Embed Size (px)

Citation preview

www.woodmac.com

Delivering commercial insight

What is This Stuff Really Worth?

A Wood Mackenzie Presentation forThe Center for Energy EconomicsBureau of Economic Geology2010 Annual Meeting and Natural Gas Forum

Edward M. KellyVice President, N Am. Gas and Power

November 29, 2010

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 2

The New Big Picture—The Resource is There, But…Gas is Available in Any Feasible Quantity at a Moderate Price …But It’s Not $4.00.

Short-Term: Through early 2012• Weighted by sluggish economic recovery and supply strength; coal displacement continues to

influence the gas market

Mid-Term: Late 2012 - 2016• With an increasing call on production as demand growth resumes, there is potential for growing

pains as the market transitions from retrenchment to expansion; prices rise to the $5.75 - $7 range.

Long-Term: 2016 and Beyond• Consistent demand growth appears likely, with the pace of growth shaped by coal retirements,

potential carbon legislation and long-term US domestic resource strength.

• With the rebuilding of the upstream, pricing remains moderate: $6.50 - $7.50

Within this Base Case view of the North American market, policy and politics will become increasingly influential, and can shift the fundamentals

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 3

What has it Taken to Get Prices Even Where they Are? A Coincidence of Strong Factors:

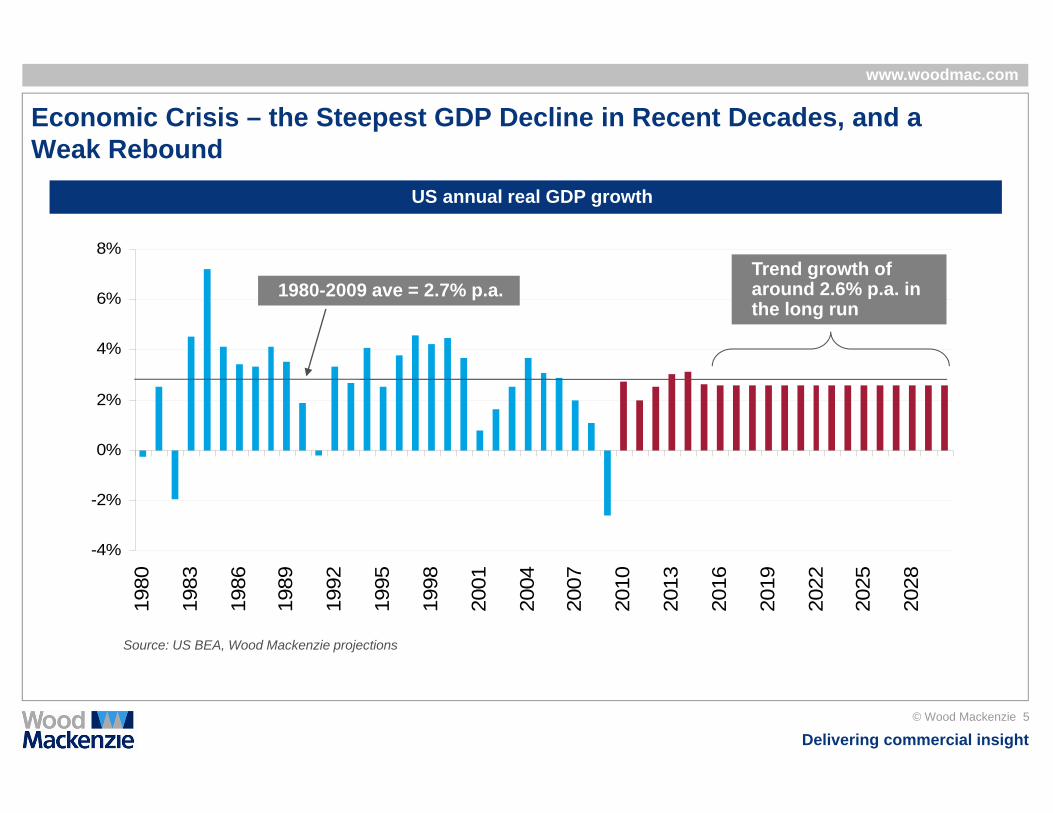

1) Economic Cataclysm• Steepest economic downturn since Great Depression …

• And a slower than average rebound

2) Demand Destruction• Approximately 1.3 Bcfd in the industrial sector in 2009, partially offset by coal displacement and

weather

3) A Production Peak• Highest rate since 1973

• Likely to see declines starting early-mid 2011

4) All-time High Storage • 1800 + Bcf, all-time high, for the spring inventory minimum

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 4

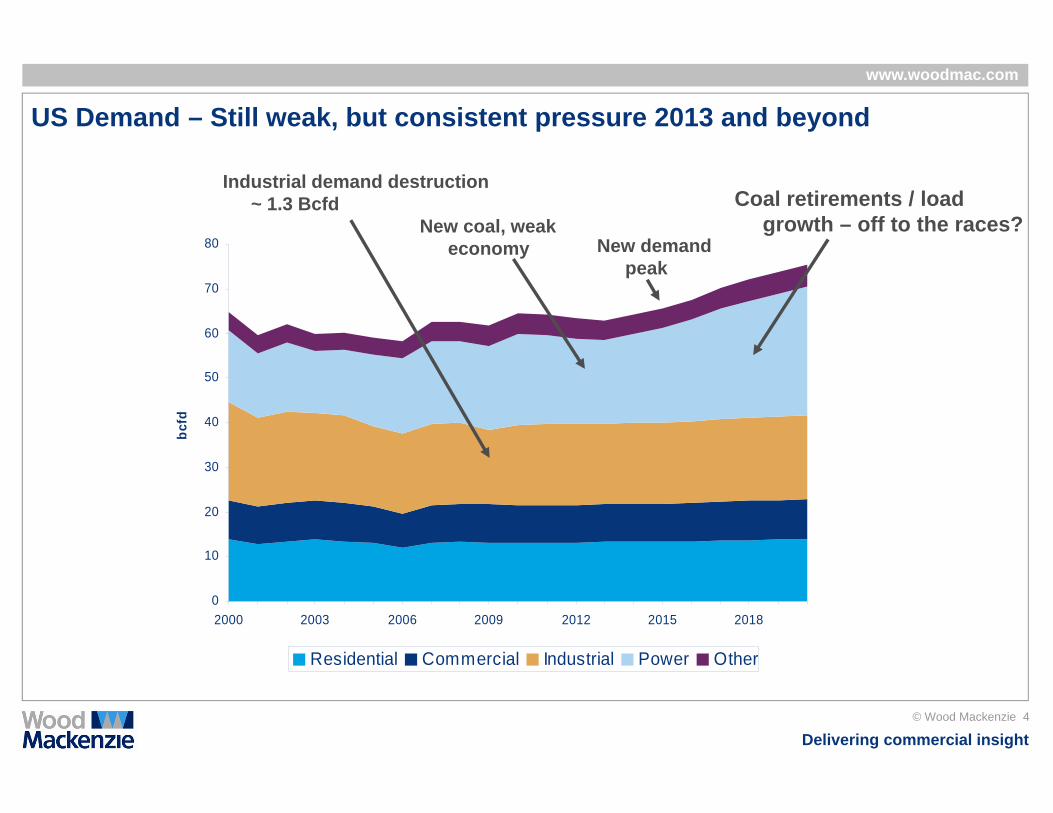

US Demand – Still weak, but consistent pressure 2013 and beyond

Industrial demand destruction ~ 1.3 Bcfd

0

10

20

30

40

50

60

70

80

2000 2003 2006 2009 2012 2015 2018

bcfd

Residential Commercial Industrial Power Other

New coal, weak economy

Coal retirements / load growth – off to the races?

New demand peak

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 5

Economic Crisis – the Steepest GDP Decline in Recent Decades, and a Weak Rebound

Source: US BEA, Wood Mackenzie projections

US annual real GDP growth

-4%

-2%

0%

2%

4%

6%

8%

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

2013

2016

2019

2022

2025

2028

Trend growth of around 2.6% p.a. in the long run

1980-2009 ave = 2.7% p.a.

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 6

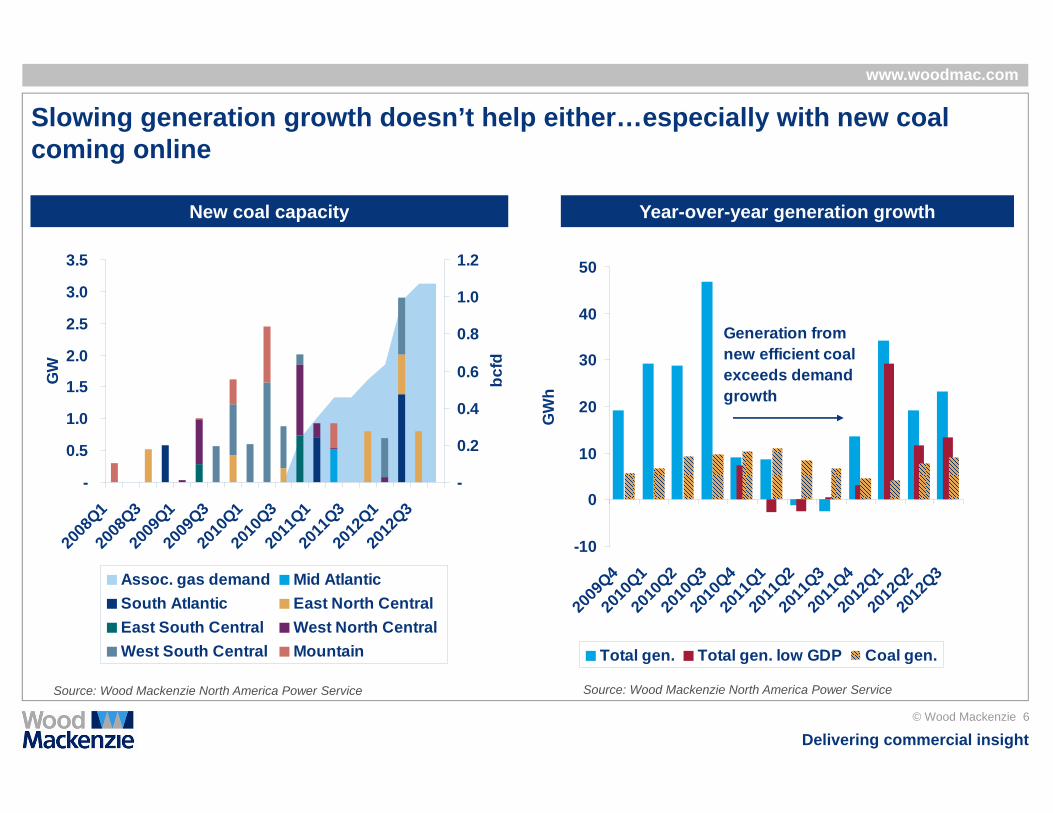

Slowing generation growth doesn’t help either…especially with new coal coming online

New coal capacity Year-over-year generation growth

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2008

Q120

08Q3

2009

Q120

09Q3

2010

Q120

10Q3

2011

Q120

11Q3

2012

Q120

12Q3

GW

-

0.2

0.4

0.6

0.8

1.0

1.2

bcfd

Assoc. gas demand Mid AtlanticSouth Atlantic East North CentralEast South Central West North CentralWest South Central Mountain

-10

0

10

20

30

40

50

2009

Q420

10Q1

2010

Q220

10Q3

2010

Q420

11Q1

2011

Q220

11Q3

2011

Q420

12Q1

2012

Q220

12Q3

GW

h

Total gen. Total gen. low GDP Coal gen.

Generation from new efficient coal exceeds demand growth

Source: Wood Mackenzie North America Power Service Source: Wood Mackenzie North America Power Service

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 7

-0.51.01.52.02.53.03.54.04.55.0

Jan-09

Apr-09

Jul-0

9Oct-

09Ja

n-10Apr

-10Ju

l-10

Oct-10

Jan-11

Apr-11

Jul-1

1Oct-

11

bcfd

-2.5-2.0-1.5-1.0-0.5-0.51.01.5

$/m

mbt

u

Mid Atlantic South Atlantic East South CentralOther Coal-gas spread

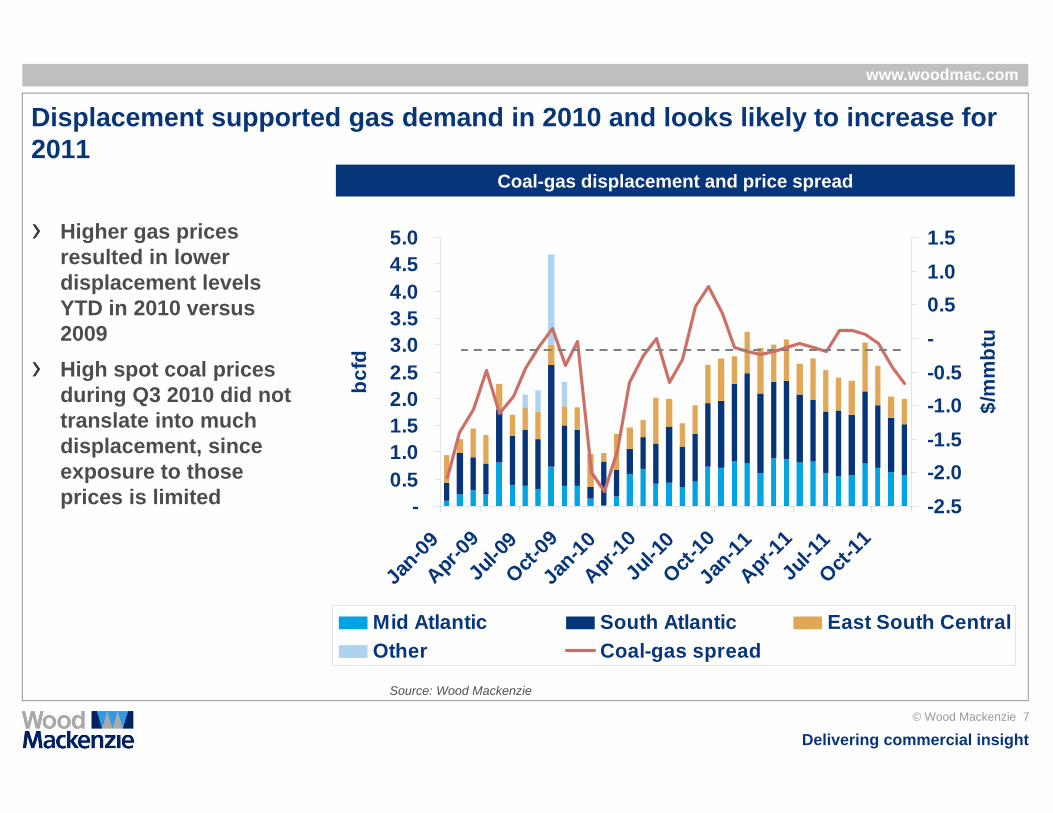

Displacement supported gas demand in 2010 and looks likely to increase for 2011

Higher gas prices resulted in lower displacement levels YTD in 2010 versus 2009High spot coal prices during Q3 2010 did not translate into much displacement, since exposure to those prices is limited

Coal-gas displacement and price spread

Source: Wood Mackenzie

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 8

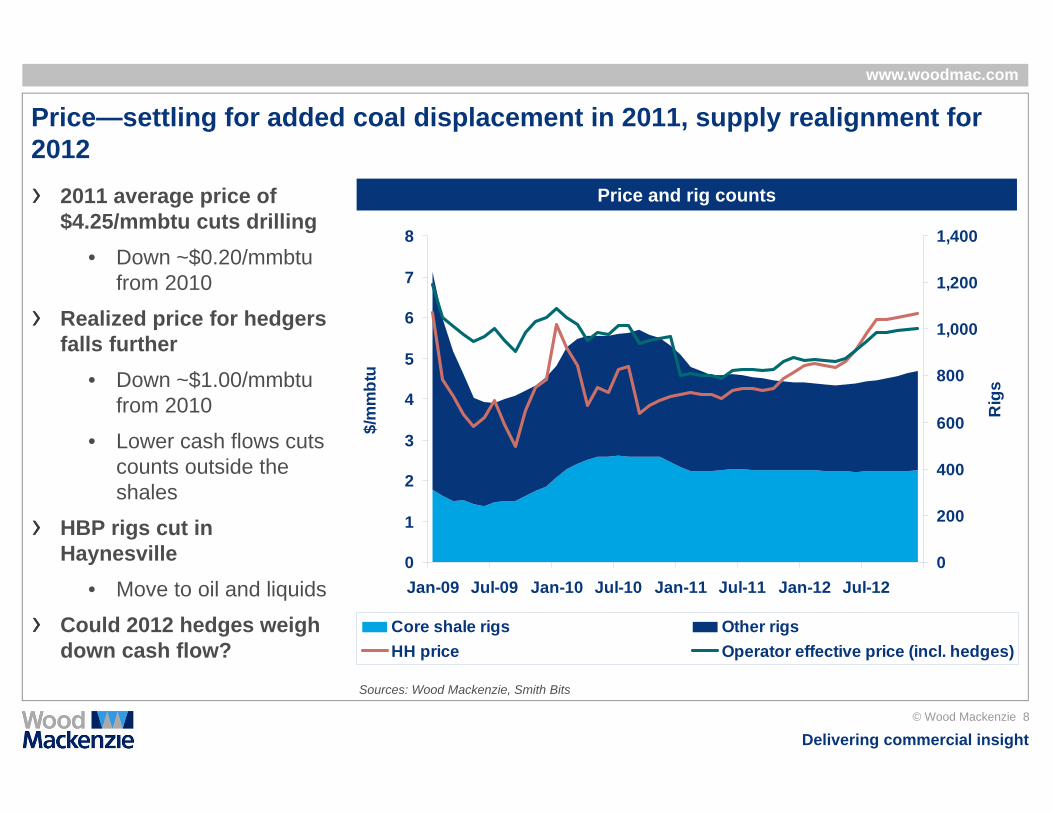

Price—settling for added coal displacement in 2011, supply realignment for 2012

2011 average price of $4.25/mmbtu cuts drilling

• Down ~$0.20/mmbtu from 2010

Realized price for hedgers falls further

• Down ~$1.00/mmbtu from 2010

• Lower cash flows cuts counts outside the shales

HBP rigs cut in Haynesville

• Move to oil and liquids

Could 2012 hedges weigh down cash flow?

Price and rig counts

0

1

2

3

4

5

6

7

8

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12

$/m

mbt

u

0

200

400

600

800

1,000

1,200

1,400

Rig

s

Core shale rigs Other rigsHH price Operator effective price (incl. hedges)

Sources: Wood Mackenzie, Smith Bits

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 9

55.5

56.0

56.5

57.0

57.5

58.0

58.5

59.0

59.5

2009 2010 2011 2012 2013 2014

bcfd

0

100

200

300

400

500

600

US Production Key Shale Other Rigs

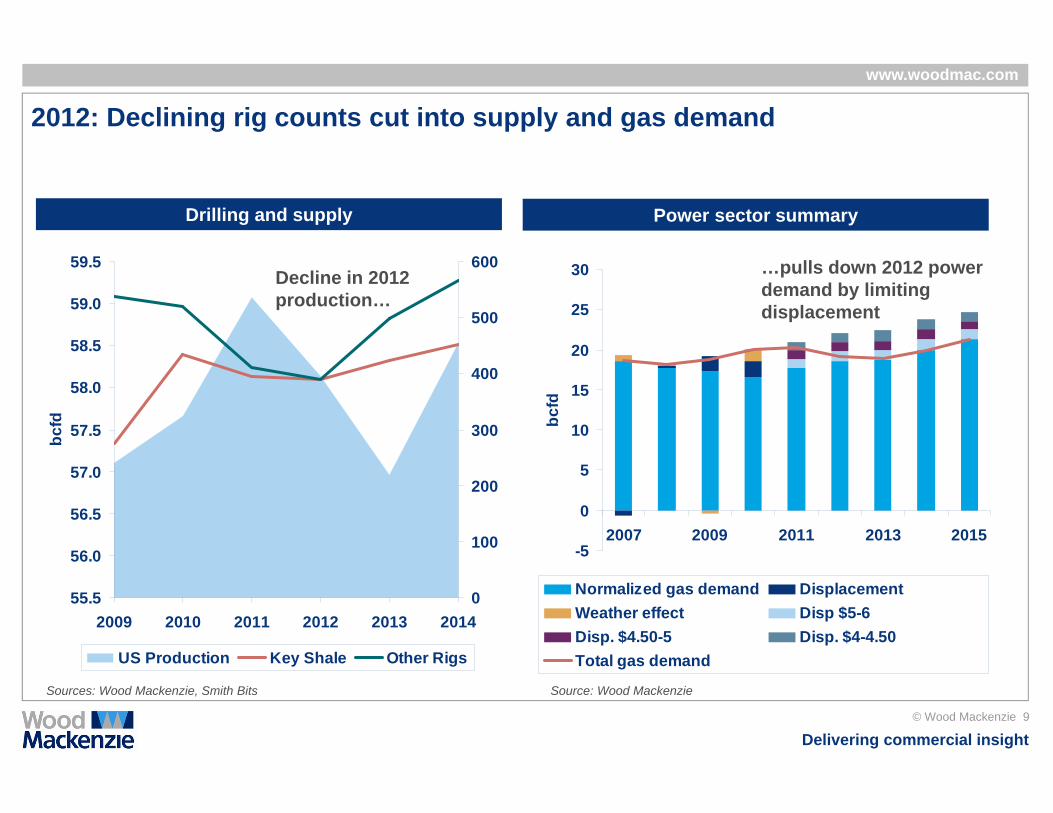

2012: Declining rig counts cut into supply and gas demand

Power sector summary

-5

0

5

10

15

20

25

30

2007 2009 2011 2013 2015bc

fd

Normalized gas demand DisplacementWeather effect Disp $5-6Disp. $4.50-5 Disp. $4-4.50Total gas demand

Drilling and supply

Decline in 2012 production…

…pulls down 2012 power demand by limiting displacement

Sources: Wood Mackenzie, Smith Bits Source: Wood Mackenzie

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 10

Drilling down the price: short-term market messages

Market soft again in 2011• Demand weakened by decelerating GDP, new coal

• Supply growth continues, but rig counts decline as HBPs, favorable hedges fade

• Added displacement balances the market

• Firming coal markets limit the price declines—Henry Hub price of $4.25/mmbtu

• Downside risk into upper $3/mmbtu from La Nina, coal market downshift, potential double-dip

2012-’13 markets transition to higher price levels• Demand potential increases, realized demand declines

• Supply drops off, competition with oil and liquids mutes rig increase as prices recover

• Henry Hub prices in the $5/mmbtu range, aligned drilling-price incentives reduce downside risk

Risks to outlook• Haynesville is key, higher-than-expected drilling levels or improved well performance would

hold price down

• How does oil play out?

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 11

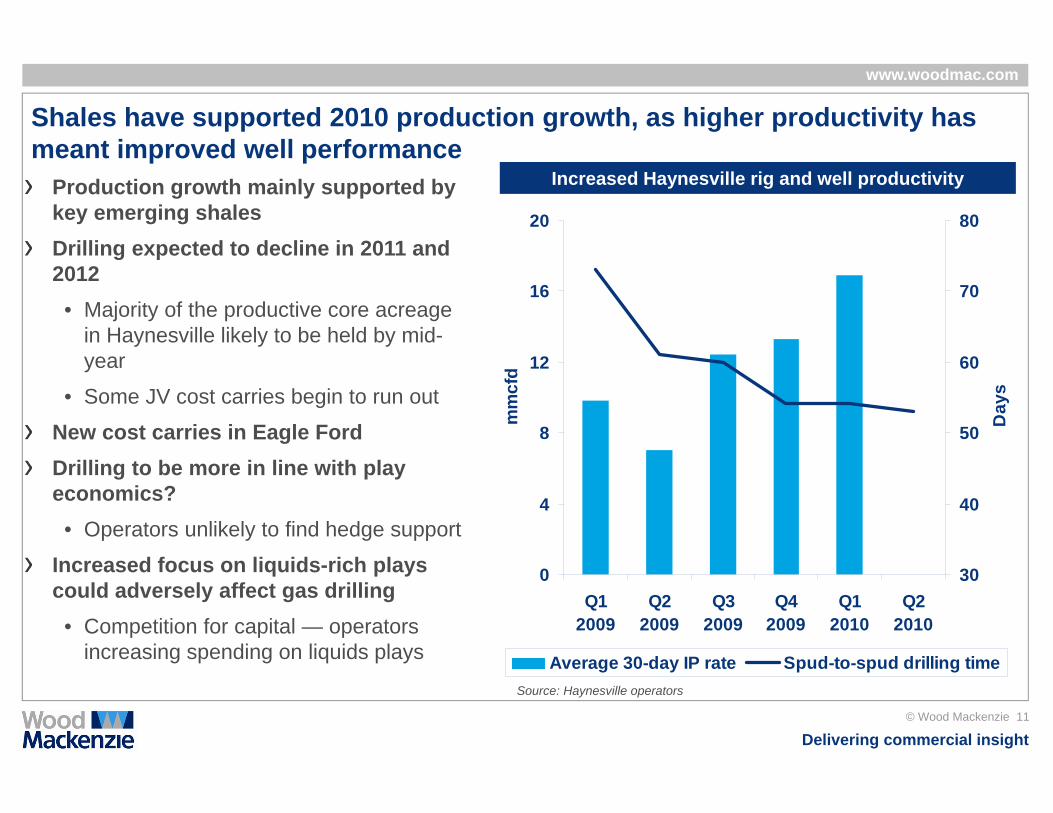

Shales have supported 2010 production growth, as higher productivity has meant improved well performance

Production growth mainly supported by key emerging shalesDrilling expected to decline in 2011 and 2012

• Majority of the productive core acreage in Haynesville likely to be held by mid-year

• Some JV cost carries begin to run out

New cost carries in Eagle FordDrilling to be more in line with play economics?

• Operators unlikely to find hedge support

Increased focus on liquids-rich plays could adversely affect gas drilling

• Competition for capital — operators increasing spending on liquids plays

Increased Haynesville rig and well productivity

0

4

8

12

16

20

Q12009

Q22009

Q32009

Q42009

Q12010

Q22010

mm

cfd

30

40

50

60

70

80

Day

s

Average 30-day IP rate Spud-to-spud drilling timeSource: Haynesville operators

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 12

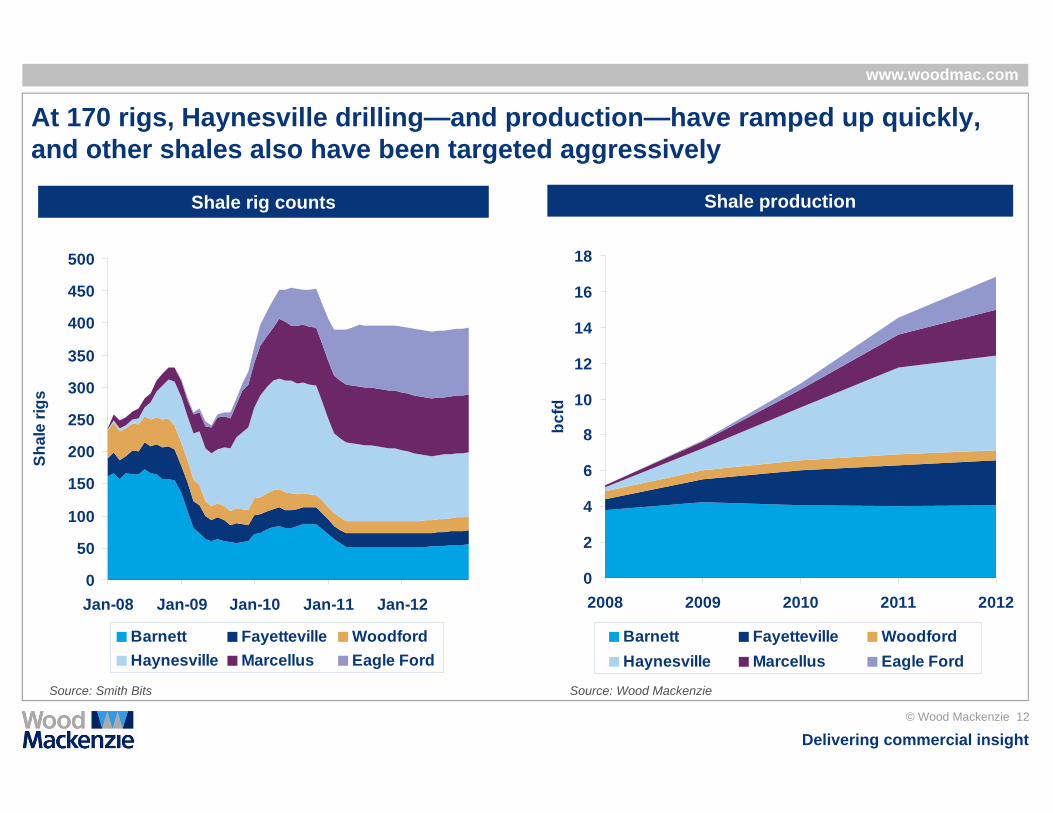

At 170 rigs, Haynesville drilling—and production—have ramped up quickly, and other shales also have been targeted aggressively

Shale rig counts Shale production

0

2

4

6

8

10

12

14

16

18

2008 2009 2010 2011 2012

bcfd

Barnett Fayetteville WoodfordHaynesville Marcellus Eagle Ford

Source: Wood MackenzieSource: Smith Bits

0

50

100

150

200

250

300

350

400

450

500

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Shal

e rig

s

Barnett Fayetteville WoodfordHaynesville Marcellus Eagle Ford

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 13

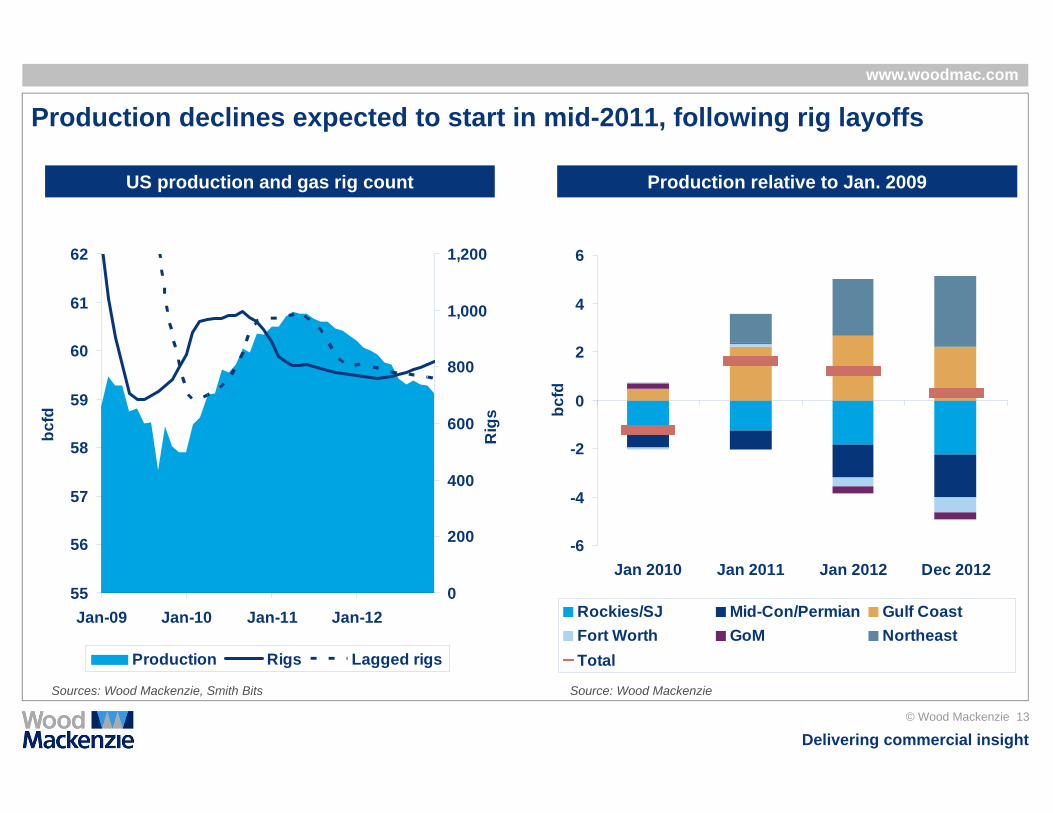

Production declines expected to start in mid-2011, following rig layoffs

Production relative to Jan. 2009US production and gas rig count

55

56

57

58

59

60

61

62

Jan-09 Jan-10 Jan-11 Jan-12

bcfd

0

200

400

600

800

1,000

1,200

Rig

s

Production Rigs Lagged rigs

-6

-4

-2

0

2

4

6

Jan 2010 Jan 2011 Jan 2012 Dec 2012bc

fd

Rockies/SJ Mid-Con/Permian Gulf CoastFort Worth GoM NortheastTotal

Source: Wood MackenzieSources: Wood Mackenzie, Smith Bits

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 14

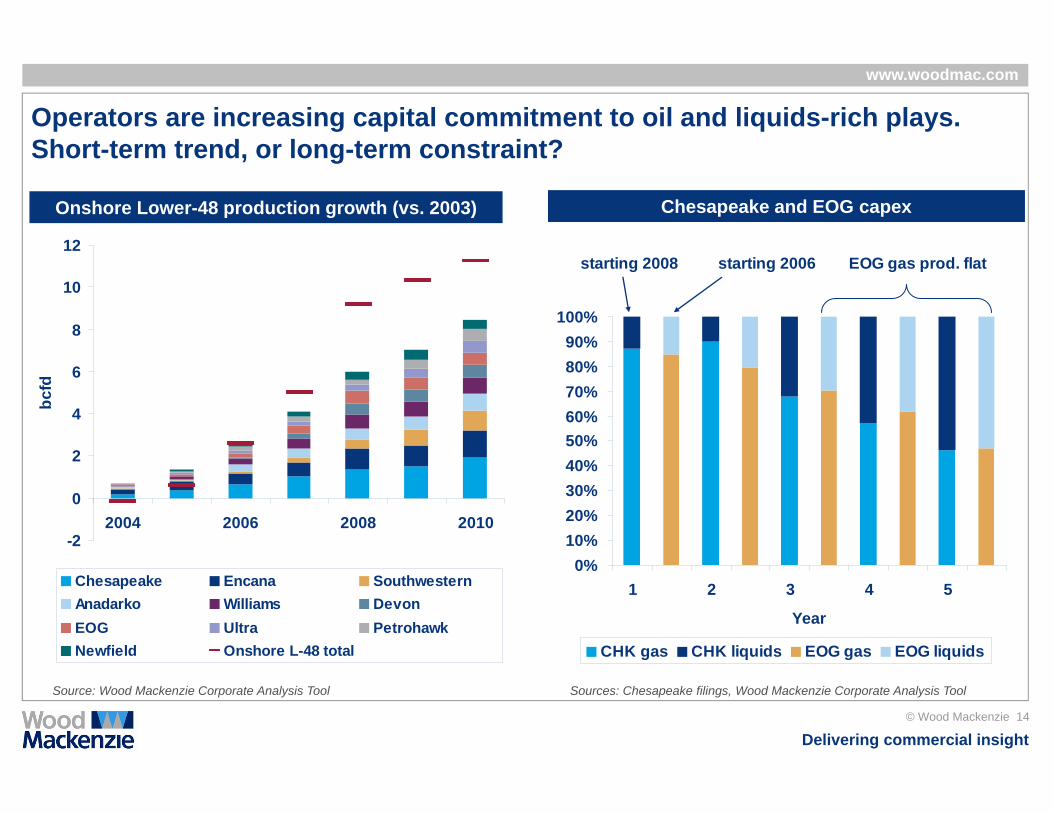

Operators are increasing capital commitment to oil and liquids-rich plays. Short-term trend, or long-term constraint?

Onshore Lower-48 production growth (vs. 2003) Chesapeake and EOG capex

-2

0

2

4

6

8

10

12

2004 2006 2008 2010

bcfd

Chesapeake Encana SouthwesternAnadarko Williams DevonEOG Ultra PetrohawkNewfield Onshore L-48 total

Sources: Chesapeake filings, Wood Mackenzie Corporate Analysis ToolSource: Wood Mackenzie Corporate Analysis Tool

0%10%20%30%40%50%60%70%80%90%

100%

1 2 3 4 5

Year

CHK gas CHK liquids EOG gas EOG liquids

starting 2008 starting 2006 EOG gas prod. flat

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 15

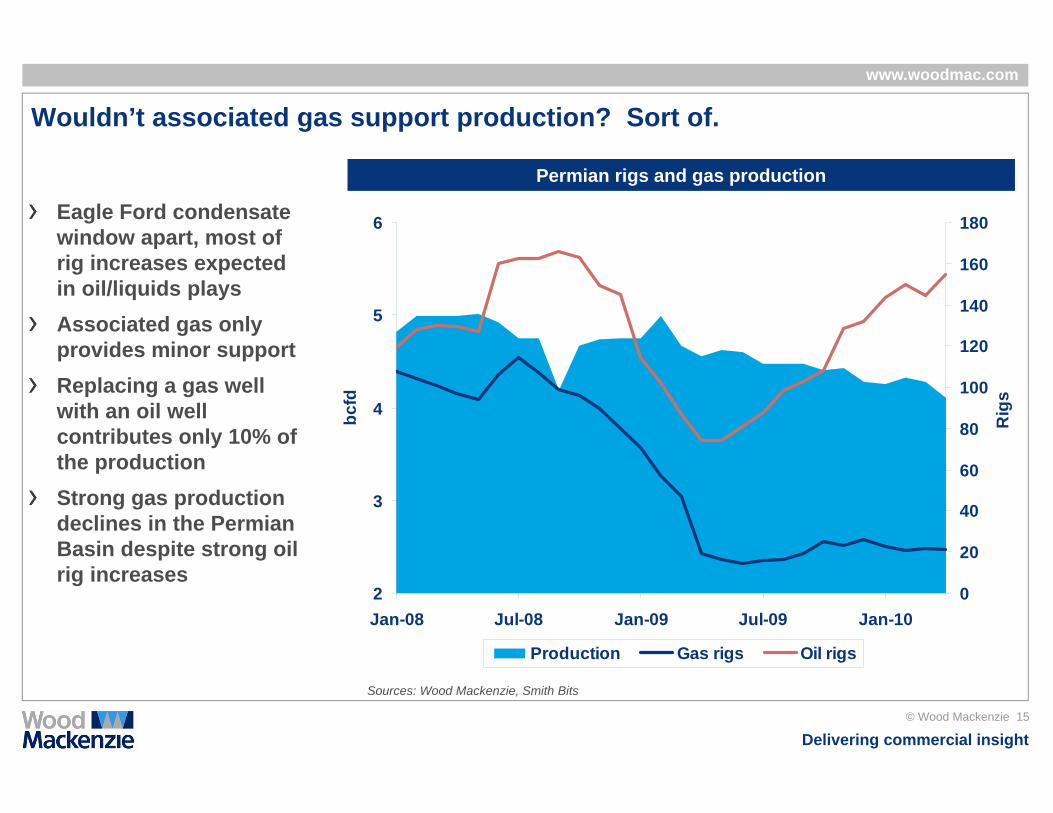

Wouldn’t associated gas support production? Sort of.

Eagle Ford condensate window apart, most of rig increases expected in oil/liquids playsAssociated gas only provides minor supportReplacing a gas well with an oil well contributes only 10% of the productionStrong gas production declines in the Permian Basin despite strong oil rig increases

Permian rigs and gas production

2

3

4

5

6

Jan-08 Jul-08 Jan-09 Jul-09 Jan-10

bcfd

0

20

40

60

80

100

120

140

160

180

Rig

s

Production Gas rigs Oil rigs

Sources: Wood Mackenzie, Smith Bits

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 16

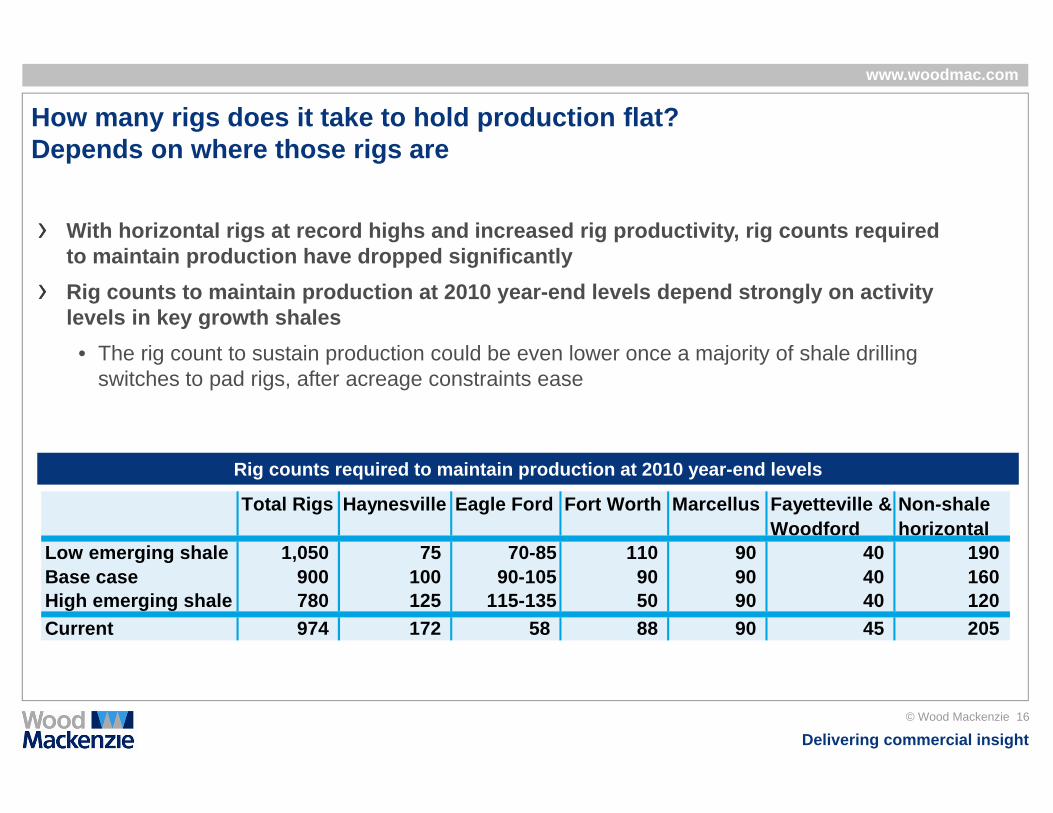

How many rigs does it take to hold production flat?Depends on where those rigs are

With horizontal rigs at record highs and increased rig productivity, rig counts required to maintain production have dropped significantlyRig counts to maintain production at 2010 year-end levels depend strongly on activity levels in key growth shales

• The rig count to sustain production could be even lower once a majority of shale drilling switches to pad rigs, after acreage constraints ease

Rig counts required to maintain production at 2010 year-end levels

Total Rigs Haynesville Eagle Ford Fort Worth Marcellus Fayetteville & Woodford

Non-shale horizontal

Low emerging shale 1,050 75 70-85 110 90 40 190Base case 900 100 90-105 90 90 40 160High emerging shale 780 125 115-135 50 90 40 120Current 974 172 58 88 90 45 205

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 17

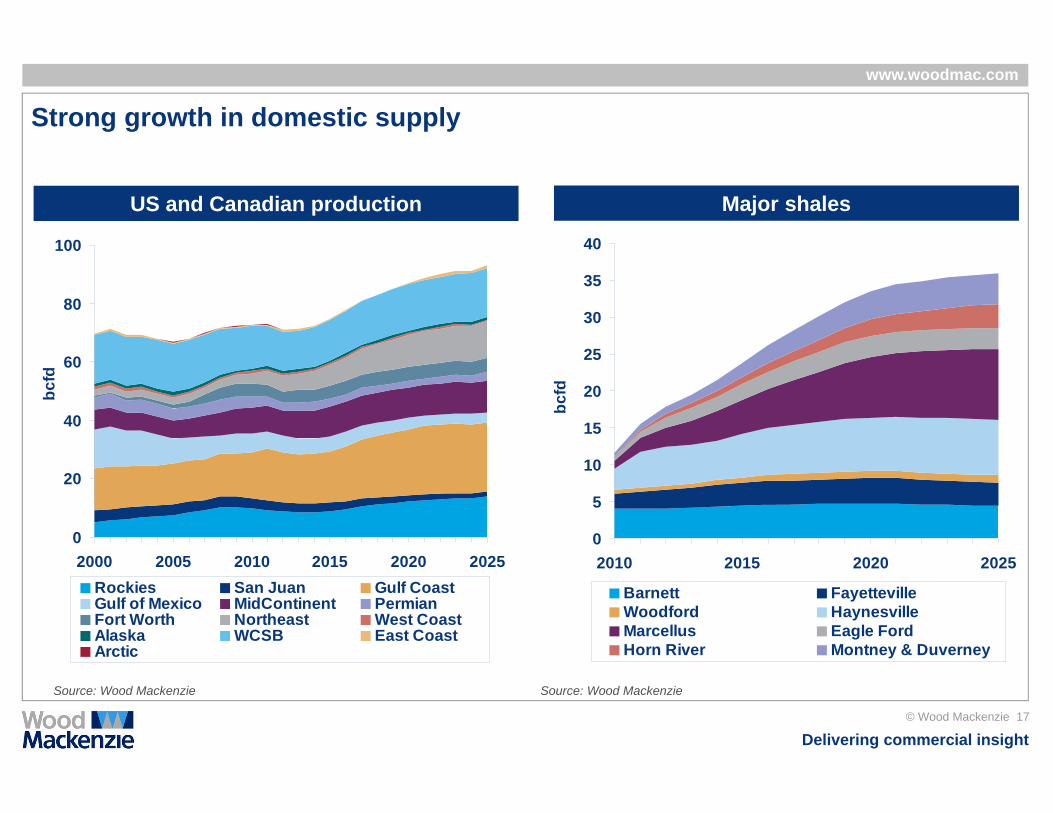

Strong growth in domestic supply

US and Canadian production Major shales

0

20

40

60

80

100

2000 2005 2010 2015 2020 2025

bcfd

Rockies San Juan Gulf CoastGulf of Mexico MidContinent PermianFort Worth Northeast West CoastAlaska WCSB East CoastArctic

0

5

10

15

20

25

30

35

40

2010 2015 2020 2025bc

fd

Barnett FayettevilleWoodford HaynesvilleMarcellus Eagle FordHorn River Montney & Duverney

Source: Wood MackenzieSource: Wood Mackenzie

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 18

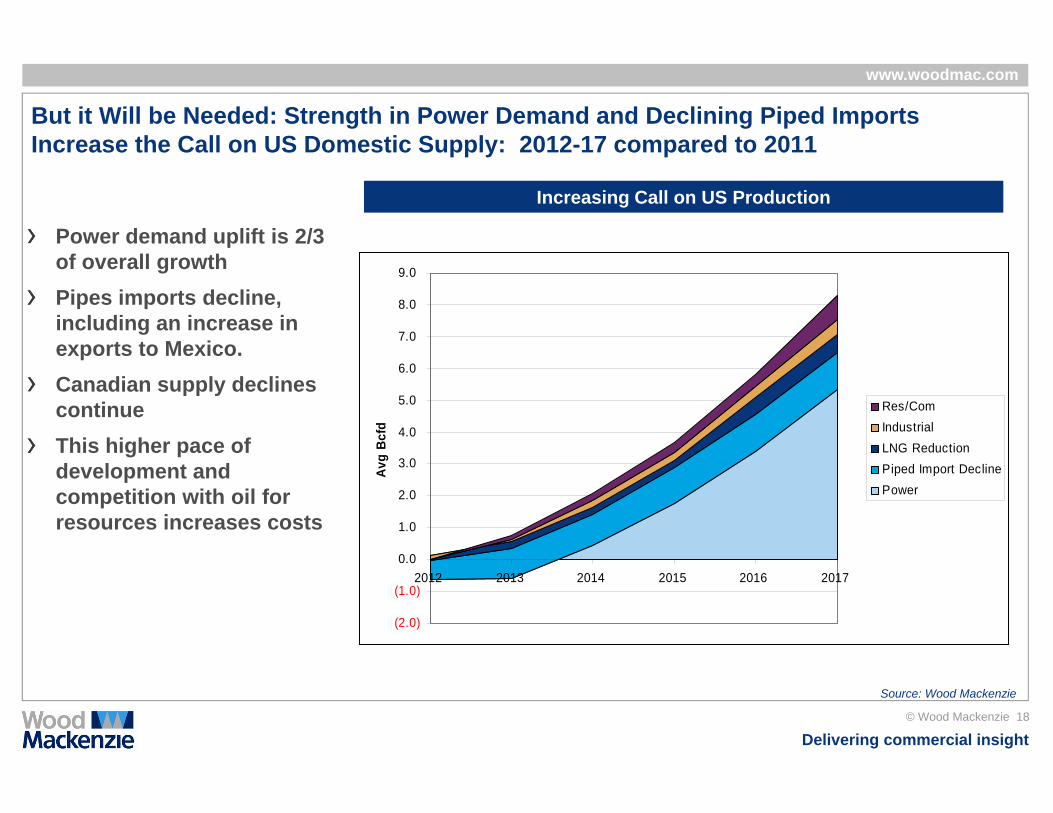

But it Will be Needed: Strength in Power Demand and Declining Piped Imports Increase the Call on US Domestic Supply: 2012-17 compared to 2011

Power demand uplift is 2/3 of overall growthPipes imports decline, including an increase in exports to Mexico.Canadian supply declines continueThis higher pace of development and competition with oil for resources increases costs

Increasing Call on US Production

Source: Wood Mackenzie

(2.0)

(1.0)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2012 2013 2014 2015 2016 2017

Avg

Bcfd

Res/ComIndustrialLNG ReductionPiped Import DeclinePower

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 19

30

35

40

45

50

55

60

65

70

75

80

2000 2004 2008 2012 2016 2020 2024

bcfd

Other Key Shale

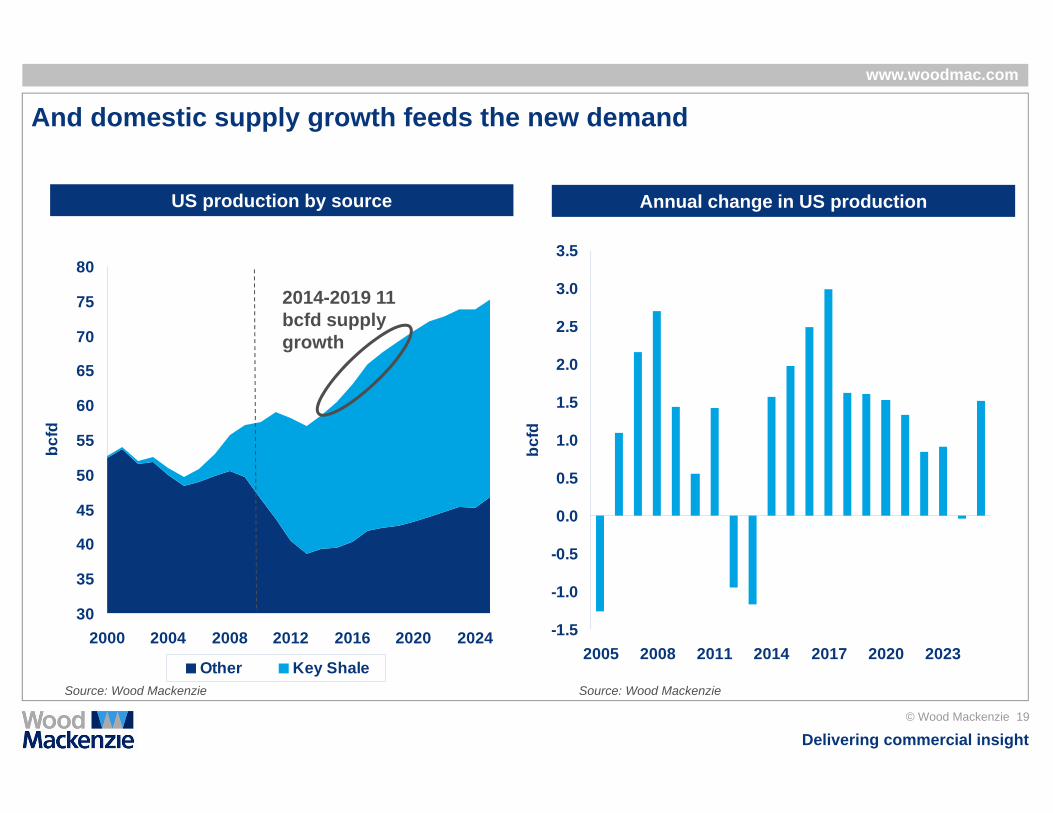

And domestic supply growth feeds the new demand

US production by source Annual change in US production

2014-2019 11 bcfd supply growth

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2005 2008 2011 2014 2017 2020 2023

bcfd

Source: Wood MackenzieSource: Wood Mackenzie

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 20

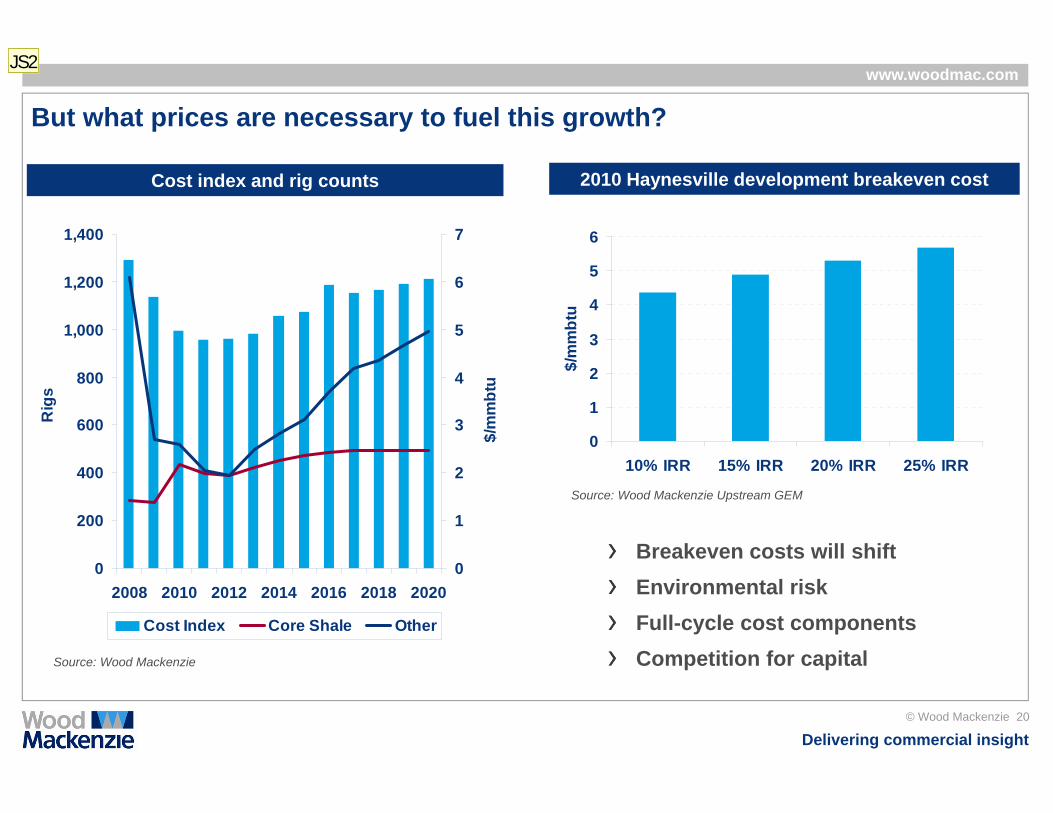

But what prices are necessary to fuel this growth?

Cost index and rig counts 2010 Haynesville development breakeven cost

Breakeven costs will shiftEnvironmental riskFull-cycle cost componentsCompetition for capital

0

200

400

600

800

1,000

1,200

1,400

2008 2010 2012 2014 2016 2018 2020

Rig

s

0

1

2

3

4

5

6

7

$/m

mbt

u

Cost Index Core Shale Other

0

1

2

3

4

5

6

10% IRR 15% IRR 20% IRR 25% IRR

$/m

mbt

u

Source: Wood Mackenzie

Source: Wood Mackenzie Upstream GEM

JS2

Slide 20

JS2 Jen Snyder, 10/12/2010

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 21

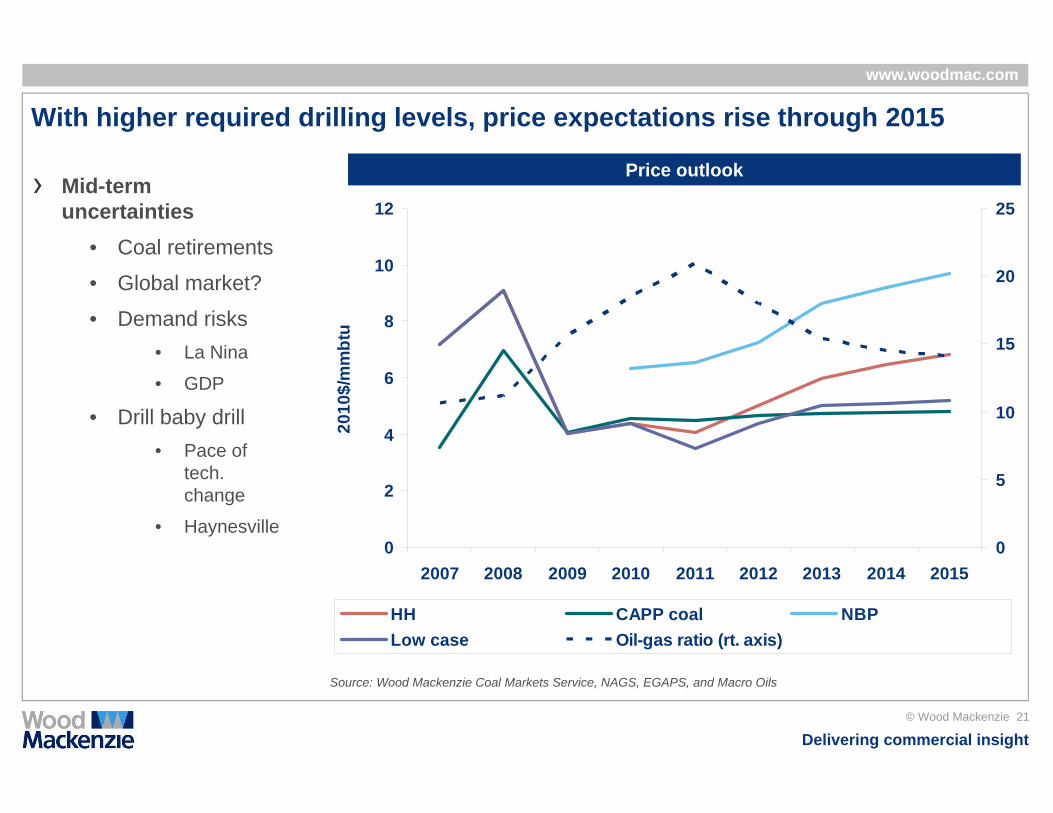

With higher required drilling levels, price expectations rise through 2015

Mid-term uncertainties

• Coal retirements

• Global market?

• Demand risks• La Nina

• GDP

• Drill baby drill• Pace of

tech. change

• Haynesville0

2

4

6

8

10

12

2007 2008 2009 2010 2011 2012 2013 2014 2015

2010

$/m

mbt

u

0

5

10

15

20

25

HH CAPP coal NBPLow case Oil-gas ratio (rt. axis)

Source: Wood Mackenzie Coal Markets Service, NAGS, EGAPS, and Macro Oils

Price outlook

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 22

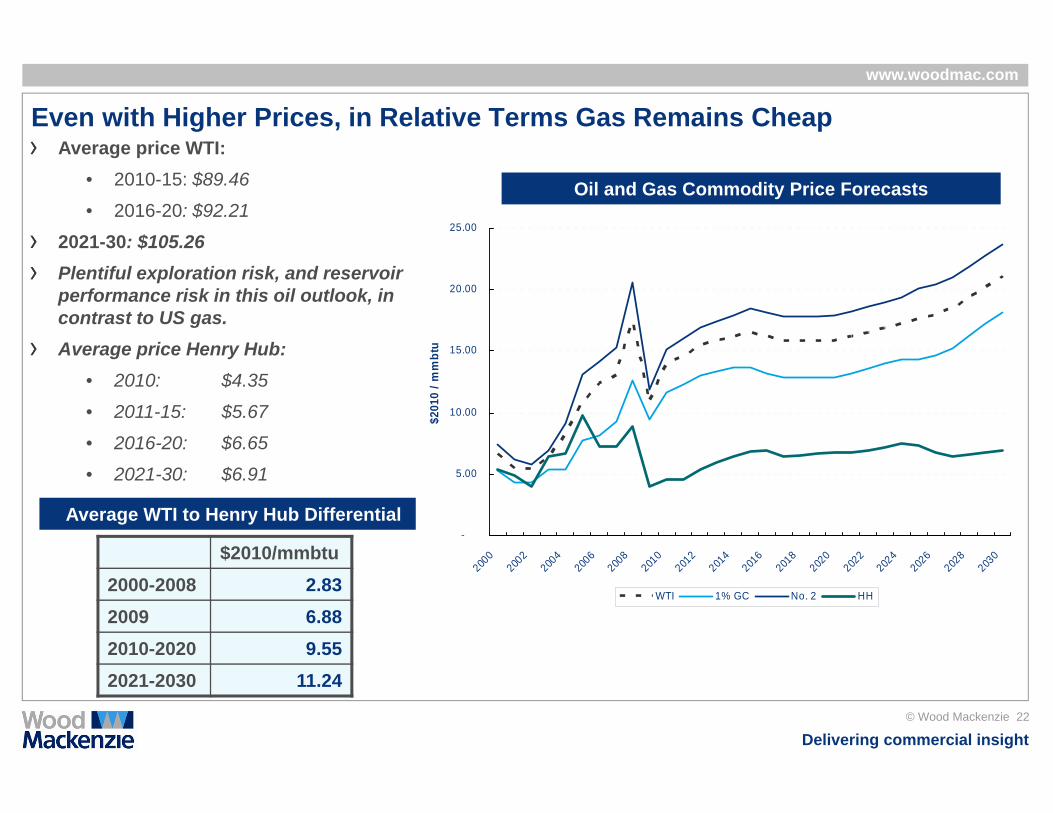

Even with Higher Prices, in Relative Terms Gas Remains Cheap

Oil and Gas Commodity Price Forecasts

Average price WTI:• 2010-15: $89.46

• 2016-20: $92.21

2021-30: $105.26Plentiful exploration risk, and reservoir performance risk in this oil outlook, in contrast to US gas.Average price Henry Hub:

• 2010: $4.35

• 2011-15: $5.67

• 2016-20: $6.65

• 2021-30: $6.91

$2010/mmbtu2000-2008 2.832009 6.882010-2020 9.552021-2030 11.24

Average WTI to Henry Hub Differential-

5.00

10.00

15.00

20.00

25.00

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

$20

10 /

mm

btu

WTI 1% GC No. 2 HH

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 23

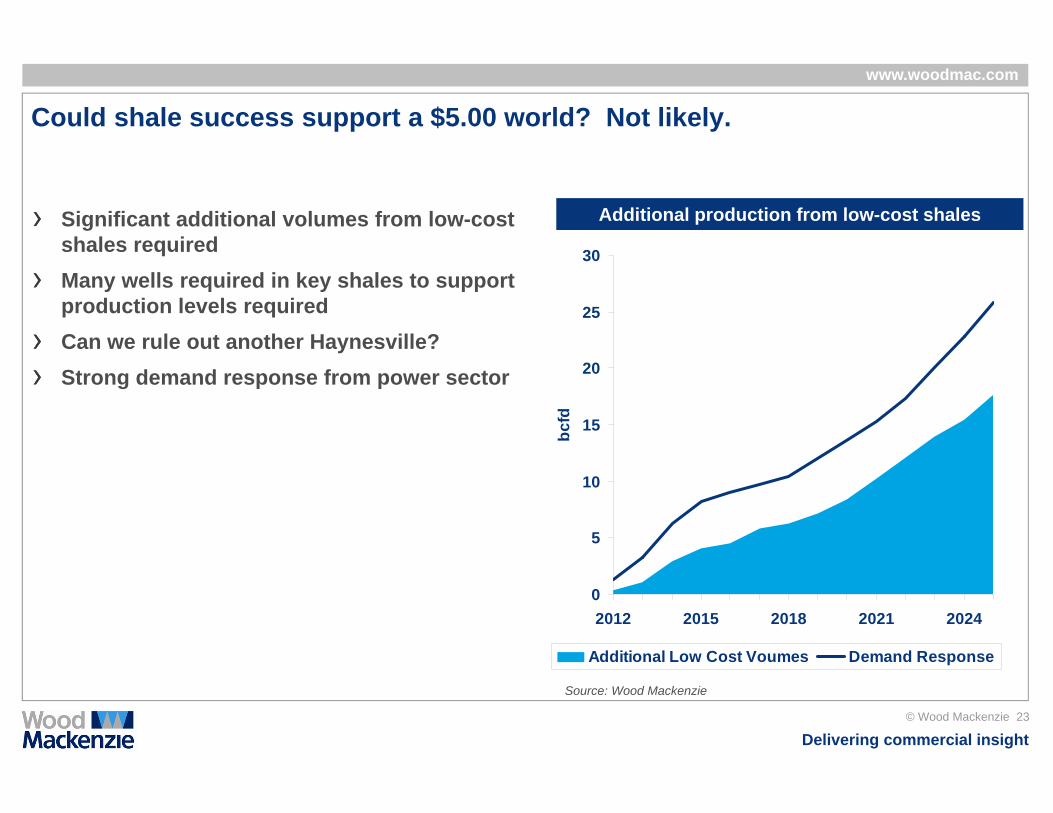

Could shale success support a $5.00 world? Not likely.

Significant additional volumes from low-cost shales requiredMany wells required in key shales to support production levels required Can we rule out another Haynesville?Strong demand response from power sector

Additional production from low-cost shales

0

5

10

15

20

25

30

2012 2015 2018 2021 2024

bcfd

Additional Low Cost Voumes Demand Response

Source: Wood Mackenzie

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 24

The Bottom Line

The Natural Gas Resource Base is There, But …

It’s Not a $4.00 - $5.00 Fuel

(Possibly $6-$7 though)

Source: Wood Mackenzie

Delivering commercial insight

www.woodmac.com

© Wood Mackenzie 25

Wood Mackenzie

Kintore House74-77 Queen StreetEdinburgh EH2 4NS

Global Contact Details

Europe +44 (0)131 243 4400Americas +1 713 470 1600Asia Pacific +65 6518 0800Email [email protected]

Global Offices

Australia - Canada - China - Japan - Malaysia - Russia - Singapore - South Africa - United Arab Emirates - United Kingdom - United States

Wood Mackenzie has been providing its unique range of research products and consulting services to the Energy industry for over 30 years. Wood Mackenzie provides forward-looking commercial insight that enables clients to make better business decisions. For more information visit: www.woodmac.com