Embed Size (px)

Citation preview

1

INDUSTRIAS BACHOCO S.A.B. DE C.V.

COVERAGE INITIATION BUY, TP MP 33.12

�

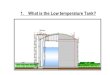

Relative Performance

We are initiating coverage on Bachoco, Mexico’s lar gest chicken producer, with a BUY recommendation and a 12-month price target of MP 33 .1 per share for a potential 35.3% return (including a 2.3% dividend yield). We believe Bachoco is a premium asset due to its leading market position, operating expertise, attractive growth prospects and low valuation.

Leading position in the Mexican poultry industry an d vertical integration. Bachoco is Mexico’s largest chicken producer with an estimated 35% market share. Founded in 1952, the company participates in every step of the chicken production process and has more than 1,000 facilities in Mexico and the US. Bachoco’s main products are chicken (82% of sales), egg (7%), balance food (7%) and others (4%).

We expect Bachoco’s EBITDA to rise at a 49.5% CAGR (considering acquisitions) during the 2012-2015E period supported by higher per capita consumption (3.5% CAGR) and the company’s ability to grow faster than the poultry industry, supported by an extensive distribution network and the integration of OK industries and Trosi de Carne. We believe our estimates are on the conservative side as they do not include any potential acquisition.

Healthy financial structure and positive free cash flow generation. Bachoco had a negative net debt of MP 1.5 billion at the end of 2Q12, given the company´s conservative policies. This is not expected to change, since Bachoco is a significant free cash flow generator.

Management. Bachoco is managed by an executive team which has a solid track record in the poultry industry.

Attractive valuation. Bachoco is currently trading at a 2013E EV/EBITDA of 4.1x and a 2013E P/E of 8.9x. These figures represent discounts of 50% and 42%, respectively, against the Mexican food industry.

Bachoco’s main operating risks are the volatility in raw material prices, FX volatility, chicken diseases and its ability to compete in the US market through OK Industries.

BUY

September 18, 2012

Actinver Corporate Headquarters Guillermo González Camarena 1200 Floor 5, Centro de Ciudad Santa Fe, México, D.F. 01210

Martín Lara � [email protected] ℡ +52 (55) 1103 6600 x 5033 Eduardo Fonseca Fons � [email protected] ℡ +52 (55) 1103 6600 x 4122

Local Ticker BACHOCO BTarget Price 33.12Last Price 24.90Div. Yield 2012 2.34%Expected Return 35.35%Mkt. Cap (Million) MP 14,940Ent. Value (Million) MP 13,330LTM Price Range (20.32 - 26.35)

60

80

100

120

140

160

180

Jan

-09

Ma

y-09

Se

p-0

9

Jan

-10

Ma

y-10

Se

p-1

0

Jan

-11

Ma

y-11

Se

p-1

1

Jan

-12

Ma

y-12

Mexbol Bachoco

Source: Bloomberg, Actinver

OPERATING INDICATORS 2011 6M12 2012E 2013E 2014E 2015ESales 27,738 18,742 38,173 40,399 42,990 45,859EBITDA 716 1,653 3,014 3,070 3,310 3,577Net Profit 128 977 1,744 1,686 1,851 2,035EPS 0.21$ 1.63$ 2.91$ 2.81$ 3.09$ 3.39$ Net Debt (1,157) (1,512) (1,673) (2,439) (3,301) (4,281)Sales Growth 12% 48% 38% 6% 6% 7%EBITDA Growth (77%) 131% 321% 2% 8% 8%EBITDA Margin 2.6% 8.8% 7.9% 7.6% 7.7% 7.8%Net Debt / EBITDA (1.6x) (0.9x) (0.6x) (0.8x) (1.0x) (1.2x)MULTIPLES 2011 6M12 2012E 2013E 2014E 2015EEV / EBITDA 19.3x - 4.4x 4.1x 3.5x 3.0xP/E 117.0x - 8.6x 8.9x 8.1x 7.3xFCF Yield (7.2%) - 5.3% 5.9% 6.5% 7.2%Dividend Yield 2.0% - 2.1% 2.4% 2.7% 2.9%P/BV 0.9x - 0.8x 0.8x 0.7x 0.7xSource: Company data, Actinver.

2

INDEX

Industry 3

Company Description 5

Business line 6

Management 7

Shareholder Structure 7

Dividends 8

Risks 8

Share performance 8

Financial results 9

Projections and prospects 11

Valuation 13

Operating Model 15

Financial Statements 16

3

Industry

Mexicans are the world´s biggest consumers of eggs, and Mexico is the world’s 5 th largest chicken and egg producer. Chicken consumption was 26.1 kg per capita in 2011 vs. 26.0 kg in 2010 (National Association of Poultry Producers or UNA). In 2011, the per capita egg consumption was 22.4 kg vs 22.8 kg in 2010. When per capita income increases, egg consumption decreases because there is a preference for chicken products.

In 2011, the Mexican poultry industry produced more than 5.4 million tons of food with an estimated value of MP 94,000 million. Chicken products contributed with MP 58,385 million, egg with MP 35,450 million and turkey with MP 694 million.

In Mexico, chicken is sold fresh, making this an im portant barrier of entry to the market . Bachoco has a 35% market share in the chicken market; Bachoco, Pil-

grim’s Pride and Tyson Foods together have 59% of the market and the rest is dis-tributed among 179 small and medium producers.

Major poultry producers have significant advantages : Ability to control feed costs, economies of scale, control of feed preparation and geographic diversification. In Mexico, having a refrigerated distribution network is key, since most of the chicken is consumed fresh.

The Mexican egg industry is more fragmented than th e chicken one. The nine largest producers have approximately 44% of the market in 2010. The largest pro-ducer is San Juan with an estimated 14% market share, followed by Bachoco with 5.2% of the market.

The US poultry industry is very different than Mexi co´s. Chicken meat is also the most popular in the US representing 40.2% of the total meat production. US consum-ers have a strong preference for “ready to eat” products and fresh chicken consump-tion is practically non-existent. Frozen meal is the best-selling. Margins are more stable, though lower, than in Mexico. Companies can negotiate input and output pric-es over longer periods, reducing volatility. There is no difference in the production of poultry.

Poultry producers in the U.S. have lower costs, sin ce feed prices are lower. Imports into Mexico, primarily of frozen parts, tak e place occasionally. Current-ly, the most imported products are chicken leg quarters, but represent a very small percentage of the market.

In the US, the largest chicken producers are Tyson Foods and Pilgrim’s Pride, which command a 22% and 17% market share, respectively. OK Industries has a 2% market share, concentrated primarily in the states of Oklahoma and Nebraska.

The chicken industry worldwide is characterized by a long-term decline in real prices, and cyclical periods of higher profitability leading to overproduction followed by periods of lower prices and lower profitability.

Worldwide, Mexico is one of the 10 main producers o f balanced feed . Corn and soybean are the main ingredients.

0.00

5.00

10.00

15.00

20.00

25.00

0

500

1,000

1,500

2,000

2,500

3,000

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Kg.

Tho

usan

d of

Ton

s

National Egg production and consumption

National Production Consumption per Cápita

0.00

5.00

10.00

15.00

20.00

25.00

30.00

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Kg.

Tho

usan

d of

Ton

s

National Chicken production and consumption

National Production Imports Consumption per Cápita

Chicken33.80%

Turkey0.15%

Egg29.52%Ovine

0.65%

Beef20.93%

Honey0.67% Pig

13.76%

Caprino0.51%

Poultry mexican production (2011)

Source: UNA

4

The main raw materials for the industry are corn, s oybean and sorghum. Corn prices have skyrocketed 21% in USD terms in 2012 due to a severe drought in the US. The sorghum price rose 8.1% in the first 6 months of the year. The soybean price grew 24.2% so far in 2012.

The Mexican egg industry was affected by the aviar flu H7N3 in the State of Jalisco. This region is the main producer of egg in the country producing more than the 50% of the country’s total production. Many of the posture chickens were sacrificed due to this disease. Bachoco’s farms were not affected due to strong bio-security policies.

These two effects boosted the price of chicken and, in particular, eggs in a significant way. Eggs more than doubled from MP 19.0 Kg. at the beginning of the year to more than MP 40.0 Kg. during the third week of August. For this reason, the Economy Min-istry allowed temporary imports of eggs and eliminated import taxes.

Bachoco has benefited from the increase in chicken and egg prices generated by the US drought and the aviar flu . The company is producing eggs at 100% of installed capacity and we believe that the company is selling at a higher prices and margins.

Chicken (2011) Industry s/ volume Bachoco s/ volume Ba choco s/ sales

Live 33% 36% 29%

Public market 20% 14% 14%

Rostisserie 26% 27% 27%

Supermarket 12% 5% 5%

Chicken parts 6% 12% 16%

Value- added products. 3% 6% 9%

Source: UNA, Company data, Actinver

Table eggs (2011) Industry s/ volume Bachoco s/ volum e Bachoco s/ sales

Bulk 80% 45% 34%

Package 14% 55% 66%

Processed 6% 0% 0%

Source: UNA, Company data, Actinver

150

170

190

210

230

250

270

may

/10

jul/1

0

sep/

10

nov/

10

ene/

11

mar

/11

may

/11

jul/1

1

sep/

11

nov/

11

ene/

12

mar

/12

may

/12

jul/1

2

Sorghum

Source: BloombergPrice per 20 metric tones

700

900

1100

1300

1500

1700

1900

ene/

09m

ar/0

9

may

/09

jul/0

9

sep/

09

nov/

09

ene/

10m

ar/1

0

may

/10

jul/1

0

sep/

10

nov/

10

ene/

11

mar

/11

may

/11

jul/1

1

sep/

11

nov/

11

ene/

12

mar

/12

may

/12

jul/1

2

Soy Bean

Source: BloombergPrice per 5,000 bushels

100200300400500600700800900

ene/

09

mar

/09

may

/09

jul/0

9

sep/

09

nov/

09

ene/

10

mar

/10

may

/10

jul/1

0

sep/

10

nov/

10

ene/

11

mar

/11

may

/11

jul/1

1

sep/

11

nov/

11

ene/

12

mar

/12

may

/12

jul/1

2

Corn

Source: BloombergPrice per 5,000 bushels

5

Company Description

Bachoco is Mexico’s largest poultry producer with a n estimated 35% market share in chicken and 5% in egg. The company started as a table egg producer in 1952 in the State of Sonora. It has been growing both organically and through acqui-sitions (see below). Bachoco’s main products are chicken (82% of sales), egg (7%), balance food (7%) and others (4%). The company has more than 1,000 facilities in Mexico and the US (see table).

Bachoco is vertically integrated as it also produces balanced feed for consump-tion and third party sales, egg incubation, poultry breeding, broiler breeding, chicken, turkey and beef. Bachoco also participates in the packaging and distribu-tion of fresh and value-added meat products.

Bachoco has the largest refrigerated storage and di stribution facilities for chicken in Mexico , which is one of its main competitive advantages. This type of distribution network is essential as most of the chicken is sold fresh.

Production Facilities Mexico U.S.

Chicken Breeding Farms 171 93

Boiler grow-out farms 518 336

Broiler processing plants 9 2

Hatchery 21 3

Egg production plants 91 -

Swine breedings farms 1 -

Swin grow-out farms 10 -

Feed mills 18 2

Process plants 4 2

Total facilities 843 438

Source: Company Data, Actinver

Chicken Mexico

77%

Chicken U.S.5%

Table eggs7%

Balanced feed7%

Other4%

Sales distribution (2011)

Source: Company data, Actinver.Value sold by line as a percentage of sales

1952 Founded by the Robinson Bours brothers as an egg producer in Sonora, México.

1963 Starts table eggs operations in Navojoa, Los Mochis y Culiacán.

1971 Starts chicken and industrial egg production in Culiacán.

1974 Establishes the production operation in Celaya to be closer to Mexico City.

1986 Starts operations in Mexico City.

1987 Stars operations in San Luis Potosí.

1988 Consolidated operations in Mexicali, Baja California.

Moves headquarters to Celaya, Guanajuato.

Starts the south-east divition in Tecamachalco, State of Mexico.

1994 Establish a productive complex in Lagos de Moreno, Jalisco.

1995 Opens industrial plant in Queretaro fodder for chicken waste processing.

1997 IPO in the Mexican Bolsa (BMV) and NYSE.

1999 Campi, enters into the chicken market in the South of Mexico.

2001 Nochistongo y Simón Bolivar poultry plants and stars operation in Gómez Palacio, Durango.

2005 Avícola Sanjor Group.

2006 Most of the assets and inventories of Del Mezquital to start a new complex located inHermosillo, Sonora.

2007 Starts the sales of turkey and beef value added products, increases the production capacityof table eggs.Assets of a balanced feed mill and a soybean processing plant from Productora deAlimentos Pecuarios de Nuevo Leon.Assets of Avi Carnes Monterrey a chicken processing plant.

Trosi de Carnes with a facility located in Monterrey, Nuevo Leon (produces and sellsprocessed beef and chicken).O.K. Industries based in Arkansas and Oklahoma.

Source: Company data, Actinver.

2011

Origins

Expansion

1993

Acquisitions

2009

6

Bachoco has been able to grow its market share in t he chicken industry both organically and through opportunistic acquisitions. During a difficult 2011, when margins were squeezed and many companies suffered, Bachoco invested around USD100 million in acquisitions. This trend is expected to continue.

Bachoco faces strong competition in the US from oth er chicken producers in all product lines . The top two companies in the US command a 39% market share and the top ten have a 75%. Bachoco’s subsidiary OK Industries has a 2% market share in the US concentrated in Arkansas and Nebraska.

OK Industries produces 100% of chicken products . It operates under OK Foods brand in the US, and exports mainly to Russia, China and Mexico and sold to differ-ent restaurant chains in the US. The company currently operates at 90% capacity and represents more than 20% of Bachoco’s sales. With this acquisition, Bachoco expanded its chicken capacity around 25%.

Business lines

1) Chicken

Bachoco ’s chicken commercialization process is divided int o 6 categories:

0.00

5.00

10.00

15.00

20.00

25.00

30.00

050,000

100,000150,000200,000250,000300,000350,000400,000

1T

08

2T

08

3T

08

4T

08

1T

09

2T

09

3T

09

4T

09

1T

10

2T

10

3T

10

4T

10

1T

11

2T

11

3T

11

4T

11

1T

12

2T

12

Chicken

Volume Price

Source: Company data, Actinver

Year Mexico

2008 31%

2008 31%

2009 33%

2010 35%

2011 35%

Source: Company Data, Actinver

Chicken Market Share

Bachoco had 22,473 employees in Mexico and 2,853 in the U.S.

Characteristics Sales %Primarily sold to w holesalersIf revenue increases, sales decreaseAlso sold to independent slaughterhouses in the southeastSold entire, ready to cookSold directly to rosticerías and supermarketsLow -price product and high-quality fast foodFresh chicken partsSold in trays or in bulkMainly sold to supermarkets,franchise fast-food and institutional food-service industriesOrdinarily sold to customers w ithout any packaging or identif ication of the producerPrimarily sold in the Midw estSold entire, gutted and max. 48 hrs after deathMarinated, breaded, pre-cooked or seasoned entire chicken or cutsSold in trays or in bulkSupermarkets, institutional and fast-food chains are the main customersEntire fresh chicken sold w ith packed offals.Sold through retail chainsBrand image

Public Market Chicken

14%

Value-added products

9%

Supermarket Chicken

5%

Live Chicken 29%

Rotisserie 27%

Chicken Parts 16%

7

2) Table egg business line

Table egg represents 7% of revenues and is sold in two presentations: bulk and package. Bulk is distributed from wholesalers to retailers in 360 egg cases. Package presentation is sold in 12, 18 and 24 egg packages through supermarkets.

3) Balance Feed

This segment represents 7% of revenues. Bachoco consumes most of its bal-anced feed production. It has 16 balanced feed facilities in Mexico, 4 of them sell to third parties.

4) Other business lines

Includes live swine, sales of value added turkey an d beef products, and other by-products (approximately 4% of revenues). Sales of value-added beef have grown due to the acquisition of Trosi in 2011.

Management

Bachoco was founded by Javier, Alfonso, Juan and Enrique Robinson Bours Almada in 1952 and the family still controls the company. Non of the family members works in the company; however the Chairman is Francisco Javier R obinson Bours Castelo.

Francisco Javier Robinson Bours Castelo is Chairman of the board since 2002, suc-ceeding the founder Enrique. He has a degree in civil engineering. He is also the Chairman of the Board of Megacable Holdings, S.A.B. de C.V.

The CEO Rodolfo Ramos Arvizu joined Bachoco in 1980. He previously served as a technical director, leading the quality control in egg and poultry administration. He has an undergraduate degree in agronomy.

The COO Ernesto Salmón Castelo joined Bachoco in 1991 and took this position in 2000. He previously worked in Gamesa, in Bachoco as sales executive in Sonora, manager in the processing plant at Celaya and manager in the northeast and south-east divisions. He has a degree in chemical engineering from and an MBA from ITESM.

The CFO Daniel Salazar joined Bachoco in 2000. He previously served as comptrol-ler and finance manager. Prior jobs include CFO of Grupo Covarrubias and comp-troller of Negromex. He is a CPA and has an MBA from ITESM.

Shareholder Structure

The Robinson Bours family own 82.8% of Bachoco. Bachoco was listed in 1997 on both the Mexican Stock Exchange and the New York Stock Exchange. The equity stake of the family is in two trusts and the 17.2% of float is distributed between the NYSE (9.60%) and the Mexican Bolsa (7.65%).

0.002.004.006.008.0010.0012.0014.0016.0018.0020.00

30,00031,00032,00033,00034,00035,00036,00037,00038,000

1T08

2T08

3T08

4T08

1T09

2T09

3T09

4T09

1T10

2T10

3T10

4T10

1T11

2T11

3T11

4T11

1T12

2T12

Egg

Volume Price

Source: Company data, Actinver

Rodolfo Ramos Arvizu Chief Executive Officer

Paul FoxChief Executive Officer, US Operations

Daniel Salazar Ferrer Chief Financial Officer

David Gastelum Cazeres Director of sales

José Luis López Lepe Director of personnel

Ernesto Salomon Castelo Director of operations

Andrés Morales Astiazarán Director of marketing

Marco Antonio Esparza Serrano Comptroller Director

Alejandro Elías Calles Gutiérrez Director of PurchasingSource: Company data, Actinver.

Board of Directors

Shares (000's)

Position

Control trust 312,000 52.0%Family trust 184,500 30.8%Mexican Bolsa 57,600 9.6%NYSE 45,900 7.7%Total 600,000 100.0%Source: Company data, Actinver

Ownership Structure

0.00

1.00

2.00

3.00

4.00

5.00

6.00

0

20,000

40,000

60,000

80,000

100,000

120,000

1T08

2T08

3T08

4T08

1T09

2T09

3T09

4T09

1T10

2T10

3T10

4T10

1T11

2T11

3T11

4T11

1T12

2T12

Balanced feed

Volume Price

Source: Company data, Actinver

8

Dividends

The company regularly pays cash dividends (see below).

Risks

Volatility in raw material prices. Bachoco’s main production costs are balanced feed, which depends on international corn and soybean prices. The company is affili-ated to ASERCA, a Mexican government sponsored program, which allows it to hedge its grains needs. Bachoco usually hedges itself for the next 3 to 6 months which exposes the company to potential increases in grain futures after this period.

FX volatility. Bachoco hedges its exchange rate exposure through financial deriva-tive instruments over a 6-month period. Around 70% of Bachoco’s cost of goods are grains, which are USD denominated. The company also financed part of the O.K. Industries acquisition with a USD 74 million dollar denominated debt. However, this is credit was refinanced into pesos.

Poultry diseases. The H7N3 virus affected some chicken farms located in the State of Jalisco. As a result, retailers have increased chicken prices in a significant way. However, it seems that the aviar flu has been controlled by the local authorities. The company has not been affected by this disease due to its strict bio-security policies.

Operations in the US market. Bachoco entered to the US through the OK Industries acquisition. However, this market behaves in a very different way as consumers pre-fer frozen foods and value added products. Also the US market is more mature and fragmented than the Mexican one. Most of the farms in the US are leased for chicken production. Any change in the contracts or in consumption preferences can affect the company’s operations.

Share performance

Bachoco’s shares were up 56% from January 2009 to June 2012 with an aver-age daily traded volume of 100,312 shares. The share price was only down 13% in 2011 as a result of the European crisis and high raw materials volatility. In 1H12 the price rose 13.4%.

The average daily traded volume has increased from 29,598 shares in 2009 to 131,266 in 2011. In 1H12, the average daily volume reached 204,707.

60

80

100

120

140

160

180

Jan-

09

May

-09

Sep

-09

Jan-

10

May

-10

Sep

-10

Jan-

11

May

-11

Sep

-11

Jan-

12

May

-12

Relative performance (2009 = 100)

Mexbol Bachoco

Source: Bloomber, Actinver

2009 2010 2011 2012Dividends per share (MP) 0.40 0.42 0.50 0.50Paid dividends (million) 250.0 250.1 299.9 300.0Pay-out Ratio N.A. 31.4% 15.1% 191.0%Net Revenue (one year earlier) (879.0) 797.6 1983.4 157.0Source: Company Data

1ADS= 12 shares

9

Financial results

2009

Revenues increased 15.6% YoY to MP 23,264 million as a result of an 17.8% in-crease in chicken (4.6% in volume and 12.6% in price), 12% in egg (-0.2% in volume and 12% increase in price), and flat sales in balance feed (decrease of 8.9% in volu-me and increase of 9.3% in price). Cost of sales grew 10.5% due to higher raw mate-rials prices, in particular soybeans. Gross margin expanded 380 bps to 16.9%. Oper-ating income rose 514% to MP 1,414 million. Net income was MP 798 million, which represent an EPS of MP 1.35 (USD 16 per ADS).

2010

Net sales were up 6.2% YoY to 24,716 million as a result of increases of 11% in chicken (7.2% in volume and 3.3% in price), 27% in pig (9.3% in volume and 16% in price) which was partially offset by an 11% decrease in egg (-1.0% in volume and –9.9% in price) and -6% in balance feed (-3.1% in volume and –2.8% in price). This year was marked by a stable demand in chicken and oversupply in eggs. Raw mate-rial prices were more stable than in 2009.

Operating income reached MP 2,463 million as a resu lt of productive efficien-cies and expense control policies. This result is partially attributed to the increase in chicken and pigs sales. The operating margin was 10.0%, which represents 368 bps expansion. Net income was MP 1,983 million, up 148.7% as a result of lower financial costs.

2011

Revenues rose 12.2% YoY due to a 2.6% prices adjust ment and a 9.0% higher volume. Chicken sales were up 12.2% as a result of a 2.9% price increase and a 9.0% volume growth. The acquisition of OK industries in November 2011 was the main factor behind the volume increase.

Table eggs sales decreased 0.8% due mainly to a 5.7 % price hike which was more than offset by a 6.1% volume decline. The latter was due to less production in the Mexicali facility which was affected by an earthquake in April 2010.

Balanced feed sales advanced 34.2% supported by a 1 6.0% price adjustment and a 15.7% volume expansion. This recovery comes after a couple of years of significant increases in production costs.

EBITDA fell 76.7% given higher commodity prices. This weak operating perfor-mance together with higher financial costs (Bachoco contracted a one-year bank credit of US$75 million dollars to pay for the acquisition of OK Industries) translated ina 92% net income decline.

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

26.0

28.0

0.0

50,000.0

100,000.0

150,000.0

200,000.0

250,000.0

300,000.0

350,000.0

1T09

2T09

3T09

4T09

1T10

2T10

3T10

4T10

1T11

2T11

3T11

4T11

1T12

2T12

Average volume and price (right axis)

AVERAGE VOLUME AVERAGE PRICE

Max Min CloseOne year

returnAccumulated return (2009)

2009 26.00 11.85 25.00 56.3% 56.3%

2010 26.99 18.40 25.55 2.2% 59.8%

2011 27.84 20.32 22.30 -12.7% 39.5%

6M12 25.10 20.59 24.90 13.4% 55.7%

Source: Bloomberg

Price performance

2010 2011 ∆%∆%∆%∆%Net Sales 24,716 27,735 12.22%Cost of sales (19,501) (24,773) 27.04%Gross profit 5,215 2,962 -43.20%Gross margin 21.1% 10.7% -1,042.0 bpsEBITDA 3,156 736 -76.68%EBITDA Margin 12.8% 2.7% -1,011.4 bpsNet majority income 1,983 157 -92.08%Source: Infosel, Company data, Actinver

Figures in million pesos

2008 2009 ∆%∆%∆%∆%Net Sales 20,125 23,264 15.6%Cost of sales (17,483) (19,327) 10.5%Gross profit 2,643 3,936 48.9%Gross margin 13.1% 16.9% 378.7 bpsEBITDA 838 2,079 148.2%EBITDA Margin 4.2% 8.9% 477.5 bpsNet majority income (879) 798 90.8%Source: Infosel, Company data, Actinver

Figures in million pesos

2009 2010 ∆%∆%∆%∆%Net Sales 23,264 24,716 6.24%Cost of sales (19,327) (19,501) 0.90%Gross profit 3,936 5,215 32.49%Gross margin 16.9% 21.1% 417.9 bpsEBITDA 2,079 3,156 0.52EBITDA Margin 8.9% 12.8% 382.9 bpsNet majority income 798 1,983 148.7%Source: Infosel, Company data, Actinver

Figures in million pesos

10

Despite two acquisitions made in 2011, Bachoco´s fi nancial condition re-mained strong. The cash position was MP 3.0 billion (vs. 4.2 billion in 2010) and total debt with cost reached MP 1.9 billion.

1H12 Results

Bachoco’s 1H12 sales were up 48% to MP 18,742 milli on as a result of the inte-gration of OK Industries and higher prices in the M exican market.

Chicken sales grew 48% to MP 15,902 million mainly to the integration of OK Indus-tries. Egg revenue rose 21% to MP 1,181 million with volume and prices rising 6% and 15%, respectively, due to the reinstallations of Mexicali farms. Balance feed sales were up 5% to MP 947 million. Other business lines advanced 38% due to a significant growth in value-added beef products resulting from the integration of a newly acquired plant located in Monterrey and higher by-products sales.

The gross profit increased 65% to MP 2,862 million. The gross margin was 15%.

Operating profit grew 254% YoY to MP 1,203 million vs. MP 339 million in 1H11 due mainly by the improvement of pricing conditions. The operating margin increased from 2.7% 1H11 to 6.4% 1H12 an expansion of 374 bps.

Net income improved 231% to MP 977 million.

The company maintained high cash levels to face the volatility of raw material costs . Cash and cash Equivalents grew 25% YoY to 3,804 million and represent 15% of total assets.

The company recently issued a MP 1,500 million bond in Mexico with the pur-pose to refinance the USD denominated bank loan use d to acquire OK Indus-tries. This new instrument pays an interest rate of TIIE +60 bps. It will have a maturi-ty period of 5 years. HR Ratings rated it HRAA and Fitch AA + (mex).

1H11 1H12 ∆%∆%∆%∆%Net Sales 12,659 18,742 48.05%Cost of sales (10,931) (15,880) 45.28%Gross profit 1,728 2,862 65.57%Gross margin 13.7% 15.3% 161.5 bpsEBITDA 686 1,653 140.91%EBITDA Margin 5.4% 8.8% 340 bpsNet majority income 292 977 234.24%Source: Infosel, Company data, Actinver

Figures in million pesos

11

PROYECTIONS and PROSPECTS

Income Statement

We expect Bachoco’s EBITDA to rise at 49.5% CAGR du ring the 2012-2015E period. The main drivers are the following:

■ The Mexican population increased at a 1.4% annual r ate during the 2000-2010 period to 112 million, according to INEGI . We expect a similar annual growth rate going forward, which should bring the Mexican population to 129 mil-lion in 2020.

■ We expect the Mexican GDP to rise at a 3.5% CAGR in real terms (around 7% nominal) during the 2012-2015E period, which means that the per capita GDP will likely rise nearly 6%.

■ Per capita chicken consumption increased at a 1.3% CAGR during the 2005-2011 period to 26.1 kilos due mainly to a higher di sposable income , the pro-tein substitution process (more chicken, less egg) and the population growth. We believe that there is ample room for expansion given that this figure reached 44 kilos in the US at the end of 2011. For this reason, we anticipate that chicken con-sumption will expand at a 1.3% CAGR during the next four years to reach 27.49 kilos in 2015E. Bachoco’s chicken volume will likely rise at an organic 4.0% CAGR as we are expecting the company to expand its current market share.

■ We anticipate that the per capita egg consumption w ill rise at a 0.3% CAGR to reach 22.7 kilos. Bachoco’s volume should rise at a similar rate given that we see no significant changes in the company’s egg market share.

■ The company’s 2012 revenue should benefit from acqu isitions of 2011 . The company purchased Trosi de Carne in Mexico and OK Foods, a vertically integra-ted U.S. company with headquarters in Fort Smith, Arkansas. Ok Indsutries contri-buted with 16% of total revenue in 4Q11 and 20% in 1H12. We expect it to repre-sent 22% of total revenues during 2012.

■ Based on these assumptions, we expect Bachoco’s rev enues to rise at 13.4% CAGR. However, most of this growth will take place in 2012 as a result of the two aforementioned acquisitions.

■ We expect the cost of sales to advance at a 12.5% C AGR during the 2012-2015E period. However, most of this growth should take place in 2013 as the company does not have any more hedges for that period. The main component of the cost of sales is grains. We believe that grain prices could continue to go up due to several external factors as weather, volume harvested, transportation costs and government policies.

■ Bachoco’s profitability levels should improve in 20 12 because of a more favorable base of comparison (in 2011 the company was affected by higher raw material prices) and synergies with OK Industries and Trosi de Carne. We expect an EBITDA margin of 7.9% in 2012 and decrease to 7.8% in 2015E.

■ Net profit should improve at a 74.0% CAGR to MP 2,0 35 million in 2015E . The net margin should stay around 4% during the 2012-2015 period.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2009

2010

2011

2012

E

2013

E

2014

E

2015

E

EBITDA and EBITDA Margin (Right axis)

EBITDA EBITDA MarginSource: Company data, Actinver

0

10,000

20,000

30,000

40,000

50,000

2009 2010 2011 2012E 2013E 2014E 2015E

Net Revenues

Source: Company data, Actinver.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

0

500

1,000

1,500

2,000

2,500

3,000

2009 2010 2011 2012E 2013E 2014E 2015EOperating profit Operating Margin

Source: Company data, Actinver.

Operating profit and operating margin (right axis)

12

Balance Sheet

The company has strong cash levels to face the vola tility in raw materials. This line represents 13% of total assets. We are anticipating that Bachoco will continue generating and accumulating cash during the next periods. We believe that the cash will increase 21.4% CAGR to MP 6,600 million in 2015E.

PP&E represents around 40% of total assets for the company, which should remain unchanged during the next few years. However, we do not rule out the pos-sibility that Bachoco continues acquiring smaller companies or expanding its facili-ties.

We believe that short term liabilities will decreas e and the long term liabilities will increase for the second half of the year. The company issued a MP 1,500 million bond to refinance the bank loan of US 75 million used to acquire OK Indus-tries. We expect that the liabilities stays equal for the 2012-2015E period.

We are estimating that the net debt will remain neg ative due to strong cash levels generation. This leads to a negative Net Debt to EBITDA ratio that goes from 0.6 x in 2012E to 1.2x in 2015.

Free Cash Flow

The company’s main inflow is the EBITDA generation that we already dis-cussed before. The main outflows are the following:

The working capital cycle is negative due that the accounts receivable and inventories increases year over year. This means that the company should im-prove their collection processes.

Capex will be around MP 982 million in 2012 (repres enting 3% of sales) and MP 1.0 billion in 2013 . We expect the capex figure to remain at around MP 1 billion per year going forward.

The tax rate will be 21.6% during the next few year s. We believe that most of the accounting taxes are cash taxes.

Bachoco should generate free cash flow of around MP 1,000 million per year . We believe that the company will continue paying di vidends for the incoming years . We are estimating dividends for MP 360 million in 2013, around 20% of the projected 2012E net income.

We expect the company to maintain a healthy balance sheet with a net cash position during the next few years . In our model we are assuming that the compa-ny accumulates cash. However, we do not rule out the possibility that Bachoco un-dertakes selective acquisitions in both Mexico and the US.

0

200

400

600

800

1,000

1,200

2009

2010

2011

2012

E

2013

E

2014

E

2015

E

CAPEX Estimated (million pesos)

Source: Company data, Actinver

FREE CASH FLOW 2011 2012E 2013E 2014E 2015E 2011 2012E 2013E 2014E 2015EEBITDA 716 3,014 3,070 3,310 3,577 (77%) 321% 2% 8% 8%Working Capital Changes (948) (854) (630) (722) (800) 55% (10%) (26%) 15% 11%Capex (662) (982) (1,020) (1,040) (1,080) 18% 48% N.A. 2% 4%Cash Taxes (22) (198) (334) (367) (404) N.A. 815% 69% 10% 10%FCFE (915) 981 1,086 1,181 1,294 (147%) (207%) 11% 9% 10%Net Interests 132 123 153 187 227 23% (7%) 24% 22% 22%Dividends (300) (310) (360) (400) (440) N.A. N.A. N.A. N.A. N.A.NET FREE CASH FLOW (1,083) 794 878 968 1,081 (160%) (173%) 11% 10% 12%Source: Actinver

13

VALUATION

We set a 12-month target price of MP 33.1 per share using a target EV/EBITDA multiple of 5.7x, which is in line with the median of the US food industry, ac-cording to our valuation table . The potential return is 35.3% against current levels. If we used a target P/E of 10.9x, we would obtain a target price of MP 30.6. However, we prefer to use the target EV/EBITDA multiple mainly because the EBITDA is less volatile that the net income.

The companies that we selected is our valuation table of the food industry are the most comparable to Bachoco in terms of market capitalization and business model. Despite the fact that Tyson Food’s market cap is higher than Bachoco’s, we also included this company in our table due mostly to the similarities of its business lines with Bachoco’s.

Price Shares Mkt. Cap EV Return Return P/BV(Local) Outsdng (Local) (USD) YTD YoY actual 2012E 2013E a ctual actual 2012E 2013E

NationalBachoco BACHOCO.MM 25.09 600.00 15,054 13,604 14.79 3.84 7.8x 4.4x 4.1x 0.9x 17. 7x 8.6x 8.9xBimbo BIMBOA.MM 30.40 4,703.20 142,977 186,148 7.30 23.23 12.4x 11.0x 9.6x 2.9x 31.2x 22.9x 19.4xGruma GRUMAB.MM 34.93 563.65 19,688 36,500 32.31 51.80 6.7x 5.6x 5.6x 1.4x 12.4x 10.6x 9.8xHerdez HERDEZ.MM 32.20 432.00 13,910 16,633 33.11 34.46 9.3x 9.2x 8.2x 3.7x 17.7x 17.7x 15.5xMedian 9.3x 9.2x 8.2x 2.9x 17.7x 17.7x 15.5xAverage 9.5x 8.6x 7.8x 2.7x 20.4x 17.1x 14.9x

InternationalCal Mine CALM.US 41.85 23.92 1,001 817 18.23 31.32 5.4x 7.8x 5.6x 2.1x 16.0x 16.5x 15.2xDole Food DOLE.US 14.10 88.95 1,254 2,822 63.01 48.42 8.3x 7.7x 7.6x 1.4x 21.3x 10.5x 9.9xMaple Leaf MFI.CA 11.51 139.52 1,612 2,737 7.42 1.27 7.5x 6.1x 5.7x 1.9x 12.9x 10.5x 9.7xPilgrim PILGRIM.US 5.27 221.42 1,363 2,547 -5.55 60.96 15.7x 13.8x 7.1x 1.6x N.A. 22.0x 13.7xTyson Foods TYSON.US 16.39 370.00 5,930 7,600 -20.08 -2.37 5.4x 5.6x 5.2x 1.0x 10.3x 10.8x 10.9xMedian 7.5x 7.7x 5.7x 1.6x 14.5x 10.8x 10.9xAverage 8.5x 8.2x 6.2x 1.6x 15.1x 14.1x 11.9x

National & InternationalMedian 7.9x 7.7x 6.4x 1.7x 16.0x 13.6x 12.3xAverage 8.8x 8.3x 6.8x 2.0x 17.4x 15.2x 13.0xSource: Bloomberg, Actinver

Food Peers Ticker EV/EBITDA P/E

EV / EBITDA 2013EEBITDA 3,070Target EV/EBITDA 5.7xNet debt (2,439)Stockholders' equity 19,513Majority interest 19,445Market value 19,872Shares outstanding 600Fair value / share (MXN) 33.12Current price (MXN) 25.09Upside to fair value 32.0%+ Dividend yield 2012 2.3%Total upside potential 34.3%Source: Actinver.

P / E 2013EEarnings 12M 1,686Target Fwd P/E 10.9xFair value / share (MXN) 30.62Current price (MXN) 25.09Upside to fair value 22.1%+ Dividend yield 2012 2.3%Total upside potential 24.4%Source: Actinver.

4.7x 5.2x 5.7x 6.2x 6.7x15% 31.6 34.6 37.5 40.4 43.410% 30.4 33.2 36.0 38.9 41.75% 29.2 31.9 34.6 37.3 40.00% 28.0 30.6 33.1 35.7 38.2-5% 26.8 29.2 31.7 34.1 36.5

-10% 25.6 27.9 30.2 32.5 34.8-15% 24.4 26.6 28.7 30.9 33.1

EV/EBITDA 2013E Target Multiple

Non

-Exp

ecte

d C

hang

e in

EB

ITD

A

9.9x 10.4x 10.9x 11.4x 11.9x15% 32.0 33.6 35.2 36.8 38.410% 30.6 32.1 33.7 35.2 36.85% 29.2 30.7 32.2 33.6 35.10% 27.8 29.2 30.6 32.0 33.4-5% 26.4 27.8 29.1 30.4 31.8

-10% 25.0 26.3 27.6 28.8 30.1-15% 23.6 24.8 26.0 27.2 28.4

PE 2013E Target Multiple

Non

-Exp

ecte

d C

hang

e in

Ear

ning

s

14

0.0x

4.0x

8.0x

12.0x

16.0x

20.0x

24.0x

28.0x

32.0x

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12

Historic Fwd EV/EBITDA multiple

Source: Bloomberg

0.0x

20.0x

40.0x

60.0x

80.0x

100.0x

120.0x

140.0x

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12

Historic Fwd P/E multiple

Source: Bloomberg

Historical multiples

Bachoco’s 2013E EV/EBITDA of 4.1x also represents a 51% discount vs. its 3-year average of 8.5x. The projected P/E of 8.9x is nearly one half its 3-year average of 18.9x.

15

INDUSTRIAS BACHOCO, S.A.B. DE C.V. - Operating Mode l(Figures in Millions of Pesos)

2010 2011 2012E 2013E 2014E 2015E

Net Revenues 24,803 27,738 38,173 40,399 42,990 45,859

Sales by Product 2010 2011 2012E 2013E 2014E 2015E

Chicken 20,157 22,626 31,806 33,906 36,214 38,792

Volume 984 1,073 1,352 1,406 1,462 1,521

Change 7.2% 9.0% 26.0% 4.0% 4.0% 4.0%

Avg. Price /Ton 20.5 21.1 23.5 24.1 24.8 25.5

Change 3.2% 3.0% 11.5% 2.5% 2.7% 3.0%

Egg 2,096 2,073 2,742 2,946 3,065 3,189

Volume 142 133 149 155 158 161

Chg. (1.0%) (6.1%) 11.9% 3.7% 2.0% 2.0%

Avg. Price /Ton 14.8 15.6 18.4 19.1 19.4 19.8

Chg. (10.2%) 5.4% 18.2% 3.6% 2.0% 2.0%

Balanced Feed 1,383 1,856 2,200 2,070 2,154 2,241

Volume 328 379 388 376 384 391

Chg. (3.1%) 15.7% 2.3% (3.0%) 2.0% 2.0%

Avg. Price /Ton 4.2 4.9 5.7 5.5 5.6 5.7

Chg. (2.7%) 16.1% 15.9% (3.0%) 2.0% 2.0%

Other 1,167 1,177 1,425 1,477 1,557 1,637

(YoY Change) 2010 2011 2012E 2013E 2014E 2015E

Net Revenues 6.6% 11.8% 37.6% 5.8% 6.4% 6.7%

Chicken 10.6% 12.2% 40.6% 6.6% 6.8% 7.1%

Egg 7.2% 9.0% 26.0% 4.0% 4.0% 4.0%

Balanced Feed (5.7%) 34.2% 18.5% (5.9%) 4.0% 4.0%

Other (5.0%) 0.9% 21.0% 3.7% 5.4% 5.1%

Breakdown of Sales by Product 2010 2011 2012E 2013E 2014 E 2015E

Net Revenues 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Chicken 81.3% 81.6% 83.3% 83.9% 84.2% 84.6%

Egg 8.5% 7.5% 7.2% 7.3% 7.1% 7.0%

Balanced Feed 5.6% 6.7% 5.8% 5.1% 5.0% 4.9%

Other 4.7% 4.2% 3.7% 3.7% 3.6% 3.6%

Source: Company, Actinver

16

INDUSTRIAS BACHOCO, S.A.B. DE C.V.(Figures in Millions of Pesos)INCOME STATEMENT 2011 2012E 2013E 2014E 2015E 2011 2012E 2013E 2014E 2015ESales 27,738 38,173 40,399 42,990 45,859 12% 38% 6% 6% 7% Cost of Sales (24,817) (32,873) (35,026) (37,186) (39,622) 27% 32% 7% 6% 7%Gross Profit 2,921 5,300 5,373 5,804 6,237 (44%) 81% 1% 8% 7%Gross Margin 10.5% 13.9% 13.3% 13.5% 13.6% General Expenses (2,980) (3,237) (3,291) (3,530) (3,752) 9% 9% 2% 7% 6%Profit Before Other Income and Expenses (60) 2,063 2,082 2,273 2,485 (102%) (3,563%) 1% 9% 9%Margin (0.2%) 5.4% 5.2% 5.3% 5.4% Other Income and Expenses (18) (51) (22) (38) (54) (86%) 189% (57%) 73% 42%Operating Profit (77) 2,012 2,060 2,235 2,431 (103%) (2,703%) 2% 8% 9%Operating Margin (0.3%) 5.3% 5.1% 5.2% 5.3% Depreciation and Amortization (775) (951) (988) (1,037) (1,092) 16% 23% 4% 5% 5%EBITDA 716 3,014 3,070 3,310 3,577 (77%) 321% 2% 8% 8%EBITDA Margin 2.6% 7.9% 7.6% 7.7% 7.8%Financial Gain 281 247 260 287 320 18% (12%) 5% 10% 12%Financial Cost (102) (33) (174) (164) (158) (12%) (68%) 428% (6%) (4%)Pre-Tax Profit 101 2,229 2,150 2,361 2,596 (96%) 2,102% (4%) 10% 10% Taxes and Profit Sharing 29 (482) (464) (510) (561) (106%) (1,755%) (4%) 10% 10% Tax and Profit Sharing Rate (28.8%) 21.6% 21.6% 21.6% 21.6%Profit from Continuing Operations 130 1,747 1,686 1,851 2,035 (93%) 1,240% (4%) 10% 10% Discontinued Operations 0 (3) 0 0 0 N.A. N.A. N.A. N.A. N.A.Net Profit Before Minorities 130 1,744 1,686 1,851 2,035 (93%) 1,238% (3%) 10% 10% Minority Interest (3) 0 0 0 0 N.A. N.A. N.A. N.A. N.A.Net Profit 128 1,744 1,686 1,851 2,035 (94%) 1,266% (3%) 10% 10%N° of Shares 600 600 600 600 600 (0%) 0% 0% 0% 0%EPS MP 0.21 MP 2.91 MP 2.81 MP 3.09 MP 3.39 (94%) 1,266% (3%) 10% 10%Source: Actinver

BALANCE SHEET 2011 2012E 2013E 2014E 2015E 2011 2012E 2013E 2014E 2015ETOTAL ASSETS 23,390 26,706 28,100 29,495 31,129 10% 14% 5% 5% 6% Current Assets 11,862 12,542 13,664 14,816 16,222 15% 6% 9% 8% 9% Cash and Temporary Investments 3,036 4,550 5,200 5,800 6,600 (27%) 50% 14% 12% 14% Long Term Assets 11,528 14,164 14,436 14,679 14,907 6% 23% 2% 2% 2% Property, Plant & Equipment 11,032 11,710 11,802 11,865 11,912 4% 6% 1% 1% 0% LT Biological Assets 0 938 998 1,058 1,118 N.A. N.A. 6% 6% 6% Intangible Assets 301 301 301 301 301 0% 0% 0% 0% 0% Other Long Term Assets 195 1,215 1,335 1,455 1,575 N.A. N.A. 10% 9% 8%TOTAL LIABILITIES 7,195 8,518 8,587 8,531 8,569 49% 18% 1% (1%) 0% Current Liabilities 4,450 4,063 4,123 4,059 4,089 105% (9%) 1% (2%) 1% Long Term Liabilities 415 4,456 4,464 4,472 4,480 (18%) 973% 0% 0% 0%TOTAL DEBT 1,879 2,877 2,761 2,499 2,319 190% 53% (4%) (9%) (7%)NET DEBT (1,157) (1,673) (2,439) (3,301) (4,281) (67%) 45% 46% 35% 30%TOTAL CAPITAL 16,194 18,188 19,513 20,965 22,560 (1%) 12% 7% 7% 8% Shareholder's Equity 16,140 18,124 19,445 20,891 22,481 (1%) 12% 7% 7% 8% Minority Interest 54 64 68 73 79 3% 18% 7% 7% 8%Source: Actinver

17

CASH FLOW STATEMENT 2011 2012E 2013E 2014E 2015E 2011 2012 E 2013E 2014E 2015EPRE-TAX PROFIT 101 2,226 2,150 2,361 2,596 (96%) 2,098% (3%) 10% 10%Investment Activity Related Items 781 785 699 721 744 16% 0% (11%) 3% 3% Depreciation and Amortization 778 994 988 1,037 1,092 12% 28% (1%) 5% 5% Gain (Loss) on Sale of P, P & E 5 (17) (59) (59) (59) (96%) (433%) 241% 0% 0%Financing Activities 255 75 88 80 73 248% (71%) 17% (9%) (9%)Pre-Tax Cash Flow 1,920 3,621 4,027 4,266 4,535 (52%) 89% 11% 6% 6%Working Capital Changes (948) (854) (630) (722) (800) 55% (10%) (26%) 15% 11% Decr. (Inc.) in Accounts Receivable (178) 121 (79) (93) (103) 199% (168%) (165%) 18% 11% Decr. (Inc.) in Inventories (873) (865) (316) (374) (414) (2,910%) (1%) (63%) 18% 11% Decr. (Inc.) en Other Accounts Rec. and Other Assets0 (60) (78) (85) (90) N.A. N.A. 29% 9% 6% Incr. (Decr.) in Suppliers 594 (98) 131 155 172 (573%) (116%) (234%) 18% 11% Incr. (Decr.) in Other Liabilities (491) 273 45 42 39 (2,058%) (156%) (83%) (7%) (7%) Taxes Paid or Accrued 0 (225) (334) (367) (404) N.A. N.A. 48% 10% 10%Cash Flow from Operations (2,123) 2,767 3,396 3,544 3,735 416% (230%) 23% 4% 5%Cash Flow from Investment (2,123) (1,581) (2,183) (2,203) (2,243) 416% (26%) 38% 1% 2% CAPEX (662) (982) (1,020) (1,040) (1,080) 18% 48% 4% 2% 4% Sale of P, P & E (84) 35 37 37 37 N.A. N.A. N.A. N.A. N.A. Other Items (108) (727) (1,200) (1,200) (1,200) 83% 573% 65% 0% 0%Cash Flow from Financing 919 328 (564) (741) (693) (242%) (64%) (272%) 31% (7%) Dividends Paid (300) (310) (360) (400) (440) N.A. N.A. N.A. N.A. N.A. Interests Paid 0 (75) (88) (80) (73) N.A. N.A. 17% (9%) (9%) Other Items 2 (316) 0 0 0 (124%) (20,805%) (100%) N.A. N.A.Net Incr. (Decr.) in Cash and T.I. (1,141) 1,514 650 600 800 (173%) (233%) (57%) (8%) 33%Net Cash and T.I. Beginning of Period 4,177 3,036 4,550 5,200 5,800 64% (27%) 50% 14% 12%Net Cash and T.I. End of Period 3,036 4,550 5,200 5,800 6,600 (27%) 50% 14% 12% 14%Source: Actinver

FINANCIAL RATIOS 2011 2012E 2013E 2014E 2015ELeverageNet Debt / EBITDA (x) (1.6x) (0.6x) (0.8x) (1.0x) (1.2x)ST Debt / Total Debt (x) 78% 35% 32% 25% 19%Interest CoverageEBITDA / Int. Paid (x) 11.3x 40.2x 35.0x 41.4x 49.1xEBITDA - Capex / Int. Paid (x) 0.9x 27.1x 23.3x 28.4x 34.3xOper. Profit / Int. Paid (x) (1.2x) 26.8x 23.5x 28.0x 33.4xInvestmentCAPEX / Sales 2% 3% 3% 2% 2%CAPEX / Depreciation 85% 103% 103% 100% 99%Source: Actinver

18

Research

Pablo Adolfo Riveroll Sánchez Managing Director of Research and Risk

(52) 55 1103-6600

x5800

Jaime Ascencio Economy & Markets (52) 55 1103-6600 x5032 [email protected]

David Foulkes Retail (52) 55 1103-6600 X5045 [email protected]

Eduardo Fonseca Food & Beverages (52) 55 1103-6600 x4122 [email protected]

Martín Lara Telecoms, Media & Financials (52) 55 1103-6600 x5033 [email protected]

Pablo Duarte Conglomerates, Industrial & Mining (52) 55 8173-5200 x80161 [email protected]

Ramón Ortiz Concessions, Construction & Real Estate (52) 55 1103-6600 x5034 [email protected]

José Luis Saiz Analyst Jr. (52) 55 1103-6600 x5023 [email protected]

Roberto Galván Technical Analysis (52) 55 1103 -6600 x5039 [email protected]

Investment Strategy

Ernesto O’Farrill Head, Investment Strategy (52) 55 1103-6645 [email protected]

Sales & Trading

Gerardo Román Head, Sales & Trading (52) 55 1103-6690 [email protected]

Julie Roberts Head, Institutional Sales (210) 298 - 5371 [email protected]

Tulio Chávez Institutional Sales (52) 55 1103-6762 [email protected]

José María Celorio Institutional Sales (52) 55 1103-6606 [email protected]

María Antonia Gutiérrez Institutional Sales (52) 55 1103-6796 [email protected]

19

Disclaimer

Analyst Certification for the following Analysts: Pablo Adolfo Riveroll Sanchez Jaime Ascencio David Foulkes Eduardo Fonseca Martin Lara Pablo Duarte Ramón Ortiz Roberto Galván

The analyst(s) responsible for this report, certifies(y) that the opinion(s) on any of the securities or issuers mentioned in this document, as well as any views or forecasts expressed herein accurately reflect their personal view(s). No part of their compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views contained in this document.

Any of the business units of Grupo Actinver or its affiliates may seek to do business with any company discussed in this research document. Any past or potential future compensation received by Grupo Actinver or any of its affiliates from any issuer mentioned in this report has not had and will not have any effect our analysts’ compensation. However, as for any other employee of Grupo Actinver and its affiliates, our analysts’ compensation is affected by the overall profitability of Grupo Actinver and its affiliates.

Guide to our Rating Methodology Total Expected Return on any security under coverage includes dividends and/or other forms of wealth distribution expected to be implemented by the issuers, in addition to the expected stock price appreciation or depreciation over the next twelve months based on our analysts’ price targets. Analysts uses a wide variety of methods to calculate price targets that, among others, include Discounted Cash Flow models, models based on expected risk-adjusted multiples, Sum-of-Parts valuation techniques, break-up scenarios and relative valuation models. Changes in our price targets and/or our recommendat ions. Companies under coverage are under constant surveillance and as a result of such surveillance our analysts update their models resulting in potential changes to their price targets. Changes in general business conditions potentially affecting either the cost of capital and/or growth prospects of all companies under coverage, or a given industry, or a group of industries are typical triggers for revisions to our price targets and/or recommendations. Other micro- and macroeconomic events could materially affect the overall prospects of an individual company under coverage and, as a result, such event-driven factors could lead to changes in our price targets and/or recommendation of the company affected. Even if our overall expectations for a given company under coverage have not materially changed, our recommendations are subject to revision if the stock price has changed significantly, as it will affect total expected return.

Terms such as "price targets, our price targets, total expected return, analyst's price targets” or any other similar phrase are used in this document as complementary to our recommendation or as a condition that could change in our point of view and, according to article 188 of Securities Market Act, do not imply in any way that Actinver, its agents, or its related companies are in any form providing assurance or guarantee, nor assuming any responsibility for the risks associated with any investment in the discussed securities.

Recommendations for companies, both in the Índice d e Precios y Cotizaciones (IPyC) Index and also not belonging to the index. For stocks, we have three possible recommendations: a) BUY, b) HOLD or c) SELL. A stock classified as BUY is expected to yield returns at least 5% above than that of the IPyC Index. Stocks rated as HOLD are expected to yield returns similar to the IPyC Index, within a range of +5/-5%. Many of the companies within this range are often times solid companies which have reached their potential in a short amount of time and should still be considered as a good investment. Stocks rated as SELL are expected to yield returns below 5% of the IPyC Index.

Rating Distribution as of June 8, 2012

All Companies in the BMV

BUY: 71%

HOLD: 23%

SELL: 6%