Embed Size (px)

Citation preview

COMPLETING THE ACCOUNTING CYCLE

1. Adjusting entries are made to ensure that:A. Expenses are recognized in the period in which they are incurred.B. Revenues are recorded in the period in which they are earnedC. Statement of financial position and statement of comprehensive income have

correct balances at the end of accounting periodD. All of the above

2. Each of the following is a major type (or category) of adjusting entries except:A. Prepaid expensesB. Accrued revenueC. Accrued expensesD. Earned revenues

3. The trial balance show Supplies RM1,350 and Supplies expense RM0. If RM600 supplies are on hand at the end of the period, the adjusting entry is:

A. Supplies 600 Supplies Expense 600B. Supplies 750 Supplies Expense 750C. Supplies Expense 750 Supplies 750D. Supplies Expenses 600 Supplies 600

4. On December 15, 2011, a company receives an order from a customer for services to be performed on December 28, 2011. Due to a backlog of orders, the company does not perform the services until January 3, 2012. The customer pays for the services on January 6, 2012. The matching principle requires the revenue to be recorded by the company on:

A. December 15, 2011.B. January 3, 2012.C. December 28, 2011.D. January 6, 2012.

5. Adjustments for prepaid expenses:A. Decrease assets and increase revenuesB. Decrease expenses and increase assetsC. Decrease assets and increase expensesD. Decrease revenues and increase assets

6. The Unearned Revenue account was not adjusted for work performed in the current period. What is the effect of this error?

A. The assets will be understated and expenses will be understated.B. The assets will be overstated and liabilities will be overstated.C. The liabilities will be overstated and revenues will be understated.D. The liabilities will be understated and revenues will be understated.

7. AG Enterprises paid RM105,000 for office furniture. The furniture is depreciated using the straight-line method and has an estimated service life of 7 years. After three years of use, the book value of the furniture will be:

A. RM45,000.B. RM60,000.C. RM90,000.D. RM105,000.

8. Which of the following are in accordance with generally accepted accounting principles?A. Accrual basis accountingB. Cash basis accountingC. Both accrual basis and cash basis accountingD. Neither accrual basis nor cash basis accounting

9. The Accounts Receivable account has a RM20,000 debit balance in the unadjusted trial balance. There is a RM1,000 debit adjustment to Accounts Receivable. The adjusted trial balance will show Accounts Receivable as a:

A. RM19,000 debit balance.B. RM21,000 credit balance.C. RM21,000 debit balance.D. RM19,000 credit balance.

10. Pedro Torreh & Partners purchased machineries by paying cash of RM24,000 and issuing a note payable of RM36,000. Which of the following journal entries would be recorded?

A. Cash is credited for RM24,000; Equipment is credited for RM60,000; and Notes payable is debited for RM36,000.

B. Cash is credited for RM24,000; Equipment is credited for RM36,000; and Notes payable is debited for RM12,000.

C. Cash is debited for RM24,000; Equipment is debited for RM36,000; and Notes payable is credited for RM60,000.

D. Cash is credited for RM24,000; Equipment is debited for RM60,000; and Notes payable is credited for RM36,000.

11. If a resource has been consumed but a bill has not been received at the end of the accounting period, then

A. an expense should be recorded when the bill is received.B. an expense should be recorded when the cash is paid out.C. an adjusting entry should be made recognizing the expense.D. it is optional whether to record the expense before the bill is received.

12. Which of the following accounts is not a commonly adjusted in an adjusting entry?A. cash - adjusted to match the bank statementB. office supplies - adjusted to record supplies used during the periodC. prepaid rent - adjusted to record rent expenseD. equipment - adjusted to record depreciation

13. Annual equipment depreciation is calculated as RM5,000. What is the adjusting journal entry?

A. debit equipment and credit depreciation expense for RM5,000B. debit depreciation expense and credit accumulated depreciation for RM5,000C. debit accumulated depreciation and credit equipment for RM5,000D. debit accumulated depreciation and credit depreciation expense for RM5,000

14. Employees are paid every two weeks. On December 31, employees are owed RM2,500 in salaries since the last payday on December 22. What is the adjusting journal entry?

A. debit cash and credit salaries expenseB. debit salaries expense and credit cashC. debit salaries payable and credit salaries expenseD. debit salaries expense and credit salaries payable

15. Which is correct concerning the adjusted trial balanceA. An adjusted trial balance lists all ledger account balances separated by assets and

liabilities.B. An adjusted trial balance is a method used to prove the accounting to date has

been posted properly.C. An adjusted trial balance is prepared after adjusting entries have been journalized

and posted.D. The balance sheet accounts in the adjusted trial balance have the proper financial

statement amounts.

16. Which of the following is not an adjusting entry?A. The supplies used during the period.B. The cash payment on a note from the bank.C. The depreciation of equipment.D. The salaries owed but not yet paid

17. A journal entry contains a debit to a liability account and a credit to a revenue account. This is an example of a(n):

A. accrued expense.B. deferred expense.C. unearned revenue.D. accrued revenue.

18. Which of the following accounts is a closing entry?A. Accounts receivable is closed to reflect the amounts paid during the year.B. Salary expense is closed to reflect the salaries owed but not yet paidC. Revenues are closed to allow an accurate account of annual revenueD. equity is closed to reflect the withdrawals during the year

19. The entry to close Income SummaryA. depends on the total amount of revenues and total amount of expenses.B. is always a debit to Income Summary and a credit to Owner's Equity. C. is always a debit to Owner's Equity and a credit to Income Summary.D. never occurs.

20. Permanent accounts include:A. cash, service revenue and land.B. cash, prepaid expenses and unearned revenue.C. cash, land and salaries expense.D. service revenue, salaries expense and utilities expense.

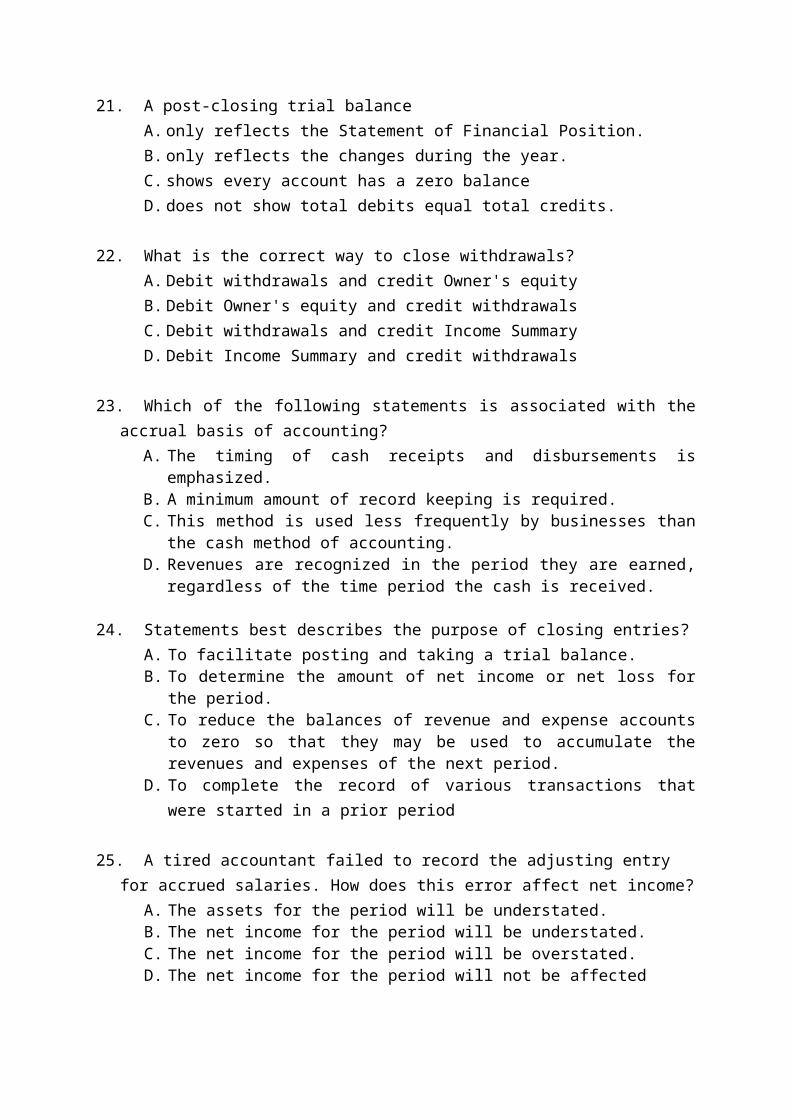

21. A post-closing trial balanceA. only reflects the Statement of Financial Position.B. only reflects the changes during the year.C. shows every account has a zero balanceD. does not show total debits equal total credits.

22. What is the correct way to close withdrawals?A. Debit withdrawals and credit Owner's equityB. Debit Owner's equity and credit withdrawalsC. Debit withdrawals and credit Income SummaryD. Debit Income Summary and credit withdrawals

23.Which of the following statements is associated with the accrual basis of accounting?A. The timing of cash receipts and disbursements is emphasized.B. A minimum amount of record keeping is required.C. This method is used less frequently by businesses than the cash method of

accounting.D. Revenues are recognized in the period they are earned, regardless of the time

period the cash is received.

24.Statements best describes the purpose of closing entries?A. To facilitate posting and taking a trial balance.B. To determine the amount of net income or net loss for the period.C. To reduce the balances of revenue and expense accounts to zero so that they may

be used to accumulate the revenues and expenses of the next period.D. To complete the record of various transactions that were started in a prior period

25. A tired accountant failed to record the adjusting entry for accrued salaries. How does this error affect net income?

A. The assets for the period will be understated.B. The net income for the period will be understated.C. The net income for the period will be overstated.D. The net income for the period will not be affected

ACCOUNTING FOR MERCHANDISING BUSINESSES & ANNUAL REPORT

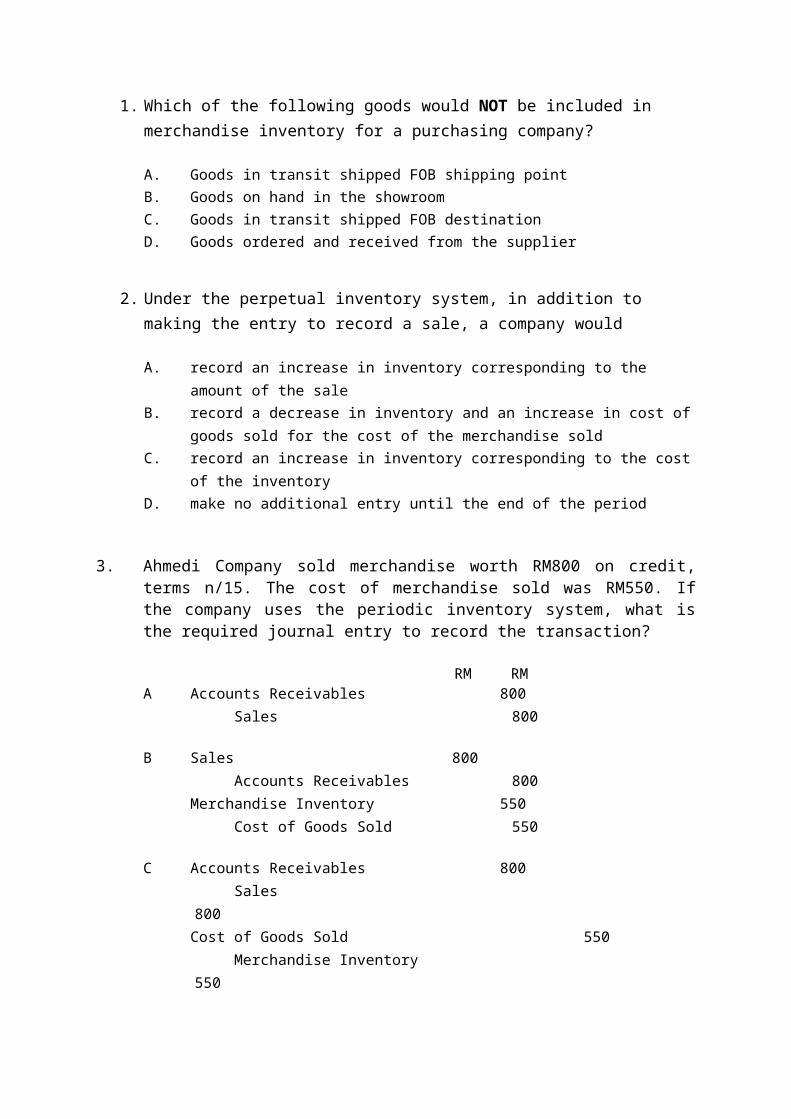

1. Which of the following goods would NOT be included in merchandise inventory for a purchasing company?

A. Goods in transit shipped FOB shipping pointB. Goods on hand in the showroomC. Goods in transit shipped FOB destinationD. Goods ordered and received from the supplier

2. Under the perpetual inventory system, in addition to making the entry to record a sale, a company would

A. record an increase in inventory corresponding to the amount of the saleB. record a decrease in inventory and an increase in cost of goods sold for the cost of

the merchandise soldC. record an increase in inventory corresponding to the cost of the inventoryD. make no additional entry until the end of the period

3. Ahmedi Company sold merchandise worth RM800 on credit, terms n/15. The cost of merchandise sold was RM550. If the company uses the periodic inventory system, what is the required journal entry to record the transaction?

RM RMA. Accounts Receivables 800

Sales 800

B. Sales 800 Accounts Receivables 800Merchandise Inventory 550 Cost of Goods Sold 550

C. Accounts Receivables 800 Sales 800Cost of Goods Sold 550 Merchandise Inventory 550

D. Merchandise Inventory 800 Sales 800Cost of Goods Sold 550 Accounts Receivables 550

4. The cost of merchandise available for sale is equal to the:

A. Cost of merchandise sold minus the Ending inventoryB. Sales revenue minus the Cost of merchandise soldC. Cost of merchandise sold plus the Ending inventoryD. Ending inventory plus the Sales revenues

5. Under the perpetual inventory system, in addition to making the entry to record a sales return, a company would __________________________

A. increase Merchandise Inventory and reduce Cost of Goods SoldB. increase Cost of Goods Sold and reduce PurchasesC. increase Cost of Goods Sold and reduce Merchandise InventoryD. make no additional entry until the end of the period

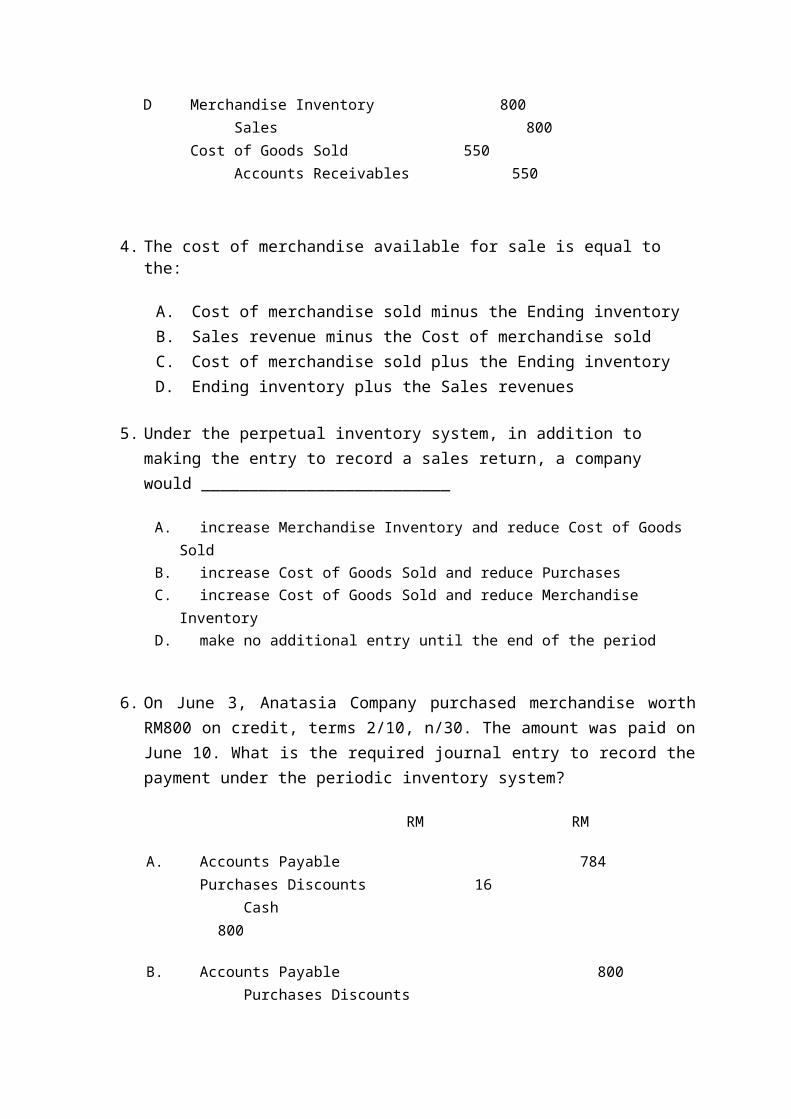

6. On June 3, Anatasia Company purchased merchandise worth RM800 on credit, terms 2/10, n/30. The amount was paid on June 10. What is the required journal entry to record the payment under the periodic inventory system?

RM RM

A. Accounts Payable 784 Purchases Discounts 16 Cash 800

B. Accounts Payable 800 Purchases Discounts 16 Cash 784

C. Accounts Payable 800 Inventory 16 Cash 784

D. Cash 800 Purchases Discounts 16 Accounts Payable 816

7. A company that uses the perpetual inventory system sold RM1,000 of goods to a customer on account. The inventory had been purchased by the company for RM400. Which of the following journal entries correctly records the Cost of goods sold?

RM RMA. Cost of goods sold 400

Sales revenue 400

B. Inventory 400 Cost of goods sold 400

C. Cost of goods sold 400 Inventory 400

D. Accounts receivable 400 Sales revenue 400

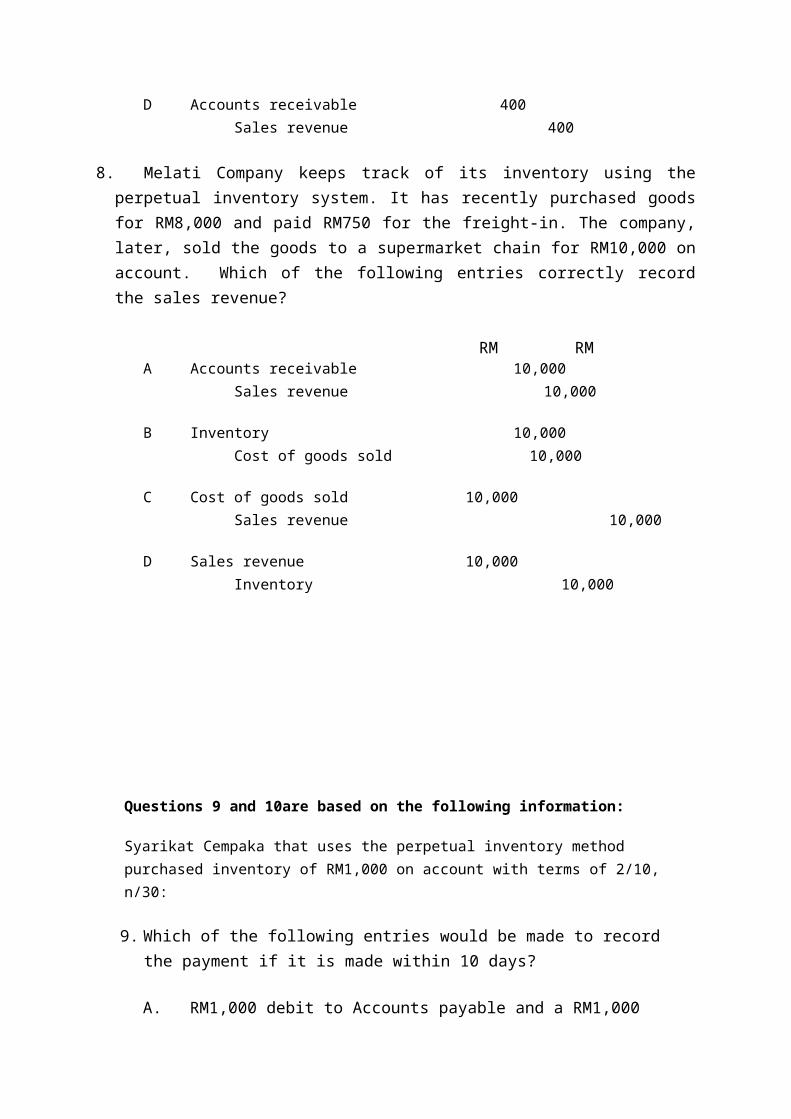

8. Melati Company keeps track of its inventory using the perpetual inventory system. It has recently purchased goods for RM8,000 and paid RM750 for the freight-in. The company, later, sold the goods to a supermarket chain for RM10,000 on account. Which of the following entries correctly record the sales revenue?

RM RMA. Accounts receivable 10,000

Sales revenue 10,000

B. Inventory 10,000 Cost of goods sold 10,000

C. Cost of goods sold 10,000 Sales revenue 10,000

D. Sales revenue 10,000 Inventory 10,000

Questions 9 and 10are based on the following information:

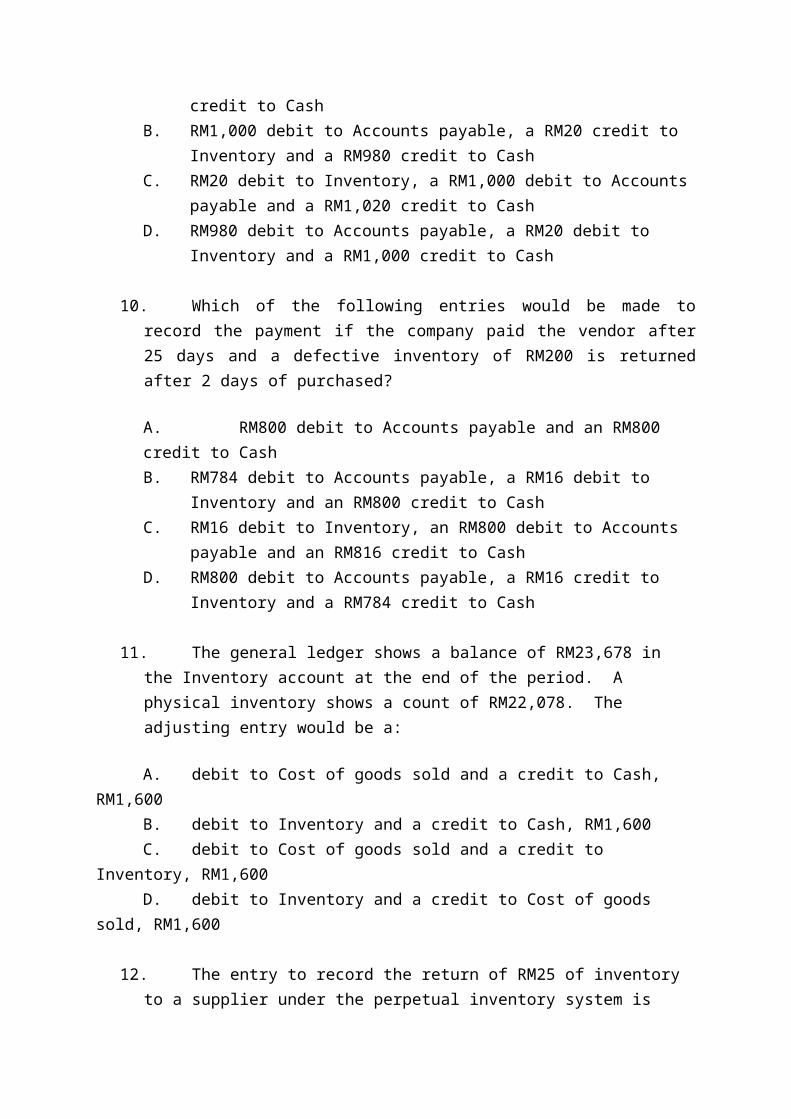

Syarikat Cempaka that uses the perpetual inventory method purchased inventory of RM1,000 on account with terms of 2/10, n/30:

9. Which of the following entries would be made to record the payment if it is made within 10 days?

A. RM1,000 debit to Accounts payable and a RM1,000 credit to CashB. RM1,000 debit to Accounts payable, a RM20 credit to Inventory and a RM980

credit to CashC. RM20 debit to Inventory, a RM1,000 debit to Accounts payable and a

RM1,020 credit to CashD. RM980 debit to Accounts payable, a RM20 debit to Inventory and a RM1,000

credit to Cash

10. Which of the following entries would be made to record the payment if the company paid the vendor after 25 days and a defective inventory of RM200 is returned after 2 days of purchased?

A. RM800 debit to Accounts payable and an RM800 credit to CashB. RM784 debit to Accounts payable, a RM16 debit to Inventory and an RM800

credit to CashC. RM16 debit to Inventory, an RM800 debit to Accounts payable and an RM816

credit to CashD. RM800 debit to Accounts payable, a RM16 credit to Inventory and a RM784

credit to Cash

11. The general ledger shows a balance of RM23,678 in the Inventory account at the end of the period. A physical inventory shows a count of RM22,078. The adjusting entry would be a:

A. debit to Cost of goods sold and a credit to Cash, RM1,600B. debit to Inventory and a credit to Cash, RM1,600C. debit to Cost of goods sold and a credit to Inventory, RM1,600D. debit to Inventory and a credit to Cost of goods sold, RM1,600

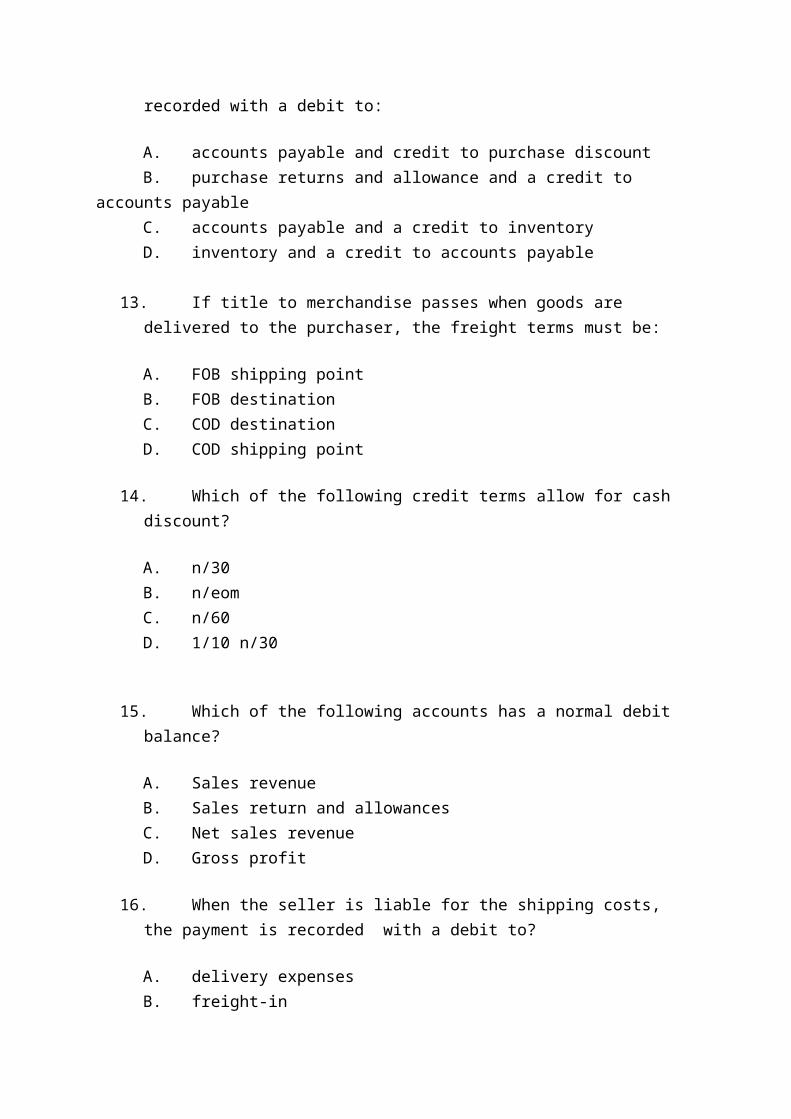

12. The entry to record the return of RM25 of inventory to a supplier under the perpetual inventory system is recorded with a debit to:

A. accounts payable and credit to purchase discountB. purchase returns and allowance and a credit to accounts payableC. accounts payable and a credit to inventoryD. inventory and a credit to accounts payable

13. If title to merchandise passes when goods are delivered to the purchaser, the freight

terms must be:

A. FOB shipping pointB. FOB destinationC. COD destinationD. COD shipping point

14. Which of the following credit terms allow for cash discount?

A. n/30B. n/eomC. n/60D. 1/10 n/30

15. Which of the following accounts has a normal debit balance?

A. Sales revenueB. Sales return and allowancesC. Net sales revenueD. Gross profit

16. When the seller is liable for the shipping costs, the payment is recorded with a debit to?

A. delivery expensesB. freight-inC. inventoryD. cash

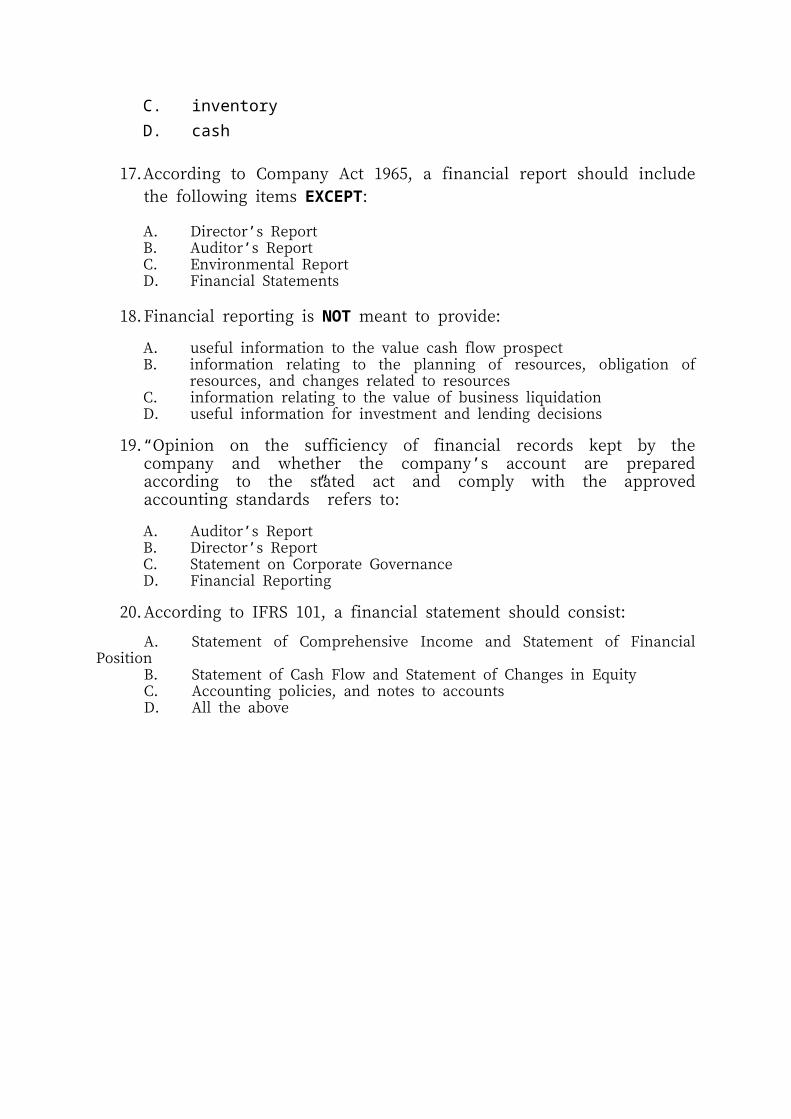

17. According to Company Act 1965, a financial report should include the following items EXCEPT:

A. Director’s ReportB. Auditor’s ReportC. Environmental ReportD. Financial Statements

18. Financial reporting is NOT meant to provide:

A. useful information to the value cash flow prospect B. information relating to the planning of resources, obligation of resources, and

changes related to resourcesC. information relating to the value of business liquidationD. useful information for investment and lending decisions

19. “Opinion on the sufficiency of financial records kept by the company and whether the company’s account are prepared according to the stated act and comply with the approved accounting standards” refers to:

A. Auditor’s ReportB. Director’s Report C. Statement on Corporate GovernanceD. Financial Reporting

20. According to IFRS 101, a financial statement should consist:

A. Statement of Comprehensive Income and Statement of Financial PositionB. Statement of Cash Flow and Statement of Changes in EquityC. Accounting policies, and notes to accountsD. All the above

FINANCIAL STATEMENT ANALYSIS

1. Which one of the following is not a characteristic generally evaluated in analyzing financial statements?

a. Liquidityb. Profitabilityc. Marketabilityd. Solvency

2. In analyzing the financial statements of the company, a single item on the financial statements

a. Should be reported in bold-face type.b. Is more meaningful in compared to other financial information,c. Is significant only if it is large.d. Should be accompanied by a note.

3. Short term creditors are usually most interested in evaluating

a. Solvency.b. Liquidity.c. Marketability.d. Profitability.

4. Long-term creditors are usually most interested in evaluating

a. Liquidity and solvencyb. Solvency and marketabilityc. Liquidity and Profitabilityd. Profitability and solvency

5. Comparisons of financial data made within a company are called Long-term creditors are usually most interested in evaluating

a. Intracompany comparisons.b. Intercompany comparisons.c. Interior comparisons.d. Intramural comparison.

6. Which of the following is not a tool in financial statement analysis?

a. Horizontal analysis.b. Circular analysis.c. Vertical analysis.d. Ratio analysis.

7. The average collection period is 73 days, what is the receivables turnover?

a. 4.68 times.b. 5.00 times.c. 2.57 times.d. None of the above.

8. If equal amounts are added to the numerator and denominator of the ratio. The ratio will always

a. Increase.b. Decrease.c. Stay at the same.d. Equal zero.

9. A company has a receivables turnover ratio of 8. The average net receivables during the period are RM400,000. What is the amount of net credit collection sales for the period?

` a. RM50, 000.b. RM3, 200,000.c. RM600, 000.d. Cannot be determined from the information given.

10. A company has an average inventory on hand of RM20, 000 and the average days to sell inventory is 14.6 days. What is cost of goods sold?

a. RM500, 000.b. RM292, 000.c. RM493, 150.e. RM136, 986.

The following information is for questions 11 and 12.

The Pokok Sena Department Store (PSDS) had credit sales of RM8,000,000 and cost of good sold of RM6,000,000 for the year. The average inventory for the year amounted to RM2,400,000.

11. The inventory turnover ratio for the year is

a. 3.3 times.b. 10 timesc. 2.5 timesd. 2 times.

12. The average number of days to sell the inventory during the year was

a. 183 days.b. 146 days.c. 61 days.d. 37 days.

13. Traditional financial statement are based on

a. Unadjusted cost.b. Price-level adjusted cost.c. The lower of cost or price-level adjusted historical costd. Fair market value

14. Net sales are RM1,300,000, beginning total assets are RM700,000, and the asset turnover is 2.5. What is the ending total asset balance?

a. RM520, 000.b. RM340, 000.c. RM700.000.d. RM875, 000.

15. If a company has an acid-test ratio of 1.2:1, what respective effects will the following of cash by short-term debt and collection of account receivables have on the ration?

Short-term borrowing Collection of Receivables

a. Increase No effectb. Increase Increasec. Decrease No effectd. Decrease Decrease

16. The acid-test ratio

a. Is a quick of an approximation of the current ratio.b. Does not include all current liabilities in the calculation.c. Does not include inventory as part of the numerator.d. Does include prepaid expenses as part the numerator.

17. Net income does appear in the numerator of the a. Profit margin.b. Return on assets.c. Return on common shareholder’s equity.d. Payout ratio.

18. A limitation in calculating ratios in financial statement is that

a. It requires a calculator.b. No one rather than management would be interested in them.c. Some account balance may reflect atypical data at year end.d. The seldom identity problem in a company

19. Earnings per share is calculated

a. only for common share. b. only for preferred sharesc. for common and preferred shares.d. only for treasury shares.

20. Justinbibir Clothing Store had a balance in the Account Receivable account of RM390,000 at the beginning of the year and a balance of RM410,000 at the end of the year. Net credit sales during the year amounted to RM5,840,000. The average collection period of the receivables in terms of days was

a. 15 days.b. 365 days.c. 50 days.d. 25 days.

MANAGERIAL ACCOUNTING

25. Management accountants would NOT:E. assist in budget planningF. prepare reports primarily for external usersG. determine cost behaviorH. be concerned with the impact of cost and volume on profits

26. Managerial accounting reports can be described as:A. general-purposeB. macro-reportsC. special purposeD. classified financial statements

27. Product costs which are considered conversion costs are:A. direct materials and direct laborB. direct labor and manufacturing overheadC. direct materials and indirect labourD. direct materials and manufacturing overhead

28. Which of the following is NOT classified as direct labour?A. bottlers of beverage in a soft drinks companyB. photocopy machines operators in a photocopy shopC. wages of supervisorsD. bakers in a bakery

29. Manufacturing company calculates cost of goods sold as:A. beginning finished goods inventory + cost of goods purchased - ending finished

goods inventoryB. ending finished goods inventory - cost of goods manufactured + beginning

finished goods inventoryC. beginning finished goods inventory - cost of goods manufactured -ending finished

goods inventoryD. beginning finished goods inventory + cost of goods manufactured - ending

finished goods inventory

30. Kinta Kimia Sdn Bhd (KKSB) reported the following year-end information: cost of goods manufactured, RM516,000; beginning finished goods inventory, RM252,000; and ending finished goods inventory, RM264,000. KKSB’s cost of goods sold for the year is:

A. RM504,000B. RM528,000C. RM476,000D. RM252,000

31. Which of the following does NOT appear on the Statement of Financial Position of a manufacturing company?

A. finished goods inventoryB. work in process inventoryC. cost of goods manufacturedD. raw materials inventory

32.Which of the following represents a period cost?A. the Vice President of Sales' salaryB. overhead allocated to the manufacturing operationsC. labor costs associated with quality controlD. retirement benefits associated with factory workers

33. A manufacturing company reports cost of goods manufactured as a(n):A. current asset on the balance sheetB. administrative expense on the income statementC. component in the calculation of cost of goods sold on the income statementD. component of the raw materials inventory on the balance sheet

Use the following information for Questions 10 - 11.

Raw materials inventory, 1 January RM 20,000Raw materials inventory, 31 December 40,000Work in process, 1 January 18,000Work in process, 31 December 12,000Finished goods, 1 January 40,000Finished goods, 31 December 32,000Raw materials purchases 1,000,000Direct labor 460,000Factory utilities 150,000Indirect labor 50,000Factory depreciation 400,000Selling and administrative expenses 420,000

34. Direct materials used are:A. RM1,060,000B. RM1,020,000C. RM1,000,000D. RM980,000

35. If the direct materials used is RM1,000,000. Total manufacturing costs is equal to:A. RM2,060,000B. RM2,054,000C. RM1,860,000D. RM2,480,000

36. Given the following data, compute the costs of goods manufactured:

RM RMDirect materials used 240,000 Beginning work in process 40,000Direct labor 100,000 Ending work in process 20,000Manufacturing overhead 300,000 Beginning finished goods 50,000Administrative expenses 350,000 Ending finished goods 30,000 A. RM660,000B. RM620,000C. RM660,000D. RM680,000

37. Which one of the following does NOT appear on the statement of cost of goods manufactured of a manufacturing company?

A. finished goods inventoryB. work in process inventoryC. cost of goods manufacturedD. raw materials inventory

38. Indirect labor is a:A. non-manufacturing costB. prime costC. product costD. period cost

39. The management of an organization performs several broad functions. They are:E. planning, directing and motivating, and selling.F. planning, directing and motivating, and controlling.G. planning, manufacturing, and controlling.H. directing and motivating, manufacturing, and controlling.

40. The following are managerial accounting users EXCEPT E. managersF. supervisorsG. regulatorsH. officers

41. Which of the following is NOT an element of manufacturing overhead?A. sales manager’s salaryB. plant manager’s salaryC. factory repairman’s wagesD. product inspector’s salary

Use the following information for Questions 18 - 19.

Presented below are incomplete manufacturing cost data:

Opening Direct

material

Direct materials purchased

Ending Direct

material

Direct labor Factory overhead

Total manufacturing

cost

RM32,000 X RM11,000 RM75,000 RM120,000 RM296,000

RM21,000 RM105,000 RM15,000 Y RM111,000 RM300,000

42. Determine XE. RM92,000F. RM80,000G. RM58,000H. RM144,000

43. Determine YE. RM90,000F. RM48,000G. RM120,000H. RM78,000

44. Below are elements of period cost EXCEPTE. advertising expenseF. salesmen’s salaryG. supervisors’ salaryH. delivery expense

45. The following are materials used in furniture factory. Which one is considered as direct material?

A. glueB. paintC. woodD. nails

Use the following information for Questions 22 - 25.

Omma Manufacturing reports the following costs and expenses in November 2012:

Factory utilities RM 8,500 Production line wages RM 55,000Depreciation on machineries 12,650 Factory managers salary 9,000Depreciation on delivery van 3,000 Administrative salary 25,000Indirect materials 39,800 Salesmen commission 33,000Direct materials 99,000 Advertising 5,000

46. Determine the prime costA. RM69,950B. RM154,000C. RM223,950D. RM163,000

47. Determine the conversion costA. RM69,950B. RM72,950C. RM135,950D. RM124,950

48. Determine the product costA. RM66,000B. RM72,000C. RM223,950D. RM226,950

49. Determine the period costA. RM66,000B. RM72,000C. RM223,950D. RM226,950

COST-VOLUME-PROFIT ANALYSIS

1. Which of the following is NOT an underlying assumption of CVP analysis?(a) Changes in the activity are the only factors that affect costs(b) Costs classifications are reasonably accurate(c) Beginning inventory is larger than ending inventory(d) Sales mix is constant

2. Variable costs are cost that:(a) Vary in total directly and proportionately with changes in the activity level.(b) Remain the same per unit at every activity level.(c) Neither of the above(d) Both (a) and (b) above

3. Mixed costs consist of a:(a) Variable cost element and fixed cost element.(b) Fixed cost element and a controllable cost element.(c) Relevant cost element and controllable cost element(d) Variable cost element and a relevant cost element.

4. Fixed costs are RM900,000 and the contribution margin per unit is RM150. What is the break-even point?(a) RM2,250,000(b) RM6,000,000(c) 2,250 units(d) 6,000 units

5. If a company had a contribution margin of RM200,000 and a contribution margin ratio of 40%, what is the total variable costs?(a) RM300,000(b) RM120,000(c) RM500,000(d) RM80,000

6. A company sells a product which has a sale price per unit of RM5, variable costs per unit of RM3 and total fixed costs of RM100,000. The number of units that the company must sell to achieve break even is: (a) 50,000 units(b) 20,000 units(c) 200,000 units(d) 33,333 units

7. Johan Enterprise sells its product at RM20 per unit, variable cost RM12 per unit, and the total fixed costs are RM160,000, how many units must be sold to earn net income of RM80,000?(a) 45,000 units(b) 30,000 units(c) 24,000 units

(d) 18,000 units

8. Kaman Sdn Bhd has fixed costs of RM600,000 and variable costs are 40% of sales. What are the required sales if the company desires net income of RM60,000?(a) RM1,100,000(b) RM1,000,000(c) RM1,650,000(d) RM1,500,000

9. The mathematical equation for computing the required sales to obtain target net income is: Required sales =:(a) Variable cost + Target net income(b) Variable cost + Fixed cost + Target net income(c) Fixed cost + Target net income(d) No correct answer is given

10. Contribution margin:(a) is revenue remaining after deducting variable costs.(b) may be expressed as contribution margin per unit.(c) is selling price less cost of goods sold.(d) Both (a) and (b) above.

Question 11 -14 are based on the following information:

The followings are the information extracted from DaDi Du Sdn Bhd projected profit for the coming year.

Items Total (RM) Per Unit (RM)Sales 200,000 20Variable expenses 120,000 12Fixed cost 64,000

11. What is the contribution margin per unit and the contribution margin ratio?(a) The contribution margin per unit is RM8 and the contribution margin ratio is

66.67%.(b) The contribution margin per unit is RM8 and the contribution margin ratio is 40%.(c) The contribution margin per unit is RM80,000 and the contribution margin ratio is

66.67%.(d) The contribution margin per unit is RM80,000 and the contribution margin ratio is

66.67%.

12. How many units must be sold to earn a profit of RM30,000?(a) 3750 units(b) 10,000 units(c) 11,750 units(d) 8,000 units

13. Suppose DaDiDu would like to earn operating income equal to 20 percent of sales revenue. How many units must be sold for this goal to be realized?(a) 16,000 units (b) 40,000 units (c) 9,600 units(d) 3,200 units

14. What is the margin of safety for the projected level of sales.(a) 66.67%(b) 40%(c) 25%(d) 20%

15. The following are the fixed costs except:(a) Insurance on factory machinery.(b) Depreciation on machinery(c) Direct labour(d) Taxes on land on which the factory is located

16. The following situations indicate the decrease in break-even point except:(a) An increase in the selling price of the product(b) A decrease in variable cost per unit(c) An increase in total fixed costs.(d) None of the above is correct.

17. Redcliff Enterprise sells a single product for RM52 per unit. If variable expenses are 70% of sales and fixed expenses total RM16,000, the breakeven point in sales dollars will be(a) RM53,333.(b) RM36,400.(c) RM22,857.(d) RM1,025.

18. At an activity level of 20,000 units produced, fixed costs total RM12,000 and variable costs total RM44,000. What would be the amount of total costs if 25,000 units are produced, assuming that this activity level is within the relevant range?

(a) RM56,000(b) RM59,000(c) RM67,000(d) RM70,000

19.The contribution margin is calculated as:(a) sales minus fixed costs, divided by sales.(b) sales minus variable costs, divided by sales.(c) sales minus fixed costs.(d) sales minus variable costs.

20. If fixed costs for a company are RM65,000 and variable costs are 20% of sales, what do total sales need to be to achieve a target net income of RM35,000?(a) RM500,000(b) RM116,250(c) RM125,000(d) RM108,750

BUDGETING

1. The following are objectives of budgeting EXCEPT:

A. Establishing organizational goalsB. Periodically compare organizational actual achievement with their goalsC. Developing appropriate organizational information systemD. Executing strategy to achieve organizational goals

2. Which of the following budget characteristics can create human behavior problems?

A. Setting a specific goalB. Setting goals which are too tightC. Setting an achievable goalD. Setting a measurable goal

3. Zero-based budgeting:

A. shows expected results of an organization for several activity levelsB. shows expected results of an organization for only one activity levelC. requires managers to prepare their budget as though its operations are being

started for the first timeD. shows organization’s yearly performance

4. _________________________ is used as the starting point to estimate the purchase budget.

A. Selling and administrative budgetB. Cost of goods sold budgetC. Sales budgetD. Cash budget

5. The following items should be considered when preparing the cash budget EXCEPT:

A. Depreciation expenseB. Total cash receiptsC. Interest on financingD. Cash payments to suppliers

6. A master budget consists of two major parts that are:

A. Cash and Inventory budgetsB. Operating and Financial budgetsC. Purchase and Sales budgetsD. Inventory and Capital Expenditure budgets

7. Given is information on BoomBoom Enterprise’s budget:

Budgeted credit sales:

July August September

RM120,000 RM211,000 RM198,000

Based on their experience:

None of the budgeted sales will be collected in the month of the sales 60% will be collected the month after sales 36% in the second month and 4% will be uncollectible

The budgeted cash receipts from accounts receivable for September would be:

A. RM196,400B. RM189,200C. RM198,670D. RM169,800

8. Given is the data for SeaMaster Enterprise’s budgeted sales of life jackets for January and February 2012:

Month Budgeted sales units Price per unit

January 3000 units RM45 per unit

February 2% more than January RM50 per unit

All sales are in cash. What is the sales budget of SeaMaster for January and February?

A. January RM135,000 and February RM153,000B. January RM153,000 and February RM135,000C. January RM135,000 and February RM155,000D. January RM155,000 and February RM135,000

Questions 9 and 10 are based on the following information:

Zania Corporation is a merchandising company. Information pertaining to the company’s sales revenues is as follows:

June RM (Actual)

JulyRM (Budgeted)

AugustRM (Budgeted)

SeptemberRM (Budgeted)

Cash Sales 80,000 100,000 60,000 70,000

Credit Sales 240,000 360,000 180,000 220,000

Total Sales 320,000 460,000 240,000 290,000

Zania’s management team estimates that:

Of the credit sales, 60% are collectible in the month of sales and the remainder is in the following month.

Purchases of inventory are 50% of the next month’s total sales. All purchases of inventory are on accounts which are paid in the month of the

purchase.

9. Zania Corporation’s budgeted cash collections in July are:

A. RM312,000B. RM460,000C. RM316,000D. RM412,000

10. Zania Corporation’s budgeted cash payments in August are:

A. RM240,000B. RM220,000C. RM145,000D. RM269,300

11. Operating budget includes all of the following EXCEPT:

A. purchase budgetB. sales budgetC. sales forecast budgetD. administrative budget

Questions 12 and 13 are based on the following information:

MydinSdnBhd is a merchandising company. Data from company’s 2012 budgeted sales for the third quarter of the year are as follows:

Month Budgeted Sales (RM)

July 80,000

August 90,000

September 70,000

Cost of goods sold equals to 65% of sales. MydinSdnBhd maintains a monthly ending inventory at 80% of the cost of goods sold

for the following month. Beginning inventory in July is RM50,000

The company is now preparing a Merchandise Purchase Budget.

12. What is the budgeted purchase for July?

A. RM63,050B. RM65,650C. RM48,800D. RM75,050

13. What is the beginning inventory for September?

A. RM19,050B. RM36,400C. RM56,000D. RM45,500

14. Which of the following are components of Financial Position Budget:

i. Cash budgetii. Inventory budget

iii. Selling and administrative budgetiv. Capital expenditure budget

A. ii, iii and ivB. i and ivC. i and iiiD. iii and iv

Questions 15 and 16 are based on the following information:

Duniawi Enterprise estimates to sell their new design shirts at RM20 each. Estimated sales for November and December are as follows:

Month November December

Units of sales 2,000 units 3,200 units

Advertising expense is expected to be 7% from the sales amount Other expenses are administrative expense of RM15,000 and depreciation expense of

RM8,000 per month

15. The estimated total selling and administrative expenses for November is:

A. RM25,800B. RM23,224C. RM25,000D. RM28,500

16. The estimated selling expenses for December are:

A. RM12,242

B. RM23,224C. RM27,480D. RM4,480

17. The operating budget process usually ends with:

A. sales budgetB. selling and administrative budgetC. income statement budgetD. balance sheet budget

18. When preparing a projected income statement, which of the following budget is firstly prepared?

A. Financial budgetB. Sales budgetC. Selling and administrative budgetD. Cost of goods sold budget

Questions 19 and 20 are based on the following information:

Syarikat Pelangi estimates to sell their product at RM20 per unit. Its estimated sales quantities for September to November 2011 are as follows:

September 1,500 unitsOctober 2,000 units November 2,500 unitsDecember 3,800 units

Advertising expense is expected to be 5% from the following month sales while other expenses are administrative expense RM25,000 and depreciation expense RM15,000 for each month.

19. The total expected sales for the 3 months are:

A. RM120,000B. RM196,000C. RM6,000D. RM9,800

20. The total selling and administrative expenses for October are:

A. RM42,500B. RM42,000C. RM41,500D. RM43,800

21. Which of the following BEST describes some of the benefits related to the preparation and use of budgets?

A. Business activities are better coordinateB. Managers become aware of other managers’ plansC. Employees may become cost conscious and try to conserve resourcesD. All of the above

22. The budget that reflects in the effect of fluctuation in the level of activity into a various budgets is known as:

A. static budgetB. flexible budgetC. operational budgetD. cash budget

23. Sahabat Company Bhd expects RM650,000 of credit sales in November and RM800,000 in December. Historically, a company collects 70% of its sales in the month of sales and 30% in the following month. How much cash does Sahabat Company Bhd expect to collect in December?

A. RM800,000B. RM560,000C. RM755,000D. RM1,015,000

24. The estimated inventory at the beginning of the year is RM45,000, and the desired inventory at the end of the year is RM60,000. The estimated cost of goods is RM500,000. What is the total purchases indicated in the purchases budget?

A. RM485,000B. RM515,000C. RM560,000D. RM605,000

25. The most effective budget figures are developed:

A. from the “top-down”B. from the “bottom-up” following a participatory processC. solely by the budget committeeD. all of the above

26. A calculator store purchased RM7,000 of calculator in September. The beginning inventory for September are RM3,000, while at the end of September the inventory are expected to be RM2,000. What is the budgeted cost of goods sold for the month of September?

A. RM5,000B. RM6,000C. RM7,000D. RM8,000

27. When preparing the cash budget, all of the following should be considered EXCEPT:

A. depreciation expenseB. cash payment to suppliersC. total cash receiptsD. interest on financing

28. Abc Company reported the following information for a year 2011:

September October November

Budgeted sales RM620,000 RM580,000 RM720,000

How much cash will Abc Company receive in November if all the sales are on credit and the company policy for credit sales is 50% collected in the month of sales and the balance is in the following month sales?

A. RM290,000B. RM650,000C. RM600,000D. RM580,000

29. Which of the following budget is considered as the most important financial budget?

A. Sales forecast budgetB. Capital budgetC. Cash budgetD. Master budget

30. Which one of the following set of items are all necessary components of the master budget?

A. sales budget, operating budgets, and historical budgetB. operating budgets, historical income statement, and budgeted balance sheetC. operating budgets, financial budgets, and capital expenditure budgetD. prior sales reports, capital expenditures budget, and financial budget

![PIRPAG Exercises Post Transtibial Amputation Exercises Post Transtibial... · q [1] Static Quadriceps • Push your legs straight out in front of you • Push the back of your knees](https://img.pdfslide.us/doc/110x75/5af593ba7f8b9a8d1c8dc60b/pirpag-exercises-post-transtibial-amputation-exercises-post-transtibialq-1.jpg)