Embed Size (px)

Citation preview

A world class convention and exhibition centre for Sydney: Pre-feasibility StudyFinal Report September 2010

Comments and queries can be directed to:

Scott Lennon Partner – PricewaterhouseCoopers T 02 8266 2765 E [email protected]

Brendan Lyon Executive Director – Infrastructure Partnerships Australia T 02 9240 2050 E [email protected]

Kylie Gillett Manager, Industry Affairs – Infrastructure Partnerships Australia T 02 9240 2059 E [email protected]

Disclaimer

This report has been prepared by PricewaterhouseCoopers (PwC) for Infrastructure Partnerships Australia (IPA).

The information, statements, statistics and commentary (together the ‘Information’) contained in this report have been prepared by PwC from material provided by the IPA, and from other industry data from sources external to IPA. PwC may at its absolute discretion, but without being under any obligation to do so, update, amend or supplement this document.

PwC does not express an opinion as to the accuracy or completeness of the information provided, the assumptions made by the parties that provided the information or any conclusions reached by those parties. PwC disclaims any and all liability arising from actions taken in response to this report. PwC disclaims any and all liability for any investment or strategic decisions made as a consequence of information contained in this report. PwC, its employees and any persons associated with the preparation of the enclosed documents are in no way responsible for any errors or omissions in the enclosed document resulting from any inaccuracy, misdescription or incompleteness of the information provided or from assumptions made or opinions reached by the parties that provided Information.

The Information contained in this report has not been subject to an Audit. The information must not be copied, reproduced, distributed, or used, in whole or in part, for any purpose other than detailed in our Engagement Letter without the written permission of IPA and PwC.

1

Contents

1 Executive summary 6

2 Introduction 31

Background 31

Scope of this study 32

3 Rationale for providing convention and exhibition facilities in NSW

33

Role of convention and exhibition facilities 33

Value of business events to the community 34

Rationale for government investment in expanding Sydney’s convention and exhibition facilities

36

4 Current facilities in Sydney 38

Current facilities in Sydney 38

Conventions and exhibitions in Australia 45

Conventions and exhibitions internationally 50

Constraints of current facilities in Sydney 56

Economic implications of these constraints 58

5 Options for new or expanded facilities in Sydney 64

Introduction to options for expansion 64

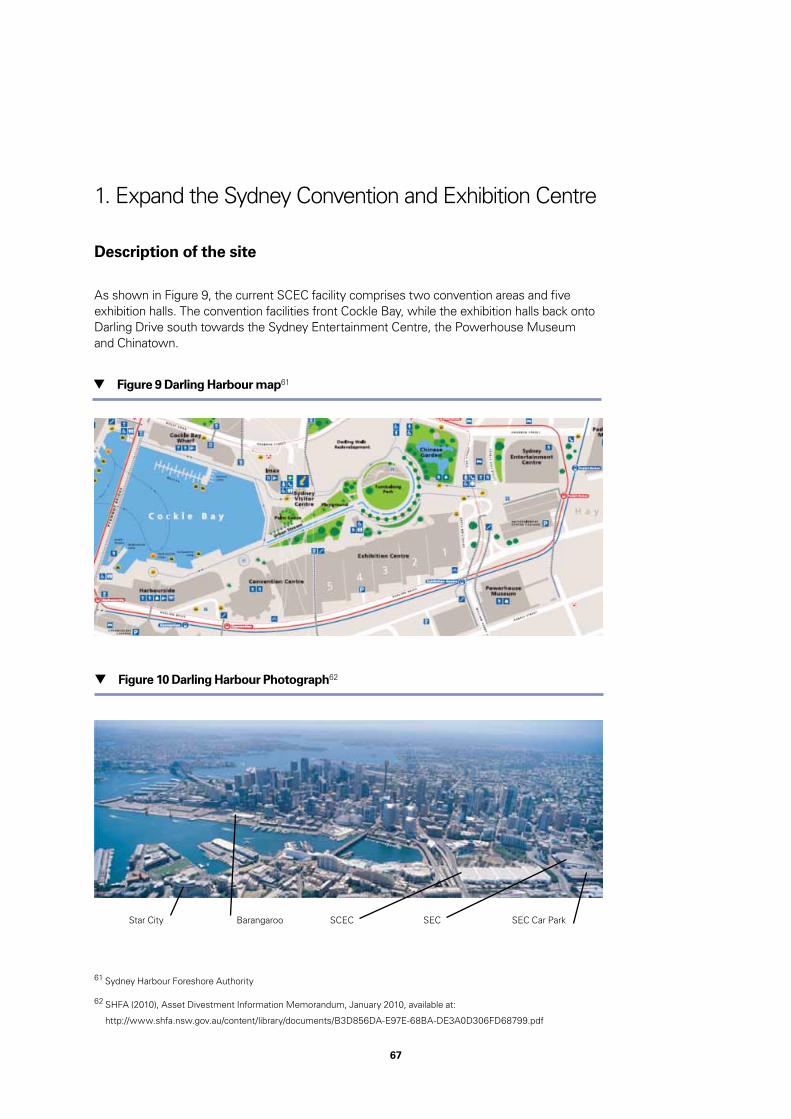

1. Expand the Sydney Convention and Exhibition Centre 67

2. Expansion of Sydney Showground 79

3. Develop airspace over Central Station 80

4. Glebe Island and White Bay 82

5. Barangaroo precinct 83

Assessment of site options 85

Economic benefits of creating an expanded, world class facility in Darling Harbour

86

6 Delivery and funding models for a new or expanded facility 88

Existing facilities in Australia 88

Private and public sector delivery options 95

Benefits of private sector participation 98

Funding options 99

Contributions from government and resulting benefits to the NSW economy

102

7 Risk allocation 103

Risk allocation matrix 103

8 Proposed way forward 108

Proposed way forward 108

Appendices 111

Appendix A – Acronyms 111

Appendix B – Artist impression of an expanded SCEC 112

Dear Mr O’Farrell,

The NSW business community welcomes your policy and project commitments to underpin economic growth and development in New South Wales.

We particularly welcome your commitment to deliver new, world class convention and exhibition space in Sydney.

As you are aware, convention and exhibition space is a key driver of this State’s economic activity. However, the age and design of the existing facilities means that New South Wales is increasingly losing ground to competitors interstate and throughout the Asia Pacific region.

The wider economic benefits delivered through a well designed, well administered and world class convention and exhibition facility would stretch far beyond Sydney.

International business events are a significant export earner for the State’s economy. International convention delegates will typically invest five or six times the expenditure of international leisure tourists.

Global and significant national events introduce new business for Sydney’s hotels, restaurants and retail businesses. Moreover, delegates to business events travel far beyond Sydney – driving economic development in regional New South Wales – and across the nation.

Because of the importance of new convention and exhibition space, we are pleased to enclose this pre-feasibility study, completed by PricewaterhouseCoopers, for your consideration.

We also acknowledge and thank Minter Ellison Partner Paul Paxton, who has provided invaluable advice and counsel throughout this process.

Our pre-feasibility study recommends that a new facility be constructed adjacent to the existing Sydney Convention & Exhibition Centre at Darling Harbour.

Darling Harbour’s position on the waterfront, its proximity to transport infrastructure and existing hotels; and the opportunity for additional revenue streams to lower the cost to taxpayers make it the stand out option.

Our study recommends the use of a Public Private Partnership, which would allow the State to drive value for money outcomes and drive down the cost to taxpayers over the life of the project. A PPP will allow the State to transfer project risks away from taxpayers and harness the private sector to deliver innovations like a new deluxe hotel for Sydney.

Foreword

A PPP will allow New South Wales to capture the sort of benefits delivered by the award winning Melbourne Convention and Exhibition Centre PPP.

Your commitment to a new convention and exhibition facility in Sydney will also be an important way to restore integrity to the State’s infrastructure programme.

During this study we have seen very significant interest from a range of respected industry participants from across the tourism and infrastructure sectors.

We note that the next phase of this process involves a consultation with interested parties, including potential financiers, constructors and operators to be overseen by an independent panel.

We believe this interactive process will be important to further refine the options in terms of site, scale and funding model. This consultation phase will allow the project to be advanced quickly from concept to commission, if you are elected to govern next March.

In summary, we have been pleased to oversee the enclosed pre-feasibility study and commend it to you.

Yours sincerely,

Matthew Hingerty Australian Tourism Export Council

Glenn Byres Property Council of Australia

Christopher Brown Tourism & Transport Forum

Brendan Lyon Infrastructure Partnerships Australia

The Hon Patricia Forsythe Sydney Business Chamber

6

The Sydney Convention and Exhibition Centre is ageing, has limited capacity and is experiencing increased competition related to the size and flexibility of its offering

This is losing economic benefit for NSW

Introduction

The Sydney Convention and Exhibition Centre (SCEC) was opened in 1988. The facility cost $287 million (or $630 million in today’s dollars), with a $57 million extension opened in 1999 ($85 million in today’s dollars).

These facilities have served Sydney well; but it is clear that the existing centre is ageing and will not be fit for purpose in the years ahead. The SCEC now requires significant investment and already the facility is often trading at full capacity because of high demand from domestic exhibitions. Additionally, the shortage of available space and the lack of flexibility in its design is increasingly impeding Sydney’s ability to meet demand.

Sydney is facing mounting domestic and regional competition for the right to host major events; without action, these circumstances will increasingly see Sydney losing market share for high value national and international business events.

The lack of investment in new convention and exhibition space means New South Wales is missing out on economic opportunities. Without investment to renew and upgrade the required infrastructure, this trend will accelerate as expanded facilities in Melbourne, Hong Kong and Singapore erode Sydney’s competitiveness.

This report provides a high level pre-feasibility study of the options that are available to deliver new or expanded convention centre capacity in Sydney.

This paper provides analysis and recommendations about the options that are available to policy makers in New South Wales to deliver world-class convention facilities for Sydney.

This study was prepared by PricewaterhouseCoopers on behalf of Infrastructure Partnerships Australia –with input from a steering committee comprised of:

• The Australian Tourism Export Council (ATEC);

• Infrastructure Partnerships Australia (IPA);

• The Property Council of Australia (PCA);

• The Sydney Business Chamber (SBC); and

• The Tourism & Transport Forum (TTF).

1. Executive summary

7

Scope of the study

This paper provides a high level pre-feasibility study of the options for new or expanded convention space in Sydney. This report considers options including the location, capacity, economic benefit and procurement model for a new facility. The terms of reference for the study are to:

• Identify the best location for a new or expanded Sydney conference and exhibition centre;

• Specify the size and key facilities required to make a convention and exhibition centre world class and internationally competitive;

• Identify vacant or underutilised state government owned land that could be used as a site to build or expand the existing convention and exhibition centre;

• Develop a funding model for the convention centre, including consideration of private investment, public private partnerships, in kind contributions from The State Government and minimising the impact on NSW taxpayers;

• Identify benefits to the NSW economy from the new facility including models to ensure that regional NSW benefits from the infrastructure; and

• Develop a target list of international conferences and events that could be attracted to the new convention centre.

The assessment draws on:

• Contributions from the steering group;

• Available literature and published data and studies;

• Other convention/exhibition developments in Australia;

• Interviews with key stakeholders including Business Events Sydney (BESydney), Tourism NSW, and the Sydney Harbour Foreshore Authority; and

• A range of private sector parties, including possible operators, financiers, construction companies and architects.

8

Rationale for providing convention and exhibition facilities in NSW

Business events generally provide significant wider economic benefits beyond what can be captured by either event organisers or the owners of the facilities required for such events. This means that there is a substantial benefit derived from cities hosting business events. However, the cost of providing quality convention and exhibition infrastructure is often too high for the facility to be self-sufficient, meaning that government investment for their construction (and sometimes operation) is generally required.

Business events allow local businesses to make overseas or interstate sales. They allow local firms to build national and global networks that later have valuable payoffs for both those companies and the State economy. Moreover, business events attract high yield visitors to Sydney who stay in hotels, eat at restaurants and shop at local retailers. Often, these visitors will extend their visits as tourists in regional New South Wales and interstate.

Every year, Australia hosts more than 300,000 business events involving more than 20 million participants. These events drive expenditure of more than $17 billion each year.

Currently, New South Wales enjoys the lion’s share of these events. A study of Australia’s business events found that while NSW hosted around 27 per cent of all meetings in Australia, it accounts for around 40 per cent of delegates and resulted in $7 billion in expenditure.

These events drive value to the economy by:

• Contributing to the economy from a tourism perspective - The business events industry is one of the highest yielding tourism segments. For example, international convention delegates will spend five or six times the expenditure of an international leisure tourist. A six day international conference for approximately 2,000 delegates contributes an average of $9 million to the NSW economy. Interstate visitors also contribute expenditure to the NSW economy that may not otherwise occur, and often comprise 20% of major trade show visitors.

• Contributing to regional areas – The economic benefits from world class convention facilities extend well beyond Sydney. For example, 46% of all international convention delegates participate in pre or post-touring to other parts of Australia, and 58% of international convention delegates indicate that they will come back to Australia for a holiday within five years. This provides tourism opportunities for regional areas in NSW and across Australia. Furthermore, the ability to portray and market Sydney as a hub for business activity supports the scope for regional areas to host side or supporting events

9

• Contributing to innovation, education, networking, trade, research and practice – The real benefits of international and national events extend significantly beyond tourism expenditure. Business events connect Australia’s businesses, professions and academics to global best practice. This ability to ensure skills and knowledge transfer in fields like medicine, law, sport and the environment in turn contributes to capacity building across the NSW economy. More broadly, business events showcase Sydney’s capacities, extending Australia’s reputation as a place of highly skilled, capable, world leading researchers.

However, these wider benefits are not easily or efficiently captured, and such a facility is unlikely to be financially self sufficient. This means that there is a case for government support. As considered further in John O’Neill’s 2007 Review into Sydney Convention and Exhibition Space, it follows that government investment in convention and exhibition facilities should maximise Sydney’s capacities to host the business events that will make the greatest contribution to NSW: that is, international conventions and major national conventions.

Current situation

Presently, Sydney’s major convention and exhibition facilities are located at the Sydney Convention & Exhibition Centre (SCEC) at Darling Harbour and the Sydney Show Ground (SSG) which is located at Sydney Olympic Park Homebush. The proximity of the Sydney Convention & Exhibition Centre to the Sydney Entertainment Centre allows SCEC to offer expanded facilities.

There are a variety of other facilities which also serve different segments of the business events market. The majority of venues available for larger scale business events are owned by the NSW Government. These facilities are outlined in Figure ES1, below.

The primary convention and exhibition space facilities in Sydney are at Darling Harbour and Sydney Olympic Park

Figure ES. 1 The five major venues in Sydney

Australian Technology Park

SCEC, Darling Harbour

Sydney Entertainment Centre, Darling Harbour

Moore Park

Sydney Showground, Homebush

10

In addition to these larger facilities, some alternative venues are also owned and operated by the private sector, including Rosehill Gardens, Star City casino, and facilities such as hotels with convention capacity which generally caters for events of up to 800 participants.

A range of recent studies have pointed to the economic benefit and importance of Sydney’s ability to successfully compete for major business events. These studies particularly point to the importance of high yield international events because of flow on benefits. Examples include John O’Neill’s 2007 study, and Revitalising the Convention & Exhibition Industry in Sydney, which was prepared for the Tourism & Transport Forum and Property Council of Australia, also in 2007.

Sydney’s market share of events in Australia is declining

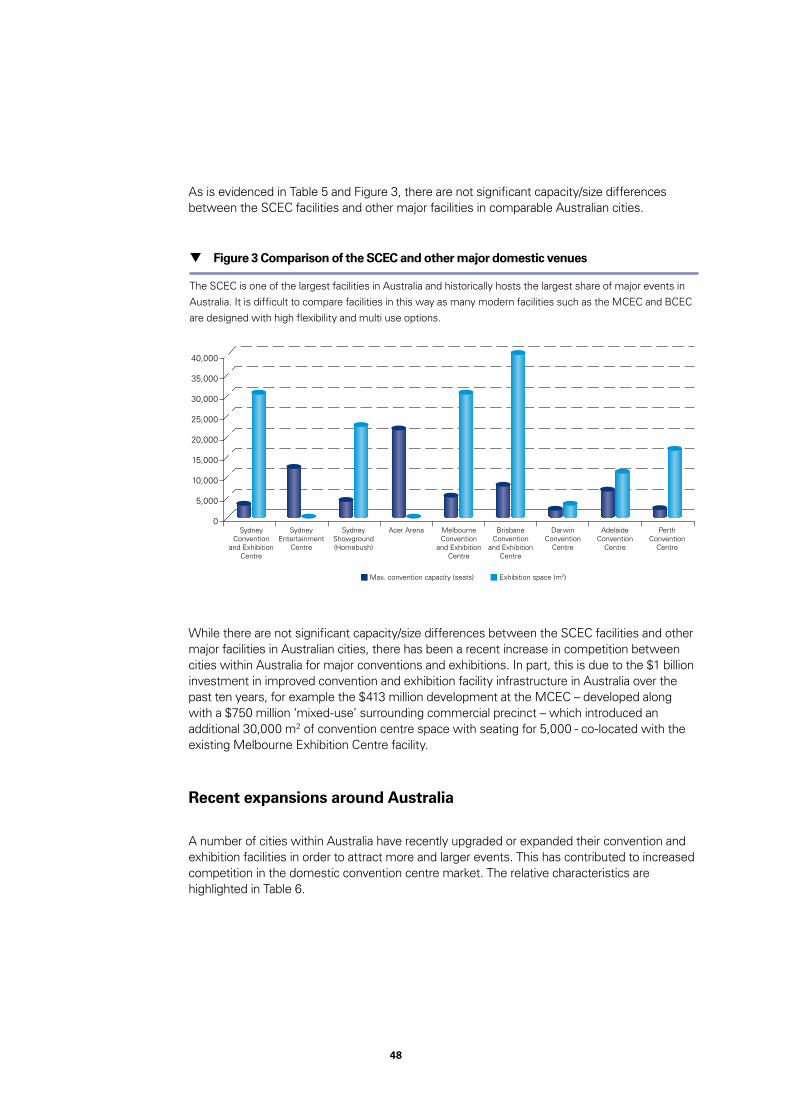

Historically, Sydney has dominated the market for major conventions and exhibitions in Australia. But now, Sydney is facing mounting competition from interstate and regional competitors. A 2007 report found that Sydney is already losing 220 business events every year, equating to lost rental revenues of around $300,000 per event – or $65 million each and every year.

While roughly comparable in size and capacity, the competition from other Australian cities has been spearheaded by almost $1 billion in new infrastructure to support better quality business events in those cities. An example would be the $413 million development at the Melbourne Convention and Exhibition Centre (MCEC) – developed along with a $750 million ‘mixed-use’ surrounding commercial precinct – which introduced an additional 30,000 m2 of convention centre space with seating for 5,000 co-located with the existing Melbourne Exhibition Centre facility.

Figure ES.2 Comparison of the SCEC and other major domestic venues

The SCEC is one of the largest facilities in Australia and historically hosts the largest share of major events in Australia. It is difficult to compare facilities in this way as many modern facilities such as the MCEC and BCEC are designed with high flexibility and multi use options.

5,000

0

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Sydney Convention

and Exhibition Centre

Sydney Entertainment

Centre

Sydney Showground(Homebush)

Acer Arena

Max. convention capacity (seats)

Melbourne Convention

and Exhibition Centre

Brisbane Convention

and Exhibition Centre

Darwin Convention

Centre

Adelaide Convention

Centre

Perth Convention

Centre

Exhibition space (m2)

Due to increased competition, Sydney is losing events to the economic equivalent of hosting a Rugby World Cup every year

11

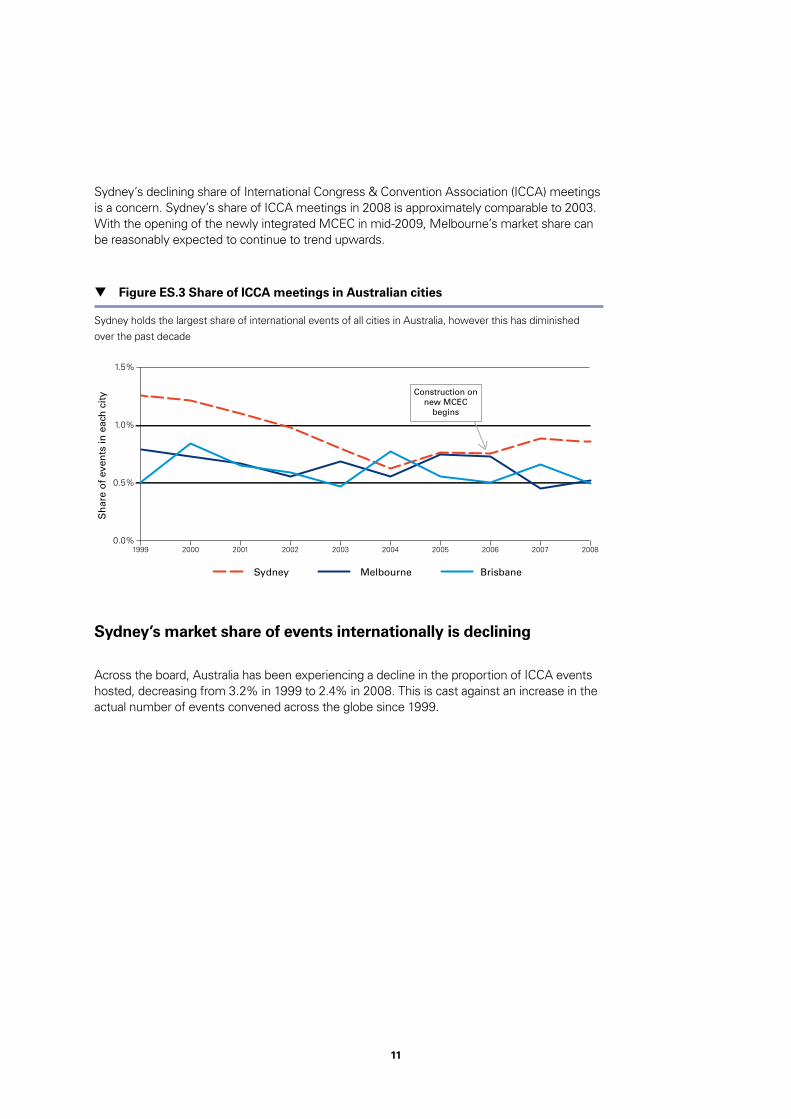

Sydney’s declining share of International Congress & Convention Association (ICCA) meetings is a concern. Sydney’s share of ICCA meetings in 2008 is approximately comparable to 2003. With the opening of the newly integrated MCEC in mid-2009, Melbourne’s market share can be reasonably expected to continue to trend upwards.

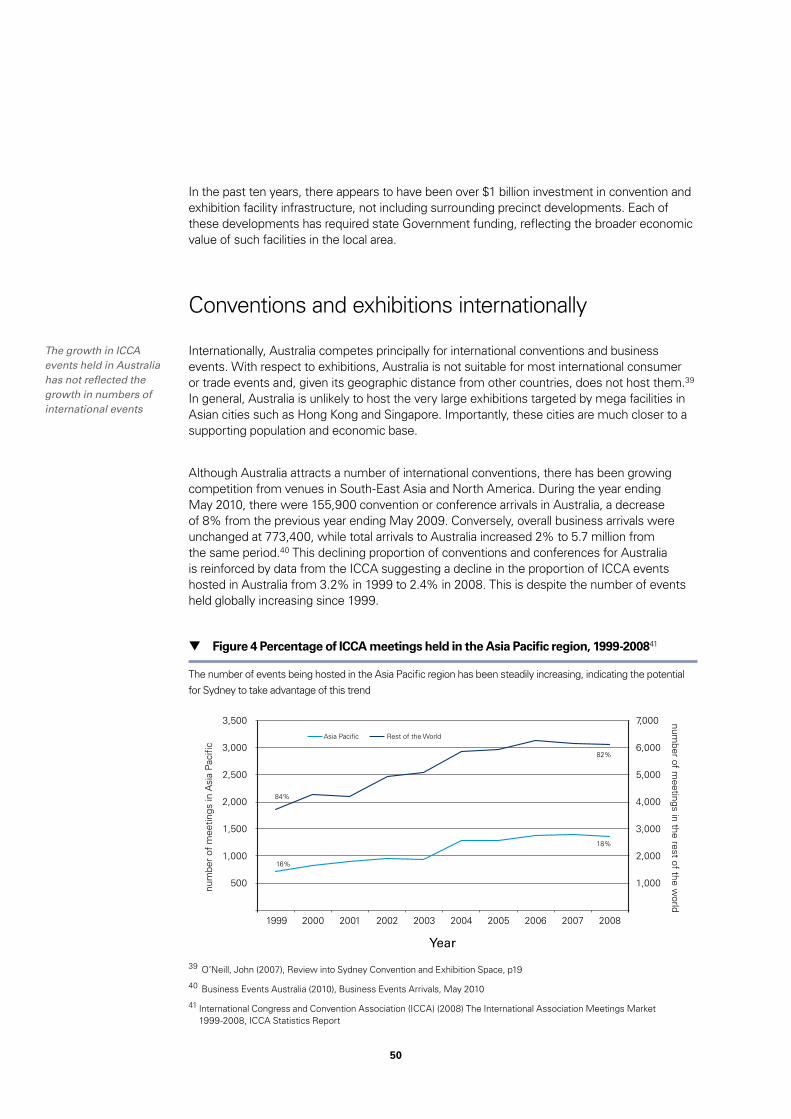

Sydney’s market share of events internationally is declining

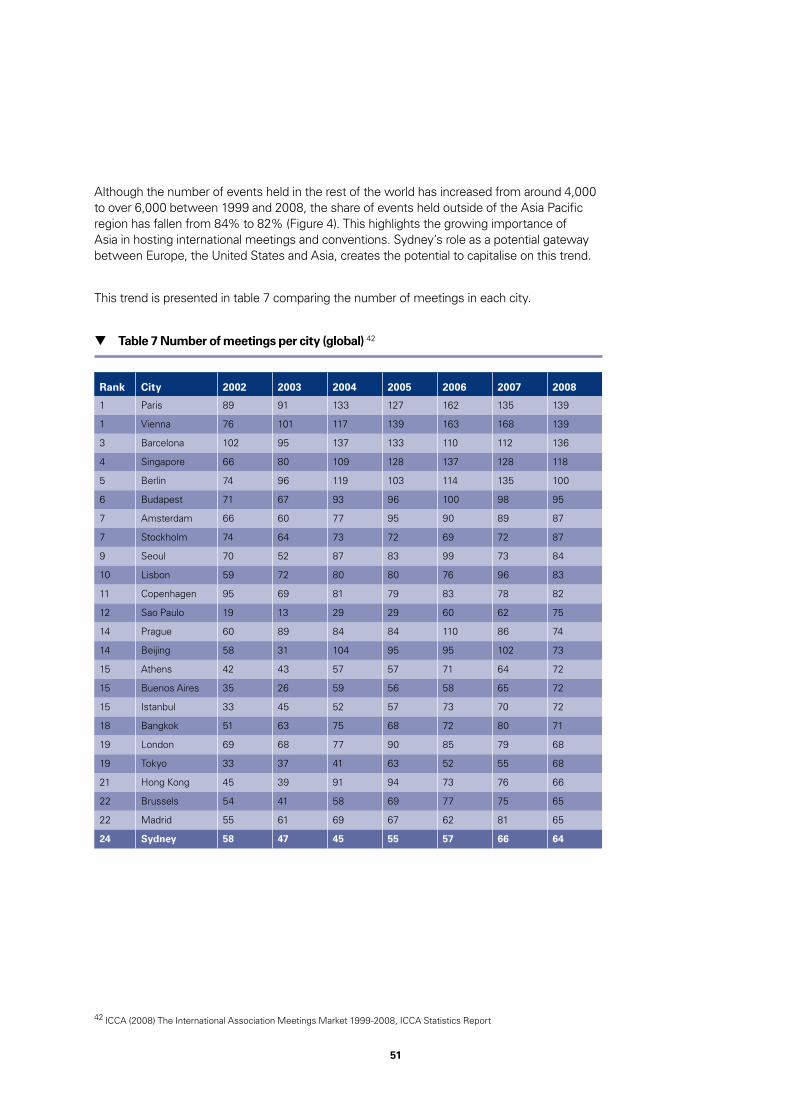

Across the board, Australia has been experiencing a decline in the proportion of ICCA events hosted, decreasing from 3.2% in 1999 to 2.4% in 2008. This is cast against an increase in the actual number of events convened across the globe since 1999.

Figure ES.3 Share of ICCA meetings in Australian cities

Sydney holds the largest share of international events of all cities in Australia, however this has diminished over the past decade

0.0%

Sydney BrisbaneMelbourne

0.5%

1.0%

1.5%

20001999 2001 2002 2003 2004 2005 20072006 2008

Construction onnew MCEC

begins

Sh

are

of

even

ts in

eac

h c

ity

12

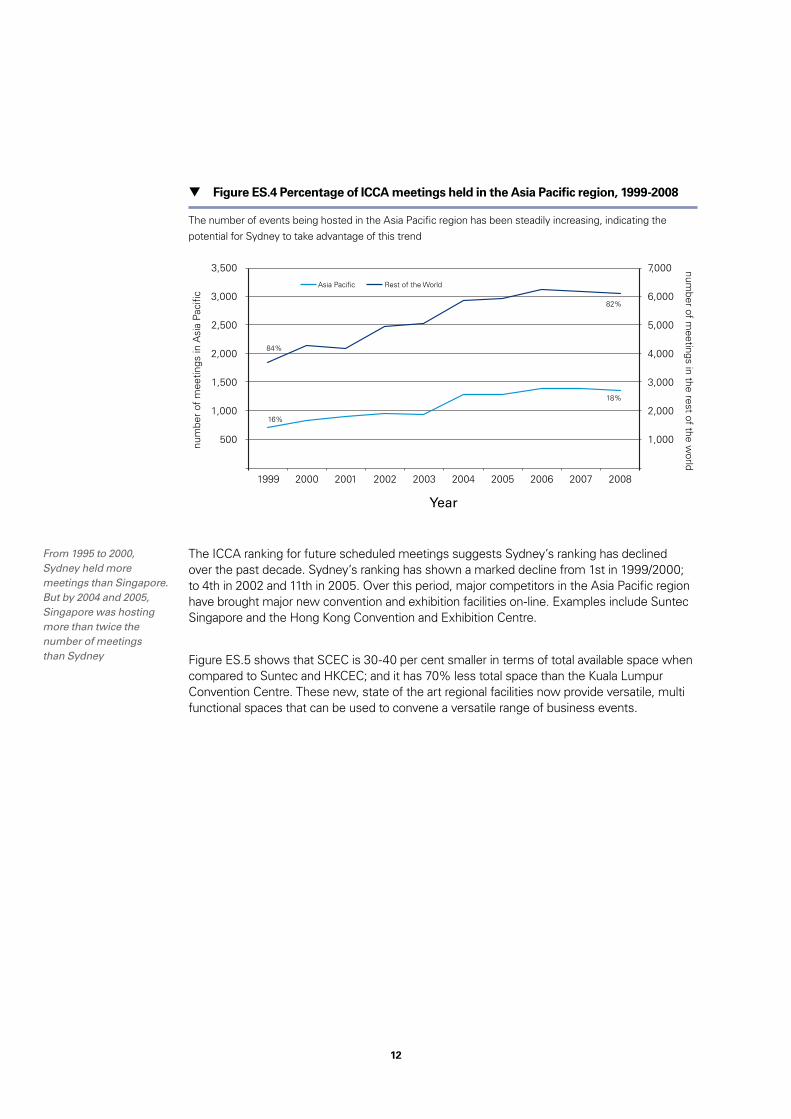

The ICCA ranking for future scheduled meetings suggests Sydney’s ranking has declined over the past decade. Sydney’s ranking has shown a marked decline from 1st in 1999/2000; to 4th in 2002 and 11th in 2005. Over this period, major competitors in the Asia Pacific region have brought major new convention and exhibition facilities on-line. Examples include Suntec Singapore and the Hong Kong Convention and Exhibition Centre.

Figure ES.5 shows that SCEC is 30-40 per cent smaller in terms of total available space when compared to Suntec and HKCEC; and it has 70% less total space than the Kuala Lumpur Convention Centre. These new, state of the art regional facilities now provide versatile, multi functional spaces that can be used to convene a versatile range of business events.

From 1995 to 2000, Sydney held more meetings than Singapore. But by 2004 and 2005, Singapore was hosting more than twice the number of meetings than Sydney

Figure ES.4 Percentage of ICCA meetings held in the Asia Pacific region, 1999-2008

The number of events being hosted in the Asia Pacific region has been steadily increasing, indicating the potential for Sydney to take advantage of this trend

3,500

3,000

2,500

2,000

1,500

1,000

500

7,000

6,000

5,000

number of m

eetings in the rest of the world

num

ber

of m

eetin

gs in

Asi

a Pa

cific

4,000

3,000

2,000

1,000

20001999 2001 2002 2003 2004 2005 2006 2007 2008

Asia Pacific

84%

16%

82%

18%

Rest of the World

Year

13

Broader economic implications if the trend of losing market share of domestic and international events continues

The Sydney Convention and Exhibition Centre makes a significant economic contribution to the State economy. That in turn means that a decline in market share for major events will reduce economic activity and opportunities for New South Wales.

SHFA indicates the economic contribution of the SCEC has declined from $478 million in 2006-07, to $474 million in 2007-08, then $466 million in 2008-09. This trend suggests an average year-on-year decline of 1% per annum – representing a 4% real decrease per annum, once inflation is taken into account.

Furthermore, the number of international events hosted at the SCEC has decreased 8% year-on-year between 2006-07 and 2008-09.

Figure ES.5 Comparison of the SCEC and world class facilities: total leasable space

The SCEC and SEC combined are approximately 30-40% smaller in terms of total space compared to Suntec and HKCEC, and 70% smaller than space at the Kuala Lumpur Convention Centre

20,000

0

40,000

60,000

80,000

100,000

120,000

SCEC(including SEC)

Approx 70,000 m2

91,500 m2

120,000 m2

100,000 m2

HKEC

Convention

Kuala Lumpur Convention Centre

SuntecSingapore

Exhibition Multi purpose & other

Do nothing scenario - if current trends continue, the economic contribution of the SCEC could decrease from the current $466 million pa to around $310 million over the next 30 years

14

The figure above shows the decreasing economic impact of the SCEC under a do nothing scenario. Simply put, a failure to invest in new and renewed capacity will see overall economic benefits decline from around $466 million per annum currently, to around $310 million per annum in 2040.

The decline in international return is the most significant, as NSW is able to fully capture this expenditure as incremental economic benefit, whereas expenditure of local intrastate domestic delegates is lower, being diluted by a substitution effect (e.g. if a Sydney resident does not attend the Motor Show they may have instead attended the movies and generated expenditure anyway).

The SCEC is also losing out on a range of valuable domestic events, because other domestic facilities offer new, larger and more modern facilities, often integrated with accommodation.

Figure ES.6 ‘Do nothing scenario’ - economic impact of the SCEC if current trends continue

If current trends continue, the SCEC’s direct economic impact could decrease from the $466 million currently to around $310 million in 2040

0

50

100

150

200

250

300

350

400

450

500

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

2032

2034

2036

2038

2040

International Domestic Total

15

Factors contributing to Sydney’s declining market share of events

The decline in market share of major international and domestic events being hosted in Sydney is attributed to factors including:

1 Ageing facilities;

2 Capacity constraints at SCEC, linked to factors such as:

• Inadequate exhibition space for some major domestic consumer and trade exhibitions;

• Occasions when facilities are unsuitable for an international convention, either because it has insufficient space for an accompanying exhibition or the size of convention space is inadequate;

• Lack of flexibility in the size of rooms as event organisers increasingly demand flexible and functional exhibition space and a mix of plenary, breakout and exhibition space;

• Inadequate IT quality, especially AV, relative to competing venues in Australia; and

• Limited kitchen capacity.

Events that could be facilitated by a world class venue in Sydney

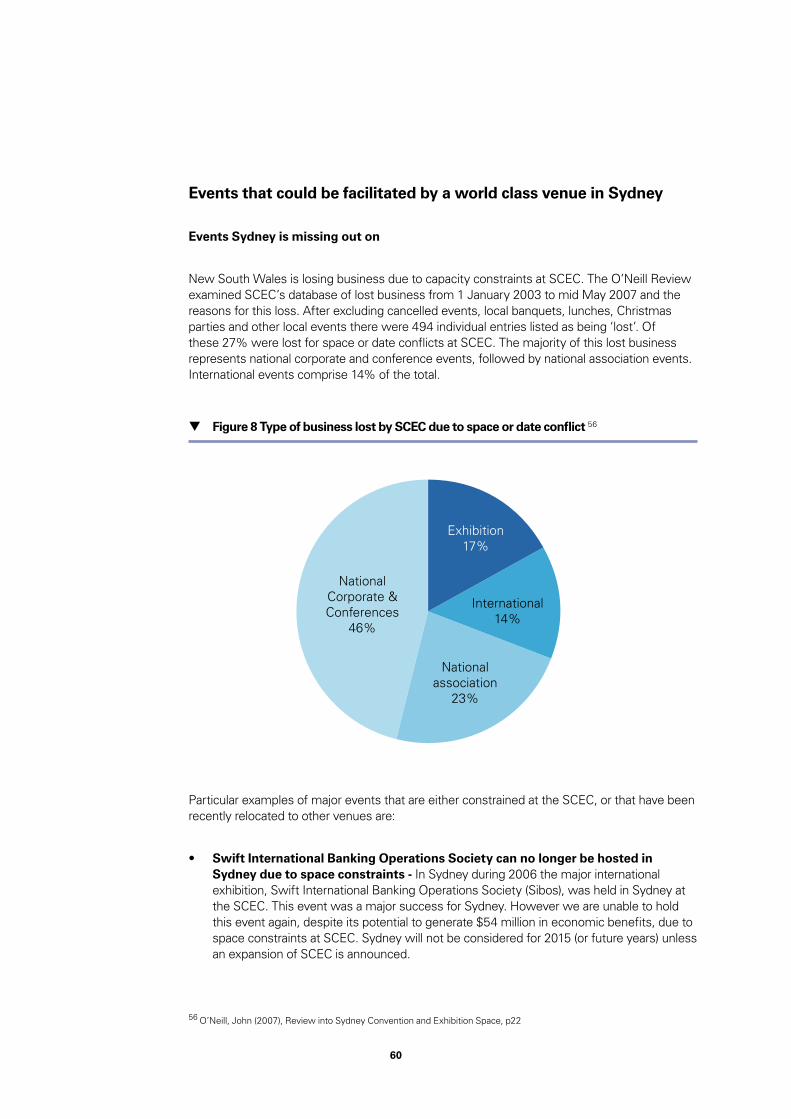

Some examples of major events that are either constrained at the SCEC, or that have been recently relocated to other venues are:

• Swift International Banking Operations Society can no longer be hosted in Sydney due to space constraints - During 2006 the major international exhibition, Swift International Banking Operations Society (Sibos), was held in Sydney at the SCEC. This event was a major success for Sydney. However we are unable to hold this event again, despite its potential to generate $54 million in economic benefits, due to space constraints at SCEC. Sydney will not be considered for 2015 (or future years) unless an expansion of SCEC is undertaken. It is being hosted in Amsterdam this year.

16

• Some current events are forced to operate at smaller than desired levels to utilise the SCEC – events such as the Motor Show, Fine Food Show, and Boat Show would use more exhibition/flexible space at the SCEC if it was available, as they currently utilise the entire centre for these events at the SCEC.

Furthermore, a world class venue would have the potential to host an increased range of international events currently hosted in other cities, including Hong Kong, Singapore and Melbourne. Examples could include:

• International Conference on Materials for Advanced Technologies, more than 3,000 delegates

• Clean Energy Expo, in 2009 over 3,500 professionals, more than 70 international exhibitors and 80 speakers from over 40 countries worldwide

• Options for the Control of Influenza, 1,200 delegates

• Corporate Social Responsibility (CSR) Asia Summit, over 300 international thought leaders

• MIPIM Asia, over 2,000 participants, 400 investors and 200 journalists from over 40 countries

• Aussiecon4 World Science Fiction Convention

• SMART Investment & International Property Expo

• World Congress on Conducive Education

• APCO Australasia Conference & Exhibition

• Sustainable Risk Rationalisation Conference

• International Conference on Solid Waste.

17

World class facilities provide flexible space that could be leased for conventions, exhibitions, entertainment acts, or a range of other events

Size and key facilities to make a convention and exhibition centre world class and internationally competitive

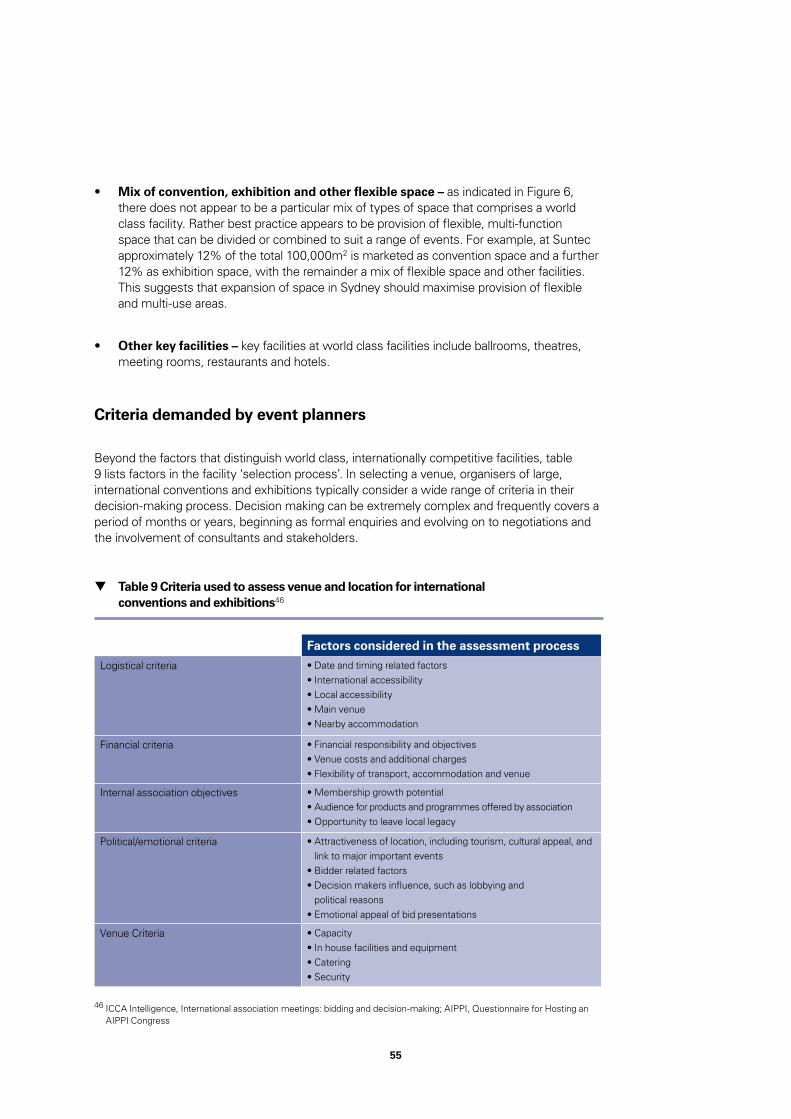

After considering the venues Sydney most competes with in the Asia Pacific, the following traits have been identified as making a convention and exhibition centre internationally competitive:

• Size – compared to other world class venues, for example the Suntec in Singapore. the HKCEC in Hong Kong, and the Kuala Lumpur Convention Centre, the SCEC and SEC combined are currently 30-70% smaller in terms of total space. These three venues claim total sizes between 90,000-120,000m2. Given the lower proportion of international exhibitions hosted in Australia, relative to these three cities, there may not be a need to expand space to this extent – although it does point to available space as a limiting factor on Sydney’s capacity.

• Location – an aspect that the SCEC already shares with the Suntec, HKCEC and other locations such as Brisbane, Darwin and Perth is a convention and exhibition facility that is not only close to the central business district (CBD) and major 5 star hotels, but it is also located on the waterfront.

• Mix of convention, exhibition and other flexible space – as indicated in Figure ES.5, there does not appear to be a particular mix of types of space that comprises a world class facility. Rather best practice appears to be provision of flexible, multi-function space that can be divided or combined to suit a range of events. For example, at Suntec approximately 12% of the total 100,000 m2 is marketed as convention space and a further 12% as exhibition space, with the remainder a mix of flexible space and other facilities. This suggests that expansion of space in Sydney should maximise provision of flexible and multi-use areas.

• Other key facilities – key facilities at world class facilities include ballrooms, theatres, meeting rooms, restaurants and hotels.

Options for expansion in Sydney

There are various options available to expand Sydney’s convention and exhibition capabilities; however not all site options are suitable. For example, while the Australian Technology Park (ATP) at Eveleigh and Moore Park both cater for boutique events, the age, heritage constraints, physical layout and the limited supporting tourism infrastructure mean that they are generally unsuitable for major international conventions.

18

The table below lists a number of site options that are considered in the context of this pre-feasibility study.

The existing Darling Harbour site has been identified as the best location for an expanded, world class conference and exhibition centre in Sydney

This report finds that the current SCEC location is the best option for a new, world class convention centre for Sydney. This recommendation takes into account the advantages and disadvantages of each site, together with the input from the tourism industry and potential project investors.

The key advantage is the ability to leverage existing facilities surrounding Darling Harbour, including integration with the existing convention and exhibition facilities. The site’s location next to Sydney’s CBD, major hotels and transport networks has obvious advantages.

Table ES.1 Potential options for expanding convention and exhibition capacity in Sydney

Facility/location Available capacity

1. Expansion of SCEC Up to 10,000-20,000 m2 of additional space if the Sydney Entertainment

centre (SEC) site and car park are incorporated, with other alternatives for

refurbishment to increase flexibility

2. Expansion of Sydney

Showground (Homebush)

Potential for additional 14,700 m2 expansion bringing total exhibition

space to 36,300 m2

3. Development at Central

Station

Up to 500,000 m2 of commercial space in airspace above railway lines,

of which 50,000-100,000 m2 could be used as convention/exhibition

space. This was proposed in Sustainable Sydney 2030

4. Development at Glebe Island 40 hectares

Potential for 40,000 m2 space (i.e. smaller than existing SCEC venue)

5. Development at Barangaroo

and Millers Point precinct

22 hectares

A previous report believed the site had potential for 40,000 m2 in

exhibition space and up to 5,000 seat capacity in a plenary hall; (TTF/

PCA 2007) but capacity is not certain, given that the commercial space is

fully allocated and retaining high levels of green space is important

The existing Darling Harbour site has been identified as the best location for an expanded Sydney conference and exhibition centre, given its iconic location and scope to expand into the SEC site

19

Other sites such as White Bay, Central Station and Barangaroo do not allow for synergies from operational integration with the existing facility. In addition, White Bay and Sydney Olympic Park do not enjoy the CBD location provided by the existing site. These sites, in particular White Bay, also have lower bases of foot traffic than Darling Harbour, resulting in lower potential to generate ancillary revenues, which will lower the eventual cost to the taxpayer.

The existing SCEC and Sydney Entertainment Centre (SEC) site also offers significant advantages because of its proximity to other major precincts and redevelopments. These include the University of Technology Sydney’s new $150 million Business School, designed by Frank Gehry and being undertaken as part of a broader master plan and proximity to Sydney University. The site will also enable greater connectivity of the city given its proximity to Darling Park, Darling Walk (currently being transformed into a $560 million dollar redevelopment combining commercial office and leisure space), Chinatown (which is planned for a major upgrade), Broadway and the $860 million redevelopment and expansion of the Star City casino. The SEC site is a 5 minute walk from the major new $6 billion Barangaroo site which will generate activity and business events for the convention and exhibition centre precinct.

In considering potential options, it was considered that any upgrade of the SCEC site to enable high yield international events and conferences to be held at the site would require relocation of some domestic and National exhibitions – this would require an expansion and upgrade of the Sydney Showground which has not been considered in the context of this study.

The NSW Government’s south Darling Harbour master plan currently being prepared will consider the best ways to integrate the Darling Harbour convention and exhibition centre precinct with popular tourist precincts including Chinatown, the Powerhouse Museum and the education precinct at the University of Technology. The developments planned in the precinct will increase pedestrian and thoroughfare activity and general ambience in the precinct, contributing to retail and hotel demand if developed at the site – an advantage not shared by the other sites identified in this study. Even before these developments, Darling Harbour attracts more than 27 million visitors each year, which supports greater ancillary revenue potential and a reduction in the extent of Government support required.

Figure ES.7 Location of the SCEC and SEC in Darling Harbour

Star City Barangaroo SCEC SEC SEC Car Park

20

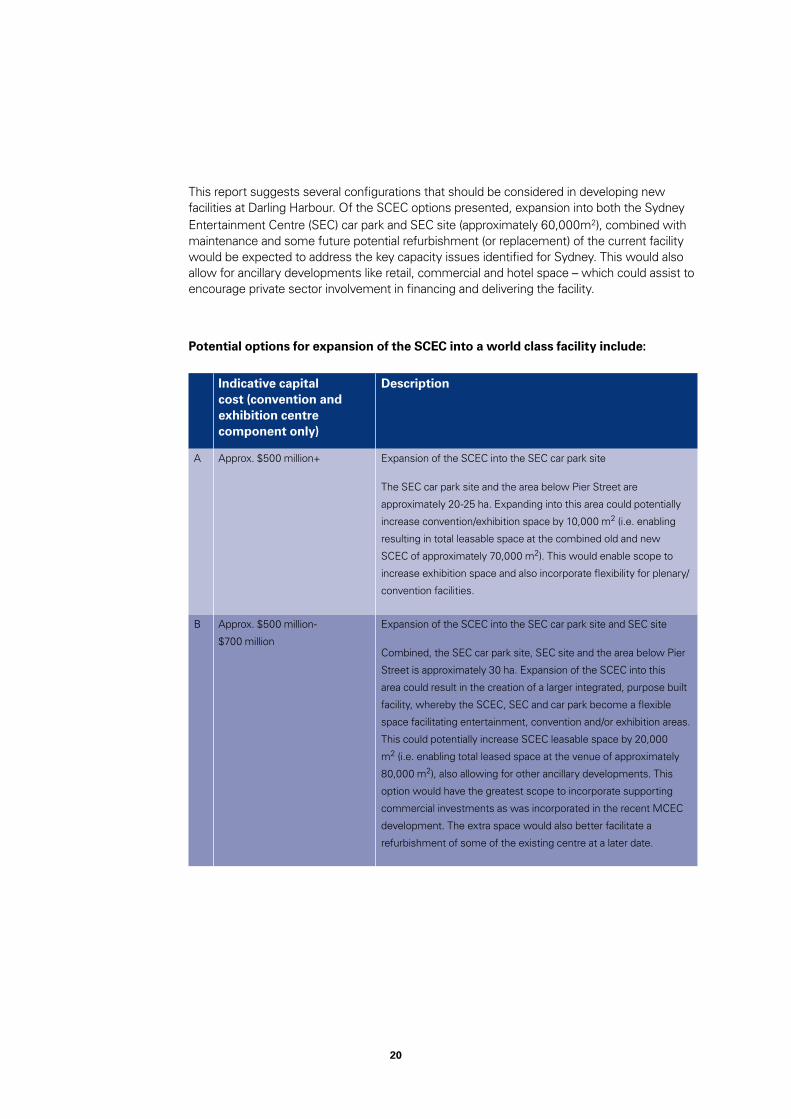

This report suggests several configurations that should be considered in developing new facilities at Darling Harbour. Of the SCEC options presented, expansion into both the Sydney Entertainment Centre (SEC) car park and SEC site (approximately 60,000m2), combined with maintenance and some future potential refurbishment (or replacement) of the current facility would be expected to address the key capacity issues identified for Sydney. This would also allow for ancillary developments like retail, commercial and hotel space – which could assist to encourage private sector involvement in financing and delivering the facility.

Potential options for expansion of the SCEC into a world class facility include:

Indicative capital cost (convention and exhibition centre component only)

Description

A Approx. $500 million+ Expansion of the SCEC into the SEC car park site

The SEC car park site and the area below Pier Street are

approximately 20-25 ha. Expanding into this area could potentially

increase convention/exhibition space by 10,000 m2 (i.e. enabling

resulting in total leasable space at the combined old and new

SCEC of approximately 70,000 m2). This would enable scope to

increase exhibition space and also incorporate flexibility for plenary/

convention facilities.

B Approx. $500 million-

$700 million

Expansion of the SCEC into the SEC car park site and SEC site

Combined, the SEC car park site, SEC site and the area below Pier

Street is approximately 30 ha. Expansion of the SCEC into this

area could result in the creation of a larger integrated, purpose built

facility, whereby the SCEC, SEC and car park become a flexible

space facilitating entertainment, convention and/or exhibition areas.

This could potentially increase SCEC leasable space by 20,000

m2 (i.e. enabling total leased space at the venue of approximately

80,000 m2), also allowing for other ancillary developments. This

option would have the greatest scope to incorporate supporting

commercial investments as was incorporated in the recent MCEC

development. The extra space would also better facilitate a

refurbishment of some of the existing centre at a later date.

21

As part of Option B, the live concert capacity of the Entertainment Centre could be replaced with the new convention and exhibition centre having a large scale flexible plenary/entertainment hall with world class stage and acoustics capable of hosting major concerts for crowds of potentially 6,000-10,000 people, depending on stage layouts. In recent years the age and quality of the Entertainment Centre has seen it experience increasing competition from venues such as Acer Arena. The inclusion of state of the art concert space within a new convention and exhibition centre would mean the CBD again has a modern, competitive and flexible live concert venue.

Both Option A and Option B will involve expansion into the Wilson Entertainment Carpark. This carpark currently has a 1,900 car capacity, and while some of these car parks may be reduced due to the expansion, there will be scope to retain some of this capacity or construct additional capacity underground. Importantly, any impact on the availability of car park spaces will be largely offset by those being constructed as part of the new Darling Walk development. This development includes an 800 space car park, with 600 spaces available to the public. Of course, there are other car park options available in the Darling Harbour district, for example the SCEC is served by its own Exhibition Centre Carpark that can accommodate 750 cars, and the SEC reports that there are around 10,000 spaces within a 10 minute walk.

Considering Options A and B above as ‘Phase 1’ of development of a world class facility in Sydney, ‘Phase 2’ following the expansion could include upgrades and refurbishment to the existing facility. However, it is expected that Phase 1 would need to be completed first to accommodate pre-booked events during construction of the new facility.

Phase 2 options for the existing facility include:

• Limited upgrades and maintenance - To address some issues related to ageing facilities relating to upgrading and maintenance of the roof, air conditioning, kitchen and loading docks. This would not expand capacity. (Cost estimate: approx. $320 million)

• Structural enhancement and refurbishment of SCEC Exhibition Halls - Converting the halls into a streamlined, flexible space. While this would not directly increase capacity, it would allow the existing venue to cater for a wider range of events, potentially simultaneously. As an extension to this option, the potential to convert the existing exhibition halls into 2-storey halls to increase capacity could be explored offset by challenges to continue operation of current facilities during construction. (Cost estimate: approx. $400 million)

• Redevelop or demolish existing SCEC site – Given the underlying costs of renovating, especially the roof, air conditioning, IT systems, loading bays and kitchens, a further Phase 2 option could be to build a new wing for the centre on the existing SCEC site to better integrate into the new Phase 1 centre.

22

Economic benefits of creating an expanded, world class facility in Darling Harbour

An expansion of the SCEC into the SEC car park and potentially also the SEC site has the potential to increase leasable entertainment, convention and exhibition space by 10,000-20,000 square metres. Importantly, it offers the opportunity to introduce more flexible space, enabling multiple events to be hosted at one time. As a result of an expanded SCEC’s ability to attract large scale events, the number and scale events hosted in Sydney would be expected to increase. Attracting additional interstate and international delegates and other visitors will generate new expenditure in NSW resulting in an increase in the economic benefit contributed by the SCEC to the NSW economy.

As indicated in the figure below, this report finds that a new, world class convention and exhibition centre will deliver additional economic benefit of between $160 million and $270 million each year, depending on which site configuration is adopted.

Figure ES.8 Possible increase in economic benefit relative to a do nothing scenario (Phase 1 SCEC expansion only)

Compared to a ‘do nothing’ scenario, expansion of the SCEC has the potential to increase economic impacts by $160-270 million pa, or $2.0-3.4 billion over 30 years in today’s dollars

0

100

200

300

400

500

600

700

800

900

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

2032

2034

2036

2038

2040

Base Case (no expansion/do nothing)

SCEC expanded into the SEC carpark and SEC site

SCEC expanded into the SEC carpark

$ m

illio

ns

23

Economic benefits experienced from the expansion of convention and exhibition facilities in other Australian jurisdictions are described below:

• The economic benefits to development of the Perth Convention Centre are derived through the extra visitors to the State, have been calculated as $2.2 billion over the life of the Centre, or approximately $63 million per year for 35 years.

• The Melbourne Convention Centre development alone is anticipated to inject around $200 million a year into Victoria’s economy for the next 25 years - a $5 billion boost to the Victorian economy. The investment will create another 2,500 new jobs on top of the almost 1,800 created during construction of the centre and commercial precinct in South Wharf.

Cost benefit analysis of a world class facility

Ideally, the economic contribution of an expanded, world class facility in Sydney would be assessed as part of a cost benefit analysis (CBA). A CBA aims to understand how efficiently funds are being allocated in order to generate benefits for NSW residents and businesses. Such an analysis requires a sizeable amount of data and which was not available to this study.

However, a CBA was undertaken for the Melbourne Convention Centre project, which suggested that the project had a strong benefit cost ratio (BCR) of over 2.5. The net benefits were driven by the expanded centre attracting more overseas visitors, a large proportion of which undertake pre or post-touring to other parts of Australia.

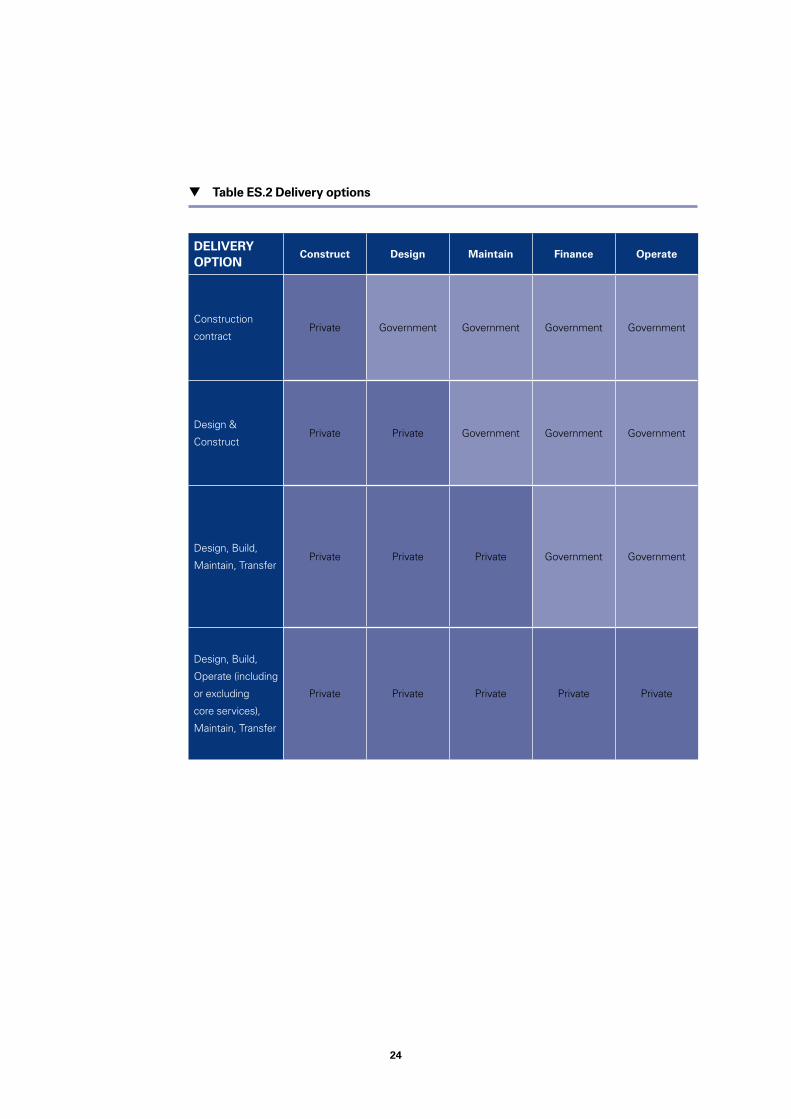

Delivery and funding models for a new or expanded facility

In spite of the significant wider economic benefits delivered by a highly functional convention and exhibition centre, the revenue generated from events, conferences and exhibitions will not be sufficient to cover upfront capital, operational and maintenance costs.

A majority of other states utilised alternative sources to fund the upfront and ongoing costs of facilities by leveraging private sector investment. There are a range of possible roles for private sector involvement in the development and operation of an expanded convention centre in Sydney. The following table presents the spectrum of possible private sector involvement in the delivery of facilities.

24

Table ES.2 Delivery options

DELIvERY OPTION

Construct Design Maintain Finance Operate

Construction

contractPrivate Government Government Government Government

Design &

ConstructPrivate Private Government Government Government

Design, Build,

Maintain, TransferPrivate Private Private Government Government

Design, Build,

Operate (including

or excluding

core services),

Maintain, Transfer

Private Private Private Private Private

25

Benefits of private sector participation

The benefits of private sector participation for the expanded Sydney Conference and Exhibition facility are likely to include:

• Risk transfer: An opportunity to transfer various risks to the private sector such as integrated design, construction and refurbishment, programming and facilitating existing conference bookings, operational, ongoing maintenance and refurbishment as well as risks inherent in various commercial opportunities (e.g. retail, parking, hotel).

• One point of contact: The State will deal with one party to build, operate and maintain the facilities reducing the risk of managing and interfacing with multiple parties. This will reduce interface risk and ongoing administrative costs.

• Innovation: An innovative, integrated design that takes into consideration the urban design and aesthetics of the environment and expanded SCEC, facilitated by a project plan that considers the complexity of a staged development, refurbishment and potential relocation of utilities and infrastructure, within the requirements of continued service delivery.

• Flexibility: A facility that can be easily and cost effectively adapted to cater for a broad range of conferences, exhibitions and activities with a particular focus on international events using leading edge technology and approaches.

• Efficiency and integration: Reducing ongoing operations and maintenance costs by introducing efficiencies through sharing and management of resources, e.g. sharing of kitchen facilities for conferences and a hotel.

• Core services: Enhancing the State’s ability to focus on the core activities of attracting and scheduling key international events for the duration of the project term.

• Whole of life costing: Securing value for money through requiring the private sector to design, operate and maintain facilities that result in designs that minimise ongoing costs and extends the life of assets.

• Technology: Obtaining higher levels of private sector innovation and technology in flexibility and conferencing by building it into the State’s requirements.

26

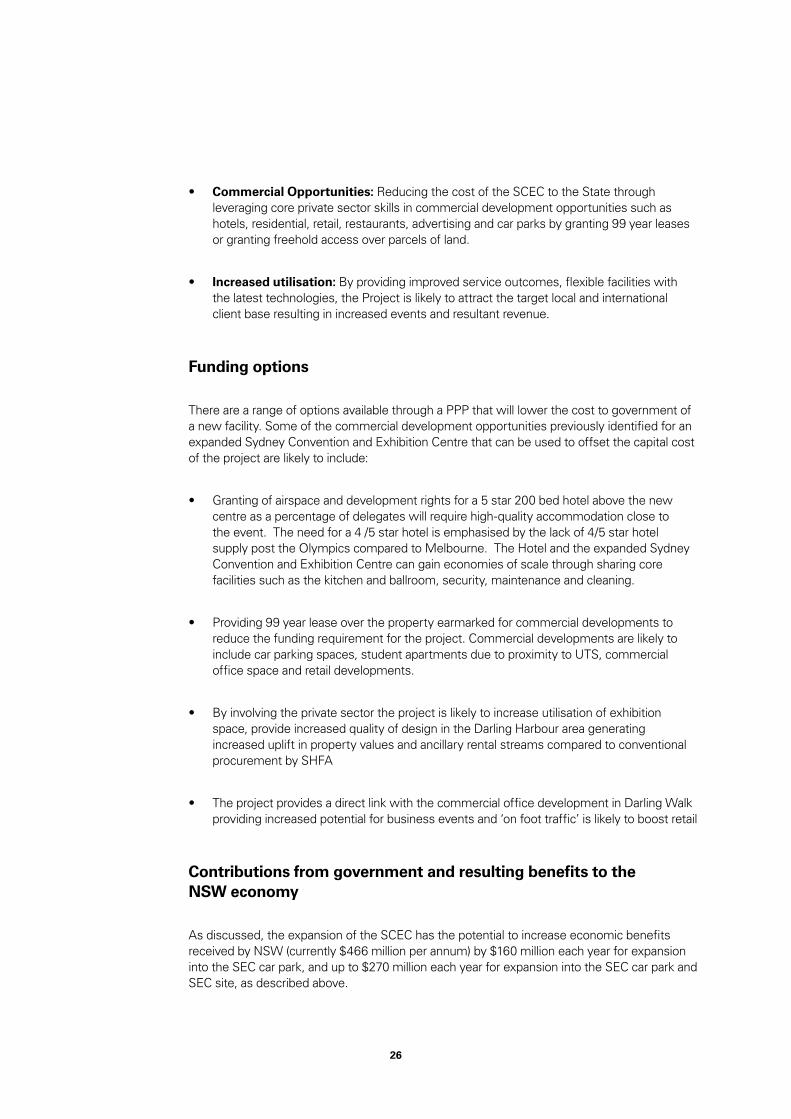

• Commercial Opportunities: Reducing the cost of the SCEC to the State through leveraging core private sector skills in commercial development opportunities such as hotels, residential, retail, restaurants, advertising and car parks by granting 99 year leases or granting freehold access over parcels of land.

• Increased utilisation: By providing improved service outcomes, flexible facilities with the latest technologies, the Project is likely to attract the target local and international client base resulting in increased events and resultant revenue.

Funding options

There are a range of options available through a PPP that will lower the cost to government of a new facility. Some of the commercial development opportunities previously identified for an expanded Sydney Convention and Exhibition Centre that can be used to offset the capital cost of the project are likely to include:

• Granting of airspace and development rights for a 5 star 200 bed hotel above the new centre as a percentage of delegates will require high-quality accommodation close to the event. The need for a 4 /5 star hotel is emphasised by the lack of 4/5 star hotel supply post the Olympics compared to Melbourne. The Hotel and the expanded Sydney Convention and Exhibition Centre can gain economies of scale through sharing core facilities such as the kitchen and ballroom, security, maintenance and cleaning.

• Providing 99 year lease over the property earmarked for commercial developments to reduce the funding requirement for the project. Commercial developments are likely to include car parking spaces, student apartments due to proximity to UTS, commercial office space and retail developments.

• By involving the private sector the project is likely to increase utilisation of exhibition space, provide increased quality of design in the Darling Harbour area generating increased uplift in property values and ancillary rental streams compared to conventional procurement by SHFA

• The project provides a direct link with the commercial office development in Darling Walk providing increased potential for business events and ‘on foot traffic’ is likely to boost retail

Contributions from government and resulting benefits to the NSW economy

As discussed, the expansion of the SCEC has the potential to increase economic benefits received by NSW (currently $466 million per annum) by $160 million each year for expansion into the SEC car park, and up to $270 million each year for expansion into the SEC car park and SEC site, as described above.

27

The annual net cost to government for an expanded SCEC procured through a service payment PPP is estimated at $40 to $60 million.

The estimated cost assumes a 30 year PPP project term with an initial capital cost of $500 million, which is offset by the realisation of commercial revenue opportunities. The quantum of commercial revenue offset reflects indicative proposals received from the private sector for an expanded SCEC. The cash flows making up the net cost is illustrated in the diagram below.

The gross annual Availability Payment reflects the total annual payment to be made by Government for the expanded SCEC. The private sector will determine and deliver the commercial opportunities that reduce the gross annual Availability Payment to $115-135 million per annum. In addition, the NSW Government would receive income from events hosted at the expanded SCEC that further reduces the net cost of the expanded SCEC to $40-60 million per annum.

Proposed way forward

A proposed way forward is described below, though this could be expanded and altered following private sector submissions and outcomes of work such as the SHFA master plan to redevelop and expand NSW’s convention and exhibition facilities (due for completion at the end of 2010):

Figure ES.9 Estimated net annual cost of an expanded SCEC procured through a PPP

PPP Grossannual

AvailabilityPayment

Service Payment$130 - 150 m

CommercialRevenue

Net Annual AvailabilityPayment

GovernmentAvailability

Payment$115 - 135m

Sydney EventsCentreIncomereceived

Net Annual Costto Government

Net Cost to NSWGovernment

$40 - 60m p.a.

Retail $5 - 6m

Car Parks $11 - 13m

Revenue from events - New facilities $65m

Revenue from events - Existing facilities $10m

28

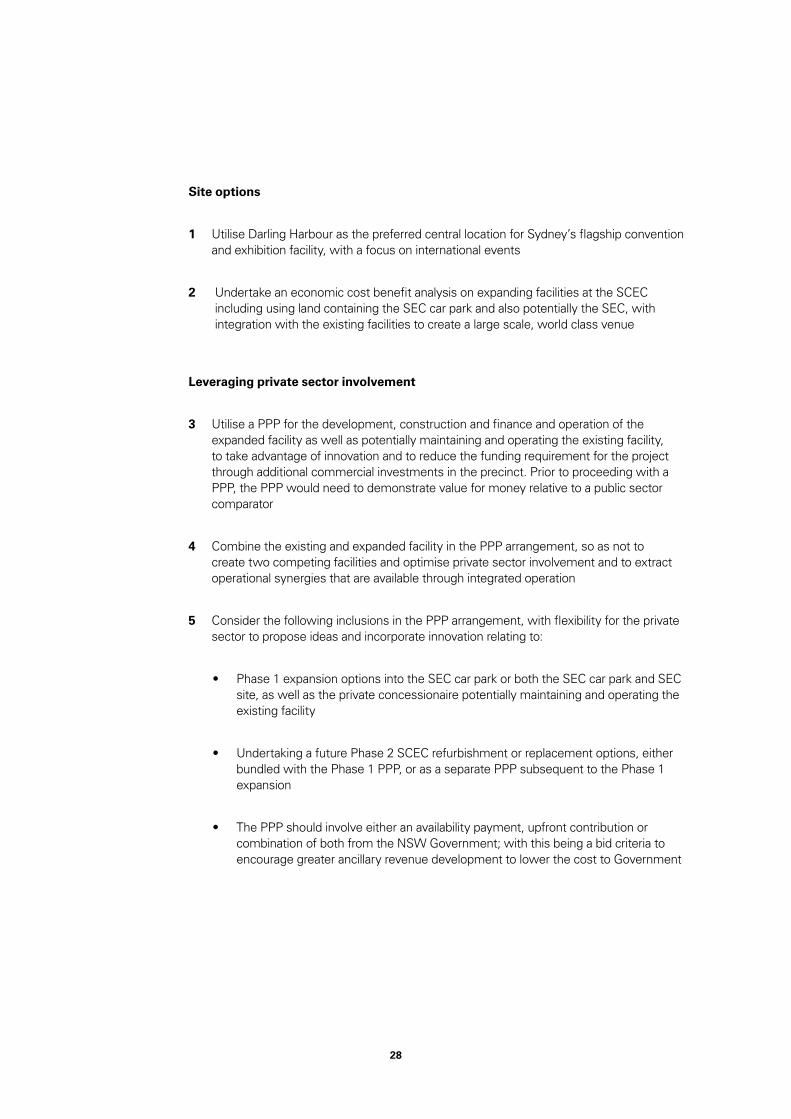

Site options

1 Utilise Darling Harbour as the preferred central location for Sydney’s flagship convention and exhibition facility, with a focus on international events

2 Undertake an economic cost benefit analysis on expanding facilities at the SCEC including using land containing the SEC car park and also potentially the SEC, with integration with the existing facilities to create a large scale, world class venue

Leveraging private sector involvement

3 Utilise a PPP for the development, construction and finance and operation of the expanded facility as well as potentially maintaining and operating the existing facility, to take advantage of innovation and to reduce the funding requirement for the project through additional commercial investments in the precinct. Prior to proceeding with a PPP, the PPP would need to demonstrate value for money relative to a public sector comparator

4 Combine the existing and expanded facility in the PPP arrangement, so as not to create two competing facilities and optimise private sector involvement and to extract operational synergies that are available through integrated operation

5 Consider the following inclusions in the PPP arrangement, with flexibility for the private sector to propose ideas and incorporate innovation relating to:

• Phase 1 expansion options into the SEC car park or both the SEC car park and SEC site, as well as the private concessionaire potentially maintaining and operating the existing facility

• Undertaking a future Phase 2 SCEC refurbishment or replacement options, either bundled with the Phase 1 PPP, or as a separate PPP subsequent to the Phase 1 expansion

• The PPP should involve either an availability payment, upfront contribution or combination of both from the NSW Government; with this being a bid criteria to encourage greater ancillary revenue development to lower the cost to Government

29

• Consider approaches for the availability payment and the role of SCEC operation undertaken (i.e. whether it includes all or only some of the following: maintenance, security, food and beverage, some event marketing, event booking, etc., noting that most of the operating roles at the existing facility are already outsourced)

• NSW Government retains control over use of the facility and the types of events hosted. To facilitate this, and to aid attraction of private sector interest, the NSW Government should retain demand risk for the number and types of events, with the private sector financially incentivised to attract extra events to increase utilisation

• Ensure new exhibition, convention and entertainment facilities developed in the expansion are flexible, multi-use space and at a minimum comprise:

- 10,000-20,000 m2 dedicated to exhibitions and conventions if the site is developed into the SEC car park site

- 20,000-30,000 m2 dedicated to exhibitions, conventions and entertainment space if the site is developed into the SEC car park site and SEC, with facilities incorporating flexibility to host live concerts for 6,000-10,000 attendees

- Innovation and connectivity, including conjoining the expanded site with the existing SCEC

- Opportunity to include underground car park

• The concession would include development rights of the precinct, which may include retail, commercial, residential, hotel – with the height, room number and rating of the hotel reflecting preferences of the private sector operator and NSW Government planning and zoning restrictions. The merit of a new 5 star 200-plus bed hotel sited above the new venue should be further considered, as few delegates choose budget accommodation when attending conferences. Post the Sydney Olympics the extent of new 4-5 star hotel supply in Sydney has been low, especially compared to Melbourne. There would be potential for the hotel and the new convention and exhibition centre to share facilities such as a kitchen and ballroom, as well as security, maintenance, cleaning and other ongoing costs, creating a range of capital and operating cost synergies.

30

6 Utilise a two-staged tender process (instead of a design competition approach with the bidders having to deliver a design, this approach assumes the bidders will put forward designs):

• Expression of interest process to canvass the private sector’s interest and potential plans, and to shortlist tenderers

• Tender process to select a preferred tenderer (with suggestions from the private sector to shortlist 2-3 parties only given the cost of bidding). This may include final negotiation to refine designs and layouts.

Indicative project timings

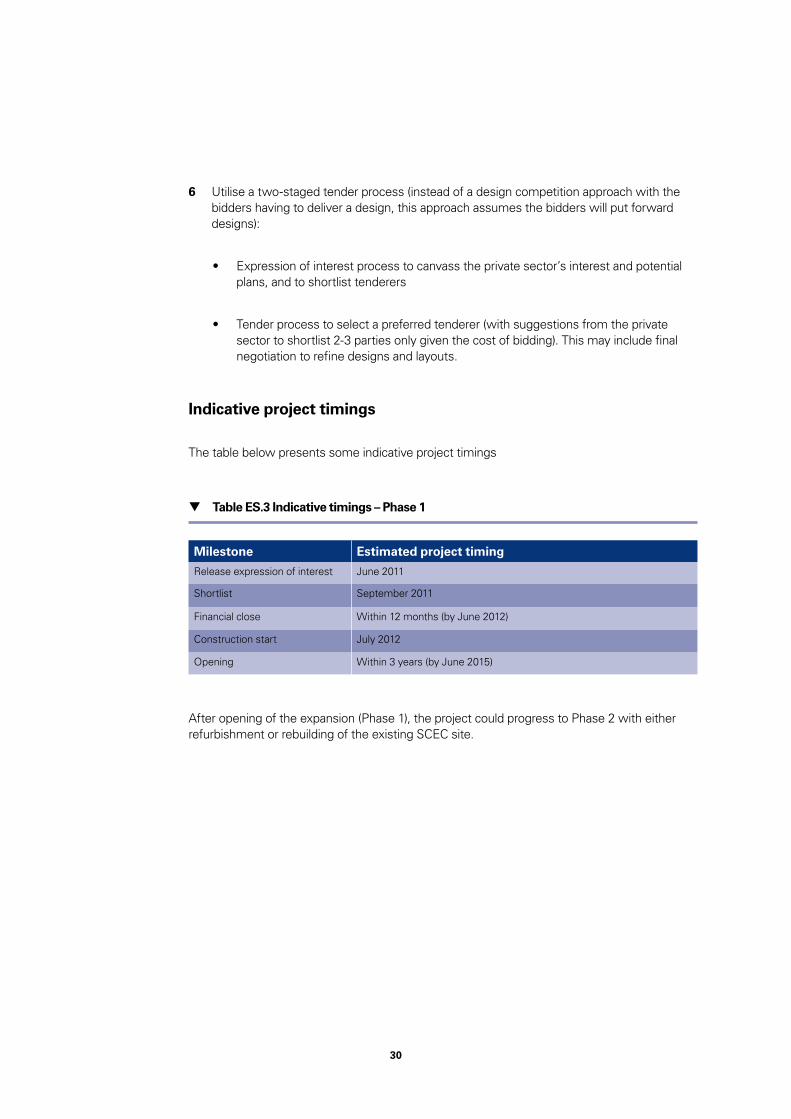

The table below presents some indicative project timings

After opening of the expansion (Phase 1), the project could progress to Phase 2 with either refurbishment or rebuilding of the existing SCEC site.

Table ES.3 Indicative timings – Phase 1

Milestone Estimated project timing

Release expression of interest June 2011

Shortlist September 2011

Financial close Within 12 months (by June 2012)

Construction start July 2012

Opening Within 3 years (by June 2015)

31

1 SCEC (2009), Fact File, February 2009, available at: http://www.scec.com.au/content/fact_files/Centre_Fact_File_2009.pdf; and Australian Bureau of Statistics (ABS) (2010), 6427.0 Producer Price Indexes, Building construction, NSW, June 2010 (10 year historical average)

2 International Congress and Convention Association (ICCA) (2008) The International Association Meetings Market 1999-2008, ICCA Statistics Report

Increased competition from other venues is challenging Sydney’s traditional role as a leader in hosting conventions and exhibitions

2. Introduction

This chapter provides background to the convention and exhibition industry in Sydney and outlines the scope of this review.

Background

The current Sydney Convention and Exhibition Centre (SCEC) was opened in 1988 for a construction cost of $287 million (or $630 million in today’s dollars), with a $57 million extension opened in 1999 ($85 million in today’s dollars).1 These facilities are ageing and its capacity is limited due to competing demand from domestic and international exhibitions and other factors related to size and flexibility of its offering.

This is contributing to Sydney’s drop from number seven in 1999 to number twenty-four in 2008 on the International Congress and Convention Association (ICCA) rankings for the number of association meetings.2

In addition to increased international competition, there has been a recent increase in competition between cities within Australia for conventions and events, following the opening of the new Melbourne Convention Centre (integrated with the Exhibition Centre to create the Melbourne Convention and Exhibition Centre (MCEC)) in 2009, and the opening of the Darwin Convention Centre in 2008. Other cities in Australia, such as Brisbane and Perth, have recently or are currently upgrading or expanding their facilities.

Although the SCEC offers a size and location comparable, or even superior, to other venues, the ageing facilities do not adequately provide for the needs of all potential conventions and exhibitions. Stakeholders have indicated that event bookings can be constrained by available space, and the facilities do not offer the flexibility increasingly demanded by event planners.

A number of recent reviews, such as that prepared by John O’Neill in 2007 and the Property Council of Australia (PCA) and Tourism & Transport Forum (TTF) also in 2007 have highlighted the importance of Sydney maintaining its competitive position with regard to conventions and exhibitions, in particular international events, given their flow on economic benefits.

32

This high level study examines the options for new or expanded convention capacity in Sydney

Scope of this study

This study is a high level pre-feasibility study of options of new or expanded convention centre capacity in Sydney. It aims to analyse options on how to best improve the ability to host conventions and exhibitions, which could be either at a new location or further extending the existing Darling Harbour site.

The study was prepared by PricewaterhouseCoopers (PwC) on behalf of Infrastructure Partnerships Australia (IPA) and in conjunction with a steering committee comprising the Australian Tourism Export Council, Property Council of Australia (PCA), Sydney Business Chamber (SBC) and Tourism and Transport Forum (TTF).

The terms of reference for the study are to:

• Identify the best location for a new or expanded Sydney conference and exhibition centre

• Specify the size and key facilities required to make a convention and exhibition centre world class and internationally competitive

• Identify vacant or underutilised state government owned land that could be used as a site to build or expand the existing convention and exhibition centre

• Develop a funding model for the convention centre, including consideration of private investment, public private partnerships, in kind contributions from the State Government and minimising the impact on NSW taxpayers

• Identify benefits to the NSW economy from the new facility including models to ensure that regional NSW benefits from the infrastructure

• Develop a target list of international conferences and events that could be attracted to the new convention centre.

Given the timings and available resources, the assessment draws heavily on available literature and published data/studies as well as other convention/exhibition developments in Australia. Data and suggestions contributed by the steering group, and other key stakeholders including Business Events Sydney (BESydney), NSW Business Chamber, Tourism NSW, Sydney Harbour Foreshore Authority (SHFA), and a range of private sector parties (including possible operators, financiers, construction companies and architects) were considered.

33

3 Deery, Margaret, Jago, Leo, Fredline Liz and Dwyerhe, Larry (2005), The National Business Events Study: An Evaluation of the Australian Business Events Sector

4 Deery et al. (2005), The National Business Events Study: An Evaluation of the Australian Business Events Sector, p19

5 Business Events Sydney (2010), Sydney and NSW Business Events Calendar, ’Examples of 2010 Sydney and NSW business events’, available at: http://www.businesseventssydney.com.au/why-sydney/business-events-calendar/; and SCEC website (2010), available at: http://www.scec.com.au/

Each year NSW hosts more than 81,000 business events involving more than 8 million participants. Nationally expenditure at business events totals $17 billion per annum

and exhibition facilities in NSW

This chapter describes the role of convention and exhibition venues facilitating business events, and the value of business events to New South Wales.

Role of convention and exhibition facilities

Convention and exhibition space exists to service business, government and industry events. Conventions are held to discuss matters of common interest among delegates. Exhibitions bring together suppliers of products, services and information within an environment to promote and display their products to prospective customers.

Each year, Australia hosts more than 300,000 business events, involving more than 20 million participants with total expenditure of $17 billion. Meeting and conference delegates contribute more than half of this expenditure.3 Of these events, NSW holds the largest share of events amongst all the states and territories. In 2003, a study into national business events found that NSW hosted 27% of all meetings in Australia, which accounted for approximately 40% of delegates and resulted in $7 billion of expenditure. In that study, Sydney hosted the largest events.4

Some of the major events hosted in Sydney in 2010 included:

• 7th International Orthodontic Congress

• International Federation of Surveyors Congress

• Lions Clubs International Convention

• Annual World Congress of the Human Proteome Organisation

• Sydney International Boat Show

• Australian International Motor Show.5

3. Rationale for providing convention

34

6 Deery et al. (2005), The National Business Events Study: An Evaluation of the Australian Business Events Sector, p19

7 Foley et al. (2010), A Scoping Study of Business Events: Beyond Tourism Benefits, Executive Summary.

8 Melbourne Convention and Visitors Bureau (2010), Business Events Facts & Figures, available at: http://www.mcvb.com.au/about-mcvb/research/business-events-facts-and-figures.aspx

9 SCEC (2009), Fact File, February 2009, available at: http://www.scec.com.au/content/fact_files/Centre_Fact_File_2009.pdf

10 SCEC (2009), Fact File, February 2009, available at: http://www.scec.com.au/content/fact_files/Centre_Fact_File_2009.pdf

Value of business events to the community

Business events contribute value to the community as a whole – not just the participants.

Although there has been substantial focus on events over the last decade, most of this has related to major events that tend to capture the imagination of the general public. The business event sector, which is an ongoing and high yield component of the event sector, is the ‘quiet achiever’ and has not received adequate recognition for its contribution.6

Business events play a vital role in the broader economic strategy of the State. Business events:

• Contribute to the economy from a tourism perspective

• Contribute in areas such as innovation, education, networking, trade, research and practice – which are likely to far outweigh the financial returns of the tourism spend.7

Tourism impact

The business events industry is one of the highest yielding tourism segments. International and interstate delegates attending business events in Sydney generate significant tourism expenditure for NSW. This contribution is driven by expenditure of these visitors across a wide range of areas from transport and entertainment through to shopping, dining and accommodation.

International delegates make a significant and disproportionately high contribution to the economy. International convention delegates spend (on average) five to six times that of international leisure tourists; and 28% of international delegates also bring their partner.8 As an example, a six day international conference for approximately 2,000 delegates contributes an average of $9 million to the NSW economy.9

At the Sydney Convention and Exhibition Centre (SCEC) in 2008-09, international delegates comprised 3% of all delegates attending events at the venue, but contributed 23% of the total delegate/visitor expenditure generated at the SCEC, with $109 million in expenditure from delegates at international conferences and congresses that year.10

35

11 Stakeholder interviews as part of this study

12 Melbourne Convention and Visitors Bureau (2010), Business Events Facts & Figures, available at: http://www.mcvb.com.au/about-mcvb/research/business-events-facts-and-figures.aspx

Interstate visitors also contribute expenditure to the NSW economy that may not otherwise occur. Interstate visitors can comprise 15-20% of major trade show visitors, further boosting visitor expenditure in NSW. This could result in $70-95 million expenditure for delegates to the SCEC alone each year.11

Regional impact

The tourism impact generated from providing world class convention and exhibition facilities in Sydney that can attract international delegates extend well beyond Sydney:

• 46% of all international convention delegates participate in pre or post-touring to other parts of Australia

• 58% of international convention delegates indicate that they will return to Australia for a holiday within the next five years, after the convention has been held.12

As this suggests, attractions such as the Western Plains Zoo in Dubbo may provide for possible pre or post-touring destinations. Furthermore, the ability to portray and market Sydney as a hub for business activity supports the scope for regional areas to host side or supporting events. In addition, business events could generate innovation and knowledge transfer for regional universities. For example, Newcastle University is known for its medical research; and hosting medical industry events in Sydney may help to promote medical activity and research more broadly in NSW.

Innovation and knowledge impact

It is well established that business events make a significant contribution to the economy from a tourism perspective. However, Foley et al. in A Scoping Study of Business Events: Beyond Tourism Benefits show that beneficial outcomes are also realised in areas including:

• Knowledge expansion

• Networking, relationships and collaboration

• Educational outcomes

36

13 Foley et al. (2010), A Scoping Study of Business Events: Beyond Tourism Benefits, p. 26

14 Foley et al. (2010), A Scoping Study of Business Events: Beyond Tourism Benefits, Executive Summary.

15 Foley et al. (2010), A Scoping Study of Business Events: Beyond Tourism Benefits, Executive Summary.

• Fundraising and future research capacity

• Raising awareness and profiling

• Showcasing and destination reputation.13

Foley et al. suggest that these benefits are realised because business events connect the world’s best practice and international knowledge with local researchers and practitioners - in fields including medicine, law, sport and the environment. In turn, growth in local NSW knowledge contributes to capacity building within each sector. Such events allow for dissemination of new knowledge, techniques, materials, and technologies in each of the sectors, providing Sydney/NSW based educators, practitioners and researchers with access to a network of international colleagues. This networking provides local delegates with new business and research collaborations, and will generate innovation, ideas and research agendas for many years to come.14

More broadly than this, business events showcase Sydney’s capacities, fostering a reputation as a place of highly skilled, capable, world leading researchers.15

Rationale for government investment in expanding Sydney’s convention and exhibition facilities

Large scale convention and exhibition centres tend to require government subsidies for their construction and, in some cases, their operation. The rationale is that some types of business events provide benefits to NSW beyond what can be captured and paid for directly by the facility.

As described in the earlier parts of this chapter, business events attract visitors to Sydney who stay at hotels, eat at restaurants, and shop at local retailers. Some of those people extend their visits as tourists and travel elsewhere in the State. Some events lead to overseas or interstate sales by local businesses or build international networks for local firms that later have valuable payoffs for those firms and the broader State economy. It is not possible for the convention and exhibition centre as a standalone entity to capture a share of these benefits adequate for the facility to be financially self-sufficient, which creates a need for Government support.

37

16 O’Neill, John (2007), Review into Sydney Convention and Exhibition Space, pp 11-12

As considered further in O’Neill’s 2007 Review into Sydney Convention and Exhibition Space, some large hotels in Sydney provide internal convention facilities. However, there is a limit on the size of convention space they can economically provide, requiring facilities to be proportionate to the number of rooms in the hotel. As such O’Neill suggests the need for government funded convention and exhibition facilities is for business events beyond the size that the private sector alone can economically provide - and particularly where those events have substantial external benefits for NSW.

Business events, particularly those with a strong international component, lead to more extensive purchase of tourism services and, in the case of major international conventions, strong interaction that enhances Sydney’s position as a global city and the international ties of its businesses and other knowledge workers.

It follows that government investment in convention and exhibition facilities should be done to serve business events of a size beyond what the private sector alone is able to cater for. Additionally, it should be offered in a way that maximises Sydney’s ability to attract business events likely to make the greatest contribution to NSW: international conventions and major national conventions.16

38

17 O’Neill, John (2007), Review into Sydney Convention and Exhibition Space, p12

18 O’Neill, John (2007), Review into Sydney Convention and Exhibition Space, p2

Sydney typically hosts international conventions and exhibitions, but not large international consumer trade shows

This chapter provides an overview of the current convention and exhibition facilities in Sydney, and how Sydney’s facilities compete both nationally and internationally for events.

Current facilities in Sydney

Convention and exhibition space exists to service business, government and industry events. Broadly, the market for such events comprises conventions and exhibition events. Although the categorisation of these events is fluid, they are generally defined as:

• Conventions are held to discuss matters of common interest among delegates. Professional conventions can encompass various commercial, academic and social groups. (Conventions, of a medium to large scale, sometimes host exhibitions simultaneously)

• Exhibitions bring together suppliers of products, services and information within an environment to promote and display their products to prospective customers. These events primarily lead with show floor activity.17

Sydney currently hosts:

• International, national and local conventions (including corporate meetings)

• National and local consumer trade shows

• Industry related exhibitions.18

Due to the typical large scale of events and relatively small market (compared to Asian centres), Australia in general is not suitable for most international consumer or trade exhibitions and does not host them. Australia is, however, competitive for international conventions due to regional location.

4. Current facilities in Sydney

39

19 Tabcorp (2010), Tabcorp increases investment at Star City, 5 August 2010, available at: http://afr.com/rw/2009-2014/AFR/2010/08/04/Photos/c257fc76-a019-11df-8dca-9e56e9d3303d_tabcorp%20increases%20invest.pdf

20 Private stakeholder interview, 9 June 2010

There are a variety of convention and exhibition facilities in Sydney, each offering different capabilities and targeting slightly different markets

There are a variety of convention and exhibition facilities in Sydney, each offering different capabilities and targeting a range of markets. A majority of the facilities in Sydney are publicly owned by the New South Wales Government. These venues are generally for larger-scale conventions and/or exhibitions, including the:

1 Sydney Convention and Exhibition Centre (SCEC), Darling Harbour

2 Sydney Entertainment Centre (SEC), Darling Harbour

3 Sydney Showground (SSG), at Sydney Olympic Park (Homebush)

4 Moore Park; and

5 The Australian Technology Park (ATP), Eveleigh.

Alternative venues are also owned and operated by the private sector, which provides:

6 Facilities for some exhibitions and plenary events – e.g. Rosehill Gardens hosts the Sydney Stitches and Craft Show and the Rosehill Gardens Boat Show; and Star City casino also provides facilities for events (with Star City’s capacity set to expand with its development of a 3,000-seat event centre comprising 2,400 m2 of column-free space and views over Sydney Harbour and the city skyline)19.

7 Facilities with convention capacity of up to 800 participants – e.g. at some hotels, with the Hilton Hotel in Sydney one option for exhibitions, with capacity of approximately 800 participants.20 Star City’s new 2,400 m2 Events Centre will be the largest event space of any hotel in Sydney.

Table 1 Sydney’s target in the international market

Sydney is a suitable venue for international and domestic conventions

Sydney • • • • •

Hong Kong • • • • • •

Singapore • • • • • •

Kuala Lumpur • • • • • •

Inte

rnat

iona

l

conv

entio

ns

Nat

iona

l

conv

entio

ns

Loca

l

conv

entio

ns

Inte

rnat

iona

l con

sum

er

and

trad

e sh

ows

Nat

iona

l con

sum

er

and

trad

e sh

ows

Loca

l con

sum

er

and

trad

e sh

ows

40

21 Private interview with industry stakeholder, June 2010

22 O’Neill, John (2007), Review into Sydney Convention and Exhibition Space, p14

The locations of the five major facilities are presented in figure 1

The major venues suitable for hosting conventions and exhibitions are geographically spread throughout the greater Sydney metropolitan area and target different markets. In addition to these larger facilities, there are a wide range of Sydney spaces for conventions; especially those catering for less than 800 delegates. These include various hotels, theatres, town halls and other purpose-built convention facilities. While stakeholders suggest that the ability of Sydney hotels to host smaller scale conventions and exhibitions may be limited when compared to Melbourne,21 the range and scope of small to medium sized facilities has not been considered as part of this study – indeed the O’Neill review suggests that there are sufficient facilities to service the needs of this segment of the market.22

Each of the current facilities is described in the table overleaf. The primary convention and exhibition space facilities in Sydney are the Sydney Convention and Exhibition Centre located at Darling Harbour and the Sydney Showground located at Sydney Olympic Park, Homebush.

Figure 1 Map of current facilities in Sydney

Australian Technology Park

SCEC, Darling Harbour

Sydney Entertainment Centre, Darling Harbour

Moore Park

Sydney Showground, Homebush

41