Embed Size (px)

Citation preview

A WORKSHEET FOR A SERVICE BUSINESS

Accounting – Chapter 6

CONCEPT: Consistent Reporting The application of the same accounting

procedures for each accounting period.

Why is this important? Comparison Accuracy

Fiscal Period

The length of time for which a business summarizes and reports its financial information

CONCEPT: Accounting Period Cycle Changes in financial information are

reported for a specific period of time in the form of financial statements

Determining the Fiscal Period There is no set rule about the length of a

company’s fiscal period How often do you want to report financial

information? Problems if the cycle is too long Problems if the cycle is too short

Analysis can be conducted at anytime Aided by computer based accounting

programs

Setting the Start Date

Considerations for starting a fiscal period Often follows the calendar year Must be done at least once a year Preparation of financial statements takes time Examine business activity

Is it better to start/end your fiscal period at a busy or a slow time in a company’s business cycle?

Sole proprietorship income is personal income Tax considerations

Work Sheet

A columnar accounting form used to summarize general ledger information needed to prepare financial statements Summarize general ledger balances to prove

that debits equal credits Plan needed changes to general ledger

accounts to bring account balances up to date

Separate general ledger balances according to the financial statements to be prepared

Calculate the amount of net income/loss for the period

Work Sheet Basics

The Work Sheet is a planning tool Must be prepared in pencil

Heading Three lines1. Name of Company2. Name of Report3. Date of Report

1. For the ____ended _____

The Trial Balance

A proof of the equality of debits and credits in a general ledger

If quality records are kept, the general ledger is all that is needed to prepare the trial balance

The general journal and source documents might be required if errors are discovered Errors are found when the trial balance

doesn’t result in debits equaling credits

Preparing the Trial Balance (pg. 154)

Write the heading on the worksheet Write the general ledger account (in order

of account number) debit balances in the Trial Balance Debit column

Write the general ledger account credit balances in the Trial Balance Credit column

Accounts with no balances are included, but no amounts are entered in the Trial Balance Columns (Income Summary, Supplies Expense and Insurance Expense)

Preparing the Trial Balance (cont’d)(pg. 154) Rule a single line across the two Trial

Balance columns below the last line on which an account title is written Showss that each column is to be added

Add the Trial Balance Debit and the Trial Balance Credit columns. If they are the same, then they are in

balance If not, recheck your math to locate the error

The remainder of the worksheet cannot be completed until the Trial Balance columns are proved

Preparing the Trial Balance (cont’d)(pg. 154) Write each column’s total below the

single ruled line Rule double lines across both Trial

Balance columns. The double lines mean that the Trial Balance column totals have been verified as correct

Complete WT 6.1 with the class WT61-63.xls

Accounting CONCEPT

Matching Expenses with Revenue Revenue from business activities and

expenses associated with earning that revenue are recorded in the same accounting period

Provides accuracy in reporting Provides information about level of

expenses required to generate level of revenue

Adjustments

Changes recorded on a work sheet to update ledger accounts at the end of a fiscal period Enables a company to apply the Matching

Revenue with Expenses concept Brings the general ledger accounts up to date What is the value of supplies used during a

specific period? Transform from assets to expenses

How much prepaid insurance was consumed during a specific period?

Any others?

Adjustment Basics

Adjustments are recorded on the worksheet

Changes are not made in general ledger accounts until adjustments are journalized and posted (chapter 8) Must check for accuracy first!

Adjustment to Supplies (pg 158) Determine the actual supplies balance at

the end of the fiscal period (HOW?) The amount of the adjustment is the

Account balance minus the actual balance Supplies must be credited (reduced) by

the amount of the adjustment Supplies Expense is debited by the

amount of the adjustment (the amount used)

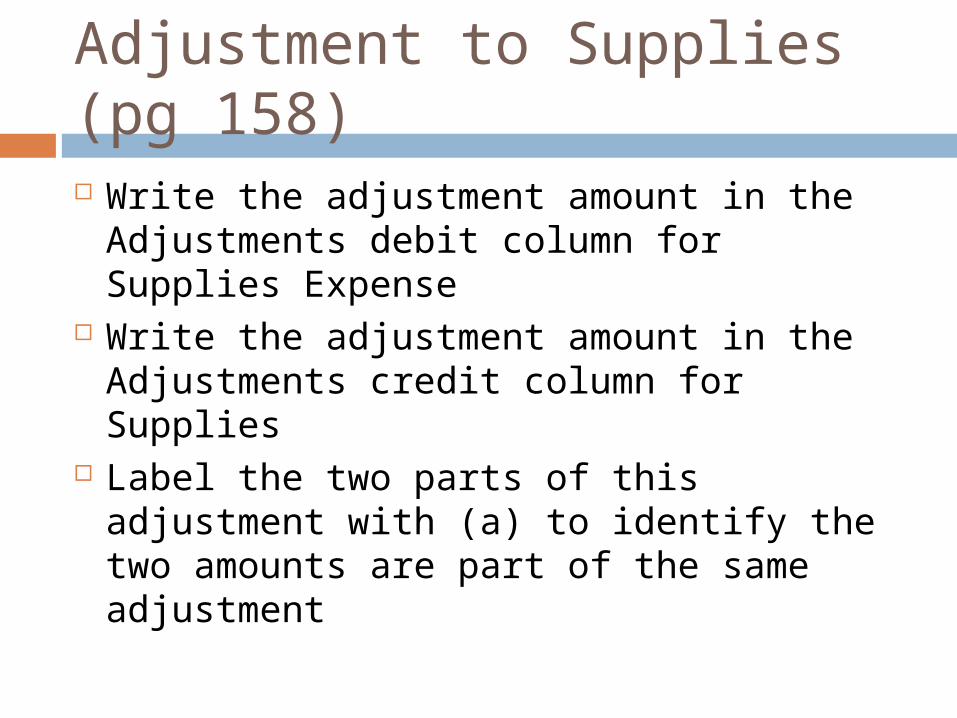

Adjustment to Supplies (pg 158) Write the adjustment amount in the

Adjustments debit column for Supplies Expense

Write the adjustment amount in the Adjustments credit column for Supplies

Label the two parts of this adjustment with (a) to identify the two amounts are part of the same adjustment

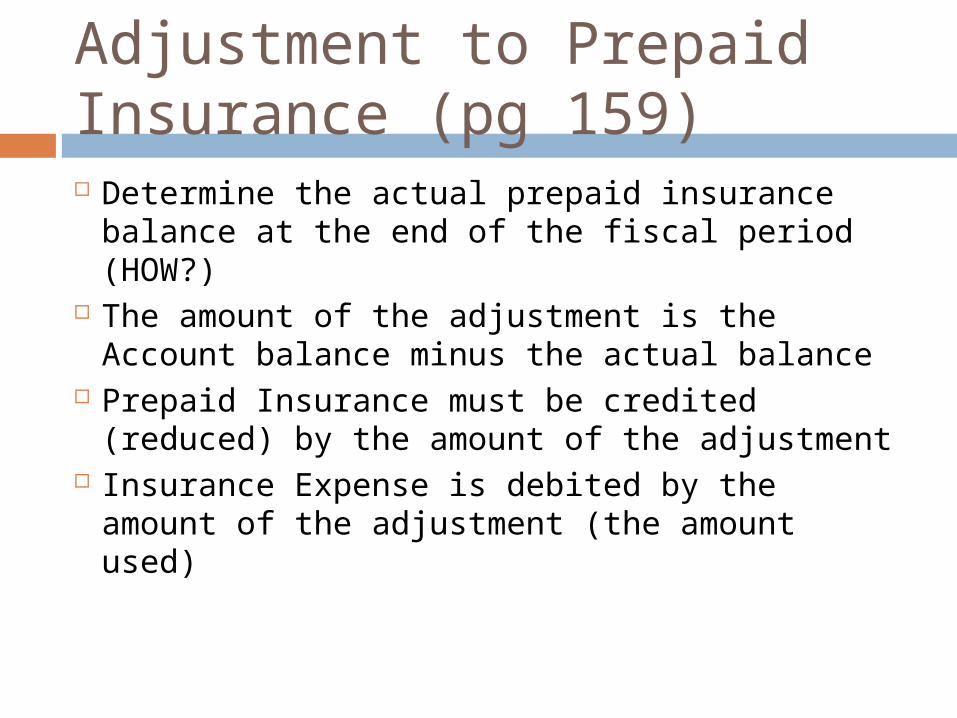

Adjustment to Prepaid Insurance (pg 159) Determine the actual prepaid insurance

balance at the end of the fiscal period (HOW?) The amount of the adjustment is the Account

balance minus the actual balance Prepaid Insurance must be credited (reduced)

by the amount of the adjustment Insurance Expense is debited by the amount

of the adjustment (the amount used)

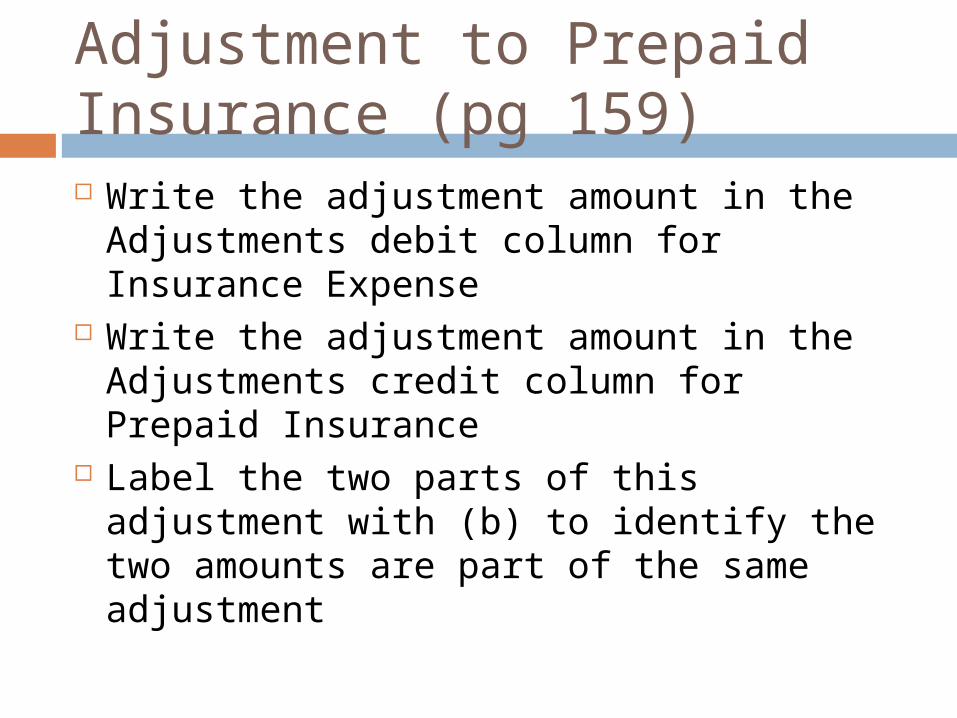

Adjustment to Prepaid Insurance (pg 159) Write the adjustment amount in the

Adjustments debit column for Insurance Expense

Write the adjustment amount in the Adjustments credit column for Prepaid Insurance

Label the two parts of this adjustment with (b) to identify the two amounts are part of the same adjustment

Proving Adjustments

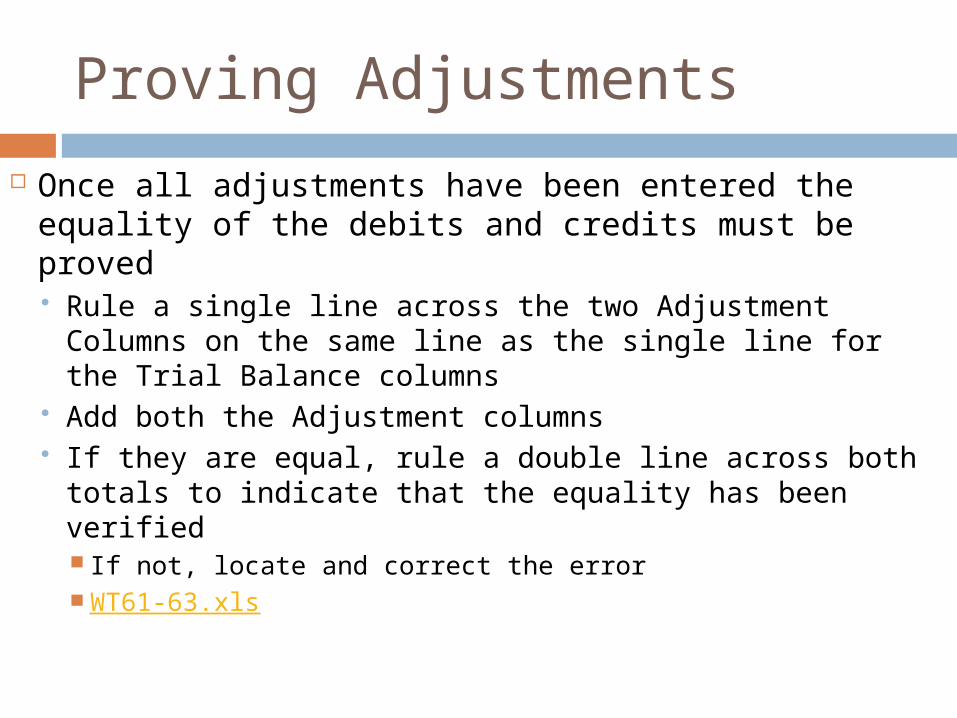

Once all adjustments have been entered the equality of the debits and credits must be proved Rule a single line across the two Adjustment

Columns on the same line as the single line for the Trial Balance columns

Add both the Adjustment columns If they are equal, rule a double line across both

totals to indicate that the equality has been verified If not, locate and correct the error WT61-63.xls

A Quick Review

CONCEPT: Consistent Reporting Accuracy and comparison

CONCEPT: Accounting Period Cycle Changes in financial information are

reported for a specific period of time in the form of financial statements aka Fiscal Period

Timing of the Fiscal Period

A Quick Review (cont’d)

Work Sheet Planning tool prepared in pencil

Trial Balance List all accounts in the first column Record debit and credit balances from the

General Ledger in the Trial Balance columns Prove debits = credits by totaling the two

Trial Balance Columns Rule a double line to indicate proof is verified WT61-63.xls

A Quick Review (yes, there’s more) CONCEPT: Matching Revenue with Expenses

Revenue from business activities and expenses associated with earning that revenue are recorded in the same accounting period

Adjustments to specific asset accounts are required to apply this CONCEPT and to update General Ledger balances Transform assets to expenses

Supplies and Prepaid Insurance

A Quick Review (that’s taking so long)

Adjustments are made in the second set of columns of the worksheet

Actual levels of supplies and prepaid insurance are determined

The actual levels of these assets are subtracted from the General Ledger account balances to determine the amount of adjustment

Last Review Slide (really)

Adjustments are entered as CREDITS to the asset accounts and DEBITS to the corresponding expense accounts

Small letters in parentheses are included to help match the entries

The adjustment columns are proved by totaling each column at the same point as the Trial Balance

Proof of debits = credits is verified by ruling a double line under the totals

Accounting CONCEPT

Accounting Period Cycle Financial statements are prepared at the

end of the accounting period cycle Can be weekly, monthly, quarterly or annually A company can prepare statements at any time SEC requires publically traded corporations to

publish financial statements quarterly (10-Q) and annually (10K)

What is the benefit of preparing financial statements?

Balance Sheet

A financial statement that reports the assets, liabilities and owner’s equity on a specific date

Snap shot in time Balance sheet account balances are

extended to the Balance Sheet Debit and Credit columns of the Work Sheet

The balance for Supplies and Prepaid Insurance are reduced by the credits in the adjustment columns

Income Statement

A financial statement showing the revenue and expenses for a fiscal period

Statement of flow Up to date balances for income

statement accounts are extended to the Income Statement Debit and Credit columns of the worksheet

Supplies Expense and Insurance Expense are included

Net Income/Loss

Total revenue – total expenses equals net income or loss for the fiscal period If revenue>expenses, then Net Income If revenue<expenses, then Net Loss

Net Income/Loss must be calculated before the Work Sheet can be balanced and ruled

Calculating Net Income/Loss

Rule a single line across the Income Stmt and Balance Sheet Columns

Total the columns and record the totals below the single line

Subtract total debits from total credits in the Income Statement columns (Revenue – Expenses)

Recording Net Income/Loss If the result is greater than zero, record the

net income below the total in the debit column If the result is less than zero, record the net

loss below the total in the credit Extend the entry to the balance sheet item

Net Income is recorded as a Credit (why?) Net Loss is recorded as a Debit (why?)

Rule a single line below the four columns Total the columns and rule a double line to

indicate proof that debits = credits

Practice and Review

Turn to page 160 to review the preparation of a Work Sheet using the book overlays

WT61-63.xls

Correcting Errors on the Work Sheet Errors are often detected only during the

preparation of the Work Sheet How do you know there is an error?

Errors on the Work Sheet must be corrected before financial statements can be prepared It is best to correct all mistakes in the Trial

Balance before moving any further Then, any additional errors occur on the Work

Sheet alone

Typical Calculation Errors

The difference is 1 ($.01, $.1, etc.) Math error – Redo calculations

The difference is divisible by 2 Look for the amount in the trial balance

column, it is likely that an item was entered in the wrong column

The difference is divisible by 9 A slide occurs when numbers are moved

one decimal place to the left or right ($25 becomes ($250)

Typical Calculation Errors

The difference is an omitted amount Look for an amount equal to the difference Often, that item has not been extended to

the Work Sheet’s Trial Balance How do you prevent errors?

Checking for Errors in the Work Sheet Check for errors in the Trial Balance

Column Have all General Ledger account balances

been entered and in the correct columns Check for errors in the Adjustment

Columns Check for errors in the Income

Statement and Balance Sheet columns

Correcting an Error in Posting to the Wrong Account Draw a line through the entire incorrect

entry Recalculate the account balance and

correct the work sheet Record the posting in the correct

account Recalculate the account balance and

correct the work sheet

Correcting an Incorrect Amount in the General Ledger

Draw a line through the incorrect amount

Write the correct amount just aboive the correction in the same space

Recalculate the account balance and correct the balance on the work sheet

Correcting an Amount Posted to the Wrong Column Draw a line through the incorrect item in

the account Record the posting in the correct amount

column Recalculate the balance Correct the Work Sheet

Checking for Errors in Journal Entries Do debits equal credits?

You can total journal columns on each page to check for accuracy

Were transactions recorded for the correct accounts?

Have all transactions been recorded? How do you know?

WT 6-4.xls