Embed Size (px)

Citation preview

Highly confidential – not for distribution

A Way Forward On Pension and Retiree Health Care

1

Regina October 2013

Pension Plan Overview

2

Current State:

• CCWIPP is the multi-employer UFCW pension managed by a board of trustees – Coca-Cola has no say or influence in the management of those funds

• Regina employees participate in the union sponsored CCWIPP plan – contributions are made directly by Coca-Cola and Employees to CCWIPP on hourly basis per employee

• 7 UFCW represented Coca-Cola locations are in this plan in Canada – one of those 7 locations (Winnipeg) has recently ratified a collective agreement which involves them exiting the plan

• Other Coca-Cola UFCW locations participate in the Company’s pension plan as well as the Company’s Benefit Plus health care plan and Health Plus retiree medical plan. For many years, the Company has made contributions to CCWIPP on an hourly basis in order to ensure employees have a full pension: Coca-Cola has put millions of dollars into CCWIPP, and employee have been relying on having a solid pension down the road

• However, CCWIPP is simply not solvent enough to deliver on the pension that has been promised

CCWIPP By The Numbers

3

Company Contributions: • CCWIPP has been in trouble for some time. A recent CCWIPP amendment

will cut pension benefits (past service and future) by 20% for active members on or before January 1, 2014 – more cuts may come after that

• CCWIPP’s solvency situation has not improved despite benefit cuts AND more contributions from employers. In fact, it is worse than ever. Lower than even 2008.

• Today, the Company contributes $1.17 per hour per employee in Regina. You also put in $0.23 per hour for a total of $1.40 per hour. Based on full-time hours (no overtime) that is ~$3000 per year per person. Nationally, Coca-Cola puts well over $1MM into CCWIPP every year

• And yet on a solvency basis CCWIPP is in more trouble today than it has ever been: it is currently funded at 35% based on last valuation (down from 38% a year prior). In other words – there is only 35 cents of funding for every $1 promised in future benefits. That is not sustainable.

Proposed Company Solution

4

Leave CCWIPP, Protect Past Service, DC Going Forward. • The Company believes it is in the best interest of employees and Company to

withdraw from CCWIPP • The Company is proposing that Regina employees leave CCWIPP. The Company

would protect all of your past service in CCWIPP by promising to fund a substantial portion of the value of your pension at the date of withdrawal under a DB formula that mirrors the CCWIPP formula in our Company pension plan

• Also, currently employees in Regina do not have retiree medical program with

the Company. As part of the deal to leave CCWIPP, the Company would offer its retiree medical plan to eligible Regina employees

Proposed Company Solution (Continued)

5

Leave CCWIPP, Protect Past Service, DC Going Forward. • Going forward for future service, the Company would contribute 4% of salary

into the Company’s DC Pension Plan. Employees would contribute nothing! In addition, employees will continue to be eligible to participate in the Company’s ESIP program and get an additional 3% in Company contributions – that totals 7% of income given by the Company per year.

• Unlike CCWIPP contributions (which are based on 2080 hours), DC

contributions are paid on all hours worked including O/T, vacation, sick leave and STD (LTD, lump sums and pay in lieu do not qualify)

• CCR’s pension plan solvency is over 90% (vs CCWIPP at 35%)

CCWIPP Benefits Cuts are Likely

6

CCWIPP Cuts by January 1, 2014? • We have been provided with a signed CCWIPP amendment that suggests

that a 20% cut to your pension benefits – past and future – has already been approved by the CCWIPP Board of Trustees. Coca-Cola had no say and was not consulted on those changes. These cuts are effective on January 1, 2014.

• The current formula for CCWIPP for Regina is a monthly benefit of $39.10 X

years or service. If all past and future benefits are cut, the value of your pension will be cut by 20% and the current benefit rate will be reduced to $31.28 even if the same contributions keep being made.

• Staying in CCWIPP means more cuts are possible in the future!

CCWIPP Withdrawal Penalties

7

• Apart from any changes regarding cuts to pension benefit levels, CCWIPP rules also require that when a bargaining unit withdraws from the plan, the pensions payable to employees under 50 years old are immediately reduced by the current deficit - currently 65% (i.e. if a pension was worth $10K per year, it will now be worth $3500 per year).

• In other words, leaving CCWIPP creates a 65% reduction in the value of pensions for those under 50 years of age but the Company has a proposed solution for that. The remaining 35% is transferable.

• We have information that this “withdrawal penalty “ was recently

amended to apply to over 50s as well – we are in the process of validating that. If so, over 50s past service benefits will be reduced by 65% while continuing to be locked into CCWIPP – funds are not transferable and are subject to future cuts

Company Proposed Solve for Past Service

8

Protect Past Service • Despite already making contributions worth millions of dollars for past

service, the Company is prepared to pay again for past service and assume the liability for past service in its own pension plan (conditional upon agreement on all financial terms, Benefits Plus etc.);

• According to our actuaries, Towers Watson, for Regina, the cost to the Company of making 100% of the shortfall (based on a solvency ratio of 38%) for all employees would be ~$2MM: • ~$270K for employees under age 50; • ~$1.7MM for employees over age 50;

• For all UFCW CCWIPP locations, the total value represents ~$20MM • That represents approximately ~$30K per employee to again pay for past

service that the Company has already “paid for”. • Over 5 years, the cost for that for the Company is equivalent to giving every

employee in Regina a wage increase of 4.38% every year for full-time employees

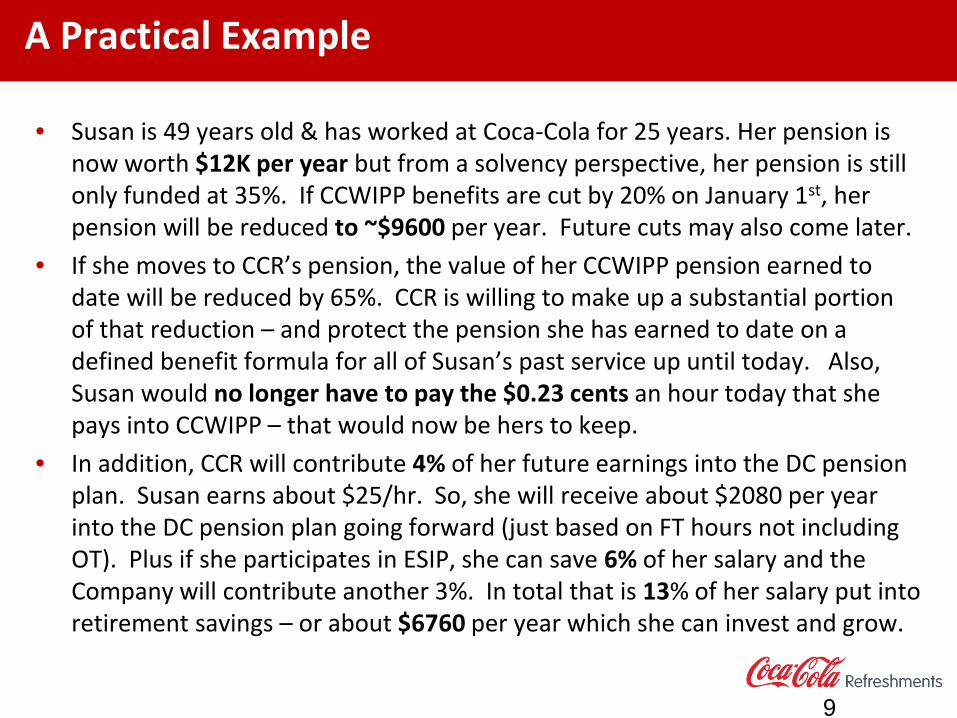

A Practical Example

9

• Susan is 49 years old & has worked at Coca-Cola for 25 years. Her pension is now worth $12K per year but from a solvency perspective, her pension is still only funded at 35%. If CCWIPP benefits are cut by 20% on January 1st, her pension will be reduced to ~$9600 per year. Future cuts may also come later.

• If she moves to CCR’s pension, the value of her CCWIPP pension earned to date will be reduced by 65%. CCR is willing to make up a substantial portion of that reduction – and protect the pension she has earned to date on a defined benefit formula for all of Susan’s past service up until today. Also, Susan would no longer have to pay the $0.23 cents an hour today that she pays into CCWIPP – that would now be hers to keep.

• In addition, CCR will contribute 4% of her future earnings into the DC pension plan. Susan earns about $25/hr. So, she will receive about $2080 per year into the DC pension plan going forward (just based on FT hours not including OT). Plus if she participates in ESIP, she can save 6% of her salary and the Company will contribute another 3%. In total that is 13% of her salary put into retirement savings – or about $6760 per year which she can invest and grow.

10

The Company’s Defined Contribution Pension Plan features include:

• One year waiting period to join for new employees (no waiting for current employees)

• Company contributes 4% of pay (base pay + overtime) • Contribution are made at each pay period • Associate contributions are not permitted • Immediate vesting • Funds are administered on a locked-in basis as per legislation and are not available

for withdrawal until minimum of age 55 • Associate chooses how the company contributions are invested • Record-keeper is Manulife Financial • Comprehensive online tools to assist with retirement planning will be provided in

addition to semi-annual statements mailed to members’ homes

Investment options provided include:

• Target Retirement Date funds • Canadian Money Market • Canadian Equity • Canadian Bond

Defined Contribution Pension Plan

• US Equity • International Equity • Global Equity

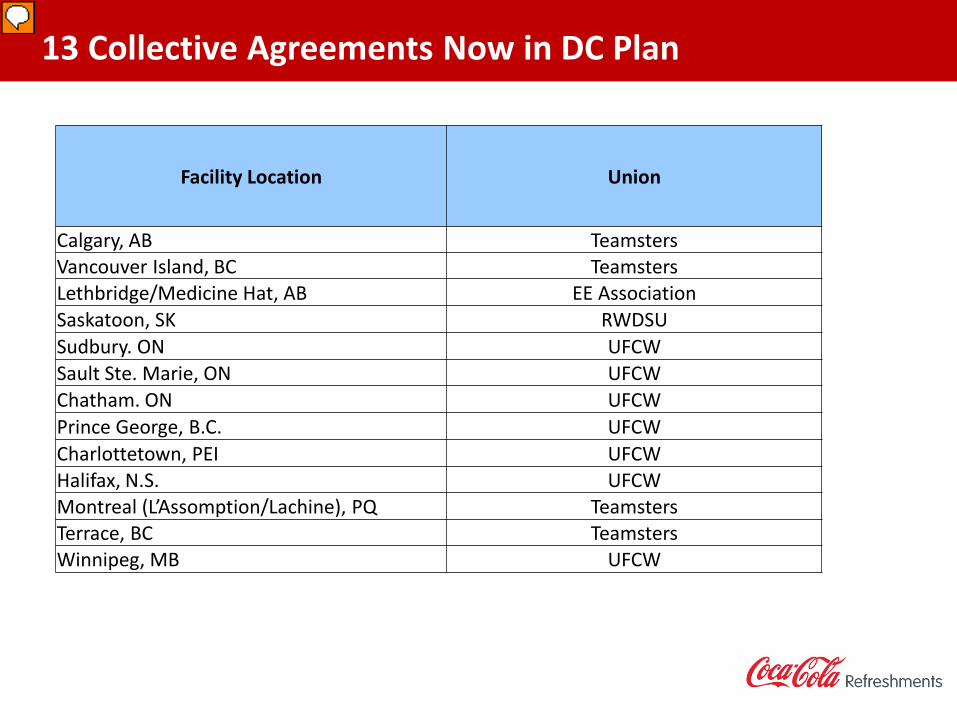

13 Collective Agreements Now in DC Plan

Facility Location Union

Calgary, AB Teamsters Vancouver Island, BC Teamsters Lethbridge/Medicine Hat, AB EE Association Saskatoon, SK RWDSU Sudbury. ON UFCW Sault Ste. Marie, ON UFCW Chatham. ON UFCW Prince George, B.C. UFCW Charlottetown, PEI UFCW Halifax, N.S. UFCW Montreal (L’Assomption/Lachine), PQ Teamsters Terrace, BC Teamsters Winnipeg, MB UFCW

12

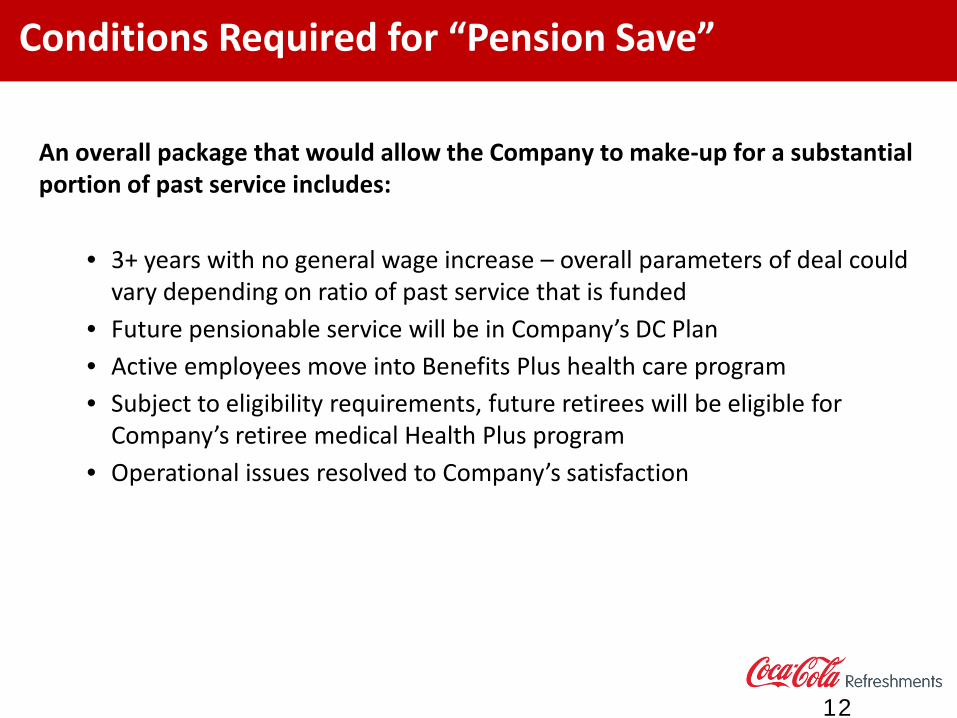

An overall package that would allow the Company to make-up for a substantial portion of past service includes:

• 3+ years with no general wage increase – overall parameters of deal could vary depending on ratio of past service that is funded

• Future pensionable service will be in Company’s DC Plan • Active employees move into Benefits Plus health care program • Subject to eligibility requirements, future retirees will be eligible for

Company’s retiree medical Health Plus program • Operational issues resolved to Company’s satisfaction

Conditions Required for “Pension Save”

13

Appendices Retiree Health Retiree Medical: Health Plus

Overview

o Provincial Medicare and other government programs form the core of CCR retirees’ coverage

o CCR provides coverage to eligible retirees that is supplemental to these core programs in two main areas:

- Health Care Expenses - Death Benefits

14

Overview (continued)

o Provincial health insurance plans cover many basic healthcare expenses, including:

- Physicians’ and surgeons’ fees - Diagnostic procedures - Standard ward accommodation - Certain prescription drugs for retirees over age 65

o CCR’s HealthPlus program provides an important supplement to provincial coverage and is comprised of two components:

- The Security Plan – provides an important supplement to provincial health coverage

- The Healthcare Spending Account (HSA) – can be used to pay for a wide range of medical and dental expenses not covered elsewhere, and/or to purchase private health insurance

Who is Eligible?

• Employees who retire at age 55 or older with a minimum of 10 years of credited service in the Coca Cola Employees’ Retirement Plan

• Eligible dependents

• Coverage is effective as of date of retirement

• Participation in the HealthPlus Plan is for Canadian residents only

How Does HealthPlus Work ?

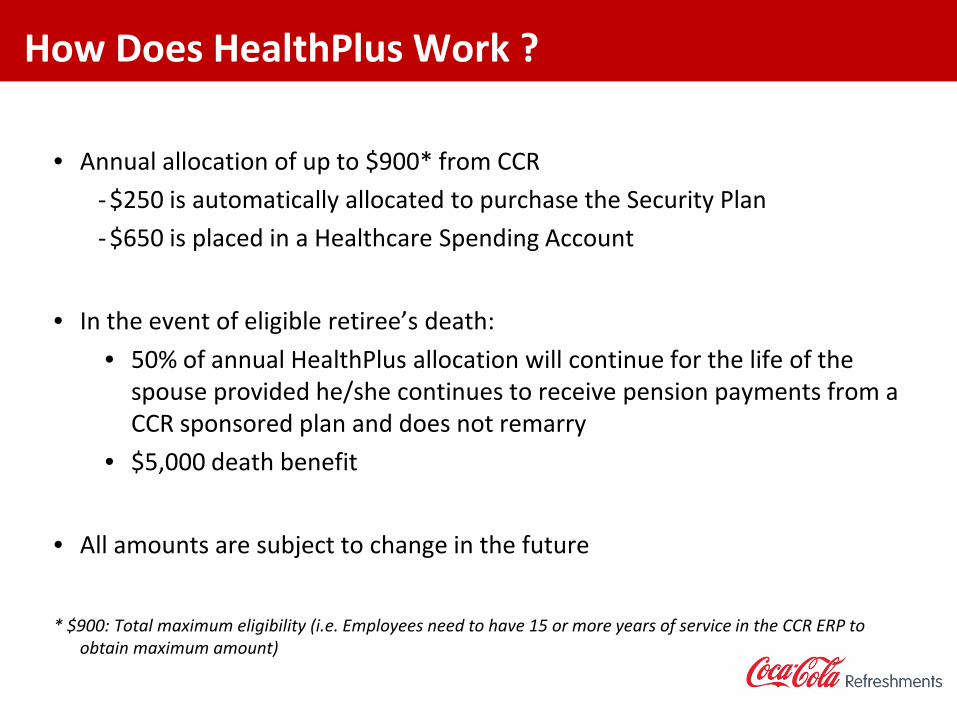

• Annual allocation of up to $900* from CCR - $250 is automatically allocated to purchase the Security Plan - $650 is placed in a Healthcare Spending Account

• In the event of eligible retiree’s death: • 50% of annual HealthPlus allocation will continue for the life of the

spouse provided he/she continues to receive pension payments from a CCR sponsored plan and does not remarry

• $5,000 death benefit

• All amounts are subject to change in the future

* $900: Total maximum eligibility (i.e. Employees need to have 15 or more years of service in the CCR ERP to

obtain maximum amount)

HealthPlus Overview

• Annual

• Healthcare Allocation

• $900

Security Plan $250

HSA Allocation $650

A Closer Look at the Security Plan

o Designed to provide protection in case of major health care expenses not covered elsewhere

o Covers 100% of eligible expenses after the combined annual deductible of $2,000 for the retiree and his/her eligible dependents

o Overall lifetime maximum of $500,000

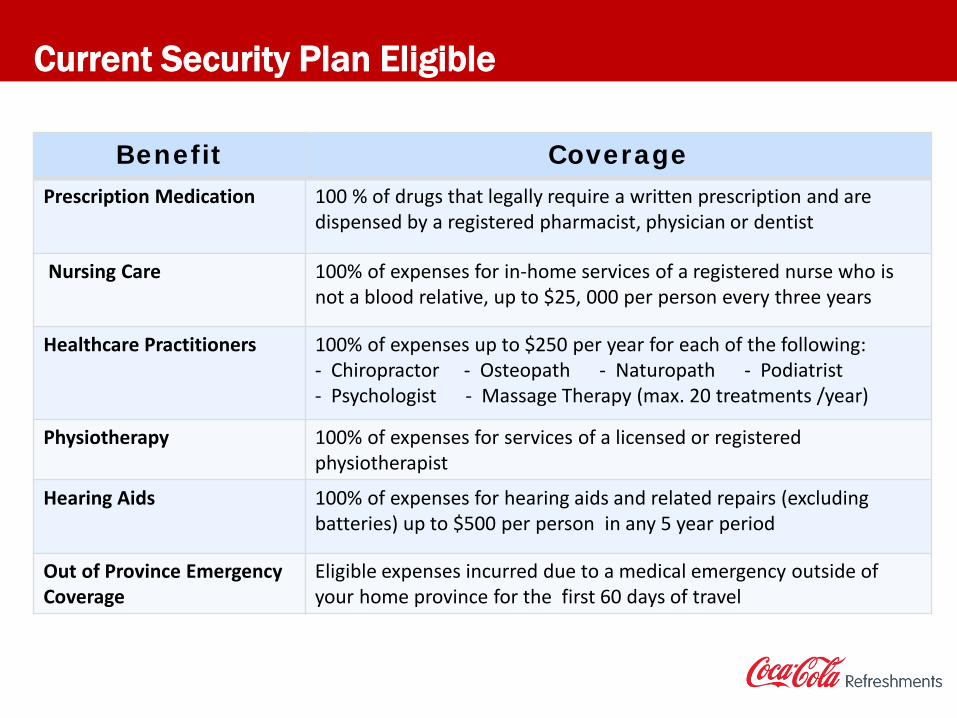

Current Security Plan Eligible Expenses (After Annual Deductible)

Benefit Coverage Prescription Medication 100 % of drugs that legally require a written prescription and are

dispensed by a registered pharmacist, physician or dentist

Nursing Care 100% of expenses for in-home services of a registered nurse who is not a blood relative, up to $25, 000 per person every three years

Healthcare Practitioners 100% of expenses up to $250 per year for each of the following: - Chiropractor - Osteopath - Naturopath - Podiatrist - Psychologist - Massage Therapy (max. 20 treatments /year)

Physiotherapy 100% of expenses for services of a licensed or registered physiotherapist

Hearing Aids 100% of expenses for hearing aids and related repairs (excluding batteries) up to $500 per person in any 5 year period

Out of Province Emergency Coverage

Eligible expenses incurred due to a medical emergency outside of your home province for the first 60 days of travel

Healthcare Spending Account

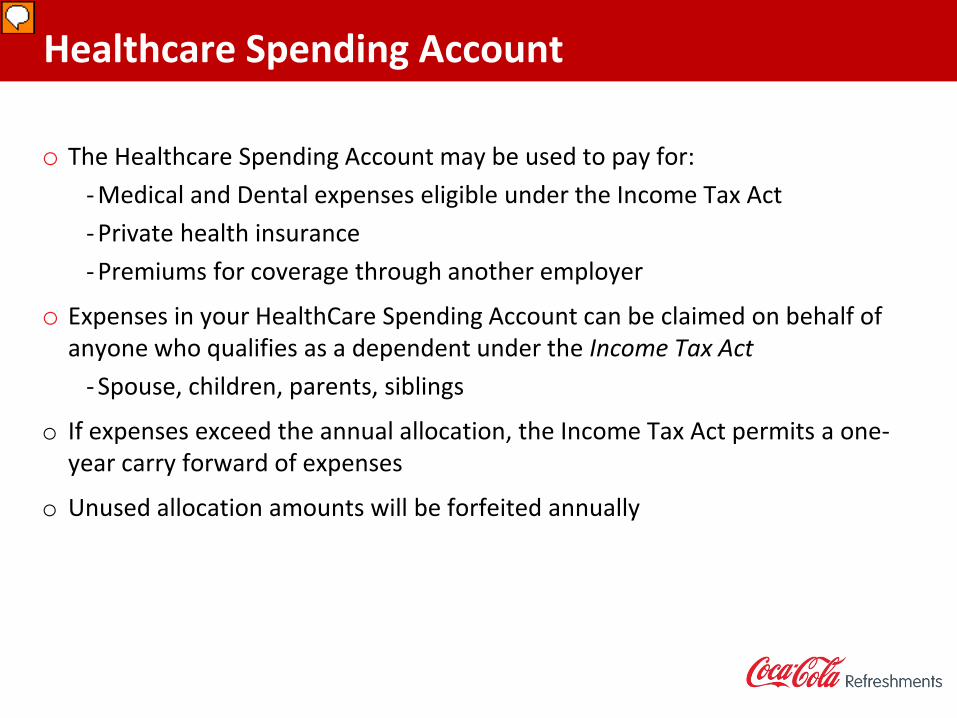

o The Healthcare Spending Account may be used to pay for: - Medical and Dental expenses eligible under the Income Tax Act - Private health insurance - Premiums for coverage through another employer

o Expenses in your HealthCare Spending Account can be claimed on behalf of anyone who qualifies as a dependent under the Income Tax Act

- Spouse, children, parents, siblings

o If expenses exceed the annual allocation, the Income Tax Act permits a one-year carry forward of expenses

o Unused allocation amounts will be forfeited annually

How the HealthPlus Plan Works

Example based on retiree has 15 years of service in ERP

$3,000 in eligible expenses

$2,000 annual deductible

$1,000 reimbursed through Security Plan

$650 H.S.A. can

be claimed to reduce the

annual deductible to

$1,350 OR

$650 can be used toward additional

expenses that are not eligible

under the Security Plan

23

Appendices Wages Collective Agreement Wage Settlements

2010-13 Wage Settlements

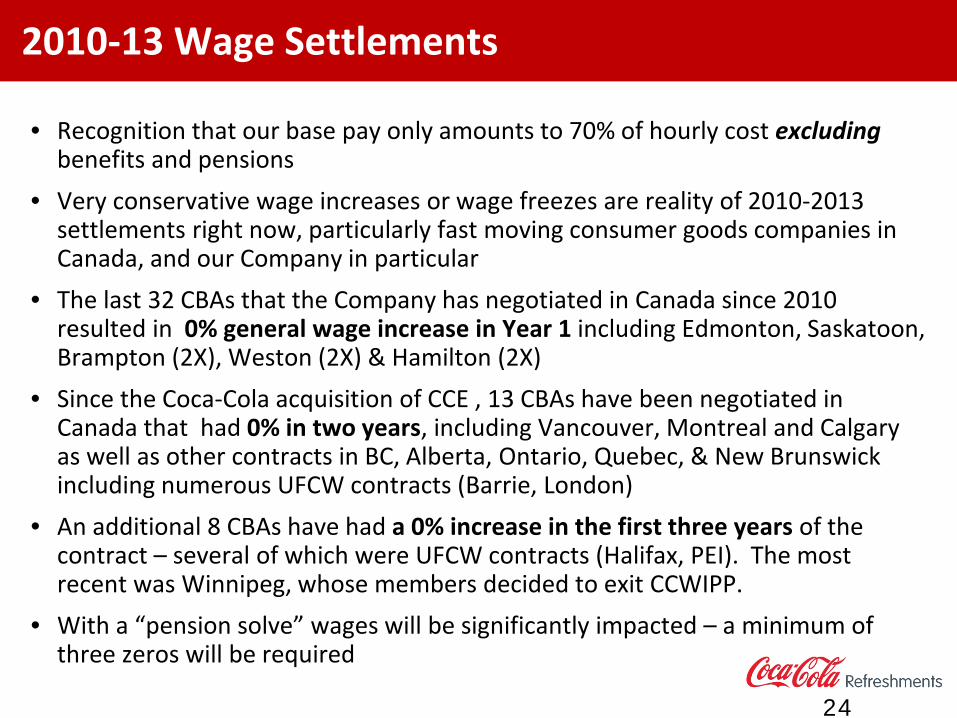

• Recognition that our base pay only amounts to 70% of hourly cost excluding benefits and pensions

• Very conservative wage increases or wage freezes are reality of 2010-2013 settlements right now, particularly fast moving consumer goods companies in Canada, and our Company in particular

• The last 32 CBAs that the Company has negotiated in Canada since 2010 resulted in 0% general wage increase in Year 1 including Edmonton, Saskatoon, Brampton (2X), Weston (2X) & Hamilton (2X)

• Since the Coca-Cola acquisition of CCE , 13 CBAs have been negotiated in Canada that had 0% in two years, including Vancouver, Montreal and Calgary as well as other contracts in BC, Alberta, Ontario, Quebec, & New Brunswick including numerous UFCW contracts (Barrie, London)

• An additional 8 CBAs have had a 0% increase in the first three years of the contract – several of which were UFCW contracts (Halifax, PEI). The most recent was Winnipeg, whose members decided to exit CCWIPP.

• With a “pension solve” wages will be significantly impacted – a minimum of three zeros will be required

24

Appendices Benefits Benefits Plus Health Care Plan

Current Per Employee Costs

• In 2013, the company will be paying an average of ~$4,468 in direct dollars for employee benefits per employee, including :

• Direct reimbursement to employees and their families for medical

and dental claims

• Premiums paid for short and long-term disability and life insurance

• Costs to provide the Employee Assistance Program

• Regina employees contribute 20% towards the cost of their long-term disability benefits coverage

• Benefits Plus health care program is a flex plan that does require employee contributions for higher levels of coverage

26

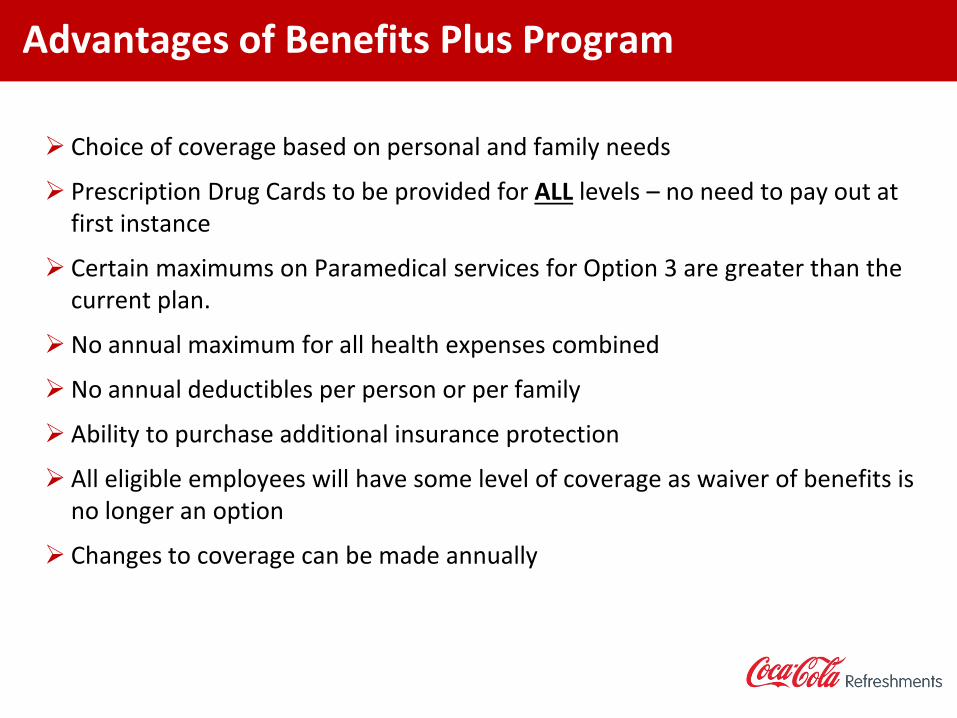

Advantages of Benefits Plus Program

Choice of coverage based on personal and family needs

Prescription Drug Cards to be provided for ALL levels – no need to pay out at first instance

Certain maximums on Paramedical services for Option 3 are greater than the current plan.

No annual maximum for all health expenses combined

No annual deductibles per person or per family

Ability to purchase additional insurance protection

All eligible employees will have some level of coverage as waiver of benefits is no longer an option

Changes to coverage can be made annually

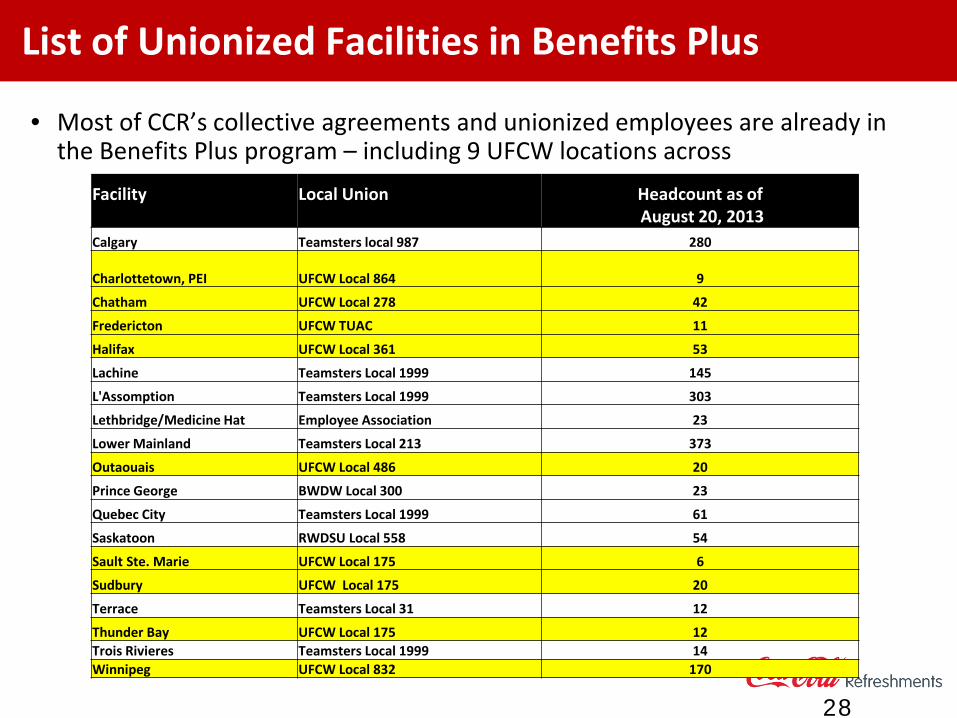

List of Unionized Facilities in Benefits Plus

• Most of CCR’s collective agreements and unionized employees are already in the Benefits Plus program – including 9 UFCW locations across

28

Facility

Local Union

Headcount as of August 20, 2013

Calgary Teamsters local 987 280

Charlottetown, PEI UFCW Local 864 9

Chatham UFCW Local 278 42

Fredericton UFCW TUAC 11

Halifax UFCW Local 361 53

Lachine Teamsters Local 1999 145

L'Assomption Teamsters Local 1999 303

Lethbridge/Medicine Hat Employee Association 23

Lower Mainland Teamsters Local 213 373

Outaouais UFCW Local 486 20

Prince George BWDW Local 300 23

Quebec City Teamsters Local 1999 61

Saskatoon RWDSU Local 558 54

Sault Ste. Marie UFCW Local 175 6

Sudbury UFCW Local 175 20

Terrace Teamsters Local 31 12

Thunder Bay UFCW Local 175 12 Trois Rivieres Teamsters Local 1999 14 Winnipeg UFCW Local 832 170

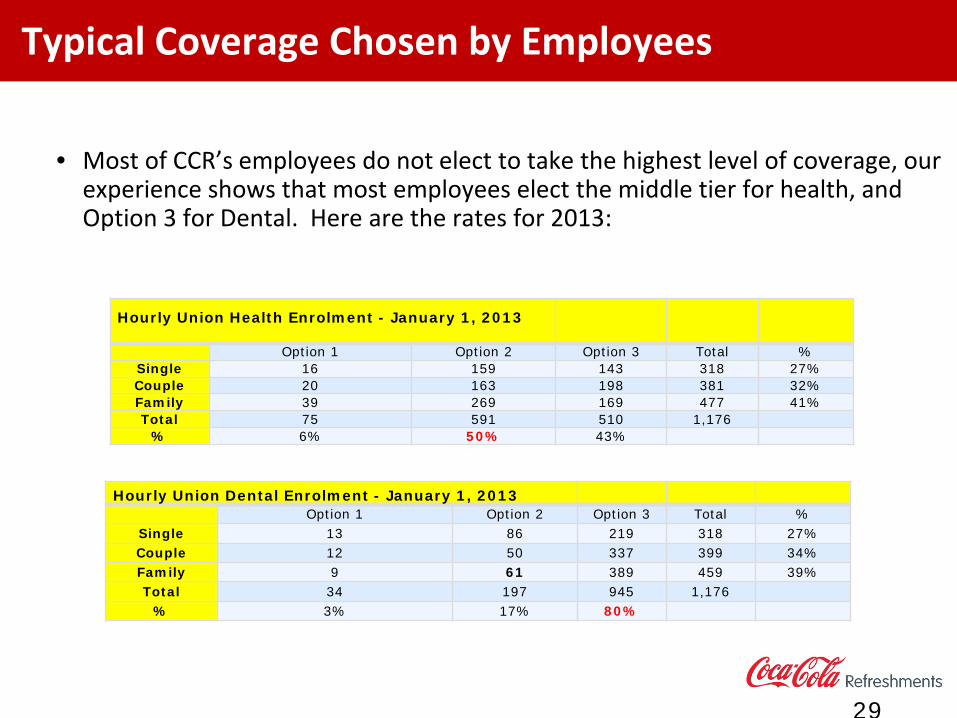

Typical Coverage Chosen by Employees

• Most of CCR’s employees do not elect to take the highest level of coverage, our experience shows that most employees elect the middle tier for health, and Option 3 for Dental. Here are the rates for 2013:

29

Hourly Union Health Enrolment - January 1, 2013

Option 1 Option 2 Option 3 Total % Single 16 159 143 318 27% Couple 20 163 198 381 32% Family 39 269 169 477 41% Total 75 591 510 1,176

% 6% 50% 43%

Hourly Union Dental Enrolment - January 1, 2013 Option 1 Option 2 Option 3 Total %

Single 13 86 219 318 27% Couple 12 50 337 399 34% Family 9 61 389 459 39% Total 34 197 945 1,176

% 3% 17% 80%

2014 Benefits Plus Rates for Employees

Option 1** Option 2 Option 3

Health Associate Only -$ 500 $ 148 $ 613 Associate +1 -$ 500 $ 295 $ 1,227

Associate +2 or more -$ 500 $ 460 $ 1,899

Option 1** Option 2** Option 3

Dental Associate Only -$ 250 -$ 100 $ 30 Associate +1 -$ 250 -$ 100 $ 60 Associate +2 or more -$ 250 -$ 100 $ 96

** Credit amounts are allocated to the HSA effective January 1, 2014 and prorated for the year

Operational challenges to be addressed • Rural vs. Urban Merchandising • Consecutive days off • Clarify OT provisions (extension and off-day) • Option to stay home on layoff when short handed in

other Departments • Post out of highly skilled roles

Highly

31