENCE INDEX

Source: DED Source: DED

BUSINESS CLIMATE INDEX

Q1

20

10

Q2

Q3

Q4

Q1

20

11Q

2Q

3Q

4Q

1 20

12 Q2

Q3

Q4

Q1

20

13 Q2

Q3

Q4

Q1

20

14 Q2

Q3

Q4

Q1

20

15 Q2

80

100

120

Decreases in both oil prices and the general index of Abu Dhabi’s stockmarket, affected the value of the Business Cycle index during the 4th quarter of 2014, signalling some uncertainty amongst those participants who were surveyed on the performance of the economy in 2015.

BUSINESS CYCLE INDEX

6 7

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ3 2015 | MACRO TRENDS REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q3 2015 | MACRO TRENDS

MARKET OVERVIEW Q3 2015

SUPPLY New supply

The most significant new supply that entered the rental market this quarter was the release of 900 apartments in Gate Towers, which had remained vacant since the project was handed over. Also on Reem Island, Sea View Tower which is situated on Shams Abu Dhabi was handed over in September, comprising 280 apartments which have all been leased to Etihad. A number of

small infill developments have completed in the last three months, including Plot C9 in Sector E-25 and Plot C149 in Sector E-19/2 on the main Abu Dhabi Island in addition to Plot C49 in Sector ME-9 in Mohammed Bin Zayed City, which together have added just over 100 apartments.

3,000

6,000

9,000

12,000

15,000

Investment AreaOn-Island Off-Island

02010 2011 2012 2013 2014 2015

Q1-Q32015 Q4 2016 2017

5,135

2,925

2,013

2,221

3,732

6752,863

3,212

5,945

2,411

3,970

4,691

2,371

1,613

4,604

1,015

1,953

2,215

396

140

379

3,755

391

3,077

5,371

632

1,845

3,769

Num

ber

of r

esid

enti

al u

nits

Pre2010*

2010 2011 2012 2013 2014 2015Q1-Q3

2015Q4

20172016

Total Supply

5.68%

187,473

3.54%

194,101

6.19%

206,121

5.37%

217,193

3.95%

225,781

2.30%

230,964

0.40%

231,879

3.11%

239,102

2.61%

245,348

0

50,000

100,000

150,000

200,000

250,0004.05%

177,400

*per UPC

Num

ber

of R

esid

enti

al U

nits

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q3 2015 | RESIDENTIAL SECTOR

THE ADIB RENTAL INDEX �� In the last 3 months MPM Properties have

renewed close to 2,700 tenancy contracts in Abu Dhabi on behalf of landlords, and granted over 252 new leases

�� ADIB Rental Index continues to show, that across its portfolio, the common rental change trend is 0 to +5% increase during the last 3 months. We expect the rents to continue growing as the market is witnessing limited residential supply entering in the prime areas of Abu Dhabi

�� There are exceptions where rents have increased by over 20% and in some cases much higher, however such cases are very limited (representing in overall terms less than 5%-7% of the portfolio) and relate predominantly to the bottom end of the rental market typically with rents below AED40,000 per annum. These exceptional increases have impacted the overall Q-on-Q average change for each zone

ADIB RENTAL INDEX NOTES �� The ADIB Rental Index relates to the

performance of the ADIB portfolio only and the data is derived exclusively from transactions completed by MPM Properties.

�� The ADIB Portfolio in Abu Dhabi comprises over 12,000 units (70% apartments, 30% villas) with a spread of quality and locations both on the Abu Dhabi Island and the growing Off-Island areas.

�� The ADIB Rental Index has been compiled with a view to enhancing transparency in the Abu Dhabi real estate market and to provide a credible market indicator for rental trend movements.

�� Rental Index Zones are identified on the Map located at the end of this report.

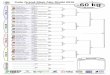

ZONE < 0% 0% to 4.99% 5% 5% to +9.99% 10% to +19.99% 10% to +19.99%

A 0% 71% 12% 9% 6% 2%

B 0% 71% 12% 9% 8% 1%

C 0% 44% 15% 25% 12% 4%

D 0% 54% 12% 18% 9% 7%

E 0% 75% 6% 3% 9% 6%

F 0% 54% 10% 15% 18% 3%

G 0% 57% 23% 11% 3% 6%

H 0% 63% 9% 13% 13% 3%

I 0% 54% 20% 26% 0% 0%

J 0% 60% 13% 20% 7% 0%

K 1% 58% 13% 22% 1% 5%

RESIDENTIAL SECTOR

Source: MPM Properties Research

Source: MPM Properties Research

ABU DHABI NEW HOUSING SUPPLY

ADIB INDEX

CUMULATIVE RESIDENTIAL SUPPLY

(see map at end of report)

8 9

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ3 2015 | RESIDENTIAL SECTOR

APARTMENT SALE PRICES Property values in the residential market have in overall terms remained stable in Q3, reflecting low transaction volumes in the secondary market. The only exception has been Al Reef Downtown where values have risen by up to 5% for some unit types, highlighting that investor demand is weighed towards the affordable end of the market driven by

attractive rental yields. The low transaction volumes are, in part, due to a lack of availability of good quality stock, as owners remain unmotivated to sell in the current market, with many enjoying healthy rental yields.

RESIDENTIAL SECTOR

0

500

1000

1500

2000

2500

Al R

eef

Do

wn

tow

n

Al G

had

eer

Cit

y o

fL

igh

ts

Mari

na

Sq

uare

Sh

am

s

Al Z

ein

a

Al M

un

eera

Gate

Dis

tric

t

Al B

an

dar

SB

R

St.

Reg

is

AE

D/s

q.ft.

0.0% 0.0% 0.0% -1.7% -1.7% 0.0% 0.0% 0.0% -3.4% -0.5% 5.3%Q-on-Q

-8.7% 11.2% -7.3% -6.6% -5.0% -2.9% -1.8% -8.6% -8.0% -5.0% 2.6%Y-on-Y

2,2

50

1,8

50

1,75

0

1,4

50

1,4

25

1,4

25

1,375

1,3

25

1,15

0

1,0

05

1,0

00

Source: MPM Properties Research

AVERAGE APARTMENT SALES PRICE AED/sq.ft. Q3 2015

RESIDENTIAL DEMANDMPM has witnessed a decline in sales enquiries during the last quarter and a corresponding fall in sales transactions closing in the secondary market. This could be attributed in part to the summer holiday period, which traditionally sees a decline in market activity, although sustained price stagnation and falling prices in Dubai is also having an impact on investor sentiment (both buyers and sellers) reducing transaction volumes. Moreover the increase in off-plan investment opportunities offering attractive

payment plan terms is also diverting some liquidity into this segment of the market.

Analysis of MPM sales leads shows demand is heavily focused towards properties priced at less than AED 2 million, comprising almost 60% of all our enquiries (39% of which are looking for properties priced less than AED 1.5 million). The most popular developments comprise Al Reef, Raha Beach and Reem Island.

An indicator that demand has weakened is the compression in interest rates which has been witnessed, with some banks reducing rates by 75 basis points as they chase market share in a bid to meet year end targets. It is too early to analyse the impact on the market at this stage.

In terms of the off-plan market, demand is driven predominantly by the reputation of the developer and the payment plan in the first instance and then by price, product quality and location.

Following a sustained period of inactivity in terms of new project launches during 2009-2013, over the last 18 months Abu Dhabi has seen 16 new developments launched to the market, comprising over 6000 units.

The first new projects launched in 2014 by Aldar and TDIC demonstrated there was very strong pent-

up demand for new prime located product from government backed developers and consequently projects sold out quickly. Whilst more recent off-plan developments released by various developers have on the whole witnessed good demand the volume of sales closed indicates a decline in demand in comparison to last year.

The principal reason for this is the change in market sentiment over the last 12 months which has seen a decline in investor confidence impacted by prices stagnating in Abu Dhabi and declining in Dubai combined with the fall in the oil price.

There is virtually no demand for developments being sold off-plan by less well known independent developers who may have to realign strategy and sell on post completion in order to achieve optimum value.

<1m

1m - <1.5m

1.5m - <2m

2m - <3m

3m - <4m

4m - <5m

5m+

12%

27%

18%

11%

15%

6%

11%

10 11

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ3 2015 | RESIDENTIAL SECTOR

APARTMENT RENTS Following a sustained period of growth over the last 18 months it appears that rents may be approaching their ceiling level at the top end of the market demonstrated by modest growth of only 1% in the last 3 months despite a lack of vacancy

and new supply in the high-end/luxury sectors. It should be noted that developments in this segment have experienced year on year growth of between 7 to 10% hence many tenants are still facing sizeable increases at lease renewal.

RENTAL DEMAND MPM has witnessed significant demand from both individuals and corporate tenants for apartments in Mussafah where demand currently outstrips supply thus providing land owners in this location with development opportunities providing potentially healthy returns.

MPM receives on average over 6,000 leasing enquiries every quarter from prospective tenants in Abu Dhabi. An analysis of these enquiries shows that demand is heavily focused at the affordable end of the market with 56% of all enquiries from tenants with a budget of less than AED 100,000 per annum.

125

175

225

160

57.

5

105

45

97.

5

85

75

77.

5

65

105

55

195

70

270

135

175

26

0

115

160 2

05

115

155

20

0

105

15018

0

97.

5 132.5

190

95

132.5

180

85 10

5 130

115

170

23

5

70 10

0 130

1 BRStudio 2 BR 3 BR

0

50

100

150

200

250

300

No

n-I

nvest

men

tZ

on

e G

rad

e B

No

n Invest

men

tP

rim

e Z

on

e

Al R

eef

Do

wn

tow

n

Sh

am

s

Mari

na

Sq

uare

Gate

Dis

tric

t

Al M

un

eera

Al Z

ein

a

Al B

an

dar

Al G

had

eer

St.

Reg

is

SB

R

-0.7% 0.0% 0.4% 0.0% 1.1% -0.3% -1.2% -4.4% 2.7% -4.6% -1.4%Q-on-Q

6%

0.0%

7% 3% 0% 8% 6% 10% 3% 6% 15% 7% 4%Y-on-Y

Source: MPM Properties Research

AVERAGE APARTMENT ANNUAL RENT Q3 2015

<50k

50k - <100k

100 - <150k

150k - <200

200k - <250k

250k+

4%

52%

22%

15%

4%3%

NEW LAW REGULATING THE ABU DHABI REAL ESTATE MARKET In June 2015 a new law was announced by the General Secretariat of the Executive Council which comes into force in January 2016.

In our view, the new law is a positive step towards attracting increased real estate investment in Abu Dhabi as it tackles many of the concerns raised by investors in the past. Some of the key provisions in the new law are outlined below:-

Regulating Real Estate Developers

& ProfessionalsReal estate developers and brokers, owners association (OA) managers, appraisers and surveyors may not engage in any activity before obtaining a licence from the Department of Municipal Affairs (DMA) and are not entitled to claim remuneration and fees if they are not licensed. Failure to comply with this requirement may lead to imprisonment and a fine between Dh50,000 and Dh200,000, or up to Dh2 million in the case of real estate developers.

Mortgage Enforcement

The law provides for more effective enforcement in the event a debtor defaults on mortgage payments. A bank can now enforce the mortgage immediately through the court after giving notice to the debtor, without having to obtain a court judgment that the debtor owes the debt.

Off-Plan Mortgage Financing

The law allows units sold off-plan to be mortgaged provided that the loan amount is paid into the relevant escrow account and the loan is allocated for payment of the purchase price. These new provisions should encourage banks to become

more actively engaged in this segment of the market

Protecting Investors

The law prohibits real estate companies from selling off-plan units unless the developer and the project have been registered with the DMA and the company has opened an escrow account for the project and obtained written permission from DMA to advertise and market it.

The law also protects investors by requiring developers to register units sold off-plan in the interim real estate register. In addition, it sets out how a breach of this requirement by developers is to be dealt with.

The law sets out clear guidelines for the DMA to follow in dealing with developers when there are delays in meeting project milestones, to ensure that investors’ rights are protected and there is no delay in legal proceedings.

Registration Fees

The law prohibits developers from collecting registration fees (usually 2% of the property price) from investors and only allows developers to charge administrative fees, which must first be approved by the DMA.

Formation of Owners Associations

The law includes provisions for setting up OAs that will be independent legal entities that hold title to the common areas and are responsible for its management in accordance with international standards.

RESIDENTIAL SECTOR

12 13

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q3 2015 | RESIDENTIAL MARKET PERFORMANCE REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q3 2015 | RESIDENTIAL MARKET PERFORMANCE

VILLA PERFORMANCE: SALES AND RENTS �� Al Zeina townhouses, Golf Gardens and Al

Reef villas continue to see healthy demand from investors and end users alike, leading to a positive increase in prices Q-on-Q. Properties under AED5 million witnessed higher transaction volume vs. properties over AED5 million

�� Aldar’s launch of West Yas was well received by the market and highlighted demand for mid-priced properties in Investment

zones that cater to investors and end users. Investors continue to prefer villas within gated communities as they are yielding healthy rental return and high occupancy

�� Saadiyat Beach townhouses, Golf Gardens, Bloom Gardens and villas within gated communities on Abu Dhabi Island continue to be popular tenant choices for families and senior management staff of Government entities and banks

RESIDENTIAL SECTOR

0

100

200

300

400

80 12

0150

125 16

0 190

140

105 12

0

275

23

0

370

33

0

28

0 320

220

220

25

5

30

0 35

0

35

0

26

0 30

0

190

30

5220

24

0

3 BR2 BR 4 BR 5 BR

Al M

ush

rif

Gard

en

s

Al B

ate

en

Gard

en

s

Blo

om

Gard

en

s

Al R

ah

aG

ard

en

s

Go

lfG

ard

en

s

SB

V(T

ow

nh

om

es)

Hyd

raV

illag

e

Al Z

ein

a

Al R

eef

Al G

had

eer

AED

/sq.

ft.

0

500

1000

1500

2,000

Blo

om

Gard

en

s

Al G

had

eer

Al R

ah

aG

ard

en

s

Go

lfG

ard

en

s

Hyd

raV

illag

e

Al Z

ein

a

Al R

eef

SB

V1,75

0

1,4

25

815975

1,0

50

1,0

05

1,15

0

620

0.0% 1.9%5.4% 0.0%0.0%4.5% 0.0%-1.7%Q-on-Q

0.0% -3.55%8.33% 3.33%-4.55%0.0% -2.43%-3.06%Y-on-Y

Source: MPM Properties Research

AVERAGE VILA SALES PRICE AED/sq.ft. Q3 2015

VILA AVERAGE ANNUAL RENTS Q3 2015

Source: MPM Properties Research

Main island KCA MBZ

Low AverageHigh

0

5

10

15

20

25

16.17

5.4

6

6.7

510.8

10.3

7

23

.0

6.5

6 14.7

8

14.0

VILLA VALUES – NON-INVESTMENT AREAS�� The analysis below is based on data gathered

from the transactions financed by ADIB, villas managed by MPM and data from agency (sales and leasing) team, for villas in non-investment zones and highlights the current prevailing prices and yields

�� The demand for villas and villa compounds was slow during Q3 2015, as multiple projects like Al Merief, Nareel plots and West Yas attracted

market demand. The market is currently witnessing mismatch in yield expectations between seller and buyer, which in turn is leading to a slow-down in transaction volumes

�� Demand for good quality villa compounds in Khalifa City “A” and Mushrif areas continues to be healthy at 8% gross yield, despite some sellers currently attempting to sell villas at 7% gross yields

0

5

10

15

20

25

Main island KCA MBZ Shakbout City

Low AverageHigh

20

.47

6.3 13

.38 2

2.0

7.4

5 14.7

2 21.0

7.3 14

.1

12.5

9.0

10.7

5

Main island KCA MBZ

Low AverageHigh

9.13

4.2 6.6

6

23

.0

4.7

13.8

6.8

6.5

6.6

5

0

5

10

15

20

25

6.0%

7.0%

8.0%

Main island KCA MBZ Shakbout City

AED

(M

illio

n)A

ED (

Mill

ion)

AED

(M

illio

n)

VILLA COMPOUND PRICES (Q3 2015)

5/6 BEDROOM VILLA PRICES (Q3 2015)

VILLA COMPOUND GROSS YIELDS (Q3 2015)

7/8 BEDROOM VILLA PRICES (Q3 2015)

Source: MPM Properties Research

Note: Data relates to compounds of 4 to 6 villas

14 15

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ3 2015 | RESIDENTIAL SECTOR REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q3 2015 | RESIDENTIAL MARKET PERFORMANCE

PROJECT IN FOCUS – MAYAN RESIDENCE

Yas Island benefits from a number of major development anchors both existing and planned that will drive demand and value creating both an attractive lifestyle destination and investment proposition.

YAS ISLAND

Mayan enjoys a prominent position on the world-renowned Yas Island, known for its destination-led lifestyle experience and the Formula One circuit which hosts the Abu Dhabi Grand Prix on an annual basis.

Yas Island, whose population is expected to grow significantly as projects both under development and planned come on stream, is already home to major retail attractions in the form of Yas Mall, IKEA, Geant and ACE Hardware.

Two theme parks are already in operation on Yas Island – Yas Water World and Ferrari World, with two more theme parks marked out for development on the island’s master plan.

Yas Island is home to numerous food and beverage and entertainment venues ranging from the Yas Island Yacht Club, to the Beach Club as well as concert venues.

MAYAN - OVERVIEW

Located in the Yas Beach area of Yas Island and adjacent to the destination’s Hotel District, Mayan is a low-rise master planned community. With no restrictions on purchaser nationality due to its Investment Zone status, Mayan has been designed to appeal to a broad base of investors and end users.

Mayan offers a range of 700 apartment choices from studios to 1,2,3 and 4 bed options as well as beach houses.

Mayan benefits from stunning golf course and sea views, in addition to a variety of high-end amenities, from luxury infinity pools overlooking the sea, gyms, steam rooms, saunas, and access to Yas Island’s members-only beach club. Residents of Mayan will benefit from private parking, an exclusive concierge service, CCTV monitored security and 24-hour maintenance.

ENTERTAINMENT

Ferrari World

Yas Water World

Marina Circuit

Warner BrosLIFESTYLE

Golf

Marina

Beach

Outdoor Sports

SHOPPING

Yas Mall

Ikea

AceFAMILY

Schools (u/c)

Dining

Parks

16 17

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ3 2015 | KEY INDUSTRY PLAYER - MARKET VIEW REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q3 2015 | KEY INDUSTRY PLAYER - MARKET VIEW

SUPPLY Q3 2015

�� The only major addition to the market in the last quarter is the office space currently being handed over at Addax Tower, where we estimate approximately 20,000 sqm (representing approximately 25% of the tower) is now available in the market for either rent or for sale

�� A number of small developments, predominantly situated off-island, have been completed this quarter which together have added a further 5,000 sqm of ancillary Grade C office space

FUTURE SUPPLY

�� There are a number of office developments which are close to entering the market, including the ADIB HQ Tower 2 situated on Airport Road, Maryah Tower on Maryah Island, developed by Al Hilal Bank and the Al Qudra HQ at Khalifa Park, which together will add approximately 60,000 sqm of net leasable space

�� Post 2015, with the exception of handover delays of existing projects , there are limited new office developments in the pipeline. The developments that are underway are predominantly owner-occupier developments like ADNOC HQ, ADIB HQ Tower 1, etc. The demand for “business park” with ample parking continues to be strong from the SME sector and this is an opportunity that needs to be tapped by developers and investors

20102009 2011 2012 2013 2014 2015Q1-Q3

2015Q4

2016 2017

Running Total New Supply Completed Scheduled New Supply

155

541

377249 99 72

67373 41

0

1,000

2,000

3,000

4,000

1,800 1,800 1,9552,495

2,872 3,121 3,220 3,292 3,359 3,733

MARKET OVERVIEW Q3 2015

On-Island Off-Island Investment Area

0 300 600 900 1200 1500

436164892

0

100

200

300

400

500

600

2010 2011 2012 2013 2014 2015Q1-Q3

2015Q4

2016 2017

Speculative Owner Occupation / Pre-Let

146

9474

67

272

105

203

45

81

1860

12

25

42

153

220

41

On-Island Off-Island Investment Area

0

100

200

300

400

500

600

125 202

64

275

235

62

80

24181

8

956

18

8

12

3

5329

2010 2011 2012 2013 2014 2015Q1-Q3

2015 Q4

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ3 2015 | OFFICE SECTOR REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q3 2015 | OFFICE SECTOR

NLA

(in

00

0’s

Sq.

m.)

NLA

(in

00

0’s

Sq.

m.)

NLA

(in

00

0’s

Sq.

m.)

NLA (in 000’s Sq.m.)

ABU DHABI OFFICE SUPPLY (2009-2017)

Source: MPM Properties Research

ABU DHABI OFFICE SUPPLY COMPOSITION

ABU DHABI NEW OFFICE SUPPLY - LOCATION

NEW SUPPLY BREAKDOWN - LOCATION

Source: MPM Properties Research

Source: MPM Properties Research

Source: MPM Properties Research

18 19

Q2 2015

Grade BGrade A S&CGrade A Fitted

1.3%

3.2%

6.1%

11.8%

10.3%

13.0%

Q-on-Q changeQ3 2015 % Y-on-Y change%

0

500

1,000

1,500

2,000

Rent

/ S

q.m

. (A

ED)

Sales Price / Sq.ft.

*as per UPC

Prestige TowerMBZ

Tamouh TowerAddaxThe WaveSky Tower0

300

600

900

1,200

1,500

1,4751,250

1,150 1,150 1,100

0.0% -4.2%-2.1% 0.0%0.0%Q-on-Q

1.0% -2.2%-15.0% 5.3%–Y-on-Y

Sale

s Pr

ice

/ Sq

.ft.

(A

ED)

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q3 2015 | OFFICE SECTOR

OFFICE RENTS �� The commercial office market remains subdued

and has seen low leasing activity during the last quarter. Although demand has declined, particularly from the government sector this has been balanced by a lack of new supply entering the market, which has resulted in marginal rental increases of between 1-3%. The lack of Grade A space available for immediate occupation is seeing rents appreciate in prime buildings which enjoy low vacancy rates

�� The lack of availability and leasing activity in the Grade A segment is having a positive impact on some Grade B office buildings where we have seen leasing transactions closing at headline rents of AED 1,325 per sqm representing growth of 8% in comparison with the previous quarter. We don’t expect to see this growth sustained given the new supply due to be delivered to the market over the next six months

OFFICE SALES �� Floors and units within Addax Tower on Reem

Island continue to be handed over to investors and hence progressively more space is becoming available in the secondary market with prices generally ranging from AED 1,050 to AED 1,200 per sqft, with some owners offering extended

payments plans. The marketability of this space is being negatively impacted by the parking ratio although we understand that Tamouh is looking to address this with the construction of a multi-storey parking structure next to the tower

OFFICE HEADLINE RENTS, Q-ON-Q% AND Y-ON-Y% CHANGE

Source: MPM Properties Research

AVERAGE OFFICE SALES PRICE

Source: MPM Properties Research

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q3 2015 | OFFICE SECTOR

OFFICE PROJECT IN FOCUS: ADIB HQ TOWER 2�� 21,869 sqm of net leasable area arranged over

ground and 12 upper floors

�� Shell & Core finish ready for tenant fit out works

�� 4 levels of basement parking providing 400 car parking spaces (1:50 sqm)

�� Additional parking available (subject to negotiation)

�� Efficient floor plates extending to 1638 sqm

Grade “A” Specification

�� Common atrium with Tower 1 (ADIB HQ) with coffee shop and retail units

�� 2700mm finished floor to ceiling height

�� Capacity for 200mm raised access floors

�� 8 high speed lifts dedicated to exclusively serve Tower 2 from B4 through to Level 12

�� Average wait time estimated at 10-15 seconds

�� LEED Gold for Building Design and Construction

�� All common areas are covered by CCTV, access control system, fire alarm and intrusion detection system

Location

The development is situated on Airport Road opposite the Hilton Hotel providing excellent connectivity to Downtown and the airport

20

MARKET OVERVIEW Q3 2015

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2009* 2010 2011 2012 2013 2014 2015Q1-Q3

2015Q4

2016 2017/19

Scheduled New Supply Running Total New Supply Completed

28

1,4281,4001,400

259113

185

342 45152

1

872

1,687 1,800 1,985 2,327 2,372 2,3732,524

*as per UPC

NLA

(in

00

0’s

) pe

r Sq

.m.

TAKE-UP & RENTS

The rents quoted above are base rents excluding any turnover provisions and service charges.

�� Retail rents across Abu Dhabi malls have remained stable during Q3 2015, although some mall tenants have started requesting for rental reductions / renewals at previous rents, driven by drop in revenues witnessed by small number of retail stores during Q3 2015. On the other hand high street retailers across Abu Dhabi’s major locations have accepted 5% rental increase on renewals as rents on high street catch-up with rents inside established malls

�� Occupancy across malls remains high within Abu Dhabi Island, with malls on Abu Dhabi mainland witnessing healthy take-up for vacant space albeit at attractive rents or with attractive tenant incentives

�� The majority of existing contracts are being renewed at turnover rent. In turn this will ensure greater involvement from mall owners to drive foot-falls and revenue to stores within their malls

SPACE TYPE AVERAGE RENT (AED) PA

Specialty Store 1,800-3,900 per sq.m.

Anchor Store (more than 1,000 sq.m.) 400-1,250 per sq.m.

F & B 3,500-5,750 per sq.m.

ATM’s 90,000-180,000

Kiosks 85,000-155,000

High street retail (Prime areas) 2,500 – 3,850 per sq.m.

High street retail (Non-prime areas) 1,550-2,850 per sq.m.

District Neighborhood Regional Super Regional

On-Island Off-Island Investment Area

763,72354%

1,365,000 97%

333,000 24%

35,000 3%

303,27722%

517,89453%147,000

15%

1,281,617 54%408,453

17%

232,256 10%

450,277 19%

920,000 90%

236,241 24%

75,4538%

436,75345%

232,256 24%

300,10931%

RETAIL SUPPLY PRE-2010

PRE-2010

NEW SUPPLY DELIVERED 2010-2015 Q3

NEW SUPPLY ADDED POST 2010

The above charts show supply of malls only and exclude all street retail. Figures are NLA (sq.m.)

RETAIL SUPPLY LOCATION AS AT Q3 2015

1,601,241 67%

471,75320%

300,10913%

RETAIL DEVELOPMENT PIPELINE

RETAIL SUPPLY AS AT Q3 2015

96,400 9%

7,300 1%

621,20061%

102,50010%

RETAIL DEVELOPMENT PIPELINE

299,00029%

ABU DHABI RETAIL SUPPLY (2009 - 2017/18)

Source: MPM Properties Research

RETAIL SPACE CLASSIFICATION

RETAIL SPACE LOCATION

SUPPLY Retail Sector Set to Grow Rapidly Over the Next Three to Four Years

Q3 2015

�� The retail sector has witnessed no major supply entering the market in Q3 with majority of the supply being driven by “street retail” on Abu Dhabi Island and mainland. This in turn is allowing the retail malls to focus on increasing their foot-falls by attracting tourists and residents

�� Apple Store has recently opened at Yas Mall and this is a major addition to the retail brands within Abu Dhabi and is expected to yield higher foot falls to the mall

FUTURE SUPPLY

�� The retail sector within Abu Dhabi is expected to see multiple community retails and convenience stores being built all across the city. This in turn is expected to increase the competition amongst supermarkets, while enhancing the lifestyle of residents with more retail options available at their door-step

�� Al Mariyah Central is on course for a Q1 2018 opening has Gulf Capital has secured a AED2.3billion funding and 1/3 rd of the mall has been pre-let with key anchors currently announced being Macy’s and Bloomingdales. The funding covers phase one of the project, which will involve 2.3 million of a total of 3.1 million square feet being developed. This will include a mall with more than 400 stores, 145 restaurants and cafes and a 20-screen cinema

22 23

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ3 2015 | RETAIL SECTOR REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q3 2015 | RETAIL SECTOR

�� Growth in guest arrivals into Abu Dhabi (up by 22% in Q2 2015 vs. Q2 2014), driven mainly by growth in tourists from China (68%), US (30%), Philipines (29%) and KSA (27%)

�� Five star hotels continue to witness the highest spend / guest at AED2,601 and was second only to Deluxe hotel apartments

�� 4 and 3 star hotels have experienced occupancy levels above 80% so far this year with 5 star properties witnessing 75% occupancy YTD this year

ARR RevPar Occupancy

0

100

200

300

400

500

600

700

800 90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Jan

-13

Feb

Mar

Ap

rM

ay

Ju

nJu

lA

ug

Sep

Oct

No

vD

ec

Jan

-14

Feb

Mar

Ap

rM

ay

Ju

nJu

lA

ug

Sep

Oct

No

vD

ec

Jan

-15

Feb

Mar

Ap

rM

ay

Ju

nJu

lA

ug

Sep

Guests 20% increase

Guest Nights 15% increase

Occupancy 6% increase

Revenues (Mil.) 14% increase

Avg Length of Stay 4% decrease

MARKET OVERVIEW Q3 2015

�� Hotel apartments continue to outperform hotels with higher occupancy and average length of stay

�� Average guest spend at Deluxe apartments was the highest across hotel establishments, greater than five star hotels as well

�� Q3 witnessed an increase in all key parameters for hotel apartments, highlighting the strength of this segment within the hospitality sector

ARR RevPar Occupancy

100%90%80%70%60%50%40%30%20%10%0%

Jan

-13

Feb

Mar

Ap

rM

ay

Ju

nJu

lA

ug

Sep

Oct

No

vD

ec

Jan

-14

Feb

Mar

Ap

rM

ay

Ju

nJu

lA

ug

Sep

Oct

No

vD

ec

Jan

-15

Feb

Mar

Ap

rM

ay

Ju

nJu

lA

ug

Sep

0

100

200

300

400

500

Guests 5% increase

Guest Nights 13% increase

Occupancy Levels 8% increase

Revenues (Mil.) 9% increase

Average Length of stay 7% increase

HOTELS 5 STAR 4 STAR 3 STAR 2 STAR 1 STAR

Guests 1,172,450 894,135 656,865 45,067 87,648

Guest Nights 3,573,210 2,497,105 1,912,751 124,381 211,341

Avg. Length of Stay 3.05 2.79 2.91 2.76 2.41

ARR 745 407 359 325 274

Occupancy 75% 82% 80% 78% 77%

RevPar 558.75 333.74 287.2 253.5 210.98

Revenues 3,049,900,000 940,380,000 639,100,000 48,020,000 70,700,000

HOTEL APARTMENTS DELUX SUPERIOR STANDARD

Guests 92,435 94,161 65,822

Guest Nights 760,762 607,209 295,815

Avg. Length of Stay 8.23 6.45 4.49

ARR 448 295 302

Occupancy 85% 86% 89%

RevPar 380.8 253.7 268.78

Revenues 244,821,691 126,815,770 64,005,852

HOTEL PERFORMANCE SNAPSHOT

Q3 PERFORMANCE BY RATING

HOTEL MAIN INDICATORS (YTD)

Source: TCA Abu Dhabi and MPM Properties Research

HOTEL APARTMENTS PERFORMANCE SNAPSHOT

Q3 HOTEL APARTMENT PERFORMANCE BY RATING

HOTEL APARTMENTS MAIN INDICATORS (YTD)

Source: TCA Abu Dhabi and MPM Properties Research

24 25

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ3 2015 | HOSPITALITY SECTOR – TRADING PERFORMANCE REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q3 2015 | HOSPITALITY SECTOR – TRADING PERFORMANCE

HOSPITALITY SECTOR – TRADING PERFORMANCE

ARR RevPAR Occupancy

100%

90%

80%

70%

60%

50%

40%

30%

20%0

100

200

300

400

500

600

700

800

Jan

-13

Feb

Mar

Ap

r

May

Ju

n

Ju

l

Au

g

Sep

Oct

No

v

Dec

Jan

-14

Feb

Mar

Ap

r

May

Ju

n

Ju

l

Au

g

Sep

Oct

No

v

Dec

Jan

-15

Feb

Mar

Ap

r

May

Ju

n

Ju

l

Au

g

Sep

SUPPLY

Ave

rage

roo

m r

ate

Num

ber

of r

oom

s

Occ

upan

cy

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Pre 2009

2009 2010 2011 20132012 2014 Q1-Q32015

Q42015

2016 2017+

Scheduled New Supply Running Total New Supply Completed

5,3742,397

2,6462,653

2,3122,805

1,483 5742,386

2,703

8,278 8,27813,652 16,049 18,695 21,348

23,66026,465 27,948 28,522

30,908

Q3 2015 saw Jannah Place on Airport Road entering the market with 62 keys. The property is deluxe hotel apartments offering short and long term stay options.

The hospitality sector is gearing up for the opening of Lourve Abu Dhabi, which is expected to increase the number of tourist arrivals into Abu Dhabi.

Q3 2015 – HOTEL APARTMENT SCHEDULED COMPLETIONS

GUEST ARRIVALS – TOP 5

GUEST ARRIVALS Q3 2015 YTD

S.NO. ESTABLISHMENT NAME EXPECTED CLASS OPENING ROOMS

1 Jannah Place Deluxe Q3 - 2015 62

TOTAL 62

RANK NATIONALITY 2015 YTD 2014 YTD GROWTH RATE %

1 United Arab Emirates 902,533 755,150 20%

2 India 173,649 142,613 22%

3 United Kingdom 142,134 122,893 16%

4 China 125,678 74,636 68%

5 USA 98,975 76,096 30%

United Arab Emirates 39%

Other GCC Countries 8%

Other Arab Countries 10%

Asia (Except Arab) 19%

Australia & Pacific 2%

Africa (Except Arab) 1%

Europe 16%

North & South America 5%

Source: TCA Abu Dhabi and MPM Properties Research

HOTEL ESTABLISHMENT PERFORMANCEHISTORICAL TRADING PERFORMANCE 2010-2015

Source: TCA Abu Dhabi and MPM Properties Research

ABU DHABI HOTEL ROOM SUPPLY (2009 - 2016+)

Source: MPM Properties Research

26 27

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ3 2015 | HOSPITALITY SECTOR – TRADING PERFORMANCE REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q3 2015 | HOSPITALITY SECTOR – TRADING PERFORMANCE

KHALED AL SOLEH BSC MRICS Head of Valuation – Abu Dhabi T: +971 (0)2 610 0085 M: +971 (0)50 722 9718 [email protected]

A collaborative team providing our integrated services

MOHAMED AL ZOUBI Head of Development Advisory BSc Civil Engineering T: +971 (0)2 610 0564 M: +971 (0)50 310 3570 [email protected]

KHALED CHAHAL Director of Agency – Abu Dhabi T: +971 (0)2 412 8402 M: +971 (0)50 110 2929 [email protected]

JASON FIELDEN BSC (HONS) MRICS Valuation Manager - Abu Dhabi T: +971 (0)2 510 0653 M: +971 (0)56 244 7696 [email protected]

PAUL MAISFIELD BSC (HONS) MRICS CEO T: +971 (0)2 610 0545 M: +971 (0)50 660 9437 [email protected]

YOUSEF AL ZAROONI Regional Head – Al Ain T: +971 (0)3 708 8636 M: +971 (0)50 600 1002 [email protected]

ABDULLAH SAID AL KUWEITI Business Development Director T: +971 (0)2 610 1554 M: +971 (0)50 623 5854 [email protected]

SAMUEL MORRIS BSC (HONS) FRICSDirector of Valuation & Regional Head - Dubai T: +971 (0)4 371 9466 M: +971 (0)50 107 1704 [email protected]

WAHIDA KARAMA Head of Property Operations T: +971 (02) 610 0435 M: +971 (0)50 765 7679 [email protected]

FRANK O’DWYER MBA (Hons); BEng.COO T: +971 (0)2 610 0402 M: +971 (0)50 812 1070 [email protected]

DOMINIC BARLOW Head of Retail, Hospitality & Leisure T: +971 (0)2 510 0655 M: +971 (0)56 288 1458 [email protected]

JUBRAN AL HASHMI Head of Property Services T: +971 (0)2 610 0232 M: +971 (0)50 122 0041 [email protected]

ALI ABDULLAH ABDUL RAHMAN Acting Regional Head – Northern Emirates T: 971 (0)6 597 2514 M: +971 (0)50 656 2486 [email protected]

VAIBHAV SHARMA MCOM; MDBA Director of Strategic Advisory and Research T: +971 (0)2 412 8914 M: +971 (0)50 660 9295 [email protected]

RESEARCH STUDY AREA

The geographical extent of the study area includes the Abu Dhabi Island, Investment Areas and the most populated Off-Island districts specifically Khalifa City A, Mohammed Bin Zayed City and Shakbout City.

RESIDENTIAL

New residential developments are classified as delivered and thus entered into the new supply category when they are made available for occupation. This is verified via a combination of site inspections and discussion with the developer and hence our supply numbers do take into consideration the phased release of large projects.

The ADIB Rental Index relates to the performance of the ADIB portfolio only and the data is derived exclusively from transactions completed by MPM Properties.

Other rental and sales trend analysis is based on transactional data derived from the MPM Properties Agency team and data sourced from developers and owners.

OFFICES

New office developments are classified as delivered and thus entered into the new supply category when they are available for tenant fit-outs.

Given the general lack of transparency in the local market rents quoted are headline rents, thus exclude any rent free period or other financial incentives that may have been negotiated between the parties. The rents quoted are also exclusive of service charges.

RETAIL

New retail developments are classified as delivered and thus entered into the new supply category when the first units are open and trading.

Our classification of malls is based on our own assessment having regard to size and the catchment area which the mall typically penetrates.

HOSPITALITY

New hotels are classified as delivered and thus entered into the new supply category when they are opened and trading. All trading performance data is provided by ADTCA.

FUTURE SUPPLY PROJECTIONS

Our future supply projections across all sectors are based on a combination of regular site inspections and discussions with developers.

DEFINITIONS & METHODOLOGY

DISCLAIMER:

The information contained in this report has been obtained

from and is based upon sources that ADIB Real Estate Services

believes to be reliable, however, no warranty or representation,

expressed or implied, is made to the accuracy or completeness

of the information contained herein, and same is submitted

subject to errors, omissions, change of price, rental or other

conditions, withdrawal without notice, and to any special listing

conditions imposed by our principals. ADIB Real Estate Services

will not be held responsible for any third-party contributions.

All opinions and estimates included in this report constitute

ADIB Real Estate Services, as of the date of this report and

are subject to change without notice. Figures contained in

this report are derived from a basket of locations highlighted

in this report and therefore represent a snapshot of the Abu

Dhabi market. Due care and attention has been used in the

preparation of forecast information. However, actual results

may vary from forecasts and any variation may be materially

positive or negative. Forecasts, by their very nature, involve

risk and uncertainty because they relate to future events and

circumstances which are beyond ADIB Real Estate Services’

control. For a full in-depth study of the market, please contact

ADIB Real Estate Services team.

BESPOKE CLIENT RESEARCH ADDING VALUE TO YOUR PROPERTY INTERESTSThe ADIB Real Estate Services team covers all sectors of the real estate market. We provide bespoke market research to our valued clients to meet their specific requirements.

We provide reports, information and presentations derived from primary market data that directly assist our clients to save or make money from real estate and shape strategies to enhance value.

28 29

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ3 2015 | DEFINITIONS & METHODOLOGY REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q3 2015

SUPPLY - PHOTO GALLERY

SAMPLE OF NEW & UPCOMING SUPPLYNEW SUPPLY (Q3 2015)

INVESTMENT AREA - UPCOMING SUPPLY

2 HYDRA AVENUE REEM ISLAND

6 JANNAH PLACE ABU DHABI

3 ALI & SONS C40 RAWDHAT

7 C9, E-25, AL NAHYAN CAMP

4 BAWABAT AL SHARQ APARTMENTS

8 C86, E-11 TCA

9 C149, E-19/2 TCA

NON INVESTMENT AREA - UPCOMING SUPPLY

20 LEAF TOWER REEM ISLAND

24 BLOOM CENTRAL AIRPORT ROAD

36 HILTON AL FORSAN

27 C38 - GSCS TOWER DANET ABU DHABI

28 C40 - UNB TOWER DANET ABU DHABI

30 JOWARAH TOWER SARAYA

29 THE VIEWS 1 & 2 SARAYA

31 MINA TOWER SARAYA

32 SARAYA

25 EMI STATE REALTY HAMDAN STREET

26 FOUNDATION PROPERTIES AIRPORT ROAD

10 FOUR SEASONS AL MARYAH ISLAND

11 HORIZON TOWERS REEM ISLAND

14 SEASIDE TOWER REEM ISLAND

15 THE KITE RESIDENCES REEM ISLAND

16 THE SHAMS TOWER REEM ISLAND

17 YASMINA RESIDENCES REEM ISLAND

18 M TOWER REEM ISLAND

19 SKY GARDENS REEM ISLAND

21 ADTC PHASE 3

33 SARAYA

22 AL JAZEERA TOWER CORNICHE

34 C74, C75 & C76 RAWDHAT

23 AWQAF BUILDING KHALIDIYAH

35 C41 RAWDHAT

1 ADDAX TOWER REEM ISLAND

5 C49, ME-9, MBZ

12 SHEIKH OMAR REEM ISLAND

13 UNB TOWER 1 & 2 REEM ISLAND

30 31

REAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEW Q3 2015 | SUPPLY - PHOTO GALLERYREAL ESTATE SERVICES | ABU DHABI REAL ESTATE MARKET OVERVIEWQ3 2015 | SUPPLY - PHOTO GALLERY

Residential

Offices

Retail

Hotels

Residential

Offices

Retail

Hotels

Q2 2014 NEW SUPPLY UNDER CONSTRUCTION

Jubail Island

Al ReemIsland

Al MaryahIsland

Al Raha Beach

MasdarCity

Saadiyat Island

Yas Island

HydraVillage

Al Reef

B

D

E F

G H

K

I

J

A

C

Salam Street

Khaleej Al Arabi Street

Airport Rd

Airport Rd

E 20

E 20

E 22

E 30

Corn

iche

Rd

Electra St

Zayed The First S

t

E12

Al Saada Stre

et

25th S

t

Salam Street

Salam Street

Sheikh Khalifa Hway

Abu D

habi

- Dub

ai Rd

Abu Dhabi - Dubai Rd

E 10

Shei

kh M

akto

um B

in R

ashi

d Rd

E 11

E 11

E 11

E 10

3

7

96

8

10

1 1811 2

1213

1415

1617

19

20

21

22

2324

26

25

27 28

35 34

2930

3132

33

36

4

5

New Supply

Investment

Non-investment

Q3 NEW & UPCOMING SUPPLY

ADIB RENTAL INDEX ZONE

COMMON TREND (Q3 2015) (ANNUAL %

RENTAL INCREASE)

Q-Q CHANGE OVERALL AVERAGE

Q3 2015 Q2 2015 Q1 2015 Q4 2014 Q3 2014 Q2 2014 Q1 2014

Zone A 0 to 4.99% 3.05% 4.58% 3.71% 8.05% 5.01% 2.37% 4.05%

Zone B 0 to 4.99% 2.60% 5.08% 6.94% 7.75% 10.56% 3.86% 6.33%

Zone C 0 to 4.99% 5.63% 7.46% 9.25% 9.79% 12.34% 10.26% 5.06%

Zone D 0 to 4.99% 6.48% 7.06% 8.51% 10.31% 10.26% 9.07% 6.18%

Zone E 0 to 4.99% 3.76% 4.02% 7.54% 5.09% 10.20% 5.32% 4.49%

Zone F 0 to 4.99% 4.77% 3.17% 4.01% 6.58% 7.63% 3.25% 2.41%

Zone G 0 to 4.99% 4.42% 2.34% 2.20% 2.59% 2.69% 2.42% 2.92%

Zone H 0 to 4.99% 3.68% 5.58% 3.46% 1.46% 3.42% 5.31% 2.44%

Zone I 0 to 4.99% 3.08% 3.41% 1.86% 5.48% 1.14% 1.33% 1.21%

Zone J 0 to 4.99% 3.32% 5.78% 0.96% 4.04% 3.06% 1.55% 1.64%

Zone K 0 to 4.99% 5.30% 5.89% 2.88% 4.31% 4.18% 3.51% 3.65%

RENTAL INDEX | ABU DHABI REAL ESTATE MARKET OVERVIEWQ3 2015

32

RENTAL INDEX | ABU DHABI REAL ESTATE MARKET OVERVIEW Q3 2015

33

OFFICE CONTACT DETAILS MPM Properties Head Office 6th Floor, Al Wahda Tower P.O Box 114686 Abu Dhabi

Tel. 02 412 8914 Email. [email protected] www.mpmproperties.ae

PAUL MAISFIELD BSC (HONS) MRICS CEO T: +971 (0)2 610 0545 M: +971 (0)50 660 9437 [email protected]

VAIBHAV SHARMA MCOM; MDBA Director of Strategic Advisory and Research T: +971 (0)2 412 8914 M: +971 (0)50 660 9295 [email protected]